UBS research focus · UBS research focus March 2009 The financial crisis and its aftermath Public...

94

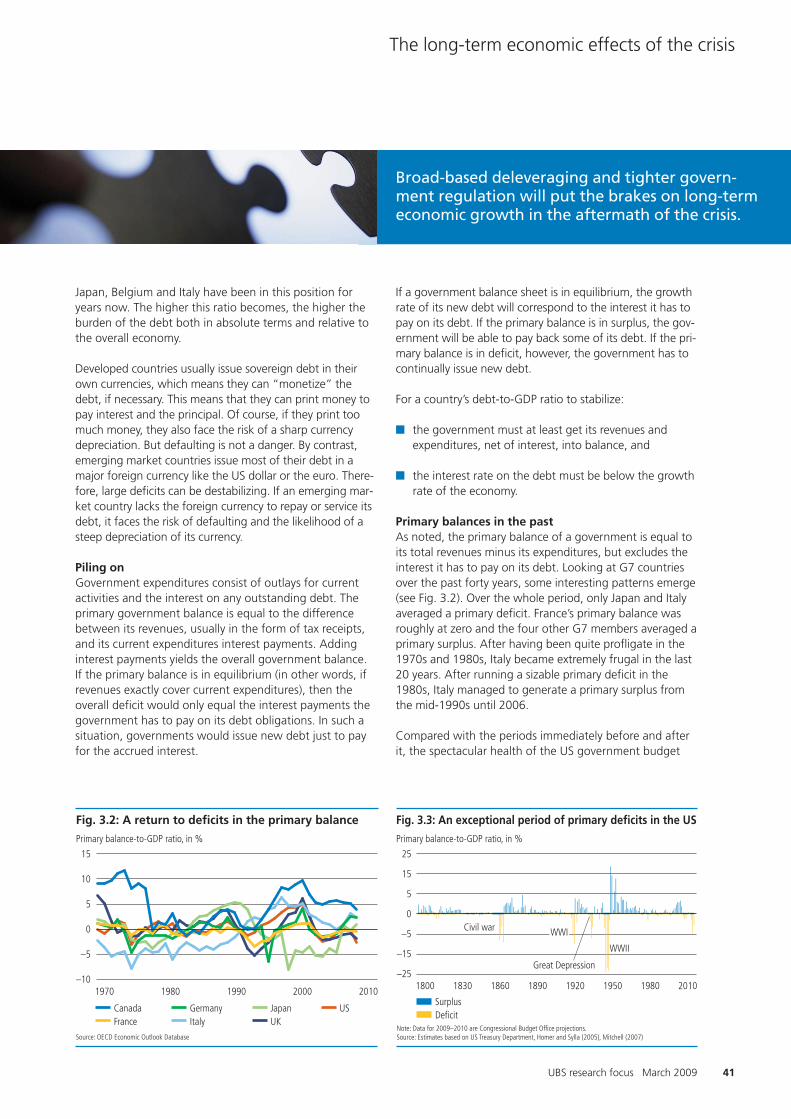

UBS research focus March 2009 A c b The financial crisis and its aftermath Public sector debt imbalances to grow more acute Lower trend economic growth, higher risk of inflation Earnings to revert to a more sustainable path Financial markets have priced in a very austere outlook Nominal bonds expensive, stocks and corporates cheap Inflation-linked bonds should top cash as a safe long-term asset

Transcript of UBS research focus · UBS research focus March 2009 The financial crisis and its aftermath Public...

UBS research focusMarch 2009

� ��

The financial crisis and its aftermath

Public sector debt imbalances to grow more acute

Lower trend economic growth, higher risk of inflation

Earnings to revert to a more sustainable path

Financial markets have priced in a very austere outlook

Nominal bonds expensive, stocks and corporates cheap

Inflation-linked bonds should top cash as a safe long-term asset

This report has been prepared byUBS Financial Services Inc. (‘‘UBSFS’’) and UBS AG

Past performance is no indication of future performance.The market prices provided are closing prices on therespective principle exchange. This applies to all perform-ance charts and tables in this publication.

Contents

UBS research focus March 2009 3

Editorial 5Summary 6

Chapter 1Reversals of fortune 9

The end of an era 10The financial crisis: an array of factors 14Pendulum swings towards the state 18

Chapter 2The rise of even bigger government 23

The new financial handbook 24Fiscal policy: money with a mission 25Monetary policy: beware of excess liquidity 29Financial industry regulation: a new framework in the making 31

Chapter 3The long-term economic effects of the crisis 39

Structural debt growth ahead 40Future economic growth 43Inflation in the future 49High and permanent fiscal deficits and inflation 50

Chapter 4A fundamental reassessment of asset returns 55

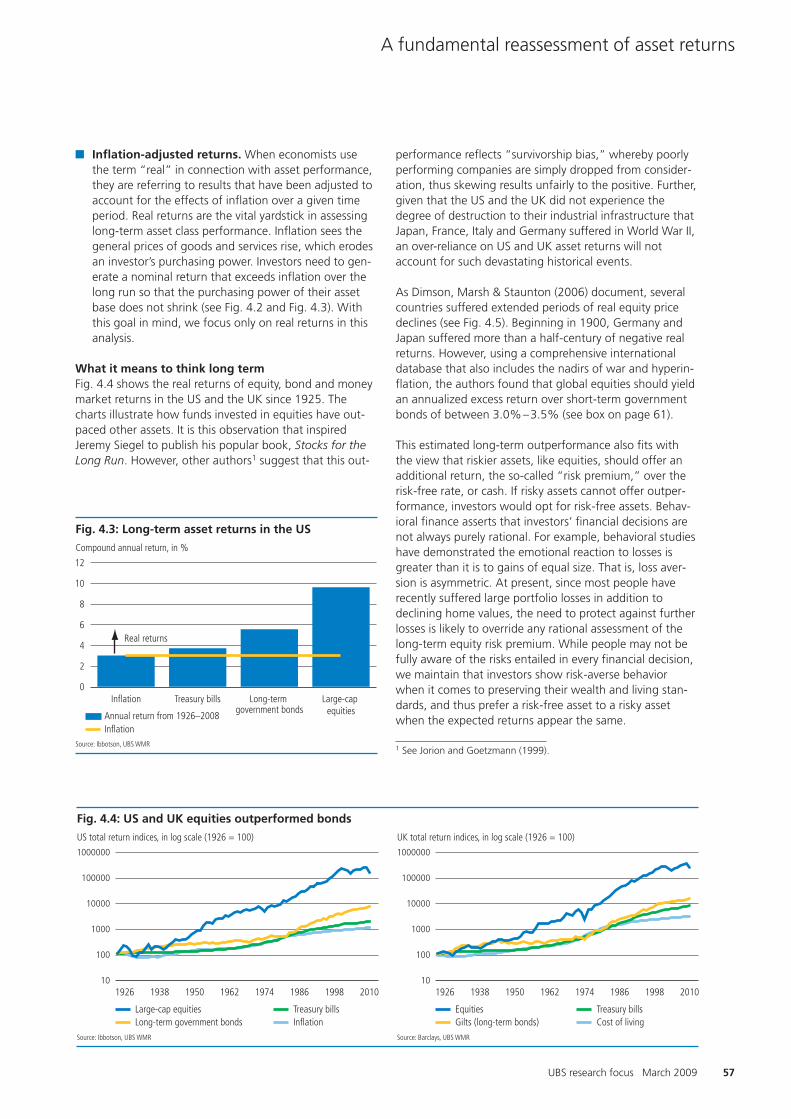

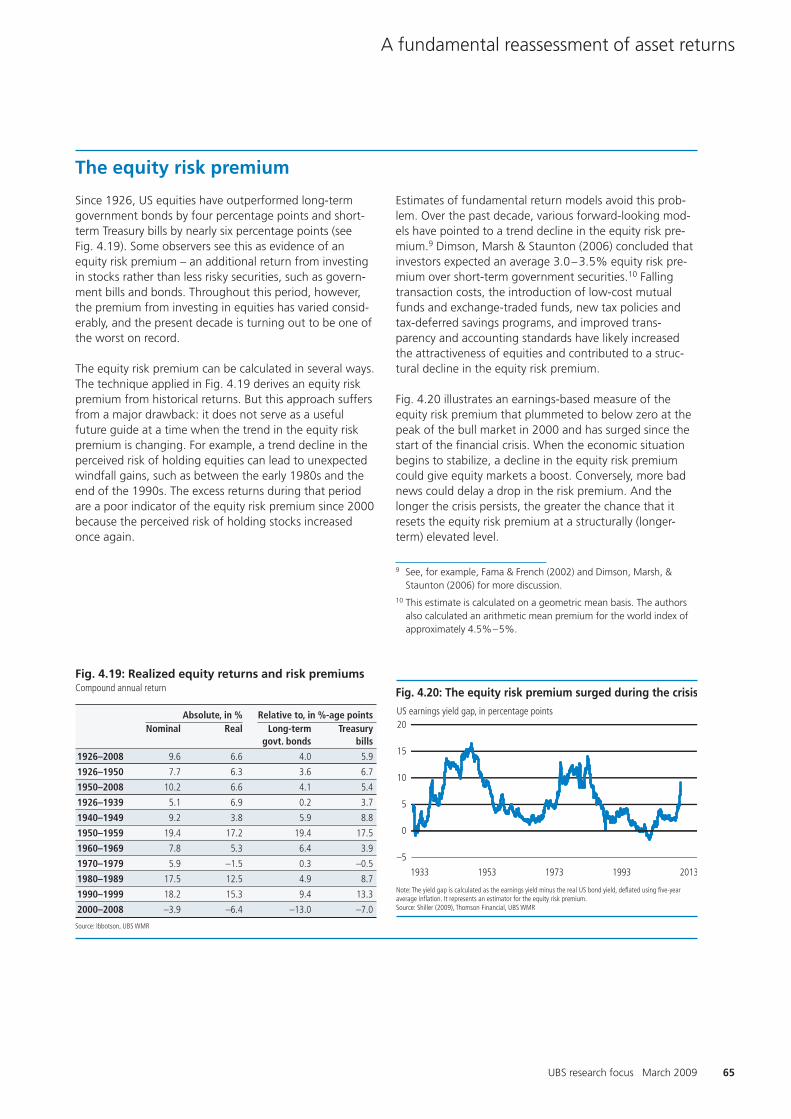

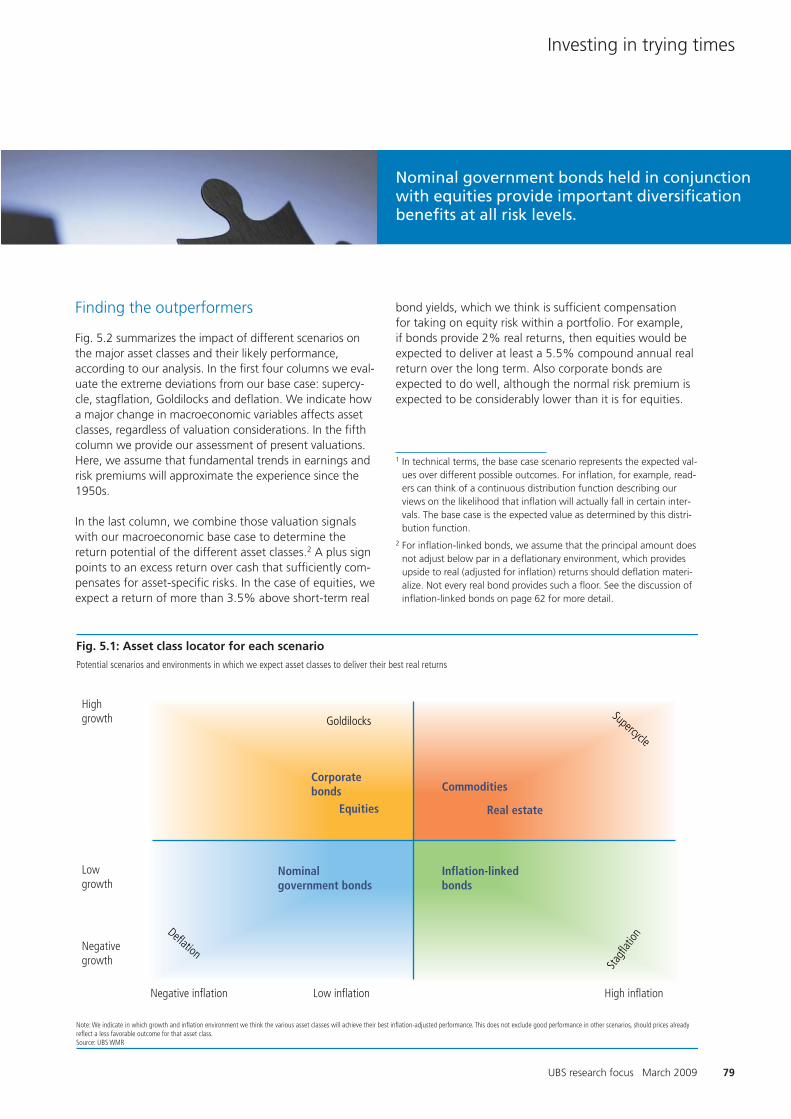

A fresh look at the investment horizon 56Nominal government bonds expensive 59Equities: value amid structural challenges 63Real estate: stricter regulation and lower yields 72Commodities: a partial inflation hedge 72Conclusion 73

