Under the Income Tax Act

18

Under the Income Tax Act, 'Profits and Gains of Business or Profession ' are also subjected to taxation. The term "business" includes any (a) trade, (b)commerce, (c)manufacture, or (d) any adventure or concern in the nature of trade, commerce or manufacture. The term "profession" implies professed attainments in special knowledge as distinguished from mere skill; "special knowledge" which is "to be acquired only after patient study and application". The words 'profits and gains' are defined as the surplus by which the receipts from the business or profession exceed the expenditure necessary for the purpose of earning those receipts. These words should be understood to include losses also, so that in one sense 'profit and gains' represent plus income while 'losses' represent minus income. The following types of income are chargeable to tax under the heads profits and gains of business or profession:- Profits and gains of any business or profession Any compensation or other payments due to or received by any person specified in section 28 of the Act Income derived by a trade, profession or similar association from specific services performed for its members Profit on sale of import entitlement licences, incentives by way of cash compensatory support and drawback of duty The value of any benefit or perquisite, whether converted into money or not, arising from business Any interest, salary, bonus, commission, or remuneration received by a partner of a firm, from such a firm Any sum whether received or receivable in cash or kind, under an agreement for not carrying out any activity in relation to any business or not to share any know-how, patent, copyright, franchise, or any other business or commercial right of similar nature or technique likely to assist in the manufacture or processing of good Any sum received under a keyman insurance policy Income from speculative transactions. In the following cases, income from trading or business is not taxable under the head "profits and gains of business or profession":- Rent of house property is taxable under the head " Income from house property". Even if the property constitutes stock in trade of recipient of rent or the recipient of rent is engaged in the

-

Upload

mandira-kollali -

Category

Documents

-

view

217 -

download

0

Transcript of Under the Income Tax Act

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 1/17

Under the Income Tax Act, 'Profits and Gains of Business or Profession' are also subjected totaxation. The term "business" includes any (a) trade, (b)commerce, (c)manufacture, or (d) anyadventure or concern in the nature of trade, commerce or manufacture. The term "profession" impliesprofessed attainments in special knowledge as distinguished from mere skill; "special knowledge" whichis "to be acquired only after patient study and application". The words 'profits and gains' are defined asthe surplus by which the receipts from the business or profession exceed the expenditure necessary for

the purpose of earning those receipts. These words should be understood to include losses also, so thatin one sense 'profit and gains' represent plus income while 'losses' represent minus income.

The following types of income are chargeable to tax under the heads profits and gains of business orprofession:-

Profits and gains of any business or profession

Any compensation or other payments due to or received by any person specified in section 28 of the Act

Income derived by a trade, profession or similar association from specific services performed forits members

Profit on sale of import entitlement licences, incentives by way of cash compensatory supportand drawback of duty

The value of any benefit or perquisite, whether converted into money or not, arising from

business

Any interest, salary, bonus, commission, or remuneration received by a partner of a firm, fromsuch a firm

Any sum whether received or receivable in cash or kind, under an agreement for not carryingout any activity in relation to any business or not to share any know-how, patent, copyright,franchise, or any other business or commercial right of similar nature or technique likely to

assist in the manufacture or processing of good

Any sum received under a keyman insurance policy

Income from speculative transactions.

In the following cases, income from trading or business is not taxable under the head "profits and gainsof business or profession":-

Rent of house property is taxable under the head " Income from house property". Even if theproperty constitutes stock in trade of recipient of rent or the recipient of rent is engaged in the

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 2/17

business of letting properties on rent.

Deemed dividends on shares are taxable under the head "Income from other sources".

Winnings from lotteries, races etc. are taxable under the head "Income from other sources".

Profits and gains of any other business are taxable, unless such profits are subjected to exemption.

General principals governing the computation of taxable income under the head "profits and gains of business or profession:-

Business or profession should be carried on by the assessee. It is not the ownership of businesswhich is important , but it is the person carrying on a business or profession, who is chargeableto tax.

Income from business or profession is chargeable to tax under this head only if the business orprofession is carried on by the assessee at any time during the previous year. This income istaxable during the following assessment year.

Profits and gains of different business or profession carried on by the assessee are notseparately chargeable to tax i.e. tax incidence arises on aggregate income from all businessesor professions carried on by the assessee. But, profits and loss of a speculative business arekept separately.

It is not only the legal ownership but also the beneficial ownership that has to be considered.

