TRI-STAR PETROLEUM COMPANY - COAG Energy Council · Tri-Star Petroleum Company welcomes the...

9

Page 1 of 8 TRI-STAR PETROLEUM COMPANY 9 GREENWAY PLAZA, SUITE 3100 LEVEL 35, 123 EAGLE STREET, BRISBANE, QLD 4000 HOUSTON, TEXAS 77046 PO BOX 7128, BRISBANE, QLD 4001 PHONE: 1 713 222 0011 PHONE: 61 7 3236 9800 FAX: 1 713 622 6812 FAX: 61 7 3221 2146 [email protected] [email protected] Incorporated in Texas, USA ARBN #050 415 739 18 October 2016 Examination of the Coverage Test COAG Energy Council Secretariat By email: [email protected] Dear Dr Vertigan Stakeholder submission – Coverage test for regulation of gas pipelines Tri-Star Petroleum Company welcomes the opportunity to respond to the consultation paper in relation to the examination of the current test for the regulation of gas pipelines (Consultation). Tri-Star Petroleum Company is part of a group of exploration and development companies owned and operated by the James H. Butler family since 1979. Group companies include: • Tri-Star Petroleum Company • Tri-Star Coal Company • Tri-Star Energy Company • Tri-Star Australia Holding Company • West Texas Oil and Gas Corporation (collectively referred to as Tri-Star) Tri-Star is involved in key aspects of the minerals and hydrocarbon supply chain, from exploration and development to production and marketing. In the USA, Tri-Star continues to focus on West Texas Intermediate crude oil production and has been drilling conventional petroleum wells in the Permian Basin since 1979. In Australia, Tri-Star is the pioneer of the coal seam gas (CSG) industry in Queensland and flared the first CSG well in 1994. Tri-Star discovered and developed key CSG fields in the Bowen Basin including Durham Ranch, Spring Gully and Fairview. Tri-Star operates both coal and gas interests, and is participating as non-operator in exploration and development joint ventures with members of CSG to liquefied natural gas (LNG) projects, including Gladstone LNG (GLNG) and Australia Pacific LNG (APLNG).

Transcript of TRI-STAR PETROLEUM COMPANY - COAG Energy Council · Tri-Star Petroleum Company welcomes the...

Page 1 of 8

TRI-STAR PETROLEUM COMPANY

9 GREENWAY PLAZA, SUITE 3100 LEVEL 35, 123 EAGLE STREET, BRISBANE, QLD 4000HOUSTON, TEXAS 77046 PO BOX 7128, BRISBANE, QLD 4001PHONE: 1 713 222 0011 PHONE: 61 7 3236 9800FAX: 1 713 622 6812 FAX: 61 7 3221 [email protected] [email protected] in Texas, USA ARBN #050 415 739

18 October 2016

Examination of the Coverage TestCOAG Energy Council SecretariatBy email: [email protected]

Dear Dr Vertigan

Stakeholder submission – Coverage test for regulation of gas pipelines

Tri-Star Petroleum Company welcomes the opportunity to respond to the consultation paper inrelation to the examination of the current test for the regulation of gas pipelines (Consultation).

Tri-Star Petroleum Company is part of a group of exploration and development companies ownedand operated by the James H. Butler family since 1979. Group companies include:

• Tri-Star Petroleum Company

• Tri-Star Coal Company

• Tri-Star Energy Company

• Tri-Star Australia Holding Company

• West Texas Oil and Gas Corporation

(collectively referred to as Tri-Star)

Tri-Star is involved in key aspects of the minerals and hydrocarbon supply chain, from explorationand development to production and marketing.

In the USA, Tri-Star continues to focus on West Texas Intermediate crude oil production and hasbeen drilling conventional petroleum wells in the Permian Basin since 1979.

In Australia, Tri-Star is the pioneer of the coal seam gas (CSG) industry in Queensland and flared thefirst CSG well in 1994. Tri-Star discovered and developed key CSG fields in the Bowen Basin includingDurham Ranch, Spring Gully and Fairview. Tri-Star operates both coal and gas interests, and isparticipating as non-operator in exploration and development joint ventures with members of CSGto liquefied natural gas (LNG) projects, including Gladstone LNG (GLNG) and Australia Pacific LNG(APLNG).