Chapter 5Investing in trying times 77

Evaluating opportunities and risks 78Finding the outperformers 79The portfolio context: putting it all together 80Conclusion 85Box: The USD remains an important risk 86

Glossary 87

Bibliography 91

Publication details 94

5UBS research focus March 2009

Editorial

Dear reader,

The financial crisis that intensified in 2008 shook theglobal economy to its foundations. It also unleashed a crisis of confidence among consumers, businesses andinvestors that threatened to unravel most forms of globalcommerce. In response, the actions taken by govern-ments – spending measures, tax cuts, reductions in short-term interest rates and purchases of financial assets – are essential steps to revive confidence and global eco-nomic activity.

In the aftermath of the crisis, a new economic era is taking shape. It is already clear that the state will play amuch bigger role in economic affairs, one that it is unlikelyto give up even after the situation stabilizes. And longer-term risks loom. One of them, inflation, is an expedienttool for policymakers to redistribute the burden of highlevels of private and public debt. Another, protectionism,is a regrettable knee-jerk reaction during times of eco-nomic upheaval.

Falling trade barriers, increased international capital flows, and the spread of private-sector activities producedenormous benefits for the world economy. At the sametime, however, these same international trade and capitalflows became increasingly unstable, as we discussed in a UBS research focus report entitled, “Currencies: a deli-cate imbalance,” early in 2008. Restoring sustainable economic growth will not be easy, but strong efforts arenow underway to reverse the downturn's momentum and offer hope for a recovery.

But we should not forget that well before the crisis hit,demographic forces were already pointing to both slowerlong-term economic growth and greater pressure on gov-ernment finances. The unwinding of household and cor-porate balance sheet leverage, as well as heightened regu-lation, are likely to slow economic activity even further.

Andreas Höfert Walter Edelmann Kurt E. ReimanGlobal Head Wealth Management Research Head Global Investment Strategy Head Thematic Research

In sum, we expect public sector imbalances to growsteadily in future as countries grapple with tough choicesover potential spending cuts or higher taxes.

Financial markets, once priced for perfection, now reflecta pessimism that is, in fact, far darker than the new eco-nomic realities indicate. Surely, the aftermath of the crisiswill seem austere given its bubbling prelude, but it willalso offer investors attractive opportunities. We think thisturning point demands a clear-eyed review not only of assets and portfolios, but also of the methods used toevaluate them. That is what we have attempted to deliverin this edition of the UBS research focus.

6 The financial crisis and its aftermath

Summary

A new post-crisis policy paradigm Measured in lost wealth, the financial crisis that erupted in2007 and intensified throughout 2008 has alreadyachieved historic proportions. Today, we are witnessingthe emergence of a new policy paradigm. After decadesof burgeoning free-market internationalism, governmentswill extend their reach as they struggle to revive theireconomies. So far, governments and their central bankshave intervened on two fronts: stabilizing and in somecases nationalizing their crippled financial sectors, andusing fiscal and monetary policy tools to counter a deepglobal recession.

In our view, these measures are crucial to turn the tide offalling demand, rising unemployment and looming defla-tion. Had governments not undertaken strong measuresduring the second half of 2008 to repair dysfunctionalfinancial markets, most forms of global commerce, whichwere already under severe stress, would have likely groundto a halt.

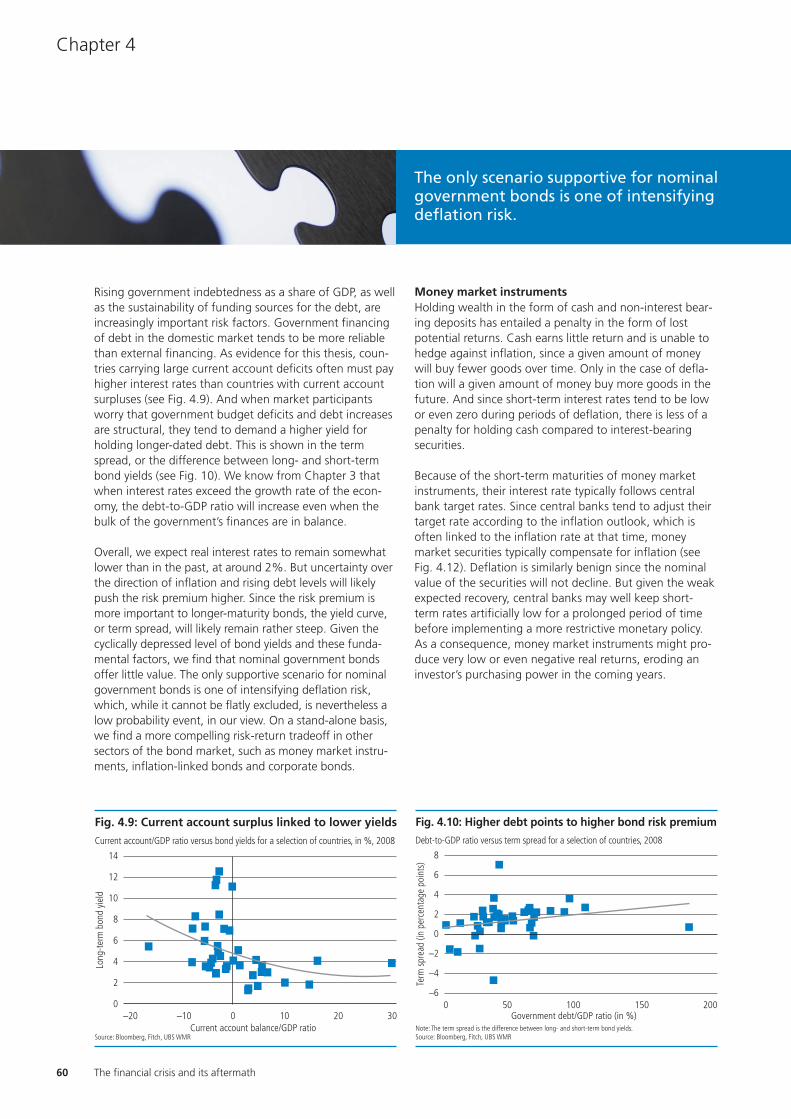

Public sector debt imbalances to grow more acuteAs credit markets seized, households and corporationsbegan reducing balance sheet leverage rapidly. This, inturn, has accelerated the contraction in overall economicactivity in the countries that were hit hardest by the finan-cial crisis. But as one set of imbalances begins to fade,another is set to grow, this time on the balance sheets ofgovernments.

With central banks having cut short-term interest rates tohistoric lows, attention now shifts to government spend-ing plans and nontraditional monetary policy tools. Thespending measures mostly target boosting short-termdemand, not returning the economy to a sustainable long-term growth path. At best, these fiscal measures will suc-ceed in dampening the impact of the recession whileallowing the private-sector imbalances in the economy toadjust. Indeed, our analysis suggests that the initial posi-tive effects of the spending measures on growth are likelyto be reversed in subsequent years.

While the effect of fiscal stimulus on the economy ishighly uncertain, and a subject of intense academicdebate, the consequences of big spending packages ongovernment deficits and debt are clear. The large fiscalpackages, the cost of bank bailouts, and the generallydiminished tax revenues have increased public-sector debtfaster than at any time since World War II.

At the same time, central bank purchases of public- andprivate- sector debt have swelled their balance sheets, andhence the money supply. In our view, the question is notwhether more central banks will undertake so-called“quantitative easing” measures – increasing the moneysupply by debt purchases (and the printing press) – buthow they will exit this path later on.

Lower trend growth, risk of higher inflationThe ongoing aging of the population coupled with bothbroad-based deleveraging and increased regulation arevery likely to significantly dampen future growth rates indeveloped countries. Consequently, governments faceever-increasing deficits and subdued growth with feweffective options at their disposal. Debt-to-GDP ratios willlikely rise unless there are cuts in discretionary and entitle-ment spending or taxes are increased. And in countriesmost exposed to the financial crisis, policymakers may pre-fer higher inflation as an antidote to ever-increasing debt.

For many, the inflation of the 1970s is still fresh and it isoften regarded as something bad. Yet inflation wouldadvance the deleveraging process. It profoundly affectswealth redistribution by reducing the real value of out-standing debt. The main problem for policymakers oncethe financial crisis has passed will be to ensure that themassive liquidity injections from governments and centralbanks do not lead to a surge in inflation. We think recenthistory has shown that the focus on consumer price stabil-ity has its practical limits. It can neither prevent “irrationalexuberance,” as the Tech, real estate and credit bubbleshave shown, nor avoid the risk of deflation when the exu-berance of market participants turns to panic.

Nominal government bonds expensiveGiven the cyclically depressed level of bond yields, we findthat nominal government bonds offer little value at pres-ent. The only supportive scenario for nominal governmentbonds is one of intensifying deflation risk, which, while itcannot be flatly excluded, is nevertheless unlikely, in ourview. On a standalone basis, we find a more compellingrisk-return tradeoff in other sectors of the bond market,such as money market instruments, inflation-linked bondsand corporate bonds.

Earnings growth to return to a more sustainable pathThe crisis has had a profound effect on the drivers of assetreturns. In our view, a sharp earnings recovery is unlikely,and trend earnings are likely to be structurally weaker.Given the diversity of sectors and companies in overallequity market indexes, the risk to the sustainable earningstrend is much less pronounced than for individual sectors.

SummaryThe financial crisis and its aftermath

7UBS research focus March 2009

Summary

Overall, we think a trend growth rate of real earnings ofabout 2.5% for the US is a reasonable assumption.Although this is significantly lower than the earningsgrowth rate during the two decades preceding the finan-cial crisis, it is broadly in line with the postwar experience.

Lower trend earnings in the financial sectorThe financial crisis faces more regulation and tightersupervision. However, too tight a grip on the industrymight undercut efforts to unclog the financial system andencourage lending. Overall, we expect that after the crisispasses, the financial sector in developed economies will bemore heavily regulated and will face more limited growthopportunities than in the past. After outpacing otherindustries since the 1980s, we expect lower trend earn-ings growth in the financial sector as regulation curtailsactivities that offer higher margins and growth, whetherbecause of market realities, loss of risk appetite orbecause of regulatory constraints.

