Update on Standards for Audits, Reviews, and Compilations...

42

4/23/2013 1 1 Update on Standards for Audits, Reviews, and Compilations Mike Glynn, CPA Senior Technical Manager AICPA Audit and Attest Standards Team [email protected] American Institute of CPAs DISCLAIMER Views expressed by AICPA employees are expressed for purposes of deliberation, providing member services and other purposes exclusive of practicing public accounting. Views expressed by AICPA staff do not necessarily represent the official views of the AICPA unless otherwise noted. Official AICPA positions are determined through certain specific committee procedures, due process and deliberation.

-

Upload

duongkhanh -

Category

Documents

-

view

216 -

download

2

Transcript of Update on Standards for Audits, Reviews, and Compilations...

4/23/2013

1

1

Update on Standards for Audits, Reviews, and Compilations

Mike Glynn, CPA

Senior Technical Manager

AICPA Audit and Attest Standards Team

American Institute of CPAs

DISCLAIMER

Views expressed by AICPA employees are expressed for purposes of deliberation, providing member services and other purposes exclusive of practicing public accounting. Views expressed by AICPA staff do not necessarily represent the official views of the AICPA unless otherwise noted. Official AICPA positions are determined through certain specific committee procedures, due process and deliberation.

4/23/2013

2

American Institute of CPAs

Session Objectives

Discuss the AICPA’s proposed accounting framework for small- and medium-sized entitiesDiscuss the AICPA’s Practice Aid “Accounting and Financial Reporting Guidelines for Cash-and Tax-Basis Financial Statements”Discuss the ARSC’s and the ASB’s Clarity projects and differences from pre-clarity standards

Slide 3

AICPA's Financial Reporting Framework for Small and

Medium-sized Entities (FRF-SME)

4/23/2013

3

American Institute of CPAs

FRF-SME

Intended for privately held small and medium-sized entities.

Blend of accrual-tax method and traditional methods of accounting.

Developed by a working group of CPAs and AICPA staff

Was exposed for public comment during the fall of 2012.

Expected to be issued in early June 2013.

American Institute of CPAs

FRF-SME

Will be a less complicated and less costly system of accounting for SMEs that do not require GAAP basis statements.

More beneficial than other OCBOAs as it will have undergone public comment and professional scrutiny.

Will not be required to be used, but can be used as soon as it is released.

Will be assessed 3-4 years after issuance for modifications but will not undergo frequent changes

4/23/2013

4

American Institute of CPAs

FRF-SME

Will use historical cost as a measurement basis – and depart from increased use of fair value measurements

Disclosure requirements will be greatly reduced

If users need additional information, they can obtain it from management

Focuses on the performance of the SME, its assets, liabilities, and cash flows

American Institute of CPAs

FRF-SME

“Similar informative disclosures”?• While financial statements will be required to include

“similar informative disclosures”, disclosure requirements in framework are intended to meet the requirement

Implementation guidance will be made available by the AICPA

4/23/2013

5

AICPA Practice Aid: Accounting and Financial Reporting Guidelines For

Cash- and Tax-Basis Financial Statements

American Institute of CPAs

PA: Cash- and Tax-Basis Financial Statements

Many smaller entities have determined that financial statements prepared by applying the cash- or tax-basis of accounting more appropriately suit their needs.

Little authoritative guidance is available with respect to the preparation of financial statements when applying the cash- or tax-basis of accounting.

4/23/2013

6

American Institute of CPAs

PA: Cash- and Tax-Basis Financial Statements

Practice Aid is intended to provide preparers with the guidelines and best practices that promote consistency and that resolve the often difficult questions regarding the preparation of cash- and tax-basis financial statements.

While nonauthoritative, this practice aid is the best source for such guidance.

All content has been reviewed by subject-matter experts.

American Institute of CPAs

PA: Cash- and Tax-Basis Financial Statements

Available at www.cpa2biz.com

• Product code APACTB12P

Also available, Applying OCBOA in State and Local Government Financial Statements

• Product code APAOCBO12P

4/23/2013

7

ASB and ARSC Clarity Projects

American Institute of CPAs

Clarity Project Goals

Address concerns over length and complexity of standards

Make standards easier to read, understand and implement

Lead to enhancements in engagement quality

4/23/2013

8

American Institute of CPAs

Clarity

Auditing Standards Convergence with ISAs

• Harmonize, not adopt

• Most audits performed internationally are of nonpublic entities –therefore, ASB and IAASB have a similar focus

• ASB standards—more use of “should” than ISAs, but fewer than existing SASs

Avoid unnecessary conflicts with PCAOB standards.

American Institute of CPAs

Clarity

SSARSs will not be converged with international standards

• Compilation engagements are not compatible

• ARSC determined to converge review standard with AU-C section 930, Interim Financial Information

4/23/2013

9

American Institute of CPAs

Clarity

Purpose of the Clarity Project is not to create additional requirements

Adjustments will have to be made to practices as a result of the clarified standards

American Institute of CPAs

Clarity Format

Introduction

Objectives

Definitions

Requirements

Application Material

Appendices and Exhibits

4/23/2013

10

American Institute of CPAs

Considerations for Audits of Smaller, Less Complex Entities

Smaller, less complex refers to characteristics such as:

• Concentration of ownership and management in a small number of individuals

• One or more of the following:

- Straight forward/uncomplicated transactions

- Simple record keeping

- Few lines of business/few products

- Few internal controls

- Few personnel with a wide range of duties

American Institute of CPAs

Considerations for Audits of Smaller, Less Complex Entities

Guidance generally results in:

