Upcoming Round 1.5. “Unconventionals”. Part I: Exploring contract terms and fiscal incentives...

26

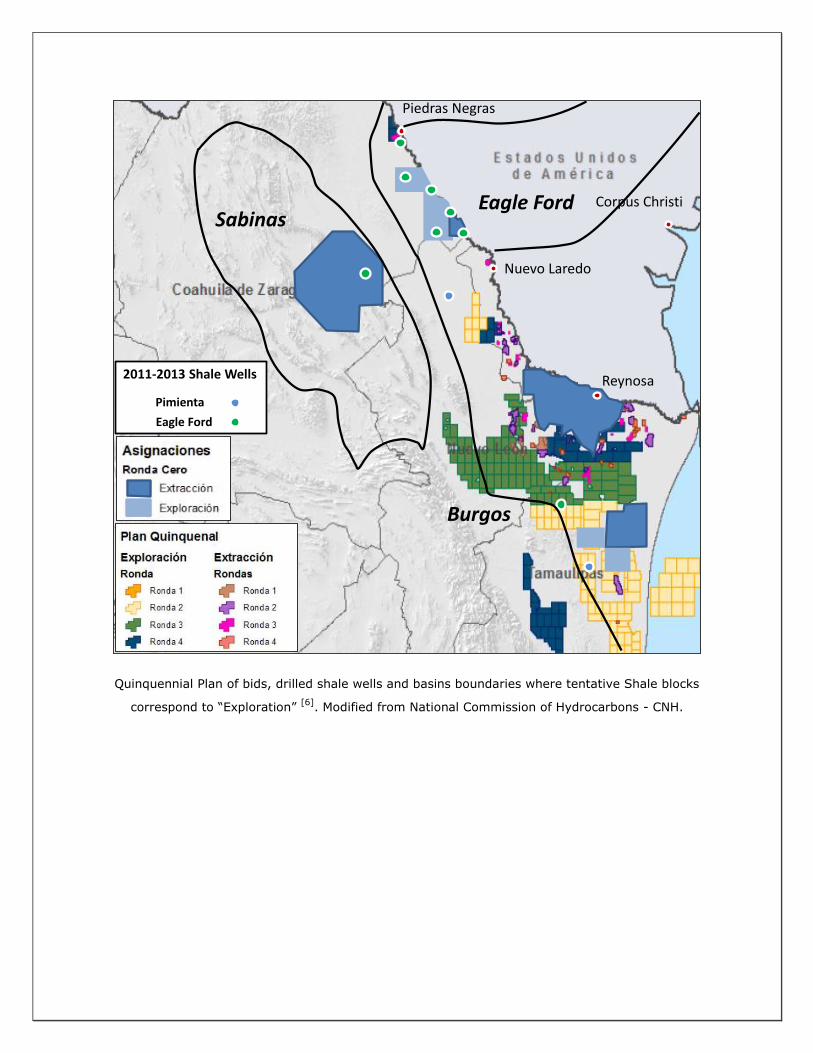

Quinquennial Plan of bids, drilled shale wells and basins boundaries where tentative Shale blocks correspond to “Exploration” [6] . Modified from National Commission of Hydrocarbons - CNH. Nuevo Laredo Reynosa Piedras Negras Eagle Ford Sabinas Burgos Corpus Christi 2011-2013 Shale Wells Pimienta Eagle Ford

-

Upload

juan-diego-suarez-fromm -

Category

Business

-

view

225 -

download

1

Transcript of Upcoming Round 1.5. “Unconventionals”. Part I: Exploring contract terms and fiscal incentives...

Quinquennial Plan of bids, drilled shale wells and basins boundaries where tentative Shale blocks

correspond to “Exploration” [6]

. Modified from National Commission of Hydrocarbons - CNH.

Nuevo Laredo

Reynosa

Piedras Negras

Eagle FordSabinas

Burgos

Corpus Christi

2011-2013 Shale Wells

Pimienta

Eagle Ford

1

Upcoming Round 1.5. “Unconventionals”.

Part I: Exploring contract terms and fiscal

incentives for Shale gas development in Mexico.

Keywords: Round One, License Contract, profitability, royalty, government take,

Mexico Shale, Eagle Ford, Type well, shale technologies, National Infrastructure

Program, gas market.

