United Arab Emirates Major Business Sectors - Iberglobal · United Arab Emirates Major Business...

13

Switzerland Global Enterprise – Major Business Sectors 1/13 United Arab Emirates Major Business Sectors Compiled by: Swiss Business Hub GCC Dubai, April 2014 OVERVIEW AND TRENDS The UAE is the most important trading hub in the GCC & the Middle East, and has a tremendously fast growing economy. In 2013, real GPD grew by 4.1% (forecast); and the country is one of the wealthiest in the region with a GDP per capita (nominal) of US $ 55,352 (2013 est.) mainly due to the country’s vast oil and gas reserves. Although the UAE remains highly dependent on oil wealth, which represents approximately 75% of total government revenues, the Government has embarked on a major economic diversification program from oil to services and manufacturing and it is already today the most diversified economy in the Middle East. On the whole, the UAE is regarded as having a transparent and favorable business climate. According to the report “Doing Business 2014”, published by the World Bank, the UAE is regarded as the best place to do business in the Middle East (23 rd worldwide) before Saudi Arabia (26 th ). In the 2013 Index of Economic Freedom by the Heritage Foundation and the Wall Street Journal the UAE economic environment is regarded as “mostly free” and ranks 3 rd in the MENA region (28 th freest in the world). OIL & GAS Despite the fact that UAE’s economy is more diversified than before, the hydrocarbon sector still represents a core pillar of the economy accounting for around 25% of the total GDP. Indeed, higher oil supply and prices have been boosting public revenues which reached a record of USD 100 billion in 2012, i.e. 10% of the OPEC total income according to the Energy Information Administration (EIA) of the US Department of Energy. The UAE has the 7th-largest proven oil and natural gas reserves in the world 1 standing at 97.8 billion barrels, i.e. around 6.6 % of the world’s total proven reserves of 1.48 trillion barrels. In this respect, Abu Dhabi remains the powerhouse of the country since 90% of the UAE oil reserves are located in this emirate. The UAE is also the 8th-largest oil producer in the world with around 1 2013 OPEC Annual Statistical Bulletin

-

Upload

truongliem -

Category

Documents

-

view

232 -

download

4

Transcript of United Arab Emirates Major Business Sectors - Iberglobal · United Arab Emirates Major Business...

Switzerland Global Enterprise – Major Business Sectors

1/13

United Arab Emirates Major Business Sectors

Compiled by:

Swiss Business Hub GCC Dubai, April 2014

OVERVIEW AND TRENDS

The UAE is the most important trading hub in the GCC & the Middle East, and has a tremendously

fast growing economy. In 2013, real GPD grew by 4.1% (forecast); and the country is one of the

wealthiest in the region with a GDP per capita (nominal) of US $ 55,352 (2013 est.) mainly due to the

country’s vast oil and gas reserves. Although the UAE remains highly dependent on oil wealth, which

represents approximately 75% of total government revenues, the Government has embarked on a

major economic diversification program from oil to services and manufacturing and it is already

today the most diversified economy in the Middle East.

On the whole, the UAE is regarded as having a transparent and favorable business climate. According

to the report “Doing Business 2014”, published by the World Bank, the UAE is regarded as the best

place to do business in the Middle East (23rd

worldwide) before Saudi Arabia (26th).

In the 2013 Index of Economic Freedom by the Heritage Foundation and the Wall Street Journal the

UAE economic environment is regarded as “mostly free” and ranks 3rd

in the MENA region (28th freest

in the world).

OIL & GAS

Despite the fact that UAE’s economy is more diversified than before, the hydrocarbon sector still

represents a core pillar of the economy accounting for around 25% of the total GDP. Indeed, higher

oil supply and prices have been boosting public revenues which reached a record of USD 100 billion

in 2012, i.e. 10% of the OPEC total income according to the Energy Information Administration (EIA)

of the US Department of Energy.

The UAE has the 7th-largest proven oil and natural gas reserves in the world1 standing at 97.8

billion barrels, i.e. around 6.6 % of the world’s total proven reserves of 1.48 trillion barrels.

In this respect, Abu Dhabi remains the powerhouse of the country since 90% of the UAE oil reserves

are located in this emirate. The UAE is also the 8th-largest oil producer in the world with around

1 2013 OPEC Annual Statistical Bulletin

Switzerland Global Enterprise – Major Business Sectors 2/13

3.1 million bbl/d of crude in 2013. The UAE exported USD 135.7bn of crude oil in 2012 of which

approximately 95% are going to the Asian market, in particular Japan. Oil production is operated by

Abu Dhabi National Oil Company (ADNOC), ), a state-owned company, working with a few

international oil companies such as BP, Shell, Total, ExxonMobil and Occidental Petroleum under

long-term concession agreements. The expiration of Abu Dhabi’s 75-year-old onshore concessions in

2014 should give opportunities for new players.

