Understanding & Managing Finance Seminar 9. Seminar Nine - Activities Preparation: read M & A...

34

Understanding & Managing Finance Seminar 9

-

Upload

prosper-newton -

Category

Documents

-

view

217 -

download

1

Transcript of Understanding & Managing Finance Seminar 9. Seminar Nine - Activities Preparation: read M & A...

Understanding & Managing Finance

Seminar 9

Seminar Nine - Activities

Preparation: read M & A Chapter 16

Exercises: Working Capital Internet Links M & A Exercise 16.3 Spreadsheet

Starting Points 1

Define what is meant by Working Capital, and name some of the important elements.

Explain what is meant by the Working Capital Cycle, and why this is important.

State what is meant by the Operating Cash Cycle, and explain how this can be calculated.

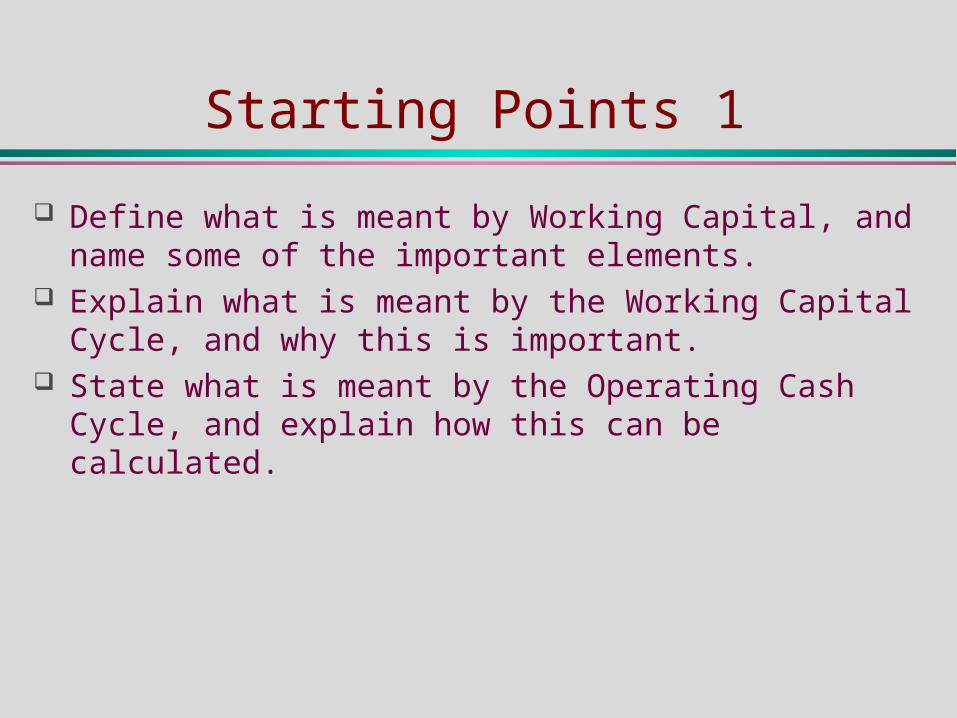

The nature and purpose of working capital

Major elements Major element

Stocks

Trade debtors

Cash (in hand and at bank)

Trade creditors

lessequals

Current liabilitiesWorking capital Current assets

The summary diagram

The summary diagram

The Working Capital Cycle

Cash sales

Trade creditors

Trade debtors

Finished goods

Cash/bank overdraft

Work-in-progress

Raw materials

Each ‘pass’ through the Working Capital Cycle will generate profit.

Each ‘pass’ through the Working Capital Cycle will generate profit.

equals

minus

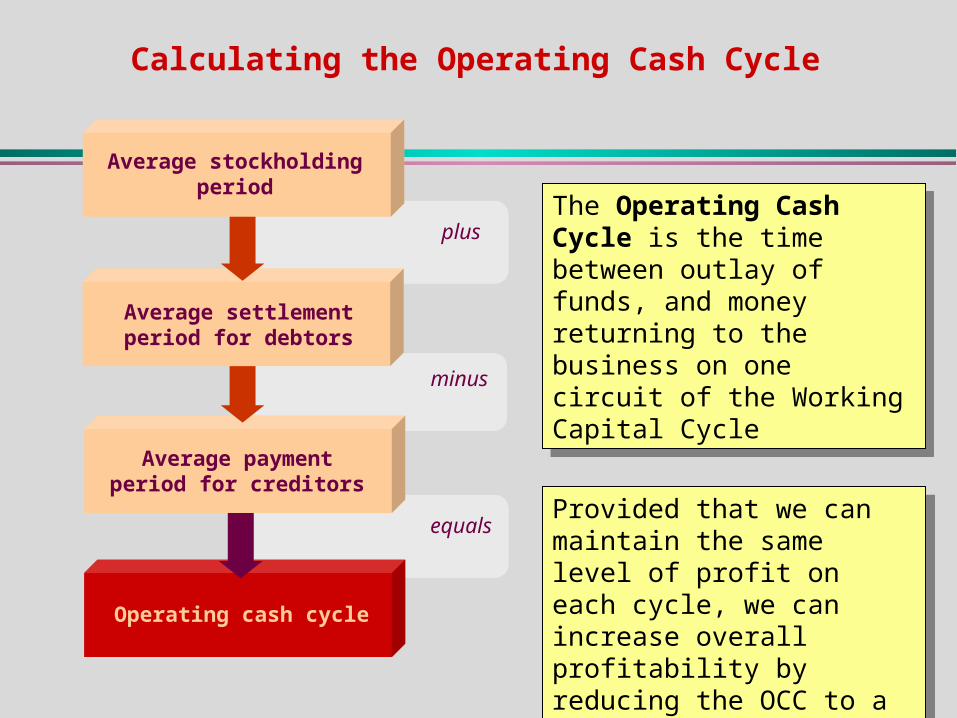

Operating cash cycle

Average payment period for creditors

Average settlement period for debtors

plus

Average stockholding period

Calculating the Operating Cash Cycle

The Operating Cash Cycle is the time between outlay of funds, and money returning to the business on one circuit of the Working Capital Cycle

The Operating Cash Cycle is the time between outlay of funds, and money returning to the business on one circuit of the Working Capital Cycle

Provided that we can maintain the same level of profit on each cycle, we can increase overall profitability by reducing the OCC to a minimum.

Provided that we can maintain the same level of profit on each cycle, we can increase overall profitability by reducing the OCC to a minimum.

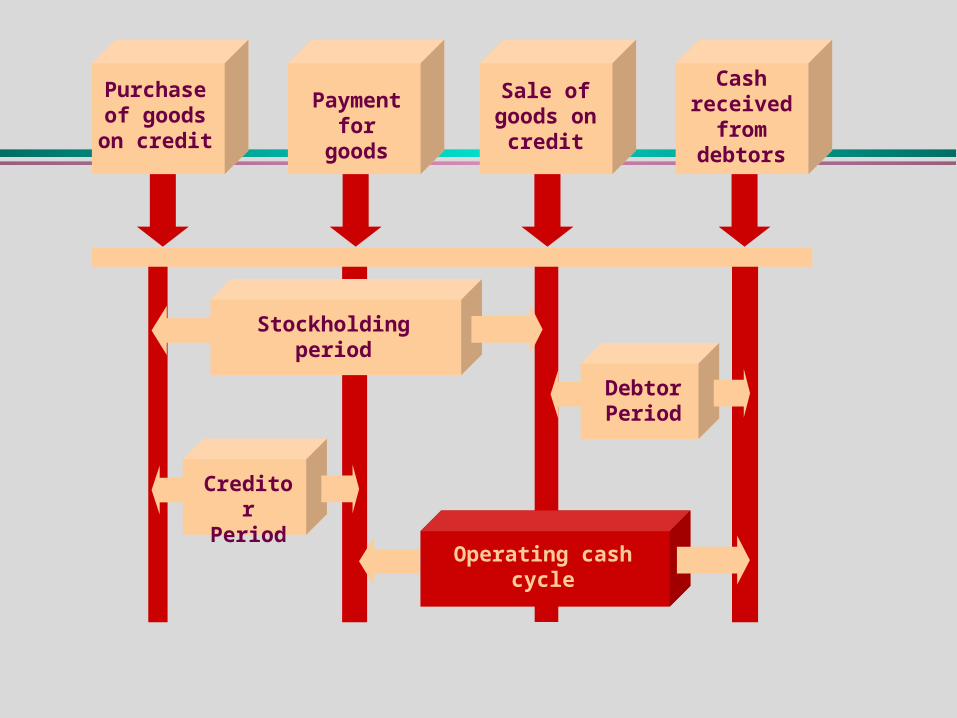

Purchase of goods on credit

Payment for goods

Sale of goods on

credit

Cash received

from debtors

Stockholding period

Operating cash cycle

Creditor Period

Debtor Period

Starting Points 2

Why might it be a good idea to minimise the the Operating Cash cycle and Working Capital Requirements?