For further details or full report please contact:

Juan Diego Suarez Fromm

Senior Reservoir Engineering Advisor

Mexico

2

“We require new strategies in the way we finance and manage shale gas/oil

projects. Shale gas eventually will become the main source of natural gas for

Mexico”. Dr. Edgar Rangel German.

3

0. Summary

Shale gas potential in Mexico has been identified by government, Mexican National Oil

Company - PEMEX, and international petroleum industry, as a great opportunity for

resources development in order to solve increasing natural gas demand.

Large gas pipeline extension and power generation projects have been launched and

others are on the way according to National Infrastructure Program. In the mid-term

U.S. gas exports are expected to continuously rise, which for some political parties is a

threat to Mexican energy independence.

The upcoming Round One bids for onshore fields will comprise Unconventional

resources including Shale Gas, Shale Oil and Chicontepec. The aim of this study is to

evaluate Shale Gas development profitability for different gas prices, costs and

royalties and more important to develop fiscal and contract incentives alternatives

based on geological trends, current well construction technologies, technical risks and

market risk.

In spite of Shale Gas Potential in Mexico and closeness to U.S. shale technologies and

human capital talent, current market conditions are not favourable for Shale Gas

development.

Basically are needed two conditions for building up the shale industry in Mexico: time

and fiscal incentives in order to mitigate market and technical risks.

Among several barriers, the following emerge as very relevant for shale development.

Low present and future prices.

The exploration and appraisal phases are time consuming; as well also it is the

cost optimization process and productivity enhancement.

Transport infrastructure requirements for the logistic of rigs and materials.

Shale industry is very capital intensive, where +90% of capital expenditures are

new wells.

Huge water resources availability for fracking.

Security issues in some places.

In this study, fiscal incentives are set by applying deductions in income taxes

permitted by “Hydrocarbon Revenue Law” [10].

4

Several economical models were run based on U.S. Eagle Ford development history;

showing that only marginal profitability is obtained under current market conditions;

even with fiscal incentives.

On the other hand, an optimistic case was run assuming well costs optimization and

more favourable sale prices; showing that fiscal incentives could be taken away.

Therefore, three general recommendations can be set for Shale gas development in

Mexico under license contracts.

1. Redefinition of contract periods: The “Exploration period” will replace

the “Evaluation Period”, which will be run before Development Period. During

the Exploration period, the Minimal Work Commitment must be fulfilled and the

operator will have the option for the continuing of operations or the end of the

contract.

2. Extension of Exploration Period: Instead of one year period, the exploration

phase will last about 5 years. During this period, operators are expected to

successfully apply well construction optimizations.

3. Fiscal incentives: During Exploration Period, all development capital

expenditures will be treated as Exploration expenditures, thus allowing 100%

deduction for income tax determination.

These fiscal incentives and contract terms or similar are strongly

recommended for Shale Gas Development in Mexico under License Contracts.

During the Exploration period, they will mitigate market and technical risks

for operators, allowing them to develop a learning curve regarding well

construction and project management in order to sustain future intensive

capital expenditures in the development period. During the second period,

where main field development takes place, incentives will no longer be

needed, favouring government income.

5

1. Introduction

1.1. The Grand Energy Transition

Robert Hefner published in 2009 “The Grand Energy Transition: THE RISE OF ENERGY

GASES, SUSTAINABLE LIFE AND GROWTH, AND THE NEXT GREAT ECONOMIC

EXPANSION”, where he states that gases will completely replace liquid and solid

carbon based fuels, leading to a low-carbon energy matrix (Chart 1).

In this transition natural gas is one link of this macro process, which presents many

advantages from technical and environmental point of view. Methane, and latterly

Propane and Butane are being used for transportation, which is a major Dioxide

Carbon generator when based on gasoline burn.

Chart 1. Energy matrix transition. From “The Grand Energy Transition”, Robert Hefner [1].

6

1.2. National market of natural gas Mexican natural gas demand has been increasing, averaging 1,4% since 2008

(Chart 2). Today, gas pipeline network covers 8,990 Km with 5,750 MMcf/d capacity,

over 19 states; and it is projected to expand 5,200 Km according National

Infrastructure Program 2014-2018 [2].

Chart 2. Mexican Gas demand by sector. From “Mexico’s new chapter in natural gas”, National

Commission of Hydrocarbons (CNH) [3].

