UMS HOLDINGS LTD - listed companyumsgroup.listedcompany.com/misc/UMS_CIMB_present… · ·...

27

Corporate Presentation @ CIMB Date: 28 September 2010 UMS HOLDINGS LTD

Transcript of UMS HOLDINGS LTD - listed companyumsgroup.listedcompany.com/misc/UMS_CIMB_present… · ·...

Corporate Presentation @ CIMBDate: 28 September 2010

UMS HOLDINGS LTD

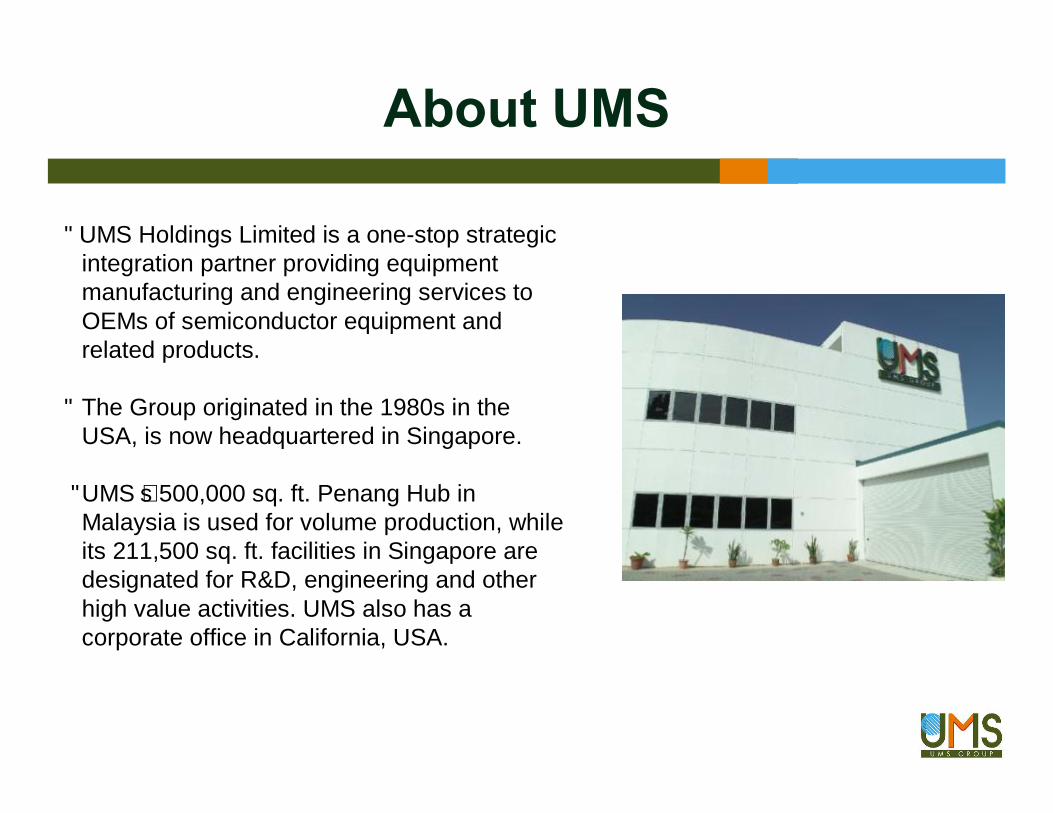

About UMS Holdings Ltd

• UMS Holdings Limited is a one-stop strategic integration partner providing equipment manufacturing and engineering services to OEMs of semiconductor equipment and related products.

• The Group originated in the 1980s in the USA, is now headquartered in Singapore.

• UMS’s 500,000 sq. ft. Penang Hub in Malaysia is used for volume production, while its 211,500 sq. ft. facilities in Singapore are designated for R&D, engineering and other high value activities. UMS also has a corporate office in California, USA.

About UMS

Our Facilities

Factory in Penang (500,000 square feet)

Headquarters in Singapore(211,500 square feet)

Vision and Mission

• Our Vision is to be a strategic global partner for successful global companies, with a full range of integrated manufacturing services.

• Our Mission is to deliver the best in-class manufacturing solutions to step up our customers’manufacturing processes and produce quality products. The company aims to continuously improve on profitability.

