Treasurer's Guidebook Text - CPE Store · Chapter 6 – Investment Management ... Split Limits...

261

Treasurer’s Guidebook CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 Steven M. Bragg

Transcript of Treasurer's Guidebook Text - CPE Store · Chapter 6 – Investment Management ... Split Limits...

Treasurer’sGuidebook

CPE EditionDistributed by The CPE Store

www.cpestore.com1-800-910-2755

Steven M. Bragg

Treasurer’s Guidebook

Steven M. Bragg

Copyright 2015 © by AccountingTools LLC. All rights reserved. Course and chapter learning objectives copyright © The CPE Store, Inc. Published and distributed by The CPE Store, Inc. www.cpestore.com No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the Publisher. Requests to the Publisher for permission should be addressed to Steven M. Bragg, 6727 E. Fremont Place, Centennial, CO 80112. Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifically disclaim any implied warranties of merchantability or fitness for a particular purpose. No warranty may be created or extended by written sales materials. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional where appropriate. Neither the publisher nor author shall be liable for any loss of profit or any other commercial damages, including but not limited to special, incidental, consequential, or other damages. Printed in the United States of America

Course Information Course Title: Treasurer’s Guidebook Learning Objectives:

Identify the aspect of a business for which the treasury function is responsible Determine which part of the treasury department executes transactions Recognize how to improve the layout of the treasury department Spot an example of a periodic bank fee Pinpoint a special event that could trigger a credit assembly by a bank Select the definition for a threshold cash sweep Choose an advantage of notional pooling Ascertain why a company might use multi-tiered banking Pinpoint aspects of the receipt and disbursements method Identify which cash forecast information is considered highly reliable Determine the purpose of a cash forecast reconciliation Recognize the function of a correspondent bank Select the definition of an on-us check Ascertain how the Continuous Linked Settlement system is used Identify a true statement regarding the laddering strategy Determine how interest rates are affected by inverted yield curves Ascertain why commercial paper has a short maturity Discern when the Regulation A exemption can and cannot be used Recognize what a solicitation of interest under Regulation A must include Pinpoint the topic of the questions typically included on the questionnaire sent to accredited

investors Identify the components of the pricing arrangement for a factoring deal Determine what is typically included in the terms of a hard money loan Recognize when a supplier is more likely to take advantage of a supply chain financing offer Spot an example of an operational hedge Ascertain how payment netting is used Determine why a call option might be used by the owner Discern what a claims-made policy provides coverage for Identify a key advantage of using credit insurance Spot the essential difference between whole life and term life Determine what happens to a company’s credit policy when the company has low product

margins Recognize documents collected as part of a credit review Ascertain when an internal credit rating system functions best Spot a business characteristic that can lead to the achievement of zero working capital Pinpoint the key issue that shifts a transaction from other comprehensive income to earnings Identify the main type of hedging classifications Determine the net result of a fully effective fair value hedge Spot a customization cost associated with a treasury management system revise the construction of the cash forecast spreadsheet Ascertain when actual funds transfers should be reconciled Discern why a restrictive legend is added to stock certificates Calculate days sales in accounts receivable

Determine what is included in the calculation of earnings on invested funds Spot a measure of the ability to pay concept

Subject Area: Finance Prerequisites: None Program Level: Overview Program Content: This course discusses how the treasury department’s performance can be organized and fine-tuned, focusing on bank relations, cash concentration systems, investment strategies, financing sources, credit management, insurance, and more. The course also addresses the administrative aspects of the treasurer’s job, including the accounting for treasury transactions, treasury management systems, controls, and measurements. Advance Preparation: None Recommended CPE Credit: 16 hours

Table of Contents Chapter 1 – Treasury Management ....................................................................................................... 1

Learning Objectives ............................................................................................................................. 1 Introduction .......................................................................................................................................... 1 Treasury Responsibilities ..................................................................................................................... 1 Treasurer Job Description .................................................................................................................... 1 Treasury Organizational Structure ........................................................................................................ 3 Treasury Centralization ........................................................................................................................ 4 Treasury Outsourcing ........................................................................................................................... 6 The Performance Culture ..................................................................................................................... 6 Schedule of Activities ........................................................................................................................... 7 Process Reviews ................................................................................................................................. 7 Department Layout............................................................................................................................... 8 Skills Review and Training ................................................................................................................... 9 Chapter Summary ................................................................................................................................ 9 Review Questions .............................................................................................................................. 10 Review Answers ................................................................................................................................ 11

Chapter 2 – Bank Relations ................................................................................................................. 13

