Turn AnnuAl Review For personal use only · 2015-11-15 · For personal use only. e AnnuAl Review...

54

Turn On 2015 ANNUAL REVIEW TEN NETWORK HOLDINGS LIMITED ABN: 14 081 327 068 For personal use only

Transcript of Turn AnnuAl Review For personal use only · 2015-11-15 · For personal use only. e AnnuAl Review...

TurnOn

2015 AnnuAl Review

TEN NETwork holdiNgs limiTEd ABN: 14 081 327 068

For

per

sona

l use

onl

y

AnnuAl Review 2015e

kFC Big BasH leagUe2015 BIG FINAL 1.o1 millioN ViEwErs

# 1IN 25 TO 54s, TOTAL PEOPLE

Family FeUdAUSTRALIA’S

# 1GAMESHOW

6%TIMESLOT GROWTH

sUCCEssFUl ProdUCT sPiN-oFFs

Have yoU Been Paying aTTenTion?

83%GROWTH ON 2014

# 2IN 25 TO 54s, UNDER 55s

SOURCE:OzTAM, 5 City Metro, Consolidated. Timeslot growth based on same timeslot in 2014.

2015

highlighTs

For

per

sona

l use

onl

y

Ten neTwork Holdings limiTed f

THe ProjeCT

6%GROWTH ON 2014

GOLD LOGIE WINNER

masTerCHeF aUsTraliaTHE WINNER ANNOUNCED2.2 millioN ViEwErs

# 1NON-SPORT TV PROGRAM OF 2015

2015 AVERAGE1.18 millioN ViEwErs

15%GROWTH ON 2014

# 1IN 25 TO 54s, TOTAL PEOPLE

51%TIMESLOT GROWTH

2015 AVERAGE742,000 ViEwErs

1.26 millioN ViEwErs

THE WINNER ANNOUNCED

i’m a CeleBriTy...geT me oUT oF Here!

CArriE BiCkmorE

For

per

sona

l use

onl

y

THE BACHELORETTE AUSTRALIATHE FINAL DECISION 1.56 MILLION VIEWERS

2015 AVERAGE 1.03 MILLION VIEWERS

68%TIMESLOT GROWTH

THE GREAT AUSTRALIAN SPELLING BEETHE WINNER ANNOUNCED947,000 VIEWERS

2015 AVERAGE 712,000 VIEWERS

48%TIMESLOT GROWTH

THE BACHELOR AUSTRALIATHE FINAL DECISION 1.52 MILLION VIEWERS

2015 AVERAGE 985,000 VIEWERS

25%GROWTH ON 2014

1TEN NETWORK HOLDINGS LIMITED

For

per

sona

l use

onl

y

CONTENTS2 About Ten network3 Key numbers5 Key events6 Chairman’s Review8 CeO’s Review11 Operational Highlights

14 Directors’ Report33 Concise Financial Report45 Shareholder information48 Financial Calendar48 Corporate Directory

This yeAR

Key develOpmenTs fOR Ten neTwORK in 2015 included significAnTly impROved Audience And Revenue shARe; OngOing expAnsiOn Of The indusTRy-leAding digiTAl plATfORm TenplAy; And The esTAblishmenT Of sTRATegic ARRAngemenTs wiTh fOxTel And mulTi chAnnel neTwORK.

For

per

sona

l use

onl

y

Ten Network Holdings is one of Australia’s leading entertainment and news content companies, with free-to-air television and digital media assets.

Ten Network Holdings includes three free-to-air television channels – TEN, ELEVEN and ONE – in Australia’s five metropolitan markets of Sydney, Melbourne, Brisbane, Adelaide and Perth, plus the digital platform tenplay.

Ten Network Holdings also has investments in RSVP Oasis Active and The Roar, and operates datacasting channels in partnership with TVSN Channel (TVSN) and Brand Developers (Spree TV).

With a focus on people 25 to 54 who are young at heart, TEN has a long and proud tradition of bringing fun, irreverent, engaging and informative content to Australians.

TEN is the home of the award-winning local news bulletins, TEN Eyewitness News First At Five, as well as the distinctly different current affairs program, The Project, and local content including Family Feud, The Living Room, MasterChef Australia, TBL Families, The Bachelor, The Bachelorette, Offspring, I’m A Celebrity… Get Me Out Of Here!, The Great Australian Spelling Bee, Shark Tank, Gogglebox, Gold Coast Cops, Bondi Vet, Bondi Rescue and Studio 10.

Live sport is a vital part of TEN, including the KFC Big Bash League, Rugby Union, Formula One, MotoGP and V8 Supercars.

The best international drama, comedies and entertainment shows are found on TEN, including NCIS, NCIS: Los Angeles, NCIS: New Orleans, Modern Family, Law & Order: SVU, The Good Wife, CSI: Cyber, The Graham Norton Show, Scorpion, Madam Secretary, The Odd Couple, Elementary, Homeland and Jamie Oliver and Sir David Attenborough television events.

TEN is broadcast in Standard Definition digital and analogue.

The home of fun and bold entertainment for a distinctly youthful audience, ELEVEN showcases a mix of Australian and international content for people 13 to 29, including Australia’s longest running serial drama, Neighbours.

ELEVEN’s international line-up includes The Simpsons, Supernatural, Tattoos After Dark, American Idol, Futurama, So You Think You Can Dance US, Everybody Loves Raymond, Empire, Snog Marry Avoid, Dexter, American Horror Story and Scream Queens.

ELEVEN is broadcast in Standard Definition digital.

The home of premium entertainment for men 25 and older, ONE content is a mix of premium scripted and reality programming, as well as local and international sports. ONE’s program line-up includes M*A*S*H, Undercover Boss, COPS, Last Man Standing, Sons of Anarchy, Monster Jam, Extreme Fishing and Extreme Collectors, plus Formula One, MotoGP, movies and Sir David Attenborough specials.

ONE was the first digital channel launched by an Australian commercial network, in April 2009. ONE is broadcast in High Definition digital.

tenplay is Ten Network’s digital platform, available on web, on mobile, on tablets and via game consoles and smart TVs, giving people access to our content anytime, anywhere and on any device. Ten Network is continuing to expand tenplay with new content and new distribution channels.

Ten Network is also home to some of the most popular social media sites in Australia. The MasterChef Australia Facebook page, for example, has more than 1.45 million “likes”.

WE CREATE INNOVATIVE AND AUTHENTIC MULTI-PLATFORM CONTENT THAT ENTERTAINS AND ENGAGES THE YOUNG AT HEART.

TEN NETWORK’S VISION

2 ANNUAL REVIEW 2015

For

per

sona

l use

onl

y

REVENUE

$654.1 MILLION

TV REVENUE INCREASE

4.6%

TV COSTS DECREASE

6.5%

TENPLAY VIDEO VIEWS

294MILLION

AUDIENCE GROWTHTEN: Up 9% in prime time in total people and also up 9% in 25 to 54s. The only commercial primary free-to-air television channel to grow in 2015. NETWORK TEN: Up 4% in prime time in total people and up 3% in 25 to 54s (excluding Commonwealth Games from 2014). The only commercial primary free-to-air television network to grow in 2015.TENPLAY: Page views up 8%. Unique visitors up 7%. Video views up 7%.Source: TV costs decrease ex-selling costs. OzTAM, 5 City Metro, 18:00-22:30, Weeks 7 to 42 (excluding Easter), consolidated (excluding Week 42 which is overnight both years). Tenplay: 12 months to August 31, 2015, Adobe Analytics.

2015 RESULTS

KEY NUMBERS

TEN NETWORK HOLDINGS LIMITED 3

NETWORK AUDIENCE SHARE, 25 TO 54s

29.2%

NETWORK AUDIENCE SHARE, TOTAL PEOPLE

24.8%

For

per

sona

l use

onl

y

ANNUAL REVIEW 20154 ANNUAL REVIEW 20154

For

per

sona

l use

onl

y

KEY EVENTS2014-15

SEPTEMBER 2, 2014: tenplay launches on FreeviewPlus.

OCTOBER 30, 2O14: Gina Rinehart resigns as a Director.

NOVEMBER 3, 2014: John Klepec appointed a Director.

DECEMBER 1, 2014: Paul Mallam resigns as a Director.

JANUARY 26, 2015: Waleed Aly joins The Project as co-host.

JANUARY 28, 2015: tenplay launches on Apple TV.

FEBRUARY 1, 2015: I’m A Celebrity… Get Me Out Of Here! Australia launches.

MAY 3, 2015: Carrie Bickmore wins TV Week Gold Logie award. Other winners include Asher Keddie and The Living Room.

JUNE 15, 2015: Strategic arrangements with Foxtel and Multi Channel Network announced.

