UK Retail sector: trading in 2018 - ey.com · Black Friday became even more of an online Since the...

12

UK Retail sector: trading in 2018 Rising to the challenge in the year ahead and beyond

-

Upload

trinhkhanh -

Category

Documents

-

view

213 -

download

0

Transcript of UK Retail sector: trading in 2018 - ey.com · Black Friday became even more of an online Since the...

UK Retail sector: trading in 2018 Rising to the challenge in the year ahead and beyond

Retail: is 2018 the beginning or the end?With turbulence and disruption in the sector, what risks and opportunities lie ahead and what are the priorities for future success? An EY panel with a wealth of retail experience held a webcast in January 2018 to discuss their views and ask participants for their insights.

Contents

2 2018 peak season trading overview

3 The retail transactional and IPO market

4 Stress in 2018: the margin vice continues to tighten

5 Mapping out the future of retail

7 Summary

1

2 UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

The 2018 peak seasonNon-food sales through stores continue to suffer

Headline economic statistics underline the key themes that impacted peak season trading in 2017. These include:

► A 0.4%1 fall in real earnings in the three months to October 2017.

► Food inflation running at 3.7% in the three months to December.2

► Consumer Confidence Index (CCI) at -13 in December,3 its lowest since 2013.

► A 3.5% decline in December footfall,4 the steepest fall in five years. Black Friday became even more of an online

