Tri-party Repo Reform policy imperatives

7

Transcript of Tri-party Repo Reform policy imperatives

3

Tri-party Repo Reform policy imperatives The Fed had 3 policy concerns about the tri-party repo market following the financial crisis: 1. Reliance on large amounts of intraday credit provided by

clearing banks to support clearing and settlement processes.

2. Poor credit and liquidity risk management practices exhibited by all market participants.

3. The lack of credible plans and resources to manage the orderly unwind of positions in the event of a large broker dealer default.

4

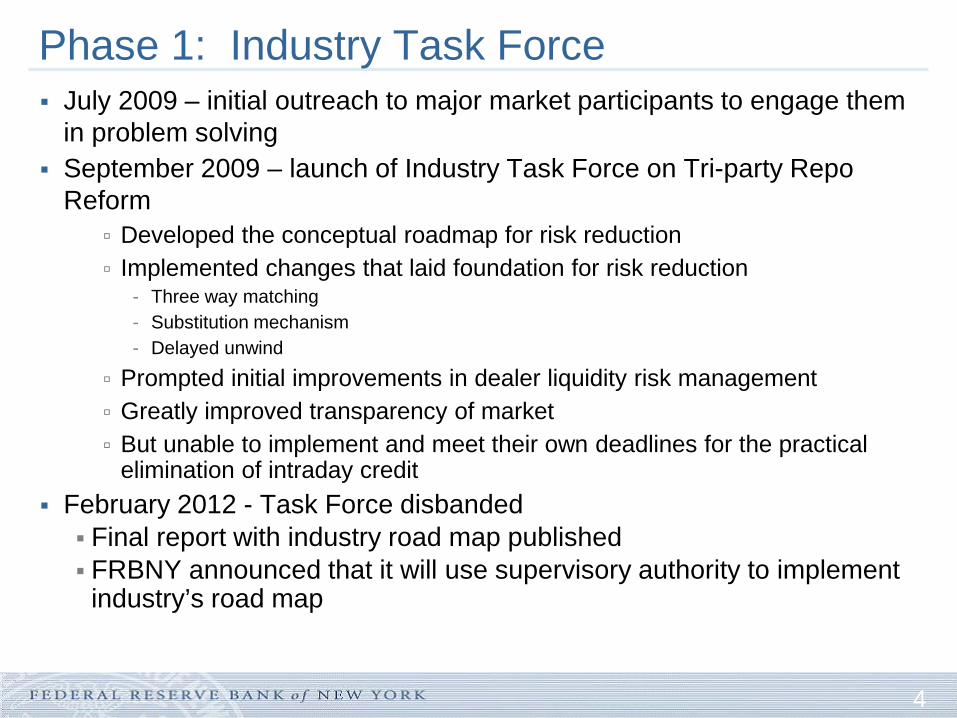

Phase 1: Industry Task Force July 2009 – initial outreach to major market participants to engage them

in problem solving September 2009 – launch of Industry Task Force on Tri-party Repo

Reform Developed the conceptual roadmap for risk reduction Implemented changes that laid foundation for risk reduction

- Three way matching - Substitution mechanism - Delayed unwind

Prompted initial improvements in dealer liquidity risk management Greatly improved transparency of market But unable to implement and meet their own deadlines for the practical

elimination of intraday credit February 2012 - Task Force disbanded Final report with industry road map published FRBNY announced that it will use supervisory authority to implement

industry’s road map

5

Final Task Force vision for reform Non-maturing trades will not unwind before maturity Multiple points of settlement after 3:30 pm Repayment is rule-based; no lender has priority Automate/centralize collateral allocation, optimization Clearing banks lend only on capped, committed basis “Simultaneous” unwind/rewind of lender financing Integrate GCF repo settlement with TPR settlement

6

Phase 2: Fed Supervision Used roadmap as benchmark for supervision of market

participants Repeated and consistent communication with firms was

paired with public statements by senior policy makers Used supervisory authority to oversee the implementation of

industry roadmap across industry at the largest firms Clearing banks BHC affiliated broker dealers BHC affiliated cash investors

Worked with the SEC to extend our influence and communication to firms we do not directly supervise Independent broker dealers Asset managers

Leveraged data, research, and industry knowledge to focus resources on different issues at various stages of reform

7

Intraday credit usage has declined below 10%