JULY 27, 2015:Hamish McLennan steps down as Executive Chairman and CEO. David Gordon appointed Chairman and Paul Anderson appointed CEO.

JULY 27, 2015:MasterChef Australia – The Winner Announced draws 2.2 million capital city viewers.

SEPTEMBER 17, 2015:The Bachelor Australia – The Final Decision attracts 1.52 million capital city viewers.

SEPTEMBER 20, 2015:Offspring Season 6 announced for 2016.

TEN NETWORK HOLDINGS LIMITED 5

For

per

sona

l use

onl

y

David GordonChairman

6 ANNUAL REVIEW 2015

Dear Fellow Shareholders,

This is my first annual review as Chairman of Ten Network and I am pleased to be able to write to you about a year of considerable achievement for our company. The past few years have been particularly challenging, but the results of strategic thinking, hard work and a great team are now realising the beginning of the turnaround that we have all been waiting for.

In 2015 Ten Network delivered significantly improved ratings by sticking to our plan of event television, premium live sport, focusing on the 25 to 54 year old demographic, maintaining a consistent program schedule and selectively developing and launching new formats.

THE COMPLETION OF THE FOXTEL AND MULTI CHANNEL NETWORK STRATEGIC TRANSACTIONS AND THE CAPITAL RAISING WILL SEE OUR COMPANY IN A SUBSTANTIALLY STRENGTHENED POSITION.

CHAIRMAN’S REVIEW

Examples of our successful event television content include MasterChef Australia, The Bachelor Australia, The Bachelorette Australia, I’m A Celebrity… Get Me Out Of Here!, the KFC Big Bash League and V8 Supercars, all of which resonated strongly with 25 to 54s.

We also launched four new shows – I’m A Celebrity… Get Me Out Of Here!, Shark Tank, Gogglebox and The Great Australian Spelling Bee – all of which were successful across multiple screens and will return next year. A fifth new hit, The Bachelorette Australia, was launched at the start of our new financial year and will also return in 2016.

During the 2015 financial year we continued our TV Everywhere strategy, extending our engagement with our audiences to great effect. In the two years since it was launched, tenplay, Ten Network’s digital platform, has become one of the leading online entertainment catch-up viewing services in Australia, with more than two million downloads of its mobile app and an average of about 25 million video views a month. In the years to come we will need to continue to innovate and our digital team will be at the heart of that growth activity.

Our delivery of better ratings and multi-platform audience engagement has also seen an improvement in our revenue – both an increasing share of spend from existing clients and

the return of a number of advertisers to Ten Network. As a result, our television revenue increased 4.6% during the 2015 financial year.

On June 15, 2015, we announced the culmination of our strategic review with the entry into arrangements with Foxtel and Multi Channel Network (MCN). That package of strategic transactions comprised:

• Foxtel investing up to $77 million to become a 15% shareholder in Ten Network.

• Ten Network becoming a 24.99% shareholder in MCN and the establishment of an advertising sales representation agreement with MCN.

• Ten Network securing a two-year option to become a shareholder in the online streaming service, Presto.

On October 22, 2015, those arrangements received the approval of the Australian Competition and Consumer Commission and the Australian Communications and Media Authority. At the time of writing this review, a number of customary conditions remain, however we are confident that these conditions will be satisfied shortly.

As a result of those approvals, on October 26, 2015, we announced a fully underwritten accelerated pro-rata renounceable entitlement offer, giving our shareholders the

For

per

sona

l use

onl

y

TEN NETWORK HOLDINGS LIMITED 7

to think independently, value diversity and to take part and be active in their communities.

On behalf of the Board, I would like to thank Paul Anderson, his senior Executives and the whole team at Ten Network for their passion, creativity and hard work during the year. The Ten Network team have much to be proud of in 2015.

I would also like to thank my fellow Board members, all of whom attended more meetings and worked harder as Non-Executive Directors than they should reasonably have expected to have done, to complete the strategic review and help set a new direction for Ten Network. And I would like to particularly acknowledge the contribution of those Directors who will be retiring from the Board later this year and who have made such a valuable contribution to the business over a great many years.

Finally, I wish to thank all of you, our shareholders, for your continuing support for Ten Network. Notwithstanding the difficulties of the past few years, we received an outstanding response to the recent entitlement offer and both your tangible and intangible investment and support of the business is much appreciated.

And so it was that 2015 was a good year for our company, the signs of a turning point, but there is still much work to do. Your board and management will remain focused and disciplined in continuing the turnaround of our business and we look forward to an even more successful year ahead.

David GordonChairman

opportunity to invest up to $77 million at a price of $0.15 per share, the same price as Foxtel’s investment. Together with Foxtel’s investment, the entitlement offer will result in us raising approximately $154 million of new equity.

The completion of these strategic transactions and the capital raising will see our company in a substantially strengthened position and well placed for the opportunities and challenges ahead. Ten Network will have:

• A restored balance sheet and the capacity to make disciplined and strategic investments.

• Through MCN, an advertising platform providing new efficiencies, improved data capability and broader integration opportunities for our advertising clients.

• A new and important strategic partner in Foxtel, alongside our long-standing and valued partnerships with CBS Studios and 20th Century Fox.

• A smaller and more nimble Board of six Directors.

It has been a very busy year at Ten Network, with the negotiation and execution of these strategic arrangements while at the same time maintaining a focus on the delivery of our operating plan, with the resultant improvement in audience growth and revenue across all our platforms. This has been achieved through our company’s greatest asset – its people.

During the year, Hamish McLennan stepped down as Executive Chairman and Chief Executive Officer. I would like to thank Hamish for the energy and commitment that he gave to the company during his tenure.

On July 27, 2015, we announced my appointment as Chairman and the appointment of Paul Anderson as the new Chief Executive Officer. Paul was formerly Chief Financial

Officer and Chief Operating Officer and has been with Ten Network for 12 years. Paul leads a hard-working and experienced management team, who did an exceptional job delivering the beginnings of our turnaround in 2015 and who continue with the business into the future.

Notwithstanding the pleasing results in 2015 and the completion of our strategic review, Ten Network continues to operate in a dynamic and changing environment. The combination of new technologies and new ways to consume media is changing viewing habits and presents new challenges.

The free-to-air television industry in Australia is subject to regulation that has been in need of change for some time. Drawn up in a different era and focused on the regulation of industries and technologies that existed 40 years ago, it now acts to limit and constrain Australian free-to-air networks, while international competitors and other domestic players face no such regulation.

Ten Network has, for many years, argued for the removal of all ownership and control restrictions, so as to free us to better compete in the marketplace. We are hopeful that the coming year finally sees the wholesale removal of these rules and not a piecemeal tinkering that will of itself only create a new set of distortions and continue to impede our competitiveness.

As a public broadcaster, Ten Network places great importance on our community and social responsibilities. We have an active set of community engagements, including our partnership with UnLtd, a not-for-profit organisation that focus on charities that help disadvantaged youth. In addition, we recently announced a partnership with High Resolves, a not-for-profit organisation that runs programs with high school students around Australia to engage and empower them to become global citizens and leaders,

For

per

sona

l use

onl

y

ANNUAL REVIEW 20158

Paul AndersonChief Executive Officer

CEO’S REVIEW

It is a great honour and privilege to be writing to you for the first time as Ten Network’s Chief Executive Officer, a role I took on in July 2015. I have worked at our company for 12 years in various senior operational and financial roles. I’m passionate about the television business, our brands, our people and our industry, and it is a pleasure to be able to work for all Ten Network shareholders.

The past 12 months have seen a lot of positive change at Ten Network, as we have moved to strengthen our balance sheet by taking on a new major shareholder and conducting a capital raising; established an innovative, industry-leadership partnership in the advertising sales area; increased our

share of the free-to-air television audience and advertising revenue market; maintained our focus on strict cost control and finding ways to work smarter; and built on the already significant success of our digital tenplay platform.

While our financial results for the 12 months to August 31, 2015, represented an improvement on the previous year, they still require further improvement. The key focus for everyone at Ten Network is on extending the ratings and revenue growth momentum we have seen this year and increasing our company’s earnings and returns to shareholders.

FOXTEL AND MULTI CHANNEL NETWORKThe strategic arrangements with Foxtel and Multi Channel Network (MCN) that were announced on June 15 this year were a major development for Ten Network. The details of the arrangements are outlined in the Chairman’s Review (see page 6).

In Foxtel, our company has gained a significant new major shareholder, one with extensive knowledge and experience in the media sector and one that will bring real long-term value to Ten Network.

The advertising sales representation agreement with MCN is a major milestone for our company. The combination of Ten Network’s three capital city free-to-air channels and the 70 subscription television channels represented by MCN creates the largest broadcast television

inventory offering in the market – plus a powerful digital media offering – and gives Ten Network access to MCN’s world-class trading and data platforms, Landmark and Multiview.

