Understanding Sukuk

54

UNDERSTANDING SUKUK BY: CAMILLE PALDI CEO OF FAAIF

-

Upload

camille-paldi -

Category

Economy & Finance

-

view

69 -

download

6

Transcript of Understanding Sukuk

UNDERSTANDING SUKUKBY: CAMILLE PALDI

CEO OF FAAIF

WHAT ARE SUKUK?

Sukuk refers to an Islamic investment certificate, which allows investors to have rights of ownership of the asset, including the cash flow and risks associated with such ownership.

WHAT ARE SUKUK?

Sukuk offers risk diversification for Investors for their portfolios.

WHAT ARE SUKUK?

Sukuk are asset-backed, tradable, and Shari’ah compatible trust certificates.

Sukuk (plural) and sakk (singular) means legal instrument, deed, and check.

It is the Arabic name for financial certificates.

It is also an Islamic debt instrument and can be referred to as securities, notes, papers, or certificates, with features of liquidity and tradability.

WHAT ARE SUKUK?

Sakk is believed to be the source root of the European Check and is referred to any certificate representing a contract or conveyance of financial rights, obligations, or money transactions that is Shari’ah compliant.

The origin of sukuk can be traced to the Middle Ages whereby sukuk were largely used by Muslims as papers representing financial obligations originating from trade and other commercial activities.

SECURITIZATION AND SUKUK

Securitization is the process of transforming illiquid assets into a liquid one.

Tawriq means to render something into cash. It is about transforming a deferred debt for the period between the establishment of the debt and the maturity period into papers, which can be traded in the secondary market.

Tasnid is the transformation of illiquid debts into negotiable papers (sanadat).

Taskik means the process of dividing assets into papers (sukuk) or certificates. Securitization of assets into papers, securities, or certificates with the features of liquidity, tradability, and cash equivalence.

SECURITIZATION AND SUKUK

Securitization transforms the originator’s role from being an accumulator to that of a distributor.

Through securitization it is possible to unbundle, split, repackage, and distribute assets into smaller units, which can be owned by each party/investor.

Hence, securitization focuses on the process of pooling assets, the process of packaging them into securities, and the process of distributing securities to investors.

SECURITIZATION AND SUKUK

This process facilitates the transforming of an asset’s future cash flow into present cash flow.

Sukuk are a securitized and therefore liquid asset class and are preferred by Issuers as they can obtain long-term financing with favorable terms.

The investors will realize the benefits from originator’s specialization, economies of scale, and returns from the asset.

SUKUK V BONDS

The funds raised through the issuance of sukuk should be applied to investment in specified assets rather than for general unspecified purposes.

This implies that identifiable assets should provide the basis for Islamic bonds.

Since the sukuk are based on the real underlying assets, income from the sukuk must be related to the purpose for which the funding is used.

SUKUK V BONDS

The sukuk certificate represents a proportionate ownership right over the assets in which the funds are being invested.

The ownership rights are transferred, for a fixed period ending with the maturity date of the sukuk, from the original owner (the originator) to the sukuk holders (IFSB, Jan. 2009).

REASONS FOR ISSUING SUKUK

Growing demand from investors to place their funds in accordance with Shari’ah compliant principles. This enables diversification of portfolios, competitive yields, and better results.

Governments or corporates are able to raise funds for their working capital or project financing for infrastructure and development projects under a Shari’ah compliant framework instead of debentures or loans with high interest rates.

The funds collected also serves the purpose of liquidity management for financial institutions and individuals undertaking Shari’ah compliant business because it complies with their internal monetary and regulatory policies.

REASONS FOR ISSUING SUKUK

They have options whereby for during excess liquidity they may purchase sukuk and when they are short of liquidity and need immediate funds, they may sell their Sukuk into the secondary market.

Both Islamic and conventional investors are comfortable with sukuk due to their innovative structures, competitive returns, and tradability.

REASONS FOR ISSUING SUKUK

The sukuk market is not restricted to Islamic banks and countries.

