TURMOIL IN PAYMENTS - CU TodayTurmoil+in+Payments.pdf · TURMOIL IN PAYMENTS ... “warm handoff”...

34

TURMOIL IN PAYMENTS Keys to Credit Union Success

Transcript of TURMOIL IN PAYMENTS - CU TodayTurmoil+in+Payments.pdf · TURMOIL IN PAYMENTS ... “warm handoff”...

TURMOIL IN PAYMENTS Keys to Credit Union Success

KEY TOPICS

▸ Overview of the payments market landscape and economics

▸ Ecosystem stakeholders–strengths, weaknesses, motivations of each

▸ Consumer priorities–changes in behavior given tech evolution

▸ Key Credit Union considerations for Apple Pay, other digital wallets

▸ Technology scan–key factors to consider, including fraud/security

▸ The path forward–opportunities for Credit Union collaboration

The traditional FI economic model remains under attack

▸ Little sign of interest rate environment returning to the “old normal”

▸ Interchange revenue under downward pressure, especially debit

▸ NSF/Overdraft revenue down more than 40% from 2009 peak

▸ Regulatory burden (and uncertainty) complicates the creation of new revenue streams to replace declining ones

» Consumer expectation of free for new services is another hurdle to overcome

▸ Value is increasingly viewed as residing in the information surrounding the payment, rather than in the payment itself

» Many market entrants show willingness to give away services FIs typically charge for, in pursuit of adjacent value streams

3.0

3.5

4.0

4.5

5.0

20141984 1994 2004

HISTORICAL NET INTEREST MARGINS (%)

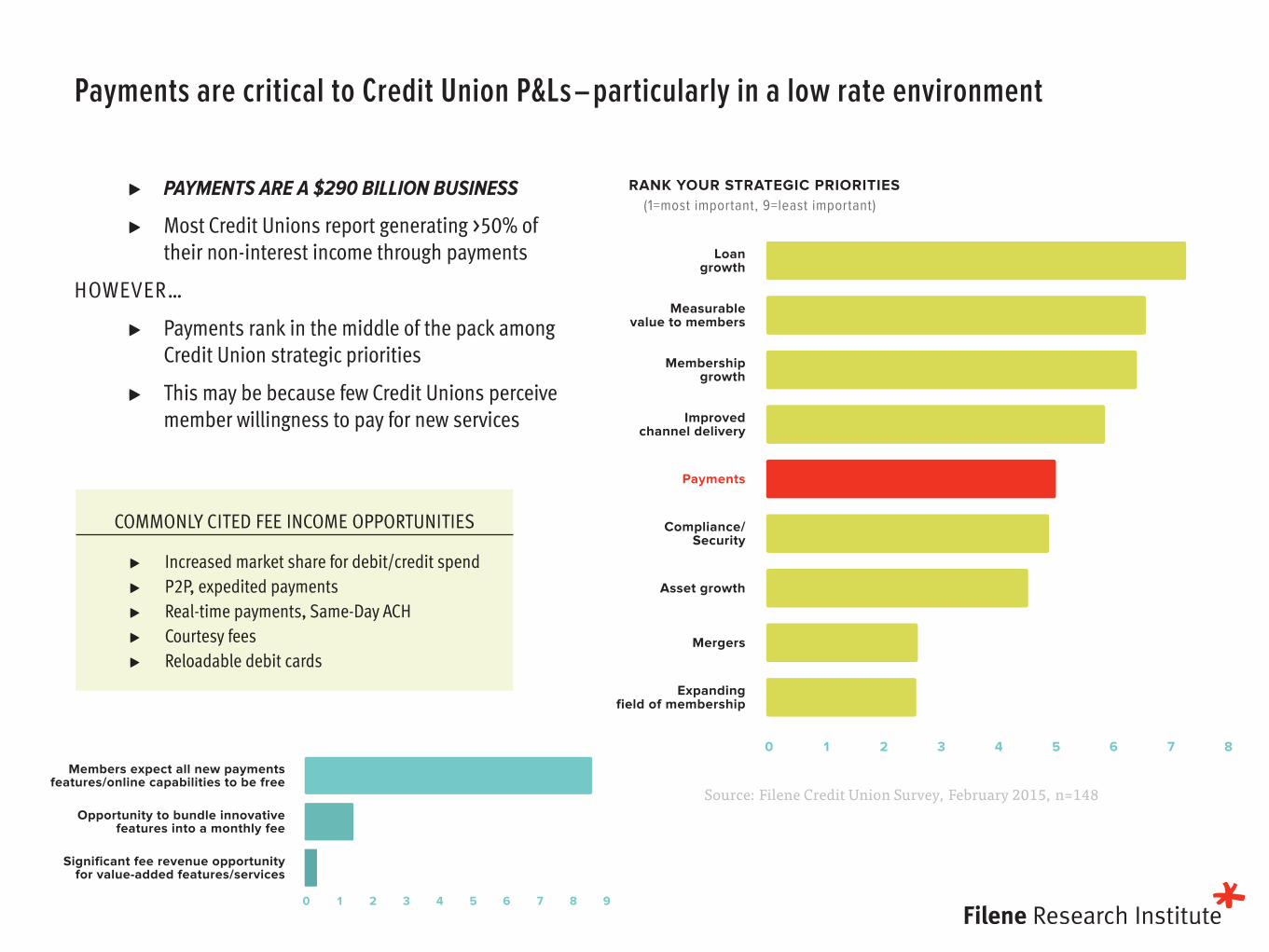

COMMONLY CITED FEE INCOME OPPORTUNITIES

▸ Increased market share for debit/credit spend ▸ P2P, expedited payments ▸ Real-time payments, Same-Day ACH ▸ Courtesy fees ▸ Reloadable debit cards

Payments are critical to Credit Union P&Ls – particularly in a low rate environment

▸ PAYMENTS ARE A $290 BILLION BUSINESS

▸ Most Credit Unions report generating >50% of their non-interest income through payments

HOWEVER…

▸ Payments rank in the middle of the pack among Credit Union strategic priorities

▸ This may be because few Credit Unions perceive member willingness to pay for new services

0 1 2 3 4 5 6 7 8 9

Members expect all new payments features/online capabilities to be free

Opportunity to bundle innovativefeatures into a monthly fee

Significant fee revenue opportunityfor value-added features/services

0 1 2 3 4 5 6 7 8 9

Membershipgrowth

Loangrowth

Improvedchannel delivery

Measurablevalue to members

Compliance/Security

Asset growth

Payments

Expandingfield of membership

Mergers

RANK YOUR STRATEGIC PRIORITIES (1=most important, 9=least important)

Source: Filene Credit Union Survey, February 2015, n=148

Source: Federal Reserve Payments Study

Noncash payments have shifted away from checks to other forms of payment, particularly cards

2003 2006 2009 2012

Checks (paid)