Taking each of the major elements of Working Capital in turn, state whether these need to go up or down, and why.

Starting Points 2

The Operating Cash Cycle is the time between paying out money, and getting a return on that money. The faster we can do this, the more opportunities there are to re-invest the money and getting a return on it.

Working Capital is the net amount of money invested in short term assets. On each pass through the Working Capital cycle we generate profits. Therefore we need to ensure that the money we have invested here is working for us effectively, invested in the right things, and that it does not stay in one place for too long.

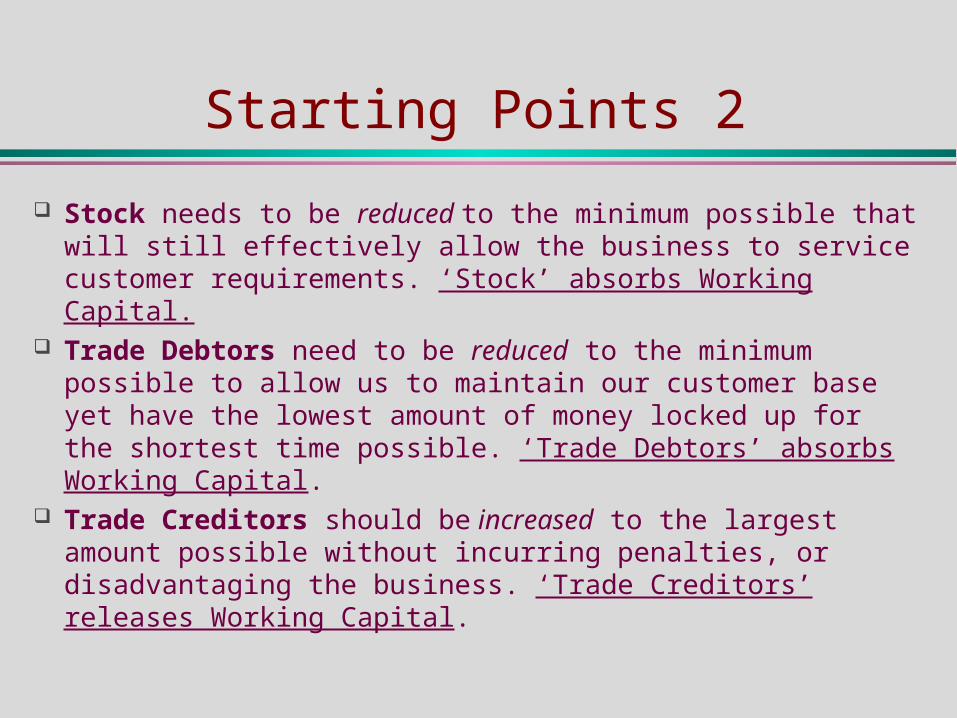

Starting Points 2

Stock needs to be reduced to the minimum possible that will still effectively allow the business to service customer requirements. ‘Stock’ absorbs Working Capital.

Trade Debtors need to be reduced to the minimum possible to allow us to maintain our customer base yet have the lowest amount of money locked up for the shortest time possible. ‘Trade Debtors’ absorbs Working Capital.

Trade Creditors should be increased to the largest amount possible without incurring penalties, or disadvantaging the business. ‘Trade Creditors’ releases Working Capital.

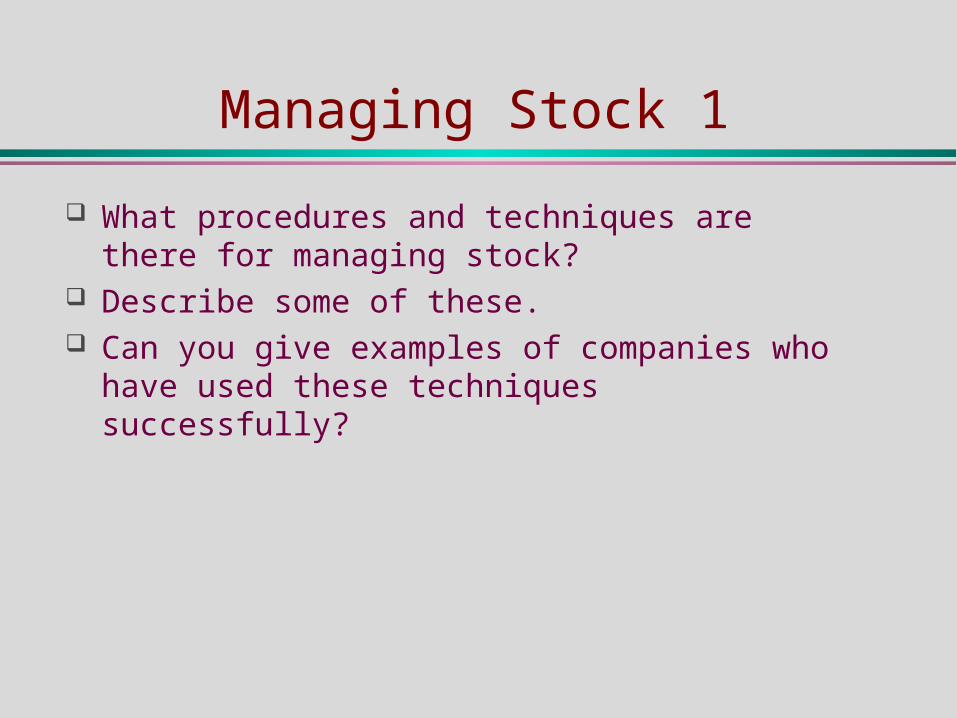

Managing Stock 1

What procedures and techniques are there for managing stock?

Describe some of these. Can you give examples of companies who have

used these techniques successfully?