Equities appear cheapStocks have tended to deliver the strongest returns afterperiods of extreme economic stress and financial marketupheaval, which, not surprisingly, were times when stockswere at their least expensive levels. Despite the weak out-look for growth in trend earnings, equities offer significantlong-term scope for gain in a scenario where the eco-nomic environment stabilizes, as we expect.

US dollar at riskWe believe the US dollar remains at risk of further depreci-ation despite its neutral valuation. The financial crisis hadits epicenter in the US, and the fiscal and monetary policyreactions there have been much more aggressive, andmuch bigger, than in the Eurozone, for example. As soonas the US economic situation starts to stabilize, this liquid-ity overhang poses a major risk to the USD. Moreover, thesupranational architecture of the European Central Bankcould help to ensure stronger inflation-fighting credentialscompared to national central banks that would face pres-sure from rapidly rising government deficits and debt. Thiswould further support the euro relative to the US dollar ifinflation expectations were to begin to diverge betweenthe two regions, as we think is increasingly likely.

Investing in trying timesAs individuals reassess their risk appetites in the aftermathof the financial crisis, we continue to stress the benefits ofdiversification at all risk levels. Knowing where the “real”risks to your portfolio lie, especially for those assets tradi-tionally perceived as safe, is more important than ever.

Although equities have fallen sharply since their peak andhave posted negative real returns during the past decade,we recommend taking on equity exposure in combinationwith bond investments. This applies even for conservativeinvestors. The traditional mix of nominal bonds and equi-ties has appeal, especially in times when extreme out-comes are probable. Nominal bonds provide shelteragainst deflation. Equities offer potentially strong returnsin the event that the economy stabilizes. We think evenfairly defensive investors can boost risk-adjusted returnsthrough corporate bond exposure. Investors with a suffi-ciently long time horizon and the ability to withstand fur-ther market volatility should consider adding more signifi-cant exposure to equities, given that deflation is anextreme scenario and not our base case.

In our view, inflation-linked bonds are the preferred long-term safe asset, and we favor them even over cash.Investors concerned about soaring inflation should con-sider investing in inflation-linked bonds, which offer a safelong-term alternative and a fixed real return. Gold mightalso play a role in a mixed portfolio context, especially ifmajor geopolitical risks were to increase. For pure protec-tion against inflation, however, we prefer inflation-linkedbonds, as gold prices have already been bid up due toheightened risk aversion.

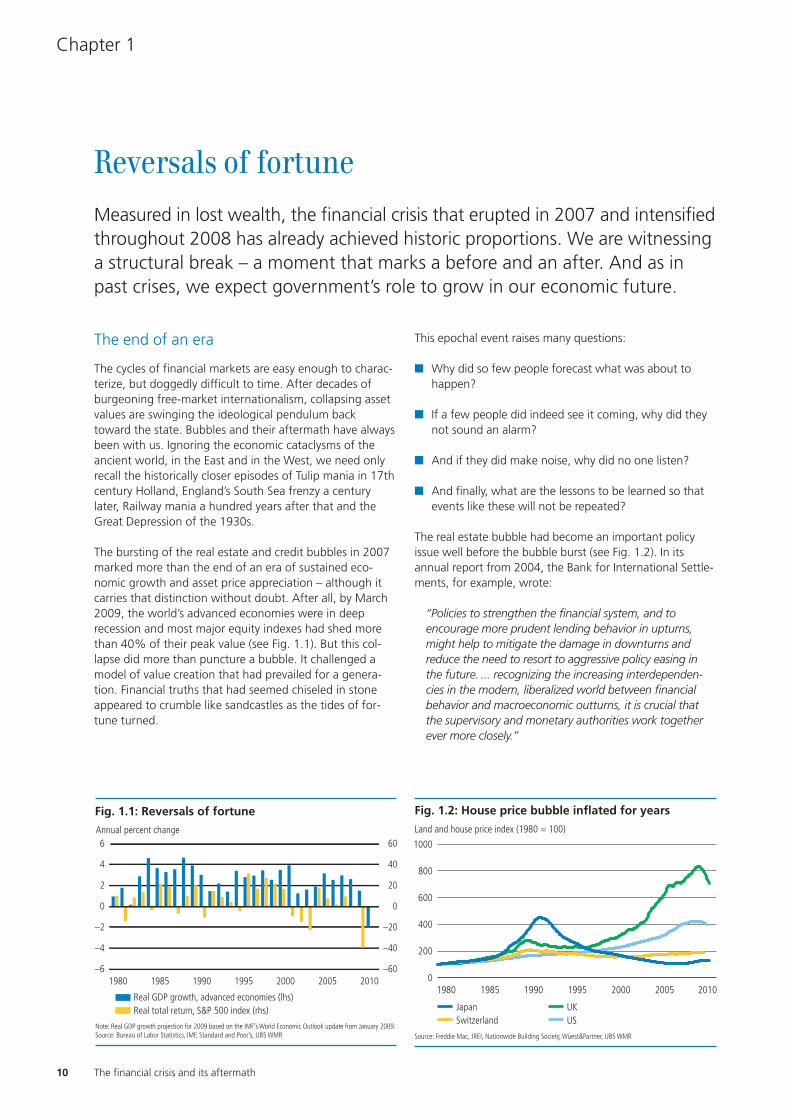

Reversals of fortuneChapter 1

10 The financial crisis and its aftermath

Chapter 1

Reversals of fortune

Measured in lost wealth, the financial crisis that erupted in 2007 and intensifiedthroughout 2008 has already achieved historic proportions. We are witnessinga structural break – a moment that marks a before and an after. And as inpast crises, we expect government’s role to grow in our economic future.

The end of an era

The cycles of financial markets are easy enough to charac-terize, but doggedly difficult to time. After decades ofburgeoning free-market internationalism, collapsing assetvalues are swinging the ideological pendulum backtoward the state. Bubbles and their aftermath have alwaysbeen with us. Ignoring the economic cataclysms of theancient world, in the East and in the West, we need onlyrecall the historically closer episodes of Tulip mania in 17thcentury Holland, England’s South Sea frenzy a centurylater, Railway mania a hundred years after that and theGreat Depression of the 1930s.

The bursting of the real estate and credit bubbles in 2007marked more than the end of an era of sustained eco-nomic growth and asset price appreciation – although itcarries that distinction without doubt. After all, by March2009, the world’s advanced economies were in deeprecession and most major equity indexes had shed morethan 40% of their peak value (see Fig. 1.1). But this col-lapse did more than puncture a bubble. It challenged amodel of value creation that had prevailed for a genera-tion. Financial truths that had seemed chiseled in stoneappeared to crumble like sandcastles as the tides of for-tune turned.

This epochal event raises many questions:

� Why did so few people forecast what was about tohappen?

� If a few people did indeed see it coming, why did theynot sound an alarm?

� And if they did make noise, why did no one listen?

� And finally, what are the lessons to be learned so thatevents like these will not be repeated?

The real estate bubble had become an important policyissue well before the bubble burst (see Fig. 1.2). In itsannual report from 2004, the Bank for International Settle-ments, for example, wrote:

“Policies to strengthen the financial system, and toencourage more prudent lending behavior in upturns,might help to mitigate the damage in downturns andreduce the need to resort to aggressive policy easing inthe future. ... recognizing the increasing interdependen-cies in the modern, liberalized world between financialbehavior and macroeconomic outturns, it is crucial thatthe supervisory and monetary authorities work togetherever more closely.”

1980 1985 1990 1995 2000 2005 2010–60

–40

–20

0

20

40

60

–6

–4

–2

0

2

4

6

Fig. 1.1: Reversals of fortune

Note: Real GDP growth projection for 2009 based on the IMF’s World Economic Outlook update from January 2009.Source: Bureau of Labor Statistics, IMF, Standard and Poor’s, UBS WMR

Annual percent change

Real GDP growth, advanced economies (lhs)Real total return, S&P 500 index (rhs)

1000

400

800

600

200

01980 1985 19951990 2000 2005 2010

Fig. 1.2: House price bubble inflated for years

Source: Freddie Mac, JREI, Nationwide Building Society, Wüest&Partner, UBS WMR

Land and house price index (1980 = 100)

UKSwitzerlandJapan

US

11UBS research focus March 2009

Reversals of fortune

After decades of burgeoning free-market inter -nationalism, governments will extend their reach as they struggle to revive their economies.

Others sounded warnings, too, but these were easyenough to ignore because growth, inflation, employment,earnings and productivity were all working so well. Butsome observers persisted in their concerns. NourielRoubini, professor of economics at New York University‘sStern School of Business and a senior economist for theCouncil of Economic Advisers during the Clinton adminis-tration, wrote in 2005 that, “…the US economy is alreadyimbalanced with low private savings, large budget deficits,large current account deficits, a real estate bubble and a‘shopped-out’ consumer.”

Alan Greenspan, chairman of the Board of Governors ofthe Federal Reserve from 1987 to 2006, was one of theleading advocates of the view that the US had entered anew era of prosperity thanks to greatly improved produc-tivity. In a widely acclaimed speech back in 2002, he saidthat the increasing use of computers and other high-techequipment was supporting the gain in productivity, muchlike the introduction of electricity and automobiles trig-gered a sharp rise in productivity a hundred years earlier.This seemed a good explanation for why the economy wasso strong. However, imbalances were growing, too. The UScurrent account deficit was widening steadily as US house-hold saving rates fell dramatically, and America’s depend-ency on China to finance these gaps was increasing.

When free markets reignedFinancial crises often spur policymakers to rethink the mer-its of the prevailing economic wisdom. We are witnessingsuch a transformation unfold today, as economists and

politicians search for new or rediscovered recipes to stimu-late the economy and avert an even wider contagion.

The last major revision of government and industrial policyemerged in the 1970s, when stagflation triggered a changein mindset. In the three decades following World War II, theindustrialized world enjoyed an extraordinary phase of economic growth characterized by accelerating productivityand incomes. This came to a screeching halt after the first oilcrisis, in 1973. Annual inflation rates soared to over 12% inthe US in the early 1970s and peaked at 14.5% in 1980 (seeFig. 1.3). In Western Europe the picture looked more or lessthe same. Unemployment rates moved higher and budgetdeficits rose amid stagnating overall economic activity.

In the search for solutions to these growing problems, Mil-ton Friedman and Robert Lucas from the University ofChicago, and Karl Brunner from the Universities ofRochester and Bern, Switzerland, challenged the then-dom-inant theory of John Maynard Keynes, which bestowed animportant role on the public sector to stimulate the econ-omy. Keynes’ General Theory of Employment, Interest andMoney (1936) gained popularity during the Great Depres-sion, when flagging demand sent the unemployment ratesoaring to 25%. Keynes argued that governments shouldcreate jobs to stimulate demand, reduce uncertainty andstabilize the economy. However, reducing public sectorspending proved difficult when the economy got back onits feet again. In the 1970s, government spending anddeficits grew steadily, and together with the decade’s twinoil crises, contributed to the extended stagflation episode.

25

20

–5

5

15

10

0

–10

–151960195019401930 1970 19901980 2000 2010

30

25

10

20

15

5

01960195019401930 1970 19901980 2000 2010

Fig. 1.3: Receding inflation and sharply higher unemployment cause concern

Source: Bureau of Labor Statistics

InflationUS consumer price index annual change, in %

UnemploymentUS unemployment rate, in %

12 The financial crisis and its aftermath

Chapter 1

The new monetarist school of thought focused its effortson fighting inflation by cutting the supply of money,although at a cost of a deep recession in the early 1980s.Attempts to bring inflation under control bore early fruit,which boosted the influence of the Chicago School. Fiscalpolicy and big spending were out of fashion, and mone-tary policy became the principal tool to smooth the busi-ness cycle, but never at the cost of letting inflation run outof control. The ideology of the next quarter-centuryreflected the belief that market liberalization, smaller gov-ernment and lower rates of inflation were the principalingredients of improved productivity, greater entrepre-neurship, solid economic growth and wealth creation.

