Trend and Seasonality; Static 1 Ardavan Asef-Vaziri Chapter 7 Demand Forecasting in a Supply Chain...

20

Trend and Seasonality; Static 1 Ardavan Asef-Vaziri Chapter 7 Demand Forecasting in a Supply Chain Forecasting -3 Static Trend and Seasonality Ardavan Asef-Vaziri Based on Supply Chain Management Chopra and Meindl

-

date post

20-Dec-2015 -

Category

Documents

-

view

230 -

download

1

Transcript of Trend and Seasonality; Static 1 Ardavan Asef-Vaziri Chapter 7 Demand Forecasting in a Supply Chain...

Trend and Seasonality; Static1Ardavan Asef-Vaziri

Chapter 7Demand Forecastingin a Supply Chain

Forecasting -3Static Trend and Seasonality

Ardavan Asef-Vaziri

Based on Supply Chain ManagementChopra and Meindl

Trend and Seasonality; Static2Ardavan Asef-Vaziri

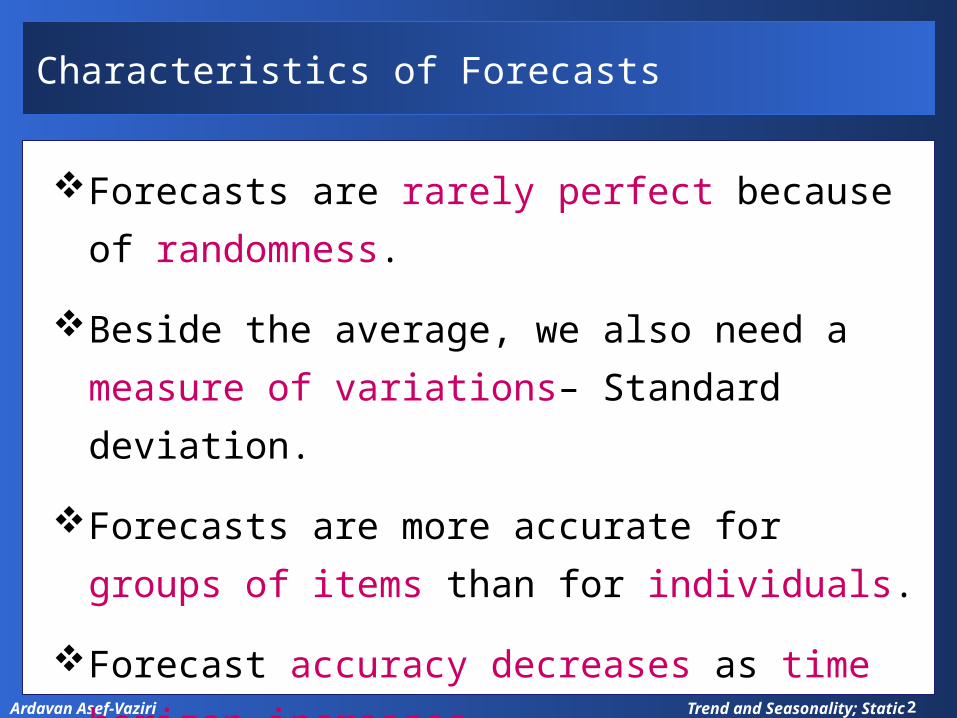

Characteristics of Forecasts

Forecasts are rarely perfect because of

randomness.

Beside the average, we also need a

measure of variations– Standard deviation.

Forecasts are more accurate for groups of

items than for individuals.

Forecast accuracy decreases as time

horizon increases.