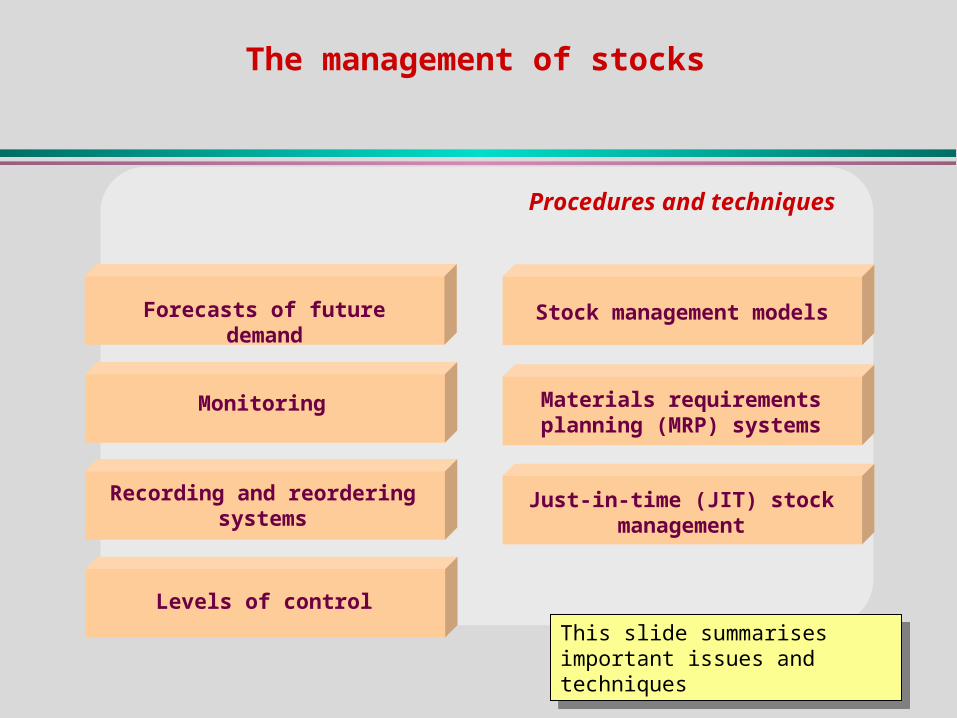

The management of stocks

Procedures and techniques

Forecasts of future demand

Monitoring

Recording and reordering systems

Levels of control

Stock management models

Materials requirements planning (MRP) systems

Just-in-time (JIT) stock management

This slide summarises important issues and techniques

This slide summarises important issues and techniques

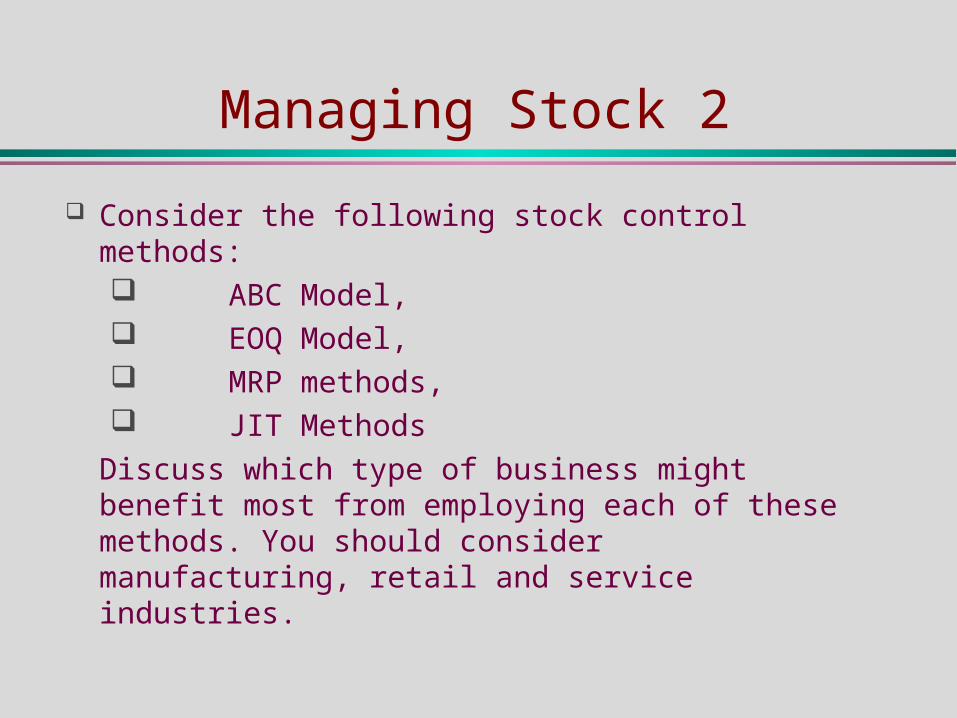

Managing Stock 2

Consider the following stock control methods: ABC Model, EOQ Model, MRP methods, JIT Methods

Discuss which type of business might benefit most from employing each of these methods. You should consider manufacturing, retail and service industries.

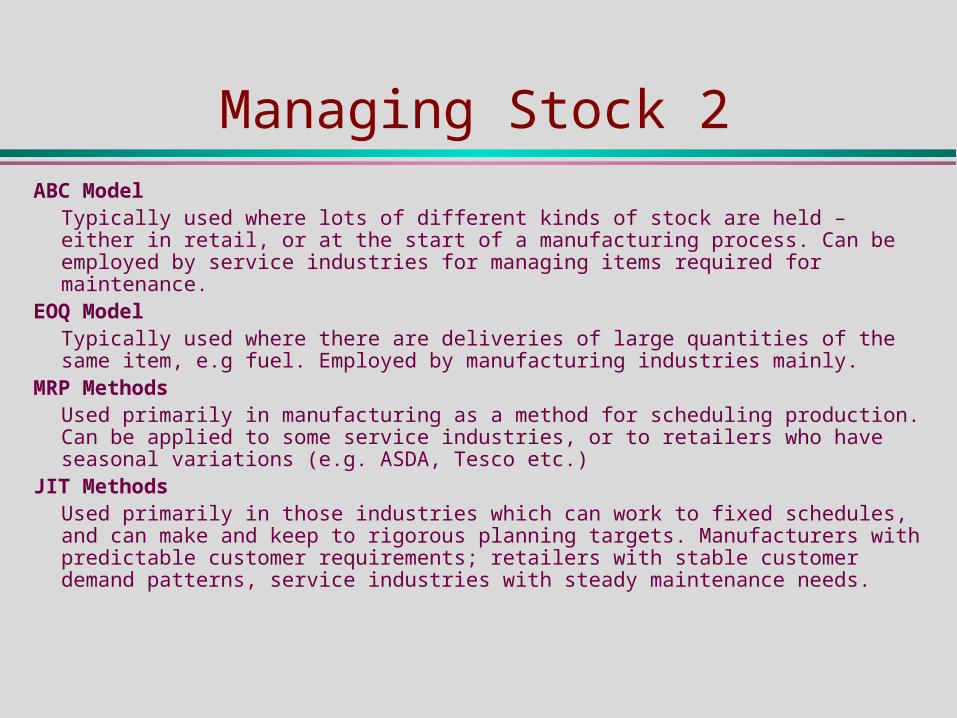

Managing Stock 2ABC Model

Typically used where lots of different kinds of stock are held – either in retail, or at the start of a manufacturing process. Can be employed by service industries for managing items required for maintenance.

EOQ ModelTypically used where there are deliveries of large quantities of the same item, e.g fuel. Employed by manufacturing industries mainly.

MRP MethodsUsed primarily in manufacturing as a method for scheduling production. Can be applied to some service industries, or to retailers who have seasonal variations (e.g. ASDA, Tesco etc.)

JIT MethodsUsed primarily in those industries which can work to fixed schedules, and can make and keep to rigorous planning targets. Manufacturers with predictable customer requirements; retailers with stable customer demand patterns, service industries with steady maintenance needs.

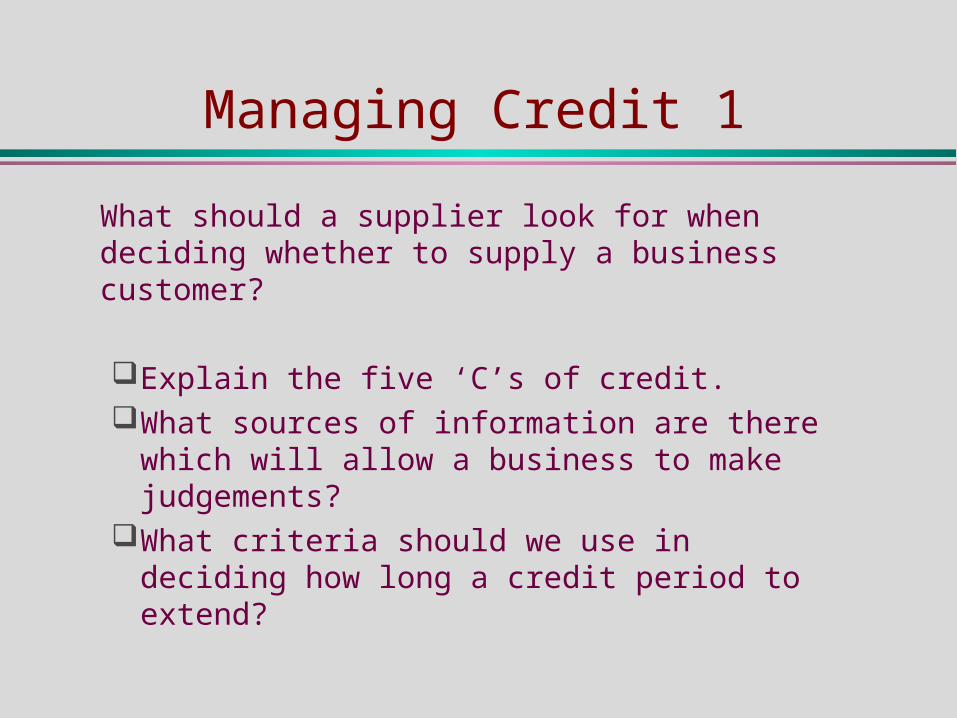

Managing Credit 1

What should a supplier look for when deciding whether to supply a business customer?

Explain the five ‘C’s of credit.What sources of information are there which will

allow a business to make judgements?What criteria should we use in deciding how long

a credit period to extend?

