Understanding MARYLAND TAXES TAX YEAR...

42

Understanding MARYLAND TAXES TAX YEAR 2013 Comptroller of Maryland January, 2014

Transcript of Understanding MARYLAND TAXES TAX YEAR...

Understanding MARYLAND TAXES

TAX YEAR 2013

Comptroller of Maryland January, 2014

1

Understanding Maryland Taxes is an online publication prepared by the Maryland Comptroller’s Office to help you understand Maryland state and local taxes, gain competence in math and social studies, and develop financial responsibility.

The material is designed to be used as the state and local tax module for Understanding Taxes material provided by the Internal Revenue Service.

You can download copies of the Understanding Maryland Taxes course on our Web site www.marylandtaxes.com, where you can learn about our online services and explore other helpful information about personal and business taxes.

Feel free to e-mail your comments or questions to [email protected].

Editor: Michael Abii

Revenue Administration Division Comptroller of Maryland

Annapolis, Maryland

E-mail: [email protected]

2

Table of Contents Understanding Maryland Taxes ……………………………………………………… 3 History of Taxes ……………………………………………………… 4 Timeline of Maryland Taxes ……………………………………………………… 6 State and Local Taxes ……………………………………………………… 9 State Taxes ……………………………………………………… 10 Local Taxes ……………………………………………………… 18 Activity #1 ……………………………………………………… 20 Activity #2 ……………………………………………………… 22 Activity #3 ……………………………………………………… 30 Where the Money Comes From ……………………………………………………… 40 Where the Money Goes ……………………………………………………… 41

3

Understanding Maryland Taxes Purpose: To help students understand that state and local governments need revenue to

provide goods and services for their citizens.

Objectives: Students will learn about the history of taxes in Maryland, and the kinds of taxes collected by Maryland state and local governments.

Students will also learn how to complete simple state tax forms, and to determine if they are exempt from employer withholding of income tax.

Content: This course material is presented in three sections: Maryland tax history, state and local taxes, and activities that include class projects regarding tax policy, as well as practical skills while completing tax forms.

Activity #1: This activity is designed to help students explore economic principles that affect government policy.

Activities #2 and #3: These activities can help students to develop mathematical skills and

financial responsibility. Students who have part-time jobs may find the section regarding the “exemption from withholding” especially useful.

Note: The materials are designed to help students become more successful in mathematics and social studies.

4

History of Taxes How do you think people paid for goods and services in earlier times? Almost anything you can imagine has been used as “money” at one time or another—from salt and shells to furs and fish. As time went on, people found a more practical and durable kind of money—namely coins made of gold and silver.

When did people start using paper money? Paper money became popular in Europe during the 1600s. It didn’t show up in North America until 1685, when playing cards began to be used as currency in Canada.

How did the currency system develop in Maryland? After Maryland was settled on March 25, 1634, tobacco soon became the most important currency in the growing colony. Official salaries, payments to members of the clergy, the cost of public buildings, and other obligations were fixed in pounds of tobacco.

In 1733, the Maryland legislature passed a paper currency bill, which provided for coins and paper money to be used as a substitute for tobacco. Tobacco remained as a legal means to pay debts until 1776.

When did Maryland impose an income tax? Although the state of Maryland imposed an income tax law as early as 1777. (later to be repealed and followed by another income tax law in 1840), it did not become a regular tax until 1937.

The lingering Depression of the 1930s prompted Maryland’s legislature to pass several social and welfare laws to ease hardships. To increase revenue, Maryland’s state income tax was proposed by a state constitutional amendment in 1937.

Maryland started collecting the modern income tax in 1939. The law set the income tax rate at one-half of one percent.

During the first filing season, 110,240 taxpayers paid approximately $1 million in state income

taxes. Today, the state income tax is Maryland’s largest single source of general fund revenue.

When did Maryland impose a sales tax? In 1947, faced with a desperate need for revenue to pay for services and projects delayed by World War II, the General Assembly imposed a 2 percent tax on retail sales. During the first year, the sales tax generated $23.6 million.

The sales and use tax is the second largest source of general fund revenue.

Are social changes reflected in tax policy? Maryland began taxing motor fuel with a gasoline tax of one cent per gallon in 1922, when automobiles began rolling towards their dominant role in the transportation scene. Alcoholic beverages became subject to state taxation after the repeal of Prohibition in 1933.

Suburban growth in the decades that followed set the stage for a greater role for local governments, and the creation of a local income tax in 1968.

The digital age opened the door for a host of computerized services allowing people and businesses to file and pay their taxes online over the Internet. The rapid growth of Internet

5

shopping has also prompted many states to consider changing their local laws and procedures affecting taxation of retail sales.

Comptroller Franchot continues to fight for Maryland students by pushing for a high school graduation requirement in personal finance.

6

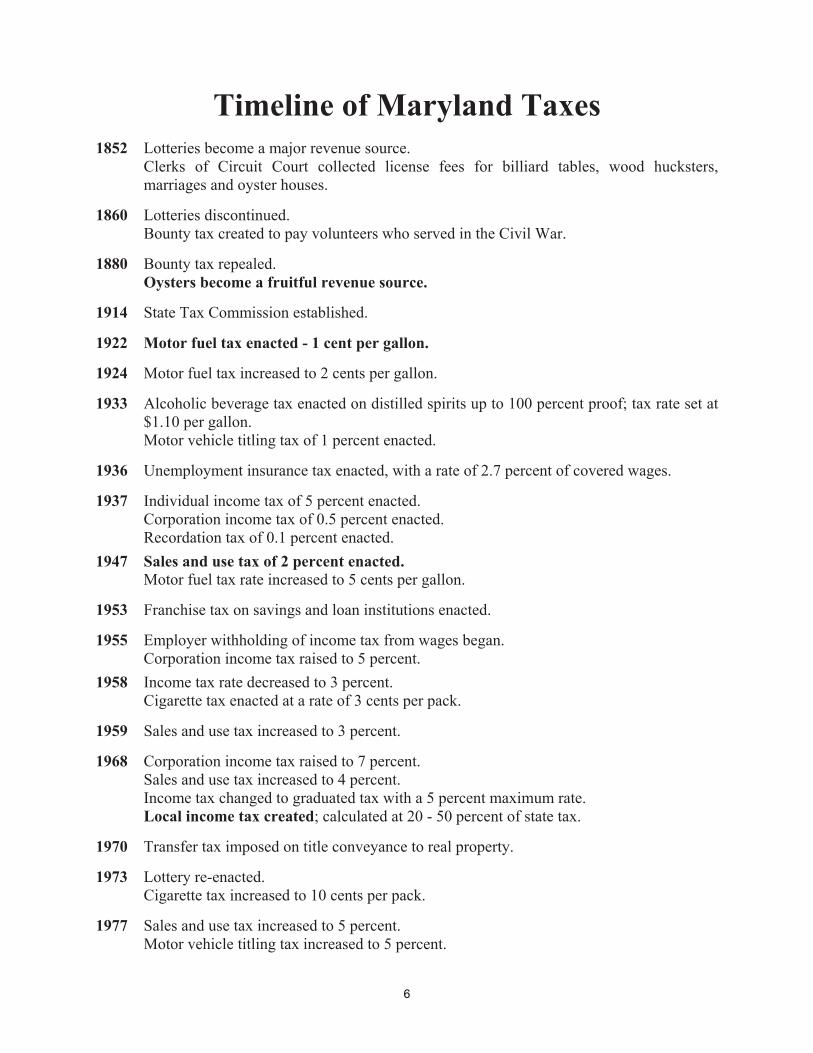

Timeline of Maryland Taxes 1852 Lotteries become a major revenue source. Clerks of Circuit Court collected license fees for billiard tables, wood hucksters,

marriages and oyster houses.

1860 Lotteries discontinued. Bounty tax created to pay volunteers who served in the Civil War.

1880 Bounty tax repealed. Oysters become a fruitful revenue source.

1914 State Tax Commission established.

1922 Motor fuel tax enacted - 1 cent per gallon.

1924 Motor fuel tax increased to 2 cents per gallon.

1933 Alcoholic beverage tax enacted on distilled spirits up to 100 percent proof; tax rate set at $1.10 per gallon.

Motor vehicle titling tax of 1 percent enacted.

1936 Unemployment insurance tax enacted, with a rate of 2.7 percent of covered wages.

1937 Individual income tax of 5 percent enacted. Corporation income tax of 0.5 percent enacted. Recordation tax of 0.1 percent enacted.

1947 Sales and use tax of 2 percent enacted. Motor fuel tax rate increased to 5 cents per gallon.

1953 Franchise tax on savings and loan institutions enacted.

1955 Employer withholding of income tax from wages began. Corporation income tax raised to 5 percent.

1958 Income tax rate decreased to 3 percent. Cigarette tax enacted at a rate of 3 cents per pack.

1959 Sales and use tax increased to 3 percent.

1968 Corporation income tax raised to 7 percent. Sales and use tax increased to 4 percent. Income tax changed to graduated tax with a 5 percent maximum rate. Local income tax created; calculated at 20 - 50 percent of state tax.

1970 Transfer tax imposed on title conveyance to real property.

1973 Lottery re-enacted. Cigarette tax increased to 10 cents per pack.

1977 Sales and use tax increased to 5 percent. Motor vehicle titling tax increased to 5 percent.

7

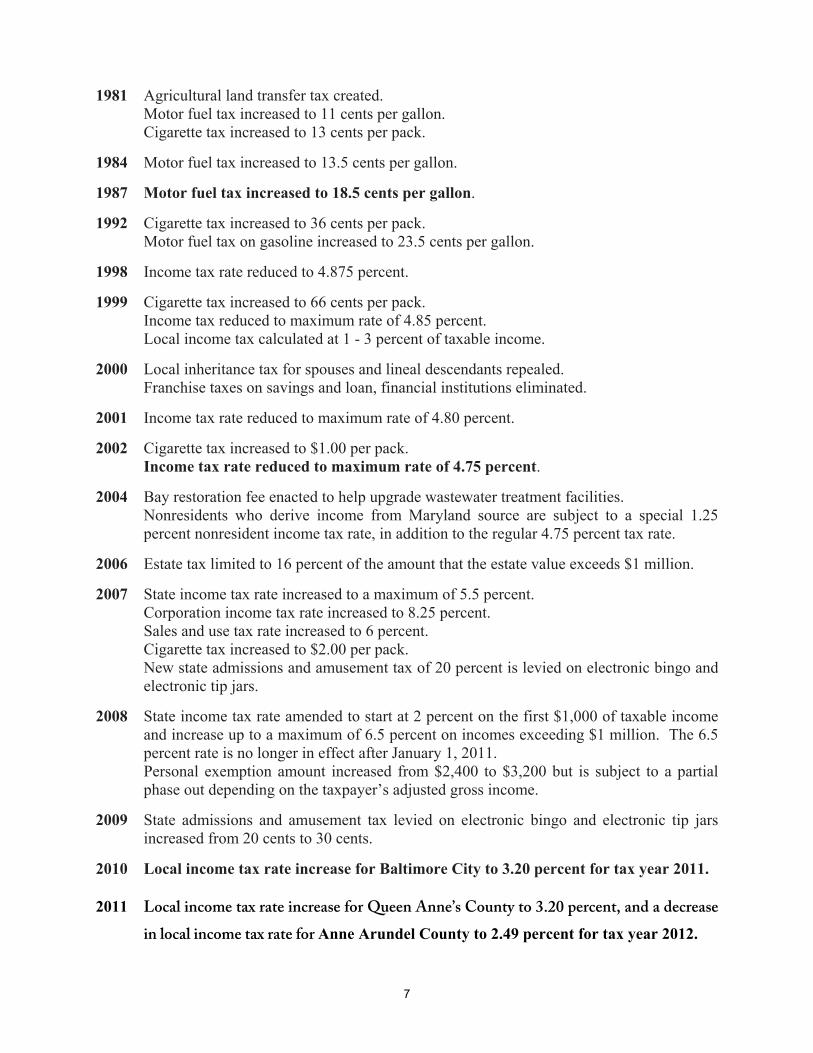

1981 Agricultural land transfer tax created. Motor fuel tax increased to 11 cents per gallon. Cigarette tax increased to 13 cents per pack.

1984 Motor fuel tax increased to 13.5 cents per gallon.

1987 Motor fuel tax increased to 18.5 cents per gallon.

1992 Cigarette tax increased to 36 cents per pack. Motor fuel tax on gasoline increased to 23.5 cents per gallon.

1998 Income tax rate reduced to 4.875 percent.

1999 Cigarette tax increased to 66 cents per pack. Income tax reduced to maximum rate of 4.85 percent. Local income tax calculated at 1 - 3 percent of taxable income.

2000 Local inheritance tax for spouses and lineal descendants repealed. Franchise taxes on savings and loan, financial institutions eliminated.

2001 Income tax rate reduced to maximum rate of 4.80 percent.

2002 Cigarette tax increased to $1.00 per pack. Income tax rate reduced to maximum rate of 4.75 percent.

2004 Bay restoration fee enacted to help upgrade wastewater treatment facilities. Nonresidents who derive income from Maryland source are subject to a special 1.25

percent nonresident income tax rate, in addition to the regular 4.75 percent tax rate.

2006 Estate tax limited to 16 percent of the amount that the estate value exceeds $1 million.

2007 State income tax rate increased to a maximum of 5.5 percent. Corporation income tax rate increased to 8.25 percent. Sales and use tax rate increased to 6 percent. Cigarette tax increased to $2.00 per pack.

New state admissions and amusement tax of 20 percent is levied on electronic bingo and electronic tip jars.

2008 State income tax rate amended to start at 2 percent on the first $1,000 of taxable income and increase up to a maximum of 6.5 percent on incomes exceeding $1 million. The 6.5 percent rate is no longer in effect after January 1, 2011.

Personal exemption amount increased from $2,400 to $3,200 but is subject to a partial phase out depending on the taxpayer’s adjusted gross income.

2009 State admissions and amusement tax levied on electronic bingo and electronic tip jars increased from 20 cents to 30 cents.

2010 Local income tax rate increase for Baltimore City to 3.20 percent for tax year 2011. 2011 Local income tax rate increase for Queen Anne’s County to 3.20 percent, and a decrease

in local income tax rate for Anne Arundel County to 2.49 percent for tax year 2012.

8

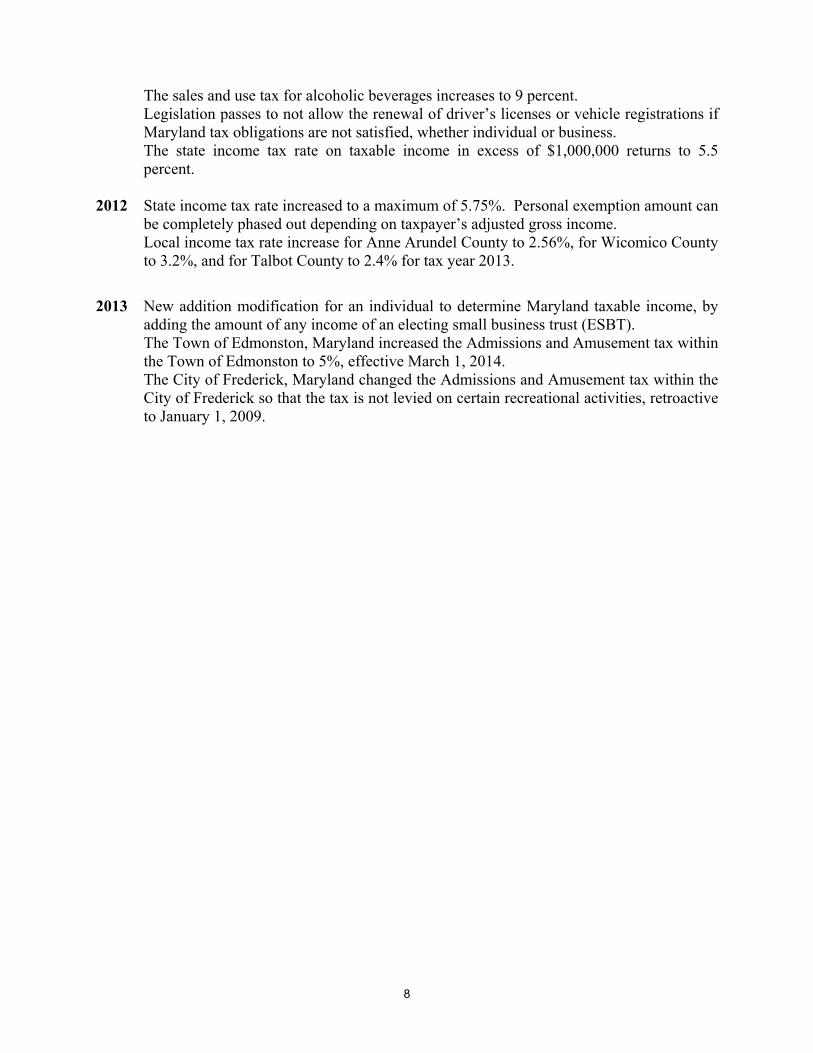

The sales and use tax for alcoholic beverages increases to 9 percent. Legislation passes to not allow the renewal of driver’s licenses or vehicle registrations if Maryland tax obligations are not satisfied, whether individual or business. The state income tax rate on taxable income in excess of $1,000,000 returns to 5.5 percent.