Our Core Business Activities

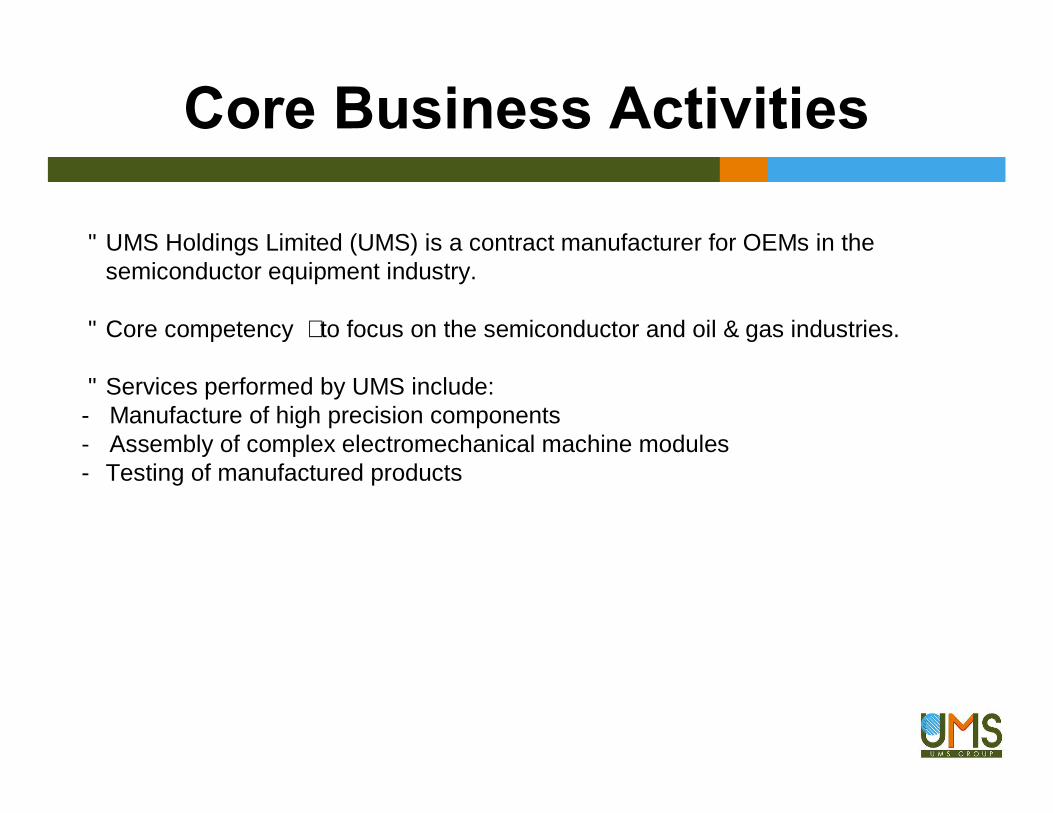

Core Business Activities

• UMS Holdings Limited (UMS) is a contract manufacturer for OEMs in the semiconductor equipment industry.

• Core competency – to focus on the semiconductor and oil & gas industries.

• Services performed by UMS include: - Manufacture of high precision components - Assembly of complex electromechanical machine modules - Testing of manufactured products