• Specifying alternate procedures appropriate for situations like:

- Scaling down audit programs and procedures

- Recognizing governance and management are the same people

- Addressing controls that are not documented or segregated

- Recognizing irrelevant requirements

4/23/2013

11

American Institute of CPAs

Considerations for Audits of Governmental Entities

Most clarified standards have guidance for audits of governmental entities• About uniqueness of governmental entities

• About uniqueness of state audit organizations

• Opinion units

• Materiality

• Laws and regulations, e.g., “withdrawal from engagements”

Accounting standards neutrality

SSARSs Clarity Project and Proposed Changes to 101-3

and SSARSs

4/23/2013

12

American Institute of CPAs

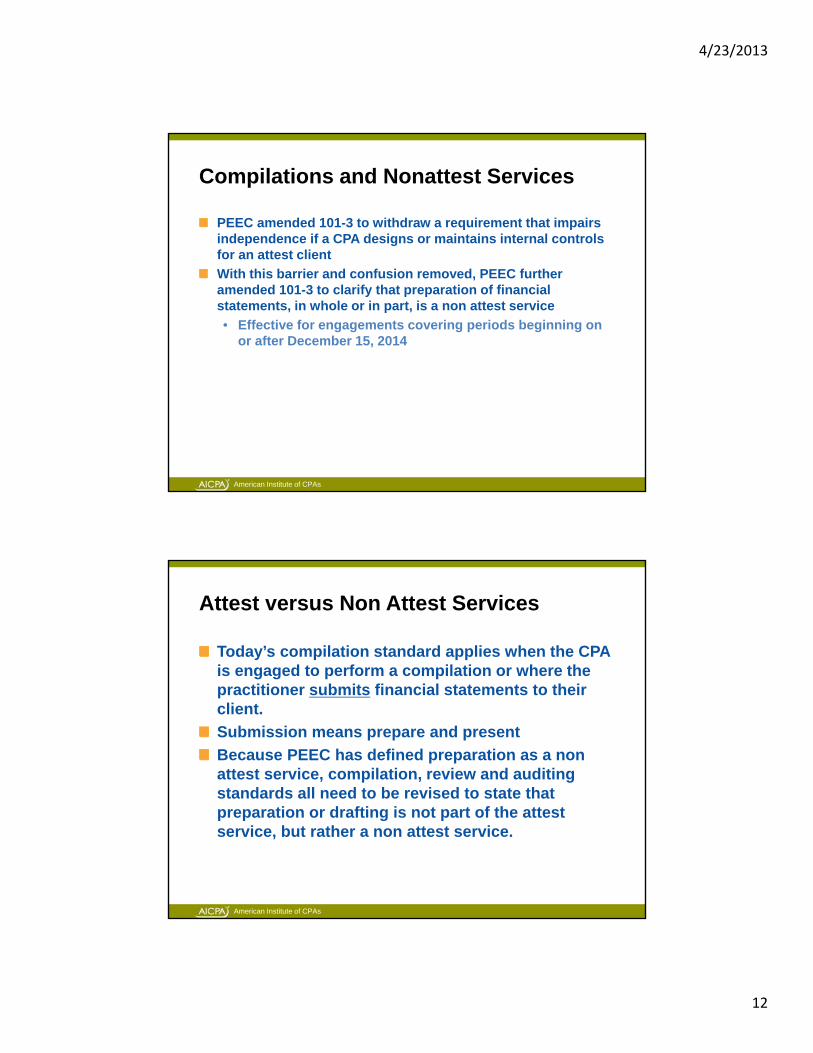

Compilations and Nonattest Services

PEEC amended 101-3 to withdraw a requirement that impairs independence if a CPA designs or maintains internal controls for an attest client

With this barrier and confusion removed, PEEC further amended 101-3 to clarify that preparation of financial statements, in whole or in part, is a non attest service

• Effective for engagements covering periods beginning on or after December 15, 2014

American Institute of CPAs

Attest versus Non Attest Services

Today’s compilation standard applies when the CPA is engaged to perform a compilation or where the practitioner submits financial statements to their client.

Submission means prepare and present

Because PEEC has defined preparation as a non attest service, compilation, review and auditing standards all need to be revised to state that preparation or drafting is not part of the attest service, but rather a non attest service.

4/23/2013

13

American Institute of CPAs

Where are the issues?

Many members incorrectly believe that attest engagement is the same as an assurance engagement, so many members don’t understand why a compilation is an attest service today• Attest engagement. An attest engagement is an engagement

that requires independence as defined in AICPA Professional Standards.

Many members (and clients) believe that compile and prepare are the same thing. So they don’t understand the nuance between attest and non attest

American Institute of CPAs

Proposed nonattest compilation standard

Remove independence from compilation standard• By definition compilation becomes a non attest service

Create a non attest compilation/preparation standard that puts requirements around what a CPA needs to do when preparing financial statements

Financial statements would include a legend that a CPA has not performed an assurance service

4/23/2013

14

American Institute of CPAs

Proposed nonattest compilation standard

Reporting in certain specific circumstances• Accountant is engaged to or decided to report on the f/s

• F/s contain known departures from the applicable FRF that are not disclosed in the notes to the f/s

• Entity does not include an appropriate legend on the f/s

• Accountant has material financial interest in the client or contingent or referral fees

Report would look significantly different from review or audit report

American Institute of CPAs

Proposed nonattest compilation standard

Aligns non attest with many state laws

Aligns the terms compile and prepare

Retains the term compilation and by making it a non attest service removes confusion around attest and assurance

