Twelfth Industrial Mathematical and Statistical Modeling ... · 10. Sivaramakrishnan, Kartik 11....

168

Technical Report #2006-6 July 24-August 1, 2006 Statistical and Applied Mathematical Sciences Institute PO Box 14006 Research Triangle Park, NC 27709-4006 www.samsi.info Twelfth Industrial Mathematical and Statistical Modeling Workshop for Graduate Students Editors: Alina Chertok, Mansoor A. Haider, Mette S. Olufsen and Ralph C. Smith This material was based upon work supported by the National Science Foundation under Agreement No. DMS-0112069. Any opinions, findings, and conclusions or recommendations expressed in this material are those of the author(s) and do not necessarily reflect the views of the National Science Foundation.

Transcript of Twelfth Industrial Mathematical and Statistical Modeling ... · 10. Sivaramakrishnan, Kartik 11....

Technical Report #2006-6July 24-August 1, 2006

Statistical and Applied Mathematical Sciences InstitutePO Box 14006

Research Triangle Park, NC 27709-4006www.samsi.info

Twelfth Industrial Mathematical andStatistical Modeling Workshop for

Graduate Students

Editors: Alina Chertok, Mansoor A. Haider,Mette S. Olufsen and Ralph C. Smith

This material was based upon work supported by the National Science Foundation under Agreement No.DMS-0112069. Any opinions, findings, and conclusions or recommendations expressed in this material are

those of the author(s) and do not necessarily reflect the views of the National Science Foundation.

i

Twelfth Industrial Mathematical and Statistical

Modeling Workshop for Graduate Students

July 24-August 1, 2006North Carolina State University

Raleigh, NC

Edited by Alina Chertock, Mansoor A. Haider, Mette S. Olufsen,and Ralph C. Smith

ii

iii

Participants

Students

1. Baker, Aditi, Montana State University2. Baker, Jeff, University of Alabama at Birmingham3. Barnard, Richard, Louisiana State University4. Belov, Sergei, Duke University5. Chen, Ye, Clarkson University6. Christov, Ivan, Texas A&M University7. Dediu, Simona, Rensselaer Polytechnic Institute8. Diver, Paul, Georgetown University9. Fertig, Elana, University of Maryland10. Gabrys, Robertas, Utah State University11. Geng, Weihua, Michigan State University12. Guevara, Alvaro, Louisiana State University13. Hariharan, Aneesh, Auburn University14. Hritcu, Roxana, Ohio University15. Jung, Minkyung, Indiana University16. King, David, Arizona State University17. Koskodan, Rachel, Texas Tech University18. Kulkarni, Mandar, University of Alabama at Birmingham19. Law, Jenny, Duke University20. Lee, Chung-min, Indiana University21. Li, Jing, UNC-Charlotte22. Li, Wanying, NCSU23. Mao, Wenjin, University of Colorado - Boulder24. Maslova, Inga, Utah State University25. Morowitz, Brent, Georgetown University26. Morton, Maureen, Michigan State University27. Murisic, Nebojsa, New Jersey Institute of Technology28. Owens, Luke, University of South Carolina29. Strychalski, Wanda, UNC-Chapel Hill30. Turkmen, Asuman, Auburn University31. Wang, Jian, University of Colorado - Boulder32. Wang, Ting, Kansas State University33. Wu, Qi, University of South Carolina34. Zhang, Joe, Purdue University35. Zhao, Gang, University of Louisville36. Zuo, Miao, Arizona State University

iv

Problem Presenters

1. Gadgil, Chetan and Potter, Laura, GlaxoSmithKline2. Jolly, Mark R. and Mellinger, Daniel, Lord Corporation3. Kennedy, Jon, MIT Lincoln Laboratory4. Maldague, Pierre, Jet Propulsion Laboratory5. Miller, Randy, Bank of America6. Ward, Carrie, Advertising.com

Faculty Consultants

1. Banks, H. T.2. Cherock, Alina3. Hu, Shuhua4. Langville, Amy5. Li, Zhilin6. Medhin, Negash7. Olufsen, Mette8. Pang, Tao9. Scroggs, Jeff10. Sivaramakrishnan, Kartik11. Smith, Ralph

v

Preface

This volume contains the proceedings of the Industrial Mathematical and Statistical Modeling Workshopfor Graduate Students that was held at the Center for Research in Scientific Computation at North CarolinaState University (NCSU) in Raleigh, North Carolina from July 24th to August 1st, 2006. This workshop wasthe twelfth to be held at NCSU and brought together 36 graduate students from a large number of graduateprograms including University of Alabama at Birmingham, Arizona State University, Auburn University, UNC-Chapel Hill, UNC-Charlotte, Clarkson University, University of Colorado-Boulder, Georgetown University,Indiana University, Kansas State University, Louisiana State University, University of Louisville, University ofMaryland, Michigan State University, Montana State University, New Jersey Institute of Technology, NorthCarolina State University, Ohio University, Purdue University, Rensselaer Polytechnic Institute, University ofSouth Carolina, Texas A&M University, Texas Tech University and Utah State University.

Students were divided into six teams to work on mathematical and statistical modeling problems presented,on the morning of the first day, by industrial scientists. In contrast to neat, well-posed academic exercises thatare typically found in coursework or textbooks, the workshop problems were challenging real-world problemsfrom industry that required the varied expertise and fresh insights of the group for their formulation, solutionand interpretation. Each group spent the first eight days of the workshop investigating their project and thenreported their findings in half-hour public seminars on the final day of the workshop.

The following is a list of the industrial presenters and the problems that they brought to the workshop:

• Carrie Ward (Advertising.com) Website Volume Prediction

• Randy Miller (Bank of America) Optimal Implied Views for Skewed Return Distributions

• Jon Kennedy (MIT Lincoln Laboratory) Bias Modeling in State Vector Estimation

• Pierre Maldague (Jet Propulsion Laboratory) Iterative Refinement Method for a Planning ProblemInvolving Resource Constraints

• Mark Jolly and Daniel Mellinger (Lord Corporation) Properties of a Gradient Descent Algorithmfor Active Vibration Control

• Chetan Gadgil and Laura Potter (GlaxoSmithKline) Analysis of Biological Interaction Networksfor Drug Discovery

These problems represent a broad spectrum of mathematical and statistical topics and applications. Whilethe problems included many aspects that are challenging to address in the nine-day duration of the workshop,the reader will observe remarkable progress on all the projects.

As the organizers, we strongly believe that this type of modeling workshop provides a highly valuable non-academic research related experience for graduate students that, simultaneously, contributes to the researchefforts of the industrial participants. In addition, the nature of this activity facilitates the development ofgraduate students’ ability to communicate and interact with scientists who are not traditional mathematicians,but require and employ mathematical tools in their work. Through this unique experience that exposesstudents to the means by which Mathematics is applied outside Academia, the workshop has helped manystudents formalize their career aspirations. In several cases, in past workshops, this help has been in the formof direct hiring by the participating companies. By broadening the horizon beyond that which is typically

vi

presented in mathematics graduate education, students interested in academic careers also find a renewedsense of excitement about applied mathematics and statistics.

Active participation of all involved during a nine day period of almost uninterrupted work, complementedby a series of social activities, greatly enhanced the success of the workshop. The organizers are most gratefulto the participants for their dedicated effort and contributions. Funding for the workshop was provided by theStatistical and Applied Mathematical Sciences Institute (SAMSI) with additional financial support, personnel,and facilities provided by the Center for Research in Scientific Computation (CRSC) and the Department ofMathematics at North Carolina State University. Finally, we would like to express our sincere gratitude to LesaDenning and Whitney Labarbera for their efforts and help in all administrative matters. We are also gratefulto John David for conducting the CRSC lab demonstration and to Brandy Benedict, Janine Haugh and SarahOlson for their assistance in providing transportation that helped make the workshop a great success.

Alina Chertock, Mansoor A. Haider, Mette S. Olufsen and Ralph C. SmithRaleigh, 2006

Contents

1 Website Volume Prediction 11.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.2 Fourier Transform Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.3 Velocity-Adjusted Moving Averages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.3.1 Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.3.2 Remarks and Accuracy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.4 Polynomial Fitting Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.4.1 Our Strategy for Special Scenarios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141.4.2 Simulation Result . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

1.5 Comparison . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181.6 Conclusion and Future Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

2 Optimal Implied Views for Skewed Return Distributions 232.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242.2 Minimum CV aR method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.2.1 Empirical Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 262.2.2 Parameterized Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 292.2.3 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

2.3 Minimizing the Tracking Error . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 342.3.1 Unconstrained Minimization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 342.3.2 Constrained Minimization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 372.3.3 The Inverse Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 372.3.4 Exact Mathematical Procedure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 412.3.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

2.4 Black-Litterman Approach with Extension to Higher Moments . . . . . . . . . . . . . . . . . . 422.4.1 Review of the BL Model and the EBL Model . . . . . . . . . . . . . . . . . . . . . . . . 432.4.2 Model Realization and Experimental Results . . . . . . . . . . . . . . . . . . . . . . . . 442.4.3 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

2.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

3 State Vector Estimation in Presence of Bias 533.1 Introduction and Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 543.2 Mathematical Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 543.3 Linearization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

vii

viii CONTENTS

3.3.1 Linearized Least Squares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 563.3.2 Weighted Least Squares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

3.4 Differential Evolution for Optimization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 583.5 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 653.6 Future directions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

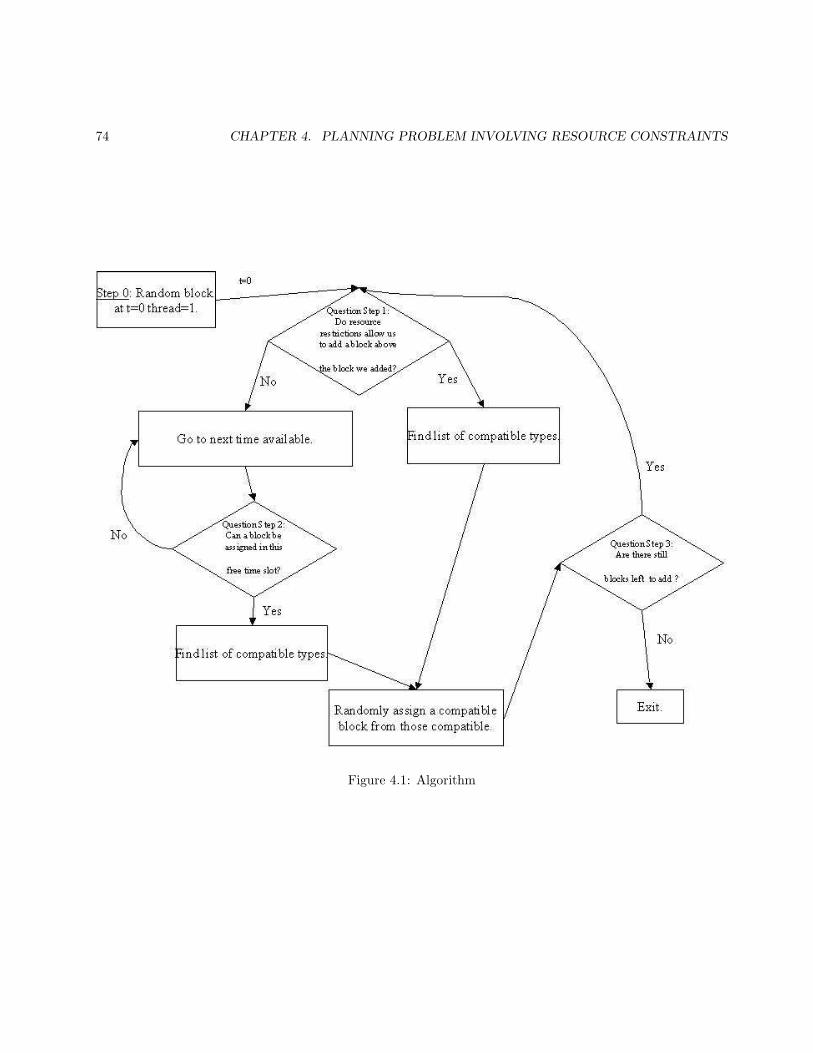

4 Planning Problem Involving Resource Constraints 694.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 704.2 Preliminaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

4.2.1 Definitions and explanation of terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 714.2.2 Problem Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