2012 State income tax rate increased to a maximum of 5.75%. Personal exemption amount can be completely phased out depending on taxpayer’s adjusted gross income.

Local income tax rate increase for Anne Arundel County to 2.56%, for Wicomico County to 3.2%, and for Talbot County to 2.4% for tax year 2013.

2013 New addition modification for an individual to determine Maryland taxable income, by adding the amount of any income of an electing small business trust (ESBT).

The Town of Edmonston, Maryland increased the Admissions and Amusement tax within the Town of Edmonston to 5%, effective March 1, 2014.

The City of Frederick, Maryland changed the Admissions and Amusement tax within the City of Frederick so that the tax is not levied on certain recreational activities, retroactive to January 1, 2009.

9

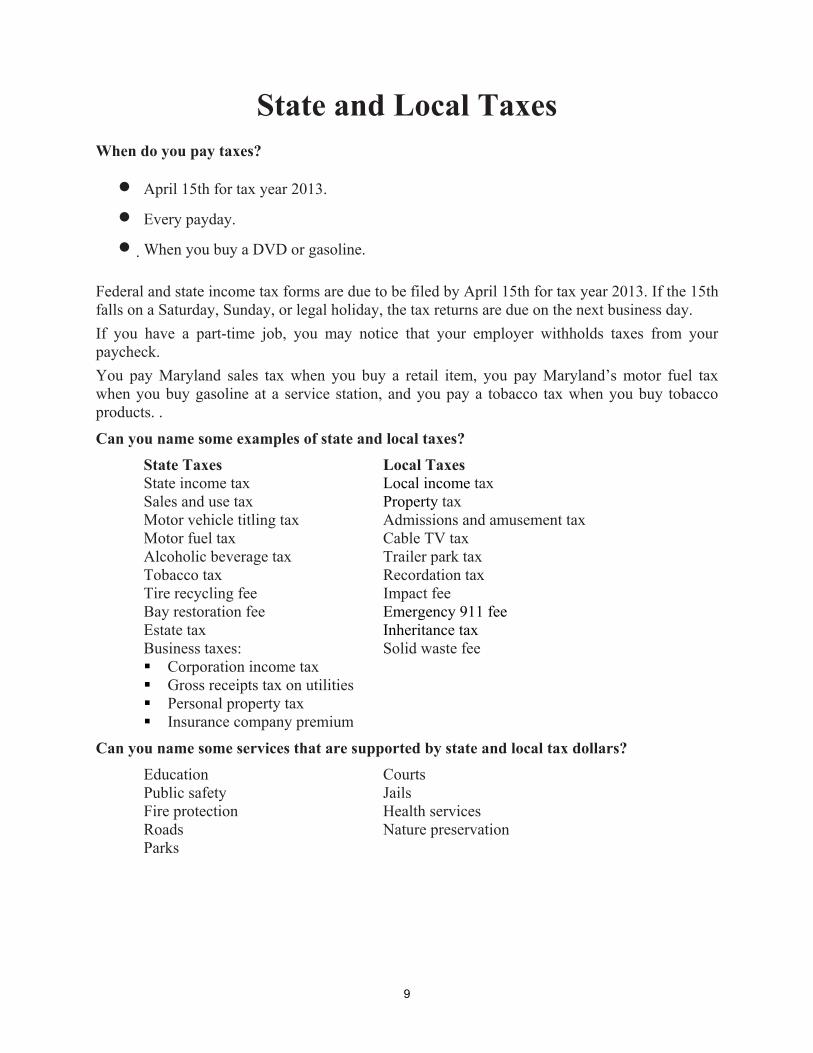

State and Local Taxes When do you pay taxes?

April 15th for tax year 2013.

Every payday.

When you buy a DVD or gasoline.

Federal and state income tax forms are due to be filed by April 15th for tax year 2013. If the 15th falls on a Saturday, Sunday, or legal holiday, the tax returns are due on the next business day.

If you have a part-time job, you may notice that your employer withholds taxes from your paycheck.

You pay Maryland sales tax when you buy a retail item, you pay Maryland’s motor fuel tax when you buy gasoline at a service station, and you pay a tobacco tax when you buy tobacco products. .

Can you name some examples of state and local taxes?

State Taxes Local Taxes State income tax Local income tax Sales and use tax Property tax Motor vehicle titling tax Admissions and amusement tax Motor fuel tax Cable TV tax Alcoholic beverage tax Trailer park tax Tobacco tax Recordation tax Tire recycling fee Impact fee Bay restoration fee Emergency 911 fee Estate tax Inheritance tax Business taxes: Solid waste fee

Corporation income tax Gross receipts tax on utilities Personal property tax Insurance company premium

Can you name some services that are supported by state and local tax dollars?

Education Courts Public safety Jails Fire protection Health services Roads Nature preservation Parks

10

State Taxes Personal Income Tax

In most states, including Maryland, the earnings of both individuals and corporations are taxed.

Maryland’s graduated personal income tax rates start at 2 percent on the first $1,000 of taxable income, and increase up to a maximum of 5.75 percent on taxable income exceeding $250,000 or $300,000 depending on the filing status of the taxpayer. Nonresidents who derive income from a Maryland source are subject to a special nonresident tax rate of 1.25 percent, in addition to the state income tax rate.

A taxpayer earns income during the year from many sources, including wages, interest from bank accounts, stock dividends and tips. This income is subject to tax.

Most personal income tax is withheld from an employee’s pay and sent to the State Comptroller’s Office regularly by the employer.

The state income tax is Maryland’s largest single source of general fund revenue.

Estimated Income Tax

The filing of a declaration of estimated Maryland income tax is a part of the pay-as-you-go plan of income tax collection adopted by the state.

If you have any income such as business income, lottery, capital gains, interest, dividends, etc., from which no tax is withheld, or wages from which not enough Maryland tax is withheld, you may have to pay estimated taxes.

How do you know if you are exempt from having to file a Maryland income tax return?

Maryland income tax law is based on federal law, with some important exceptions. State tax law treats students as single individuals, which means you are subject to the same filing requirements as a single individual. If you earned less than $10,000 in calendar year 2013, you generally are not required to file a Maryland tax return.

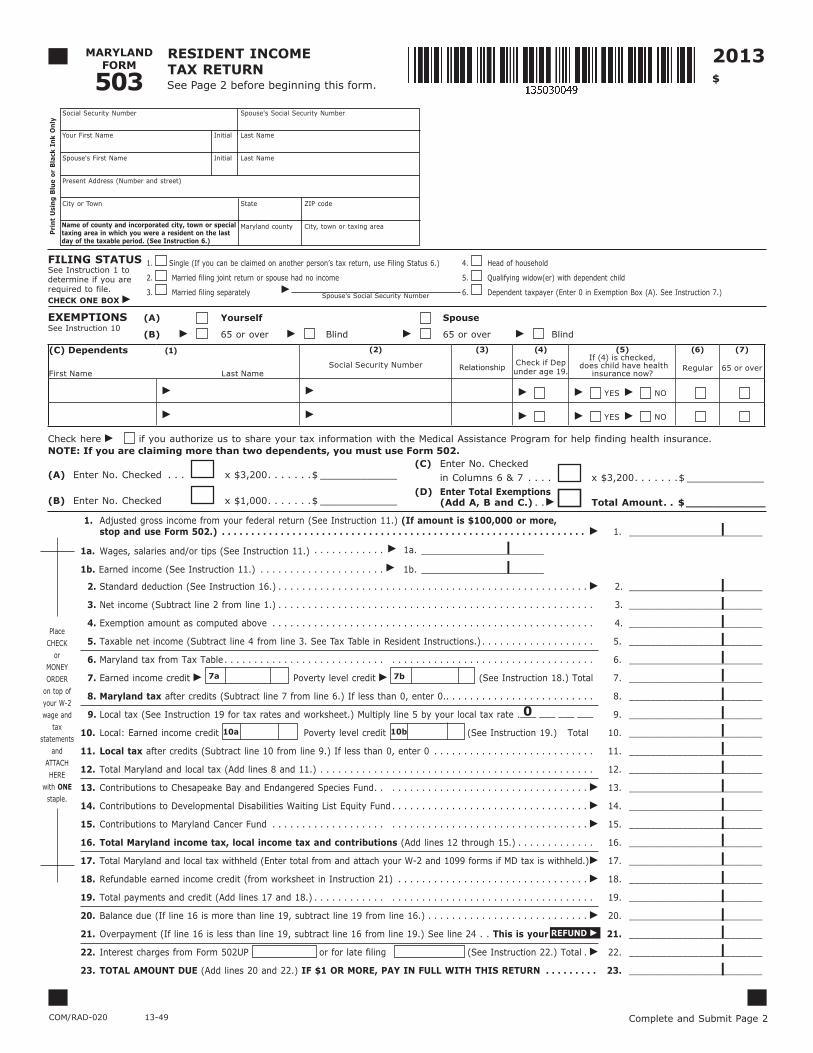

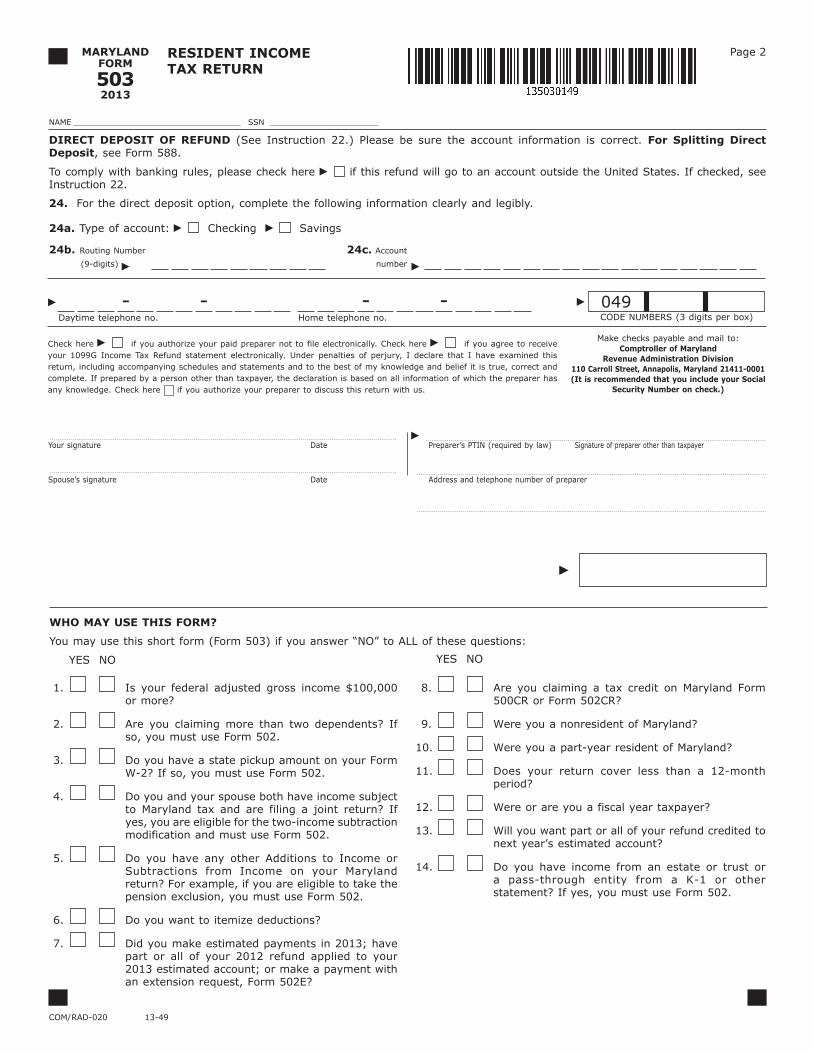

If you are not required to file but you had state and local income taxes withheld from your paycheck, you can get a refund of state and local taxes paid by filing short Form 503.

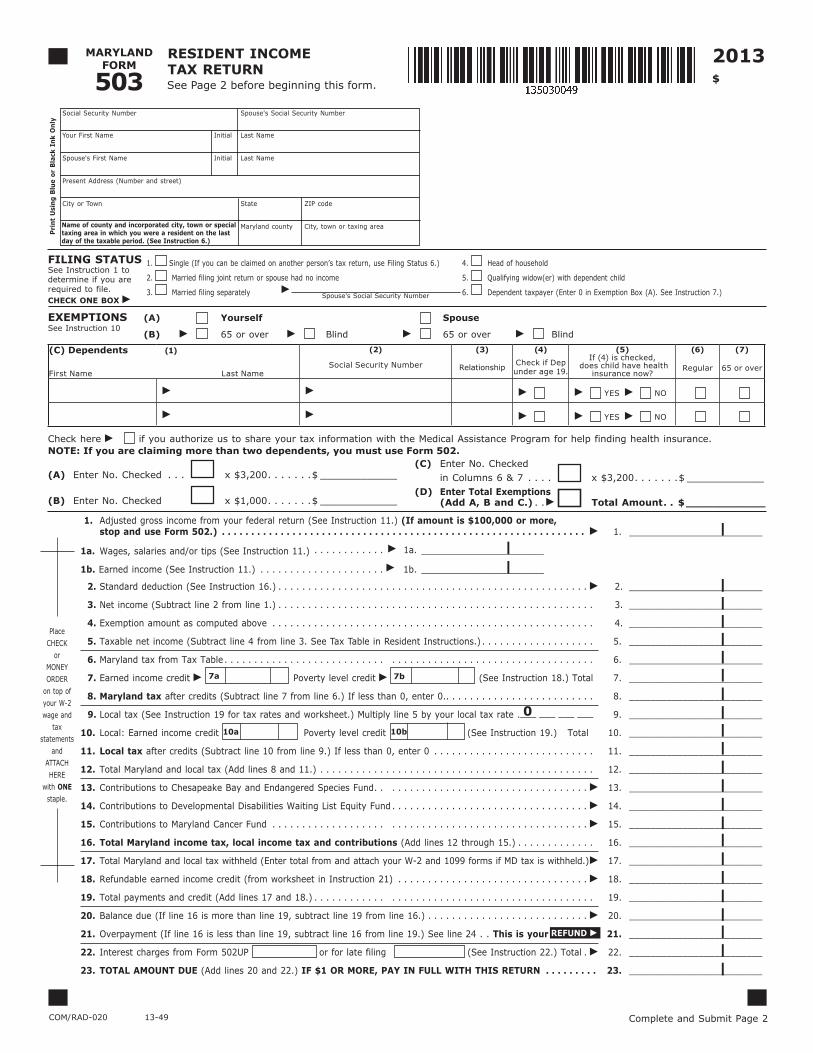

Complete all of the information at the top of Form 503, as well as the following lines: 1, 7a, 10a, 13-19 and 21.

Sign the form, and attach your withholding statement, or withholding statements (all W-2, 1099, and K-1 forms).

2013

$

MARYLAND FORM

503

COM/RAD-020 13-49

RESIDENT INCOME TAX RETURN

1. Adjusted gross income from your federal return (See Instruction 11.) (If amount is $100,000 or more, stop and use Form 502.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1. _________________________

1a. Wages, salaries and/or tips (See Instruction 11.) . . . . . . . . . . . . . 1a. _______________________

1b. Earned income (See Instruction 11.) . . . . . . . . . . . . . . . . . . . . . 1b. _______________________

2. Standard deduction (See Instruction 16.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. _________________________

3. Net income (Subtract line 2 from line 1.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3. _________________________

4. Exemption amount as computed above . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4. _________________________

5. Taxable net income (Subtract line 4 from line 3. See Tax Table in Resident Instructions.) . . . . . . . . . . . . . . . . . . . 5. _________________________

6. Maryland tax from Tax Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6. _________________________

7. Earned income credit Poverty level credit (See Instruction 18.) Total 7. _________________________

8. Maryland tax after credits (Subtract line 7 from line 6.) If less than 0, enter 0. . . . . . . . . . . . . . . . . . . . . . . . . . 8. _________________________

9. Local tax (See Instruction 19 for tax rates and worksheet.) Multiply line 5 by your local tax rate .___ ___ ___ ___ 9. _________________________

10. Local: Earned income credit Poverty level credit (See Instruction 19.) Total 10. _________________________

11. Local tax after credits (Subtract line 10 from line 9.) If less than 0, enter 0 . . . . . . . . . . . . . . . . . . . . . . . . . . . 11. _________________________

12. Total Maryland and local tax (Add lines 8 and 11.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12. _________________________

13. Contributions to Chesapeake Bay and Endangered Species Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13. _________________________

14. Contributions to Developmental Disabilities Waiting List Equity Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14. _________________________

15. Contributions to Maryland Cancer Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15. _________________________

16. Total Maryland income tax, local income tax and contributions (Add lines 12 through 15.) . . . . . . . . . . . . . 16. _________________________

17. Total Maryland and local tax withheld (Enter total from and attach your W-2 and 1099 forms if MD tax is withheld.) 17. _________________________

18. Refundable earned income credit (from worksheet in Instruction 21) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18. _________________________

19. Total payments and credit (Add lines 17 and 18.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19. _________________________

20. Balance due (If line 16 is more than line 19, subtract line 19 from line 16.) . . . . . . . . . . . . . . . . . . . . . . . . . . . 20. _________________________

21. Overpayment (If line 16 is less than line 19, subtract line 16 from line 19.) See line 24 . . This is your 21. _________________________

22. Interest charges from Form 502UP or for late filing (See Instruction 22.) Total . 22. _________________________

23. TOTAL AMOUNT DUE (Add lines 20 and 22.) IF $1 OR MORE, PAY IN FULL WITH THIS RETURN . . . . . . . . . 23. _________________________

0

REFUND

Place CHECK

or MONEY ORDER

on top of your W-2 wage and

tax statements

and ATTACH HERE

with ONE staple.

