Unit 53_Risks Associated With Investing in Bonds_2013

16

www.proschoolonline.com/ 1 Risks Associated with Investing in Bonds Reading - 53 Fixed Income

description

Risks associated with investing in bonds

Transcript of Unit 53_Risks Associated With Investing in Bonds_2013

www.proschoolonline.com/ 1

Risks Associated with Investing in Bonds

Reading - 53

Fixed Income

www.proschoolonline.com/ 2

Interest Rate Risk

Facts:

• The price of the bond is inversely proportional to Interest rate or yields.

• Hence, this raises the risk for bondholder known as the interest rate risk.

• A bond will trade at par if the coupon rate is equal to the required yield by market.

• If coupon rate > yield required by market then, Price > par value.

• If coupon rate < yield required by market then, Price < par value.

www.proschoolonline.com/ 3

Interest Rate Risk

Example:

Par value = Rs.100

Coupon Rate = 6%, 20 year bond

Yield required by market = 6.5%

Price of bond = Rs.94.45

Settlement Date

= 15-03-1990

www.proschoolonline.com/ 4

Features of bond affecting Interest Rate Risk

Impact of Maturity

Longer the maturity of bond, greater is the bond’s price sensitivity to change in interest rate.

Example:

Case - IPar value = Rs.100Coupon Rate = 7%, 20 year bondYield required by market = 7.5%Price of bond = Rs.94.86Change = -5.14%

Case - IIPar value = Rs.100Coupon Rate = 7%, 5 year bondYield required by market = 7.5%Price of bond = Rs.97.95Change = -2.05%

www.proschoolonline.com/ 5

Features of bond affecting Interest Rate Risk

Impact of Coupon Rate

Lower the required rate, greater is the bond’s price sensitivity to change in interest rate.

Example:

Case - IPar value = Rs.100Coupon Rate = 8%, 20 year bondYield required by market = 6.5%Price of bond = Rs.116.66

Case - IIPar value = Rs.100Coupon Rate = 8%, 20 year bondYield required by market = 7%Price of bond = Rs.110.68

www.proschoolonline.com/ 6

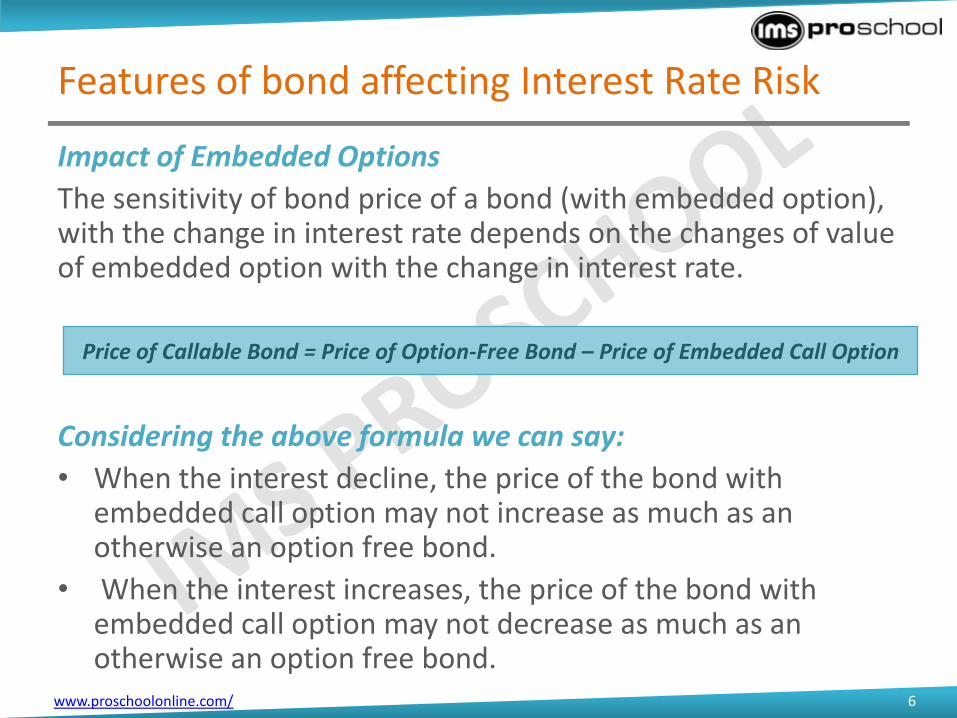

Features of bond affecting Interest Rate Risk

Impact of Embedded Options

The sensitivity of bond price of a bond (with embedded option), with the change in interest rate depends on the changes of value of embedded option with the change in interest rate.

Considering the above formula we can say:

• When the interest decline, the price of the bond with embedded call option may not increase as much as an otherwise an option free bond.

• When the interest increases, the price of the bond with embedded call option may not decrease as much as an otherwise an option free bond.

Price of Callable Bond = Price of Option-Free Bond – Price of Embedded Call Option

www.proschoolonline.com/ 7

Impact of Yield Level

Higher the bonds yield, lower is its price sensitivity.

