Update on Belgian and international VAT … on Belgian and international VAT developments Johan Van...

93

Update on Belgian and international VAT developments Johan Van der Paal Ivan Massin Thomas Vanhee Deloitte Academy 9 December 2015

Transcript of Update on Belgian and international VAT … on Belgian and international VAT developments Johan Van...

Update on Belgian and

international VAT developments

Johan Van der Paal

Ivan Massin

Thomas Vanhee

Deloitte Academy 9 December 2015

Agenda

• Belgian developments

− The new tax point rules 2016

− Company cars – new circular letter

− The new VAT regime applicable to directors-companies

− Other key changes

• International developments

− European Commission workplan and key projects

− Interesting VAT Committee Guidelines

− VAT Expert Group position papers

− Key European Court of Justice rulings

− OECD VAT/GST guidelines

Belgium

New tax point rules 2016

Tax point rules 2016

• New tax point rules introduced as per 1 January 2013

− In framework of implementation of second Invoicing Directive

− E-invoice promoted

− Invoice wording

− Reliable audit trail

− Etc.

− Tax point rules

− Advance invoice no longer a tax point

− Local transactions

• Supply – completion of service

• Advance payment

Tax point rules 2016

• New tax point rules introduced as per 1 January 2013

− Transitional regimes 2013 – 2014

− Choice between old and new regime

− 2014: advance invoice allowed also under new regime but reporting on the

basis of the legal principles

− ‘Final’ or ‘definitive’ regime 2015

− Advance invoice completely restored as tax point

− Payment and recovery no longer linked ratio of new legislation !

− ‘Window’-periode of 3 months to correct initial recovery

• New government end 2014: ‘evaluation’ of these tax point rules

− New draft law introduced in Parliament

Tax point rules 2016

• New regulation does not change:

− Requirement to issue an invoice

− Invoicing wording

− Term to issue an invoice

− Competent member state to determine the invoicing rules

− Definition of taxable event

• In essence: invoice is restored as central document to determine the tax point

and hence the reporting period of transactions

This presentation is based on draft legislation and may be subject to change

New rules

Local supplies: invoice is

tax point

New rules

Local supplies

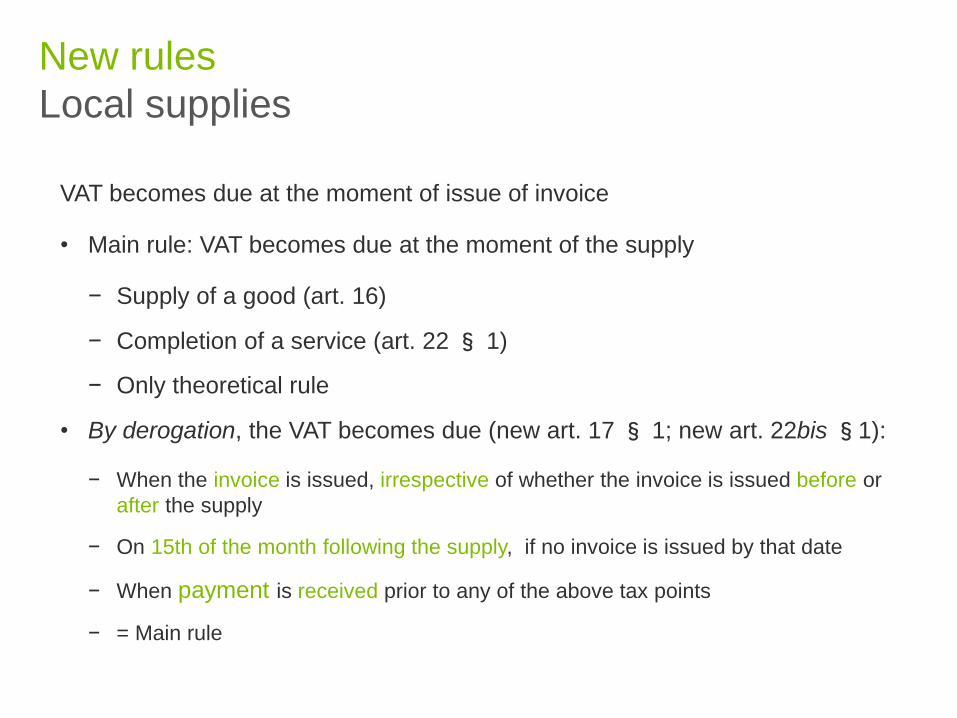

VAT becomes due at the moment of issue of invoice

• Main rule: VAT becomes due at the moment of the supply

− Supply of a good (art. 16)

− Completion of a service (art. 22 § 1)

− Only theoretical rule

• By derogation, the VAT becomes due (new art. 17 § 1; new art. 22bis§1):

− When the invoice is issued, irrespective of whether the invoice is issued before or

after the supply

− On 15th of the month following the supply, if no invoice is issued by that date

− When payment is received prior to any of the above tax points

− = Main rule

New rules

Local supplies

VAT becomes due at the moment of issue of invoice

• Relevance of moment of supply (taxable event)

− Starting point of ultimate date to issue an invoice

− VAT becomes due even if no invoice is issued

• Date of taxable event

− Has to be mentioned on the invoice (see above, relevance of date of

supply)

− If different from the invoice date

• Pro memorie: local sale =

− Local supply of goods, loca (reverse charge) services, international B2B

services, cross-border services other than the ones covered by main B2B

rule, …

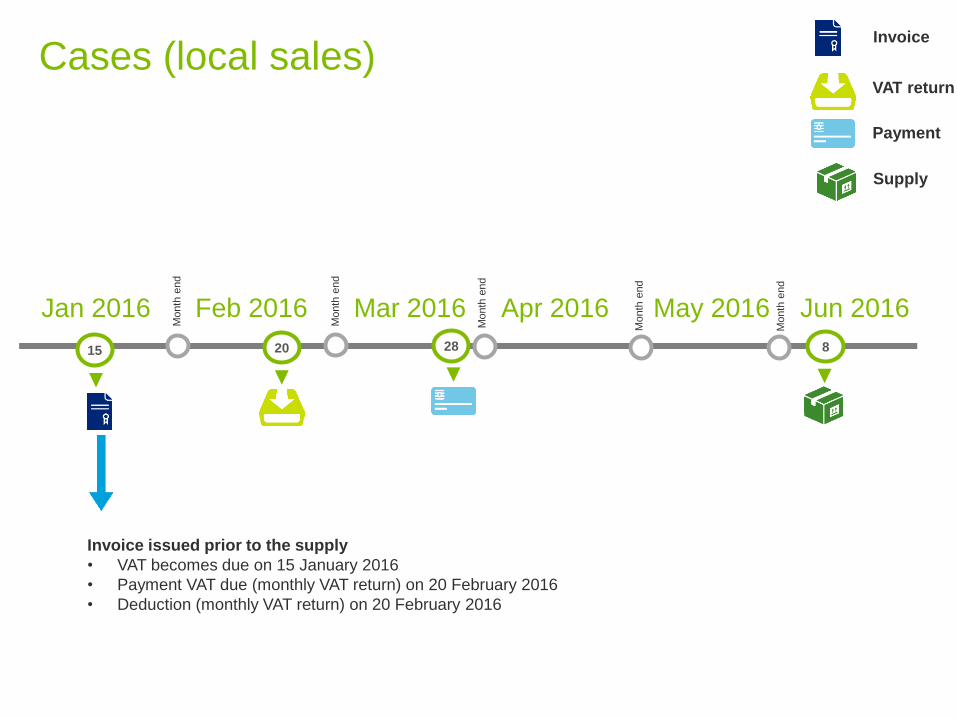

Cases (local sales)

