Understanding the customer base of service providers: An ...

24

University of Central Florida University of Central Florida STARS STARS Faculty Bibliography 2000s Faculty Bibliography 1-1-2000 Understanding the customer base of service providers: An Understanding the customer base of service providers: An examination of the differences between switchers and stayers examination of the differences between switchers and stayers Jaishankar Ganesh University of Central Florida Mark J. Arnold University of Central Florida Kristy E. Reynolds University of Central Florida Find similar works at: https://stars.library.ucf.edu/facultybib2000 University of Central Florida Libraries http://library.ucf.edu This Article is brought to you for free and open access by the Faculty Bibliography at STARS. It has been accepted for inclusion in Faculty Bibliography 2000s by an authorized administrator of STARS. For more information, please contact [email protected]. Recommended Citation Recommended Citation Ganesh, Jaishankar; Arnold, Mark J.; and Reynolds, Kristy E., "Understanding the customer base of service providers: An examination of the differences between switchers and stayers" (2000). Faculty Bibliography 2000s. 7859. https://stars.library.ucf.edu/facultybib2000/7859

Transcript of Understanding the customer base of service providers: An ...

University of Central Florida University of Central Florida

STARS STARS

Faculty Bibliography 2000s Faculty Bibliography

1-1-2000

Understanding the customer base of service providers: An Understanding the customer base of service providers: An

examination of the differences between switchers and stayers examination of the differences between switchers and stayers

Jaishankar Ganesh University of Central Florida

Mark J. Arnold University of Central Florida

Kristy E. Reynolds University of Central Florida

Find similar works at: https://stars.library.ucf.edu/facultybib2000

University of Central Florida Libraries http://library.ucf.edu

This Article is brought to you for free and open access by the Faculty Bibliography at STARS. It has been accepted for

inclusion in Faculty Bibliography 2000s by an authorized administrator of STARS. For more information, please

contact [email protected].

Recommended Citation Recommended Citation Ganesh, Jaishankar; Arnold, Mark J.; and Reynolds, Kristy E., "Understanding the customer base of service providers: An examination of the differences between switchers and stayers" (2000). Faculty Bibliography 2000s. 7859. https://stars.library.ucf.edu/facultybib2000/7859

Customer Base of Service Providers / 65Journal of MarketingVol. 64 (July 2000), 65–87

Jaishankar Ganesh, Mark J. Arnold, & Kristy E. Reynolds

Understanding the Customer Base ofService Providers: An Examination

of the Differences BetweenSwitchers and Stayers

Creating and maintaining customer loyalty has become a strategic mandate in today’s service markets. Recentresearch suggests that customers differ in their value to a firm, and therefore customer retention and loyalty-build-ing efforts should not necessarily be targeted to all customers of a firm. Given these sentiments, it is becomingincreasingly necessary for firms to have a thorough understanding of their customer base. Yet current knowledgeis limited in providing insights to firms regarding the differences within their customer base. This research com-prises two studies in which the authors examine the differences among internal customer groups in a service indus-try. As theory suggests and as is empirically validated here, customers who have switched service providersbecause of dissatisfaction seem to differ significantly from other customer groups in their satisfaction and loyaltybehaviors. The findings offer some interesting implications for both marketing theory and practice.

Jaishankar Ganesh, Mark J. Arnold, and Kristy E. Reynolds are assistantprofessors, Department of Marketing, University of Central Florida. Theauthors thank the anonymous JM reviewers for their insightful commentsand constructive feedback that helped shape this article. The authorsgratefully acknowledge the financial support of the Department of Market-ing and the Office of Sponsored Research at the University of CentralFlorida. The authors thank Alicia Leuven for her assistance in data collec-tion and Ronald Michaels, Raj Echambadi, Ronald Hess, and Chris Whitefor their insightful comments and suggestions.

Over the past decade, researchers have recognizedthat customer switching behavior can have deleteri-ous effects on the profitability and viability of firms

in today’s marketplace. For example, statistics reveal thatU.S. corporations lose half their customers in five years andthat customer disloyalty at these rates stunts corporate per-formance by 25% to 50% (Reichheld and Teal 1996). How-ever, researchers have also observed that with each addi-tional year of a relationship between a company and aconsumer, the customer becomes less costly to servebecause of learning effects and decreased servicing costs.Over time, loyal customers build businesses by buyingmore, paying premium prices, and providing new referralsthrough positive word of mouth (Keaveney 1995; O’ Brienand Jones 1995; Reichheld and Kenny 1990). Given thisevidence, it is no wonder that companies are rushing toimplement retention and loyalty programs.

However, for all the anticipated benefits of customerretention and loyalty, problems have become evident insome of these efforts (Dowling and Uncles 1997). Central tothese concerns is researchers’ and practitioners’ realizationthat (1) not all customers should be targeted with retentionand loyalty efforts and (2) some of the most satisfied andloyal customers might still switch for reasons beyond thecontrol of the firm and at times even beyond the control of

the customer. Although it is encouraging to note the increas-ing awareness that not all customers are alike (Blattberg andDeighton 1996; Reichheld 1993), little is known about howand why they differ. Simply put, if important attitudinal andbehavioral differences can be identified among various cus-tomer groups, service providers can efficiently identify andtarget customers as part of a broader acquisition, valueassessment, and retention strategy. This, in essence, is thefocus of the current study.

A basic assumption of this research is that, at its mostfundamental level, a firm’s customer base can be thoughtto comprise two groups of customers: (1) customers whohave switched from other service providers (whom werefer to as “switchers”) and (2) those who have not (thefirst-time adopters whom we refer to as “stayers”). Theswitchers can be further classified into two types: dissatis-fied switchers and satisfied switchers (customers whoswitch for reasons other than dissatisfaction, e.g., job-related relocation). An understanding of how these cus-tomer groups differ in their attitude and behavior towardthe firm might provide crucial insights for designing andimplementing effective customer acquisition and retentionstrategies.

Prior research has related switching behavior/intentionsto perceptions of quality (Rust and Zahorik 1993), dissatis-faction (Crosby and Stephens 1987), and service encounterfailures (Kelley, Hoffman, and Davis 1993). However, thepredominant focus of the research addressing customerswitching behavior has been the costs to a firm because ofcustomer switching and the costs of replacing customerswho have defected (Keaveney 1995). In other words, priorresearch has focused on the “switched-from” firm and notthe “switched-to” firm. There is a dearth of research exam-ining what happens to customers after they have switched inregard to satisfaction with and loyalty to the new firm.

66 / Journal of Marketing, July 2000

We address this issue by proposing that customers whoswitch to a firm because of dissatisfaction with a previousservice provider constitute a key customer group that ischaracterized by a propensity for higher levels of satisfac-tion with and loyalty toward the new firm and accordinglycould be central to a firm’s acquisition and retention efforts.Drawing from rich theories on customer satisfaction andloyalty, we attempt to identify attitudinal and behavioralfactors that differentiate the three groups of customers (dis-satisfied switchers, satisfied switchers, and stayers) in theretail banking industry. In effect, the major objectives of thisstudy are

1. to examine whether the three groups of customers differ intheir overall satisfaction with the service provided by thecurrent firm (in the case of switchers, this would be theswitched-to firm),

2. to investigate the role of satisfaction with the various aspectsof the service in differentiating among the groups, and

3. to examine whether the groups differ in their involvementwith and loyalty behavior toward the service.

This research comprises two studies. In Study 1, on thebasis of a thorough review of relevant literature, we developand test research hypotheses pertaining to the objectives ofthe study. Then we describe the data, the analyses used intesting the hypotheses, and the research results. Study 2replicates the findings of Study 1 in a larger sample andexplores some interesting issues that arise from the resultsof the first study. The issues we examine in Study 2 include(1) the influence of time (tenure as a customer with the cur-rent firm) on the hypothesized difference among the groupsin terms of their overall satisfaction with the serviceprovider, (2) differences within the switcher groups in termsof their prior switching experiences, and (3) differenceswithin the three groups in terms of other relevant variables,such as commitment, dependence, and risk aversion. InStudy 2, we discuss the relevant literature pertaining to thesethree issues and empirically examine these relationships.Finally, on the basis of the findings of both studies, we drawmanagerial implications, discuss limitations pertaining tothe generalizability of the results, and offer guidelines forfurther research.

Theoretical Foundation andResearch Hypotheses

The literature on service satisfaction and switching behaviorsuggests that three critical constructs should be examinedwhen the differences among customers are investigated:customer loyalty, customer satisfaction, and involvement.First, the core of a valuable customer base consists of loyalcustomers. Research has shown that loyal customers aremore profitable not only in the short run because they spendmore (O’Brien and Jones 1995) but also in the long runbecause they spread positive word of mouth (Reichheld andTeal 1996). Loyal customers most directly affect profit byensuring a steady stream of future customers (Oliver 1997).Because of their current and potential future value, loyalcustomers are logically at the heart of a company’s mostvaluable customer group.

