TSX: PPL; NYSE: PBA TSX: VSN - Veresen Inc. · PDF fileTSX: PPL; NYSE: PBA TSX: VSN....

19

TSX: PPL; NYSE: PBA TSX: VSN

Transcript of TSX: PPL; NYSE: PBA TSX: VSN - Veresen Inc. · PDF fileTSX: PPL; NYSE: PBA TSX: VSN....

TSX: PPL; NYSE: PBA

TSX: VSN

Forward-looking statements and information

This presentation is for information purposes only and is not intended to, and should not be construed to constitute, an offer to sell or the solicitation of an offer to buy, securities of Pembina Pipeline Corporation ("Pembina"). This

presentation and its contents should not be construed, under any circumstances, as investment, tax or legal advice. Any person accepting delivery of this presentation acknowledges the need to conduct their own thorough investigation

into Pembina and its activities before considering any investment in its securities.

This presentation contains certain forward-looking statements and information that are based on Pembina's expectations, estimates, projections and assumptions in light of its experience and its perception of historical trends as well as

current market conditions and perceived business opportunities. In some cases, forward-looking information can be identified by terminology such as "expects", "will", "would", "anticipates", "plans", "estimates", "develop", "intends",

"potential", "continue", "could", "create", and similar expressions suggesting future events or future performance.

In particular, this presentation contains forward-looking statements, including certain financial outlooks, pertaining to, without limitation: the proposed acquisition of Veresen Inc (the "Transaction"), including the expected closing date and

the anticipated benefits of the Transaction to Pembina's and Veresen's securityholders, the expected size and processing capabilities of the combined company, as well as anticipated synergies (including strategic integration and

diversification opportunities, tax benefits and the accretion to cash flow of Pembina), financial results related to and growth opportunities associated with the assets acquired pursuant to the Transaction, future dividends which may be

declared on Pembina's common shares and any future dividend payment date; the ongoing utilization and expansions of and additions to Pembina's business and asset base, the timing and anticipated receipt of required regulatory,

court and securityholder approvals for the Transaction, expectations regarding the combined company's anticipated credit rating, the composition of Pembina's board of directors following closing of the Transaction and expectations

regarding future commodity market supply, demand and pricing and supply and demand for hydrocarbon and derivatives services.

Undue reliance should not be placed on these forward-looking statements and information as they are based on assumptions made by Pembina as of the date hereof regarding, among other things, the ability of the parties to satisfy the

conditions to closing of the Transaction in a timely manner, that favourable growth parameters continue to exist in respect of current and future growth projects (including the ability to finance such projects on favorable terms), future

levels of oil and natural gas development, potential revenue and cash flow enhancement; future cash flows, with respect to Pembina's dividends: prevailing commodity prices, margins and exchange rates, that Pembina's businesses will

continue to achieve sustainable financial results and that the combined company's future results of operations will be consistent with past performance of Pembina and Veresen and management expectations in relation thereto, the

availability and sources of capital, operating costs, ongoing utilization and future expansion for the combined company, the ability to reach required commercial agreements, and the ability to obtain required regulatory approvals.

While Pembina believes the expectations and assumptions reflected in these forward-looking statements are reasonable as of the date hereof, there can be no assurance that they will prove to be correct. Forward-looking statements

are subject to known and unknown risks and uncertainties which may cause actual performance and financial results to differ materially from the results expressed or implied, including but not limited to: the ability of the parties to

receive, in a timely manner, the necessary regulatory, court, securityholder, stock exchange and any other third-party approvals, including but not limited to the receipt of applicable competition approvals; the ability of the parties to

satisfy, in a timely manner, the other conditions to the closing of the Transaction; the failure to realize the anticipated benefits or synergies of the Transaction following closing due to integration issues or otherwise and expectations and

assumptions concerning, among other things: customer demand for the combined company's services, commodity prices and interest and foreign exchange rates, planned synergies, capital efficiencies and cost-savings, applicable tax

laws, future production rates, the sufficiency of budgeted capital expenditures in carrying out planned activities, the impact of competitive entities and pricing; reliance on key industry partners, alliances and agreements; the strength and

operations of the oil and natural gas industry and related commodity prices; the regulatory environment and the ability to obtain regulatory approvals; fluctuations in operating results; the availability and cost of labour and other materials;

the ability to finance projects on advantageous terms; and tax laws and tax treatment. In addition, the closing of the Transaction may not be completed, or may be delayed if the parties' respective conditions to the closing of the

Transaction, including the timely receipt of all necessary regulatory approvals, are not satisfied on the anticipated timelines or at all. Accordingly, there is a risk that the Transaction will not be completed within the anticipated time, on the

terms currently proposed or at all.

Additional information on these factors as well as other risks that could impact Pembina's operational and financial results are contained in Pembina's Annual Information Form and Management's Discussion and Analysis for the year

ended December 31, 2016, and described in our public filings available in Canada at www.sedar.com and in the United States at www.sec.gov. Readers are cautioned that this list of risk factors should not be construed as exhaustive.

The forward-looking statements contained in this document speak only as of the date of this document. Except as expressly required by applicable securities laws, Pembina and its subsidiaries assume no obligation to update forward-

looking statements and information should circumstances or management's expectations, estimates, projections or assumptions change. The forward-looking statements contained in this document are expressly qualified by this

cautionary statement. Readers are cautioned that management of Pembina approved the financial outlooks contained herein as of the date of this presentation. The purpose of the financial outlooks contained herein is to give the reader

an indication of the value of Pembina's current and anticipated growth projects, including with respect to the acquisition of assets pursuant to the Transaction. Readers should be cautioned that the information contained in the financial

outlooks contained herein may not be appropriate for other purposes.