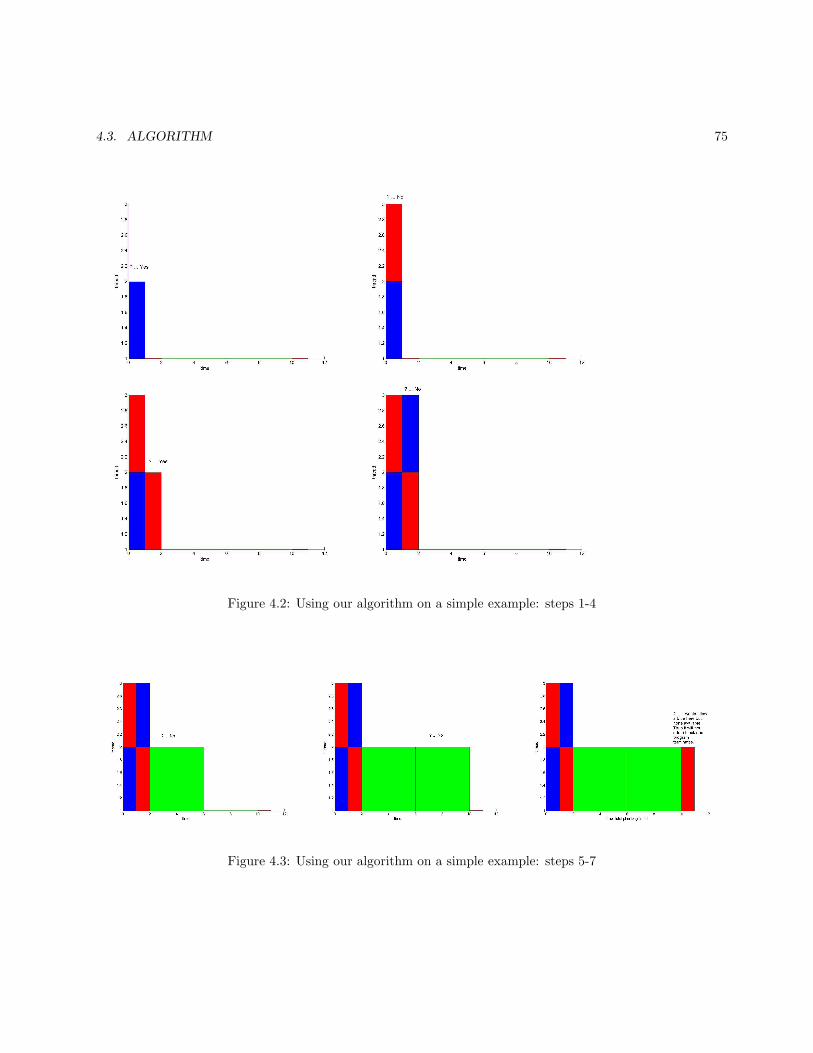

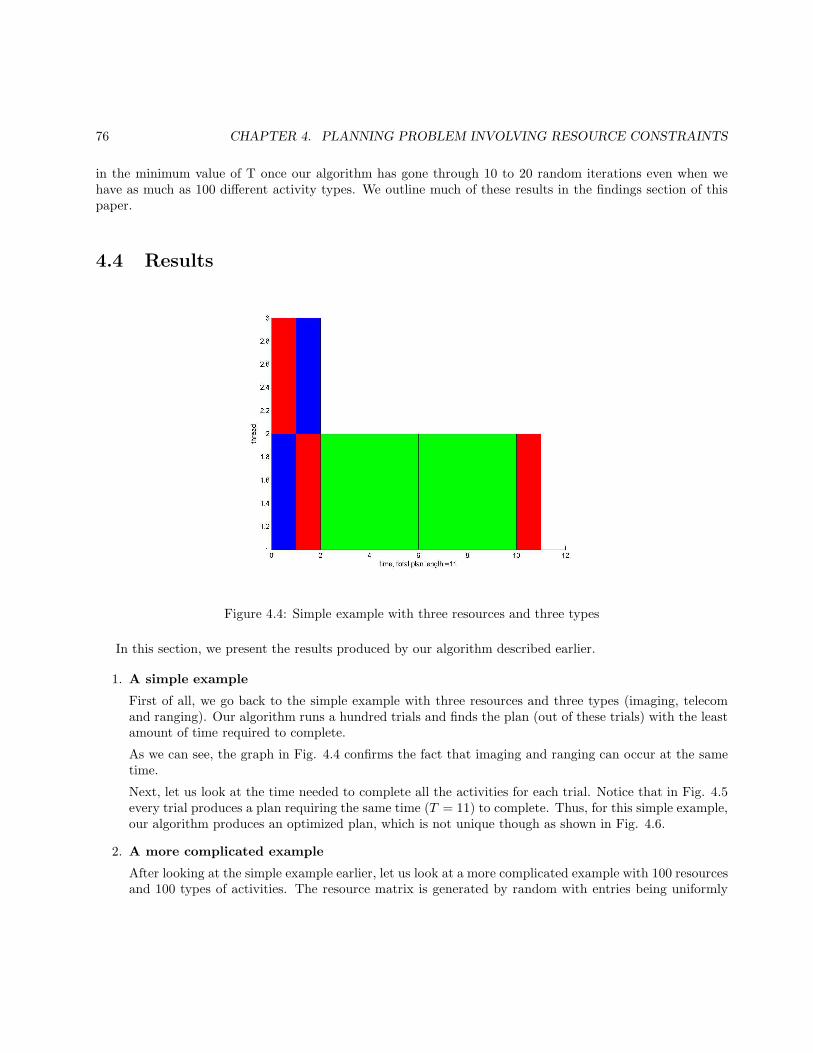

4.3 Algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 724.4 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 764.5 Future work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

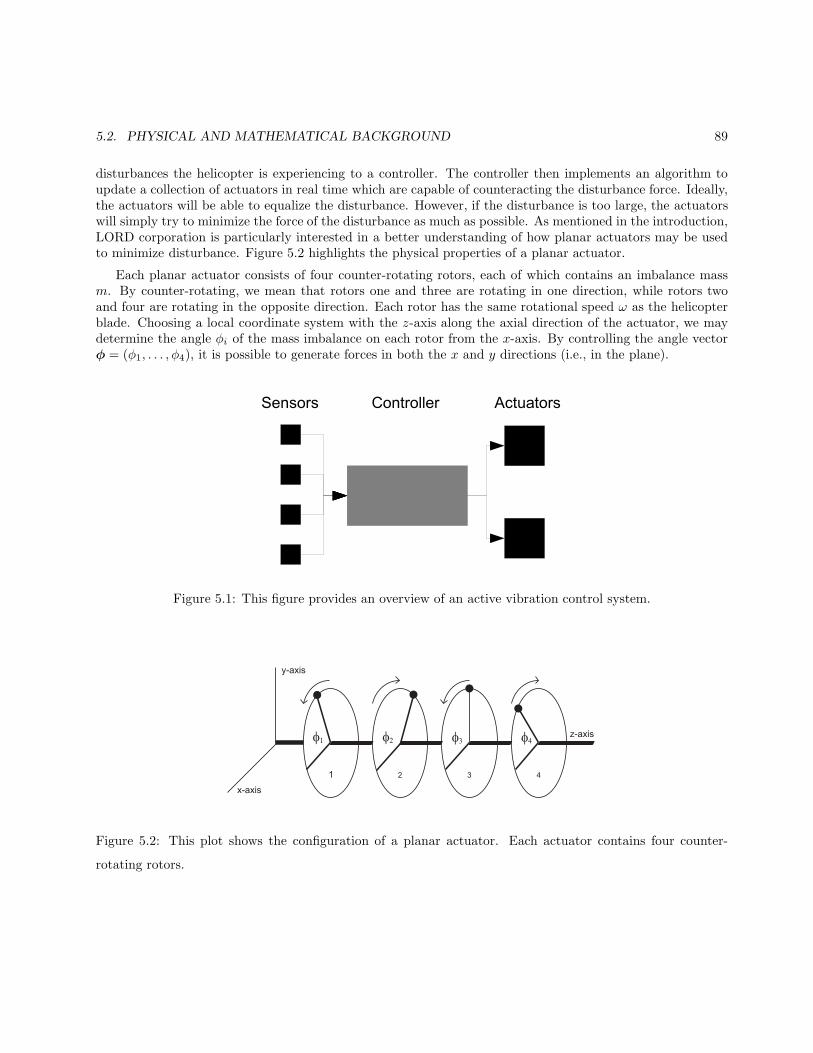

5 Properties of a Gradient Descent Algorithm 895.1 Introduction and Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 905.2 Physical and Mathematical Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

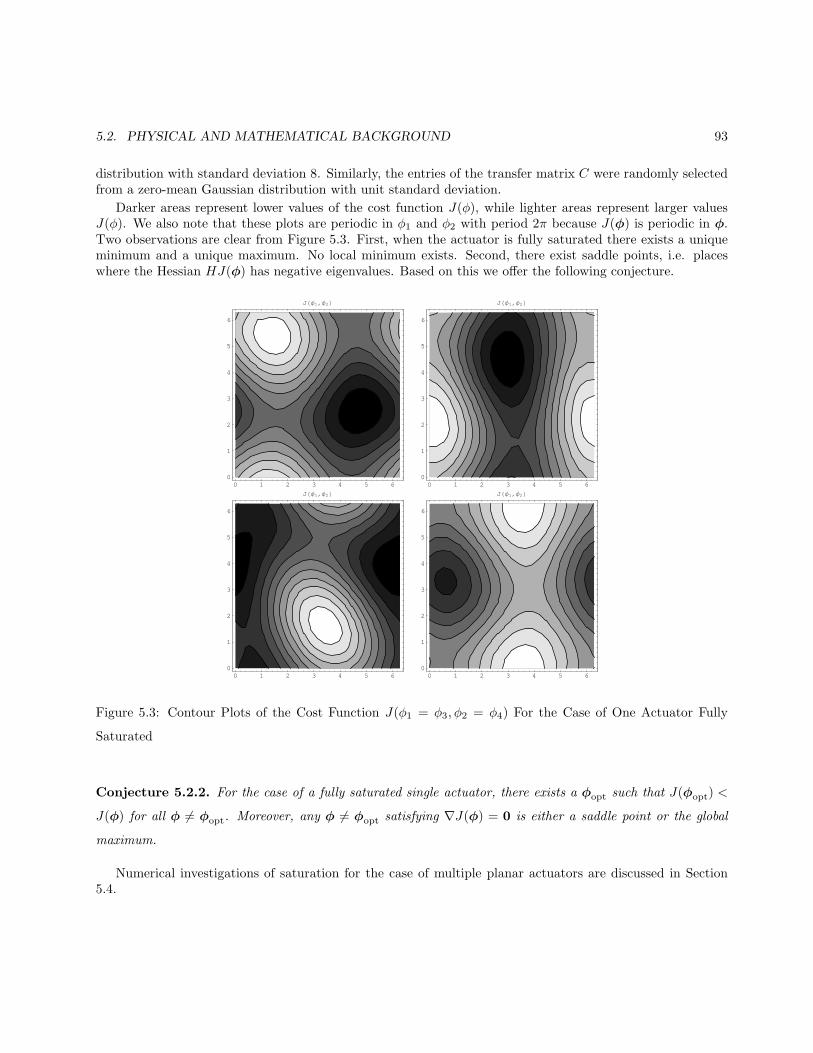

5.2.1 Mathematical Formulation of the Active Vibration Control System . . . . . . . . . . . . 925.2.2 A Comparison of Linear Actuators and Planar Actuators . . . . . . . . . . . . . . . . . 935.2.3 Saturation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

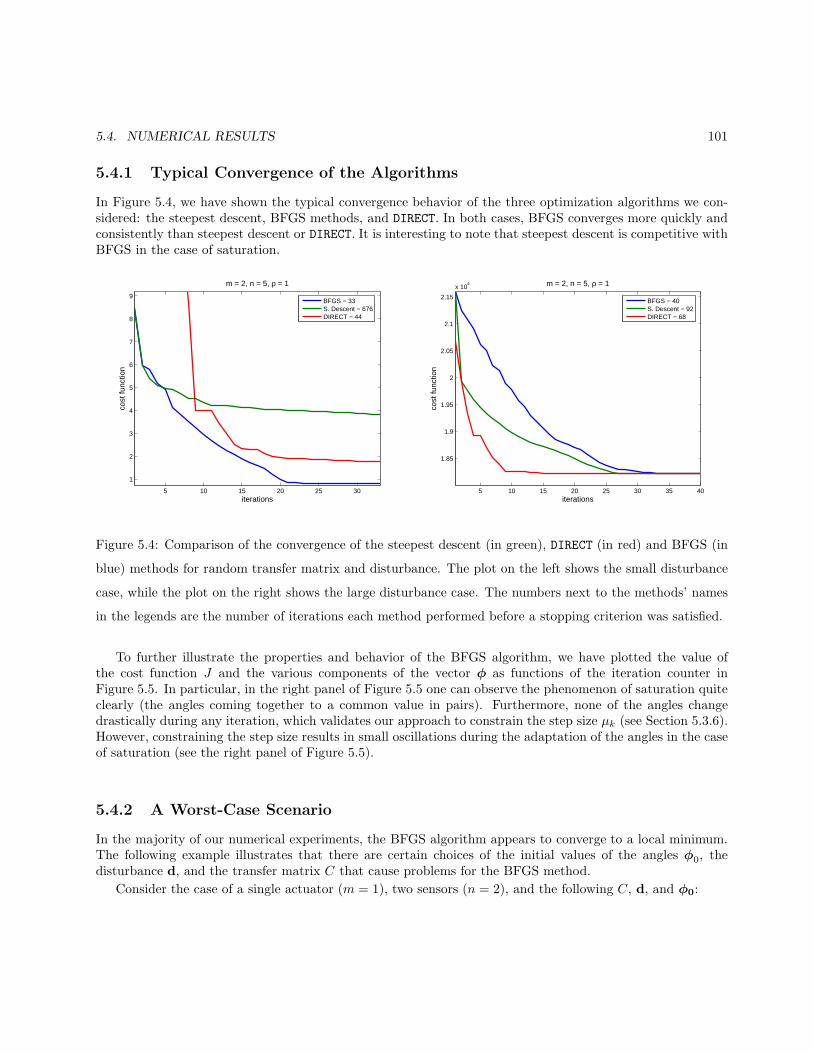

5.3 Numerical Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 965.3.1 The Method of Steepest Descent . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 965.3.2 Newton’s Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 975.3.3 The BFGS Quasi-Newton Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 975.3.4 Convergence of Descent Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 985.3.5 The Hessian . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1005.3.6 Decreasing the Step-Size to Satisfy Angular Constraints . . . . . . . . . . . . . . . . . . 1015.3.7 Global Minimization Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

5.4 Numerical Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1025.4.1 Typical Convergence of the Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . 1035.4.2 A Worst-Case Scenario . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1035.4.3 Modeling Error in the System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1055.4.4 Dependence of Jmin on n . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1065.4.5 Adapting to a changing disturbance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