TOTAL

Credit card

Debit card

Prepaid card

ACH

2003–12 2009–12

4.7%

-7.6%

10.9%

3.7%

13.0%

30.7%

18.3

22.1

26.2

47.0

9.2

24.5

19.1

21.0

37.5

5.9

30.5

14.6

21.7

25.0

3.3

37.3

8.8

19.0

15.6

0.8

4.4%81.4 95.2 108.1 122.8

-9.2%

5.1%

7.6%

7.7%

15.8%

NONCASH PAYMENT TRANSACTIONS BY PAYMENT TYPE, BILLIONS CAGR*

*Compound Annual Growth Rate

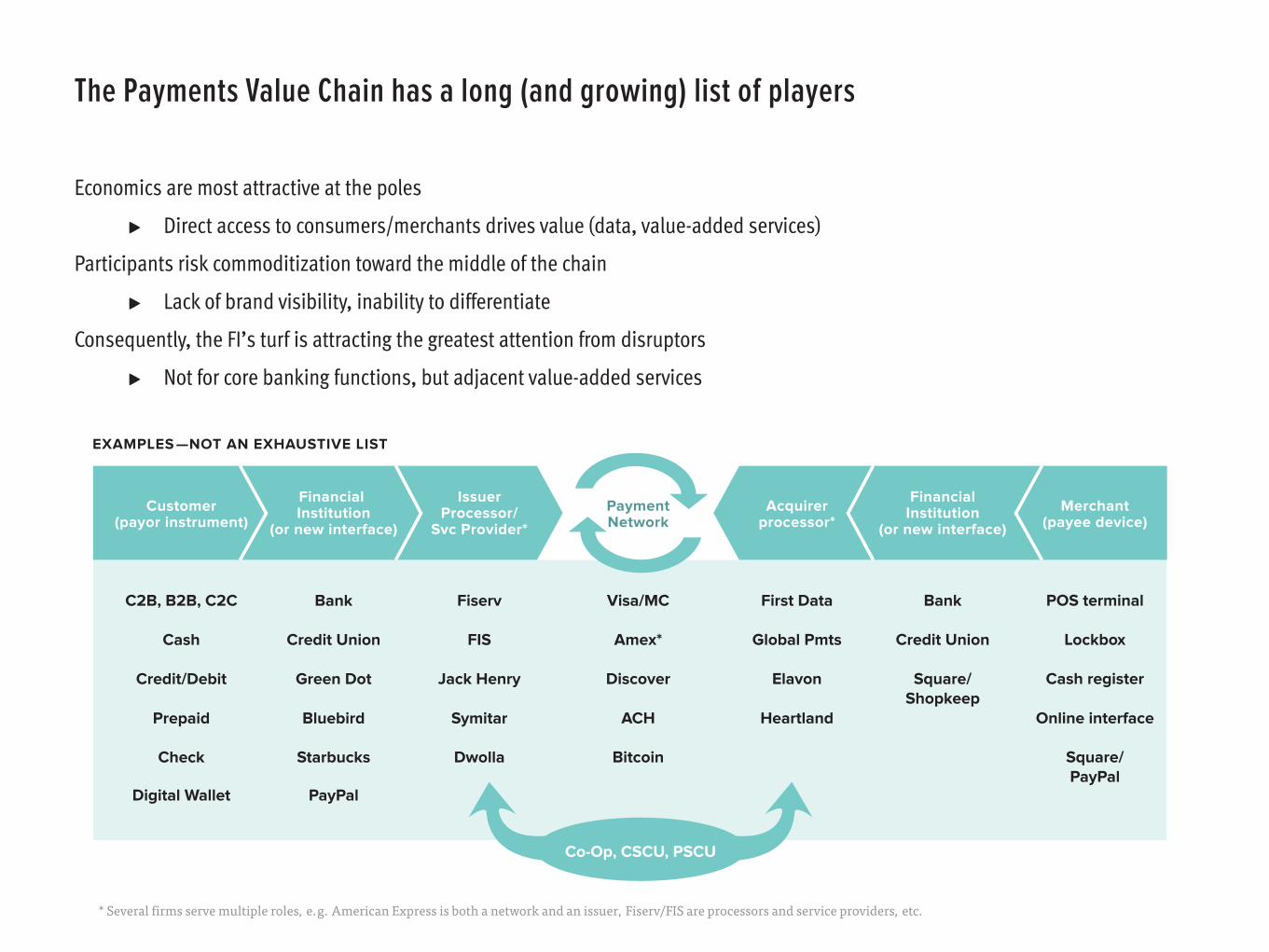

The Payments Value Chain has a long (and growing) list of players

Economics are most attractive at the poles

▸ Direct access to consumers/merchants drives value (data, value-added services)

Participants risk commoditization toward the middle of the chain

▸ Lack of brand visibility, inability to differentiate

Consequently, the FI’s turf is attracting the greatest attention from disruptors

▸ Not for core banking functions, but adjacent value-added services

Customer(payor instrument)

Financial Institution

(or new interface)

IssuerProcessor/

Svc Provider*

PaymentNetwork

Acquirerprocessor*

FinancialInstitution

(or new interface)

Merchant(payee device)

C2B, B2B, C2C

Cash

Credit/Debit

Prepaid

Check

Digital Wallet

Bank

Credit Union

Green Dot

Bluebird

Starbucks

PayPal

Fiserv

FIS

Jack Henry

Symitar

Dwolla

Visa/MC

Amex*

Discover

ACH

Bitcoin

First Data

Global Pmts

Elavon

Heartland

Bank

Credit Union

Square/Shopkeep

POS terminal

Lockbox

Cash register

Online interface

Square/PayPal

* Several firms serve multiple roles, e.g. American Express is both a network and an issuer, Fiserv/FIS are processors and service providers, etc.

Co-Op, CSCU, PSCU

EXAMPLES —NOT AN EXHAUSTIVE LIST

Each participant in the ecosystem has unique motivations, strengths and weaknesses

WEAKNESSES

STRENGTHS

DRIVERS

Consumer Financial Institution

IssuerProcessor/

Svc Provider

PaymentNetwork

Acquirerprocessor Disruptors Merchant/

Retailer

Source: Filene Credit Union Survey, February 2015, n=148

Views vary on which group wields the greatest ecosystem power… but it’s not the FIs

▸ Consensus that power is shifting from networks to retailers

▸ Executive interviews placed consumers and retailers in the top positions

▸ Virtually no respondents believe FIs hold a strong position in the power dynamic

» “Whoever has the customer’s ear holds the power”

» “Visa held all the cards until Apple made it clear where the power really resides”

▸ However, networks realize only a small share of overall payments revenue

0 1 2 3 4 5

Consumers

Retailers

FinancialInstitutions

New marketentrants

Credit Unionservice providers

PaymentsNetworks

0 25 50 75 100

75%InstrumentIssuer

17%TransactionAcquirer

8%Network/Processor

WHO DO YOU BELIEVE HOLDS THE MOST POWER IN THE PAYMENTS ECOSYSTEM?

ESTIMATED REVENUE SHARE

1=most powerful, 6=least powerful

Source: Accenture Payment Study

Current dominant payment forms are slated to decline, with most of the shift coming from cash.

+3%

6%

9%

+2%

6%

8%

+1%

7%

8%

+10%

8%

18%

+2%

11%

13%

+7%

14%

21%

0%

17%

17%

-3%

52%

55%

-6%

53%

59%

-12%

54%

66%

Future

Future

Today

Today

Ranked by Instrument Usage Levels Today

At least daily + At least weekly

Popmoney®/ClearXchange

WireTransfer/Western

Union

MoneyOrder/

CertifiedCheck

DigitalCurrency

Prepaid/Gift Card

PayPal Check CreditCard

DebitCard

Cash

THE USE OF PAYMENT INSTRUMENTS IS DIFFERENT TODAY THAN IT WILL BE IN 2020

Q: How often do you use the following payment instruments to complete a transaction? Q: How frequently do you anticipate you will use the following payment instruments to

complete a transaction by 2020?

Source: Accenture (2014)

The trend toward consumer unbundling is unlikely to abate

▸ As consumers unbundle their financial services, the threat of bank disintermediation multiplies

» This is particularly true for the under 35 segment, whose formative financial experiences are less likely to be with a financial institution

▸ Numerous success stories, mostly with Gen X adoption

» PayPal, Amex Bluebird, Venmo, LendingClub, Credit Karma

▸ How can Credit Unions collaborate/co-exist in such an environment?

» Don’t fight irresistible forces, determine where partnering makes sense

HOW LIKELY WOULD YOU BE TO BANK WITH A NON-FINANCIAL INSTITUTION?