Together, Ten Network and MCN capture approximately 41% of viewers in the key advertiser demographic of 25 to 54 year olds. This combined share provides advertisers and agencies with access to a large audience and more efficient transactions. Ten Network and MCN cover a large selection of channels, programs and brands that will offer and unlock significant new cross-platform and integration opportunities.

FINANCIAL AND AUDIENCE RESULTS Ten Network’s financial results for the 2015 year reflected the increased audience and revenue shares achieved during the year. Television revenue increased 4.6%, which was a strong result given the capital city free-to-air television advertising market was flat during that period. From January to September 2015, our share of the revenue market increased by 2.6 percentage points.

Television costs, ex-selling costs, declined 6.5% during the 2015 financial year. After adjusting for corporate activity costs and the renewal of the Formula One broadcasting agreement, costs declined 8.4%. We have guided the market that our television costs are expected to increase 6.5% during the 2016 financial year, due to program

THE PAST 12 MONTHS HAVE SEEN A STRONG RATINGS AND AUDIENCE PERFORMANCE BY TEN NETWORK ACROSS ITS TELEVISION AND DIGITAL BUSINESSES.

For

per

sona

l use

onl

y

TEN NETWORK HOLDINGS LIMITED 9

contractual increases, inflationary increases and selective investments in new prime time content to continue our ratings growth. Non-programming costs are expected to be flat for the year.

For 2015, we reported a television earnings before interest, tax, depreciation and amortisation loss of $12.0 million compared with a loss of $79.3 million for the previous financial year.

The non-recurring items of $262.9 million for 2015 included the $251.2 million television license impairment charge announced with the release of our first half results on April 30, 2015. The net loss attributable to members for the 2015 financial year was $312.2 million and the underlying net loss attributable to members was $50.5 million.

The past 12 months have seen a strong ratings and audience performance by Ten Network across its television and digital businesses. The main TEN channel and Network Ten are the only primary commercial free-to-air channel and the only commercial free-to-air network to have increased their prime time audiences this year. The growth of established programs and the successful launch of new shows saw both TEN and Network Ten achieve their highest commercial audience shares since 2011 (see Operational Highlights, page 11).

OUR PRIORITIESThe strategic goals for Ten Network over the next 12 months are very clear:

• We are focussed on improving our profitability and returns to our shareholders.

• We will continue to grow our revenue across all platforms.

• We will work closely with MCN to increase our “power ratio”, that is, closing the gap between our share of television viewers and our share of the capital city free-to-air television advertising market.

• We will continue to lead the industry on the digital and social media front, engaging with audiences across all platforms.

• We will continue to make strategic and disciplined investments in new content to increase our audience year-on-year.

• We will focus on improving the performance of our digital platform and our multi-channels ELEVEN and ONE.

OUR PEOPLEThere is no doubt that Ten Network’s greatest asset is the 800 people who work across our television and digital operations around the country. They are talented, enthusiastic, professional and smart, and I want to thank them for all their contributions over the past 12 months.

My thanks also to our company’s senior management team, who continue to work extremely hard and with great dedication during a challenging but rewarding period for our company. This team has been tasked with executing the strategic plan and they are working tirelessly to make this happen. The senior team grew on November 2 this year, when Dave Boorman joined as Chief Financial Officer. Dave has held senior executive roles at leading media and telecommunications companies in Australia, the UK and Ireland, including Seven West Media and Vodafone Hutchison. Welcome Dave.

Finally, I would like to extend my thanks to the Board for their constant support, guidance and commitment over the past 12 months.

Paul AndersonChief Executive Officer

Our online catch-up and streaming service, tenplay, had another strong year. It continued to expand its distribution, which is now the broadest among its peers (tenplay is now on 12 distribution platforms), and continued to generate significant growth in video views, page views, unique visitors and advertising revenue.

Thanks to the talent, passion and hard work of our Programming department, led by Chief Programming Officer, Beverley McGarvey, TEN now has a suite of programs that are at different points in their life cycles – from Shark Tank, I’m a Celebrity… Get Me Out of Here!, The Great Australian Spelling Bee and The Bachelorette Australia which are moving into their second years, to The Bachelor Australia, which will have its fourth season in 2016, and the phenomenon that is MasterChef Australia, which will return for its eighth season in 2016.

Ten Network works with the best production and content partners in the business and I would like to extend my thanks to 20th Century Fox, CBS Studios, Endemol Shine Australia, FremantleMedia, Roving Enterprises, Working Dog Productions, WTFN, ITV Studios Australia, Cordell Jigsaw Zapruder, McAvoy Media, Warner Bros, Fresh One, BBC Worldwide, So Television, Cricket Australia, Formula One Management, V8 Supercars Australia, Australian Rugby Union and Dorna Sports. They all play supportive and crucial roles in our content and programming strategies.

For

per

sona

l use

onl

y

ANNUAL REVIEW 201510

For

per

sona

l use

onl

y

TEN NETWORK HOLDINGS LIMITED 11

Ten Network’s 2015 strategic focus was on prime time for the TEN primary channel, delivering a consistent schedule across the survey year with the continued focus on the 25 to 54 demographic, supported by our industry-leading digital platform, tenplay.

The company invested in event television programming through 2015 across live premium sport with the KFC Big Bash League cricket competition, Formula One, MotoGP, Rugby Union and RPM. V8 Supercars also returned home to TEN in 2015 after a nine-year absence.

Investment in general entertainment content across proven domestic franchises continued in 2015 with MasterChef Australia, The Bachelor Australia and The Living Room. Family Feud continued to grow consistently, lifting the 6pm prime time weekday audience and contributing to a lift in audience and commercial share for The Project.

Successful new franchises launched in the 2015 financial year included I’m a Celebrity...Get Me Out of Here!, Shark Tank, Gogglebox and The Great Australian Spelling Bee.

Investment in domestic production will continue in the 2016 financial year with the successful launch of The Bachelorette Australia in September 2015 and the return of Offspring in 2016.

The company will continue to strengthen the TEN schedule and provide improved rating performance across key timeslots and demographics, focussing on the 25 to 54 demographic, fresh formats, cost-effective local production, premium live sporting events and a leading digital platform.

Ten Network continues to focus on strict cost control, identifying new, smarter and more efficient ways to operate productively. Revenue momentum will continue through exploiting new streams, including InTENsify and tenplay, growing our audiences across all screens and by increasing our power ratio in association with Multi Channel Network.

Ten Network is the only commercial free-to-air network to grow its prime time audience this year. Ten Network’s

OPERATIONAL HIGHLIGHTS

2015

strong growth in ratings and audience share was reflected in its share of the capital city free-to-air television advertising market. During the first nine months of calendar 2015, Ten increased its revenue share by 2.6 points.

BROADCASTTEN is the only commercial primary free-to-air channel that has increased its prime time audience during the 2015 ratings year. Network Ten is the only commercial free-to-air network to grow its prime time audience this year.

In the ratings period weeks 7 to 42, the main TEN channel’s prime time audience increased 9% in total people, 9% in 25 to 54s, 8% in under 55s and 11% in grocery buyers. TEN recorded its highest commercial shares in total people and 25 to 54s since 2011. In weeks 7 to 42, 2015, TEN had a 29.2% share in 25 to 54s and a 24.8% share in total people. TEN recorded audience growth on every night of the week except Saturday nights.

Some of the audience and audience share growth was driven by the four new, differentiated formats launched on TEN in 2015. I’m A Celebrity…Get Me Out Of Here!, Shark Tank, Gogglebox and The Great Australian Spelling Bee produced strong ratings and audience growth in the timeslots they occupied. All four new series were successful across multiple screens, not just the

television screen, and have been renewed for 2016.

The 2015 financial year also saw audience growth for many established TEN formats, including MasterChef Australia, Family Feud, The Bachelor Australia, The Project, The Living Room, Have You Been Paying Attention? and Bondi Rescue.

After growing its audience 31% in 2014, MasterChef Australia increased another 15% this year. The Winner Announced episode had 2.2 million capital city viewers and at the time this report was written, ranked as the #1 non-sport television program in 2015. Family Feud has given Network Ten its best 6pm to 6.30pm weekday audience numbers since 2009.

On ELEVEN, the iconic Australian series Neighbours celebrated its 30th anniversary, cementing its position as the long-running drama series in local television history.

TEN’s biggest hits will return in 2016 to complete a strong line-up of local and international hits. The iconic and highly successful local drama series Offspring is back on TEN next year, along with what will be one of the television events of 2016 – Brock.

TEN will have new seasons of key shows from its overseas suppliers, including Modern Family, NCIS, The Graham Norton Show and Madam Secretary.