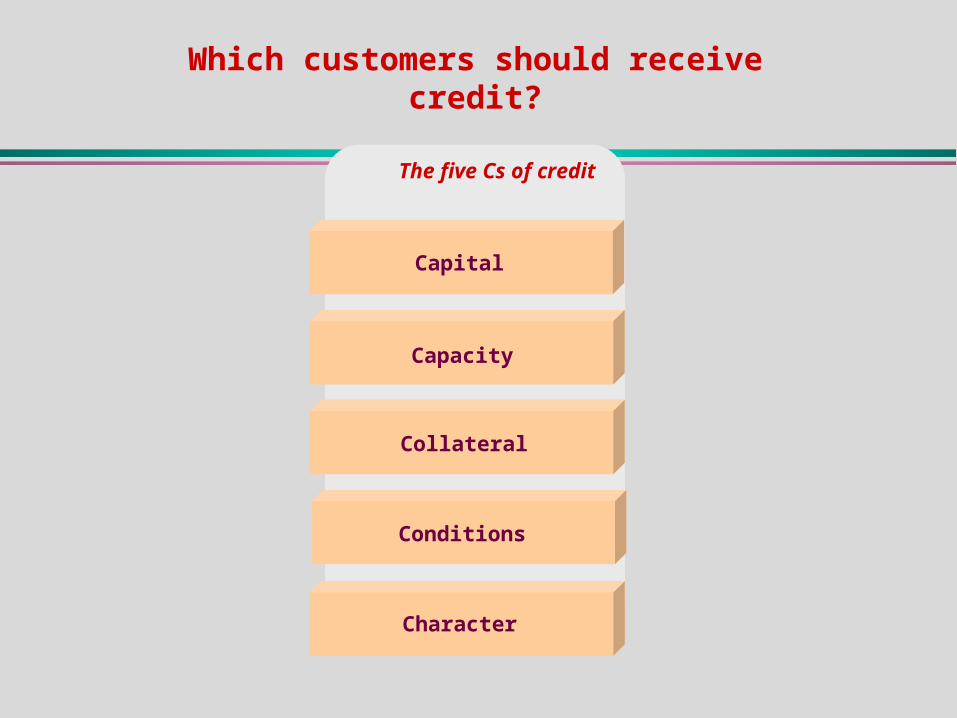

The five Cs of credit

Capital

Capacity

Collateral

Conditions

Character

Which customers should receive credit?

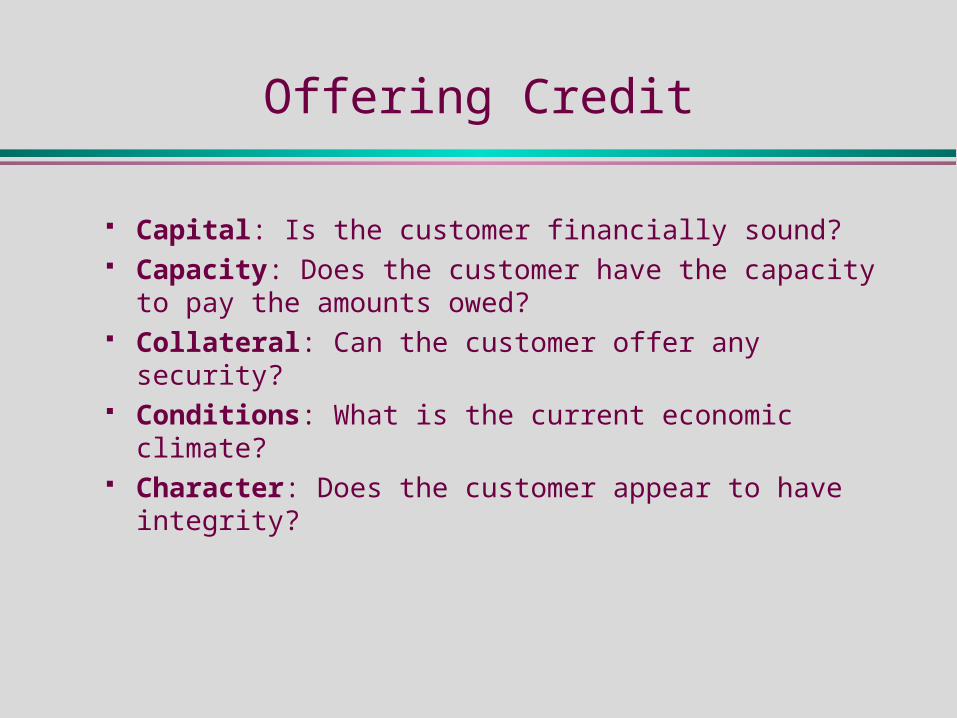

Offering Credit

Capital: Is the customer financially sound? Capacity: Does the customer have the capacity to

pay the amounts owed? Collateral: Can the customer offer any security? Conditions: What is the current economic climate? Character: Does the customer appear to have

integrity?

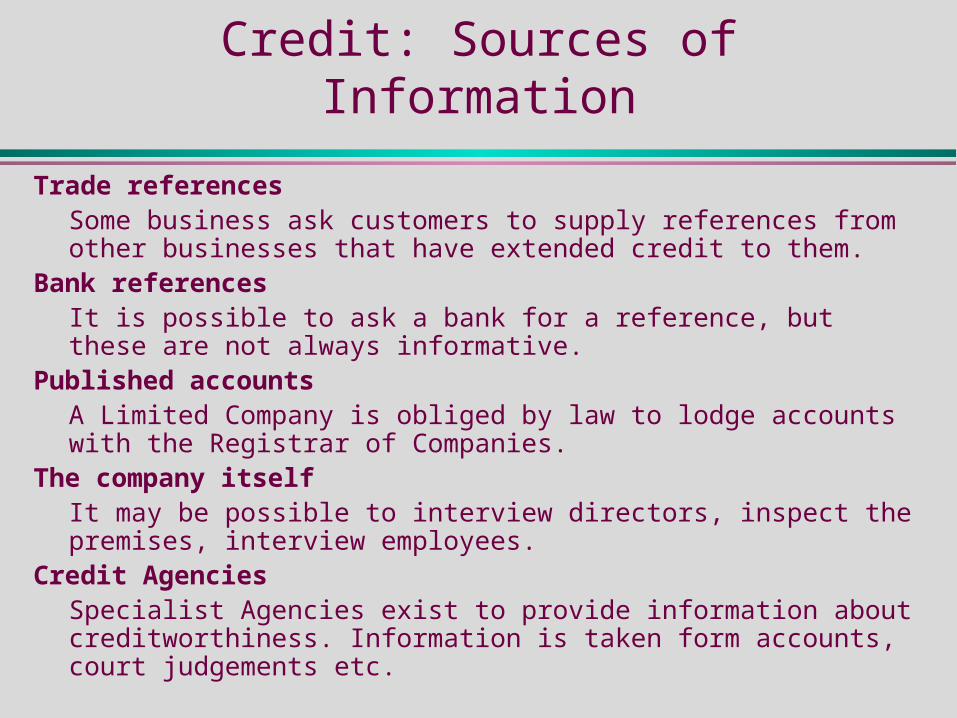

Credit: Sources of Information

Trade referencesSome business ask customers to supply references from other businesses that have extended credit to them.

Bank referencesIt is possible to ask a bank for a reference, but these are not always informative.

Published accountsA Limited Company is obliged by law to lodge accounts with the Registrar of Companies.

The company itselfIt may be possible to interview directors, inspect the premises, interview employees.

Credit AgenciesSpecialist Agencies exist to provide information about creditworthiness. Information is taken form accounts, court judgements etc.

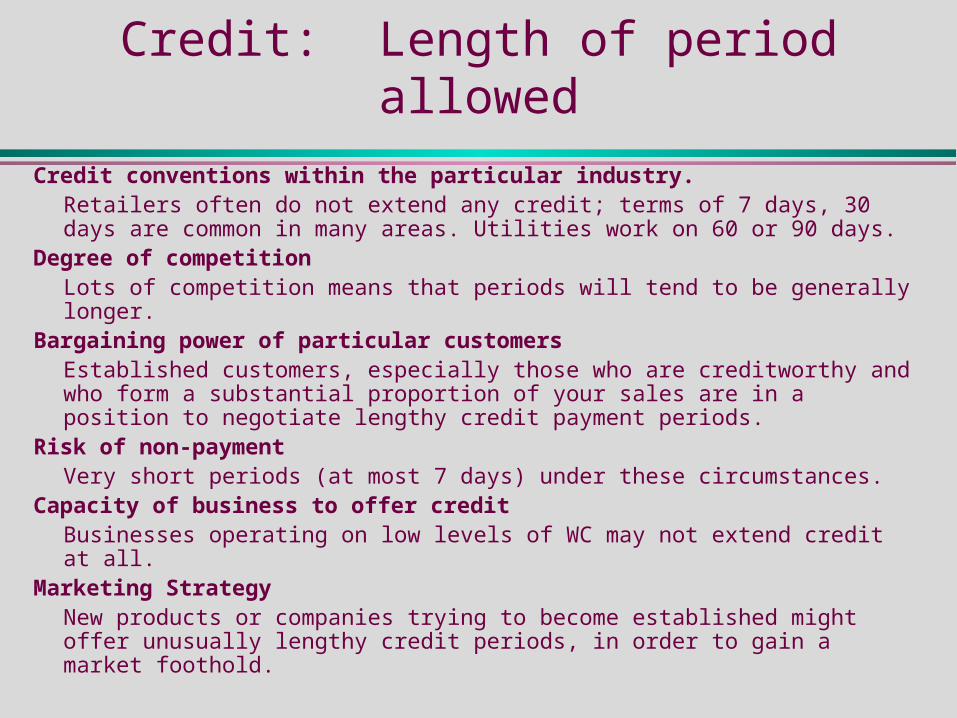

Credit: Length of period allowed

Credit conventions within the particular industry.Retailers often do not extend any credit; terms of 7 days, 30 days are common in many areas. Utilities work on 60 or 90 days.

