Unilever pakistan

75

-

Upload

raja-noman -

Category

Business

-

view

2.123 -

download

25

Transcript of Unilever pakistan

HISTORY• Lever brothers is founded by

WILLIAM HESKETH LEVER in 1890

• Key player in food & household product industry

• Historically grew through acquisitions

INTRODUCTION

LEVER BROTHERS, THE OLD NAME OF UNILEVER CHANGED INTO UNILEVER AFTER THE MERGER OF LEVER BROTHERS & MARGARINE UNIE IN 1930

UNILEVER IS A MULTI NATIONAL COMPANY

IT IS ONE OF THE LARGEST CONSUMER GOODS COMPANIES IN THE WORLD

ITS BRANDS ARE ON SALE IN 151 COUNTRIES

UNILEVER STAFF

TODAY UNILEVER EMPLOYEES 179,000 PEOPLE IN 150 COUNTRIES WORLDWIDE

TODAY UNILEVER EMPLOYEES IN PAKISTAN ARE1677.

VISION STATEMENT

“We help people around the world to meet everyday needs for nutrition, hygiene and well being, with brands that help people look good, feel good and get more out of life”

MISSION STATEMENT

“Vitality is at the heart of everything we do. It’s in our brand, our people

and our approach to business”

OBJECTIVES

• To be honest transparent and ethical

• To win hearts and minds of consumers

• To deliver what we promise

• To become empowered leaders

• To believe in trust, truth and team work

• To care and actively contribute the community

LOGO

This is the logo of “UNILEVER”

SLOGAN

“FEEL GOOD, LOOK GOOD AND GET MORE OUT OF

LIFE…”

CEO UNILEVER

“PAUL POLMAN”CEO OF UNILEVER (FROM OCT. 08)

UNILEVER PAKISTAN(1948)

4 WHOLLY OWNED AND 6 3RD PARTY MANUFACTURING SITES

FIRST SITE IN PAKISTAN WAS IN RAHIM YAR KHAN

LARGEST FMCG COMPANY NOW OPERATING AT SIX LOCATIONS IN PAKISTAN

CEO UNILEVER PAKISTAN

MR.EHSAN A.MALIK CEO IN PAKISTAN

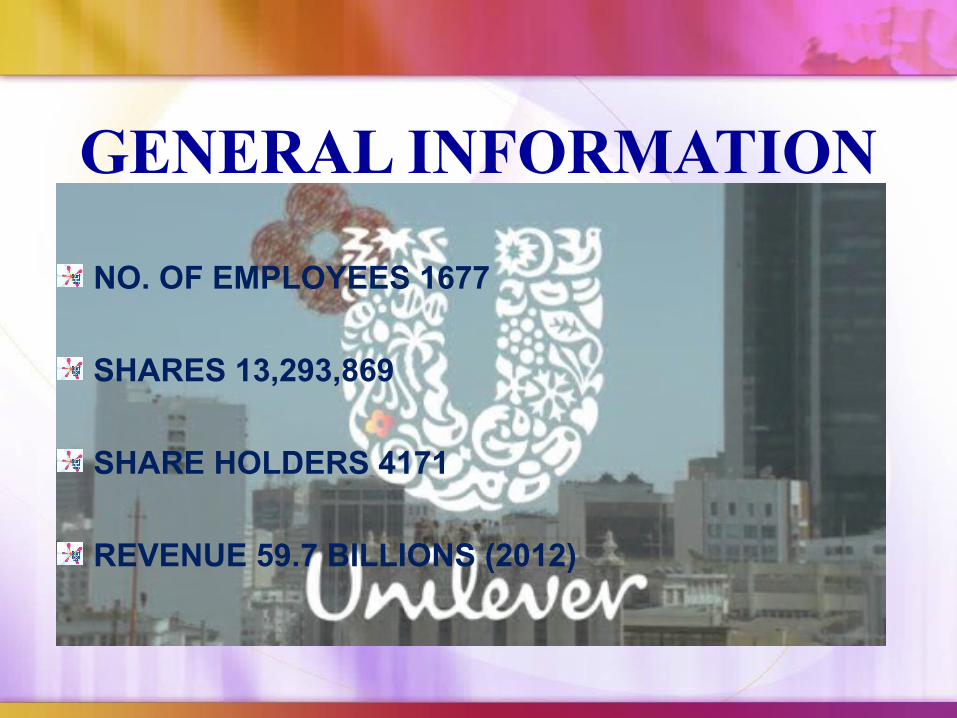

GENERAL INFORMATION

NO. OF EMPLOYEES 1677

SHARES 13,293,869

SHARE HOLDERS 4171

REVENUE 59.7 BILLIONS (2012)