Second, satisfaction is also acknowledged as a key deter-minant of not only continued patronage but also firm prof-itability. Prior research has shown that satisfied customersexhibit reduced price elasticities and greater competitiveresistance and that firms enjoy reduced failure costs and anenhanced reputation (Anderson, Fornell, and Lehman 1994;Fornell 1992). The perspective of the satisfaction and servicesresearch suggests that satisfaction is also a significantantecedent to postpurchase attitude and repeat purchase inten-tions, as well as several other beneficial behavioral intentions(Anderson 1994; Zeithaml, Berry, and Parasuraman 1996).

Third, involvement has been shown to play a key role inthis area of research. Researchers have shown the importantmoderating influence of both purchase involvement (Oliva,Oliver, and MacMillan 1992) and ego involvement (Bloe-mer and Kasper 1995) on the satisfaction–loyalty relation-ship and the antecedent role that these variables play indetermining brand commitment (Beatty, Kahle, and Homer1988).

However, to our knowledge, no research has yet exam-ined whether or how these critical variables are likely to dif-fer among the three customer groups—dissatisfied switch-ers, satisfied switchers, and stayers. Drawing on the richtheoretical foundation in this area, in the current study weattempt to formulate and test specific hypotheses regardingdifferences among the three customer groups in terms ofcustomer satisfaction, involvement, and loyalty.

Overall Customer Satisfaction

Two broad theoretical bases are directly relevant to our study:the expectancy–disconfirmation paradigm (Oliver 1980) andcomparison-level theory (Thibaut and Kelly 1959).

Expectancy–disconfirmation theory. According to theexpectancy–disconfirmation paradigm (Oliver 1980), con-sumers judge satisfaction with a product by comparing previ-ously held expectations with perceived product performance.If performance is above (below) expectations, positive (neg-ative) disconfirmation occurs and increases (decreases) insatisfaction are expected. Thus, consumer satisfaction is afunction of expectations and disconfirmation, and predictiveexpectations are used as the standard of comparison.

More important, Oliver (1997) suggests that two under-lying forces drive the expectancy–disconfirmation process:assimilation and contrast effects. Assimilation strategyimplies a heavy reliance on expectations in arriving at satis-faction judgments, such that consumers are thought to assim-ilate performance toward previously held expectations(Oliver 1997). Similar to adaptation-level theory (Helson1964), expectations are viewed as the anchor for future per-formance evaluations and are believed to take on increasedimportance under conditions of high performance ambiguity.

Alternatively, contrast effects manifest themselves insatisfaction judgments, as consumers are likely to exagger-ate the perceived levels of performance so that performancelevels that exceed expectations tend to be rated much higherthan they really are (Oliver 1997). In effect, a consumer isbelieved to magnify perceptions of performance in thedirection of the performance discrepancy. Oliver (1997)notes that disconfirmation, a proxy for contrast effects, is

Customer Base of Service Providers / 67

strongest under conditions of high salience, or involvement,and when consumers are easily able to discern performancedifferences.

In this context, the dissatisfied switchers are likely toexperience higher levels of involvement (discussed subse-quently) and thus should easily discern changes in the per-formance levels from the previous dissatisfying serviceexperience to the new one. Thus, higher involvement sug-gests that the satisfaction judgments of the dissatisfiedswitchers will be disconfirmation driven. However, involve-ment tends to have the effect of magnifying disconfirmationeffects, regardless of whether an expectation is positively ornegatively confirmed. As such, elevated levels of involve-ment can, in some cases, have a deleterious effect on the dis-satisfied switcher’s level of satisfaction as well (Oliver1997). Thus, the question becomes whether the dissatisfiedswitchers are likely to experience positive disconfirmationor negative disconfirmation, a question addressed by com-parison-level theory.

Comparison-level theory. According to Thibaut andKelley (1959), the key to determining the level of satis-faction with and motivation to remain in a relationship isthe concept of comparison levels, of which two standardsare employed: the comparison level and the comparisonlevel for alternatives. The comparison level is “the stan-dard against which a member evaluates the ‘attractiveness’of the relationship or how satisfactory it is” (Thibaut andKelley 1959, p. 21). Thibaut and Kelley (1959) advancethe general hypothesis, which is central to our researchfocus, that the comparison level tends to move to the levelof outcomes currently being attained. Thus, a customerwho has experienced declining outcomes with a previousservice provider and switches because of dissatisfactionwill enter a new relationship with a reduced comparisonlevel. Therefore, we expect this customer to exhibit highlevels of satisfaction relative to other customers who haveexperienced relatively little change in their comparisonlevels.

Prior consumer research (e.g., LaTour and Peat 1979,1980), as well as interorganizational exchange research(e.g., Anderson and Narus 1990), has generally found sup-port for comparison-level theory predictions regarding priorexperience and satisfaction. However, although theory isinstructive regarding the generalized operation of expecta-tions and comparison standards, it remains relatively silenton the specific time frame in which these operations are sup-posed to occur. Therefore, the predictions that are suggestedby comparison-level theory should be treated with a degreeof caution.

In summary, expectancy–disconfirmation theory pre-dicts that satisfaction judgments of the dissatisfied switcherswill be disconfirmation driven, largely because of thesalience of the service to the customer, and that satisfactionjudgments will be more extreme for this group. Considera-tion of this theoretical prediction in the light of comparison-level predictions of higher satisfaction, or positive discon-firmation, suggests that the dissatisfied switchers will bemore satisfied than the other customer groups with their newservice provider. Therefore,

H1: All else being equal, compared with satisfied switchersand stayers, dissatisfied switchers are more satisfied withtheir current service providers.

A fundamental difference between customers who haveswitched for reasons other than dissatisfaction and customerswho have not switched at all is the notion that the satisfiedswitchers have prior experience with other service providersin the same category (i.e., experience-based norms). Thissuggests that differences exist in the sets of expectations usedby these two groups and accordingly implies differences inthe levels of subsequent satisfaction judgments. Althoughdissatisfied switchers also possess prior experience, thenature and valence of their experience differ from that of sat-isfied switchers, and this difference suggests opposite effectsin subsequent satisfaction judgments.

Researchers have shown that the nature and amount of aconsumer’s experience with an evoked set of brands areimportant determinants of the satisfaction process (Cadotte,Woodruff, and Jenkins 1987; Woodruff, Cadotte, and Jenk-ins 1983). Focal brand expectations are likely to result fromthe decision to use the brand, but consumers also enter thisscenario with different levels of prior product experience.Specifically, consumers with broader experience are likelyto develop different standards of comparison than con-sumers with less experience, such that prior experienceinfluences both focal brand expectations and product-cate-gory performance norms. These latter standards are closelyaligned with norms that reflect what the focal brand shouldbe able to achieve, not just predictions as to what the focalbrand will achieve. Although research in this area specifiesthe overall nature of these expectation processes, little guid-ance is offered regarding the specific time frame for theseoperations.

Oliver (1997) suggests that these experience-basednorms, when employed as expectations, determine the rela-tive level of a consumer’s expectations in a better than/worsethan sense. As such, it is reasonable to suggest that expecta-tions held by satisfied switchers will be at least at the levelspreviously held. This line of argument finds support in stud-ies that suggest that a positive relationship exists betweenprior experience and current levels of expectations (Zei-thaml, Berry, and Parasuraman 1993), as well as the upwardshift of should expectations over time (Boulding et al. 1993).The preceding discussion suggests the following:

H2: Compared with stayers, satisfied switchers are less satis-fied with their current service providers.

Customer Satisfaction with Service Dimensions

Although investigations of overall satisfaction provide use-ful insights into the various customer groups, further explo-ration of satisfaction with service dimensions provides amore detailed look into the factors that drive customer satis-faction. Researchers have suggested that satisfaction withspecific service attributes should be measured routinelywhen customer satisfaction and switching behavior areinvestigated (Rust and Zahorik 1993). The reasoning behindsuch advice relies on the multidimensional nature of per-ceptions of service quality and satisfaction, such that some

68 / Journal of Marketing, July 2000

dimensions may be perceived as more important than othersin determining overall satisfaction and intentions to repa-tronize or switch. Furthermore, by investigating individualservice dimensions, researchers are better able to provideactionable managerial guidance regarding which serviceareas a firm should concentrate on in efforts to build loyaltyamong current customers and attract profitable prospects.

Service quality research has shown that five dimensionsof service are most relevant in determining perceptions ofservice quality and satisfaction: tangibility, reliability,responsiveness, assurance, and empathy (Parasuraman, Zei-thaml, and Berry 1985, 1988, 1994). Other research hasshown that service factors such as convenience and warmthare dimensions of service satisfaction and loyalty (Rust andZahorik 1993). An underlying element of these various ser-vice dimensions is the notion of interaction with firm repre-sentatives, or a broader “people factor,” which theory sug-gests may be the most important determinant of overallsatisfaction and repeat patronage intentions in many serviceindustries.