British Prime Minister Margaret Thatcher and US PresidentRonald Reagan were the champions of this new approach,despite strong opposition from labor unions and otherpolitical opponents. During his first inaugural address, in1981, Reagan declared, “In this present crisis, governmentis not the solution to our problem; government is the prob-lem.“ Early success at restoring vibrancy to their economiessilenced many critics and paved the way for a prolongedperiod of market liberalization, privatization, tax cuts, glob-alization, and disinflation during the remainder of thetwentieth century.

� Market liberalization. US President Jimmy Cartermarked what is now seen as a watershed in deregula-tion when he signed the Airline Deregulation Act of1978 and, with the stroke of a pen, removed govern-ment control over many aspects of commercial aviation.Reagan took another large step when he dismantledthe federal air traffic controllers union in 1981.Together with Thatcher, they initiated a steady streamof liberalization that eventually included financial mar-kets and international capital flows (see Fig. 1.4).

� Privatization. In Britain, state-owned companiesaccounted for 12% of GDP in 1979 but only around2% by 1997. Privatization in Continental Europe had

also become more widely accepted by the mid-1990s(see Fig. 1.5). Germany, Spain and even the Socialist-governed France privatized large sectors of the econ-omy, like telecommunications, airlines, and broadcast-ing. Increasing productivity, soaring financial marketsand high rates of economic growth were the proof thatneo-liberalism functioned. Megginson et al. summedup the benefits of this policy in a paper in 2001:

“The political and economic policy of privatization,broadly defined as the deliberate sale by a govern-ment of state-owned enterprises or assets to privateeconomic agents, is now in use worldwide. Since itsintroduction by Britain’s Thatcher government in theearly 1980s to a then-skeptical public (that includedmany economists), privatization now appears to beaccepted as a legitimate – often a core – tool ofstatecraft by governments of more than 100 coun-tries. Privatization is one of the most important ele-ments of the continuing global phenomenon of theincreasing use of markets to allocate resources.”

In the US, privatization had less of an impact becausefewer sectors were state-owned to begin with. How-ever, Reagan’s ambitions to scale back governmentwere on display when he implemented a sweepinground of supply-side tax cuts in 1981. Reagan’s initialapproach was a simple one: the best way to shrink gov-ernment was to starve it of funding.

1 Concerning trade, there are no fundamental differences between theKeynesians and the monetarists. The theory of comparative advan-tage, developed by David Ricardo in 1810, is still widely accepted. Ina simple two-country, two-commodity framework, Ricardo demon-strated that trade is beneficial for all countries even if one countryproduces both items more cheaply. Politicians are prone to restrictfree trade during hard economic times because their increasinglyunemployed constituents see international competition as destroyingdomestic jobs. In fact, according to Ricardo’s theory, the opposite istrue: protectionism reduces productivity and efficiency.

0

700

200

500

400

600

300

100

–1001980 1985 19951990 2000 2005 2010

Fig. 1.4: Foreign assets poured into the US

Source: Bank for International Settlements, Bureau of Economic Analysis

Net capital inflows to the US, four-quarter moving average, in billions of USD

OfficialPrivate

200

120

160

80

40

01983 1985 19891987 1991 1993 19971995 20011999

Fig. 1.5: Governments shed state-owned enterprises

Source: Megginson et al. (2004)

Global privatization receipts, in billions of USD

13UBS research focus March 2009

Reversals of fortuneReversals of fortune

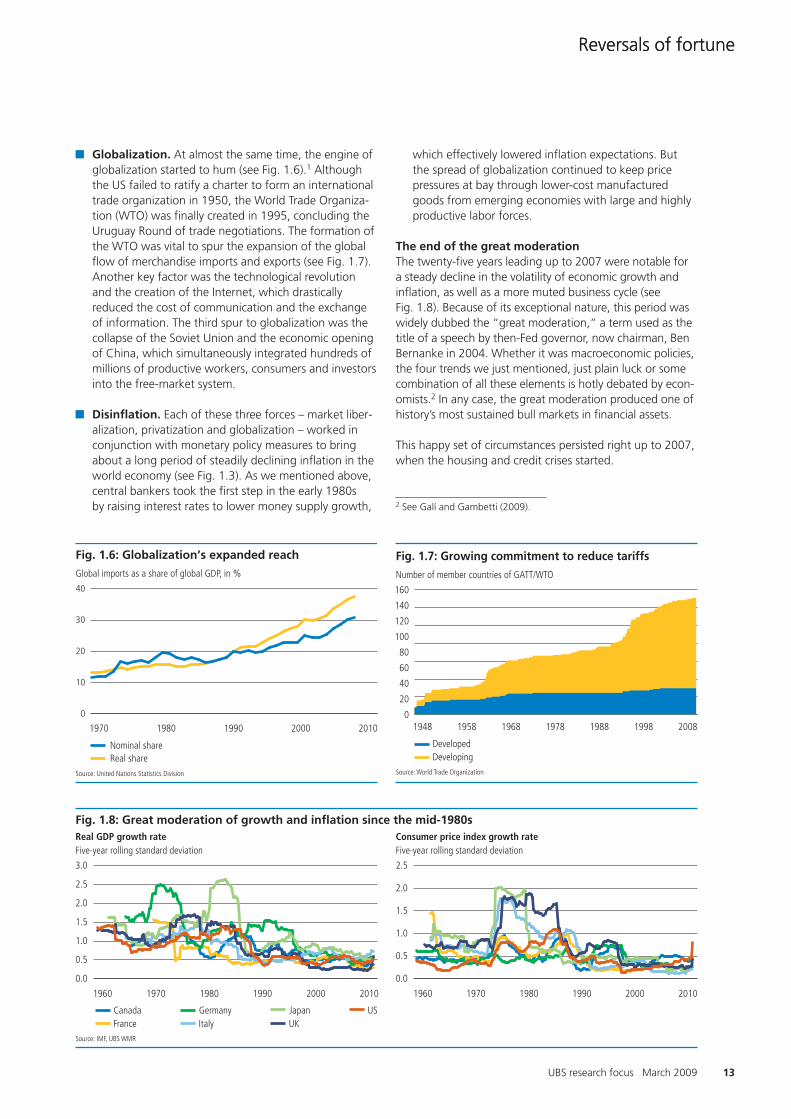

� Globalization. At almost the same time, the engine ofglobalization started to hum (see Fig. 1.6).1 Althoughthe US failed to ratify a charter to form an internationaltrade organization in 1950, the World Trade Organiza-tion (WTO) was finally created in 1995, concluding theUruguay Round of trade negotiations. The formation ofthe WTO was vital to spur the expansion of the globalflow of merchandise imports and exports (see Fig. 1.7).Another key factor was the technological revolutionand the creation of the Internet, which drasticallyreduced the cost of communication and the exchangeof information. The third spur to globalization was thecollapse of the Soviet Union and the economic openingof China, which simultaneously integrated hundreds ofmillions of productive workers, consumers and investorsinto the free-market system.

� Disinflation. Each of these three forces – market liber-alization, privatization and globalization – worked inconjunction with monetary policy measures to bringabout a long period of steadily declining inflation in theworld economy (see Fig. 1.3). As we mentioned above,central bankers took the first step in the early 1980s by raising interest rates to lower money supply growth,

which effectively lowered inflation expectations. But the spread of globalization continued to keep pricepressures at bay through lower-cost manufacturedgoods from emerging economies with large and highlyproductive labor forces.

The end of the great moderationThe twenty-five years leading up to 2007 were notable for a steady decline in the volatility of economic growth andinflation, as well as a more muted business cycle (see Fig. 1.8). Because of its exceptional nature, this period waswidely dubbed the “great moderation,“ a term used as thetitle of a speech by then-Fed governor, now chairman, BenBernanke in 2004. Whether it was macroeconomic policies,the four trends we just mentioned, just plain luck or somecombination of all these elements is hotly debated by econ-omists.2 In any case, the great moderation produced one ofhistory’s most sustained bull markets in financial assets.

This happy set of circumstances persisted right up to 2007,when the housing and credit crises started.

40

10

20

30

0

1970 1980 1990 2000 2010

Fig. 1.6: Globalization’s expanded reach

Source: United Nations Statistics Division

Global imports as a share of global GDP, in %

Real shareNominal share

160

140

100

120

80

60

20

40

019581948 1968 19881978 20081998

Fig. 1.7: Growing commitment to reduce tariffs

Source: World Trade Organization

Number of member countries of GATT/WTO

DevelopedDeveloping

1960 1970 19901980 2000 2010 1960 1970 19901980 2000 2010

Fig. 1.8: Great moderation of growth and inflation since the mid-1980s

Source: IMF, UBS WMR

Real GDP growth rateFive-year rolling standard deviation Five-year rolling standard deviation

GermanyFranceCanada

ItalyJapanUK

US

Consumer price index growth rate

3.0

1.0

2.0

2.5

1.5

0.5

0.0

2.5

1.0

2.0

1.5

0.5

0.0

2 See Galí and Gambetti (2009).

14 The financial crisis and its aftermath

Chapter 1

The financial crisis: an array of factors

There is no single catalyst that triggered the present financialcrisis (see box on page 16). Rather, it took a wide array ofinstitutions and innovations to bring about the demise of thefinancial system as we knew it over the past quarter century.Considered in isolation, each individual factor seemed capa-ble of having only a marginal impact on markets, but in com-bination they have had a near lethal effect on the globalfinancial system. We examine some of the principal causes ofthe financial crisis with an eye to understanding how this willimpact the structural make-up of financial markets in future.

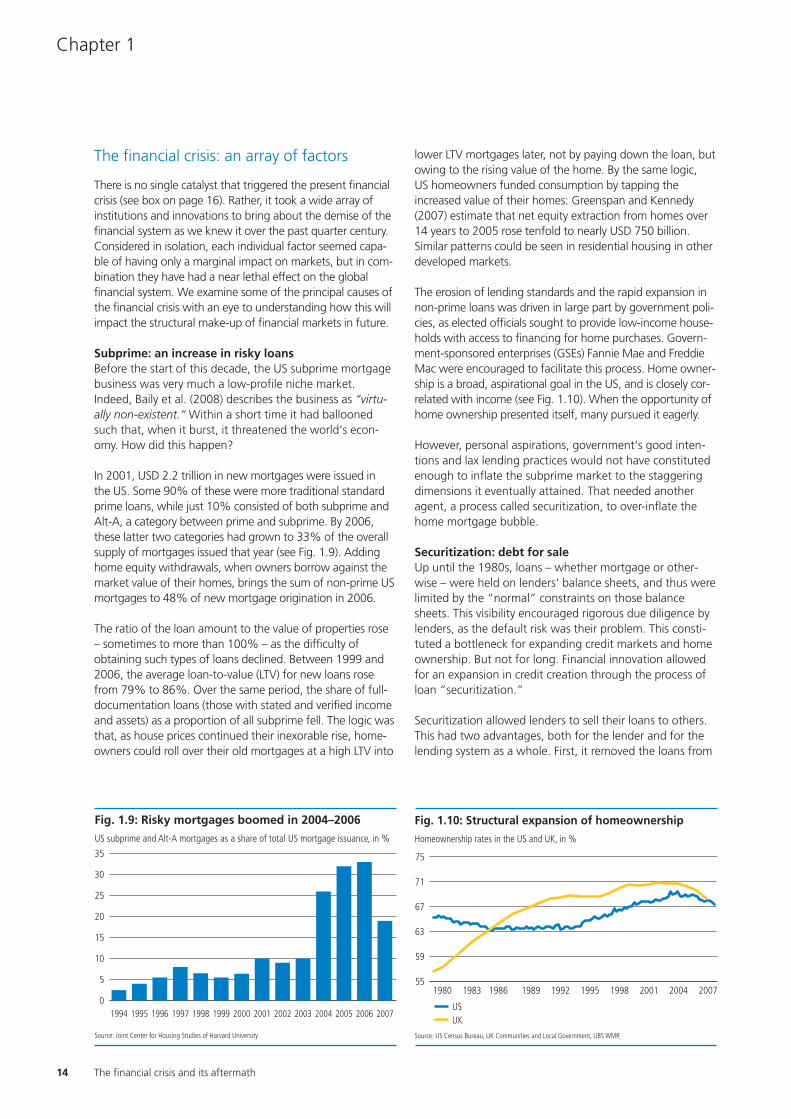

Subprime: an increase in risky loansBefore the start of this decade, the US subprime mortgagebusiness was very much a low-profile niche market.Indeed, Baily et al. (2008) describes the business as “virtu-ally non-existent.“ Within a short time it had balloonedsuch that, when it burst, it threatened the world‘s econ-omy. How did this happen?