Profits made by an assessee in winding up of a business or profession are not taxable, as nobusiness is carried on in that case. However, such profits may be taxable as capital gains or asbusiness income, if the process of winding up is such as to involve the carrying on of a trade.

Taxable profit is the profit accrued or arising in the accounting year. Anticipated or potentialprofits or losses, which may occur in future, are not considered for arriving at taxable income.Also, the profits, which are taxable, are the real profits and not notional profits. Real profitsfrom the commercial point of view, mean a gain to the person carrying on the business and notprofits from narrow, technical or legalistic point of view.

The yield of income by a commercial asset is the profit of the business irrespective of themanner in which that asset is exploited by the owner of the business.

Any sum recovered by the assessee during the previous year, in respect of an amount orexpenditure which was earlier allowed as deduction, is taxable as business income of the year in

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 3/17

which it is recovered.

Modes of book entries are generally not determinative of the question whether the assessee hasearned any profit or loss.

The Income tax act is not concerned with the legality or illegality of business or profession.Hence, income of illegal business or profession is not exempt from tax.

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 4/17

1. What is ‘Business’? (Back to top)

The term "business" includes:

a. trade,b. commerce,c. manufacture, or d. any adventure or concern in the nature of trade, commerce or manufacture.

2. What is ‘Profession’? (Back to top)

The term "profession" implies professed attainments in special knowledge as distinguished

from mere skill; "special knowledge" which is "to be acquired only after patient study andapplication". Profession basically refers to the exploitation or utilization of one’s skills andknowledge independently. Profession includes vocation. Some examples are legal, medical,engineering, architecture, accountancy, technical consultancy, interior decoration, artists,writers, and so on.

3. What are the ‘profits and gains’? (Back to top)

The words 'profits and gains' are defined as the surplus by which the receipt from thebusiness or profession exceeds the expenditure necessary for the purpose of earning those

receipts.

4. What are the general principles governing the computation of taxable income under the head "profits and gains of business or profession?

(Back to top)

There are certain basic rules that apply when you are assessing your taxable income fromeither of these 2 heads, these are as follows:

Business or profession should be carried on by you i.e. the assessee. It is not the

ownership of business which is important, but it is the person carrying on a business or profession, who is chargeable to tax. For example, you may be drawing a salary from thebusiness, even if you are not the owner of the business. This would count as incomefrom business, and would become taxable.

Income from business or profession is chargeable to tax under this head only if thebusiness or profession is carried on by the assessee at any time during the previousyear. This income is taxable during the following assessment year.

Profits and gains of different business or profession carried on by the assessee are notseparately chargeable to tax i.e. tax incidence arises on aggregate income from all

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 5/17

businesses or professions carried on by the assessee. But, profits and loss of aspeculative business are kept separately.

It is not only the legal ownership but also the beneficial ownership that has to beconsidered.

Profits made by an assessee in winding up of a business or profession are not taxable,as no business is carried on in that case. However, such profits may be taxable ascapital gains or as business income, if the process of winding up is such as to involve thecarrying on of a trade.

Taxable profit is the profit accrued or arising in the accounting year. Anticipated or potential profits or losses, which may occur in future, are not considered for arriving attaxable income. Also, the profits, which are taxable, are the real profits and not notionalprofits. Real profits from the commercial point of view mean a gain to the person carryingon the business and not profits from narrow, technical or legalistic point of view.

The yield of income by a commercial asset is the profit of the business irrespective of themanner in which that asset is exploited by the owner of the business.

The Income tax act is not concerned with the legality or illegality of business or profession. Hence, income of illegal business or profession is not exempt from tax.

5. What books of account have been prescribed to be maintained by a person carrying onbusiness under the Income tax Act?(Back to top)

The Act does not prescribe any specific books of account for business. However you areexpected to maintain your accounts in such a fashion that the net profit of the business canreasonably and easily be arrived at. For companies the books of account are prescribed

under the Companies Act.

6. Are professionals required to maintain any books of account under the Income taxAct?(Back to top)

Yes. The following books and documents are to be maintained mandatory:

0. Cash book1. Journal in case of mercantile system of accounting

2. Ledger 3. Carbon copies or counter foils of all bills issued, being serially numbered4. Original copies of all expenditure bills.