Learning Objectives ........................................................................................................................... 13 Introduction ........................................................................................................................................ 13 Bank Centralization ............................................................................................................................ 13 Banker Dialog .................................................................................................................................... 13 Frequency of Reporting ...................................................................................................................... 14 Bank Fees ......................................................................................................................................... 14 Loan Covenants ................................................................................................................................. 15 Collateral ........................................................................................................................................... 15 Account Signers ................................................................................................................................. 15 Credit Assessment ............................................................................................................................. 16 Causes for Change ............................................................................................................................ 16 Chapter Summary .............................................................................................................................. 17 Review Questions .............................................................................................................................. 18 Review Answers ................................................................................................................................ 19

Chapter 3 – Cash Concentration ......................................................................................................... 21

Learning Objectives ........................................................................................................................... 21 Introduction ........................................................................................................................................ 21 The Need for Cash Concentration ...................................................................................................... 21 Cash Sweeping .................................................................................................................................. 22

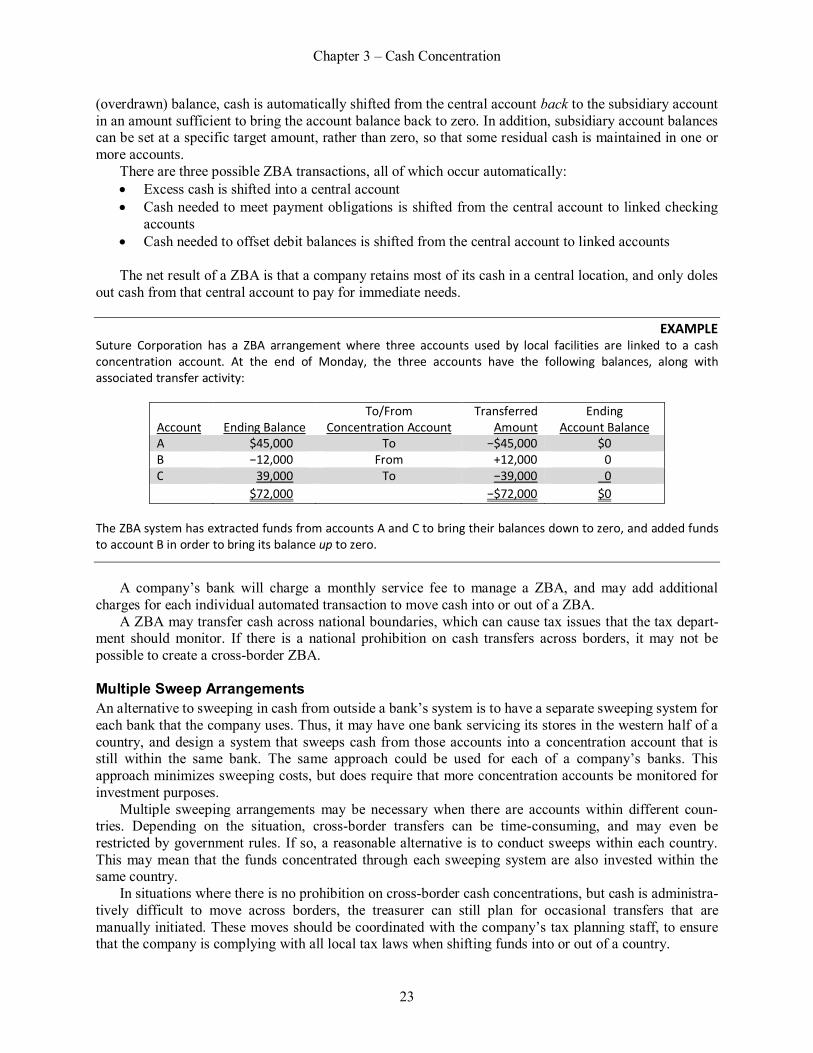

The Zero Balance Account ............................................................................................................. 22 Multiple Sweep Arrangements ........................................................................................................ 23 Manual Sweeping ........................................................................................................................... 24 Sweeping Rules ............................................................................................................................. 24 Sweep Problems ............................................................................................................................ 24 Sweep Costs .................................................................................................................................. 25 Section Summary ........................................................................................................................... 26

Notional Pooling ................................................................................................................................. 26 Notional Pooling Problems .............................................................................................................. 26 Notional Pooling Costs ................................................................................................................... 27 Section Summary ........................................................................................................................... 27

Multi-Tiered Banking .......................................................................................................................... 27 Hybrid Pooling Solutions .................................................................................................................... 27 Cash Concentration Best Practices .................................................................................................... 28 Cash Concentration Alternatives ........................................................................................................ 28 Chapter Summary .............................................................................................................................. 29

Table of Contents

ii

Review Questions .............................................................................................................................. 31 Review Answers ................................................................................................................................ 32

Chapter 4 – Cash Forecasting............................................................................................................. 33