According to the services marketing literature, serviceencounters are first and foremost social encounters (Berry1983; Czepiel 1990). The purchase of a service is a processthat relies on the interaction between the service providerand the customer, and therefore service encounters are con-sidered interpersonally relational in nature (see Crosby,Evans, and Cowles 1990; Crosby and Stephens 1987;Iacobucci and Ostrom 1996; Ostrom and Iacobucci 1995).As a result, customer perceptions of contact employees willaffect their perceptions of the company and greatly influ-ence customer satisfaction (Bitner, Booms, and Mohr 1994;Goff et al. 1997; Iacobucci and Ostrom 1996; Rust andZahorik 1993; Westbrook 1981).

This factor may be best understood as a problem-solvingissue. Service failure and recovery research suggests that inter-personal contact during service recovery is a factor in deter-mining ultimate satisfaction and perceptions of service quality(Kelley, Hoffman, and Davis 1993). In other words, servicepersonnel appear to be key to service recovery and otherrelated encounters, and because of this the customer’s ultimatesatisfaction or dissatisfaction is likely to be couched in termsof how the employees handled the service problem. Therefore,it makes sense that the people factor would discriminate betterthan other factors among customer groups with presumablydiffering service experiences. However, note that the impor-tance of the people factor is likely to vary across industries.

In summary, this research implies that satisfaction withservice dimensions related to interaction with a firm’s repre-sentatives is likely to be more important than satisfaction withthe other service dimensions and, in the research context here,is likely to be a discriminator among the various customergroups of interest. As such, we hypothesize the following:

H3: Satisfaction with the people factor of the service is astronger discriminant of the three groups of customers thansatisfaction with the other aspects of the service.

Involvement

The two forms of involvement relevant to this research arepurchase and ego involvement. Purchase involvement

relates to the level of concern for or interest in the purchaseprocess that is triggered by the need to consider a particularpurchase. Purchase involvement can best be understood asthe cost, effort, or investment in a purchase (Mittal and Lee1989; Zaichkowsky 1985). It is the outcome of a person’sinteraction with a product and the purchase situation(Beatty, Kahle, and Homer 1988) and is similar to, but morenarrowly focused than, Houston and Rothschild’s (1978)definition of situational involvement. Because customersare likely to experience changes in levels of purchaseinvolvement when key facets of the relevant environmentchange (Beatty, Kahle, and Homer 1988), such as a serviceswitch, stayers are not likely to experience purchaseinvolvement in a manner similar to that of switchers. There-fore, we hypothesize differences only between the twoswitching groups.

Switchers who are dissatisfied should be expected tohave experienced critical changes in levels of perceived ser-vice quality, whether they relate to core service failures, ser-vice encounters, or service design (Keaveney 1995). Nega-tive outcomes from such experiences are highly salient andare likely to be distinctive, atypical, and emotionallycharged, and such information is bound to be encoded morethoroughly and be more easily retrieved from memory(Folkes 1988). Such prior experiences will be factored intoexpectations and apprehensions about future service experi-ences (Oliver and Winer 1987), thereby affecting perceivedrisk associated with service selection and use (Mittal andLee 1989). Because the result of such cognitive evaluationsis an increase in purchase involvement (Bloch 1982; Blochand Richins 1983; Houston and Rothschild 1978), weexpect that the dissatisfied switchers experience greater lev-els of purchase involvement than customers who switch forother reasons. This suggests the following:

H4: Compared with satisfied switchers, dissatisfied switchersexhibit higher levels of purchase involvement.

Ego involvement has been defined as the “importance ofthe product to the individual and to the individual’s self con-cept, values, and ego” (Beatty, Kahle, and Homer 1988, p.150). Ego involvement is similar to enduring involvement,which is defined as an ongoing concern for a particularproduct class and relatively independent of purchase situa-tions (Bloch and Richins 1983; Richins and Bloch 1986).Although ego involvement has also been conceptualized asa relatively stable phenomenon (Richins and Bloch 1986),researchers have recognized several psychological mecha-nisms that are likely to influence the levels of ego involve-ment people experience.

One such mechanism is familiarity, which according toSherif and Cantril (1947), can increase ego involvement.Customers who have experience with only one serviceprovider—the stayers—are more likely to experience higherdegrees of familiarity and to develop a favorable attitudetoward a particular service provider and the service categoryin general. Thus, their level of ego involvement is likely tobe higher than that of the other customer groups. Therefore,we hypothesize the following:

H5: Compared with stayers, both dissatisfied and satisfiedswitchers exhibit lower levels of ego involvement.

Customer Base of Service Providers / 69

Customers who switch because of dissatisfaction arelikely to experience changes in their levels of ego involve-ment with a specific service category. A previously positiveelement of self-definition that has now become negative(i.e., the service) is not likely to continue to play the samerole in defining the customer’s self-identity. The manifesta-tion of this cognitive process is a reduction in the level ofego involvement by the customer regarding the service rela-tionship. Such changes in ego involvement are not unex-pected, as ego involvement has long been conceptualized aschanging in response to the stresses and strains that peopleexperience (Sherif and Cantril 1947).

Furthermore, dissatisfying service experiences, particu-larly those that result from service failures, accumulate up tothe point of service switching and are salient and memo-rable. This negative consumption experience should influ-ence the extent of enduring importance that a person placeson the product or service category (Bloch and Richins1983). This is particularly relevant because consumerresearchers have identified several psychological copingmechanisms that relate to devaluing, or decreasing theimportance of, the object causing psychological stress(Pearlin and Schooler 1978). A dissatisfying relationshipthat results in termination would influence the degree ofimportance consumers place on that service in defining theirself-concept and as a result would influence the level of egoinvolvement associated with that service category. Thisleads us to hypothesize the following:

H6: Compared with satisfied switchers, dissatisfied switchersexhibit lower levels of ego involvement.

Customer Loyalty

An important consideration in a service firm’s customerbase is the degree to which its customers are loyal. We con-ceptualize customer loyalty as a combination of both com-mitment to the relationship and other overt loyalty behav-iors. This is consistent with prior loyalty research (see Day1969; Dick and Basu 1994). Again, we rely on the work ofThibaut and Kelley (1959) and the loyalty literature in for-mulating our hypotheses related to group differences.

Comparison-level theory revisited. The comparison levelfor alternatives is the standard a person uses in decidingwhether to remain in a relationship and can be defined infor-mally as the “lowest level of outcomes a person will acceptin light of available alternative opportunities” (Thibaut andKelley 1959, p. 21). The position of the comparison level foralternatives on a person’s hypothetical outcome continuumis based largely on the range of outcomes believed to exist inthe next best alternative relationship, and as soon as currentperceived outcomes drop below comparison level for alter-natives, the person is motivated to leave the relationship.

Several points become relevant regarding customer loy-alty. First, Thibaut and Kelley (1959) suggest that thegreater the distance between the comparison level for alter-natives and actual outcomes, the closer the person comes tomaximizing the rewards–cost trade-off in the relationship—therefore, the greater is the dependence and commitment onthe part of the customer to continue the relationship. Recentresearch has shown the fundamental role that commitment

plays in the construct of customer loyalty (Assael 1987;Morgan and Hunt 1994), as well as the close relationshipdependence and commitment have in relational exchanges(Bendapundi and Berry 1997; Ganesan 1994).

Second, the outcome continuum allows for the relativepositions of comparison level, comparison level for alterna-tives, and actual outcomes to differ (Thibaut and Kelley1959), such that certain orderings are suggestive of strong,or true, customer loyalty, whereas other orderings suggestconditions similar to spurious loyalty (e.g., Day 1969; Dickand Basu 1994). For example, when a customer’s compari-son level exceeds actual outcomes as well as the comparisonlevel for alternatives, the customer is relatively dissatisfiedyet is also relatively dependent on the relationship—a situa-tion that is analogous to spurious loyalty. Thus, the applica-tion of comparison-level theory to customer loyaltyprocesses exhibits a certain degree of theoretical discrimi-nation in regard to the different types of customer loyalty.

Finally, a closer inspection of switching behavior in lightof the dynamics of comparison levels provides further insightinto the loyalty phenomenon. As perceived outcomes fallbelow a person’s comparison level for alternatives, that personis motivated to leave the relationship, the consideration set foravailable alternatives is reduced, and the comparison level foralternatives falls to represent the next best set of outcomes thatcould be attained (Thibaut and Kelley 1959). As such, com-pared with other customer groups, dissatisfied switchers arelikely to move from a state in which both outcomes and thecomparison level are below the comparison level for alterna-tives to a state in which perceived outcomes are significantlyabove both the comparison level and the comparison level foralternatives—a situation that is conducive to higher levels ofboth satisfaction and loyalty. Prior research has provided alimited test of this proposition, showing that consumers withpoor prior experience exhibit higher satisfaction and repeatpurchase intentions with the new brand (LaTour and Peat1980; Mazursky, LaBarbera, and Aiello 1987).

