UNIVERSITÀ DEGLI STUDI DI TRIESTE - justin will creations · UNIVERSITÀ DEGLI STUDI DI TRIESTE ....

49

UNIVERSITÀ DEGLI STUDI DI TRIESTE MASTER IN COFFEE ECONOMICS AND SCIENCE – ERNESTO ILLY MASTER THESIS “Collaborative International Expansion of Smallholder Coffee Farms: A Business Model for Partnerships in Consuming Markets” Student: Supervisors: Justin Will Prof. Pierpaolo Andriani Prof. Eliana Cossio Prof. Andrea Tracogna Anno Accademico 2015/2016

Transcript of UNIVERSITÀ DEGLI STUDI DI TRIESTE - justin will creations · UNIVERSITÀ DEGLI STUDI DI TRIESTE ....

UNIVERSITÀ DEGLI STUDI DI TRIESTE

MASTER IN COFFEE ECONOMICS AND SCIENCE – ERNESTO ILLY

MASTER THESIS

“Collaborative International Expansion of Smallholder Coffee Farms:

A Business Model for Partnerships in Consuming Markets”

Student: Supervisors: Justin Will Prof. Pierpaolo Andriani Prof. Eliana Cossio Prof. Andrea Tracogna

Anno Accademico 2015/2016

ACKNOWLEDGEMENTS

Special thanks to:

- My family and cohort, who are always ready to listen to my ideas,

no matter how outlandish they may be.

- My ever-supportive advisors, Professors Andriani, Cossio, and

Tracogna.

- The Ernesto Illy Foundation for creating such an amazing

program, and the Master’s Staff who made it so much more!

- And finally, my wife Elise, for whom there are no words to

express the endless contributions she’s made to my life, and to

my personal and professional development.

. . : : Hic sunt leones : : . .

ABSTRACT

In a word, the goal of this thesis is disintermediation, or the empowerment that comes to

small businesses by removing intermediaries that are unnecessary to them. Even for the

professional coffee farmer, the supply chain is nearly incomprehensible. Its length, costs, and

sheer geographical span are immensely complex and diverse. A farmer, like a consumer,

doesn’t have the time to study-up on how to best use its complexity. To address this issue, I

am proposing a collaborative business partnership that will unite farmer and roaster in a

dynamic equity venture with the objective of stabilizing each other’s financial forecasts and

enabling future growth. Furthermore, this partnership will bridge the information gap

between farm and cup by directly aligning the business interests of both entities, creating a

direct communication channel to the consumer never before seen in the coffee industry.

TABLE OF CONTENTS

CHAPTER I. INTRODUCTION a. Abstract b. Wait, but why? c. How?

CHAPTER II. GOALS a. Identify the interests and benefits for roasters and farmers b. Numerically estimate the value created by an international partnership c. Consider strategies for implementation

CHAPTER III. METHODS CHAPTER IV. MARKET CONDITIONS

a. System b. Smallholder Farms c. Small Business Roasters

CHAPTER V. EXISTING MODELS a. Traditional Commodity Supply Chain b. Traceable Sourcing c. Direct Trade d. Vertical Integrations

CHAPTER VI. PROPOSED MODEL a. Bulk Investment Mechanism b. Continuous Equity Dispersal Mechanism

CHAPTER VII. FINDINGS AND RESULTS a. Data Parameters b. Cost Escalation c. Profit d. Direct Trade

CHAPTER VIII. DISCUSSION a. Barriers b. Advantages of the International Partnership c. Disadvantages of the International Partnership d. Thoughts on Implementation

CHAPTER IX. CONCLUSIONS CHAPTER X. BIBLIOGRAPHY

..:: 1 ::..

CHAPTER I. INTRODUCTION

a. Wait, but why?

Coffee commodity markets are notoriously complex and undifferentiated, not to mention

volatile. For coffee, it is a labyrinth of stakeholders spread across the world, making

communication unreliable and inconsistent from one end of the chain to the other. This lack of

information fosters a significant misunderstanding of coffee’s true value, leaving the end

consumer grossly under-informed. This is not the ideal system for smallholder farms, most of

whom lack the time and resources to play on this level.

Such a coffee farmer becomes a “price-taker” because their produce is valued by the

speculative commodity market, not by the end consumer, forcing the farmer to accept

whatever price the market is offering. This unpredictability to the farmer’s finances makes

year-to-year forecasting and investments very difficult to manage, in addition to a lack of

available business loans.

Furthermore, smallholder coffee farmers are struggling to keep pace with the global

challenges. There are increasing demands and costs put on coffee producers. Climate Change

for example, has had devastating effects on coffee farms in places like South America and

Africa, and may threaten the majority of suitable land on these continents over the next

several decades. In the meantime, worldwide consumption is increasing, putting more and

more pressure on farmers to simultaneously increase quantity and quality, all-the-while only

receiving a fraction of what the customer pays per cup.

Likewise, small business roasters face challenges when competing with the big players in the

industry. Although growing in popularity, third wave coffee shops and coffee roasters

represent a small portion of the US market for coffee, limiting their influence on the global

market. Roasters face equally difficult challenges when faced with the market volatility, and

opportunities for expansion.

..:: 2 ::..

b. How?

As is often the solution for small businesses, partnerships can address some of these

difficulties in the coffee industry. An international partnership between smallholder farms and

small business roasters can help serve as a stabilizing force to both businesses, as well as

enabling them for improved growth.

..:: 3 ::..

CHAPTER II. GOALS

The purpose of this thesis is to explore opportunities for direct international partnerships and

disintermediation to improve the business prospects for smallholder coffee farms and small

coffee roasters. To this end, the goals of this thesis will be:

i. Identify the interests and benefits for roasters and farmers

ii. Numerically estimate the value created by an international

partnership

iii. Consider strategies for implementation

..:: 4 ::..

CHAPTER III. METHODS

I will begin with a review of existing literature and market conditions to describe the current

business environment, as well as elaborate on the troubles experiences by these small

businesses. I will then analyze the current supply chain models and their capacity to address

the struggles of small business. Next, using real world transactions as the dataset, I will present

the status quo for supply chain actors, estimating their value-additions and profit share in the

chain. Finally, I will propose and describe an international partnership model aimed at

stabilizing and enabling the market for small coffee businesses. I will contextualize this

proposal using those same real world transactions, concluding with numerical and qualitative

estimates to the value it would create for these key smallholder players.

..:: 5 ::..

CHAPTER IV. MARKET CONDITIONS

a. The Coffee Industry

Market Volatility

One of the first things any coffee trader will tell you, is that the market for coffee is heavy with

speculation, causing it to behave very erratically. Over the last few decades, the market price

has doubled and halved, multiple times, compared to its long-run average of around $1.03 / lb.

Figure 1: Graph of Coffee Price History (www.ico.org)

When the price of coffee fluctuates, the frequency of fluctuations benefits those that can stay

informed. This is not an advantage of smallholder farms that are already minimally staffed, and

can’t afford to engage in speculation or hedging. Large coffee farming operations and

exporters may be able to afford to employ a commodity trader whose sole task is to optimize

their company’s performance in the commodity market. There’s simply no way a smallholder

farmer can compete with that, and the end result is that farmers must accept whatever price is

offered, while informed traders can play the market to their own profit.