Learning Objectives ........................................................................................................................... 33 Introduction ........................................................................................................................................ 33 The Cash Forecast............................................................................................................................. 33

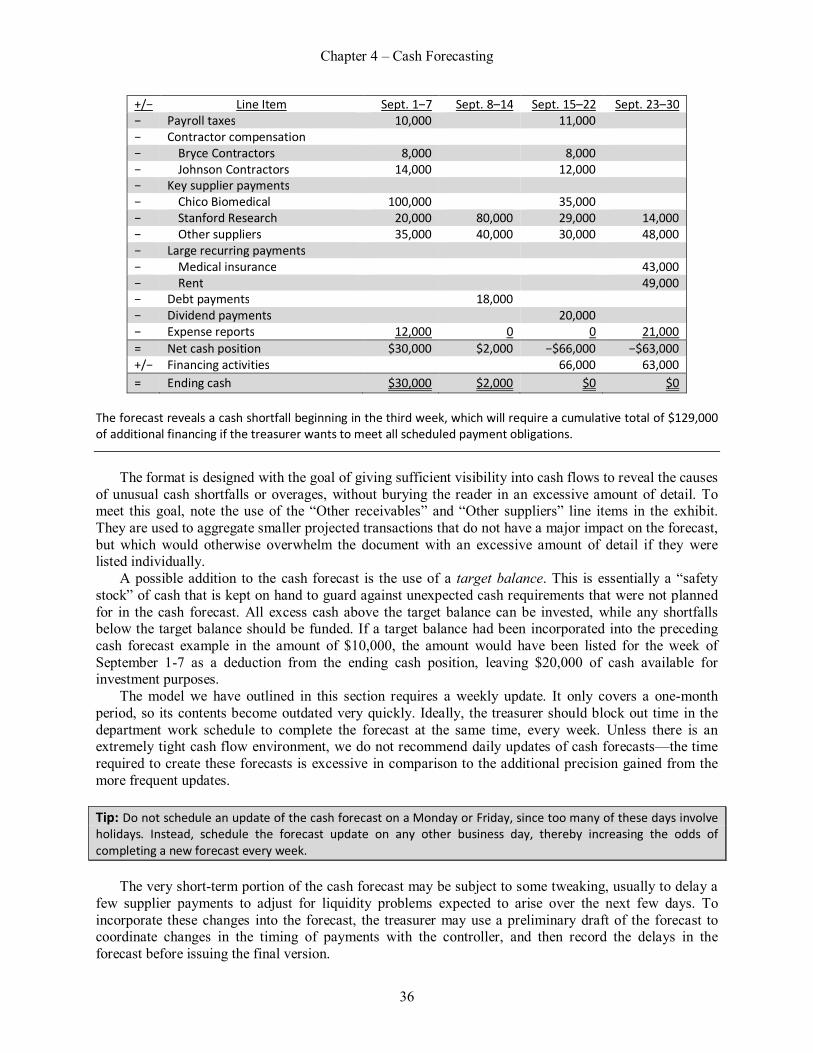

The Short-Term Cash Forecast....................................................................................................... 34 The Medium-Term Cash Forecast .................................................................................................. 37 The Long-Term Cash Forecast ....................................................................................................... 37 The Use of Averages ...................................................................................................................... 38

Automated Cash Forecasting ............................................................................................................. 38 The Reliability of Cash Flow Information ............................................................................................. 39 The Impact of Special Events ............................................................................................................. 40 Cash Forecasting Documentation....................................................................................................... 41 The Foreign Currency Cash Forecast ................................................................................................. 41 Cash Forecast Reconciliation ............................................................................................................. 41 Chapter Summary .............................................................................................................................. 42 Review Questions .............................................................................................................................. 43 Review Answers ................................................................................................................................ 44

Chapter 5 – Clearing and Settlement Systems ................................................................................... 45