Trend and Seasonality; Static3Ardavan Asef-Vaziri

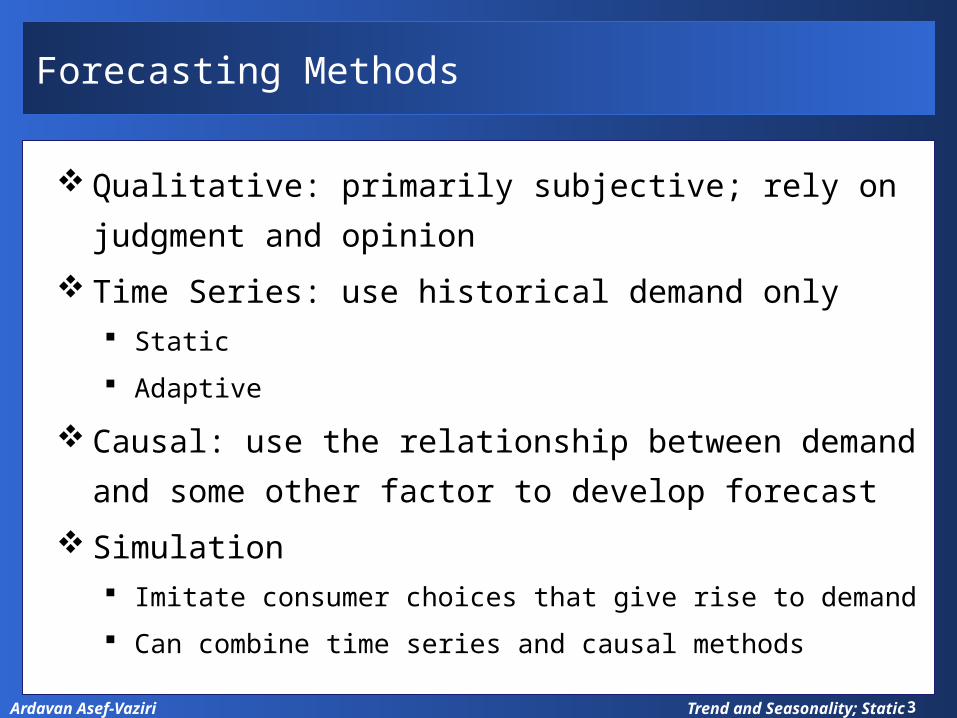

Forecasting Methods

Qualitative: primarily subjective; rely on judgment

and opinion

Time Series: use historical demand only Static

Adaptive

Causal: use the relationship between demand and

some other factor to develop forecast

Simulation Imitate consumer choices that give rise to demand

Can combine time series and causal methods

Trend and Seasonality; Static4Ardavan Asef-Vaziri

Components of an Observation

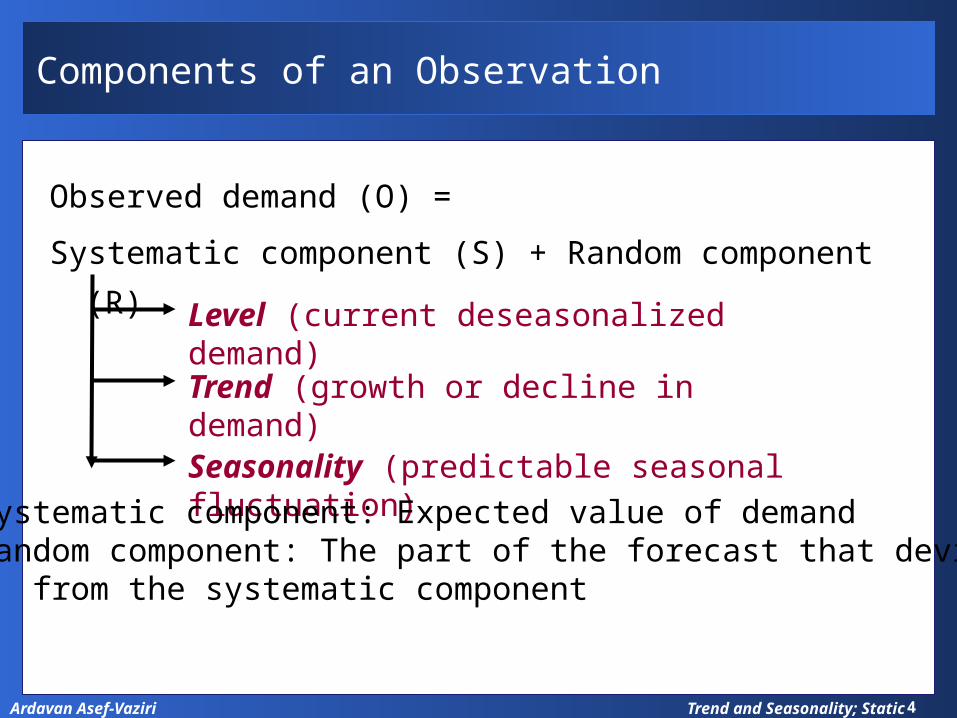

Observed demand (O) =

Systematic component (S) + Random component (R)

Level (current deseasonalized demand)

Trend (growth or decline in demand)

Seasonality (predictable seasonal fluctuation) Systematic component: Expected value of demand Random component: The part of the forecast that deviates

from the systematic component

Trend and Seasonality; Static5Ardavan Asef-Vaziri

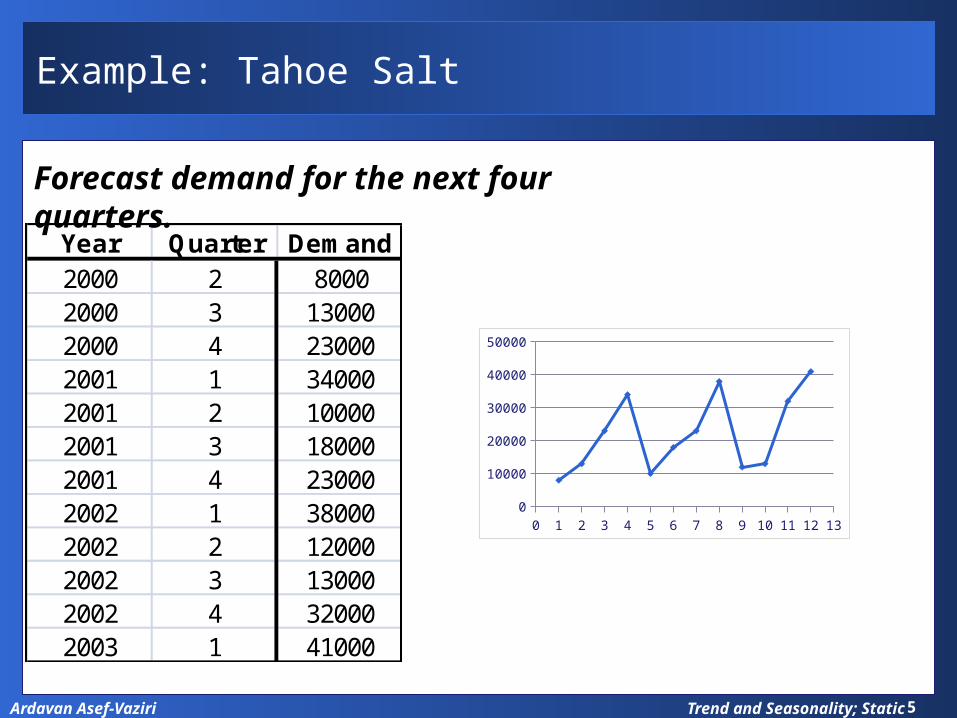

Example: Tahoe Salt

Year Quarter Demand2000 2 80002000 3 130002000 4 230002001 1 340002001 2 100002001 3 180002001 4 230002002 1 380002002 2 120002002 3 130002002 4 320002003 1 41000

Forecast demand for the next four quarters.

0 1 2 3 4 5 6 7 8 9 10 11 12 130

5000

10000

15000

20000

25000

30000

35000

40000

45000

Trend and Seasonality; Static6Ardavan Asef-Vaziri

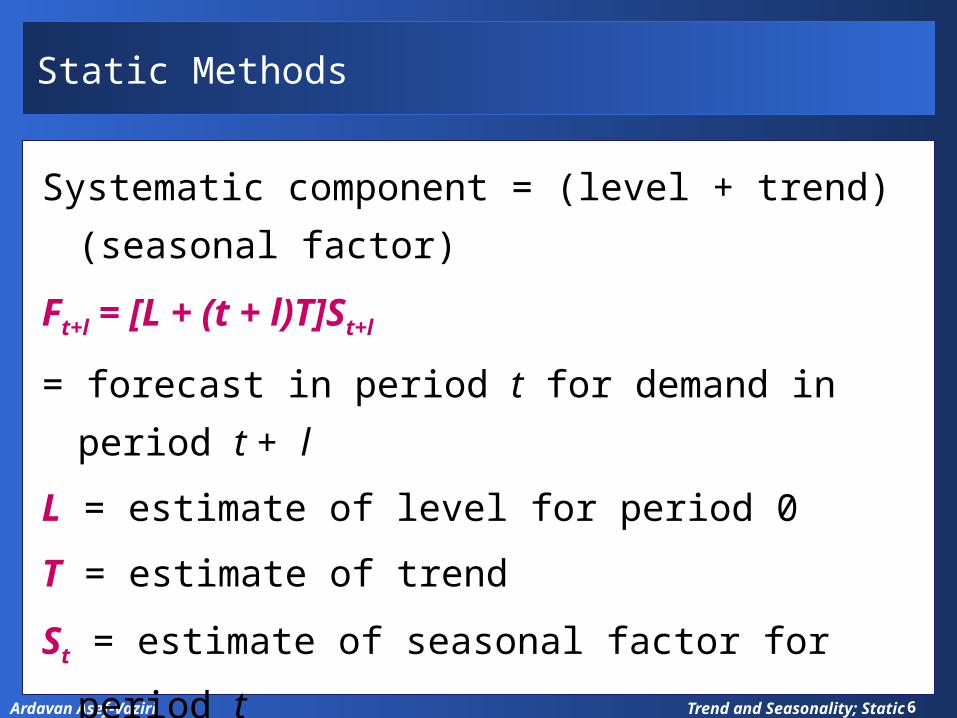

Static Methods

Systematic component = (level + trend)(seasonal factor)