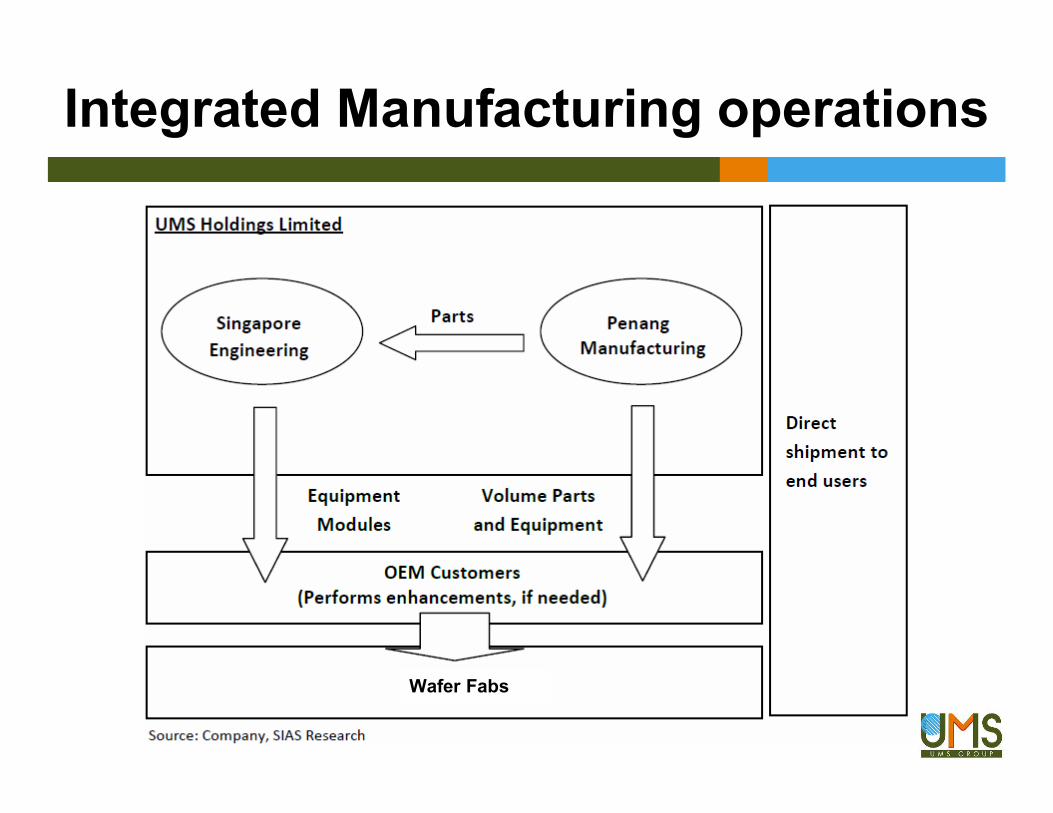

Integrated Manufacturing operations

Wafer Fabs

Our Fundamental Drivers

1: Ready For Growth

• Ready Capacity

- Our Penang Hub and Singapore headquarters provide more than 700,000 sq. ft. of space to expand production.

- As of 2Q FY10, our capacity utilization rate is 65%, up from 20% in 3Q FY09.

- Target to ramp up production by at least 20% over 2H FY10, any remaining unutilized capacity will support top-line expansion over FY11 and FY12

2. Ability to capture greater market share3. Entrenched position in semicon

• Ability to capture a greater share of the semiconductor market

- We are also well placed to capture more outsourcing business, as we can respond quickly to service requests from the more than 30 semiconductor manufacturing facilities in Singapore, which produces 11% of global output.

• Entrenched position

- Our edge is in the semiconductor equipment industry, where we have a ready set of strategic customers and qualifications to perform more than 70 special processes for the semiconductor industry.

- Entrants to the industry will first have to win customer qualifications for individual processes and are hence, less responsive to customers’ production needs.

• Our key customer reported:

- “Backlog increased to $3 billion, reflecting a healthy order book across all of segments.”

- 19 May 2010

• Close proximity to key customer- Upon the entry of its key customer into Singapore, UMS has seen local sales

grow by more than five times on Q-o-Q basis in 1Q10 to $13m. While in 2Q10, sales in Singapore grew by 47.4% Q-o-Q, as its key customer ramped up production in Singapore.

- Key customer intends to channel more than 50% or $1.4b, of shipments through this centre in the next few years. Meanwhile, it also plans to relocate 75% of work outsourced to contract manufacturers to lower cost regions by 2011.

- Shares investment, 13 Aug 2010

4: Beneficiary of Key Customer’s strong growth momentum

5: More Integration More effective Supply Chain Management

• Greater integration to shorten supply chain and improve margins

- By integrating and testing systems as a one-stop shop, UMS shortens customers’ supply chains and provides them with cost efficiencies and faster time-to-end market. This increases customer-supplier reliance just as customers are streamlining their supplier base and also extending outsourcing activities.

• Cost Competitiveness, being located in Penang, Malaysia

- Since 2009, we have also improved cost efficiencies by shifting part of our production to the Penang Hub, which enjoys a 10 year tax holiday, better labour, utilities and land costs. This strengthens the company’s competitive edge in the industry.