For

per

sona

l use

onl

y

ANNUAL REVIEW 201512

TEN NETWORK: CHAMPIONING CHANGETen Network has been a member of the Male Champions of Change (MCC) since 2014. The MCC comprises Chief Executives from leading Australian organisations and aims to increase the representation of females in leadership roles in companies across Australia.

Ten Network is committed to leading the media industry in the MCC while we drive and improve our own strong internal gender balance. Ten Network’s focus on addressing barriers that face women in their career has seen the following initiatives implemented:

• All Roles Flexible At Ten has been implemented to make flexible work normal for everyone, for any reason.

This represents a significant change from flexibility being only available to some people, to flexible work practices becoming available to all at Ten Network. This long-term initiative will enable our employees to balance their careers with their differing personal needs.

• Through the MCC, Ten Network has begun to understand the impact that domestic and family violence can have on women in the workplace. We are committed to supporting our employees through raising awareness and implementing a range of recognised support initiatives.

Several Ten Network Executives have become White Ribbon Australia Ambassadors and Ten Network has developed strong ties with the organisation, devoting advertising airtime to support their message on violence against women.

• To ensure pay equity between male and female employees, Ten Network has implemented pay practices to evaluate and close gaps. Ten Network has also hosted and participated in business forums to raise awareness of the gender pay gap.

across Android, iOS and Windows devices. Its reach extends across smart televisions, Microsoft’s Xbox 360 and Xbox One platforms, FreeviewPlus, Apple TV and Fetch TV, giving tenplay broader distribution than similar online television services.

The strong growth of TEN shows on television has been mirrored in their rapid growth online. In the 12 months to August 31, 2015, tenplay recorded growth of 8% in page views, 7% in video views and 7% in unique visitors.

Key shows including MasterChef Australia and The Bachelor Australia saw substantial growth in video views on tenplay this year. MasterChef Australia recorded 22.4 million video views, up 38% year-on-year. The Bachelor Australia achieved 15.5 million view views across this year’s season, up 60% on 2014. The Bachelor Australia also recorded the biggest ever number of video views for a single program on tenplay in one week – 2.49 million.

The company’s digital advertising revenue increased 21% during the 2015 financial year, with premium advertising rates across the online inventory.

In 2016, tenplay will continue to expand its content and function. This will include more live streaming of Ten Network’s early evening and big prime-time shows, plus new distribution channels such as Sony’s PlayStation 4 console, Telstra TV and the native application for Android’s TV operating system.

SOCIAL MEDIA Ten Network’s strategy of reaching consumers where and when they are engaging with our content extends to communicating to them through social media. Every day, millions of Australians share their television viewing experience with others on Twitter and Facebook –

DIGITAL Television is no longer a linear viewing experience. Recognising that the way people want to consume media and entertainment content has changed, Ten Network has delivered a free, premium video catch-up and streaming platform that gives Australians what they want to watch, when they want to watch, and where and how they want to watch it.

The tenplay online catch-up and streaming product takes content across multiple screens, creating deeper audience engagement and a richer consumer experience. Since it was introduced in September 2013, tenplay has led the market in terms of innovation and growth. There have been more than two million downloads of the free mobile device tenplay app

For

per

sona

l use

onl

y

TEN NETWORK: GIVING BACK TO THE COMMUNITYTen Network is committed to supporting and giving back to the communities in which we operate and helping our staff find ways to work with a diverse range of foundations and not-for-profit organisations.

Every year, all Ten Network channels around the country promote charitable causes through on-air promotional campaigns, including community service announcements. These campaigns cover many national and local not-for-profit organisations and involve Ten Network providing air-time and technical assistance, including script writing, filming and editing support.

Over the past 12 months, our community partnerships have included organisations such as Blue September, Bowel Cancer Australia, Cure Brain Cancer Foundation, MS Walk and Fun Run, Murdoch Children’s Research Institute, Ovarian Cancer Research Foundation and Soldier On.

Ten Network’s community support and engagement activities grew in October 2014 with the launch of TEN Gives, a workplace giving program set up and run in partnership with UnLtd, a not-for-profit foundation that works across the media and marketing industries to help eliminate the consequences of youth disadvantage in Australia.

The idea behind TEN Gives was simple. It was created as a way for Ten Network staff to give their time, talent, resources and money to help charities that help disadvantaged youth. Every dollar given by a staff member is matched by the company.

TEN Gives started in the TEN Sydney station with four charity partners: Batyr, KYDS, Musicians Making A Difference and Youth Off The Streets. Today, it operates in all five Ten Network stations around the country and encompasses another seven charities: Big Brothers Big Sisters, Camp Quality, Melbourne City Mission, Radio Lollipop, The Pyjama Foundation, Uniting Care Wesley Port Adelaide and Youth Opportunities SA.

During its first year, TEN Gives raised more than $1 million in cash and kind for its 11 partners.

The scope of TEN Gives’ activities included staff fundraisers, running social media campaigns, the mentoring of our partners’ staff, volunteering with the charities, creating videos and other marketing materials, and connecting the charities with TEN programs such as The Project, TEN Eyewitness News First At Five, Studio 10, The Loop and Couch Time.

UnLtd General Manager Carol Morris thanked Ten Network staff for how generous they have been in giving their time, talent and money.

“TEN Gives is most certainly our showcase partnership. They have embraced our call to join the movement and created a very powerful, measureable and highly effective social impact program,” she said.

and Ten Network leads its rivals in terms of the breadth and depth of its social media activities and engagement with consumers.

The company runs more than 150 different social media channels and accounts spanning Twitter, Facebook and Instagram. These accounts have more than 10 million followers in total, a number that increased 15% over the past year. That growth was driven by social media sensations such as The Bachelor Australia, MasterChef Australia, I’m a Celebrity… Get Me Out of Here! and The Project.

Those shows, and others, successfully tap into social media to build a deep engagement with viewers and to create consumer-led communities around Ten Network content and on-air personalities.

MasterChef Australia, The Bachelor Australia and I’m A Celebrity... Get Me Out Of Here! all ranked as the #1 television show on Twitter during their run.

MasterChef Australia also remains the most popular Australian television program on Facebook, with more than 1.45 million “likes”.

MULTI CHANNEL NETWORKTen Network’s sales representation agreement with Multi Channel Network was announced on June 15, 2015, and took effect on September 1.

MCN is now responsible for all broadcast and digital selling activities, including employing sales and support staff. Ten Network retained responsibility over all strategic functions including pricing, commercial integration and the setting of rate cards.

The partnership is a game changer for Ten Network, MCN, the television industry and the broader advertising

and media sectors. For advertisers and agencies, the combination of Ten Network’s three capital city free-to-air channels and the 70 subscription television channels represented by MCN creates the largest broadcast television inventory offering in the market.

The partnership gives advertisers a new way to reach consumers across all video content distribution platforms. It creates a business that can offer scale with one transaction, including mass targeting and minimal wastage, new content alignment opportunities and smarter, more efficient trading.

Together, Ten Network and MCN capture about 41% of viewers in the key advertiser demographic of 25 to 54 year olds. That large audience share provides advertisers and agencies with access to a large audience and more efficient transactions, with negligible duplication between Ten Network and MCN.

In the digital world, tenplay has now joined with other leading platforms such as Telstra, Fox Sports and Foxtel – making MCN the second largest digital publisher in Australia.

The partnership gives Ten Network access to MCN’s world-class audience targeting and trading platforms Landmark and Multiview. Landmark is one of the world’s most advanced television trading systems, automating the television and digital buying process. Landmark will improve Ten Network’s ability to provide highly targeted, effective and cost efficient results for advertisers and agencies.

Multiview is the most sophisticated audience targeting television product in Australia. Advertisers are able to purchase actual consumer segments, based upon real purchasing behaviour.

TEN NETWORK HOLDINGS LIMITED 13

For

per

sona

l use

onl

y

AnnuAl Review 201514

Directors’ report

The Directors’ Report, Concise Financial Report and Auditor’s Statement contained within this document represent a Concise Report. The Concise Financial Report contained within this document has been derived from the Full Financial Report of Ten Network Holdings Limited for the financial year ended 31 August 2015 and cannot be expected to provide as full an understanding of the financial performance, financial position and financing and investing activities of the consolidated entity as the Full Financial Report. Further financial information can be obtained from the Full Financial Report and the report is available on the Ten website.

The Directors of Ten Network Holdings Limited present their report on the consolidated entity, consisting of Ten Network Holdings Limited (“the Company”) and its controlled entities, for the year ended 31 August 2015.

