Update on ROK Energy Sector and Energy...

26

Update on ROK Energy Sector and Energy policies May, 2013 Chung, Woojin ([email protected]) Nautilus Institute – East Asia Working Group Meeting

Transcript of Update on ROK Energy Sector and Energy...

Update on ROK Energy Sector and Energy policies

May, 2013

Chung, Woojin([email protected])

Nautilus Institute – East Asia Working Group Meeting

Korea Energy Economics Institute

Content

I Energy Situation and Challenges in Korea

II Energy Policies and Projections

Korea Energy Economics Institute3

I Energy Situation and Challenges in Korea

Korea Energy Economics Institute4

Economic and energy growth

2.00

2.20

2.40

2.60

2.80

3.00

3.20

3.40

100

300

500

700

900

1100

1300

1500

1700

1900

GDP Energy Consumption

Energy/GDP(RHS)

275.7 Mtoe(2011)

toe/th. wonIndex : 1970=100

AAGR(`70~`11)Economy : 7.2%Energy : 6.7%

Korea Energy Economics Institute5

Primary energy shares by sources

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

38.1%

27.8%

2.5%

16.8%

11.7%

0.6%2.4%

Firewood

Oil

Coal(Bituminous)

Coal(Anthracite) Natural gas

Nuclear powerRenewablesHydro

Korea Energy Economics Institute6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

50.2%

16.5%

10.3%

19.3%

0.8%2.9%

Final energy shares by sources

Oil

Coal

Town gas

Electricity

RenewablesHeat

(2011)

Korea Energy Economics Institute7

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Industry Transport R&C Public

Industry

51.3%Transport

19.2%

R&C

26.2%

Public

3.4%

Industry

62.6%Transport

17.5%

R&C

17.7%

Public

2.3%

(1990)

(2011)

Final energy shares by sectors

(Mtoe)

* R&C: Residential & Commerce

Korea Energy Economics Institute8

Generation by energy sources

0

100,000

200,000

300,000

400,000

500,000

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Nuclear Power

Coal

GasCoal

30.2%

Nuclear

24.8%

Gas

27.8%

Oil6.3%

Hydro7.5%

Reneaw

bles

3.3%

Power capacity shares by energy souces

Mar., 2013

Oil(2.5)

Hydro(1.6%)

Renewables(2.5%)Heat(1.5%)

31.1%

40.2%

20.4%

MWh

Korea Energy Economics Institute9

Energy imports

3833 32

3849

67

8695

141

91

122

172

184

9 8 6 7 1015

2124

3823

32

52 56

200

300

400

500

600

700

0

20

40

60

80

100

120

140

160

180

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Energy importcost

Energy import volume(RHS)

Petroleum export revenue

Overseas dependency : 96.3%, Middle Eastern oil dependency : 87%

MtoeBillion US$

Energy import : $184 billion, Energy import/Total import : 32.8%

Korea Energy Economics Institute10

Energy efficiency

0

0.05

0.1

0.15

0.2

0.25

0.3

* The higher share of manufacturing industry in GDP- Share of service industry : ROK 40.1%, Japan 68.2%, USA 76.5%

* The higher share of heavy energy consuming industries in manufacturing- Share of Cement and Steel, Petrochemical in total energy : ROK 45%, OECD 22%

Toe/1,000GDP, 2005 USD

Source : IEA, 2013

Energy efficiencies of selected OECD countries

Korea Energy Economics Institute11

Greenhouse Gas Emission

Energy

85.2%

Industry process9.4%

Agriculture

3.3%

Waste

2.1%

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Million ton CO2eq

* Korea is the World 9th largest GHG emission country

* In 2008, the Korean Government announced a GHG reduction goal of 30% below the BAU level by 2020

GHG shares by sectors(2010)