Leading international banks are also tapping into the sukuk market including HSBC, Citigroup, UBS, Goldman-Sachs, and BNP Paribas in order to meet the requirements of investors.

REASONS FOR ISSUING SUKUK

Sukuk investment involves the funding of underlying tangible assets.

It is largely associated with economic development, real estate, and infrastructure related assets, which are long term projects.

Long-term investment through sukuk is preferred by institutional investors due to its stable returns, positive effects for growth and because it promotes financial market stability.

Hence, investors feel safe as the probability of short term speculativev fund movements and potential financial crisis is very remote.

REASONS FOR ISSUING SUKUK

To facilitate the development of the local, regional, and global sukuk market, and to tap into a wider investor base.

Sukuk are a means for the equitable distribution of wealth as it allows all investors to share returns from the true profits generated from the asset.

Many governments around the world are passing legislation to facilitate sukuk issuances, levelling the playing field with conventional bonds.

RIGHTS TO UNDERLYING ASSET AND ITS CASHFLOW

Sukuk represents ownership of assets, its usufruct or services (the underlying asset), the claim embodied in the sukuk is not just a claim on the underlying asset used in the sukuk transaction, but also the right to the cashflow and proceeds from the sale of the asset.

For example, in ijarah sukuk, the sukuk is akin to trust certificates establishing undivided ownership of the leased asset and the right to the cashflow arising from it.

RIGHTS TO CASHFLOW FROM THE CONTRACT OF EXCHANGE, BUT NOT THE ASSET

In the case of a sukuk issued as evidence of indebtedness arising from the sale of asset-based on contracts of exchange other than ijarah, such as those originating from bai bithamin ajil, murabahah, and istisna’a, the claim is on the obligation stemming from the applied contract of exchange, and now ownership of the physical asset, as ownership has been transferred to the obligor.

RIGHTS TO UNDIVIDED INTEREST IN SPECIFIC INVESTMENT

In the case of special investment activities funded through musharakah and mudharabah, the sukuk represents the holders’ undivided interests in the specific investments.

Mudharabah sukuk is used to raise fund for projects on the basis of partnership contracts.

The sukuk musharakah holders or investors then become the owners of the project, in proportion to their respective shares.

RIGHTS TO UNDIVIDED INTEREST IN SPECIFIC INVESTMENT

Profits are distributed according to a pre-agreed proportion while losses are pro-rated according to their equity share.

Each mudharabah sukuk holder or investor, on the other hand, holds equal value in the mudharabah equity.

Profits will be shared on a pre-agreed ratio between the mudharabah investors and the sukuk shared equally among the mudharabah investors.

SHARI’AH CONTRACTS UNDERLYING SUKUK STRUCTURES

Sukuk can be structured in different ways depending on the underlying contract.

A sukuk can be structured based on any or a combination of two or more, of the Islamic contracts of transactions such as the contracts of participation (uqud ishtirak) of mudarabah and musharakah, and contracts of exchanges (uqud mu’awadat) such as bai bithamin ajil, murabahah, salam, istisna’a, and ijarah.

The application of these contracts of transaction results in the sukuk backed or secured by such assets, thus having an in-built security to the investments.