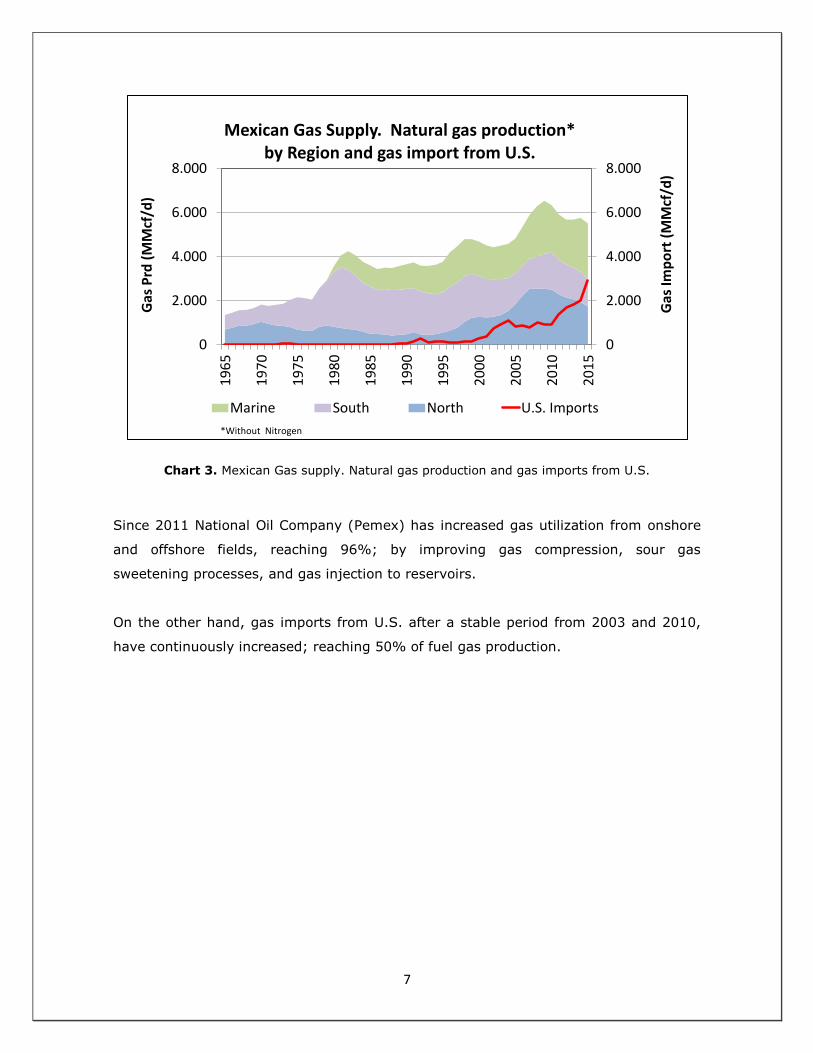

Gas production peaked in 2009, boosted by Marine and North regions. Since then it

has declined due to onshore fields depletion (Chart 3).

7

Chart 3. Mexican Gas supply. Natural gas production and gas imports from U.S.

Since 2011 National Oil Company (Pemex) has increased gas utilization from onshore

and offshore fields, reaching 96%; by improving gas compression, sour gas

sweetening processes, and gas injection to reservoirs.

On the other hand, gas imports from U.S. after a stable period from 2003 and 2010,

have continuously increased; reaching 50% of fuel gas production.

0

2.000

4.000

6.000

8.000

0

2.000

4.000

6.000

8.000

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

Gas

Imp

ort

(M

Mcf

/d)

Gas

Prd

(M

Mcf

/d)

Mexican Gas Supply. Natural gas production*by Region and gas import from U.S.

Marine South North U.S. Imports

*Without Nitrogen

8

1.3. Natural gas from North Mexico. Multiple Service Contracts in

Burgos

Natural gas plays a central role in North Mexico for power generation industry. The

Northwest region has high electric power consumption due to fans, air-conditioning,

refrigerators, and agricultural irrigation systems. And the Northeast has a vast

manufacture industry as steel, cement, chemical, and glass among others, very energy

demanding [2].

Mexican gas industry started in 1945 with the discovery of “Mision” field in Burgos

Basin. This basin is the main non associated natural gas resource in Mexico, extending

in the U.S. as “Rio Grande” basin. Located at Northwest, it develops over States of

Tamaulipas and Nuevo Leon, and covers 30,000 Km2 (Chart 4).

Chart 4. Petroleum provinces in Mexico. From “National Hydrocarbon Commission” (CNH).