If current production levels are kept, the UAE’s oil reserves are expected to last for about 90 years. It

is highly unlikely that new oil discoveries be made in the future; however, the UAE’s oil production

capacity is expected to rise significantly in the medium term. The Government plans to spend USD

60bn over the next 5 years in order to raise production capacity production to nearly 4m bbl/d by

2020.

Beyond the large oil reserves, the UAE has also the 7th

world biggest natural gas reserve in the

world with 215 trillion cubic feet in 20122. Like oil, natural gas reserves are mostly located in Abu

Dhabi (94%). It is furthermore the 16th

biggest natural gas producer in the world with 54.31 bcm of

gas produced in 20123. Notwithstanding, rising domestic demand for subsidized energy and electricity

over the past decade has caused the UAE to become a net importer of natural gas since 2008.

While most of the UAE natural gas is exported to Japan, India, Kuwait and Taiwan, its imports stem

mostly from Qatar via the Dolphin Gas Project’s export pipeline. With USD 25bn-worth of projects

planned in Abu Dhabi, gas and oil production are expected to rise in the future. At the same time, the

global dynamics in the fossil energy production and marketing are changing due to the harnessing of

tight oil and gas as well as to technological advances (fracking) and as well as environment factors

which may well affect also the UAE in the future.

TRADE & COMMODITIES

The UAE is recognized as an international trading hub and the largest re-export hub in the

region. A 5% customs duty is applied on most goods. Dubai is the premier trading hub for precious

metals accounting for around 25% of the global physical gold trade. The UAE is also the largest re-

exporting destination for food products (meat processing, dairy products, vegetable oils, sugar

refineries, bakeries, deserts, bottled water, etc.) within the GCC countries.

The country displays a significant annual trade surplus of around USD 91bn, i.e. 9.3% of GDP in

2012. The total exports amounted to USD 368.9 bn (2013 est.), whereas total imports USD 249.6 bn

(2013 est.). The country ranks 17th

worldwide for merchandise exports and 46th

for commercial

services exports.

Merchandise exports are principally made up of fuel and mining products (37%) and manufacture

products (20%), whereas commercial service exports are composed principally of travel (73%) and

transportation services (27%). As regards exports, the UAE ranks 23th in merchandise imports and

19th

in commercial services imports4. Merchandise imports are made up principally of

manufactured products (55.4%), whereas commercial services imports include mainly transportation

(76%) and travel services (14%)5.

The UAE’s main export trading partners are Japan (15%) India (13%), Iran (11%), Thailand (%),

Singapore (6%) and South Korea (5%) while the most important import partners are India (17%),

China (14%), the USA (11%), Germany (5%) and Japan (4%). Switzerland is among the highest trade

partners in trade volume with a total of CHF 568 mio worth of exports to Switzerland against CHF 3.3

bn worth of imports from Switzerland in 2013, i.e. an increase of 3 % and 2% respectively over 2012.

2 BP Statistical Review of World Energy, 2013

3 Annual Statistical Bulletin, 2013

4 World Trade Organisation (WTO), 2013

5 World Trade Organisation (WTO), 2013

Switzerland Global Enterprise – Major Business Sectors 3/13

The country is member of the World Trade Organization (WTO) since 1996 and it has a liberal

trade regime, with low tariffs and few non-tariff barriers to trade. The UAE is a member of the Gulf

Cooperation Council (GCC) customs union, which came into effect at the start of 2003, and under

which its members - the UAE, Bahrain, Kuwait, Oman, Qatar and Saudi Arabia operate a single

customs policy at a general tariff rate of 5% and 50% and 100% for alcohol and tobacco respectively.

A currency union is under discussion but will certainly not be realized in the coming years. Along with

other GCC countries, the UAE have also signed the Greater Arab Free Trade Area (GAFTA), i.e. a

pan-Arab free trade area.

The FTA EFTA-GCC has just been ratified. Soon, it will be effective where the Swiss government and

its representations in the GCC will make the respective announcements. The Agreement covers

different areas of cross-border activities including the trade of goods. Most but not all customs duties

will be eliminated, some after a transitional period of five years. Rules of origin apply to different goods

categories.

Further information you find on:

http://www.seco.admin.ch/themen/00513/02655/02731/04117/index.html?lang=en

CONSTRUCTION & INFRASTRUCTURE

The construction industry accounted for $41bn in 2013 (15 % of total GDP), representing a real

value annual growth of 4.5%, is the third-largest sector of the UAE economy, after oil and trade. The

UAE has, for the first time since the crash, overtaken Saudi Arabia as the biggest construction

market in the Middle East, according to a report by Deloitte (2013). The UAE distinguishes itself

with the biggest construction market in the MENA region with USD 16.2bn of contracts awarded in

2012, mainly focused on commercial (62%) and energy infrastructures (19%). The industry boasts

the highest per-capita expenditure on construction in the world.

According to the Global Competitiveness Report 2013-2014, issued by the World Economic Forum

(WEF), the UAE was ranked 4th

globally in terms of infrastructure quality.