This price volatility also impacts life for the roaster who relies on buying low to make profit as

well. On the other hand, for a roaster, the only thing worse than overpaying for coffee, is not

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

Coffee Prices to the Farmer(1990 – 2016)

Coffee Prices

..:: 6 ::..

having any. So this leaves the roaster with equally little choice, and is likewise forced to be a

“price-taker”.

Figure 2: Constructing the Coffee Commodity Price

The unpredictability is worse when you factor in the price differential. Typically, in the

commodity coffee market, coffee pricing is based on two factors, the market price, and a price

differential. The commodity price is what fluctuates erratically with the stock market, but the

“differential is determined by the coffee broker, the farm, or the country of origin, and is

based on the quantity and quality available, in the long and short term.” (Graham, S.) Price

differentials can be positive (a.k.a. premiums) or negative (a.k.a. discounts).

Differential Countries

- $0.04/lb Dominican Republic, Ecuador, and Peru

- $0.03/lb Burundi, India, and Rwanda

- $0.01/lb Honduras and Venezuela

At Par Costa Rica, El Salvador, Guatemala, Kenya, Mexico, New

Guinea, Nicaragua, Panama, Tanzania, and Uganda

+ $0.02/lb Colombia

Table 1: Price Differentials by Country (www.stocktongraham.com)

Total Coffee Price

Commodity Price

Premium (usually for quality)

..:: 7 ::..

Climate Change

In the world of commodity economics, coffee has a special personality. It is one of the most

traded commodities in the world, but it’s almost exclusively produced in developing countries

and consumed in developed ones. Climate Change is the biggest challenge facing this industry,

and the planet for that matter. It is increasing global temperatures, shifting and intensifying

weather patterns, and causing increasingly restrictive governmental policies aimed at

improving sustainability. Farmers certainly have their work cut out for them.

In the next several years, the land considered suitable for coffee production will decrease

considerably (Figure 2). This can be the result of both increases in temperature, known as

global warming, or changing weather patterns that cause extensive droughts (Figure 3) or

untimely frosts. These effects are most extreme in places like Brazil, where the change in

climate will damage much of their current farmland. And as the world’s biggest coffee-

producing country, Brazil’s climate issues have significant ripple effects on the coffee

commodity market.

Figure 3: Changes in Suitable Coffee-growing Land in Central America (World Coffee Research)

..:: 8 ::..

Another example of the destructive power of climate change is Columbia, for reasons that

might not be evident to consumers, which is all the more reason to bring both sides to the

table. Columbia is in a region of South America that is directly affected by the temperature

shifts of the Pacific Ocean, something known as the El Niño and La Niña effects. Both are

naturally occurring cycles in the earth’s climate, but when global temperatures shift, so do the

intensity of these cycles. In the case of Columbia, this can mean extremely wet seasons, filled

with near-constant, and heavy rains (Figure 3). This sounds horrible already, but one might not

realize the effects that extensive rain can have – not just on the crops, but on the diseases and

pests that feed on them. One in particular, coffee rust, is a fungus that spreads from plant to

plant through wind and rain splatter, so when it rains continuously, the growth becomes

epidemic. And this is precisely what happened in 2008 when Columbia lost nearly a third of

their crop to rust. Columbia, the third largest producer in the world, losing so much coffee had

a huge impact on the market. It wasn’t until 2014 that they fully recovered to pre-epidemic

production levels.

Figure 4: Changes in Precipitation Patterns of South America (National Geographic)

..:: 9 ::..

Communication

The coffee supply chain is a geographically spread out series of multiple actors. By magnitude

alone it is an inefficient system for communication, as messages are changed and

miscommunicated throughout each link of the chain. The result of these inefficiencies is a

dissonance between what a consumer wants, and what a farmer believes the consumer wants

– or vice versa, what a farmer does, and what a consumer believes a farmer does. It is a system

that is currently incapable of overcoming the geographical and technological distances

between these two parties.

This lack of information fosters a significant misunderstanding of the coffee’s impact. For much

of the coffee available, labor conditions and production methods differ from that which the

consumer might prefer if he or she readily had access to that knowledge. But this is not the

fault of the consumers, nor the producers. It’s an institutionalized shortcoming that results

from systemic complexity, allowing only the most quantifiable and binary information to pass

through. This is why “yes or no” characteristics like Organic and Fair Trade Certifications can

work, or why cup quality scores have so much bearing – they are all easily described and

translated across the chain. Consumer behavior isn’t that binary however, and customer

preferences can fluctuate on intangible characteristics like fads and marketing that have no

relevance to the farmer, proving the disconnect.

b. The Smallholder Farm

Profit Share

One of the downsides of having such a long and complicated supply chain is that

intermediaries are often necessary to move the product along. Each intermediary in turn

performs an action and receives a profit, which adds to the total cost of that product. This

phenomenon is called “cost escalation” and it is particularly relevant in the coffee supply

chain.

..:: 10 ::..

Sources vary on what percentage of the final price is received by the coffee farmer, but it’s

generally considered to be very low. PBS estimates that 12% of every dollar ends up in the

farmers’ hands, but even that seems optimistic. (Whalen, K.) In a later section I’ll discuss how

these compare to my own findings, and how it would be affected by an international

partnership.

Supply Chain Actor Share of Revenue

Farmers 10-12%

Traders 2-3%

Shippers 4%

Roasters 65-70%

Retailers 10-15%

Table 2: Revenue Share by Supply Chain Actor (www.pbs.org)

Certifications

As mentioned above, certifications serve as a more efficient and binary manner of conveying

information up the supply chain by consolidating all the information about organics, fair trade,

sustainability etc. into a simple up or down vote. There are conflicting opinions in the world

about whether this is a positive or a negative for the industry, but if nothing else, it does give

the customer at least some level of specific evaluation criteria with which to judge products.

For the farmers however, certifications can often feel like an over-burdensome set of

restrictions, and even worse, a costly expense when it comes to paying for inspectors to visit

every year. (Janssen, R.) (Charles, D.)

Price-fixing certifications like Fair Trade are most useful to farmers when the market price is

low, ensuring that the farmers are receiving enough to survive. When the market is up,

however, the certification isn’t really contributing to the farmers’ bottom line, and it often

leads them to seek market pricing for their best specialty coffees which can fetch even more

than the fair trade price. The trouble with this strategy is similar to other challenges faced by

smallholder farms, they simply aren’t market experts. Smallholder farms have to rely on supply

..:: 11 ::..

chain intermediaries to seek out the best price, like coffee traders, who in turn take a share of

the profit.

Access to Finance

One of the least understood problems for farmers is their lack of access to modern financial

instruments. It’s a trouble that’s rooted in how agricultural capital management compares to

other industries, because farming involves large transaction costs, very long-term capital

investments, high costs associated with operating in isolated markets, and low-value, high-

volume returns.

In the meantime, farmers have little access to credit, and therefore have little credit history or

familiarity with credit processes. This has an even more profound effect when considering that

their social circles also lack credit experience, creating a society-wide lack of credit culture.

This makes financing riskier for lenders, who expect borrowers to have a good grip on payback

policies and the consequences of default. Without a culture of crediting, farmers lack the

experience to properly manage their financial risks, and without experience in lending to the

agricultural sector, lenders are unable to properly manage transaction and market risks.

(Galindo, M.)

..:: 12 ::..

Figure 5: Perceived Risks and Access to Financing (Galindo, M.)