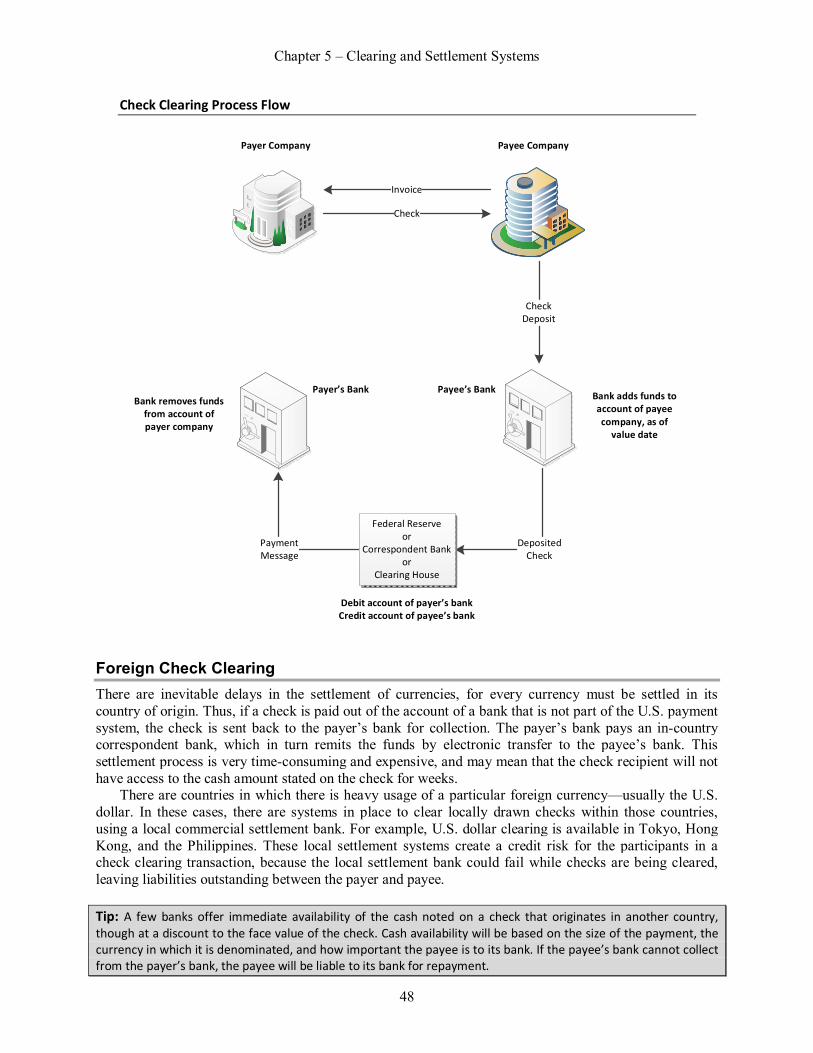

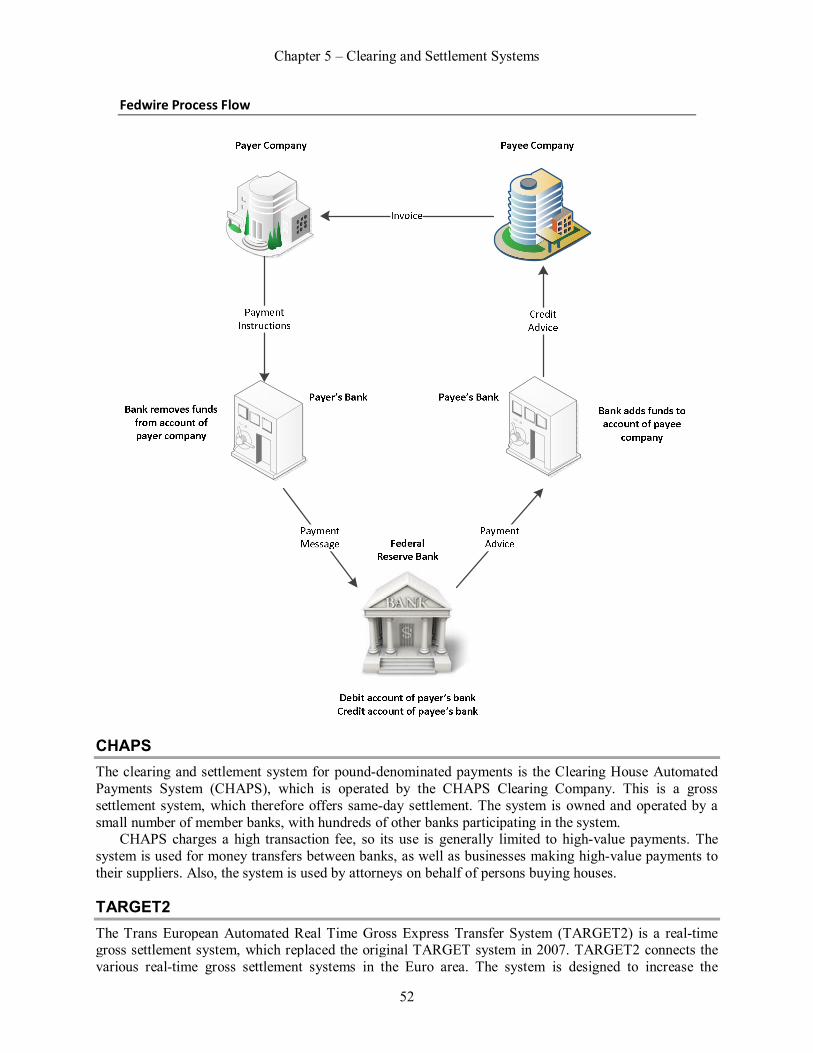

Learning Objectives ........................................................................................................................... 45 Introduction ........................................................................................................................................ 45 The Clearing and Settlement Process ................................................................................................ 45 Correspondent Banks ........................................................................................................................ 46 Check Clearing .................................................................................................................................. 46 Foreign Check Clearing...................................................................................................................... 48 The Automated Clearing House System (ACH) .................................................................................. 49 CHIPS ............................................................................................................................................... 50 Fedwire .............................................................................................................................................. 51 CHAPS .............................................................................................................................................. 52 TARGET2 .......................................................................................................................................... 52 Continuous Linked Settlement ............................................................................................................ 53 SWIFT ............................................................................................................................................... 53 Chapter Summary .............................................................................................................................. 55 Review Questions .............................................................................................................................. 56 Review Answers ................................................................................................................................ 57

Chapter 6 – Investment Management ................................................................................................. 59

Learning Objectives ........................................................................................................................... 59 Introduction ........................................................................................................................................ 59 Investment Guidelines ........................................................................................................................ 59 Cash Availability Scenarios ................................................................................................................ 61 Investment Strategy ........................................................................................................................... 62 Types of Investments ......................................................................................................................... 64

Repurchase Agreements ................................................................................................................ 64 Time Deposits ................................................................................................................................ 64 Certificates of Deposit..................................................................................................................... 64 Bankers’ Acceptances .................................................................................................................... 65 Commercial Paper .......................................................................................................................... 65 Money Market Funds ...................................................................................................................... 65 U.S. Government Debt Instruments ................................................................................................ 65 State and Local Government Debt .................................................................................................. 66 Bonds ............................................................................................................................................. 66

The Primary and Secondary Markets.................................................................................................. 67 The Discounted Investment Formula .................................................................................................. 67

Table of Contents

iii

Chapter Summary .............................................................................................................................. 67 Review Questions .............................................................................................................................. 68 Review Answers ................................................................................................................................ 69