Ft+l = [L + (t + l)T]St+l

= forecast in period t for demand in period t + l

L = estimate of level for period 0

T = estimate of trend

St = estimate of seasonal factor for period t

Dt = actual demand in period t

Ft = forecast of demand in period t

Trend and Seasonality; Static7Ardavan Asef-Vaziri

Static Methods

Estimating level and trend

Estimating seasonal factors

Trend and Seasonality; Static8Ardavan Asef-Vaziri

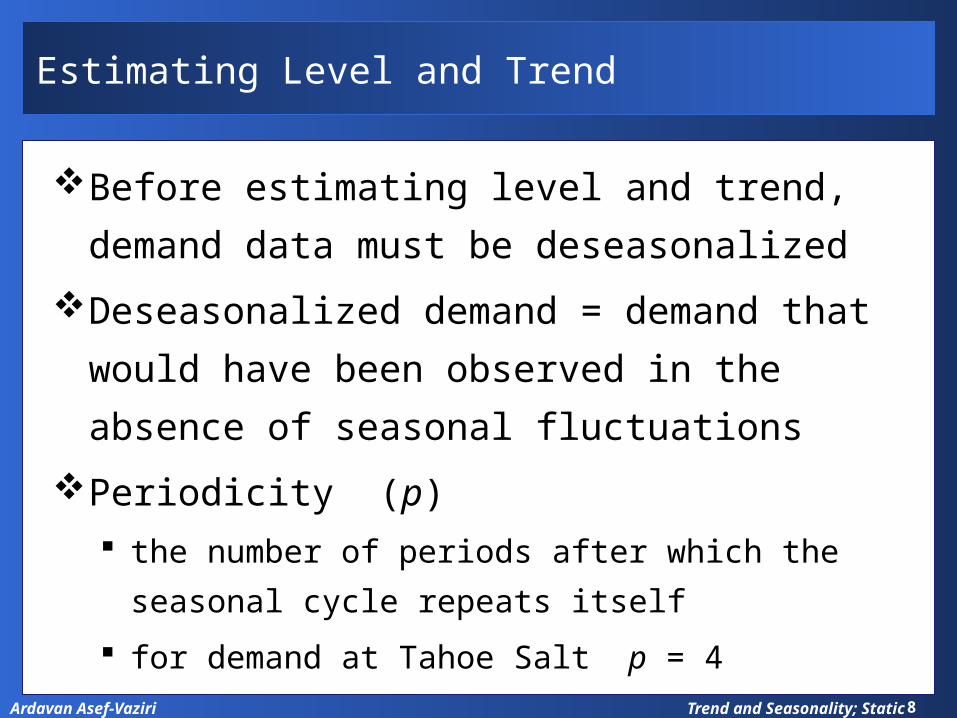

Estimating Level and Trend

Before estimating level and trend, demand

data must be deseasonalized

Deseasonalized demand = demand that

would have been observed in the absence

of seasonal fluctuations

Periodicity (p) the number of periods after which the seasonal

cycle repeats itself

for demand at Tahoe Salt p = 4

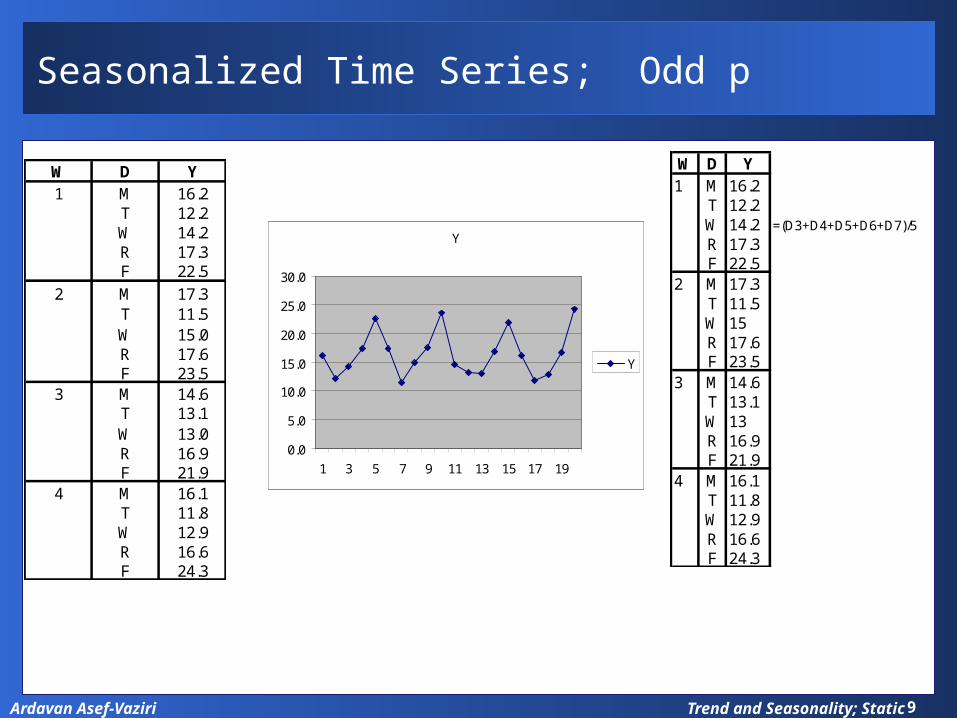

Trend and Seasonality; Static9Ardavan Asef-Vaziri

Seasonalized Time Series; Odd p

W D Y1 M 16.2

T 12.2W 14.2R 17.3F 22.5

2 M 17.3T 11.5W 15.0R 17.6F 23.5

3 M 14.6T 13.1W 13.0R 16.9F 21.9

4 M 16.1T 11.8W 12.9R 16.6F 24.3

Y

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1 3 5 7 9 11 13 15 17 19

Y

W D Y1 M 16.2

T 12.2W 14.2 =(D3+D4+D5+D6+D7)/5

R 17.3F 22.5

2 M 17.3T 11.5W 15R 17.6F 23.5

3 M 14.6T 13.1W 13R 16.9F 21.9

4 M 16.1T 11.8W 12.9R 16.6F 24.3

Trend and Seasonality; Static10Ardavan Asef-Vaziri

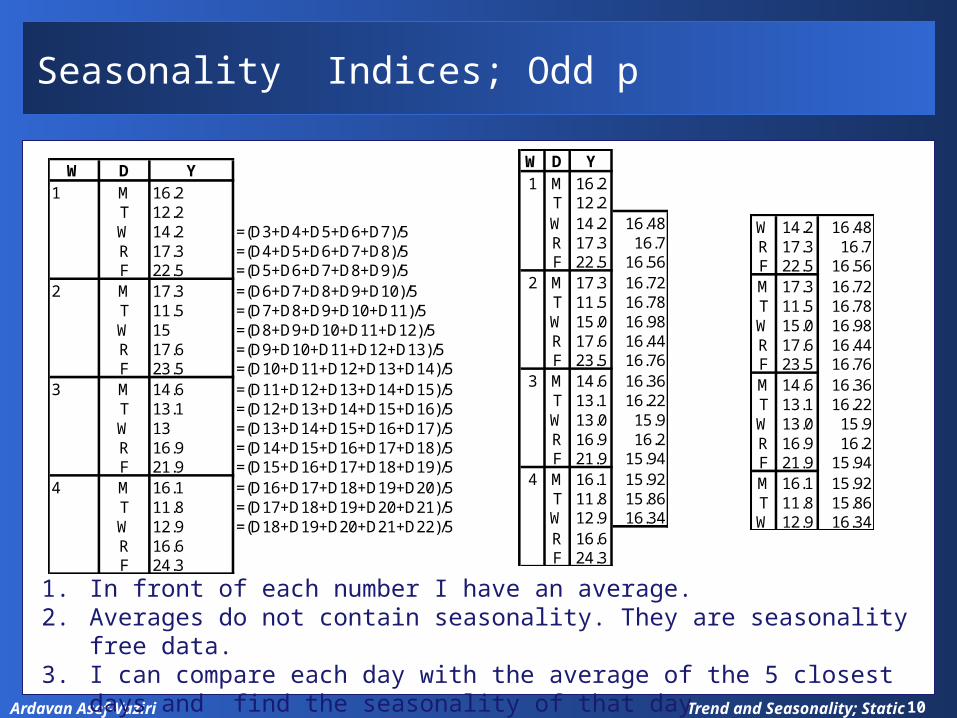