Additionally, farmers cannot offer much in terms of collateral, which in other cases may

assuage wary lenders. There are options out there for farmers to leverage their harvest as

collateral, but time has shown that these farmers tend to find themselves in a perpetual state

of debt, having given away their entire crop before they have even harvested it.

The situation is not limited to coffee farmers either. According to multiple sources, global

unmet demand for smallholder finance is estimated between $200 and $450 billion, and

bound to increase as the global food demand increases with population growth. (Carroll, T.)

(CSAF)

Smallholders

The majority of coffee farmers in the world are smallholder farmers, meaning they cultivate on

small tracts of land, the size of which varies by country and climate. (United Nations) In

Colombia, for example, despite its contribution as the third largest coffee-producing country,

..:: 13 ::..

the average plantation is just 2 hectares. (Café de Colombia) But size isn’t the only

characteristic of a smallholder farm, because the term also describes the economic prospects

of the business. They are generally engaged in non-farming income streams as well, so they

often find themselves in a vulnerable position of being impacted by market volatility, yet less

able to respond to market shifts.

In simpler terms, smallholder farms do not benefit from economies of scale like larger farms,

so they are often hindered in their ability to compete. This is a natural occurrence in free

markets, to be sure, but as customer preferences continue to narrow from origin country, to

origin region, to origin farm, smallholder farmers are facing an incredible opportunity to

prosper.

c. The Small Business Roaster

Third Wave Coffee

This shift in customer preferences is credited to what’s called, the third wave coffee

movement. It’s characterized with increasing standards in coffee sourcing and beverage

preparation. It’s similar to the emergence of the craft beer industry – in both cases, a

traditional industry has been challenged by the emergence of an artisan elite, crafting a new

level of appreciation. Arguably, this may have been the case for the rise of fine wines and

scotches as well.

Customers are demanding specialized coffees that are distinguished, either with certifications,

or colorful histories. One of the histories popular as of late, is “Farm-to-cup” identification.

This isn’t a certification, per se, but rather a description of the sourcing channel, a concept

valued by young consumers that participate in “glocal” consumption schemes. When a

consumer can link their beverage with a time and place in the world, they feel connected, an

intangible value-addition to the pastime.

..:: 14 ::..

Small Business Failure Rates

The market response to a “glocally-minded” customer base has been an expansion in the

number of small roasters that coincide with the growth of coffee chains like Starbucks. Small

roasters are riding the tide in increasing coffee consumption, but offer something the national

chains can’t – a way to create a uniquely-local relationship with the surrounding community.

The trouble with any small business however, is the mediocre probability of economic success.

According to the US Small Business Association (SBA), one third of all small businesses fail

within the first 2 years, and 50% within in 5 years. The good news though, for those that make

it past year 5, the failure rate levels out and the outlook is very positive. Additionally, the food

industry demonstrates similar failure rates to all other industries, which contradicts the

conventional wisdom that it’s a riskier business to go into.

However, a substantial threat still looms when small businesses have to compete with national

chains, and that is the advantages of economies-of-scale. Big players can compete better on

price because of their size, leaving small businesses to fight out the battle of start-up and

operating costs with significantly less resources.

Roaster Costs

In the case of the coffee shop, start-up costs are high compared to the value of the product

being sold. Coffee, for example, is a lot less expensive that an entrée served at a restaurant,

though similar requirements exists for equipment and infrastructure needed to meet health

codes in a café. However, in the event that the roaster is not selling brewed coffee on-site, and

instead focuses on wholesale, the costs are more manageable, along the lines of the following

estimates:

..:: 15 ::..

Start-up Costs $

Roasting Machine $15,000

Packaging Equipment $5,000

Quality Control Equipment $5,000

Space Modifications $15,000

First Rent and Deposit $4,000

Raw Materials (500kg) $5,000

TOTAL $49,000

Table 3: Roaster Start-up Costs

Operating Costs $/lb

Fixed Costs (Rent, Labor) $3.00

Variable Costs (Coffee, Fuel) $5.37

Roasting Losses (15%) $0.95

TOTAL COGS $9.32

Table 4: Roaster Operating Costs

Fortunately, the market for a pound of locally-roasted coffee is asking about $22.00 / lb in

retail, and $15 / lb in wholesale. At that rate, assuming the roaster sells 500 lbs / month, it will

take him/her 1.5 years to get out of the red.

Figure 6: Breakeven Curve for a Typical Roaster

-$60,000

-$40,000

-$20,000

$0

$20,000

$40,000

$60,000

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct

..:: 16 ::..

CHAPTER V. EXISTING MODELS

Do international partnerships already exist? Well, yes and no. There does not appear to be any

evidence of an original partnership being formed between roaster and farmer, however we

have seen evidence of vertically integrated coffee companies, as well as a trend of roasters

purchasing from coffee farmers through a single intermediary.

Based on my research and experience, I have identified 4 categories of supply chain models

within the coffee industry, each with its own level of fidelity when it comes to buyer-grower

relations:

1. Traditional Commodity Chain

2. Traceable Sourcing

3. Direct Trade

4. Vertical Integrations

a. Traditional Commodity Chain

The traditional commodity supply chain is composed of multiple independent actors, each

contributing a value addition. The many actors in this arrangement make for a very specialized

and effective chain. Each level is beholden to its customer at the next level, so the business

focus is often narrowed to one level up, or one level down. The levels are also dispersed

geographically, as the product moves from origin to consuming countries.

..:: 17 ::..

Figure 7: Diagram of the Typical Coffee Supply Chain (www.forbes.com)

In simpler terms though, and for the sake of argument in this thesis, we can view the supply

chain as just 5 or 6 levels: Farmer, Exporter, Freight Forwarder, Import, Roaster, and in some

cases, an independent Retailer.

Figure 8: Typical Actors in the Coffee Supply Chain

..:: 18 ::..

b. Traceable Sourcing

Coffee can be referred to as traceable when, even at the end of the chain, it can be tracked

back to the original farm or co-op. While the physical coffee can still be traded between

multiple parties in the supply chain, as long as the final roaster knows the origin, it can be

marketed as a traceable coffee. Traceability is useful when building regional or farm

reputations in the market, and recognizing consistent quality from specific sources that can

then be reflected in the market price. It’s also very useful in tracking down the precise source,

or ground zero, of defects and diseases. The consumer market is increasingly demanding

traceability, and many coffee-producing countries are incorporating traceability into their

national coffee programs and regulations. The comparison to fine wines and scotches becomes

yet again, apparent.

The short-coming of traceable coffees is that they are not synonymous with quality coffee.

While it may be worth a few dollars in retail value to be able to identify the origin of a coffee, if

the quality is not consistent with the marketing value of that origin, then the customer will

move on. The risk is a result of branded products that make it possible for a customer to

associate a bad quality coffee to an origin, and specifically avoid anything with that

brand/origin in the future.

c. Direct Trade

Independent Roasters however, don’t simply opt for traceable sourcing because it may still

require several intermediaries, resulting in some of the communication and cost challenges I

mentioned before. Instead, ambitious roasters reach out directly to farmers in coffee-

producing countries. This often involves research trips to origin countries where the roaster

visits farms and interviews farmers in search of sourcing partners. This arrangement is often

credited for having a true hands-on approach to sourcing, giving the roaster the most control

over the product with minimal interference. The communication channel that is established

between the grower and roaster is very useful in collaboratively improving quality of product,

and quality of business. The two are able to communicate defects or customer feedback in

order to continue to improve quality over time. When a deal is made, a third-party freight

entity is usually used for the physical movement of goods and customs clearance.

