UAE Food and Livestock Opportunities_Honors Program Capstone Project_2012

51

Bentley University Honors Economics-Finance Program Capstone Project Developing Economic Evaluation Methods in the Gulf Focus: Food & Livestock Opportunity Nour Halabi

-

Upload

nour-halabi -

Category

Documents

-

view

49 -

download

14

Transcript of UAE Food and Livestock Opportunities_Honors Program Capstone Project_2012

Bentley University Honors Economics-Finance Program Capstone Project Developing Economic Evaluation Methods in the Gulf Focus: Food & Livestock Opportunity Nour Halabi

With current events shaping our economy into the “free market” society economists read about in their university textbooks, the reality of the matter begs the question: are we teetering on the brink of a new economic Cold War, the kind that puts competing economic systems face-to-face in a battle for global market dominance? In fact, it has been this authoritarian attitude that has led a number of governments thirsty capitalism’s economic power yet wary of uncontrolled free markets to invent a system known as state capitalism. This kind of system has opened up doors for governments to use the market’s creation of wealth in whatever political direction officials want. State capitalism can branch into the sands of Saudi Arabia where royals bask in massive oil revenues to buy domestic security and loyalty from citizens; where the Chinese government officials send state-owned firms abroad on missions seeking oil, gas, metals, and minerals in the race for global economic power over commodities; where retail supermarkets in Russia are controlled by direct orders from the prime minister which puts fiscal economics into the hands of politicians. Communism, having collapsed as a form of economic power, is revived by these fundamentals of state-owned wealth, investments, and corporations working under autocratic rule. The idea of governments dominating main domestic economic activities, and oil companies controlling three quarters of the world’s crude oil reserves translates state capitalism into meaning that state-owned companies march up the ladder of control in global markets for telecoms, shipping, power generation, petrochemicals, aviation, shipping, and more. Eventually, the governments of these countries build enormous investment funds that become vitally important sources of global capital, and the power remains mainly in their hands. Some economists will argue that state capitalism threatens the future of free-markets. Others agree that more good can come out of the country specific investments generated by the wealth of a state capitalism. Where this idea may threaten free-market’s competitive edge, it may also work to the advantage of the global economy. After the financial crisis and in spite of the looming global recession, free-market democracies have been bombarded by the skepticism of those who believe the free-market has failed. A fresh global attitude has set the foundation for new economies led by the state to set national economic performance. I set out to assess the ways in which this emerging trend could positively impact certain economies and focused on the relatively new emergence of the United Arab Emirates economy – a model of state capitalism at its finest. The United Arab Emirates has profited more handsomely as the fashionable international business hub of the Middle East than any other country in the region; the determination of politicians has allowed the ruling families to control most of the local and federal economies although financial and political rivalries

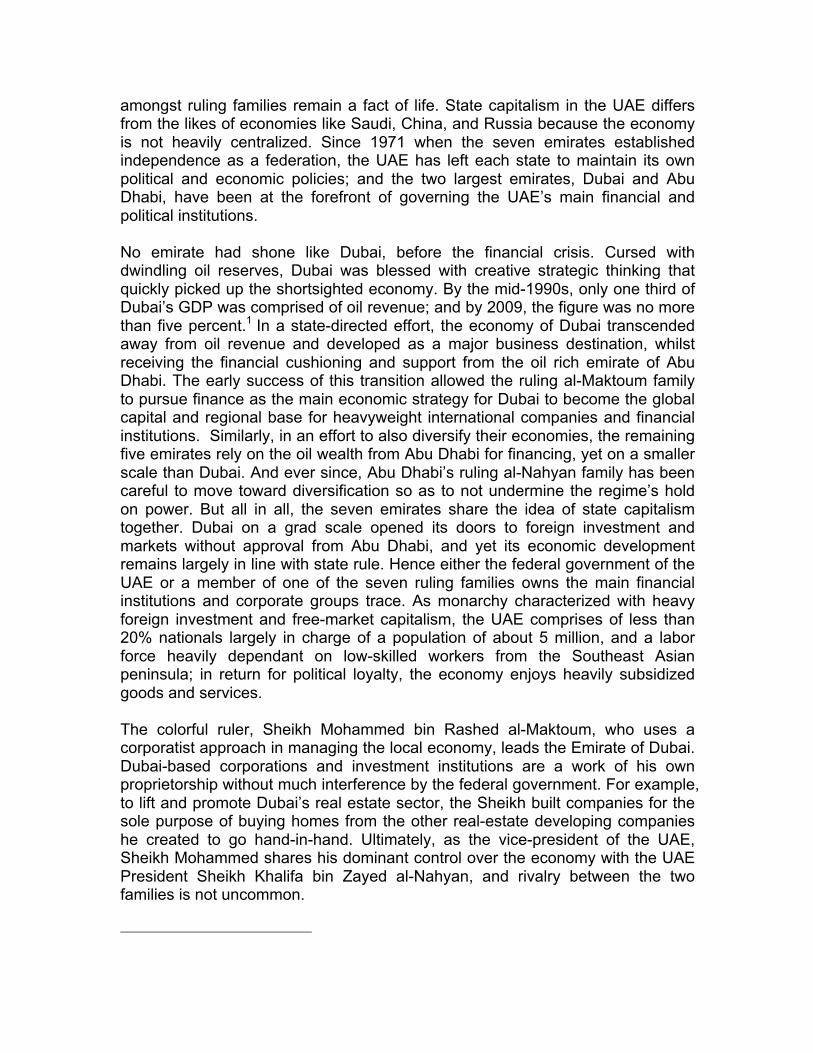

amongst ruling families remain a fact of life. State capitalism in the UAE differs from the likes of economies like Saudi, China, and Russia because the economy is not heavily centralized. Since 1971 when the seven emirates established independence as a federation, the UAE has left each state to maintain its own political and economic policies; and the two largest emirates, Dubai and Abu Dhabi, have been at the forefront of governing the UAE’s main financial and political institutions. No emirate had shone like Dubai, before the financial crisis. Cursed with dwindling oil reserves, Dubai was blessed with creative strategic thinking that quickly picked up the shortsighted economy. By the mid-1990s, only one third of Dubai’s GDP was comprised of oil revenue; and by 2009, the figure was no more than five percent.1 In a state-directed effort, the economy of Dubai transcended away from oil revenue and developed as a major business destination, whilst receiving the financial cushioning and support from the oil rich emirate of Abu Dhabi. The early success of this transition allowed the ruling al-Maktoum family to pursue finance as the main economic strategy for Dubai to become the global capital and regional base for heavyweight international companies and financial institutions. Similarly, in an effort to also diversify their economies, the remaining five emirates rely on the oil wealth from Abu Dhabi for financing, yet on a smaller scale than Dubai. And ever since, Abu Dhabi’s ruling al-Nahyan family has been careful to move toward diversification so as to not undermine the regime’s hold on power. But all in all, the seven emirates share the idea of state capitalism together. Dubai on a grad scale opened its doors to foreign investment and markets without approval from Abu Dhabi, and yet its economic development remains largely in line with state rule. Hence either the federal government of the UAE or a member of one of the seven ruling families owns the main financial institutions and corporate groups trace. As monarchy characterized with heavy foreign investment and free-market capitalism, the UAE comprises of less than 20% nationals largely in charge of a population of about 5 million, and a labor force heavily dependant on low-skilled workers from the Southeast Asian peninsula; in return for political loyalty, the economy enjoys heavily subsidized goods and services. The colorful ruler, Sheikh Mohammed bin Rashed al-Maktoum, who uses a corporatist approach in managing the local economy, leads the Emirate of Dubai. Dubai-based corporations and investment institutions are a work of his own proprietorship without much interference by the federal government. For example, to lift and promote Dubai’s real estate sector, the Sheikh built companies for the sole purpose of buying homes from the other real-estate developing companies he created to go hand-in-hand. Ultimately, as the vice-president of the UAE, Sheikh Mohammed shares his dominant control over the economy with the UAE President Sheikh Khalifa bin Zayed al-Nahyan, and rivalry between the two families is not uncommon.