The economic crisis of 2008 caused the construction sector to slump, in particular in Dubai where a

burst of a real estate bubble eroded almost 60% of property values. Over the past years, however, the

sector has displayed again the signs of a notable recovery. Most of the construction activities are

taking place in Abu Dhabi and Dubai where many projects have been restarted or newly launched.

The Dubai Government has announced, among many others, the launch of the Mohammed Bin

Rashid City mega project, which will feature the world’s largest shopping centre and 100 hotels, the

Dubai Creek Harbour and the expansion of the existing and construction of a second Dubai

International Airport. Abu Dhabi announced the construction, among other, of the Etihad Rail

Network, the Baraka Nuclear Power Plant, and the Khalifa Industrial Zone in Abu Dhabi (Kizad).

Real estate developments have been focused principally on high-end mixed-use developments. The

performance of the real estate market is however different in Abu Dhabi, where rents and prices are

flatter due to oversupply, and Dubai where the recovery is more pronounced. In parallel, the country

has been witnessing an increasing number of green buildings projects most of which are still under

construction.

Among the main project developers, we can consider Emaar Properties, Nakheel, Meraas, Al

Habtoor, Al Dar & Damac Properties. The construction sector remains however largely supported by

the UAE Federal Government through big projects launched by the state-owned or government near

institutions, such as ADEWA and DEWA. Again, the construction industry is a very promising market,

Switzerland Global Enterprise – Major Business Sectors 4/13

although it is highly reliant on oil prices and on immigrant workforce. There is currently still a shortage

of professional workers in the market.

TOURISM

The total contribution of travel and tourism to GDP was 14.2% in 20136 (est.), which is well above the

world average of 9%. It is forecast to rise by 5.0% pa by 2023 (16.4% of GDP).The Arab Spring of

2011 had a major impact on the UAE tourism leading to an unprecedented influx of tourists. Today,

Dubai is regarded among the top 10 world tourism destination. The city, which is by far the preferred

destination in the UAE, attracted over 11 million tourists in 2013 (i.e. +10% compared to 2012) and

counts around 600 hotels. Abu Dhabi, on the other hand, attracted around 3 million visitors (i.e. +27%

compared to 2012). Visitors come principally from Arab countries, especially Saudi Arabia, Europe

(25%) and Asian countries (20%).

The development of tourist infrastructure and attractions is one of the government's top priorities to

diversify the economy. According to the “Travel & Tourism Competitiveness Report 2013”, the UAE

continue to lead the MENA region at 28th out of 140 nations (up two places since the last

assessment), attracting both leisure and business travelers, with several major and growing number of

international fairs and exhibitions and increasingly diverse creative industries.

The most important competitive advantage of the UAE is its world-class international hub for global air

travels. Furthermore, the country has carried out effective marketing and branding campaigns and has

adopted policy rules and regulations that are conducive to the development of the sector such as a

liberal visa regime.

Hotel prices are however, seasonally, somewhat high by international standards. Nonetheless, this did

not prevent hotel performance to be good. Occupancy rates in Dubai reached 80% (remained

stable compared to 2012), that is among the highest in the world, and hotel room rates display an

average daily rate (ARR) of around USD 278 in 2013 (i.e. +6.4% compared to 2012), leading

revenue per available room (RevPAR- a benchmark for performance) to reach $223 (i.e. +5.9%

compared to 2012) although the total number of rooms offered in the UAE grew by around 8% in

2012. Meanwhile in Abu Dhabi hotels, occupancy rose 1% to 77%, while ARR climbed 6% to USD

207 and RevPAR grew by 7.4% to USD 160. According to the UN’s World Tourism Organization

(UNWTO), the UAE topped the Middle East region for international tourism receipts amounting to

USD 46.7bn in 2012.

The Dubai Government announced its aim to attract 20 million visitors by 2020 which appears to be

a very realistic scenario according to forecasts and after having won the bid to host Expo 2020. In

addition, the country is striving to develop its potential for medical tourism.

INVESTMENT & FREE ZONES

In 2013, foreign direct investments (FDI) in the UAE reached USD 12bn. Dubai, which accounted

for almost 90% of the inflows, is seen as an attractive location for global investors and has largely

benefited from the regional turmoil by attracting capital inflows.

There are two options to establish a business in the UAE: outside or inside a free zone.

The investment regime onshore favors local over foreign investors. All investment projects have to

have 51% domestic capital meaning that these companies are allowed a maximum of 49% foreign

ownership.

6 Travel & Tourism - Economic Impact, 2013

Switzerland Global Enterprise – Major Business Sectors 5/13

Business companies that are outside a free zone are treated as a fully Emirati entity and have to

comply with the local law through the licensing authority of the emirate. The UAE require investors to

have a local sponsor or partner or service agent.

Generally, the Limited Liability Company (LLCs) is the most common form of enterprise used.

There are four major laws related to FDIs in the UAE: the Federal Companies Law, the Commercial

Agencies Law, the Federal Industry Law, and the Government Tenders Law. As some of these

laws are under review, investment law is expected to become more and more conducive to FDIs in

the future.