4/23/2013

15

SSARSs Clarity Project: Proposed Review

SSARSs

30

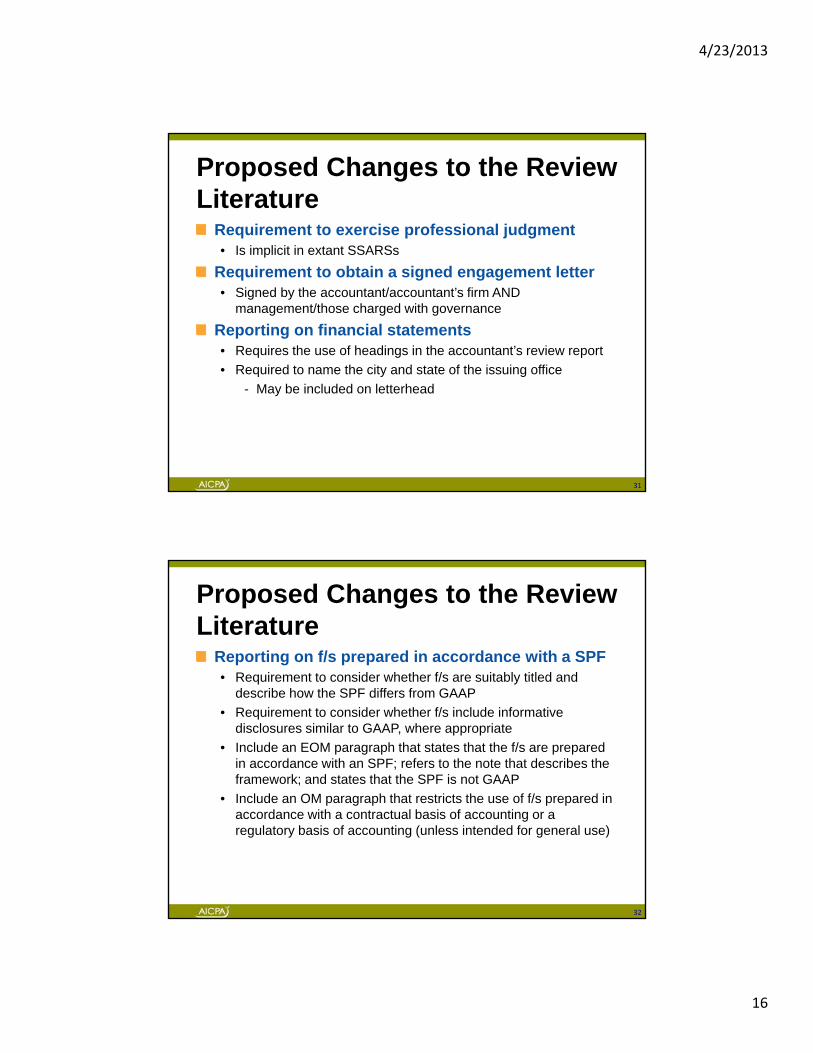

Proposed Changes to the Review Literature

The SSARSs review literature will be converged with the requirements of AU-C section 930, Interim Financial Information• Will result in consistency between limited assurance

engagements.

Scope• The Standard may be applied to historical financial information

other than historical financial statements, such as:

- Specified elements, accounts, or items of a f/s

- Supplementary information

- Required supplementary information

- Financial information included in a tax return

4/23/2013

16

31

Proposed Changes to the Review Literature

Requirement to exercise professional judgment• Is implicit in extant SSARSs

Requirement to obtain a signed engagement letter• Signed by the accountant/accountant’s firm AND

management/those charged with governance

Reporting on financial statements• Requires the use of headings in the accountant’s review report

• Required to name the city and state of the issuing office

- May be included on letterhead

32

Proposed Changes to the Review Literature

Reporting on f/s prepared in accordance with a SPF• Requirement to consider whether f/s are suitably titled and

describe how the SPF differs from GAAP

• Requirement to consider whether f/s include informative disclosures similar to GAAP, where appropriate

• Include an EOM paragraph that states that the f/s are prepared in accordance with an SPF; refers to the note that describes the framework; and states that the SPF is not GAAP

• Include an OM paragraph that restricts the use of f/s prepared in accordance with a contractual basis of accounting or a regulatory basis of accounting (unless intended for general use)