• Recurring Business from Spares

- Estimate of spares business to be about 15 - 20% of total revenue.

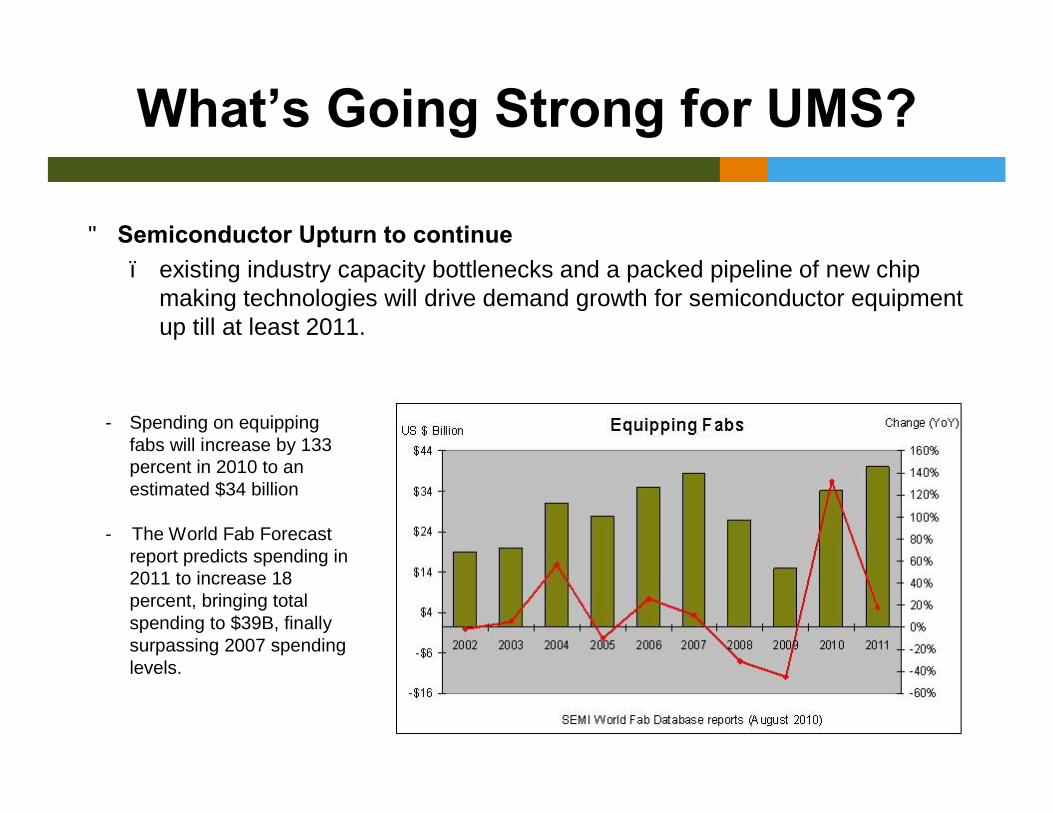

• Semiconductor Upturn to continue– existing industry capacity bottlenecks and a packed pipeline of new chip

making technologies will drive demand growth for semiconductor equipment up till at least 2011.

What’s Going Strong for UMS?

- Spending on equipping fabs will increase by 133 percent in 2010 to an estimated $34 billion

- The World Fab Forecast report predicts spending in 2011 to increase 18 percent, bringing total spending to $39B, finally surpassing 2007 spending levels.

• Strong balance sheet & experienced Management Team- Management team is headed by founder – Mr Andy Luong, who has 26

years of experience in the business.- Balance sheet to remain strong as orders continue to be strong and the lack

of any major capex in the coming quarters/coming year.- Consistent dividend track record

What’s Going Strong for UMS?