In this presentation, we refer to certain financial measures such as adjusted EBITDA, adjusted cash flow from operating activities, total enterprise value and operating margin, among others that are not determined in accordance with

International Financial Reporting Standards ("Canadian GAAP"). Management believes these non-GAAP and additional GAAP measures provide an indication of Pembina's ability to generate liquidity through cash flow from operating

activities and the expected effect of growth projects on Pembina's current business, as well as the anticipated effect of integration of Pembina's and Veresen's businesses as a result of the Transaction. These measures may also be

used by investors and analysts for assessing financial performance and for the purpose of valuing an issuer, including calculating financial and leverage ratios. The information contained herein with respect to non-GAAP and additional

GAAP measures may not be appropriate for other purposes. For more information about these non-GAAP and additional GAAP measures, see the Appendix to this presentation. All financial information is expressed in Canadian dollars

unless otherwise specified.2

Transaction overview

3

Transaction creates a premier, integrated North American energy infrastructure company

Transaction

Overview

• Offer to acquire all outstanding shares of Veresen in exchange for 0.4287 common shares of Pembina

or $18.65 in cash for each Veresen share, subject to pro ration(1)

• 21.8% premium to Veresen's 20-day weighted average share price of $15.31

Financial

Highlights

• Increases Pembina's long-term, fee-for-service revenue 85%+ fee-for-service over the long term

• Combined company is expected to maintain strong BBB investment grade credit rating

• Increases Pembina's enterprise value by 45% ~$33 BB

• Combined 2018 adjusted EBITDA of $2.55 - $2.75 BB

• Expected annual synergies of $75 - $100 MM and accretive to Pembina's ACFPS in 2018

• Upon close of the transaction Pembina will increase its divided by 5.9% ($2.16 per share annualized)

• Combined near term growth projects of ~$6 BB and unsecured growth projects of ~$20 BB

Regulatory /

Timing

• Expected closing in Q3 – Q4 2017(2), subject to customary regulatory approvals required in Canada and U.S.

• Pembina's senior executive will lead combined company, with Mick Dilger as President and CEO

• Three of Veresen directors will be appointed to Pembina's Board at closing

(1) Subject to proration, a maximum of approximately 99.5 million Pembina common shares to be issued and maximum cash consideration of approximately $1.523 billion.(2) Subject to Veresen's shareholder approval.See "Forward-looking statements and information."

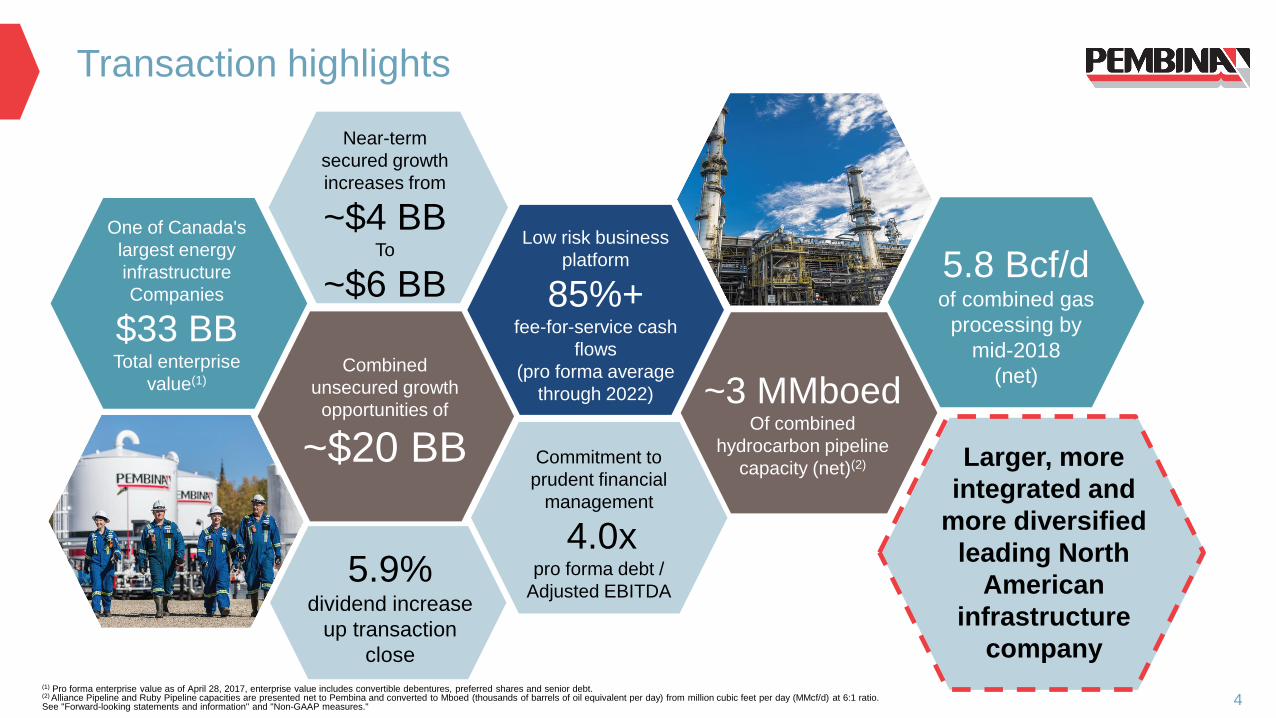

Transaction highlights

4

One of Canada's

largest energy

infrastructure

Companies

$33 BBTotal enterprise

value(1)Combined

unsecured growth

opportunities of

~$20 BB

Near-term

secured growth

increases from

~$4 BBTo

~$6 BB

Low risk business

platform

85%+fee-for-service cash

flows

(pro forma average

through 2022)

5.8 Bcf/dof combined gas

processing by

mid-2018

(net)

Commitment to

prudent financial

management

4.0xpro forma debt /

Adjusted EBITDA

~3 MMboedOf combined

hydrocarbon pipeline

capacity (net)(2)

(1) Pro forma enterprise value as of April 28, 2017, enterprise value includes convertible debentures, preferred shares and senior debt.(2) Alliance Pipeline and Ruby Pipeline capacities are presented net to Pembina and converted to Mboed (thousands of barrels of oil equivalent per day) from million cubic feet per day (MMcf/d) at 6:1 ratio.See "Forward-looking statements and information" and "Non-GAAP measures."