4/23/2013

17

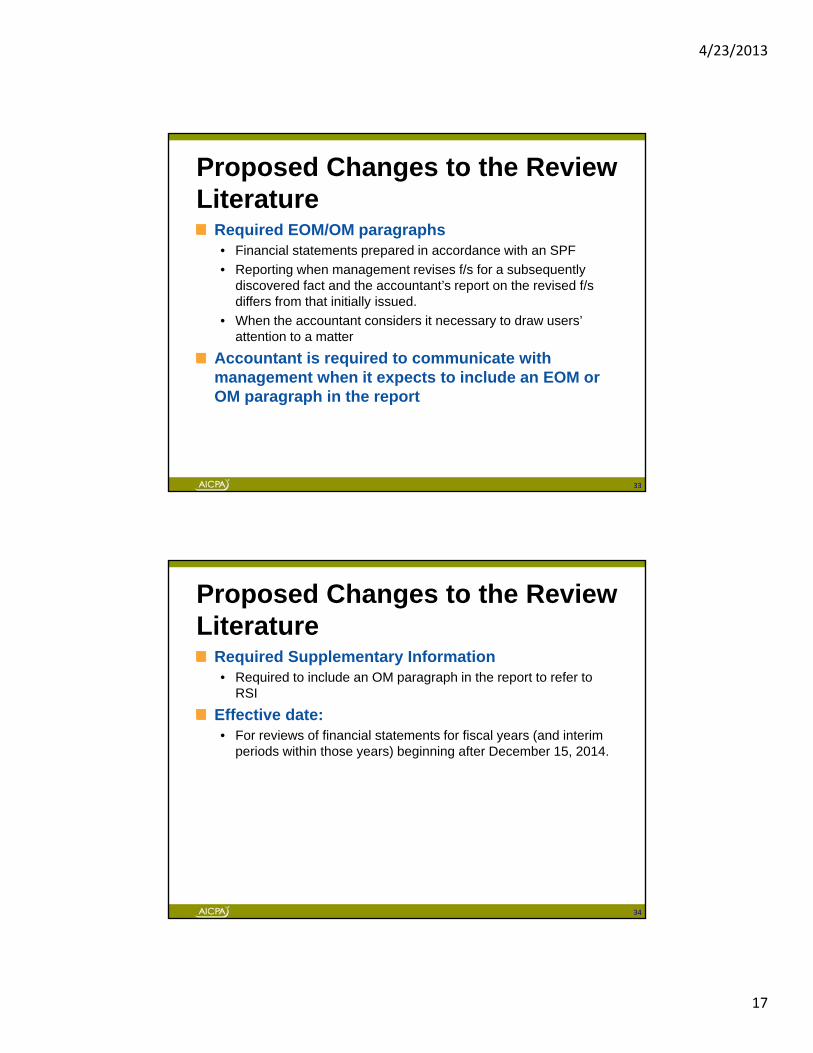

33

Proposed Changes to the Review Literature

Required EOM/OM paragraphs• Financial statements prepared in accordance with an SPF

• Reporting when management revises f/s for a subsequently discovered fact and the accountant’s report on the revised f/s differs from that initially issued.

• When the accountant considers it necessary to draw users’ attention to a matter

Accountant is required to communicate with management when it expects to include an EOM or OM paragraph in the report

34

Proposed Changes to the Review Literature

Required Supplementary Information• Required to include an OM paragraph in the report to refer to

RSI

Effective date:• For reviews of financial statements for fiscal years (and interim

periods within those years) beginning after December 15, 2014.

4/23/2013

18

Clarified Auditing Standards

American Institute of CPAs

Clarity Project Status

One SAS not yet clarified• Use of Internal Auditors

- delayed to enable the ASB to align with the IAASB’s revisions to clarified ISA 610

4/23/2013

19

37

Clarity Project

Clarified SASs codified with new section numbers designated “AU-C”

• AU section numbers changed to converge with ISA numbering

38

Changes to Auditing Standards

• New terms

- Applicable financial reporting framework

- Emphasis-of-matter and other-matter paragraphs replace explanatory paragraphs

- Group engagement partner and component auditor replace principal auditor and other auditor, respectively.

4/23/2013

20

American Institute of CPAs

Most Significant Areas of Implementation Issues

Terms of EngagementInitial Audits

Auditor’s Reports

GROUP AUDITS

American Institute of CPAs

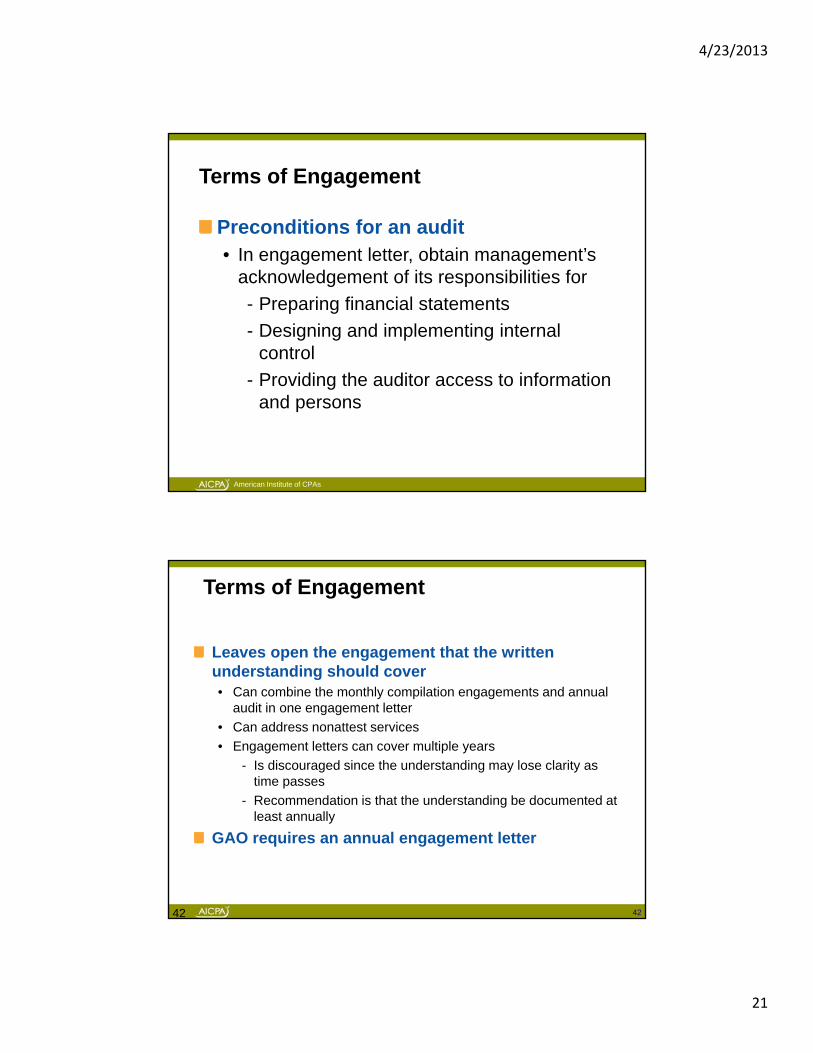

Terms of Engagement

Preconditions for an audit• Determine the financial reporting framework

is acceptable

- Was implicit in extant SASs

- Change is not expected to affect practice

4/23/2013

21

American Institute of CPAs

Terms of Engagement

Preconditions for an audit• In engagement letter, obtain management’s

acknowledgement of its responsibilities for

- Preparing financial statements

- Designing and implementing internal control

- Providing the auditor access to information and persons

42 42

Terms of Engagement

Leaves open the engagement that the written understanding should cover• Can combine the monthly compilation engagements and annual