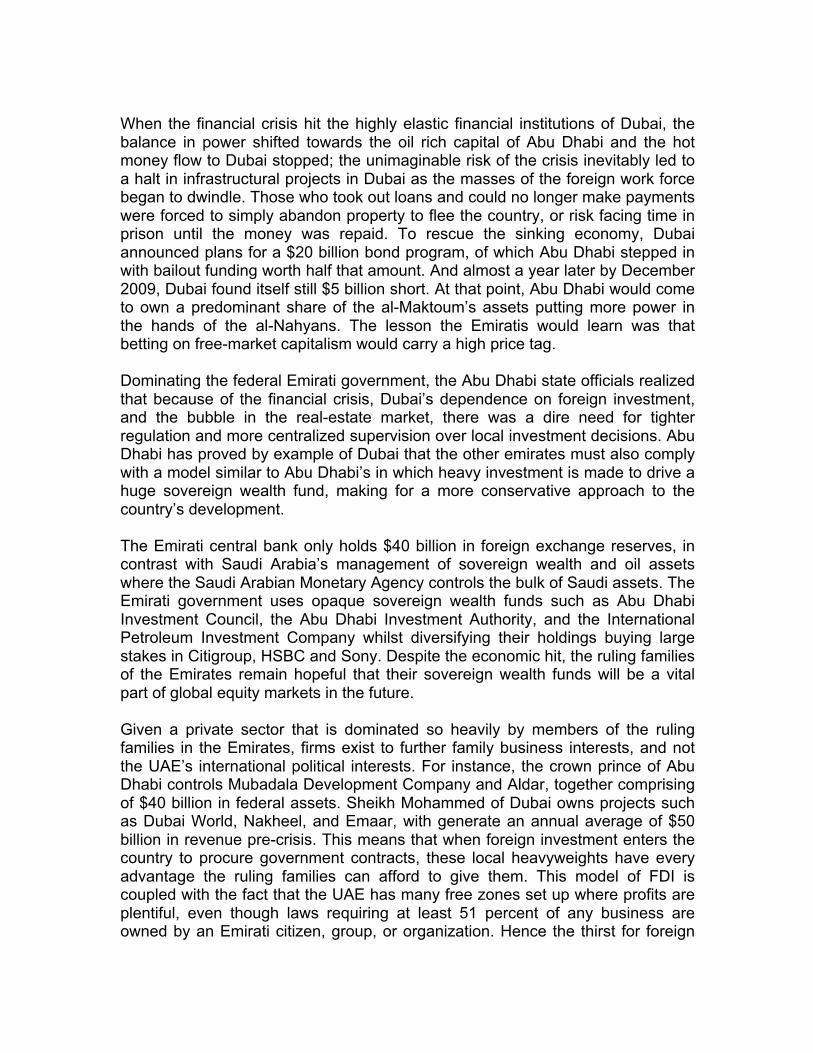

When the financial crisis hit the highly elastic financial institutions of Dubai, the balance in power shifted towards the oil rich capital of Abu Dhabi and the hot money flow to Dubai stopped; the unimaginable risk of the crisis inevitably led to a halt in infrastructural projects in Dubai as the masses of the foreign work force began to dwindle. Those who took out loans and could no longer make payments were forced to simply abandon property to flee the country, or risk facing time in prison until the money was repaid. To rescue the sinking economy, Dubai announced plans for a $20 billion bond program, of which Abu Dhabi stepped in with bailout funding worth half that amount. And almost a year later by December 2009, Dubai found itself still $5 billion short. At that point, Abu Dhabi would come to own a predominant share of the al-Maktoum’s assets putting more power in the hands of the al-Nahyans. The lesson the Emiratis would learn was that betting on free-market capitalism would carry a high price tag. Dominating the federal Emirati government, the Abu Dhabi state officials realized that because of the financial crisis, Dubai’s dependence on foreign investment, and the bubble in the real-estate market, there was a dire need for tighter regulation and more centralized supervision over local investment decisions. Abu Dhabi has proved by example of Dubai that the other emirates must also comply with a model similar to Abu Dhabi’s in which heavy investment is made to drive a huge sovereign wealth fund, making for a more conservative approach to the country’s development. The Emirati central bank only holds $40 billion in foreign exchange reserves, in contrast with Saudi Arabia’s management of sovereign wealth and oil assets where the Saudi Arabian Monetary Agency controls the bulk of Saudi assets. The Emirati government uses opaque sovereign wealth funds such as Abu Dhabi Investment Council, the Abu Dhabi Investment Authority, and the International Petroleum Investment Company whilst diversifying their holdings buying large stakes in Citigroup, HSBC and Sony. Despite the economic hit, the ruling families of the Emirates remain hopeful that their sovereign wealth funds will be a vital part of global equity markets in the future. Given a private sector that is dominated so heavily by members of the ruling families in the Emirates, firms exist to further family business interests, and not the UAE’s international political interests. For instance, the crown prince of Abu Dhabi controls Mubadala Development Company and Aldar, together comprising of $40 billion in federal assets. Sheikh Mohammed of Dubai owns projects such as Dubai World, Nakheel, and Emaar, with generate an annual average of $50 billion in revenue pre-crisis. This means that when foreign investment enters the country to procure government contracts, these local heavyweights have every advantage the ruling families can afford to give them. This model of FDI is coupled with the fact that the UAE has many free zones set up where profits are plentiful, even though laws requiring at least 51 percent of any business are owned by an Emirati citizen, group, or organization. Hence the thirst for foreign

investment of the UAE economy and the political loyalty required by state officials has marked it necessary for the establishment of a national think tank. The fact remains that there are billions of dollars worth of untapped assets that the UAE needs to use to target specific industries in the economy; the UAE faces many challenges and opportunities that an independent research institute modeled as a think tank would study and provide appropriate policies. There is little local literature on these challenges and opportunities; and the existing local literature does not capture the state of the Emirates in a manner that would be illuminating to its stakeholders. In sight of it’s Vision Plan for 2020, the UAE economy will move toward a less oil dependent diversification plan only if fresh thinking can contribute to an increased role in local entrepreneurship and research and development – a call for the establishment of a national think-tank The think tank would need to provide analyses and research activities that are academic and policy oriented, high quality, objective, and confidential when required for public and private clients. The center will not be filled with consultants chasing personal business and slanting findings accordingly. Instead, it would work for the good of the country and region as a whole. The opinions and findings can be trusted and would have the academic and professional credibility to ensure the results and reputation. The UAE’s Emirates Center for Strategic Studies and Research (ECSSR) was the only Center in the Gulf to provide some local political analyses. Further, when the Dubai based Gulf Research Center was operational and hosted a symposium on 23-24 November 2010 at the Millennium Hotel in Sharjah entitled, “The Role of Centers for Research, Political and Strategic Studies in the Arab World: Challenges and Prospects,” the main theme and conclusion of this symposium affirmed that the

“…staunch conviction of the importance of the role research centers could assume, particularly in view of the current problems and sweeping challenges confronting the Arab World.”2

The Bahrain Centre for Studies and Research promotes itself as “...a think-tank and the first institution for applied research in the Kingdom of Bahrain”. Its Mission Statement is: “To serve the Bahraini community by conducting applied research, particularly of a contractual type, and to offer consultancies to leaders and decision makers in both the public and the private sectors.”3 Similar to the ECSSR in Dubai, this does not encompass the entire region and is locally focused. In terms of economic geography, the UAE, though insulated, is surrounded by instable countries. Yemen is in the process of a transition of power, requiring

diplomatic and economic support. Iran, with its nuclear ambitions, would require an overdue review of its international strategy. Iraq still struggles with political strife under sectarian strain. Saudi suffers from its demographic time bomb of employment stability. And with the recent events of the Arab Spring, Syria and Egypt require a fundamental rethink of regional landscape. Establishment of a national think tank would allow for these challenges and opportunities to be studied whilst disregarding the distractions of the executive government; it would help build a multi-layer of ties between the UAE’s federal government, business community, intelligentsia and wider society. The relationships must not be built only with the think-tank itself but also between those four parties themselves. Too often, the miscommunication — or lack of it altogether — between those groups has produced antagonism and a general lack of endorsement. More often, the lack of cooperation has led to counter-productive results. A relevant dialogue between the think-tank and each of those four stakeholders on the areas above would herald a new era in public engagement in the UAE. Ideas include:

1. Town hall meetings across the nation to increase awareness of the UAE's goals, challenges and opportunities and serve as field research of public sentiment and priority. 2. A monthly open majlis that would host the nation's seasoned, emerging thinkers and analysts to discuss key issues. 3. Discussions with the business community to develop mutually beneficial ways by which they positively contribute to the UAE's long-term sustainability and competitiveness. 4. Sector-based roundtables with government officials where successes are studied and failures analyzed.

Like think tanks around the world, this one would offer fellowships for ex-officials whose term has ended. A series of ‘civil servant in residence' would be very successful since currently most senior government officials exit the public sphere and semi-retire while dabbling in business. The world as a whole, and not only the Arab part, is witnessing a ruthless spring that just won't wait for one or all. A national think-tank can help the UAE not just keep up but also lead.