PERCENTAGE OF RESPONDENTS WHO WOULD BE LIKELY TO BANK WITH AT LEAST ONE NON- FINANCIAL SERVICES COMPANY

0 25 50 75 100

27%

72%

Boomers (55+) Millenials (18–34)0 25 50 75 100

28%

58%

77%

18–34 yr olds 35–54 yr olds 55+ yr olds

Source: American Bankers Association

The regulatory landscape continues to evolve—creating new complexities

WHAT’S CHANGED?

▸ OCC Guidance on Third Parties

▸ Federal Reserve guidance on Third Parties

▸ New focus on Operational Risk Management

▸ CFPB focus on DDA fee structures & overdraft

▸ Mortgage Lending Reform & Basel III for banks

▸ Dodd Frank Act pace accelerated through 2014

▸ Consumer Protection + Surveillance + Aggressive Regulators = Increased oversight

▸ Governance, Risk & Compliance focus areas are affecting all size organizations.

▸ Examination oversight and market reaction are creating risk of broader change than specific regulations themselves

DFA-RELATEDREGULATORYPROPOSAL PAGES

DFA-RELATEDFINAL REGS &

GUIDANCE PAGES

6,304 8,231

as of January 6, 2015

and counting

REDUCED FI BANDWIDTH TO ADDRESS CRITICAL BUSINESS NEEDS (E.G. INNOVATION)

THEREFORE

The mixed blessing of the “Branch of the Future”

▸ 62% of respondents of Filene survey report seeing declines, 52% report changes in the nature of that traffic

▸ Opportunity for cost saving

▸ All demographic segments still coming to branch, only for different reasons than before

▸ HOWEVER we have yet to identify an effective substitute for the “warm handoff” of a qualified lead

REMOTE MODELS MUST DEMONSTRATE THE ABILITY TO IDENTIFY AND CONVERT “MOMENTS OF TRUTH”THEREFORE

Source: McKinsey Consumer Financial Life Survey

0%

20%

2009 2010 2011 2012 2013 2014

40%

60%

80%

Withdraw cash at ATM

Use online banking

Use branch monthly

Deposit checks at ATM

Ever use mobile banking

Remote check deposit

-1%

+2%

-4%

-2%

+3%

+2%

ADOPTION OF CHANNEL USES, % OF BANKED HOUSEHOLDS

ANNUAL GROWTH 2011—2014

Source: McKinsey Consumer Financial Life Survey, 2014

Two thirds of US consumers' payment preferences align with digital wallet capabilities

▸ Many consumers are loyal to one method; others use a variety depending on the circumstance

DEBIT CARD USERS28% of U.S. households27 POS transactions/month

22% of U.S. households24 POS transactions/month

19% of U.S. households28 POS transactions/month

11% of U.S. households34 POS transactions/month

10% of U.S. households35 POS transactions/month

4% of U.S. households20 POS transactions/month

4% of U.S. households21 POS transactions/month

2% of U.S. households27 POS transactions/month

CASH USERS CREDIT CARD USERS CREDIT & CASH USERS

DEBIT & CASH USERS

DEBIT CASH CREDIT CHECK PREPAID DEBIT EBT CARD PAYPAL OTHER

CHECK WRITERS EBT & CASH USERS PREPAID DEBIT CARD USERS

83

74

4 3

79

10

53 3

58

18

12

75

4536

11

5 3

4924

10

106

87

64 3

14

56

16

74 3

14

4524

8

6 4

POS PAYMENT BEHAVIORAL CLUSTERS

% of POS payments made using each method1

1 “Debit” does not include “Prepaid debit”

A successful digital wallet will bring a seamless, elegant interface to a complex tangle of sub-systems

Participants’ mobile expectations at the 2013 Filene Colloquium proved optimistic, but 2015 respondents remain bullish about mobile’s prospects

Respondents still foresee “A Thousand Flowers Blooming” scenario

▸ Adopt solutions tailored to member needs

▸ Use new channels to enhance trusted partner role

▸ Small merchants could be a logical Credit Union niche

▸ How to get Credit Unions to rally around a small set of solutions?

▸ Need full integration to cement value proposition

Some regression to the midpoint, especially on open vs. closed systems

▸ “Walled Garden” scenario places a premium on Credit Union collaboration

▸ Would also make a Credit Union- specific solution challenging

WALLED GARDENS

FORTIFIED OUTPOST NO ONE COMES TO THE PARTY

fast/high

slow/low

open/diverseclosed/consolidated

# OF WINNERS & LEVEL OF OPENNESS

SPEED OF ADOPTION &DEPTH OF PENETRATION

A THOUSAND FLOWERS BLOOMING

Apple pay: hype vs. reality

▸ First, kudos to Apple Pay’s MANY breakthroughs

» Single-handedly revived NFC

» Fraud approach may be the hidden breakthrough

» Broke the Google Wallet/MCX/Softcard logjam

» Did not attempt to re-invent the payment rails

» Remarkable success on awareness, FI/merchant participation

▸ However, jury still out on consumer adoption

» 85% of iPhone 6 owners have not yet tried/loaded

» 2/3 of consumers express no interest in cellphone payments

» Highly favorable marks among small base

▸ Cook: “Still first inning,” “start of roadmap”

▸ Lack of loyalty component is critical (see above point)

▸ iOS market share still only ~40%

▸ Friend or foe to Banks/Credit Unions?

» Interchange door now cracked open?

» Don’t fight forces of nature?

» Top of wallet implications!Source: comScore MobiLens

TOP SMARTPHONE PLATFORMS

*Total U.S. smartphone subscribers Age 13+

ANDROID 52.0 0.6 52.6APPLE 42.0 -0.2 41.8

MICROSOFT 3.5 -0.1 3.4BLACKBERRY 2.3 -0.3 2.0

SYMBIAN 0.1 0.0 0.1SHARE %AUG.2014

SHARE %NOV.2014

POINTCHANGE

“Acceptable risk given likely

share of overall transactions”

“Better than getting a higher

percentage of nothing”

“I realize we’re sleeping with

the enemy”“I trust Apple

...for now”

