Understanding Disability Benefit Taxation Tax implications should be considered when designing...

23

Understanding Disability Benefit Taxation Tax implications should be considered when designing effective disability benefit plans. Who pays the premium How they pay for it A change/restructure of disability benefit plans is viewed as an ineffective, confusing process. There are several ways disability plans can be structured to improve the coverage of employees and

-

Upload

bernard-parrish -

Category

Documents

-

view

223 -

download

1

Transcript of Understanding Disability Benefit Taxation Tax implications should be considered when designing...

Understanding Disability Benefit Taxation

Tax implications should be considered when designing effective disability benefit plans.

Who pays the premium How they pay for it

A change/restructure of disability benefit plans is viewed as an ineffective, confusing process.

There are several ways disability plans can be structured to improve the coverage of employees and benefit the bottom line of the employer.

Goals

100% Employer Paid Plans Non-Contributory Gross-Up Tax Choice

Non-Contributory Plan

Employer offers the coverage to all employees.

100 percent of the premium is paid by the employer

Pre-tax dollars Disability benefits are fully

taxable as income

Non-Contributory Plan

Easy to administer Pre-tax dollars

Beneficial to the employer from a tax deduction perspective

The negative impact to the amount of benefit available to an employee at the time they need it most is severe.

Gross-Up Plan

Employer pays 100 % of the premium

Post-tax dollars Benefits are not taxable Premium assessed for

100% participation

“Gross-Up” - an amount equal to the premium is included in the employee’s W-2.

Employee pays tax on the premium, allows disability benefits to be tax-free

Gross-Up Plan

The decision to offer a Gross-Up plan is made at the employer level.

Ensuring 100 percent participation.

Employer chooses to gross-up income for entire employee population, or an entire class, but not for individuals.

If the gross-up occurs retroactively, or appears to be done so benefits are nontaxable, may be viewed as manipulation of income.

Gross-Up Plan

The additional effort to administer gross-up amounts for employees is a small price to pay for the advantages offered by a Gross-Up plan.

Particularly true for groups with high income earners

A Gross-Up plan offers a more cost efficient way to provide higher levels of income protection to higher income earners.

Gross-Up can also be done for individual policies, often referenced as Section 162 bonus plans.

Tax Choice Plan

The employer pays 100 percent of the premium.

The employee has a choice of whether that premium is paid before or after taxes.

Annual Tax Choice Election One-Time or “Evergreen”

Tax Choice Election Negative Tax Choice

Election

Annual Tax Choice Election

The employer pays the premium on a pre-tax basis.

Prior to a new plan year, each employee may make an irrevocable election to have the premium paid by the employer on a post-tax basis instead for the upcoming plan year.

If an election is not made by an employee the premium will be paid by the employer on a pre-tax basis.

One-Time or “Evergreen” Tax Choice Election

The employer pays the premium on a pre-tax basis.

Prior to the first year of the new plan, each employee makes an irrevocable election to have the premium paid by the employer on a post-tax basis instead.

The employee’s election will continue for each subsequent plan year unless formally changed by the employee before the beginning of a new plan year.

Negative Tax Choice Election

The employer pays the premium on a pre-tax basis, unless an employee formally elects to have premium paid on a pre-tax basis prior to the beginning of a new plan year.

Premium payment on a post-tax basis is automatic, unless changed by the employee.

Tax Choice Plan

For post-tax treatment, an amount equal to the premium for disability insurance is included in the W-2.

May or may not include an amount to cover the income, FICA and Medicare taxes

The result is that tax is paid on the “premium” for the disability insurance, allowing any disability benefits to be tax-free.

The choice in tax treatment applies to the entire cost of the insurance.

Tax Choice Plan

Carrier/Broker Annual Tax Choice ensures

benefits communication and enrollment opportunity exists at least once a year.

Employer The Negative Tax Choice

Election is easiest to administer

The tax choice election made for the plan year in which disability manifests determines how benefit payments will be taxed.

Goals

Contributory Plan

Core/Buy-Up Plan

Voluntary Plans

Tax Implication Impact Benefit Replacement Ratio

Contributory Plan

The employer and employee share in the cost of the insurance.

Employer determines the portion of the premium they will be accountable for

Employees have the option to enroll for the coverage and pay the balance of the premium

Typically require 75 percent participation or greater in return for more favorable group rates.

Contributory Plan

The Internal Revenue Code outlines the rules for taxing benefits under a Contributory plan.

“Three-year look back rule”

An alternative for employers who want to pay the premium for disability insurance for employees but are unable to pay the full premium.

Core/Buy-Up Plan

Two plans in one. Core Plan

Employer pays to insure a portion of employee income

Buy-Up Plan Employees have the option

to purchase additional coverage

Tax implications under the Core plan depend on the structure of the Core plan.