..:: 19 ::..

The struggle for roasters is that they rarely have the time and resources to do such origin trips.

Small businesses are very time-demanding, and a small roaster will likely have to cease

operations while he/she is on a trip. Secondly, while origin trips are not expensive by vacation-

standards, they are not like a weekend at the lake either. Flights can cost upwards of $600-

1000 round-trip, plus all of the missed revenue and income while he or she is away. And lastly,

a roaster also lacks the professional network to plan an ad hoc origin trip. A roaster would

need to spend more time and money making the connections necessary to fill an itinerary and

make the trip worthwhile. And, not to mention, that’s all assuming that a roaster even knows

what to look for!

Figure 9: Three-way Direct Trade Relationships

d. Vertical Integrations

The next level of direct sourcing is to own both ends of the chain. We’ve seen several

examples of large roasters buying farms, like Starbucks in China and Costa Rica, and

occasionally farmers opening their own roasters. The latter case however, is much more

difficult because of the reverse flow of purchasing power between currencies. A large roaster

from the US has the advantage of the currency exchange rate when expanding into producing

countries. It does happen, however. El Recreo in Boston and La Fortuna in Chicago, are both

farmers that own and operate a café, roastery and distribution center in the US. In both cases,

the farmers were successful family-run farms that sought to move to and open a café in the

..:: 20 ::..

states. With the help of third-party investors, they were able to open shops, begin roasting,

and have been very successful in offering direct farmer-to-customer interactions and

education programs.

One of the drawbacks of either of these integrations is that it does not immediately rectify the

geographic knowledge gap. The lack of familiarity a farmer has with the consumer psychology

is inherent, as is that of a roaster going into the farming business. Farmer-led education

programs will offer authentic insight, but farmer-led marketing and niche market-building are

bound to experience a steeper learning curve.

..:: 21 ::..

CHAPTER VI. THE PROPOSED PARTNERSHIP MODEL

Given the market conditions, the problems faced by small businesses on both ends, and the

inability for current models to address them, there are two effects any solution must have in

order to be effective. The solution must be both stabilizing, and enabling.

Stabilizing Enabling

A solution must offer stability for

both roaster and farmer in their

capacity to forecast pricing, locate

sources and markets, and maintain

positive yet simple control over their

business relationships.

A solution must enable small

businesses to survive in an

industry dominated by big players

by creatively managing equity and

creating a niche market.

With these effects in mind, my proposed model uses two equity-earning mechanisms in

conjunction with a direct trade relationship. The first mechanism addresses the initial start-up

of a new roaster. The second describes a model for continued partnership through the on-

going supply of raw materials (e.g. green coffee). The direct trade format is utilized in order to

minimize the presence, and profit-share, of intermediary entities while maximizing the

influence and control of the business owners.

Figure 10: Direct Trade Partners

..:: 22 ::..

a. The Bulk Investment Mechanism

Opening a roaster, as I’ve shown, is a costly endeavor – perhaps even riskier as a small

business entrepreneur. In simplest term, this first mechanism is intended to pool the

resources of both parties to alleviate the financial burden of opening a roaster, while offering

the farmer a valuable intangible benefit in return, stability. The farmer will provide the raw

materials (e.g. green coffee) to the roaster in exchange for equity in the business. The material

provision will decrease the initial cash outlay for the roaster, as well as decrease the negative

cash flow for the goods sold in the first several operational cycles.

Figure 11: Bulk Investment Diagram

Based on the numbers earlier, we estimated that a new wholesale roaster will cost around

$50,000 to open, and the roaster will make about a $5 margin on each pound of coffee sold.

Also continuing with the estimate of a roaster selling 500 lbs/month, or about 588 lbs in green

beans (before roasting losses), the farmer can provide the first year’s-worth of coffee. This

would be about 7,000+ lbs of green coffee, worth roughly $30,000 in equity. If equity were

dispersed dollar-for-dollar, $30,000 would be 42% when compared to the roasters initial

investment of the remaining $41,000, including the anticipated cost of raw materials for one

year.

..:: 23 ::..

Figure 12: Breakeven Curve for a Roaster Employing the Bulk Investment Mechanism

As you can see by this graph, the roasting business will begin operating in the black within the

first 3 quarters of operation, indicating that the farmer’s infusion of investment-in-kind

significantly reduces the financial burden and risk of starting up.

b. Continuous Equity Dispersal Mechanism

The obvious flaw in this mechanism is that a farmer cannot possibly forgo $30,000 in revenue

for the year without going-under him/herself. Instead, it makes sense to pair the bulk

investment mechanism with a long-term one. For example, let’s say the initial investment was

set to a maximum of $10,000, or roughly a 4 months’ supply of coffee. After this initial supply

of raw materials is used up, a standardized equity-payment plan will take over.

The premise of this mechanism is based on that little country-by-country variance built into

coffee market pricing, the price differential. The flexibility of this pricing scheme is repurposed

as an opportunity to create stability for the farmer, and also enable the roaster. In terms of

cash-flow, this mechanism will help the roaster by allowing him/her to pay for a portion of the

raw materials in shares instead of cash. This is similar to the first mechanism, except that it

only applies to the portion of the total coffee price that covers a “premium”, leaving the

commodity price intact for the farmer to receive in cash. This mechanism also ensures that the

premium will be paid in a value equivalent to or better than what a certification such as Fair

-$60,000

-$40,000

-$20,000

$0

$20,000

$40,000

$60,000

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct

New Breakeven Point

..:: 24 ::..

Trade would offer. In simple terms, it guarantees that the farmer pockets a minimum amount

of cash, while paying out equity as rewards for high quality.

Figure 13: Diagram of Payments for Continuous Equity Dispersal Mechanism

In keeping with the roaster projections we’ve been analyzing, a combined arrangement of both

mechanisms will look like the graph below. A maximum investment is made in-kind by the

farmer with $10,000-worth of green coffee, and then sells coffee after month 4 in accordance

with the cash-equity payment plan. The roaster will breakeven after 4 quarters, much less than

the 1.5 years he/she would otherwise need on their own.

Figure 14: Breakeven Curve for a Roaster Employing Both Mechanisms

-$60,000

-$40,000

-$20,000

$0

$20,000

$40,000

$60,000

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct

New Breakeven Point

..:: 25 ::..