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 6/17

7. I am a small time trader. Do I need to maintain any accounts?(Back to top)

Any business or profession that has an annual turnover/gross receipts exceeding rupees ten

lakh and net profit of rupees one lakh twenty thousand, must maintain such books of account and documents from which its income can be reasonably ascertained by the incometax department.

8. Where should the books of account of my business be kept and for how long? (Back to top)

All the books of account and related documents should be kept at the main place of business i.e. where the business or profession is generally carried on. These should bepreserved for a minimum of six years.

9. Do I have to keep an accountant to maintain my account? (Back to top)

This depends upon your ability and need. You may even prefer to use the accountingsoftware available in the market. However, you should remember that in case of turnover exceeding Rs. 60 lakh per annum in a business and gross receipts exceeding Rs. 15 lakhper annum in a profession, a professional charted accountant must audit your accounts.

10. What is meant by audit of the books of account?(Back to top)

Auditing means checking the correctness and genuineness of your accounts and verifyingwhether accounting principles and standards have been properly followed in conduct of your business and preparation of accounts. Under Income Tax Act, this verification will have to becarried out by an independent Chartered Accountant.

11. In my business it is impossible to issue bills for every transaction. How can I beexpected to maintain proper accounts?

(Back to top)

There can be no excuse for not maintaining the bill books. However, if you are a smalltimeretail trader with your annual turnover of less than Rs. 60 lakh, then you are permitted todeclare your income on presumption at 8% of your actual sales. In that event no books of account need be maintained.

12. I am a medical practitioner. Do I need to maintain any accounts?(Back to top)

Yes. All the books and document prescribed for professional need to be maintained. Additionally, a daily case register in prescribed form no.3C and an inventory of drugs,consumables and other stocks also need to be maintained.

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 7/17

13. How do I take full advantage of all my business related expenses? (Back to top)

All your work/business related expenses can be claimed as business expenses.

Vouchers/bills would be required to support expenses and hence book keeping is importantfor this category. A variety of expenses including rent or home office expense, travel costs,communication costs (telephone, internet), business meetings, supplies and utilities can beclaimed as expenses. For being deductible, expenses must be both ordinary (common andaccepted) and necessary (appropriate and helpful) in your work/business. If such expensesare incurred partly for work purposes and partly for personal purposes, you can deduct onlythe work related portion. One can also claim depreciation on work related assets likelaptops/computers, furniture, UPS and vehicles. Hence bills of capital expenditures shouldalso be maintained.

14. Can I save tax by distributing my business income? (Back to top)

If you have family members who can help in various aspects of your business, it makessense to employ them (legitimately) and offer an appropriate remuneration. By hiring afamily member to work, you will effectively shift a part of your income to your relative.

Accordingly, your business can take a deduction for reasonable compensation paid to anemployee (relative), which in turn reduces the amount of taxable business income that flowsthrough to you.

One can also form a Hindu Undivided Family (HUF) as a separate entity, which helps further distribute income to this entity as well.

