UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH … · university of kansas medical center research...

29

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC. CONSOLIDATED FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION YEARS ENDED JUNE 30, 2015 AND 2014 WITH INDEPENDENT AUDITOR’S REPORT

-

Upload

dangnguyet -

Category

Documents

-

view

214 -

download

0

Transcript of UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH … · university of kansas medical center research...

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED FINANCIAL STATEMENTS

WITH

SUPPLEMENTARY INFORMATION

YEARS ENDED JUNE 30, 2015 AND 2014

WITH

INDEPENDENT AUDITOR’S REPORT

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED FINANCIAL STATEMENTS

WITH

SUPPLEMENTARY INFORMATION

YEARS ENDED JUNE 30, 2015 AND 2014

WITH

INDEPENDENT AUDITOR’S REPORT

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED JUNE 30, 2015 and 2014

TABLE OF CONTENTS Independent Auditor’s Report .......................................................................................... 1 - 2 Consolidated Financial Statements: Consolidated Statements of Financial Position .......................................................... 3 Consolidated Statements of Activities ........................................................................ 4 - 5 Consolidated Statements of Cash Flows ................................................................... 6 - 7 Notes to Consolidated Financial Statements ............................................................. 8 - 19 Supplementary Information: Consolidating Statement of Financial Position ........................................................... 20 Consolidating Statement of Activities ......................................................................... 21 Functional Expenses .................................................................................................. 22 - 23 Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards. ........................... 24 - 25

This is a copy of the Research Institute’s annual financial statements reproduced from an electronic file. An original copy of this document

is available at the Research Institute’s office.

301 N. Main, Suite 1700 ● Wichita, Kansas 67202-4868 ● (316) 267-7231 ● (316) 267-0339 fax ● www.aghlc.com

INDEPENDENT AUDITOR’S REPORT

Board of Directors University of Kansas Medical Center Research Institute, Inc. Kansas City, Kansas Report on the Financial Statements We have audited the accompanying consolidated financial statements of the University of Kansas Medical Center Research Institute, Inc., which comprise the consolidated statements of financial position as of June 30, 2015 and 2014, and the related consolidated statements of activities and cash flows for the years then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

2

Opinion In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of the University of Kansas Medical Center Research Institute, Inc. as of June 30, 2015 and 2014, and the changes in its net assets and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America. Other Matters – Supplementary Information Our audits were conducted for the purpose of forming an opinion on the consolidated financial statements as a whole. The accompanying supplementary information as listed in the table of contents is presented for purposes of additional analysis rather than to present the financial position, change in net assets and cash flows of the individual entities, and is not a required part of the consolidated financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the consolidated financial statements. The information has been subjected to the auditing procedures applied in the audit of the consolidated financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the consolidated financial statements or to the consolidated financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the consolidated financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated September 3, 2015 on our consideration of the University of Kansas Medical Center Research Institute, Inc.’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering University of Kansas Medical Center Research Institute, Inc.’s internal control over financial reporting and compliance.

Allen, Gibbs & Houlik, L.C. CERTIFIED PUBLIC ACCOUNTANTS September 3, 2015 Wichita, KS

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

June 30, 2015 and 2014

The accompanying notes are an integral part of these consolidated financial statements.

3

ASSETS

2015 2014 Assets

Cash and cash equivalents $ 9,391,824 $ 11,039,479 Investments 43,522,566 41,796,626 Precede Fund, L.C. investments 409,989 376,835 Reimbursable costs incurred in excess of research

revenues received, net 9,356,088 8,399,485 Accounts receivable 817,375 34,089 Interest receivable 57,043 36,672 Prepaid expenses 198,967 112,766 Bond issuance costs 304,157 325,502 Land, equipment and leasehold improvements, net 268,007 273,441

Total assets $ 64,326,016 $ 62,394,895

LIABILITIES AND NET ASSETS

Liabilities Accounts payable $ 3,277,174 $ 3,048,131 Accrued expenses 304,758 246,440 Accrued interest payable 228,871 256,927 Revenue distribution payable 762,688 -- Deferred revenue - clinical trials 9,452,963 7,745,901 Deferred revenue - other 5,620,786 7,924,373 Deferred revenue - federal grants 860,162 583,500 Deferred revenue - state grants 521,370 190,209 Bonds payable 22,938,303 25,287,745

Total liabilities 43,967,075 45,283,226

Net assets Unrestricted:

Designated 25,067,387 24,562,965 Undesignated (14,853,538) (14,905,654)Noncontrolling interest in subsidiary 135,296 123,855

Temporarily restricted 10,009,796 7,330,503

Total net assets 20,358,941 17,111,669

Total liabilities and net assets $ 64,326,016 $ 62,394,895

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED STATEMENT OF ACTIVITIES

Year Ended June 30, 2015

The accompanying notes are an integral part of these consolidated financial statements.

4

2015

Unrestricted Temporarily Restricted Total

Revenues, gains and other support Direct research income $ 81,303,972 $ -- $ 81,303,972 Clinical trials 7,170,792 -- 7,170,792 Clinical trial IRB and administrative fees 1,044,292 -- 1,044,292 Facilities & administrative revenue 22,388,853 -- 22,388,853 Research facilities renovation grants -- 2,640,000 2,640,000 Public support -- 126,000 126,000 Extramural funding -- 175,000 175,000 Research Properties, Inc. rental income 208,643 -- 208,643 Support for KU Center for Technology

Commercialization, Inc. 740,000 -- 740,000 Royalties and technology income 1,242,385 -- 1,242,385 Investment return 490,383 -- 490,383 Other income 616,544 -- 616,544

115,205,864 2,941,000 118,146,864

Satisfaction of program restrictions 261,707 (261,707) --

Total revenues, gains and other support 115,467,571 2,679,293 118,146,864

Functional Expenses Direct research 93,630,614 -- 93,630,614 Facilities 1,570,131 -- 1,570,131 University support 10,966,530 -- 10,966,530 Royalties and technology 1,291,307 -- 1,291,307 Research administration 2,382,748 -- 2,382,748 Management and general 2,089,243 -- 2,089,243 Research Properties, Inc. 577,278 -- 577,278 KU Center for Technology

Commercialization, Inc. 2,391,741 -- 2,391,741

Total expenses 114,899,592 -- 114,899,592

Change in net assets before transfers 567,979 2,679,293 3,247,272

Transfers to University -- -- --

Consolidated change in net assets after transfers 567,979 2,679,293 3,247,272

Net assets, beginning of year 9,781,166 7,330,503 17,111,669

Net assets, end of year $ 10,349,145 $10,009,796 $ 20,358,941

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED STATEMENT OF ACTIVITIES

Year Ended June 30, 2014

The accompanying notes are an integral part of these consolidated financial statements.