In 2001, USD 2.2 trillion in new mortgages were issued in the US. Some 90% of these were more traditional standardprime loans, while just 10% consisted of both subprime andAlt-A, a category between prime and subprime. By 2006,these latter two categories had grown to 33% of the overallsupply of mortgages issued that year (see Fig. 1.9). Addinghome equity withdrawals, when owners borrow against themarket value of their homes, brings the sum of non-prime USmortgages to 48% of new mortgage origination in 2006.

The ratio of the loan amount to the value of properties rose– sometimes to more than 100% – as the difficulty ofobtaining such types of loans declined. Between 1999 and2006, the average loan-to-value (LTV) for new loans rosefrom 79% to 86%. Over the same period, the share of full-documentation loans (those with stated and verified incomeand assets) as a proportion of all subprime fell. The logic wasthat, as house prices continued their inexorable rise, home-owners could roll over their old mortgages at a high LTV into

lower LTV mortgages later, not by paying down the loan, butowing to the rising value of the home. By the same logic, US homeowners funded consumption by tapping theincreased value of their homes: Greenspan and Kennedy(2007) estimate that net equity extraction from homes over14 years to 2005 rose tenfold to nearly USD 750 billion. Similar patterns could be seen in residential housing in otherdeveloped markets.

The erosion of lending standards and the rapid expansion innon-prime loans was driven in large part by government poli-cies, as elected officials sought to provide low-income house-holds with access to financing for home purchases. Govern-ment-sponsored enterprises (GSEs) Fannie Mae and FreddieMac were encouraged to facilitate this process. Home owner-ship is a broad, aspirational goal in the US, and is closely cor-related with income (see Fig. 1.10). When the opportunity ofhome ownership presented itself, many pursued it eagerly.

However, personal aspirations, government‘s good inten-tions and lax lending practices would not have constitutedenough to inflate the subprime market to the staggeringdimensions it eventually attained. That needed anotheragent, a process called securitization, to over-inflate thehome mortgage bubble.

Securitization: debt for saleUp until the 1980s, loans – whether mortgage or other-wise – were held on lenders‘ balance sheets, and thus werelimited by the “normal” constraints on those balancesheets. This visibility encouraged rigorous due diligence bylenders, as the default risk was their problem. This consti-tuted a bottleneck for expanding credit markets and homeownership. But not for long. Financial innovation allowedfor an expansion in credit creation through the process ofloan “securitization.”

Securitization allowed lenders to sell their loans to others.This had two advantages, both for the lender and for thelending system as a whole. First, it removed the loans from

35

25

30

20

15

10

5

020012000199919981997199619951994 20032002 2004 2005 20072006

Fig. 1.9: Risky mortgages boomed in 2004–2006

Source: Joint Center for Housing Studies of Harvard University

US subprime and Alt-A mortgages as a share of total US mortgage issuance, in %

75

71

67

59

63

551980 1983 19891986 1992 1995 2004 200720011998

Fig. 1.10: Structural expansion of homeownership

Homeownership rates in the US and UK, in %

Source: US Census Bureau, UK Communities and Local Government, UBS WMR

USUK

15UBS research focus March 2009

Reversals of fortune

lenders’ balance sheets, which in turn allowed them toextend many more loans. Second, in exchange for the rev-enue stream from those loans, securitization spread therisk to market participants who were most prepared totake it. The immediate effect was to increase the supply ofloans and – in theory, at least – increase market trans-parency and efficiency. But securitization also had a funda-mental disadvantage when compared to the previousapproach: the originators of the loans no longer bore thefull risk, and, inevitably, their interest in assuring the qualityof the loans they issued waned. Securitization encouragedlenders to lend, which in turn fanned the borrowing binge.

Individual loans were initially packaged together as mort-gage-backed securities (MBSs) and sold on to investors.Freddie Mac produced the first MBS in 1983. With theseinstruments, the payment streams on the pools of mort-gages were “passed through” to investors. Risk was splitbetween the MBS purchaser, who was exposed to interestrate and prepayment risks, and the issuing government-sponsored enterprises (GSE), which guaranteed the MBSand thus retained the default risk on the underlying mort-gages. Over time, the private sector entered the MBSissuance game, eventually constituting the majority of thenew issue market. MBSs issued by private-sector financialinstitutions were generally not guaranteed and most weremade up of non-conforming mortgages, and increasinglythe Alt-A and subprime segments.

Over time, the securitization process became increasinglycomplex, as these “pass-through” securities were thenrepackaged into other types of instruments known as col-lateralized mortgage obligations (CMO). Within a CMO,the pass-through income streams that investors receivefrom private-sector MBS were also carved up into differentclasses or “tranches.” Rather than providing equal pro-ratadisbursement of cash flows to all bond holders, the CMOallowed the cash flows to be segregated by targeting thereturns of principal by tranche holder. All principal repay-ments were initially targeted to shorter-dated tranches,intermediate- and longer-term tranches had principalreturn deferred. This allowed for the creation of MBS withdifferent effective maturity profiles from the existing pass-through securities (see Fig. 1.11).

CDOs: more than the sum of their parts?The next link in the chain formed when MBS become sub-sumed within collateralized debt obligations (CDO). CDOscan resemble MBSs, except that CDOs contain bonds andother assets. They combine different tranches of MBSstogether with other asset-backed securities; for instance,credit card, student, car or business loans. As with mort-gage-backed securities, these were divided into differenttranches: senior, mezzanine and equity. Over ten years to2006, annual CDO issuance went from virtually nil to morethan USD 500 billion (see Fig. 1.12). This in turn provided ahuge source of funding for the subprime market, furtherstimulating demand. By combining apparently uncorrelateddebt, the perceived risk profile of these CDOs was judgedto be lower than their individual parts.

Fig. 1.11: Different risk and return for different investors

Source: Baily et al (2008), UBS WMR

First loss

Last loss Lowest risk

Lowerexpected

yield

Higherexpected

yield

Highestrisk

Pool ofmortgageloans

SeniorEquity

Individualmortgages

Mezzanine

AAA/Aaa

AA/Aa

A/A

BBB/Baa

BB/Ba

B/B

unrated

600

400

500

300

200

100

02000 2001 20032002 2004 2005 20072006 2008

Fig. 1.12: Securitization jumps to half a trillion in 2006

Source: Securities Industry and Financial Markets Association

Annual CDO issuance, in billions of USD

As household and corporate imbalances beginto fade, another one, this time on the balancesheets of governments, is set to grow.

16 The financial crisis and its aftermath

Chapter 1

Crisis timeline: how it all unraveled

Source: Bloomberg, Factiva, MSCI, UBS WMR

1800

1400

1600

1200

1000

800

600Dec 06 Mar 07 Sept 07Jun 07 Dec 07 Mar 08 Sept 08Jun 08 Dec 08 Mar 09

1 2 43

5

6

78

910

1112

13

1418

16

22

1721

19

20

15

23

24

25

27

26

28

2930

31

32

33

34

Fig. 1.13: Timeline of the financial crisis

MSCI world equity market index

1. December 28, 2006Ownit Mortgage Solutions, which described itself as a leading lender to homeowners withweak credit or none at all, closes on 6 December and files for bankruptcy on 28 December.

2. February 7, 2007HSBC Holdings announces a bigger charge than expected for bad debt in its USsubprime portfolio, likely to exceed USD 10.5 billion for 2006.

3. February 27, 2007Freddie Mac announces it will no longer buy the riskiest subprime mortgages andmortgage-related securities.

4. April 2, 2007The second-biggest subprime mortgage lender in the US, New Century Financial, filesfor Chapter 11 bankruptcy protection.

5. July 31, 2007Bear Stearns’ two hedge funds investing in mortgage-backed securities file for Chapter15 bankruptcy protection after collapsing in mid-July.

6. August 2, 2007German bank IKB Deutsche has to be bailed out due to troubles from its exposure toUS subprime loans.

7. August 6, 2007American Home Mortgage Investment Corporation files for Chapter 11.

8. August 9, 2007The amount of ABCP outstanding falls, signaling a seizure of credit markets.

9. August 17, 2007Countrywide, the biggest mortgage lender in the US, is forced to draw on its entireUSD 11.5 billion line of credit, and its debt is downgraded to just a notch above junk.

10. December 13, 2007Citigroup brings USD 49 billion in distressed assets onto its balance sheet.

11. January 11, 2008Bank of America announces that it will purchase Countrywide in a transaction worthabout USD 4 billion.

12. March 21, 2008The Fed announces that it will provide term financing to facilitate JPMorgan Chase’s acquisition of Bear Stearns.

13. July 15, 2008The SEC issues an emergency order temporarily prohibiting “naked” short selling in thesecurities of Fannie Mae, Freddie Mac, and Wall Street’s primary dealers.

14. July 30, 2008The Housing and Economic Recovery Act is passed. It authorizes the Treasury topurchase GSE obligations and reforms regulatory supervision of the GSEs.

15. September 7, 2008Fannie Mae and Freddie Mac enter US government conservatorship.

16. September 15, 2008Bank of America announces its intent to purchase Merrill Lynch for USD 50 billion.Lehman Brothers files for Chapter 11.

17. September 17, 2008The SEC announces an emergency ban on the short selling of stocks of all companiesin the financial sector.

18. September 21, 2008The Fed approves the applications of investment banks Goldman Sachs and Morgan Stanley to become bank holding companies.

19. September 25, 2008The Office of Thrift Supervision closes Washington Mutual Bank; JPMorgan Chaseacquires WaMu’s banking operations.

20. September 29, 2008Bradford & Bingley becomes the second British bank to be nationalized.

21. First week of October, 2008Iceland’s banks collapse; the IMF extends USD 2.1 billion loan a month later.

22. October 8, 2008The UK launches its first bank bailout, making GBP 500 billion available.

23. October 12, 2008The Fed approves the acquisition of Wachovia by Wells Fargo.

24. October 14, 2008The US Treasury Department announces the Troubled Asset Relief Program (TARP) thatwill purchase capital in financial institutions, making USD 250 billion available.

25. November 10, 2008The Fed and the US Treasury announce restructuring of the government’s financialsupport of AIG, with Treasury to purchase USD 40 billion of AIG preferred shares underthe TARP.

26. November 12, 2008The US Treasury decides not to use TARP funds to purchase illiquid mortgage-relatedassets from financial institutions.

27. November 18, 2008Executives of Ford, General Motors, and Chrysler testify before Congress, requestingaccess to the TARP for federal loans.

28. November 23, 2008The US Treasury, Fed and FDIC announce an agreement with Citigroup to provide apackage of guarantees, liquidity access, and capital.

29. November 25, 2008The Fed announces the creation of the Term Asset-Backed Securities Lending Facility(TALF), under which the Fed will lend up to USD 200 billion on a non-recourse basis toholders of AAA-rated asset-backed securities and recently originated consumer andsmall business loans.