Chapter 7 – Equity Financing .............................................................................................................. 71

Learning Objectives ........................................................................................................................... 71 Introduction ........................................................................................................................................ 71 Regulation A Stock Sales ................................................................................................................... 71

Solicitations of Interest .................................................................................................................... 72 Forms 1-A and 2-A ......................................................................................................................... 72

Regulation D Stock Sales ................................................................................................................... 74 Regulation D Rules ......................................................................................................................... 74 Regulation D Process Flow ............................................................................................................. 74 The Form D Filing ........................................................................................................................... 76

The Accredited Investor ..................................................................................................................... 77 Private Investments in Public Equity ................................................................................................... 77 Seasoned Equity Offerings ................................................................................................................. 78 The Rights Offering ............................................................................................................................ 78 Dilution .............................................................................................................................................. 79 Chapter Summary .............................................................................................................................. 80 Review Questions .............................................................................................................................. 81 Review Answers ................................................................................................................................ 82

Chapter 8 – Debt Financing ................................................................................................................. 83

Learning Objectives ........................................................................................................................... 83 Introduction ........................................................................................................................................ 83 Overview of Debt Financing ............................................................................................................... 83 The Line of Credit .............................................................................................................................. 83 The Borrowing Base ........................................................................................................................... 84 Invoice Discounting ............................................................................................................................ 85 Factoring............................................................................................................................................ 86 Receivables Securitization ................................................................................................................. 86 Inventory Financing ............................................................................................................................ 87 Loan Stock ......................................................................................................................................... 87 Purchase Order Financing.................................................................................................................. 88 Hard Money Loans ............................................................................................................................. 88 Mezzanine Financing ......................................................................................................................... 88 The Long-Term Loan ......................................................................................................................... 89 Bonds ................................................................................................................................................ 90 Debt for Equity Swaps ........................................................................................................................ 91 Chapter Summary .............................................................................................................................. 91 Review Questions .............................................................................................................................. 92 Review Answers ................................................................................................................................ 93