Page 2 of 8

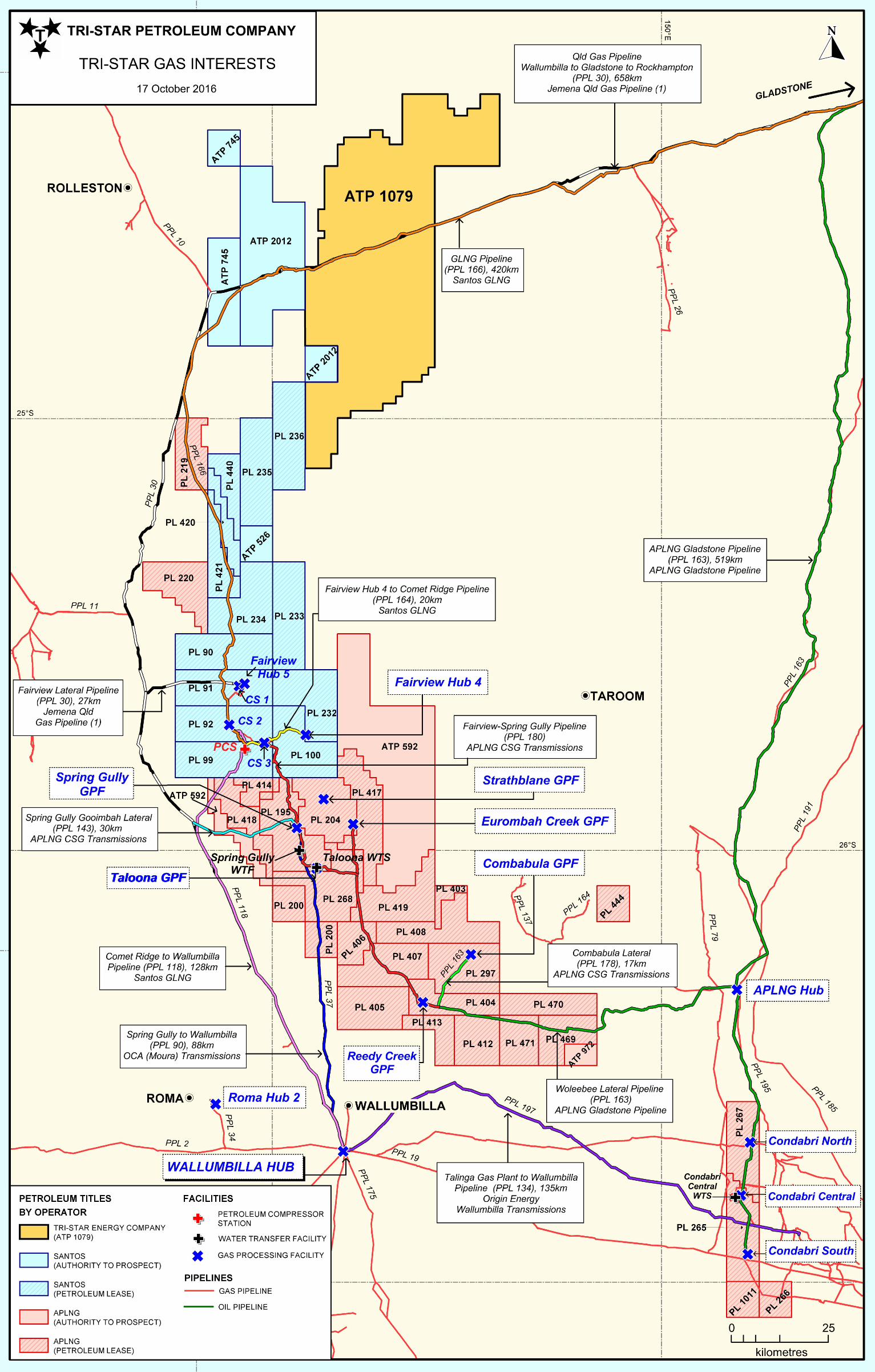

Tri-Star has non-operated working interests and/or reversionary interests in tenures in the followingfields:

• Operated by GLNG (shown in blue on the attached map)

Fairview

• Operated by APLNG (shown in red on the attached map)

Durham Ranch, Spring Gully, Combabula, Reedy Creek, Gilbert Gully, Condabri

Tri-Star’s non-operated working interests allow Tri-Star to take and sell approximately 1 to 3 TJ ofCSG per day. To date, Tri-Star has not sold any of this CSG as it has not been able to obtaincommercially viable terms to do so.