FOOD BRANDS

• Badami• Blue band• Brooke bond supreme• Energile• Knorr• lipton

• Pearl dust• Rafhan• Wall’s

PERSONAL CARE BRANDS

• Clear shampoo• Close up• Dove• Fair & lovely• Lifebuoy shampoo• Lifebuoy soap• Lux

• Pond’s• Rexona• Sunsilk• Vaseline

HOME CARE BRANDS• Comfort• Rin• Sunlight• Surf excel• vim

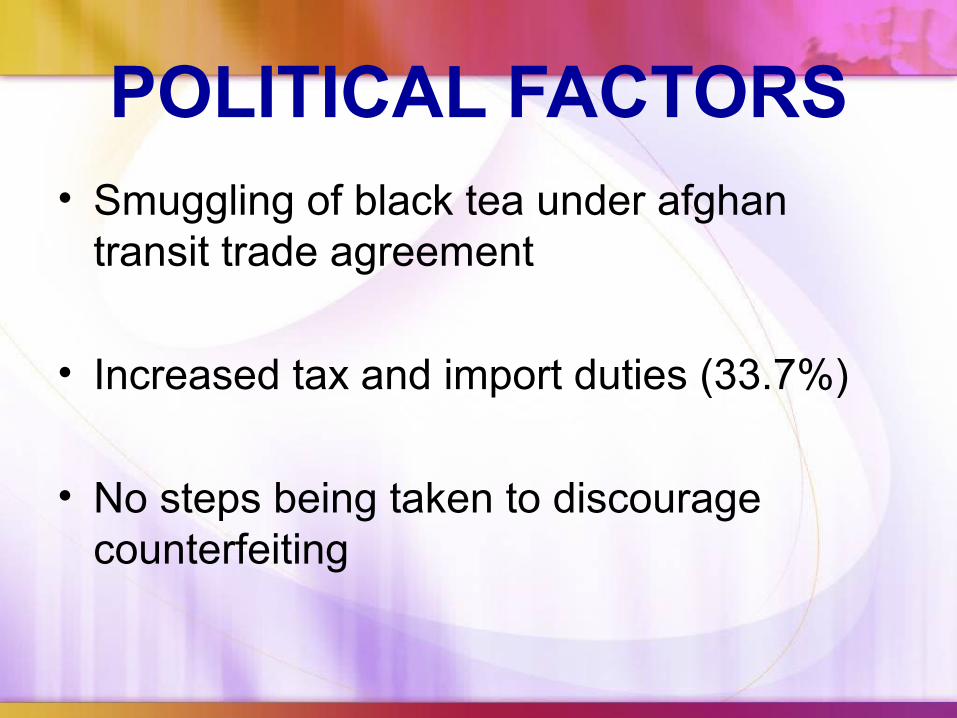

PESTEL ANALYSIS

POLITICAL FACTORS• Smuggling of black tea under afghan

transit trade agreement

• Increased tax and import duties (33.7%)