Source: McKinsey Consumer Financial Life Survey

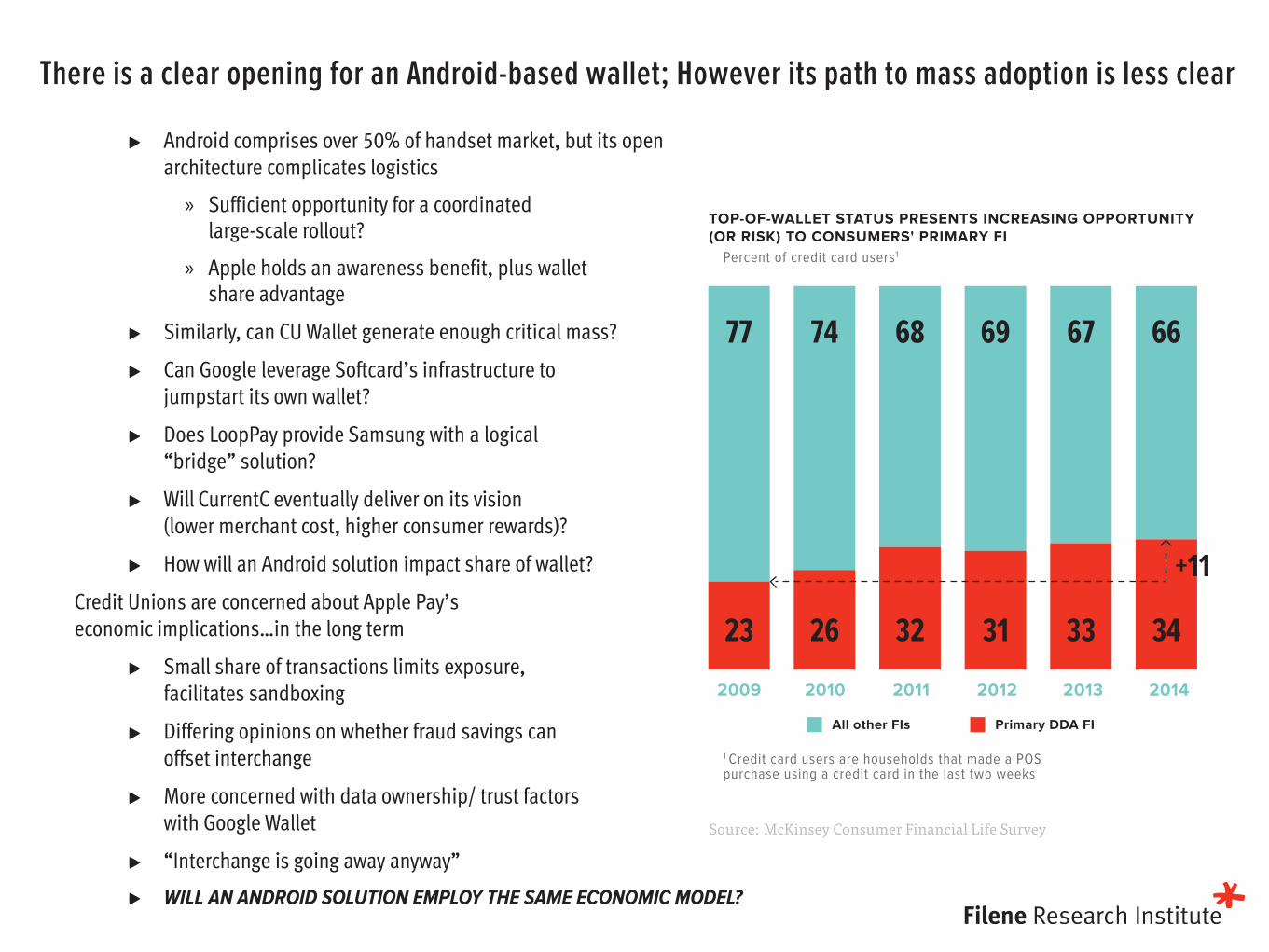

▸ Android comprises over 50% of handset market, but its open architecture complicates logistics

» Sufficient opportunity for a coordinated large-scale rollout?

» Apple holds an awareness benefit, plus wallet share advantage

▸ Similarly, can CU Wallet generate enough critical mass?

▸ Can Google leverage Softcard’s infrastructure to jumpstart its own wallet?

▸ Does LoopPay provide Samsung with a logical “bridge” solution?

▸ Will CurrentC eventually deliver on its vision (lower merchant cost, higher consumer rewards)?

▸ How will an Android solution impact share of wallet?

Credit Unions are concerned about Apple Pay’s economic implications…in the long term

▸ Small share of transactions limits exposure, facilitates sandboxing

▸ Differing opinions on whether fraud savings can offset interchange

▸ More concerned with data ownership/ trust factors with Google Wallet

▸ “Interchange is going away anyway”

▸ WILL AN ANDROID SOLUTION EMPLOY THE SAME ECONOMIC MODEL?

There is a clear opening for an Android-based wallet; However its path to mass adoption is less clear

All other FIs Primary DDA FI

77 74 68 69 67 66

23 26 32 31 33 34

+11

2009 2010 2011 2012 2013 2014

TOP-OF-WALLET STATUS PRESENTS INCREASING OPPORTUNITY (OR RISK) TO CONSUMERS' PRIMARY FI

Percent of credit card users1

1 Credit card users are households that made a POS purchase using a credit card in the last two weeks

Source: Accenture (2014); n=4,000

Consumers lack consensus on a logical mobile payments provider; FIs fare better than Telcos, but not as well as PayPal or the card networks

CONSUMERS PREFER NETWORK CARD PROVIDERS AS THEIR MOBILE PAYMENT PROVIDERS—FOR NOW.*

Q: Which of the following types of companies would you prefer to use as a mobile payments provider?

* Preference levels shown are not indicative of the companies listed as examples.

Network Providers

Emerging PaymentProviders

Established Retail Bank

Larger TechCompanies

Large Merchant/Retailer

Large TelcoProvider

Tech Start-Ups

Network Providers

Emerging PaymentProviders

Established Retail Bank

Larger TechCompanies

Large Merchant/Retailer

Large TelcoProvider

Tech Start-Ups

% OF ALL RESPONDENTS BY AGE % OF ALL RESPONDENTS BY INCOME LEVEL

55+ 35–54 18–34 $150,000+ $50,000–$149,999

<$49,999

61

7376

44

66

76

44

6264

36

5767

3652

59

3248

56

1234

50

81

7664

74

68

61

72

6450

69

6050

6254

47

60

5239

5140

29

Tech Start-Upsi.e., Square 36%

Large TelcoProvider

i.e., U.S.–Verizon, AT&T,Sprint Canada–TELUS, Rogers & Bell

48%

Large Merchant/Retailer

i.e., BestBuy, Walmart, Target52%

Larger TechCompanies

i.e., Apple, Google, Amazon 57%

EstablishedRetail Bank

i.e., JP Morgan, USBancorp,TD & RBC

59%

Emerging PaymentProviders

i.e., PayPal66%

NetworkProviders

i.e., Visa, MasterCard, & Amex 72%

Sources: Seventh Annual Billing Household Survey, Fiserv, Inc., 2014; 2013 Fiserv Consumer Trends Survey

A successful wallet will appeal to a broad cross-section of consumerbehaviors—and/or create sufficient incentive to change behavior

TODAY’S CONSUMERS ARE BILL PAY OMNIVORES

VIEWING ACCOUNT INFORMATION, PAYING BILLS AND TRANSFERRING FUNDS TOP ONLINE BANKING ACTIVITIES

Number of bill payment methods consumers use monthly as a percent of all U.S. households.

Online banking users: Please indicate which of the following features of online banking you used last month.

17%

23%

23%

18%

9%

5%

5%

ONE

TWO

THREE

FOUR

FIVE

SIX

SEVEN

63%View real-timeaccount information

52%Use online bill pay

52%Transfer funds betweenmy accounts (same bank)

48%View monthly statement

28%View cleared checks

28%Alerts regardingaccount activity

21%Transfer funds between myaccounts (different banks)

18%Receive electronic bills

16%Online customer service(e.g., to order checks)

Sources: Bain Online Survey 2013; Bain/Research Now Retail Banking NPS Survey, July 2012 (n=~10,000)

Purchasing power and demographic metrics make a strong argument for a mobile strategy

0yrs

10yrs

20yrs

30yrs

40yrs

50yrs 3.0

1.3

2.1

1.4

2.4

1.41.5

1.21.3 1.3

1.6

2.0

1.0

0.0$0K

$20K

$40K

$60K

$80K

US UK Germany

Those interested in mobile payments are getting younger... ...generally more affluent...

Payment method of total in-store spending per month

...and spend twice as much in retail.