Regarding its reversionary interests, Tri-Star contends that its significant reversionary interests in thetenures operated by APLNG have crystallised. APLNG disputes this and the matter is currently thesubject of legal proceedings before the Supreme Court of Queensland. Upon reversion, Tri-Star willbe one of the top ten largest producers of CSG on the East Coast of Australia, with production ofapproximately 400 to 450 TJ of CSG per day and reserves in the order of 3,500 PJ (3.5 Tcf) of 2P1 or5,000 PJ (5Tcf) of 3P + 3C.2

In addition, Tri-Star is the 100% holder and operator of ATP 1079, which is currently the subject ofexploration and development activities (shown in yellow on the attached map). This field is locatednext to the successful Fairview field and has both the GLNG export pipeline and the Queensland Gaspipeline passing over it. If successful, Tri-Star conservatively estimates that ATP 1079 could supportproduction of 100 to 150 TJ of CSG per day from a field of some 1,000 wells (the first of which is tobe drilled in 2017).

Executive Summary

Broadly speaking, Tri-Star supports the ACCC’s recommended reforms to the east coast gas market,namely where the focus of these reforms is on:

• encouraging more gas supply and more gas suppliers, taking account of each jurisdiction'scircumstances;

• better information for trading in the market;

• creation of trading hubs in the North and South;

• improved access to transport infrastructure; and

• better pricing information.

The current regime for access to natural gas pipelines contained in the National Gas Law (NGL) andNational Gas Rules (NGR) is inefficient because market power is being exercised by existing pipelineowners,3 which is limiting the activities of exploration and development companies and thusconstraining the medium and long term supply of natural gas in Australia. This is in the face ofsignificant demand for natural gas from end users, both in Australia and internationally.

1 2P means Proved plus Probable Reserves within the meaning of the Petroleum Resources Management System, 2011.2 3P + 3C means Proved plus Probable plus Possible Reserves + Proved plus Probable plus Possible Contingent Resources within themeaning of the Petroleum Resources Management System, 2011.3 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 8.

Page 3 of 8

This inefficient situation in Australia should be addressed by replacing the current test for coveragewith the test proposed by the ACCC in its April 2016 Report4 (which test focuses on whether apipeline has substantial market power) (ACCC Test). This test would address the inefficiencyidentified above by lowering the hurdle for coverage and preventing pipeline owners from imposingmonopoly prices for the use of their infrastructure.

The ACCC Test should apply to all pipelines, irrespective of whether or not they are subject to a 15year no-coverage determination. A consistent application of the coverage test would reflect the factthat gas pipelines are part of a network and inefficiency may arise from the weakest link in thatnetwork.

The scope of the review should also include a recommendation as to whether the application of thecoverage test in the NGL should be extended to apply not only to gas pipelines, but also facilitiessuch as upstream gas processing facilities that are necessary and integral to the extraction andtransportation of gas to markets.

We expand upon each of these points below.

If you would like to discuss further any of the issues raised in this submission, please contact PeterBorg on (07) 3236 9800 or [email protected].

Current regime constraining exploration and development of upstream projects

The current regime for access to natural gas pipelines contained in the NGL and NGR is inefficientbecause market power is being exercised by existing pipeline owners which is limiting the activitiesof exploration and development companies and thus constraining the medium and long term supplyof natural gas in Australia.