With the rise of Dubai as a regional hub for many international companies, one of the most successful

policies has been the development of offshore free zones. There are today around 50 free zones

scattered all over the UAE (link: http://www.uaefreezones.com/), which host more than 17,000

companies. Free zones in the UAE can be attractive for the following reasons: “one-stop-shop” (easy

procedures), 100% foreign ownership, 100% repatriation of capital and profits, 0% corporate tax for

up to 50 years, 0% import and re-export duties, no personal income taxes, free capital transfer, no

currency restriction, unlimited foreign employees, low operating costs, state-of-art facilities, efficient

communication infrastructure, as well as company assistance (labour recruitment, worker housing,

etc.). On the other hand, companies set up in free zones cannot exercise commercial activities in the

UAE (onshore).

An independent Free Zone Authority (FZA) governs each free zone and is responsible for assisting

companies when they establish themselves in it. Free zones are generally dedicated to specific

sectors. The most popular free zones are Jebel Ali Free Zone (JAFZA), the first free zone

established in the region, Dubai Airport Free Zone (DAFZA), and Dubai International Financial

Centre (DIFC). Other well-known free zones include Ras Al Khaimah (RAK) and Dubai Multi

Commodities Centre (DMCC).

Free zones play a considerable role in the UAE economy since two-third of the non-oil products are

exported from them, in particular machines and electronic devices.

TRANSPORT

The transport sector accounted 7% of the GDP in 2012. The UAE has one of the largest air transport

industries in the world with its 5 airlines and its 3 major airports. Aviation passenger traffic is soaring in

the country due to the increasing inflow of tourists and a higher number of expatriates. Dubai

International Airport strengthened this year its position as the world’s fourth busiest airport with 66.4

million passengers (+15.2% over 2012) and announced a major modernization and expansion

program which will increase its capacity to 90 million passengers by 2018. Dubai’s airline industry

achieved its most important milestone when it opened the Al Maktoum International Airport which is

expected to be the world’s largest airport once it will be fully completed (very soon). The first of 5

runways opened in October 2013 for commercial flights. The Abu Dhabi International Airport, which

also hit a record of passengers this year, announced a redevelopment and expansion project - The

Midfield Terminal Complex (USD 3.2bn), which is due to open by 2017 and which is expected to be

used by 20 million of passengers in the future.

The UAE’s airline industry benefits from “open skies” policies and is expanding its network

continuously. The UAE has two world-class airlines: Emirates Airline, which is owned by the Dubai

government and one of the largest carriers in the world, and Etihad Airways, the UAE’s national

airline. Both are in a fast process of growth.

Abu Dhabi has been also at the forefront of the GCC’s rail transformation with the 1’200-kilometre

Etihad Rail network (USD 11bn) due to be completed by 2018. The Etihad Railway will run through

Kuwait, Saudi Arabia and Oman and will make it easier to move goods and commodities between

Switzerland Global Enterprise – Major Business Sectors 6/13

these countries and thus will further improve the UAE’s role as a regional trade hub. Over the last

year, the country has also launched two metro projects, i.e. the Abu Dhabi Metro/light railway (USD

7bn) and the Dubai Metro expansion (USD 7bn).

Dubai’s two important marine ports are Port Rashid and Jebel Ali Port, the latter being the busiest

port in the region and the 10th largest in the world in terms of throughput. Other major ports in the UAE

include Mina Zayed (Abu Dhabi), Mina Khalid (Sharjah) and Khor Fakkan (Sharjah).

FINANCIAL SERVICES

Since the 2009 Dubai debt crisis, government policies related to the financial sector have been

focused on protecting the banking sector and increasing its liquidity. After a challenging period during

the financial crisis, the financial sector has again started to recover. The UAE banking sector is today

well-capitalized, liquid and it is one of most important financial centers in the world.

This success of the UAE financial sector is mainly due to the booming local economy and a sharp

increase in retail and corporate lending, as consumer and investment confidence and spending

increase. The UAE’s banking sector is however very divergent between Abu Dhabi and Dubai. The

former is characterized by the dominance of the public sector, whereas the latter by the private sector.

The UAE has a remarkably high number of banks which remained steady during the year 2013. Over

the 12 last months until July 2013 deposits have increased by 12%. At the same time, bank lending in

the UAE reached their highest level since the financial crisis. The loan-to-deposit ratio across the UAE

banking sector was 92.6 at the end of July 2013. Despite it, the UAE banking system is very

interconnected with GREs (government-related entities) and lacks transparency, which still

present a systemic risk according to the International Monetary Fund (IMF). Nonetheless, planned

restriction on mortgage lending and loan concentration limits on GRE’s and the emirate Government

should help to mitigate this risk.

As mentioned earlier, Dubai hosts the Dubai International Financial Centre (DIFC), a self-regulating

financial free zone, which has its own jurisdiction and which is now one of the largest financial hubs in

the region. Abu Dhabi has also announced last year the creation of its own financial free zone, the

Global Marketplace Abu Dhabi.