Seasonality Indices; Odd p

W D Y1 M 16.2

T 12.2W 14.2 =(D3+D4+D5+D6+D7)/5R 17.3 =(D4+D5+D6+D7+D8)/5F 22.5 =(D5+D6+D7+D8+D9)/5

2 M 17.3 =(D6+D7+D8+D9+D10)/5T 11.5 =(D7+D8+D9+D10+D11)/5W 15 =(D8+D9+D10+D11+D12)/5R 17.6 =(D9+D10+D11+D12+D13)/5F 23.5 =(D10+D11+D12+D13+D14)/5

3 M 14.6 =(D11+D12+D13+D14+D15)/5T 13.1 =(D12+D13+D14+D15+D16)/5W 13 =(D13+D14+D15+D16+D17)/5R 16.9 =(D14+D15+D16+D17+D18)/5F 21.9 =(D15+D16+D17+D18+D19)/5

4 M 16.1 =(D16+D17+D18+D19+D20)/5T 11.8 =(D17+D18+D19+D20+D21)/5W 12.9 =(D18+D19+D20+D21+D22)/5R 16.6F 24.3

W D Y1 M 16.2

T 12.2W 14.2 16.48R 17.3 16.7F 22.5 16.56

2 M 17.3 16.72T 11.5 16.78W 15.0 16.98R 17.6 16.44F 23.5 16.76

3 M 14.6 16.36T 13.1 16.22W 13.0 15.9R 16.9 16.2F 21.9 15.94

4 M 16.1 15.92T 11.8 15.86W 12.9 16.34R 16.6F 24.3

W 14.2 16.48R 17.3 16.7F 22.5 16.56M 17.3 16.72T 11.5 16.78W 15.0 16.98R 17.6 16.44F 23.5 16.76M 14.6 16.36T 13.1 16.22W 13.0 15.9R 16.9 16.2F 21.9 15.94M 16.1 15.92T 11.8 15.86W 12.9 16.34

1. In front of each number I have an average.2. Averages do not contain seasonality. They are seasonality free data. 3. I can compare each day with the average of the 5 closest days and find the

seasonality of that day

Trend and Seasonality; Static11Ardavan Asef-Vaziri

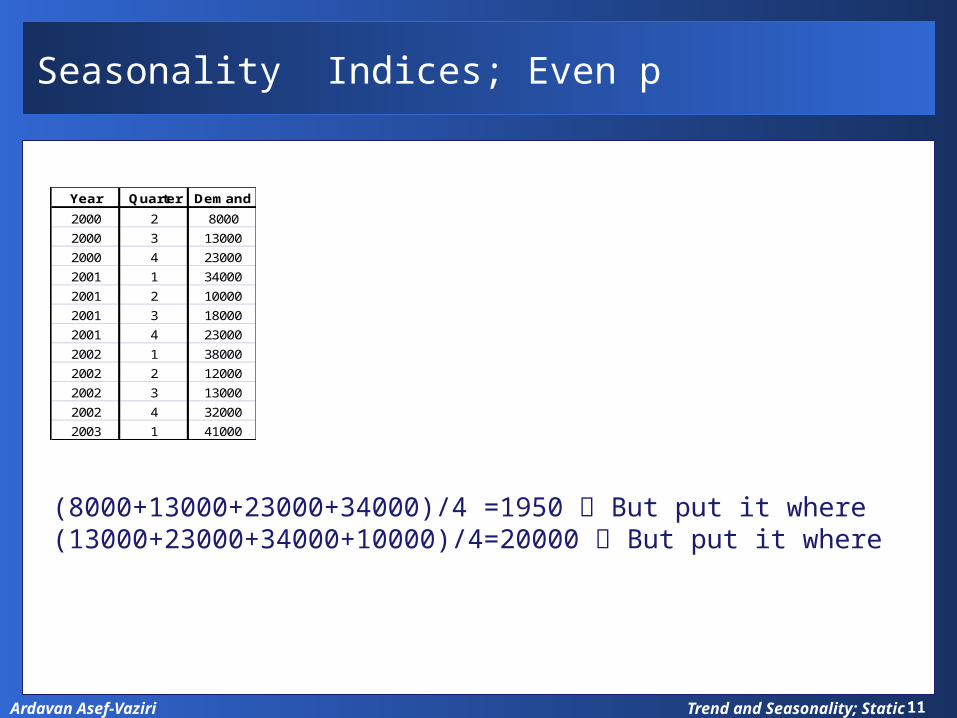

Seasonality Indices; Even p

(8000+13000+23000+34000)/4 =1950 But put it where(13000+23000+34000+10000)/4=20000 But put it where