The ACCC concluded that there is a need for more sources of gas supply in Australia, particularly inthe southern states.5 Reserves at existing sources of supply are finite. The ACCC concluded that themost likely outcome is that gas supply from existing sources, including the Cooper Basin, OtwayBasin and Gippsland Basin will decline in the near future and that this will place pressure on thedomestic market6 in the form of steadily increasing unfulfilled demand.7

Continuing exploration and development is therefore critical to ensuring that sufficient gas isavailable to meet domestic and international needs. However, gas exploration and productionprojects are high risk, have high capital costs and have long timeframes. The commercial viability ofsuch projects is dependent upon gas producers having certainty that they will be able to transportgas to markets without pipeline owners extracting all potential profits through the imposition ofmonopoly prices. Unlike in other jurisdictions (discussed further below), the current regulatoryapproach in Australia does not provide gas producers with that certainty.

Currently, the vast majority (more than 80%) of the gas transmission pipelines on Australia's eastcoast are unregulated.8 This reflects the inappropriately high hurdle to declaration of transmissionpipelines arising from the coverage criteria currently set out in section 15 of the NGL (discussedfurther below).

4 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 138.5 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 18.6 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 18.7 ACCC, Inquiry into the East Coast Gas Market, April 2016, Chart 2 on page 4.8 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 10.

Page 4 of 8

The ACCC recently concluded that a large number of existing pipelines have been engaging inmonopoly pricing.9

In consequence, the lack of regulation of Australia's gas transmission pipelines is creating significantinefficiency. That inefficiency takes a number of forms, including:

less than efficient levels of exploration and reserve development; and

less than efficient use of gas from existing reserves. This includes lower gas use than wouldbe efficient and also distortions in gas flows resulting in gas not being used where it is mostvaluable.10

The key dilemma facing gas producers is that assets and projects they develop may becomeeffectively stranded because there is no means to cost effectively transport gas from those projectsto users. The options for the owner of a stranded project are either to pay significant transportationcosts to the monopoly pipeline operators or sell the interest (or gas) to another industry participantwho has a transportation option. Both options materially decrease the return to the explorationcompany.

Although gas producers could, as a matter of theory, construct competing pipelines, it would not becommercially viable, or socially efficient to do so. That is for a number of reasons.

First, it is clear that gas pipelines are natural monopoly facilities. There are significant economies ofscale for gas pipelines including in relation to the pipeline diameter, the expansion of capacitythrough the addition of compressor stations and looping and the fact that a large proportion of thetotal costs are fixed.11

Second, at this time, most gas exploration projects are not large enough to require their owntransmission pipeline. As such, the existing transmission pipelines, particularly where those pipelineshave unused capacity, create an economic barrier to the construction of a new pipeline.

ACCC's proposed coverage test should replace the current coverage test

Australia should address the current inefficient situation by replacing the current test for coveragewith the test proposed by the ACCC in its April 2016 Report (ACCC Test).12

The key problem with the existing regime is that criterion (a) of section 15 of the NGL (NGL Criterion(a)) is unlikely to be satisfied for Australia's east coast gas pipelines13 because:

9 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 8.10 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 111.11 Incenta Economic Consulting, Assessment of the coverage criteria for the gas pipeline access regime, September 2015, page 8.12 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 138.13 This is on the basis of the traditional and likely future interpretation of NGL Criterion (a) under which the criteria is only satisfied ifdeclaration (ie access on reasonable terms) would promote a material increase in competition in a separate market as compared to thelevel of competition in that market likely to exist in the absence of declaration (ie access on the terms imposed by the monopoly provider).We acknowledge that the recent decision of the Australian Competition Tribunal in the Port of Newcastle matter (Application by GlencoreCoal Pty Ltd [2016] ACompT 6) adopted a different interpretation of the similarly worded criterion (a) of Part IIIA of the Competition andConsumer Act 2010 (Cth) (Part IIIA Criterion (a)) which would result in a much lower standard for satisfaction of that criterion. However,that decision did not relate to NGL Criterion (a). Further, to the extent that it may influence the interpretation of NGL Criterion (a), thedecision has been appealed. Finally, in any case the Australian Government has indicated an intention to adopt the ProductivityCommission's recommendation to amend the language of criterion (a) in a manner that would make clear that the traditional approachdescribed above is correct (see Australian Government Response on the National Access Regime, published on 24 November 2015, page2).