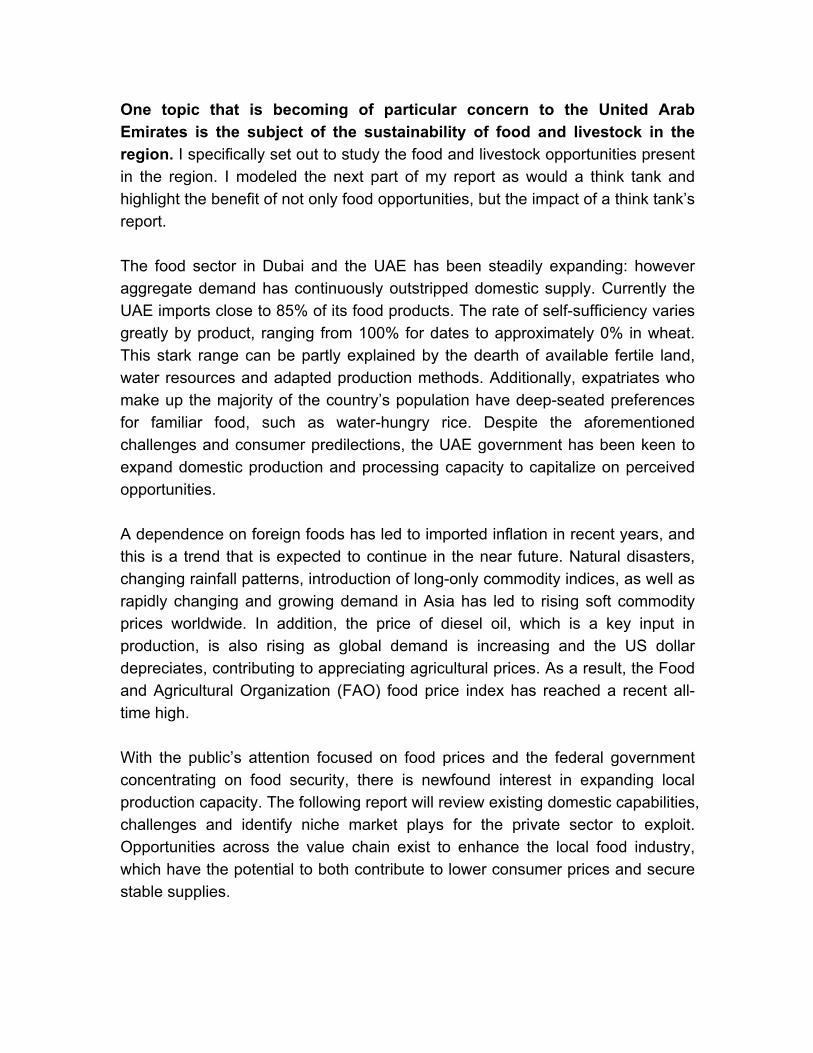

One topic that is becoming of particular concern to the United Arab Emirates is the subject of the sustainability of food and livestock in the region. I specifically set out to study the food and livestock opportunities present in the region. I modeled the next part of my report as would a think tank and highlight the benefit of not only food opportunities, but the impact of a think tank’s report. The food sector in Dubai and the UAE has been steadily expanding: however aggregate demand has continuously outstripped domestic supply. Currently the UAE imports close to 85% of its food products. The rate of self-sufficiency varies greatly by product, ranging from 100% for dates to approximately 0% in wheat. This stark range can be partly explained by the dearth of available fertile land, water resources and adapted production methods. Additionally, expatriates who make up the majority of the country’s population have deep-seated preferences for familiar food, such as water-hungry rice. Despite the aforementioned challenges and consumer predilections, the UAE government has been keen to expand domestic production and processing capacity to capitalize on perceived opportunities. A dependence on foreign foods has led to imported inflation in recent years, and this is a trend that is expected to continue in the near future. Natural disasters, changing rainfall patterns, introduction of long-only commodity indices, as well as rapidly changing and growing demand in Asia has led to rising soft commodity prices worldwide. In addition, the price of diesel oil, which is a key input in production, is also rising as global demand is increasing and the US dollar depreciates, contributing to appreciating agricultural prices. As a result, the Food and Agricultural Organization (FAO) food price index has reached a recent all-time high. With the public’s attention focused on food prices and the federal government concentrating on food security, there is newfound interest in expanding local production capacity. The following report will review existing domestic capabilities, challenges and identify niche market plays for the private sector to exploit. Opportunities across the value chain exist to enhance the local food industry, which have the potential to both contribute to lower consumer prices and secure stable supplies.

By virtue of its location and existing world-class infrastructure, Dubai stands to benefit from both regional and international trade in foodstuffs. At the current time, Dubai is not only a manufacturer of food but also the world’s third largest re-exporter. The Emirate has also taken a leadership role in trading commodities grown in nearby South Asia, such as tea. The same domestic assets these businesses see as competitive advantages can also be used by other

commercial ventures. Traders, fishermen, food processors and packaging manufacturers stand to benefit from the identified investment opportunities herein. Global food prices have risen to an all-time nominal and real highs in recent months, and many experts are predicting the trend to either continue or for price levels to hold over the medium term. Aside from swiftly changing global weather patterns and diseases that affect crop production, one of the major underlying reasons for the recent price spike is the financialization of soft commodities. While grain exchanges and forward contracts have existed for over 150 years, market participants had traditionally been intimately involved in foods. In 1999 however, the US Commodities Futures Trading Commission deregulated futures

80.00

100.00

120.00

140.00

160.00

180.00

200.00

Jan-‐90

Jan-‐91

Jan-‐92

Jan-‐93

Jan-‐94

Jan-‐95

Jan-‐96

Jan-‐97

Jan-‐98

Jan-‐99

Jan-‐00

Jan-‐01

Jan-‐02

Jan-‐03

Jan-‐04

Jan-‐05

Jan-‐06

Jan-‐07

Jan-‐08

Jan-‐09

Jan-‐10

Jan-‐11

Food Prices Reach All-‐Time High

FAO Food Price Index

markets and speculators could join the fold. Bankers quickly introduced long-only commodity indices, which included food products among others. Yet the impact of increased speculation only occurred after the bursting of the tech bubble, and has been further magnified since the Great Recession of 2008. Following the year 2000, there has been a 50-fold increase of investments in commodity index funds. Within five years prior to the Great Recession, the volume of index fund speculation increased by 1,900%. Furthermore, investors are no longer concentrated solely in the United States, but rather span the globe. Currently, speculators in wheat, a key worldwide agricultural commodity, outnumber market participant hedgers four to one. As of May 2011, corn futures are up 98%; wheat 67%, raw sugar 44%, and rice gained 25%. The advent of high finance in agriculture appears to be a permanent transformation. Its reach stretches not only into end products such as bushels of wheat, but also into inputs such as seed and fertilizer. As a result, both farmers and consumers are vulnerable to price swings. Furthermore, the structure of investment products in this market is designed primarily to push up prices. Given that indices such as the Goldman Sachs Commodities Index (GSCI) are long only, there is no short option available for investors. Speculators betting on declining values of agricultural commodities can only sell off/liquidate their index positions as happened recently in early May 2011. The nature of financialization in agriculture, however, seems aimed at increasing food prices rather than moderating their ups and downs. The high dependence on food imports allows UAE authorities little control over domestic food prices. Authorities have recently held meetings with major retail outlets to freeze and even lower the price of basic staples for a defined period of time to ease inflationary effects on consumers. Farmers are now provided with official prices, which they are not allowed to exceed. Products included in a March 2011 list championed by the Ministry of Economy’s Consumer Protection Department were as follows: milk, tea, rice, sugar, oil, canned food, coffee, pasta, flour, sauces, pickles and biscuits. An updated list was created in late May 2011 to include a wider spectrum of 400 goods. Such efforts by the government are aimed at moderating consumer prices, and have thus far been voluntarily taken on. Supermarkets and manufacturers are not allowed to increase retail prices without obtaining permission from the Ministry of the Economy. Municipality officials have levied fines against companies that have raised prices without

approval. Yet these are short-term measures and do not address long-term factors. In order to address continuing pricing and supply issues, the UAE government has initialed a variety of measures ranging from common to innovative strategies. The most frequently pursued one is a similar route taken by other Gulf countries, namely purchasing farmland abroad. While this strategy has the potential to secure crops and offers an opportunity for vertical integration, the effects are not dissimilar to mercantilist policies, which ultimately drive up global prices. Most recently, Abu Dhabi and Fujairah have initiated a more cost-effective grains storage project. Authorities are already planning to rival the world’s top oil bunkering hubs in Fujairah, and now expect to do the same with 100 million tons of grains storage capacity. Moreover, Abu Dhabi has invested significant capital in a trading house for agricultural products called Abu Dhabi Sources (ADS Holding). ADS’ extensive mandate stretches across the whole chain of commodities from logistics, infrastructure, and production all the way through processing. The federal government ahs also supported agricultural growth by promoting the establishment of food processing plants. By committing over 5 billion Dirhams in investments, it is providing ample opportunities for the private sector to expand its role in domestic food production. With the UAE being a large food importer, it is an opportune time to initiate a range of measures to secure stable supplies and ample liquidity in local commodity markets, which in turn will control consumer costs. One of the primary vehicles is to boost domestic food production in a cost effective manner by implementing methods devised in the research and development phase. Review of farming capabilities While the majority of land in the country is currently unsuitable for farming, new production methods are being invested in to enhance farming capabilities. Existing UAE farmland is overwhelmingly concentrated in Abu Dhabi (84%), which is also the largest Emirate by landmass. Total farm area in the country amounted to 222,862 hectares as of 2008, of which some 7% lay fallow. The country is keen to expand the physical amount of

farmland available. A recently commissioned Abu Dhabi Soil survey suggested cultivation could occur in a strategic reserve almost three times the size of its current farmland. While a soil database is already in place for Dubai, the Abu Dhabi Executive Council is funding surveys in the Northern Emirates. Despite such efforts, agricultural land is not likely to surpass 10% of the total landmass. Many of the identified farms in Abu Dhabi are dual use, with livestock also being bred on them. Close to 65% of Abu Dhabi farms raise sheep, goats and/or camels amounting to nearly 15,000 farms. Some 40% of farms also have greenhouses in addition to open fields, while merely 4% have greenhouse production only; implying most produce a variety of crops. A prevailing majority of farmers consider their farms a part time of hobby activity. Given a challenging climate, lack of suitable land and farmers who view the activity as an enjoyable past time, most Abu Dhabi farms are small. Farms are even lesser in size outside of Abu Dhabi. The average UAE farm is diminutive compared to those observed in developed countries where economies of scale are employed. While the average 2003 – 2005 farm size in Abu Dhabi was 9.5 hectares and 4.7 in Dubai, the average farm size in the United States stood at 169 hectares in the same year. The