5.9% dividend increase

up transaction

close

Larger, more

integrated and

more diversified

leading North

American

infrastructure

company

Strong alignment in strategy

5

Veresen's asset base supports the continued execution of Pembina's long-term strategy

Pembina's strategy

Preserve value by providing safe, cost-effective, reliable services

Diversify our asset base along the hydrocarbon value chain to provide integrated service offerings

which enhance profitability and customer service

Implement growth by pursuing projects or assets that are expected to generate cash flow per

share accretion and capture long-life, economic hydrocarbon reserves

Maintain a strong balance sheet with prudent financial management in all business decisions

Veresen's alignment

Both companies have a proven record of supporting safe, reliable and

cost effective midstream services for their customers

Extends and further integrates our value chain through basin,

currency, customer and product diversification

Increases our secured growth opportunity by ~$1.5 BB to ~$6 BB and

unsecured growth opportunities to ~$20 BB

The combined company will continue to maintain one of the strongest

balance sheets in the sector ~4x debt / adjusted EBITDA (2018)

See "Forward-looking statements and information" and "Non-GAAP measures."

Canada79%

US21%

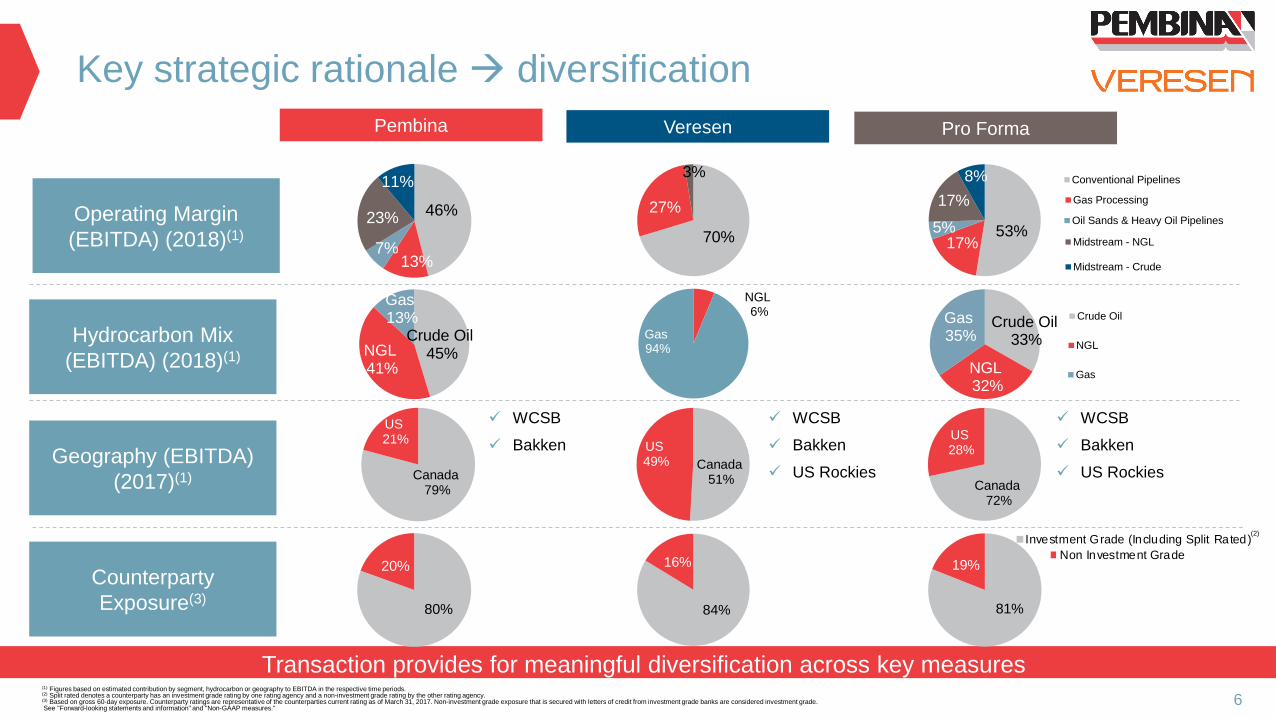

Key strategic rationale diversification

6

Operating Margin

(EBITDA) (2018)(1)

Pembina Veresen Pro Forma

Hydrocarbon Mix

(EBITDA) (2018)(1)

Geography (EBITDA)

(2017)(1)

Counterparty

Exposure(3)

WCSB

Bakken

WCSB

Bakken

US Rockies 76%

24%

Investment Grade (Including Split Rated) Non Investment Grade

46%

13%7%

23%

11%

70%

27%

3%

53%17%

5%

17%

8%

Crude Oil45% NGL

41%

Gas13%

NGL6%

Gas94%

Crude Oil33%

NGL32%

Gas35%

Canada51%

US49%

Canada72%

US28%

80%

20%

84%

16%

81%

19%

Transaction provides for meaningful diversification across key measures(1) Figures based on estimated contribution by segment, hydrocarbon or geography to EBITDA in the respective time periods.(2) Split rated denotes a counterparty has an investment grade rating by one rating agency and a non-investment grade rating by the other rating agency.(3) Based on gross 60-day exposure. Counterparty ratings are representative of the counterparties current rating as of March 31, 2017. Non-investment grade exposure that is secured with letters of credit from investment grade banks are considered investment grade.See "Forward-looking statements and information" and "Non-GAAP measures."