Page 5 of 8

it is directed to instances of vertically integrated monopolies who can use market powerarising from a monopoly facility to hinder its competitors, and therefore lessen competitionin a related upstream or downstream market;

however, the owners of transmission pipelines on Australia's east coast are typically notvertically integrated but instead specialise in the provision of pipeline services (SpecialistPipeline Operators), with the effect that price gouging behaviour does not lessencompetition in upstream or downstream markets.

This problem appears to have arisen because NGL Criterion (a) is drafted to align with criterion (a)(Part IIIA Criterion (a)) of the declaration criteria for access to services set out in Part IIIA of theCompetition and Consumer Act 2010 (Cth) (Part IIIA). However, the manner in which the Australiangas industry has developed makes the alignment of those criteria inappropriate.14 The access regimein Part IIIA addresses a different economic problem to that faced by the Australian gas industry.15

Specifically, Part IIIA is directed to the regulation of vertically integrated monopolies who can usemarket power in one market to hinder competition in separate markets as described above. Part IIIAwas never intended to provide a regime for price regulation of instances of market power bySpecialist Pipeline Operators.16

In consequence, pipeline owners are able to impose monopoly prices and create the inefficienciesidentified above without any risk that their pipelines will be regulated.

In contrast to the existing test, which is not effective in regulating pipelines owned by SpecialistPipeline Operators, the ACCC Test is focuses on the key question from the perspective of efficiencyand the national gas objective, namely whether a pipeline has substantial market power.17

In consequence, the ACCC Test would address the inefficiency identified above by lowering thehurdle for coverage (ie regulation) and therefore increasing the ability of gas producers to gainaccess to gas transportation agreements on reasonable terms to support the development of themultiple new projects in Australia that will be required to meet the increasing unfulfilled demand forgas in the years up to 2025 identified by the ACCC and beyond.18

Introducing the ACCC Test would not necessarily create any additional regulatory cost. For example,a covered pipeline may be subject to light regulation which involves a negotiate/arbitrate model.Under this form of regulation, it may that the threat of arbitration would be sufficient to preventpipeline owners from imposing monopoly prices for the use of their infrastructure. However, in theevent that commercial negotiation failed to achieve an appropriate outcome, the ACCC Test wouldincrease the likelihood of coverage, and therefore increase the likelihood that gas producers wouldhave a commercially viable avenue through which to seek access to an existing pipeline oncommercially reasonable terms.

14 Castalia Strategic Advisors, AEMC Gas Access Regime Advice, 10 August 2015, page 16.15 Incenta Economic Consulting, Assessment of the coverage criteria for the gas pipeline access regime, September 2015, page 30.16 Incenta Economic Consulting, Assessment of the coverage criteria for the gas pipeline access regime, September 2015, page 30.17 Specifically, the ACCC Test involves the Minister being satisfied that: the pipeline has substantial market power; it is likely the pipelinewill continue to have substantial market power in the medium term; and coverage will or is likely to contribute to the achievement of thenational gas objective.18 ACCC, Inquiry into the East Coast Gas Market, April 2016, Chart 2 on page 4.

Page 6 of 8

Coverage test should apply to all pipelines, including those subject to a 15 year no-coveragedetermination

The ACCC Test should apply to all pipelines, irrespective of whether or not they are subject to a 15year no-coverage determination (NCD).

It is acknowledged that NCDs are intended to provide regulatory certainty and encourage efficientinvestment in new pipeline infrastructure. However, the current protections for pipeline owners gosignificantly too far. Even if pipelines the subject of NCDs recover the cost of their constructionwithin 15 years, there is not currently any obligation on the owners of such pipelines to offer accessfrom that time on more reasonable terms. The ACCC's 2015 inquiry identified two pipelines that hadalready recovered their construction costs following the imposition of prices on foundation usersthat resulted in an accelerated recovery.19 However, neither pipeline had reduced its prices to alevel based on operating and maintenance costs. Instead, the ACCC concluded that the prices beingimposed by those pipelines were between two and five times higher than the likely price if thepipelines were subject to economic regulation.20

Furthermore, the basis for a no coverage determination is that not all of the pipeline coveragecriteria are met.21 In the majority of cases therefore, the original basis for a no coveragedetermination is likely to have been that the pipeline would not satisfy NGL Criterion (a). Inconsequence, if it is determined that the coverage criteria, including in particular NGL Criterion (a)are inappropriate and should be changed, then the original basis for the no coverage determinationarguably falls away.