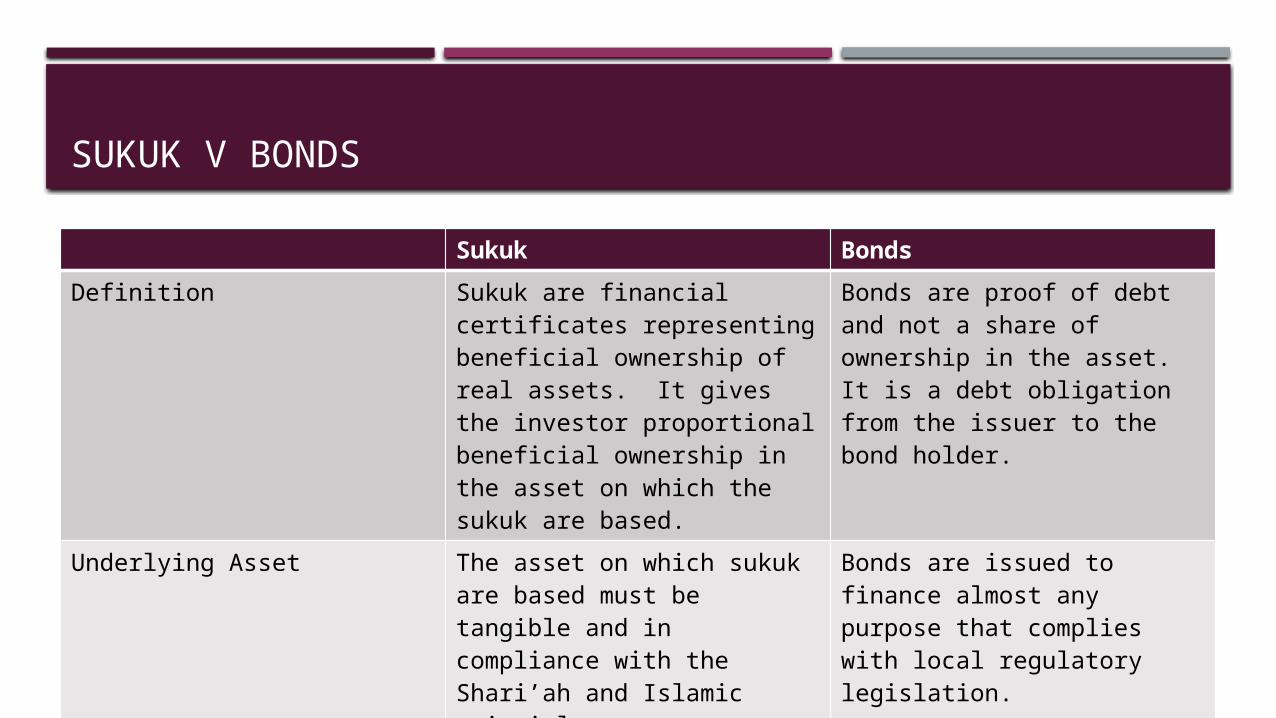

SUKUK V BONDS

Sukuk Bonds

Definition Sukuk are financial certificates representing beneficial ownership of real assets. It gives the investor proportional beneficial ownership in the asset on which the sukuk are based.

Bonds are proof of debt and not a share of ownership in the asset. It is a debt obligation from the issuer to the bond holder.

Underlying Asset The asset on which sukuk are based must be tangible and in compliance with the Shari’ah and Islamic principles.

Bonds are issued to finance almost any purpose that complies with local regulatory legislation.

Issuer Representation In sukuk, the issuer is not a borrower, but can either be: A buyer in a sale contract; A lessee in a lease contract; A partner in a partnership contract.

Bonds are debts, whereby Issuers are the borrowers from the investors (bond holders).

Issue Unit Each sukuk represents a share of the underlying asset.

Each bond represents a share of debt

SUKUK V BONDSSukuk Bonds

Issue Price The face value of sukuk is based on the market value of the underlying asset.

The face value of a bond price is based on the issuer’s creditworthiness (including it’s rating).

Returns Sharing Returns are termed as dividends and will depend on the underlying Shari’ah contract used. Sukuk holders receive a share of profits from the underlying asset (and accept a share of any loss incurred). The amount of profit cannot be ascertained, it could be fixed or vary as it is based on the sharing of profit and loss.

Returns are termed as coupons. Bond holders returns can be ascertained and they receive regularly scheduled (and often fixed rate) interest payments for the life of the bond regardless of Issuer’s loss or gain.

Capital Guarantee The capital is not guaranteed for sukuk holders. Upon maturity, Sukuk is valued based on the market value, a pre-arranged figure (agreed upon by the two parties) or a fair value.

The bond principal amount is guaranteed uon and payable upon maturity date.

