Undertanding the global rivalry between OPEC and IEA · Understanding the global rivalry between...

16

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 1 A Note by Puguh Bodro Irawan (Vienna-Austria, 18.04. 2012) Undertanding the global rivalry between OPEC and IEA Oil production management vs. Strategic petroleum reserves arrangements By Puguh Bodro Irawan 1 [email protected] OPEC versus IEA: a bitter, but complementary rivalry Organization of the Petroleum Exporting Countries (OPEC) and International Energy Agency (IEA) are two international energy organizations which might be connoted as a double-sided coin. Two faces, but two different appearances. Likewise, both have different backgrounds and objectives of their establishments, frequently opposite each other. But both need each other. Their energy interests are complementary each to other. In a simple way, OPEC is the seller and IEA is the buyer of crude oil. OPEC is committed to sell its crude oil with the price as high as possible, as an effort to optimalize the revenues of its member countries. On the contrary, IEA intends to buy the crude oil as cheapest as possible from the market, in order to minimalize the costs of production inputs in refining the crude oil into petroleum products, such as gasoline, diesel, and jet kerosene. OPEC is an association of the world’s main oil producing and exporting countries. All of its members are categorized as developing, less-industrial countries. Whereas IEA identifies itself as a representative of the world’s main oil consuming countries. All of IEA member countries are also the members of Organization for Economic Co-operation and Development – OECD, or most developed industrial countries. Both the Secretariats of OPEC and IEA in principle serve as advisory. They are think-tank agencies, providing recommendations and advice to their member countries on strategic issues related to oil and energy policies. Their day-to-day 1 Author is an analyst specializing on socio-economic and public policy related issues (labour force, poverty & inequality, human development economics, energy/oil market analysis), and presently lives in Vienna, Austria. This article is purely the author’s independent opinion. E-mail: [email protected]

Transcript of Undertanding the global rivalry between OPEC and IEA · Understanding the global rivalry between...

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 1

A Note by Puguh Bodro Irawan (Vienna-Austria, 18.04. 2012)

Undertanding the global rivalry between OPEC and IEA Oil production management vs. Strategic petroleum reserves arrangements

By Puguh Bodro Irawan1

OPEC versus IEA: a bitter, but complementary rivalry

Organization of the Petroleum Exporting Countries (OPEC) and

International Energy Agency (IEA) are two international energy organizations

which might be connoted as a double-sided coin. Two faces, but two different

appearances. Likewise, both have different backgrounds and objectives of their

establishments, frequently opposite each other. But both need each other. Their

energy interests are complementary each to other. In a simple way, OPEC is the

seller and IEA is the buyer of crude oil. OPEC is committed to sell its crude oil

with the price as high as possible, as an effort to optimalize the revenues of its

member countries. On the contrary, IEA intends to buy the crude oil as cheapest

as possible from the market, in order to minimalize the costs of production inputs

in refining the crude oil into petroleum products, such as gasoline, diesel, and jet

kerosene.

OPEC is an association of the world’s main oil producing and exporting

countries. All of its members are categorized as developing, less-industrial

countries. Whereas IEA identifies itself as a representative of the world’s main oil

consuming countries. All of IEA member countries are also the members of

Organization for Economic Co-operation and Development – OECD, or most

developed industrial countries.

Both the Secretariats of OPEC and IEA in principle serve as advisory. They

are think-tank agencies, providing recommendations and advice to their member

countries on strategic issues related to oil and energy policies. Their day-to-day

1 Author is an analyst specializing on socio-economic and public policy related issues (labour force, poverty &

inequality, human development economics, energy/oil market analysis), and presently lives in Vienna, Austria. This article is purely the author’s independent opinion. E-mail: [email protected]

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 2

activities are to carry out research, analyses, and monitoring over the latest

development of the world oil and energy markets. The outcomes of these analyses

are regularly published in their oil market reports and oil/energy outlooks –

reflecting the voices of their standpoints on a range of the world critical oil and

energy issues. These analyses are then used as a basis of informed decision

makings by both agencies for the interests of their member states.

OPEC, with its secretariat headquarter in Vienna – Austria, has a main

objective to coordinate the strategy of its 12 members in managing their oil

production. Member Countries of OPEC are Algeria, Angola, Ecuador, Iran, Iraq,

Kuwait, Libya, Nigeria, Qatar, Saudi Arabia, United Arab Emirates and

Venezuela.2 OPEC was established on the 14th of September 1960 in Baghdad –

Iraq, with its headquarter initially in Geneva – Switzerland, before it moved to

Vienna in 1962.3

OPEC was established as a co-operation between major oil producing

countries in response to the hegemony of the Seven Sisters of international oil

majors for decades prior to 1960 which exclusively controlled the prices of crude

oil.4 Its establishment was clearly intended as a kind of protesting against these

Seven Sisters which had been exploiting their natural resources for long time.