9

Gas production stabilized in 600 MMcf/d between late 60’s and 70’s. In early 80’s it

declined steadily, reaching 200 MMcf/d in mid-90’s (Chart 5). In response to this

situation, PEMEX retook exploration and development, achieving production

enhancement to 1.000 MMcf/d by 2000. Even so, U.S. gas import continuously

increased, reaching 300 MMcf/d at 2000. Consequently, PEMEX called International Oil

Companies looking for private investment and knowhow. By 2003, PEMEX awarded 7

fields in Burgos basin, opening for first time the petroleum industry to private

operators, with “Multiple Service Contracts” (MSC). In the second (2004-2005) and

third call (2007), three additional blocks were awarded.

Chart 5. Gas supply in North Mexico. Burgos’s production and U.S. imports.

The MSC contracts allow Burgos production enhancement from 2005 to 2009, boosted

by high gas prices (Chart 6). By 2004 prices were around 6 usd/MMbtu (Henry Hub)

and 50 usd/bbl (West Texas Intermediate), being very attractive market conditions for

PEMEX, allowing profitable development for these service contracts.

0

500

1000

1500

2000

2500

3000

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

Gas

[M

Mcf

/d]

Gas supply in North Mexico.Burgos's production & U.S. imports

U.S. Imports Burgos's Nat Gas prd.

Sabinas development

Burgos new developments

(Pemex)

Burgos's COPFContracts

10

On the other hand, by late 2009, oil and gas prices were decoupled. Gas price dropped

from 13 usd/MMbtu in 2008 to 3 usd/MMbtu in 2009, staying between 2 and 4,5

usd/MMbtu since then. Therefore PEMEX decreased capital expenditures in Burgos, in

traditional fields and MSC contracts, and thus redirecting investment on condensate

fields.

Lately, oil price crisis directed PEMEX to cut off almost all capital expenditures in

Burgos, keeping only operation and maintenance budgets. This situation explains total

production decline since 2010.

Chart 6. Henry Hub and West Texas Intermediate prices.

0

2

4

6

8

10

12

14

16

18

20

0

20

40

60

80

100

120

140

160

180

200

19

95

20

00

20

05

20

10

20

15

He

nry

Hu

b [

USD

/MM

BTU

]

WTI

[U

SD/B

BL]

WTI & Henry Hub

WTI (USD/bbl) Henry Hub (usd/Mmbtu)

Burgos COPFContracts

11

1.4. The U.S. Shale boom

Shale resources have a long history; since War World Two, shale has been identified by

U.S. government as a future oil source. But it development had to wait until market

conditions incentivized by Federal government promoted the investigation of new

technologies that jointly triggered shale industry development (Chart 7). By 2000

shale production accounted for only 1.6 percent of total U.S. natural gas production,

while currently it accounts for 40 percent (Chart 8).

Chart 7. U.S. shale plays. From EIA.

12

Chart 8. U.S. shale plays production and rig count.

Shale oil and gas production has allowed declining energy imports in U.S. Energy

imports decreased from 30% of total energy consumption in 2005 to 13% in 2013.

It is interesting to analyse the critical conditions that lead to the shale boom in U.S.

The following summary is taken from the publication “US Shale Gas Development,

What Led to the Boom?”, by Zhongmin Wang and Alan Krupnick.

A number of factors converged in the early 2000s government policy by

deregulating gas prices (which led to high natural gas prices), tax incentives,

favorable geology, private land and mineral rights ownership, market

structure, water availability, and natural gas pipeline infrastructure, but that

the most important factor was innovations in technology. Some of the key

technological innovations resulted from government research and

development (R&D) programs and private entrepreneurship that aimed to

develop unconventional natural gas, but other important technologies were

largely developed by the oil industry for use in oil exploration and production.

-

10.000

20.000

30.000

40.000

50.000

60.000

-

1.000

2.000

3.000

4.000

5.000

6.000

Gas

Prd

(M

Mcf

/d)

Oil

Prd

(M

bp

d),

rig

co

un

tU.S. Shale Production

Rig count Oil (Mbbl/d) Total prd Natural gas (MMcf/d) Total prd

13

The most important energy-related technological innovations were assessed

in 1980s and the 1990s, which included three technologies that are critical to

shale gas development: horizontal drilling, three-dimensional (3-D) seismic

imaging, and fracturing technology.