Jan 2016

15

Month

end

Feb 2016 Mar 2016M

onth

end

2820 8

Invoice issued prior to the supply

• VAT becomes due on 15 January 2016

• Payment VAT due (monthly VAT return) on 20 February 2016

• Deduction (monthly VAT return) on 20 February 2016

Month

end

Apr 2016

Month

end

Month

end

Jun 2016May 2016

Invoice

VAT return

Payment

Supply

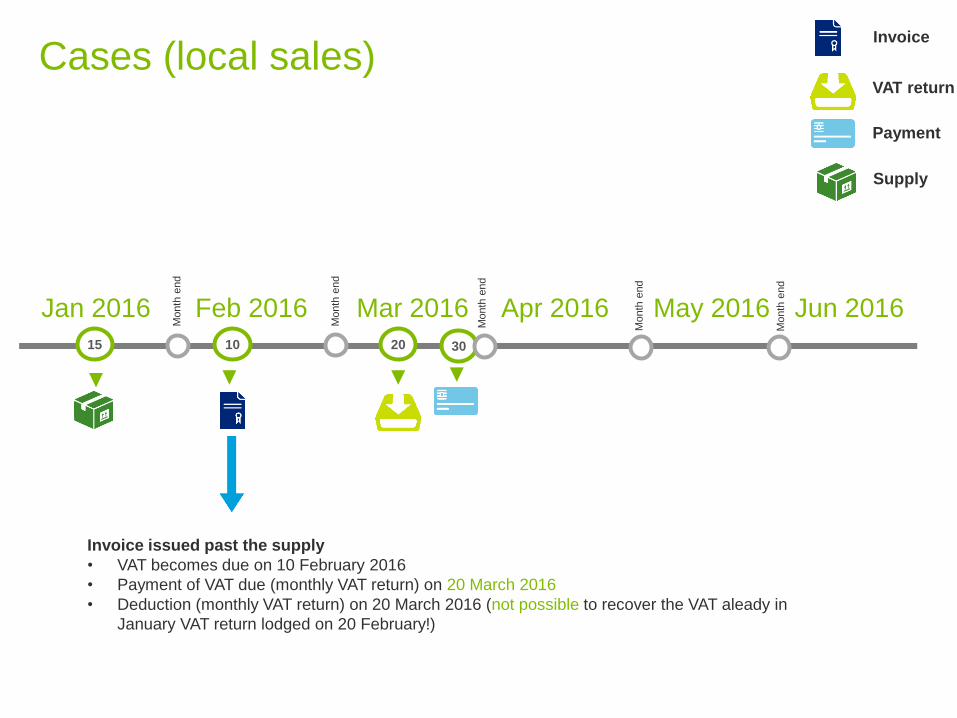

Cases (local sales)

Jan 2016

15

Month

end

Feb 2016 Mar 2016M

onth

end

3010 20

Invoice issued past the supply

• VAT becomes due on 10 February 2016

• Payment of VAT due (monthly VAT return) on 20 March 2016

• Deduction (monthly VAT return) on 20 March 2016 (not possible to recover the VAT aleady in

January VAT return lodged on 20 February!)

Month

end

Apr 2016

Month

end

Month

end

Jun 2016May 2016

Invoice

VAT return

Payment

Supply

Cases (local sales)

Jan 2016

17

Month

end

Feb 2016 Mar 2016M

onth

end

225 20

No invoice issued on 15th of month following the supply

• VAT becomes due on 15 February 2016

• Payment of VAT due (monthly VAT return) on 20 March 2016

• Deduction (monthly VAT return) on 20 March 2016 (provided invoice received by then – see

general formal conditions to recover upstream VAT)

Month

end

Apr 2016

Month

end

Month

end

Jun 2016May 2016

Invoice

VAT return

Payment

Supply

15

Cases (local sales)

Jan 2016

15

Month

end

Feb 2016 Mar 2016M

onth

end

3010 20

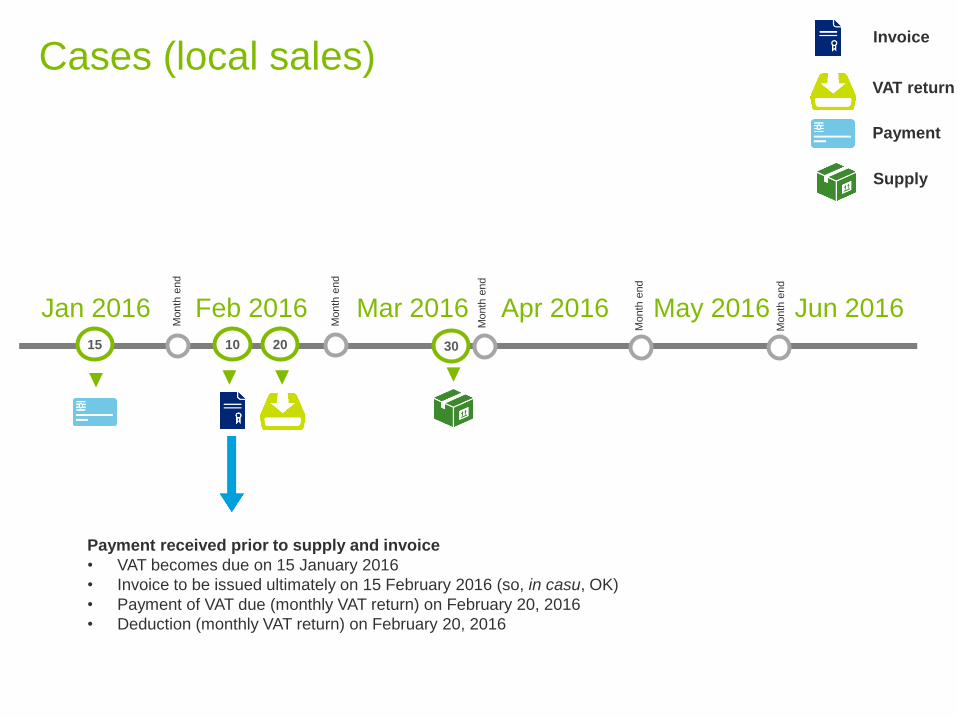

Payment received prior to supply and invoice

• VAT becomes due on 15 January 2016

• Invoice to be issued ultimately on 15 February 2016 (so, in casu, OK)

• Payment of VAT due (monthly VAT return) on February 20, 2016

• Deduction (monthly VAT return) on February 20, 2016

Month

end

Apr 2016

Month

end

Month

end

Jun 2016May 2016

Invoice

VAT return

Payment

Supply

New rules

When?

• The new rules will enter into force on 1 January 2016

• For supplies when the VAT becomes due as per 1 January 2016

• Transtional rules needed ?

− Supply on 17 December 2015

− Invoice on 10 January 2016

− Tax point 17 December 2015 (old rules) or 10 January 2016 (new rules)?

New rules

Intracommunity trans-

actions: no changes

Other rules

Intracommunity supplies of goods and services

These rules are not changed

• Intracommunity supplies of goods : tax point arises :

− At invoice date, if invoice issued for a supply made

− Ultimately 15th of the month following the supply date, if no invoice is issued by then

− Advance invoice cannot trigger tax point

− Also advance payment is disregarded

• Intracommunity services : tax point arises at :

− Completion of the service

− Receipt of an advance payment

− Advance invoice cannot trigger tax point

• Transitional regimes allow flexibility via administrative tolerances : to be continued ?

Cases (intracommunity supply goods)

Jan 2016

17

Month

end

Feb 2016 Mar 2016M

onth

end

225 20

Invoice issued prior to supply (cf. tolerance)

• VAT becomes due on date of invoice provided the invoice ‘confirms’ the supply = earliest tax

point possible is supply

• Invoice/payment not reported

• Transaction reported in March 2016 VAT return (due on 20 April 2016)

Month

end

Apr 2016

Month

end

Month

end

Jun 2016May 2016

Invoice

VAT return

Payment

Supply

15

Cases (intracommunity services)

Jan 2016

17

Month

end

Feb 2016 Mar 2016M

onth

end

225 20

Invoice issued prior to supply

• VAT becomes due on date of payment = earliest tax point possible is supply

• Transaction reported in February 2016 VAT return (due on 20 March 2016)

Month

end

Apr 2016

Month

end

Month

end

Jun 2016May 2016

Invoice

VAT return

Payment

‘Completion’

15

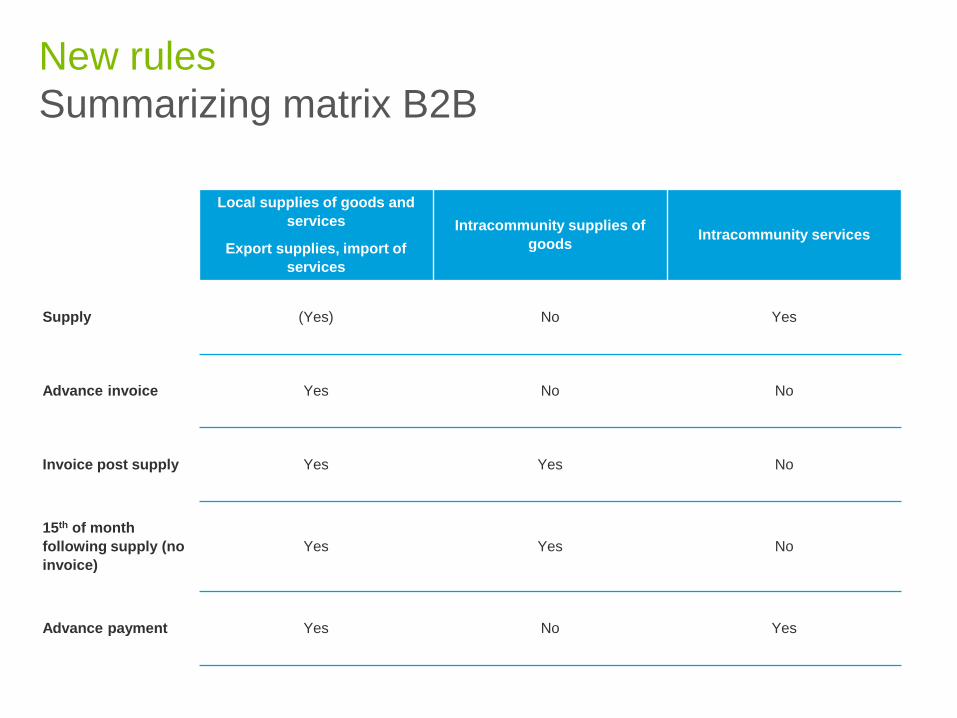

Local supplies of goods and

services

Export supplies, import of

services

Intracommunity supplies of

goods Intracommunity services

Supply (Yes) No Yes

Advance invoice Yes No No

Invoice post supply Yes Yes No

15th of month

following supply (no

invoice)