Degree of competitionLots of competition means that periods will tend to be generally longer.

Bargaining power of particular customersEstablished customers, especially those who are creditworthy and who form a substantial proportion of your sales are in a position to negotiate lengthy credit payment periods.

Risk of non-paymentVery short periods (at most 7 days) under these circumstances.

Capacity of business to offer creditBusinesses operating on low levels of WC may not extend credit at all.

Marketing StrategyNew products or companies trying to become established might offer unusually lengthy credit periods, in order to gain a market foothold.

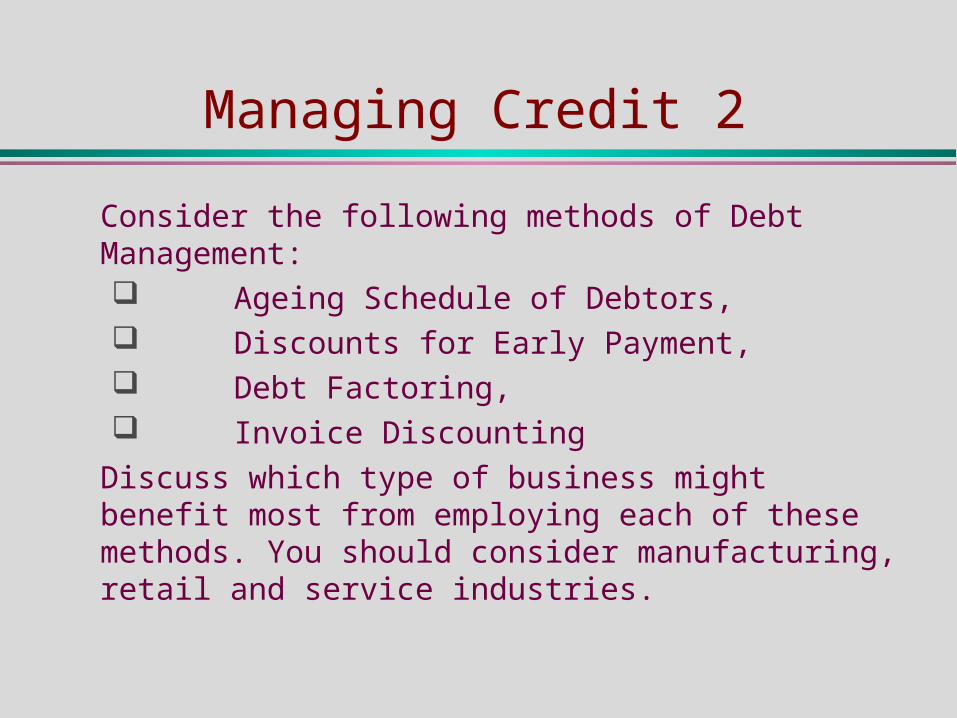

Managing Credit 2

Consider the following methods of Debt Management: Ageing Schedule of Debtors, Discounts for Early Payment, Debt Factoring, Invoice Discounting

Discuss which type of business might benefit most from employing each of these methods. You should consider manufacturing, retail and service industries.

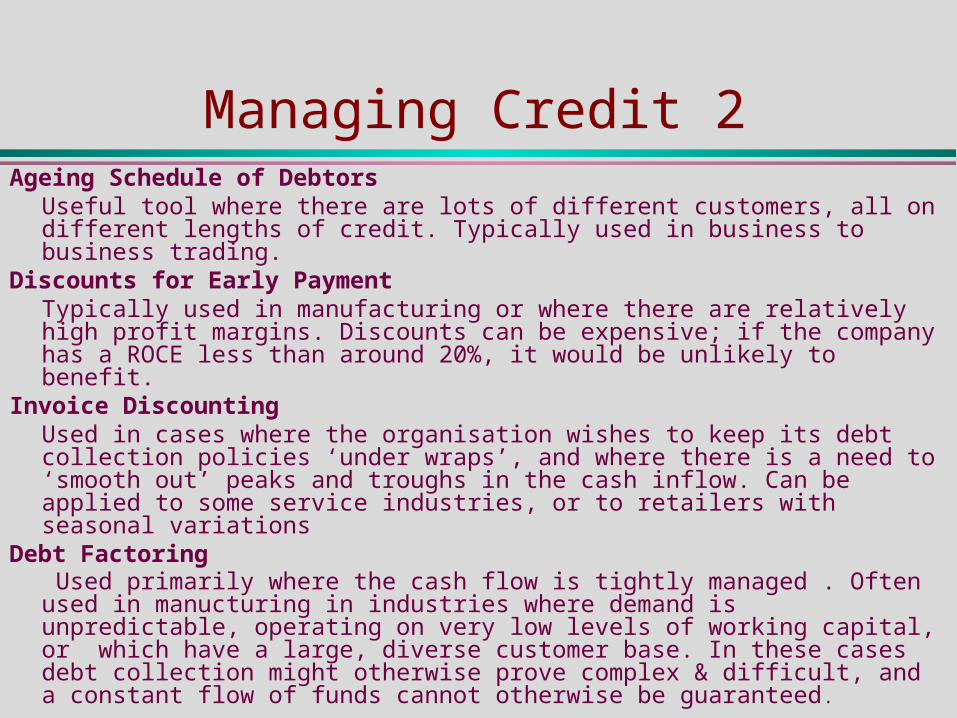

Managing Credit 2Ageing Schedule of Debtors

Useful tool where there are lots of different customers, all on different lengths of credit. Typically used in business to business trading.

Discounts for Early PaymentTypically used in manufacturing or where there are relatively high profit margins. Discounts can be expensive; if the company has a ROCE less than around 20%, it would be unlikely to benefit.

Invoice DiscountingUsed in cases where the organisation wishes to keep its debt collection policies ‘under wraps’, and where there is a need to ‘smooth out’ peaks and troughs in the cash inflow. Can be applied to some service industries, or to retailers with seasonal variations

Debt Factoring Used primarily where the cash flow is tightly managed . Often used in manucturing in industries where demand is unpredictable, operating on very low levels of working capital, or which have a large, diverse customer base. In these cases debt collection might otherwise prove complex & difficult, and a constant flow of funds cannot otherwise be guaranteed.