Horizontal Drilling. Few practical applications of horizontal drilling took place

until the early 1980s and it did not achieve commercial viability until the late

1980s.

Massive Hydraulic Fracturing. Agarwal et al. (1979, 172) note that MHF was

already “a proven technique for developing commercial wells in low-

permeability or ‘tight’ gas formations.” With financial assistance from DOE,

Mitchell Energy conducted in 1978 what was, at the time, the largest MHF in a

tight gas formation. Mitchell Energy quickly applied MHF to the Barnett shale.

3-D Seismic Imaging. Limited commercial application of 3-D seismic

technology began in the early 1980s (Haar 1992). 3-D seismic imaging

provides a better picture of the structure and properties of subsurface rocks

than the earlier two-dimensional (2-D) method.

Microseismic Fracturing Mapping. Since the early 2000s, microseismic frac

monitoring has played a key role in optimizing how shale gas wells are

hydraulically stimulated. Unlike 3-D seismic imaging, microseismic fracture

monitoring is a passive method that uses sensors to listen for underground

seismic energy and record the minor seismic events generated during the

fracturing of a nearby well. This technology can reveal the height, length,

orientation, and other attributes of induced fractures.

From “US Shale Gas Development, What Led to the Boom?”, by Zhongmin Wang and

Alan Krupnick.

14

1.5. Shale Resources in Mexico

Mexico’s shale resources hold fourth Global place according to World Shale Gas

Resources from U.S. Energy Information Administration publication (EIA) [4]

(Chart 9).

Chart 9. Worldwide shale resources, Proved Reserves and cumulative production. From

“Mexico’s new chapter in natural gas”, National Commission of Hydrocarbons (CNH) [3].

15

Mexico’s Shale potential is located in four onshore petroleum provinces, according to

EIA’s and PEMEX studies (Chart 10).

1. Burgos.

2. Sabinas.

3. Tampico-Misantla.

4. Veracruz.

The following information is taken from the book from EIA “Technically Recoverable

Shale, Oil and Shale Gas Resources in Mexico” [5].

16

Chart 10. Prospective shale basins in Mexico [5]

. From EIA.

According to EIA assessment, Burgos and Sabinas basins account with large Shale Gas

resources, while Shale Oil potential is located in Burgos and Tampico-Misantla basins.