EXEMPTIONS (A) Yourself Spouse

(B) 65 or over Blind 65 or over Blind

FILING STATUS See Instruction 1 to determine if you are required to file.CHECK ONE BOX

1. Single (If you can be claimed on another person’s tax return, use Filing Status 6.)

2. Married filing joint return or spouse had no income

3. Married filing separately

4. Head of household

5. Qualifying widow(er) with dependent child

6. Dependent taxpayer (Enter 0 in Exemption Box (A). See Instruction 7.)

See Instruction 10

(C) Dependents (1)

First Name Last Name

(2)

Social Security Number

(3)

Relationship

(4)

Check if Dep under age 19.

(5)If (4) is checked,

does child have health insurance now?

(6)

Regular

(7)

65 or over

YES NO

YES NO

(A) Enter No. Checked . . . x $3,200 . . . . . . .$ _____________

(B) Enter No. Checked x $1,000 . . . . . . .$ _____________

(C) Enter No. Checked in Columns 6 & 7 . . . . x $3,200 . . . . . . .$ _____________(D) Enter Total Exemptions (Add A, B and C.) . . Total Amount . . $ ____________

Check here if you authorize us to share your tax information with the Medical Assistance Program for help finding health insurance. NOTE: If you are claiming more than two dependents, you must use Form 502.

Social Security Number Spouse's Social Security Number

Your First Name Initial Last Name

Spouse's First Name Initial Last Name

Present Address (Number and street)

City or Town State ZIP code

Maryland county City, town or taxing area Name of county and incorporated city, town or special taxing area in which you were a resident on the last day of the taxable period. (See Instruction 6.)

Pri

nt

Usi

ng

Blu

e o

r B

lack

In

k O

nly

Spouse's Social Security Number

Complete and Submit Page 2

See Page 2 before beginning this form.

10a 10b

7a 7b

|

||||||||||||||||||||||

||

MARYLANDFORM

5032013

COM/RAD-020 13-49

RESIDENT INCOME TAX RETURN

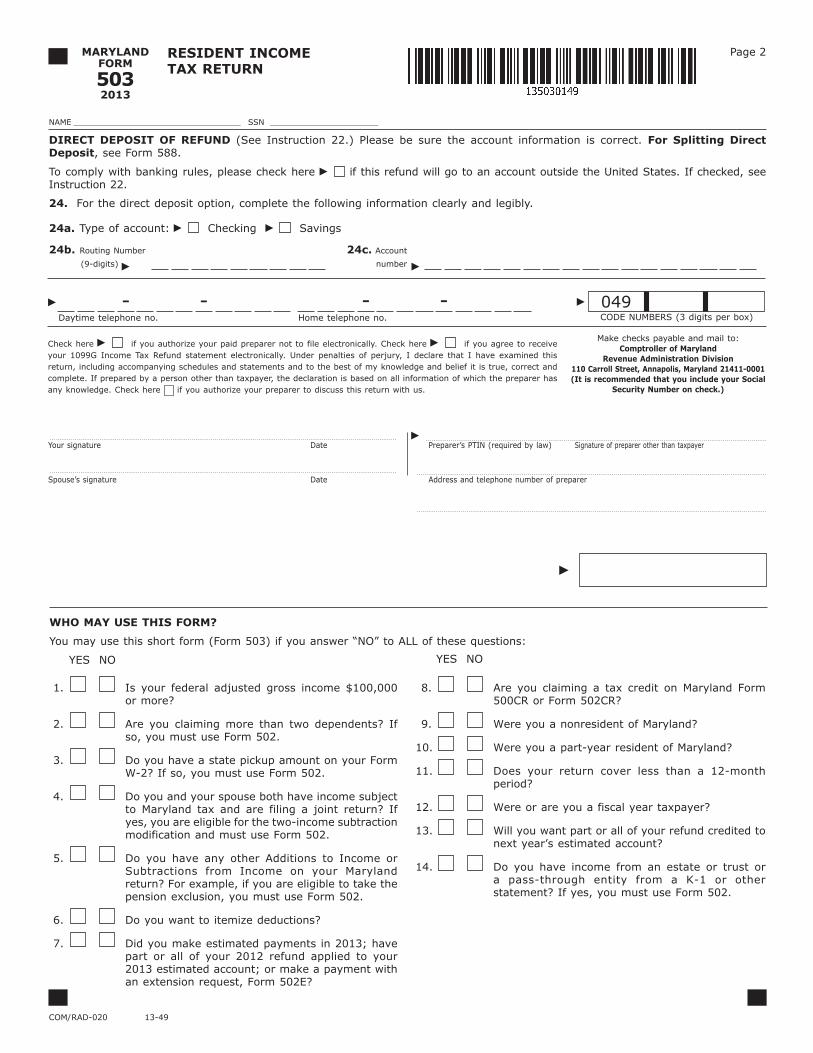

1. Is your federal adjusted gross income $100,000 or more?

2. Are you claiming more than two dependents? If so, you must use Form 502.

3. Do you have a state pickup amount on your Form W-2? If so, you must use Form 502.

4. Do you and your spouse both have income subject to Maryland tax and are filing a joint return? If yes, you are eligible for the two-income subtraction modification and must use Form 502.

5. Do you have any other Additions to Income or Subtractions from Income on your Maryland return? For example, if you are eligible to take the pension exclusion, you must use Form 502.

6. Do you want to itemize deductions?

7. Did you make estimated payments in 2013; have part or all of your 2012 refund applied to your 2013 estimated account; or make a payment with an extension request, Form 502E?

8. Are you claiming a tax credit on Maryland Form 500CR or Form 502CR?

9. Were you a nonresident of Maryland?

10. Were you a part-year resident of Maryland?

11. Does your return cover less than a 12-month period?

12. Were or are you a fiscal year taxpayer?

13. Will you want part or all of your refund credited to next year’s estimated account?

14. Do you have income from an estate or trust or a pass-through entity from a K-1 or other statement? If yes, you must use Form 502.

WHO MAY USE THIS FORM?

You may use this short form (Form 503) if you answer “NO” to ALL of these questions:

YES NO YES NO

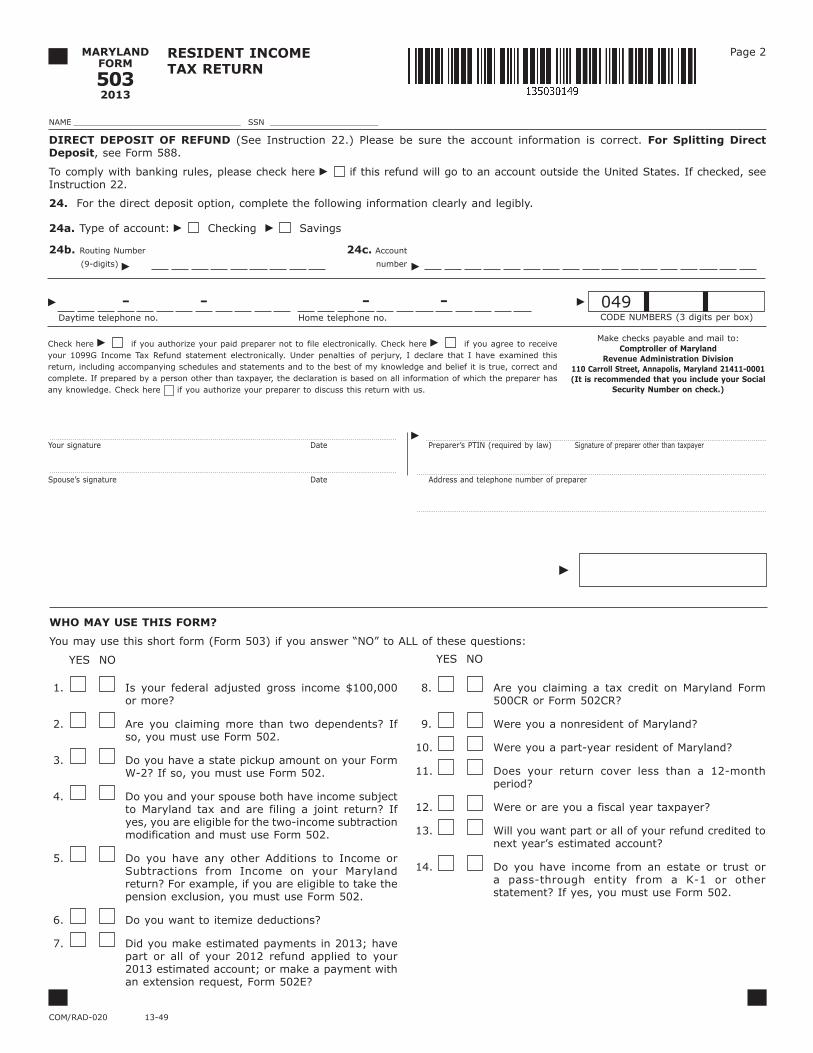

DIRECT DEPOSIT OF REFUND (See Instruction 22.) Please be sure the account information is correct. For Splitting Direct Deposit, see Form 588.

To comply with banking rules, please check here if this refund will go to an account outside the United States. If checked, see Instruction 22.

24. For the direct deposit option, complete the following information clearly and legibly.

24a. Type of account: Checking Savings

24b. Routing Number 24c. Account

(9-digits) number

Make checks payable and mail to:Comptroller of Maryland

Revenue Administration Division110 Carroll Street, Annapolis, Maryland 21411-0001 (It is recommended that you include your Social

Security Number on check.)

Daytime telephone no. Home telephone no.-- --

Check here if you authorize your paid preparer not to file electronically. Check here if you agree to receive your 1099G Income Tax Refund statement electronically. Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge. Check here if you authorize your preparer to discuss this return with us.

CODE NUMBERS (3 digits per box)049

NAME __________________________________ SSN ______________________

Your signature Date Preparer’s PTIN (required by law) Signature of preparer other than taxpayer

Spouse’s signature Date Address and telephone number of preparer

Page 2

13

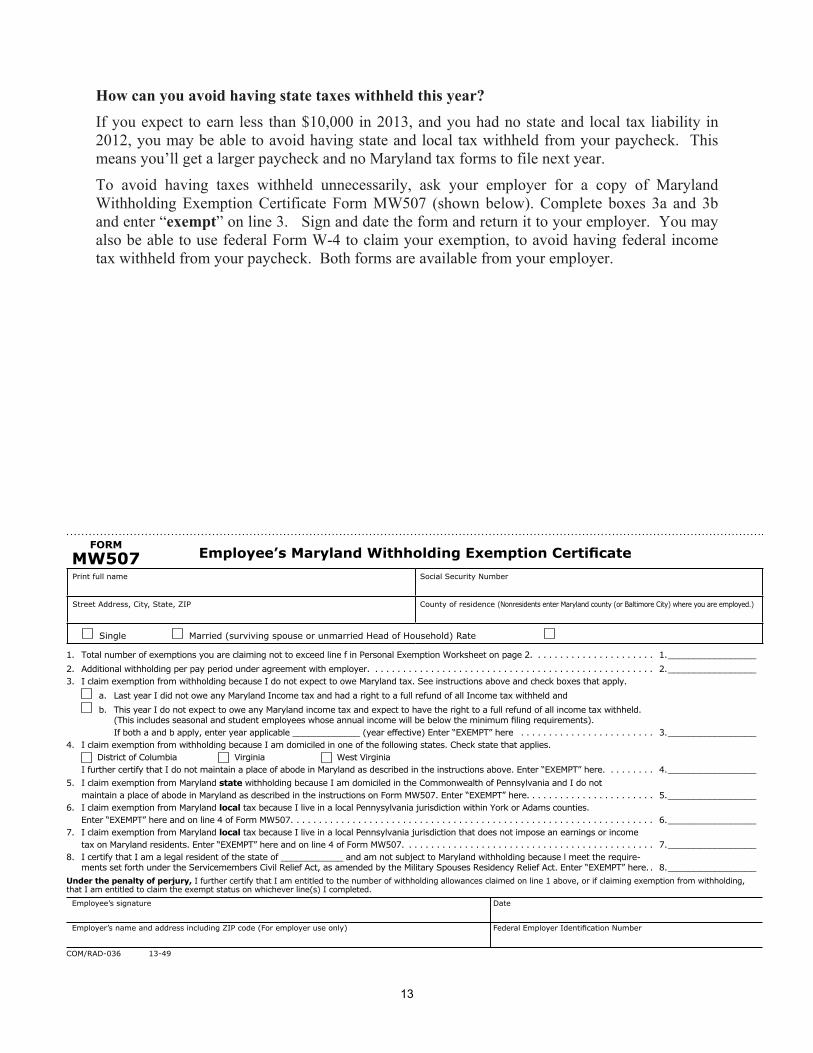

How can you avoid having state taxes withheld this year?

If you expect to earn less than $10,000 in 2013, and you had no state and local tax liability in 2012, you may be able to avoid having state and local tax withheld from your paycheck. This means you’ll get a larger paycheck and no Maryland tax forms to file next year.

To avoid having taxes withheld unnecessarily, ask your employer for a copy of Maryland Withholding Exemption Certificate Form MW507 (shown below). Complete boxes 3a and 3b and enter “exempt” on line 3. Sign and date the form and return it to your employer. You may also be able to use federal Form W-4 to claim your exemption, to avoid having federal income tax withheld from your paycheck. Both forms are available from your employer.

Under the penalty of perjury, I further certify that I am entitled to the number of withholding allowances claimed on line 1 above, or if claiming exemption from withholding, that I am entitled to claim the exempt status on whichever line(s) I completed.

Employee’s signature Date

Employer’s name and address including ZIP code (For employer use only) Federal Employer Identification Number

1. Total number of exemptions you are claiming not to exceed line f in Personal Exemption Worksheet on page 2. . . . . . . . . . . . . . . . . . . . . . 1. _________________

2. Additional withholding per pay period under agreement with employer. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. _________________3. I claim exemption from withholding because I do not expect to owe Maryland tax. See instructions above and check boxes that apply.

a. Last year I did not owe any Maryland Income tax and had a right to a full refund of all Income tax withheld and

b. This year I do not expect to owe any Maryland income tax and expect to have the right to a full refund of all income tax withheld. (This includes seasonal and student employees whose annual income will be below the minimum filing requirements). If both a and b apply, enter year applicable _____________ (year effective) Enter “EXEMPT” here . . . . . . . . . . . . . . . . . . . . . . . . 3. _________________

4. I claim exemption from withholding because I am domiciled in one of the following states. Check state that applies. District of Columbia Virginia West Virginia

I further certify that I do not maintain a place of abode in Maryland as described in the instructions above. Enter “EXEMPT” here. . . . . . . . . 4. _________________

5. I claim exemption from Maryland state withholding because I am domiciled in the Commonwealth of Pennsylvania and I do not maintain a place of abode in Maryland as described in the instructions on Form MW507. Enter “EXEMPT” here. . . . . . . . . . . . . . . . . . . . . . . 5. _________________

6. I claim exemption from Maryland local tax because I live in a local Pennysylvania jurisdiction within York or Adams counties. Enter “EXEMPT” here and on line 4 of Form MW507. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6. _________________

7. I claim exemption from Maryland local tax because I live in a local Pennsylvania jurisdiction that does not impose an earnings or income tax on Maryland residents. Enter “EXEMPT” here and on line 4 of Form MW507. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7. _________________

8. I certify that I am a legal resident of the state of ____________ and am not subject to Maryland withholding because l meet the require- ments set forth under the Servicemembers Civil Relief Act, as amended by the Military Spouses Residency Relief Act. Enter “EXEMPT” here. . 8. _________________

COM/RAD-036 13-49

Employee’s Maryland Withholding Exemption CertificateFORM

MW507Print full name Social Security Number

Street Address, City, State, ZIP County of residence (Nonresidents enter Maryland county (or Baltimore City) where you are employed.)

Single Married (surviving spouse or unmarried Head of Household) Rate

14

Can you file your Maryland tax return electronically?

Yes. There are three methods to choose from for filing your Maryland tax return electronically:

File your Maryland return online for free, using the Comptroller’s iFile service on our Web site at www.marylandtaxes.com.

Use commercial software to file online.

File electronically through a commercial tax preparer.