GHG Emission

Korea Energy Economics Institute12

II Energy Policies and Projections

Korea Energy Economics Institute13

Energy policy direction

Expansion in supply of renewable energy

Increase in capacity of nuclear power

Green technology development both in domestic and towards global markets

Strengthening overseas resources development

Stable energy supply

Energy efficiency improvement

Market-based price system

Low Carbon & Low Energy Consumption Low Fossil Fuel

Development of Green Energy Industry

Promotion of Energy Security

Active involvement in global initiatives for climate change

Basic Policy 1 Basic Policy 2 Basic Policy 3 Basic Policy 4

Energy Vision: Low Carbon Green Growth

The 1st National Energy Basic plan(2009-2030)(established in 2008)

* The national energy basic plan should be revised every 5 year over a period of 20 years by law

Korea Energy Economics Institute 14

Energy demand projection and policy targets

• BAU Scenario : Business as usual(improving energy efficiency at a same speed as in the past

• Target Scenario : Aggressive policies for improving energy efficiency - National plan

0.17

0.22

0.27

0.32

0.37

230

250

270

290

310

330

350

2006 2010 2015 2020 2025 2030

Plan for energy demand & efficiency

12.4% (42Mtoe)Reduction

Demand(BAU)

Demand(Target)

Efficiency-RHS(BAU)

Efficiency(Target)

Mtoe Toe/M.Won

Korea Energy Economics Institute 15

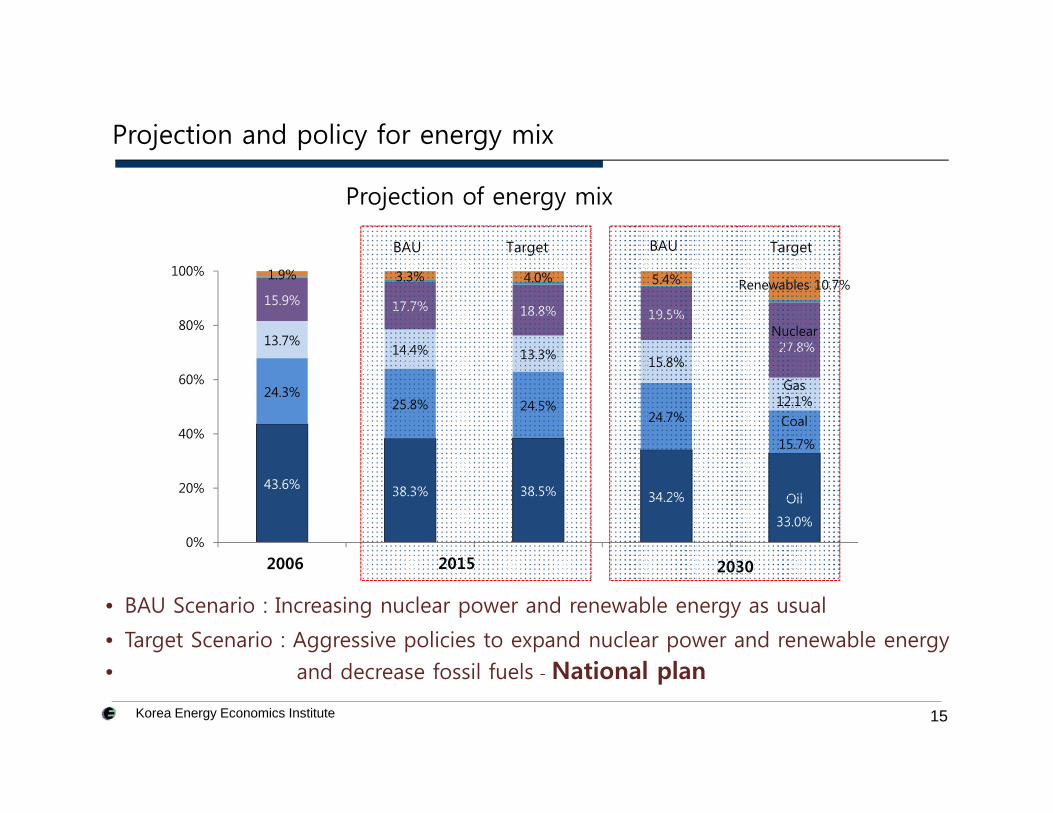

Projection and policy for energy mix

43.6% 38.3% 38.5% 34.2% Oil

33.0%

24.3%25.8% 24.5%

24.7% Coal

15.7%

13.7%14.4% 13.3% 15.8%

Gas12.1%

15.9% 17.7% 18.8% 19.5%Nuclear27.8%

1.9% 3.3% 4.0% 5.4% Renewables 10.7%

0%

20%

40%

60%

80%

100%

2006 2015 20302015 2030

BAU BAUTarget Target

2006

Projection of energy mix

• BAU Scenario : Increasing nuclear power and renewable energy as usual

• Target Scenario : Aggressive policies to expand nuclear power and renewable energy