The growing nationalism spirit among developing countries seemed to reach its

height in the early 1960s.

The Seven Sisters at that time were in a full control over all accesses to oil

industry in OPEC member countries, including information on oil reserves sites,

exploration and production technologies, distribution and sale of crude oil. And

even the most critical one was that these companies were in charge of

determining the selling price of crude oil to the market. Since the creation of

OPEC, its members started to nasionalize the international oil companies in their

countries, and collectively manage their own oil production, including the selling

prices to the world market.

IEA is an autonomous organization of most advanced industrial countries

with the headquarter located in Paris, France. IEA was created within the

2 Indonesia was a member of OPEC during 1962-2008, and Gabon during 1975-1994.

3 The founding countries of OPEC in 1960 were Saudi Arabia, Venezuela, Iraq, Iran and Kuwait.

4 The Seven Sisters of international oil majors consisted of Standard Oil of New Jersey & Standard Oil Company of

New York (now known as ExxonMobil), Standard Oil of California (now Chevron), Gulf Oil (taken over by Chevron in 1985), Texaco, Royal Dutch Shell and Anglo-Persian Oil Company (now British Petroleum-BP).

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 3

framework of OECD in 1974, in reaction to the oil crisis in 1973 when OAPEC 5

launched an embargo over the selling of their crude oil to the world as a protest

against the USA’s decision for supporting Israel in the Yon Kipur war. IEA has a

main mission to consolidate a collective strategy for its 28 member states in

securing their energy needs in a sustainable and effective way.6 IEA’s mission

therefore focuses on the need for sustainable oil and energy supply security. This

is certainly in contrast with OPEC’s mission which emphasizes on the need for

sustainable oil demand security – a guarantee that there are markets or buyers

for their oil.

IEA was initially established to help its member states overcome physical

disruptions of oil supply for their regular energy domestic needs. Oil supply

disruptions occur when there are any security problems in major oil

producing/supplying regions, such as in Middle East and Northern African

(MENA) region. IEA is also responsible for providing its members information

and data pertaining to the latest dynamics of the world oil and energy markets.

IEA plays a role as a policy advisor to its members on energy-related issues, and

maintains intensive co-operations with non-members, including Russia, China

and India.

At the present time, the main policy portfolios of IEA focus on the so-called

4Es, namely energy security, environmental protections, economic development,

and engagement worldwide in and for all 28 members. The second E –

environmental protection emphasizes on a strategy of mitigating the climate

change. In recent years, IEA aggressively promotes the radical need for

developing renewable energy sources. The Agency also frequently campaigns

about the need for rational energy policies, such as the abolishment subsidies of

energy prices, intensifying international co-operations for developing energy-

efficient technologies.

One of the most important policy interventions of IEA is its direction for

obligatorily requiring its member states to storing the domestic oil stocks at least

90 days of the last year averaged net oil imports. The logical argument is that

5 Members of the Organization of Arab Petroleum Exporting Countries – OAPEC are all OPEC member Arabic

countries (Algeria, Arab Saudi, Irak, Kuwait, Libya, Qatar dan UAE), plus Bahrain, Egypt, Syria and Tunisia. http://www.oapecorg.org/ 6 Members of IEA are Australia, Austria, Belgium, Canada, Czech Republic, Denmark, Finland, France, Germany,

Greece, Hungary, Ireland, Italy, Japan, Republic of Korea, Luxembourg, The Netherlands, New Zealand, Norway, Poland, Portugal, Slovak Republic, Spain, Sweden, Switzerland, Turkey, United Kingdom, and United Sattes. Chile, Estonia, Iceland, Israel, Mexico and Slovenia are members of OECD, but not IEA at the moment. http://www.iea.org/country/index.asp

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 4

adequate oil stocks, both for strategic reserves and for commercial/industria

regular needs, is the IEA’s main safeguard to counter-balance any oil supply

disruptions that might potentially occur in the future, either due to geopolitical

and security reasons in major oil supplying regions, or direct interventions by

main oil producing countries – especially OPEC in adjusting its production

targets as efforts to influence the world oil markets.

Crude Oil Production Management: Main mandate of OPEC

The main mission of OPEC to coordinate and unify the oil related policies

of its Member Countries. It is also to ensure the stabilization of oil markets in

securing an efficient, economic and regular supply of petroleum to consumers, a

steady income to producers and a fair return on capital for those investing in the

petroleum industry.7 As developing countries, the economy of all OPEC members

heavily relies on the revenues from the sales of crude oil to the world market.