Yes Yes No

Advance payment Yes No Yes

New rules

Summarizing matrix B2B

New rules

New cash regime ‘B2G’

New rules

B2G

Introduction of new tax point rule for supplies to ‘public bodies’

• Already administrative tolerance: VAT becomes due at the moment of approval of the

invoiced amount (= date formal approval – Decision nr. E.T. 124.433 dd. 17 April 2014)

• New regulation (new art. 17 § 4 – art. 22bis§ 4)

− Public body = art. 6

− Also includes public bodies with VAT number

− Does not include ‘public companies’ (= regular, art. 4 VAT taxable persons)

− At the moment (part of) the price is received

− Not applicable in the case of reverse charge

− VAT number of the public body (cf. immovable work)

− Immovable transactions (cf. DBFM)

Other rules

B2C

These rules will not change

• VAT becomes due at the moment of receipt of payment

− Even if invoice (voluntarily) is issued prior to payment

Belgium

Company cars

Company cars

• Circ. letter n°. AOIF 36/2015 of 23 November 2015

− Additional comments to regime introduced 2011 (applicable as of 2013)

• Recap

− Private use for free or against consideration

− If for free, private use taxed through recovery limitation (art. 45 § 1quinquies

VAT Code)

− Fringe benefit no longer subject to VAT

− 3 methods

• Kilometres

• Semi lump sum (formula)

• 35%

− If against contribution, VAT due on this contribution

− But de minimis via ‘normal value’

Company cars

• What’s new ?

− Consideration

− Also via R/C – C/C or through ‘salary sacrifice’

− Car options

• Car remains for free

• Full recovery of VAT on option cost

• Conditions

− For free

− Commuting (management companies)

− Recovery requires minimal professional use (10%)

• But not applicable in the case of ‘salary policy’

− 3 methods and mixed VATable persons

• Expense * (50 – 35%) * Pro rata

Other business items

• Fuel card (when not combined with company car)

− 75% rule not allowed

− Real use (kilometre administration – agreement with the VAT authorities)

• Electricity and heating (management company)

− Full recovery

− VAT on fringe benefit income taxes

Belgium

Directors-companies

Introduction

• Decision n°. E.T.125.180 dd. 20.11.2014

− Until now, director acting through a company (‘director-co’) in principle was

subject to VAT, unless ‘option’ not to VAT register (1994)

− Over past period, few changes (option: in principle ‘all or nothing’ and

‘definitive’)

− Directors-physical persons: not subject to VAT

• What changes ?

− Director-co becomes VAT taxable person (option regime is abolished) as of 1

April 2016 (see below on entry into force)

− Director-physical person: no changes

Impact: VAT leakage

• Due to ‘option’ regime, director-co is mostly optimised in practice

− No VAT on director fees if the company in which the director is appointed,

cannot (fully) recover VAT

− Legal qualification as director fee gives blanket VAT exemption

− Limited VAT cost in the hands of the director-co

− Director-co in fully VAT taxable person, mostly subject to VAT

• New regime will imply VAT leakage when director-co is appointed in exempt

business or (passive) holding:

− ‘Care’ sector (hospitals, elderly homes)

− Financial intermediaries

− Non-profit (cultural sector)

− Private equity sector (holdings)

− Public sector

Impact: VAT leakage

• Cut off date of 1 April 2016

− ‘Tantièmes’ : date of approval by the General Assembly

− If later in 2016: then VAT applies, irrespective of closing date annual

accounts ?

− Periodical payments: normal tax point date

− End of period to which the periodical fee relates

• E.g. invoice May 6 for fee covering January – April 2016: no VAT

• ‘Advance’ invoice prior to 1 April 2016 ?

Alternatives (all sectors)

• Switch to director-physical person

− Formalities (dismiss co and appoint physical person)

− Liability

• Regulation for small enterprises (25,000 euro cap as per 1 January 2016)

• Billing before 1 April 2016

− One-off benefit

− ‘Intermediate tantième’ granted prior to 1 April 2016 ?

Alternatives (all sectors)

• VAT grouping

− Director-co’s and Opco create VAT grouping

− Director fees covered by VAT grouping – No VAT

− ‘Large’ interpretation of financial link

• Bottom-up approach

• No link required between the management companies

− No abuse

Alternatives (VAT exempt sectors)

• Combination of director fee with operational services (exempt)

− Most straightforward approach : split between

− director fee as physical person

− VAT exempt operational services by the company

− Split between ‘service fee’ (exempt) and director’s fee

− 25% rule as lump sum allocation of fee to director’s services

− If not possible, combination of 25,000 euro cap for ‘director-co’-fees, with

exemption for remainder regarding operational services

− Contract should foresee in split

− Support for valuation

• ‘Part Service’ case law

Belgium

Other key changes 2016

New rules

New control centre ‘Large enterprises’

• 7 regional control centres (Antwerp, Bruges, Brussels, Charleroi, Ghent,

Liège, Louvain) and 1 central control centre (specialised teams)

• Competent for large enterprises

− Criteria

− > 100 employees, or

− Two out of three:

• (i) Average number of employee 50 or (ii) Annual turnover 7.3 MEUR or (iii)

Balance sheet total 3.65 MEUR

− Always: finanial sector, funds – VAT grouping

− Practical impact

− Who to contact ?

− First experiences ?

New rules

Extension of local reverse charge (announced)

Extension of local reverse charge for a number of specific types of supplies

(immovable work, investment gold, greenhouse gas emission trading)

• Supply of waste products becomes subject to reverse charge

− Current 0% VAT rate

Reverse charge for foreign taxable persons also will apply when recipient is

another non-resident business with a direct VAT registration

− Currently only for recipient resident business and for non-resident with

fiscal representative

Cost sharing exemption

Existing legislation

On EU level and in Belgium, a VAT exemption applies for cost sharing

arrangements if the following conditions are met:

• Independent group of persons supplying services;

• The members render VAT exempt activities or do not qualify as VAT taxable

person;

• The services of the independent group of persons are directly necessary for the

exercise of the (VAT exempt) activities of the members;

• Exact reimbursement of the expenses;

• Should not distort competition.

Infringement by European Commission

The European Commission has initiated a procedure against Belgium on the cost

sharing exemption.

The main points of criticism :

• the eligibility of the Members : possibility to have members who use the shared services

for taxable services within a certain threshold

• the "out of the scope" qualification of the resources shared by a Member towards a cost

sharing association organised as an indivision;

• the deductibility of the input VAT suffered by the cost sharing association at the level of its

members (pass-through VAT).

Also Luxembourg has been attacked before the CJEU on similar points.