• and decrease fossil fuels - National plan

Korea Energy Economics Institute16

Fukushima nuclear power accident in 2011

Anti-nuclear movements spread across the nation

Shale gas revolution and decreasing gas price

Change(?) the economics of coal and renewable, nuclear power over gas

Policy failure for market value electricity price

Electricity consumption encouraged and energy efficiency deteriorated

New government and policy review

Less emphasis(?) on “Low Carbon Green Growth”

Factors Impacts

Key factors to affect energy situation after the 1st planning

Korea Energy Economics Institute17

Energy Prices Policy and Its impacts

100

150

200

250

300

350

400

2000200120022003200420052006200720082009201020112012100

120

140

160

180

200

220

2000200120022003200420052006200720082009201020112012

2000=100 2000=100

Electricity

Town gas

Heavy fuel oil

Town gasElectricity

Final energy

Petroleum

Price Consumption

Energy demand in 2012 : (Plan ) 268.Mtoe, (Actual) 277.6Mtoe

Energy efficiency(Toe/GDP) in 2012 : (Plan ) 0.222, (Actual) 0.251

3.4% ↑

13.6% ↓

GDP in 2012 : (Plan ) 1,209 t.won, (Actual) 1,104 t.won 8.7% ↓

Actual/National plan

Korea Energy Economics Institute18

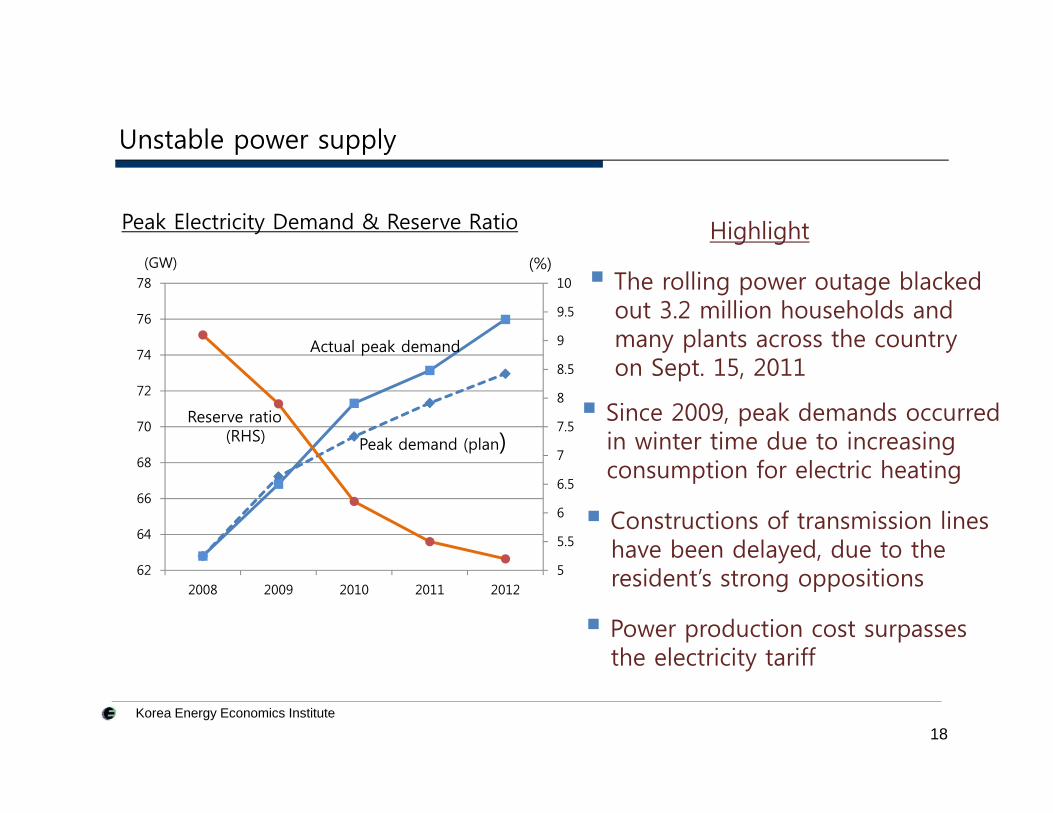

Unstable power supply

5

5.5

6

6.5

7

7.5

8

8.5

9

9.5

10

62

64

66

68

70

72

74

76

78

2008 2009 2010 2011 2012

Reserve ratio(RHS)

Actual peak demand

Peak demand (plan)

The rolling power outage blackedout 3.2 million households andmany plants across the country on Sept. 15, 2011

Since 2009, peak demands occurredin winter time due to increasing consumption for electric heating

(GW) (%)

Peak Electricity Demand & Reserve Ratio

Power production cost surpasses the electricity tariff

Highlight

Constructions of transmission lineshave been delayed, due to theresident’s strong oppositions

Korea Energy Economics Institute19

Measures for unstable power supply

• Completing new power plants early, delaying the abolishment of existingpower plants, and arranging repair work schedules

Measures for tight supply of electricity

• Reducing peak demand with focus on big consumers (more than 1,000kW, 4,000consumers) through incentives