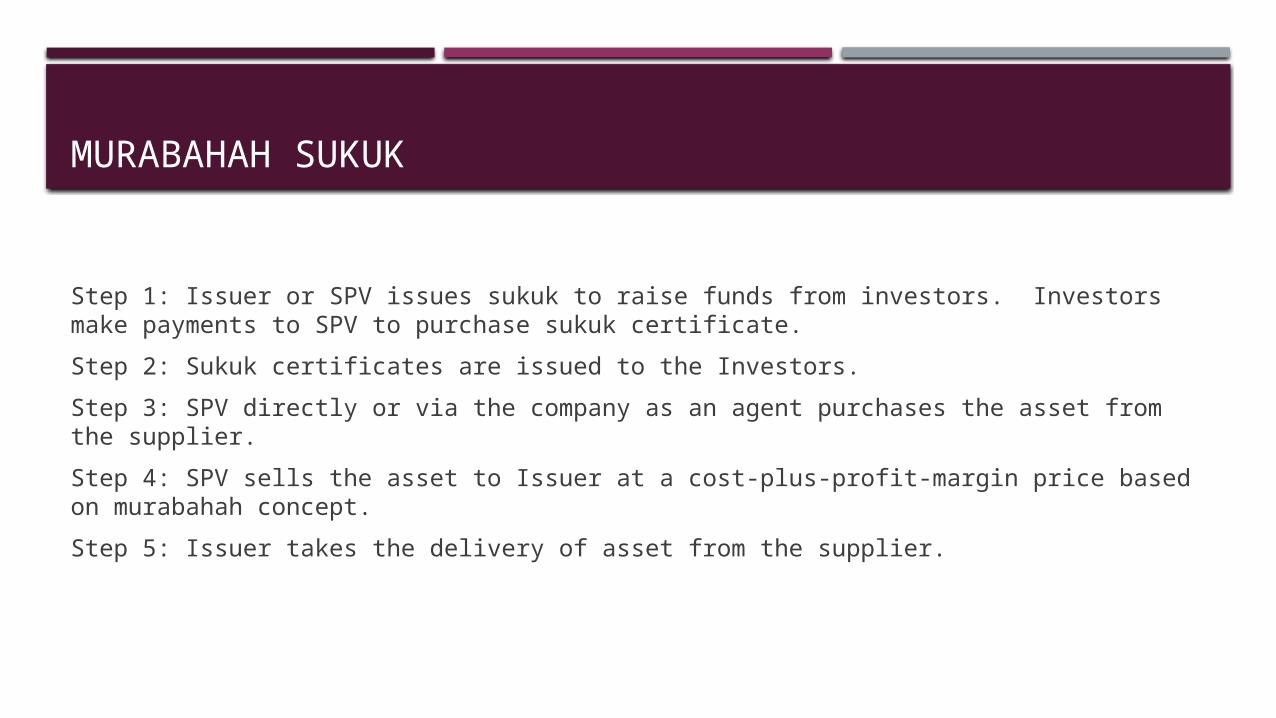

MURABAHAH SUKUK

Step 1: Issuer or SPV issues sukuk to raise funds from investors. Investors make payments to SPV to purchase sukuk certificate.

Step 2: Sukuk certificates are issued to the Investors.

Step 3: SPV directly or via the company as an agent purchases the asset from the supplier.

Step 4: SPV sells the asset to Issuer at a cost-plus-profit-margin price based on murabahah concept.

Step 5: Issuer takes the delivery of asset from the supplier.

MURABAHAH SUKUK

Step 6: Issuer makes periodic payment against the mark-up price to the SPV.

Step 7: SPV in turn distributes the payment for principal to investors.

BAI BITHAMAN AJIL SUKUK

Sukuk based on bai bithamin ajil (BBA) is a contract on a sale of an asset to the investors, with a promise by the issuer to buy the asset back in the future at a pre-determined price, which includes a margin of profit as well.

The difference between the two is that in BBA, disclosure of the cost price is not a condition and BBA is practiced for long term financing.

The BBA sukuk structure is similar to the Murabahah sukuk structure.