• No steps being taken to discourage counterfeiting

ECONOMIC FACTORS• UPL uses palm oil as a major input, but

price fluctuations

• Energy crises is effecting the ice-cream segment

• High inflation rate

SOCIAL CULTURAL FACTORS

• Growing urbanization

• Higher number of youngster

• Rising income

These factors led to change consumer life style

• Total population 173.51 million

• 110.46 million rural areas

• 63.05 million urban areas

TECHNOLOGICAL FACTORS

• Spent 891 million Euros on R & D in pak

• UPL uses internet to train its employees

• Energy crises

LEGAL FACTORS• Changing legislation

• Minimum wages of unskilled workers increased from 6000 to 7000 rs in 2010

• As per law after 9 months temporary workers should me made permanent

STRENGTH’S• Customer loyalty

• High dividend payout

• International brand strength

• Market share of 41%

• Oldest MNC of Asia

• Strong financial position

• Vast distribution network

• Large range of brands

• Well established brand name

• Latest state of art and technologies

• Established raabta consumer care line

WEAKNESSES

• Costly products

• Discrimination among employees

• Weak web presence

• Only 1500 employees are on their payroll

• Many protests by labor unions

• Using nameless factories in Karachi

• Had to sale dalda

opportunities• Could develop new product

• Local competitors have poor products

• Unrelated diversification

• Around 40% smuggled tea can be catered

• Urban areas are only familiar with shampoo

• End user respond to new ideas

• Strategic acquisitions can help to expand further

• Huge potential in rural areas

• Young generation is becoming beauty concious

• New soaps can be introduced in winter

• Forward integration can be done

• Pakistan is 3rd largest importer of tea, huge potential in tea farming

THREATS• Legislation could impact

• Retention of key staff critical

• Major competitor

• Competitor aggressive marketing

• Security conditions

• Energy shortage

• High taxation

• Price war

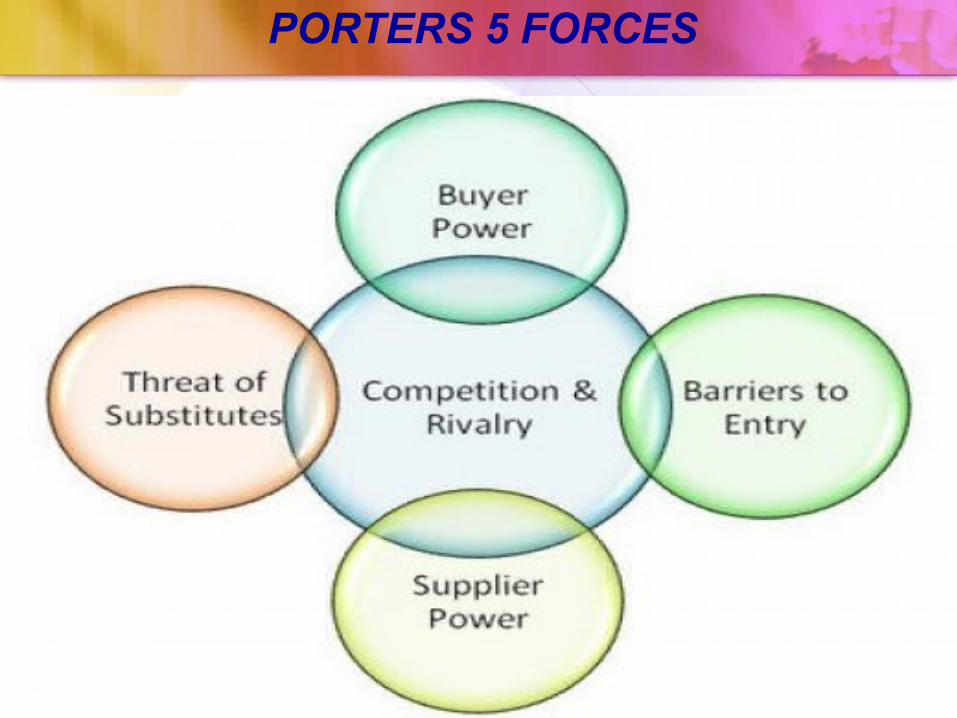

PORTERS 5 FORCES

BARGAINING POWER OF BUYERS

UPL has to be precautious on deciding about prices and satisfying customers to avoid of switching customers