• Strengthening demand management, shifting from regulatory measures toincentives

Challenge

• Introducing an electricity tariff system which induces energy conservation

“ The Korean government announced in June, 2009 to introduce an electricity pricing system that changes in line with international energy, but it has been suspended until now “

Korea Energy Economics Institute

Pressure to reduce nuclear share in energy mix

Challenges in nuclear power

Japan’s nuclear power accident

Loss of the public trusts of nuclear power

Other challenges in nuclear power

Fukushima challenge

• Setting the policy direction for high level radioactive waste

- Full capacity of temporary storage facilities in 2016, but no securing of interim storage- Negotiations on enriching uranium and recycling of spent fuel with US Gov. who

is reluctant to accept Korea’s demand

• Deciding whether to expand the life of nuclear powers- Delaying a decision to expand the life of two aging reactors due to resident and

NGO’s strong protests, though IAEA confirmed safety on them

• Securing the sites for new nuclear power plants- Two places are candidates, but the final decision is uncertain due to anti-nuclear

movements

20

Korea Energy Economics Institute21

Challenges in renewable energy industry

2.4

2.6

2.8

3

3.2

3.4

2008 2009 2010 2011

Failure in reaching a target, though rapidgrowth of renewable industries

Too aggressive target(?)Target

Actual shares

• The number of company : 2.2 times• The number of employees : 4.0 times• Company revenues : 8.2 times• Export of materials and appliances : 8 times

The growth of renewable industry (2007-2011)

↑↑

↑↑

Shrinking renewable markets from domestic and global recession

Introducing RPS system in 2012, replacingFIT scheme

success in inducing investments on renewable energy (?)

*RPS(Renewable Portfolio Standard) is the scheme toforce power producers to supply a certain amount of their power generation portfolio from NRS

*FIT(Feed-In Tariff) is the scheme of the government to compensate producers for the differences between the cost of electricity generated from NRS and thermal generation

<Renewable energy shares for primary energy> Highlight(%)