5.5 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

6 Analysis of Biological Interaction Networks 1216.1 Introduction and Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1226.2 MAPK (Mitogen-Activated Protein Kinase) Model . . . . . . . . . . . . . . . . . . . . . . . . . 1236.3 Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

6.3.1 The L2 measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1236.3.2 Statistical measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1266.3.3 Skewness based measure within different classes . . . . . . . . . . . . . . . . . . . . . . . 1276.3.4 Measure of difference in frequency domain: Wavelet Index of the Change (WIC) . . . . 128

6.4 Generating Test Curves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

CONTENTS ix

6.4.1 Generated signal data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1296.4.2 MAPK knockout curves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

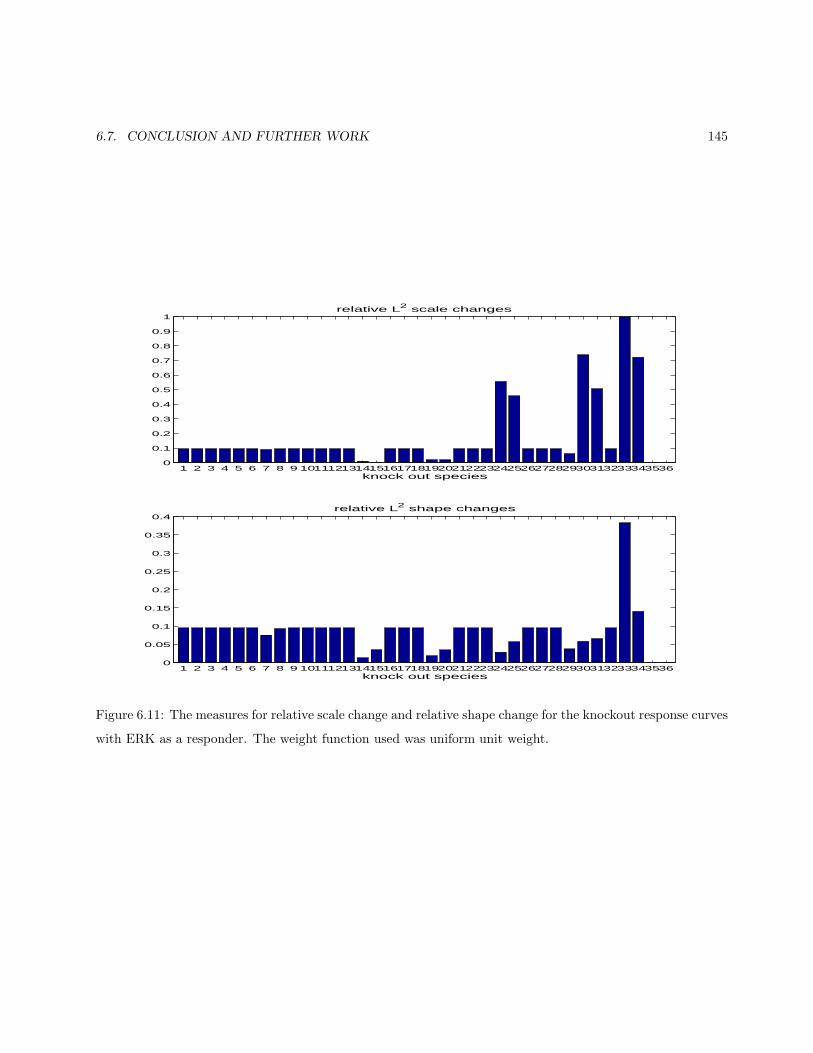

6.5 Simulation Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1296.5.1 Results of applying L2 measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1296.5.2 Results for applying statistical measures . . . . . . . . . . . . . . . . . . . . . . . . . . . 1316.5.3 Results for applying skewness based measure within different classes . . . . . . . . . . . 1316.5.4 Results for applying WIC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

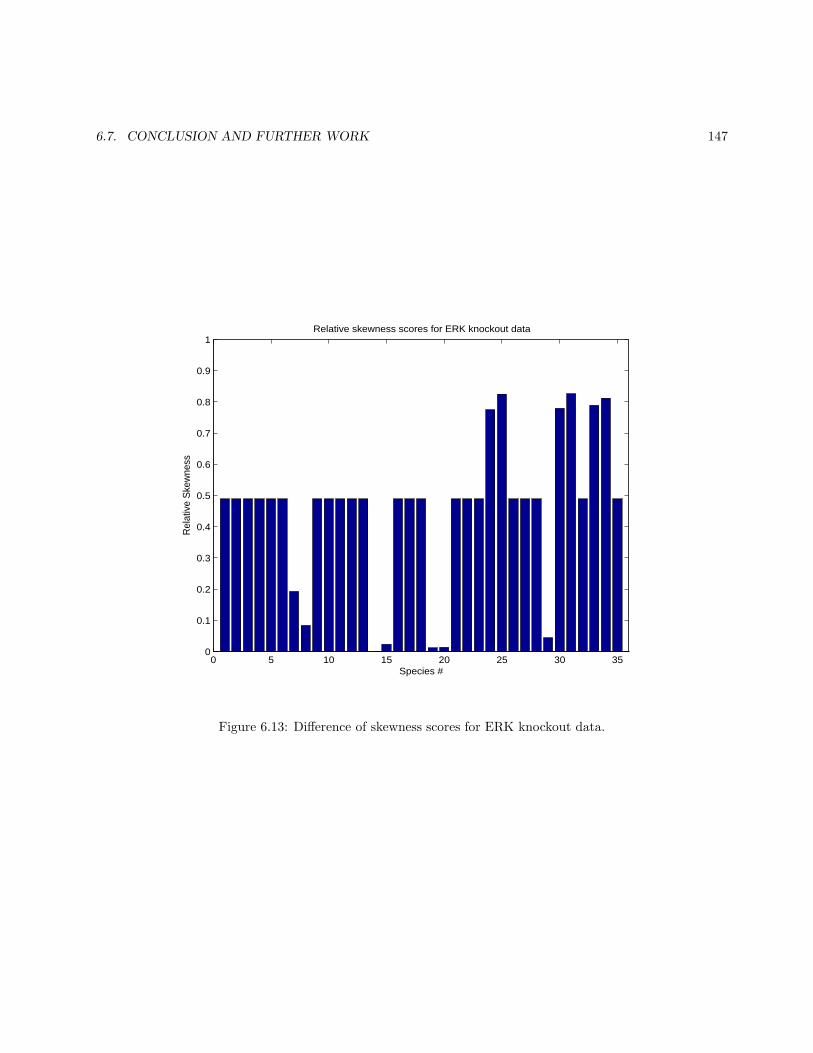

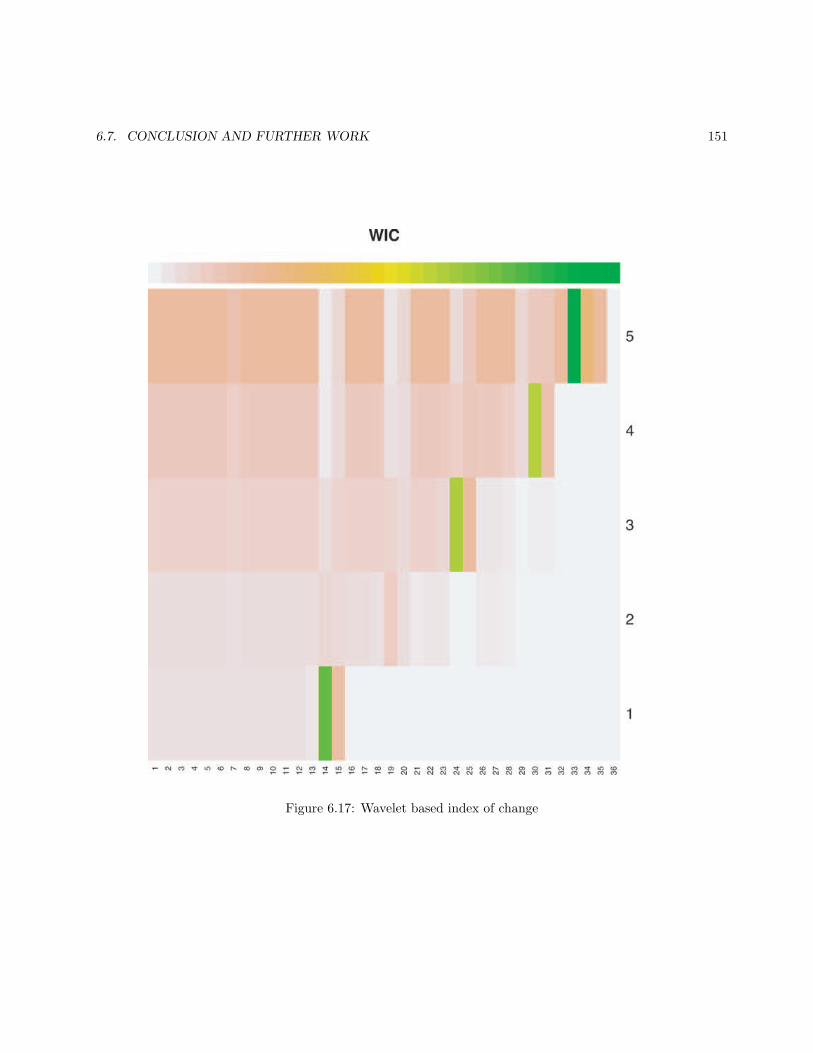

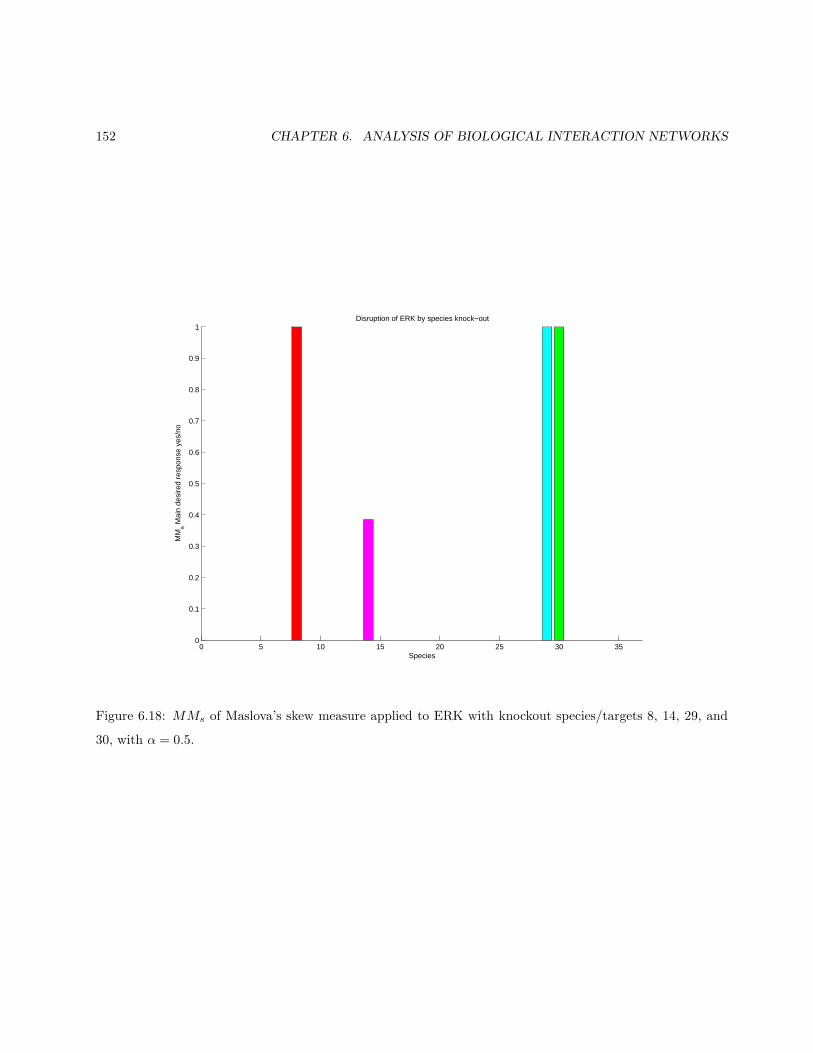

6.6 Measuring the Network Response and Identifying Target . . . . . . . . . . . . . . . . . . . . . . 1326.7 Conclusion and Further Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1356.8 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 158

x CONTENTS

Chapter 1

Website Volume Prediction

Richard Barnard1, Paul Diver2, Roxana Hritcu3, Asuman Turkmen4, Joe Zhang5, Gang Zhao6

Problem Presenter:Carrie Ward

Advertising.com

Faculty Consultants:Dr. Amy Langville

College of Charleston&

Dr. Zhilin LiNorth Carolina State University

Abstract

The volume of traffic on a particular website often follows some pattern such as Time of the Day (TOD)or Day of the Week (DOW) trends. We developed three mathematical models to capture these patterns, sowe can predict future volume based on previous data. The first model is based on Fourier transformations[7],[8], andFig. it shows good performance when the main frequency of the wave is relatively low. The secondmodel is based on velocity and can adjust the prediction with the latest available data. The third model usespolynomial fitting [5] to predict DOW behavior and will also adjust the predictions according to the latestdata.

1Louisiana State University2Georgetown University3Ohio University4Auburn University5Purdue University6University of Louisville

1

2 CHAPTER 1. WEBSITE VOLUME PREDICTION

1.1 Introduction

A significant number of firms, from small businesses to multinational corporations, use online advertising asa part of their marketing strategy. Online advertisements typically involve at least two separate firms: theadvertiser (or agency) which purchases or sponsors the advertisement and the publisher or network whichdistributes the advertisements for display. Advertising.com is a specialized company that mediates betweenadvertisers and publishers. Advertisers have to know exactly who saw an advertisement, how it impactedthem, what actions they took as a result, and what creative format worked best. Advertising.com providesanswers to these questions by accurately monitoring and measuring online performance and optimizing websiteplacements.