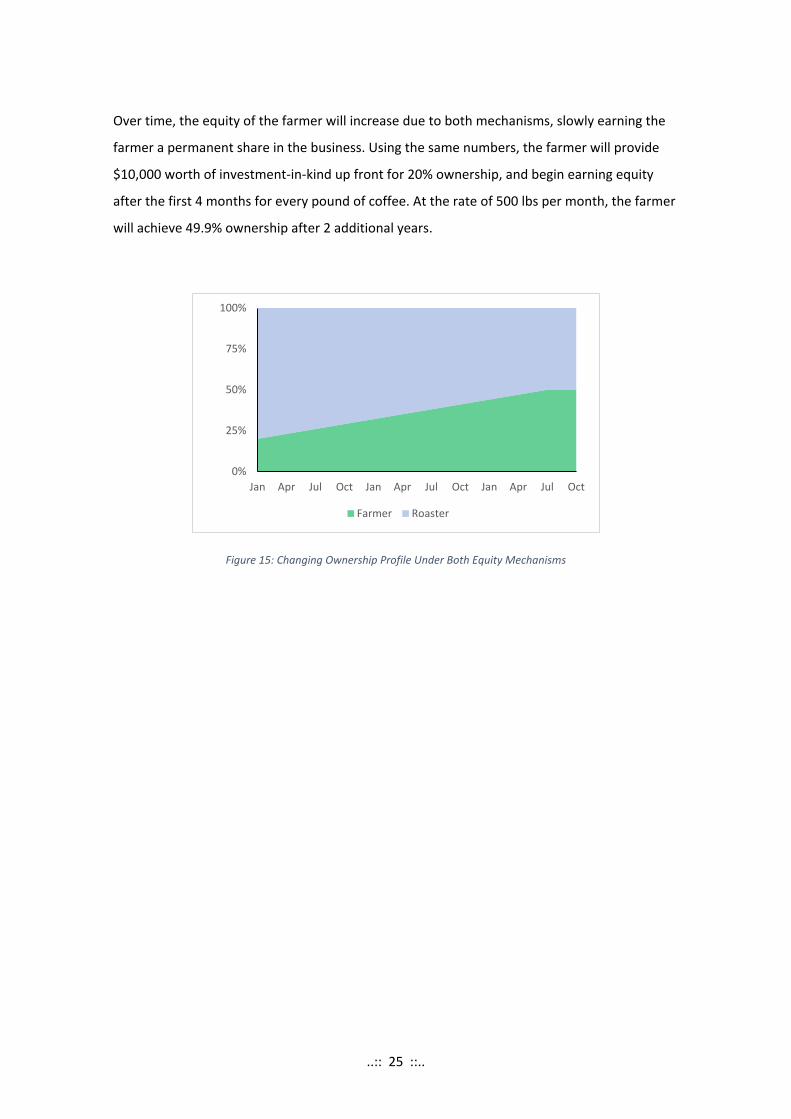

Over time, the equity of the farmer will increase due to both mechanisms, slowly earning the

farmer a permanent share in the business. Using the same numbers, the farmer will provide

$10,000 worth of investment-in-kind up front for 20% ownership, and begin earning equity

after the first 4 months for every pound of coffee. At the rate of 500 lbs per month, the farmer

will achieve 49.9% ownership after 2 additional years.

Figure 15: Changing Ownership Profile Under Both Equity Mechanisms

0%

25%

50%

75%

100%

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct

Farmer Roaster

..:: 26 ::..

CHAPTER VII. FINDINGS AND RESULTS

a. Data Parameters

In order to determine if this model will meet my desired effects of stability and enabling, we

must first establish a baseline average for the coffee industry. There are a number of problems

that I wish to address, but I believe the single best indicator will be to improve farmer profits,

with a neutral or similarly positive effect on the roaster’s. Because this model is based on the

premise of disintermediation, i.e. direct trade, much of this profit increase will be withdrawn

from the supply chain itself, because the final price of the (specialty) coffee will not change.

In order to realistically analyze data coming from a diverse market like coffee, where many,

many variables are present, I set the following parameters to control the variables:

Controlled Variable #1: Average retail price of specialty coffee is $21.94 / lb

(Transparent Trade Coffee Organization)

Controlled Variable #2: Coffee is rated as “specialty”, with a cup (Q) score above 85

Controlled Variable #3: Coffee is destined for the US market

I briefly mentioned earlier what the revenue share looked like in the industry according to PBS.

In order to corroborate these numbers, I investigated several other independent channels of

trade. While not identical, one can distill averages from the results. I chose 4 additional

channels with which to compare the PBS numbers. These channels represent different origins,

logistics channels, and organizational levels, and are all real-world cases, though the names

have been changed for privacy purposes.

1. PBS, public broadcasting in the United States, using data from Guatemala

2. Economics Intelligence Unit, The Economist magazine in the United

Kingdom

..:: 27 ::..

3. Tsongo Café, coffee exporter in the Democratic Republic of Congo

4. Tierra Real, coffee exporter in Colombia

5. Hacienda Optima, prospective direct trade farmer in Nicaragua

In order to standardize costs across the different sources and channels, I categorized all supply

chain costs under the 6 supply chain actors we’ve mentioned before.

Controlled Variable #4: There are 6 levels of the supply chain

Figure 16: Typical Supply Chain Actors + Retail

There are a number of fees and costs at each level, so to be consistent, I’ve grouped them to

each of the 6 levels using the following criteria.

FARM EXPORT FREIGHT IMPORT ROAST RETAIL Production Milling Land Transport

Exporter Fees Preparation Port Fees Traders

Transport Insurance

Importer Fees Duties Port Fees

Roaster 15% Loss Wholesale

Beverage Prep. Sales Tax

Table 5: Supply Chain Costs Grouped by Category

b. Cost Escalation

When compiling these supply chain breakdowns, it is important to differentiate two metrics of

comparison: cost escalation, and revenue share. Cost escalation is the increasing price paid

between the levels of the supply chain, leading to the higher, end-user price. Revenue share is

..:: 28 ::..

the portion of the end-user price that is received by each level of the chain. Both of these

numbers, in addition to operating costs, are necessary to reach our final metric, Profit Share.

SELLING PRICE PBS EIU Tsongo Tierra Optima

Farm $2.63 $2.90 $1.18 $2.67 $2.71

Export $3.29 $4.86 $1.53 $3.77 $3.05

Freight $4.17 $5.45 $1.65 $3.89 $3.16

Import $4.83 $6.65 $2.65 $5.06 $4.16

Roast $19.09 $18.67 $15.56 $18.69 $17.52

Retail $21.94 $21.94 $21.94 $21.94 $21.94

Table 6: Selling Prices at Each Level of the Supply Chain

REVENUE SHARE PBS EIU Tsongo Tierra Optima

Farm 12% 13% 5% 12% 12%

Export 3% 9% 2% 5% 2%

Freight 4% 3% 1% 1% 1%

Import 3% 5% 5% 5% 5%

Roast 65% 55% 59% 62% 61%

Retail 13% 15% 29% 15% 20%

Table 7: Revenue Share at Each Level of the Supply Chain

c. Profit

While the numbers above for revenue are fairly reliable because they are public information,

calculating profit and profit share is based on closely-held accounting. The operational costs of

a business are key to its success, and reveal their profit margin, so most businesses are not

quick to share them. I was able to obtain these cost estimates on the condition anonymity.

Because of this unreliability, the next variable I had to control was with regard to the

operational costs of each level, in particular the coffee roaster. Since most coffees are

imported green and roasted in the states, I felt it was appropriate to use the same import and

..:: 29 ::..

roasting costs for all sourcing channels. Note: These are the same numbers that were used in

the cost estimates above for the roaster.

Controlled Variable #5: All channels experience similar roasting and importing costs

Standardized Costs $/lb

Sea Freight $0.10

Air Freight $1.13

Importer $0.30

Roaster $9.32

Table 8: Standardized Cost Assumptions for Supply Chain Actors

PROFIT PBS EIU Tsongo Tierra Optima

Farm $1.53 $1.80 $0.88 $1.57 $1.36

Export $0.41 $1.71 $0.10 $0.85 $0.09

Freight $0.83 $0.54 $0.07 $0.07 $0.06

Import $0.36 $0.90 $0.70 $0.87 $0.70

Roast $4.94 $2.70 $3.59 $4.31 $4.04

Retail $1.85 $1.35 $5.38 $2.25 $3.42

Table 9: Gross Profit for Each Level of the Supply Chain

PROFIT SHARE PBS EIU Tsongo Tierra Optima

Farm 15% 20% 8% 16% 14%

Export 4% 19% 1% 9% 1%

Freight 8% 6% 1% 1% 1%

Import 4% 10% 7% 9% 7%

Roast 50% 30% 33% 43% 42%

Retail 19% 15% 50% 23% 35%

Table 10: Profit Share for Each Level of the Supply Chain

..:: 30 ::..