199228

2699 7489 7603 4274

779 790

Farm Area by Emirate in 2008, hectares

Abu Dhabi

Dubai

Sharjah

Ras Al Khaimah

Fujairah

Umm Al Quwain

Ajman

average Abu Dhabi farm size grew to 20.5 hectares by 2009; which is still far below what is observed in agriculturally rich countries. The primary factor behind this disparity lies with the lesser domestic soil quality and difficult topography. Given the small size of farms, the value of agricultural goods produced in Abu Dhabi remains limited. In 2007, 62% of national farms were located in the capital Emirate, which accounts for 87% of the UAE’s landmass.

Abu Dhabi produced agricultural goods worth in excess of 4 billion Dirhams. Close to 98% of the crops produced in farms are sold domestically, with the

0 1 2 3 4 5 6 7 8 9 10

Abu Dhabi Umm Al Quwain

Dubai Ras Al Khaimah

Ajman Sharjah Fujairah

Hectares

Average Farm Size by Emirate, 2005

2560854

1431645

60183

Abu Dhabi Farming Products, 2007 (1,000 Dh)

Crop & Fodder

Fruits

Vegetables

remainder sold to neighboring GCC states. The 2007 range of agricultural products is practically diverse, with crops and fodder leading followed by fruits and vegetables a distant third. Yet the most recent data available shows water-intensive grasses, used as livestock feed, capturing over 90%. Given local constraints, this predilection for feed production is now being targeted by authorities. On a national level, agricultural/food production is more diverse, however traditional products dominate. In terms of both volume and value of different products, dates dwarf all other items. In fact, dates are the only significant agricultural export out of the UAE, claiming 37% worldwide market share according to the Food and Agriculture Organization (FAO).

Meanwhile, most other crops produced in the country are aimed at domestic consumers. Abu Dhabi statistics point to significant Rhodes grass production for livestock rearing, which is primarily for chickens, camels, cattle and goats. Yet fodder production is often water-intensive and the government has recently offered subsidies to farmers who discontinue growing such products. Instead,

755000 215000

140000

16500

22000 20000

12300 17200

11500

17500

Top Indigenous Food Commodities, 2009 Production MTs

Dates

Tomatoes

Vegitables fres nes

Onions(inc. Shallots), green

Eggplants (aubergines)

Pumkins, squash and Gourds

Lemons and limes

Cucumbers and gherkins

Cauli[lower and broccoli

Cabbages and other Brassicas

new production methods, which use limited supplies of water, are being favored. Tomatoes and fresh vegetables are both large individual categories, followed by a variety of other fruits and vegetables. Organic farming has become an active niche market in the UAE, with a variety of customers interested in local produce. Obtaining a fast field-to-the-table turnover arguably makes fruits and vegetables taste better. As compared to perishable imports from abroad that endure a long journey after being picked prematurely, products grown locally are often in good shape. The country already has twenty organic farms as of the beginning of 2011, and will likely reach fifty by the end of this year. This follows the encouragement of the Ministry of Environment and Water, which is transforming 23 conventional farms into organic operations. The top agricultural imports to the UAE are both water-intensive and cater to expatriate tastes. A majority of products are sourced from South and Southeast Asia, as the top food import, rice. Tea registers as a very large import category; however a majority of it is re-exported in either bagged or raw form. The UAE hosts Unilever’s Lipton factory as well as the Dubai Tea Trading Center (DTTC). Dubai remains the second largest export destination for both Indian and Sri Lankan tea.

Other large agricultural imports include items not produced in the country such as cook oils, wheat, chocolates, sugar products as well as fruits and vegetables. Nearly the entire top finished food imports consist of items not suitable for local production. Jenan oil in Jebel Ali is however following in the footsteps of Al Khaleej sugar refinery and importing raw food materials to process in Dubai. Efforts are underway in the UAE to enlarge the area available for cultivation, capabilities to grow products in an economical fashion and extend the range of agricultural products. The government has been studying ways to increase agricultural output by extending the cultivated land area and by introducing honed production methods suitable to the local climate. Local governments have been particularly active in reclaiming fallow land and redistributing it to farmers. By experimenting with new systems, farmers are aiming to extend the growing season and further expand the variety of products. Local authorities have also rolled out extensive training programs as well as technical services and provided necessary equipment at little to no cost.

$1,498,960

$452,111 $374,083

$297,613

$200,771

$173,660

$171,041

$153,659

$145,327

$136,075 $128,233

Top Imports of Food Commodities, 2009 $1,000s

Rice Milled

Tea

Palm Oil

Wheat

Chocolate Prsnes

Pastry

Sugar Re[ined

Repaseed

Vegetables fresh nes

Apples

Soybeans

Each Emirate either has, or is developing, a soil survey and supporting database. The captured data is intended to document which areas are suitable for farming activities. In addition, the government has started a program of palm tree plating to create shaded areas for crops that would otherwise wilt. Factors including soil salinity and proximity to water resources are critical to such analyses. Assessing whether and how fallow land can be used for agricultural endeavors is essential when attempting to conserve precious water resources. According to the Environment Agency Abu Dhabi (EAD), agriculture account for nearly 80% of water consumption, while contributing only 4% of GDP. While definitions and ratios vary across the Emirates, the fact remains that expensively produced desalinated water are being used in an activity that yields little economic returns. In order to expand production while at the same time conserve water, new technologies are being invested in to increase effective yields. Innovative ideas include the use of treated liquid sewage for irrigation, which is being studied by authorities. More broadly, multiple research bodies including the EAD are championing the application of protected agriculture. Most research facilities and biotechnology-focused laboratories in the UAE concentrate on aspects surrounding the propagation and tissue culture of its top agricultural product, date palms. In addition, there is a Dubai-based center which focuses on applied research in saline irrigate agriculture across different crops. The results from protected agriculture experiments have been selectively transferred to famers by each Emirate’s extension service. While somewhat disconnected from commercial applications outside of date palms, it is clear agricultural biotechnology has opened up new possibilities. New methods in crop production are being experimented with to make optimal use of scarce domestic resources. The concept of vertical farming, invented in 1999 to grow food in crowded urban areas, is popular and even being implemented within restaurants. Crops are watered using condensation from a building or establishment’s air conditioning system. Several experiments currently underway in the UAE implement the seawater greenhouse concept, which combines a solar desalination system with cooling and humidification for crops. Using even fewer water resources, hydroponic greenhouses are catching on across several Emirates including Dubai and Ajman. A government initiative