audit in one engagement letter

• Can address nonattest services

• Engagement letters can cover multiple years

- Is discouraged since the understanding may lose clarity as time passes

- Recommendation is that the understanding be documented at least annually

GAO requires an annual engagement letter

4/23/2013

22

American Institute of CPAs

Other Acceptance Considerations

Terms of Engagement

• If management imposes a scope limitation that would result in qualified opinion or disclaimer, precluded from accepting engagement

- Inability to observe inventory due to timing of acceptance of engagement is circumstantial, NOT management imposed

Initial Audits• Looking at predecessor workpapers is useful but can’t be the

only procedure to verify opening balances

American Institute of CPAs

Auditor’s Reports

Headings are REQUIRED for every paragraph

Title of report = first paragraph heading

If letterhead includes city and state, not necessary to put at bottom of report• For multi-office firms, to not repeat city and state, letterhead

should be clear as to which office is issuing the report

Reports covering 2012 and 2011 may use new wording for both periods

4/23/2013

23

American Institute of CPAs

45

Modifications to the Opinion (AU-C 705)

Basis for qualified, adverse, or disclaimer (placed before opinion paragraph)

Modified opinion (Qualified, Adverse, or Disclaimer

American Institute of CPAs

46

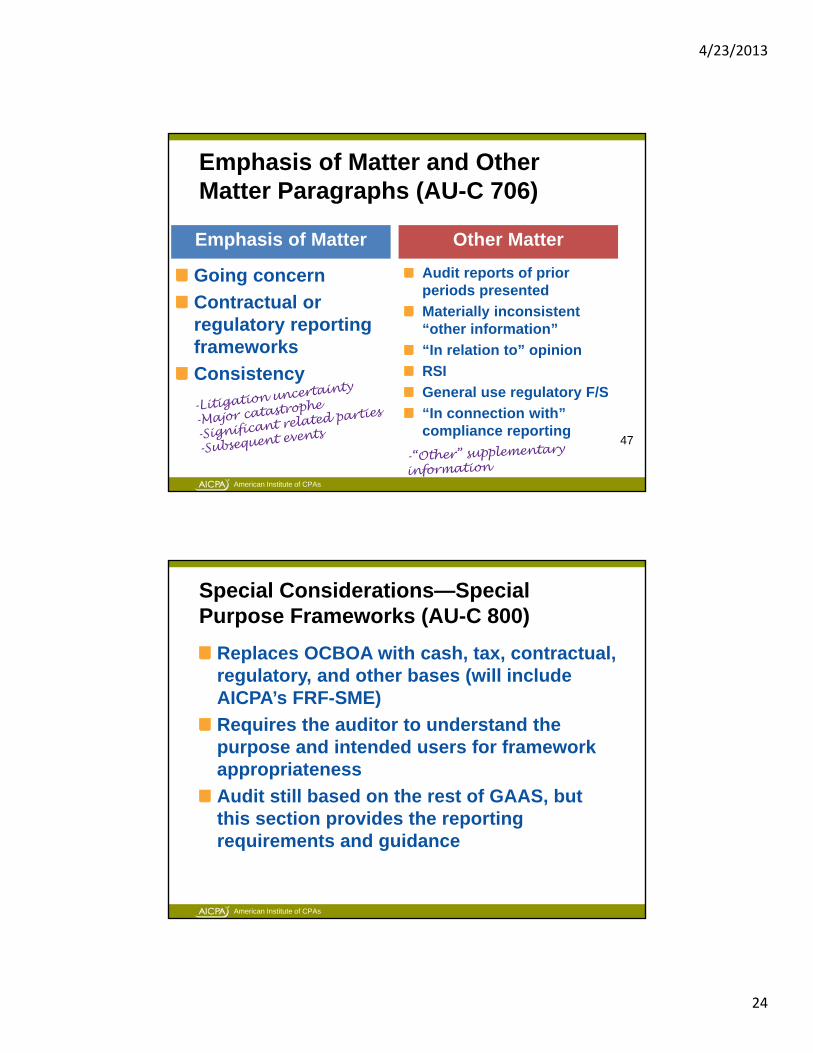

Emphasis of Matter and Other Matter Paragraphs (AU-C 706)

Emphasis of Matter• Matters appropriately

presented or disclosed

Other Matter• To understand audit matters

(Combining statements, SI, RSI, SEFA)

4/23/2013

24

American Institute of CPAs

Emphasis of Matter and Other Matter Paragraphs (AU-C 706)

Going concern

Contractual or regulatory reporting frameworks

Consistency

47

Audit reports of prior periods presented

Materially inconsistent “other information”

“In relation to” opinion

RSI

General use regulatory F/S

“In connection with” compliance reporting

Emphasis of Matter Other Matter

American Institute of CPAs

Special Considerations—Special Purpose Frameworks (AU-C 800)

Replaces OCBOA with cash, tax, contractual, regulatory, and other bases (will include AICPA’s FRF-SME)

Requires the auditor to understand the purpose and intended users for framework appropriateness

Audit still based on the rest of GAAS, but this section provides the reporting requirements and guidance

4/23/2013

25

American Institute of CPAs

Special Considerations—Special Purpose Frameworks ( AU-C 800)

Cash Basis Tax Basis Contractual Regulatory

Restricted General

Opinion Single Single Single Single Dual

Use EOM? Yes Yes Yes Yes No

DescribePurpose

No No Yes Yes Yes

Restrict use?