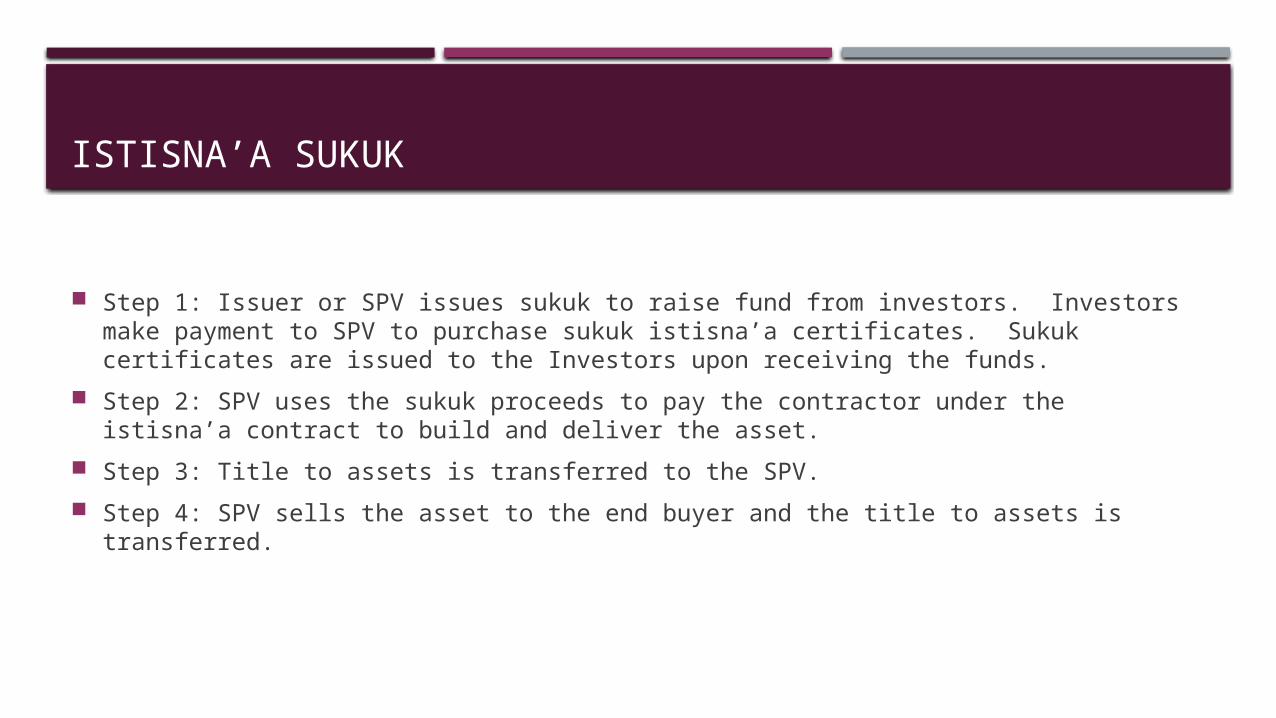

ISTISNA’A SUKUK

Step 1: Issuer or SPV issues sukuk to raise fund from investors. Investors make payment to SPV to purchase sukuk istisna’a certificates. Sukuk certificates are issued to the Investors upon receiving the funds.

Step 2: SPV uses the sukuk proceeds to pay the contractor under the istisna’a contract to build and deliver the asset.

Step 3: Title to assets is transferred to the SPV.

Step 4: SPV sells the asset to the end buyer and the title to assets is transferred.

ISTISNA’A SUKUK

Step 5: The end buyer makes periodic payments to the SPV.

Step 6: SPV in turn distributes the payment to investors.

Step 7: Upon completion, the asset is delivered to the end buyer.