The volume of a certain website is defined as the number of visits to that specific site. Accurate estimatesfor the volume on the available web space in the network are required to allocate advertisements accordingly.Many factors can influence website volume trends such as sale of a publisher’s space directly to advertisers orto other networks. In addition, changes in time can cause fluctuations in the volume of the website.

This project aims to predict future website volume based on the knowledge of historical volumes. Thechallenge lies in making volume predictions robust to random or periodic shutdowns and state changes.Three methods are used to provide a model for volume predictions: a Fourier transform approach, veloc-ity/exponentially weighted moving average(V-EWMA) approach, and polynomial interpolation.

The Fourier transform approach fits a curve based on the given volumes by using the Fourier series toapproximate the curve. To reduce computation, only the most significant coefficients are included in themodel. The velocity-EWMA approach deals with non-periodic behavior by adjusting using a common movingaverage method. It takes into account the velocity of the recent data to predict new volumes. The polynomialfitting approach finds seven polynomials for each weekday and fits given data points well. The followingsections give detailed information on the proposed methods.

Real data sets are used to compare the performance of the three methods.

1.2 Fourier Transform Approach

Fig. 1.1 shows the original data of one particular website, that is referred to as niche67.The horizontal axis represents hours; hour 1 corresponds to the starting point of the data, 12:00 am on

6/24/2006, and the ending hour 729 represents the last recorded data point, 8:00 am on 7/24/2006. Thevertical axis is a particular website’s volume. We thought the first step to predict future volume would be tofind a pattern in historical data. Subsequently, we would try to find a function whose graph fits the historicaldata well.

From Fig. 1.1, we can observe a periodic pattern in the volume. Specifically, the website’s volume is quiteconsistent from one week to the next. Based on this observation, we thought it might be prudent to do aFourier transform on the historical data. Initially, we used a built-in Curve Fitting Tool(CFTOOL) interfacein Matlab to fit the data with Fourier transform. However, the maximum degree CFTOOL can offer forFourier fitting is 8 a nd our 1-month data contains 700+ hours. The 8-degree Fourier transform does not fitour data very well, which can be seen from Fig. 1.2.

To obtain a better fitting, we wrote a Matlab script which can use at most 728 degrees. When usingthis maximum, we observe that the Fourier transform is quite successful, as seen in Fig. 4.3. The absoluteerror between the data and fit is also plotted in Fig. 4.3 and is consistently on the scale of 10−9. However,the problem with this high degree transform is that there are more than 700 coefficients involved, which isobviously neither efficient nor convenient to deal with. As a result, we try to single out the most significant

1.2. FOURIER TRANSFORM APPROACH 3

0 100 200 300 400 500 600 700 8000

1

2

3

4

5

6

7

8

9

10x 10

6

Hour

Vol

ume

Original Website Volume

Figure 1.1: A Given Website Volume VS Hour

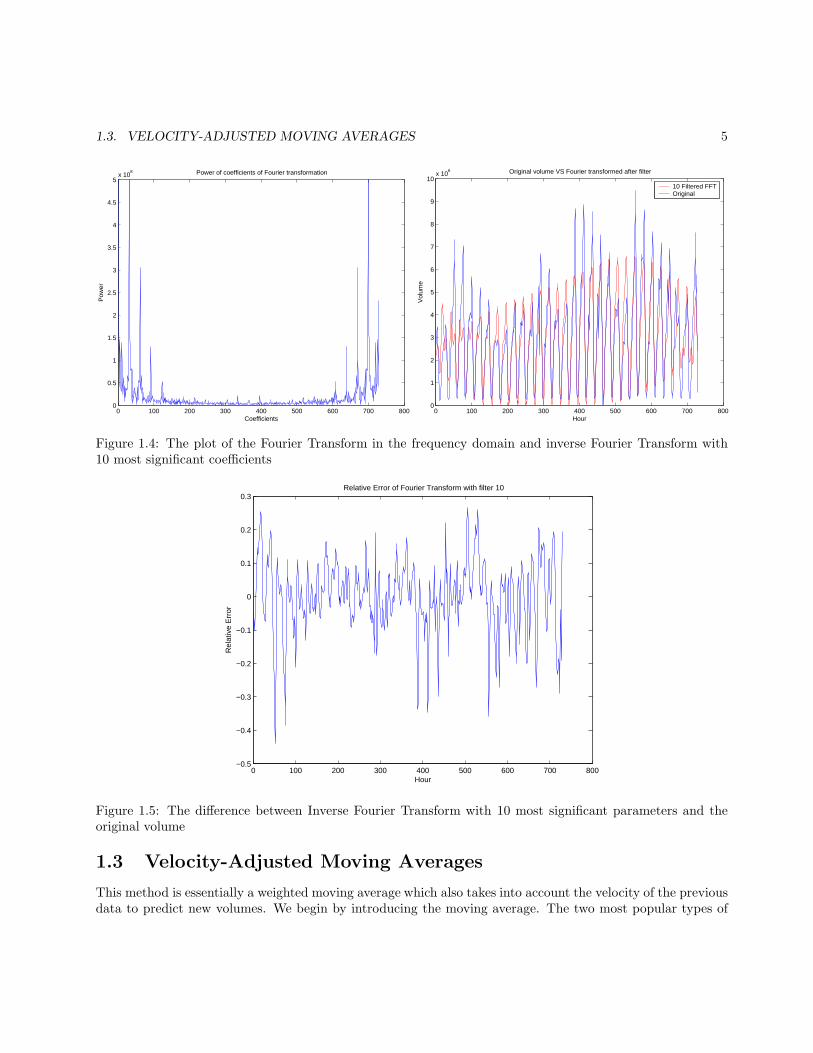

coefficients and filter out the unimportant ones. We measure the significance of each coefficient by calculatingthe square root of the sum of the squares for each pair of coefficients. As Fig. 1.4 suggests, we observe themajority of coefficients are quite small, only dozens of them are significant.

After singling out the 10 most significant coefficients, we overwrite the remaining coefficients with 0. Next,we do the Fourier transform using only these 10 coefficients. In Fig. 1.4, we observe the Fourier Transformwith filter 10 is roughly like the original curve. The shape is close, although the magnitudes differ at certainhours. To better measure the performance of the transform, we plot the relative difference at each hour inFig. 1.5. It shows, on average, the relative error is around 10%, which is quite good in most cases.

By keeping more coefficients, we could decrease the relative error. For example, Fig. 1.6 shows relativeerrors with filters of 50 and 100. They lower the relative error to around 6% and 3% respectively. The obvioustradeoff is between relative error and the number of coefficients kept. The Fourier Transform approach hasits advantages and disadvantages. On one hand, it provides very good curve fitting with low expense, whichcan be used to do analysis on historical data. On the other hand, the fitting curve is periodic in nature sinceFourier transform essentially is a linear combination of sine and cosine functions. In other words, if the periodis 700 hours, then the volume at hour 800 would be predicted to be identical to the volume at hour 100.Therefore, the Fourier approach would work best when the volume is periodic and consistent. If this is notthe case then other factors should be taken into consideration, such as the slope at the most recent hours.The approach with this adjustment will be discussed in the following section of this report.

4 CHAPTER 1. WEBSITE VOLUME PREDICTION

0 100 200 300 400 500 600 700

0

1

2

3

4

5

6

7

8

9

x 106

Vol vs. HourIndexfit 1

Figure 1.2: The filtered data using 8 selected coefficients, the solid line represents the fitting curve, and dotsdenotes the original data

0 100 200 300 400 500 600 700 8000

1

2

3

4

5

6

7

8

9

10x 10

6

Hour

Vol

ume

Fourier Transform on Volume

0 100 200 300 400 500 600 700 800−3

−2.5

−2

−1.5

−1

−0.5

0

0.5

1

1.5

2x 10

−9

Hour

Abs

olut

e E

rror

Absolute error between Fourier transformed and original volume

Figure 1.3: Left figure shows Fourier Transform on volume with 728 selected coefficients and right figure showsdifferences between Fourier transform and original volume

1.3. VELOCITY-ADJUSTED MOVING AVERAGES 5

0 100 200 300 400 500 600 700 8000

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5x 10

8

Coefficients

Pow

er

Power of coefficients of Fourier transformation

0 100 200 300 400 500 600 700 8000

1

2

3

4

5

6

7

8

9

10x 10

6

HourV

olum

e

Original volume VS Fourier transformed after filter

10 Filtered FFTOriginal

Figure 1.4: The plot of the Fourier Transform in the frequency domain and inverse Fourier Transform with10 most significant coefficients

0 100 200 300 400 500 600 700 800−0.5

−0.4

−0.3

−0.2

−0.1

0

0.1

0.2

0.3Relative Error of Fourier Transform with filter 10

Hour

Rel

ativ

e E

rror

Figure 1.5: The difference between Inverse Fourier Transform with 10 most significant parameters and theoriginal volume

1.3 Velocity-Adjusted Moving Averages

This method is essentially a weighted moving average which also takes into account the velocity of the previousdata to predict new volumes. We begin by introducing the moving average. The two most popular types of

6 CHAPTER 1. WEBSITE VOLUME PREDICTION

0 100 200 300 400 500 600 700 800−0.3

−0.25

−0.2

−0.15

−0.1

−0.05

0

0.05

0.1

0.15

0.2Relative Error of Fourier Transform with filter 50

Hour

Rel

ativ

e E

rror

0 100 200 300 400 500 600 700 800−0.15

−0.1

−0.05

0

0.05

0.1

0.15

0.2

0.25Relative Error of Fourier Transform with filter 100

HourR

elat

ive

Err

or

Figure 1.6: The difference between Inverse Fourier Transform with 50 (100) most significant parameters andthe original volume

the moving average method are the Simple Moving Average (SMA) and the Exponential Moving Average(EMA). A simple moving average is formed by computing the average (mean) volume of a website over aspecified number of periods. All moving averages are lagged indicators. To reduce the lag in simple movingaverages, one often uses exponential moving averages (also called exponentially weighted moving averages).EMA reduces the lag by applying more weight to recent volumes relative to older volumes. The calculationassociated with the EMA is much more expensive than the calculation using a SMA.

To predict the volume at a specified time, we average over multiple days the corresponding hour’s volume,that is

A(t) =

n∑

i=1

WiXi(t) (1.1)

where n is the total number of days we are using, Xi(t) is the niche’s volume of the ith day at the tth hour,and the Wi are the related weights via the exponentially weighted moving average algorithm (EWMA),

Wi = (1 − λ)λn−i. (1.2)

The weights decrease exponentially as we move further back in the past, so that more emphasis is put on recentdata. We then take the data from previous days and find the slope of the smoothing spline approximatingthe past data points to approximate the shift in velocities, which are called Vi(t). Taking the same weights asabove, we get the average slope by

S(t) =n∑

i=1

WiVi(t). (1.3)

This is used to obtain the velocity by evolving the previous volume along the slope,

V EL(t) = Xn(t− 1) + S(t). (1.4)

1.4. POLYNOMIAL FITTING METHOD 7

We repeat using the previous volume along with the current average slope to generate a prediction for thenext time period.

1.3.1 Methodology

The procedure runs as follows. We begin with a set of past data along with a weight and specified lag between1 and 4(though this is not capped). The process assumes that the delayed reception of data takes place slightlybefore the new prediction is made. We take the exponentially weighted moving average(EWMA) using theinputed constant.

Following this, we take the velocity average (VEL) described above and weight it using the same exponentialweight process. We take the mean of the two predictions for the first several iterations,

V (ti) =EWMA(ti) + V EL(ti)

2. (1.5)

After we begin receiving the delayed data, we slide the interval of past data forward to take the new informationinto account. Once we have this new data, we can evaluate how well our prediction fit the data at that time.Using this, we can weight our two predictions, EWMA(ti − j) and V EL(ti − j), using a lag of j hours. Wefind the appropriate β that solves

D(ti − j) = β(EWMA(ti − j)) + (1 − β)(V EL(ti − j)), (1.6)

where D(ti) is the actual data at time ti. If β ∈ [0, 1], we use this weight to make our latest prediction bytaking the weighted average of the two predictions. It can be seen that β > 1 implies that the weighted movingaverage is between the actual data and the velocity-based estimate and so we take only the weighted movingaverage in our new prediction. On the other hand, β < 0 implies that the velocity-based estimate is betweenthe data and the weighted moving average and so we take only this estimate for our prediction.

1.3.2 Remarks and Accuracy

After having run several sets of data through the process, we see that a combination of the two provides abetter estimate (Figs. 1.7-1.10).

A possible source for this improvement is that the velocity based prediction is able to adjust to a recentchange in volume magnitude. However, on its own it can be extremely erratic in terms of error, both relativeand absolute, as it can in a few time steps escape the actual data. This tends to be corrected by the weightedmoving average. We show the results from some simulated data. Each column of graphs corresponds to oneof the three prediction methods and the rows show actual volume, absolute error, and relative error:

R(ti) =|V (ti) −D(ti)|maxD(ti)

(1.7)

where V (ti) is the prediction given by the above process. The model does suffer a performance drop underlonger lag periods, but does perform better than the EWMA method on its own. The model tends to performworse when less data is available to make a prediction; however, this change is not great.