WCSB

Bakken

US Rockies

76%

24%

Investment Grade (Including Split Rated) Non Investment Grade

33%

32%

35%

Crude Oil NGL Gas

33%

32%

35%

Crude Oil NGL Gas

33%

32%

35%

Crude Oil NGL Gas

(2)

52%

18%

5%17%

8%

Conventional Pipeline Gas Processing Oil Sands & Heavy Oil Midstream - NGL Midstream - Crude

52%

18%

5%17%

8%

Conventional Pipeline Gas Processing Oil Sands & Heavy Oil Midstream - NGL Midstream - Crude

52%

18%

5%17%

8%

Conventional Pipeline Gas Processing Oil Sands & Heavy Oil Midstream - NGL Midstream - Crude

52%

18%

5%

17%

8%

Conventional Pipelines Gas Processing Oil Sands & Heavy Oil Pipelines Midstream - NGL Midstream - Crude

52%

18%

5%

17%

8%

Conventional Pipelines Gas Processing Oil Sands & Heavy Oil Pipelines Midstream - NGL Midstream - Crude

7

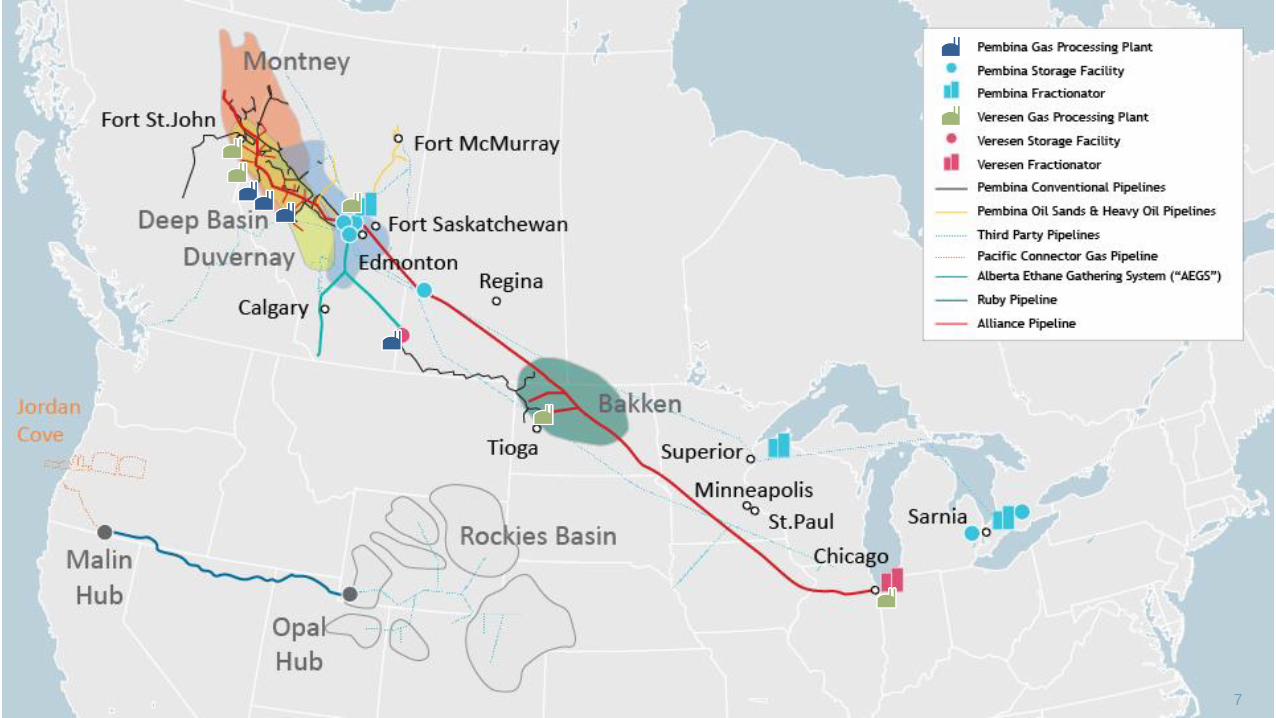

Integrated, customer-focused value chain

8

Refining (Partial

Upgrading)

MarketingOil / C5 / Oil Sands Terminalling

NGL Storage Fractionation Distribution

Consumption

Gathering, Processing,

Field Extraction

Field Terminals Consumption

Propane exports

Redwater + Empress East + Sarnia & Corunna

Mainline Extraction, Fractionation, Distribution

PDH/PPProduction

Natural Gas

Pipelines

(Alliance)

Fractionation

(Aux Sable)NGL Distribution

(Aux Sable)

Mainline

Extraction

(Aux Sable)

Via NGTL

NGL Midstream

Crude Oil Midstream

Oil &

Condensate

Value Chain

("LVP") Production

Value chain extension opportunities

Crude Oil Midstream

Gas/NGL

Value Chain

("HVP")

Combination of Veresen and Pembina adds fully integrated, parallel natural gas value chain