France

Users UserWilling WillingUnwilling

Spain US UK Germany France Spain US UK Germany France Spain

Average age of survey respondents by mobile proximity payments usage

Average income of survey respondents bymobile proximity payments usage ($US)

Ratio of spending compared with nonusersunwilling to try mobile payments

US

Average Mobilepayment

users

UK

Mobilepayment

users

Average

Germany

Mobilepayment

users

Average

France

Mobilepayment

users

Average

Spain

Mobilepayment

users

Average

CASH OTHERDEBIT CARD CREDIT CARD MOBILE PHONE AS REPLACEMENT FOR PAYMENTPREPAID VOUCHER

0

20

40

60

80

100

CONSUMERS WHO USE MOBILE PAYMENT TEND TO BE YOUNGER, MORE AFFLUENT AND MORE LIKELY TO SPEND MORE ON RETAIL

NOTE: Data pre-dates Apple Pay launch

Source: Bain Online Survey 2013

However, international use case data indicates mobile wallets may initially be a defensive play more than a revenue opportunity

Payment method of total in-store spending per month

US

Average Mobilepayment

users

UK

Mobilepayment

users

Average

Germany

Mobilepayment

users

Average

France

Mobilepayment

users

Average

Spain

Mobilepayment

users

Average

CASH OTHERDEBIT CARD CREDIT CARD MOBILE PHONE AS REPLACEMENT FOR PAYMENTPREPAID VOUCHER

0

20

40

60

80

100

EARLY USE OF MOBILE PAYMENTS SUGGESTS CONSUMERS USE THEM MORE LIKE CREDIT CARDS THAN CASH

Percentage of monthly spending

APPLE PAY GOOGLE WALLET SAMSUNG PAY CU WALLET CURRENTC (MCX)

UBIQUITY awareness

Apple approach

(member) driven

HANDSETS devices capable smartphones like enrollment trigger

smartphones

smartphones

MERCHANTS

POS presence at any card POS

provide near ubiquity merchant base

PROCESS authentication

newer terminals

POS terminals

“tech agnostic” “tech agnostic”

ECONOMICS of interchange

plans to monetize thru data access

Samsung will receive share of interchange

quo likely

merchant interchange savings (steering)

in flux

SECURITYadvancement

enrollment fraud

Pay (tokenization?)

data

Apple Pay

approach?

REWARDS existing programs

to make a key feature

merchant level

DATA OWNERSHIP

existing models

on Google’s access to data share for revenue split

The rapidly evolving Digital Wallet landscape...

Paydiant Backbone

>75% of respondent Credit Unions plan to have Apple Pay live in 2015.

Nearly half will offer a digital wallet by 2015.

▸ Focus is on security, seamless user experience

▸ Little traction for loyalty, coupons

» Yet MCX is deemed an “awake at night” threat; inconsistency?

Example of the“hype cycle”: in a February Technology Association of Georgia poll of industry experts, over 60% believe Apple Pay will capture 5% of POS transactions within 12 months

▸ This would match the POS share of Amex or Discover!!

Digital wallet rollouts are focusing on “bread and butter” features

0 1 2 3 4 5

Debit & CreditCard Availability

Easy selection ofmultiple card options

Best of breedsecurity

Ubiquitousacceptance

Seamless,single-step use

Loyaltyprograms

Coupons/targeted offers

WHAT ARE THE MOST IMPORTANT FEATURES FOR A DIGITAL WALLET?

1 = most important, 7 = least importantCurrentlyin market

22% 15%

Rolling outin 2015

55% 31%

Interested, butnot 2015

20% 45%

No plansto offer

3% 8%

APPLEPAY

DIGITALWALLET

Source: Filene Credit Union Survey, February 2015, n=148

Source: Accenture (2014); n=1,577

Rewards have lagged behind on the wallet roadmap, but may be the key to consumer adoption

CONSUMERS ARE INTERESTED IN INCENTIVES TO USE MOBILE PAYMENTS

Q: Would you increase the amount you use your phone to make a payment if the following services were offered?

(% of respondents who chose definitely increase or may increase usage)

You are offered discount pricing/coupons basedon past usage of your phone as a payment device

Upon purchase, your payment device receives andstores all receiptsin a secure database and

seamlessly tracks spending habits

You have the ability to scan a product and are provided theoption to purchase immediately through your payment

device, eliminating the requirement for checkout

You receive a special offer of rewards pointswith your reward card stored on the phone

You receive valued customer treatment,such as a separate line to speed payment

You are able to pay for public transportationand receive reward points towards a free use

You receive notifications for upcomingevents and/or product releases at the store

You are able to scan a product and are presentedinformation about the product (consumer reviews,

comparable products, retailer price comparison)

79%

77%

71%

69%

67%

66%

66%

61%

Source: Bain Online Survey 2013 (n=562 US consumers who are unwilling to try mobile payments)

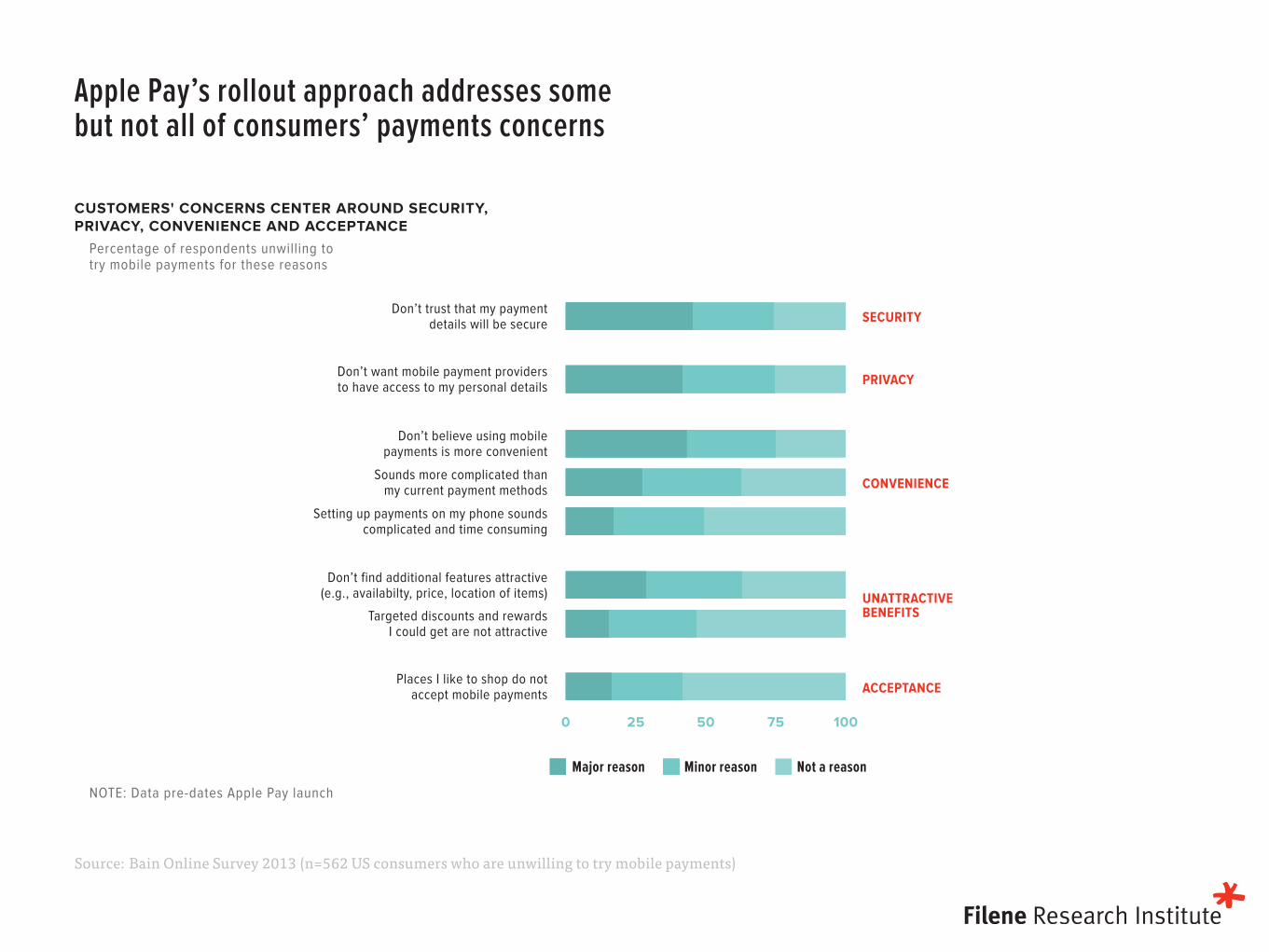

Apple Pay’s rollout approach addresses some but not all of consumers’ payments concerns