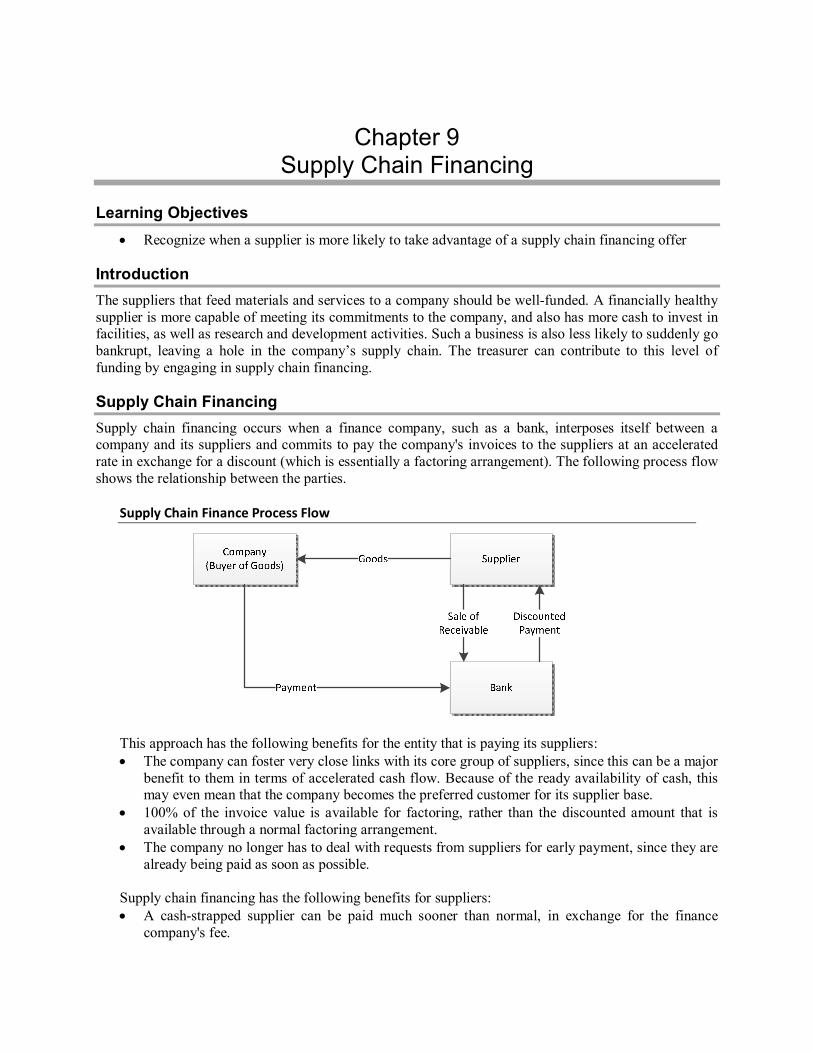

Chapter 9 – Supply Chain Financing .................................................................................................. 95

Learning Objectives ........................................................................................................................... 95 Introduction ........................................................................................................................................ 95 Supply Chain Financing ..................................................................................................................... 95 Early Payment Discounts ................................................................................................................... 96 Chapter Summary .............................................................................................................................. 97 Review Questions .............................................................................................................................. 98 Review Answers ................................................................................................................................ 99

Chapter 10 – Treasury Risk Management ......................................................................................... 101

Learning Objectives ......................................................................................................................... 101 Introduction ...................................................................................................................................... 101 Benefits of Risk Management ........................................................................................................... 101

Table of Contents

iv

Funding Risk .................................................................................................................................... 102 Credit Policy Risk ............................................................................................................................. 103 Credit Exposure Risk ....................................................................................................................... 103

Terms Alterations ......................................................................................................................... 103 Receivables Financing .................................................................................................................. 103 Outside Financing......................................................................................................................... 104 Portfolio Approach to Risk ............................................................................................................ 104

Cross-Selling Credit Exposure Risk .................................................................................................. 105 Credit Concentration Risk ................................................................................................................ 105 Foreign Exchange Risk Overview ..................................................................................................... 105 Foreign Exchange Risk Management ............................................................................................... 106

Take No Action ............................................................................................................................. 107 Avoid Risk .................................................................................................................................... 107 Shift Risk ...................................................................................................................................... 107 Time Compression ....................................................................................................................... 108 Payment Leading and Lagging ..................................................................................................... 108 Build Reserves ............................................................................................................................. 108 Maintain Local Reserves............................................................................................................... 109 Hedging ........................................................................................................................................ 109 Section Summary ......................................................................................................................... 110

Types of Foreign Exchange Hedges ................................................................................................. 110 Loan Denominated in a Foreign Currency ..................................................................................... 110 The Forward Contract ................................................................................................................... 110 The Futures Contract .................................................................................................................... 111 The Currency Option .................................................................................................................... 112 The Cylinder Option ...................................................................................................................... 113 Swaps .......................................................................................................................................... 113

Netting ............................................................................................................................................. 114 Interest Risk Overview ..................................................................................................................... 115 Interest Rate Risk Management ....................................................................................................... 116

Take No Action ............................................................................................................................. 116 Avoid Risk .................................................................................................................................... 116 Asset and Liability Matching.......................................................................................................... 116 Hedging ........................................................................................................................................ 116

