Understanding Reps & Warranties Insurance in M&A

14

Toll-free USA 800.380.7652 | Worldwide 408.717.4955 ShareVault.com ShareVault is a registered trademark of Pandesa Corporation, dba ShareVault Javier Enrile, Senior M&A Executive Understanding Reps & Warranties Insurance in M&A

Transcript of Understanding Reps & Warranties Insurance in M&A

Toll-free USA 800.380.7652 | Worldwide 408.717.4955

ShareVault.com

ShareVault is a registered trademark of Pandesa Corporation, dba ShareVault

Javier Enrile, Senior M&A Executive

Understanding Reps & Warranties Insurance in M&A

ShareVault | Understanding Reps & Warranties Insurance in M&A

1

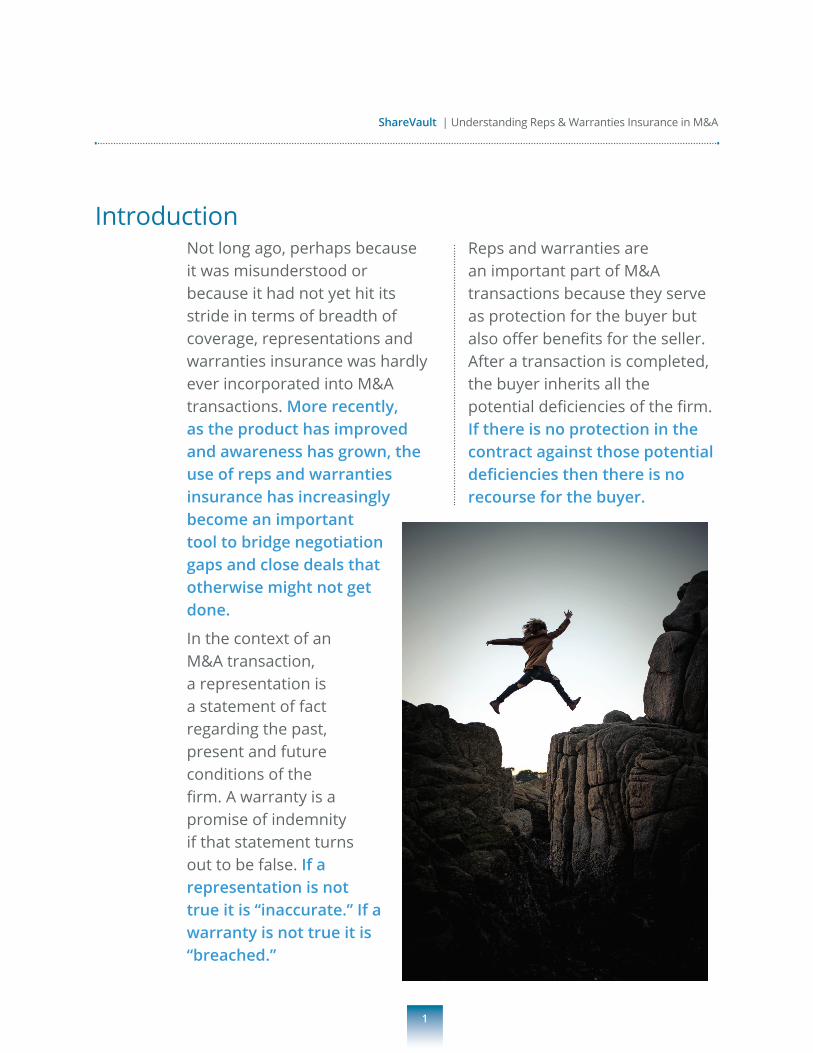

Not long ago, perhaps because it was misunderstood or because it had not yet hit its stride in terms of breadth of coverage, representations and warranties insurance was hardly ever incorporated into M&A transactions. More recently, as the product has improved and awareness has grown, the use of reps and warranties insurance has increasingly become an important tool to bridge negotiation gaps and close deals that otherwise might not get done.

In the context of an M&A transaction, a representation is a statement of fact regarding the past, present and future conditions of the firm. A warranty is a promise of indemnity if that statement turns out to be false. If a representation is not true it is “inaccurate.” If a warranty is not true it is “breached.”