NOTE: Data pre-dates Apple Pay launch

SECURITY

PRIVACY

CONVENIENCE

UNATTRACTIVEBENEFITS

ACCEPTANCE

Don’t trust that my paymentdetails will be secure

Don’t want mobile payment providersto have access to my personal details

Don’t believe using mobilepayments is more convenient

Sounds more complicated thanmy current payment methods

Setting up payments on my phone soundscomplicated and time consuming

Don’t find additional features attractive(e.g., availabilty, price, location of items)

Targeted discounts and rewardsI could get are not attractive

Places I like to shop do notaccept mobile payments

Major reason Minor reason Not a reason

0 25 50 75 100

CUSTOMERS' CONCERNS CENTER AROUND SECURITY, PRIVACY, CONVENIENCE AND ACCEPTANCE

Percentage of respondents unwilling to try mobile payments for these reasons

Source: Federal Reserve Payments Study

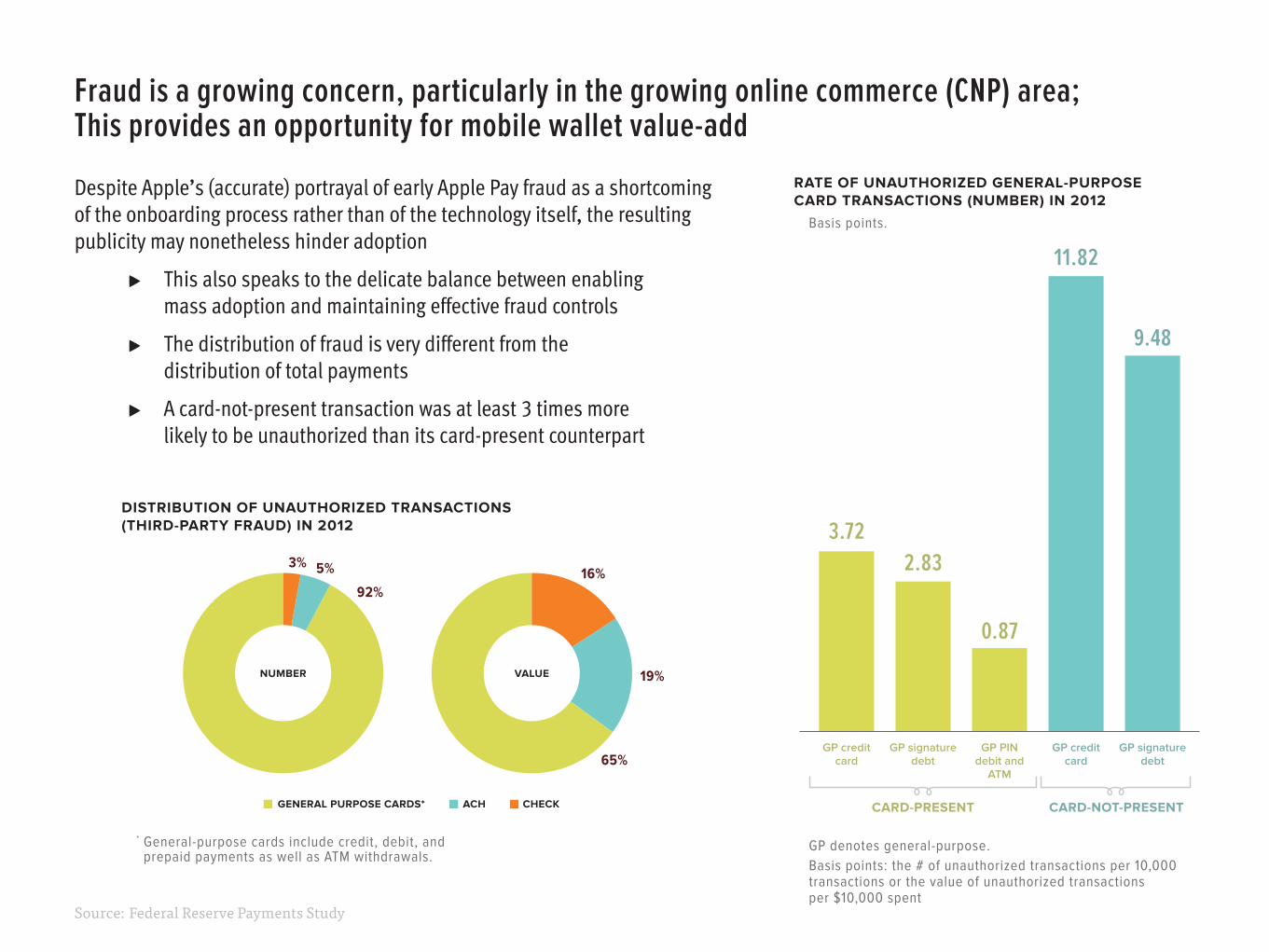

Fraud is a growing concern, particularly in the growing online commerce (CNP) area; This provides an opportunity for mobile wallet value-add

Despite Apple’s (accurate) portrayal of early Apple Pay fraud as a shortcoming of the onboarding process rather than of the technology itself, the resulting publicity may nonetheless hinder adoption

▸ This also speaks to the delicate balance between enabling mass adoption and maintaining effective fraud controls

▸ The distribution of fraud is very different from the distribution of total payments

▸ A card-not-present transaction was at least 3 times more likely to be unauthorized than its card-present counterpart

GENERAL PURPOSE CARDS* ACH CHECK

5% 3%

92%

19%

16%

65%

NUMBER VALUE

DISTRIBUTION OF UNAUTHORIZED TRANSACTIONS (THIRD-PARTY FRAUD) IN 2012

* General-purpose cards include credit, debit, and prepaid payments as well as ATM withdrawals.

3.722.83

0.87

11.82

9.48

GP creditcard

GP signaturedebt

GP PINdebit and

ATM

GP creditcard

GP signaturedebt

CARD-PRESENT CARD-NOT-PRESENT

RATE OF UNAUTHORIZED GENERAL-PURPOSE CARD TRANSACTIONS (NUMBER) IN 2012

Basis points.

GP denotes general-purpose. Basis points: the # of unauthorized transactions per 10,000 transactions or the value of unauthorized transactions per $10,000 spent

Technology Review

TOKENIZATION

Apple Pay’s “hidden gem”; foreshadows a future

without plastic?

OPEN/CLOSED SYSTEMS (E.G. IOS VS. ANDROID)

Inherent tradeoffs re: innovation, adoption, control, security

IN-APP PURCHASES

Logical workflow enhancement for mobile wallets; simplifies

shopping experience

BEACON TECHNOLOGY (AUTO-CHECKOUT)

The logical extension of NFC? Still further in future, but holds potential to greatly improve the

shopping experience

FASTER PAYMENTS/SAME-DAY ACH

Separate initiatives from Fed, The Clearing House; business

case remains challenging

CRYPTOCURRENCY

Bitcoin and potential successors; sound concept facing regulatory

and business case hurdles

EMV (EURO MASTERCARD VISA)

a/k/a “Chip and PIN”; a major (card present) security advancement,

but requires significant capital investment/training regimen

NFC (NEAR FIELD COMMUNICATION)