Semiconductor Growth

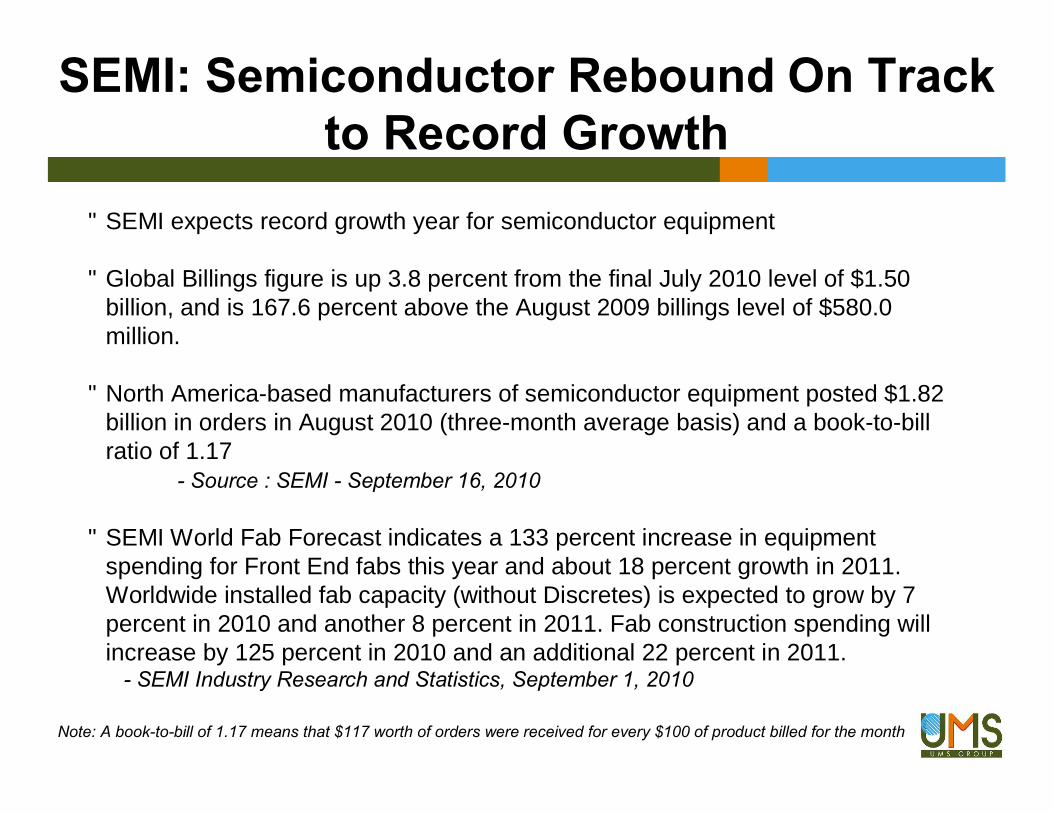

SEMI: Semiconductor Rebound On Track to Record Growth

• SEMI expects record growth year for semiconductor equipment

• Global Billings figure is up 3.8 percent from the final July 2010 level of $1.50 billion, and is 167.6 percent above the August 2009 billings level of $580.0 million.

• North America-based manufacturers of semiconductor equipment posted $1.82 billion in orders in August 2010 (three-month average basis) and a book-to-bill ratio of 1.17

- Source : SEMI - September 16, 2010

• SEMI World Fab Forecast indicates a 133 percent increase in equipment spending for Front End fabs this year and about 18 percent growth in 2011. Worldwide installed fab capacity (without Discretes) is expected to grow by 7 percent in 2010 and another 8 percent in 2011. Fab construction spending will increase by 125 percent in 2010 and an additional 22 percent in 2011.

- SEMI Industry Research and Statistics, September 1, 2010

Note: A book-to-bill of 1.17 means that $117 worth of orders were received for every $100 of product billed for the month