Finally, a consistent application of the coverage test to all pipelines is necessary to achieve theefficiencies that would flow from the adoption of the ACCC Test. This is because the existing gaspipelines on Australia's east coast are part of a very thin network and inefficiency arises inconsequence of the weakest link in that network. For example, where access to two separatetransmission pipelines is necessary to transport gas from a basin to end users, coverage of only oneof those pipelines is not sufficient to provide gas producers with appropriate transport costs.Instead, it is only when both transmission lines are covered that gas producers have the certaintynecessary to engage in the exploration and development required to undertake new gas supplyprojects.

If it is considered necessary to protect regulatory certainty, a transitional measure could be adoptedto address the change in approach under which no coverage decisions which were made prior to thechange in the coverage criteria.

Scope of review should include access to all facilities necessary and integral to the extraction andtransportation of gas to markets, including upstream gas processing facilities

The scope of the review should also include a recommendation as to whether the application of thecoverage test in the NGL should be extended to apply not only to gas pipelines, but also facilitiessuch as upstream gas processing facilities that are necessary and integral to the extraction andtransportation of gas to markets.

19 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 106.20 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 108.21 NGL, section 154(2).

Page 7 of 8

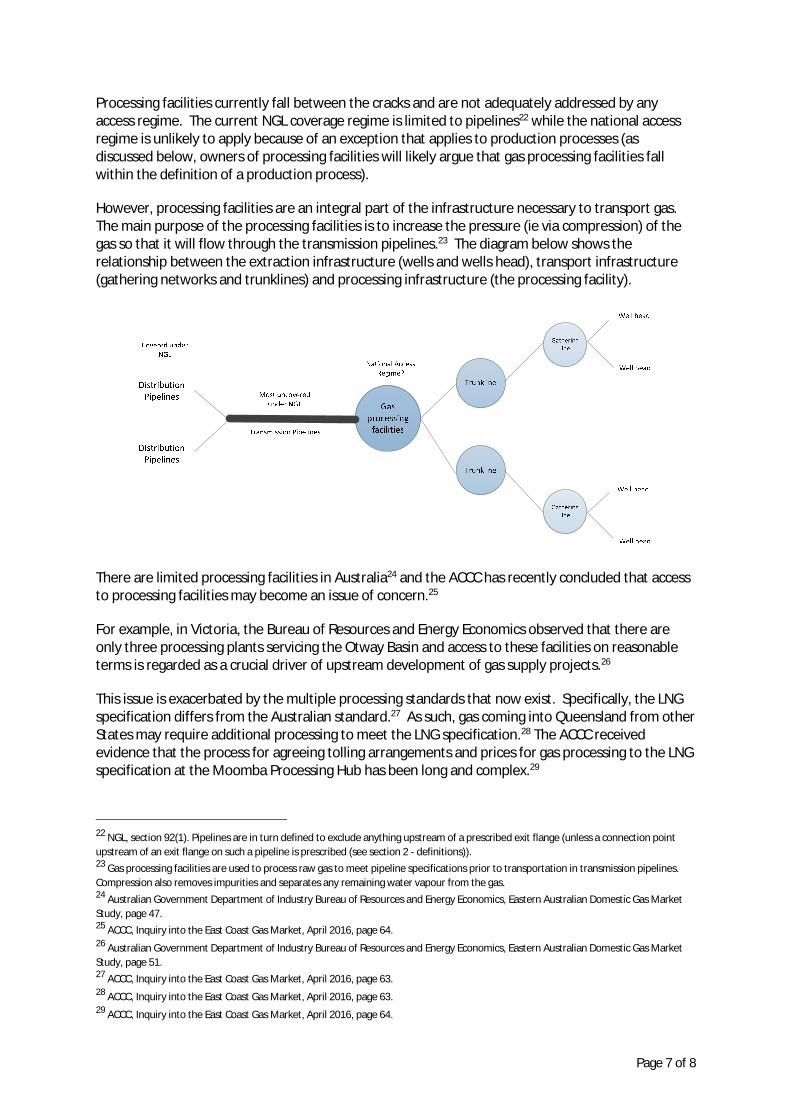

Processing facilities currently fall between the cracks and are not adequately addressed by anyaccess regime. The current NGL coverage regime is limited to pipelines22 while the national accessregime is unlikely to apply because of an exception that applies to production processes (asdiscussed below, owners of processing facilities will likely argue that gas processing facilities fallwithin the definition of a production process).

However, processing facilities are an integral part of the infrastructure necessary to transport gas.The main purpose of the processing facilities is to increase the pressure (ie via compression) of thegas so that it will flow through the transmission pipelines.23 The diagram below shows therelationship between the extraction infrastructure (wells and wells head), transport infrastructure(gathering networks and trunklines) and processing infrastructure (the processing facility).

There are limited processing facilities in Australia24 and the ACCC has recently concluded that accessto processing facilities may become an issue of concern.25

For example, in Victoria, the Bureau of Resources and Energy Economics observed that there areonly three processing plants servicing the Otway Basin and access to these facilities on reasonableterms is regarded as a crucial driver of upstream development of gas supply projects.26