Year Quarter Demand

2000 2 8000

2000 3 13000

2000 4 23000

2001 1 34000

2001 2 10000

2001 3 18000

2001 4 23000

2002 1 38000

2002 2 12000

2002 3 13000

2002 4 32000

2003 1 41000

Trend and Seasonality; Static12Ardavan Asef-Vaziri

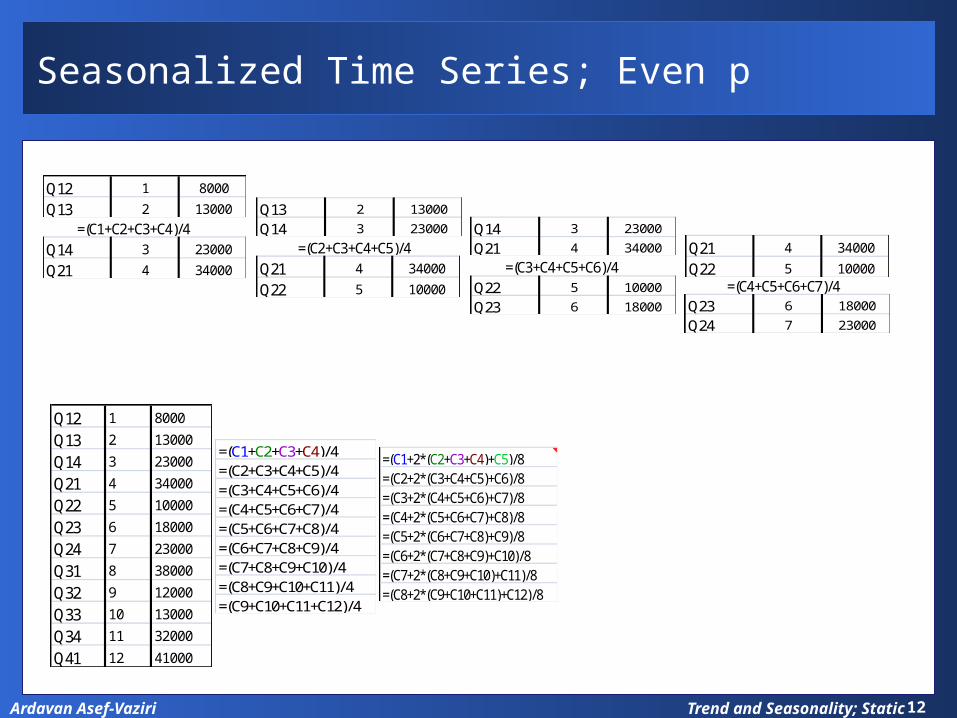

Seasonalized Time Series; Even p

Q12 1 8000

Q13 2 13000

Q14 3 23000

Q21 4 34000

Q13 2 13000

Q14 3 23000

Q21 4 34000

Q22 5 10000

Q14 3 23000

Q21 4 34000

Q22 5 10000

Q23 6 18000

Q21 4 34000

Q22 5 10000

Q23 6 18000

Q24 7 23000

=(C1+C2+C3+C4)/4=(C2+C3+C4+C5)/4

=(C3+C4+C5+C6)/4=(C4+C5+C6+C7)/4

Q12 1 8000

Q13 2 13000

Q14 3 23000

Q21 4 34000

Q22 5 10000

Q23 6 18000

Q24 7 23000

Q31 8 38000

Q32 9 12000

Q33 10 13000

Q34 11 32000

Q41 12 41000

=(C1+C2+C3+C4)/4=(C2+C3+C4+C5)/4=(C3+C4+C5+C6)/4=(C4+C5+C6+C7)/4=(C5+C6+C7+C8)/4=(C6+C7+C8+C9)/4=(C7+C8+C9+C10)/4=(C8+C9+C10+C11)/4=(C9+C10+C11+C12)/4

=(C1+2*(C2+C3+C4)+C5)/8=(C2+2*(C3+C4+C5)+C6)/8=(C3+2*(C4+C5+C6)+C7)/8=(C4+2*(C5+C6+C7)+C8)/8=(C5+2*(C6+C7+C8)+C9)/8=(C6+2*(C7+C8+C9)+C10)/8=(C7+2*(C8+C9+C10)+C11)/8=(C8+2*(C9+C10+C11)+C12)/8

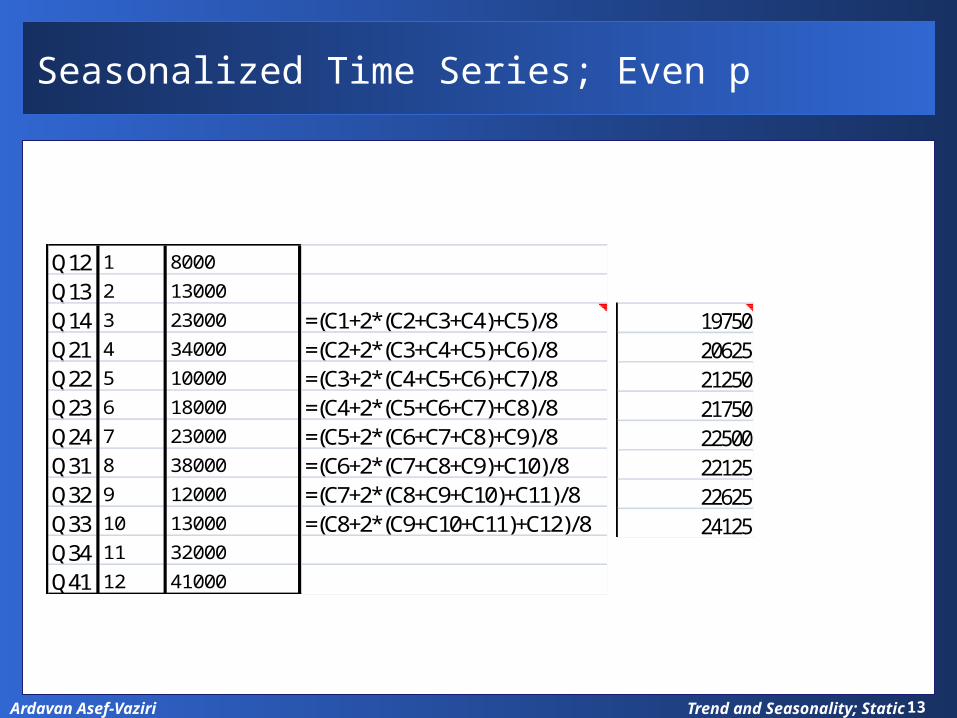

Trend and Seasonality; Static13Ardavan Asef-Vaziri

Seasonalized Time Series; Even p

Q12 1 8000

Q13 2 13000

Q14 3 23000 =(C1+2*(C2+C3+C4)+C5)/8Q21 4 34000 =(C2+2*(C3+C4+C5)+C6)/8Q22 5 10000 =(C3+2*(C4+C5+C6)+C7)/8Q23 6 18000 =(C4+2*(C5+C6+C7)+C8)/8Q24 7 23000 =(C5+2*(C6+C7+C8)+C9)/8Q31 8 38000 =(C6+2*(C7+C8+C9)+C10)/8Q32 9 12000 =(C7+2*(C8+C9+C10)+C11)/8Q33 10 13000 =(C8+2*(C9+C10+C11)+C12)/8Q34 11 32000