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 8/17

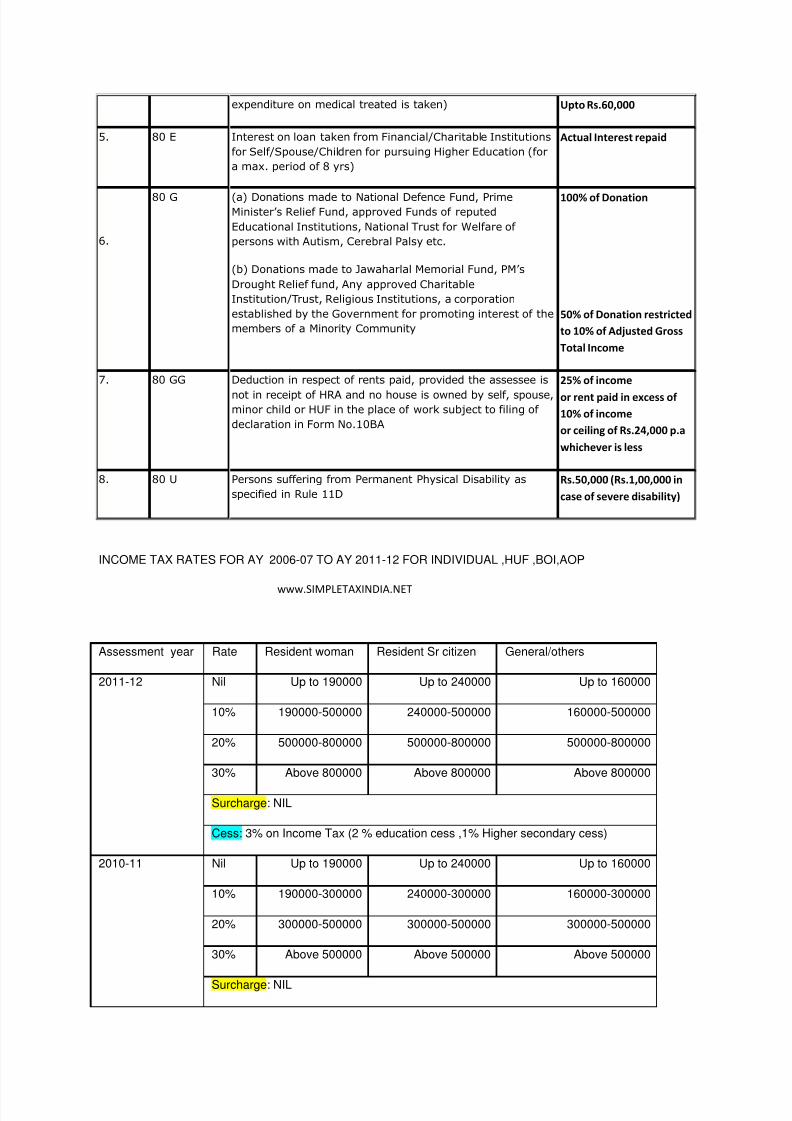

DEDUCTIONS FROM GROSS TOTAL INCOME (CHAPTER VIA):

Sl.No. I.T. Sec. Nature of Deduction Amount of deduction

1.

a.

b.

c.

80 CCE

80 C

80 CCC

80 CCD

Limit on Deduction u/s.80C, 80CCC & 80CCD

Life Insurance Premia, PF, PPF, NSC, ELSS, Units of Mutual

Fund referred to u/s.10(23D), Tuition Fees(max. 2 Children),Repayment of Principal of Housing loan, Bank Fixed Deposit

of 5 yrs period, notified Bonds of NABARD, Deposit in an

account under Senior Citizens Savings Scheme rules, 5 year

time deposit in an account under Post Office Time Deposit

Rules, 1981 etc.

Premium paid towards approved Pension Fund (like LIC’s

Jeevan Suraksha) max. 1 lakh.

Contribution to Central Government Pension Schemes. Upto

10% of salary with matching contribution from

Government.

Maximum overall

Deductions

allowed u/s. 80C,

80CCC & 80CCD

is Rs. 1,00,000

(Employer contribution

is deductible without any

limit from fy 2011-12)

2. 80 CCF Amount paid/deposited as subscription to long-term

infrastructure bonds being notified by the Central

Government.

Rs. 20,000

3. 80 D (a) Medical Insurance Premium paid by an individual/HUF by

any mode of payment other than cash to effect or keep in

force an insurance on the health of the assessee(self) or his

family(spouse & dependent children) for policies taken from

General Insurance Corporation /other approved Insurance

Regulatory and Development Authority or any contribution

made to the Central Government Health Scheme.

(b) Medical Insurance Premium paid by an individual/HUF by

any mode of payment other than cash to effect or keep inforce an insurance on the health of his/her parent or parents

for policies taken from General Insurance Corporation /other

approved Insurance Regulatory and Development Authority

or any contribution made to the Central Government Health

Scheme.

(c) For Senior Citizens

Upto Rs.15,000

Upto Rs.15,000

Upto Rs.20,000

3. 80 DD (a) Any expenditure for Medical, Nursing & Rehabilitation

incurred on dependant suffering from permanent disability

including blindness, mental retardation, autism, cerebral

palsy or multiple disabilities

(b) Deposits under LIC, UTI’s Scheme & other IRDA

approved insurers for the benefit of physically handicapped

dependent

Rs.50,000 (Rs.1,00,000 if

the disability is severe

exceeding 80%)

4. 80 DDB (a) Actual expenditure incurred on Medical treatment of Self

or dependant or a member of HUF suffering from terminal

diseases like Cancer, AIDS, Renal failure etc.

(b) For Senior Citizens(self or dependent on whom

Upto Rs.40,000

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 9/17

expenditure on medical treated is taken) Upto Rs.60,000

5. 80 E Interest on loan taken from Financial/Charitable Institutions

for Self/Spouse/Children for pursuing Higher Education (for

a max. period of 8 yrs)

Actual Interest repaid

6.