Because of this oil dependency, OPEC is commited to collectively strive

in achieving a stable world oil market with a fair price. It is a price of crude oil

which is reasonably profitable for oil producers and investors, and the level of

price which is still sensibly conducive for the economies of consuming countries,

especially OECD countries.

It is evident that oil price volatility deteriorates the performance of

macro-economic indicators in many countries around the world. These include

the slowdown in the world economic growth, mounting inflation pressures, and

pushing the uncertainties of the overall economic condition which all in all

dampens investments in the oil industry. A tight oil market commonly causes a

fear over the scarcity of oil supply, leading to the concern towards the overall

prospect of the world’s energy security.

The oil price volatility directly affects the amount of oil demand from major

oil consumers of OECD to major oil producers, both OPEC and non-OPEC. Drops

in oil production for OPEC members mean declines in the revenues generated

from the exports of crude oil. This is certainly not expected by OPEC members

which all heavily depend on crude oil exports revenues to finance their countries’

development.

7 http://www.opec.org/opec_web/static_files_project/media/downloads/publications/OS.pdf

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 5

In order to stabilize the world oil market, the market does not only need an

efficient oil supply security from major producing countries (i.e. OPEC), but

it also requires a steady oil demand security from main consuming countries

(i.e. OECD). The main bargaining power of OPEC is its abundant oil reserves,

estimating at 1.2 trillion barrel, or 81% of the world total oil reserves (1.5 trillion

barrel). More crucially, OPEC member countries collectively have a great

flexibility in ‘managing’ (by increasing or reducing) the supply of its crude oil to

the world market, with a production level in 2010 averaging at 29.2 million barrel

per day (mb/d), or almost 42% of the world total production (69.7 mb/d).8

This current production level could be very comfortably increased, given

the sustainable crude oil production capacity of OPEC member countries

at present being estimated at around 34.2 mb/d. It means that OPEC has a crude

oil production spare capacity at approximately 5 mb/d, which is readily

produced to supply the market within a reasonably short period of time.9

OPEC’s strategy understandably focuses on the oil production

management of its member countries, with the aims at stabilizing the oil

market (prices) and at the same time safeguarding its interest in maintaining

stable, favourable revenues from the exports of its member’s crude oil.

There are at least two scenarios likely taking place in OPEC’s oil production

management, namely:

If the crude oil prices tend to decline sharply within a short period of

time, which is normally influenced by drastic slowdown in oil demand and

rapid increases in major OECD’s oil stocks, OPEC in its regular Meetings of

Ministerial Conferences would be more likely to decide crude oil

production cuts from all its members.

On the contrary, if the oi prices tend to increase significantly and

rapidly, which is commonly preceded by oil supply disruptions due to

geo-political, security factors or major maintainance, continued strong rise

in oil demand, drops or withdrawals in OECD oil stocks, OPEC is likely to

take on a decision for crude oil production increases.

Such a strategy of oil production management is intended as an effort for

stabilizing the world oil market balance – between supply and demand. The

8 OPEC (2011) ‘Annual Statistical Bulletin 2010/2011 Edition”.

9 Sustainable crude oil production capacity is defined as a maximum level of daily crude oil production which shall

be attained within 30 days, and the level can be sustained at least during 90 days.

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 6

volume of crude oil production cuts or increases as decided by the OPEC

Conferences is usually allocated to each member on proportional basis from its

production level at that time as compared to the OPEC total production. The final

distribution of oil production to all 12 current members of OPEC is often called as

production quota or allocation.

Both scenarios: “price decline » production cut” dan “price increase

» production increase” seems to result in straight and predictable decisions,

as being closely monitored by oil market analysts, media, and concerned policy

makers. Even more if both conditions are clearly followed by a steady increase in

oil demand and well adequate oil stocks (commercial and public) in major OECD

countries.

However, in some cases, both scenarios could be not valid. For example,

crude oil prices increase, but OECD oil stocks remain well adequate. Likewise, the

world oil demand also tends to be stagnant, yet the prices continue to rise. Or the

world oil market is not stable due to uncertainties in the world economic

conditions, or due to geo-political factors, i.e. security-driven disruptions in oil

supply.

Therefore, when the overall world oil market is uncertain, OPEC is

most likely to decide to maintain its production level at that time.

It is understood that the OPEC’s decision making in reducing or increasing

its oil production is very likely based on the analysis of the world oil market by

closely monitoring the trends of oil prices and patterns of oil supply-demand

balance. Analysis of supply-demand balance from OPEC’s perspective, as

regularly reported in its flagship publication of Monthly Oil Market Report, can

be used as a basis for estimating the volume of deficit or surplus in the available

world oil supply.