5

2014

Unrestricted Temporarily Restricted Total

Revenues, gains and other support Direct research income $ 75,159,906 $ -- $ 75,159,906 Clinical trials 6,581,817 -- 6,581,817 Clinical trial IRB and administrative fees 756,524 -- 756,524 Facilities & administrative revenue 22,016,308 -- 22,016,308 Research facilities renovation grants -- 2,640,000 2,640,000 Public support -- 130,000 130,000 Extramural funding -- 150,000 150,000 Research Properties, Inc. rental income 181,235 -- 181,235 Support for KU Center for Technology

Commercialization, Inc. 740,000 -- 740,000 Royalties and technology income 1,513,107 -- 1,513,107 Investment return 349,205 -- 349,205 Other income 750,727 -- 750,727

108,048,829 2,920,000 110,968,829

Satisfaction of program restrictions 1,750,040 (1,750,040) --

Total revenues, gains and other support 109,798,869 1,169,960 110,968,829

Functional Expenses Direct research 87,598,538 -- 87,598,538 Facilities 984,675 -- 984,675 University support 10,966,490 -- 10,966,490 Royalties and technology 871,214 -- 871,214 Research administration 2,222,054 -- 2,222,054 Management and general 1,506,655 -- 1,506,655 Research Properties, Inc. 559,318 -- 559,318 KU Center for Technology

Commercialization, Inc. 1,759,411 -- 1,759,411

Total expenses 106,468,355 -- 106,468,355

Change in net assets before transfers 3,330,514 1,169,960 4,500,474

Transfers to University (330,009) -- (330,009)

Consolidated change in net assets after transfers 3,000,505 1,169,960 4,170,465

Net assets, beginning of year 6,780,661 6,160,543 12,941,204

Net assets, end of year $ 9,781,166 $ 7,330,503 $ 17,111,669

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

Years Ended June 30, 2015 and 2014

The accompanying notes are an integral part of these consolidated financial statements.

6

2015 2014

Operating Activities Cash received from direct research revenues $ 110,158,947 $ 110,471,919 Cash received from royalties, technology, rents and other 3,108,572 3,374,724 Investment income received 443,788 326,514 Cash paid to employees and suppliers (113,053,311) (108,433,243)Interest paid (1,028,152) (1,133,209)

Net cash flow from operating activities (370,156) 4,606,705

Investing Activities Acquisition of investments (24,693,453) (18,416,551)Proceeds from disposition of investments 22,980,954 18,142,696 Payments for renovations of research facilities,

transferred to University --

(330,009)

Net cash flow from investing activities (1,712,499) (603,864)

Financing Activities Payments on bonds payable (2,205,000) (2,095,000)Contributions restricted for research facilities

renovations 2,640,000 2,640,000

Net cash flow from financing activities 435,000 545,000

Change in cash and cash equivalents (1,647,655) 4,547,841

Cash and cash equivalents, beginning of year 11,039,479 6,491,638

Cash and cash equivalents, end of year $ 9,391,824 $ 11,039,479

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

Years Ended June 30, 2015 and 2014

The accompanying notes are an integral part of these consolidated financial statements.

7

2015 2014

Reconciliation of change in net assets to net cash flow from operating activities:

Consolidated change in net assets $ 3,247,272 $ 4,170,465 Adjustments to reconcile consolidated change in net assets

to net cash flow from operating activities: Depreciation 5,434 7,843 Amortization of bond premium and issuance costs (123,097) (123,096)Realized loss on Precede Fund, L.C. investment -- 1,352 Impairment loss on Precede Fund, L.C. investment -- 150,000 Unrealized (gain)/loss on investment (46,595) (114,388)Contributions restricted for research facilities

renovations (2,640,000) (2,640,000)Transfers to University for research facilities renovations, and assumptions of University bonds -- 330,009 Changes in assets and liabilities: Receivables (803,657) 186,899 Reimbursable costs incurred in excess of research

revenues received (956,603) 3,020,756 Prepaid expenses (86,201) 16,202 Accounts payable 229,043 (2,991,357) Accrued expenses 58,318 (131,501) Accrued interest payable (28,056) (26,188) Revenue distribution payable 762,688 -- Deferred revenue 11,298 2,749,709

Net cash flow from operating activities $ (370,156) $ 4,606,705

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

8

1. NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Operations – The University of Kansas Medical Center Research Institute, Inc. (RI), a not-for-profit organization, manages grants and contracts and earns facilities and administration (F&A) reimbursement and contract administration fees in connection with projects conducted by principal investigators who serve as faculty at the University of Kansas Medical Center (KUMC). The mission of RI is to promote additional medical research at KUMC. RI was established by KUMC in 1992; it is governed by a Board of Directors whose membership includes the KU Chancellor, KUMC faculty, KUMC administrators and community members. Funding for research activities of RI is derived from federal and state grants, privately funded grants provided by corporations and from other not-for-profit organizations and royalties and licensing fees. Although RI is a not-for-profit organization, which is exempt from federal income taxes under Section 501(c)(3) of the Internal Revenue Code (IRC), the accounts of RI are reported in the consolidated financial statements of KUMC due to the commonality of management, control and mission shared by the two organizations. The consolidated financial statements of KUMC are in turn reported in the consolidated financial statements of the University of Kansas (University). RI has two subsidiary corporations: 1) Research Properties, Inc. is tax exempt under IRC Section 501(c)(2) as a title holding corporation, and 2) KU Center for Technology Commercialization, Inc. (KUCTC), d/b/a University of Kansas Innovation and Collaboration (KUIC), is tax exempt under IRC Section 501(c)(3). KUCTC was organized effective July 1, 2008 to facilitate and support the research and technology transfer operations of the University of Kansas and its affiliated tax exempt research institutions. See Note 8 for details regarding activities and transactions with related entities.