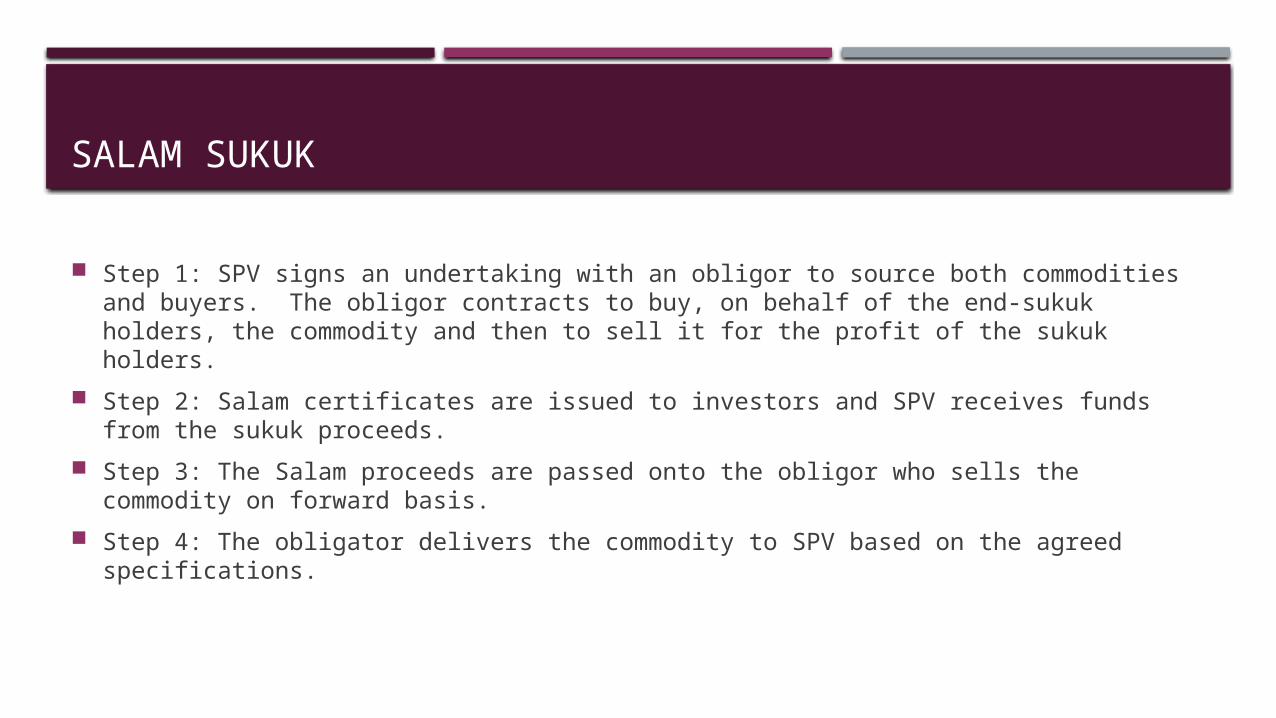

SALAM SUKUK

Step 1: SPV signs an undertaking with an obligor to source both commodities and buyers. The obligor contracts to buy, on behalf of the end-sukuk holders, the commodity and then to sell it for the profit of the sukuk holders.

Step 2: Salam certificates are issued to investors and SPV receives funds from the sukuk proceeds.

Step 3: The Salam proceeds are passed onto the obligor who sells the commodity on forward basis.

Step 4: The obligator delivers the commodity to SPV based on the agreed specifications.

SALAM SUKUK

Step 5: Obligor, on behalf of sukuk holders, sells the commodities for a profit.

Step 6: Sukuk holders receive the commodity sale proceeds or the sale price of the salam goos sold through a parallel salam.

IJARAH SUKUK

Ijarah sukuk are issued on a sale and lease back arrangement (ijarah) of real estate and have been a popular structure and is internationally accepted.

The sukuk holders get the right to own the unit of real estate, receive the rent and dispose of their sukuk in a manner that does not affect the right of the lessee, as it is easily tradable in the secondary market.

Ijarah sukuk are certificates of equal value evidencing the certificate holders undivided ownership of the leased asset and/or usufruct and/or services and rights to the rental receivables from the said leased asset and/or usufruct and/or services.”

IJARAH SUKUK

It represents title deeds of equal shares in a leasing project, usually equipment or real estate and entitles the holders the right to own shares, receive rental fees and/or dispose of their sukuk in a manner that does not affect the right of the lessee.