What Analyst Say about UMS

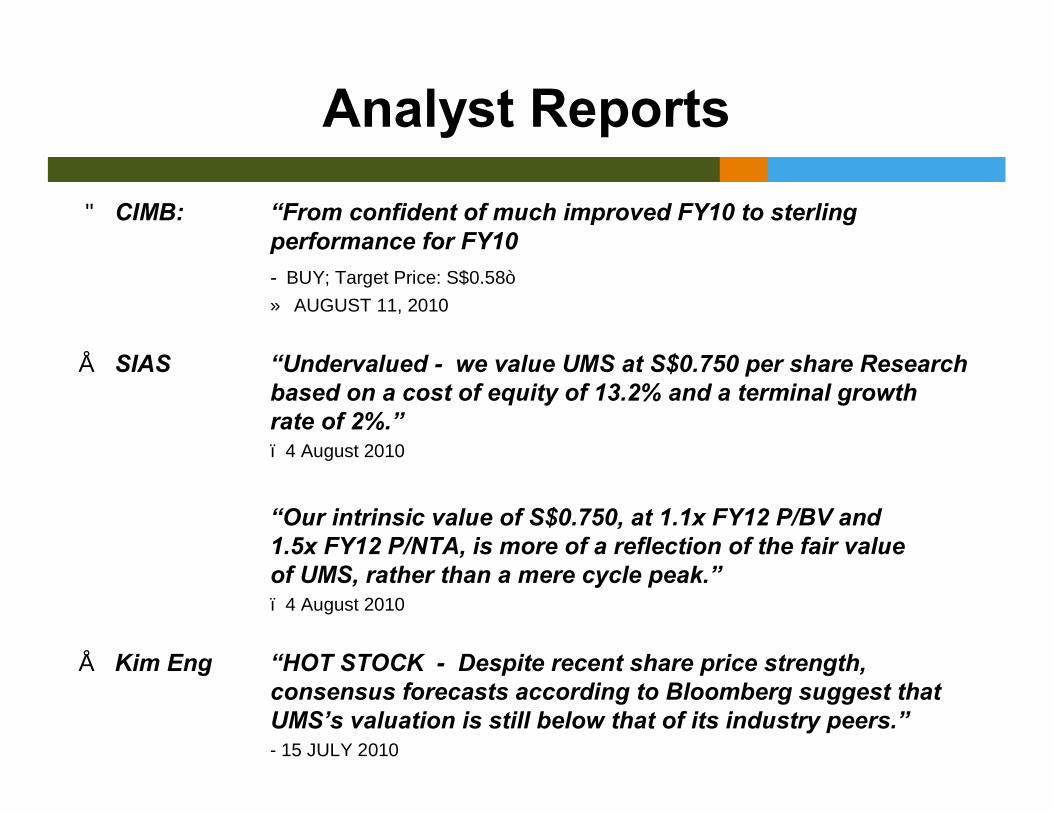

• CIMB: “From confident of much improved FY10 to sterling performance for FY10- BUY; Target Price: S$0.58”» AUGUST 11, 2010

• SIAS “Undervalued - we value UMS at S$0.750 per share Researchbased on a cost of equity of 13.2% and a terminal growth rate of 2%.”– 4 August 2010

“Our intrinsic value of S$0.750, at 1.1x FY12 P/BV and 1.5x FY12 P/NTA, is more of a reflection of the fair value of UMS, rather than a mere cycle peak.”– 4 August 2010

• Kim Eng “HOT STOCK - Despite recent share price strength, consensus forecasts according to Bloomberg suggest that UMS’s valuation is still below that of its industry peers.”- 15 JULY 2010

Analyst Reports

Our Financials

Financial Highlights

2Q FY10 2Q FY09 ChangeRevenue (S$'000) 35,274 7,305 383%Net Profit 7,480 -22,917 NM

Financial Ratios 2Q FY10 2Q FY09 ChangeNet Profit margin 21% NM NM

• Financial Ratios:

• Financial Highlights:

2Q FY10 (3 months) FY 2009

ROE 4.42% NM

ROA 3.61% NM

Current Ratio 2.2 2.2

Debt Equity Ratio 0.06 0.13

Dividend Track Record

- The Group gave out interim dividend in 2Q FY2010

S$ cents per share

Share Price as of 24 September 2010

Summary

Summary

• Profitable performance

• Healthy dividend track record

• Low gearing

• Strong cash balance - which is still growing

• Continued strong orders in the pipeline

• Beneficiary of the sustained semicon upturn and the rising outsourcing opportunities from USA to Asia

• Experienced and committed management team

• Available capacity for more orders to increase market share

• Undervalued share

Q&A

Thank YouFor further enquiries, please contact:

Stratagem ConsultantsMs Tham Moon Yee ([email protected])

Mr Lee Yew Meng ([email protected])Ms Tanna Khoo ([email protected])

Tel: 65-6227 0502

UMS Holdings LimitedStanley Loh ([email protected])

25 Changi North RiseChangi North Industrial Estate

Singapore 498778Tel: 65-6543 2272

Website: www.umsgroup.com.sg