Q41 12 41000

1975020625212502175022500221252262524125

Trend and Seasonality; Static14Ardavan Asef-Vaziri

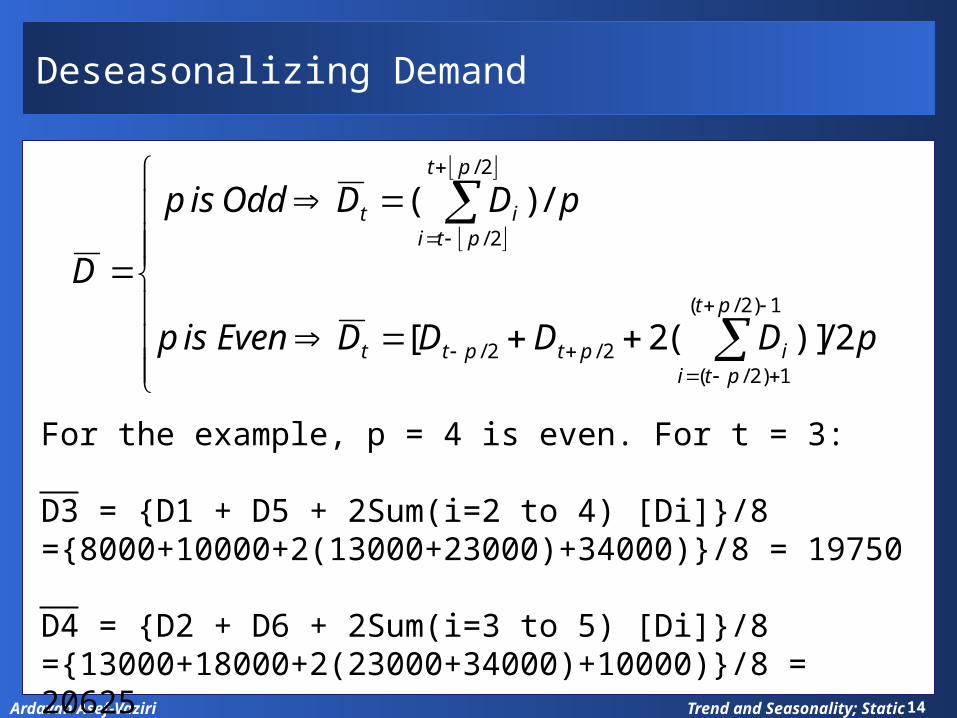

Deseasonalizing Demand

pDDDDEvenisp

pDDOddisp

Dpt

ptiiptptt

pt

ptiit

2/)](2[

/)(

1)2/(

1)2/(2/2/

2/

2/

For the example, p = 4 is even. For t = 3:

D3 = {D1 + D5 + 2Sum(i=2 to 4) [Di]}/8={8000+10000+2(13000+23000)+34000)}/8 = 19750

D4 = {D2 + D6 + 2Sum(i=3 to 5) [Di]}/8={13000+18000+2(23000+34000)+10000)}/8 = 20625

Trend and Seasonality; Static15Ardavan Asef-Vaziri

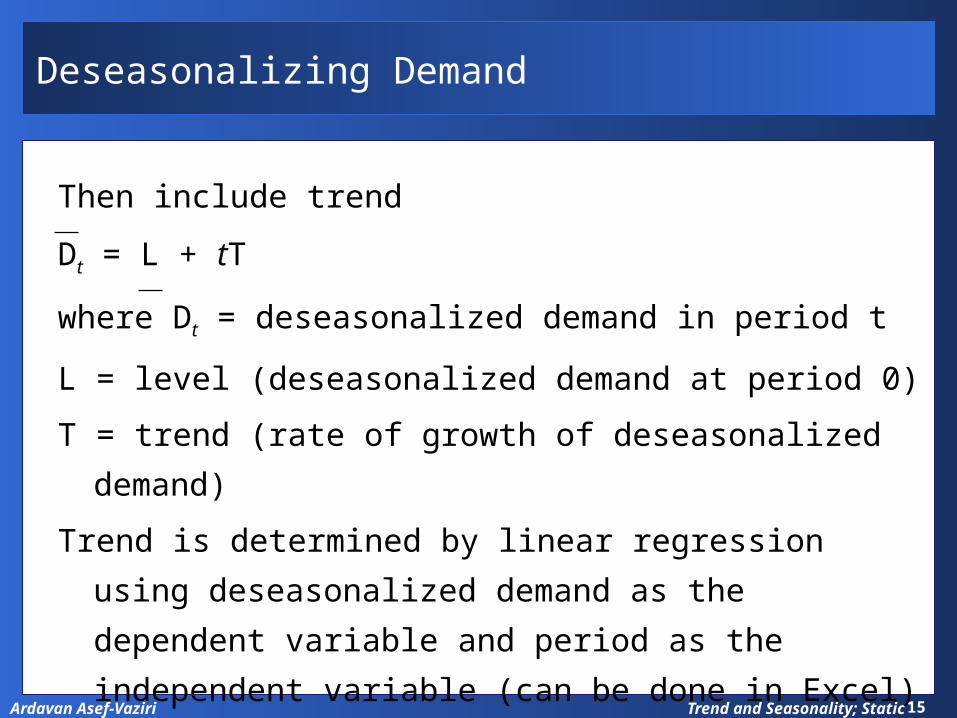

Deseasonalizing Demand

Then include trend

Dt = L + tT

where Dt = deseasonalized demand in period t

L = level (deseasonalized demand at period 0)

T = trend (rate of growth of deseasonalized demand)

Trend is determined by linear regression using deseasonalized

demand as the dependent variable and period as the independent

variable (can be done in Excel)