Electronic filing is a convenient, safe and fast way to do your taxes. If you have a bank account and choose direct deposit when you file electronically, your state tax refund can be deposited in your bank account within several days from the date your return is accepted and processed.

In addition, many people can also file their federal taxes electronically for free, using the FreeFile service offered on the IRS Web site at www.irs.gov.

Corporation Tax

Most states, including Maryland, impose a corporate income tax based on the earnings and profits of a company or business.

Maryland’s corporate income tax rate is 8.25 percent.

If the company operates in other states as well as in Maryland, the tax is based on the share of the company’s business in Maryland. For more information, visit our Web site at www.marylandtaxes.com and review the Business Taxpayers section.

15

Sales and Use Tax The Maryland sales and use tax is imposed upon the sale or use of tangible personal property at the rate of 6 percent unless a specific exemption is provided, and 9 percent on the sale of alcoholic beverages.

Common taxable items include clothing and computers. All sales of food through vending machines, and soft drinks are subject to tax. There are exemptions for some food items purchased in grocery stores, medicine, and energy used for heating or cooling homes.

There are 45 states, including Maryland, which impose a tax on sales, and also have a companion tax on out-of-state purchases. This companion tax is called a use tax. The use tax is applied to all taxable property that you use in Maryland, even if you bought it out of state directly, through mail order, by telephone or on the Internet.

The sales and use tax is a very important source of revenue for Maryland. It is the state’s second largest source of general fund revenue. Unlike many states, there are no general sales or use taxes levied by Maryland’s local areas.

How do you know when the use tax applies?

If you would have paid tax on the purchase if you made it in Maryland, you should pay tax on the same item if it was purchased untaxed outside of Maryland and used in Maryland.

Why does Maryland have a use tax?

The use tax protects Maryland businesses from unfair competition. If tax isn’t paid on items bought out of state and brought into Maryland, local businesses who levy the 6 or 9 percent sales tax, as required by law, are at a competitive disadvantage.

Suppose you paid sales tax on an item you bought in another state? Are you going to be taxed twice?

No. Maryland grants a credit for sales tax paid to another state, up to the amount of Maryland’s 6 or 9 percent sales and use tax liability. For example, if you paid a 4 percent sales tax to another state, you would be liable only for the difference. To pay this tax, you would use Maryland Form ST-118A/B (Consumer Use Tax Return).

Motor Fuel Tax

Some taxes place the burden of paying a tax on the producer or wholesaler. One example is the motor fuel tax. In Maryland, the motor fuel tax rate on gasoline was 23.5 cents per gallon prior to July 1, 2013. The Transportation Infrastructure Investment Act of 2013 was effective on July 1, 2013, and it increased motor fuel tax in order to increase transportation funding. It increases motor fuel tax rates by indexing the rates to growth in the Consumer Price Index. It also imposes a sales and use tax equivalent rate on all motor fuel except for aviation and turbine fuel. The equivalent rate is not a sales and use tax on motor fuel, but it is an increase to the motor fuel tax.

The motor fuel tax is levied on the producer or wholesaler, and passed on to the consumer at the gasoline pump. The tax rate on gasoline is 27 cents per gallon, as of July 1, 2013. Trucking companies are also required to pay a tax based on the miles they drive on Maryland highways.

Most of the revenue collected goes to the Maryland Department of Transportation for state and local transportation projects, such as roads, bridges and transportation systems.

16

Alcoholic Beverage Taxes

The tax is levied on the producer or wholesaler and is passed on to the consumer. In Maryland, the distilled spirits tax is $1.50 per gallon. The wine tax is 40 cents per gallon. The beer tax is 9 cents per gallon.

Tobacco Tax

The Maryland tobacco tax on cigarettes is currently $2.00 per pack of 20. It is levied on the wholesaler and passed on to the consumer. Maryland also imposes a tax at the wholesale level on other tobacco products, such as premium cigars at 15 percent, and other cigars at 70 percent. Pipe tobacco, chewing tobacco, and snuff are taxed at 30 percent.

Admissions and Amusement Tax

Electronic bingo machines and electronic tip jars are subject to a state admissions and amusement tax imposed at a 30 percent rate on the taxable net proceeds, for all counties except Calvert County. Effective July 1, 2012, the state admissions and amusement tax is imposed on electronic bingo and electronic tip jars in Calvert County at a 33 percent rate on the taxable net proceeds.

Estate Tax

The estate tax is imposed on the transfer of a Maryland estate valued at a minimum of $1 million. The tax is based on the difference between the local inheritance tax and the maximum federal tax credit that IRS allowed before 2001 for state death taxes, and is limited to 16 percent of the amount that exceeds $1 million.

Motor Vehicle Titling Tax The motor vehicle titling tax is collected when you sell a car, truck or other motor vehicle. This is not a sales tax. The revenue goes to the Department of Transportation for state and local transportation projects.

Tire Recycling Fee

There is an 80-cent fee on each new tire sold in Maryland. The revenue goes to a special fund administered by the Department of Environment to fund scrap tire removal and recycling.

Bay Restoration Fee

This is a fee that is levied on users of wastewater facilities, sewage disposal systems and holding tanks to provide funds for upgrading wastewater treatment plants in Maryland. The fee is set at varying rates and is collected by local governments and other billing authorities. The revenue goes to the Comptroller of Maryland.

17

Business Taxes

Many businesses must pay the state’s 8.25 percent corporate income tax. Some other businesses, such as partnerships, pay income taxes on the personal tax return.

Public utilities and insurance companies pay taxes specific to their industries.

Maryland also levies a personal property tax on businesses.

Maryland law requires employers to contribute to the Unemployment Insurance Fund, which helps to provide unemployment benefits. In addition, employers must also obtain workers’ compensation insurance, to provide benefits to injured or disabled workers.

18

Local Taxes Are all local taxes in Maryland collected by the local governments?

No. Many local taxes, like property taxes, are collected by local governments. But there are some important local taxes that are actually collected by the Maryland Comptroller’s Office.

Property Tax

Property taxes are set by local governments and are the most important source of income for these jurisdictions.

The revenue from property taxes helps to pay for education, police protection, and other local services.

The amount of tax to be paid is figured on a percentage of the value of the property as determined by the Maryland Department of Assessments and Taxation.

Admissions and Amusement Tax Local governments impose a local admissions and amusement tax which is collected by the State Comptroller’s Office for Maryland’s 23 counties, Baltimore City, the Maryland Stadium Authority and the state’s incorporated cities and towns.

Local elected officials set the rates, which vary from one-half of 1 percent to 10 percent of the admission or amusement cost for activities such as movies, athletic events, concerts and golf.

Inheritance Tax The inheritance tax is a local tax imposed by Maryland’s 23 counties and Baltimore City on the value of property that passes from a deceased person to certain beneficiaries.

The tax is collected by the local Registers of Wills and is set at a 10 percent rate. Property

passing to a child or other lineal descendant, spouse, parent, grandparent, stepchild or

stepparent, siblings or a corporation having some of these persons as stockholders is exempt from

the tax.

19

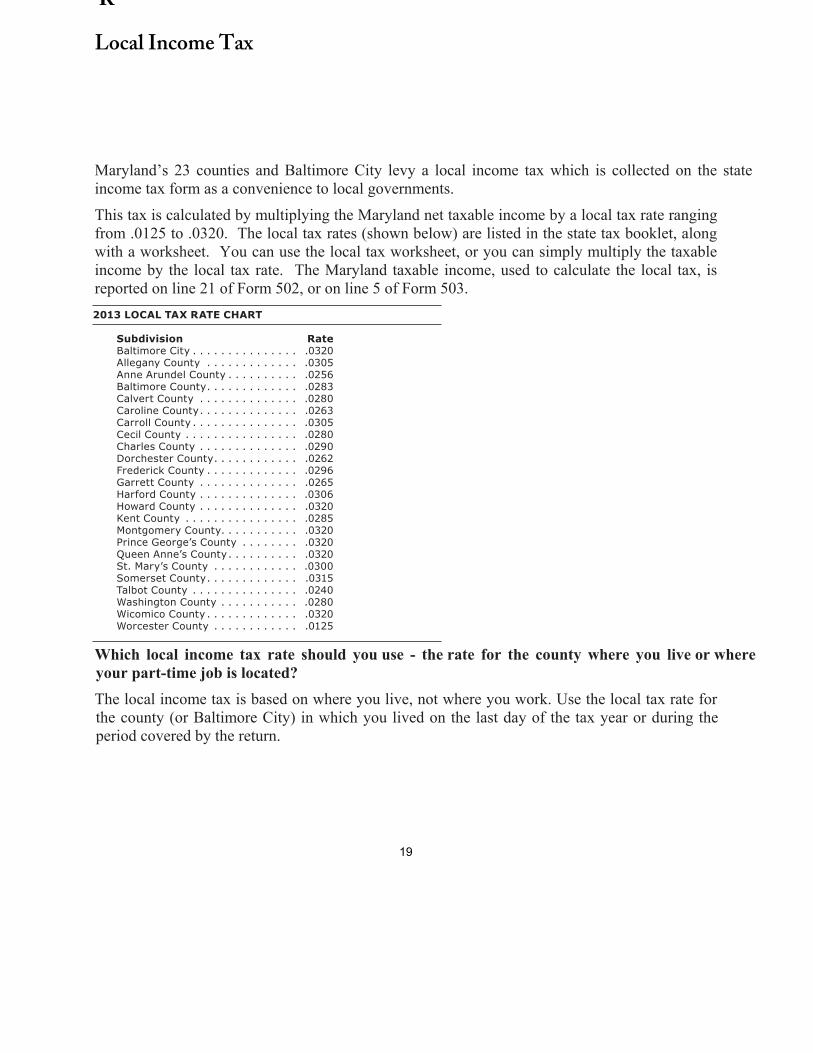

Local Income Tax

Maryland’s 23 counties and Baltimore City levy a local income tax which is collected on the state income tax form as a convenience to local governments.

This tax is calculated by multiplying the Maryland net taxable income by a local tax rate ranging from .0125 to .0320. The local tax rates (shown below) are listed in the state tax booklet, along with a worksheet. You can use the local tax worksheet, or you can simply multiply the taxable income by the local tax rate. The Maryland taxable income, used to calculate the local tax, is reported on line 21 of Form 502, or on line 5 of Form 503.

Which local income tax rate should you use - the rate for the county where you live or where your part-time job is located? The local income tax is based on where you live, not where you work. Use the local tax rate for the county (or Baltimore City) in which you lived on the last day of the tax year or during the period covered by the return.

2013 LOCAL TAX RATE CHART

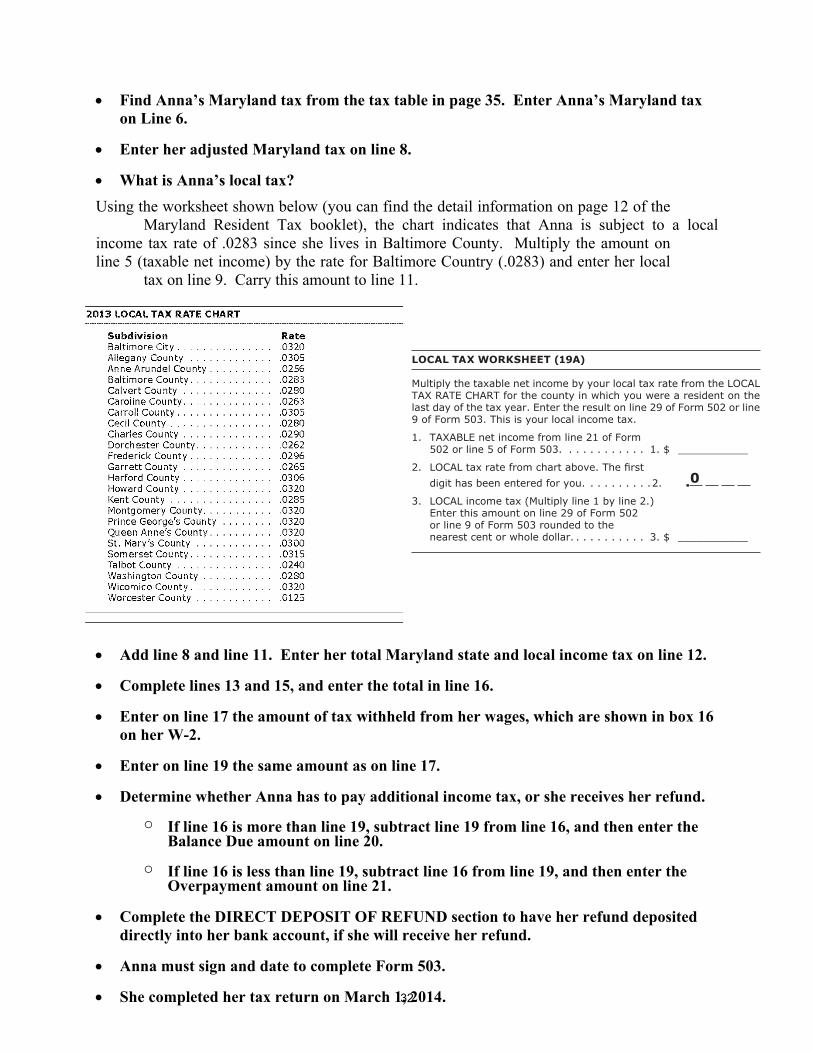

Subdivision RateBaltimore City . . . . . . . . . . . . . . . .0320 Allegany County . . . . . . . . . . . . . .0305 Anne Arundel County . . . . . . . . . . .0256Baltimore County . . . . . . . . . . . . . .0283 Calvert County . . . . . . . . . . . . . . .0280 Caroline County . . . . . . . . . . . . . . .0263 Carroll County . . . . . . . . . . . . . . . .0305 Cecil County . . . . . . . . . . . . . . . . .0280 Charles County . . . . . . . . . . . . . . .0290 Dorchester County . . . . . . . . . . . . .0262 Frederick County . . . . . . . . . . . . . .0296 Garrett County . . . . . . . . . . . . . . .0265 Harford County . . . . . . . . . . . . . . .0306 Howard County . . . . . . . . . . . . . . .0320 Kent County . . . . . . . . . . . . . . . . .0285 Montgomery County. . . . . . . . . . . .0320 Prince George’s County . . . . . . . . .0320Queen Anne’s County . . . . . . . . . . .0320 St. Mary’s County . . . . . . . . . . . . .0300 Somerset County . . . . . . . . . . . . . .0315 Talbot County . . . . . . . . . . . . . . . .0240 Washington County . . . . . . . . . . . .0280 Wicomico County . . . . . . . . . . . . . .0320 Worcester County . . . . . . . . . . . . .0125

20

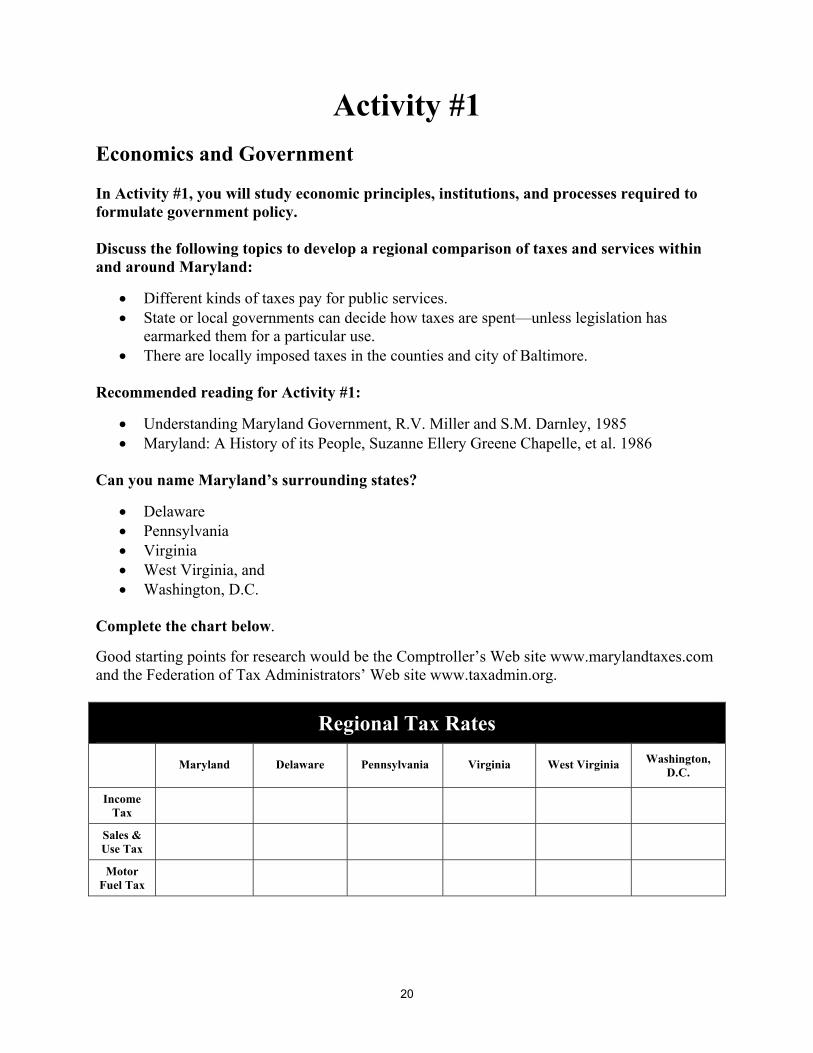

Activity #1

Economics and Government In Activity #1, you will study economic principles, institutions, and processes required to formulate government policy. Discuss the following topics to develop a regional comparison of taxes and services within and around Maryland:

Different kinds of taxes pay for public services. State or local governments can decide how taxes are spent—unless legislation has

earmarked them for a particular use. There are locally imposed taxes in the counties and city of Baltimore.