This estimated deficit or surplus, or simply called as balance, in supply-

demand analysis is the outcome of comparing between: (1) world oil demand, (2)

total supply excluding OPEC crude, (3) difference (1) – (2) as ‘call on OPEC’,10

and (4) OPEC crude oil production. The difference between (4) and (3) is the

balance, showing a deficit (sign ) or a surplus (sign +).

10

‘Call on OPEC’ is simply calculated as the difference between the world oil demand and total supply excluding OPEC crude, indicating the total volume of crude oil by which OPEC is expected to supply in order to stabilize the supply-demand balance or the world oil market.

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 7

Component (2) ‘total supply excluding OPEC crude’ is very crucial in

the analysis of the world oil supply-demand balance, thus the dynamics of this

component is always closely monitored by oil market analysts. Component (2)

consists of two sources, namely ‘non-OPEC supply’ (mostly from Former Soviet

Unions – FSU including Russia, Kazakhstan, Azerbaijan, Norway, UK, USA,

Mexico, Brazil, Canada, Indonesia, etc) and ‘OPEC NGLs & non-conventionals’.

Table 1 illustrates an analysis of the world oil supply-demand balance as

published by OPEC. This supply-demand balance analysis is believed being used

as a basis for the well recognized decision by the OPEC Ministerial Conference to

cut the crude oil production level of all OPEC members by 4.2 mb/d in its

meeting in December 2008.11

Table 1. Supply-Demand Balance from OPEC’s Perspective, December 2008 (Estimation of 2008 & Forecast of 2009, in million barrels per day)

2007 1Q08 2Q08 3Q08 4Q08 2008 1Q09 2Q09 3Q09 4Q09 2009

(1) World oil demand 85.9 86.7 85.4 85.0 86.3 85.8 85.9 85.0 85.1 86.8 85.7

(2) Total supply excluding OPEC crude

53.7

54.2

54.5

53.4

54.7

54.2

55.7

55.3

55.2

55.7

55.5

Non-OPEC supply 49.5 49.7 49.9 48.8 49.9 49.6 50.7 50.2 49.8 50.2 50.2

OPEC NGLs &

non-conventionals

4.1 4.4 4.6 4.6 4.8 4.6 5.0 5.1 5.3 5.4 5.2

(3) Difference (1) – (2) ‘Call on OPEC’

32.2 32.5 30.9 31.5 31.6 31.6 30.2 29.7 29.9 31.1 30.2

(4) OPEC crude oil production 29.9 32.1 32.1 32.3 (5) Balance -1.3 -0.4 1.2 0.8

Source: OPEC Monthly Oil Market Report, December 2008, Table 32 & 33 (p. 58).

First, Table 1 suggests that the 2008 supply-demand balance indicates a

slowdown in the world oil market fundamentals. Between 2007 and 2008, while

the world oil demand tended to be unchanged, total supply excluding OPEC

crude increased by 0.5 mb/d from 53.7 to 54.2 mb/d. The increase was largely

attributed to a rise in OPEC NGLs & non-conventionals. As a consequence, ‘call

on OPEC’ in 2008 was estimated at 31.6 mb/d, or a drop by 0.6 mb/d from the

2007 level. More interestingly, analysis on quarterly basis in 2008 shows that

‘call on OPEC’ in Q-1 was larger than OPEC reported crude oil production that

is 32.5 as compared to 32.1 mb/d, indicating a deficit of (minus) 0.4 mb/d. In Q- 11

Decision to cut the production by 4.2 mb/d from the September 2008 level of 29.045 mb/d to 24.845 mb/d was announced in Press Release of the 151

st (Extraordinary) Meeting of the OPEC Conference, 17 December 2008, Oran,

Algeria. http://www.opec.org/opec_web/en/945.htm

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 8

2, however, the balance experienced a surplus of (plus) 1.2 mb/d, as a result of

larger OPEC reported production than ‘call on OPEC’. Likewise, the balance in Q-

3 also experienced a surplus of 0.8 mb/d. The surplus was expected to

materialize again in Q-4, 2008.

The 2009 prospect also has a tendency for a surplus balance, given the

world oil demand being relatively stable, while total supply excluding OPEC

crude – notably non-OPEC supply continued to increase. If this situation is

untouched, surplus balance would cause the world oil supply in excess, leading to

a pressure on oil prices. Such an oil market condition with continued drops in oil

prices is certainly not expected by major oil producing countries, including

OPEC, and also oil investors. Based on such a supply-demand analysis, OPEC

decided to cut its members’ crude oil production level by 4.2 mb/d, from 29.045

mb/d (2008 September data is a basis) to 24.845 mb/d. Iraq was excluded in this

production cut.