Principles of Consolidation – The accompanying consolidated financial statements include the accounts of RI, its wholly owned subsidiaries, Research Properties, Inc. and KUCTC, and its majority-owned subsidiary, Precede Fund, L.C. All intercompany transactions and balances have been eliminated in consolidation. Net Assets – For financial reporting purposes, net assets and revenues, expenses, gains and losses are classified into one of three categories, based on the existence or absence of donor-imposed restrictions as follows: Unrestricted net assets. Unrestricted assets are expendable resources used to support RI’s core operating activities. Contributions received without donor stipulations are reported as unrestricted revenue and net assets. All expenses are recorded as a reduction of unrestricted net assets. This category includes activities related to RI’s operating fund, and net assets held for Research Properties, Inc., KU Center for Technology Commercialization, Inc., Precede Fund, L.C. Additionally, certain amounts are designated for specific purposes as described below:

KUMC institutional reserves represent portions of facilities and administration (F&A) revenues earned by RI as a result of the KUMC research enterprise that are administered by the Executive Vice Chancellor of KUMC under the terms of RI’s operating agreement with KUMC. F&A revenues are distributed for use by KUMC for its operations,

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

9

1. NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

by RI for research administration, and to deans and departments of KUMC to further research. F&A revenues in excess of these distributions are recorded as institutional reserves.

Funds held for researchers represents the residual remaining after grants and clinical trials are closed that are not required to be returned to the original funding source, and include F&A revenues returned to departments. Under RI’s operating agreement with KUMC, these monies are to be held by RI to support further research by principal investigators of KUMC.

Board designated funds represent miscellaneous other funds as designated by RI’s board of directors.

A summary of amounts comprising designated net assets for the years ended June 30, 2015 and 2014 follows:

2015 2014 Net assets designated for: KUMC institutional reserves $ 7,946,666 $ 9,194,663 Funds held for researchers 16,831,677 14,940,273 Board designated 289,044 428,029 Total designated net assets $ 25,067,387 $ 24,562,965

Temporarily restricted net assets. Temporarily restricted net assets consist of research grant funds or other contributions that are subject to donor-imposed restrictions that expire with the passage of time or specific actions undertaken by RI, at which time they are released and reclassified to unrestricted support. Donor restricted resources for research facilities renovation projects are initially recorded as temporarily restricted, and released from their restrictions and reclassified as unrestricted support as the renovations are completed.

Use of Estimates – The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues, expenses, gains, losses and other changes in net assets during the reporting period. Actual results could differ from those estimates.

Cash Equivalents – RI considers all liquid investments with original maturities of three months or less to be cash equivalents. At June 30, 2015 and 2014, cash equivalents consisted primarily of money market funds.

At times during the year, RI may hold deposits in excess of federal depository insurance limits, resulting in a concentration of credit risk.

Investments and Investment Return – Investments in equity and debt securities having a readily determinable fair value are carried at fair value. Equity securities, including interests in start-up companies that do not have a readily determinable fair value, are recorded at cost,

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

10

1. NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) which is evaluated for impairment. Investment return includes dividend, interest and other investment income; realized and unrealized gains and losses on investments carried at fair value; and realized gains and losses on other investments. Other investment return is recorded in the statements of activities as unrestricted or temporarily restricted based upon the existence and nature of any donor or legally imposed restrictions. Bond Issuance Costs – Bond issuance costs of $405,549 incurred in connection with the October 2010 bond issue (see Note 6) are being amortized over the life of the bonds. Amortization expense was $21,345 as of June 30, 2015 and 2014. Amortization expense is expected to be $21,345 annually for the life of the bonds. Property and Equipment – Property and equipment consist of land held for development by Research Properties, Inc., as well as leasehold improvements, furniture and fixtures associated with the administrative offices occupied by RI in the KUMC facility and the life sciences incubator managed by Research Properties, and computers and software (see Note 5). Depreciation is computed on the straight-line basis over estimated useful lives. Assigned lives are as follows:

Leasehold improvements 15 yearsFurniture and equipment 7 yearsComputers and software 3 years

Revenue Recognition – RI receives grant revenues from federal, state, and private sources, as well as from clinical trials. Research revenues from Federal, state, and certain private grants considered to be sponsored research are received in connection with exchange transactions wherein the RI is obligated to provide certain goods and / or services. Receipts for research projects received in advance of costs incurred are recorded as deferred revenue. Certain other private grants generally provide support that is considered contributions, and therefore temporarily restricted until the contracted services have been performed or expenses have been incurred. Grants from these programs are reported as increases in temporarily restricted net assets. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restrictions. Costs incurred in excess of research revenues received are recorded as a receivable equal to the amount expensed for which RI has not yet received reimbursement. An allowance for uncollectible receivables is provided for based on management’s evaluation of potential uncollectible cost reimbursement amounts at year end. Collectability is considered potentially impaired for accounts with grant periods ending more than one year prior to the balance sheet date. Factors management considers in establishing the allowance for uncollectible receivables include an aging of accounts receivable and the likelihood of

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

11

1. NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

collection of individual accounts based on historical experience and established action plans for collections. The allowance as of June 30, 2015 and 2014 was $102,434 and $43,770, respectively.

Clinical trials are considered exchange transactions since the resource provider generally designates the specific research plan, and retains the rights to any results of the trials. Support may be received either on a cost reimbursement basis or in advance of costs incurred. Any funds received in advance are deferred and recognized over the periods in which the trials are conducted. To the extent that support exceeds expenses with respect to corporation-funded contract grants for the purpose of conducting clinical trials, RI’s policy is to commit 100% of such excess, if any, to extended research in pursuit of its mission.

Indirect costs recovered on direct research grants (F&A revenues) are based on cost reimbursement rates, which are negotiated with the U.S. Department of Health and Human Services or the respective private grant donor, as included in each grant agreement.

Grant activities and outlays are subject to audit and acceptance by the granting agency and, as a result of such audit, adjustments could be required.