Replaces swipe with tap; appeared to be near

extinction pre-Apple Pay

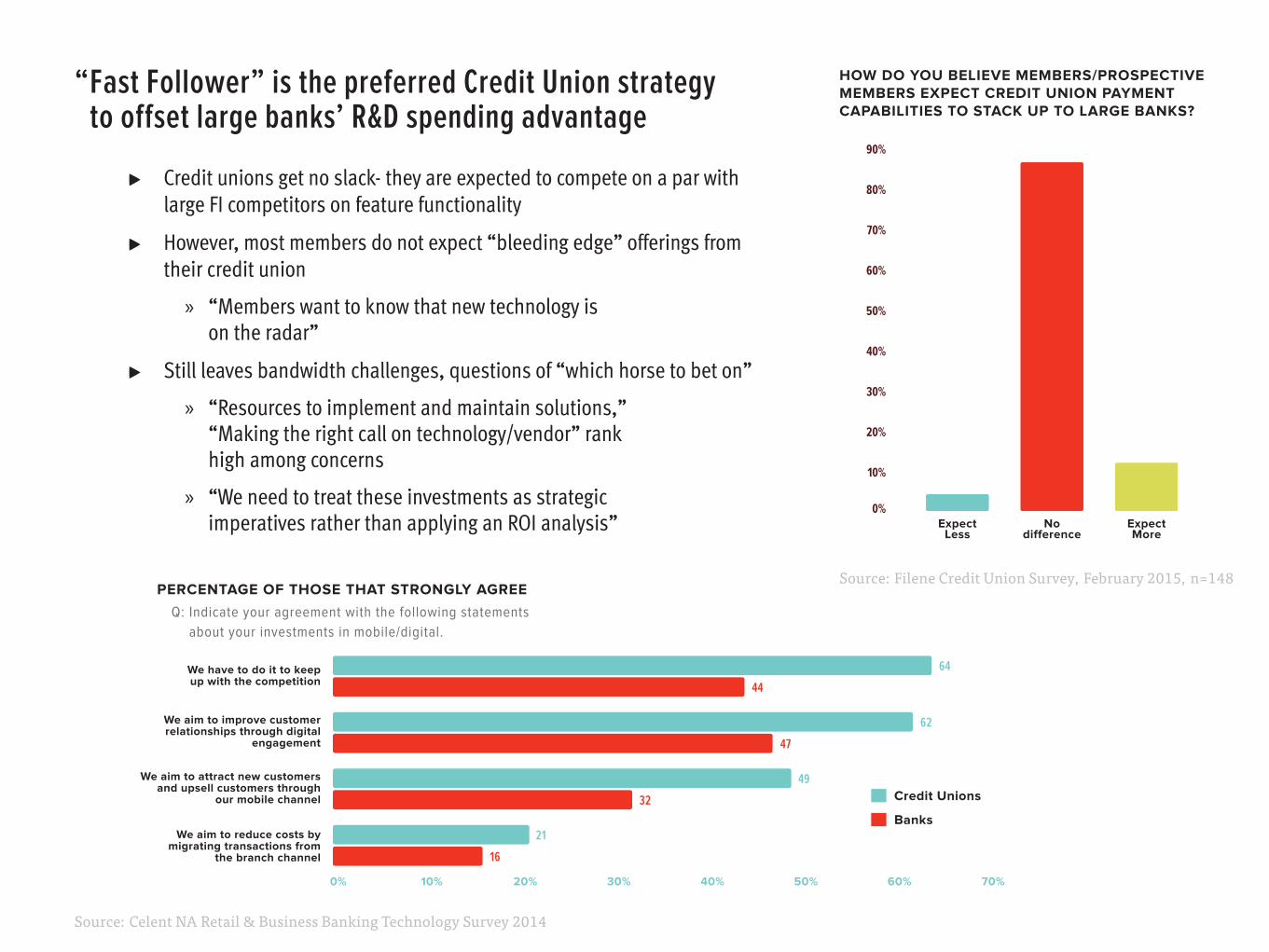

“ Fast Follower” is the preferred Credit Union strategy to offset large banks’ R&D spending advantage

▸ Credit unions get no slack- they are expected to compete on a par with large FI competitors on feature functionality

▸ However, most members do not expect “bleeding edge” offerings from their credit union

» “Members want to know that new technology is on the radar”

▸ Still leaves bandwidth challenges, questions of “which horse to bet on”

» “Resources to implement and maintain solutions,” “Making the right call on technology/vendor” rank high among concerns

» “We need to treat these investments as strategic imperatives rather than applying an ROI analysis”

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

ExpectLess

Nodifference

ExpectMore

HOW DO YOU BELIEVE MEMBERS/PROSPECTIVE MEMBERS EXPECT CREDIT UNION PAYMENT CAPABILITIES TO STACK UP TO LARGE BANKS?

Source: Filene Credit Union Survey, February 2015, n=148PERCENTAGE OF THOSE THAT STRONGLY AGREE

Q: Indicate your agreement with the following statements about your investments in mobile/digital.

0% 10% 20% 30% 40% 50% 60% 70%

We have to do it to keepup with the competition

We aim to improve customer relationships through digital

engagement

We aim to attract new customers and upsell customers through

our mobile channel

We aim to reduce costs bymigrating transactions from

the branch channel

64

62

44

47

49

32

21

16

Credit Unions

Banks

Source: Celent NA Retail & Business Banking Technology Survey 2014

▸ Unregulated disruptors

» “A workaround that cuts the FI out of the consumer equation”

▸ A data breach, especially if responsibility can be traced back to a Credit Union

» Major merchant disruption

» “Blame the messenger” aspect even if a breach isn’t Credit Union’s fault

▸ Continuing downward pressure on interchange

» “Plan for interchange to be gone in 5-10 years”

» “Retailers increasingly calling the shots” (MCX concern)

▸ Losing a deep understanding of members

» Have expanded fields of membership contributed to this risk?

▸ Striking a balance across security/convenience/privacy in products

Data breaches head the list of greatest Credit Union fears, but they have company

Fraud/data breaches

Loss of interchange

Disintermediation

Disruptors/ongoing new entrants

Retailers’ growing power (MCX)

Resources to implement/maintain soln's

Making right call on technology/vendor

Top of wallet status

44

17

13

10

8

763

TOP CONCERNS (#MENTIONS)

10010010101001001010001101100101110011010011011011101101101111001010011

10010010101001001010001101100101110011010011011011101101101111001010011

Source: Filene Credit Union Survey, February 2015, n=148

“COLLABORATION IS A NECESSITY—WE SIMPLY DON’T HAVE THE R&D FUNDS TO COMPETE WITH THE LARGE BANKS OTHERWISE”