Customers who switch for other reasons or customerswho do not switch at all will experience relatively smallshifts in their comparison level and comparison level foralternatives largely because perceived actual outcomes withtheir current service provider change little and their consid-eration set for available alternatives remains relativelyunchanged. The likely result of such mechanics is sugges-tive of considerable differences in both satisfaction and loy-alty between customers who have switched serviceproviders because of dissatisfaction and other customergroups. This leads us to hypothesize the following:

H7: Compared with satisfied switchers and stayers, dissatisfiedswitchers are more loyal to their current service.

Intuitively, it appears that customers who have switchedservice providers for reasons other than dissatisfaction areless likely to hold negative attitudes and feelings towardtheir previous service provider. Many of these customers arelikely to remember their previous service provider in a pos-itive light and factor their previous experience into currentexpectations, emotions, and behavior. Although these vari-ous psychological constructs have been conceptualized to beantecedents to customer loyalty (Dick and Basu 1994), one

70 / Journal of Marketing, July 2000

particularly important variable appears to be the conativeantecedent of perceived switching costs. Higher perceivedswitching costs are believed to result in higher loyalty atti-tudes and intentions. Because satisfied switchers have priorexperience with other service providers as well as theprocess of switching service providers, it can reasonably beassumed that the inhibiting influence of perceived switchingcosts will be less prevalent within this group and subse-quently will have a negative influence on the formation ofloyalty.

We also see evidence in the brand-switching literature,which has shown that consumers who switch because ofextrinsic factors (e.g., coupons, price) are more likely toexhibit lower satisfaction and repeat purchase intentionswith the switched-to brand than consumers who are intrinsi-cally motivated (e.g., dissatisfaction, the desire to try a newbrand) (LaBarbera and Mazursky 1983; Mazursky, LaBar-bera, and Aiello 1987). Given this evidence, we have a basisfor suggesting that the satisfied switchers are likely toexhibit lower levels of loyalty than their nonswitching coun-terparts. Therefore, we hypothesize the following:

H8: Compared with stayers, satisfied switchers are less loyal totheir current service providers.

Research MethodInstrument Design and Data Collection

To test the hypotheses, we designed an instrument to collectinformation on (1) consumers’ use of banking services (e.g.,presence of accounts in more than one bank; type ofaccounts held; whether the customer had switched banks; ifso, why), (2) overall satisfaction with the current primarybank, (3) satisfaction with the individual aspects of thebanking service, (4) purchase and ego involvement associ-ated with the choice and usage of the bank, (5) consumers’sense of loyalty toward the bank, and (6) demographic char-acteristics. Trained interviewers obtained the data for thestudy over the telephone. We pretested the instrument on asmall sample (n = 10), and on the basis of the results of thepretest, we reduced the length of the instrument and refinedthe script.

Trained interviewers, using the final script, conductedthe interviews, which lasted an average of 12 minutes. Thesample was randomly drawn from the residential section ofthe current local telephone directory of a major metropolitanarea in the southeast region of the United States. Samplingunits were selected from the directory proportionate to thealphabetical listings. Because this approach toward sam-pling excludes households with unlisted numbers, it (unlikea random-digit dialing approach) has the potential to intro-duce biases. However, the bias can be considered minimal,given the relatively low proportion of unlisted numbers inthe general population.

Respondents were first asked two screening questions tocheck whether they currently have an account (any type)with a bank and qualify them as the household decisionmaker regarding banking services. Also, because some cus-tomers were likely to have accounts in multiple banks, therespondents (in such cases) were specifically requested to

answer all the questions with respect to their primary bank,that is, the bank they consider their major banking servicesupplier.

Calls were made during weekday evening hours to max-imize the probability of reaching the decision maker. Inter-viewers made 828 calls, which resulted in 217 completedinterviews. A total of 333 calls resulted in no answer, a busysignal, or no contact after two callback attempts. Refusalstotaled 278, which resulted in an effective response rate of43.8% (217/495). Seventeen of the completed interviewswere later considered unusable because of missing values,which resulted in 200 usable responses.

Measures of Constructs

To classify customers into the three hypothesized groups onthe basis of their switching behavior, respondents were askeda two-part question: (1) whether their current bank was theirfirst bank or they had switched from a previous bank and (2)if they had switched, the reason they switched from their pre-vious bank to their current bank. The options for switchingincluded (1) overall dissatisfaction with the service of the pre-vious bank or (2) reasons other than dissatisfaction (e.g., jobrelocation, moving out of the previous bank’s service area, theprevious bank closed down or was bought out by a differentbank). Respondents were then placed into one of three cate-gories: (1) those for whom their current bank was their firstbank (i.e., those who had never switched—the stayers), (2)those who switched because they were dissatisfied overallwith the service they received from their previous bank (i.e.,the dissatisfied switchers), and (3) those who switched for rea-sons other than dissatisfaction (i.e., the satisfied switchers).

We hypothesize that these three groups differ in their sat-isfaction with the service of their current bank, their level ofpurchase and ego involvement with the banking service, andtheir loyalty behaviors toward the current bank. Several mea-sures of these three constructs have been proposed and empir-ically validated in the literature. The items used to measurethese constructs in this research were obtained from priorstudies that were most relevant to the current research setting.

For example, measures of consumer satisfaction found inthe literature include those proposed by Anderson and Sulli-van (1993), Bearden and Teel (1983), Churchill and Suprenant(1982), Fornell (1992), Fornell and colleagues (1996), Oliva,Oliver, and MacMillan (1992), Oliver (1980, 1992, 1993),Oliver and Swan (1989), Rust and Zahorik (1993), Tse andWilton (1988) and Westbrook and Oliver (1981). On the basisof prior research measures, we measure satisfaction in twoways. First, we obtained a global measure of satisfaction bymeans of a single item: “Overall, how satisfied are you withyour bank?” Second, to measure consumers’ satisfaction withthe various aspects of the banking service, we employed ascale comprising 11 items. Given the boundaries of thisresearch study, the scale was composed mostly of items devel-oped by Rust and Zahorik (1993). On the basis of an exami-nation of the literature and of focus groups conducted in a pre-vious study, Rust and Zahorik (1993) identify nine keyattributes that define customers’ ongoing relationships withtheir primary bank. Two items were added to this nine-itemscale, and all items were measured on a five-point Likert scalethat ranged from “very dissatisfied” to “very satisfied.”

Customer Base of Service Providers / 71

The literature also provides several definitions and mea-sures of involvement (Cohen 1983). Because of the currentresearch context, we restricted the measures of involvementto those that apply specifically to purchase and ego involve-ment. We used a total of nine items adapted from prior stud-ies (Beatty and Smith 1987; Bloch 1982; Bloemer andKasper 1995; Laurent and Kapferer 1985; Mittal 1989; Mit-tal and Lee 1989; Richins and Bloch 1986; Salma andTashchian 1985; Zaichkowsky 1985) to measure theinvolvement constructs.

Finally, early studies on brand loyalty measure loyalty onthe basis of repeat patronage or repeat purchase intentions.But researchers generally agree that operationalizing loyaltysimply as repeat patronage is too simplistic and does not cap-ture the multidimensionality of the construct (Bloemer andKasper 1995; Day 1969; Dick and Basu 1994; Jacoby andChestnut 1978; Jacoby and Kyner 1973). In line with thisargument, recent studies have defined and measured loyaltyusing multiple items including repeat patronage, self-statedretention, price insensitivity, resistance to counterpersua-sion, and the likelihood of spreading positive word of mouth(e.g., Dick and Basu 1994; Fornell 1992; Fornell et al. 1996;Jacoby and Kyner 1973). Adapting these measures, we usesix related items to operationalize the customer loyalty con-struct. We measured the items for both involvement and loy-alty constructs on a five-point Likert scale that ranged from“strongly disagree” to “strongly agree.”

Data Analysis and ResultsA preliminary analysis of the data revealed that the respon-dents were almost evenly split by sex (51.5% male and 48.5%female). Approximately 47% of the respondents were 35years of age or younger, and the average household income ofapproximately 36% of the sample was greater than $50,000.Almost 57% of the sample had earned at least an undergradu-ate degree, and approximately 62% of the sample was mar-ried. Of the 200 respondents, 27% were stayers, 15.5% weredissatisfied switchers, and the remaining 57.5% were satisfiedswitchers. The percentage of dissatisfied switchers seems tobe in line with the findings of Rust and Zahorik (1993), whoreport that approximately 21% of switchers were dissatisfiedwith their previous bank. Overall, the data revealed good vari-ance in the responses for all other items measured. In Table 1,we provide a correlation matrix of the research constructs.