Fair Value of Financial Instruments – Financial instruments are described as cash or contractual obligations or rights to pay or to receive cash. The fair value for certain financial instruments, including cash and cash equivalents, receivables, accounts payable, and accrued liabilities, approximates the carrying value because of the short-term nature of these instruments. The fair value of instruments is determined based on quoted market prices, other than as described above. The fair value of fixed rate bonds is estimated to approximate carrying value based on the borrowing rates currently available to the University for debt with similar terms and maturities. Estimates of fair values are subjective in nature and involve uncertainties and matters of significant judgment and, therefore, cannot be determined with precision. Changes in assumptions could affect the estimates.

Functional Allocation of Expenses – The costs of supporting the various programs and other activities have been summarized on a functional basis in the statements of activities. Certain costs have been allocated among the program and management and general categories based on estimates of time incurred, usage and other relevant factors.

Transfers to University – RI incurs construction costs for renovations to facilities that will be assets of KUMC and the University of Kansas. As expenditures are incurred, such costs are transferred to KUMC and the University of Kansas and are recorded as “Transfers to University” on the statement of activities. See Notes 5 and 7.

Income Taxes – The RI follows accounting requirements related to uncertain tax positions. Tax positions taken may include positions that the RI is exempt from income taxes or be related to how the RI determines its unrelated business income. The RI recognizes the financial statement effects of a tax position only when it believes it can more likely than not sustain the position upon an examination by the relevant tax authority. Tax years that remain open to review by the Internal Revenue Service include fiscal years ending 2012, 2013, 2014 and 2015. Subsequent Events – Subsequent events have been evaluated through September 3, 2015, which is the date the financial statements were available to be issued.

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

12

2. INVESTMENTS AND INVESTMENT RETURN

Following is a summary of investments and restricted investments by major types at June 30, 2015 and 2014:

2015 2014

Government agencies $ 12,281,001 $ 15,840,551Certificates of deposit 12,531,930 13,287,818Collateralized mortgage obligations 18,680,550 12,639,172Investment in start-up ventures 29,085 29,085

$ 43,522,566 $ 41,796,626

Investment return consisted of the following for the years ended June 30, 2015 and 2014:

2015 2014

Interest income $ 999,901 $ 739,477 Unrealized gain (loss) on investments 46,595 113,039 Net write-off and income (loss) from

Precede Fund, L.C. investments (65) (1,352)Amortization of premiums and discounts (556,977) (484,743)Realized gain (loss) on sales of securities 929 (17,216)

$ 490,383 $ 349,205

As part of its mission, KUCTC enters into joint ventures with start-up companies to further develop and market research technology developed under research projects conducted at KUMC and the University of Kansas. In exchange for the technology and intellectual rights of a project, KUCTC receives partnership interests or common stock in the start-up companies. At the time of transfer and throughout the development of the companies, no market exists for the interests and/or stock. Accordingly, a value is established only after an initial public offering. Thereafter, a quoted market price is used to determine the market values of KUCTC’s interests. Income from joint ventures is reinvested into new research projects at RI or the University of Kansas Center for Research.

At June 30, 2015, KUCTC had equity interests in 27 such companies. Two companies, in which KUCTC owns common shares, are publicly traded, and therefore, the investments were recorded at fair value, based on quoted market prices.

RI holds a 67% interest in the capital (73% income interest) of Precede Fund, L.C., a majority-owned subsidiary established to invest in start-up companies associated with medical research and technology. Investments held by the Precede Fund, L.C. typically have no readily determinable fair value, and thus are recorded using the cost method of accounting and adjusted for other-than-temporary impairment. Certain investments may convert to having a readily determinable fair value, such as after an initial public offering. When that occurs, a value is established for the investment based on a quoted market price, and the investment is recorded at fair value. The aggregate cost of cost-method investments held by the Precede Fund, L.C. totaled $308,525 and $353,525 at June 30, 2015 and 2014, respectively. The evaluation of impairment requires the use of estimates, including an estimate of fair value. RI

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

13

2. INVESTMENTS AND INVESTMENT RETURN (CONTINUED) did not estimate the fair value of these investments; management does not consider it practicable to do so since quoted market prices are not available. During fiscal 2015, one investment was revalued at fair value, due to the investee having a public offering, and thus having a quoted market price. The fair value of this investment at June 30, 2015 was $79,566. Additionally, RI was notified of a change in circumstances with one investee company during 2014, which notified RI of its intent to dissolve the company. Therefore, the Precede Fund’s investment in this company of $150,000 was deemed to be impaired, and was written off in fiscal 2014. The RI did not identify any other events or changes in circumstances that would have a significant adverse effect on the fair value of the investments.

3. FAIR VALUE OF FINANCIAL INSTRUMENTS

Generally accepted accounting principles provide guidance which defines fair value, establishes a framework for measuring fair value under current accounting pronouncements that require or permit fair value measurement, and enhances disclosures about fair value measurements.

This guidance enables the reader of the financial statements to assess the inputs used to develop those measurements by establishing a hierarchy for ranking the quality and reliability of the information used to determine fair values. The statement requires that assets and liabilities carried at fair value will be classified and disclosed in one of the following three categories:

Level 1 Inputs – Quoted prices in active markets for identical assets or liabilities. Level 2 Inputs – Observable market based inputs or unobservable inputs that are corroborated

by market data. Level 3 Inputs – Unobservable inputs that are supported by little or no market activity and that

are significant to the fair value of the assets or liabilities.

Fair values for U.S. government agency securities are determined using quoted prices in principal active markets for identical assets as of the valuation date. The certificates of deposit are brokered between financial institutions, and therefore fair values are estimated using quoted prices in markets that are not active, or from price quotations provided between brokers for comparable investments. The fair value of the collateralized mortgage obligations (CMOs) is based on a model that predicts cash flows, while using some observable inputs for benchmark yields and information about the underlying collateral pool.

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

14

3. FAIR VALUE OF FINANCIAL INSTRUMENTS (CONTINUED)

The following tables set forth RI’s financial assets that were measured at fair value on a recurring basis as of June 30, 2015 and 2014.