THEREFORE

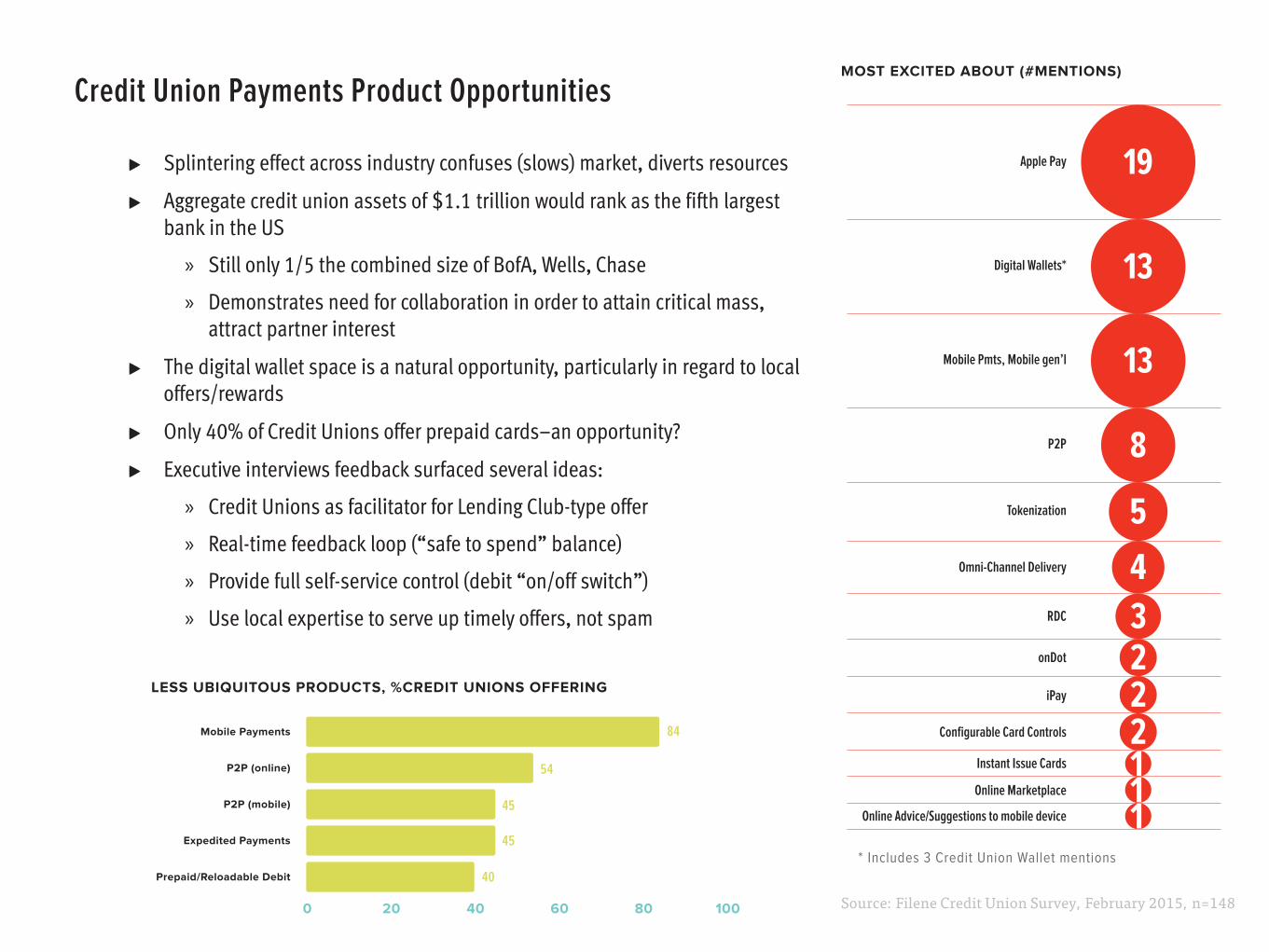

▸ Splintering effect across industry confuses (slows) market, diverts resources

▸ Aggregate credit union assets of $1.1 trillion would rank as the fifth largest bank in the US

» Still only 1/5 the combined size of BofA, Wells, Chase

» Demonstrates need for collaboration in order to attain critical mass, attract partner interest

▸ The digital wallet space is a natural opportunity, particularly in regard to local offers/rewards

▸ Only 40% of Credit Unions offer prepaid cards–an opportunity?

▸ Executive interviews feedback surfaced several ideas:

» Credit Unions as facilitator for Lending Club-type offer

» Real-time feedback loop (“safe to spend” balance)

» Provide full self-service control (debit “on/off switch”)

» Use local expertise to serve up timely offers, not spam

Credit Union Payments Product Opportunities

Apple Pay

Digital Wallets*

Mobile Pmts, Mobile gen’l

P2P

Tokenization

Omni-Channel Delivery

RDC

onDot

iPay

Configurable Card Controls

Instant Issue Cards

Online Marketplace

Online Advice/Suggestions to mobile device

19

13

13

8

5

43222111

MOST EXCITED ABOUT (#MENTIONS)

LESS UBIQUITOUS PRODUCTS, %CREDIT UNIONS OFFERING

* Includes 3 Credit Union Wallet mentions

0 20 40 60 80 100

Mobile Payments

P2P (online)

P2P (mobile)

Expedited Payments

Prepaid/Reloadable Debit

84

54

45

45

40

Source: Filene Credit Union Survey, February 2015, n=148

An agnostic, “wait for the winners to emerge” approach will likely leave credit unions behind the curve.

Potential scenarios for Credit Union advocacy to define the market and shape ongoing role:

1) Credit Union–specific prepaid/reloadable debit proposition

Pros: Promising source of fee income; rounds out product portfolio; reinforces financial responsibility message; potentially attracts new members

Cons: Sufficient basis for collaborative action? Need to differentiate vs. existing providers

2) Credit Union–specific wallet solution

Pros: Leverage community ties, reinforce “Shop Local” messaging; consider bundling with financial responsibility messaging

Cons: Limited scale to attract major merchants; Lacks handset “pull” of competing wallet propositions; Who manages local merchant outreach?

3) Clearinghouse for direct lending

Pros: Large potential market; addresses incursion by new market entrants; source of new members; can position as a more consumer-friendly solution

Cons: Significant operational undertaking; potential regulatory hurdles; need to develop equitable business model across Credit Unions

Credit Union Collaboration – Hypothetical Scenarios ???

In addition to considering opportunities for collaboration, each credit union should individually assess the following:

▸ Preparedness for a dramatic drop in interchange revenue within 5 years

▸ Avenues for individual member engagement in an era of limited branch visits (identify new cross-sell triggers)

▸ Beliefs on Apple Pay adoption curve, and implications (good and bad) for Credit Union P&L

▸ Adequacy of “fast follower” as a technology strategy, and means of execution (e.g. partnership, level of R&D spending)

▸ Approach to Android market

▸ Approach to rewards/loyalty programs

▸ Segmentation strategy, e.g. “follow the money” vs. “cultivate the next generation of members” (hopefully both!)

Recommendations for individual Credit Unions !!!

About the Author

▸ Co-Lead of McKinsey & Company’s Global Concepts payments unit 2006–2013

» Firm’s subject matter expert on electronic banking, bill payment and e-billing

» Created McKinsey’s Global Payments Map, US Personal Financial Services profit pool

▸ Various senior operating and financial roles at CheckFree 1996–2005 (prior to Fiserv acquisition)

» Negotiated partnerships, integrated acquisitions

» Electronic Commerce Division CFO

» GM of Payment Solutions business

» Investor Relations, Strategic Planning

▸ Led consumer and business check programs at Deluxe Corporation 2013–2014

» Launched e-check initiative through 5,500 FI client base

» Led M&A for diversification in Payments space

▸ 1984–86: Examiner, Federal Reserve Bank of Chicago

▸ 1986–88: Founding Director/Startup Team, University of Pennsylvania Students Federal Credit Union

▸ 2009–present: Board member, Technology Association of Georgia’s FinTech Society

Glen SarvadyFounder and Principal,

154 Advisors

About Filene

Filene Research Institute is an independent, consumer finance think and do tank. We are dedicated to scientific and thoughtful analysis about issues affecting the future of credit unions, retail banking, and cooperative finance.

Deeply embedded in the credit union tradition is an ongoing search for better ways to understand and serve credit union members. Open inquiry, the free flow of ideas, and debate are essential parts of the true democratic process. Since 1989, through Filene, leading scholars and thinkers have analyzed managerial problems, public policy questions, and consumer needs for the benefit of the credit union system. We support research, innovation, and impact that enhance the well-being of consumers and assist credit unions and other financial cooperatives in adapting to rapidly changing economic, legal, and social environments.

We’re governed by an administrative board made up of credit union CEOs, the CEOs of CUNA & Affiliates and CUNA Mutual Group, and the chairman of the American Association of Credit Union Leagues (AACUL). Our research priorities are determined by a national Research Council comprised of credit union CEOs and the president/CEO of the Credit Union Executives Society.

We live by the famous words of our namesake, credit union and retail pioneer Edward A. Filene: “Progress is the constant replacing of the best there is with something still better.” Together, Filene and our thousands of supporters seek progress for credit unions by challenging the status quo, thinking differently, looking outside, asking and answering tough questions, and collaborating with like-minded organizations.

Filene is a 501(c)(3) not-for-profit organization. Nearly 1,000 members make our research, innovation, and impact programs possible. Learn more at filene.org.

“Progress is the constant replacing of the best there is with something still better."

—Edward A. Filene

612 W. Main StreetSuite 105Madison, WI 53703

p 608.661.3740f 608.661.3933

Publication #357 (3/15)