COMPETITIVE RIVALARY

• Large num of competitors P & G

• Substitute products and low prices of competitors

• UPL have capacity of mass production

THREAT OF SUBSTITUTE

• Should focus on R & D to avoid substitute products

• Substitutes has reduced brand loyalty

THREAT OF NEW ENTRANT

• In pak less legal requirements and capital is required

• ULP’s brand image is a strong barrier

SUPPLIERS BARGAINING POWER

• ULP has policy of local buying and local manufacturing

• Blanket agreements with suppliers

• Built strong relations with supplier by treating them fairly

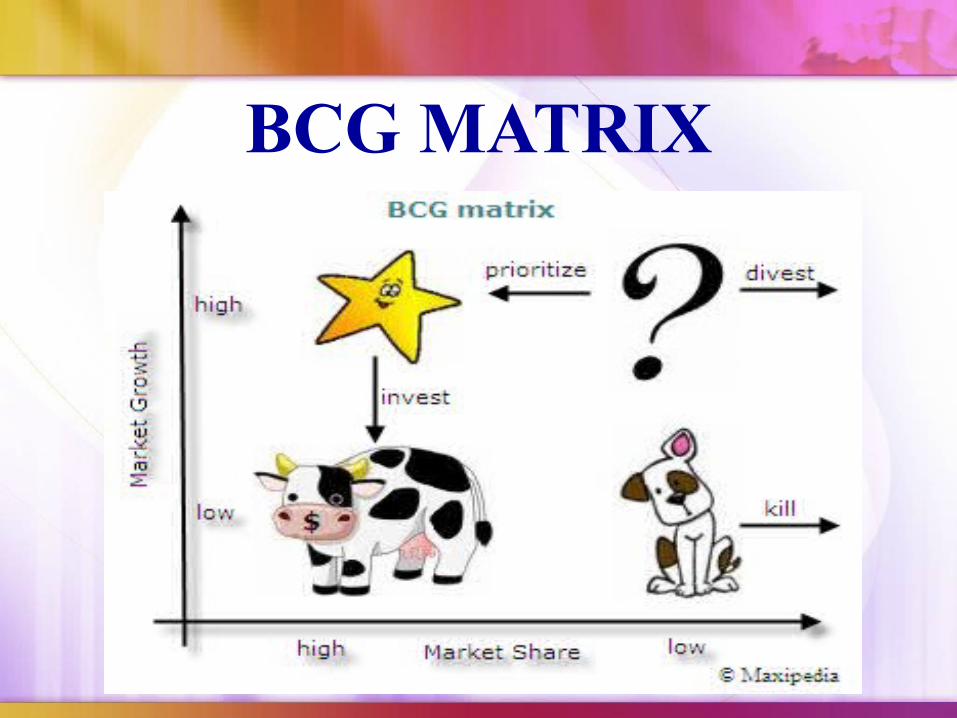

BCG MATRIX

BCG MATRIX

STARS PRODUCTS OF ULP

High growth rate & high market share

Walls

Lux

Surf excel

Fair and lovely

CASH COWS

Low growth rate & high market share

• Sunsilk• Ponds• Lipton• Blue band

DOGS

Low growth rate & low market share

• Rexona

• Lifebuoy shampoo

QUESTION MARKS

High growth rate & low market share

• Lifebuoy soap• Clear shampoo

BRAND LIFE CYCLE

INTRODUCTION• Domex

GROWTH• Lux• Sunsilk• Clear shampoo

MATURITY• Surf excel• Ponds• Lipton

DECLINE• rexona

VALUE CHAIN ANALYSIS

Focusing on cost leadership in shampoo markets

Firms infrastructure

• Knowledgeable experts

• Effective management information system

• Marketing research department shares consumer research data

Human resource management

• Skilled, qualified and expert management

• Formal and informal network communications

• Training programs and seminars

Technological development

• R&D brought improvement in shampoos

procurement

• Outsource raw materialEurope, America, far east and local

availability

• Automatic replenishment systems

• Packaging material from packages limited Lahore

operations

• Have got economies of scale to reduce unit cost

• Production process of sunsilk and lifebuoy is reliable

distribution

• Shipped to 6 depots via truck

• Transportation cost is beard by whole sellers

Relationship and marketing

• Incase of lifebuoy focus only on males and ignore female

• Incase of shampoo main focus is on females

• No strategy to make good relationships with retailers

• One thing they lag’s in is centralized long term strategies

STRATEGIES

MARKET PENTRATION

• Clear shampoo

• Badami

• Vim

• Walls

Bill boards, launching new advertisements

• Surf excel

ad campaign (daag to achay hote hain)

• Lifebuoy

Hand washing campaign

MARKET DEVELOPMENT

• Vaseline

Old product but working on its development

• Sunsilk

Exploit the religious Semitism of Muslim women (hijabi women's)

PRODUCT DEVELOPMENT

• Domex

launched against harpic

• Fair menz

A new product for men fairness

FORWARD AND BACKWARD INTEGRATION

ULP has never indulged in backward and forward integration

HORIZONTAL INTEGRATION• Polka (1998)

• Knorr (2000)

• Lipton (1988)

• Brokebond (1997)

• Glaxose-D (1999)

DEFENSIVE STRATEGY

• Increase scale of economy to reduce unit cost

RETRECHMENT STRATEGY

• In 2007 292 contract employees were fired

CONTINUES IMPROVEMENT

• 41% reduction in CO2

• 65% reduction in water use

• 73% reduction in total waste

STRATEGIC TYPE

• Unilever is a prospector with fairly broad product line and focuses on

InnovationMarket opportunities

Determining the sustainability

• There is a huge chance of imitability in FMCG’s

THE END…!!

ANY DOUBTS OR QUESTIONS???

THANK YOU!!!