The UAE has three domestic stock markets, the Dubai Financial Market (DFM) and the Abu Dhabi

Securities Market (ADSM) both launched in 2000. In September 2005 a third capital market - the

NASDAQ Dubai (former Dubai International Financial Exchange (DIFX) - began to operate as the

centerpiece of the Dubai International Financial Center (DIFC).

Islamic banking is taking an ever more prominent role in the UAE due to the increasing size of

Islamic finance under asset over the last years. Dubai in particular has strengthened its position as

Islamic financial hub over the last years. The Government announced recently its plans to develop the

UAE further as an international centre for Islamic finance in particular for “sukuk” (Islamic bonds).

The country created the Dubai Center for Islamic Banking and Finance in 2013 and plans to

establish an independent authority which will supervise the country’s Islamic finance industry.

According to the Islamic Finance Country Index 2013 (IFCI), the UAE is the 2nd largest issuer of

“sukuk” among the GCC countries after Saudi Arabia and 4th in the world in 2013.

Switzerland Global Enterprise – Major Business Sectors 7/13

TRADE FAIRS & EXHIBITIONS

The UAE has become the most important hub in the region for international trade fairs, exhibitions,

conferences and seminars. Dubai has two premier venues - the Dubai International Convention

and Exhibition Centre and Al Maktoum International Airport.

Abu Dhabi, that also aims at becoming a trade fair hub, hosts the Abu Dhabi National Exhibitions

Company (ADNEC).

More than 100 exhibitions, trade fairs and conferences with regional and global reach cover a wide

range of sectors including health, oil & gas, construction & real estate, entertainment, fashion,

electronics & IT, travel & tourism, education, food, defense, and a vast range of special events are

held every year in the UAE. The Big 5, The Arab Health, Gulfood, Gitex & Dubai Airshow are well

known exhibitions in Dubai with Swiss pavilions and different Swiss exhibitors every year.

As for Abu Dhabi, there are few worldly known events like: World Future Energy Summit (WEFS),

International Defense Exhibition (IDEX) & “Adipec”.

A list of trade fairs in the UAE can be found on the internet at:

www.dwtc.com (Dubai),

www.adnec.ae (Abu Dhabi).

HEALTHCARE

According to the World Health Organisation (WHO), the UAE are among the world’s top 20 in

healthcare-related spending per capita. The UAE has a comprehensive government-funded health

service financing two thirds of the UAE’s healthcare spending in 2012. The Government supports in

selected medical care cases for sending its nationals abroad, in particular to the US or Germany for a

total of USD 2.5bn in 2012.

Over the past few years, the healthcare industry has displayed extraordinary growth due to rising

standard of living of the population, the population increase and lifestyle diseases which are on the

rise in the Gulf countries. This led the sector to triple in the past 5 years.

The UAE is today regarded among the world’s top 20 destinations for medical tourism due to a

rising demand over the last years and an increasing offer of hospitals and clinics. According to the

Dubai Health Authority, the number of medical tourists in Dubai raised up to 10-15% compared to last

year. One of the main advantages of the UAE lies in its ability to offer medical services at lower costs

compared to North America and the European countries. According to Euromonitor International, the

UAE’s medical tourism market was worth around USD 1.6bn in 2012 and ranked 2dn in the region

according to the World Bank.

The UAE has established specialized health related free zones, such as the Dubai Healthcare City

(DHCC), which have been attracting the interest of international healthcare players. Another initiative

is the Dubai Biotechnology and Research Park (DuBiotech), launched in 2005, which offers the

possibility to companies and universities to set up their research facilities. Sharjah also announced the

creation of the Sharjah HealthCare City (SHCC) to attract healthcare companies.

Public healthcare services are administered by different authorities including the UAE Ministry of

Health, the Health Authority-Abu Dhabi (HAAD), the Dubai Health Authority (DHA) and the Emirates

Health Authority (EHA). As part of the Dubai Health Strategy 2013-2015, the Dubai Health Authority

aims to reach internationally recognized levels of healthcare. Among the key projects launched by the

Dubai Health Authority (DHA) are the rebuilding of Rashid Hospital at a cost of around USD 820m, the

opening of 3 new hospitals and 40 health centres. The federal government plans also to manage 70%

of the UAE’s hospital by private operators by 2015.

Switzerland Global Enterprise – Major Business Sectors 8/13

AGRICULTURE

Limited arable land and scarce water limit agricultural production in the UAE. The arable land

represents only 0.8% of the total land of which 0.5% is used for permanent crop. Agriculture plays

therefore a minor part of the UAE economy amounting to less than 1% of the GDP. The UAE meets

only around 18% of its domestic food demand, which makes the country a major net food importer.

Notwithstanding, food production has increased over the last years thanks to development of ground

water reserves, increase in water desalination capacities and the installation of high-performance

pumps. The UAE is today as the second largest food producer in the GCC after Saudi Arabia.

The most productive region is Ras al-Khaimah which has larger underground water supplies.