Reps and warranties are an important part of M&A transactions because they serve as protection for the buyer but also offer benefits for the seller. After a transaction is completed, the buyer inherits all the potential deficiencies of the firm. If there is no protection in the contract against those potential deficiencies then there is no recourse for the buyer.

Introduction

ShareVault | Understanding Reps & Warranties Insurance in M&A

2

Traditionally, both parties in a transaction are protected by placing a portion of the purchase price in escrow. That money can be released to either party post-closing based on certain triggers that are defined in the contract. For example, if there were financial representations made by the seller that turn out to inaccurately represent a fair picture of the firm, a portion of the money held in escrow might be returned to the buyer. On the other hand, if the seller meets certain performance milestones, such as defined in an earnout structure, then money held in escrow might be paid to the seller.

Reps and warranties insurance is a different way of handling the same risk. When reps and warranties insurance is utilized in a purchase agreement, it means that an insurer underwrites the reps and warranties defined in the contract. Post-closing, if there is a breach in the seller’s representations then instead of making a claim against the seller and that money coming out of escrow, the buyer makes the claim against the insurer.

Imagine that you’ve purchased a technology firm that is run by two founders, both of whom essentially hold all of the intellectual property. They are also instrumental in the development of new intellectual property, so they’re critical to the future of the business. The two founders have a relationship with all of the company’s clients; they’re the face of the firm. Essentially, they are the assets that you as a buyer are buying.

Several months after closing the transaction you discover that there is some discord between the two founders and one of them is threatening to leave the firm. This turmoil eventually becomes known to the company’s clients resulting in a 50% decline in revenue. After investigating a bit more, you discover that the two founders were threatening to sue each other before the transaction closed.

Reps and warranties insurance protects the buyer from this type of unknown. If a statement of fact turns out to be incorrect post-transaction then the buyer can make a claim against the insurer and recoup their losses.