As you can see, the bulk of the profit is retained by the roaster, followed by the retailer and

farmer. This makes sense given that the costs of operating and living in the consuming

countries is a lot higher than in the producing countries. To account for this disparity, I’ve

adjusted the profits using the Purchasing Power Parity conversion factor at the World Bank to

more accurately reflect the value of these incomes in the countries in which they are received.

PROFIT (PPP) PBS EIU Tsongo Tierra Optima

Farm $3.07 $3.60 $1.47 $3.93 $3.40

Export $0.82 $3.42 $0.17 $2.13 $0.23

Freight $0.83 $0.54 $0.07 $0.07 $0.06

Import $0.36 $0.90 $0.70 $0.87 $0.70

Roast $4.94 $2.70 $3.59 $4.31 $4.04

Retail $1.85 $1.35 $5.38 $2.25 $3.42

Table 11: Gross PPP Profit for Each Level of the Supply Chain

PPP SHARE PBS EIU Tsongo Tierra Optima

Farm 26% 29% 13% 29% 29%

Export 7% 27% 2% 16% 2%

Freight 7% 4% 1% 1% 1%

Import 3% 7% 6% 6% 6%

Roast 42% 22% 32% 32% 34%

Retail 16% 11% 47% 17% 29%

Table 12: PPP Profit Share for Each Level of the Supply Chain

When accounting for purchasing power, the farmer comes off much better than before, even

competing with the roaster at times. It also illustrates the differences between these supply

channels. The farmer receives the least in Congo, likely a reflection of the market price, and

the country’s coffee supply chain’s reputation on the world stage.

We also see a stark difference in the EIU numbers when it comes to the Exporter’s profit share.

This is likely because this channel includes a dedicated coffee trader, whose role fell under

..:: 31 ::..

Exporter in our data arrangement, and he/she has created an arbitrage market for him/herself

to thrive on. This role will not exist in shorter supply chains, and especially not in direct trade.

d. Direct Trade

So the question remains, what impact does direct trade have on profit? Using the standardized

numbers above, we can estimate the cost escalation and profit share of a direct trade model,

but we’ll need to establish more parameters.

Controlled Variable #6: Coffee farmers have the capacity to export their coffee

Controlled Variable #7: Coffee roasters import their own coffee, or hire a courier

By assuring that the farmer can export his/her own coffee, we can remove that individual from

the chain. This is not an unusual capacity for a professional farmer to have, particularly in

moderately proficient coffee producing countries. Large exporters like Brazil, Ethiopia and

Colombia have more restrictions though, because the market has been become its own

bureaucracy. On the other hand, low volume countries like Congo and Indonesia have less

restrictions, but farmers are simply too far removed from the market to be involved in

exporting. The better candidates are in countries like Honduras and Guatemala where the

process for becoming a legal exporter costs a less-than-outrageous sum of money and an

acceptable amount of time to fill out the paperwork. Furthermore, with a direct trade

relationship, there is no need for trading or buyer-finding, so there’s no need for a trader.

On the roaster side, in most cases, direct trade quantities are small and do not require specific

customs brokering. This is particularly relevant when using express couriers like UPS, DHL or

FedEx because they are able to clear customs on behalf of the recipient. For this reason, we

have calculated the cost of direct trade for both air and sea freight.

..:: 32 ::..

SELLING PRICE Direct (Air) Direct (Ship)

Farm $3.90 $3.90

Export $3.90 $3.90

Freight $5.03 $4.02

Import $5.03 $4.02

Roast $18.88 $17.99

Retail $21.94 $21.94

Table 13: Selling Prices for Each Level of the Supply Chain under Direct Trade

REVENUE SHARE Direct (Air) Direct (Ship)

Farm 18% 18%

Export 0% 0%

Freight 5% 1%

Import 0% 0%

Roast 63% 64%

Retail 14% 18%

Table 14: Revenue Share for Each Level of the Supply Chain under Direct Trade

And finally, we have to establish some specific locations and prices in order to estimate the

profit share. For the sake of argument, we will use the same Hacienda Optima farm as our

source, which will allow us to compare it side-by-side with the 5th channel from above.

Controlled Variable #8: The direct trade farmer is located in Nicaragua

Controlled Variable #9: Direct trade will pay $1 more / lb than the next best channel

Our objective in pricing is going to parallel that of Fair Trade arrangements, and in this case,

we’re going to guarantee at least $1 higher per lb than the next best channel, which in our

data set is in the EIU numbers. So for this example, we will use a farm price of $3.90 / lb.

..:: 33 ::..

PROFIT (PPP) Direct (Air) Direct (Ship)

Farm $7.00 $7.00

Export $0.00 $0.00

Freight $0.13 $0.07

Import $0.00 $0.00

Roast $4.03 $4.15

Retail $2.06 $2.95

Table 15: Gross PPP Profit for Each Level of the Supply Chain under Direct Trade

PPP SHARE Direct (Air) Direct (Ship)

Farm 53% 49%

Export 0% 0%

Freight 1% <1%

Import 0% 0%

Roast 30% 29%

Retail 16% 21%

Table 16: PPP Profit Share for Each Level of the Supply Chain under Direct Trade

PROFIT (PPP) 5-Channel Average Direct Trade (Air)

Farm $3.09 $7.00

Roaster $3.92 $4.03

Table 17: Comparing the 5 Channel Average for Gross PPP Profit to Direct Trade

PPP Profit has doubled for the farmer via either air or sea freight, with no appreciable change

to the roaster’s gross profits. It’s interesting to note that the increased freight charges of air

shipments don’t actually affect the profit margins much for either entity. This makes sense

given the immense volumes handled by express couriers, and therefore the efficiency with

which they’re able to move goods. In a sense, despite direct trade being considered

disintermediation, it does in fact only consolidate the roles in the middle of the chain, allowing

the one-stop-shop couriers to handle all of the similar logistics tasks at once.

..:: 34 ::..

CHAPTER VIII. DISCUSSION

a. Barriers

There are many reasons why direct trade hasn’t replaced the commodity market already,

many of which are simply the result of a geographically spread-out industry. Fortunately for

the future however, the internet has already helped close some of these divides, and it can be

leveraged to help small businesses cross distances they never could have dreamt of before.

Restricted Professional Networks

The world of coffee, and logistics for that matter, is an “old world” industry of paper reports

and phone calls. It’s a mesh network of experienced professionals who make things happen,

and products move, based on who and what they know. These networks are not documented,

traceable, or easy to learn. Expanding one’s professional network in such a spread out industry

isn’t easy, and would require ample amounts of time and financial resources. With limits like

these on the personal interconnectedness of the industry professionals, the speed of change is

slackened.