Overall Satisfaction

H1 and H2 pertain to differences among the three groups inregard to their overall satisfaction with their current primarybank. H1 states that compared with satisfied switchers andstayers, dissatisfied switchers are more satisfied with theircurrent service providers, and H2 states that satisfied switch-ers are less satisfied with their current service providers thanstayers. To test these hypotheses, we compared group meanson the overall satisfaction item using analysis of variance(ANOVA). The results (see Table 2) reveal that the groupsdiffer significantly in their overall satisfaction with theircurrent bank. Furthermore, the results show that the dissat-isfied switchers (mean score = 4.61) are significantly moresatisfied with their current bank than the other two groups

and that the satisfied switchers (mean score = 4.04) are sig-nificantly less satisfied than the stayers (mean score = 4.28).This provides support for hypotheses H1 and H2.

To test the subsequent hypotheses related to group differ-ences with regard to satisfaction with the individual aspects ofthe service, involvement, and loyalty, the individual measuresof these constructs were factor analyzed to determine theirmeasurement properties and dimensionality. For the satisfac-tion items, a scree plot of the eigenvalues indicated a four-fac-tor solution. In Table 3, we present the items and the corre-sponding factor loadings. Four items loaded highly on the firstfactor. Because these items referred to problem-solving andhuman dimensions of the bank, they were interpreted as the“people factor.” Three items loaded on the second factor,which was labeled “locational convenience,” and the third fac-tor was characterized as “ease of transaction” and includedthree items. One item, which refers to satisfaction with the costof checking account, loaded on its own and was termed the“cost factor.” Furthermore, the test of intercorrelation amongthe items loading on the individual factors suggests a highdegree of reliability: Cronbach’s coefficient alphas valueswere .92, .86, and .75, respectively, for the first three factors.

A factor analysis of the involvement items revealed a two-factor solution. The six items loading on the first factor corre-sponded to being involved with the particular purchase deci-sion of choosing a bank. Therefore, this factor was interpretedas “purchase involvement.” The second factor, which con-tained three items, pertains to the “ego involvement” dimen-sion. In Table 4, we present the involvement items and the cor-responding factor loadings. The coefficient alphas for the itemsloading on the factors are .84 and .71, respectively, which indi-cates an acceptable level of reliability (Nunnally 1978).

A factor analysis of the six items that measured customers’loyalty toward their current banks revealed a clean two-factorsolution. We present the items and the corresponding factorloadings in Table 5. On the basis of prior research findings, weexpected all six items to load highly on a single factor. Thisresult (a two-factor solution), though surprising, makes intu-itive sense. The three items that load on the first factor corre-spond to customers’ willingness to spread positive word ofmouth and their intentions to use more of the bank’s services.The remaining three items loading on the second factor corre-spond to competitive price immunity and self-stated retention.Therefore, we label our first factor “active loyalty” and the sec-ond factor “passive loyalty.” The coefficient alphas for theitems loading on the factors are .77 and .72, respectively, whichindicates an acceptable level of reliability (Nunnally 1978).

For a test of the remainder of our hypotheses, we per-formed a multiple discriminant analysis. We used discrimi-nant analysis, because this method determines the ability ofthe criterion variables to discriminate among the threegroups of customers. To check the validity of the models, weemployed a proportional 50/50 split-sample validationapproach, and we present the results for both the analysisand the holdout sample for each of the three cases.

To test H3–H8, we performed individual discriminantanalyses using the four satisfaction, the two involvement,and the two loyalty dimensions. Subsequently, we per-formed an overall discriminant analyses that included alleight factors as criterion variables. Because the results of the

72 / Journal of Marketing, July 2000

TAB

LE

1C

orr

elat

ion

Mat

rix

Ove

rall

Peo

ple

Lo

cati

on

alE

ase

of

Pu

rch

ase

Eg

oA

ctiv

eP

assi

veS

atis

fact

ion

Fact

or

Co

nven

ien

ceTr

ansa

ctio

nC

ost

Invo

lvem

ent

Invo

lvem

ent

Loy

alty

Loy

alty

1.00

(.01

)

.60

1.00

(.01

)(.

01)

.10

.09

1.00

(.17

)(.

23)

(.01

)

.07

.03

.31

1.00

(.30

)(.

68)

(.01

)(.

01)

.31

.41

–.03

–.01

1.00

(.01

)(.

01)

(.65

)(.

83)

(.01

)

.04

.13

–.05

–.07

.04

1.00

(.58

)(.

06)

(.49

)(.

30)

(.60

)(.

01)

.20

.19

–.01

.02

.05

.06

1.00

(.01

)(.

01)

(.99

)(.

76)

(.49

)(.

41)

(.01

)

.27

.23

.02

–.14

.15

.24

.12

1.00

(.01

)(.

01)

(.81

)(.

05)

(.04

)(.

01)

(.10

)(.

01)

.17

.16

.04

.06

.06

.09

.28

.05

1.00

(.01

)(.

03)

(.59

)(.

44)

(.41

)(.

20)

(.01

)(.

50)

(.01

)

Customer Base of Service Providers / 73

Measure

Overall, how satisfied areyou with your bank?

Groups

Stayers(n = 54)

Satisfied switchers(n = 115)

Dissatisfied switchers(n = 31)

Mean Scoresa

4.28(.0001)

4.04(.0001)

4.61(.0001)

Difference BetweenMeansb

Stayers versus satisfied switchers .24

Stayers versus dissatisfied switchers –.33

Satisfied switchers versus dissatisfied switchers –.57

TABLE 2Overall Satisfaction Measure: Difference Between Group Means

aNumbers in the parentheses represent p values.bThe differences between group means were all significant at the p = .05 level.

TABLE 3Exploratory Factor Analysis Results for Satisfaction Items

People Locational Ease ofItems Factor Convenience Transaction Cost

The friendliness of the bank employees .910 .037 –.005 .112How well the bank managers know me .842 .006 .005 .183How well the bank listens to my needs .939 .025 .016 .016The quality of service offered by the bank .890 .080 .034 .117How close the bank is to my home .057 .791 .209 –.056How close the bank is to my place of employment –.001 .914 .100 .016How convenient the bank is to my route to work .067 .905 .089 .004The number of ATM machines the bank has around town –.024 .241 .689 –.167How many tellers are available during busy times .064 .090 .871 .068How convenient the banking hours are –.004 .072 .850 .064The cost of a checking account .301 –.027 –.006 .937

Eigenvalue 3.31 2.36 2.02 1.07

TABLE 4Exploratory Factor Analysis Results for Involvement Items

Purchase EgoItems Involvement Involvement

I constantly compare the prices and rates offered by various banks in my area. .796 –.040I visited multiple banks in the area before I opened an account with the current bank. .887 .046I compared the prices and rates of several banks in my area before I selected

my current bank. .858 –.004After deciding on my current bank, I have discussed my choice with family and friends. .551 .125After deciding on my current bank, I have compared my bank with other banks in

the area. .726 –.084After deciding on my current bank, I have weighed the pros and cons of my choice. .632 .093The brand image of the bank played a major role in my decision to become a customer

of the bank. .053 .632The bank I use says a lot about who I am. .031 .822It is important for me to choose a bank that “feels” right. –.009 .795

Eigenvalue 3.39 1.74

individual discriminant analyses were in complete agree-ment with the overall analyses, we restrict our discussion tothe findings of the overall analyses. In Table 6, we providethe results of the three-group discriminant analysis per-formed with all eight factors included as criterion variables.Both discriminant functions are significant, and the results

reveal that six of the eight factors are significant in discrim-inating among the groups. The potency indices suggest thaton the basis of relative discriminatory power, the variablescan be ordered as follows: the people factor, cost, egoinvolvement, purchase involvement, active loyalty, and pas-sive loyalty. A stepwise discriminant analysis resulted in the

74 / Journal of Marketing, July 2000

TABLE 5Exploratory Factor Analysis Results for Loyalty Items

Active Loyalty Passive LoyaltyItems Behavior Behavior

I would highly recommend my bank to my friends and family. .864 .137I am likely to make negative comments about my bank to my friends

and family. –.823 –.046In the near future, I intend to use more of the services offered by

my bank. .614 –.160If my current bank were to raise the price of my checking account,

I would still continue to be a customer of the bank. –.007 .787If a competing bank were to offer a better rate or discount on their

services, I would switch. .060 –.753As long as I live in this neighborhood, I do not foresee myself switching

to a different bank. .057 .732

Eigenvalue 1.81 1.77

same six factors being a part of the final solution. (For thesake of brevity, the results of the stepwise analysis are notreported here.)