DirectorsThe Directors that have been in office at any time during or since year end are:

Mr DL Gordon (ChairmanA)

Mr BJ Long (Deputy Chairman) (Alternate Mr DL Gordon)

Mr JJ Cowin (Alternate Mr PV Gleeson)

Mr PV Gleeson (Alternate Mr JJ Cowin)

Mr DD Hawkins (Alternate Mr DL Gordon)

Ms CW Holgate (Alternate Mr DL Gordon)

Ms SL McKenna (Alternate Mr BJ Long)

Mr J Klepec B (Alternate Mr BJ Long)

Mr HR McLennan C

Mr PR Mallam D

Ms GH Rinehart E

A: Mr DL Gordon was appointed as Chairman effective 27 July 2015.B: Mr J Klepec appointed as Director effective 3 November 2014.C: Mr HR McLennan resigned as Executive Chairman effective

27 July 2015.D: Mr PR Mallam resigned as Director effective 29 November 2014.E: Ms GH Rinehart resigned as Director effective 31 October 2014.

principal ActivitiesThe principal activity of the Company is the investment in The Ten Group Pty Limited (“Ten Group”) and controlled entities, whose principal activities are the operation of multi-channel commercial television licences in Sydney, Melbourne, Brisbane, Adelaide and Perth, a national online media platform, and out-of-home advertising in the United States of America.

operating and Financial reviewIn July 2015 Hamish McLennan resigned as Chief Executive Officer and Executive Chairman. David Gordon was appointed Chairman and Paul Anderson was promoted from the Chief Operating Officer role to Chief Executive Officer. The Management Team supporting the CEO has been stable over the period.

In June 2015 the Company and The Multi Channel Network Pty Ltd (MCN) announced a long-term agreement for MCN to represent the Company’s television, catch-up and digital properties for advertisers. MCN commenced sales representation on behalf of the Company from 1 September 2015. The agreement allows the Company to gain scale, new efficiencies, improved data capability and broader integration opportunities for advertising clients.

The Company grew ratings and revenue through 2015, resulting from the clear strategic focus on:

• Event television

• Premium live sport

• 25-54 demographic

• Consistency in program schedules

• Development of new formats

• Expansion of digital platforms and revenue.

The strategic focus has resulted in strengthening of programming across the schedule, providing improved revenue and ratings performance in the 2015 calendar year with approximately 67% of all time-slots in prime time showing year on year growth.

Financial Performance and HighlightsA summary of the consolidated results for the year ended 31 August 2015 are set out as follows:

2015$’000

2014$’000

(Loss) before income tax (i) (305,050) (166,606)

Income tax (expense)/benefit (ii) (3,400) 3,137

(Loss) for the year (308,450) (163,469)

Profit attributable to non-controlling interests 3,798 4,846

(Loss) attributable to members of the Company (312,248) (168,315)

(i) Includes $262.9m net loss of individually significant items that are non-recurring in nature in 2015 (2014: $54.2m).(ii) Includes $1.1m of non-recurring tax benefit in 2015 (2014: $1.3m tax benefit).

For

per

sona

l use

onl

y

Ten neTwork Holdings limiTed 15

For the year ending 31 August 2015, the Company reported a net loss after tax of $308.5m (2014: loss of $163.5m). This included $262.9m net loss of individually significant items that are non-recurring in nature (2014: $54.2m).

The Company’s revenues from continuing operations grew 4.5% to $654.1m (2014: $626.0m).

The Company’s Earnings before Interest, Tax, Depreciation and Amortisation (EBITDA) before non-recurring items for 2015 was a loss of $12.0m (2014: loss of $79.3m).

The Company’s net cash outflows generated from operating activities in 2015 was $55.0m (2014: net cash outflow of $38.7m).

Expenses in the television segment decreased year on year. 2014 programming costs included the XXII Olympic Winter Games in Sochi and XX Commonwealth Games in Glasgow, not occurring in 2015. Operating cost savings were realised in 2015, resulting from the news and operational restructures in 2014 and ongoing strict cost control.

The net operating loss after tax from continuing operations included the following revenue and costs that are significant and non-recurring in nature:

• $251.2m impairment of the television licence

• $6.7m provision for onerous contracts in Eye Corp’s US business

• $6.3m of restructuring costs.

Partially offset by the following revenue item:

• $1.3m gain on sale of Our Deal Pty Limited.

Total borrowings (all non-current) was $154.9m as at 31 August 2015 which includes:

• A bank loan of $135m drawn on the $200m Revolving Cash Advance Facility

• Capitalised interest and commitment fees of $10.8m

• Shareholder guarantor fees of $11.2m

• Less: Capitalised transaction costs of $2.1m.

Net debt relating to the Company’s Revolving Cash Advance Facility at 31 August 2015 was $131.4m (loan of $135m, capitalised interest and commitment fees of $10.8m less cash of $14.4m).

Total cash and equivalents of $14.4m as at 31 August 2015 was $0.9m above the prior year.

Cash outflows from operating activities of $55.0m are driven by the operating loss for the period, partly offset by the reduction of interest paid due to the capitalisation of interest costs for the full year compared to six months in the prior year. These will be payable on maturity of the bank facility in December 2017.

Cash inflows from investment activities of $14.8m represent the deferred consideration received in December 2014 in relation to the sale of Eye Corp Pty Limited in November 2012, funding received in the form of a government grant as a result of a change in television spectrum, as well as proceeds from the sale of Our Deal Pty Limited, offset by fixed asset additions. Prior year investing cash inflows included proceeds from the sale of the Perth property and Oasis.

Cash inflows from financing activities of $40.3m are mainly due to net loan drawdowns and repayments made on the $200m Revolving Cash Advance Facility. Prior year financing activities also included the repayment of the A$150m US Private Placement Facility.

Significant balance sheet movements during the year were as follows:

• The estimated recoverable amount of the Television CGU, based on value-in-use, equals its carrying amount following a $251.2 impairment loss booked during the year.

• The Onerous contracts provision reduced from $35.3m in 2014 to $18.0m, reflecting the utilisation of $24.0m provisions in 2015 (including an interest charge for the unwinding of the provisions and foreign exchange), and $6.7m additional provisions recognised as non-recurring charges.

Operational HighlightsIn 2015 the Company continued its strategy focusing on Event TV, including premium sport, aimed at people aged 25 to 54.

For the 2015 survey year to August, TEN primary channel and Network Ten have achieved their biggest audiences in total people and 25-54s since 2012 and their highest commercial share in total people and 25-54s since 2011. TEN is the only commercial primary channel and Network Ten is the only commercial network to grow in total people (OzTAM, 5 City Metro, Zone 1, Weeks 7-35 2015 vs. 2014, excl. Easter).

Business and Strategic RisksBusiness risks that could affect the achievement of the Company’s financial prospects include:

• Failure of the MCN partnership to generate sufficient sales revenue, with negative impacts on revenue and cash flow. The Company has developed strong communication channels and reporting protocols with MCN to mitigate this risk along with retaining key sales management at the Company working with MCN to ensure the relationship operates effectively.

• The Company is unable to negotiate and secure funding to refinance debt as a result of internal and external influences. The Company launched a share entitlement offer to existing shareholders alongside an issue of new shares to Foxtel, which is expected to raise up to $154 million of gross proceeds. See Events Subsequent to Balance Date note for further details.F

or p

erso

nal u

se o

nly

AnnuAl Review 201516

Directors’ report CONTINUED

• An inability to secure and develop appropriate program rights, from both the domestic and overseas market, that generate ratings and in turn, revenues. Controls over the selection, commissioning and approval of content mitigate this risk, with programming decisions backed by research and executive approval to ensure spend is aligned to the strategic plan.

• Inability to react to structural changes and market pressures in the free to air advertising market. To mitigate this risk, the Company continues to invest in and develop the Company’s digital platform (tenplay); has entered into an SVOD Option Agreement with Presto; and follows a structured approach to reviewing investment opportunities to capitalise on new and emerging trends.

• A significant and sustained transmission failure. The Company continues to have robust controls in place to mitigate this risk, including redundancy, dual transmission sites, dual paths of carriage, backups and real-time incident monitoring. The Company also maintains prudent insurance coverage.

Business strategies and outlookThe 2015 strategic focus has been on prime time for the TEN primary channel, delivering a consistent schedule across the survey year, with the continued focus on the 25-54 demographic, supported by tenplay.

The Company invested in Event TV programming through 2015 across premium sport with the KFC Big Bash League cricket competition, V8 Supercars (new to 2015), Formula One, MotoGP and RPM.

Investment in general entertainment content across proven domestic franchises continued in 2015 with MasterChef Australia, The Bachelor Australia and The Living Room. Family Feud continued to grow consistently, lifting the 6.00pm prime time weekday audience and contributing to a lift in audience and commercial share in The Project. Successful new franchises launched in 2015 included I’m a Celebrity.. Get Me Out of Here!, Shark Tank, Gogglebox and The Great Australian Spelling Bee.

Investment in domestic production continues in 2016 with the return of Offspring and the launch of The Bachelorette Australia.