Communication Challenges

It is inherent in a complex system to struggle with communication. The logistics system of the

world is an ad hoc arrangement of independent intermediaries that speak thousands of

languages, currencies and cultures, all of which do not always coordinate or co-develop. There

are international standards, to be sure, but the system will always be restricted by the lowest

common denominator. The best example of this is the continued reliance on paper bills of

laden (BOL), the proof of ownership document necessary for international logistics. There have

been several tech start-ups that have tried to revolutionize this system with an electronic BOL,

but it just hasn’t stuck. (Demetriou, N.) Like any platform, or technological innovation, it only

works if everyone uses it, and that’s hard with several countries around the world experiencing

different levels of technological access.

..:: 35 ::..

Limited Access to Knowledge

Knowledge of the supply chain is tribal, passed from person to person by necessity and lore.

There’s no “Coffee Logistics for Dummies” book that can teach someone everything about the

system, and even if there was, it would be outdated immediately because the system is so

complex, minute changes will happen fast and often.

It’s also difficult to gather hard numbers from anyone in the supply chain because there is a

protective culture of information, each person fearful of losing their competitive advantage.

Most crucially, there is a widespread dearth of familiarity with other parts of the supply chain.

While there may be some camaraderie between supply chain actors for participating in the

same global industry, they are not familiar with the requirements and objectives of each

other’s roles in it. The gap is largest between the top and the bottom, where consumers and

farmers are on different planets when it comes to trans-world understanding.

Inertia of Traditions

For many, the system is working just fine the way it is, and there is no reason to change it.

Tradition has served them well, whether they are a farmer or a roaster, they’ve always sold in

the market and are comfortable where they’re at. For many as well, the income they’re

making is just enough to feed their families, so any risk is unwelcome.

Fear of the Unknown

General fear of the unknown makes any industry development or change unnerving. New

business ventures, such as an international partnership, means new people and new risks.

Without more education or exposure, currently prevented by the previously-mentioned

barriers, fear will always slow the pace of worldwide progress.

..:: 36 ::..

b. Advantages of the International Partnership

The advantages of an international direct trade partnership, especially one with collaborative

investments like the proposed model, are numerous and varied.

Farmer Roaster

Stab

ilizi

ng - Predictable sales location

- Predictable sales price - Predictable sales quantity - Less price volatility - Evened out cash flow thru

season - Time saved “following the

market” - Increased profit share - Won’t need to pursue

certifications

- Ease of sourcing raw materials - Semi-controllable quality - Direct information channel - Shared investment costs - Lowered COGS

Enab

ling - Expand business operations

- Build equity - Direct customer feedback - Potential for future profit

earnings - Potential to sell other farm

products - Can invest without cash

- (Best) Farm to Cup Story - Potential for site visits by farmer - Potential for field trips to origin - Potential for other farm products

Table 18: Advantages of the International Partnership

Stabilizing

Some benefits are simply good for predictability and peace of mind, a.k.a. stability. This

includes knowing in advance how much coffee the farmer is going to sell, for how much, and

to whom. Essentially, it liberates the farm from the effort normally required to follow the

market and sell his/her coffee for the best price, to the point where the farmer doesn’t even

need to follow the commodity market. Time-saving is a big deal for smallholder farmers, so

they’re eager to reclaim time that can be used to accomplish other tasks. On a similar note, the

farmer may not have the same incentives to pay for the time and expenses of certifications,

adding more to his savings.

..:: 37 ::..

It also means the bookkeeping is more predictable, so capital investments in farm equipment

can be planned out more easily. This also applies to the roaster, who can keep his/her own

accounts steady with accurate revenue and cost forecasts. The roaster enjoys a lower cost of

goods sold (COGS) under both investment mechanisms as well, substantially reducing the risk

of failure during the critical first couple years of operation.

Furthermore, the roaster is reassured of the quality coming in because he/she knows that

there is a communication channel open with which to have some control over the raw

materials he’s using.

Enabling

The partnership is also a boon to business, enabling the farm by building direct equity in

another business, and offering him new incentives and tools to improve his existing

operations. Communication is the key to the later, and a direct relationship is simply the best

way to communicate up and down the chain. As the farmer’s quality improves with the

collaboration of the partnership, so will the value of both of his businesses.

The farmer can also earn through more income streams. For example, once the direct supply

channel is established, the farmer can also offer related products like Cascara, or cultural

merchandise. And better yet, with equity shares in the roaster, the farmer will be entitled to a

growing business’ increasing worth, and depending on the agreement, perhaps a direct share

of the profits. What’s more, this model enables a farmer to expand his business without having

to invest cash, but instead welcomes an investment-in-kind that is more readily accessible to

him/her.

For the roaster, it’s all about the marketing. The third wave coffee movement is here to stay,

and a thoroughly Farm-to-Cup enterprise is bound to succeed. The roaster will not only be able

to claim the most direct connection with a farmer, but also offer a suite of other products and

..:: 38 ::..

services tied to it, such as origin trips, cultural merchandise, and seminar visits from the

farmers themselves.

c. Disadvantages of the International Partnership

There are certainly disadvantages to this partnership model as well, and it wouldn’t work or be

the best fit for everyone. The scalability is limited by these restrictions, as well as the greater

ethos of the “glocal” movement, which is basically antithetical to the concept of scalability.

Farmer Roaster

Disa

dvan

tage

s - Added risk of roaster viability - Miss out on high price markets - Opportunity Cost of Investment

- Reliance on a single source - Shared ownership control

Table 19: Disadvantages of the International Partnership

Both parties are accepting a new risk that they were not previously familiar with, and that’s

the human risk of a business partner. In both directions, each person runs the risk of the other

being incapable of managing a profitable business, or worse, that the person is a scammer.

This issue of trust is best addressed by building a background together through conversations,

visits, and whenever possible, through mutual acquaintances that can serve as character

witnesses.

The farmer also runs the risk of missing out on higher market prices that could be available

elsewhere had he/she sold their coffee directly to market. This can be addressed by giving the

farmer the option to sell a portion or all of his crop to market if it will serve him better, but

ultimately I believe it will be better for him to accept the already negotiated high price because

of the predictability it offers him in the long run. For example, it is highly unlikely the market

price for coffee will rise anywhere near $3.90 / lb, which is what our direct trade model

offered the partner farmer earlier in our analysis.

..:: 39 ::..

For the roaster, the main concern is sourcing from a single farm. Should the farm experience

any harvest mishaps and not be able to deliver, the roaster will have to source from

somewhere else, leaving him right where he was when he started. While market-sourcing still

works as a distant back-up option, additional mechanisms can be arranged in advance that

keep with the social mission as well. One idea would be to build a community of local roasters,

each with their own direct trade relationships spread out around the world. If something were

to happen to a source farm, other roasters in the community would be able to provide green

coffee from their own direct trade farms to help cover the loss. This would ensure the

continuity of the direct trade mission, and build collaboration communities at home.

Additionally, both parties will undoubtedly struggle with the idea of sharing control. This is a

common problem in all partnerships, personal and professional, and it will have to be

discussed during contracting – topics such as naming rights, dividends, profit reinvestment,

and marketing strategies to name a few.

d. Thoughts on Implementation

Discussions on contracting bring up a lot of concerns about how to actually implement an

international partnership. There are nearly unlimited ways to structure the business

relationship, but there are some key attributes that would be ideal to find in the target

candidates for such a collaboration.

Identifying the Right Candidate

Farmer Roaster

..:: 40 ::..