Working Capital Management

Working Capital Activity McLaney & Atrill Exercise 16.3

Working

Capital Activity

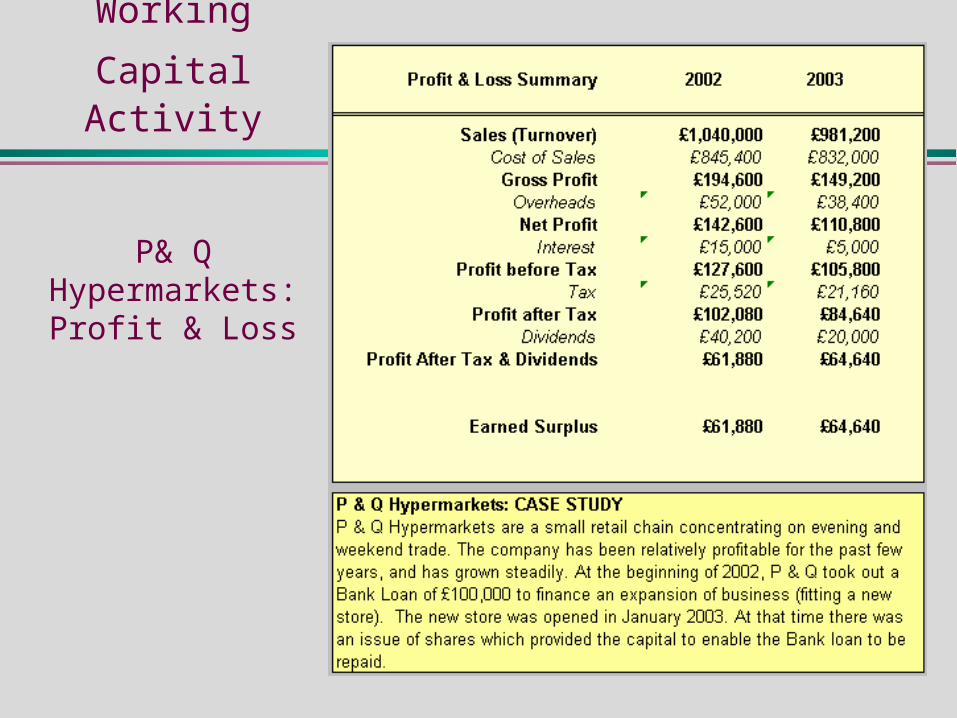

P& Q Hypermarkets:Profit & Loss

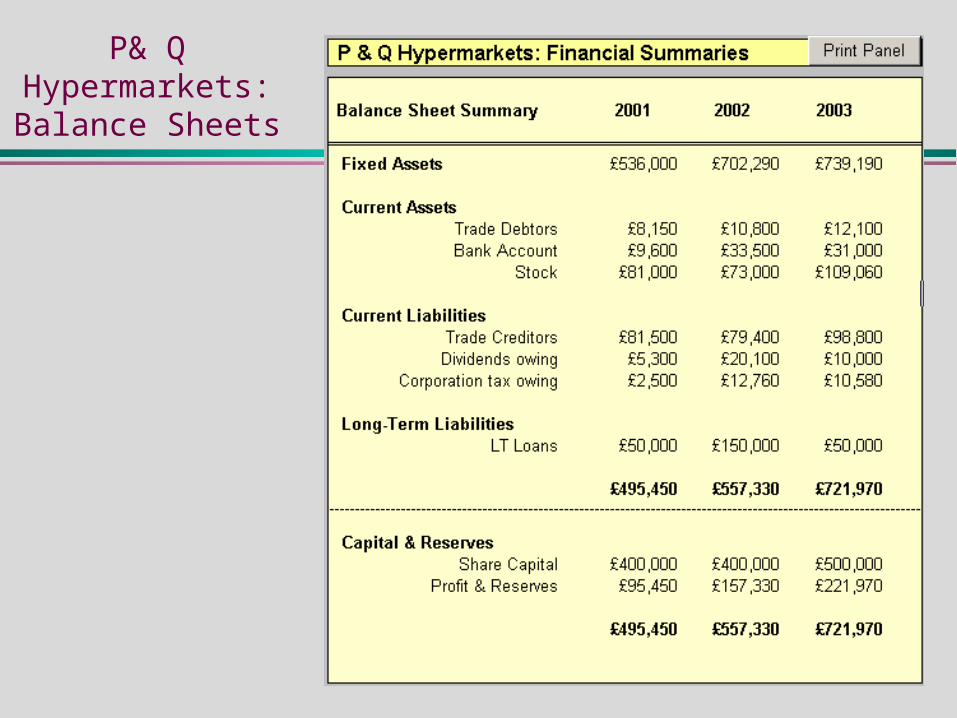

P& Q Hypermarkets:Balance Sheets

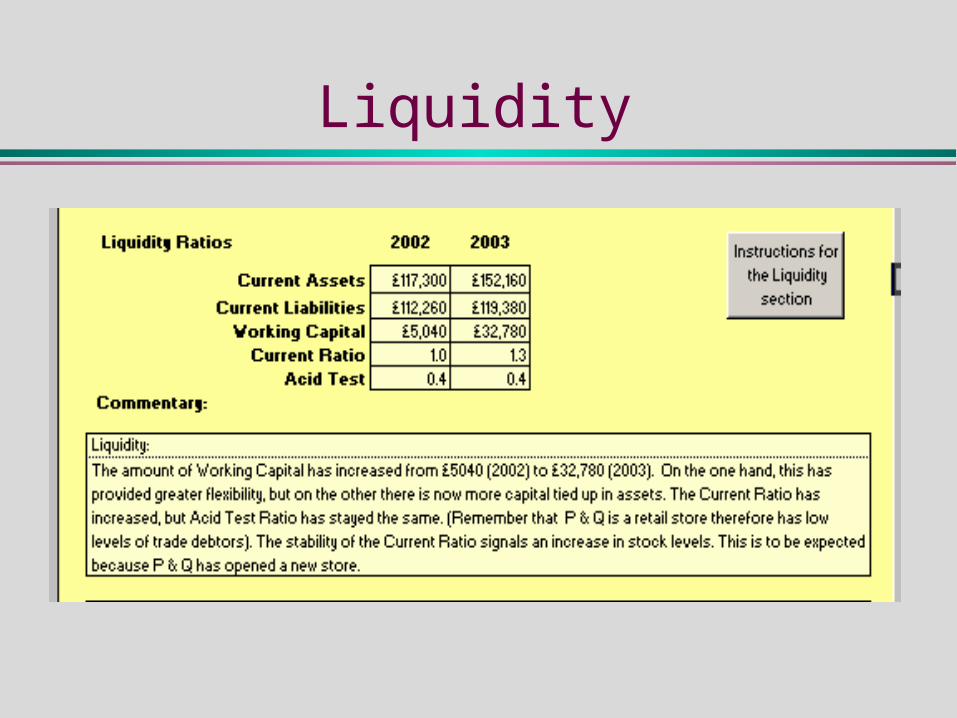

Liquidity

Efficiency

Working Capital Activity

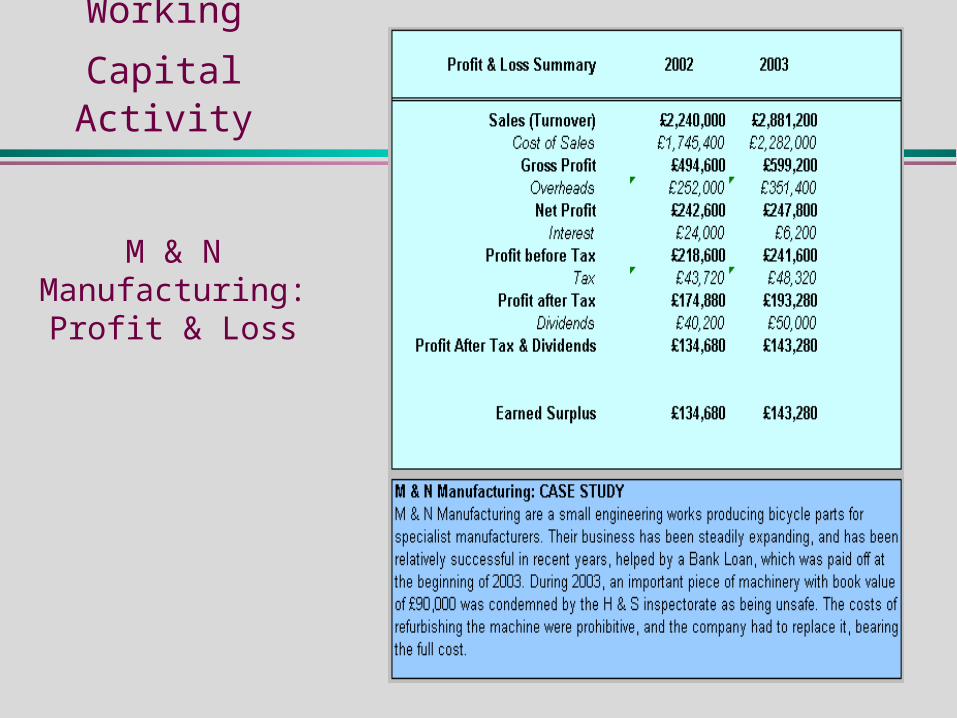