Recommended reading for Activity #1:

Understanding Maryland Government, R.V. Miller and S.M. Darnley, 1985 Maryland: A History of its People, Suzanne Ellery Greene Chapelle, et al. 1986

Can you name Maryland’s surrounding states?

Delaware Pennsylvania Virginia West Virginia, and Washington, D.C.

Complete the chart below.

Good starting points for research would be the Comptroller’s Web site www.marylandtaxes.com and the Federation of Tax Administrators’ Web site www.taxadmin.org.

Regional Tax Rates

Maryland

Delaware

Pennsylvania

Virginia

West Virginia Washington, D.C.

Income Tax

Sales & Use Tax

Motor Fuel Tax

21

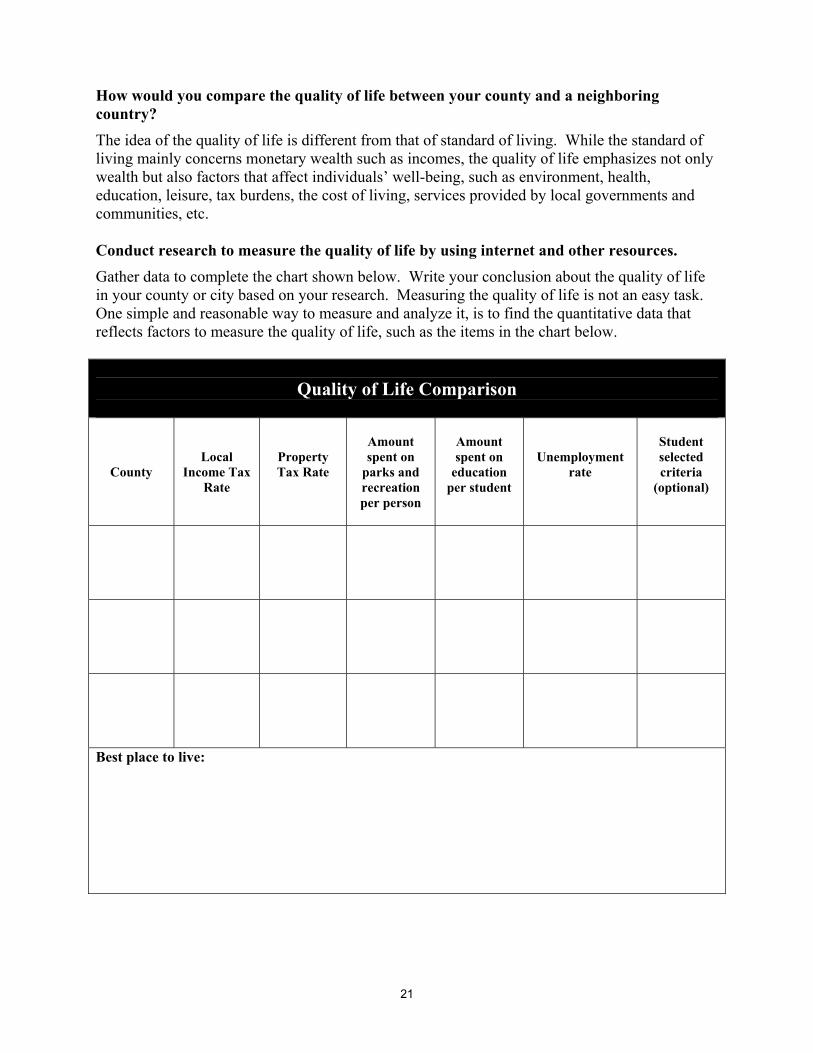

How would you compare the quality of life between your county and a neighboring country? The idea of the quality of life is different from that of standard of living. While the standard of living mainly concerns monetary wealth such as incomes, the quality of life emphasizes not only wealth but also factors that affect individuals’ well-being, such as environment, health, education, leisure, tax burdens, the cost of living, services provided by local governments and communities, etc. Conduct research to measure the quality of life by using internet and other resources. Gather data to complete the chart shown below. Write your conclusion about the quality of life in your county or city based on your research. Measuring the quality of life is not an easy task. One simple and reasonable way to measure and analyze it, is to find the quantitative data that reflects factors to measure the quality of life, such as the items in the chart below.

Quality of Life Comparison

County

Local Income Tax

Rate

Property Tax Rate

Amount spent on

parks and recreation per person

Amount spent on

education per student

Unemployment rate

Student selected criteria

(optional)

Best place to live:

22

Activity #2

CASE 1—Student Worker Filing Maryland Tax Return In Activity #2, you will complete a Maryland income tax return for a student with a part-time job. You will use the Form 503 to complete the Maryland income tax return by using information and instructions provided. After finishing, compare your responses to the answer keys. Information: Francis Scott Key is a senior in a high school. He worked as a part-time office assistant at the local library during his summer break in 2013. He made $2,772 from working at the library during the summer, and had $118 of Maryland state and local income tax withheld from his pay. He also earned $178 by selling a collection of poems, which he wrote last spring and then sold 178 copies at $1.00 each to his family members, friends, neighbors and local bookstores. In addition, he received $102 interest income from a back account his parents opened for him when he started the grade school. Francis received most of his information from the W-2 form received from his employer, which stated his total wages, and the Maryland state and local income tax withheld from his wages. The information on the form 1099, which he received from the bank, stated his interest income. No tax was withheld from the $178 earned from his poetry sales, and he must report the $178 as additional income. He wants to make contributions of $4 for Chesapeake Bay and Endangered Species Fund, and $4 for Maryland Cancer Fund. He still lives at home, and is supported by his parents, who claim Francis as a dependent on their tax return. Additional information needed for Francis Scott Key’s Maryland Tax Return: Name: Francis Scott Key Address 849 Harbor Road Annapolis, MD 21401 Anne Arundel County Social Security Number: 123-45-6789 Bank Account: Checking Account Bank Routing Number—142257134 Bank Account Number—17210231

23

Questions and Instruction for Activity #2 Q1. What is Francis’ total income in 2013? ............................................................ Q2. Does Francis have to file a Maryland tax return? ..........................................

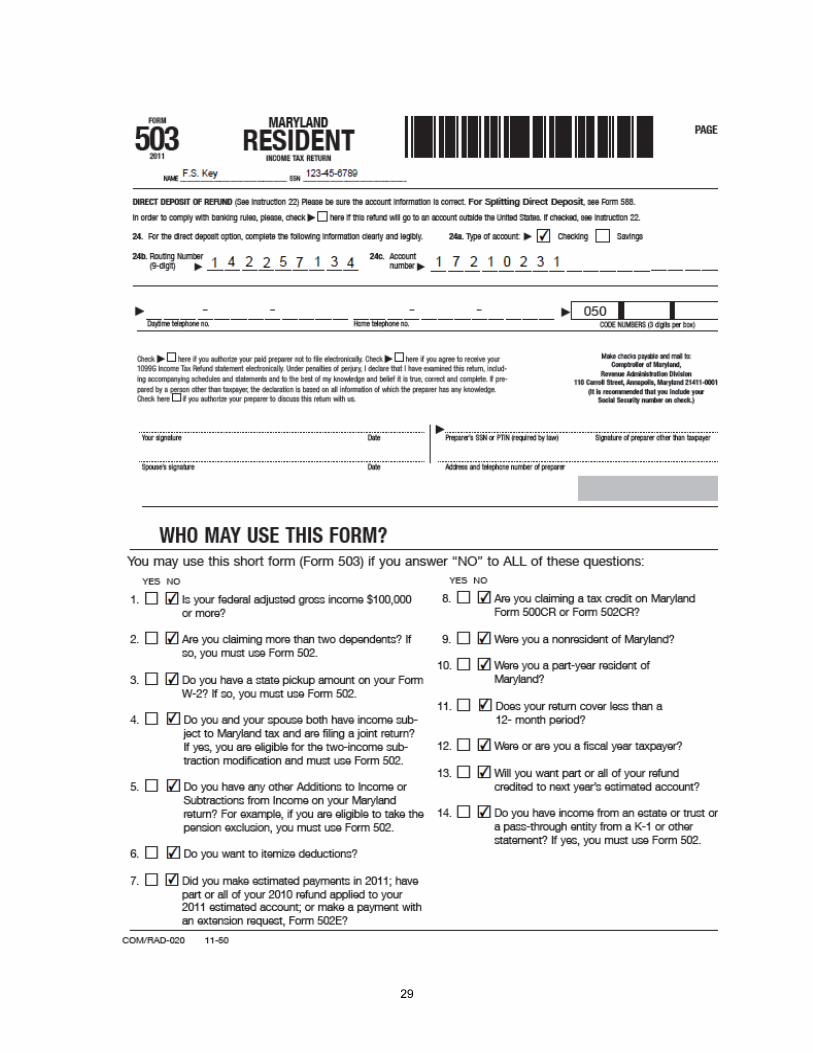

How can Francis get a refund of Maryland taxes withheld from his pay? First, you need to determine which form(s) you can use. Francis is eligible to use Form 503 (a blank Form 503 is provided in pages 24 and 25 for this activity.) To be eligible for you to use Form 503, ALL of your answers must be NO to the questions on the back of Form 503. He must complete Form 503 to get his refund.

Enter Francis’ name, address and Social Security number in the appropriate spaces on the front of Form 503.

Complete the sections for filing status and exemptions. Francis is a dependent taxpayer since he claimed as a dependent of his parents return. Dependents cannot claim an exemption for themselves, so check box number 6, Dependent taxpayer, and enter 0 in the Exemption Box (A).

Enter Francis’ total income on line 1. Q3. Does Francis qualify for an earned income credit

or a poverty level credit on line 7? ....................................................................

Complete lines 13 and 15, and enter the total in line 16.

Enter on line 17 the amount of tax withheld from his wages which are shown in box 16 on his W-2.

Enter on line 19 the same amount on line 17.

Subtract the amount on line 16 from line 19, to determine the amount of Francis’ refund and enter on line 21.

Complete the DIRECT DEPOSIT OF REFUND section to have his refund deposited directly into his bank account.

Francis must sign and date to complete Form 503.

He completed his tax return on February 28, 2014.

2013

$

MARYLAND FORM

503

COM/RAD-020 13-49

RESIDENT INCOME TAX RETURN

1. Adjusted gross income from your federal return (See Instruction 11.) (If amount is $100,000 or more, stop and use Form 502.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1. _________________________

1a. Wages, salaries and/or tips (See Instruction 11.) . . . . . . . . . . . . . 1a. _______________________

1b. Earned income (See Instruction 11.) . . . . . . . . . . . . . . . . . . . . . 1b. _______________________

2. Standard deduction (See Instruction 16.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. _________________________

3. Net income (Subtract line 2 from line 1.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3. _________________________

4. Exemption amount as computed above . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4. _________________________

5. Taxable net income (Subtract line 4 from line 3. See Tax Table in Resident Instructions.) . . . . . . . . . . . . . . . . . . . 5. _________________________

6. Maryland tax from Tax Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6. _________________________

7. Earned income credit Poverty level credit (See Instruction 18.) Total 7. _________________________

8. Maryland tax after credits (Subtract line 7 from line 6.) If less than 0, enter 0. . . . . . . . . . . . . . . . . . . . . . . . . . 8. _________________________

9. Local tax (See Instruction 19 for tax rates and worksheet.) Multiply line 5 by your local tax rate .___ ___ ___ ___ 9. _________________________

10. Local: Earned income credit Poverty level credit (See Instruction 19.) Total 10. _________________________

11. Local tax after credits (Subtract line 10 from line 9.) If less than 0, enter 0 . . . . . . . . . . . . . . . . . . . . . . . . . . . 11. _________________________

12. Total Maryland and local tax (Add lines 8 and 11.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12. _________________________

13. Contributions to Chesapeake Bay and Endangered Species Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13. _________________________

14. Contributions to Developmental Disabilities Waiting List Equity Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14. _________________________

15. Contributions to Maryland Cancer Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15. _________________________

16. Total Maryland income tax, local income tax and contributions (Add lines 12 through 15.) . . . . . . . . . . . . . 16. _________________________

17. Total Maryland and local tax withheld (Enter total from and attach your W-2 and 1099 forms if MD tax is withheld.) 17. _________________________

18. Refundable earned income credit (from worksheet in Instruction 21) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18. _________________________

19. Total payments and credit (Add lines 17 and 18.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19. _________________________

20. Balance due (If line 16 is more than line 19, subtract line 19 from line 16.) . . . . . . . . . . . . . . . . . . . . . . . . . . . 20. _________________________

21. Overpayment (If line 16 is less than line 19, subtract line 16 from line 19.) See line 24 . . This is your 21. _________________________

22. Interest charges from Form 502UP or for late filing (See Instruction 22.) Total . 22. _________________________

23. TOTAL AMOUNT DUE (Add lines 20 and 22.) IF $1 OR MORE, PAY IN FULL WITH THIS RETURN . . . . . . . . . 23. _________________________

0

REFUND

Place CHECK

or MONEY ORDER

on top of your W-2 wage and

tax statements

and ATTACH HERE

with ONE staple.

EXEMPTIONS (A) Yourself Spouse

(B) 65 or over Blind 65 or over Blind

FILING STATUS See Instruction 1 to determine if you are required to file.CHECK ONE BOX

1. Single (If you can be claimed on another person’s tax return, use Filing Status 6.)

2. Married filing joint return or spouse had no income

3. Married filing separately

4. Head of household

5. Qualifying widow(er) with dependent child

6. Dependent taxpayer (Enter 0 in Exemption Box (A). See Instruction 7.)

See Instruction 10

(C) Dependents (1)

First Name Last Name

(2)

Social Security Number

(3)

Relationship

(4)

Check if Dep under age 19.

(5)If (4) is checked,

does child have health insurance now?

(6)

Regular

(7)

65 or over

YES NO

YES NO

(A) Enter No. Checked . . . x $3,200 . . . . . . .$ _____________

(B) Enter No. Checked x $1,000 . . . . . . .$ _____________

(C) Enter No. Checked in Columns 6 & 7 . . . . x $3,200 . . . . . . .$ _____________(D) Enter Total Exemptions (Add A, B and C.) . . Total Amount . . $ ____________

Check here if you authorize us to share your tax information with the Medical Assistance Program for help finding health insurance. NOTE: If you are claiming more than two dependents, you must use Form 502.

Social Security Number Spouse's Social Security Number

Your First Name Initial Last Name

Spouse's First Name Initial Last Name

Present Address (Number and street)

City or Town State ZIP code

Maryland county City, town or taxing area Name of county and incorporated city, town or special taxing area in which you were a resident on the last day of the taxable period. (See Instruction 6.)

Pri

nt

Usi

ng

Blu

e o

r B

lack

In

k O

nly

Spouse's Social Security Number

Complete and Submit Page 2

See Page 2 before beginning this form.

10a 10b

7a 7b

|

||||||||||||||||||||||

||

MARYLANDFORM

5032013

COM/RAD-020 13-49

RESIDENT INCOME TAX RETURN

1. Is your federal adjusted gross income $100,000 or more?

2. Are you claiming more than two dependents? If so, you must use Form 502.

3. Do you have a state pickup amount on your Form W-2? If so, you must use Form 502.

4. Do you and your spouse both have income subject to Maryland tax and are filing a joint return? If yes, you are eligible for the two-income subtraction modification and must use Form 502.

5. Do you have any other Additions to Income or Subtractions from Income on your Maryland return? For example, if you are eligible to take the pension exclusion, you must use Form 502.

6. Do you want to itemize deductions?

7. Did you make estimated payments in 2013; have part or all of your 2012 refund applied to your 2013 estimated account; or make a payment with an extension request, Form 502E?

8. Are you claiming a tax credit on Maryland Form 500CR or Form 502CR?

9. Were you a nonresident of Maryland?

10. Were you a part-year resident of Maryland?

11. Does your return cover less than a 12-month period?

12. Were or are you a fiscal year taxpayer?

13. Will you want part or all of your refund credited to next year’s estimated account?

14. Do you have income from an estate or trust or a pass-through entity from a K-1 or other statement? If yes, you must use Form 502.

WHO MAY USE THIS FORM?

You may use this short form (Form 503) if you answer “NO” to ALL of these questions:

YES NO YES NO

DIRECT DEPOSIT OF REFUND (See Instruction 22.) Please be sure the account information is correct. For Splitting Direct Deposit, see Form 588.