Trend and Seasonality; Static16Ardavan Asef-Vaziri

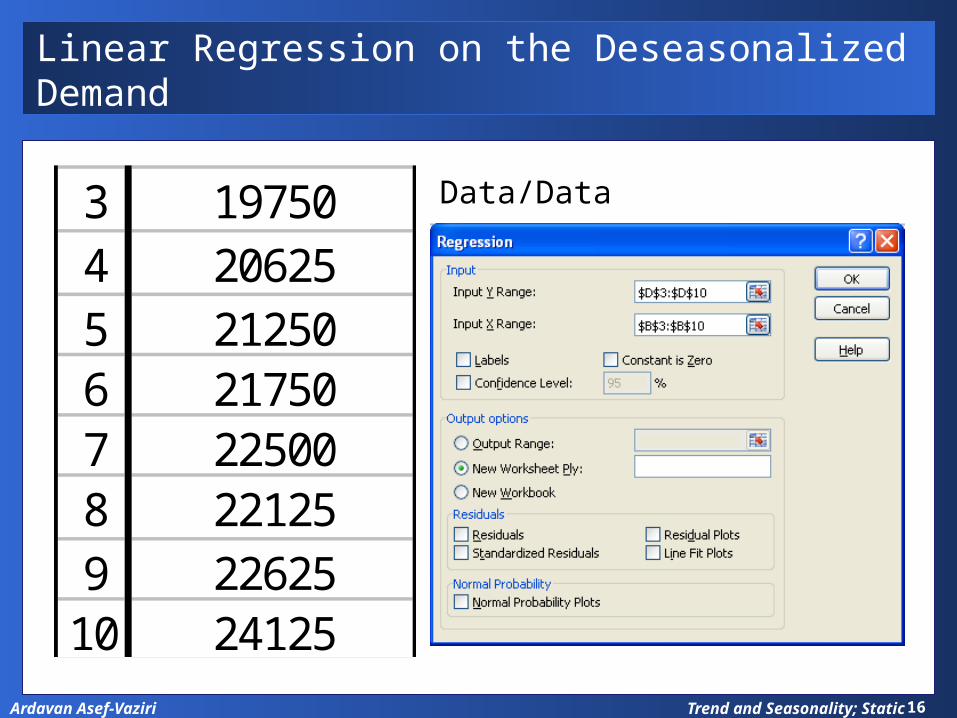

Linear Regression on the Deseasonalized Demand

3 197504 206255 212506 217507 225008 221259 22625

10 24125

Data/Data Analysis/Regression

Trend and Seasonality; Static17Ardavan Asef-Vaziri

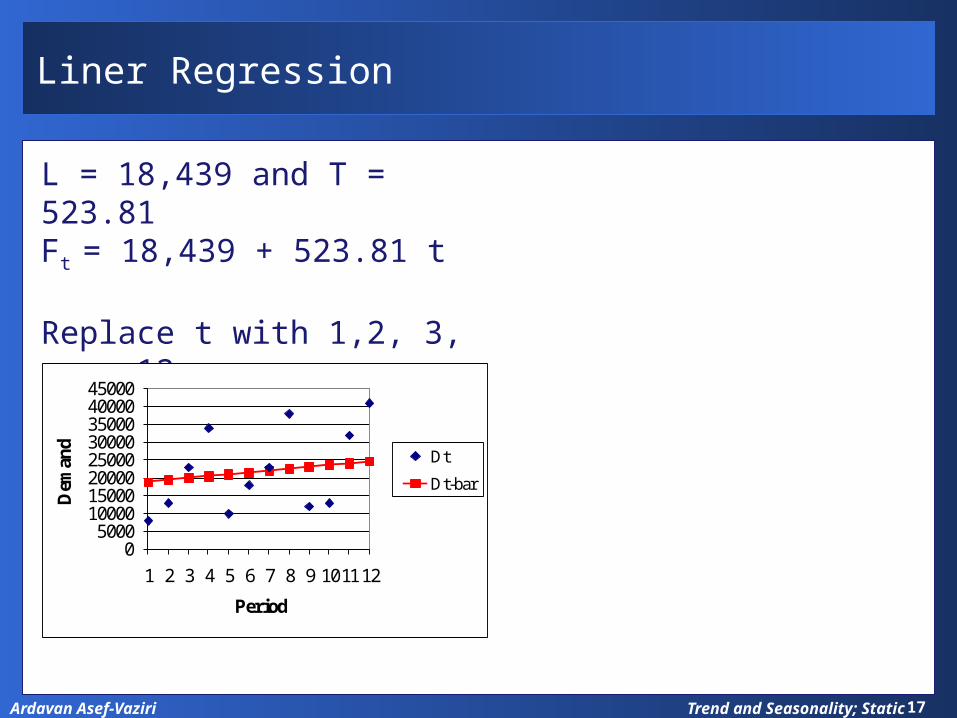

Liner Regression

L = 18,439 and T = 523.81Ft = 18,439 + 523.81 t

Replace t with 1,2, 3, ….., 12

05000

1000015000200002500030000350004000045000

1 2 3 4 5 6 7 8 9 1011 12

Demand

Period

Dt

Dt-bar

Trend and Seasonality; Static18Ardavan Asef-Vaziri

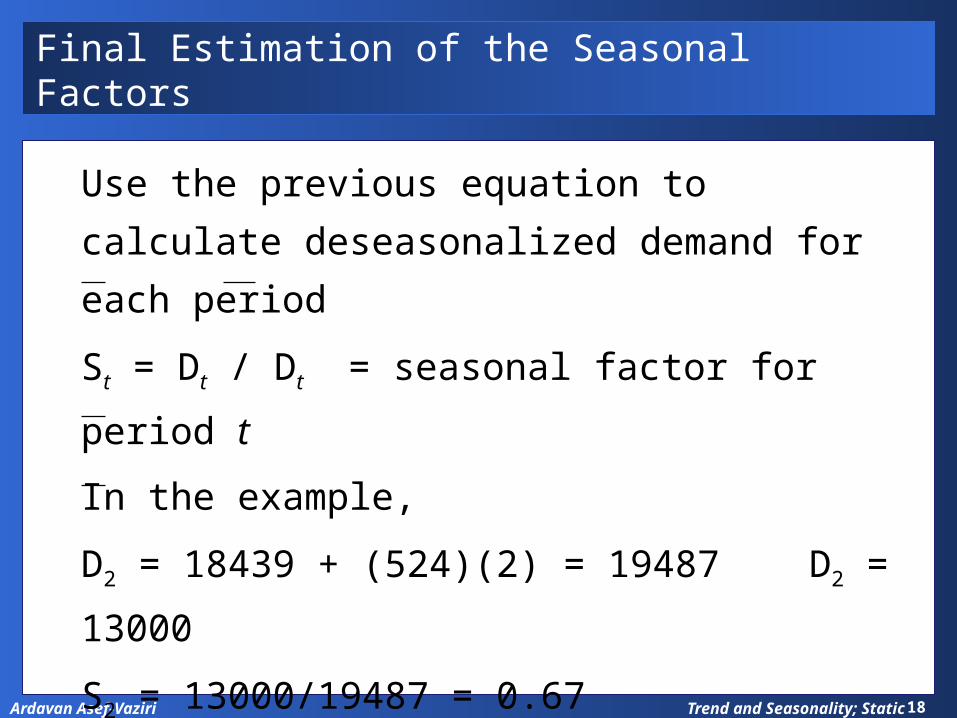

Final Estimation of the Seasonal Factors

Use the previous equation to calculate

deseasonalized demand for each period

St = Dt / Dt = seasonal factor for period t

In the example,

D2 = 18439 + (524)(2) = 19487 D2 =

13000

S2 = 13000/19487 = 0.67

The seasonal factors for the other periods