30. December 19, 2008The US Treasury Department authorizes loans of up to USD 13.4 billion for GeneralMotors and USD 4.0 billion for Chrysler from the TARP.

31. January 16, 2009The Treasury, Fed, and FDIC announce a package of guarantees, liquidity access andcapital for Bank of America.

32. January 28, 2009US House of Representatives passes a USD 819 billion stimulus package, which is laterreduced to USD 787 billion during Congressional reconciliation.

33. February 10, 2009US Treasury Secretary Timothy Geithner announces a Financial Stability Plan involvingTreasury purchases of convertible preferred stock in eligible banks, the creation of afund to acquire troubled loans and other assets from financial institutions, expansionof the Fed’s TALF, and initiatives to stem residential mortgage foreclosures and tosupport small business lending. -and- The Fed says that is prepared to expand the TALF to as much as USD 1 trillion,supported by USD 100 billion from the TARP.

34. February 18, 2009President Obama announces the Homeowner Affordability & Stability Plan, whichpermits the refinancing of conforming home mortgages owned or guaranteed byFannie Mae or Freddie Mac that currently exceed 80% of the value of the underlyinghome.

Sequence of events

17UBS research focus March 2009

Reversals of fortune

Ratings agencies: financial alchemyGrowth in CDO issuance received a huge boost from theratings agencies that were assumed to be accurately moni-toring the default risk in the underlying pools of assets.With an assigned triple-A rating, investors and lenders fac-ing low yields on credit instruments were more willing toignore some of the underlying risks and implicitly acceptthe ratings agencies’ guidance.

This leap of logic (or faith) meant that the income stream of aCDO assigned a AAA credit quality by rating agencies couldflow from junior-rated securities. The underestimation of riskturned out to have been partly because the ratings agencies’default estimates only considered data from the early 1990sonwards, a period when defaults were historically low, andalso because the estimates assumed a low probability of anationwide downturn in the US housing market.

Transformed from MBSs to CDOs, subprime mortgagedebt thus morphed into AAA-rated securities. But sub-prime debt retained the risks inherent in its name. Thesewere merely hidden in their new guise as CDOs, but theirrisk was unchanged. And many of the MBSs and CDOsthat were not granted the highest rating by the credit rat-ings found their way to triple-A status anyway through theprovision of credit insurance. “Monoline” insurers, whosetraditional mainstay had been offering default insuranceon US municipal bonds, extended their business into insur-ing securitized assets using credit default swaps (CDSs) toremove the default risk.

SIV: off balance sheet risksBanks and other financial institutions were limited in termsof how much of these securitized assets they could hold ontheir balance sheets. After all, they must meet requiredminimum capital requirements in the form of shareholder’sequity and retained earnings, which limits their profitabilityand the degree to which they can employ leverage. In anincreasingly competitive business environment, financialinstitutions sought ways of circumventing the restrictions

placed on their operations by regulators in order toincrease the return on capital. This opened the door for theuse of off-balance-sheet financing mechanisms.

In this case, the masterstroke involved shifting debt-basedassets such as CDOs into off-balance-sheet entities thatwere called structured investment vehicles (SIV), thus tech-nically separating these assets from the banks. This circum-vented banks’ capital requirements, enabling a higherdegree of gearing (debt) than regulations would allow foron-balance-sheet holdings. These assets were bought byissuing short-term debt in the form of asset-backed com-mercial paper (ABCP). This conduit served to expand thepool of funding for off balance debt, and encouragedbanks to increase their leverage.

Short-term ABCP issuance – with a maturity between oneand four days – climbed evermore steeply between early2004 and their peak in 2007. In contrast, the issuance ofpaper with maturities of 21 days and more remained fairlyflat over this period. This led to what has been termed a“maturity mismatch:“ short-term financing of long-termliabilities. Baily et al. (2008) estimate that by 2007, “invest-ment banks were rolling over liabilities equal to one quar-ter of their balance sheets overnight.” This system workedas long as liquidity flowed.

7

6

4

5

3

2

1

019941990 1998 2002 20102006

Fig. 1.14: Global central bank reserves skyrocket

Source: Bloomberg, IMF

Foreign exchange reserves held at central banks, in trillions of USD

Rest of the worldChina

JapanRussia

Taiwan KoreaIndia

6

5

4

7

1

2

3

0

1970 1980 1990 2000 2010

Fig. 1.15: Large global imbalances in trade and capital flows

Source: IMF World Economic Outlook October 2008

Absolute sum of current account balances as a share of world GDP, in %

3 See, in particular, the UBS research focus entitled, “Currencies: a deli-cate imbalance“ (March 2008) and the UBS global outlook from January2006. In the latter, we wrote: “US consumption, the only real enginedriving global growth, could be on the verge of faltering. The incomestream generated by the rise in the price of private residential property islikely to run dry in the near future. Savings activity has also plunged intonegative territory, which means that consumption is partly beingfinanced by debt. This not only applies to the average private US house-hold; the whole of the United States is financing a portion of its currentexpenditure abroad via a sizeable current account deficit.... Even Asia,the world’s most dynamic region, will be unable to decouple from theslowdown in the US economy despite the increase in intra-Asian trade.”

18 The financial crisis and its aftermath

Chapter 1

25

15

20

10

5

02004200320022001200019991998 2005 20072006 20092008

Fig. 1.17: Borderline borrowers suddenly unable to repay

Source: Mortgage Bankers Association

Conventional subprime mortgage payments past due, in %

160

100

140

120

80

60

401999 2000 20022001 2003 2004 2005

Fig. 1.16: High leverage coincides with housing bubbles

Source: Banco de España, Datastream, Eurostat, IMF staff estimates

Ratio of household debt to gross disposable income, in %

GermanyFranceEurozone

SpainUKUS

Governments: supercharging the Western consumerWhere did all this money come from? Over the past threeyears, we have been drawing attention to the dangersinvolved in the increasingly delicate imbalances in interna-tional trade and capital flows (see Fig. 1.14 & 1.15).3

Countries including China, Germany and Japan producedmore than they consumed as their economies grewincreasingly dependent on exports to heavy-spendingcountries such as the UK, Spain – and, of course, the US.The resultant excess savings among the prudent wereexported to the spendthrifts to fund their consumption.

These capital flows helped, in part, to inflate huge assetprice bubbles in the spending nations, which in turn werefuelled by debt (see Fig. 1.16). As the theory goes, the“global savings glut” lowered bond yields in the spendingcountries compared to where they might otherwise havebeen. Lower yields, reflected through lower borrowingcosts, stimulated borrowing. They also lowered the discountrate, which raised the value of fixed assets such as homes,which then fueled even more borrowing, such as homeequity release plans and the ever-more inventive mortgageproducts designed to tempt the would-be homeowner.

This spiral was further exacerbated by an extended periodof loose monetary policy after the Tech bubble bust andthe September 11 terrorist attacks. In fairness, this loose-money approach seemed a low-risk path at the time giventhe disinflationary effect of globalization. But in dodgingthe potential deflationary effects of the burst Tech bubbleat the start of this decade, the Fed unwittingly stoked thehousing frenzy and the credit explosion that fed it.

When the music stoppedIn a world of rising asset prices, the credit spiral is not a problem. However, when asset prices stopped rising, the entire construct was threatened with collapse, trig-gered by rising delinquencies in the US subprime market (see Fig. 1.17).

The financial crisis was ultimately caused by a deterioration infundamentals – house prices eventually succumbed to eco-nomic gravity in the wake of rising interest rates and highenergy prices. The dominoes fell (see box on page 20). Withdebt dereliction rising, and mortgage defaults leading thepack, the value of financial instruments tied either directly orindirectly to leverage, such as CDOs, MBSs, and CDSs,became increasingly worrisome. The short-term financingthat had sustained the SIVs stocked with CDOs and MBSshad dried up. Banks became reluctant to lend to counterpar-ties because they did not know their default risk. Ultimately,credit, which had oiled the wheels of commerce, had evapo-rated. The conditions that, for a quarter of a century, hadallowed both individuals and institutions to add leveragewith impunity had shifted in a sudden and violent manner.

Pendulum swings toward the state

The bull market of the 1980s and 1990s was not immune tosevere corrections and crises. Despite the great moderationin growth and inflation, large market gyrations seemed tooccur with greater frequency. From Greenspan’s definingmoment, the stock market crash of 1987, to the currentcredit crisis, the last twenty-five years have been marked bya series of extreme market events: the US savings and loancrisis, the real estate bubbles and subsequent busts inEurope and Japan in the early 1990s, the currency crisis inEurope in 1992, the Mexican crisis, the Asian crisis, the Russ-ian crisis, the implosion of Long-Term Capital Management,and the bursting of the Tech bubble all come to mind.

So far, governments and their central banks have inter-vened on two fronts: stabilizing and in some cases nation-alizing their crippled financial sectors, and using fiscal andmonetary policy tools to counter the resulting recessions.In our view, it is reasonable to assume that they will extendtheir reach in future as they struggle to revive theirwounded economies (see box on page 19).

19UBS research focus March 2009

Reversals of fortune

There is a certain inescapable logic to the notion that theone who pays has the right to decide. Thus, re-regulationof the financial market and financial intermediaries isinevitable, in our view. In the UK and the US, the toughquestioning of the most senior bankers presages a roughinstitutional environment for the industry.

There is also a large and growing consensus among thebroader public and policymakers that central banks ingeneral – and the Fed in particular – made tactical errorsleading up to the financial crisis. By keeping interest ratestoo low for too long after the Tech bubble burst, the Fedmay have fuelled the housing bubble and, therefore,shares at least some responsibility for the current crisis.

Moreover, the role of central banks as guarantors andsupervisors of the financial system is also now in question.

But the main problem that governments will have totackle once the financial crisis is passed and the recessionovercome is to control the potential damage from theflood of liquidity and a massive increase in public debtthat will accompany the rescue packages. As one set ofimbalances begins to fade, another one, this time on thebalance sheets of governments, is set to grow. Just howgovernments will make their presence felt in financialmarkets – operationally and strategically, short-term andlong – is the subject of the balance of our study.

The state versus the market

Debates over regulation and government involvement infinancial markets often cite the dispute between the twoeconomics giants of the twentieth century, John MaynardKeynes and Friedrich von Hayek. While Hayek championedthe wisdom of market forces, Keynes saw the need for government intervention. In his The General Theory ofEmployment, Interest and Money, Keynes stressed the “vitalimportance of establishing certain central controls in matterswhich are now left in the main to individual initiative.“This view is enjoying a currency that it has not seen for30 years. With markets in disarray and with so much wealthdestroyed, the era of unfettered markets appears to be over.

Many voices today point to the failure of private markets asevidence of the need for greater government involvement.They argue that the crisis is in part due to what economistscall the “asymmetric information“ of buyers and sellers. Intheory, in efficient markets all information is reflected inprices. But do buyer and seller have the same informationlevels, for instance, with a secondhand car? The next timeyou walk onto a car dealer’s lot, would you be satisfiedwith the dealer’s handshake only, or would you want tofeel that the law backed you up in the event that the caryou bought was not what you thought?

Applied to the current crisis, some argue that the subprimemarket collapsed because the buyers of subprime mort-gages were badly informed about the underlying quality ofthe houses and the respective securitized loans. Credit rat-ings overstated the reliability of the income from thesemortgages, so demand for these investments exceededsustainable levels. This laid the foundation for the crisis.The breakdown in interbank lending points to the sameproblem, as individual banks started to doubt the creditquality and solvency of counterparties.

It can also be argued that state involvement is necessary ifprivate activity has public effects, for example, if a privatecompany causes environmental pollution. Regulatory activitycan address this through taxes, fines or environmental regula-tion. Well-functioning banks normally have positive externaleffects: banks have traditionally been the hub of moderneconomic activity, which is based on paper money and credit.When banks fail, the negative external effects are huge andsocieties look to governments to repair the damage.