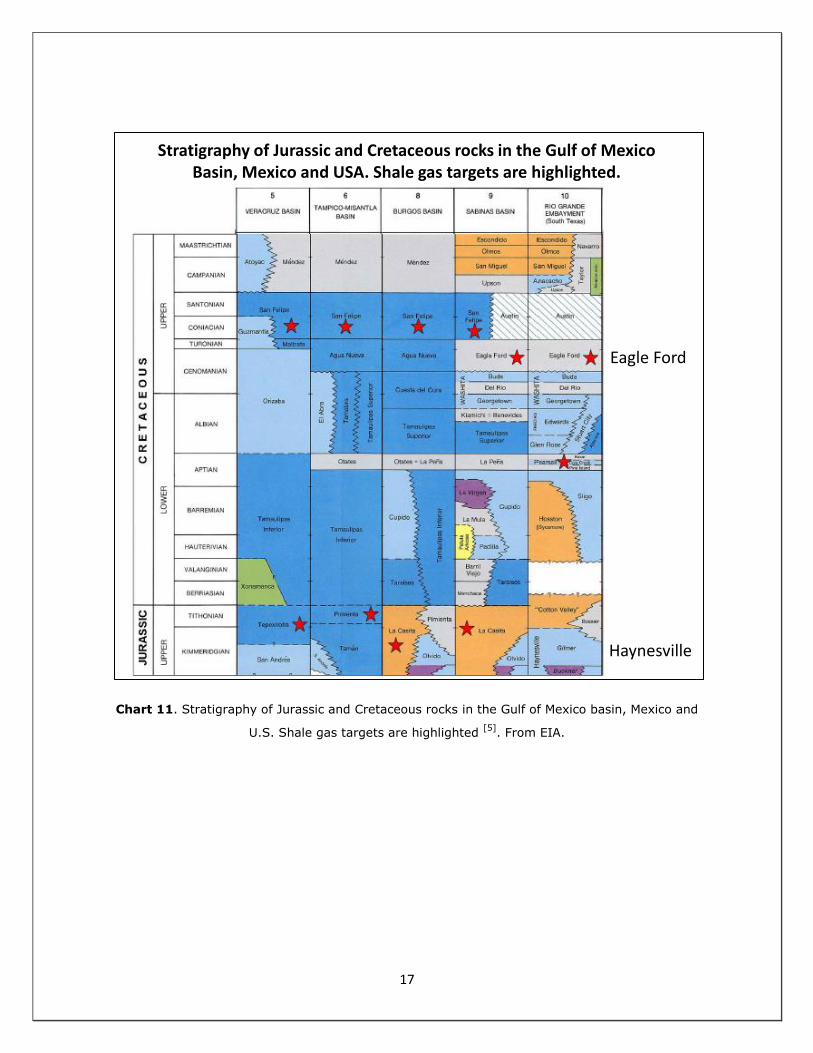

In Mexico two shale formations: Cretaceous “San Felipe” and Jurassic “Pimienta-La

Casita” are developed over these regions (Chart 11). They are organic rich marine

deposits with suitable thermal maturity, areal extension and good gross thickness.

They are main source rocks for conventional oil and gas fields in Mexican petroleum

provinces, and correlate with two U.S. Shale Plays: Cretaceous Eagle Ford and Jurassic

Haynesville.

17

Chart 11. Stratigraphy of Jurassic and Cretaceous rocks in the Gulf of Mexico basin, Mexico and

U.S. Shale gas targets are highlighted [5]

. From EIA.

Stratigraphy of Jurassic and Cretaceous rocks in the Gulf of Mexico Basin, Mexico and USA. Shale gas targets are highlighted.

Eagle Ford

Haynesville

18

About 14 shales wells have been drilled and tested in Burgos and Sabinas basins by

the National Oil Company - Pemex between 2011 and mid-2013, targeting Eagle Ford

and Pimienta formations. The rest of petroleum provinces have some indirect

antecedents from conventional wells, increasing the geological risk.

If U.S. Shale boom could be replicated in Mexico has not a straight forward answer.

Many barriers will be needed to overcome:

Low present and future oil and gas prices.

The exploration and appraisal phases are time consuming; as well also it is the

cost optimization process and productivity enhancement.

Transport infrastructure requirements for the logistic of rigs and materials.

Shale industry is very capital intensive, where +90% of capital expenditures are

new wells.

Huge water resources availability for fracking.

Security issues in some places.

From government point of view, some incentives should be set in order to promote

private interest in the upcoming bids of Unconventional resources.

19

2. Technical and economical assessment for Shale Gas development in

North Mexico. Evaluation of fiscal incentives for License Contracts.

2.1. Geological overview

Upcoming onshore bids will be the so called “Unconventionals”, which comprises Shale

Oil & Gas Exploration, and Chicontepec field development. The last is a tight oil Play,

and despite of it is not a shale formation same development technologies are applied.

This paper will be devoted to Shale Gas, which is located in Northern Burgos and

Sabinas basins.

The following chart shows Quinquennial Plan of bids [6], drilled shale wells and basins

boundaries where tentative Shale blocks correspond to “Exploration” (Opening

Chart).

Whereas Mexico’s marine-deposited shales appear to have good rock quality,

the geologic structure of its sedimentary basins often is considerably more

complex than in the U.S. Compared with the broad and gently dipping shale

belts of Texas and Louisiana, Mexico’s coastal shale zone is narrower, less

continuous and structurally more disrupted [5].

Regional compression and thrust faulting related to the formation of the

Sierra Madre Ranges have squeezed Mexico’s coastal plain, creating a series

of discontinuous sub-basins. Many of Mexico’s largest conventional oil and

gas fields also occur in this area, producing from conventional sandstone

reservoirs of Miocene and Pliocene age that were sourced by deep, organic-

rich and thermally mature Jurassic and Cretaceous-age shales. These deep

source rocks are the principal targets for shale gas/oil exploration in Mexico

[5].

From U.S. Energy Information Administration - EIA, “Technically Recoverable Shale, Oil

and Shale Gas Resources in Mexico”, September 2015.

20

Chart 12. Burgos and Sabinas basins. Structural and geological features. Drilled shale wells

2011-2013. Modified from PEMEX.

Burgos

2011-2013 Shale Wells

Eagle Ford

Piedras NegrasB

B’

Sabinas

Salt Dome

Thrust fault

Anticline

Pimienta

Eagle Ford

21

Chart 13. General Cross section Burgos and Sabinas basins [7]

.