Cost sharing exemption

Way forward – change of legal regime

Current “cost sharing exemption” regime is about to change (draft law in preparation)

• Threshold of max 10% of taxable activities abandoned

- Members can have taxable activities but exempt activities should be predominant

- Only services that are directly necessary and contribute to the achievement of the

corporate purpose of the members

- Services can be provided to third parties:

- Services can be to members and non-members but only services to members eligible for

exemption - CSA may become mixed taxpayer

- Limitation: 50% maximum threshold for services to non-members to ensure mutualisation

approach

• Notification of the existence of a cost sharing association and VAT reporting

obligations

Cost sharing exemption

New rules

Changes in VAT rates real estate

• Renovation of dwellings

• Dwellings older than 5 year increased to 10 years

• Transitional regime for dwellings 2007 – 2010 can continue at 6% up till

end of 2017 if :

− Building permit obtained before 31 December 2015

− Contract lodged with local VAT office before 31 December 2015

• Introduction of 6% for construction and renovation of schools

• Introduction of 12% for private investors in social housing

International

developments

Agenda

• International developments

− Introduction

− The European Commission work programme

− VAT committee

− VAT expert group

− Key CJEU case law

− OECD

Introduction

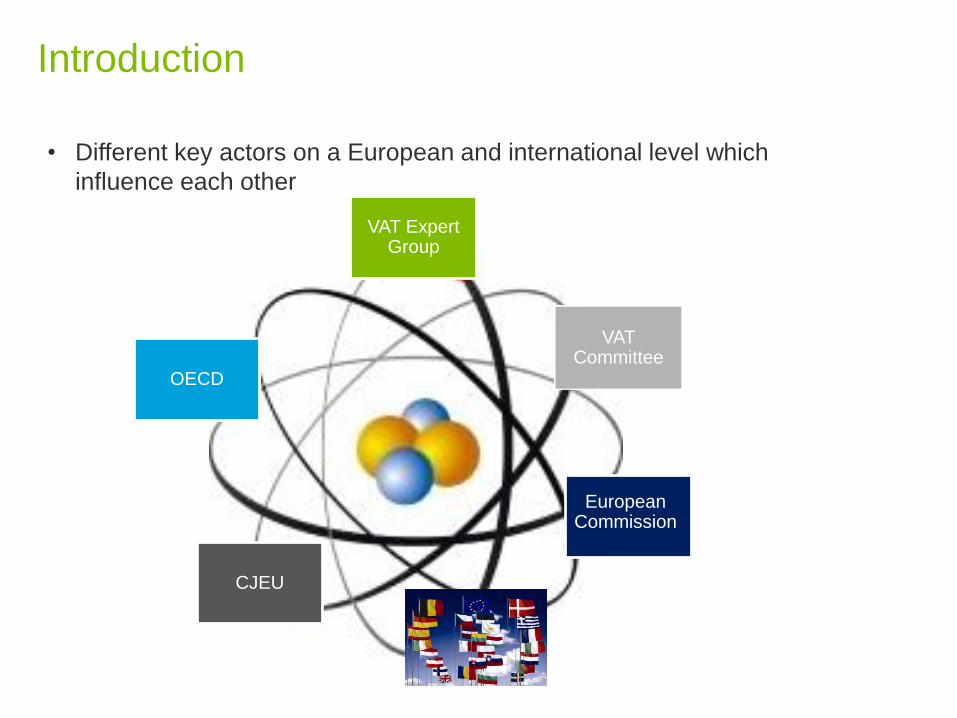

Introduction

• Different key actors on a European and international level which

influence each other

VAT Expert Group

OECD

VAT Committee

European Commission

CJEU

European Commission

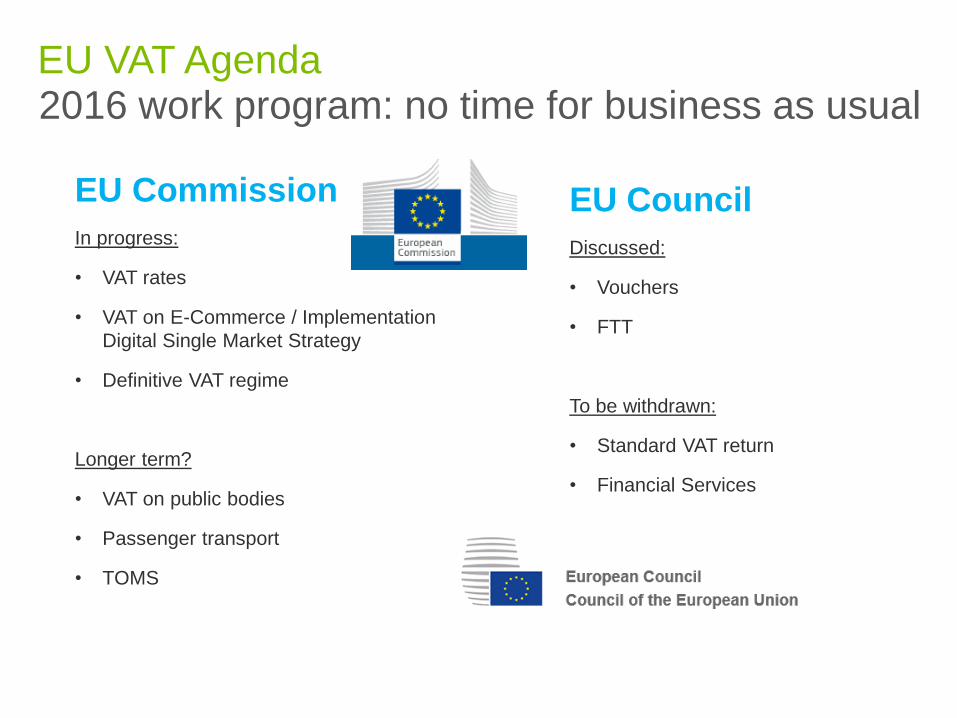

EU VAT Agenda2016 work program: no time for business as usual

EU Council

Discussed:

• Vouchers

• FTT

To be withdrawn:

• Standard VAT return

• Financial Services

EU Commission

In progress:

• VAT rates

• VAT on E-Commerce / Implementation

Digital Single Market Strategy

• Definitive VAT regime

Longer term?

• VAT on public bodies

• Passenger transport

• TOMS

Digital Single Market Strategy

Proposal in 2016 – policy options

1. Status quo

2. Abolish the Low Value Consignment Relief (LVCR) and the thresholds for distance

sales – No simplifications

3. Abolish LVCR and distance sales thresholds + implement a low threshold for

incidental cross border supplies (in addition to the local threshold)

4. Add a Single Electronic Mechanism (SEM) applying to all intra-EU B2C supplies of

goods and services and for imports up to 150 EUR

5. Add home country legislation and control, limit SEM to VAT rates and exemptions of

the MS where the supply takes place, or

6. Add fully harmonized rules for the SEM subject to applying the VAT rates and

exemptions of the MS where the supply takes place

European Commission

Explanatory notes on POS services connected with

immovable property

• Article 47 EU VAT directive:

“The place of supply of services connected with immovable property, including the

services of experts and estate agents, the provision of accommodation in the hotel

sector or in sectors with a similar function, such as holiday camps or sites

developed for use as camping sites, the granting of rights to use immovable

property and services for the preparation and coordination of construction work,

such as the services of architects and of firms providing on-site supervision, shall

be the place where the immovable property is located.”

• Provisions Implementing Regulation entering into force on 1 January 2017

• Explanatory notes not legally binding – constitute the view of the Commission

European Commission

Explanatory notes on POS services connected with

immovable property

• Immovable property

• Any specific part of the earth, on or below its surface, over which title and possession

can be created

• Any building or construction fixed to or in the ground above or below sea level which

cannot be easily dismantled or moved

• Any item that has been installed and makes up an integral part of a building or

construction without which the building or construction is incomplete, such as doors,

windows, roofs, staircases and lifts

• Any item, equipment or machine permanently installed in a building or construction

which cannot be moved without destroying or altering the building or construction

European Commission

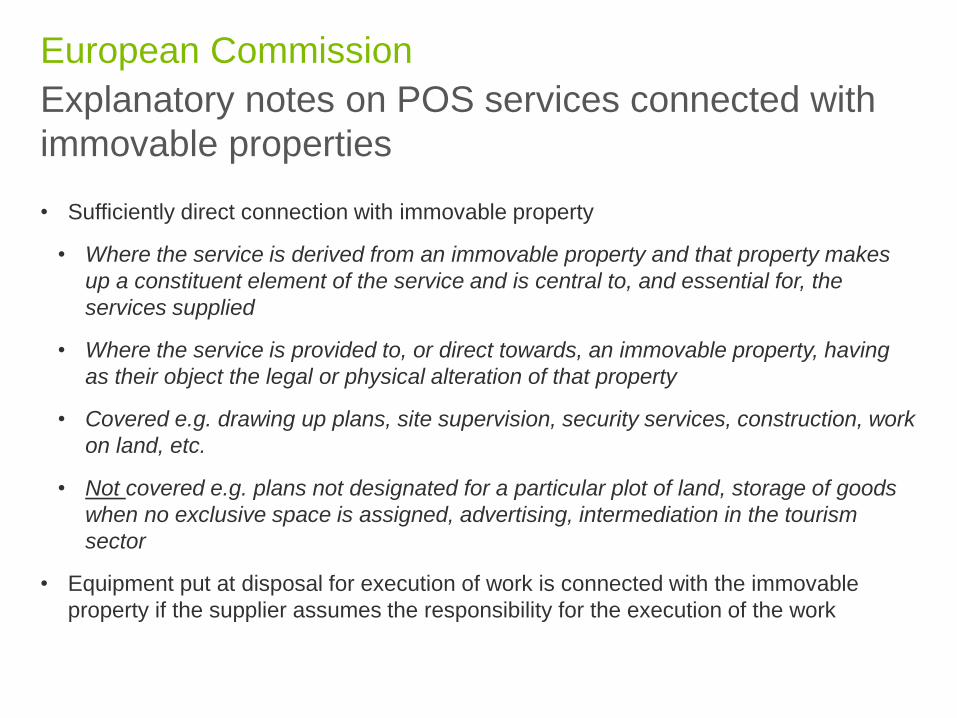

Explanatory notes on POS services connected with

immovable properties

• Sufficiently direct connection with immovable property

• Where the service is derived from an immovable property and that property makes

up a constituent element of the service and is central to, and essential for, the

services supplied

• Where the service is provided to, or direct towards, an immovable property, having

as their object the legal or physical alteration of that property

• Covered e.g. drawing up plans, site supervision, security services, construction, work

on land, etc.