80 G (a) Donations made to National Defence Fund, PrimeMinister’s Relief Fund, approved Funds of reputed

Educational Institutions, National Trust for Welfare of

persons with Autism, Cerebral Palsy etc.

(b) Donations made to Jawaharlal Memorial Fund, PM’s

Drought Relief fund, Any approved Charitable

Institution/Trust, Religious Institutions, a corporation

established by the Government for promoting interest of the

members of a Minority Community

100% of Donation

50% of Donation restricted

to 10% of Adjusted Gross

Total Income

7. 80 GG Deduction in respect of rents paid, provided the assessee is

not in receipt of HRA and no house is owned by self, spouse,minor child or HUF in the place of work subject to filing of

declaration in Form No.10BA

25% of income

or rent paid in excess of

10% of income

or ceiling of Rs.24,000 p.a

whichever is less

8. 80 U Persons suffering from Permanent Physical Disability as

specified in Rule 11D Rs.50,000 (Rs.1,00,000 in

case of severe disability)

INCOME TAX RATES FOR AY 2006-07 TO AY 2011-12 FOR INDIVIDUAL ,HUF ,BOI,AOP

www.SIMPLETAXINDIA.NET

Assessment year Rate Resident woman Resident Sr citizen General/others

2011-12 Nil Up to 190000 Up to 240000 Up to 160000

10% 190000-500000 240000-500000 160000-500000

20% 500000-800000 500000-800000 500000-800000

30% Above 800000 Above 800000 Above 800000

Surcharge: NIL

Cess: 3% on Income Tax (2 % education cess ,1% Higher secondary cess)

2010-11 Nil Up to 190000 Up to 240000 Up to 160000

10% 190000-300000 240000-300000 160000-300000

20% 300000-500000 300000-500000 300000-500000

30% Above 500000 Above 500000 Above 500000

Surcharge: NIL

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 10/17

Cess: 3% on Income Tax (2 % education cess ,1% Higher secondary cess)

2009-10 Nil Up to 180000 Up to 225000 Up to 150000

10% 180000-300000 225000-300000 150000-300000

20% 300000-500000 300000-500000 300000-500000

30% Above 500000 Above 500000 Above 500000

Surcharge: 10 % on Income Tax if income Exceeding Rs 10,00,000

Cess: 3% on Income Tax & surcharge (2 % education cess ,1% Higher secondary

cess)

2008-09 Nil Up to 145000 Up to 195000 Up to 110000

10% 145000-300000 195000-300000 110000-300000

20% 300000-500000 300000-500000 300000-500000

30% Above 500000 Above 500000 Above 500000

Surcharge: 10 % on Income Tax if income Exceeding Rs 10,00,000

Cess: 3% on Income Tax & surcharge (2 % education cess ,1% Higher secondary

cess)

2006-07 and

2007-08

Nil Up to 135000 Up to 185000 Up to 100000

10% 135000-300000 185000-300000 100000-300000

20% 300000-500000 300000-500000 300000-500000

30% Above 500000 Above 500000 Above 500000

Surcharge: 10 % on Income Tax if income Exceeding Rs 10,00,000

Cess: 2% on Income Tax & surcharge (2 % education cess )