Benefits under the Buy-Up plan are tax-free.

Core/Buy-Up Plan

Ideal for employers who want to pay for disability insurance for employees, but are prohibited from paying the full cost.

Structuring the Core plan to provide a tax-free benefit or give employees the option of a tax-free benefit, maximizes employer benefit dollars.

Availability of a Buy-Up option allows employees to secure additional, valuable income protection at affordable group rates.

Voluntary Plan

For employers who want to offer disability insurance as part of a competitive benefits package, but don’t have the dollars available.

The employee pays 100% of the premium

Payroll deduction or alternative electronic payment method

Disability benefits are tax-free because the premium is paid by the employee with post-tax dollars.

Typically require a minimum percentage of employees to participate in exchange for group rates and benefits.

Voluntary Plan

Many employers offer benefits through a POP.

Employees pay the premiums with pre-tax dollars

Taxable income is lowered

Pre-taxing the premium for disability insurance results in benefits that are fully taxable. The savings on the front end is minimal compared to the major reduction in benefits due to taxes at the time of disability.

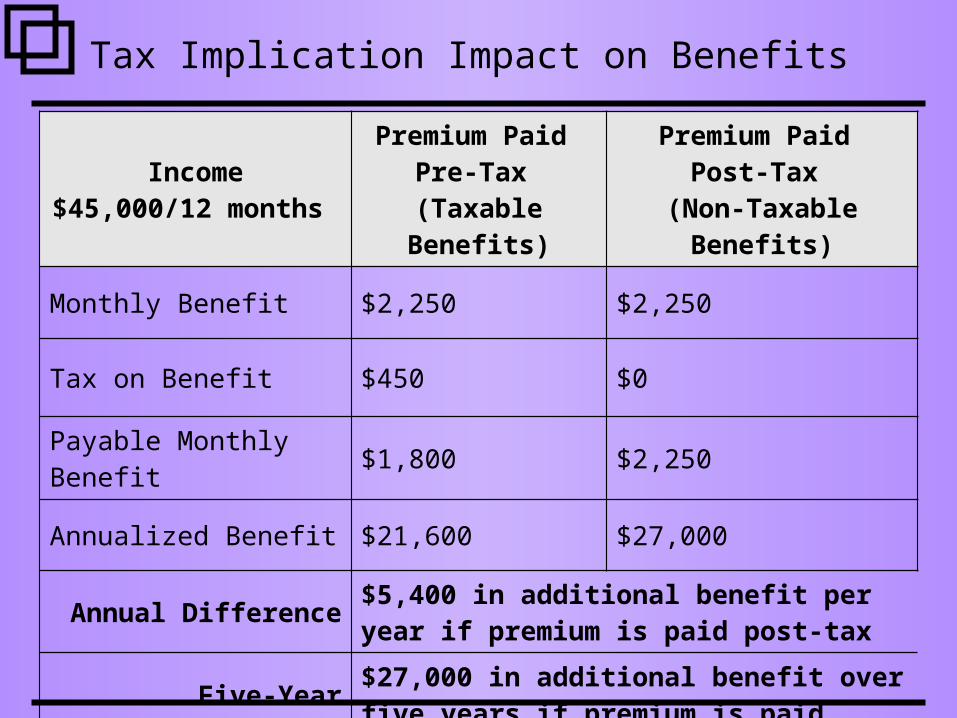

Tax Implication Impact on Benefits

Income$45,000/12 months

Premium Paid Pre-Tax

(Taxable Benefits)

Premium Paid Post-Tax

(Non-Taxable Benefits)

Monthly Benefit $2,250 $2,250

Tax on Benefit $450 $0

Payable Monthly Benefit $1,800 $2,250

Annualized Benefit $21,600 $27,000

Annual Difference $5,400 in additional benefit per year if premium is paid post-tax

Five-Year Difference $27,000 in additional benefit over five years if premium is paid post-tax

Tax Implication Impact on the Replacement Ratio

Income$45,000/12 months

60% BenefitPre-Tax

60% Benefit

Post-Tax

70% BenefitPre-Tax

70% Benefit

Post-Tax

A: Gross Monthly Income $3,750 $3,750 $3,750 $3,750

B: Take Home Pay $3,000 $3,000 $3,000 $3,000

C: Gross Monthly Benefit $2,250 $2,250 $2,625 $2,625

D: Tax on Benefit $450 $0 $525 $0

E: Payable Monthly Benefit $1,800 $2,250 $2,100 $2,625

F: Replacement Ratio (E/B) 60% 75% 70% 87.5%

Summary

100% Employer Paid plans Non-Contributory Gross-Up Tax Choice

Contributory Plan

Core/Buy-Up Plan

Voluntary Plans

Tax Implication Impact Benefit Replacement Ratio