• Not covered e.g. plans not designated for a particular plot of land, storage of goods

when no exclusive space is assigned, advertising, intermediation in the tourism

sector

• Equipment put at disposal for execution of work is connected with the immovable

property if the supplier assumes the responsibility for the execution of the work

European Commission

Explanatory notes on POS services connected with

immovable properties

• When analysing the following elements should be taken into account (not

comprehensive)

• Where the services cover more than one jurisdiction, the taxation rights should be

split proportionally between the jurisdictions concerned

• Where more than one immovable property is involved in the supply each of them has

to be clearly identified or identifiable

• Several specific immovable properties? Service cannot be considered as lacking a

sufficiently direct connection with immovable property

• Supply off-site, not directly to the owner or to a client in a different country is not

decisive on its own

=> Influence on Belgian practice and practice in other EU MS?

European Commission

VAT Committee

Role & recent topics

• Task:

- Article 398 of the VAT Directive

- To promote the uniform application of the provisions of the VAT Directive

- Advisory committee only, no legislative power

- Cannot take legally binding decisions

- Guidance on the application of the VAT Directive

• Members:

- Consists of representatives of the EU MS and of the Commission

- The chairman of the Committee shall be a representative of the Commission

VAT Committee

Guidelines

The VAT Committee examines questions concerning the application of EU VAT provisions

raised by the Commission or a Member State. As a result of the discussion, the VAT

Committee may agree guidelines on specific matters:

o Merely views of an advisory committee

o They do not constitute an official interpretation of EU law and do not necessarily

have the agreement of the European Commission

o They do not bind the European Commission or the Member States who are free

not to follow them

o Comprehensive summary of guidelines approved by the VAT Committee

between November 1977 and November 2015

o Rapid publication of new meeting documents and guidelines - transparency

VAT Committee

Recent interesting topics discussed - crowdfunding

• Donation based crowdfunding no VAT issues should arise since the contributor

expects no reward and none is given

• Reward based crowdfunding

− Taxable transaction provided there is a direct link between the supply of goods or services

and its correspondencing consideration and the entrepreneur is acting as such

− Goods or services are identified precisely, contribution is regarded as a payment

− Reward is of symbolic value? Needs to be assessed on a case by case basis

• Crowd-investing

- Supply by the entrepreneur is a taxable supply

- If the financial reward is participation in securities, it supply may be exempt

• Crowd-lending

- Taxable transactions which is VAT exempt

• Intermediation by crowdfunding platforms

− Economic activities which could be VAT exempt

VAT Committee

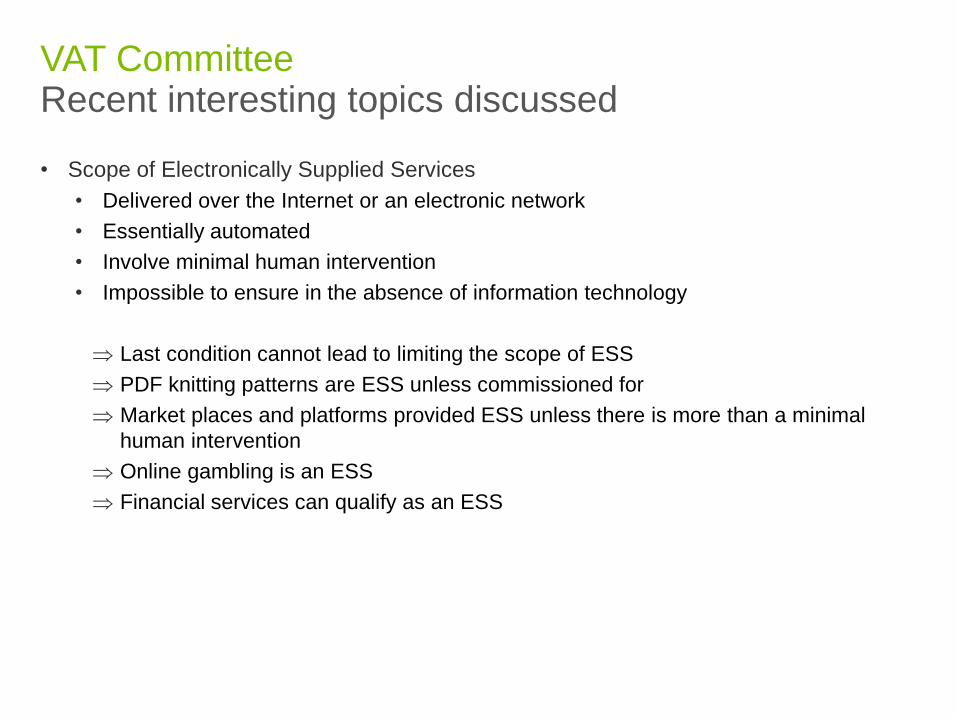

Recent interesting topics discussed

• Scope of Electronically Supplied Services

• Delivered over the Internet or an electronic network

• Essentially automated

• Involve minimal human intervention

• Impossible to ensure in the absence of information technology

Last condition cannot lead to limiting the scope of ESS

PDF knitting patterns are ESS unless commissioned for

Market places and platforms provided ESS unless there is more than a minimal

human intervention

Online gambling is an ESS

Financial services can qualify as an ESS

VAT Committee

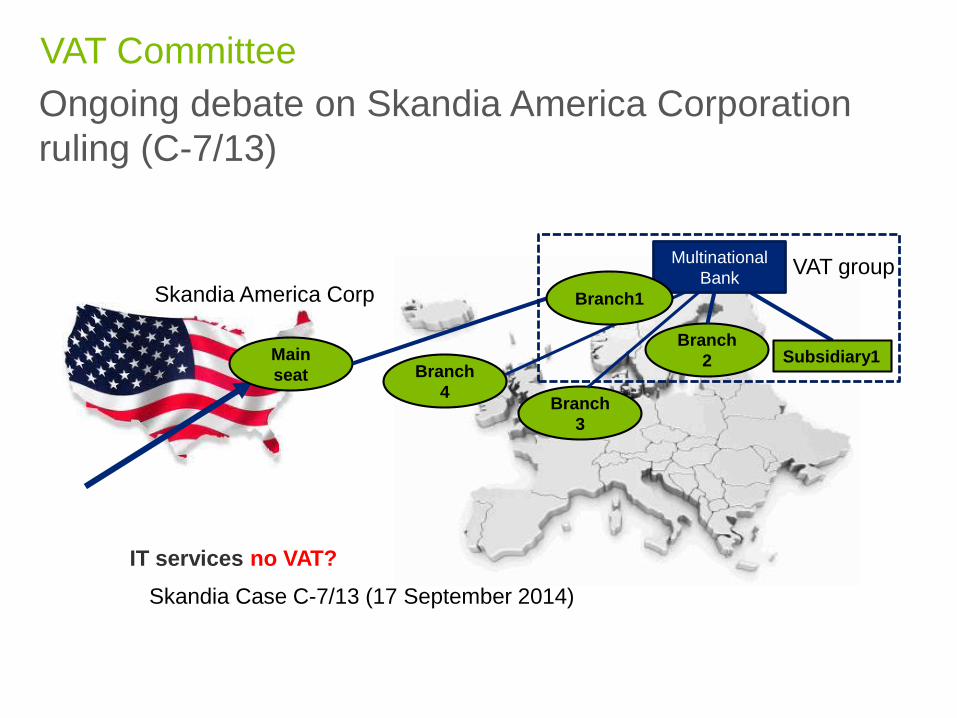

Ongoing debate on Skandia America Corporation

ruling (C-7/13)

IT services no VAT?

Skandia Case C-7/13 (17 September 2014)

Branch

2 Main

seat

Branch

3

Branch

4

Subsidiary1

VAT group

Skandia America Corp

Multinational

Bank

Branch1

VAT Committee

CJEU: in that particular case: supply from head office to branch subject to VAT since

branch member of VAT group

Different interpretations in EU Member States… or no interpretation yet

European Commission working paper :

EU VAT Expert group recommendations:

− Strict interpretation (“Swedish” style VAT groups, involvement 3rd countries,

inbound supplies)

− To be seen in context of abuse: only if no anti-abuse provisions implemented

− Change Directive to tax all head office – branch transactions?