Conventional Pipelines

Conventional / Oil Sands

Pipelines

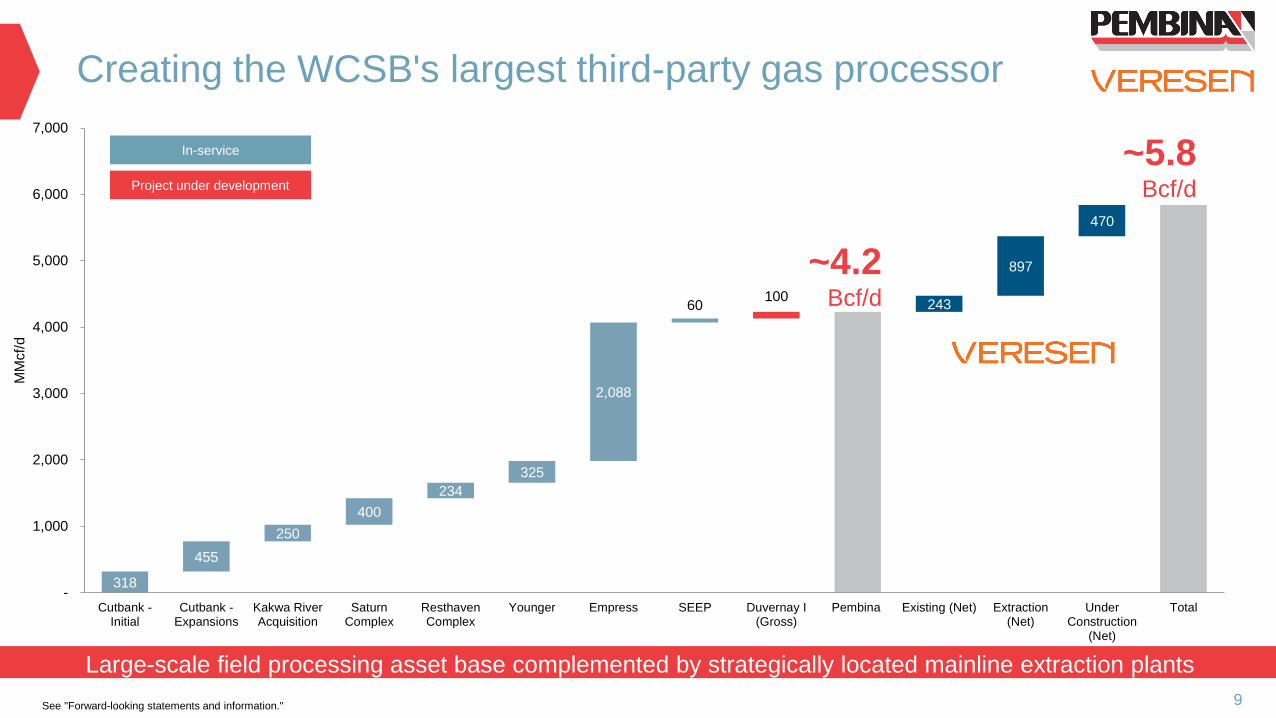

318

455

250

400

234

325

2,088

60 100

243

897

470

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Cutbank -Initial

Cutbank -Expansions

Kakwa RiverAcquisition

SaturnComplex

ResthavenComplex

Younger Empress SEEP Duvernay I(Gross)

Pembina Existing (Net) Extraction(Net)

UnderConstruction

(Net)

Total

MM

cf/

d

Creating the WCSB's largest third-party gas processor

9

Large-scale field processing asset base complemented by strategically located mainline extraction plants

~5.8Bcf/d

~4.2Bcf/d

In-service

Project under development

See "Forward-looking statements and information."

65

8 9

73

55

18

20

56

-

50

100

150

200

250

300

350

RFS I RFSDebottleneck

RFS C3+Debottleneck

(Q1 2016)

RFS II(Q1 2016)

RFS III(Q3 2017)

RFS III Growth(Potential)

Sarnia Pembina Aux Sable (Net) Total

Mbpd

Fractionation capacity across three NGL market hubs

10

~300 mbpd of NGL fractionation capacity in three of North America's premier liquids markets

~300 Mbpd

~250Mbpd

Uncommitted ProjectIn-service Project under development

See "Forward-looking statements and information."