Korea Energy Economics Institute22

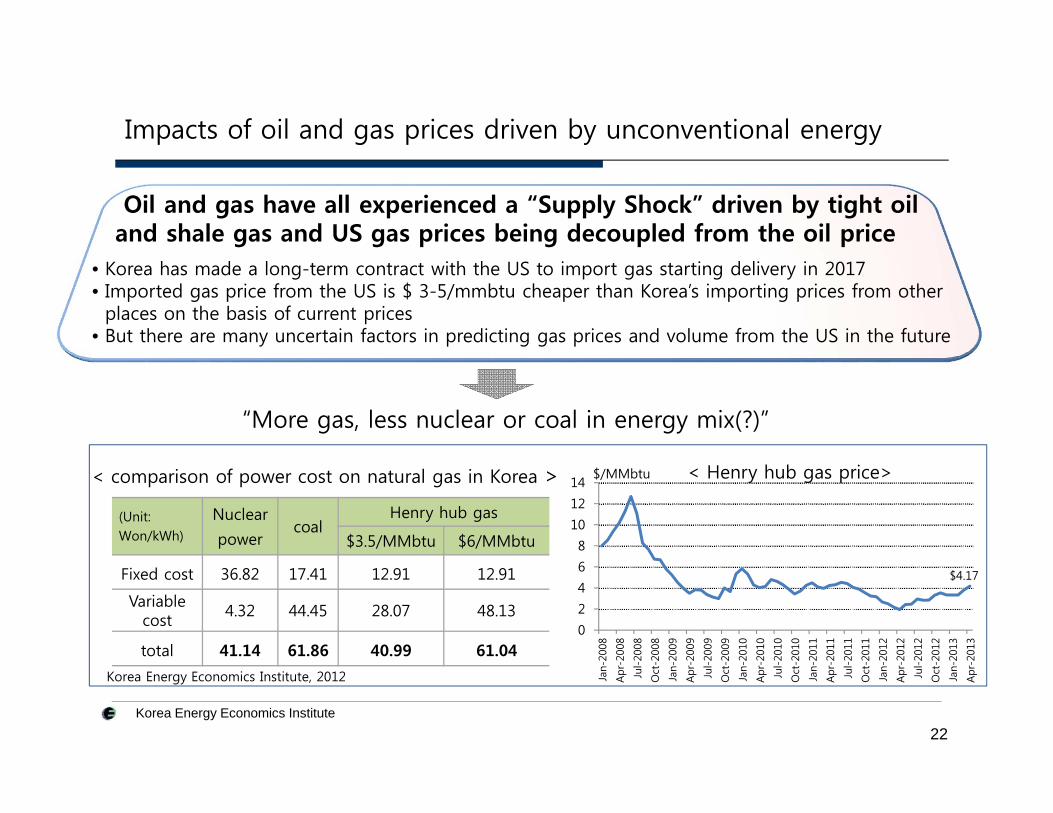

Impacts of oil and gas prices driven by unconventional energy

Oil and gas have all experienced a “Supply Shock” driven by tight oil and shale gas and US gas prices being decoupled from the oil price

• Korea has made a long-term contract with the US to import gas starting delivery in 2017 • Imported gas price from the US is $ 3-5/mmbtu cheaper than Korea’s importing prices from other places on the basis of current prices

• But there are many uncertain factors in predicting gas prices and volume from the US in the future

(Unit: Won/kWh)

Nuclear

powercoal

Henry hub gas

$3.5/MMbtu $6/MMbtu

Fixed cost 36.82 17.41 12.91 12.91

Variable cost

4.32 44.45 28.07 48.13

total 41.14 61.86 40.99 61.04

“More gas, less nuclear or coal in energy mix(?)”

< comparison of power cost on natural gas in Korea >

Korea Energy Economics Institute, 2012

0

2

4

6

8

10

12

14

Jan-

2008

Apr-

2008

Jul-20

08

Oct

-200

8

Jan-

2009

Apr-

2009

Jul-20

09

Oct

-200

9

Jan-

2010

Apr-

2010

Jul-20

10

Oct

-201

0

Jan-

2011

Apr-

2011

Jul-20

11

Oct

-201

1

Jan-

2012

Apr-

2012

Jul-20

12

Oct

-201

2

Jan-

2013

Apr-

2013

< Henry hub gas price>

$4.17

$/MMbtu

Korea Energy Economics Institute23

Energy policy of new government

The new government in Korea will follow the previous government’senergy policies, but with different weights on policies

The details of the policies have not been set yet

Energy policies of new government

• Strengthening the safety management and supervision of energy facilities including nuclear power

• Encouraging more competitive markets and market value prices in energy industries