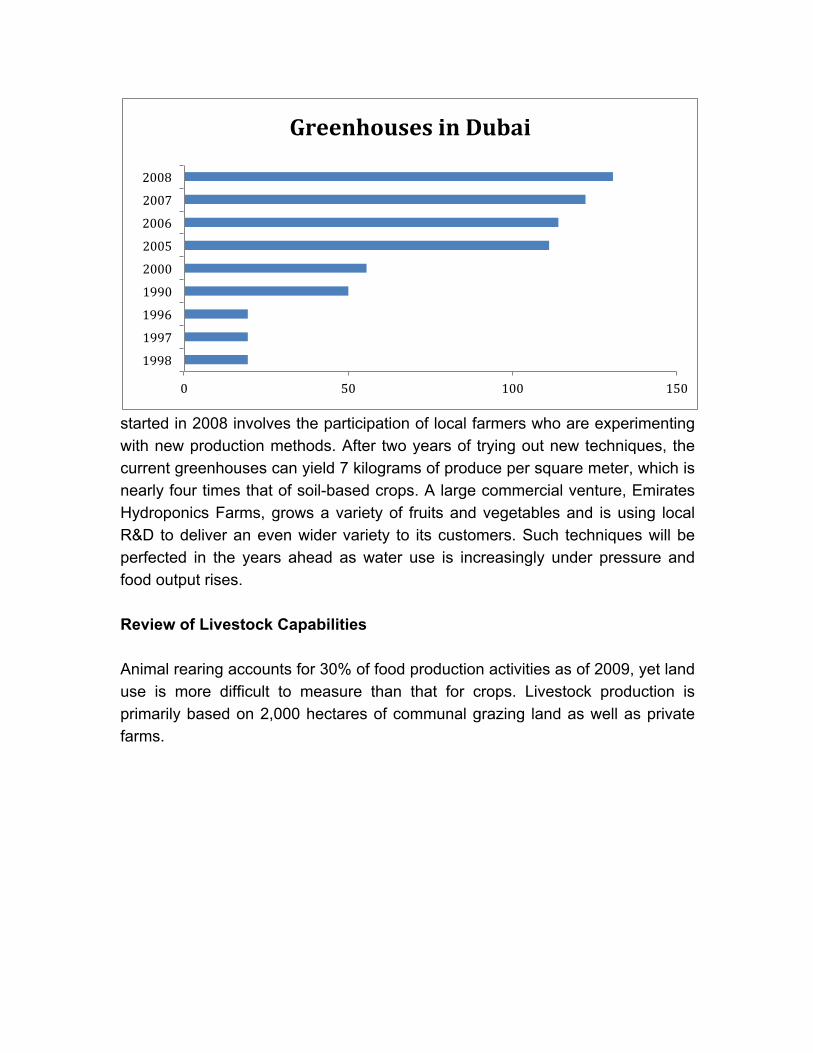

started in 2008 involves the participation of local farmers who are experimenting with new production methods. After two years of trying out new techniques, the current greenhouses can yield 7 kilograms of produce per square meter, which is nearly four times that of soil-based crops. A large commercial venture, Emirates Hydroponics Farms, grows a variety of fruits and vegetables and is using local R&D to deliver an even wider variety to its customers. Such techniques will be perfected in the years ahead as water use is increasingly under pressure and food output rises. Review of Livestock Capabilities Animal rearing accounts for 30% of food production activities as of 2009, yet land use is more difficult to measure than that for crops. Livestock production is primarily based on 2,000 hectares of communal grazing land as well as private farms.

0 50 100 150

1998

1997

1996

1990

2000

2005

2006

2007

2008

Greenhouses in Dubai

As mentioned previously, nearly two-thirds of Abu Dhabi farms raise some form of livestock. Given ample availability of feed and generous subsidies, the number of livestock has grown from 0.4 million in 1970, to 1.5 million in 1994 to over 3.5 million in early 2011.

An ongoing livestock registry in Abu Dhabi has tagged close to 2 million animals, which the government intends to use in monitoring the size and composition of herds as well as their location. In return for participation in the compulsory program, farmers are able to obtain free vaccinations and liberal feed subsidies.

226,751

1,732,988

31,232 Abu Dhabi Livestock Composition, 2011 AIRS

Camels

Sheep & Goats

Cows

398,107 65,179

1,793,695

1,233,953

UAE Livestock in 2008

Camels

Cattle

Goats

Sheep

The battle against animal borne diseases is of particular concern to authorities after a brucellosis scare in late 2010 proved the culling of at least 500 sheep. Meanwhile, the individual local authorities as well as the Federal Ministry of Environment and Water monitor livestock in other Emirates. An additional measure of growing livestock herds is the increasing amounts of feed imported from abroad in addition to what is grown at home. The overwhelming majority of agricultural products in Abu Dhabi are hays, grasses and corn, which are all used for livestock. Feed imports plug the demand gap that exists after accounting for what is produced in the UAE. As the population grows and tastes evolve, the demand for meat products has risen considerably. The market for fodder has grown strongly in the UAE, to the point where imports reached an estimated 1.2 million tons in 2010. Half of these come from the United States; however the composition may change over the next two years when UAE farms overseas start supplying the Emirates. The livestock numbers quoted above do not include poultry, which is a large industry in the UAE. As of 2008, approximately 15.5 million chickens are raised in 40 farms across the UAE. A quarter of all farms are located in Abu Dhabi, while the rest are spread out over the other Emirates. Most poultry farms are large commercial operations, while individual and organic farms also raise chickens. Free-range chickens are a new concept in the UAE, and the vast majorities sold by high-end restaurants are imported from abroad. Yet the growing interest of consumers to acquire and consume healthy foods may encourage their provision and alter the incentives for domestic farmers. The UAE produces considerably more plant than animal products. In terms of volume, milk alone accounts for more than all meat and poultry products combined. Given the cost structure and extensive water usage requirements for raising cattle solely for beef production, little of it is done domestically. Instead, livestock are primarily used to generate animal derivatives such as dairy products and eggs given the cost of breeding and/or importation.

As a result, the country’s self-sufficiency ratio for fresh milk is 83% and eggs is 40%, while that of meat is 31% and poultry is only 17%. As the number of animals bred in the UAE is rising, entrepreneurs and food processors are thinking of inventive ways to make optimal use of them prior to slaughter. The country’s largest sub-sector of animal products, namely milk and dairy, is also its most innovative and highly profitable. Over 30 diaries are in operation across the country and are in direct competition with far larger regional rivals such as SADAFCO and Al Marai of Saudi Arabia. Domestic dairies are continuously introducing new products across pr

product categories as well as experimenting with new packaging. As they expand

29150

304

90277

29150

Compostion of UAE Animal Derivatives, 2003, tons

Red Meat

White Meat

Eggs

Milk

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

Cow Milk

Sheep Milk

Goat Milk

UAE Milk Production, 2008 tons

their business activities, they are also increasing the efficiency with which their existing operations are run. While traditionally focused on cow-based milk products, domestic producers are increasingly diversifying into camel milk both at home and for export. Domestic producers focus on supplying camel, mutton, chicken, beef and goat meat as well as a range of dairy products. While sheep, camels and lamb are mostly raised in open grazing pastures, chicken and cows are primarily held in contained areas. Local production of meats and by-products is geared toward domestic and regional consumption. A vast majority of livestock projects are privately owned and operated, and as a result, efficiently managed. All meat produced in the UAE is halal. Sheep and goats have long been raised in arid conditions such as the Gulf. As such, there is a native breed of black sheep, which is popular between UAE and Omani consumers, partly for being smaller in size than the imported Australian or New Zealand variety. Local single-humped camels had traditionally been used for racing and transportation, but are now increasingly used for meat and milk production. Modern poultry farming has been an advent in the UAE market, with the majority of hatchlings imported from abroad. Most meat products consumed in the UAE are halal, apart from limited imported pork products available in select supermarkets. Dairy products are very popular in the UAE and production is expanding rapidly. Domestically produced items include: milk, health conscious blends of milk, condensed/evaporated variety, coffee whitener, drinking and flavored yoghurts, cream, cheese, ice cream, chilled and shelf stable desserts. The second largest producer, Al Rawabi, has seen demand for its products increasing at a rate of 20% per annum. Accordingly, the company is purchasing 2,000 new cows by the end of 2011 and plans to open a new farm in Liwa to service an expanding market in the western region with a further 5,000 cows by 2013. A majority of livestock imports to the UAE originate from non-Muslim countries, which have specialized facilities for halal production. While the composition of imports varies each year, the majority comes from Australia, Brazil, Canada, Ireland, New Zealand and the United States.

Malaysia is the only Muslim country that has taken a strong interest in halal meat production for export, while others are more inwardly focused. UAE-based Al Islami Foods has started to assume a regional leadership role; however it is starting from a low base. The majority of livestock imports are in product categories in which domestic manufacturers are not competitive or have limited market share as in dried milk. The UAE is also working to acquire land abroad for halal livestock production as well as farmland. Government officials are in negotiations with Thailand to develop large-scale farms producing goats, sheep and other animals. The efforts run parallel to those announced by Saudi Arabia and Bahrain to invest in developing agricultural facilities in Asia and Africa. The proposals are part of a broader initiative of the Islamic Chamber of Commerce and Industry to develop a halal food production chain covering multiple countries to improve food security. The UAE has research facilities dedicated to enhance the livestock sector’s competitive position as well as significant in-house Livestock producers themselves are heavily investing in improving their efficiency and introducing new derived products to improve their bottom line. Initiatives vary from the introduction of new feed blends for livestock to new farming techniques to new consumer product offerings. Advances developed by industry and universities aim to improve profitability and provide the grounds for expansion. All efforts are ultimately designed to improve UAE food security.