No No Yes Yes No

American Institute of CPAs

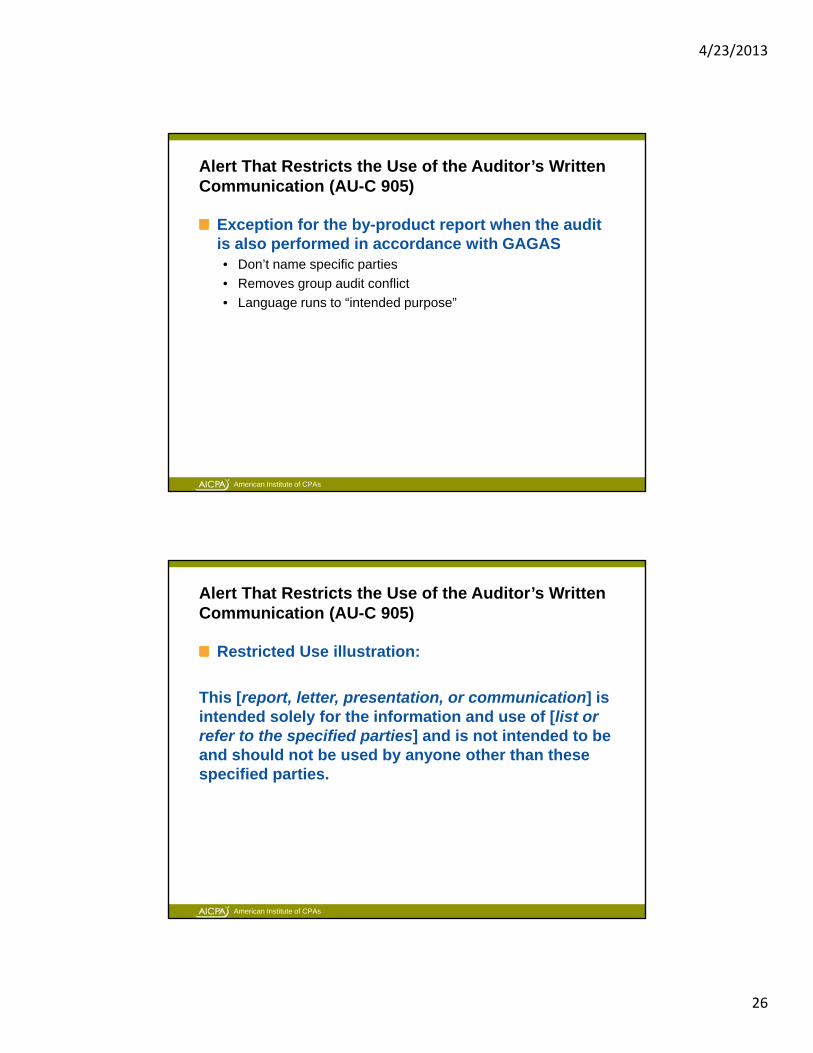

Alert That Restricts the Use of the Auditor’s Written Communication (AU-C 905)

Auditor should include an alert which restricts the use of the auditor’s communication when the subject matter is based on:• Measurement or disclosure requirement criteria that are

determined by the auditor to be suitable only for a limited number of users who can be presumed to have an adequate understanding of the criteria,

• Measurement or disclosure criteria that are available only to the specified parties, or

• Matters identified by the auditor during the course of the audit engagement when the identification of such matters is not the primary objective of the audit engagement (commonly referred to as a by-product report)

4/23/2013

26

American Institute of CPAs

Alert That Restricts the Use of the Auditor’s Written Communication (AU-C 905)

Exception for the by-product report when the audit is also performed in accordance with GAGAS• Don’t name specific parties

• Removes group audit conflict

• Language runs to “intended purpose”

American Institute of CPAs

Alert That Restricts the Use of the Auditor’s Written Communication (AU-C 905)

Restricted Use illustration:

This [report, letter, presentation, or communication] is intended solely for the information and use of [list or refer to the specified parties] and is not intended to be and should not be used by anyone other than these specified parties.

4/23/2013

27

American Institute of CPAs

Alert That Restricts the Use of the Auditor’s Written Communication (AU-C 905)

Restricted Purpose illustration:The purpose of this [report, letter, presentation, or communication] is solely to [describe the purpose of the auditor’s written communication, such as to describe the scope of our testing of internal control over financial reporting and compliance, and the result of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control over financial reporting or on compliance]. This [report, letter, presentation, or communication] is an integral part of an audit performed in accordance with Government Auditing Standards in considering [describe the results that are being assessed, such as the entity’s internal control over financial reporting and compliance]. Accordingly, this [report, letter, presentation, or communication] is not suitable for any other purpose.

American Institute of CPAs

Alert That Restricts the Use of the Auditor’s Written Communication (AU-C 905)

New:

An auditor’s written communication that includes an alert that restricts its use may be included in a document that also contains an auditor’s written communication that is for general use. In such circumstances, the use of the general use communications is not affected.