The first function accounts for 64% of the total varianceexplained, and the second function explains 36% of theremaining variance. The squared canonical correlations are.40 and .27, respectively, for the two functions. The value ofthe Wilks’ lambda is .43 and is significant at p < .01. Fur-thermore, the hit ratios for the analysis sample (72.8%) andthe holdout sample (70.0%) are above the proportionalchance criterion (of 42.8%), and the corresponding Press Q-statistic is significant at the .01 level for both the analysisand the holdout sample. Table 6 also presents group meansfor all eight criterion variables.

Satisfaction with the Individual Dimensions of theService

The hypotheses pertaining to customers’ satisfaction withthe individual aspects of the banking service state that sat-isfaction with the people factor of the service will be astronger discriminant of the three groups of customers thansatisfaction with other aspects of the service. As men-tioned previously, the factor analysis of the 11 items relat-ing to the key attributes of the banking service revealed afour-factor solution: the people factor, locational conve-nience, ease of transaction, and cost. Thus, support for thishypothesis requires that the discriminant analysis resultsreveal that the people factor is significantly better in dis-criminating among the three groups than the other threefactors.

The results, illustrated in Table 6, reveal that only twoof the four factors are significant in discriminating amongthe groups: the people and the cost factors. Furthermore,an examination of the discriminant loadings, standardizedcoefficients, and potency index suggests that the influenceof the people factor on the discriminant function isstronger than the influence of the cost factor. Finally, as isshown in Table 6, the group means suggest that as in thecase of the overall satisfaction variable, the mean satis-faction level decreases from the dissatisfied switchers tostayers to the satisfied switchers. This provides supportfor H3.

Purchase and Ego Involvement

H4 states that the dissatisfied switchers exhibit higher levelsof purchase involvement than the satisfied switchers. Like-wise, H5 states that the switchers exhibit lower levels of egoinvolvement than the stayers, and H6 states that the dissatis-fied switchers exhibit lower levels of ego involvement thanthe satisfied switchers. Support for these hypothesesrequires that (1) the overall discriminant function is signifi-cant, (2) both purchase and ego involvement factors are sig-nificant in discriminating among the three groups, and (3)the group means are in the hypothesized directions.

Table 6 reveals that both purchase and ego involvementare significant in discriminating among the groups and thatthe group means are in the hypothesized direction. Also, anexamination of the discriminant loadings and standardizedcoefficients suggests that the impact of ego involvement onthe discriminant function is stronger than the influence of pur-chase involvement. This provides support for H4, H5, and H6.

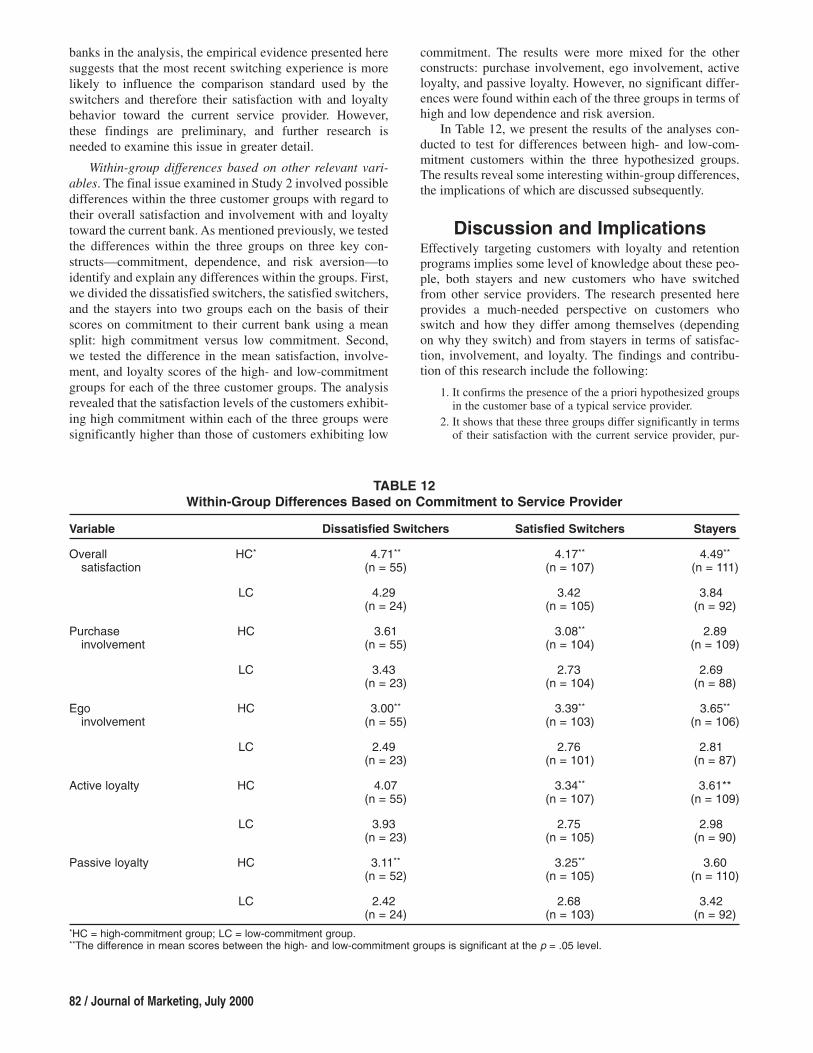

Customer Loyalty

H7 and H8 pertain to group differences with regard to thegroups’ loyalty toward the bank, stating that the dissatisfiedswitchers are more loyal to their current service providerthan the other two groups. In addition, a comparison of thesatisfied switchers and the stayers reveals that the former isless loyal. As mentioned previously, factor analysis per-formed on the six items measuring the loyalty constructrevealed a two-factor solution: active and passive loyalty.

Therefore, support for these hypotheses requires that (1)the overall discriminant function is significant, (2) bothactive and passive loyalty factors are significant in discrim-inating among the three groups, and (3) the group means arein the hypothesized directions; that is, the dissatisfiedswitchers are the most loyal, followed by the stayers andfinally the satisfied switchers.

Table 6 reveals that both active and passive loyalty fac-tors are significant in discriminating among the groups. Fur-thermore, an examination of the potency index suggests thatactive and passive loyalty have almost equal influence onthe discriminant function. But an examination of the groupmeans reveals that whereas the means are in the hypothe-sized direction for active loyalty, such is not the case for

Customer Base of Service Providers / 75

TAB

LE

6O

vera

ll D

iscr

imin

ant

An

alys

is R

esu

lts*

Sta

nd

ard

ized

Co

effi

cien

tD

iscr

imin

ant

Lo

adin

gs

Un

ivar

iate

FG

rou

p M

ean

s

Po

ten

cyD

issa

tisf

ied

Sat

isfi

edA

ttri

bute

Fu

nct

ion

1F

un

ctio

n 2

Fu

nct

ion

1F

un

ctio

n 2

Rat

ioP

rob

abili

tyIn

dex

Sw

itch

ers

Sw

itch

ers

Sta

yers

Peo

ple

fact

or**

.65

.34

.62

.51

34.7

8.0

1.3

404.

633.

614.

20Lo

catio

nal c

onve

nien

ce.0

6.1

8.0

8.1

1.8

7.4

2.0

083.

973.

803.

93E

ase

of t

rans

actio

n.1

8–.

26.0

7–.

06.4

7.6

2.0

043.

843.

733.

69C

ost**

*.3

7.4

7.4

9.5

426

.38

.01

.259

4.42

3.08

4.05

Pur

chas

e in

volv

emen

t**.3

5–.

46.2

9–.

349.

82.0

1.0

953.

442.

992.

69E

go in

volv

emen

t**

–.53

.51

–.28

.49

14.2

5.0

1.1

372.

813.

223.

67A

ctiv

e lo

yalty

†.2

5–.

37.3

0–.

176.

90.0

1.0

684.

103.

283.

46P

assi

ve lo

yalty

**–.

36.2

2–.

20.3

06.

03.0

1.0

582.

813.

313.

60

Fu

nct

ion

1F

un

ctio

n 2

Eig

enva

lue

(pro

port

ion)

.64

.36

Squ

ared

can

onic

alco

rrel

atio

n.4

0.2

7

Val

ue

FP

rob

abili

ty

Wilk

s’la

mbd

a.4

312

.24

.01

Per

cen

t C

orr

ectl

y C

lass

ifie

d (

Hit

Rat

io)

Ana

lysi

s sa

mpl

e72

.8%

Hol

dout

sam

ple

70.0

%P

ropo

rtio

nal c

hanc

e cr

iterio

n42

.8%

Pre

ss Q

-sta

tistic

69.1

4(a

naly

sis

sam

ple)

(.01

)P

ress

Q-s

tatis

tic60

.50

(hol

dout

sam

ple)

(.01

)

*Ast

epw

ise

disc

rimin

ant

anal

ysis

rev

eale

d th

at t

he s

ame

six

of t

he e

ight

fac

tors

wer

e si

gnifi

cant

in d

iscr

imin

atin

g am

ong

the

thre

e gr

oups

.**

Gro

up m

eans

are

sig

nific

antly

diff

eren

t at

the

p=

.05

leve

l.**

*The

diff

eren

ce in

mea

ns b

etw

een

diss

atis

fied

and

satis

fied

switc

hers

and

bet

wee

n st

ayer

s an

d sa

tisfie

d sw

itche

rs is

sig

nific

ant

at t

he p

= .