To comply with banking rules, please check here if this refund will go to an account outside the United States. If checked, see Instruction 22.

24. For the direct deposit option, complete the following information clearly and legibly.

24a. Type of account: Checking Savings

24b. Routing Number 24c. Account

(9-digits) number

Make checks payable and mail to:Comptroller of Maryland

Revenue Administration Division110 Carroll Street, Annapolis, Maryland 21411-0001 (It is recommended that you include your Social

Security Number on check.)

Daytime telephone no. Home telephone no.-- --

Check here if you authorize your paid preparer not to file electronically. Check here if you agree to receive your 1099G Income Tax Refund statement electronically. Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge. Check here if you authorize your preparer to discuss this return with us.

CODE NUMBERS (3 digits per box)049

NAME __________________________________ SSN ______________________

Your signature Date Preparer’s PTIN (required by law) Signature of preparer other than taxpayer

Spouse’s signature Date Address and telephone number of preparer

Page 2

26

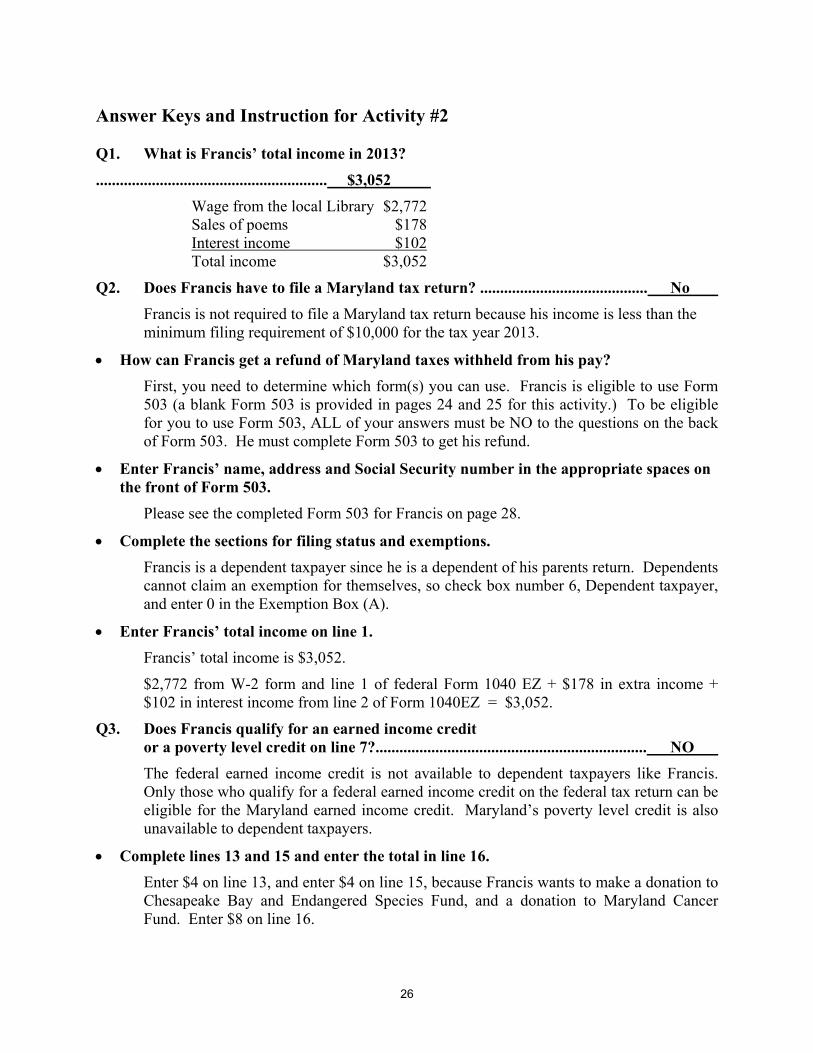

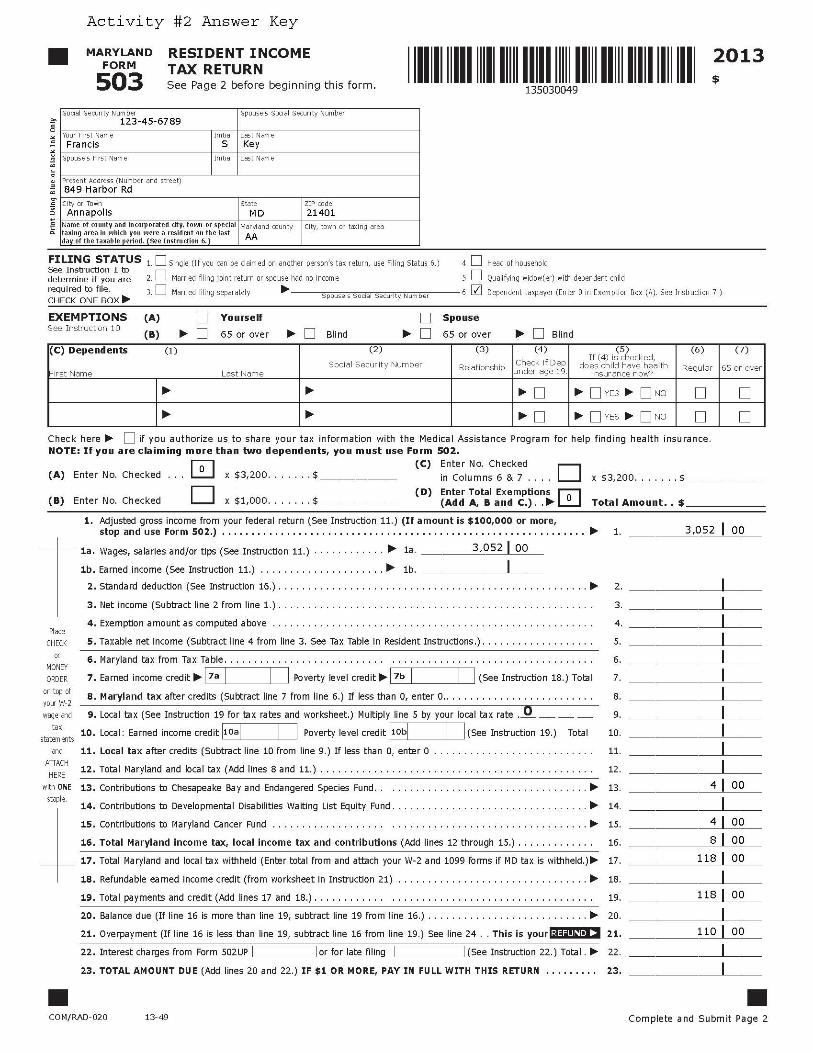

Answer Keys and Instruction for Activity #2 Q1. What is Francis’ total income in 2013? .......................................................... $3,052 Wage from the local Library $2,772 Sales of poems $178 Interest income $102 Total income $3,052

Q2. Does Francis have to file a Maryland tax return? .......................................... No Francis is not required to file a Maryland tax return because his income is less than the minimum filing requirement of $10,000 for the tax year 2013.

How can Francis get a refund of Maryland taxes withheld from his pay? First, you need to determine which form(s) you can use. Francis is eligible to use Form 503 (a blank Form 503 is provided in pages 24 and 25 for this activity.) To be eligible for you to use Form 503, ALL of your answers must be NO to the questions on the back of Form 503. He must complete Form 503 to get his refund.

Enter Francis’ name, address and Social Security number in the appropriate spaces on the front of Form 503.

Please see the completed Form 503 for Francis on page 28.

Complete the sections for filing status and exemptions. Francis is a dependent taxpayer since he is a dependent of his parents return. Dependents cannot claim an exemption for themselves, so check box number 6, Dependent taxpayer, and enter 0 in the Exemption Box (A).

Enter Francis’ total income on line 1. Francis’ total income is $3,052.

$2,772 from W-2 form and line 1 of federal Form 1040 EZ + $178 in extra income + $102 in interest income from line 2 of Form 1040EZ = $3,052.

Q3. Does Francis qualify for an earned income credit or a poverty level credit on line 7?.................................................................... NO The federal earned income credit is not available to dependent taxpayers like Francis. Only those who qualify for a federal earned income credit on the federal tax return can be eligible for the Maryland earned income credit. Maryland’s poverty level credit is also unavailable to dependent taxpayers.

Complete lines 13 and 15 and enter the total in line 16. Enter $4 on line 13, and enter $4 on line 15, because Francis wants to make a donation to Chesapeake Bay and Endangered Species Fund, and a donation to Maryland Cancer Fund. Enter $8 on line 16.

27

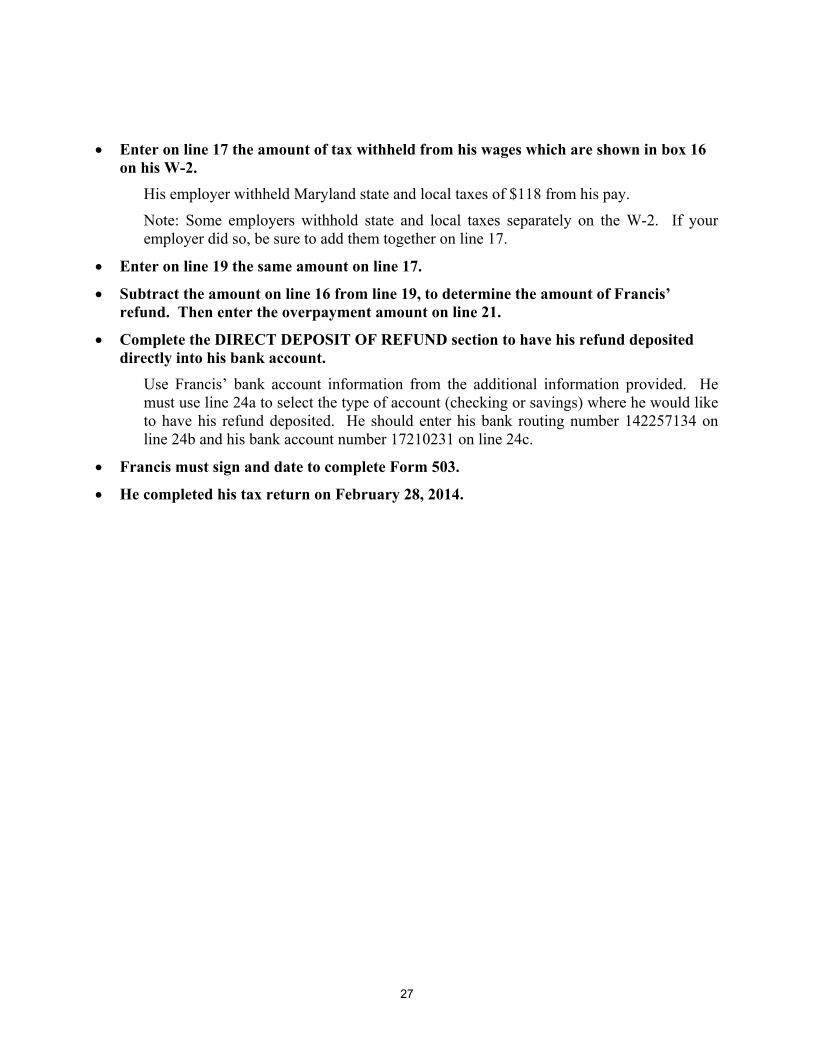

Enter on line 17 the amount of tax withheld from his wages which are shown in box 16 on his W-2.

His employer withheld Maryland state and local taxes of $118 from his pay.

Note: Some employers withhold state and local taxes separately on the W-2. If your employer did so, be sure to add them together on line 17.

Enter on line 19 the same amount on line 17.

Subtract the amount on line 16 from line 19, to determine the amount of Francis’ refund. Then enter the overpayment amount on line 21.

Complete the DIRECT DEPOSIT OF REFUND section to have his refund deposited directly into his bank account.

Use Francis’ bank account information from the additional information provided. He must use line 24a to select the type of account (checking or savings) where he would like to have his refund deposited. He should enter his bank routing number 142257134 on line 24b and his bank account number 17210231 on line 24c.

Francis must sign and date to complete Form 503.

He completed his tax return on February 28, 2014.

29

Activity #2 Answer Key

30

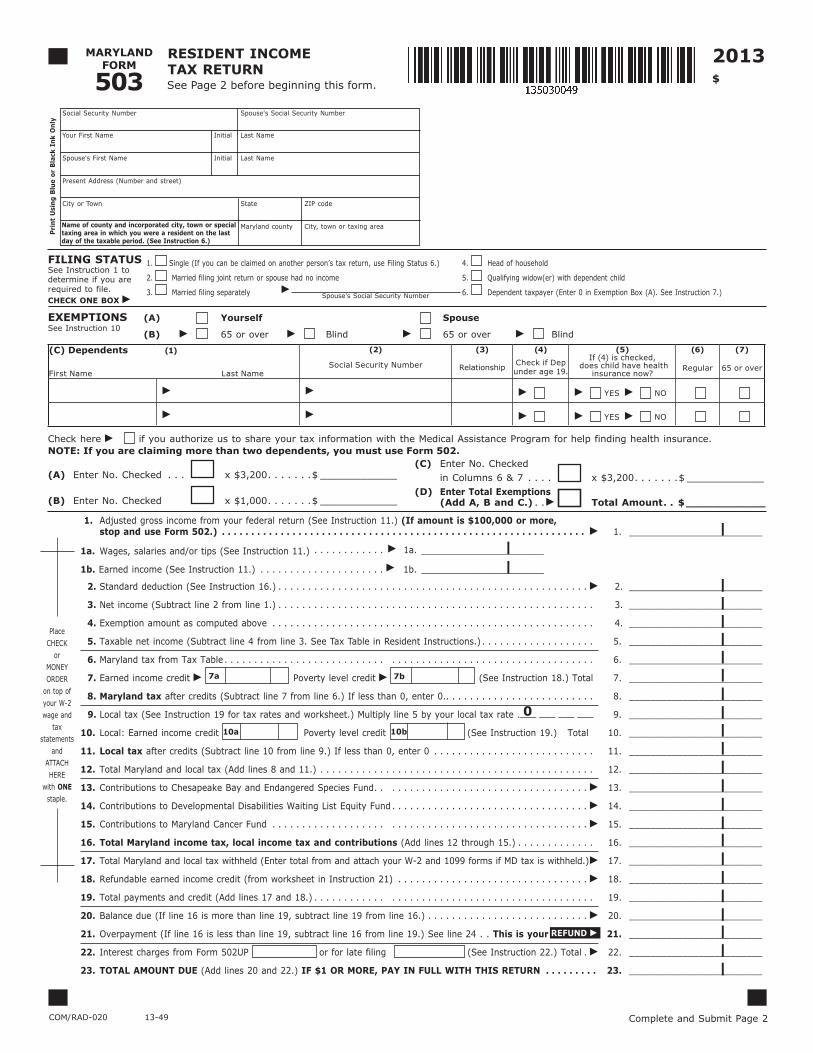

Activity #3

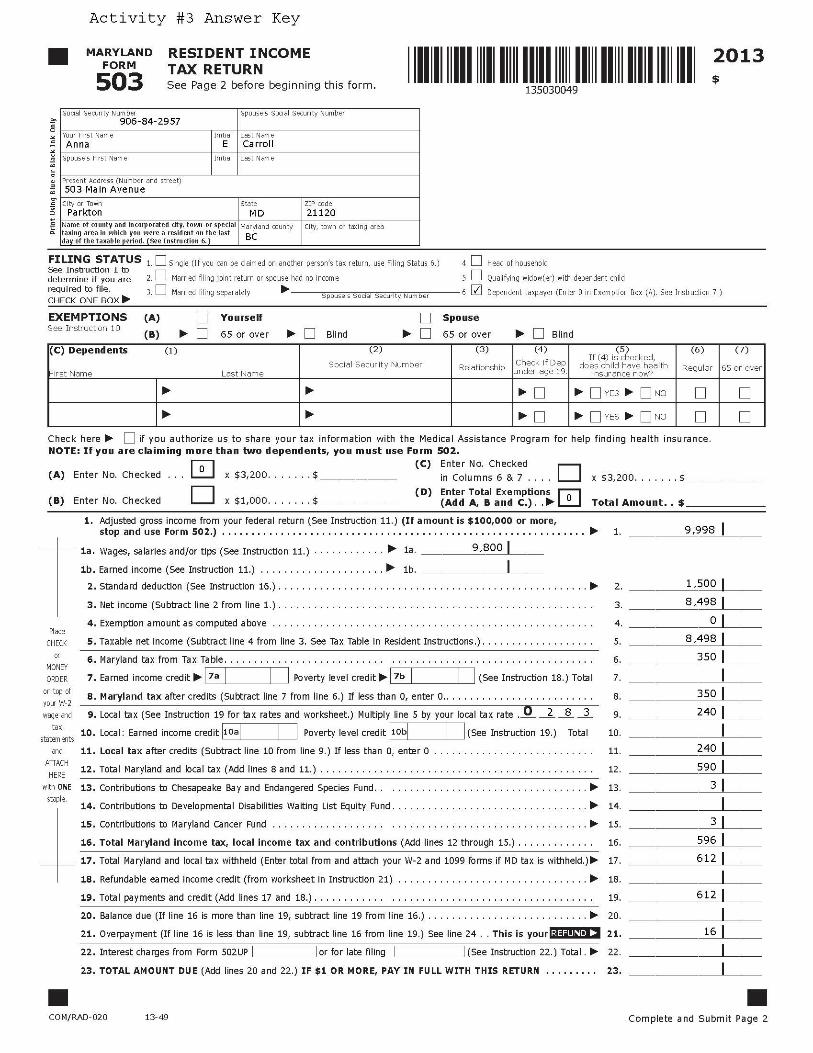

CASE—Student Worker with Higher Income Filing Maryland Tax Return In Activity #3, you will complete a Maryland income tax return for a student who earned more money from a part-time job than the student in Activity #2. Again, you will use the Form 503 to complete the Maryland income tax return by following the instructions below. After finishing, compare your responses to the answer keys. Information: Ann Ella Carroll is a senior in high school. During 2013, she worked part-time in the evenings during semesters, and full-time during school breaks, as an assistant to a political lobbyist. She earned $9,850 during 2013, and had $298 in bank interest on money she saved. Her employer withheld Maryland income tax of $623. Anna wants to contribute $3 to the Chesapeake Bay and Endangered Species Fund, and $3 to the Maryland Cancer Fund when she files her Maryland tax return. She still lives with her parents. They provide more than half of her support and claim her as a dependent on their tax return. Additional information needed for Anna Ella Carroll’s Maryland Tax Return: Name: Anna Ella Carroll Address 503 Main Avenue Parkton, MD 21120 Baltimore County Social Security Number: 906-84-2957 Bank Account: Saving Account Bank Routing Number—138227514 Bank Account Number—17420524