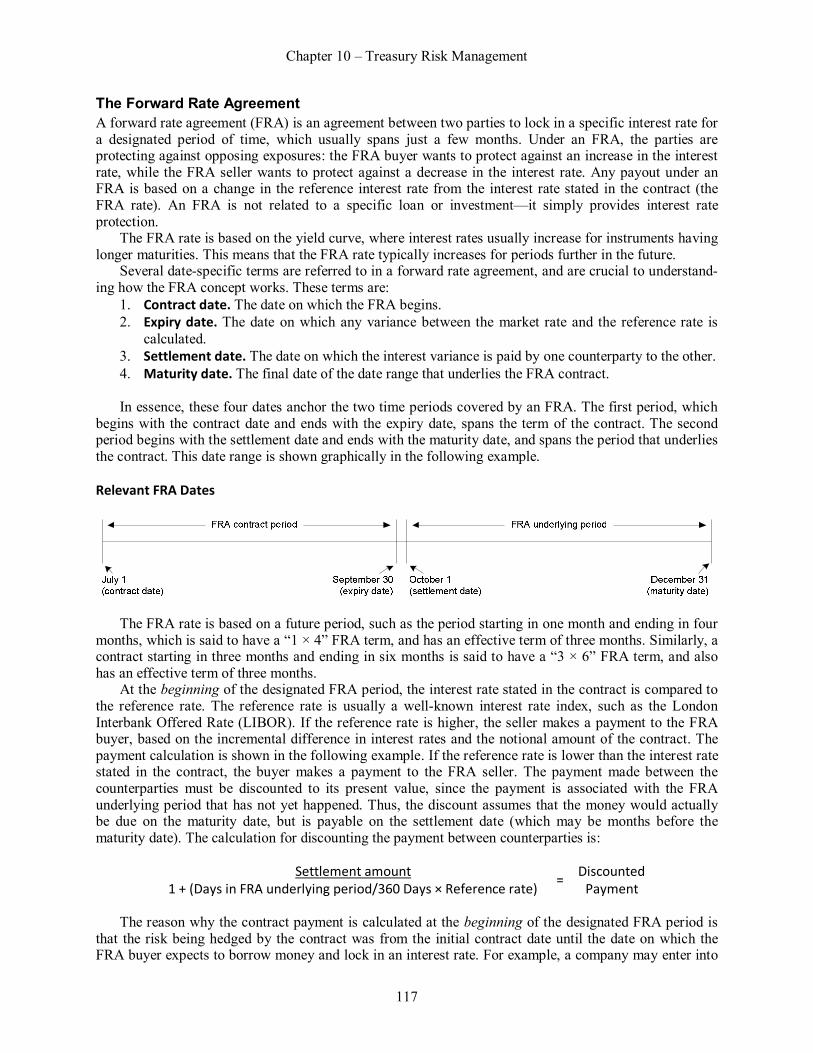

Types of Interest Rate Hedges ......................................................................................................... 116 The Forward Rate Agreement ....................................................................................................... 117 The Futures Contract .................................................................................................................... 118 The Interest Rate Swap ................................................................................................................ 120 Interest Rate Options .................................................................................................................... 121 Interest Rate Swaptions ................................................................................................................ 123

Chapter Summary ............................................................................................................................ 124 Review Questions ............................................................................................................................ 125 Review Answers .............................................................................................................................. 126

Chapter 11 – Insurance ..................................................................................................................... 127

Learning Objectives ......................................................................................................................... 127 Introduction ...................................................................................................................................... 127 Insurance Distribution ...................................................................................................................... 127 Insurance Policy Terms and Conditions ............................................................................................ 128

Indemnity ..................................................................................................................................... 128 Deductibles .................................................................................................................................. 128 Limit of Insurance ......................................................................................................................... 128 Coinsurance ................................................................................................................................. 128 Exclusions .................................................................................................................................... 129 Insurance Riders .......................................................................................................................... 129 Perils ............................................................................................................................................ 129 Endorsements .............................................................................................................................. 129

Table of Contents

v

Who is the Payee? ........................................................................................................................... 130 Insurance Company Analysis ........................................................................................................... 130 Insurer Financial Performance.......................................................................................................... 130 Boiler and Machinery Insurance ....................................................................................................... 131 Business Interruption Insurance ....................................................................................................... 131

Policy Inclusions ........................................................................................................................... 132 Additional Coverages.................................................................................................................... 132 Management Actions .................................................................................................................... 133

Commercial Automobile Insurance ................................................................................................... 133 Commercial Crime Insurance ........................................................................................................... 134 Commercial General Liability Insurance ........................................................................................... 134

Coverage Limitations .................................................................................................................... 135 Umbrella Coverage ....................................................................................................................... 135