Sukuk holders bear all the cost of maintenance of and damage to the assets and to maintain it in such a manner that the lessee may derive as much usufruct from it as possible. Normally, the maintenance is assigned back to the issuer through an agency agreement.

IJARAH SUKUK

The duration of the rental and the fee are agreed in advance and ownership of the asset remains with the lessor.

Subject to risks related to the ability and desirability of the lessee to pay the rental instalments and risks arising from potential charges in asset-pricing and in maintenance and insurance costs.

The Issuer is required by Shari’ah law to undertake the major maintenance of the asset, but will often appoint the obligor/company to carry out such activity.

IJARAH SUKUK

The client or an obligor will sell one or some of its assets to a special purpose vehicle (SPV) to fulfill its monetary needs.

The SPV will finance the client and buy the asset by issuing ijarah sukuk equal to the amount of the asset’s purchase price.

The investors will own the part of the underlying asset as sukuk holders.

After the SPV buys the asset, it leases it back to the client for predetermined amount of money.

IJARAH SUKUK

The lease rental payments represent the periodical payments for the investors.

At maturity, the SPV will sell the asset back to the client for the same amount plus the late payment.

The investors will get their full amount of sukuk payment and their principal of the ijarah sukuk.

MUDHARABAH SUKUK

The investors subscribe to the certificates issued by a mudarib and share the profits and bear the losses arising from the mudharabah operations.

The returns to the holders are dependent on the revenue by the underlying investment.

MUDHARABAH SUKUK

Sukuk holders are considered to be owners of common shares in the mudharabah capital and all benefits and returns are related to the investor’s percentage of ownership in the capital.

The issuer of these certificates is the mudarib, the subscribers are the capital providers, and the realized funds are the mudharabah capital.

A mudharabah sukuk gives its owner the right to receive his capital at the time the sukuk are surrendered, and an annual proportion of the realized profits as agreed.

MUDHARABAH SUKUK

Upon the expiry of the specified period of the subscription, the sukuk holders are given the right to transfer the ownership by sale or trade in the securities market at their discretion.

Mudharabah sukuk neither yield interest nor entitle owners to make claims for many definite annual interest.

MUDHARABAH SUKUK

A mudarib can raise funds by issuing mudharabah sukuk to the investor.

The investors will buy sukuk under mudharabah agreement and will provide funds to the mudarib to execute the project or business.

The mudarib will provide an undertaking to buy back the asset.

Then, he will start working on the project and the profit that is generated from the project will be divided between the partners according to the predetermined percentage.

MUDHARABAH SUKUK

Revenues generated from the project are considered as the sukuk payments for the investors.

At maturity, if the project generates enough revenue for the mudarib to buy back the asset as per undertaking to pay off the sukuk holder, then, they will receive the face value and share of their dividends.

In the event the project does not generate sufficient revenue, the sukuk holders will either receive their principal and dividend later or they could be no payment at all.

MUSHARAKAH SUKUK

Musharakah sukuk are participatory types of investment sukuk that are based on profit-sharing terms and for mobilizing funds for establishing new large scale projects or developing existing ones, or financing business activities on the basis of equity partnerships.

The certificate holders become the owners of the project or the assets of the activity as per their respective shares as they are all considered to be the investors.

MUSHARAKAH SUKUK

It represents the ownership of the project or the assets of the activity as per their respective shares in the musharakah venture i.e profit and loss sharing business venture.

All providers of capital are entitled to participate in management, but is not necessarily required to do so. Normally, the issuer is appointed as the musharakah partners’ agent in managing the business.

The profit is distributed among the partners in pre-agreed ratios, while the loss is borne by every partner strictly in proportion to respective capital contributions.

MUSHARAKAH SUKUK

Musharakah sukuk is treated as negotiable instruments and can be bought and sold in the secondary market.

MUSHARAKAH SUKUK

Musharakah sukuk are issued for funding and the units of each partner for partnership are determined based on the investment need.

The funds from the sukuk will be utilized for executing the project.

The musharakah sukuk will be utilized for executing the project.

The musharakah sukuk certificate evidences the capital contribution of the investors and the ‘indicative rate of profit.’