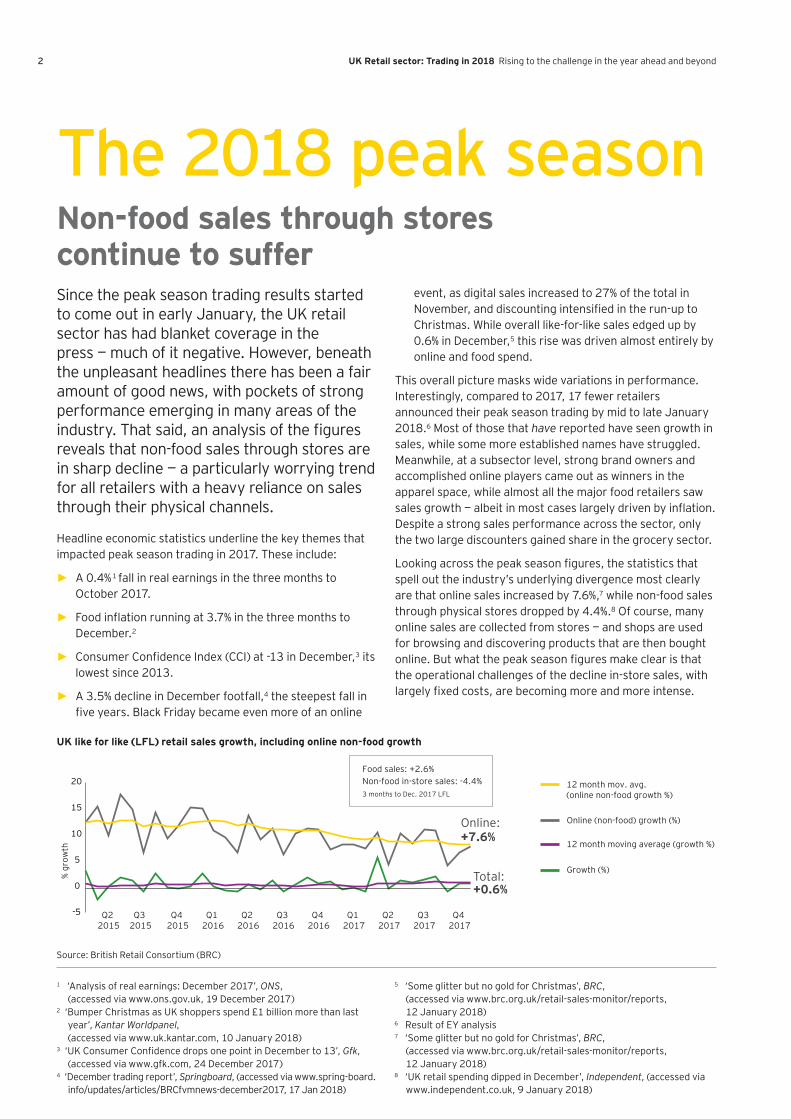

Since the peak season trading results started to come out in early January, the UK retail sector has had blanket coverage in the press — much of it negative. However, beneath the unpleasant headlines there has been a fair amount of good news, with pockets of strong performance emerging in many areas of the industry. That said, an analysis of the figures reveals that non-food sales through stores are in sharp decline — a particularly worrying trend for all retailers with a heavy reliance on sales through their physical channels.

1 ‘Analysis of real earnings: December 2017’, ONS, (accessed via www.ons.gov.uk, 19 December 2017)

2 ‘Bumper Christmas as UK shoppers spend £1 billion more than last year’, Kantar Worldpanel, (accessed via www.uk.kantar.com, 10 January 2018)

3 ‘UK Consumer Confidence drops one point in December to 13’, Gfk, (accessed via www.gfk.com, 24 December 2017)

4 ‘December trading report’, Springboard, (accessed via www.spring-board.info/updates/articles/BRCfvmnews-december2017, 17 Jan 2018)

5 ‘Some glitter but no gold for Christmas’, BRC, (accessed via www.brc.org.uk/retail-sales-monitor/reports, 12 January 2018)

6 Result of EY analysis7 ‘Some glitter but no gold for Christmas’, BRC,

(accessed via www.brc.org.uk/retail-sales-monitor/reports, 12 January 2018)

8 ‘UK retail spending dipped in December’, Independent, (accessed via www.independent.co.uk, 9 January 2018)

UK like for like (LFL) retail sales growth, including online non-food growth

Source: British Retail Consortium (BRC)

event, as digital sales increased to 27% of the total in November, and discounting intensified in the run-up to Christmas. While overall like-for-like sales edged up by 0.6% in December,5 this rise was driven almost entirely by online and food spend.

This overall picture masks wide variations in performance. Interestingly, compared to 2017, 17 fewer retailers announced their peak season trading by mid to late January 2018.6 Most of those that have reported have seen growth in sales, while some more established names have struggled. Meanwhile, at a subsector level, strong brand owners and accomplished online players came out as winners in the apparel space, while almost all the major food retailers saw sales growth — albeit in most cases largely driven by inflation. Despite a strong sales performance across the sector, only the two large discounters gained share in the grocery sector.

Looking across the peak season figures, the statistics that spell out the industry’s underlying divergence most clearly are that online sales increased by 7.6%,7 while non-food sales through physical stores dropped by 4.4%.8 Of course, many online sales are collected from stores — and shops are used for browsing and discovering products that are then bought online. But what the peak season figures make clear is that the operational challenges of the decline in-store sales, with largely fixed costs, are becoming more and more intense.

-5

0

5

10

15

20

% gr

owth

Growth (%)

Online (non-food) growth (%)

12 month moving average (growth %)

12 month mov. avg. (online non-food growth %)

Food sales: +2.6%Non-food in-store sales: -4.4%3 months to Dec. 2017 LFL

Online: +7.6%

Total: +0.6%

Q2 2015

Q3 2015

Q4 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q1 2017

Q2 2017

Q3 2017

Q4 2017

The retail transactional and IPO marketStill quiet

However, it is clear that funding remains wary of the industry — a situation reflected in the sector’s IPO activity. While 2017 saw notable growth in UK IPO volumes generally, with 77 IPOs generating £13 billion, this total included only

When asked to assess investor and lender confidence in the retail sector for the year ahead, webcast participants gave a decidedly downbeat response — with less than 2% rating the mood as ‘positive’, and over 80% opting for ‘cautious’. Compared with last year’s vote, the bright spot is that the proportion characterising investors’ mood as ‘reluctant’ declined from 27% to 17.5% — suggesting that the prospects for investments into the industry may be improving slightly, as 2017’s cost pressures ease off.