M & N Manufacturing:Profit & Loss

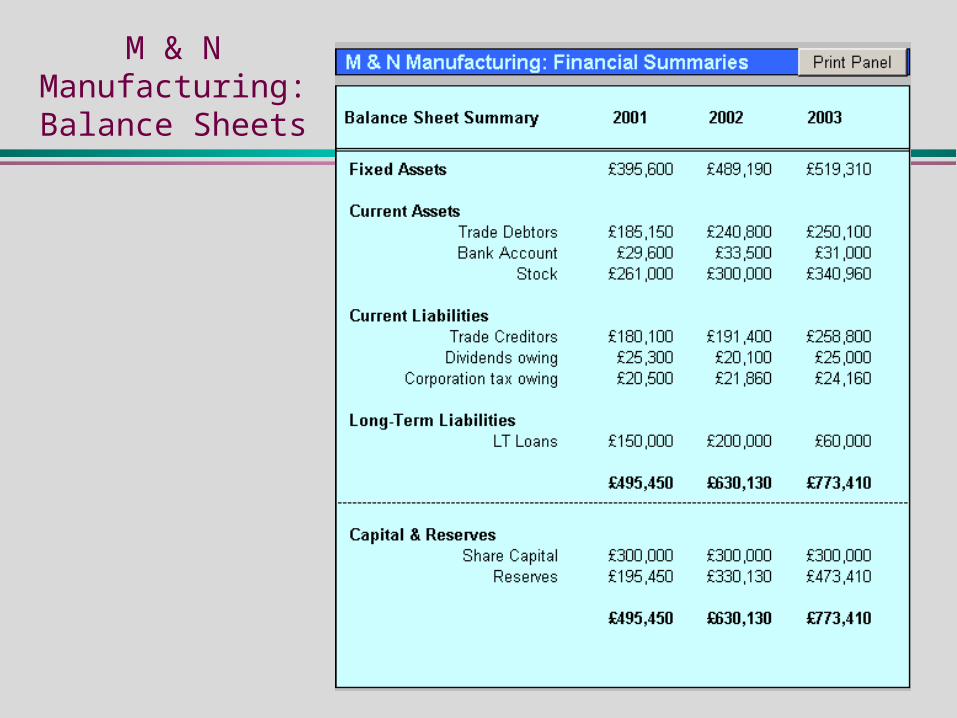

M & N Manufacturing:Balance Sheets

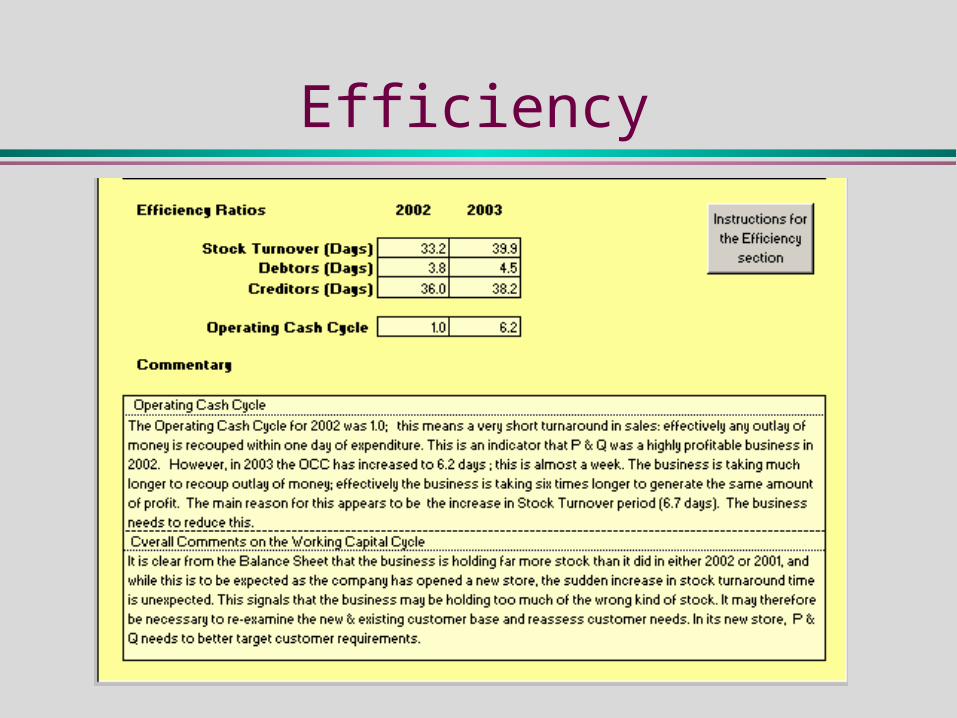

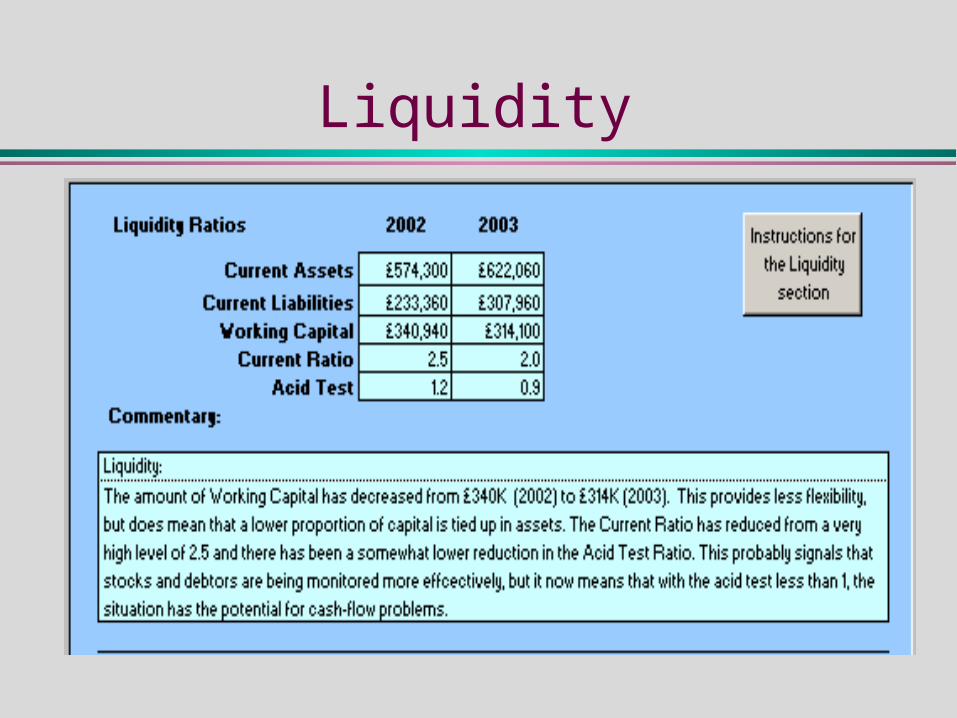

Liquidity

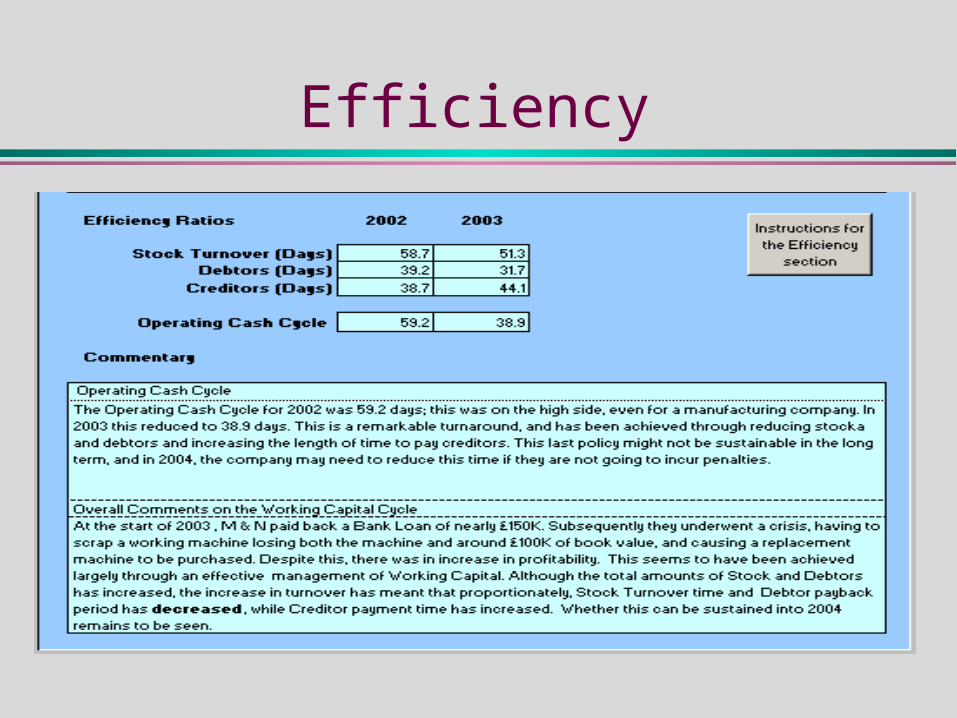

Efficiency

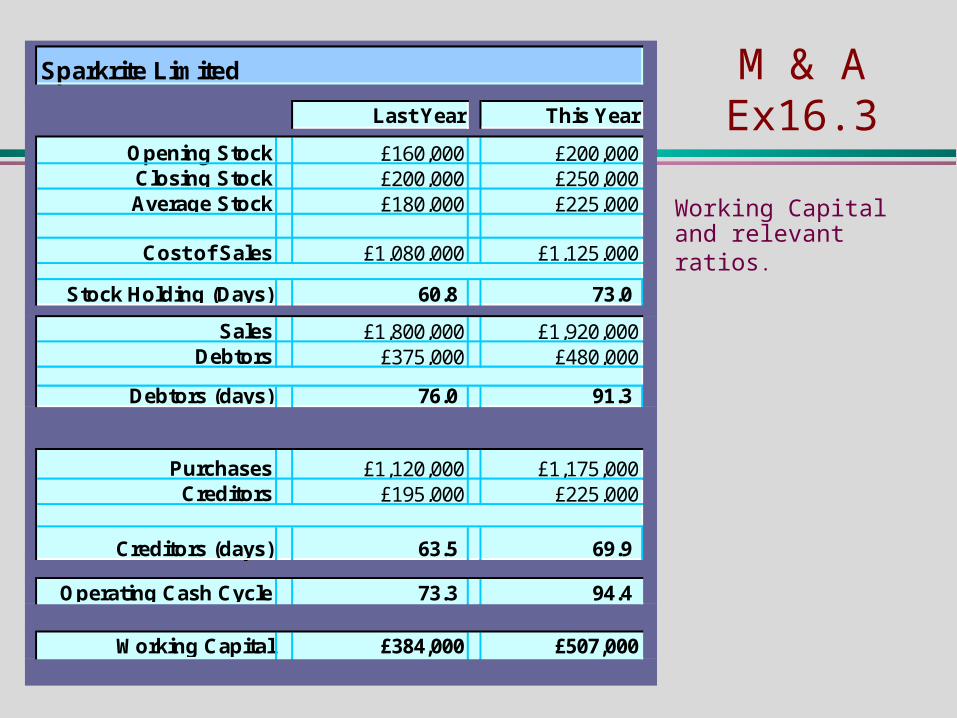

M & A Ex16.3

Working Capital and relevant ratios.