The extent to what implications of this OPEC’s decision for production cut

by 4.2 mb/d for helping stabilize the oil prices afterwards is interesting to

observe. As an association of major oil producing countries, if not to say as a

cartel of most important commodity assets in the world, is OPEC still effective in

‘regulating’ the world oil market? Analysis of oil prices trends indicate that the oil

prices tended to increase since the OPEC Conference’ decision was taken in

December 2008.

Graph 1 report that the averaged price of crude Brent in December 2008

was at around US$40/barrel. This level then increased to $44 in January 2009,

$50 in April 2009, and it reached $70/barrel at the end of 2009. Although the

realization of the agreed production cut, or often called as ‘compliance’, only

reached around 75% or less (of total cut 4.2 mb/d), such a decision was

acknowledged by many oil market pundits that OPEC’s strategy seems to remain

fairly effective in managing its members’ production for influencing the world oil

markets.

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 9

Source: http://www.opec.org/opec_web/en/data_graphs/40.htm.

The effectiveness of OPEC’s strategy in directing its members’ oil

production is also currently under a close scrutiny by oil market community in

the world. It is especially in responding to stubbornly high oil prices in the range

of above $100/barrel since February 2011 up to NOW (March 2012). During the

most recent OPEC Ministerial Conference meeting in 14 December 2011,12 the

Conference decided to maintain OPEC’s production level at that time at 30 mb/d,

upon the outcomes of analysis of the latest world oil market trends, especially

from the outlook in 2012.

According to the OPEC Conference in its press statement, oil prices

volatility witnessed during 2011 was largely driven by the growing practices of

commodity market speculations, aggravated by geo-political factors (Middle East

and North Africa), rather than being related to the dynamics of oil market

fundamentals. Downrisks in the overall world economy was partly taken into

account, including Eurozone debt crisis, continued high unemployment rates in

12

The 160th

OPEC Ministerial Conference meeting was held in Vienna, Austria, on 14 December 2011.

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 10

some OECD countries, as well as inflation risks in emerging economies. Budget-

tightening policies recently adopted in Eurozone and other OECD countries were

likely to adversely affect these countries’ economic growth in the near future.

Although the world oil demand was forecasted to increase during 2012, the

increase would be compensated by the anticipated increase in non-OPEC supply.

Hence, following this argument over the uncertainties in the world oil demand,

the Conference decided to keep the OPEC current production level in December

2011 unchanged.

It can be argued that OPEC’s decision to keep its production unchanged

implicitly suggests OPEC’s acceptance with the current level of oil prices ranging

around US$110/barrel. When the Conference took place in 14 December 2011,

the monthly averaged price of Brent in November 2011 was $111/barrel. This

level dropped slightly to $108 in December 2011, but then increased to $111 in

January 2012, $115 in February 2012 and continued to sharply increase to

$125/barrel in March 2012. To what extent the relationship between OPEC’s

decision to maintain its current production and oil prices in the coming six

months prior to the next Conference in June 2012 would be certainly interesting

to verify the effectiveness of its decision in directing the world oil markets (read:

oil prices).

Oil Stocks: IEA’s Main Bargaining Power

The main mission of IEA is very much related to a mechanism to tackle any

emergency conditions concerning with major disruptions of energy (mostly oil)

supplies in its 28 state members. IEA is also responsible for carrying out analyses

of the world energy markets as a basis for providing strategic policy

recommendations and advocacies to its members, as well as promoting the

development of low carbon and energy-efficient technologies. Its function in

tackling the disruption of energy/oil supplies is very crucial for the existence of

IEA. In implementing this function, all state members are required to maintain a

minimum oil stockholding obligation, at least covering 90 daily oil net imports. 13

13

Just an example, the total averaged imports of crude oil and petroleum products for USA was 11.2 mb/d in 2011. With the total averaged exports at 2.4 mb/d ( http://www.eia.gov ), USA had net oil imports = 11.2 – 2.4 mb/d = 8.8 mb/d in 2011. By 2012, USA is thus theoretically obliged to hold minimum oil stocks, amounting = 90 days X 8.8 mb/d = 792 million barrel. Based on the latest data published by the US Energy Information Administration (EIA), the strategic petroleum reserves (SPR) of USA in the beginning of 2012 was 1.756 billion barrel, consisting of 696 million barrel of the government-controlled SPR and 1.060 billion barrel of commercial/industry stocks. From a different perspective: USA oil consumption is estimated at 18.5 mb/d in 2012 (slightly down from 19 mb/d in 2011),

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 11

Only 3 of 28 state members, namely Canada, Denmark and Norway, do not

necessarily follow this obligation as these countries are net oil exporters.