Television is no longer purely a linear viewing experience and the tenplay digital platform represents the first phase of the Company’s TV Everywhere strategy. tenplay takes content across multiple screens with deeper audience engagement. tenplay has surpassed 2 million downloads of its mobile device app across Android, iOS and Windows devices, and reach extends across smart TVs, Microsoft’s Xbox 360, Xbox One platforms and through FreeviewPlus, Apple TV and Fetch TV. The Company’s digital advertising revenue increased 21% over the past year with premium advertising rates across the online inventory.

Demand in the television advertising market remains subdued, characterised by short-term booking cycles. Despite these conditions, the Company’s television revenue grew by 4.6% in 2015.

The Company will continue to strengthen the schedule and provide improved ratings performance across key timeslots and demographics, focussing on the 25 to 54 demographic, fresh formats, cost effective local production, premium sporting events and a leading digital platform.

The Company continues to focus on strict cost control, identifying efficiencies to work more productively.

DividendsThe Company did not pay any dividends during the period.

significant changes in the state of AffairsIn June 2015 the Company and The Multi Channel Network Pty Ltd (MCN) announced a long-term agreement for MCN to represent the Company’s television, catch-up and digital properties for advertisers. MCN commenced sales representation on behalf of the Company from 1 September 2015. The agreement allows the Company to gain scale, new efficiencies, improved data capability and broader integration opportunities for advertising clients. The Company will become a 24.99% shareholder in MCN and have a seat on the MCN board.

events subsequent to Balance DateOn 22 October 2015, approval was received from the Australian Competition and Consumer Commission (‘ACCC’) and the Australian Communications and Media Authority (‘ACMA’) for the proposed equity raising transaction between Ten Network Holdings Limited and Foxtel Management Pty Limited (‘Foxtel’).

On 26 October 2015, the Company launched a fully underwritten pro-rata renounceable share entitlement offer to existing shareholders of up to $77m. This entitlement offer is to be conducted in conjunction with an issue of shares to Foxtel for gross proceeds of up to $77m which would result in Foxtel becoming a shareholder of up to 15%.

Settlement of the share entitlement offer and Foxtel placement are subject to the completion of certain customary conditions and other approvals, including from the Foreign Investment Review Board, which are expected to be obtained in the ordinary course.

No other matters or circumstances have arisen since balance date that have significantly affected or may significantly affect:

• the operations in financial years subsequent to 31 August 2015 of the consolidated entity; or

• the results of those operations; or the state of affairs in financial years subsequent to 31 August 2015 of the consolidated entity.

For

per

sona

l use

onl

y

Ten neTwork Holdings limiTed 17

information on DirectorsDavid L Gordon Director since 1 April 2010.

experience and expertise

Mr Gordon is a former M&A partner at the Sydney law firm, Freehills (now Herbert Smith Freehills), and subsequently at former corporate advisory firm, Wentworth Associates Pty Ltd, prior to founding Lexicon Partners Pty Ltd, an independent corporate advisory and investment firm based in Sydney and with a specialisation in technology, media and telecommunications. Mr Gordon has advised and acted for a number of Australia’s major media businesses over the last 30 years.

He is a Director of RCG Corporation Limited. He holds a Bachelor of Commerce and Bachelor of Laws degrees from the University of New South Wales and is a member of the Australian Institute of Company Directors.

other current directorships

RCG Corporation Limited (appointed 19 October 2006)

Former directorships in last 3 years

None

special responsibilities

Chairman – appointed 27 July 2015

Chairman of Remuneration Committee – appointed 17 September 2014

interests in shares and options

Ordinary shares – 247,500

Brian J Long Director since 1 July 2010.

experience and expertise

Mr Long previously chaired the Global Governance and Advisory Council of EY and also chaired the Council for the firm’s Oceania Area. He was a Partner of EY for almost 30 years and was one of the firm’s most experienced audit partners. He retired from EY on 30 June 2010.

Mr Long is a Director of the Commonwealth Bank of Australia and Chairman of its Audit Committee. He is a non-executive Director of Brambles Limited and Chairman of its Audit Committee and is also a Director of Cantarella Bros Pty Ltd. Mr Long is Chairman of the Audit Committee of the University of New South Wales and is also a member of the University’s Council. He is Chairman of the charitable organisation, United Way Australia.

Mr Long is a Fellow of the Institute of Chartered Accountants in Australia and has been a member since 1972.

other current directorships

Commonwealth Bank of Australia (appointed 1 September 2010)

Brambles Limited (appointed 1 July 2014)

Former directorships in last 3 years

None

special responsibilities

Deputy Chairman

Member of Audit/Risk/Treasury Committee

Member of Remuneration Committee

Chairman of Board Performance and Renewal Committee

interests in shares and options

Ordinary shares – 533,250

Jack J cowin Director since April 1998.

experience and expertise

Mr Cowin is the Founder and Chairman of Competitive Foods Australia Limited, Director of Fairfax Media and BridgeClimb and the largest shareholder and Chairman of Domino’s Pizza Enterprises.

Mr Cowin is Chancellor Elect for Western University in London, Ontario.

other current directorships

Fairfax Media Group Limited (appointed 19 July 2012)

Domino’s Pizza Enterprises Limited (appointed 20 March 2014)

Former directorships in last 3 years

Chandler Macleod Group (appointed 1 March 2011), delisted 7 April 2015.

special responsibilities

Member of Remuneration Committee

Member of Board Performance and Renewal Committee

interests in shares and options

Ordinary shares – 2,475,000

paul V Gleeson Director since February 1998.

experience and expertise

Mr Gleeson holds a Bachelor of Economics degree and is a member of the Institute of Chartered Accountants in Australia.

other current directorships

None

Former directorships in last 3 years

None

special responsibilities

Chairman of the Audit/Risk/Treasury Committee

interests in shares and options

Ordinary shares – 2,938,274For

per

sona

l use

onl

y

AnnuAl Review 201518

Directors’ report CONTINUED

Dean D Hawkins Director since 1 April 2010.

experience and expertise

Mr Hawkins has led international businesses at the forefront of the broadband, digital media, television and sports industries in Australia and overseas for the past 19 years. Mr Hawkins is Chairman of the Advisory Board at Skins Global Holdings AG and a strategic advisor to the media and telecommunications industries. His previous positions include Executive Director of Video Networks Limited (VNL), UK’s first IPTV platform, Executive Director of Chello Media, a European broadband ISP and digital media company, and Managing Partner at the venture capital firm, OneVentures.

He is a member of the British Academy of Film and Television Arts, having received BAFTA and Emmy awards for TV channels created by his teams at VNL, was a director of Sydney Dance Company until August 2012 and was a founding board member of the Salvation Army Oasis Centre, a centre for homeless youths and suicide prevention services in Sydney.

He is a chartered accountant, was previously an investment banker in Australia and Europe and holds a Bachelor of Commerce degree.

other current directorships

None

Former directorships in last 3 years

None

special responsibilities

Member of the Audit/Risk/Treasury Committee

interests in shares and options

Ordinary shares – 135,000

christine W Holgate Director since 1 April 2010.

experience and expertise

Ms Holgate has over 30 years of diverse international experience leading in highly regulated industries, including healthcare, media, telecommunications and finance and is presently the Chief Executive Officer of Blackmores, appointed November 2008.

In September 2015, Ms Holgate was appointed Chair of the ASEAN Australia Council Advisory Board by the Government. In 2013 Ms Holgate was honoured with the Rotary Paul Harris Award and in 2011 the (inaugural) International Executive Study Scholarship by Chief Executive Women and the Women’s Leadership Institute Australia.

other current directorships

Blackmores Limited (appointed November 2008)

Former directorships in last 3 years

None

special responsibilities

Member of the Remuneration Committee

interests in shares and options

Ordinary shares – 69,920

siobhan L McKenna Director since 26 June 2012.

experience and expertise

Ms McKenna is Managing Partner of Illyria Pty Ltd, non-executive Director of Nova Entertainment, non-executive Director of The Australian Ballet and Trustee of the MCG Trust.

Ms McKenna is a former Partner of management consulting firm McKinsey & Company. She has also held previous roles as Commissioner of the Productivity Commission and non-executive Director of NBN Co.

other current directorships

None

Former directorships in last 3 years

Prime Media Group Limited (from 20 August 2009 to 29 March 2012)

special responsibilities

Member of the Audit/Risk/Treasury Committee

Member of the Remuneration Committee

interests in shares and options

None

John Klepec Director since 3 November 2014.

experience and expertise

Mr Klepec is the Chief Development Officer for Hancock Prospecting Pty Limited.

Mr Klepec was proposed for appointment as a Director of the Company by Hanrine Investments Pty Limited, which is a major shareholder in the Company.