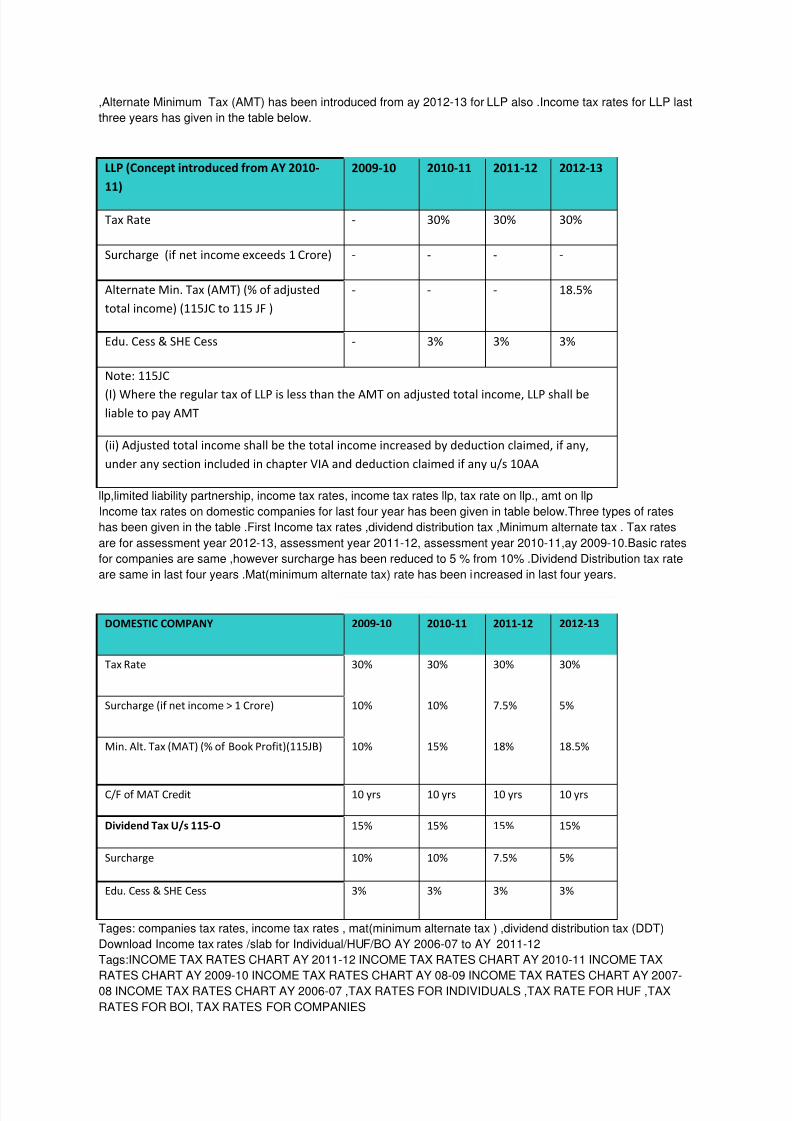

Income Tax rates applicable on partnership firm is listed below. Basic rates were unchanged in last four yearshowever effective rates were reduced after removal of surcharge from firm tax . Hope you may find this useful.

www.SIMPLETAXINDIA.NET Assessment year

FIRM 2009-10 2010-11 2011-12 2012-13

Tax Rate 30% 30% 30% 30%

Surcharg e (if net income exceeds 1 Crore) 10% - - -

Edu. Cess & SHE Cess 3% 3% 3% 3%

Income tax rates of LLP(limited partnership Firm ) is listed out for assessment year 2012-13 , 2011-12 and 2010-

11.The basic rates has no change in last three year . However from assessment year 2012-13

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 11/17

,Alternate Minimum Tax (AMT) has been introduced from ay 2012-13 for LLP also .Income tax rates for LLP last

three years has given in the table below.

LLP (Concept introduced from AY 2010-

11)

2009-10 2010-11 2011-12 2012-13

Tax Rate - 30% 30% 30%

Surcharge (if net income exceeds 1 Crore) - - - -

Alternate Min. Tax (AMT) (% of adjusted

total income) (115JC to 115 JF )

- - - 18.5%

Edu. Cess & SHE Cess - 3% 3% 3%

Note: 115JC

(I) Where the regular tax of LLP is less than the AMT on adjusted total income, LLP shall be

liable to pay AMT

(ii) Adjusted total income shall be the total income increased by deduction claimed, if any,

under any section included in chapter VIA and deduction claimed if any u/s 10AA

llp,limited liability partnership, income tax rates, income tax rates llp, tax rate on llp., amt on llp

Income tax rates on domestic companies for last four year has been given in table below.Three types of rates

has been given in the table .First Income tax rates ,dividend distribution tax ,Minimum alternate tax . Tax rates

are for assessment year 2012-13, assessment year 2011-12, assessment year 2010-11,ay 2009-10.Basic rates

for companies are same ,however surcharge has been reduced to 5 % from 10% .Dividend Distribution tax rate

are same in last four years .Mat(minimum alternate tax) rate has been increased in last four years.