Edmonton Sarnia, Ontario US Midcontinent

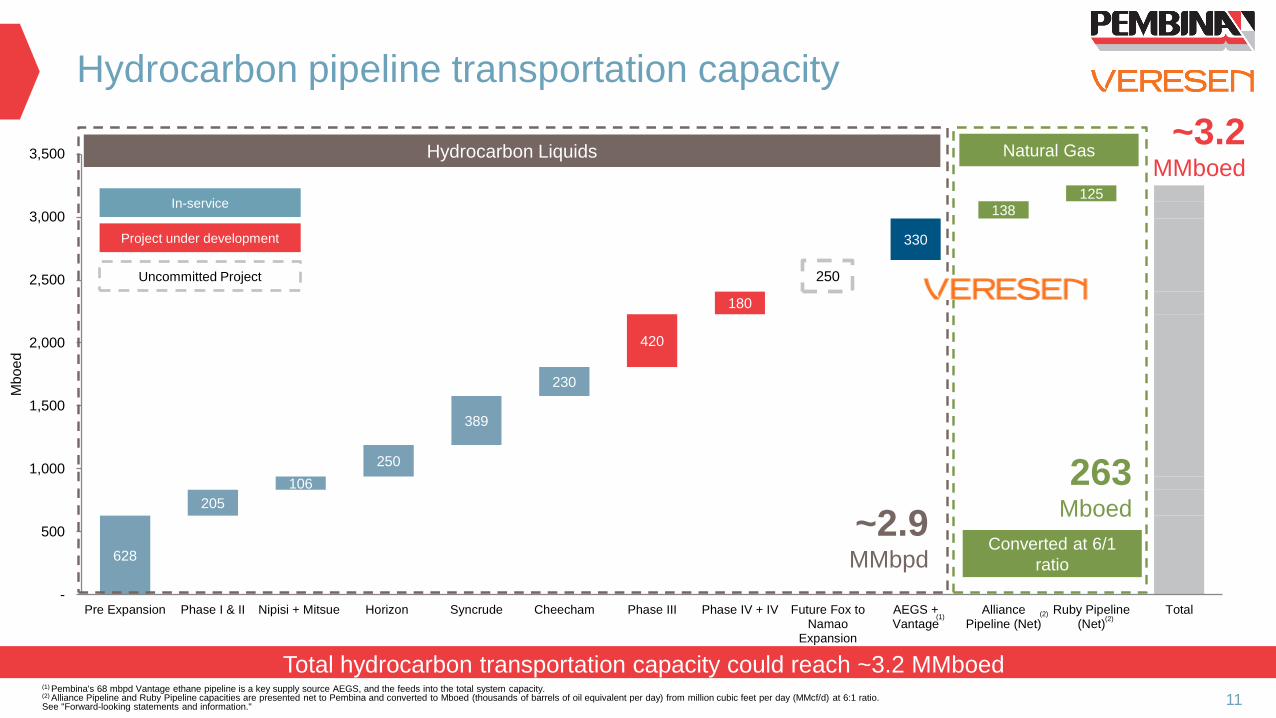

628

205

106

250

389

230

420

180

250

330

138 125

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Pre Expansion Phase I & II Nipisi + Mitsue Horizon Syncrude Cheecham Phase III Phase IV + IV Future Fox toNamao

Expansion

AEGS +Vantage

AlliancePipeline (Net)

Ruby Pipeline(Net)

Total

Mboed

Hydrocarbon pipeline transportation capacity

11

Total hydrocarbon transportation capacity could reach ~3.2 MMboed

Natural Gas

~2.9 MMbpd

263Mboed

(1) Pembina's 68 mbpd Vantage ethane pipeline is a key supply source AEGS, and the feeds into the total system capacity.(2) Alliance Pipeline and Ruby Pipeline capacities are presented net to Pembina and converted to Mboed (thousands of barrels of oil equivalent per day) from million cubic feet per day (MMcf/d) at 6:1 ratio.See "Forward-looking statements and information."

(2)(1)

In-service

Project under development

Uncommitted Project

Hydrocarbon Liquids~3.2

MMboed

Converted at 6/1

ratio

(2)

Financial 'Guard Rail' considerations

12

Veresen transaction fits well with Pembina's financial 'Guard Rails'

1

2

3

4

5

Maintain target of 80% fee-for-service contribution to

EBITDA

Maintain 'strong' BBB credit rating

Target 75% credit exposure from investment grade

and secured counterparties(1)

Target <100% payout of fee-for-service distributable

cash flow by 2018(2)

Target 8 -10% cash flow per share growth without

putting guard rails at risk

Pembina Combined

~84% (2018 – 2022)

~87% (2018 – 2022)

>20% FFO / Debt >20% FFO / Debt

80% 81%

85% 80%

Low End High End

(1) Based on gross 60-day exposure. Counterparty ratings are representative of the counterparties current rating as of March 31, 2017. Non-investment grade exposure that is secured with letters of credit from investment grade banks are considered investment grade. (2) Illustrative calculation based on total common share dividends, preferred share dividends, interest, general and administrative expenses and illustrative cash taxes as compared to consolidated fee-for-service net operating income. Payout ratio calculation is inclusive of increase dividend upon transaction close. See "Forward-looking statements and information" and "Non-GAAP measures."