05 le

vel.

† The

diff

eren

ce in

mea

ns b

etw

een

diss

atis

fied

and

satis

fied

switc

hers

and

bet

wee

n di

ssat

isfie

d sw

itche

rs a

nd s

taye

rs is

sig

nific

ant

at t

he p

= .

05 le

vel.

76 / Journal of Marketing, July 2000

passive loyalty. The dissatisfied switchers are not higher inpassive loyalty than the other groups. Indeed, they exhibitthe lowest levels of passive loyalty. The group means indi-cate that the stayers exhibit the highest passive loyalty, fol-lowed by the satisfied switchers and finally the dissatisfiedswitchers. This finding thus provides only partial support forH7 and H8. The implications of this finding are discussedsubsequently.

Finally, to check for differences based on the duration ofstay with the current service provider, we split the groups intotwo (less than five years and more than five years). A test ofgroup means revealed no significant difference in satisfac-tion, loyalty, and involvement measures for all three groups ofcustomers. The small size of the subgroups (particularly thedissatisfied switchers and the stayers) prevented us fromusing duration of stay as a continuous variable in the analysis.

Premise for Study 2Although the findings of Study 1 that support the hypothe-ses offer rich academic and managerial implications, someother relevant issues, if explored, have the potential to offerfurther insights in this area. First, given our focus on a ser-vice industry in one geographic location, replication in alarger sample would help establish the external validity ofthese findings. Second, Study 1 reveals some interestingresults regarding the influence of past switching behavior onsubsequent satisfaction levels, but it provides little insightregarding (1) the relevant time frame in which these effectsare likely to operate or (2) the effects of any prior switcheson current satisfaction levels. Finally, although we definedand tested these three distinct customer groups on the basisof their switching or a lack of switching experience, we havelittle knowledge as to the potential differences within thesethree customer groups in terms of other relevant variables,such as commitment, dependence, and risk aversion.

Therefore, we conducted Study 2 with the objective ofreplicating the findings of Study 1 and offering some theo-retical and empirical insights on the abovementioned issues.It is imperative to state here that the issues addressed herehave not been fully explored in the literature and warrant theundivided attention of a broader research study. Therefore,we treat these issues here as largely exploratory and make afirst attempt to understand these relationships and providesome guidelines for further research that focuses on theseissues in greater breadth and depth. We now discuss each ofthese three issues in greater detail.

Duration of Stay

The literature suggests that time influences expectations andsatisfaction in several important ways. Research investigat-ing expectations in satisfaction and service quality evalua-tions suggests that as time spent as a customer with theprovider increases, the expectations used as a basis of com-parison tend to adjust to the new service provider. For exam-ple, Boulding and colleagues (1993) argue that consumers’current perceptions of service quality of a firm just after aservice contact are in part influenced by their prior expecta-tions of what will and what should transpire during the con-tact. They argue that over time, will expectations are

updated with each new service encounter and prior willexpectations. Applied here, this suggests that for satisfactionjudgments arrived at through the expectancy–disconfirma-tion paradigm, it is expected that customers adapt over timeto the new levels of service provided by the switched-tofirm.

Furthermore, researchers have also suggested that withthe passage of time, customers are more likely to employsimilar types of expectations. For example, Woodruff,Cadotte, and Jenkins (1983) theorize that customers withextensive brand experience are more likely to employ focalbrand expectations than customers with limited brand expe-rience, who in turn are more likely to employ experience-based norms. The implication of this research is that astenure with the brand (or firm) increases, customers arelikely to employ common sets of expectations (focal brand),with the effect of mitigating large discrepancies in satisfac-tion scores early in their tenure with the firm. These argu-ments lead us to pose the following question:

RQ1: Do the differences among the three groups in terms oftheir overall level of satisfaction change with increasingtenure with the switched-to bank?

More generally, is there a relationship between durationof stay with the current bank and a customer’s overall satis-faction with the bank? Theory generally does not providespecific guidance regarding the relevant time frames inwhich the hypothesized relationships are supposed to oper-ate. Although we found no significant difference among thegroups based on duration of stay (five years), further inves-tigation with an adequate sample size would be particularlyuseful in providing insights into this important and relevantissue on postswitching behavior.

Mixed Switching Experiences

In addition to the effects of duration of stay on levels of satis-faction, the literature suggests that differences also exist in sat-isfaction with the current bank among customers with multipleswitching experiences. Research in memory recall bias (Folkes1994) and heuristic processing (Tversky and Kahneman 1974)suggests that the most emotionally charged and atypical expe-riences are likely to play a large role in establishing future com-parison standards. For example, Folkes (1988, 1994) notes thatpast experiences that are distinctive and easily distinguishedfrom others are likely to be sampled more readily by con-sumers when they recall service experiences and establishexpectations. This is particularly true when consumers elabo-rate on such distinctive events and attach strong affective tracesto these memories. Even when consumers have difficultyrecalling specific events or are not motivated to do so, heuris-tic processing that relies on recalling past service exemplars isoften employed. In the current context, a dissatisfied switch isassumed to be more emotionally taxing than a satisfied switch,which would then imply that a dissatisfied switch (irrespectiveof when it occurred) might be the most salient one.

In contrast, recency bias suggests that the most recentswitching event plays an influential role in establishing thecomparison standards for the current service experience.Essentially, recency bias suggests that people are morelikely to recall more recent events than more distant ones

Customer Base of Service Providers / 77

(Crano 1977; Greene 1986; Pieters and Bijmolt 1997). Thisoccurs in part because of retroactive interference (Burke andSrull 1988) and context-dependent (Greene 1986) memoryprocesses, as well as because more recent events/memoriesare easier to discriminate (Crowder 1976). In this study,recency bias suggests that the more recent switching experi-ence is likely to be given more weight in developing futureexpectancies, irrespective of whether the most recent switchwas a dissatisfied or a satisfied switch.

In summary, recency bias theory suggests that the mostrecent service experience plays a dominant role in establish-ing future expectancies. In contrast, research in memoryrecall bias and heuristic processing suggests that the mostemotionally taxing and distinctive service experience playsa major role in establishing future expectancies. AlthoughStudy 1 provides evidence that the three customer groupsidentified in this study differ significantly in their satisfac-tion with the current service provider on the basis of theirmost recent switching experience (or lack thereof), we haveno information on the motivations for any previous switchesand their possible impact on the current level of satisfaction.In simple terms, in a two-switch sequence, does the reasonfor switching from the bank at time t – 2 to the bank at timet – 1 influence customers’ satisfaction with their currentbank (bank at time t)?

We classify customers as satisfied switchers or dissatisfiedswitchers on the basis of their most recent switching experi-ence and report that on average, the dissatisfied switchersexhibit a higher level of satisfaction with the current serviceprovider than the satisfied switchers. However, the customersclassified as satisfied switchers on the basis of their mostrecent switching experience could have switched previouslybecause of either dissatisfaction or satisfaction. The same istrue for those customers classified as dissatisfied switchers. Itwould be interesting to know whether the reasons for any priorswitches play a role in influencing the satisfaction with the cur-rent service provider. In other words, are there differences insatisfaction levels within the satisfied switcher group based ontheir previous switching experiences? The same question canbe asked of the dissatisfied switchers. Such an analysis wouldprovide us with some insight as to which switch, the mostrecent or the most emotionally taxing, is the most salientregarding comparison levels employed with the current serviceprovider. Hence, we formulate our second research question:

RQ2: Are there differences in the current levels of satisfactionamong customers with mixed switching experiences?

Within-Group Differences Based on Other Rele-vant Variables

Finally, although Study 1’s results show that the three groupsbased on the switching behavior differ in terms of their satis-faction and involvement with and loyalty toward the bank,there could exist subgroups within these three homogeneousgroups that differ in terms of other relevant variables. Anunderstanding of these differences (if any) within the groupswould provide some insights into how the subgroups differ interms of their satisfaction, involvement, and loyalty behaviors.