DOMESTIC COMPANY 2009-10 2010-11 2011-12 2012-13

Tax Rate 30% 30% 30% 30%

Surcharge (if net income > 1 Crore) 10% 10% 7.5% 5%

Min. Alt. Tax (MAT) (% of Book Profit)(115JB) 10% 15% 18% 18.5%

C/F of MAT Credit 10 yrs 10 yrs 10 yrs 10 yrs

Dividend Tax U/s 115-O 15% 15% 15% 15%

Surcharge 10% 10% 7.5% 5%

Edu. Cess & SHE Cess 3% 3% 3% 3%

Tages: companies tax rates, income tax rates , mat(minimum alternate tax ) ,dividend distribution tax (DDT)

Download Income tax rates /slab for Individual/HUF/BO AY 2006-07 to AY 2011-12

Tags:INCOME TAX RATES CHART AY 2011-12 INCOME TAX RATES CHART AY 2010-11 INCOME TAX

RATES CHART AY 2009-10 INCOME TAX RATES CHART AY 08-09 INCOME TAX RATES CHART AY 2007-

08 INCOME TAX RATES CHART AY 2006-07 ,TAX RATES FOR INDIVIDUALS ,TAX RATE FOR HUF ,TAX

RATES FOR BOI, TAX RATES FOR COMPANIES

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 12/17

Read more: http://www.simpletaxindia.net/2011/11/income-tax-rate-chart-slab-fy-11-12-ay.html#ixzz1nGIoZ3tC

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 13/17

INCOME FROM

OF BUSINE

PROFESS

Business : -

Business includes

trade, comme

manufacture or an

or concern in the

nature of trade, c

manufacture. Itnecessary that the

a series of trans

business

and that it should

on permanently

repetition nor c

similar transa

necessary. Profit o

an isolated transa

taxable under

provided that it is

the nature or

trade. IN

this connection

important that the

purchase or

should be to sell a

Profession -

means the ac

earning livelihood

intellectual skill

skill, e.g. the work

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 14/17

of a lawyer, doc

engineer and

Profession include

Vocation means

which are perform

in order to earn li

brokerage, insuran

music etc.

Taxable income

head of

profession

Profits and g

business and

include following

* The profits and

business or profe

was carried o

assessee at any

the precious year.

* Any interest, s

commission or r

due to or rece

partner of a firm p

it has been allowe

as deduction in co

taxable profits of s

* Income from

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 15/17

transactions (But

betting business

kept separate fr

income )

* If the business

is to invest in se

profit or loss incu

sale/ purchase of

be calculate

under this he

debentures will

under this head )

Member (Accoun

[ Scorecard :

Posted 2 years ago

* Apart f rom the above, income of trade unions key man insurance policy

amount, specific receipts related to import-export, agency commission etc.

Important facts relating to business or profession

* Tax is chargeable from the person who carries out on the business or

profession . The essential requirement is that he should be entitled to carry out

the business. It is immaterial if the Assessee (owner of the business ) carries

on the business through a manager/

servant /agent etc (sec. 28)

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 16/17

* Whether the business is legal or illegal , the profits will be calculated under

this head only (profits due to betting, smuggling etc. )

* Losses are also considered in the head of business or profession and are

adjusted against income from other sources. If it cannot be adjusted then it

can be forwarded to adjust income of coming years.

* Estimated or imaginary profits are not taxable .

Expressly Disallowed Deduction

Out of the various expenses occurring on business or profession the

some expenses are not allowed for deduction form income from the head of

business or profession, few are as under

Payment of direct taxes - Payment of income tax /wealth tax and related

penalty or interest.

Capital Expenditures - For fixed assets such as land , building , car

etc.

Penalty - Any type of penalty relating to direct-indirect

tax, legal-illegal

business

Capital losses - Losses incurred due to sale of capital assets.

7/28/2019 Under the Income Tax Act

http://slidepdf.com/reader/full/under-the-income-tax-act 17/17

Inpidual expenses - Assessee`s inpidual expenses such as domestic

expenses, life insurance premium etc.

Member (Accoun

[ Scorecard :

Posted 2 years ago

insurance premium etc.

Payment to relatives - If the assessee is paying any unreasonable

amount to his relative or sister

in concern with the business or profession then such amount is not allowed for

deduction

Interest on personal capital It the owner of the business debits any interests

from his account (on personal capital or loan )

then such interest is not allowed for deduction

Cash payments U/S 40A (3) if payment of any expenditure (incurred

after 1st April 07)

of more than Rs. 20000/- is made in cash (but

not through a/c payee

cheque or DD etc ) then such expenditure shall

be fully (i.e.100%) disallowed

(Excluding particular situations mentioned in

rule 6DD