2.2. Main evaluation assumptions

Some assumptions were made for shale gas development evaluation in Mexico.

Economical evaluation will be based on “Eagle Ford” formation:

The “Eagle Ford” has been developed in U.S. over last 10 years. Public

information is available for evaluation of production performance and costs.

“Eagle Ford” is the main shale target regarding EIA evaluation.

Expected shale blocks distribution will favour Eagle Ford development, mainly

for gas development.

In spite of shale gas potential for “Pimienta – La Casita”, for simplicity this evaluation

will only cover “Eagle Ford” development.

To sum up, only “Eagle Ford” development will be evaluated assuming natural

gas window for shale blocks to be auctioned.

B B’

BurgosBasin

SabinasBasin

La CasitaPimienta

Terciary

22

2.3. Main evaluation results

Main evaluation results are presented in the following charts.

Income tax deductions play a very relevant role for shale development profitability

under License Contracts. The Base Case needs them in order to achieve a profitable

case. In this scenario all development capital expenditures are considered as

Exploration capital expenditures, thus generating an income tax deduction of 100%.

Chart 14. Gas production profile for Base Case. The economic limit is 0,2 MMcf/d per well.

Chart 15. Capital and Operation Expenditure’s for Base Case. The economic limit is 0,2

MMcf/d per well.

0

20

40

60

80

0 1 2 3 4 5 6 7 8 9 10 11 12

[MM

pc/

d]

year

Gas production profile for Base Case

G Inc MMpc/d G Base MMpc/d

-100,00

-80,00

-60,00

-40,00

-20,00

0,00

0 1 2 3 4 5 6 7 8 9 10 11 12 13

[MM

usd

/ye

ar]

Year

Capital & Operation Expenditure's for Base Case

CAPEX [Mmusd/year] OPEX [Mmusd/year]

23

Chart 16. Sensibility analysis results for Shale gas development with License Contract.

Reference case is Base case (3 usd/MMbtu, 60 usd/bbl and additional royalty 5%). Income

Tax deductions treatment for development capital expenditures: Exploration -100%

deductible.

24

Chart 17. Sensibility analysis results for Shale gas development with License Contract.

Percentages represent variations respect to Base Case. Reference case is Base case (3

usd/MMbtu, 60 usd/bbl and additional royalty 5%). Income Tax deductions treatment for

development capital expenditures: Exploration -100% deductible.

25

4. References

1. Hefner III, Robert. “The Grand Energy Transition: THE RISE OF ENERGY GASES,

SUSTAINABLE LIFE AND GROWTH, AND THE NEXT GREAT ECONOMIC EXPANSION”,

WILEY, 2009.

2. Presidencia de los Estados Unidos Mexicanos. “National Infrastructure Program

2014-2018”, “Programa Nacional de Infraestructura 2014 – 2018”, December 2015

3. Rangel Germán, Edgar. “Mexico’s new chapter in natural gas”, National Commission

of Hydrocarbons (CNH), 16th Mexican Energy Conference, November 13-14, 2012,

Houston, Texas.

4. U.S. Energy Information Administration. “World Shale Gas Resources: An Initial

Assessment of 14 Regions Outside the United States”, April 2011.

5. U.S. Energy Information Administration. “Technically Recoverable Shale, Oil and

Shale Gas Resources in Mexico”, September 2015.

6. National Hydrocarbon Comission - CNH. “Quinquenial Program of Bids for

Exploration and Production– 2015-2019”, “Plan Quinquenal de Licitaciones para la

Exploracion y Extraccion de Hidrocarburos. 2015-2019”, 2014.

7. Dyer, M.J. and Bartolini, C. “Sabinas Basin Lower Cretaceous to Jurassic

Production—Comparison to South Texas Equivalents”. IHS Energy

8. Hughes, David. “DRILLING DEEPER: A REALITY CHECK ON U.S. GOVERNMENT

FORECASTS FOR A LASTING TIGHT OIL & SHALE GAS BOOM, PART 2: TIGHT OIL”,

post carbon institute.

9. U.S. Energy Information Administration. “Annual Energy Outlook 2015, with

projections to 2040”, April 2015.

10. Cámara de Diputados del Honorable Congreso de la Unión. “Mexican Hydrocarbon

Revenue Law”, “Ley de Ingresos sobre Hidrocarburos”.