Idea

l Tra

its - Access to coffee processing

(preferably in-house) - Able to export - Small to Medium-sized farm - Able to invest ~ $10,000 of

coffee - Professional, entrepreneurial

attitude - Wants more stability over prices - Wants to expand operations - Willing to hear customer

feedback

- Looking for investment partner - Able to import coffee - Interested in direct trade - Wants to sell a story - Wants better access to coffee

origins - Sells 500+ lbs per month - Experienced roaster - Interested in coffee education

Table 20: Identifying the Ideal Traits

There are a lot of desirable qualities, but in both cases the ideal candidates will be professional

and entrepreneurial-minded individuals. There will need to be a desire and a willingness to

deal in direct trade, coffee education programs, and more importantly, a mutually-constructive

collaboration relationship with someone on the other side of the world.

A farmer should be small to medium-size, and have the ability to process and export their

coffee. A roaster should have the ability to import coffee themselves, or through a contracted

courier, and sell at least 500 lbs of roasted coffee per month.

Furthermore, there is a lot of room for flexibility in the terms of the contract regarding

quantities, prices, timing and equity dispersal methods. A farmer may settle on virtually any

percentage as an equity goal, but I imagine that most roasters will not be willing to give up

more than 49%. There is also room to split up that 49% among multiple farms, in the event

that an international partnership is formed between a roaster and a farming co-op or guild.

The specific conditions and terms of a contract are best left to a legal expert, and would be an

interesting follow-on topic for this thesis.

..:: 41 ::..

CHAPTER IX. CONCLUSIONS

Collaboration is the ultimate tool for small businesses because it serves as a force-multiplier

that lets limited-resource entities compete with big players. In the case of coffee, we are

talking about smallholder farms, local roasters, and independent cafes. It’s a small, but

turbulent niche market though. There are competing demands to produce commercial volume,

high quality products, and at the same time, maintain the intimacy of local sourcing. This is the

proving ground for small businesses – a time to capitalize on a market that craves them. They

only need the tools to enter the game. Collaboration is that tool, and partnerships are the

most direct manifestation of it. In the long-run, smallholder farmers can benefit tremendously

from setting up an international partnership, and in-turn, help a small roaster survive a start-

up period that’s known to be rife with difficulties. Collaborative partnerships offer a

harmonious balance of stability and enabling to keep the company both steady and forward-

moving.

There are clear communication benefits as well, all of which help advance the industry as a

whole, rather than only furthering the needs of individual businesses. By bridging the global

communication gap in the coffee supply chain, small coffee businesses will be able to connect

consumers directly with their products’ origin, a concept under-realized by the status quo of

traceability and certifications. With a direct channel from farmer to roaster, i.e. Farm-to-Cup,

consumers will consume not only coffee, but specific knowledge and personal familiarity with

coffee farming. And this is good news for all specialty coffee businesses, because better

consumer education leads to more-informed purchases, and more purchases means more

business in the café. As they say, “a rising tide lifts all ships”.

..:: 42 ::..

CHAPTER X. BIBLIOGRAPHY

Cafe De Colombia. "The Coffee People." Cafe De Colombia, n.d. Web. 16 Sept. 2016.

<http://www.cafedecolombia.com/particulares/en/la_tierra_del_cafe/la_gente_del_cafe/>.

Carroll, Tom, Andrew Stern, and Dan Zook. "Catalyzing Smallholder Agricultural Finance." Catalyzing

Smallholder Agricultural Finance Acknowledgements and Authorship (2012): n. pag. Dalberg. Sept. 2012.

Web. 16 Sept. 2016. <http://dalberg.com/documents/Catalyzing_Smallholder_Ag_Finance.pdf>.

Charles, Dan. "Coffee For A Cause: What Do Those Feel-Good Labels Deliver?" NPR. NPR, 24 Apr. 2014.

Web. 16 Sept. 2016.

Council on Smallholder Agricultural Finance. "2014 Year In Review." (2015): n. pag. The Council on

Smallholder Agricultural Finance (CSAF), 16 July 2015. Web. 16 Sept. 2016. <http://www.csaf.net/wp-

content/uploads/2015/07/2014-Year-In-Review-web.pdf>.

Demetriou, Nicholas. "Electronic Bills of Lading: Why It’s Different This Time." The Baltic Briefing.

EssDOCS, 4 Mar. 2015. Web. 16 Sept. 2016. <http://thebalticbriefing.com/2015/03/04/electronic-bills-

of-lading-why-its-different-this-time/>.

Field, Anne. "A Supply Chain Overhaul To Boost Coffee Farmers' Income 400%." Forbes. Forbes

Magazine, 16 July 2014. Web. 16 Sept. 2016. <http://www.forbes.com/sites/annefield/2014/07/16/a-

supply-chain-overhaul-to-boost-coffee-farmers-income-400/#2eccd76947b3>.

Galindo, Mauricio. "Climate Change and Coffee." Masters of Coffee Science and Economics - Ernesto Illy.

Trieste, Italy. Lecture.

Gualdi, Silvio. "Coffee Cultivation and Climate Changes." Masters of Coffee Science and Economics -

Ernesto Illy. Trieste, Italy. Lecture.

Graham, Stockton. "What Determines the Price of Green Coffee? -." Stockton Graham Co. N.p., 12 Aug.

2014. Web. 16 Sept. 2016.

Janssen, Rivers. "The Certificate Conundrum." Roast Magazine (2011): n. pag. Roast Magazine. Web. 16

Sept. 2016.

Lyall, Sarah. "Trying to Pin Down the Mosaic of Millennial Tastes." The New York Times. The New York

Times, 15 May 2016. Web. 15 June 2016.

National Coffee. "What Are We Drinking? Understanding Coffee Consumption Trends." The First Pull.

National Coffee Association USA, 19 Mar. 2016. Web. 15 June 2016.

..:: 43 ::..

Peressotti, Alessandro. "Coffee Cultivation and Climatic Changes." Masters of Coffee Science and

Economics - Ernesto Illy. Trieste, Italy. Lecture.

SBA Office of Advocacy. "Small Business Economics." (n.d.): n. pag. Small Business Administration (SBA),

June 2012. Web. 16 Sept. 2016. <https://www.sba.gov/sites/default/files/Business-Survival.pdf>.

Specialty Coffee Retail Price Index. "Specialty Coffee Retail Price Index – 2015, Q2." Transparent Trade

Coffee Organization (TTCO), 15 July 2015. Web. 16 Sept. 2016.

<http://transparenttradecoffee.org/insights/specialty-coffee-retail-price-index-2015-q2>.

United Nations. Food and Agricultural Organization (FAO). Framework for Analysing Impacts of

Globalization on Smallholders. By John Dixon, Aysen Tanyeri-Abur, and Horst Wattenbach. Rome:

Agricultural Management, Marketing and Finance Service (AGSF), 2004. Smallholders,globalization and

Policy Analysis. Agricultural Management, Marketing and Finance Service (AGSF), 2004. Web. 16 Sept.

2016.

Whalen, Kelly. "Your Coffee Dollar." PBS. PBS, May 2003. Web. 16 Sept. 2016.

The End

![Blandino GIovanni MD CV January 2013 31[1] · p53 axis promotes aggressiveness in breast cancer", Università degli Studi di Trieste, Trieste, Italy 2010 (Opponent). Organization](https://static.fdocuments.in/doc/165x107/5b2dd5797f8b9a594c8cef3e/blandino-giovanni-md-cv-january-2013-311-p53-axis-promotes-aggressiveness.jpg)