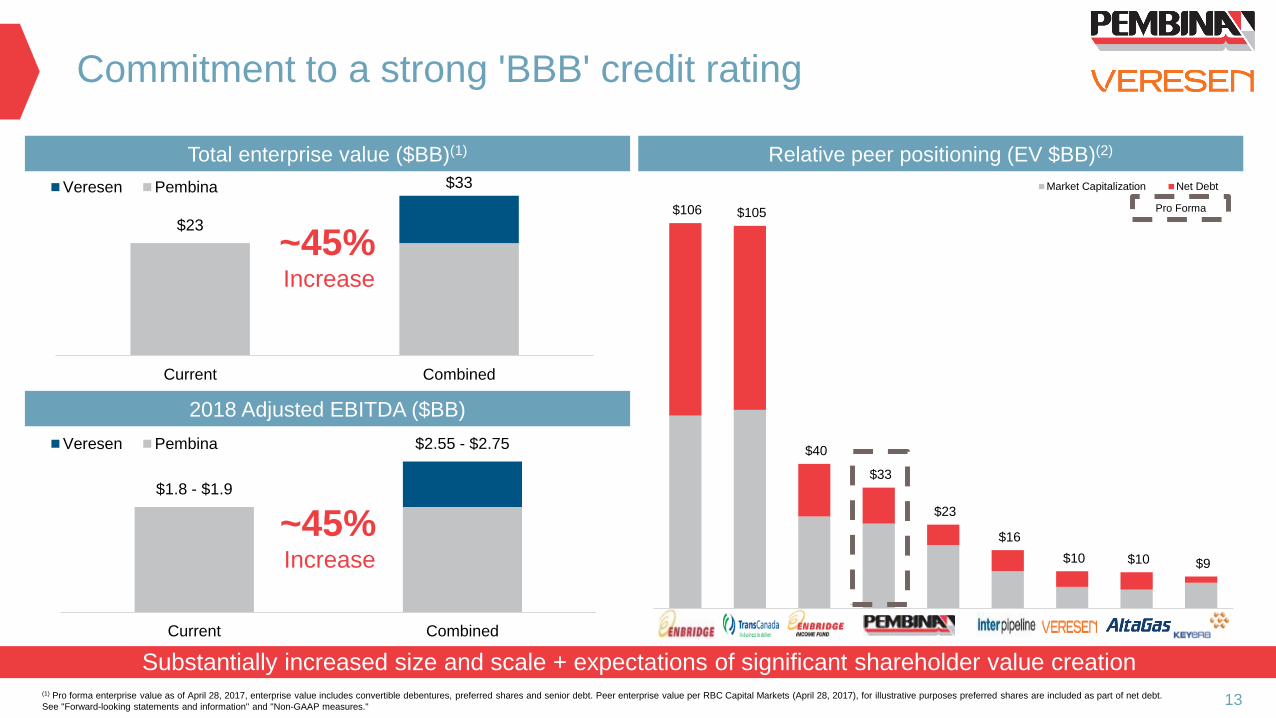

$106 $105

$40

$33

$23

$16

$10 $10 $9

Market Capitalization Net Debt

Commitment to a strong 'BBB' credit rating

13

Substantially increased size and scale + expectations of significant shareholder value creation

Relative peer positioning (EV $BB)(2)Total enterprise value ($BB)(1)

2018 Adjusted EBITDA ($BB)

(1) Pro forma enterprise value as of April 28, 2017, enterprise value includes convertible debentures, preferred shares and senior debt. Peer enterprise value per RBC Capital Markets (April 28, 2017), for illustrative purposes preferred shares are included as part of net debt.

See "Forward-looking statements and information" and "Non-GAAP measures."

~45%Increase

~45%Increase

Pro Forma

$23

$33

-

$5

$10

$15

$20

$25

$30

$35

Current Combined

Veresen Pembina

$1.8 - $1.9

$2.55 - $2.75

-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

Current Combined

Veresen Pembina

~44%

~64% ~61%

~65%

~63%

~33%

~13%

~19%

~18%

~24%

~22%

~19%

~15%

~13%

~10%

~1%

~4%

~5%

~4%

~4%

-

$1

$1

$2

$2

$3

$3

$4

2015A 2016A 2017E 2018E 2018(Combined)

We are committed to a low-risk business platform

14

85%+ of operating margin is expected to be generated from fee-for-service contracts in 2018

Summary of operating margin by type ($MM)(1)

(1) 2014 - 2016 figures based on actual results (including internal allocations), while forward years are based on Pembina's current long-term forecast and actual results may vary depending on asset utilization, project in-service dates, commodity pricing and other factors.

See "Forward-looking statements and information" and "Non-GAAP measures."

Fee-for-Service Take-or-Pay / Cost-of-Service Product Margin Frac Spread

Total fee-

based =

77%

Total fee-

based =

77%

Total fee-

based =

80%

Total fee-

based =

83%

Total fee-

based =

86%

2014 2015 2016 2017 2018

-

$1.0

$2.0

$3.0

2014 2015 2016 2017 2018

$B

B

Capital Expenditures Internal Equity DRIPPreferred Shares Common Equity DebtVeresen Power Asset Sale

Pembina's financial outlook and considerations

Pembina has developed a well thought out financing plan that ensures strong financial position

15

Capital expenditure funding Financing considerations

• Commitment to Pembina's financial objectives:

− Financing growth 50% debt / 50% equity over

the investment cycle

− Conservative credit metrics to maintain 'strong'

BBB rating

− Ensuring ample liquidity

• The ~$1.5 BB cash portion of the transaction will be

initially funded through Pembina's revolving credit

facility, with subsequent preferred share and medium

term note offerings

− No common equity requirements foreseen,

(DRIP or public issuance)

See "Non-GAAP measures." & "Forward-looking statements and information."

2017 / 2018 Capital

~$3.5 BB

Commitment to a strong 'BBB' credit rating(Managing toward target credit metrics)

16

Through the transaction Pembina will ensure prudent financial management and a strong balance sheet

Debt / Adjusted EBITDA (x) (2018 Forecast)(1)Credit Highlights

Fund from Operations / Debt (%) (2018 Forecast)(3)Debt to Total Capitalization (%) (2018 Forecast)(2)

(1) Debt to adjusted EBITDA calculated as total debt divided by adjusted EBITDA, on a proportionate consolidation basis.(2) Debt to total capitalization calculation assumes exclusion of debt related to Veresen's subsidiaries.(3) Debt to funds from operations calculated as per Standard and Poor's methodology.

See "Forward-looking statements and information" and "Non-GAAP measures."