9 Result of EY analysis, Mergermarket, (accessed via www.mergermarket.com, January 2018)

3UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

Jan. 2015–Jan. 2018 retail share performance vs. FTSE 350

Source: Capital IQ

two retail IPOs.9 In fact, similarly low levels of retail IPOs have been a consistent trend since the peak of 13 achieved in 2014. A look at the relative performance of quoted retailers against the overall FTSE 350 index from 2015 through to January 2018 shows that retail stocks have generally under performed, with general retailers’ shares in particular well off the pace. Food retailers have been more stable, and actually outperformed the FTSE 350 over the last quarter — although this trend has been distorted by two particular stocks with specific events driving an increase.

Turning to the transaction environment, the number of retail deals has been at a relatively consistent level since the trough of 2013. However, retail acquisitions by UK private equity have generally remained at subdued levels, reflecting the lack of confidence in retail as a whole, the perceived lack of debt capacity in retail, and a reduced willingness to lend to the bricks-and-mortar retail segment in particular. However, one measure that appears possible to increase in 2018 is the number of distressed situations: these are already starting to drive deals, and are likely to do so increasingly in the coming months.

Q2 2015

Q3 2015

Q1 2015

Q4 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q1 2017

Q2 2017

Q3 2017

Q4 2017

Q1 2018

(estimate)

60

70

80

90

100

110

120

130

Inde

x (r

ebas

ed)