The Government continues to support agriculture also for political reasons (food security), but it is

aware that self-sufficiency in food is unattainable. The Abu Dhabi Government has established the

Abu Dhabi Food Control Authority (ADFCA), which is responsible for food safety and agriculture,

and which works in collaboration with the Abu Dhabi Farmers’ Services Centre (ADFSC) aiming at

helping farmers to boost their productivity though more efficient methods. In 2013, the Government of

Abu Dhabi launched a program called the “Ziraai” which supports citizens working in the agricultural

sectors. The UAE environment ministry supports furthermore the development of organic farms.

Foreigners other than GCC nationals are not allowed to own agricultural land. Al Dahra Agriculture

Company, a privately held company, is currently the biggest supplier of hay, rice and other

commodities in the UAE. With growing population and the high dependence on food imports, food

security remains a key challenge for the country.

THE UAE IS A MEMBER OF THE GULF FREE-TRADE ZONE

The UAE is a member of the Gulf Cooperation Council (GCC) customs union, which came into effect

at the start of 2003. Under the agreement all six members of the GCC (Bahrain, Kuwait, Oman, Qatar,

Saudi Arabia and the UAE) operate a single customs policy, at a unified tariff rate of 5%. The customs

union is working, creating the Arab world’s largest trade bloc and establishing one of the most

important single consumer markets in Asia, with total goods imports of close to USD 100bn a year. In

addition, a currency union is planned but will not be realized in the upcoming years.