Mr Klepec has a very broad experience of over 20 years prior to his current position, having held senior management roles in business development, finance and operations at BHP Billiton Limited, Mayne Group Limited and BGC Group Pty Ltd.

Mr Klepec holds a Bachelor of Commerce from the University of Western Australia, is a certified practicing accountant with the Australian Society of CPA’s and is a Fellow of FINSIA.

other current directorships

None

Former directorships in last 3 years

None

special responsibilities

None

interests in shares and options

NoneFor

per

sona

l use

onl

y

Ten neTwork Holdings limiTed 19

stephen partington – company secretaryexperience and expertise

Mr Partington was appointed as Company Secretary of The Ten Group Pty Limited in October 1996 and as Company Secretary of Ten Network Holdings Limited in June 2001. He also held the position of Group General Counsel from 1996 to 2011.

Mr Partington graduated with a Bachelor of Commerce and Bachelor of Laws from the University of New South Wales and Masters of Laws from each of Sydney University and the University of Technology, Sydney.

He is a fellow of the Governance Institute of Australia and the Institute of Chartered Secretaries and Administrators and a member of the Law Society of New South Wales and Australian Corporate Lawyers Association.

He has been admitted as a solicitor in New South Wales since 1980.

Directors’ MeetingsThe number of meetings of the Company’s Board of Directors and of each Board Committee held during the year ended 31 August 2015, and the number of meetings attended by each Director were:

DiReCtOR’S Name/aLteRNate Name (iF aPPLiCaBLe)

Date aPPOiNteD

DateReSigNeD

meetiNg OF DiReCtORS

auDit/ RiSk/ tReaSuRy

COmmitteeRemuNeRatiON

COmmittee

BOaRDPeRFORmaNCe aND ReNewaL

COmmittee

meetings a B a B a B a B

Mr DL Gordon 01/04/10 Continuing 23 21 – – 2 2 – –

Mr BJ Long (Alternate) 01/07/10 Continuing – 2 – – – – – –

Mr BJ Long 01/07/10 Continuing 23 20 3 3 2 2 4 4

Mr DL Gordon (Alternate) 21/06/12 Continuing – 3 – – – – – –

Mr JJ Cowin 03/04/98 Continuing 23 20 – – 2 2 4 4

Mr PV Gleeson (Alternate) 22/11/10 Continuing – 3 – – – – – –

Mr PV Gleeson 16/02/98 Continuing 23 21 3 3 – – – –

Mr JJ Cowin (Alternate) 10/12/10 Continuing – 2 – – – – – –

Mr DD Hawkins 01/04/10 Continuing 23 23 3 3 – – – –

Mr DL Gordon (Alternate) 24/11/10 Continuing – – – – – – – –

Ms CW Holgate 01/04/10 Continuing 23 22 – – 2 1 – –

Mr DL Gordon (Alternate) 14/12/10 Continuing – 1 – – – 1 – –

Ms SL McKenna 26/06/12 Continuing 23 21 3 3 2 2 – –

Mr BJ Long (Alternate) 20/10/14 Continuing – 1 – – – – – –

Mr J Klepec 3/11/14 Continuing 18 17 – – – – – –

Mr BJ Long (Alternate) 14/06/15 Continuing – 1 – – – – – –

Mr HR McLennan 08/04/13 27/07/15 21 21 – – – – 3 3

Mr PR Mallam 13/12/10 29/11/14 7 7 1 1 – – – –

Ms GH Rinehart 13/12/10 31/10/14 5 – – – – – 1 –

Mr J Klepec (Alternate) 16/10/13 31/10/14 – 4 – – – – – –

Mr JJ Cowin (Alternate) 10/11/11 31/10/14 – 1 – – – – – –

A Number of meetings held during the year during which the Director was in office

B Number of meetings attendedFor

per

sona

l use

onl

y

AnnuAl Review 201520

Directors’ report CONTINUED

remuneration reportThe Directors present the 2015 remuneration report for Ten Network Holdings Limited, outlining key aspects of remuneration policy and framework, and remuneration awarded to Key Management Personnel this year.

The information provided in this remuneration report has been audited as required by section 308(3C) of the Corporations Act 2001.

summary of 2015 outcomesThe table below summarises the specific items that impacted remuneration during the Company’s 2015 financial year which covers the period 1 September 2014 to 31 August 2015.

Short term incentive scheme (STI)

In the 2015 financial year, some but not all of the performance hurdles were met. As a result, no STI payments will be made to participants. However, the Directors agreed that an ex-gratia bonus payment be made to certain executives to reflect their significant efforts over the past financial year. This is also in recognition that some performance targets were met and that there has been a recent improvement in the performance of the Company. This improvement is evidenced through ratings and revenue growth in the 2015 year. Ratings grew across key timeslots and demographics, with 2015 ratings up +1.4% to 24.7% audience share (2014: 23.3%). This has driven a 2015 revenue share growth of +1.3% to 21.8% (2014: 20.5%). These factors have led to an improvement in underlying EBITDA to a ($12.0m) loss, up $67.3m or 84.9% from a ($79.3m) loss in 2014.

Long term incentive scheme (LTI)

Allocations of Loan Funded Shares (described in Section (d) of the remuneration report) were made in 2015 under the Ten Executive Incentive Plan, which was introduced in 2014 following shareholder approval in December 2013. All allocations made under this Plan in the 2014 and 2015 financial years are subject to the satisfaction of performance hurdles at the end of a 3 year performance period.

For 2016, the Board does not intend to make allocations of Loan Funded Shares but instead, the Board has determined that allocations of performance rights will be made under an amended Ten Executive Incentive Plan. Performance rights will be subject to revenue share and EPS performance hurdles, with a performance period of 3 years. At the date of this report, the details of the performance rights entitlement and allocations to individual executives have not yet been determined.

Termination payments Mr HR McLennan, the former Executive Chairman and Chief Executive Officer, provided 12 months’ notice of termination on 27 July 2015. This remuneration report includes as termination payments any amounts paid, payable or expensed in relation to the termination agreement signed by Mr HR McLennan and the Company. This includes payments totalling $1,975,000 (equal to Mr HR McLennan’s annual salary) to be made over the twelve month notice period and a negotiated termination payment of $250,000 at the end of the twelve month period, reflecting his contractual STI incentive entitlements during his notice period.

Expenses for Loan Funded Shares issued under the 2014 and 2015 Ten Executive Incentive Plan have been accelerated under requirements of AASB 2 Share-Based Payment. In order for these grants to be exercised, they need to meet certain hurdles as disclosed in section (d). The first measurement dates for these grants are 31 August 2016 and 31 August 2017 respectively. Also included is an estimate of Mr HR McLennan’s pro-rata contractual entitlement to participate in the 2016 LTI plan.

contents of the remuneration reportThis remuneration report contains the following sections:

(a) Key Management Personnel (KMP) covered in this report

(b) Board Remuneration Committee

(c) Principles used to determine the nature and amount of executive remuneration

(d) Executive pay framework

(e) Relationship between remuneration and Company performance

(f) Non-executive Director remuneration

(g) Details of remuneration

(h) Details of share-based compensation and bonuses

(i) Equity instruments held by Key Management Personnel

(j) Service agreements.

For

per

sona

l use

onl

y

Ten neTwork Holdings limiTed 21

(a) key management Personnel (kmP) covered in this report

Non-executive Directors

Name Name

Mr DL Gordon (Chairman from 27 July 2015) Mr J Klepec (from 3 November 2014)

Mr JJ Cowin Mr BJ Long

Mr PV Gleeson Mr PR Mallam (to 29 November 2014)

Mr DD Hawkins Ms SL McKenna

Ms CW Holgate Ms GH Rinehart (to 31 October 2014)

other (executive) Key Management personnel

Name POSitiON

Mr PD Anderson Chief Executive Officer – from 27 July 2015Chief Operating Officer and Chief Financial Officer – to 27 July 2015

Ms B McGarvey Chief Programming Officer

Mr HR McLennan Executive Chairman and Chief Executive Officer – to 27 July 2015

(b) Board Remuneration CommitteeThe Board Remuneration Committee reviews remuneration and incentive policies and practices and provides specific recommendations to the Board on remuneration packages and other terms of employment for executive Directors and other senior executives. Reviews are undertaken annually, taking into account competitor practices and performance. The Board approves remuneration for executive Directors, other senior executives and non-executive Directors.

The objective of the Company’s executive reward framework is to ensure reward for performance is competitive and appropriate for the results delivered. The framework aligns executive reward with achievement and sustainability of profit and the creation of value for shareholders. The Board ensures that executive reward satisfies the following key criteria for good reward governance practices:

• Performance linkage / alignment of executive compensation

• Transparency

• Capital management

(c) Principles used to determine the nature and amount of executive remunerationThe Company has in the current and in previous years consulted with external remuneration consultants to structure an executive remuneration framework that is intended to align with shareholders’ and executives’ interests.