Ongoing debate on Skandia America Corporation ruling (C-

7/13)

VAT Committee

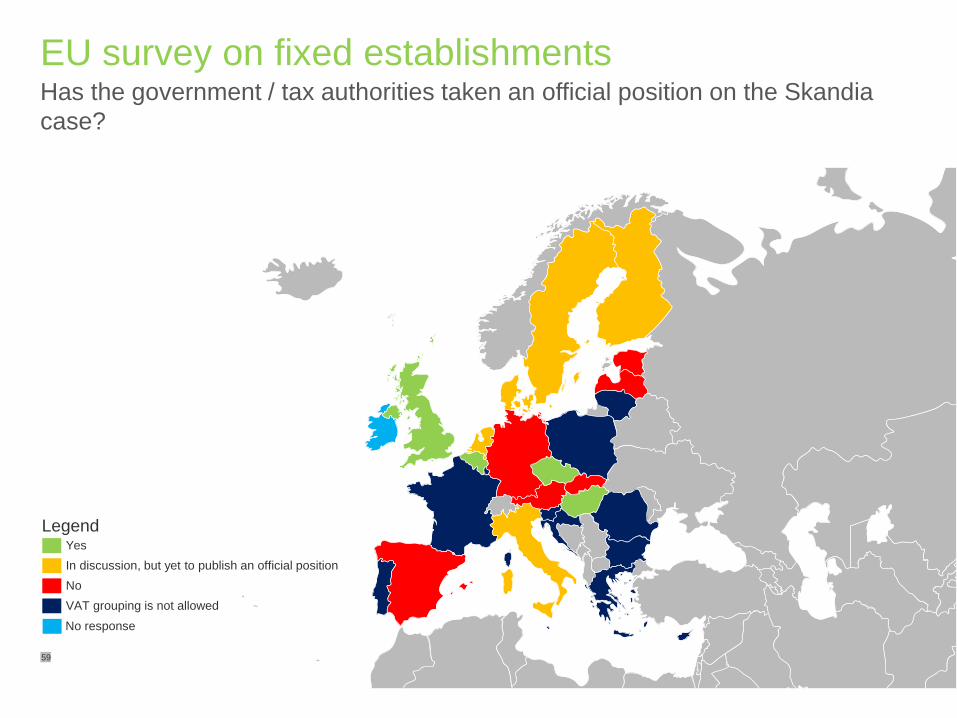

© 2015 Deloitte The Netherlands

Has the government / tax authorities taken an official position on the Skandia

case?

EU survey on fixed establishments

59

Yes

In discussion, but yet to publish an official position

No

VAT grouping is not allowed

Legend

No response

• Decision E.T. 127.577 of 3 April 2015

• Apply Skandia with all situation with multiple establishments where one

establishment is in Belgium

• Also apply Skandia between fixed establishments of a taxable person if

one of the fixed establishments is part of a VAT group in Belgium

• VAT recovery depends on the VAT status of the VAT group

• No VAT recovery when supplies invoiced to the Belgian head office but

essentially supplied for the purposes of the foreign branch

• Article 19bis of the Belgian VAT code abolished

• Administration applies the regime as of 1 July 2015

Broad implementation of Skandia principlesBelgian position

VAT Expert Group

Role & recent topics

• Assisting and advising the European Commission on VAT matters

• Members are businesses, business associations and consulting companies

• Relevant recent topics

• Future of intra-community supplies of goods

− According to a recent study:

− A significant reduction in compliance cost is achieved when the regime applicable to intra-community

supplies of goods is aligned with the principles applicable to B2B supplies of services

− A significant reduction in the scale of VAT fraud is achieved when i) taxing goods following the flow of

their goods with the supplier charging the VAT of the MS of destination, or ii) taxing goods following the

contractual flow with the supplier charging the VAT of the MS of destination – reporting through an OSS

- VEG’s opinion

- Need to further study the concept of an enhanced one stop shop, the concept of certified taxable person

(CTP) with the reverse charge mechanism, a special scheme for call-off stocks and possible anti-evasion

measures

EU VAT Expert Group

Role & recent topics

• Proof of evidence for intra-Community supplies

− Uniform documentary evidence for ICS?

− No one size fits all approach but a selection of 3 elements of non-contradictory evidence from

a pre-established list (similar to the provisions in place for TBE-services)

− Will now be submitted to the VAT committee for discussions

EU VAT Expert Group

Court of Justice of the

European Union

On the agenda

Court of Justice of the European Union

• VAT PE (Welmory)

• Use of exemptions & flash title supplies (Fast

Bunkering Klaipeda)

• VAT recovery for holding companies (Larentia +

Minerva)

• Sveda

• NLB Leasing

16 October 2014 - Welmory (C-605/12)

Welmory Sp. Z.o.o Welmory Ltd.

Sale of bids

Bids

Goods

Cooperation agreement

Reverse charge service invoice(advertising, servicing, provision of information & data processing)

FE? Invoice + Polish VAT?

Court of Justice of the European Union

VAT PE

• What can we learn from Welmory?

• Digital services: suitable structure requires computer equipment,

servers & software

• Being able to receive & use the services for performing its

economic activities

• Absence of human presence could suffice

• However reference to the national court, no fixed decision

• Not determining factors:

• Fact that economic activities of both companies, which are linked

to a cooperation agreement, form an economic whole

• Fact that results of combined efforts essentially benefit consumers

in Poland

VAT PE

• What can we learn from Welmory?

• Required suitable structure could be owned by a third party

• Level of control of that structure to be determined

• Seems to allow to still distinguish purchase FE from sales FE (cf.

auxiliary & preparatory)

VAT PE

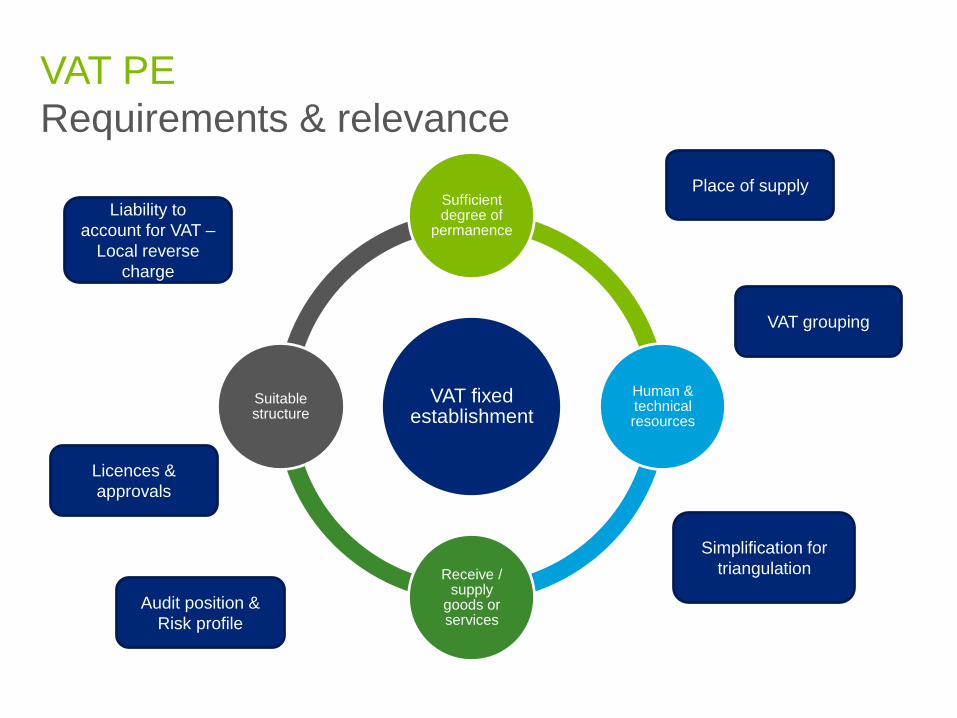

Requirements & relevance

VAT fixedestablishment

Sufficientdegree of

permanence

Human & technicalresources

Receive / supply

goods or services

Suitablestructure

Place of supply

Licences &

approvals

Liability to

account for VAT –

Local reverse

charge

Simplification for

triangulation

Audit position &

Risk profile

VAT grouping

VAT PE

• Although legal definition & high practical relevance >< concept not fully

clear

• Different notions of “established” for different VAT rules?

• Purchase (passive) FE; Sales (active) FE; other?

• “Suitable structure”

• Determine in function of nature of business carried out?

e.g. fully digitalised services vs. ‘traditional‘ supply of goods

• Also if merely auxiliary and preparatory activities?

• Today: not all questions answered > uncertainty for businesses

… But also opportunities

• National evolutions (rulings, case law, etc.)