Example:

Case - IPar value = Rs.100Coupon Rate = 8%, 20 year bondYield required by market = 6.5%Price of bond = Rs.116.66

Other things held constant, if the yield increases by 100 basis points then,

Yield required by market = 7.5%Price of bond = Rs.105.14% Change in Price = -9.87%

Case - IIPar value = Rs.100Coupon Rate = 8%, 20 year bondYield required by market = 7%Price of bond = Rs.110.68

Other things held constant, if the yield increases by 100 basis points then,

Yield required by market = 8%Price of bond = Rs.100% Change in Price = -9.65%

www.proschoolonline.com/ 8

Interest Rate Risk for Floating-Rate Securities

Factors causing fluctuations in price of floating-rate securities:

Note:

The coupon rate is set periodically, based on the prevailing marketinterest rate that is used as a reference rate plus a quoted margin.

Longer the duration between current and next coupon resetdate, higher is the possibility of price fluctuation.

If there is a change in the required margin of investors, theprice of floating-rate security might fluctuate.

The floating-rate securities usually have a cap which mightresult in fluctuation of the price based on different situations.The risk for a floating rate security is known as cap risk

www.proschoolonline.com/ 9

Measuring Interest Rate

Price change of bonds can be seen in terms of:

• Percentage change in price from initial price.

• Absolute price change from initial price.

Percentage Price change

It is calculated by taking average of percentage change in price resulting from an increase and a decrease in interest rates by same number of basis points.

Approximate percentage change for a 100 basis point change in yield

Price if yield decline - Price if yield rise

2 x Initial Price x Change in yield in decimal

The change in yield is referred as

“Rate Shock”

www.proschoolonline.com/ 10

Measuring Interest Rate

Example:

Suppose a bond is currently selling at Rs.94 to yield 7%. Now if the interest rate shoots up by 50 basis points, the price of the bond declines to Rs.92 and if the interest rates take a dip by 50 basis points, the price of the bond increases to Rs.97. Estimate the approximate percentage price change for a 100 basis point change in yield.

Solution:

% change in price for a 100 basis

point change in yield

= (97 – 92)/[2 x 94 x .005]

= 5.31%

Note:• Percentage price change for a 100

basis point change in yield is called “Duration”.

• “Duration” is a measure of price sensitivity of a bond to a change in yield.

www.proschoolonline.com/ 11

Yield CurveThe graphical depiction of the relationship between the yield and maturity is known as yield curve.

Bond Portfolio

Parallel shift in yield curve of +50 basis points

www.proschoolonline.com/ 12

Yield Curve

Non-Parallel shift in yield curve of +50 basis points

Shift in Yield Curve

Parallel shift in Yield Curve Non-Parallel shift in Yield Curve

www.proschoolonline.com/ 13

Call or Prepayment Risk

A bond that includes a call option allows the issuer to call all or a part of the issue prior to maturity. Reason why they would exercise the call option:

• If the issuer receives surplus cash with no investment opportunities, they may wish to repay their debt thus saving on interest.

• If interest rates fall, the issuer may wish to refinance existing debt at a lower interest rate. They can do this by repaying the existing debt and issuing new debt at the lower interest rate.

Disadvantages of a callable security

• Cash Flow is uncertain

• Reinvestment Risk

• Price compression

www.proschoolonline.com/ 14

Reinvestment Risk

It refers to the risk that the interim cash flows received from a bond which are available for investing again might have to be invested at a rate lower than the rate at which they were invested previously.

A security has more reinvestment risk when:

• It carries a higher coupon rate then prevailing market rate.

• It has a call or prepayment option.

• It is an amortizing security. Note:A Zero coupon bond has zeroinvestment risk but thisadvantage is offset by theirgreater duration and interestrate risk.

www.proschoolonline.com/ 15

Credit Risk

• Default risk is the risk that an issuer will fail to perform on its obligations under the terms of a bond contract with respect to the timing of payments, and the amount owed to investors.

• Credit risk reflect the riskiness of an investment as perceived by the market.

• An increase in credit risk will translate into an increase in the required yield and force the bond’s price to lower. This is known as credit spread risk.

• Downgrade risk is the risk that credit rating agencies will downgrade the credit rating of a particular issue.

Credit Risk = Yield on a risky bond – Yield of risk free bond

www.proschoolonline.com/ 16

More Risks

Liquidity Risk: It the risk that an investor has to sell his investments at a lower price than its indicated value.

Exchange Risk: It refers to the risk of receiving a lower amount at maturity of a foreign currency denominated bond than invested to acquire the bond.

Inflation Risk: It refers to the declining in the purchasing power of the security’s cash flows due to inflation.

Event Risk: A natural disaster may impair issuer’s ability to satisfy debt obligations.

Sovereign Risk: It is a risk that a foreign government may be unable to satisfy its debt obligations.