ShareVault | Understanding Reps & Warranties Insurance in M&A

3

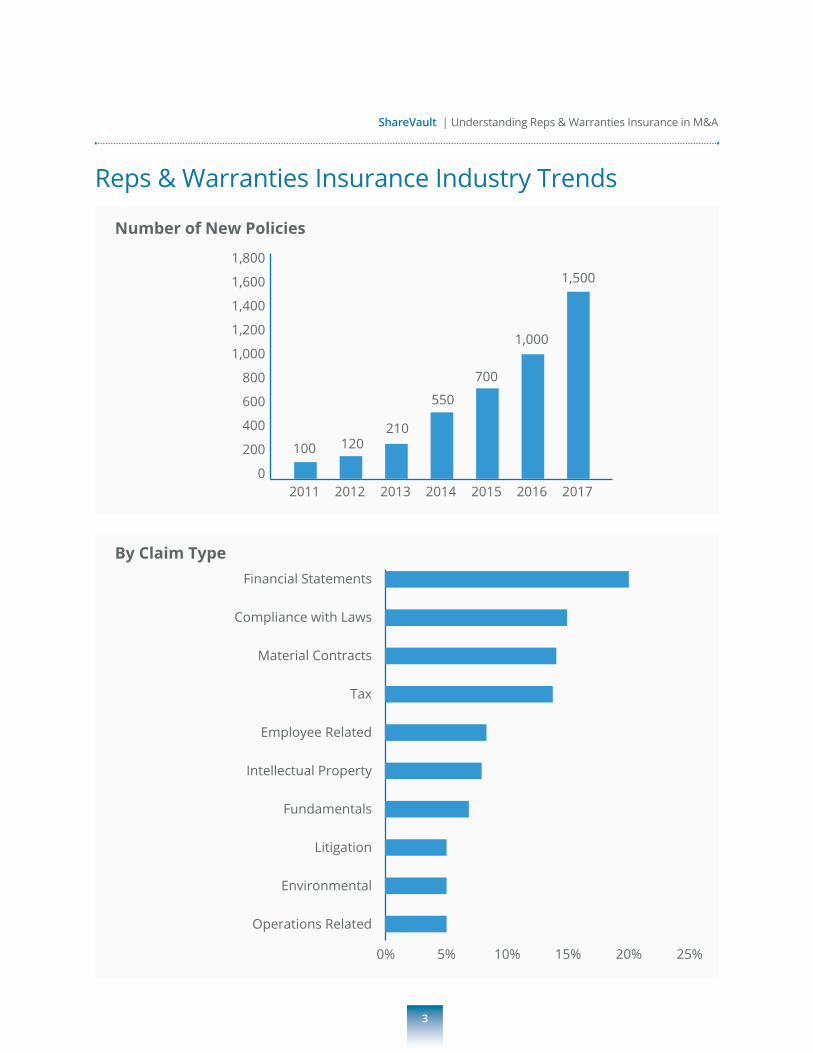

Reps & Warranties Insurance Industry Trends

By Claim Type

0% 10% 20%5% 15% 25%

Financial Statements

Compliance with Laws

Material Contracts

Tax

Employee Related

Intellectual Property

Fundamentals

Litigation

Environmental

Operations Related

Number of New Policies

02011

100

2012

120

2013

210

2014

550

2015

700

2016

1,000

1,500

2017

200

400

600

800

1,000

1,200

1,400

1,600

1,800

ShareVault | Understanding Reps & Warranties Insurance in M&A

The reps and warranties section of an M&A agreement can be 20 or 30 pages. When insurance is in place, sellers are much more amenable to agreeing to a broader range of representations and

warranties because the risk has been shifted from them to the insurance company. This reduces the time and energy it takes to negotiate the multitude of reps and warranties that are a part of most transactions.

4

Three Reasons Reps & Warranties Insurance Is Gaining Traction

Benefits for the Transaction

Benefits for the Seller

12

3

Broader Coverage

Better Pricing

Proven Product (Claims are getting paid)

Benefit number one for the seller is security over the proceeds. For example, let’s say the buyer and the seller have agreed on a purchase price of $100M. Traditionally, a portion of that money will be held in escrow. If, post-closing, there’s a breach of warranty, then money will come out of escrow and be paid to the buyer. So, instead of getting $100M the seller may only get $90M.

When reps and warranties insurance is in place the proceeds go to the seller in full. There’s no escrow and there’s no scenario where the seller has to pay money back for breaches of warranty; the insurer covers those breaches. So, while the seller has to pay the premium, they have the benefit of knowing that they’re going to get the full $100M.

ShareVault | Understanding Reps & Warranties Insurance in M&A

5

Another benefit is when there are passive sellers involved. They may be responsible for the fundamental warranties, but not all the warranties. Passive

sellers will be very uneasy being responsible for the full gamut of warranties, so they’ll be very happy to see insurance in place.

The primary benefit of insurance for the buyer is that it reduces counterparty risk. Normally, if there’s a breach of warranty, the buyer has to make a claim against the seller. That involves risk because the seller could declare bankruptcy and claim they have no money. With the insurance that risk is shifted. The buyer doesn’t have to worry about the seller’s ability to pay because the claim goes against the insurance firm, which is a much better credit risk for the buyer.

The second benefit for the buyer is that when insurance is in place, sellers, knowing they’re protected, will generally agree to giving more coverage and broaden the scope of the warranties. That’s obviously good for the buyer.

The third benefit is relational. Very often the management

of the firm that the buyer is acquiring continues with the business. They’re colleagues. In that situation, if there’s a breach of warranty, then the buyer’s recourse is to engage in litigation. Essentially, they’re suing the folks they’re working with. When insurance is in place, that claim is made against the insurer, which makes things much easier.

Reps and warranties insurance is also a way for buyers to make their offer more appealing. When insurance is in place, indemnity for sellers is reduced or eliminated making the offer more attractive.

The final benefit for the buyer is that the insurance will typically cover fraud. Without insurance, the buyer’s only recourse is with the law. The buyer has to sue the seller. This could be litigation against a management team—

Benefits for the Buyer

ShareVault | Understanding Reps & Warranties Insurance in M&A

6

your colleagues—who you’ve been working with on a day-to-day basis for a long time. When

insurance is in place and there’s fraud, that claim is simply made against the insurance.

Reps and warranties insurance can be structured from both the buy side and the sell side. About 80% of policies in the US are structured from the buy side.

Pricing, Retention, Survival Periods & Exclusions

Typically, the maximum amount the insurance will cover is a percentage of the purchase price, usually anywhere from 10 to 20 percent. If the purchase price of the transaction is $100M, the insurance might cover breaches from $10M to $20M.