FTSE 350

General retailers

Food and drug retailers

4 UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

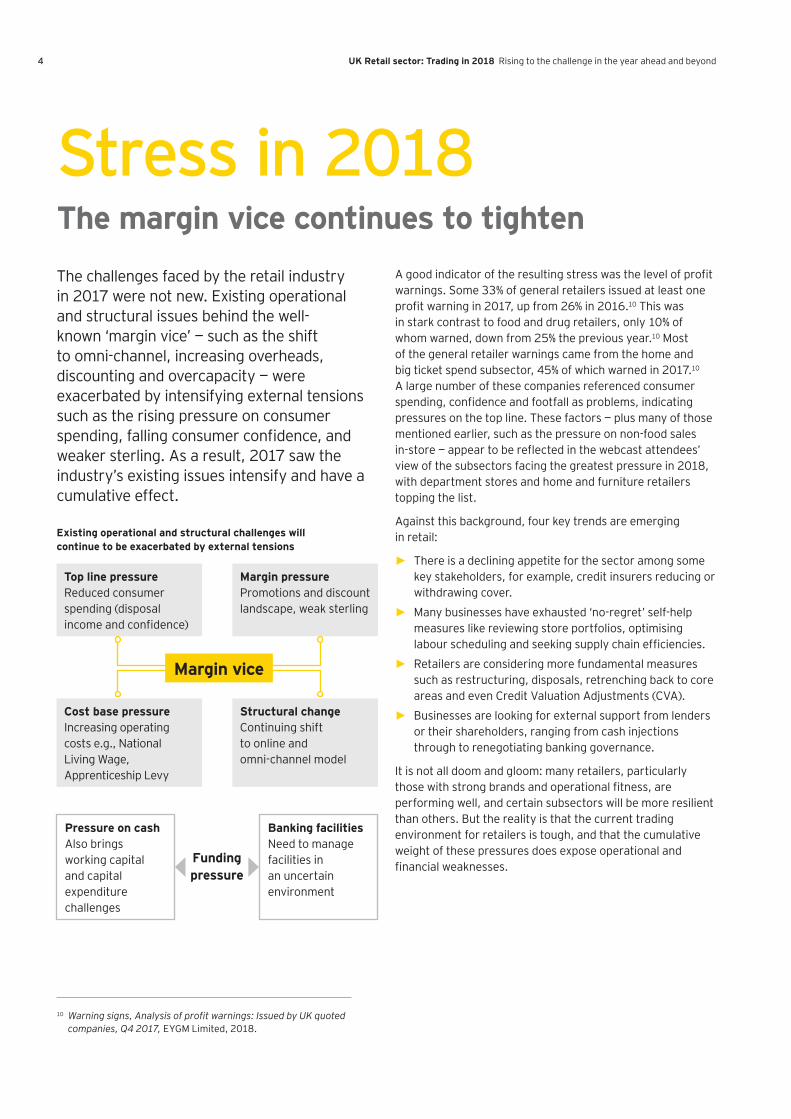

Stress in 2018The margin vice continues to tighten

A good indicator of the resulting stress was the level of profit warnings. Some 33% of general retailers issued at least one profit warning in 2017, up from 26% in 2016.10 This was in stark contrast to food and drug retailers, only 10% of whom warned, down from 25% the previous year.10 Most of the general retailer warnings came from the home and big ticket spend subsector, 45% of which warned in 2017.10 A large number of these companies referenced consumer spending, confidence and footfall as problems, indicating pressures on the top line. These factors — plus many of those mentioned earlier, such as the pressure on non-food sales in-store — appear to be reflected in the webcast attendees’ view of the subsectors facing the greatest pressure in 2018, with department stores and home and furniture retailers topping the list.

Against this background, four key trends are emerging in retail:

► There is a declining appetite for the sector among some key stakeholders, for example, credit insurers reducing or withdrawing cover.

► Many businesses have exhausted ‘no-regret’ self-help measures like reviewing store portfolios, optimising labour scheduling and seeking supply chain efficiencies.

► Retailers are considering more fundamental measures such as restructuring, disposals, retrenching back to core areas and even Credit Valuation Adjustments (CVA).

► Businesses are looking for external support from lenders or their shareholders, ranging from cash injections through to renegotiating banking governance.

It is not all doom and gloom: many retailers, particularly those with strong brands and operational fitness, are performing well, and certain subsectors will be more resilient than others. But the reality is that the current trading environment for retailers is tough, and that the cumulative weight of these pressures does expose operational and financial weaknesses.

The challenges faced by the retail industry in 2017 were not new. Existing operational and structural issues behind the well-known ‘margin vice’ — such as the shift to omni-channel, increasing overheads, discounting and overcapacity — were exacerbated by intensifying external tensions such as the rising pressure on consumer spending, falling consumer confidence, and weaker sterling. As a result, 2017 saw the industry’s existing issues intensify and have a cumulative effect.

10 Warning signs, Analysis of profit warnings: Issued by UK quoted companies, Q4 2017, EYGM Limited, 2018.

Existing operational and structural challenges will continue to be exacerbated by external tensions

Margin vice

Top line pressure Reduced consumer spending (disposal income and confidence)

Cost base pressure Increasing operating costs e.g., National Living Wage, Apprenticeship Levy

Margin pressure Promotions and discount landscape, weak sterling

Structural change Continuing shift to online and omni-channel model

Pressure on cash Also brings working capital and capital expenditure challenges

Banking facilities Need to manage facilities in an uncertain environment

Funding pressure

2018 and beyondThe changing fabric of retail

The future of retail can be considered through three lenses:

The macroeconomic backdrop — and here it is vital to remember how critical consumer spending is to the overall UK economy. The good news is that the squeeze on the consumer seen in 2017 should ease during 2018 as inflation falls back and real wages start to rise again. However, the upside to consumer spending is likely to be limited by slower employment growth and the uncertainty that Brexit has caused around business investment. So the wallet for UK retail is stable at best — and given the rising competitive intensity and proliferating alternative uses for that wallet, ‘stability’ for traditional retail appears unlikely.