2015 Fair Value Measurements Using

Level 1 Level 2 Level 3 Total

Fair Value

Government agencies Federal bonds (AAA) $ 12,281,001 $ -- $ -- $ 12,281,001

Certificates of deposit -- 12,531,930 -- 12,531,930CMO's -- 18,680,550 -- 18,680,550KUCTC investment in startup ventures (equities) 29,085 -- -- 29,085

$ 12,310,086 $ 31,212,480 $ -- $ 43,522,566

2014 Fair Value Measurements Using

Level 1 Level 2 Level 3 Total

Fair Value

Government agencies Federal bonds (AAA) $ 15,840,551 $ -- $ -- $ 15,840,551

Certificates of deposit -- 13,287,818 -- 13,287,818CMO's -- 12,639,172 -- 12,639,172KUCTC investment in

startup ventures (equities) 29,085 -- -- 29,085$ 15,869,636 $ 25,926,990 $ -- $ 41,796,626

4. CONDITIONAL GRANTS AND CONTRIBUTIONS RI expects to receive future funding as a result of conditional grants relating to its research projects program. Conditional grants promised for future fiscal years ending June 30 are summarized as follows:

Fiscal Years Ending June 30, 2016 $ 14,302,058 2017 6,102,435 2018 3,979,441 2019 219,000 2020 219,000

$ 24,821,934 RI has an agreement with the Kansas Bioscience Authority to assist with funding certain research facilities renovations (see Note 9). $7,920,000 will be paid to RI over the next three years in installments of $2,640,000 annually, assuming milestones are achieved. These amounts are included in the annual totals above.

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

15

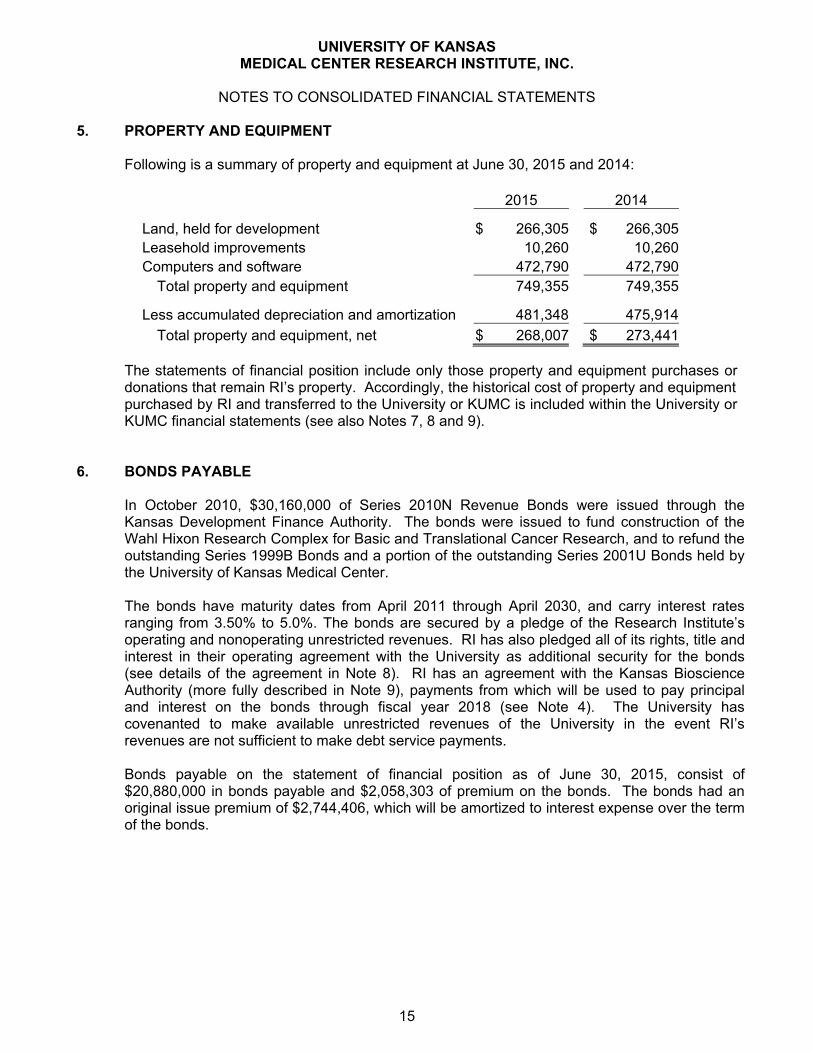

5. PROPERTY AND EQUIPMENT Following is a summary of property and equipment at June 30, 2015 and 2014:

2015 2014

Land, held for development $ 266,305 $ 266,305 Leasehold improvements 10,260 10,260 Computers and software 472,790 472,790

Total property and equipment 749,355 749,355

Less accumulated depreciation and amortization 481,348 475,914

Total property and equipment, net $ 268,007 $ 273,441

The statements of financial position include only those property and equipment purchases or donations that remain RI’s property. Accordingly, the historical cost of property and equipment purchased by RI and transferred to the University or KUMC is included within the University or KUMC financial statements (see also Notes 7, 8 and 9).

6. BONDS PAYABLE

In October 2010, $30,160,000 of Series 2010N Revenue Bonds were issued through the Kansas Development Finance Authority. The bonds were issued to fund construction of the Wahl Hixon Research Complex for Basic and Translational Cancer Research, and to refund the outstanding Series 1999B Bonds and a portion of the outstanding Series 2001U Bonds held by the University of Kansas Medical Center.

The bonds have maturity dates from April 2011 through April 2030, and carry interest rates ranging from 3.50% to 5.0%. The bonds are secured by a pledge of the Research Institute’s operating and nonoperating unrestricted revenues. RI has also pledged all of its rights, title and interest in their operating agreement with the University as additional security for the bonds (see details of the agreement in Note 8). RI has an agreement with the Kansas Bioscience Authority (more fully described in Note 9), payments from which will be used to pay principal and interest on the bonds through fiscal year 2018 (see Note 4). The University has covenanted to make available unrestricted revenues of the University in the event RI’s revenues are not sufficient to make debt service payments.

Bonds payable on the statement of financial position as of June 30, 2015, consist of $20,880,000 in bonds payable and $2,058,303 of premium on the bonds. The bonds had an original issue premium of $2,744,406, which will be amortized to interest expense over the term of the bonds.