1.4 Polynomial Fitting Method

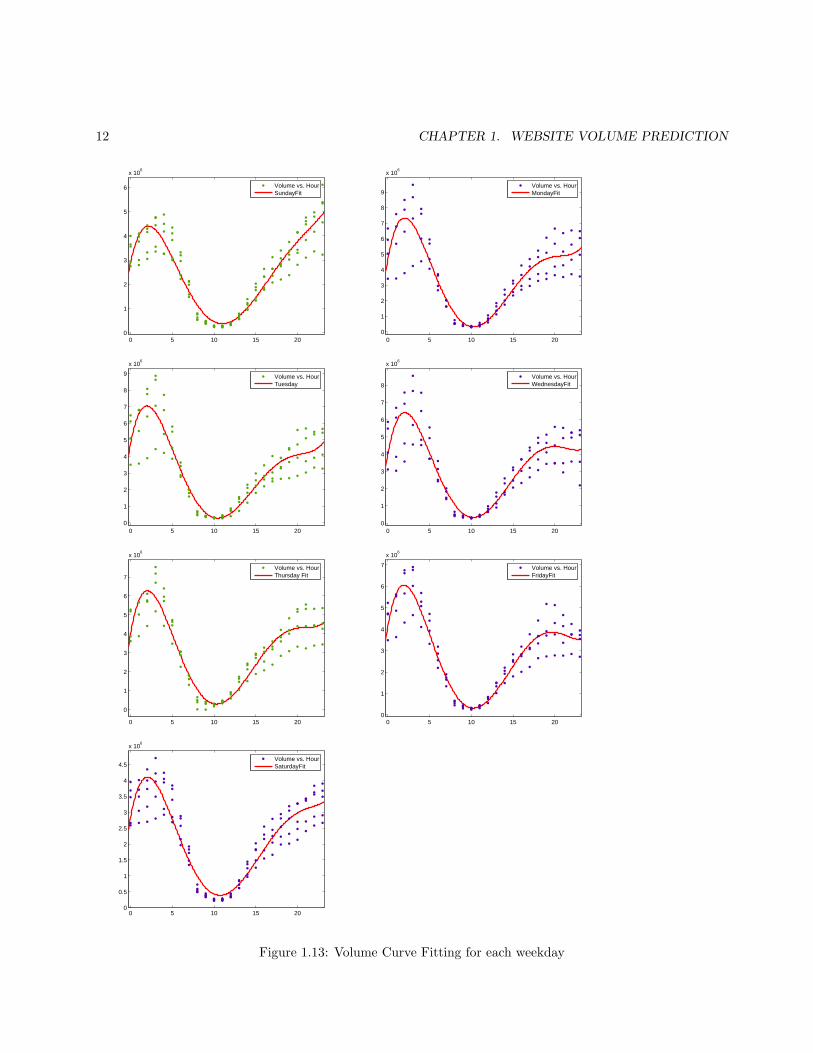

From Fig. 1.11 and Fig. 1.12, we can see that the volumes exhibit a weekly pattern. There are two peak values

8 CHAPTER 1. WEBSITE VOLUME PREDICTION

3.2042 3.2044 3.2046 3.2048

x 105

−5

0

5

10x 10

6 Velocities vs Data

Hour

Vol

ume

VelData

3.2042 3.2044 3.2046 3.2048

x 105

0

2

4

6

8x 10

6 EWMA vs Data

Hour

Vol

ume

3.2042 3.2043 3.2044 3.2045 3.2046 3.2047 3.2048

x 105

0

2

4

6

8x 10

6 Adjusted Average vs Data

Hour

Vol

ume

DataEWMA

DataAvg

3.2042 3.2043 3.2044 3.2045 3.2046 3.2047 3.2048

x 105

0

1

2

3

4x 10

6 Absolute Error of Velocity

Hour

Err

or

3.2042 3.2043 3.2044 3.2045 3.2046 3.2047 3.2048

x 105

0

1

2

3

4

5x 10

6 Absolute Error of EWMA

Hour

Err

or

3.2042 3.2043 3.2044 3.2045 3.2046 3.2047 3.2048

x 105

0

0.5

1

1.5

2

2.5x 10

6 Absolute Error of Average

Hour

Err

or

3.2042 3.2043 3.2044 3.2045 3.2046 3.2047 3.2048

x 105

0

0.1

0.2

0.3

0.4

0.5Relative Error of Velocity

Hour

Err

or

3.2042 3.2043 3.2044 3.2045 3.2046 3.2047 3.2048

x 105

0

0.2

0.4

0.6

0.8Relative Error of EWMA

Hour

Vol

ume

3.2042 3.2043 3.2044 3.2045 3.2046 3.2047 3.2048

x 105

0

0.1

0.2

0.3

0.4Relative Error of Average

Hour

Err

or

Figure 1.7: One month’s data used for predicting next day with one hour lag.

in each day: early morning and late night. At noon, volume reaches its lowest point of the day. For differentweekdays, we can see that peak values are quite different. But for the same weekday of different weeks, wecan see the peak values are similar.

Based on this observation, we model these weekdays separately. In Fig. 1.13, we can see 5th-order polyno-mial curve fitting for each weekday based on four weeks data. The common formula for 5th-order polynomialcurve fitting is as follows:

V = f(t) = p5t5 + p4t

4 + p3t3 + p2t

2 + p1t+ p0. (1.8)

1.4. POLYNOMIAL FITTING METHOD 9

3.2042 3.2044 3.2046 3.2048

x 105

−4

−2

0

2

4

6

8x 10

6 Velocities vs Data

Hour

Vol

ume

VelData

3.2042 3.2044 3.2046 3.2048

x 105

0

2

4

6

8x 10

6 EWMA vs Data

Hour

Vol

ume

3.2042 3.2044 3.2046 3.2048

x 105

0

2

4

6

8x 10

6 Adjusted Average vs Data

Hour

Vol

ume

DataEWMA

DataAvg

3.2042 3.2044 3.2046 3.2048

x 105

0

1

2

3

4

5

6x 10

6 Absolute Error of Velocity

Hour

Err

or

3.2042 3.2044 3.2046 3.2048

x 105

0

1

2

3

4

5x 10

6 Absolute Error of EWMA

Hour

Err

or

3.2042 3.2044 3.2046 3.2048

x 105

0

1

2

3

4

5x 10

6 Absolute Error of Average

Hour

Err

or

3.2042 3.2044 3.2046 3.2048

x 105

0

0.2

0.4

0.6

0.8Relative Error of Velocity

Hour

Err

or

3.2042 3.2044 3.2046 3.2048

x 105

0

0.2

0.4

0.6

0.8Relative Error of EWMA

Hour

Vol

ume

3.2042 3.2044 3.2046 3.2048

x 105

0

0.2

0.4

0.6

0.8Relative Error of Average

Hour

Err

or

Figure 1.8: Same month’s data used for predicting next day with four hours lag.

10 CHAPTER 1. WEBSITE VOLUME PREDICTION

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

−2

0

2

4

6x 10

6 Velocities vs Data

Hour

Vol

ume

VelData

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

2

4

6x 10

6 EWMA vs Data

Hour

Vol

ume

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

2

4

6x 10

6 Adjusted Average vs Data

Hour

Vol

ume

DataEWMA

DataAvg

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.5

1

1.5

2

2.5

3x 10

6 Absolute Error of Velocity

Hour

Err

or

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.5

1

1.5

2

2.5

3x 10

6 Absolute Error of EWMA

Hour

Err

or

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.5

1

1.5

2x 10

6 Absolute Error of Average

Hour

Err

or3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.1

0.2

0.3

0.4Relative Error of Velocity

Hour

Err

or

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.2

0.4

0.6

0.8Relative Error of EWMA

Hour

Vol

ume

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.1

0.2

0.3

0.4Relative Error of Average

HourE

rror

Figure 1.9: Four days data used for predicting next day with one hour lag.

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

−2

0

2

4

6x 10

6 Velocities vs Data

Hour

Vol

ume

VelData

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

2

4

6x 10

6 EWMA vs Data

Hour

Vol

ume

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

2

4

6x 10

6 Adjusted Average vs Data

Hour

Vol

ume

DataEWMA

DataAvg

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

1

2

3

4x 10

6 Absolute Error of Velocity

Hour

Err

or

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

1

2

3

4x 10

6 Absolute Error of EWMA

Hour

Err

or

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

1

2

3

4x 10

6 Absolute Error of Average

Hour

Err

or

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.2

0.4

0.6

0.8Relative Error of Velocity

Hour

Err

or

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.2

0.4

0.6

0.8Relative Error of EWMA

Hour

Vol

ume

3.1984 3.1985 3.1986 3.1987 3.1988

x 105

0

0.2

0.4

0.6

0.8Relative Error of Average

Hour

Err

or

Figure 1.10: Four days data used for predicting next day with four hours lag.

1.4. POLYNOMIAL FITTING METHOD 11

0 5 10 15 20 25 300

2

4

6

8

10x 10

6

Vol

ume

Day

Figure 1.11: Volume changes in a month

0 50 100 150 2000

2

4

6

8

10x 10

6

Hour

Vol

ume

First WeekSecond WeekThird WeekFourth week

Figure 1.12: Volume changes in a week

12 CHAPTER 1. WEBSITE VOLUME PREDICTION

0 5 10 15 200

1

2

3

4

5

6

x 106

Volume vs. HourSundayFit

0 5 10 15 200

1

2

3

4

5

6

7

8

9

x 106

Volume vs. HourMondayFit

0 5 10 15 200

1

2

3

4

5

6

7

8

9

x 106

Volume vs. HourTuesday

0 5 10 15 200

1

2

3

4

5

6

7

8

x 106

Volume vs. HourWednesdayFit

0 5 10 15 20

0

1

2

3

4

5

6

7

x 106

Volume vs. HourThursday Fit

0 5 10 15 200

1

2

3

4

5

6

7

x 106

Volume vs. HourFridayFit

0 5 10 15 200

0.5

1

1.5

2

2.5

3

3.5

4

4.5

x 106

Volume vs. HourSaturdayFit

Figure 1.13: Volume Curve Fitting for each weekday

1.4. POLYNOMIAL FITTING METHOD 13

Day P5 P4 P3 P2 P1 P0Sunday 26.27 -1903 4.937e+004 -5.139e+005 1.6e+006 2.888e+006Monday 68.45 -4605 1.098e+005 -1.054e+006 3.048e+006 4.646e+006Tuesday 61.35 -4120 9.833e+004 -9.451e+005 2.682e+006 4.74e+006Wednesday 57.29 -3930 9.51e+004 -9.224e+005 2.707e+006 3.978e+006Thursday 56.07 -3817 9.193e+004 -8.892e+005 2.587e+006 3.982e+006Friday 51.55 -3529 8.496e+004 -8.157e+005 2.296e+006 4.102e+006Saturday 27.07 -1920 4.823e+004 -4.843e+005 1.429e+006 2.829e+006

Table 1.1: The coefficients for the polynomial fit in Fig. 1.13

Day SSE R-square Adjusted R-square RMSESunday 3.539e+013 0.8792 0.8739 5.572e+005Monday 9.973e+013 0.8115 0.801 1.053e+006Tuesday 8.127e+013 0.8282 0.8187 9.503e+005Wednesday 8.419e+013 0.7918 0.7803 9.672e+005Thursday 4.36e+013 0.879 0.8723 6.96e+005Friday 3.525e+013 0.8863 0.88 6.259e+005Saturday 2.589e+013 0.8655 0.8596 4.766e+005

Table 1.2: Measures of fit for the polynomial curve fitting seen in Fig. 1.13.

We used a 5th-order polynomial to fit the data in each weekday, which resulted in 7 polynomial functions.Their parameters are listed in Table 1.1 and the goodness of fit is shown in Table 1.2. We use f(t, i), i ∈0, 1, ..., 6 to denote the curve we use to base our prediction on data from the ith day of week (Sunday is the0th day and Saturday is the 6th day). For instance, f(t, 0) represents the curve we get based on data fromSundays.

So the predicted volume can be obtained by

V = f(t, i) = p5(i)t5 + p4(i)t

4 + p3(i)t3 + p2(i)t

2 + p1(i)t+ p0(i). i ∈ 0, 1, ..., 6, t ∈ 0, 1, ..., 23. (1.9)

pj(i) represents the parameter pj on the ith day of the week. However, the theory value usually does not fitthe actual volume very well and we need to adjust our prediction based on the difference between actual valueand predicted value. There are several methods available to do that, however, we have focused on the movingaverage method. For our method, we assume that the curve for each weekday will stay almost the same.However, we will also take the difference between actual value and predicted value into account. So we willapply the weight vector to the theory value and previous volumes. For example, suppose we use the previoustwo weeks’ data to predict the volume with weight vector [0.1, 0.3, 0.6]. On the same day in the previous twoweeks, volumes are V ol((t−7)∗ 24) and V ol((t−2)∗ 7 ∗ 24)(t is the current hour, i denotes on which day t is),respectively. Then the predicted volume is PreV (t) = 0.6f(t mod 24, i) + 0.3V ol((t − 7) ∗ 24) + 0.1V ol((t −2) ∗ 7 ∗ 24).

14 CHAPTER 1. WEBSITE VOLUME PREDICTION

1.4.1 Our Strategy for Special Scenarios

The algorithm we discussed above does not account for some special cases of website volume behavior. Inorder to address these situations, we have added automatic adaption into our algorithm.

1. Periodical Shutdown

If the period for the shutdown is exactly one week, our algorithm can work without adjustment. However,if the period is not one week, our assumption that the volume will follow DOW is no longer true. We usuallycannot pinpoint the time when a server is shut down. We can get the period T of shutdown according to thepoints where volume is zero. Assuming we want to predict ith-hour’s volume, we will apply the weight vectorto i − T , i − 2T , i − 3T . This way, we can make the prediction match the actual volume accurately. Thefollowing function can give us the prediction,

PreV (t) = V ol(t− T ) ∗W (1) + V ol(t− 2T ) ∗W (2) + V ol(t− 3T ) ∗W (3), (1.10)

where PV (i) is the predicted volume for hour t, V (t) is real volume in hour t and W (i) is the weightvector’s ith element.