Government intervention in commerce may also havesocial aims, for example, to redistribute income or extendhealthcare services or educational opportunities. Whengovernments become shareholders, they have the power,for example, to influence bonuses and benefits towards amore socially equitable distribution than might result fromfree-market values.

Other voices argue that governments cannot have suffi-cient information to operate efficiently. People make theirpreferences felt through the market. To believe that gov-ernment can do a better job satisfying people’s needs, sayfree-market advocates, one must believe that governmentsknow what individuals want better than the individualsthemselves. And the consequences of this belief system arewhat Hayek warned about in The Road to Serfdom. Thetitle says it all. What is more, government officials are vul-nerable to the lobbying of private interest groups, againgiving rise to skewed outcomes.

The interdependencies between regulation and markets arecomplex. There are valuable insights in both viewpoints.Our intention here is to outline these positions rather thantake sides. What is certain, however, is that those advocat-ing increased regulation are now setting the agenda. Andthe concrete consequences of this sea change will pro-foundly influence the investment environment.

20 The financial crisis and its aftermath

Chapter 1

Lost wealth

Barely a week passes without news of another unprece-dented loss in financial markets. Indeed, “unprecedented”became one of the most overused words of 2008. But justhow much has been lost? And what do these cash valuesmean in practical terms?

There have been some quite stunning numbers tossedaround in the media. In early 2009, respected individualsand institutions have estimated that the crisis has led tototal wealth destruction of between 16% and 40% fromthe peaks in equity and real estate markets. And few areasserting that we have reached bottom yet. An IMF studyof crises (Claessens et al., 2008) estimated that a creditcrunch episode typically lasts two and a half years, withnearly a 20% decline in credit, while a housing busttended to last four and a half years, with a 30% fall in real(inflation-adjusted) house prices.

Focusing on losses in equity and real estate markets todate, data is so thin and dispersed on the actual size andcomposition of global wealth that it is difficult to establisha measure with any real confidence. However, the UN(Davies et al., 2008) estimates that global wealthamounted to some USD 125 trillion in 2000. We calculatethat about USD 53 trillion was accounted for by equities,with the remainder in property, both residential and com-mercial. The exact split is not known.

However, the global value of equities grew by about USD9.5 trillion between the height of the Tech bubble inMarch 2000 and the market peak of October 2007, about17.5%. Property markets vary enormously from country tocountry, and between commercial and residential. Fromthe start of this decade to the market peak, both US andUK markets more than doubled, although these areextreme examples. Global listed real estate more thandoubled in the three years to the market peak in February2007. Then, too, we have surging commodity prices overthe same period. So, conservatively, we think we can pin avalue of USD 150 trillion on global wealth by 2007. Withthis established, we can attempt to determine how muchhas evaporated since.

EquitiesOver the course of the crisis, the capitalization of the USmarket slid from USD 19.1 trillion at its October 2007peak to USD 9.2 trillion in late February 2009; a nearlyUSD 10 trillion destruction. The market cap of the TokyoStock Exchange fell from JPY 578 trillion at its June 2007high point to JPY 244 trillion in February 2009, or down58%. A similar Bloomberg series for world market capital-ization went from USD 63 trillion to USD 28 trillion – aloss of USD 35 trillion, or a 56% fall (see Fig. 1.18).

70

50

60

40

30

202004 2005 20072006 20092008

Fig. 1.18: Value destruction in equity markets

Source: Bloomberg

Estimated world market capitalization, in trillions of USD

21UBS research focus March 2009

Reversals of fortune

4 Space limitations force us to oversimplify. The important thing to notewith declining housing values is not the headline figure. That yourhouse has a lower price today than it did a month ago is not in itselfsignificant; but the fact that rising residential values had boosted con-sumption is. Meanwhile, tighter lending standards and greater eco-nomic uncertainty also constrain demand. We examine past housingcrises and their implications for the current one in an Education Noteentitled, “Crawling from the rubble,” from 26 September 2008, and in an Investment Theme “Home is where the heartache is,” from11 February 2009.

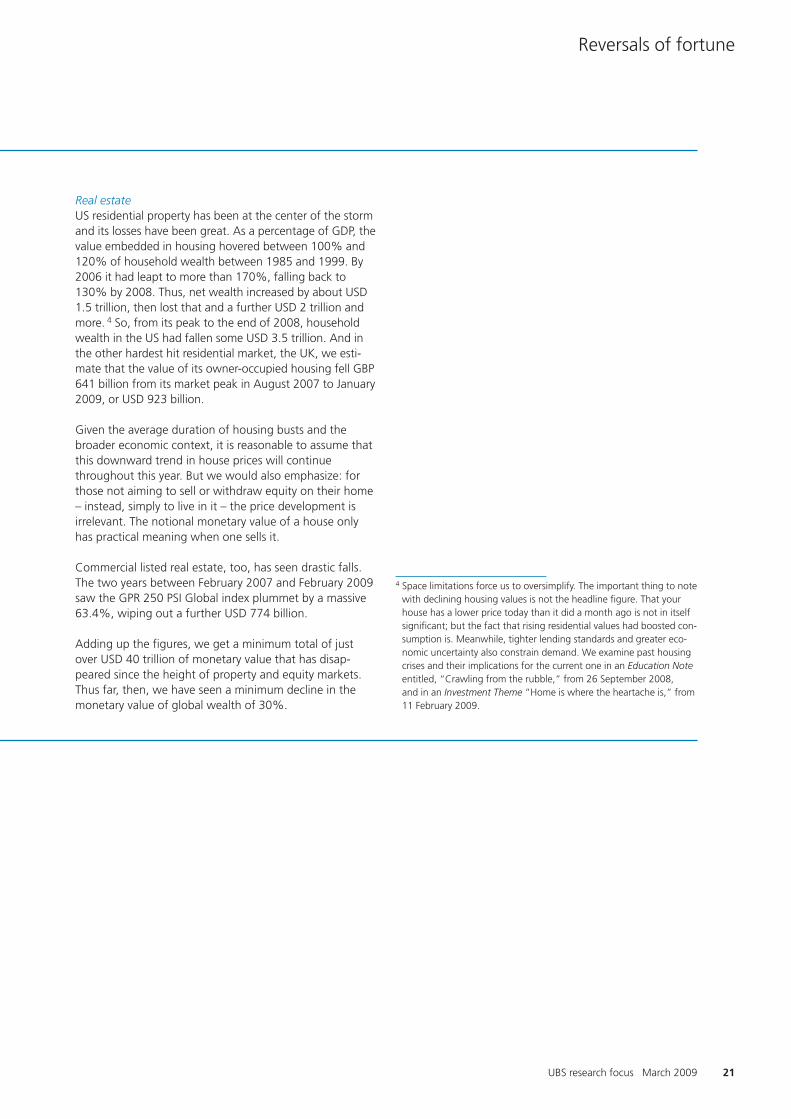

Real estateUS residential property has been at the center of the stormand its losses have been great. As a percentage of GDP, thevalue embedded in housing hovered between 100% and120% of household wealth between 1985 and 1999. By2006 it had leapt to more than 170%, falling back to130% by 2008. Thus, net wealth increased by about USD1.5 trillion, then lost that and a further USD 2 trillion andmore. 4 So, from its peak to the end of 2008, householdwealth in the US had fallen some USD 3.5 trillion. And inthe other hardest hit residential market, the UK, we esti-mate that the value of its owner-occupied housing fell GBP641 billion from its market peak in August 2007 to January2009, or USD 923 billion.

Given the average duration of housing busts and thebroader economic context, it is reasonable to assume thatthis downward trend in house prices will continuethroughout this year. But we would also emphasize: forthose not aiming to sell or withdraw equity on their home– instead, simply to live in it – the price development isirrelevant. The notional monetary value of a house onlyhas practical meaning when one sells it.

Commercial listed real estate, too, has seen drastic falls.The two years between February 2007 and February 2009saw the GPR 250 PSI Global index plummet by a massive63.4%, wiping out a further USD 774 billion.

Adding up the figures, we get a minimum total of justover USD 40 trillion of monetary value that has disap-peared since the height of property and equity markets.Thus far, then, we have seen a minimum decline in themonetary value of global wealth of 30%.

The rise of even bigger governmentChapter 2

24

Chapter 2

The financial crisis and its aftermath

The rise of even bigger government

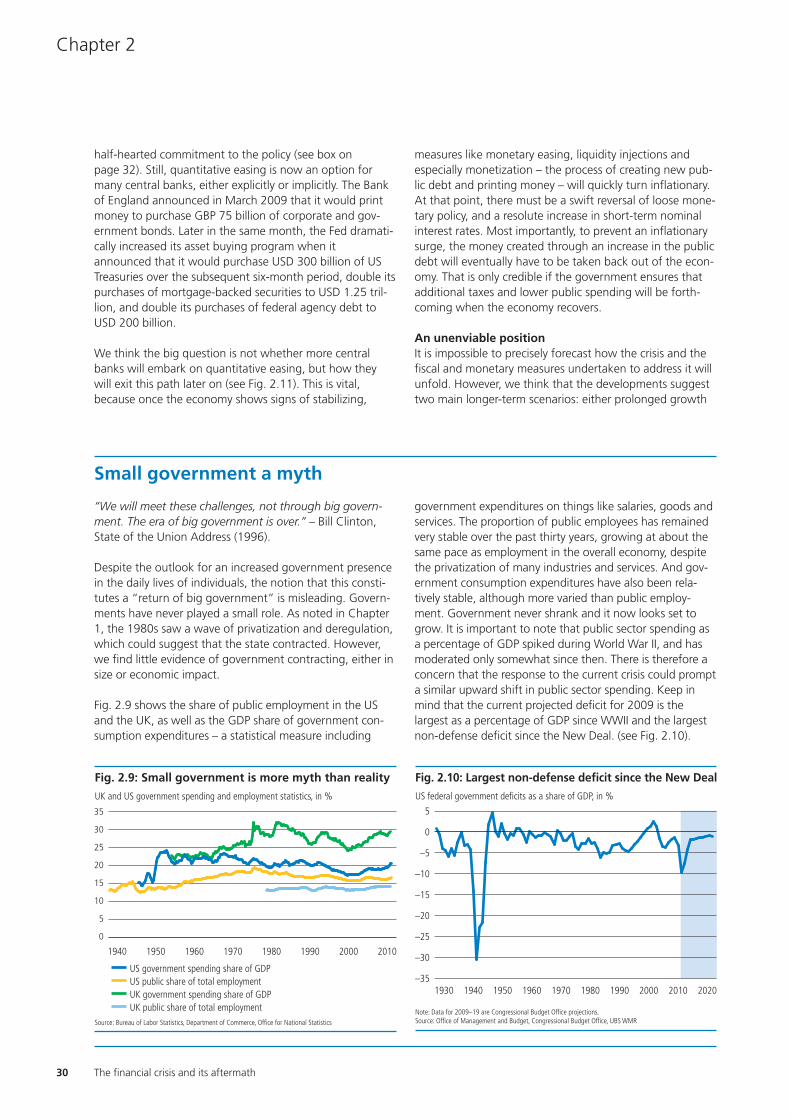

Governments are unveiling mammoth fiscal stimulus packages and, at thesame time, preparing to impose far sharper regulatory oversight upon thefinancial industry. Even during the era of small government, the state never really shrank, which suggests many of these changes are here to stay.