Switzerland Global Enterprise – Major Business Sectors 9/13

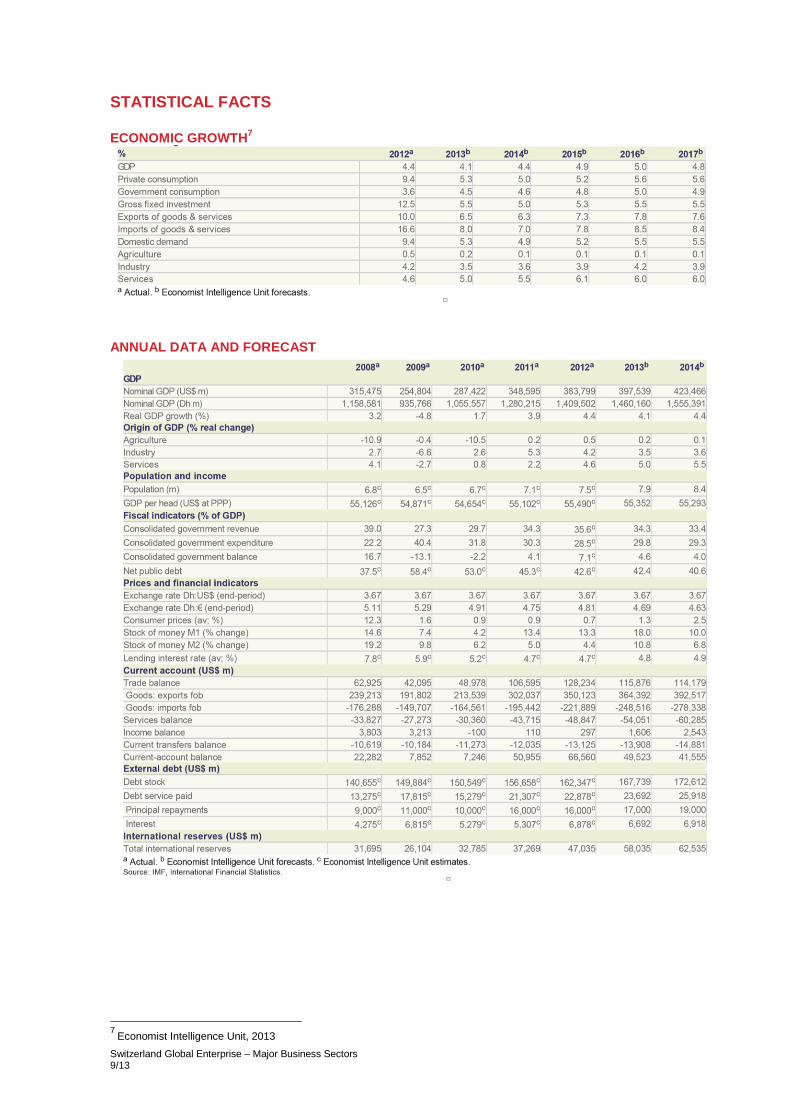

STATISTICAL FACTS

ECONOMIC GROWTH7

ANNUAL DATA AND FORECAST

7

Economist Intelligence Unit, 2013

Switzerland Global Enterprise – Major Business Sectors 10/13

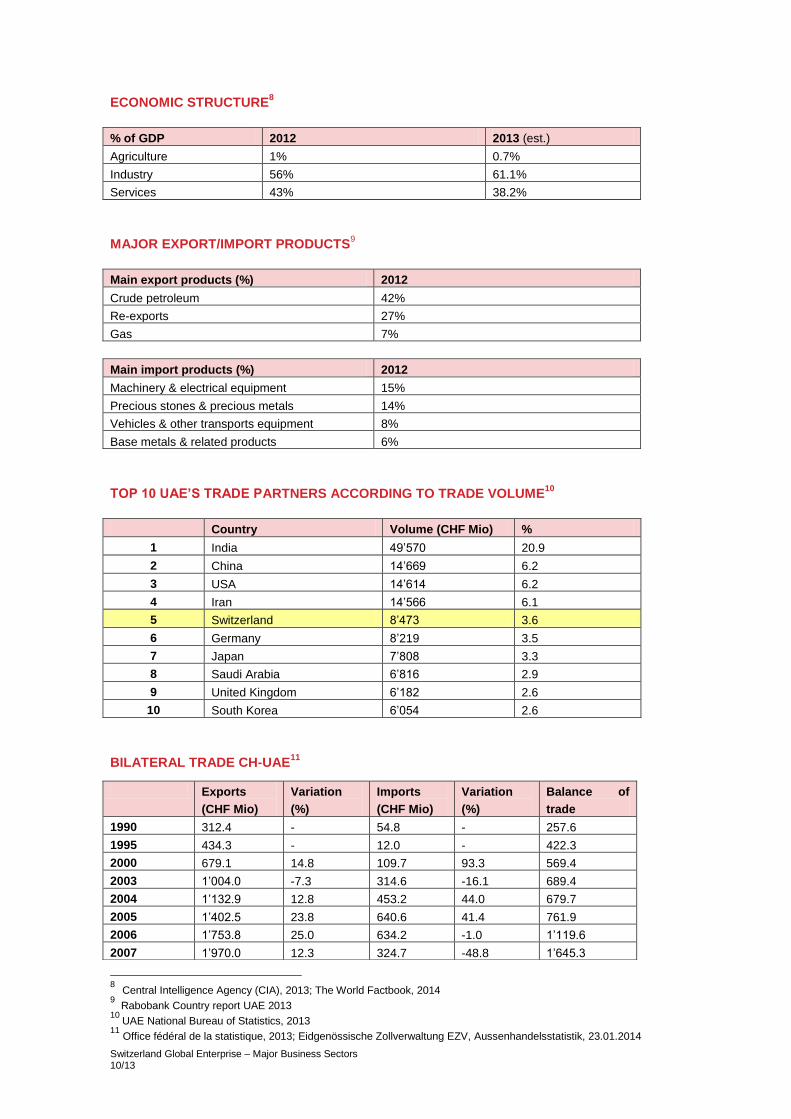

ECONOMIC STRUCTURE8

% of GDP 2012 2013 (est.)

Agriculture 1% 0.7%

Industry 56% 61.1%

Services 43% 38.2%

MAJOR EXPORT/IMPORT PRODUCTS9

Main export products (%) 2012

Crude petroleum 42%

Re-exports 27%

Gas 7%

Main import products (%) 2012

Machinery & electrical equipment 15%

Precious stones & precious metals 14%

Vehicles & other transports equipment 8%

Base metals & related products 6%

TOP 10 UAE’S TRADE PARTNERS ACCORDING TO TRADE VOLUME10

Country Volume (CHF Mio) %

1 India 49’570 20.9

2 China 14’669 6.2

3 USA 14’614 6.2

4 Iran 14’566 6.1

5 Switzerland 8’473 3.6

6 Germany 8’219 3.5

7 Japan 7’808 3.3

8 Saudi Arabia 6’816 2.9

9 United Kingdom 6’182 2.6

10 South Korea 6’054 2.6

BILATERAL TRADE CH-UAE11

8 Central Intelligence Agency (CIA), 2013; The World Factbook, 2014

9 Rabobank Country report UAE 2013

10 UAE National Bureau of Statistics, 2013

11 Office fédéral de la statistique, 2013; Eidgenössische Zollverwaltung EZV, Aussenhandelsstatistik, 23.01.2014

Exports

(CHF Mio)

Variation

(%)

Imports

(CHF Mio)

Variation

(%)