At present time, the total SPR of OECD is estimated at 4.2 billion

barrel, comprising 1.5 billion barrel of the government-controlled SPR (public

stocks) and 2.7 billion barrel of privately controlled commercial/industry oil

stocks.14 1.8 billion barrel alone, or around 43% of the OECD total SPR, belongs

to the USA.

Based on the author’s own rough estimation, the total SPR in non-OECD

countries is estimated at around 3.4 billion barrel in the end of 2011. The biggest

holders of non-OECD SPR are China (470 million barrel), Saudi Arabia (315

million barrel) and Russia (276 million barrel). Some ASEAN countries also have

SPR, for example, Thailand (40 million barrel), Indonesia (38 million barrel),

Singapore (24 million barrel), The Philippines (12 million barrel). With the oil

consumption at around 1.1 mb/d, Indonesian SPR would be only covering around

35 days if an emergency condition takes place in the country.

Back to the discussion about SPR of OECD countries, which are mostly also

members of IEA, the holding of adequate SPR allows the IEA countries

collectively manage their oil stocks as deemed extremely necessary at the time of

regular oil supplies being badly disrupted. During the normal time, which is

often coupled with relative cheap oil prices, IEA/OECD countries are most

likely to take on oil stocks build. On the other hand when the oil supply from

major oil producing countries experiences chronic disruptions due to war or

other security reasons, which is sometime followed by significant increases in

oil prices, IEA could anticipate taking on oil stocks withdrawal, releasing

some of their members’ SPR to help stabilize the oil markets.

IEA’s interventions in both oil stocks build and withdrawal are the key

strategy in ‘directing’ the world oil markets. It is indeed a mechanism of counter-

response to any disruptions or interventions affecting the oil supply from the side

of oil producing countries, notably OPEC member countries. IEA’s interventions

are understandably intended for the optimal interest of its members, in securing

the sustainable supplies of large amount of energy/oil needed to support the daily

economic activities, including for manufacturing industries, transportation,

heating, household energy needs, and military purposes.

thus the oil stocks at 1.757 billion barrel in a emergency condition could cover approximately 95 daily oil consumption (1.757 billion divided by 18.5 million). 14

http://www.eia.gov/emeu/ipsr/appa.html.