0 100 200 300 400 500 600 700−0.5

0

0.5

1

1.5

2

2.5

3

3.5x 10

4

Hour

Vol

ume

actual volumepredicted volumedifference

Figure 1.14: Prediction for periodic shutdown (based on two weeks data we predict the coming two week’svolume)

From Fig. 1.14, we can see that our strategy works well in this scenario.

2. Random Shutdown

For random shutdown, we did not find a very effective method. However, we assume that a website’svolume pattern will remain similar. So if we want to predict a website’s volume after a shutdown S, we willtrace back to find the latest shutdown S1 and use S1’s volume as the prediction. We did not realize this in

1.4. POLYNOMIAL FITTING METHOD 15

our algorithm. On the other hand, when we get some data indicating the volume for a website is quite low,the program will generate a warning.

3. State Change

When a website’s volume pattern changes suddenly, our algorithm will fail to predict a reasonable volumefor a website. We assume that the shape will stay the same although the magnitude will change. So we willchange the parameters of the seven curves for each weekday accordingly.

Now we determine a scale factor according to the ratio r of average volume in the past one day to theaverage volume in the past one week. If r > 1.6 or r < 0.6, we will multiply pi(i ∈ 0, 1, ..., 5) by r. We canexpress the function as follows:

r =

1

24

24−1∑

i=0

(PreV (t− l − i) − V ol(t− l− i))

1

168

7∗24−1∑

i=0

(PreV (t− l − i) − V ol(t− l − i))

(1.11)

V ol(i) is the real volume in the ith hour. PreV (i) is the predicted volume for the ith hour. l is the time lag.Fig. 1.15 shows an example of a prediction when volume increases dramatically. We can see that the

prediction follows the actual volume curve.

0 100 200 300 400 500 600 700−4

−2

0

2

4

6

8

10x 10

6

Hour

Vol

ume

actual volumepredicted volumedifference

Figure 1.15: Prediction for state change, volume increases significantly(based on two weeks data we predictthe coming two weeks volume)

Fig. 1.16 shows an example of prediction when volume decreases dramatically.

16 CHAPTER 1. WEBSITE VOLUME PREDICTION

0 200 400 600 800−4

−2

0

2

4

6

8x 10

6

Hour

Vol

ume

actual volumepredicted volumedifference

Figure 1.16: Prediction for state change, volume decreases significantly (based on two weeks data we predictthe coming two weeks volume)

4. Slight State Change

If the data we use is slightly different from the incoming data, we adjust our prediction according to thefollowing three measures:

First, if the hour to be predicted (we use t to represent it) is within rush hours (i.e. 19-6 GMT, thoughwe can adjust the definition according to specific time zones), we will adjust the prediction according to theprediction error in the latest three hours, i.e. from t− l− 2 to t− l (l is the data lag) if these three hours arein the rush hours. Before denoting the adjustment, we define function IsRushHour(t) first,

IsRushHour(t) =

1, if t is between 19pm and 6am0, otherwise

(1.12)

ErrorPercent1 =

2∑

j=0

(PreV (t− l − j) − V ol(t− l − j))

maxVIsRushHour(t− l − j)

∑2h=0 IsRushHour(t− l − h)

(1.13)

Adjust1 =

−MaxV ∗ ErrorPercent, if ErrorPercent1′s absolute value is bigger than 0.050, otherwise

(1.14)

where

maxV = Max(V ol(t− l − i)), 0 ≤ i ≤ 7 ∗ 24 (1.15)

1.4. POLYNOMIAL FITTING METHOD 17

Second, if the hour to be predicted is within rush hours(i.e. 19-6 GMT), we will adjust the predictionaccording to prediction error in the past t− 25 to t− 23 hours if these hours are in the rush hours.

ErrorPercent2 =

1∑

j=−1

(PreV (t− 24 − j) − V ol(t− 24 − j))

maxVIsRushHour(t− 24 − j)

∑1h=−1 IsRushHour(t− 24 − h)

(1.16)

Adjust2 =

−MaxV ∗ ErrorPercent, if ErrorPercent2′s absolute value is bigger than 0.050, otherwise

(1.17)

Third, we will adjust the prediction according to the average error in the past day if the average error isbigger than some threshold.

Adjust3 = −

23∑

j=0

(PreV (t− 24 − j) − V ol(t− 24 − j))

24(1.18)

Then we will add a weighted average of three adjustments to the prediction.

Adjust = W1 ∗Max(Adjust1, Adjust2) +W2 ∗Adjust3. (1.19)

Fig. 1.17 shows an example.

0 100 200 300 400 500 600 700−4

−2

0

2

4

6

8

10x 10

6

Hour

Vol

ume

actual volumepredicted volumedifference

Figure 1.17: Prediction for state slight change (based on two weeks data we predict the coming two weeksvolume)

18 CHAPTER 1. WEBSITE VOLUME PREDICTION

5. Special Days

For special days such as Mother’s Day, Independence Day etc., we need data on these days to predictwhether they follow some pattern. If they follow the same pattern, we can use previous special days to predictthe coming special day. If not, we check whether some special day has similar features. For instance, we checkall Mother’s Days in the past.

1.4.2 Simulation Result

In Fig. 1.18, we can see an example of our prediction using our method with weight vector [0.05, 0.2, 0.8, 0.05].Based on data in the past three weeks and the volume we calculated from the fitting curves, we take weightedaverage and get our prediction. We can see that our prediction follows the actual curve well. However, thedifference is large when there is a dramatic change.

0 100 200 300 400 500 600 700 800−2

0

2

4

6

8

10x 10

6

Hour

Vol

ume

actual volumepredicted volumedifference

Figure 1.18: Prediction based former three weeks’ data for the coming one week

In Fig. 1.19, we show the average errors of moving averages under different weight averages. The vector[0.5, 0.5, 0] corresponds to the simple moving average method. It takes the average volume of the past twoweeks on the same day as the prediction value and involves no curve fitting. We can see that when the weightfor the theory value obtained from Eqn. 1.9 increases, the average error decreases except when its weight is0.1. When the weight for the most recent data is large, average error is even worse than the SMA. However,we cannot say that when the weight for the theory value is large, WMA will perform better than it will whenthe weight for the theory value is small. We need other standards to evaluate this method.

1.5 Comparison

If we compare these three approaches, we see each has its advantages and disadvantages.

1.5. COMPARISON 19

0 2 4 6 8 10 12 14 16 180

0.5

1

1.5

2

2.5

3x 10

6

website

aver

age

erro

r

[0.5 0.5 0][0.2 0.4 0.4][0.1 0.6 0.3][0.1 0.3 0.6][0.1 0.8 0.1][0.1 0.1 0.8]

Figure 1.19: Average Error of moving average method with different weight vector for 18 websites

The Fourier transform approach requires the largest amount of data to observe a possibly periodic patternand the corresponding length of each period. Therefore, if we have several months’ or years’ data, and we wantto have a long-term picture about website volume, then we can try the Fourier transform to fit the historicaldata and predict the future based on the filtered Fourier function. However, the Fourier transform approachis not good at predicting short-term volume since it is not sensitive to the most recent trend.

To predict website volume in the coming hours, Velocity-Adjusted Moving Average approach would be thebest choice. This approach only requires historical data from the past couple of days, instead of data frompast years as required by the Fourier transform approach. However it becomes more accurate with more data,reaching reasonable errors with 2-4 weeks of data. Another advantage is that it catches the current trendvery well. It takes the slope, i.e. the velocity of volume into consideration, and predicts future volume basedon the weighted average of Exponentially Weighted Moving Average and Velocity Average. In particular, theweight is dynamically decided based on the most recent incoming data. This approach is more accurate whenpredicting short period and becomes less reliable when the prediction period becomes longer, because the errorfrom each step accumulates and could become quite large after a couple of weeks.

The Polynomial Fitting lies somewhere in the middle between Fourier Approach and Velocity-AdjustedMoving Average approach. It requires several weeks’ instead of years’ or days’ historical data to do theprediction. Contrast to Velocity-Adjusted Moving Average approach, it is capable of predicting longer period.With two weeks’ historical data, we have predicted the following two weeks’ volume with satisfactory relativeerrors. Another nice feature is that this approach includes a prediction tube, or range, which is used todetects slight state change and drastic state change. Then it handles them separately. For slight state change,it makes prediction adjustments based on recent prediction errors. For a large state change, it calculatesthe multiplier and imposes it on the original polynomial. The major drawback of this approach is that itcan not effectively deal with sudden drastic pattern changes, which includes not only magnitude changes butalso shape changes. Fortunately, this situation doesn’t happen very often in most websites. When this does

20 CHAPTER 1. WEBSITE VOLUME PREDICTION

happen, the Velocity-Adjusted Moving Average can be applied to make short-term prediction.Based on business needs and historical data, and how long we want to predict into the future, we can make

the best choice among these three approaches.

1.6 Conclusion and Future Work

For the second and third model, we simply fixed some parameters and so these parameters are likely notoptimal. Probably we should study the relationship between the optimal value and different configurationsand develop some strategy to adjust our parameters to achieve the best performance. Moreover, we shouldrun our program with large real historical data to see their average performance. Finally, we should realizethe Kalman Filter method and compare its performance with ours.

Bibliography

[1] “Moving average”, http://www.stockcharts.com/education/IndicatorAnalysis/indic movingAvg.html.

[2] “Time Series Analysis”, http://www.statsoft.com/textbook/sttimser.html.

[3] “Introduction to Time Series Analysis”, http://www.itl.nist.gov/div898/handbook/pmc/section4/.

[4] “The R Project for Statistical Computing”, http://www.r-project.org/.

[5] Quarteroni, A., Sacco, R. and Saleri, F. (2000) Numerical Mathematics, Springer.

[6] Popova, E. and Wilson, J.G. (2000) Adaptive time dynamic model for production volume prediction,INT.J.Prod, 38(13):3111-3130.

[7] Bellanger, M. (1984) Digital Processing Of Signals, Theory And Practice, John Wiley and Sons, UK.

[8] Stein, J. (2000) Digital Signal Processing, A Computer Science Perspective, John Wiley and Sons, USA.

[9] Jiang, R. and Szeto, K.Y (2003) Extraction of investment strategies based on moving averages: A geneticalgorithm approach, Computational Intelligence for Financial Engineering, pp. 403-410.

[10] Tabbane, N., Tabbane, S. and Mehaoua, A. (2004) Autoregressive, moving average and mixedautoregressive-moving average processes for forecasting QoS in ad hoc networks for real-time servicesupport, Vehicular Technology Conference(VTC), 5:2580-2584.

[11] Dandawate, A. and Giannakis, G.B (1996) Modeling (almost) periodic moving average processes usingcyclic statistics, IEEE Transactions on Signal Processing, 44(3):673-684.

21

22 BIBLIOGRAPHY

Chapter 2

Optimal Implied Views for Skewed

Return Distributions

Robertas Gabrys1, Weihua Geng2, Rachel Koskodan3, Jing Li4, Luke Owens 5, Qi Wu 6,Miao Zuo7

Problem Presenter:Randy Miller

Bank of America

Faculty Consultants:Dr. Tao Pang and Dr. Jeff ScroggsNorth Carolina State University

Abstract

An important aspect of banking is determining how optimally to allocate a fixed quantity of money amongdifferent companies requesting loans from a bank. This problem can be mathematically formulated as a mini-mization (of risk) or a maximization (of utility) problem with certain constraints. We solve this minimizationproblem using two different measures of risk and varying constraints. We also solve the maximization prob-lem for certain utility functions. In addition to this optimal allocation problem, banks face the challenge of

1Utah State University2Michigan State University3Texas Tech University4UNC-Charlotte5University of South Carolina6University of South Carolina7Arizona State University

23

24 CHAPTER 2. OPTIMAL IMPLIED VIEWS FOR SKEWED RETURN DISTRIBUTIONS

communication among different portfolio managers, as each has his/her own view on the correct allocationof the assets. A possible approach to this problem is determining the necessary implied returns of each man-ager’s portfolio position. This would indicate how far his/her portfolio allocation is from the mathematicallydetermined optimal allocation. The challenge of determining the implied returns is the inverse of the aboveproblem. We solve this problem using the same measures of risk and utility.