• Establishing a society system of resource circulation

• Prompting energy cooperation with Northeast Asian countries through grid networks and energy trading

• Enriching energy supports for low income-households

Korea Energy Economics Institute24

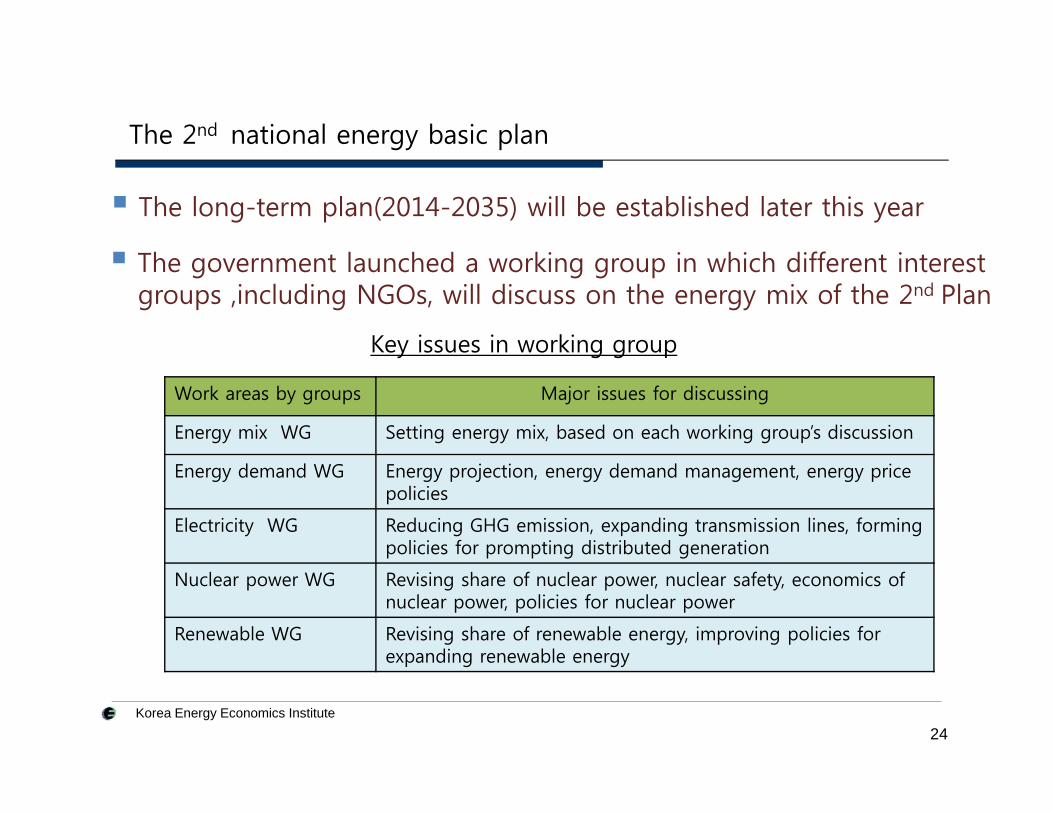

The 2nd national energy basic plan

The government launched a working group in which different interestgroups ,including NGOs, will discuss on the energy mix of the 2nd Plan

The long-term plan(2014-2035) will be established later this year

Work areas by groups Major issues for discussing

Energy mix WG Setting energy mix, based on each working group’s discussion

Energy demand WG Energy projection, energy demand management, energy price policies

Electricity WG Reducing GHG emission, expanding transmission lines, forming policies for prompting distributed generation

Nuclear power WG Revising share of nuclear power, nuclear safety, economics of nuclear power, policies for nuclear power

Renewable WG Revising share of renewable energy, improving policies for expanding renewable energy

Key issues in working group

Korea Energy Economics Institute25

• There is a likelihood that the share of nuclear energy down in energymix of the 2nd national plan

• Then, the shares of fossil fuels like coal or gas would rise, which create conflicts with low carbon policies

The projection of energy mix in the 2nd national plan

• It isn’t expected that the share of renewable energy rises in the 2nd

plan. The share could rather down

Korea Energy Economics Institute26

Thank you for your attention !