Alignment to shareholders’ interests is achieved by:

• Having revenue share, net profit after tax and positive cash flow as core components of the Company’s short term incentive plan design and EPS and revenue share as core components of the Company’s long term incentive plan design

• Including a focus on key non-financial drivers of value

• Requiring that a significant proportion of executive pay be received as shares

• Deferring vesting of shares subject to continued service and achievement of performance hurdles over a number of years

• Only retaining the service of high performing executives who continue to deliver results.

Alignment to executives’ interests is achieved by:

• Establishing a rewards basis that is fair given capability and experience

• Reflecting individual and team performance

• Providing a transparent structure for earning rewards

• Providing recognition for contribution.

(d) executive pay frameworkThe framework for the year ending 31 August 2015 provides a mix of fixed and variable pay, and a blend of short and long term incentives. As executives attain more accountability within the group, the balance of this mix shifts to a higher proportion of “at risk” rewards.

The current executive pay and reward framework has three components:

• Base pay and benefits

• Short-term performance incentives

• Long term incentives through participation in the Ten Executive Incentive Plan.

The combination of these components comprises the executives’ total remuneration.

Base pay and benefitsBase pay is structured as fixed remuneration that may be delivered as a combination of cash, superannuation and salary packaged benefits, including motor vehicles.

Base pay for senior executives is reviewed annually. External remuneration consultants periodically provide analysis and advice to ensure base pay is set to reflect the market for a comparable role. Preference is given to matching pay with market levels of direct competitors if this information is available, rather than a broad based group of comparator companies. The Company must recruit and retain talent from a relatively small pool of candidates with industry experience. Given the size of the talent pool, senior executive roles attract a remuneration premium across the industry.

For

per

sona

l use

onl

y

AnnuAl Review 201522

Directors’ report CONTINUED

The Company has benchmarked its fixed pay against its direct competitors and this has highlighted that the Company’s KMPs are rewarded at lower levels than these direct competitors.

Some executives have fixed annual base pay increases included as a term of their employment contract. Retirement benefits may be delivered under an accrued benefit superannuation fund sponsored by the Company or through contributions to a superannuation fund nominated by the executive.

incentivesSenior executives are entitled to a maximum contracted total incentive in addition to their total fixed remuneration and the amount of that maximum contracted total incentive is equal to a percentage of that total fixed remuneration. The maximum contracted total incentive is divided into a short term and a long term incentive component.

The short term incentive component for senior executives comprises 25% of the maximum contracted total incentive. If the specified performance hurdles for the short term incentive component for the year are met, a cash award up to that amount will be paid. No short term incentives were awarded for the 2015 financial year due to some but not all performance hurdles being met.

However, the Directors agreed that an ex-gratia bonus payment be made to certain executives to reflect their significant efforts over the past financial year. This payment is also in recognition that some performance targets were met and that there has been a recent improvement in the performance of the Company. This improvement is evidenced through ratings and revenue growth in the 2015 year.

The long term incentive component for senior executives comprises 75% of the maximum contracted total incentive. In 2014, the Remuneration Committee implemented the current long term incentive scheme (“Ten Executive Incentive Plan”) for senior executives to bolster the Company’s remuneration framework and to ensure that the Company is able to attract, retain and incentivise highly skilled executives.

The scheme is also designed to enhance the alignment between senior executive compensation and the future return to the Company’s shareholders.

Assessing performance and claw-back of remunerationThe Remuneration Committee is responsible for assessing performance against key performance measures and determining the short and long term incentives to be paid. To assist in this assessment, the Committee receives objective feedback on performance from management which is based on independently verifiable data, such as financial measures and individual performance against targets.

In the event of serious misconduct or a material misstatement in the Company’s financial statements, the Remuneration Committee can cancel or defer performance-based remuneration and may also claw back performance-based remuneration paid in previous financial years.

Further details on short and long term incentives are provided below and in the following pages.

short term incentivesShort Term Incentives (STIs) are available through cash bonuses to certain executives as determined by the Remuneration Committee. No STIs were awarded for the 2015 financial year due to some but not all performance hurdles being met.

However, the Directors agreed that an ex-gratia bonus payment be made to certain executives to reflect their significant efforts over the past financial year. This payment is also in recognition that some performance targets were met and that there has been a recent improvement in the performance of the Company. This improvement is evidenced through ratings and revenue growth in the 2015 year. Ratings grew across key timeslots and demographics with 2015 ratings up +1.4% to 24.7% audience share (2014: 23.3%). This has driven a 2015 revenue share growth of +1.3% to 21.8% (2014: 20.5%). These factors have led to an improvement in underlying EBITDA to a ($12.0m) loss, up $67.3m or 84.9% from a ($79.3m) loss in 2014.

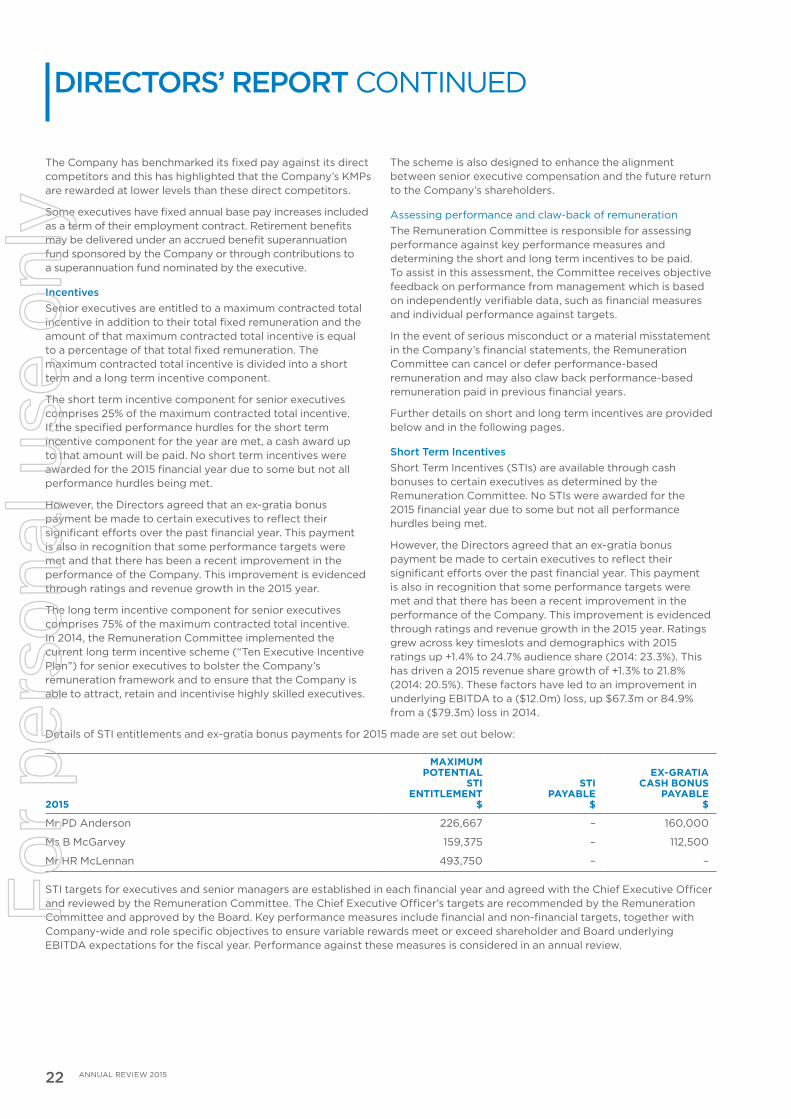

Details of STI entitlements and ex-gratia bonus payments for 2015 made are set out below:

2015

maximumPOteNtiaL

Sti eNtitLemeNt

$

Sti PayaBLe

$

ex-gRatiaCaSH BONuS

PayaBLe$

Mr PD Anderson 226,667 – 160,000

Ms B McGarvey 159,375 – 112,500

Mr HR McLennan 493,750 – –

STI targets for executives and senior managers are established in each financial year and agreed with the Chief Executive Officer and reviewed by the Remuneration Committee. The Chief Executive Officer’s targets are recommended by the Remuneration Committee and approved by the Board. Key performance measures include financial and non-financial targets, together with Company-wide and role specific objectives to ensure variable rewards meet or exceed shareholder and Board underlying EBITDA expectations for the fiscal year. Performance against these measures is considered in an annual review.

For

per

sona

l use

onl

y

Ten neTwork Holdings limiTed 23

exeCutive kmP key PeRFORmaNCe meaSuReS FOR tHe 2015 FiNaNCiaL yeaR