2.1 Introduction

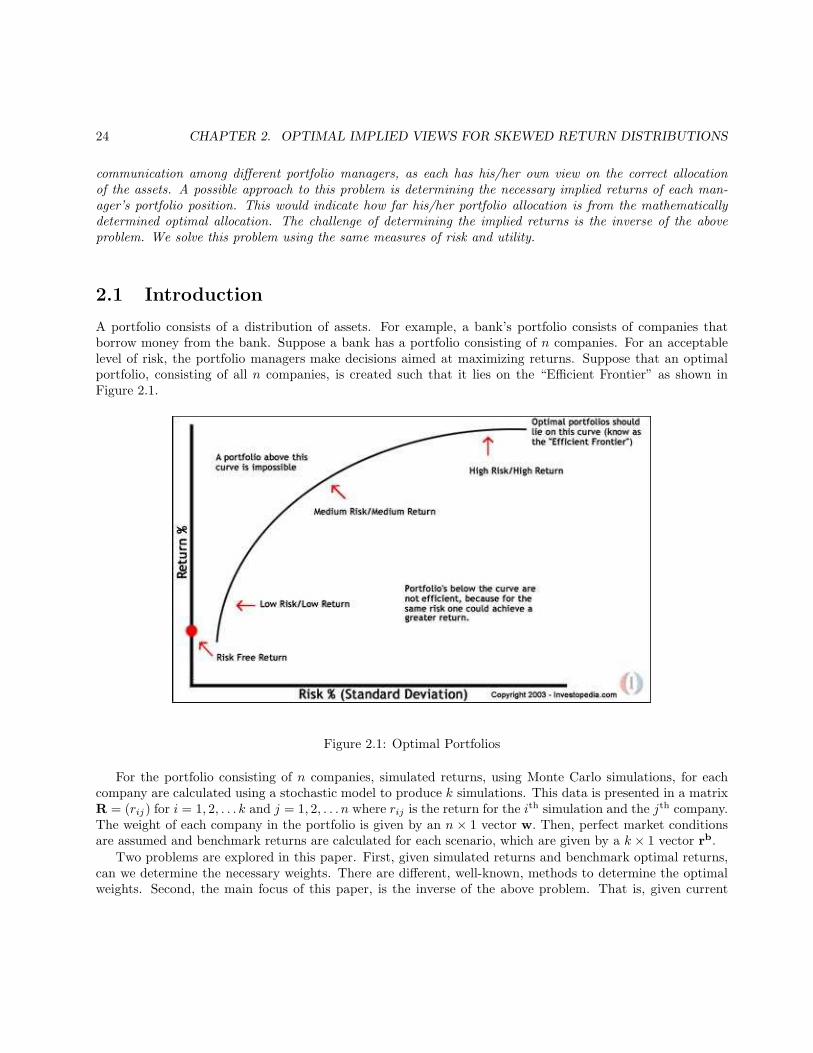

A portfolio consists of a distribution of assets. For example, a bank’s portfolio consists of companies thatborrow money from the bank. Suppose a bank has a portfolio consisting of n companies. For an acceptablelevel of risk, the portfolio managers make decisions aimed at maximizing returns. Suppose that an optimalportfolio, consisting of all n companies, is created such that it lies on the “Efficient Frontier” as shown inFigure 2.1.

Figure 2.1: Optimal Portfolios

For the portfolio consisting of n companies, simulated returns, using Monte Carlo simulations, for eachcompany are calculated using a stochastic model to produce k simulations. This data is presented in a matrixR = (rij) for i = 1, 2, . . . k and j = 1, 2, . . . n where rij is the return for the ith simulation and the jth company.The weight of each company in the portfolio is given by an n × 1 vector w. Then, perfect market conditionsare assumed and benchmark returns are calculated for each scenario, which are given by a k × 1 vector rb.

Two problems are explored in this paper. First, given simulated returns and benchmark optimal returns,can we determine the necessary weights. There are different, well-known, methods to determine the optimalweights. Second, the main focus of this paper, is the inverse of the above problem. That is, given current

2.2. MINIMUM CV AR METHOD 25

−5 0 50

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4Normal distribution

VaR

CVaR

Figure 2.2: VaR and CVaR in Standard Normal Distribution

weights and benchmark returns, can we derive the implied expected returns that make the portfolio optimal.Three approaches to solve the above problems are considered. Section 2.2 examines solutions that minimizethe conditional-value-at-risk, CV aR. Section 2.3 examines solutions that minimize the tracking error in amean-square sense. Section 2.4 examines solutions found using an extended Black-Litterman (EBL) approach.

To compare the three approaches, an example using a 10 company portfolio is examined for solving theinverse problem using each of the three methods described in Sections 2.2-2.4. The model problem considersthe returns of the first 400 simulations of the first 10 companies with the corresponding benchmark returnvector, and assumes that the assets are distributed equally among all 10 companies. That is, w(i) = 0.1 for1 ≤ i ≤ 10.

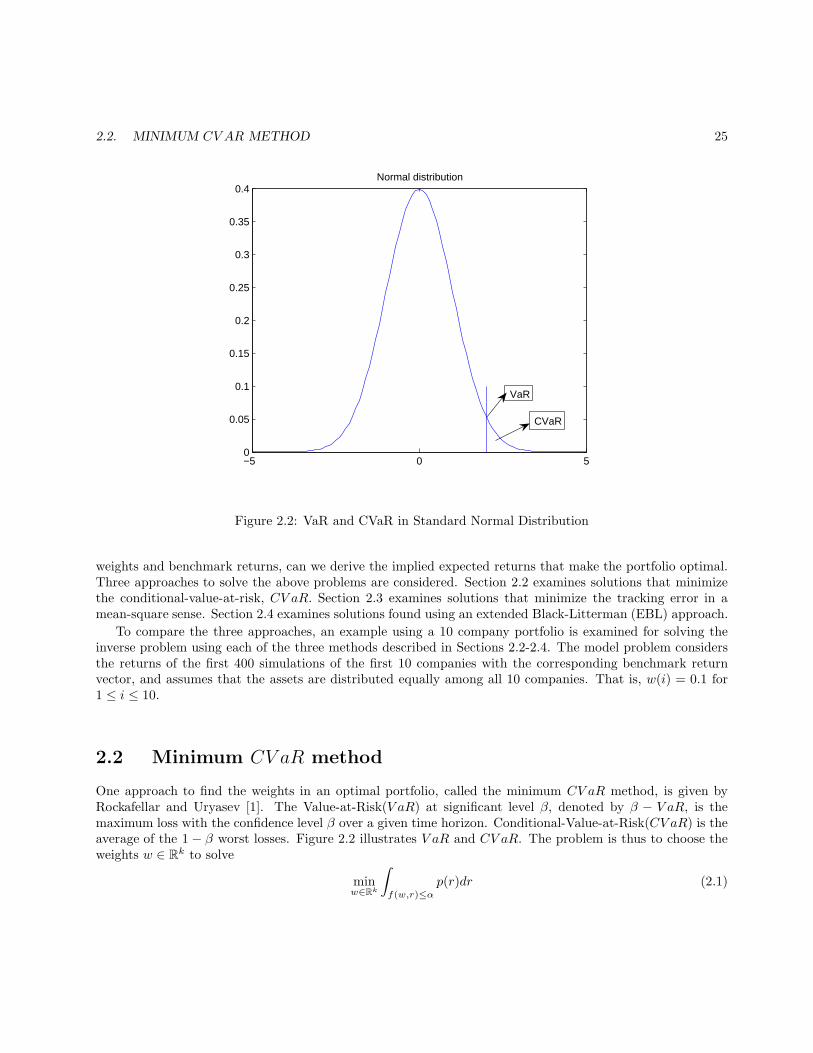

2.2 Minimum CV aR method

One approach to find the weights in an optimal portfolio, called the minimum CV aR method, is given byRockafellar and Uryasev [1]. The Value-at-Risk(V aR) at significant level β, denoted by β − V aR, is themaximum loss with the confidence level β over a given time horizon. Conditional-Value-at-Risk(CV aR) is theaverage of the 1 − β worst losses. Figure 2.2 illustrates V aR and CV aR. The problem is thus to choose theweights w ∈ Rk to solve

minw∈Rk

∫

f(w,r)≤α

p(r)dr (2.1)

26 CHAPTER 2. OPTIMAL IMPLIED VIEWS FOR SKEWED RETURN DISTRIBUTIONS

where f(w, r) is the loss function whose detailed definition will be given later, α is β − V aR, p(r) is theprobability distribution function, pdf, of the random variable r. Rockafellar and Uryasev showed the aboveproblem is equivalent to a linear programming problem on a convex set. The MatLab optimization toolboxcan solve this problem directly using the command linprog.

On the other hand, the inverse problems of this optimization problem will be considered. One thing welike to point out is that, if we solve for returns given the weights, there will be many more unknowns thanequations. Therefore, it will be an under-determined problem if we following that direction. There is anotherpossible way. First we compute variance and covariance implied by historic data. Then, we use the variance,covariance information and the return at each mode to simulate a new return of each company and then geta new w∗. In this way, at each mode of discretized return space, we have an optimal weight corresponding toit. If there are some good properties of this correspondence (eg. monotonicity), then we can find the impliedreturn for a given set of weights. Unfortunately, this method cannot work either. First of all, if there are onlytwo or three companies, then there’s no problem of discretizing a two or three-dimension return space. Butif there are more than 5 (200 in our database) companies, then the discretization will become impractical.Secondly, there is no reason for the weight to be monotone with respect to the return in the large system ofhundreds of companies.

Therefore, instead of trying the straightforward methods we mentioned above, we tried the following twomethods to solve this problem:

1. Empirical Method : Solve for the weights given the returns and determine if there is a relationship betweenthem.

2. Parameterized Method : Analyze the relationship between the parameterized returns and the risk accord-ing to the given weights.

We have obtained some satisfactory results, and details will be given in the next two subsections.

2.2.1 Empirical Method

In this method, we are going to solve for weights, given the returns for each company. According to R-U [1],minimizing CV aR can be reduced to the linear programming problem:

minw∈Rn,z∈RJ ,α∈R

α+1

(1 − β)J

J∑

j=1

zj (2.2)

The constraints are

zj ≥ (bj −n∑

i=1

wirij) − α

zj ≥ 0

1 > wi > 0.001

1 =

n∑

i=1

wi

2.2. MINIMUM CV AR METHOD 27

Company V*M Var Mean Weight1 Weight2 Weight3 Weight4 Weight5

14 ~0 ~0 0.0001 0.976 throw away throw away throw away throw away

1 ~0 ~0 0.0002 0.001 0.977 throw away throw away throw away

15 ~0 ~0 0.0018 0.001 0.001 0.8981 throw away throw away

3 0.35 0.0005 0.0007 0.001 0.001 0.0809 0.979 throw away

19 0.42 0.0001 0.0042 0.001 0.001 0.001 0.001 0.3031

6 0.76 0.0002 0.0038 0.001 0.001 0.001 0.001 0.0978

17 1.02 0.0002 0.0051 0.001 0.001 0.001 0.001 0.2858

9 2.16 0.0009 0.0024 0.001 0.001 0.001 0.001 0.2964

13 2.78 0.0139 0.0002 0.001 0.001 0.001 0.001 0.001

8 3.4 0.001 0.0034 0.001 0.001 0.001 0.001 0.001

2 4.23 0.0009 0.0047 0.001 0.001 0.001 0.001 0.001

24 6.21 0.0069 0.0009 0.001 0.001 0.001 0.001 0.001

4 6.38 0.0011 0.0058 0.001 0.001 0.001 0.001 0.001

20 6.66 0.0018 0.0037 0.001 0.001 0.001 0.001 0.001

5 7.4 0.002 0.0037 0.001 0.001 0.001 0.001 0.001

25 7.56 0.0036 0.0021 0.001 0.001 0.001 0.001 0.001

12 9.75 0.0065 0.0015 0.001 0.001 0.001 0.001 0.001

23 10.83 0.0057 0.0019 0.001 0.001 0.001 0.001 0.001

7 15.39 0.0027 0.0057 0.001 0.001 0.001 0.001 0.001

10 23.56 0.0019 0.0124 0.001 0.001 0.001 0.001 0.001

22 23.76 0.0012 0.0198 0.001 0.001 0.001 0.001 0.001

11 24.75 0.0025 0.0099 0.001 0.001 0.001 0.001 0.001

18 30.45 0.0145 0.0021 0.001 0.001 0.001 0.001 0.001

21 34.8 0.006 0.0058 0.001 0.001 0.001 0.001 0.001

16 61.36 0.0104 0.0059 0.001 0.001 0.001 0.001 0.001

Figure 2.3: Relation of weight to mean and variance

where α is the V aR, b = (b1, ...bJ) is the benchmark, rij is historical return of ith company in the jth scenario,wi is the weight, zj ’s are dummy variables, i = 1, ..., n and j = 1, ...J .

There are two different ways to define the loss function. We will explore both of them next.

First Way to Define the Loss Function

The first definition of the loss function defines fj(w, r) =∑n

i=1(wirij). Figure 2.3 shows that companieswith very small average returns and very small variances will have the largest weights. To combine those twofactors, first we define mean return as µ and variance as σ2, then set up a trial function: g(µ, σ2) = µ× σ2.

As shown in Figure 2.3, for the first 400 scenarios of the 25 companies, companies 14, 1 and 15 have thesmallest trial function values. Company 14 has the minimum average return, the minimum variance, and hasthe largest weight, 0.976. If we discard the company with the minimum trial function value, and just considerthe remaining companies, then the company which has the second smallest trial function value will have thelargest weight, and so on. The covariances also have an impact on the weights. But in this investigationcovariances are not considered for the reason of complicity.

The conclusion is that the weight is approximately monotone with respect to the trial function g. Reviewingthe data, we see that the variance affects the value of weight. For instance, Company 14 has the smallestvariance, meaning it has stable returns and a very small risk of loss. Although the return is small, the companyis assigned a very large weight. Thus, for a given weight w = (w1, w2, . . . , w25), if a wi has a much largervalue than others, then the company corresponding to this weight should have a very small value of the trialfunction, compared to those companies that follow it in Figure 2.3.

28 CHAPTER 2. OPTIMAL IMPLIED VIEWS FOR SKEWED RETURN DISTRIBUTIONS

−5 0 5 10 15 20

x 10−3

0

0.2

0.4

0.6

0.8

mean

wei

ght

0 0.002 0.004 0.006 0.008 0.01 0.012 0.014 0.016 0.0180

0.2

0.4

0.6

0.8

variance

wei

ght

Figure 2.4: Relation of weight to mean and variance

Second Way to Define the Loss Function

In this part we consider the loss function defined as the following

fj(w, r) = bj −n∑

i=1

(wirij), (2.3)

where the bj is benchmark. Figure 2.4 shows the relation of weight versus the mean return along with theweight versus the variance of the return. There does not appear to be a clear relation between the weightand the mean. In the plot of the weight versus the variance, we can clearly see that the weight is high forcompanies with low variances. So a company with high risk tends to attain a small weight.