This issue is exacerbated by the multiple processing standards that now exist. Specifically, the LNGspecification differs from the Australian standard.27 As such, gas coming into Queensland from otherStates may require additional processing to meet the LNG specification.28 The ACCC receivedevidence that the process for agreeing tolling arrangements and prices for gas processing to the LNGspecification at the Moomba Processing Hub has been long and complex.29

22 NGL, section 92(1). Pipelines are in turn defined to exclude anything upstream of a prescribed exit flange (unless a connection pointupstream of an exit flange on such a pipeline is prescribed (see section 2 - definitions)).23 Gas processing facilities are used to process raw gas to meet pipeline specifications prior to transportation in transmission pipelines.Compression also removes impurities and separates any remaining water vapour from the gas.24 Australian Government Department of Industry Bureau of Resources and Energy Economics, Eastern Australian Domestic Gas MarketStudy, page 47.25 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 64.26 Australian Government Department of Industry Bureau of Resources and Energy Economics, Eastern Australian Domestic Gas MarketStudy, page 51.27 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 63.28 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 63.29 ACCC, Inquiry into the East Coast Gas Market, April 2016, page 64.

Page 8 of 8

Although a processing facility forms an integral and necessary part of the equipment required to usea gas transmission pipeline, and may be owned by the same entity as the transmission pipeline, theyare not currently subject to the access regime set out in the NGL.

Further, the national access regime is unlikely to provide gas producers with the ability to access gasprocessing facilities. This is because:

a service that is the use of a 'production process' cannot be declared under Part IIIA30 section44B; and

given that processing facilities are used to process natural gas, owners of processing facilitieswill likely argue that services provided by a gas processing facility are part of a 'productionprocess'.31

As such, the limitation to 'pipelines' of the current access regime in the NGL has the potential toundermine the entire regime because processing facility owners (who may be the same entities asthe pipeline owners) can extract monopoly rents through prices for access to the gas processingfacilities attached to the pipelines.

To address this, the application of the NGL coverage regime should be expanded to include not onlypipelines, but also facilities that are necessary and integral to the extraction and transportation ofgas to markets. An express reference to upstream gas processing facilities should be included tomake clear that such facilities fall within the scope of the NGL regime.

Please feel free to contact us should you wish to discuss any issues further.

Yours faithfullyTRI-STAR PETROLEUM COMPANY

Peter BorgSenior Executive – Legal

30 Competition and Consumer Act 2010 (Cth), section 44B.31 Bureau of Resources and Energy Economics in its Eastern Australian Domestic Gas Market Study, page 54.