Balance of

trade

1990 312.4 - 54.8 - 257.6

1995 434.3 - 12.0 - 422.3

2000 679.1 14.8 109.7 93.3 569.4

2003 1’004.0 -7.3 314.6 -16.1 689.4

2004 1’132.9 12.8 453.2 44.0 679.7

2005 1’402.5 23.8 640.6 41.4 761.9

2006 1’753.8 25.0 634.2 -1.0 1’119.6

2007 1’970.0 12.3 324.7 -48.8 1’645.3

Switzerland Global Enterprise – Major Business Sectors 11/13

BILATERAL TRADE CH-UAE: MAJOR PRODUCTS12

EXPORTS FROM SWITZERLAND TO UAE IN 2013

Most Important Industry Sectors (2013) +/- % Mio. CHF

Jewellery +21.6% 1’194.5

Watches +9.2% 934.1

Machinery (elec. & non) -31.0% 282.2

Pharmaceuticals +3.3% 247.6

EXPORTS FROM UAE TO SWITZERLAND IN 2013

Most Important Industry Sectors (2013) +/- % Mio. CHF

Jewellery +5.8% 468.8

Watches +5.7% 51.7

Vehicles & Aircrafts -36.4% 6.9

Machinery (elec. & non) -31.2% 5.9

12

Eidgenössische Zollverwaltung EZV, Aussenhandelsstatistik, 23.01.2014

2008 2’841.0 44.1 443.7 36.8 2’397.3

2009 2’226.3 -21.6 534.2 20.4 1’652.9

2010 2’251.1 1.1 755.8 41.4 1’495.3

2011 2’785.9 23.8 496.3 -34.3 2’289.6

2012 3’177.1 14.0 551.1 11.0 2’626.1

2013 3’252.8 2.4 568.0 3.1 2’684.8

Switzerland Global Enterprise – Major Business Sectors 12/13

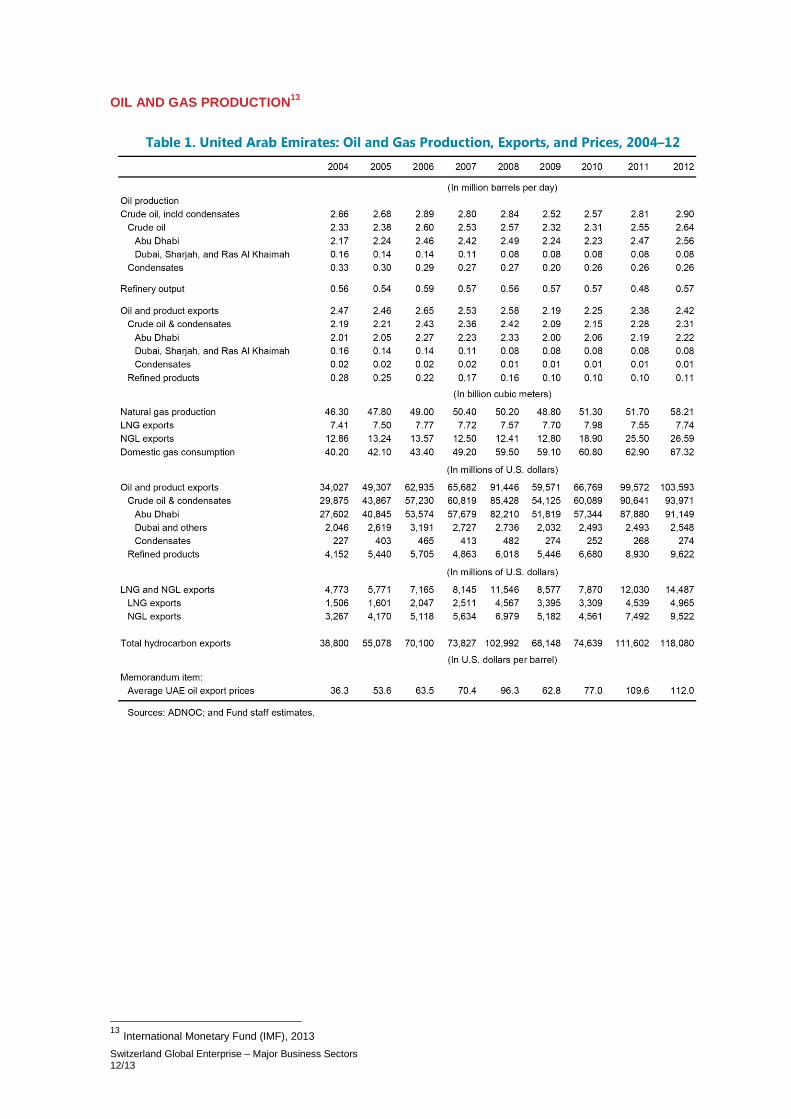

OIL AND GAS PRODUCTION13

13

International Monetary Fund (IMF), 2013

Switzerland Global Enterprise – Major Business Sectors 13/13

DATA SOURCES

- World Bank – Doing Business 2013

- International Monetary Fund (IMF) – Article IV Consultation/ UAE: Selected Issues, 2013

- The Central Bank of the UAE

- United Arab Emirates Ministry of Foreign Trade – Why UAE 2012

- UAE National Bureau of Statistics

- US Department of State – 2013 Investment Climate Statement UAE

- Embassy of Switzerland in the UAE - Economic report 2012-2013

- SECO – Foreign trade statistics

- Economic Intelligence Unit (EIU) – Country report UAE 2013

- Central Intelligence Agency (CIA) – CIA World Factbook

- World Economic Forum (WEF) – World Competitiveness Report 2013-2014

- Local newspapers

- BP Statistical Review of World Energy, 2013

Date: April, 2014

Swiss Business Hub GCC

c/o Consulate General of Switzerland

P.O. Box 9300

Dubai, United Arab Emirates

Tel. +971 4 329 09 99

Fax. +971 4 331 36 79