4/23/2013

28

American Institute of CPAs

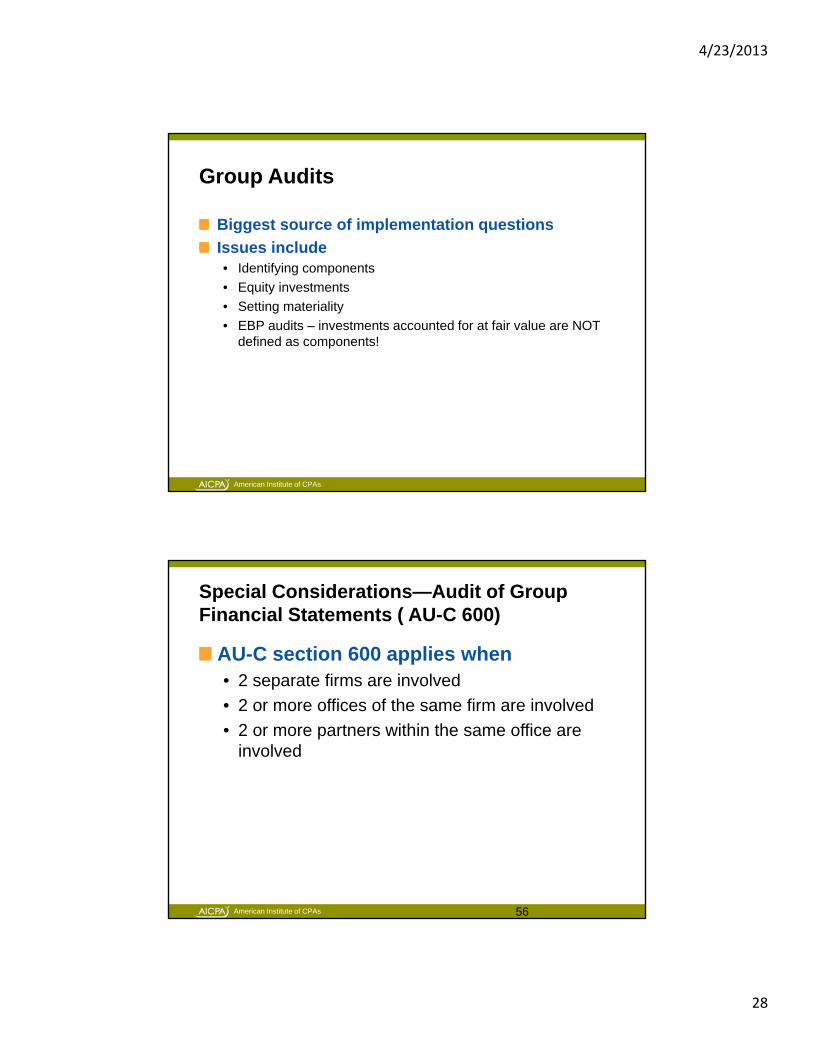

Group Audits

Biggest source of implementation questions

Issues include• Identifying components

• Equity investments

• Setting materiality

• EBP audits – investments accounted for at fair value are NOT defined as components!

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

AU-C section 600 applies when• 2 separate firms are involved

• 2 or more offices of the same firm are involved

• 2 or more partners within the same office are involved

56

4/23/2013

29

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Group – All the components whose financial information is included in the group financial statements

Group management – Management responsible for the preparation of the group financial statements

Group-wide controls – Controls designed, implemented, and maintained by group management over group financial reporting

57

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Component – an entity or business activity for which the group prepares financial information required by the reporting framework

Component materiality – Materiality for a component as determined by group engagement team for purposes of the group audit

58

4/23/2013

30

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Significant component – One identified by the group engagement team that is of individual financial significance to the group OR due to its circumstances is likely to include significant RMM to the group financial statements

59

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Considerations for governments• Existence of components evaluated within

individual opinion units

- Each opinion usually its own group

- Exception when there are other auditors or legally separate entities would automatically be considered a component

60

4/23/2013

31

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Considerations for governments• For governments with multiple opinion units,

components will commonly exist within:

- Aggregate discretely presented component units

- Individual component units whether audited by same audit firm or other auditors

- Aggregate remaining fund information:

- Pension or OPEB trust funds

- Investment trust funds

61

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Considerations for governments• Departments within a major fund that are

separately managed may also be components

• Most governments with multiple opinion units will be a group audit

62

4/23/2013

32

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Risk based approach• Group engagement team should obtain sufficient understanding

of the group, its components, and their environment to:

- Identify and assess risks of material misstatement at the group level

- Identify significant accounts and disclosures and related assertions at the group level

- Confirm identification of significant components

- Determine the timing and type of work to be performed at significant and non-significant components

- Determine which work will be performed by the group and component auditor

- Determine the nature, timing, and extent of work to be performed at the group level

63

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Obtain an understanding of the component auditor• Whether CA will comply with ethical requirements, especially

independence

• About the CA’s professional competence

• The extent, if any, the GA will be able to be involved in the CA’s work

• Whether the GA will be able to obtain information affecting the consolidation process

• Whether a CA operates in a regulatory environment that oversees auditors

64

4/23/2013

33

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

When a CA does not meet the independence requirements relevant to the group audit or the GA has serious concerns about the CA, the GA should obtain sufficient appropriate audit evidence relating to the financial information of the component without making reference to the audit of that component auditor in the auditor’s report on the group financial statements or otherwise using the work of that CA.