31

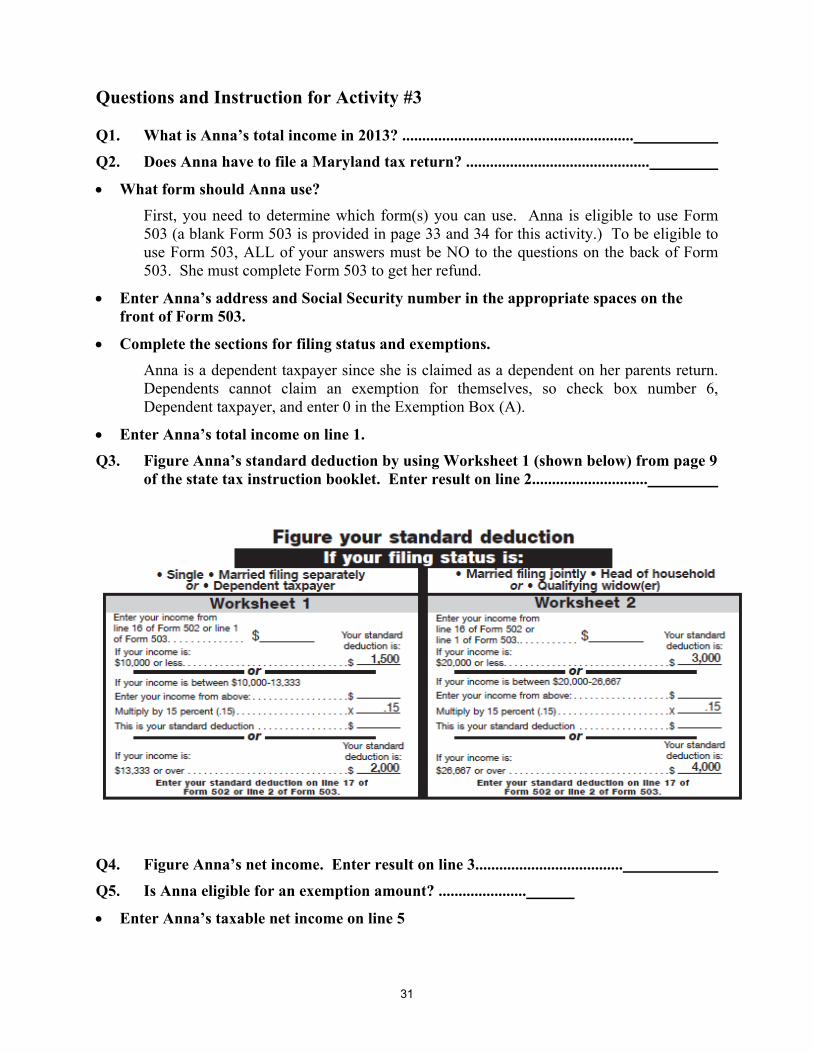

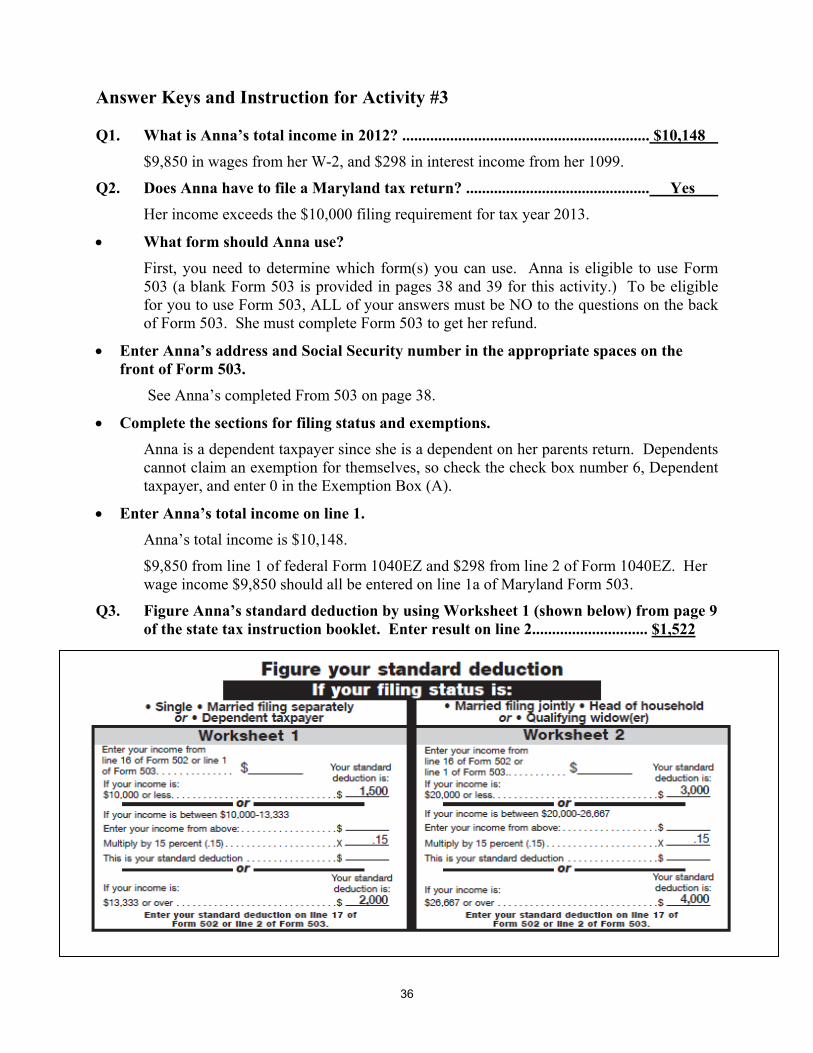

Questions and Instruction for Activity #3 Q1. What is Anna’s total income in 2013? .......................................................... Q2. Does Anna have to file a Maryland tax return? ..............................................

What form should Anna use? First, you need to determine which form(s) you can use. Anna is eligible to use Form 503 (a blank Form 503 is provided in page 33 and 34 for this activity.) To be eligible to use Form 503, ALL of your answers must be NO to the questions on the back of Form 503. She must complete Form 503 to get her refund.

Enter Anna’s address and Social Security number in the appropriate spaces on the front of Form 503.

Complete the sections for filing status and exemptions. Anna is a dependent taxpayer since she is claimed as a dependent on her parents return. Dependents cannot claim an exemption for themselves, so check box number 6, Dependent taxpayer, and enter 0 in the Exemption Box (A).

Enter Anna’s total income on line 1. Q3. Figure Anna’s standard deduction by using Worksheet 1 (shown below) from page 9

of the state tax instruction booklet. Enter result on line 2............................. Q4. Figure Anna’s net income. Enter result on line 3..................................... Q5. Is Anna eligible for an exemption amount? ......................

Enter Anna’s taxable net income on line 5

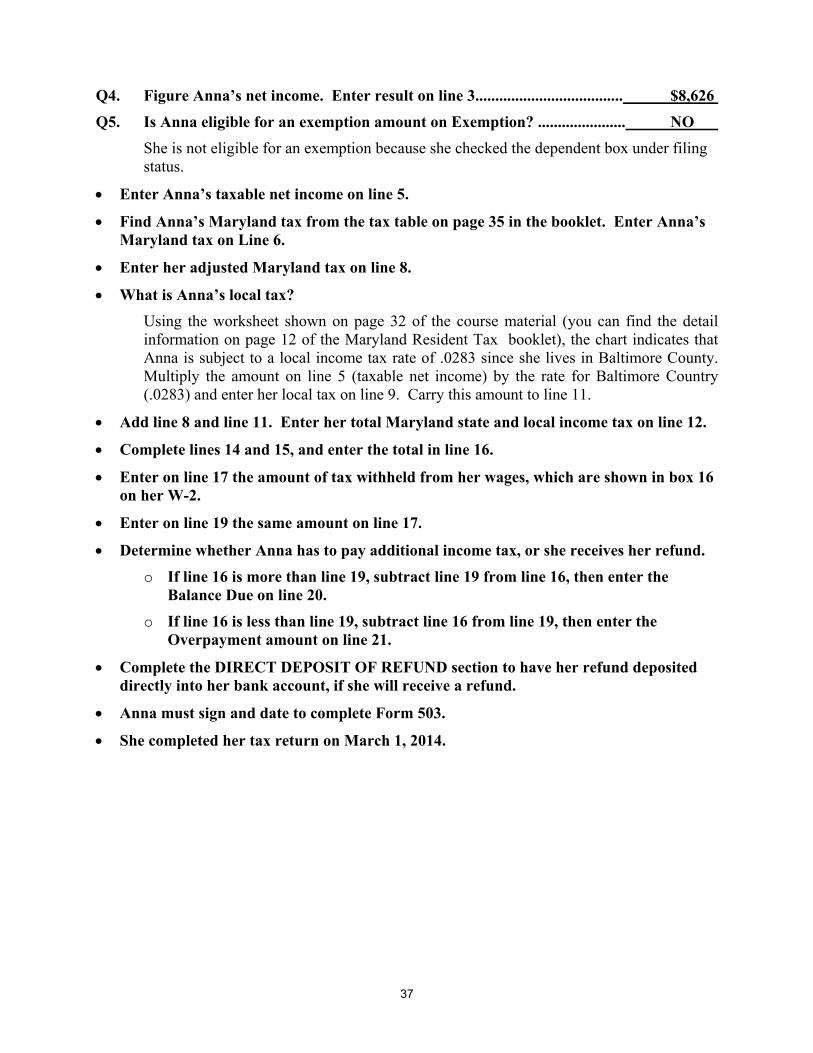

32

Find Anna’s Maryland tax from the tax table in page 35. Enter Anna’s Maryland tax on Line 6.

Enter her adjusted Maryland tax on line 8.

What is Anna’s local tax? Using the worksheet shown below (you can find the detail information on page 12 of the

Maryland Resident Tax booklet), the chart indicates that Anna is subject to a local income tax rate of .0283 since she lives in Baltimore County. Multiply the amount on line 5 (taxable net income) by the rate for Baltimore Country (.0283) and enter her local

tax on line 9. Carry this amount to line 11.

Add line 8 and line 11. Enter her total Maryland state and local income tax on line 12.

Complete lines 13 and 15, and enter the total in line 16.

Enter on line 17 the amount of tax withheld from her wages, which are shown in box 16 on her W-2.

Enter on line 19 the same amount as on line 17.

Determine whether Anna has to pay additional income tax, or she receives her refund. o If line 16 is more than line 19, subtract line 19 from line 16, and then enter the

Balance Due amount on line 20. o If line 16 is less than line 19, subtract line 16 from line 19, and then enter the

Overpayment amount on line 21.

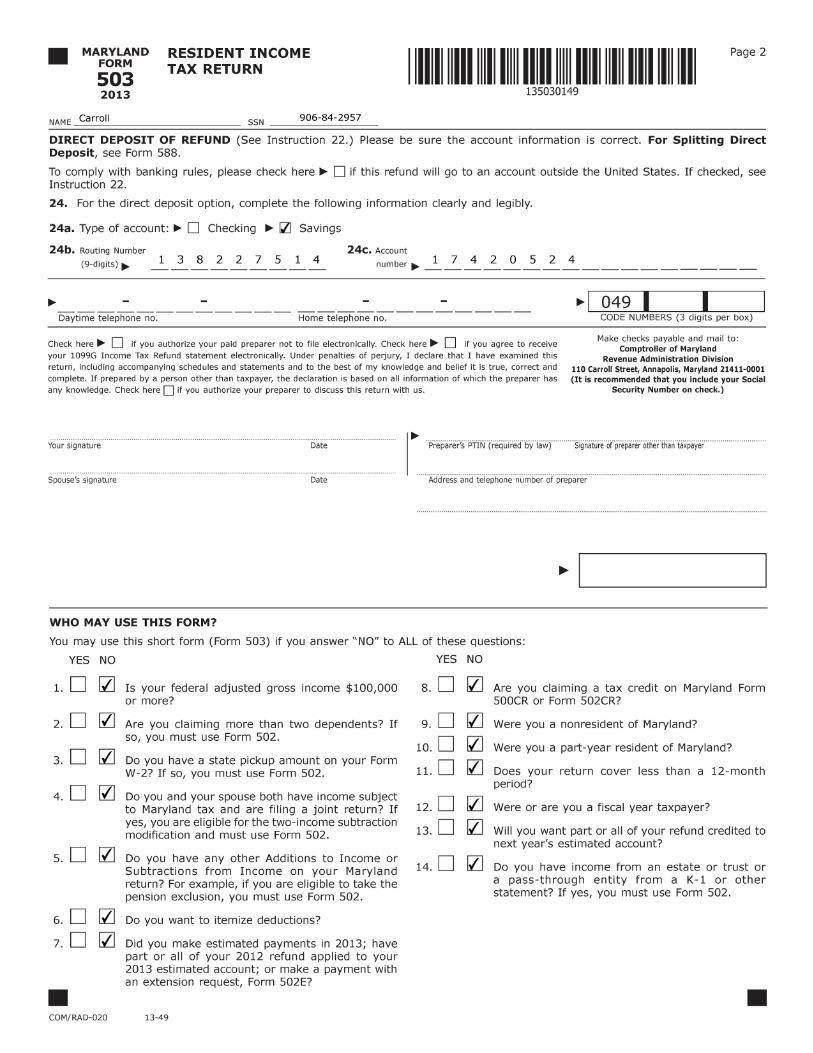

Complete the DIRECT DEPOSIT OF REFUND section to have her refund deposited directly into her bank account, if she will receive her refund.

Anna must sign and date to complete Form 503.

She completed her tax return on March 1, 2014.

LOCAL TAX WORKSHEET (19A)

Multiply the taxable net income by your local tax rate from the LOCAL TAX RATE CHART for the county in which you were a resident on the last day of the tax year. Enter the result on line 29 of Form 502 or line 9 of Form 503. This is your local income tax.

1. TAXABLE net income from line 21 of Form 502 or line 5 of Form 503. . . . . . . . . . . . 1. $ ___________

2. LOCAL tax rate from chart above. The first

digit has been entered for you. . . . . . . . . .2.