are calculated in the same manner

Trend and Seasonality; Static19Ardavan Asef-Vaziri

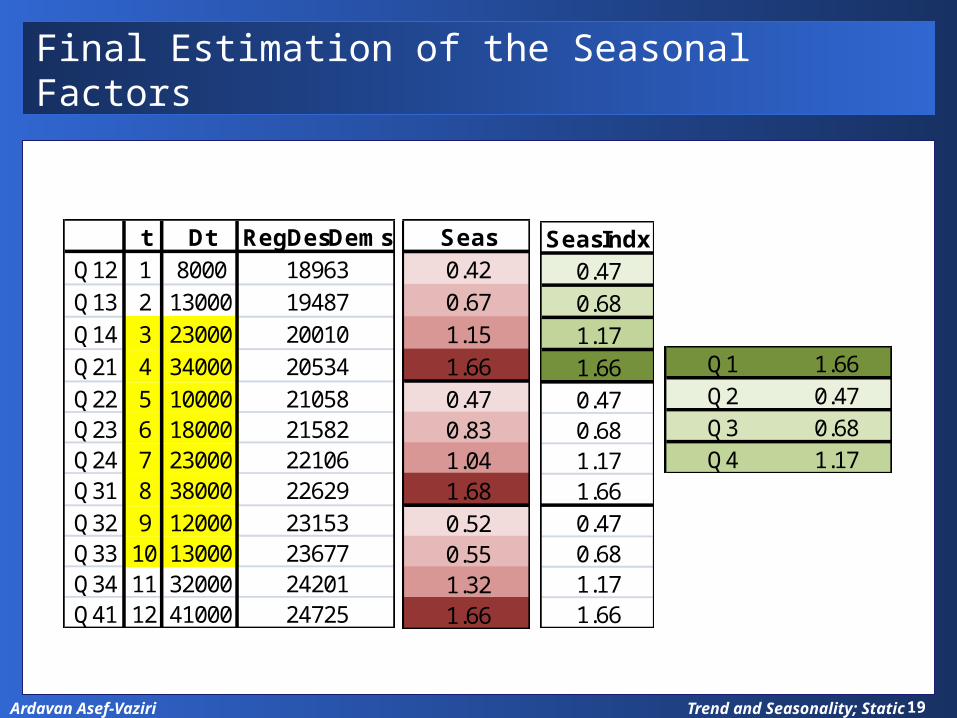

Final Estimation of the Seasonal Factors

t Dt RegDesDemsQ12 1 8000 18963Q13 2 13000 19487Q14 3 23000 20010Q21 4 34000 20534Q22 5 10000 21058Q23 6 18000 21582Q24 7 23000 22106Q31 8 38000 22629Q32 9 12000 23153Q33 10 13000 23677Q34 11 32000 24201Q41 12 41000 24725

Seas0.420.671.151.660.470.831.041.680.520.551.321.66

SeasIndx0.470.681.171.660.470.681.171.660.470.681.171.66

Q1 1.66Q2 0.47Q3 0.68Q4 1.17

Trend and Seasonality; Static20Ardavan Asef-Vaziri

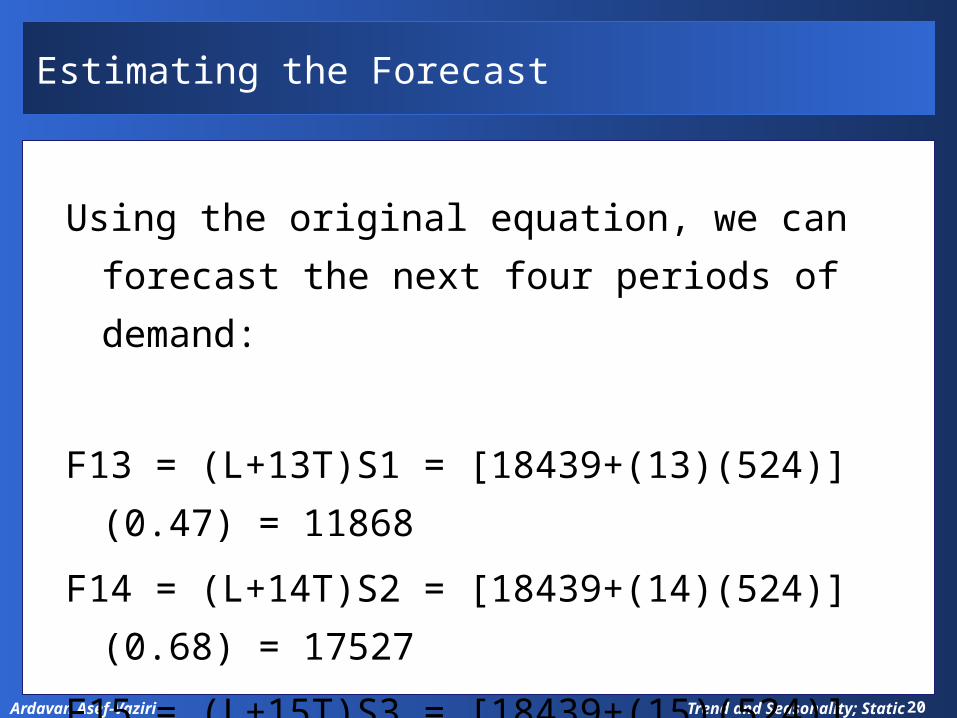

Estimating the Forecast

Using the original equation, we can forecast the next

four periods of demand:

F13 = (L+13T)S1 = [18439+(13)(524)](0.47) = 11868

F14 = (L+14T)S2 = [18439+(14)(524)](0.68) = 17527

F15 = (L+15T)S3 = [18439+(15)(524)](1.17) = 30770

F16 = (L+16T)S4 = [18439+(16)(524)](1.67) = 44794