65

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements ( AU-C 600)

Materiality – the GA should determine:• Materiality, incl. performance materiality, for group

financial statements• Whether specific circumstances exist for which

something less than materiality would influence users; if so, apply a different materiality to those transactions, balances, or disclosures

• Component materiality for components that will be audited – component materiality s/b lower than group materiality and component performance materiality s/b lower than group performance materiality

• Threshold below which misstatements are trivial

66

4/23/2013

34

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements (AU-C 600)

Performing procedures

For components with significant RMM – an audit or other specific procedures to address those RMM

For components that are not significant, the GA performs analytical procedures

67

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements (AU-C 600)

The requirements for a group auditor who does not make reference to a component auditor’s report, and decides instead to take responsibility for the work of a component auditor has a SIGNIFICANT increase in requirements compared to:

• Current guidance on the matter

• When making reference under this new AU section

68

4/23/2013

35

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements (AU-C 600)

The procedures required for group audits in a financial statement audit apply to federal compliance procedures.

The most likely places group audits applies:• Relying on other auditors who audit major programs

• Auditing major programs when the administration of a major program has “components”

69

American Institute of CPAs

Special Considerations—Audit of Group Financial Statements (AU-C 600)

Understanding the Responsibilities of Auditors for Audits of Group Financial Statements - AICPA Audit Risk Alert• Contains a decision making flowchart

• Examples for not-for-profit organizations and a local government

Product# ARAGRP12P

70

4/23/2013

36

American Institute of CPAs

Technical Practice Aids for Group Audits

41 Technical Questions and Answers

Nonauthoritative guidance to address various questions

Available• in TIS Section 8800, Audits of Group Financial Statements and

Work of Others (AICPA, Technical Practice Aids)

• on AICPA Website at http://www.aicpa.org/interestareas/frc/pages/recentlyissuedtechnicalquestionsandanswers.aspx

American Institute of CPAs

Attestation Standards

4/23/2013

37

American Institute of CPAs

Clarifying the Attestation Standards

Use of clarity format (same as for auditing standards)

Existing attestation standards include four general standards that provide a framework for developing an attestation engagement:• AT section 20, Defining Professional Requirements in

Statements on Standards for Attestation Engagements

• AT section 50, SSAE Hierarchy

• AT section 101, Attest Engagements (which addresses examination and review engagements)

• AT section 201, Agreed-Upon Procedures Engagements

American Institute of CPAs

Clarifying the Attestation Standards

New structure for the general attestation standards:

• Initial section that contains concepts common to all attestation engagements

• Three separate sections for examinations, reviews, and agreed-upon procedures

• These four sections would supersede AT sections 20, 50, 101 and 201

4/23/2013

38

American Institute of CPAs

Clarifying the Attestation Standards

Subject-matter-specific attestation standards:

• Separate sections for each of the six subject-matter-specific AT sections, which address:

- prospective financial information

- pro forma financial information

- internal control over financial reporting

- compliance with laws and regulations

- management’s discussion and analysis

- controls at service organizations

• Build on, not repeat, the requirements and guidance in the applicable general attestation standards

American Institute of CPAs

Clarifying the Attestation Standards

Convergence with standards of the IAASB• Foundation for the common concepts, examination, and review

sections of the proposed attestation standards:

- IAASB exposure draft, ISAE 3000, “Assurance Engagements Other than Audits or Reviews of Historical Financial Information” (April 2011)

- ISAE 3000 is IAASB’s framework standard for assurance engagements (equivalent of attestation engagements)

- ISAE 3410, Assurance Engagements on Greenhouse Gas Emissions

- AICPA’s attestation standards

4/23/2013

39

American Institute of CPAs

Clarifying the Attestation Standards

Exposure drafts

• Proposed common concepts, examination, and review sections

- Expected issuance for comment by end of June (estimate)

• Proposed subject-matter-specific sections

- One or more exposure drafts

- Expected issuance for comment in late 2013 or early 2014 (estimate)

• Will be posted at http://www.aicpa.org/Research/ExposureDrafts/AccountingandAuditing/Pages/ExposureDrafts_ASB.aspx

American Institute of CPAs

Clarifying the Attestation Standards

Final clarified SSAE containing all attestation standards

• One SSAE (SSAE No. 18) even though two or more exposure drafts

- Expected issuance in second half of 2014 (estimate)

- Proposed effective date:

- effective for attestation engagements for which the subject matter or assertion is as of or for a period ending on or after December 15, 2014

4/23/2013

40

American Institute of CPAs

Clarity Project Website Resources

Guide to Clarified and Converged Standards for Auditing and Quality Control

Clarity Project FAQs

Mapping of Existing AUsections to AU-C sections

Listing of Effective Dates of Each AU-C section

Summary of Differences Between Existing SASs and Clarified SASs

American Institute of CPAs

Clarity Project Website Resources

Substantive Differences Between theISAs and GAAS

Scalability of GAAS to theSize and Complexity of an Entity

Videos

4/23/2013

41

81

Helpful Information and Resources

American Institute of CPAs

Helpful Information and Resources

Authoritative standards for non-issuers (SASs, SSARSs, SSAEs, SQCSs) as of June 1 are available at http://www.aicpa.org/Professional+Resources/Accounting+and+Auditing/Audit+and+Attest+Standards/Authoritative+Standards+and+Related+Guidance+for+Non-Issuers/default.htm

4/23/2013

42

American Institute of CPAs

Helpful Information and Resources

AICPA Accounting and Auditing Technical Hotline

• (877) 242-7212• [email protected]

• http://www.aicpa.org/Professional+Resources/Accounting+and+Auditing/Accounting+and+Auditing+Technical+Help/

Questions?