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 12

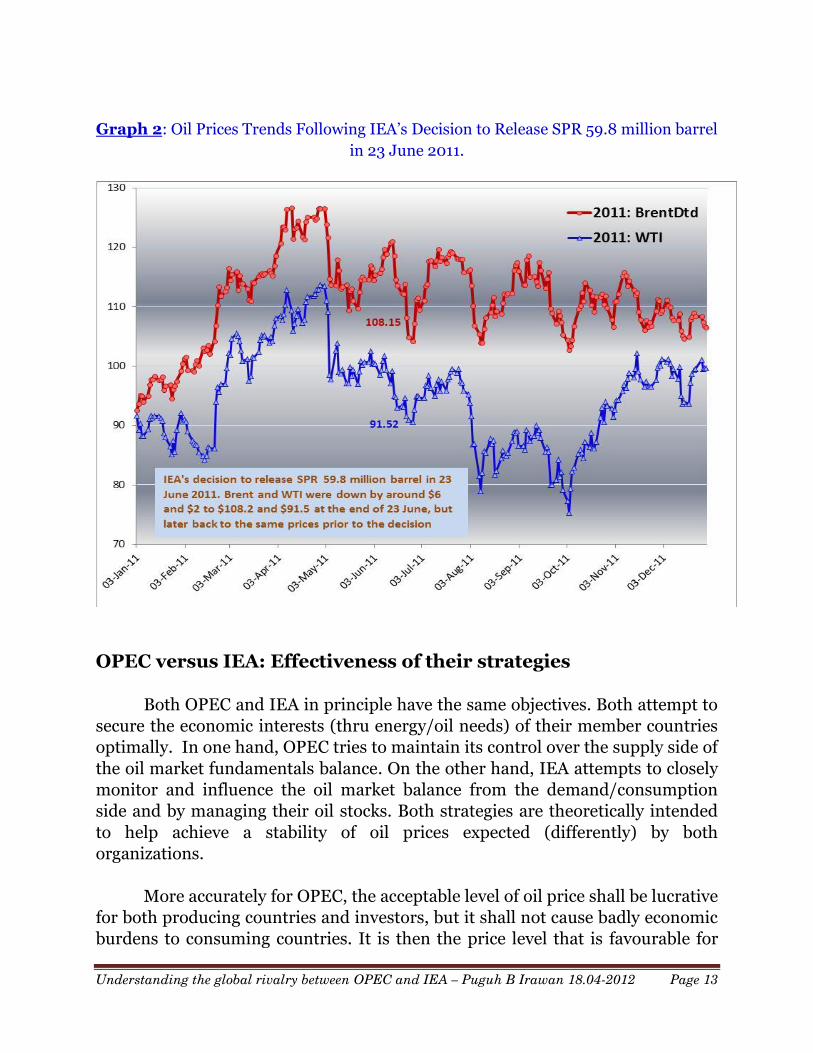

The most recent SPR-related intervention took place in 23 June 2011 when

IEA released 59.8 million barrel from its member’s SPR for the duration of one

month. 40 million barrel of this amount came from public stocks, and the

remaining was from commercial/industry oil stocks. The United States alone was

expected to release 30.6 million barrel of light sweet crude from its SPR through

auction. OECD Pacific and European countries released 6 and 3.6 million barrel

of crude oil, and 5.4 and 14.3 million barrel of petroleum products respectively.

IEA’s decision to release its members’ SPR was believed as an attempt to

tackle oil supply disruptions from Libya, coupled with OPEC’s failure to agree to

increase its members’ crude oil production during the Conference in 8 June 2011.

And at the same time, IEA’s intervention was also driven by the concern over the

condition of the world economic recovery at that time. This intervention was the

third time ever since the establishment of IEA.

The first one was in 1991 as a response to Iraqi attack to Kuwait, by which

the world oil supply lost 4.3 mb/d from both countries’ crude oil production at

that time. IEA in January 1991 decided to release 21 million barrel from its

members’ oil inventories. The second intervention was made in 2005 as an

anticipation of the impacts of Katrina and Rita hurricanes in the Gulf of Mexico.

At that time, IEA used 60 million barrel from its members’ SPR, coupled with

policies for increasing their own crude oil production and reductions in oil

demand.

Both previous interventions were taken immediately when the supply

disruption occurred. Whereas the IEA’s latest intervention in June 2011 was

decided more than three months after the disruption in Libya took place. This

latest decision was obviously intended for merely driving the market sentiment

toward the oil prices. It was not to balance the loss or deficit in the world oil

supply. The decision seemed to be political in nature, for diverting the US public

anger due to the skyrocketing price of gasoline reaching almost US$4 per gallon.

Is there any concrete impact of IEA’s decision to release its members’ SPR

on the worl oil market, as indicated by oil prices? Just after the decision was

announced in 23 June 2011, the prices of Brent and WTI crudes dropped by

around $6 and $2 respectively from the previous day to $108.2 and $91.5/barrel

at the end of 23 June. The prices went down slightly for the coming few days. And

less than two weeks later, the prices were back to the same level prior to the IEA’s

decision at $108/barrel. (See Graph 2 below)

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 13

Graph 2: Oil Prices Trends Following IEA’s Decision to Release SPR 59.8 million barrel

in 23 June 2011.

OPEC versus IEA: Effectiveness of their strategies

Both OPEC and IEA in principle have the same objectives. Both attempt to

secure the economic interests (thru energy/oil needs) of their member countries

optimally. In one hand, OPEC tries to maintain its control over the supply side of

the oil market fundamentals balance. On the other hand, IEA attempts to closely

monitor and influence the oil market balance from the demand/consumption

side and by managing their oil stocks. Both strategies are theoretically intended

to help achieve a stability of oil prices expected (differently) by both

organizations.

More accurately for OPEC, the acceptable level of oil price shall be lucrative

for both producing countries and investors, but it shall not cause badly economic

burdens to consuming countries. It is then the price level that is favourable for

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 14

the increases in revenues from oil sales for producing countries and oil investors.

But it is also the price level that is acceptable by the world oil market, as

specifically indicated by the continued demand from OECD countries the oil from

producing countries, including OPEC.

The synergy between the oil price and the world oil demand is closely

monitored by both OPEC and IEA. Their main concern is how to ensure that the

movements and levels of oil prices shall not be detrimental towards the world

economic growth. Volatile fluctuations in the oil prices negatively affect the world

economy, which in turn causes the slowdown in the world oil demand, directly

bringing down the oil supply – crude oil production from countries like OPEC,

and thus drops in revenues from the oil sales.

It is commonly believed that the oil price at around US$75/barrel could be

assumed as reasonably profitable for most OPEC countries, and also for other oil

producers. Therefore, the current oil prices which stubbornly range around $110

– $120/barrel are understandably regarded as rather too expensive. However, it

might be argued that as the world oil supply-demand in 2011 and 2012 outlook is

expected to be relatively balanced,15 thus the current oil price level seems to be

absorbed by the market.