$537,464

$246,446 $204,226

$188,352

$132,335

$129,908

Top Imports of Livestock Commodities, 2009 $1,000s

Chicken meat

Milk Whole Dried

Meat-‐ CattleBonless(Beef&Veal)

Sheep meat

Milk Whole Evp

The UAE’s largest dairy producer to optimize its use of the costly and scarce resource is deploying a new water treatment technology. Al Ain Diary has chosen to roll out Dow’s Fimtec ultra filtration and reverse osmosis process to convert wastewater into a reusable resource. The scale of implementation is impressive, amounting to 300,000 cubic liters of water a day. As a result, the farm in question will be able to use the recycled water for irrigation and cleaning needs, as well as to keep the cattle cool in brutal summer months. The experiment will not only save the company in water usage charges, but also boost the productivity of its cows by keeping them at an ideal temperature year round. Similar measures are being studied by other dairy farms. The largest Emirati dairy company is also diversifying its consumer range by introducing a range of camel milk products. Al Ain Diary had already been active in introducing a low fat drinking yoghurt range, and has now honed its interest in expanding beyond cow milk derivatives. Camel milk has long been a staple of Bedouins, and a recent UAE University survey has shown it is more popular in rural areas of the country than urban zones where expats are concentrated. Camel milks’ nutritional and health benefits are less well known, and diary companies are planning on touting them to a wider populace. Able to boost the body’s immune system, rich in anti-oxidants, alpha-hydroxyl acids and vitamins A, B2 and D, camel milk is also lower in fat, cholesterol and more easily digestible. Like human milk, camel milk does not contain lacto globulin, the protein present in cows', goats' and horses' milk that is the main cause of cow’s milk allergy. Already sold in drinkable and chocolate form, new derivatives are being experimented with. Soap, cheese, coffee whitener, sports protein powder and ice cream are all viable alternatives and Al Ain Dairy is at the forefront of product development research. As camel, chicken and cow populations grow rapidly, so does the need to supply fodder for animals. The Emirate of Abu Dhabi is currently the largest single importer, with 22 distribution centers, which is sourced domestically and from multiple countries abroad. Given that feed constitutes approximately 75% of the cost of raising poultry, it is vital to secure dependable and inexpensive sources of fodder. The UAE University, namely using date pits to feed livestock, is looking into one potential domestic source. They may also serve as a healthy alternative to antibiotics currently administered to chickens, which humans already ingest too much of. The UAE’s date industry is estimated to discard 50,000 tons of pits annually as a by-product of processing. The use of date pits as feed therefore not

only makes economic sense, but also improves the Emirates’ food security and can provide health benefits to consumers. By innovating and optimizing the use of scarce domestic resources, the UAE to benefit not only in agriculture but in livestock rearing as well. Research centers and industry is focused on enhancing efficiency and widening existing product ranges to maximize profitability and food safety. Authorities are eager to promote the wise use of scarce resources such as water, and are creating incentives for farmers to that effect. Review of Fishing/Aquaculture Capabilities The country has a long history of fishing, pearl diving and sea-faring trade. Dubai was first a fishing village before the widened Creek attracted merchants from the region and grew exponentially as an entrepot. Local fish has been part of traditional Emirati cuisine, yet large-scale development and natural disasters have pared down the availability of both wild and farmed fish. In the UAE, the numbers of hammour (red snapper), spangled emperor fish, painted sweetlip

s and the golden trevally fell by 80% between 1978 and 2002. The increased salinity of Gulf waters following the expansion of desalination facilities and warmer global temperatures has compounded the effects of overfishing. Shark, which had been widely consumed in local dishes, is now rarely caught in Gulf

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Fish Production by Emirate, tons

Other Emarates

Dubai

Abu Dhabi

waters. While the country has heretofore been self sufficient in fish, the red algae bloom of 2008/2009 caused catches to decline and the largest aquaculture facility to shut down operations. As the salinity and temperature levels of the water increase, local fishing is increasingly under threat. The expansion of large port and storage facilities across the UAE is restricting the area used by fishermen, in addition to large land reclamation works in Dubai and Abu Dhabi.

In consequence, the overwhelming majority of fishing operations are now concentrated in the northern Emirates. Authorities have responded to the decline with support measures, most prominently by providing fishermen with boats and engines. Yet subsidies have thus far been unable to reverse the dominant trend of reduced catches. While the volume of fish being caught has been declining, their value has been increasing in the past four years. The growth in catches by type of fish is concentrated in demersal fish. In Abu Dhabi as of 2009, emperor breams and jack mackerels are the most caught fish species by volume. These fish are not the most valuable however, with grouper (hammour), mackerels and tuna being highly prized in the region.

0

100

200

300

400

500

600

2005 2006 2007 2008

Number of Marine Engines offered to Fishermen, by Emirate

Fujairah

Ras Al Khaimah

Umm Al Quwain

Ajman

Sharjah

Dubai

Abu Dhabi

Hammour is the most commonly found fish on restaurant menus in the UAE, while lobster and salmon come close and are exclusively imported. A vast number of applications have been registered to open aquaculture facilities in the UAE, however few are implemented. A coastline of over 600 kilometers and inexpensive energy to power pumped water systems are appealing to any business considering the UAE as a base. However challenging conditions, including brutal summer weather, and high salinity that kills off many species, preclude many entreprenueurers from moving forward. So while there is potential for fish farms across the region, and many licenses are distributed, few proceed with setting up operations. Acclimating techniques to the local climate and conditions is particularly difficult and limits the immediate yield on returns. Aquaculture production has declined from its previously attained highs given the identified challenges. At present there is only one commercial operation in Fujairah named Mubarak Fisheries, which produces approximately 400 tons per year. The previously successful International Fish Farming Company (ASMAK), established in 1999, was active across four Emirates until red tide in 2009 caused it to discontinue operations. ASMAK had previously produced 1,200 tons of fish per year. The large blooms of oxygen-depleting algae had caused many of its fish to suffocate and perish, along with tow-thirds of fish in the waters around Dibba. Despite the environmental catastrophe that caused it to cease farming, a financial bailout is ensuring its activities are revived. The Royal Group, which heretofore controls 47% of ASMAK, has agreed to buy two-year convertible bonds worth 420 Dirhams. In addition to finance, the government-controlled

0 5 10 15 20 25 30 35

0

200

400

600

800

1000

1200 Abu Dhabi Caught Fish by Type, 2009

Quanitity (rt)

Value, mn AED

Marine Resources Research Centre is helping the industry to resuscitate by providing fingerlings from its hatchery. Fishing farming has commanded most of the industry’s resources; however a recently commenced project farming caviar has captured public attention. A joint venture between the local Bin Salem Holding and United Food Technologies is in the process of founding the Middle East’s largest aquaculture plant in Abu Dhabi. The final stage of the plant is designed to produce 32 tons of caviar and 490 tons of sturgeon per year. Although fraught with engineering challenges derived from a lack of fresh water sources, the company is implementing its own R&D to overcome them. The recirculation and purification systems are intended to cleanse the water and ensure accommodating temperatures. The result will be an aquaculture venture on an enormous scale adjacent to its customer base. The UAE has research facilities dedicated to enhance the fisheries sector’s competitive position. The government-run Marine Resources Research Center runs a farming operation and a hatchery to study different fish species applicability to local conditions. There is also a large aquaculture center on Abu Al Abya Island that studies the benefits of hormonal injections in fish, the brood stock feed, stocking density and water temperature conditions. This in turn has allowed profitable pilot-scale production of tilapia and other species to take place in both marine cages and freshwater ponds. One of the primary takeaways from contained research and recent events are more focus is needed on containing mortalities in the summer months. The high temperatures and salinity levels observed in June-August affects both wild and farmed fish. In order to minimize loss, water temperature and conditions need to be controlled. Research centers are now focusing on how to do so in the most cost-effective manner possible for operators. Subsidies for Domestic Food Production Local agricultural production faces environmental and topographical challenges, which has heretofore been overcome by government incentive programs. Although prevalent across the world, agriculture subsidies are particularly generous in the UAE. In addition to running small farms with few economies of scale, farmers are eligible to receive in excess of 200,000 Dirhams per annum in support. The level of financial incentives for farming varies across Emirate,

however it is clear that without such extensive support, much of it would not occur. The government has recognized this and is increasingly targeting its support toward activities it views as valuable. The leading agricultural services provided by or through the federal Ministry of Environment and Water include:

- Distribution of subsidized seeds, fertilizers and pesticides at 50% cost; - Loans for pumps and other machinery needed for plant protection; - Free maintenance of field machinery; - Free well drilling; - Free land leveling; - Human resource training; - Extension services (also specific to each Emirate’s needs).

The most significant agricultural producing Emirate, Abu Dhabi, has extensive outreach and support programs. Services for its local farmers include:

- Free land grants (also exists in other Emirates); - Free extension services; - Free water drilling and pump for first well; - Free machinery for pest-control; - Free vegetable seedlings; - Free wind-breakers; - Free land preparation; - Free plastic containers to hold vegetables; - Salary for one laborer up to two years; - Refund of 50% for fencing implementation; - Refund of 50% for irrigation systems; - Refund of 50% for fertilizer provision.