However, we believe that the means also play an important role in determining the weights. Intuitively,people invest in the assets with higher returns. We tried the trial function g(µ, σ) = µ − 2σ. This trialfunction makes perfect sense. For a normal distribution, the 5th percentile is approximately µ− 2σ, which isthe definition of V aR of the standardized normal distribution. For the normal distribution, minimizing V aRis equivalent to minimizing CV aR. We can see that the value of g is in the positive direction of the mean,and negative direction of the variance.

Figure 2.5 is the plot of weight versus the trial function g. It shows that there is some trend between theweight and the value of g. It is approximately a monotone increasing function. A reasonable conclusion isthat the higher the return of a company, the higher the weight of the company; the less the stability of thereturn of a company, the lower weight the company should have. Thus, for a given weight of a company, ifit is much higher than the other companies, it should be more stable and have a higher return as compared

2.2. MINIMUM CV AR METHOD 29

−0.3 −0.25 −0.2 −0.15 −0.1 −0.05 0 0.050

0.1

0.2

0.3

0.4

0.5

0.6

0.7

test function

we

igh

t

test function = mean - 2* SD

Figure 2.5: Relation between weight and trial function

with other companies.In the next subsection, how the weights affect the mean returns under the optimal assumption is analyzed.

2.2.2 Parameterized Method

In the previous section, we managed to see relationships between the weights and the returns. However, wecould not find one-to-one correspondence or an explicit function between them. Since this system is highlyunder-determined, we can change the assumption that the return of a certain company has the same changein different scenarios. The changes depend on the δ ∈ Rn. The vector of δ is called parameter. Thus theproblem becomes

minδ∈Rn,z∈RJ ,α∈R

α+1

(1 − β)J

J∑

j=1

zj (2.4)

s.t.

zj ≥ bj − (Rδw)j − α

zj ≥ 0

Here Rδ is the new return matrix with the ith column of this matrix defined as the corresponding column ofthe original matrix plus a constant δi. Since the magnitudes of mean of the each company are largely different,the numbers we add to each company are set to be proportional to the original mean of the company.

30 CHAPTER 2. OPTIMAL IMPLIED VIEWS FOR SKEWED RETURN DISTRIBUTIONS

0 0.005 0.01 0.015 0.02 0.025 0.03 0.035−0.02

0

0.02

0.04

0.0610000 scenarios

risk

retu

rn

0 0.005 0.01 0.015 0.02 0.025 0.03 0.035−0.02

0

0.02

0.04

0.06

0.08400 scenarios

risk

retu

rn

Figure 2.6: Relation between return and risk based on different number of scenarios

We did the numerical experiment for the first 10 companies. We are only able to use < 500 scenarios inproglin command in MatLab. 400 scenarios is too small to catch the basic rules in financial world. First, thelong run mean return should be nonnegative. In Figure 2.6, we can see for 10,000 scenarios there is only 1negative return, while there are several companies which have negative returns. Second, the empirical datashould have return increases when the risk increases. We can clearly see this pattern in the 10,000 scenarioplot. However in the 400 scenarios, even high risk companies have 0 returns.

In the following two methods, we are going to take the weight to be the same for all companies we chose.The empirical return increases with respect to the risk. Now if we set the weight to be the same, the newreturns corresponding to the given equal weights should also increase with respect to the risk.

Multiplicative Parameterize

A variation we consider is to multiply a constant to different company return. To minimize CV aR under thegiven weights, the magnitude of the return of each company in every scenario should increase by a multipleof the original return. Let δ = (δ1, ..., δn) be a vector of multiples, δi is the constant multiplied to ith column.Thus the problem is

minδ∈Rn,z∈RJ ,α∈R

α+1

(1 − β)J

J∑

j=1

zj (2.5)

2.2. MINIMUM CV AR METHOD 31

Company MultiplierOriginal Mean Variance New Mean New Variance Trial Function g

1 3.6845 0.0002 0.0021 0.0006 0.0078 -0.0062

2 2.3192 0.0052 0.0297 0.0121 0.069 -0.084

3 0.4319 0.0004 0.026 0.0002 0.0112 -0.0776

4 0.5573 0.0051 0.0371 0.0028 0.0207 -0.1063

5 0.4032 0.0051 0.0387 0.0021 0.0156 -0.111

6 2.4758 0.0034 0.0167 0.0084 0.0414 -0.0467

7 0.3084 0.0047 0.0578 0.0014 0.0178 -0.1687

8 0.2788 0.003 0.0343 0.0008 0.0096 -0.0999

9 0.4253 0.0022 0.032 0.0009 0.0136 -0.0937

10 0.9811 0.0115 0.048 0.0113 0.047 -0.1323

Figure 2.7: New return by given equal weight

s.t.

zj ≥ bj −n∑

i=1

wi(rijδi) − α

zj ≥ 0

Figure 2.7 shows the implied returns for each company. The implied returns are listed with the originalreturns, variances and the values of the trial function defined previously. We highlight four companies withhighest value of trial function. Out of those four companies, three get the highest multipliers. After plottingthe implied return against the historic variance, we can see some obvious relation between the return and therisk in Figure 2.8. The return increases with respect to the variance.

If we multiply a constant to a random variable, we are changing the mean and variance together. That isthe drawback of this method, since there is no reason that the mean and standard derivation should changetogether by the same amount. Moreover, if we change two quantities together, we are not able to see how theweight will impact each of them. We believe that is why we can not see the pattern in the mean or variancechange according to the given weight.

Additive Parameterize

Instead of multiplying a constant to each column, we want to improve the parameterized model by adding aconstant return to each company. Each column of this matrix is equal to the corresponding column of theoriginal matrix plus a constant. Considering the magnitude of the mean of each company is largely different,the numbers we add to each company are set to be proportional to the original mean of the company.

We consider the following problem:

minδ∈Rn,z∈RJ ,α∈R

α+1

(1 − β)J

J∑

j=1

zj (2.6)

32 CHAPTER 2. OPTIMAL IMPLIED VIEWS FOR SKEWED RETURN DISTRIBUTIONS

0 0.01 0.02 0.03 0.04 0.05 0.06 0.070

0.002

0.004

0.006

0.008

0.01

0.012

0.014

Risk (Variance)

Ret

urn

(Mea

n)

Equal Weight Under Multiplicative Model

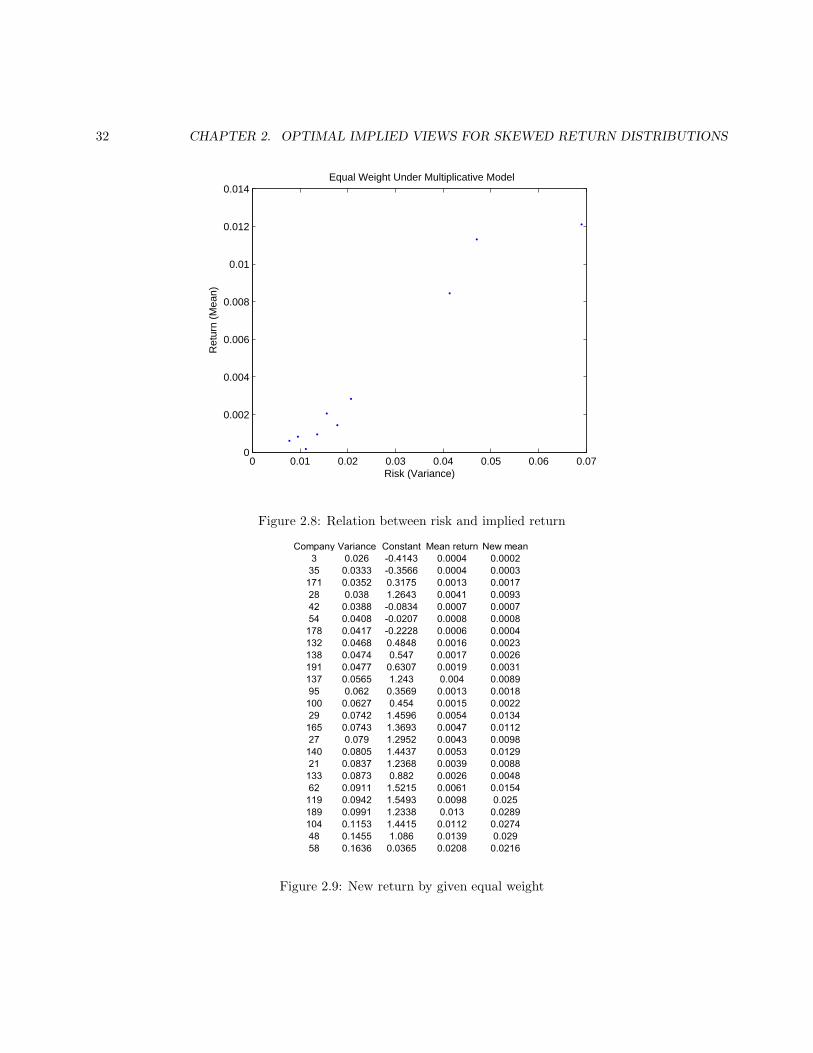

Figure 2.8: Relation between risk and implied return

Company Variance Constant Mean return New mean

3 0.026 -0.4143 0.0004 0.0002

35 0.0333 -0.3566 0.0004 0.0003

171 0.0352 0.3175 0.0013 0.0017

28 0.038 1.2643 0.0041 0.0093

42 0.0388 -0.0834 0.0007 0.0007

54 0.0408 -0.0207 0.0008 0.0008

178 0.0417 -0.2228 0.0006 0.0004

132 0.0468 0.4848 0.0016 0.0023

138 0.0474 0.547 0.0017 0.0026

191 0.0477 0.6307 0.0019 0.0031

137 0.0565 1.243 0.004 0.0089

95 0.062 0.3569 0.0013 0.0018

100 0.0627 0.454 0.0015 0.0022

29 0.0742 1.4596 0.0054 0.0134

165 0.0743 1.3693 0.0047 0.0112

27 0.079 1.2952 0.0043 0.0098

140 0.0805 1.4437 0.0053 0.0129

21 0.0837 1.2368 0.0039 0.0088

133 0.0873 0.882 0.0026 0.0048

62 0.0911 1.5215 0.0061 0.0154

119 0.0942 1.5493 0.0098 0.025

189 0.0991 1.2338 0.013 0.0289

104 0.1153 1.4415 0.0112 0.0274

48 0.1455 1.086 0.0139 0.029

58 0.1636 0.0365 0.0208 0.0216

Figure 2.9: New return by given equal weight

2.2. MINIMUM CV AR METHOD 33

0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.180

0.005

0.01

0.015

0.02

0.025

0.03

Risk (Variance)

Ret

urn

(Mea

n)

Equal Weight under Additive Model

Figure 2.10: Relation between risk and implied return

s.t. zj ≥ bj −n∑

i=1

wi(rij + δiri) − α

zj ≥ 0n∑

i=1

wiδi = 0

where ri is the mean of column i.Figure 2.9 shows the implied return for each company. Given equal weights, it is expected that the

companies with high risk have high returns. After plotting the implied return against the historic variance,we can see a positive trend between return and risk in Figure 2.10. So this kind of result is reasonable: Thecompany with a higher implied return generally has a higher risk of loss.

2.2.3 Conclusion

Thus, our conclusion of minimization of CV aR is

1. We are not able to find the one to one correspondence between the returns and the weights.

2. Some relationship can be found between the characteristics (mean, variance) of the return matrix andthe weights.

In the next section we will look at the method of minimizing the tracking error.

34 CHAPTER 2. OPTIMAL IMPLIED VIEWS FOR SKEWED RETURN DISTRIBUTIONS

2.3 Minimizing the Tracking Error

The tracking error(TE) is defined as

TE =

√√√√√k∑

i=1

n∑

j=1

rijwj − rbi

2

= ‖Rw− rb‖ , (2.7)

where ‖ · ‖ is the vector norm, R is the return matrix, w is the vector of weights, and rb is the benchmarkreturn. First, we wish to determine the weights of the companies that give expected portfolio returns closestto the optimal returns in a mean square sense. Then we will consider the inverse problem. That is, given areturn matrix, a vector of weights, and a benchmark vector, we try to determine how the return matrix hasto change to minimize TE.

First, we consider the problem of finding the vector of weights that minimizes TE when the return matrixand benchmark vector are given. This problem is analyzed with and without financially motivated constraintson the weights. Secondly, the inverse problem will be considered. We like to point out that the straightforwardinverse problem is not well-posed in the sense that given w and rb, there are infinitely many ways to changeR to minimize the tracking error. Hence, we put restrictions on how R is allowed to change in order to getmeaningful unique solutions.

2.3.1 Unconstrained Minimization

First, we investigate determining the weights that minimize the tracking error. That is, find w ∈ Rn such that

‖Rw− rb‖ (2.8)

is minimized.In general, we minimize ‖Ax− b‖2 over x ∈ Rn where A ∈ Rk×nand b ∈ Rk. Consider

‖Ax− b‖2 = (Ax − b)T (Ax − b)

= [(Ax)T − bT ][(Ax) − b]

= (Ax)T (Ax) − (Ax)Tb − bT (Ax) + bTb

= (Ax)T (Ax) − 2xTAT b + bT b.

The minimum is found by taking the derivative with respect to x and setting it equal to zero. By doing thatwe can get the normal equation

ATAx = ATb. (2.9)

If k ≥ n and A has full rank, then ATA can be inverted and the unique solution of the least squares problemis

x = (ATA)−1ATb