Hence, the latest OPEC Ministerial Conference in December 2011 decided

to maintain the oil production level at that time 30 mb/d unchanged. This

decision has been effectively implemented since January 2012. This latest

OPEC’s decision will take time to give impacts in favourably driving the oil

market sentiment, whether the oil prices would remain stable or fluctuating with

some volatility. It is also interesting to know later on if with this latest decision

OPEC could repeat its success enjoyed in its previous Conference’ decision of

production cut 4.2 mb/d in December 2008 which was viewed as an effective

strategy in driving the oil prices as expected by that time.

15

Based on the latest OPEC Monthly Oil Market Report, April 2012), the world oil demand in 2011 was estimated at 87.8 mb/d, and the global oil supply at 87.5 mb/d with OPEC production at around 29.8 mb/d. It means there was a balance of minus (deficit) 300 tb/d which is perceived as ‘balanced’. The 2012 Outlook 2012 in this report indicates that the world oil demand in 2012 is projected to increase by 860 tb/d from 2011 to reach 88.64 mb/d. With the total supply excluding OPEC crude at 58.62 mb/d, the call on OPEC (demand for OPEC crude) for 2012 is estimated at 30.01 mb/d. However, the actual OPEC crude oil production during the first quarter 2012 has reached an average of 31.11 mb/d, or 1.11 mb/d higher than the OPEC Conference’ target of 30 mb/d. Thus, if the OPEC current production level of 31.1 mb/d remains to be maintained during the coming three quarters of 2012, the world oil market balance would experience a surplus, a situation that expects to put pressure down on the oil prices.

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 15

The level of oil prices at that time increased by around 75% from the end of

2008 to the end of 2009. Brent crude, for instance, rose sharply from

US$40/barrel in December 2008 to $74/barrel in December 2009. Apart from

the fact that not all member countries of OPEC obeyed over the targeted

production cuts allocated for each of them – with the compliance level at around

60-70% of the total cut 4.2 mb/d, the decision at that time definitely gave a

positive sentiment toward the world oil market. In addition, the overall condition

of the world oil market in 2009 also supported the increases in oil prices. At that

time, the world oil market was as a matter of fact relatively ‘imbalanced’, with a

deficit at 500 tb/d.16

In short, the effectiveness of OPEC’s oil production management strategy

in influencing the world oil market (oil prices) largely depends on the overall

condition of the world oil supply-demand balance. The total amount of oil

production cut or increase by OPEC and the compliance level of each member

countries in implementing their production target would be obviously a key

factor in determining the effectiveness of OPEC policies in controlling the

supply/production of its members’ oil production.

How about with IEA? From the previous discussion, IEA’s decision in

releasing its members’ SPR on 23 June 2011 was proven to have created the

sentiment of the oil market only on temporary, short period of time. In other

words, the latest IEA’s strategy was not quite effective in influencing the world oil

market.

First, the total amount of SPR being released was in fact not too significant

– that was only 59.8 million barrel during a month. This amount certainly did not

help relieve the overall world oil market at that time, when it was compared to

the total world oil market at 87.8 million barrel per day in 2011. Around 46 mb/d

of this total world oil demand alone, or approximately 52%, was for the own

consumption of OECD countries.17 Second, the influence of the oil market

fundamentals (supply, demand and stocks) on the dynamics of the worl oil

market has been recently weakening, in line with the strengthening determinant

of non-fundamental factors – notably commodity market speculative practices, in

driving the oil prices.

16

This was based on the world oil demand at 84.7 mb/d and the global supply at 84.2 mb/d, while the OPEC crude oil production averaged at 31.3 mb.d in 2009 (which was lower than the 2008 production at 28.8 mb/d). Thus, there was in fact a big drop in the global supply in 2009 by around 2.5 mb/d. 17

OPEC, Monthly Oil Market Report, January 2012.

Understanding the global rivalry between OPEC and IEA – Puguh B Irawan 18.04-2012 Page 16

Non-fundamental factors in influencing the world oil market is quite

interesting to further discuss in detail and carefully. Such an analysis is expected

to give a more comprehensive understanding and useful mechanism of early

warning in anticipating the dynamics of oil and energy markets in the future,

notably with regard to avoiding excessive price volatilities which are detrimental

to the world economic health.

**********************

![A CITIZENS’ GUIDE TO ENERGY SUBSIDIES IN NIGERIA · (ieA, organization of the Petroleum exporting countries [oPec], organisation of economic co-operation and development [oecd]](https://static.fdocuments.in/doc/165x107/5f37be7995c36627ee4c1647/a-citizensa-guide-to-energy-subsidies-in-nigeria-iea-organization-of-the-petroleum.jpg)