• Notion of VAT PE subject to further investigation of EU VAT expert group:

► determine criteria for VAT PE

• being able to perform the full supply vs. preparatory &

auxiliary?

• TP remuneration type (cost plus vs. profit split)?

• technical resources prevail over human presence ?

• business dependent?

=> Report VEG will be submitted to the VAT committee

VAT PE

Background

VAT exemptions & flash title supplies

• Traders established in one country trading goods situated in/moving

between many countries

• VAT exemptions (with credit) are crucial to minimising VAT registration

requirements and cash flow implications of trade:

• Exemptions for intra-Community transactions

• Exemptions on exportation / importation

• Exemptions related to international transport

• Exemptions for transactions relating to international trade (warehouses /

tax suspension)

Fast Bunkering Klaipeda UAB (C-526/13)

VAT exemptions & flash title supplies

FBK (LT) INTERMEDIARIE

S

CUSTOME

R

Sale

VAT?

Sale

VAT exempt?

148 (a) VAT

Dir

• Fuel physically delivered by FBK to vessel operator; legal ownership (and

invoices) through intermediary

• Likely that legal ownership only passed to intermediaries once fuel

delivered to vessel operator

• Fuelling intermediaries prefer not to be charged VAT – and to have no

domestic VAT registration / credit position

Fast Bunkering Klaipeda UAB

VAT exemptions & flash title supplies

Fast Bunkering Klaipeda UAB

VAT exemptions & flash title supplies

Question referred

Article 148(a)- exemption (with credit) on goods supplied for fuelling and

provisioning of vessels:

Must this provision mean that exemption from VAT is available to both

− The supplies to the vessel operator; and also

− The supplies to the intermediaries where the ultimate use of the

goods is known in advance (and duly evidenced in accordance with

national law)?

Fast Bunkering Klaipeda UAB

VAT exemptions & flash title supplies

A judgment of two halves: (a) Velker remains good law

• Velker (C-185-89): exemption may only apply to the final supply to vessel operator – exemption is not applicable to supplies to intermediaries

However… (b) FBK’s facts differed from Velker

• Transfer of ownership in FBK’s case may have taken place only at end of loading > ownership does not transfer to intermediaries until vessel operators are entitled to dispose of fuel (as owners)

• Therefore, intermediaries have at no time been in position to dispose of fuel

• Paragraph 52: Transactions carried out by FBK:

• Cannot be classified as supplies to intermediaries, but instead

• Should be regarded as exempt supplies to vessel operators

• National Court to determine whether ownership transferred “at the earliest at the same time” when vessel operators able to dispose of fuel

Fast Bunkering Klaipeda UAB

VAT exemptions & flash title supplies

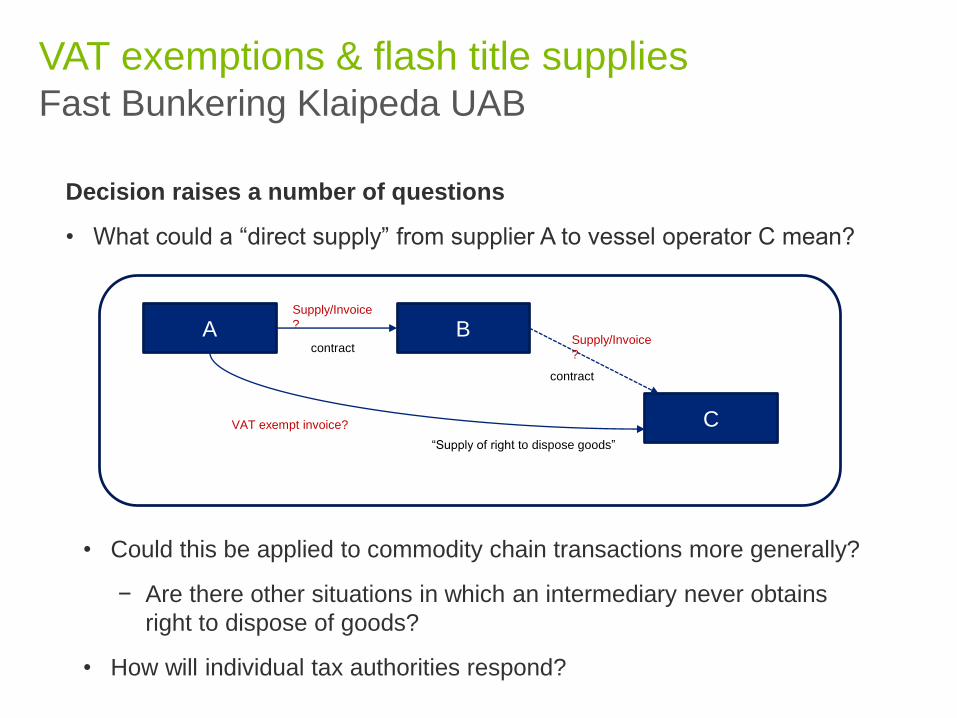

Decision raises a number of questions

• What could a “direct supply” from supplier A to vessel operator C mean?

• Could this be applied to commodity chain transactions more generally?

− Are there other situations in which an intermediary never obtains

right to dispose of goods?

• How will individual tax authorities respond?

A B

C

contract

Supply/Invoice

?

contract

Supply/Invoice

?

VAT exempt invoice?

“Supply of right to dispose goods”

Larentia & Minerva (C-108/14, C-109/14)

VAT recovery of holding companies

Larentia &

Minerva

Holding

Sub 1 Sub 2

Administrative +

commercial servicesAdministrative +

commercial services

Costs acquisition participations

(EUR 764k VAT)

L&M: Attraction of EUR 25M new

capital, 77.69% invested in subs

DE tax authorities reject

77.69% of input VAT

Larentia & Minerva

VAT recovery of holding companies

• Confirmation of principle of VAT recovery for holding companies

− actively managing their subsidiaries

− for consideration

• Unless (part of) the services rendered to the subsidiaries should be

considered as VAT exempt

• Mixed holding companies (managing some subs but not all, passive

managment): partial rejection of VAT recovery

• apportionment between economic and non-economic activities

• based on an investment formula, a transaction formula or any other

appropriate formula

Larentia & Minerva

VAT recovery of holding companies

• Former practice:

• often VAT recovery limitations because of out of scope activities

− rejection based on pro rata – including dividends

can now be countered:

assess possibility to reclaim previous non-recovered VAT

• Positive development for holding companies and private equity

investment funds: improve ability to recover VAT

• By developing service activities in those companies (which are now

sometimes in other companies)

Attention point upon restructuring of holding companies

Organisation for

Economic Cooperation

and Development

OECD Technical Advisory Group on VAT

OECD Technical Advisory Group on VAT/GST Guidelines (TAG)

Mixed government and business members, ca 40 in total - Deloitte has two seats

Roundtable discussions twice a year – February, September

Members input in personal capacity as technical experts, Chatham house rules

TAG reports to Working Party 9

Task teams used for technical research and drafting

Player Role

OECD Government

Committee on

Fiscal Affaires

Direction Setting

Working Party 9 Indirect Taxes

Technical

Advisory Group

VAT/GST Guidelines Project

Task Teams Day to Day Technical Work

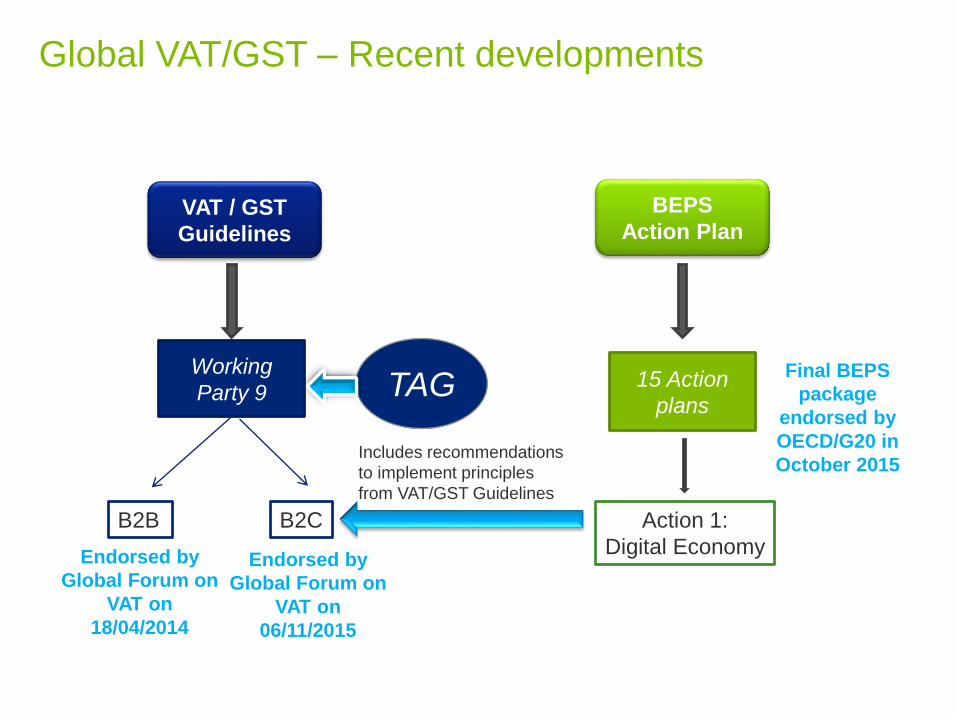

Global VAT/GST – Recent developments

Working

Party 915 Action

plans

Action 1:

Digital Economy

B2B B2C

VAT / GST

Guidelines

BEPS

Action Plan

Endorsed by

Global Forum on

VAT on

06/11/2015

Endorsed by

Global Forum on

VAT on

18/04/2014

Final BEPS

package

endorsed by

OECD/G20 in

October 2015Includes recommendations

to implement principles

from VAT/GST Guidelines

TAG

VAT/GST Guidelines

International VAT/GST Guidelines

OECD International VAT/GST Guidelines

2

0

1

4

Core features of Value Added Taxes Covered by

the Guidelines

VAT Neutrality

Place of Taxation of B2B Supplies of Services and

Intangibles

Place of Taxation of B2C Supplies of Services and

Intangibles

2

0

1

5Provisions on the Guidelines in Practice

Aim and structure

• The Guidelines are

developed to create

global standard on

VAT/GST to address

uncertainty and risks of

double and non-

taxation.

• The Guidelines are

increasingly used by

Governments of both

OECD and non-OECD

countries as a basis for

changes to their VAT

systems.

International VAT/GST GuidelinesContent of the Guidelines

Destination principle

Guideline 3.1

General Rules Specific Rules

B2B

Customer location

Guideline 3.2 [business location]

Guideline 3.3 [business agreement]

Guideline 3.4 [multiple location

entities]

Evaluation

Framework

E.g. on-the-

spot

supplies

Guideline

3.7

Location of

immovable

property

Guideline

3.8

B2C On spot

Place of performance

Guideline 3.5

Other

Customer’s usual

residence

Guideline 3.6

Core principles

Destination

principle :

Transactions are

subject to VAT in the

jurisdiction of

consumption

Neutrality

principle:

VAT is a tax on final

consumption that

should be neutral for

business

• 3.1 General: destination principle – taxation in the jurisdiction of

consumption.

• 3.2- 3.3 ‘Main rule’ - the jurisdiction in which the customer is located has the

taxing rights. Identity of the customer determined by the business agreement.

• 3.4 Multiple location entities - when customer has establishments in more than

one jurisdiction, the taxing rights accrue to the jurisdiction(s) where the

establishment(s) using the service or intangible is (are) located.

• 3.5-3.6 Specific rules - taxing rights may be allocated by a proxy other than

customer location, when the main rule does not lead to an appropriate result and

another proxy would lead to significantly better result.

• For services and intangibles directly connected with immovable property, the

taxing rights may be allocated to the jurisdiction where the immovable

property is located.

B2B trade in services and intangiblesGuidelines

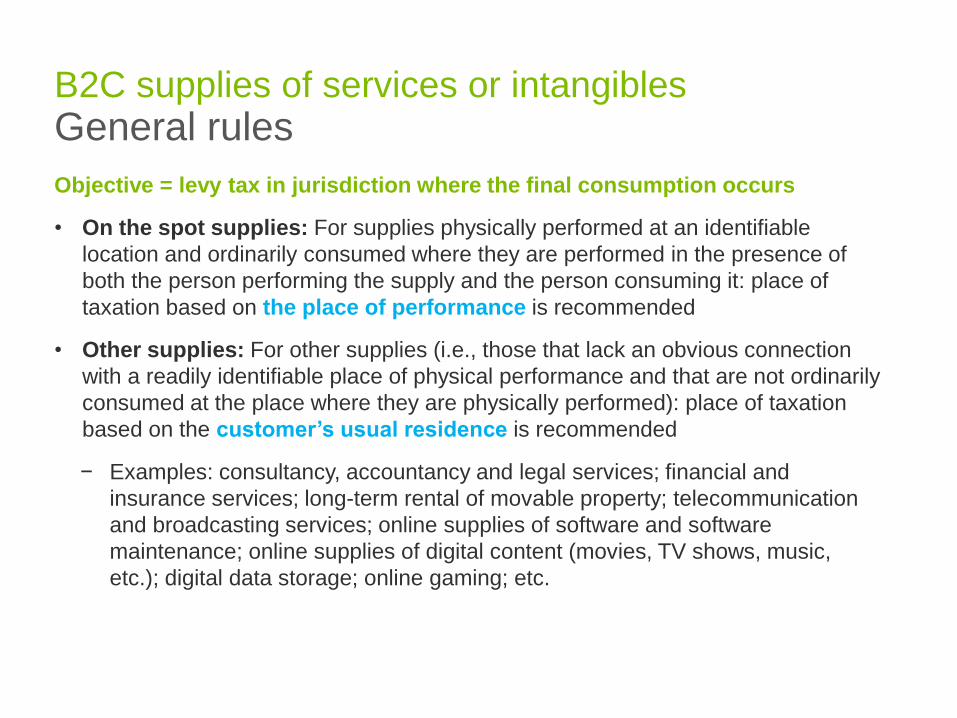

Objective = levy tax in jurisdiction where the final consumption occurs

• On the spot supplies: For supplies physically performed at an identifiable

location and ordinarily consumed where they are performed in the presence of

both the person performing the supply and the person consuming it: place of

taxation based on the place of performance is recommended

• Other supplies: For other supplies (i.e., those that lack an obvious connection

with a readily identifiable place of physical performance and that are not ordinarily

consumed at the place where they are physically performed): place of taxation

based on the customer’s usual residence is recommended

− Examples: consultancy, accountancy and legal services; financial and

insurance services; long-term rental of movable property; telecommunication

and broadcasting services; online supplies of software and software

maintenance; online supplies of digital content (movies, TV shows, music,

etc.); digital data storage; online gaming; etc.

B2C supplies of services or intangiblesGeneral rules

• VAT collection

• The most effective and efficient approach to ensure the appropriate collection

of VAT on cross-border B2C supplies is to require the non-resident supplier

to register and account for the VAT in the jurisdiction of taxation

• It is recommended that jurisdictions consider establishing a simplified

registration and compliance regime to facilitate compliance for non-resident

suppliers

• B2C specific rules (same as B2B)

• Applicable in cases where the general rules may not give an appropriate result

and another proxy would lead to significantly better result.

• Examples: services directly related to immovable property; international

transport of persons; provision of internet access; services connected with

movable tangible property.

B2C supplies of services or intangibles

Objective = provide guidance to jurisdictions in developing practical legislation

that will facilitate a smooth interaction between national VAT systems, with a

view to minimizing the potential for double taxation and unintended non-

taxation and creating more certainty for business and tax authorities

• Mechanisms: Facilitate the consistent implementation of the principles of the

guidelines in national legislation, as well as their consistent interpretation by tax

administrations, in order to minimize both the risk of such double taxation or

unintended non-taxation and the potential for resulting disputes, and for dealing

with evasion and avoidance

• Mutual cooperation (multilateral and bilateral), exchange of information, and

other arrangements allowing tax administrations to communicate and work

together

• Provide taxpayers with readily accessible and easily understood guidance

• Creation of points of contact with tax administrations allowing for one to make

inquiries as well as to inform on perceived disparities

Supportive provisions

Mutual cooperation and dispute resolution

Next steps

Areas of future work, suggested by the third Global Forum on VAT:

• Development of implementation packages to support consistent implementation of the

Guidelines

• To work on areas not yet covered by Guidelines:

− Research and analysis of approaches to improve neutrality and overall performance of the

VAT systems, e.g. design and implementation of efficient VAT Refund mechanisms and risk

assessment processes

− Develop a framework for exchange of information and enhanced admin. cooperation in VAT

− VAT on cross-border trade on goods, including VAT collection on low value imports and on

good practices to address compliance issues

− Interaction between VAT and international direct tax framework, notably in the area of transfer

pricing

• Design an even more inclusive framework to support and carry out this work with the

involvement of all interested countries and jurisdictions particularly developing

economies, on an equal footing.

International VAT/GST Guidelines

Thank you for your attention

Questions?

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and

their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not

provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected

network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the

insights they need to address their most complex business challenges. Deloitte’s more than 200,000 professionals are committed to becoming the standard of

excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively,

the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for

any loss whatsoever sustained by any person who relies on this communication.

© 2015. For information, contact Deloitte Belgium