Given the extreme and ongoing structural pressures on the retail sector’s operational and financial state, it is clear that the handle of the margin vice will continue to turn. Faced with such a situation, it is all too easy for retail businesses to look inwards and think about how to react internally to those pressures, rather than directing at least some of their attention outwards to the market, to consumers and the competition. To survive and thrive, this is what they will need to do.

1

5UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

Impact on shopping habits

Customer experience

86% 82% 78%

Brand’s clear purpose

Good treatment

of staff

6 UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

11 If brand + trust = value, how are you solving the equation?, EYGM Limited, 2017

The changing fabric of retail itself, as the disruptors redefine consumer expectations by bringing them control, transparency and speed. Consumers are looking for the right experience: in a recent EY survey of more than 2,500 UK consumers, 86% of consumers noted shopping experience as the top influencer on their buying behaviour.11 Given that footfall and online traffic are the new currency, the question is whether retailers can provide an experience that competes with the leisure experience and is also consistent across the ‘micro-moments’ that make up the customer journey. This requires personalisation, which demands data. Retailers must be able to use data to target customers across channels and segment them by behaviour, while also — as General Data Protection Regulation (GDPR) looms — maintaining security around their customer data. This brings us to trust, which is increasingly imperative, with 74% of consumers telling us they would boycott a brand that they didn’t trust,11 and 78% saying their purchasing decisions are strongly influenced by how a brand treats its employees.11

What will the UK retail landscape look like in 10 years’ time? In our view, consumers will become more asset-light, and will shift towards choosing a smaller number of products — because the rest will be done for them by algorithms. So, the fight for that small choice will be even more intense, and consumer businesses will need to focus less on product and even more on lifestyle. Similarly, the trust equation will become ever more important. Obviously, this future will bring challenges. But for those players with good brands and good strategic assets, there are exciting times ahead — and they absolutely can play to win.

2018 and beyondThe changing fabric of retail

2 3

SummaryThe time for half-measures is over

The picture emerging from our retail trading 2018 webcast is of a fast-changing retail environment in which non-food bricks-and-mortar retailers are especially exposed, and those with strong brands and differentiated online capabilities and customer experience have the edge. At the same time, the industry challenges seen over Christmas 2017 continue to be reflected in limited acquisition lending and lukewarm private equity interest, and the likelihood of more M&A driven by distress situations. Yet, some very interesting and positive things are happening in terms of innovation — particularly around consumer experiences and trust.

A new retail paradigm demands new thinking — and for those able to develop and apply it — 2018 is the beginning, not the end.

7UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

8 UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

8UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

9UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

Contacts

David LarssonPartner, EY-Parthenon UK & Ireland Ernst & Young LLP

T: + 44 20 7951 8239 E: [email protected]

Jessica ClaytonPartner, Head of Retail for Transaction Advisory Services UK & Ireland Ernst & Young LLP

T: + 44 20 7951 3034 E: [email protected]

Julie CarlylePartner, Head of Retail UK & Ireland Ernst & Young LLP

T: + 44 20 7951 3034 E: [email protected]

Martin CarrStrategic Retail Advisor UK & Ireland Ernst & Young LLP

T: + 44 20 7760 9219 E: [email protected]

Christian MoleAssociate Partner, Transaction Diligence UK & Ireland Ernst & Young LLP

T: + 44 20 7951 3034 E: [email protected]

9UK Retail sector: Trading in 2018 Rising to the challenge in the year ahead and beyond

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLPThe UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

© 2018 Ernst & Young LLP. Published in the UK. All Rights Reserved.

EYG no. 01361-184GBL

ED None

EY-000054876.indd (UK) 03/18. Artwork by Creative Services Group London.

In line with EY’s commitment to minimise its impact on the environment, this document has been printed on paper with a high recycled content.

Information in this publication is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice. Ernst & Young LLP accepts no responsibility for any loss arising from any action taken or not taken by anyone using this material.

ey.com/uk