The Abu Dhabi Food Control Authority (ADFCA) has recently announced a new campaign to boost productivity and crop quality in the Emirate. The measures are meant to encourage farmers to adopt best practices in land cultivation and environmental protection. Authorities intend to disseminate cutting edge technologies and capabilities in order to improve yields and minimize their water consumption. ADFCA has announced farmers will receive 100,000 Dirhams per year in cash, in addition to other aid, in order to refrain from water-intensive

cultivation. The measure is of particular importance, because farmers have overwhelmingly been shifting production to animal feed (Rhodes grass), which is water intensive. In order to reverse the recent trend and promote sustainable agricultural production that will diversify its economy, the Emirate is adjusting and increasing its subsidy program. Generous monetary incentives are designed to wean farmers off of water-intensive production methods and goods without changing its end user price. Water is an increasingly precious resource, which is heavily used in irrigation. Wastage of water in agriculture and out-of-date irrigation channels is a key concern, which is being addressed on a small scale initially. Groundwater resources are scarce and declining, while increased production of desalinated water is negatively affecting Gulf waters and fish catches. Stopping short of altering the price of water for consumers (whether it be for farmers or residents), government authorities are instituting change by increasing direct agricultural subsidies Although an expensive route, it is hoped farmers will be induced to produce alternate, water-efficient and highly valued crops. Farmers not only pay the same water tariffs as everyone else, so too do they pay the identical electricity rates. As the price of crude oil increases, local utility companies such as DEWA have raised rates for consumers. This has a direct impact on dairy and farming operations, and worsens their competitive position vis-à-vis Saudi producers who continue to benefit from unchanged heavily subsidized rates. This in turn has caused local firms to lobby the government for more protectionist measures; however authorities have so far resisted closing markets. The government has instead decided to promote local agriculture to be the most efficient possible, rather than instituted artificial barriers, which cannot be sustained in the long term. Just as in California with grape production, the UAE is involving local universities, research centers and extension services to teach best practices to farmers. New technologies such as G-Earth are being transferred through the Abu Dhabi Farmer’s Services Center in order to reduce the reliance on the power grid and consumption of desalinated water. The ultimate goal is to compensate farmers as they set up operations and help them achieve profitability by passing on suitable skills and raw materials. Authorities are intent on encouraging a broader variety of crops and other agricultural activities that expand production in a sustainable manner.

Food Processing Sector. A successful area of the food sector, which thrives without any direct subsidies, is food manufacturing. With a growing domestic population and budding markets in the near abroad, supply had traditionally been sourced from outside the region. The strategic geographical location of Dubai, in addition to world-class logistical capabilities, is now encouraging investment in processing from numerous foreign and domestic manufacturers. Whether it is producing Kit-Kats or fruit and nut snacks in the Dubai Investment Park, making cooking oil in Jebel Ali, milling oats at the Al Ghurair factory or manufacturing biscuits in Sharjah, food processing is increasingly based in the UAE. The industry has skyrocketed recently, tripling in size in the past two years according to a recent estimate. The food-manufacturing sector has traditionally been a growth area, albeit at a lesser pace than in the recent past. The sector has grown at an average annual rate of 10% between 1980 and 2005. Food industry investments in 2008 accounted for 42% of all manufacturing capital deployments. Currently, there are more than 350 food processing establishments in the UAE, which accounts for approximately 9% of manufacturing plants. Dubai houses over half of the country’s food manufacturing units. The net value added by food processing accounts for approximately 8% of all manufacturing activity. A majority of food produced in the UAE is consumed domestically; however, exports are increasing as new plants scale up in size. The industry is increasingly establishing a presence in the UAE but primarily sources its ingredients from abroad. Whether it is sugar, cocoa beans, wheat or spices, many of the food processing industry’s inputs are imported to create a local product. The Middle East is a major market for Dubai foods, of which there are more than 135 distinct products. The advantage of locating in Dubai or the UAE is the close proximity to the customer base and being able to cater to local tastes. For example, prior to the Emke Group-Rose Poultry joint venture, many halal meat and seafood processed foods had to be imported from Malaysia, which often use unfamiliar flavors to Gulf consumers. Adding spices and flavors to meats and oils is done in the UAE as well. Many industries go on to expand across the production chain, such as in the pasta sub-sector. The advantage of controlling the entire process allows the manufacturer to tweak the recipes and accommodate new trends instantaneously! New activity is concentrated in frozen,

convenience and ready-to-eat meals, which are popular among consumers who face time pressure and often need to eat at least one meal on their employers’ premises. Given the dominant climate in the Gulf, food packaging is of the utmost importance. When distributing processed foods in and out of the Middle East, ensuring its freshness can only be achieved by using appropriate bottling and/or packaging techniques. Whether it is implementing Dupont Surlyn, Tetra Recart or Plastipak technologies, using less plastic (PET) in an effective manner can lengthen a product’s shelf life while simultaneously saving money and reducing companies’ environmental footprint. The evolution in packaging allows domestic producers to reach a wider customer base across the Middle East and Africa with minimal inventory losses. Continued innovation and investment in packaging materials will ensure increased profitability for domestic manufacturers. For example, Food Specialties was the first company to introduce a squeezable honey bottle with a non-drip nozzle to the region in 2006, which led to increased sales across the GCC. Offering new packaging solutions is an additional avenue available for UAE-based manufacturers to gain share in new export markets. The food processing industry is set for further expansion in the years ahead as demand across the region increases and Dubai becomes a manufacturing hub. Investment and Export Opportunities Given the government’s focus on improving food security and the industry’s increasing competitiveness, there are many investment and export opportunities available. The following section outlines several unexplored or neglected ventures, which would be profitable to undertake!

1. Pesticide-free certification and production. The Farmers’ Services Center has embarked on numerous technology transfer and agriculture support mission to enhance Abu Dhabi’s farming community. A recent initiative to promote organic farming by the Ministry of Environment and Water has commenced and is likely to substantially increase its share of domestic production. While demand for organic foods is rising among increasingly health-conscious consumers, a recent survey has shown they are willing to pay a significant premium for produce free of chemicals. By introducing

a pesticide-free certification in addition to overseeing organic farms, the Ministry of Environment and Water could open a market with high premiums. Consumers have signaled a willingness to purchase chemical-free produce, and government support could create a new market opportunity for domestic farmers. The certification could not only monitor the use of pesticides on farms, but also institute quality gradations. A common problem in UAE supermarkets is that produce of varying age and quality is thrown in together, often souring consumers’ appetite. Instead, many opt for expensive produce imported from further afield primarily because it looks better. By promoting the introduction of a pesticide-free certification and gradations of quality, the Ministry of Environment and Water would greatly improve the image of local farmers and their ability to yield good returns. The local extension service centers would help in imparting best practices to farmers seeking the certification and filtering their produce to be sent to the market. Crops that are able to naturally withstand high temperatures could easily be rolled out with the certification such as asparagus, lemongrass, mangoes and sweet potatoes. Efforts already undertaken by the Abu Dhabi Food Control Authority to ensure proper storage could be strengthened and taken up on a national level. Innovations achieved by food manufacturers in packaging could be channeled to help national transport of fresh fruits and vegetables. The result would be reduced spoilage, an improved image of local farming and higher yields for farmers that sell pesticide-free produce.

2. Aloe Vera Production. As Abu Dhabi seeks to wean its farmers off of water-intensive agriculture, identifying which items are more suitable to the UAE environment is of paramount importance. The ale Vera plant grows well in similar climates and has extensive uses, including locally produced medicines. The plant is closely related to the Aloe perryi species, which is endemic in nearby Yemen. Both species are able to survive in areas of low natural rainfall and able to resist most insects and pests. Large-scale agricultural production of Aloe Vera is currently undertaken across several different continents, yet nowhere in the Gulf. By farming aloe vera in large quantities, the plant’s byproducts can be used in a range of different consumer products. Many of the inputs could be used by

industries already existing in the UAE including beverages, desserts, lotions/creams and yoghurts. Aloe vera juice is also consumed (non-orally) in order to relieve digestive problems such as heartburn and irritable bowel syndrome. The plant’s byproducts are commonly used in producing incense, makeup, moisturizers, shampoos, shaving creams, soaps, sunscreens and tissues. Aloe vera is sometimes used as a food substance in creative dishes. In addition, the aloe vera plant has been shown to promote the rate of healing, and is therefore effective in the treatment of wounds. With such a wide variety of applications, the plant can easily find applications in the UAE industrial manufacturing chain. A combination of suitable climate, low water consumption and wide applicability make farming aloe vera an attractive option for the UAE’s farmers. By introducing the plant and cultivation techniques through the separate Emirates’ extension services, the government could easily promote its production and use.

3. Organic free-range chicken production. The demand for free-range organic chickens already exists in the UAE, yet the majority of restaurants currently source them from outside the country. Consumers have already been introduced to the concept through the availability of organic eggs. The success of the Organic Foods & Café chain in the UAE has prompted other retailers and restaurants to expand their organic offerings. Periodic markets have been set up in the Dubai Mall and Masdar City in Abu Dhabi to sell local organic produce. A permanent store is being set up in the Jumeirah Lakes Towers, which will sell Abu Dhabi Organic Farms produce. While organic gods are primarily produce, the aforementioned producer also sells organic free-range chicken and eggs. At the moment it is only on an extremely small scale however, especially as they do not grow as fast as commercial chickens. Yet demand for organic chicken continues to grow, and domestic producers are unable to meet consumer needs. As a result, the share of regional exports served to UAE diners has risen considerably. At government-affiliated Emaar hotels and restaurants for example, organic chicken on restaurant menus is sourced from neighboring Oman. Similarly, the Dubai branch of Baker & Spice restaurant is interested in but unable to source large quantities of domestic organic meats and vegetables for its patrons (as well as for the weekend organic

market where it is held during winter months). While consumers are increasingly buying organic food, domestic production has not kept pace. A range of customers would welcome establishing a commercial free-range organic chicken operation(s). Retail and restaurant venues are both eager for local organic meat. Raising free-range chicken is not a novel concept in the UAE, however achieving the required scale has not yet been accomplished. Demand already exists in the domestic market and, if commercial targets can be achieved, regional consumption could be a target as well.