There is also the element of retention. Retention is very much like an insurance deductible. It’s the amount of losses that must be incurred before the insurer honors a claim. Retention is typically an expense shared between the buyer and the seller. Retention rates are typically 1 to 3 percent

of the limit of coverage.

The survival period defines how long the insurance provides coverage. Typically, reps and warranties protection lasts 12 to 18 months. However, with insurance, the protection can be anywhere from 3 years for warranty breaches to 6 years for more fundamental representations and tax filings.

The fourth element is exclusions. Essentially, there are two types of exclusions. There is the standard one, which is essentially things that insurance never covers, such as purchase price adjustments and things known at the time of the transaction. Then there are specific representations spelled out during the transaction, perhaps because they are very broad, that the insurance company will not be comfortable covering so they will be excluded.

Common Structures

ShareVault | Understanding Reps & Warranties Insurance in M&A

7

Common Buyer Structure($100 Purchase Price)

$100 Purchase Price

$10 Escrow/Indemnity Gap

$90 Proceeds$99.2 Proceeds

$0.5 Escrow

$0.3 Premium

$100 Purchase Price

Absent reps and warranties insurance at a $100M purchase price the seller indemnity cap and corresponding escrow are assumed at 10 percent of the purchase price. With reps and warranties insurance, a seller can reduce their indemnity cap and escrow down to 0.5% of the purchase price to satisfy half of the retention under the

policy at 1% (the other half is assumed to be covered by the buyer). This allows the seller to receive more proceeds. In the first scenario, the seller could be on the hook for the full amount placed in escrow, or $10M. In the second scenario, the seller is paying $500,000 in premiums, but is receiving $99.2M in proceeds.

The Process—How It WorksTypically at the beginning of an M&A transaction, either the buyer or the seller will approach

an insurance broker and discuss the general parameters of the insurance and what the

ShareVault | Understanding Reps & Warranties Insurance in M&A

8

objectives are. Armed with that information, the insurance broker will require some basic information from both the buyer and the seller, such as the most recent version of the purchase price agreement, a management presentation, an investment memorandum, an audit or management accounts from the seller. The broker will then go out and solicit quotes from different insurance firms and present them to the requesting party. The buyer or seller then selects the one that is most beneficial to them and the underwriting commences. The insurance company will then require access to the data room and all the transaction documents, schedules, and reports being produced by third parties and consultants. They will also have meetings with the deal team and specific subject matter experts on each of the functional work streams to fully understand the due diligence process.

After that process is complete the buyer or seller will receive a draft policy from the insurance company and negotiations will begin. There may be some

negotiations about pricing and terms, but for the most part, the negotiations will focus on exclusions.

If the insurance company is uncomfortable covering certain warranties, the insured party has two options. One is to provide more information with the hope that the insurance company becomes comfortable with insuring it. The other is for both parties to agree that that representation and warranty is not going to be covered by the insurance.

There may be other represen-tations and warranties that the insurance company is uncomfortable covering not because there’s a lack of due diligence, but because the scope of the representation is too broad. In that case, the rep and warranty may have to be refined so that it is more specific or narrower so that the insurance is comfortable covering it.

The other situation that can arise is that the seller has agreed to a warranty on the condition that it will be covered by the insurance. If the insurance company excludes that warranty

ShareVault | Understanding Reps & Warranties Insurance in M&A

9

from the policy then the buyer must renegotiate with the seller. So, policy negotiations are not just with the insurance company; they will also involve a back and forth with the seller.

The last step in the process is binding and issuing the policy. When a policy is “bound” it means that the policy is in place although it

has yet to be “issued.” Often, binding takes place through a verbal agreement, in person or over the telephone. It can also occur through electronic communication, such as an email or text message. Binders are typically valid for 30 days, by which time the actual policy should be issued.

Two Case Studies

Case Study 1:

In this scenario, there was a representation in the contract that there was no threatened or pending litigation against the selling firm or among its employees and shareholders. Months later the buyer discovers that, in fact, there was threatened litigation between the founders of the firm, which has resulted in significantly reduced revenue.

As a result, the buyer makes a claim with the insurance company and provides them with evidence that there has been a breach of warranty. The insurance firm agrees that there was, in fact, a breach of warranty and that the evidence quantifying the loss is credible and they pay back the buyer for the full amount of the loss.