Profit, if any, will be shared between the Issuer and Investors at an agreed sharing ratio.

MUSHARAKAH SUKUK

Financial loss will be borne by all certificate holders proportionate to their respective investment.

At maturity, if the project generates enough revenue for issuer to buy back the asset as per undertaking to pay off the sukuk holder and they will receive their face value and share of their dividends.

HYBRID SUKUK

It is a type of sukuk structure in which the underlying pool of assets consists of two or more Islamic finance contracts.

For example, the funds may be mobilized based on an istisna’a contract, an ijarah contract, and a mudarabah contract, all at the same time and within the same structure.

The hybrid structure enhances mobilization of funds as it allows the use of Shari’ah compatible financing contracts for refinancing means.

HYBRID SUKUK

It also bears resemblance to a conventional securitization structure, since debt receivables can be sold to a special purpose vehicle (SPV) over which the SPV entity issues bonds.

In a hybrid sukuk structure, the originator transfers tangible assets (which are the underlying of different contracts) to the special purpose vehicle.

In turn, the SPV issues sukuk to investors (who become the sukuk holders) and receives sukuk proceeds from them.

HYBRID SUKUK

The proceeds are used to pay the originator, while the revenues realized from the underlying assets are paid through to the sukuk holders.

At maturity, the originator purchases back the underlying assets from the SPV, while the sukuk holders receive fixed payments of return on assets (ROA) and the sukuk are paid off.

SUKUK PAYMENT STRUCTURES

Generally, the payments on the sukuk are structured in two forms:

1. The payments representing the amortising of the invested capital together with the profits (fixed or floating) derived from the investments. This is normally known as Amortising Securities or Amortising Sukuk.

2. The payments of the derived profits (fixed or floating) are made periodically during the tenure of the sukuk, while the payment that represents the invested sum is scheduled at the end of period i.e. at the final maturity date of the sukuk. This is normally known as non-amortizing securities or non-amortizing sukuk.

SUKUK PAYMENT STRUCTURES

However, there have been innovations whereby the redemptions to the sukuk are in the form of exchangeable such as equities or commodities.

In the case of exchangeable with equity, the periodic payments to the sukuk could be from the dividend income stream paid to the equity.

TRADABILITY OF SUKUK

The sukuk can be classified as tradable and non-tradable based on the underlying tangible assets or proportionate ownership of a business or investment portfolio.

Tradable sukuk are very essential for Islamic financial institutions to enable them to manage their short-term liquidity requirements.

TRADABLE SUKUK

Sukuk, to be tradable, must be owned by sukuk holders, with all rights and obligations of ownership in real assets, whether tangible, usfructs or services, capable of being owned and sold legally as well as in accordance with the rules of Shari’ah, relating to Articles (2)1 and (5/1/2)2 of the AAOIFI Shari’ah Standard (17) on Investment Sukuk.

The Manager issuing sukuk must certify the transfer of ownership of such assets in its (sukuk) books, and must not keep them as his own assets.

TRADABLE SUKUK

Sukuk, to be tradable, must not represent receivables or debts, except in the case of a trading or financial entity selling all its assets or a portfolio with a standing financial obligation, in which some debts, incidental to physical assets or usufruct, were included unintentionally, in accordance with the guidelines mentioned in AAOIFI Shari’ah Standard (21) on Financial Papers.

As per AAOIFI Sukuk based on ijarah, istisna’a, mudharabah, or musharakah principles are tradable. Non-tradable sukuk represent receivables of cash or goods. For example, sukuk of salam or murabahah are non-tradable sukuk.

TRADABLE SUKUK

In Malaysia, as per the resolution of the SAC of the SC, bai al dayn is permissible and it must be made in cash.

It recognizes bai al dayn or debt trading as one of the acceptable principles for sukuk issuances whereby Shari’ah compliant cash receivables arising from contracts such as murabahah, bai bithamin ajil (BBA), ijarah or istisna’a are converted into tradable debt instruments.

This enables tradability of debt and equity based sukuk in the secondary market in accordance with Shari’ah principles.

THE END