3. LOCAL income tax (Multiply line 1 by line 2.) Enter this amount on line 29 of Form 502 or line 9 of Form 503 rounded to the nearest cent or whole dollar. . . . . . . . . . . 3. $ ___________

2013

$

MARYLAND FORM

503

COM/RAD-020 13-49

RESIDENT INCOME TAX RETURN

1. Adjusted gross income from your federal return (See Instruction 11.) (If amount is $100,000 or more, stop and use Form 502.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1. _________________________

1a. Wages, salaries and/or tips (See Instruction 11.) . . . . . . . . . . . . . 1a. _______________________

1b. Earned income (See Instruction 11.) . . . . . . . . . . . . . . . . . . . . . 1b. _______________________

2. Standard deduction (See Instruction 16.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. _________________________

3. Net income (Subtract line 2 from line 1.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3. _________________________

4. Exemption amount as computed above . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4. _________________________

5. Taxable net income (Subtract line 4 from line 3. See Tax Table in Resident Instructions.) . . . . . . . . . . . . . . . . . . . 5. _________________________

6. Maryland tax from Tax Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6. _________________________

7. Earned income credit Poverty level credit (See Instruction 18.) Total 7. _________________________

8. Maryland tax after credits (Subtract line 7 from line 6.) If less than 0, enter 0. . . . . . . . . . . . . . . . . . . . . . . . . . 8. _________________________

9. Local tax (See Instruction 19 for tax rates and worksheet.) Multiply line 5 by your local tax rate .___ ___ ___ ___ 9. _________________________

10. Local: Earned income credit Poverty level credit (See Instruction 19.) Total 10. _________________________

11. Local tax after credits (Subtract line 10 from line 9.) If less than 0, enter 0 . . . . . . . . . . . . . . . . . . . . . . . . . . . 11. _________________________

12. Total Maryland and local tax (Add lines 8 and 11.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12. _________________________

13. Contributions to Chesapeake Bay and Endangered Species Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13. _________________________

14. Contributions to Developmental Disabilities Waiting List Equity Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14. _________________________

15. Contributions to Maryland Cancer Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15. _________________________

16. Total Maryland income tax, local income tax and contributions (Add lines 12 through 15.) . . . . . . . . . . . . . 16. _________________________

17. Total Maryland and local tax withheld (Enter total from and attach your W-2 and 1099 forms if MD tax is withheld.) 17. _________________________

18. Refundable earned income credit (from worksheet in Instruction 21) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18. _________________________

19. Total payments and credit (Add lines 17 and 18.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19. _________________________

20. Balance due (If line 16 is more than line 19, subtract line 19 from line 16.) . . . . . . . . . . . . . . . . . . . . . . . . . . . 20. _________________________

21. Overpayment (If line 16 is less than line 19, subtract line 16 from line 19.) See line 24 . . This is your 21. _________________________

22. Interest charges from Form 502UP or for late filing (See Instruction 22.) Total . 22. _________________________

23. TOTAL AMOUNT DUE (Add lines 20 and 22.) IF $1 OR MORE, PAY IN FULL WITH THIS RETURN . . . . . . . . . 23. _________________________

0

REFUND

Place CHECK

or MONEY ORDER

on top of your W-2 wage and

tax statements

and ATTACH HERE

with ONE staple.

EXEMPTIONS (A) Yourself Spouse

(B) 65 or over Blind 65 or over Blind

FILING STATUS See Instruction 1 to determine if you are required to file.CHECK ONE BOX

1. Single (If you can be claimed on another person’s tax return, use Filing Status 6.)

2. Married filing joint return or spouse had no income

3. Married filing separately

4. Head of household

5. Qualifying widow(er) with dependent child

6. Dependent taxpayer (Enter 0 in Exemption Box (A). See Instruction 7.)

See Instruction 10

(C) Dependents (1)

First Name Last Name

(2)

Social Security Number

(3)

Relationship

(4)

Check if Dep under age 19.

(5)If (4) is checked,

does child have health insurance now?

(6)

Regular

(7)

65 or over

YES NO

YES NO

(A) Enter No. Checked . . . x $3,200 . . . . . . .$ _____________

(B) Enter No. Checked x $1,000 . . . . . . .$ _____________

(C) Enter No. Checked in Columns 6 & 7 . . . . x $3,200 . . . . . . .$ _____________(D) Enter Total Exemptions (Add A, B and C.) . . Total Amount . . $ ____________

Check here if you authorize us to share your tax information with the Medical Assistance Program for help finding health insurance. NOTE: If you are claiming more than two dependents, you must use Form 502.

Social Security Number Spouse's Social Security Number

Your First Name Initial Last Name

Spouse's First Name Initial Last Name

Present Address (Number and street)

City or Town State ZIP code

Maryland county City, town or taxing area Name of county and incorporated city, town or special taxing area in which you were a resident on the last day of the taxable period. (See Instruction 6.)

Pri

nt

Usi

ng

Blu

e o

r B

lack

In

k O

nly

Spouse's Social Security Number

Complete and Submit Page 2

See Page 2 before beginning this form.

10a 10b

7a 7b

|

||||||||||||||||||||||

||

MARYLANDFORM

5032013

COM/RAD-020 13-49

RESIDENT INCOME TAX RETURN

1. Is your federal adjusted gross income $100,000 or more?

2. Are you claiming more than two dependents? If so, you must use Form 502.

3. Do you have a state pickup amount on your Form W-2? If so, you must use Form 502.

4. Do you and your spouse both have income subject to Maryland tax and are filing a joint return? If yes, you are eligible for the two-income subtraction modification and must use Form 502.

5. Do you have any other Additions to Income or Subtractions from Income on your Maryland return? For example, if you are eligible to take the pension exclusion, you must use Form 502.

6. Do you want to itemize deductions?

7. Did you make estimated payments in 2013; have part or all of your 2012 refund applied to your 2013 estimated account; or make a payment with an extension request, Form 502E?

8. Are you claiming a tax credit on Maryland Form 500CR or Form 502CR?

9. Were you a nonresident of Maryland?

10. Were you a part-year resident of Maryland?

11. Does your return cover less than a 12-month period?

12. Were or are you a fiscal year taxpayer?

13. Will you want part or all of your refund credited to next year’s estimated account?

14. Do you have income from an estate or trust or a pass-through entity from a K-1 or other statement? If yes, you must use Form 502.

WHO MAY USE THIS FORM?

You may use this short form (Form 503) if you answer “NO” to ALL of these questions:

YES NO YES NO

DIRECT DEPOSIT OF REFUND (See Instruction 22.) Please be sure the account information is correct. For Splitting Direct Deposit, see Form 588.

To comply with banking rules, please check here if this refund will go to an account outside the United States. If checked, see Instruction 22.

24. For the direct deposit option, complete the following information clearly and legibly.

24a. Type of account: Checking Savings

24b. Routing Number 24c. Account

(9-digits) number

Make checks payable and mail to:Comptroller of Maryland

Revenue Administration Division110 Carroll Street, Annapolis, Maryland 21411-0001 (It is recommended that you include your Social

Security Number on check.)

Daytime telephone no. Home telephone no.-- --

Check here if you authorize your paid preparer not to file electronically. Check here if you agree to receive your 1099G Income Tax Refund statement electronically. Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements and to the best of my knowledge and belief it is true, correct and complete. If prepared by a person other than taxpayer, the declaration is based on all information of which the preparer has any knowledge. Check here if you authorize your preparer to discuss this return with us.

CODE NUMBERS (3 digits per box)049

NAME __________________________________ SSN ______________________

Your signature Date Preparer’s PTIN (required by law) Signature of preparer other than taxpayer

Spouse’s signature Date Address and telephone number of preparer

Page 2

18

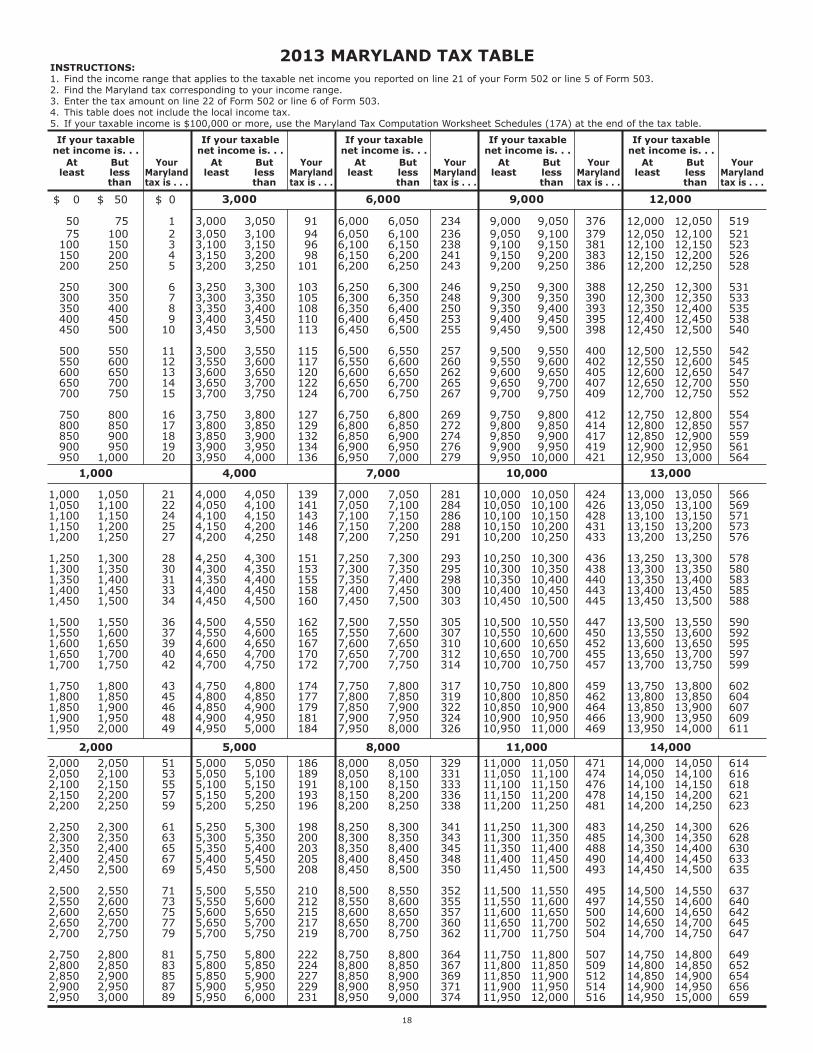

2013 MARYLAND TAX TABLEINSTRUCTIONS:1. Find the income range that applies to the taxable net income you reported on line 21 of your Form 502 or line 5 of Form 503.2. Find the Maryland tax corresponding to your income range.3. Enter the tax amount on line 22 of Form 502 or line 6 of Form 503.4. This table does not include the local income tax.5. If your taxable income is $100,000 or more, use the Maryland Tax Computation Worksheet Schedules (17A) at the end of the tax table.

3,000 6,000 9,000 12,000

50 75 1 3,000 3,050 91 6,000 6,050 234 9,000 9,050 376 12,000 12,050 519 75 100 2 3,050 3,100 94 6,050 6,100 236 9,050 9,100 379 12,050 12,100 521 100 150 3 3,100 3,150 96 6,100 6,150 238 9,100 9,150 381 12,100 12,150 523 150 200 4 3,150 3,200 98 6,150 6,200 241 9,150 9,200 383 12,150 12,200 526 200 250 5 3,200 3,250 101 6,200 6,250 243 9,200 9,250 386 12,200 12,250 528

250 300 6 3,250 3,300 103 6,250 6,300 246 9,250 9,300 388 12,250 12,300 531 300 350 7 3,300 3,350 105 6,300 6,350 248 9,300 9,350 390 12,300 12,350 533 350 400 8 3,350 3,400 108 6,350 6,400 250 9,350 9,400 393 12,350 12,400 535 400 450 9 3,400 3,450 110 6,400 6,450 253 9,400 9,450 395 12,400 12,450 538 450 500 10 3,450 3,500 113 6,450 6,500 255 9,450 9,500 398 12,450 12,500 540

500 550 11 3,500 3,550 115 6,500 6,550 257 9,500 9,550 400 12,500 12,550 542 550 600 12 3,550 3,600 117 6,550 6,600 260 9,550 9,600 402 12,550 12,600 545 600 650 13 3,600 3,650 120 6,600 6,650 262 9,600 9,650 405 12,600 12,650 547 650 700 14 3,650 3,700 122 6,650 6,700 265 9,650 9,700 407 12,650 12,700 550 700 750 15 3,700 3,750 124 6,700 6,750 267 9,700 9,750 409 12,700 12,750 552

750 800 16 3,750 3,800 127 6,750 6,800 269 9,750 9,800 412 12,750 12,800 554 800 850 17 3,800 3,850 129 6,800 6,850 272 9,800 9,850 414 12,800 12,850 557 850 900 18 3,850 3,900 132 6,850 6,900 274 9,850 9,900 417 12,850 12,900 559 900 950 19 3,900 3,950 134 6,900 6,950 276 9,900 9,950 419 12,900 12,950 561 950 1,000 20 3,950 4,000 136 6,950 7,000 279 9,950 10,000 421 12,950 13,000 564 1,000 4,000 7,000 10,000 13,000

1,000 1,050 21 4,000 4,050 139 7,000 7,050 281 10,000 10,050 424 13,000 13,050 566 1,050 1,100 22 4,050 4,100 141 7,050 7,100 284 10,050 10,100 426 13,050 13,100 569 1,100 1,150 24 4,100 4,150 143 7,100 7,150 286 10,100 10,150 428 13,100 13,150 571 1,150 1,200 25 4,150 4,200 146 7,150 7,200 288 10,150 10,200 431 13,150 13,200 573 1,200 1,250 27 4,200 4,250 148 7,200 7,250 291 10,200 10,250 433 13,200 13,250 576

1,250 1,300 28 4,250 4,300 151 7,250 7,300 293 10,250 10,300 436 13,250 13,300 578 1,300 1,350 30 4,300 4,350 153 7,300 7,350 295 10,300 10,350 438 13,300 13,350 580 1,350 1,400 31 4,350 4,400 155 7,350 7,400 298 10,350 10,400 440 13,350 13,400 583 1,400 1,450 33 4,400 4,450 158 7,400 7,450 300 10,400 10,450 443 13,400 13,450 585 1,450 1,500 34 4,450 4,500 160 7,450 7,500 303 10,450 10,500 445 13,450 13,500 588

1,500 1,550 36 4,500 4,550 162 7,500 7,550 305 10,500 10,550 447 13,500 13,550 590 1,550 1,600 37 4,550 4,600 165 7,550 7,600 307 10,550 10,600 450 13,550 13,600 592 1,600 1,650 39 4,600 4,650 167 7,600 7,650 310 10,600 10,650 452 13,600 13,650 595 1,650 1,700 40 4,650 4,700 170 7,650 7,700 312 10,650 10,700 455 13,650 13,700 597 1,700 1,750 42 4,700 4,750 172 7,700 7,750 314 10,700 10,750 457 13,700 13,750 599

1,750 1,800 43 4,750 4,800 174 7,750 7,800 317 10,750 10,800 459 13,750 13,800 602 1,800 1,850 45 4,800 4,850 177 7,800 7,850 319 10,800 10,850 462 13,800 13,850 604 1,850 1,900 46 4,850 4,900 179 7,850 7,900 322 10,850 10,900 464 13,850 13,900 607 1,900 1,950 48 4,900 4,950 181 7,900 7,950 324 10,900 10,950 466 13,900 13,950 609 1,950 2,000 49 4,950 5,000 184 7,950 8,000 326 10,950 11,000 469 13,950 14,000 611

2,000 5,000 8,000 11,000 14,000 2,000 2,050 51 5,000 5,050 186 8,000 8,050 329 11,000 11,050 471 14,000 14,050 614 2,050 2,100 53 5,050 5,100 189 8,050 8,100 331 11,050 11,100 474 14,050 14,100 616 2,100 2,150 55 5,100 5,150 191 8,100 8,150 333 11,100 11,150 476 14,100 14,150 618 2,150 2,200 57 5,150 5,200 193 8,150 8,200 336 11,150 11,200 478 14,150 14,200 621 2,200 2,250 59 5,200 5,250 196 8,200 8,250 338 11,200 11,250 481 14,200 14,250 623

2,250 2,300 61 5,250 5,300 198 8,250 8,300 341 11,250 11,300 483 14,250 14,300 626 2,300 2,350 63 5,300 5,350 200 8,300 8,350 343 11,300 11,350 485 14,300 14,350 628 2,350 2,400 65 5,350 5,400 203 8,350 8,400 345 11,350 11,400 488 14,350 14,400 630 2,400 2,450 67 5,400 5,450 205 8,400 8,450 348 11,400 11,450 490 14,400 14,450 633 2,450 2,500 69 5,450 5,500 208 8,450 8,500 350 11,450 11,500 493 14,450 14,500 635

2,500 2,550 71 5,500 5,550 210 8,500 8,550 352 11,500 11,550 495 14,500 14,550 637 2,550 2,600 73 5,550 5,600 212 8,550 8,600 355 11,550 11,600 497 14,550 14,600 640 2,600 2,650 75 5,600 5,650 215 8,600 8,650 357 11,600 11,650 500 14,600 14,650 642 2,650 2,700 77 5,650 5,700 217 8,650 8,700 360 11,650 11,700 502 14,650 14,700 645 2,700 2,750 79 5,700 5,750 219 8,700 8,750 362 11,700 11,750 504 14,700 14,750 647

2,750 2,800 81 5,750 5,800 222 8,750 8,800 364 11,750 11,800 507 14,750 14,800 649 2,800 2,850 83 5,800 5,850 224 8,800 8,850 367 11,800 11,850 509 14,800 14,850 652 2,850 2,900 85 5,850 5,900 227 8,850 8,900 369 11,850 11,900 512 14,850 14,900 654 2,900 2,950 87 5,900 5,950 229 8,900 8,950 371 11,900 11,950 514 14,900 14,950 656 2,950 3,000 89 5,950 6,000 231 8,950 9,000 374 11,950 12,000 516 14,950 15,000 659

$ 0 $ 50 $10

If your taxable net income is. . .

At least

But less than

Your Maryland tax is . . .

If your taxable net income is. . .