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

16

6. BONDS PAYABLE (CONTINUED)

Annual maturities of bonds payable are as follows:

Fiscal Years Ending June 30, 2016 $ 2,310,0002017 2,430,000 2018 2,550,0002019 910,0002020 940,000

Thereafter 11,740,000

$ 20,880,000 Interest paid during the years ending June 30, 2015 and 2014, was $1,027,709 and $1,132,459, respectively, and was included with Facilities Expenses on the statement of activities.

7. CHANGES IN CONSOLIDATED UNRESTRICTED NET ASSETS

Unrestricted net assets are the result of three components: 1) operating activities of RI, 2) amounts designated under RI’s operating agreement with KUMC as described in Notes 6 and 8, and 3) the impact of transfers to the University for Research Facilities Renovation Projects. Since 2009, RI has incurred expenses in excess of revenues for University activities totaling $20,833,596. The deficit in this category of unrestricted net assets will be partially recovered in future years from funding to be received from the Kansas Bioscience Authority (see Notes 4 and 9), and as the bonds payable discussed in Note 6 are repaid. Changes in unrestricted net assets attributable to the Research Institute (the parent) and the noncontrolling interest are as follows: Noncontrolling Controlling Interest Interest Total Unrestricted Unrestricted FHFR & Precede Unrestricted Operations for University Inst. Reserves Fund Net Assets Balance, June 30, 2013 $ 8,459,760 $ (25,783,587) $ 23,930,186 $ 174,302 $ 6,780,661Change in net assets before

transfers 536,211 2,640,000 204,750 (50,447) 3,330,514Transfers to University -- (330,009) -- -- (330,009) Balance, June 30, 2014 8,995,971 (23,473,596) 24,134,936 123,855 9,781,166Change in net assets before

transfers (2,726,869) 2,640,000 643,407 11,441 567,979Transfers to University -- -- -- -- -- Balance, June 30, 2015 $ 6,269,102 $ (20,833,596) $ 24,778,343 $ 135,296 $ 10,349,145

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

17

8. RELATED PARTY TRANSACTIONS Operating Agreement with University of Kansas. RI has an operating agreement with the University of Kansas (which includes KUMC). Significant provisions of the agreement are as follows: that RI will manage and administer all KUMC extramural grants and contracts (including clinical trials); certain facilities and administrative (indirect) costs collected will be utilized by RI as directed by KUMC; RI will occupy and use facilities of KUMC based on its agreement that the recovery of F&A and contract administration fees be shared with or used as designated by KUMC. A significant portion of RI’s grant expenditures are paid through the KUMC payroll and procurement system and RI reimburses all such expenditures to KUMC. The total amount owed to related parties as of June 30, 2015 and 2014 was $1,614,729 and $1,284,370, respectively. RI acquires a significant amount of equipment for use through its research projects program. Under the operating agreement noted above, after purchase, ownership of the equipment is transferred to KUMC for further use by its faculty. No depreciation expense is recognized by RI with respect to equipment acquired for use in research projects; instead, the entire amount of such equipment acquisitions is charged to program expense under the captions “Capital Equipment Donation to KUMC” and “Equipment and other non-capital items donation to KUMC” in the period of acquisition. The total amount of capital equipment and other non-capital items donated to KUMC for the years ended June 30, 2015 and 2014 was $3,530,865 and $1,376,381, respectively. Facilities Renovations. RI also incurs construction costs for renovations to facilities that will be assets of KUMC and the University of Kansas. As expenditures are incurred, such costs are transferred to KUMC and the University of Kansas and are recorded as “Transfers to University” on the statement of activities. See also Note 9. During the current fiscal year, RI began a project to renovate the Simulation Center on the KUMC campus. For the year ended June 30, 2015, construction expenditures were $691,632 and recorded as “Capital asset donations to KUMC” on the Functional Expenses statement. Leases. Effective October 15, 2012, RI entered into a new lease agreement with FOBN, LLC, a subsidiary of the KU Endowment Association for new commercial office space. This lease expires December 31, 2015. The future minimum lease payments amount to $151,784 for the fiscal year ending June 30, 2016. Rent expense related to this lease totaled $288,964 for the year ended June 30, 2015. KUMC funded leasehold improvements and furniture and equipment totaling approximately $430,000 for the new leased space, by directing funds to be utilized from the net assets held by RI as KUMC Institutional Reserves. KUMC retained title in all such capital assets. RI has not recorded a value for use of these contributed long-lived assets, as such value on an annual basis over the life of the assets is not considered material to the financial statements. KUMC Debt Service. During the years ended June 30, 2015 and 2014, RI paid $4,066,530 and $4,173,869, respectively of debt service related to a KUMC bond issue. The expense was recorded within University Support on the statement of activities.

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

18

8. RELATED PARTY TRANSACTIONS (CONTINUED) KUCTC. KUCTC has an agreement to provide technology transfer services to all campuses of the University of Kansas. The University of Kansas Center for Research, Inc. (KUCR) and RI share the cost of operations of KUCTC, based on services provided at each campus. During the years ended June 30, 2015 and 2014, KUCR provided $740,000 of support to KUCTC each year to fund operations, and RI provided $447,375 of support each year, which was eliminated in consolidation. KUCTC has a revenue sharing agreement with KU and the RI. Annually, a calculation is done of net assets in excess of KUCTC’s operating expenses for the following fiscal year as defined by the agreement. Such excess is to be distributed to KU and the RI, as agreed-upon between the parties. For the year ended June 30, 2015, $1,016,918 was the total to be distributed, with $762,688 allocated to KU, and the remainder to the RI. The allocation to KU is recorded as a revenue distribution payable; the amount for the RI was eliminated in consolidation. Other. Through its relationship with KU and KUMC, RI is also affiliated with the University of Kansas Memorial Corporation, KU Health Partners, Inc., and the Student Union Corporation of the University of Kansas Medical Center. For the years ended June 30, 2015 and 2014, RI had no transactions with these entities.