Prior research on maintaining customer relationships(e.g., Bendapudi and Berry 1997; Morgan and Hunt 1994),

as well as related research on switching behavior (e.g., Raju1980), suggests that the constructs of dependence, commit-ment, and risk aversion are particularly important for betterunderstanding the reasons customers stay with a firm.Dependence and commitment have been associated withseveral critical outcomes (Ganesan 1994; Morgan and Hunt1994) and reflect fundamental differences in the way a cus-tomer views an ongoing relationship (Bendapudi and Berry1997). Risk aversion reflects a general exploratory tendencythat is relevant to understanding a customer’s propensity toswitch or stay for intrinsic reasons (Raju 1980). We brieflyreview each of these three constructs.

First, customers exhibiting high levels of commitmentare more likely to maintain a dedication-based relationship,in which customers are motivated to maintain the relation-ship because they genuinely want to (Bendapudi and Berry1997; Morgan and Hunt 1994). Customers who are highlycommitted to an ongoing relationship are also likely to seekgreater relationship expansion and enhancement, identifystrongly with the partner, view such a relationship as a team,engage in behaviors such as open advocacy of the partner(Bendapudi and Berry 1997), cooperate with the partner,and stay in the relationship (Morgan and Hunt 1994). There-fore, commitment appears to be an influential variable onseveral attitudinal and behavioral variables measured here.

Second, customers who are highly dependent on a rela-tionship are more likely to maintain a constraint-based rela-tionship, or a relationship in which customers believe that theymust remain in the relationship, not that they want to (Benda-pudi and Berry 1997). Constraint-based relationships lead topreservation of the relationship only as long as the perceivedconstraints exist (Bendapudi and Berry 1997). Customers highin dependence are more likely to acquiesce to the partner’srequests or policies and, in line with reactance theory (Brehm1966), actively seek alternatives (Bendapudi and Berry 1997).

Third, customers who are particularly risk averse areless likely to take risks or be adventurous (Raju 1980). Riskaversion/risk taking has long been viewed as a manifestationof human exploratory behavior, such that the amount of riska consumer is willing to take in a choice situation is seen asa larger effort to adjust the level of actual stimulation to theoptimal level (Baumgartner and Steenkamp 1996; Berlyne1960; Raju 1980). Prior research has supported the notionthat being loyal to a brand is a strategy consumers employto control the risk inherent in certain buying situations (e.g.,Arndt 1968). Therefore, customers high in risk aversion arelikely to exhibit differences in loyalty toward the currentservice provider compared with customers who are less riskaverse. Taken together, the evidence from research ondependence, commitment, and risk aversion provides thebasis for the following research question:

RQ3: Are there subgroups within the three main customergroups that differ in terms of commitment, dependence,and risk aversion, and if so, do they exhibit significantdifferences in their overall satisfaction, involvement, andloyalty behaviors?

We first discuss the data collection process involved inthe second study and then discuss the results of the replica-tion analyses. Subsequently, we report the results of the

78 / Journal of Marketing, July 2000

analyses conducted to investigate each of the three researchquestions. Following this, we discuss our findings from bothstudies, offer theoretical and practical implications, and dis-cuss limitations and future research opportunities.

Study 2: Instrument Design, DataCollection, and Preliminary AnalysesAs mentioned previously, we conducted Study 2 to replicatethe findings of Study 1 and to address other interestingissues. Again, we used a telephone interview method to col-lect the data and adopted all the screening procedures usedin the first study. However, in the second study we used arandom-digit dialing approach to identify potential respon-dents located in the Northeast and the Southwest regions ofthe United States.

In total, 6678 calls were made; 1763 of these were madeto businesses, government entities, or nonworking numbers,and 376 calls reached either fax machines or modems. The

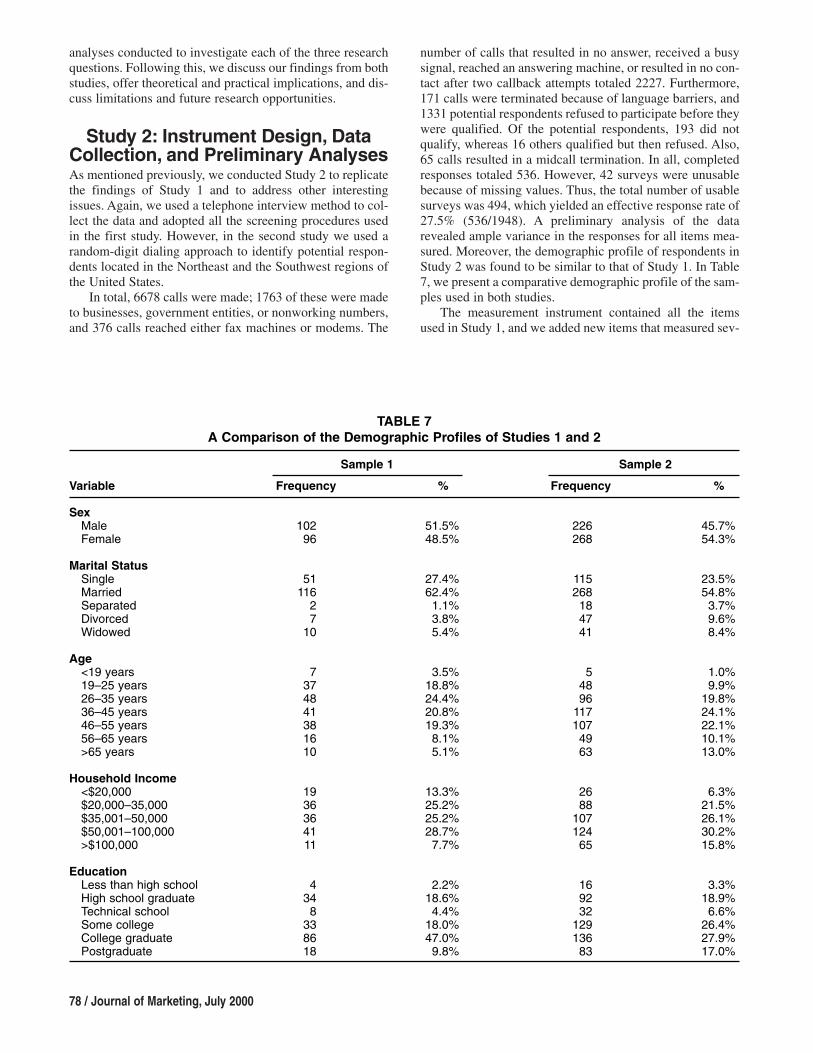

number of calls that resulted in no answer, received a busysignal, reached an answering machine, or resulted in no con-tact after two callback attempts totaled 2227. Furthermore,171 calls were terminated because of language barriers, and1331 potential respondents refused to participate before theywere qualified. Of the potential respondents, 193 did notqualify, whereas 16 others qualified but then refused. Also,65 calls resulted in a midcall termination. In all, completedresponses totaled 536. However, 42 surveys were unusablebecause of missing values. Thus, the total number of usablesurveys was 494, which yielded an effective response rate of27.5% (536/1948). A preliminary analysis of the datarevealed ample variance in the responses for all items mea-sured. Moreover, the demographic profile of respondents inStudy 2 was found to be similar to that of Study 1. In Table7, we present a comparative demographic profile of the sam-ples used in both studies.

The measurement instrument contained all the itemsused in Study 1, and we added new items that measured sev-

TABLE 7A Comparison of the Demographic Profiles of Studies 1 and 2

Sample 1 Sample 2

%

45.7%54.3%

23.5%54.8%3.7%9.6%8.4%

1.0%9.9%

19.8%24.1%22.1%10.1%13.0%

6.3%21.5%26.1%30.2%15.8%

3.3%18.9%6.6%

26.4%27.9%17.0%

Frequency

226268

115268184741

54896

1171074963

2688

10712465

169232

12913683

%

51.5%48.5%

27.4%62.4%1.1%3.8%5.4%

3.5%18.8%24.4%20.8%19.3%8.1%5.1%

13.3%25.2%25.2%28.7%7.7%

2.2%18.6%4.4%

18.0%47.0%9.8%

Frequency

10296

51116

27

10

7374841381610

1936364111

4348

338618

Variable

SexMaleFemale

Marital StatusSingleMarriedSeparatedDivorcedWidowed

Age<19 years19–25 years26–35 years36–45 years46–55 years56–65 years>65 years

Household Income<$20,000$20,000–35,000$35,001–50,000$50,001–100,000>$100,000

EducationLess than high schoolHigh school graduateTechnical schoolSome collegeCollege graduatePostgraduate

Customer Base of Service Providers / 79

eral other constructs to investigate the issues mentioned pre-viously. First, in addition to measuring the reasons forswitching from the previous bank (i.e., the bank at time t –1) to the current bank (i.e., the bank at time t), we measuredrespondents’ reasons for switching from their bank at timet – 2 to the bank at time t – 1. Also, we measured respon-dents’ overall satisfaction with their previous bank (time t –1) and the duration of stay (in years) at the current and pre-vious banks.