4.0x

3.75x - 4.25x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

Pro Forma Target

20%

18% - 22%

-

5%

10%

15%

20%

25%

Pro Forma Target

38%

38% - 40%

-

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Pro Forma Target

• Increased size, scale and asset diversity serve to create

enhanced credit profile

• Combined balance sheet remains strong only a modest

increase in near term leverage

• The combined company will maintain a strong BBB

investment grade credit rating

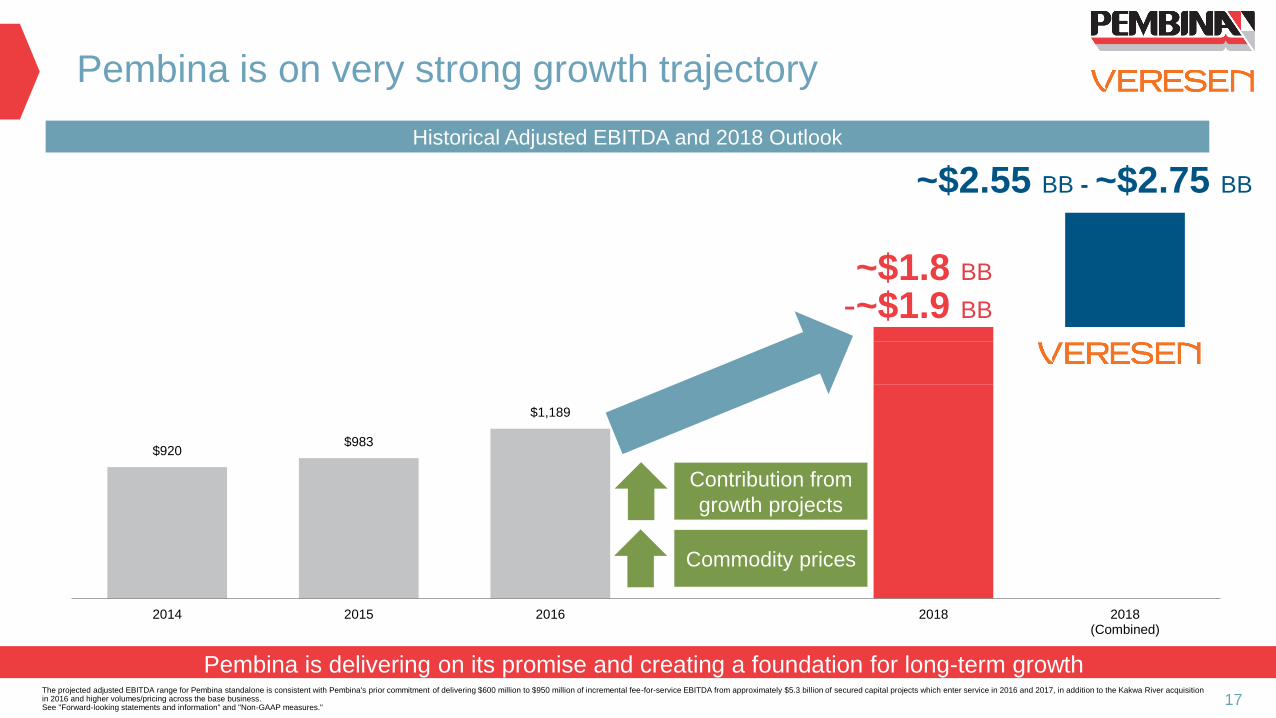

$920 $983

$1,189

2014 2015 2016 2018 2018(Combined)

Pembina is on very strong growth trajectory

17

Pembina is delivering on its promise and creating a foundation for long-term growth

~$1.8 BB

-~$1.9 BB

The projected adjusted EBITDA range for Pembina standalone is consistent with Pembina's prior commitment of delivering $600 million to $950 million of incremental fee-for-service EBITDA from approximately $5.3 billion of secured capital projects which enter service in 2016 and 2017, in addition to the Kakwa River acquisition in 2016 and higher volumes/pricing across the base business. See "Forward-looking statements and information" and "Non-GAAP measures."

Historical Adjusted EBITDA and 2018 Outlook

~$2.55 BB - ~$2.75 BB

Commodity prices

Contribution from

growth projects

Conclusions

18

This transaction is expected to drive meaningful value for shareholders and customers

Proven history of safe and reliable operations while developing enduring relationships with local communities

Our long term strategy remains unchanged and continues to create significant shareholder value

Committed to delivering 2018 Adjusted EBITDA of $2.55 BB to $2.75 BB (pro forma)

The transaction significantly increases Pembina's size, diversification, and enhances customer service offering

Substantial portfolio of opportunities support Pembina's 8 – 10% adjusted cash flow per share growth target

See "Forward-looking statements and information" and "Non-GAAP measures."

Non-GAAP measures

This presentation uses certain terms that are not defined by GAAP but are used by management of Pembina to evaluate the Veresen transaction.

Non-GAAP financial measures do not have a standardized meaning prescribed by GAAP and are therefore unlikely to be comparable to similar

measures presented by other companies.

Pembina uses the non-GAAP terms: Total Enterprise Value (market value of Pembina's common shares plus preferred shares and convertible

debentures plus senior debt less cash and cash equivalents), Adjusted EBITDA (earnings for the year plus share of profit (loss) from equity

accounted investees (before tax, depreciation and amortization) plus net finance costs plus income taxes plus depreciation and amortization

(included in operations and general and administrative expense) and unrealized gains or losses on commodity-related derivative financial

instruments. Adjusted EBITDA also includes adjustments for loss (gain) on disposal of assets, transaction costs incurred in respect of

acquisitions, impairment charges or reversals and write-downs in respect of goodwill, intangible assets and property plant and equipment, non-

cash provisions and ), Adjusted Cash Flow from Operating Activities (cash flow from operating activities plus the change in non-cash operating

working capital, adjusting for current tax and share-based payment expenses, and deducting preferred share dividends declared), and the

additional GAAP term Operating Margin (gross profit before depreciation and amortization included in operations and unrealized gain/loss on

commodity-related derivative financial instruments). Adjusted EBITDA is used interchangeably with EBITDA in this presentation.

Management believes these non-GAAP measures provide an indication of the results generated by Pembina's business activities and the value

those businesses generate. Investors should be cautioned that these non-GAAP measures should not be construed as an alternative to net

earnings, cash flow from operating activities or other measures of financial performance determined in accordance with GAAP as an indicator of

Pembina's performance. For additional information with respect to financial measures which have not been identified by GAAP, including

reconciliations to the closest comparable GAAP measure, see Pembina's Management's Discussion and Analysis for the fiscal year ended

December 31, 2016, available on SEDAR at www.sedar.com or in Pembina's annual report on Form 40-F for the fiscal year ended December 31,

2016 available on EDGAR at www.sec.gov.

19