9. FACILITIES RENOVATIONS

Construction costs related to research facilities that will be assets of KUMC and the University are included with the Transfers to University expenditures on the statements of activities. RI previously provided funding and construction for one facility as described below. RI began a $34,000,000 project to renovate the Wahl Hixon Research Complex for Basic and Translational Cancer Research in fiscal 2009. Construction was financed by the 2010N Revenue Bonds described in Note 6. Additional funding for costs of construction, as well as the repayment of debt service on the bonds is provided, in part, by an agreement with the Kansas Bioscience Authority (KBA) for a grant that would cover up to $26,400,000 of the total project cost. The grant is to be distributed from KBA to RI in equal installments over ten years. Payments received from KBA are contingent upon RI meeting milestones as outlined in the agreement related to the construction plan, recruitment and retention of research scholars, and continuing use of the facility for research. Receipt of payments is also contingent upon the KBA maintaining sufficient funding to meet commitments going forward. KBA is funded by the State of Kansas based on a formula outlined in Kansas statutes. The statutes have been amended in recent years to place further limits on the amount of funding provided to the KBA. Due to these contingencies, the funding has not been reflected on the statement of financial position as a receivable. For the years ended June 30, 2015 and 2014, construction expenditures were $0 and $330,009, and research facilities renovation grant revenue recognized from the KBA was $2,640,000 each year.

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

19

10. DEFINED CONTRIBUTION RETIREMENT PLAN

RI maintains with Principal a mandatory, contributory funded 403(b) retirement plan for employees. All employees are eligible except students, seasonal, temporary and part-time employees who work less than 1,000 hours in a 12-month period. When an employee becomes eligible to participate in the plan, participation is a condition of employment or continuing employment. Eligible employees are required to contribute 5.5% of gross earnings by payroll deduction (pre-tax). In addition, RI contributes 8.5% of the employee’s gross earnings. For the fiscal years ended June 30, 2015 and 2014, the amount of retirement plan expense was $231,008 and $210,636, respectively. RI provides a voluntary tax-sheltered annuity program which is separate from the Defined Contribution Retirement Plan. Employees who have not yet completed the one-year waiting period for participation in the Defined Contribution Retirement Plan and/or employees who want to defer additional salary may do so in a Principal Voluntary Retirement Annuity.

SUPPLEMENTARY INFORMATION

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATING STATEMENT OF FINANCIAL POSITION

June 30, 2015

Research ResearchInstitute Properties KUCTC Eliminations Consolidated

AssetsCash and cash equivalents $ 8,235,594 $ -- $ 1,156,230 $ -- $ 9,391,824Investments 43,493,481 -- 29,085 -- 43,522,566Precede Fund, L.C. investments 409,989 -- -- -- 409,989Reimbursable costs incurred in excess of research

revenues received, net 9,356,088 -- -- -- 9,356,088Accounts receivable 447,375 -- 370,000 -- 817,375Interest receivable 57,043 -- -- -- 57,043Prepaid expenses 182,323 -- 16,644 -- 198,967Due from KUCTC 254,230 -- -- (254,230) --Bond issuance costs 304,157 -- -- -- 304,157Land, equipment and leasehold improvements, net -- 268,007 -- -- 268,007

Total assets $ 62,740,280 $ 268,007 $ 1,571,959 $ (254,230) $ 64,326,016

LiabilitiesAccounts payable $ 3,181,646 $ 56,782 $ 38,746 $ -- $ 3,277,174Accrued expenses 244,578 -- 60,180 -- 304,758Accrued interest payable 228,871 -- -- -- 228,871Revenue distribution payable -- -- 1,016,918 (254,230) 762,688Deferred revenue - clinical trials 9,452,963 -- -- -- 9,452,963Deferred revenue - other 5,620,786 -- -- -- 5,620,786Deferred revenue - federal grants 860,162 -- -- -- 860,162Deferred revenue - state grants 521,370 -- -- -- 521,370Bonds payable 22,938,303 -- -- -- 22,938,303

Total liabilities 43,048,679 56,782 1,115,844 (254,230) 43,967,075

Net assetsUnrestricted:

Designated 25,067,387 -- -- -- 25,067,387Undesignated (15,520,878) 211,225 456,115 -- (14,853,538)Noncontrolling interest in subsidiary 135,296 -- -- -- 135,296

Temporarily restricted 10,009,796 -- -- -- 10,009,796

Total net assets 19,691,601 211,225 456,115 -- 20,358,941

Total liabilities and net assets $ 62,740,280 $ 268,007 $ 1,571,959 $ (254,230) $ 64,326,016

20

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

CONSOLIDATING STATEMENT OF ACTIVITIES

Year Ended June 30, 2015

Research ResearchInstitute Properties KUCTC Eliminations Consolidated

Revenues, gains and other supportDirect research income $ 81,303,972 $ -- $ -- $ -- $ 81,303,972Clinical trials 7,170,792 -- -- -- 7,170,792Clinical trial IRB and administrative fees 1,044,292 -- -- -- 1,044,292Facilities & administrative revenue 22,388,853 -- -- -- 22,388,853Research facilities renovation grants 2,640,000 -- -- -- 2,640,000Public support 126,000 -- -- -- 126,000Extramural funding -- -- 175,000 -- 175,000Research Properties, Inc., rental income

and RI support -- 577,278 -- (368,635) 208,643Support for KU Center for Technology

Commercialization, Inc. -- -- 1,187,375 (447,375) 740,000Revenue distribution 254,230 -- -- (254,230) --Royalties and technology income 1,158,047 -- 358,066 (273,728) 1,242,385Investment return 490,383 -- -- -- 490,383Other income 601,816 -- 14,728 -- 616,544

117,178,385 577,278 1,735,169 (1,343,968) 118,146,864

Satisfaction of program restrictions -- -- -- -- --

Total revenues, gain andother support 117,178,385 577,278 1,735,169 (1,343,968) 118,146,864

Functional ExpensesDirect research 93,630,614 -- -- -- 93,630,614 Facilities 1,570,131 -- -- -- 1,570,131 University support 10,966,530 -- -- -- 10,966,530 Royalties and technology 1,565,035 -- -- (273,728) 1,291,307 Research administration 2,382,748 -- -- -- 2,382,748 Management and general 2,089,243 -- -- -- 2,089,243 Research Properties, Inc. 368,635 577,278 -- (368,635) 577,278 KU Center for Technology

Commercialization, Inc. 447,375 -- 2,645,971 (701,605) 2,391,741

Total expenses 113,020,311 577,278 2,645,971 (1,343,968) 114,899,592

Change in net assets before transfers 4,158,074 -- (910,802) -- 3,247,272

Transfers to University -- -- -- -- --

Consolidated change in net assets after transfers 4,158,074 -- (910,802) -- 3,247,272