The new financial handbook

The policy response to the financial crisis began modestly,with a few half-point interest rate cuts in the US in Sep-tember 2007 (see Fig. 2.1). This was nothing new for theFederal Reserve, which had launched its 2001 rate-cuttingcampaign with a succession of 50 basis point rate reduc-tions amid the implosion of the Tech bubble. In August2007, when the first evidence of a wider subprime crisisbegan to emerge, the Fed held two inter-meeting confer-ence calls to discuss developments, but opted to leave itsmonetary policy unchanged. Within the next year, how-ever, the US central bank would slash its fed funds rate bya total of 325 basis points, eventually trimming the targetrate nearly to zero.

Just as “zero” was acquiring almost an iconic status inglobal monetary policy, many more zeros were beingadded to the cost of bank bailouts and fiscal stimulus pack-ages. The sums under discussion were incomprehensible,even surreal for many observers as trillions replaced bil-lions. But this numerical escalation advanced steadily: fromthe USD 152 billion Housing and Economic Recovery Act inthe summer of 2008, to the USD 700 billion committed tothe Troubled Asset Relief Program (TARP), and the nearlyUSD 800 billion economic stimulus package approved inFebruary 2009. Costs directly or indirectly related to thefinancial crisis soon carried a dozen zeros.

In January 2009, the International Monetary Fund esti-mated that potential write-downs on US-originatedcredit assets could exceed USD 2.2 trillion. No surprisethen that the Federal Reserve’s balance sheet more than doubled to USD 2 trillion during the final fourmonths of 2008 (see Fig. 2.2). And estimates of the US federal deficit for fiscal year 2009 alone balloonedfrom roughly USD 215 billion in August 2007 to nearlyUSD 1.4 trillion by February 2009 (see Fig. 2.3). Accord-ing to UBS estimates when this report went to press,governments worldwide had already pledged 3.1% ofglobal GDP, or USD 2.4 trillion, to get the economy back on its feet.

Not only have mountains of money been set in motionby the financial crisis, the entire deeply shaken globalfinancial edifice – banks, markets and regulators – standsat the precipice of an extensive overhaul. In one epochalswoop, financial institutions and markets are about to beremade to meet shifting economic realities. We think thechanges will be less an about-face, and more a modera-tion of extreme positions, especially the dogmatic notionthat free markets always represent the optimal solutionto both economic and financial market problems. But wehave no doubt that governments are increasing their rolein the economic world. In the balance of this chapter, weexamine some of the ideological shifts underway, con-sider their real-world implications – especially for banks –

1985 1990 20001995 2005 2010

10

12

8

6

2

4

0

Fig. 2.1: The new US “zero” interest rate policy

Source: Federal Reserve

Fed funds target rate, in %

2003 2004 2006 20082005 20092007 2010

Fig. 2.2: Fed’s balance sheet explodes

Source: Federal Reserve

Balance sheet of the Federal Reserve, in trillions of USD

2.5

1.5

1.0

2.0

0.5

0

25

The rise of even bigger government

UBS research focus March 2009

Fiscal and monetary policy measures are crucial to combat waning demand, rising unemploymentand the looming threat of deflation.

and argue that the enlarged role of government in eco-nomic affairs is unlikely to quickly fade even after thecurrent crisis passes.

Fiscal policy: money with a mission

At its November 2008 summit in Washington, DC, leadersof the Group of 20 pledged to “use fiscal measures tostimulate domestic demand to rapid effect, as appropri-ate, while maintaining a policy framework conducive tofiscal sustainability.” Since then, many governments haveunveiled fiscal stimulus in the form of economic recoverypackages to offset the slowdown in domestic privatedemand and to boost household spending and businessinvestment. The economic stimulus measures take manyforms, including tax cuts, a tighter safety net for theunemployed and people earning low incomes, as well as spending on public infrastructure and services.

Despite these good intentions, the debate among econo-mists about whether fiscal stimulus works to revive a fal-tering economy is very much alive (see box on page 27).Those who favor government spending point out that theeconomy could otherwise enter a vicious cycle of fallingdemand and higher unemployment. Critics of governmentrescue packages usually note that deficit spending canmake matters worse in the long run and that the economyis going through a healthy and necessary adjustment tobring spending, investment and stock prices down to alevel that reflects a new lower path of long-term eco-nomic growth.

This philosophical debate over the responsibility of govern-ment in the economy is critical in informing policymakersabout their role during normal business cycle fluctuations.However, purging past excesses and imbalances built upover past decades make this downturn decidedly differentand this debate a moot one. In our view, these spendingmeasures represent crucial steps – in conjunction withmonetary policy stimulus – to turn the tide of fallingdemand, rising unemployment and looming deflation. Hadgovernments not taken strong measures during the secondhalf of 2008 to repair the dislocations in financial markets,most forms of global commerce, which were already undersevere stress, would have likely ground to a halt. With cen-tral banks having already cut short-term interest rates tohistoric lows, attention now shifts to fiscal policy to do theheavy lifting. Here, we provide a broad outline, as well as asense of the extent, the timing and the potential effective-ness of the various fiscal stimulus packages.

Stimulus packages vary widelyThe G20 countries have either adopted or are planning toadopt fiscal stimulus measures that would amount toaround 0.5% of their collective GDP in 2008, rising to1.5% in 2009, and falling slightly to 1.25% in 2010. As ashare of global GDP, the announced stimulus measuresroughly match the 2% minimum threshold that the Inter-national Monetary Fund (IMF) deemed necessary to tacklethe crisis.

The US, China and Japan have announced USD 424 billionof stimulus measures during 2009, which account for thelion’s share of the total. The US contributes nearly 40% ofthe overall stimulus in 2009, while China and Japanaccount for 13% and 10% of the total, respectively. US fis-cal stimulus in 2009 amounts to 1.9% of its 2008 GDP –somewhat higher in China at 2.1% and smaller in Japan at1.4%. For the remaining G20 economies, the fiscal stimu-lus measures are more moderate, amounting to 1.0% oftheir overall 2008 GDP.

In 2010, the US share of the total announced fiscal stimu-lus increases to over 60%; China and Germany run a dis-tant second and third, respectively. The 2010 fiscal stimu-lus in the US grows to around 2.9% of its 2008 GDP,whereas China plans to spend 2.3% and Germany 2.0%.Fiscal stimulus plans in other major economies are mini-mal. For example, new spending announced in Italy failsto exceed 0.5% of the country’s GDP. And in the UK,which is particularly hard hit by the current crisis, fiscalstimulus has so far played only a minor role. Therefore,

Fig. 2.3: Steadily upward revisions to the US deficit

Source: Congressional Budget Office

Estimates of 2009 US federal deficit in trillions of USD

1.4

1.0

0.8

0.4

0.2

1.2

0.6

0Jan 07 Sep 08Aug 07 Jan 08 Jan 09 Feb 09

26

Chapter 2

while almost every country has signed on to one form offiscal stimulus package or another, the size varies substan-tially across countries.

Composition of spending mattersBesides considerable variation in size there is also variationin the composition of the stimulus packages. Among theG20 countries, but excluding the US, about one-third ofthe stimulus is accounted for by tax cuts and the remainderby spending measures. In the US, the share devoted to taxrelief is somewhat higher (see Fig. 2.4). Some countries,including Brazil, Russia and the UK, have focused almostentirely on tax cuts. Others, including China and India,have mostly proposed spending measures.

In general, direct expenditure measures are likely to pro-duce a stronger near-term effect on economic growth thanrevenue measures, such as tax cuts. Thus, three-quarters ofthe G20 countries have announced plans to increasespending on infrastructure, largely on transportation net-works (Canada, China, France, Germany, Indonesia, Italyand the US, among others).

About half of the G20 countries have announced sizeablecuts in personal income taxes (including Canada, Germany,Indonesia, Italy, the UK and the US); while around one-thirdhave announced reductions in indirect taxes. At the sametime, about half of the G20 countries also have plans to cutcorporate income taxes (Canada, France, Germany, Indone-sia, Korea, Russia, Spain, and the US, among others).

In addition, many countries have announced plans to pro-tect credit and cash-constrained or vulnerable socialgroups, through higher unemployment benefits (Canada,Russia, the UK and US), cash transfers, (Canada, Korea,Japan), or support to children (Australia, Germany) or pen-sioners (Australia, Canada). A few G20 countries are alsostepping up support for small- and medium-sized enter-prises (Korea) and strategic or vulnerable sectors, such asconstruction (Canada), the automobile sector (Germany),

and defense and agriculture (Russia). Finally, a few coun-tries are using stimulus measures to address longer-termpolicy challenges, such as improving the quality of healthand education (Australia, China, and Saudi Arabia) orintroducing incentives for developing environmentallyfriendly technologies (Canada, China, Germany, the US).

Aim for a quick fixAt first glance, there appears to be a good deal of front-loading, meaning that most of the fiscal stimulus packagesaim for a maximum impact in 2009. Only four of the G20countries (China, Germany, Saudi Arabia and the US) planto spend as much, or even more as a share of GDP in 2010than in 2009. We should also note that some countriesrecognized the extent of the crisis early and implementedstimulus plans at some point in 2008. This list includes Aus-tralia, China, Japan, Korea, Saudi Arabia, South Africa,Spain, UK and the US.

However, a significant share of fiscal stimulus may becomeeffective only in 2010. Reasons for delay in implementingthe various programs are manifold, including the vagariesof national budget processes, diverging assessments of theduration of the recessions, or simply different stages of theelection cycles. The danger here is that a significant shareof fiscal measures become effective at the point in thebusiness cycle when economic activity has already stabi-lized, leading to the crowding-out of viable private invest-ment projects, the misallocation of resources and possiblyinflation.

Growth effects are uncertainAccording to IMF estimates, the combined fiscal stimuluscurrently planned is expected to lift G20 GDP growth in2009 by around 0.5 to 1.25 percentage points. The effectson advanced and emerging economies would be broadlysimilar. According to the IMF’s assessment, the growthimpact among the advanced economies is expected to behighest in Canada, Germany, Japan, Korea, and the US.Among the emerging economies, China, Russia, and SouthAfrica are expected to receive the most significant boost togrowth. In 2010, under current information regarding thesize of fiscal packages, the additional growth effect wouldbe minimal.

In general, we doubt that fiscal stimulus packages will havea lasting beneficial effect on economic activity. Thus, theefficacy of these packages will depend not only on thecharacteristics of the programs, but also on the conditionsprevailing in the individual countries. Past experience sug-gests that fiscal expansion is more likely to be successfulgiven the following conditions:

� Large underinvestment in infrastructure and edu-cation. Countries like Italy, Greece and Portugal wouldhave the most to gain from public investment programs.The same is true for Spain, where the government delib-erately restrained public infrastructure investment duringthe private property boom. Of the major advanced

The financial crisis and its aftermath

0 15050 100 200 250 300

Fig. 2.4: Part tax cuts and part spending

Source: White House

US fiscal stimulus by category, in billions of USD

Tax relief

Infrastructure and science

Protecting the vulnerable

Education and training

Energy

State and local fiscal relief

Healthcare

Other

27

The rise of even bigger government

UBS research focus March 2009

economies, the UK and the US would also seem to be ina position to benefit. However, under this criterion,emerging markets, such as China, would appear to be inthe best position to spend their way out of the crisis.

� Low propensity of households to save. The overallimpact of fiscal policy on aggregate demand cruciallydepends on how private-sector saving responds tochanges in fiscal policy. In principle, the effect ofincreased government spending can either be offset orreinforced by changes in private-sector saving. The crit-ical factor is the credibility of governments. If house-holds and firms are confident that the public debt bur-den will remain manageable in future, they might beinclined to spend a relatively large share of the addi-tional money they receive in the form of tax cuts. Bycontrast, if households lose confidence in governmentsand decide to increase their savings to pay for futuretax increases or reduced benefits, the fiscal expansionbecomes counterproductive. Developed countries with

adequate social safety nets may not question the gov-ernment’s credibility, whereas fiscal largess in emergingmarkets could end up bolstering already high levels ofprecautionary savings.