In this case, being able to approach the insurance company with the claim, and not the seller, made the process much easier. The seller is also happy because the insurance company has paid the buyer for the loss rather than that money coming out of the seller’s escrow.

ShareVault | Understanding Reps & Warranties Insurance in M&A

10

Case Study 2:

In this scenario, there’s a manufacturing firm being acquired by another manufacturing firm. The nature of the business means that there are significant receivables and inventory. After closing the transaction, the buyer decides to take the company public. They perform an audit on the firm’s earnings, the same earnings they used to value the firm before buying it, and the audit uncovers that the inventory of receivables was undervalued substantially therefore what they paid for the firm was overvalued.

As a result, the buyer makes a claim against the insurance company based on the fact that the firm’s financial statements were inaccurate and that they were not following GAP rules. After reviewing the forensic evidence, the insurance company agrees that there was a financial statement warranty breach and they pay the buyer back a portion of the purchase price. It’s important to understand in this case that the buyer both produced evidence that the warranty was breached, but also was able to quantify the loss.

Q&AQ: Are there any specific information gaps that can lead to elongation of the underwriting process or time frame?

A: Let’s assume the firm being purchased is a technology firm that is heavily dependent on intellectual property. The buyer is very comfortable with the IP so they don’t feel the need to incur the cost of in-depth due diligence. The insurance company, on the other hand,

will want to ensure that the critical assets of the firm and other critical sources of value have been subjected to rigorous due diligence before insuring the reps and warranties associated with those assets. When an insurance company is uncomfortable with a warranty due to lack of information, they are either going to exclude that warranty from the policy or require more due diligence from the buyer. This obviously draws out the process.

ShareVault | Understanding Reps & Warranties Insurance in M&A

11

It’s also important to remember that once a draft of the policy has been completed, it’s often more difficult to change the insurer’s mind. It’s better to provide the insurance company with in-depth due diligence at the outset than to iterate the information later on.

Q: Who pays for the policy, the buyer or the seller?

A: It can be either. In many cases the seller will pay for the policy because having insurance in place avoids the need for a portion of the purchase price to be put in escrow; instead, they get the entire purchase price upfront and there is no risk. In other cases, especially if there is a very competitive sale process or auction, the buyer will purchase the insurance

because it makes their bid more attractive to the seller.

Q: For cross-border deals, do you have any specific recommendations for sellers in terms of selecting reps and warranties vendors? Do they need an in-country office?

A: That probably depends on whether the local insurance company is comfortable underwriting the risk associated with the transaction’s reps and warranties. A lot of reps and warranties have legal and regulatory issues that might require expertise from someone from that particular country. In that case, a local office might be essential. It really comes down to what the insurance company is comfortable underwriting.

ShareVault | Understanding Reps & Warranties Insurance in M&A

About Javier EnrileJavier is a senior executive with 15 years of experience in corporate M&A, private equity, venture capital, and corporate development/strategy.

Having a strong track record as a principal investor and operator, Javier has built significant domain expertise in the financial services industry with a focus in the investment management, fintech, payments, retirement, and insurance sectors. Additionally, Javier has transacting and operating experience in the US, Europe, Asia, and Latin America.

Javier has played leadership roles in all phases of the M&A investment process: strategy design and formulation, deal sourcing, screening, valuation/return/financial analysis, investment memorandum, investment committee/board approvals, structuring, negotiations, due diligence, integration, and post-investment support for portfolio companies (e.g., business management, FP&A, financial reporting, strategic planning, and growth initiatives).

Currently, Javier is leading the private investments practice - a family office (primarily seed and Series A investments). Most recently, Javier was the Managing Director of M&A at Principal Global Investors. He is an accomplished author with numerous publications on M&A topics.

12

About ShareVaultShareVault® is the industry leader in supplying intuitive, innovative virtual data rooms that provide a simple and secure way to share sensitive documents with third parties during the due diligence process.

The on-demand platform is an innovative cloud-computing solution that enables its customers to manage critical time-sensitive and document-centric processes faster and more intuitively. ShareVault offers the highest degree of security and reliability combined with unparalleled speed, ease of use and functionality. Backed by the experience of billions of dollars in successful deal transactions, along with industry-leading customer support, ShareVault can be a critical tool in accelerating deal transaction times and increasing deal success rates.

For more information, visit www.sharevault.com or email [email protected].