Net assets, beginning of year 15,533,527 211,225 1,366,917 -- 17,111,669

Net assets, end of year $ 19,691,601 $ 211,225 $ 456,115 $ -- $ 20,358,941

21

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

FUNCTIONAL EXPENSES

Year Ended June 30, 2015

Personnel $ 46,467,977 $ 42,721,974 $ -- $ -- $ -- $ -- $ 761,723 $ 1,746,059 $ 1,238,221

Fringe benefits 11,999,252 11,083,552 -- -- -- -- 184,050 444,128 287,522

Contract services 167,187 154,020 -- -- -- -- -- 3,332 9,835

Travel, food and meetings 1,863,514 1,767,561 -- -- -- -- 43,387 23,430 29,136

Professional fees 4,583,103 3,095,126 -- -- 468,665 363,812 459,064 73,174 123,262

Subaward payments 9,991,227 9,991,227 -- -- -- -- -- -- --

Supplies 7,245,402 7,221,109 -- -- (17,131) 937 775 5,539 34,173

Depreciation 5,434 -- -- -- -- 1,650 3,784 -- --

Payments to students & subjects 1,909,861 1,909,461 -- -- -- -- -- -- 400

Fees, dues, charges 10,063,929 9,883,041 1,500 -- 1,514 25 91,005 38,499 48,345

Capital asset donation

to KUMC 3,452,955 2,557,859 691,632 -- -- -- -- 27,472 175,992

Equipment and other non-capital

items 769,542 662,473 -- -- -- -- 69,885 1,442 35,742

Services 2,803,147 2,520,963 -- -- 1,971 210,854 12,880 19,673 36,806

F&A transfer for University

operations 10,966,530 -- -- 10,966,530 -- -- -- -- --

Revenue distributions 762,688 -- -- -- -- -- 762,688 -- --

Royalty distributions 838,788 -- -- -- 836,288 -- 2,500 -- --

Interest expense 1,000,096 -- 1,000,096 -- -- -- -- -- --

Amortization of bond premium

and issuance costs (123,097) -- (123,097) -- -- -- -- -- --

Uncollectible receivable expense 56,948 56,948 -- -- -- -- -- -- --

Impairment loss -- -- -- -- -- -- -- -- --

Insurance 75,109 5,300 -- -- -- -- -- -- 69,809

Total $ 114,899,592 $ 93,630,614 $ 1,570,131 $ 10,966,530 $ 1,291,307 $ 577,278 $ 2,391,741 $ 2,382,748 $ 2,089,243

22

2015 Management and General2015 Totals Direct Research

Royalties and Technology

Research Properties

2015 Programs

University SupportFacilities KUCTC

Research Administration

UNIVERSITY OF KANSAS MEDICAL CENTER RESEARCH INSTITUTE, INC.

FUNCTIONAL EXPENSES

Year Ended June 30, 2014

Personnel $ 46,903,597 $ 43,754,563 $ -- $ -- $ 29,115 $ -- $ 678,633 $ 1,613,860 $ 827,426

Fringe benefits 12,405,722 11,609,009 -- -- 8,761 -- 154,024 428,896 205,032

Contract services 123,897 123,897 -- -- -- -- -- -- --

Travel, food and meetings 2,049,855 1,956,677 -- -- 643 -- 46,023 28,615 17,897

Professional fees 4,445,782 2,851,846 -- -- 232,405 354,630 815,194 74,495 117,212

Subaward payments 7,211,769 7,211,769 -- -- -- -- -- -- --

Supplies 6,238,995 6,203,826 -- -- 113 -- 179 12,871 22,006

Depreciation 7,843 -- -- -- -- 2,512 5,331 -- --

Payments to students & subjects 1,590,251 1,590,251 -- -- -- -- -- -- --

Fees, dues, charges 8,972,142 8,875,894 750 -- 4,664 60 29,500 19,462 41,812

Capital equipment donation

to KUMC 772,640 753,260 -- -- -- -- -- -- 19,380

Equipment and other non-capital

items 606,433 588,130 -- -- 2,692 -- 328 347 14,936

Services 2,384,273 2,079,416 -- -- 1,904 202,116 30,199 43,508 27,130

F&A transfer for University

operations 10,966,490 -- -- 10,966,490 -- -- -- -- --

Royalty distributions 590,917 -- -- -- 590,917 -- -- -- --

Interest expense 1,107,021 -- 1,107,021 -- -- -- -- -- --

Amortization of bond premium

and issuance costs (123,096) -- (123,096) -- -- -- -- -- --

Uncollectible receivable expense -- -- -- -- -- -- -- -- --

Impairment loss 150,000 -- -- -- -- -- -- -- 150,000

Insurance 63,824 -- -- -- -- -- -- -- 63,824

Total $ 106,468,355 $ 87,598,538 $ 984,675 $ 10,966,490 $ 871,214 $ 559,318 $ 1,759,411 $ 2,222,054 $ 1,506,655

23

Research Administration

2014 Management and General

2014 Programs

2014 Totals Direct Research FacilitiesUniversity

SupportRoyalties and

TechnologyResearch Properties KUCTC

301 N. Main, Suite 1700 ● Wichita, Kansas 67202-4868 ● (316) 267-7231 ● (316) 267-0339 fax ● www.aghlc.com

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL

OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS

PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS Board of Directors University of Kansas Medical Center Research Institute, Inc. Kansas City, Kansas We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the consolidated financial statements of the University of Kansas Medical Center Research Institute, Inc. (RI) which comprise the consolidated statement of financial position as of June 30, 2015, and the related consolidated statements of activities and cash flows for the year then ended, and the related notes to the financial statements, and have issued our report thereon dated September 3, 2015. Internal Control Over Financial Reporting In planning and performing our audit of the consolidated financial statements, we considered the RI’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the RI’s internal control. Accordingly, we do not express an opinion on the effectiveness of the RI’s internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

25

Compliance and Other Matters As part of obtaining reasonable assurance about whether the RI's consolidated financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the result of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on comp0liance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Allen, Gibbs & Houlik, L.C. CERTIFIED PUBLIC ACCOUNTANTS September 3, 2015 Wichita, Kansas