Sparkrite Limited

Last Year This Year

Opening Stock £160,000 £200,000Closing Stock £200,000 £250,000Average Stock £180,000 £225,000

Cost of Sales £1,080,000 £1,125,000

Stock Holding (Days) 60.8 73.0

Sales £1,800,000 £1,920,000Debtors £375,000 £480,000

Debtors (days) 76.0 91.3

Purchases £1,120,000 £1,175,000Creditors £195,000 £225,000

Creditors (days) 63.5 69.9

Operating Cash Cycle 73.3 94.4

Working Capital £384,000 £507,000

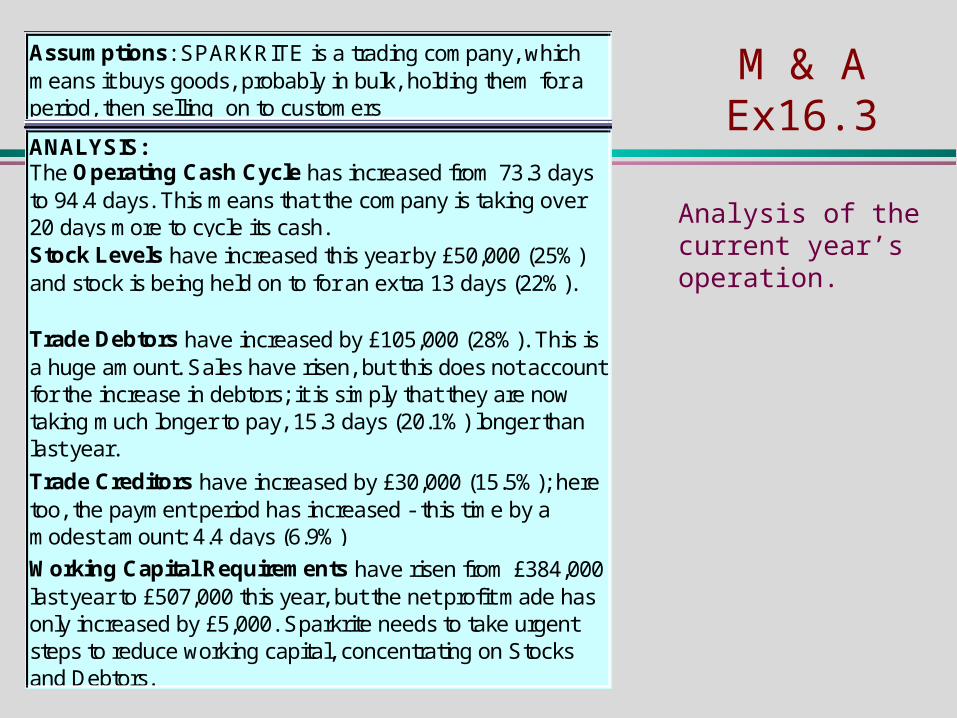

M & A Ex16.3

Analysis of the current year’s operation.

ANALYSIS:

Trade Creditors have increased by £30,000 (15.5%); here too, the payment period has increased - this time by a modest amount: 4.4 days (6.9%)

Working Capital Requirements have risen from £384,000 last year to £507,000 this year, but the net profit made has only increased by £5,000. Sparkrite needs to take urgent steps to reduce working capital, concentrating on Stocks and Debtors.

Trade Debtors have increased by £105,000 (28%). This is a huge amount. Sales have risen, but this does not account for the increase in debtors; it is simply that they are now taking much longer to pay, 15.3 days (20.1%) longer than last year.

Assumptions: SPARKRITE is a trading company, which means it buys goods, probably in bulk, holding them for a period, then selling on to customers

The Operating Cash Cycle has increased from 73.3 days to 94.4 days. This means that the company is taking over 20 days more to cycle its cash.Stock Levels have increased this year by £50,000 (25%) and stock is being held on to for an extra 13 days (22%).

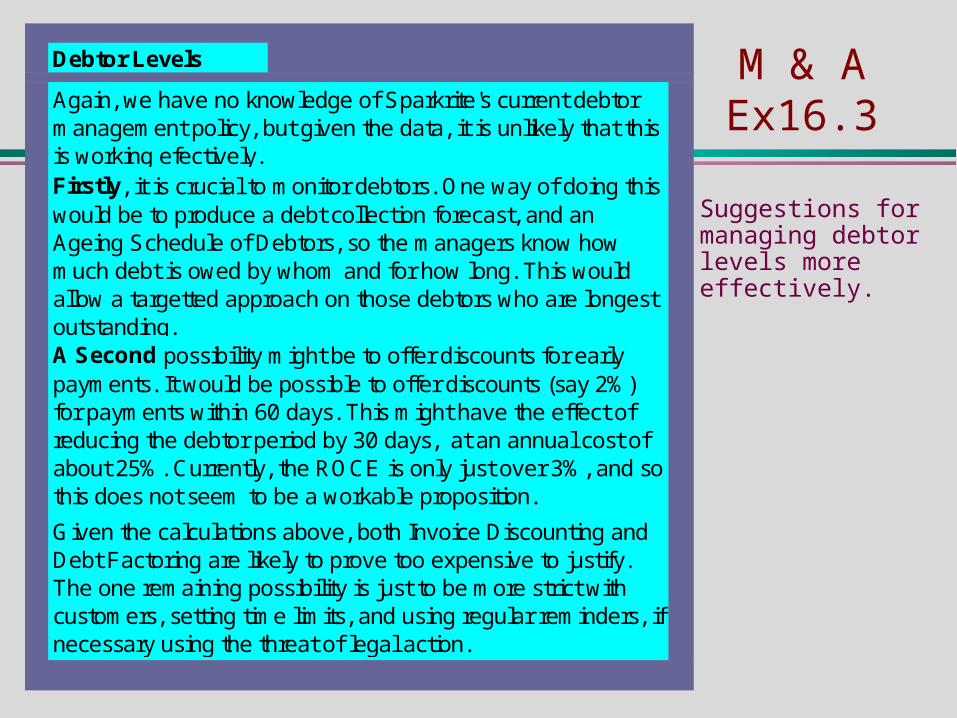

M & A Ex16.3

Suggestions for managing debtor levels more effectively.

Debtor Levels

A Second possibility might be to offer discounts for early payments. It would be possible to offer discounts (say 2%) for payments within 60 days. This might have the effect of reducing the debtor period by 30 days, at an annual cost of about 25%. Currently, the ROCE is only just over 3%, and so this does not seem to be a workable proposition.

Given the calculations above, both Invoice Discounting and Debt Factoring are likely to prove too expensive to justify. The one remaining possibility is just to be more strict with customers, setting time limits, and using regular reminders, if necessary using the threat of legal action.

Again, we have no knowledge of Sparkrite's current debtor management policy, but given the data, it is unlikely that this is working efectively.Firstly, it is crucial to monitor debtors. One way of doing this would be to produce a debt collection forecast, and an Ageing Schedule of Debtors, so the managers know how much debt is owed by whom and for how long. This would allow a targetted approach on those debtors who are longest outstanding.

M & A Ex16.3

Suggestions for managing stock levels more effectively.

Stock Levels

Sparkrite is a trading company, but we have no knowledge of its internal workings, so we are limited in what we can suggest.Firstly, it is crucial to undertake a sales analysis, to know what is being sold and when, the points at which there are demand peaks & troughs, and what those demand levels are, producing a sales forecast. As a result of this the simple solution might be to better match the goods that are being bought in with those that are being sold. Secondly, an ABC Analysis would allow Sparkrite to target specifically those goods which are the most expensive. The sales information will show whether or not this is feasible, however it is highly likely that some of these goods can be monitored and stock levels reduced, which would yield drastic reductions in total stock value.

Thirdly, using EOQ decision models, we could work out optimum levels of stock holding for each item. With this & the sales information, a suggestion would be to adopt a 'Just-in-Time' stock-delivery policy for the larger selling (by volume) items.