4. Organic lassis, yoghurts, shakes and puddings.

Given how popular dairy is amongst consumers, and organic methods are increasingly in demand, it is a natural evolution to offer a variety of processed organic dairy products. Domestic dairies have heretofore been extremely innovative in introducing goods with different flavors and alternative sizes; yet none have ventured into organic milk. By introducing organic milk and processing it, along with locally produced organic fruits, local dairies could introduce another range of products with little competition. The current offerings available in retail locations are imported from Germany and elsewhere, whereas local producers are absent. With local dairies starting organic milk production, their prices would most certainly is competitive vis-à-vis the offerings in the Organic Foods & Café supermarket chains. Organic yoghurts and milkshakes blended with organic fruits come immediately to mind. Producing organic lassis, with a ready South Asian target market ready at hand, would also be a viable option. Yet a diary product category, which has barely been explored, is flavored puddings. In the United States and Europe, many different manufacturers have introduced dairy-based desserts aside from ice cream, which currently dominate the market in the UAE. Introducing a domestic range of products would be the next step in product diversification. Introducing organic dairy-based products would capitalize on two strong trends observed in the domestic market and compete with expensive imports only available in select stores. Domestic dairies, already innovative and resourceful, would be wise to expand their product offerings in the area.

5. Canned Soup.

The amount of domestically processed food available is impressively large; however, no canned soup is produced in the UAE. Imported canned soups are available in a variety of retail stores, yet none have penetrated the market in an appreciable way. The most popular soups are dehydrated ones from packets, with Maggi and Knorr dominating the market for prepared soup. The two brands, owned respectively by Nestle and Unilever, represent over 80% of the market in soup. While the climate favors cold versus warm soup, little gazpacho is available. Soups of better quality are primarily served in restaurants with ethnic themes. With few quality soups available in a market worth 20 million Dirhams, an opportunity exists to invest in domestic canned soup production. While soup is increasingly in demand among consumers who perceive it as a healthy snack, the dominance of dehydrated soup leaves significant room for growth for alternatives. Canned soup offers the possibility of including more vegetables and retaining more vitamins for the consumer. With a superior option that appeals to a more health-conscious consumer, canned soup is a segment with potential for expansion. Currently, the only canned-soup brand with significant market penetration is Campbell’s. With no domestic competitor in the marketplace, an attractive growth opportunity exists. In order for the manufacturer to be successful, it is paramount that they follow consumer trends and a stringent quality process. The variety of expats in the UAE allows for an opportunity to service multiple consumer tastes. Often consumers revert to brands available from their home countries, however these are often expensive and a local alternative is always in demand. If the local product offered is made with high-grade ingredients and goes through quality checks, many consumers will opt for the less expensive domestic brand. In addition to what is inside the can, an attractive and memorable design, pared with a good marketing campaign, will be proven way to attract consumers’ attention.

6. Water-free solutions for food preparations. Given how scarce water is in the UAE, any solution to reduce consumption is a worthwhile endeavor. Restaurants and work camp kitchens prepare a large portion of food consumed in the country, and therefore their water usage is of paramount importance. New rinse-free formulas for preparing fruits and

vegetables are available, and could drastically contribute to reducing overall water usage. Water-saving products are being experimented with; however, municipality authorities are unfamiliar with them. A product currently being used on a trail basis by some restaurants is Oxytech, which is a German chlorine-free food and vegetable disinfectant. Oxytech is based on hydrogen peroxide and silver, which are non-toxic ingredients that pose no health risk to consumers. The solution has no wastage after use, instead returning to hydrogen and oxygen after application. The company’s regional headquarters is based in Al Quoz area of Dubai and has already formed strategic partnerships across the GCC. While the product has shown promise, Dubai Municipality inspectors have shown resistance to a product they are unfamiliar with. Health authorities across the UAE should receive training on and provide encouragement for the roll out of such products. The benefit of saving an increasingly precious and valuable resource should be incentive enough. Yet without a federal initiative from the Ministry of Environment and Water or drastically increased water tariffs, nothing material will change. Given that water rates will not be increased for agricultural endeavors, it is safe to assume that fees for restaurants and work camp kitchens will remain stable. Oxytech, or a domestically produced alternative, could play a substantial role in curbing excessive water use and aiding the environment.

7. Farming tilapia, cobia and sea bream. While fish catches in Gulf waters have decreased in the Emirates, the consumption has continued to rise. Aquaculture is an option to counter rising imports of frozen fish, and is a budding industry in the UAE. Yet the few existing enterprises have seen their fair share of challenges in recent years. Red tides off of the Gulf of Oman decimated the previous large-scale farm and fish in the surrounding waters of Liwa. Yet this has not dissuaded all market participants, and in fact the largest caviar farm in the Middle East is currently being established in the UAE. With three commercial farms in various stages of expansion, the question remains of which fish species are best placed to be grown in the dominant environment.

Research centers in Abu Dhabi have studied the local water conditions and what inhibits the environment for fish cultivation. Besides red tides, rising temperatures and salinity levels in summer months is particularly challenging to fish stocks. The sturgeon farm is solving the problem by moving all of their fish tanks indoors. While hoped to be an alternative solution, hormonal injections have not been proven to help survival or development rates. Instead, particular type of fish that adapt well to the local climate and environmental conditions are the best way forward for large aquaculture endeavors. Three fish species have shown to be both suitable for cultivation and in demand by local consumers. Tilapia and cobia have both been featured in local research center studies and have shown particular promise. Seam bream is another type of fish, which has potential, and is already being raised in Mubarak fishery operations. In order to best support the development of aquaculture ventures, the local research centers and Emirate-specific extension services should work more closely to support them through imparting best practices and technology. Monitoring conditions and especially focusing on mitigation efforts vis-à-vis summer months is critical for aquaculture operation sustainability. Export Opportunities

1. Goat and Camel Milk Yoghurts and Ice Cream. As livestock numbers continue to increase in the UAE, using their byproducts effectively is paramount to extract as much value as possible. While goat milk is the highest type produced by volume, cow and camel milk are the primary varieties available in retail locations. Camel milk is perceived as a novel product beyond Arab consumers, and will gain popularity as it reaches European supermarket shelves. Yet as the marketing effort is underway to broaden camel milk’s exposure to a wider array of consumers, the question of product diversification arises. The benefits of camel milk, being easily digestible, higher in nutrition and lower in fat – could easily be enjoyed in alternative ways. Al Ain Dairy is already experimenting with camel milk ice cream, yet no other food processor has ventured into making camel milk yoghurts or smoothies. Foreign producers have successfully marketed goat milk yoghurt and ice cream, and two distinct brands are available in the UAE. The goat milk yoghurt is produced in the UK, while the US-produced goat milk ice cream is found in the

Organics Food & Café chain. Both items have a wide customer base, while being expensive given that they are chilled imported products. Producing a domestic alternative with the large quantities of goat milk available would be advisable. Given the popularity of goat’s milk in the Middle East, an Arab brand should face few hurdles to gain acceptance. Catering to local tastes, as with organic milkshakes and puddings, is of critical importance to achieve commercial success. Not only would the flavors need to match established trends, but appropriate animal feed would need to be utilized as well. For example, North American consumers are partial to grain-fed beef rather than grass-fed. Milk also takes on the taste of the animals’ feed. By carefully controlling animals’ feed as well as selecting appropriate flavors, goats’ and camels’ milk can be used to produce healthier and less expensive alternatives to import.

2. Date Feed Blend. Growing global livestock numbers are fed with grains and maize; however antibiotics are increasingly entering animals’ diets. Modern livestock rearing requires packed quarters, which increases the possibility of transmitted disease. Farmers are forced to protect their investments by feeding antibiotics to animals that shield them from disease but at the same time transmit them to consumers. The risk of passing through high amounts of medicinal quantities is especially high when animals are fed antibiotics three or four days prior to culling. Human beings are already consuming an abundance of antibiotics, so much so that certain types are no longer effective and viruses are mutating into deadlier forms. In order to reverse this damaging trend, dominant culling practices need to be revised. A primary method to challenge transference of antibiotics into the human food chain is to eliminate them from animal feed. Researchers in the UAE have found that date pits naturally contain many of the elements found in common antibiotics. Testing on chicken of date feed has proven to be effective in protecting the animals against Campylobacter, E. coli, Salmonella and Shigella. Given the early signs of effectiveness of a natural alternative, further conclusive research should be preformed.

With positive early signs, date pit feed for chickens and potentially other animals would be an excellent export venture for the UAE. With tens of thousands of date pits generated as a by-product of processing, the raw material can be found in abundance. The UAE University is in the process of patenting its findings, and it could easily license the production of a blended feed product for export. By mixing together crushed date pits, maize and other ingredients, it could market the feed in the UAE and the near abroad.