Credit Insurance............................................................................................................................... 135 Directors and Officers Liability Insurance .......................................................................................... 136

Management Actions .................................................................................................................... 137 Additional Coverages.................................................................................................................... 137

Inland Marine Insurance ................................................................................................................... 137 Life Insurance .................................................................................................................................. 137 Property Insurance ........................................................................................................................... 138

Types of Property ......................................................................................................................... 138 Policy Inclusions ........................................................................................................................... 138 Policy Exclusions .......................................................................................................................... 139 Additional Coverages.................................................................................................................... 139 Coverage Limitations .................................................................................................................... 139 Valuation Issues ........................................................................................................................... 140 Management Actions .................................................................................................................... 140

Surety Bonds ................................................................................................................................... 140 Surplus Lines Insurance ................................................................................................................... 141 Managing the Cost of Insurance ....................................................................................................... 141

Broker Training ............................................................................................................................. 142 Odds Analysis .............................................................................................................................. 142 Insurer Messaging ........................................................................................................................ 142 Covered Items Analysis ................................................................................................................ 142 Double Coverage Analysis ............................................................................................................ 142 Split Limits Elimination .................................................................................................................. 142 Continual Policy Updates .............................................................................................................. 143 Unlikely Rider Payouts .................................................................................................................. 143 Non-Comparability ........................................................................................................................ 143 Deductibles Analysis..................................................................................................................... 143 Small Claims Avoidance ............................................................................................................... 143 Self-Funded Insurance ................................................................................................................. 144 Captive Insurance Company ......................................................................................................... 144

Insurance Claims Administration ...................................................................................................... 145 Chapter Summary ............................................................................................................................ 145 Review Questions ............................................................................................................................ 147 Review Answers .............................................................................................................................. 148

Chapter 12 – Credit Management...................................................................................................... 149

Learning Objectives ......................................................................................................................... 149 Introduction ...................................................................................................................................... 149 Overview of the Credit Policy ........................................................................................................... 149 Credit Policy: Mission ....................................................................................................................... 149 Credit Policy: Goals.......................................................................................................................... 150 Credit Policy: Responsibilities........................................................................................................... 150 Credit Policy: Required Documentation ............................................................................................ 151 Credit Policy: Review Frequency ...................................................................................................... 152

Table of Contents

vi

Credit Policy: Credit Calculation ....................................................................................................... 152 Credit Policy: Terms of Sale ............................................................................................................. 153 Credit Policy: Revision Frequency .................................................................................................... 153 The Credit Application ...................................................................................................................... 154 Adjustments to the Credit Application ............................................................................................... 155 Trade References ............................................................................................................................ 156 Updating the Credit Application ........................................................................................................ 157 The Credit Rating ............................................................................................................................. 157 Internal Credit Rating Systems ......................................................................................................... 157 Third Party Credit Ratings ................................................................................................................ 159 Use of Credit Ratings ....................................................................................................................... 160 Credit Rating Errors ......................................................................................................................... 160 Credit Documentation ...................................................................................................................... 161 Indicators of Future Payment Delinquency ....................................................................................... 161 Ongoing Credit Monitoring Actions ................................................................................................... 163 Requests for Credit Increases .......................................................................................................... 165 The Riskiest Customers ................................................................................................................... 165 Chapter Summary ............................................................................................................................ 166 Review Questions ............................................................................................................................ 167 Review Answers .............................................................................................................................. 168

Chapter 13 – Working Capital Management ..................................................................................... 169

Learning Objectives ......................................................................................................................... 169 Introduction ...................................................................................................................................... 169 The Nature of Working Capital ......................................................................................................... 169 The Importance of Working Capital .................................................................................................. 170 The Optimum Amount of Working Capital ......................................................................................... 170 Zero Working Capital ....................................................................................................................... 171 Working Capital for a Growing Business ........................................................................................... 172 Working Capital for a Declining Business ......................................................................................... 173 Responsibility for Working Capital .................................................................................................... 174 The Receivables Component of Working Capital .............................................................................. 174 Receivables Strategy ....................................................................................................................... 175 Inventory Strategy ............................................................................................................................ 176

Replenishment Strategy ............................................................................................................... 176 Fulfillment Strategy ....................................................................................................................... 177 Customization Strategy ................................................................................................................. 178 Startup Outsourcing Strategy ........................................................................................................ 178

Payables Strategy ............................................................................................................................ 179 Chapter Summary ............................................................................................................................ 179 Review Questions ............................................................................................................................ 180 Review Answers .............................................................................................................................. 181

Chapter 14 – Accounting for Treasury Transactions ....................................................................... 183

Learning Objectives ......................................................................................................................... 183 Introduction ...................................................................................................................................... 183 Other Comprehensive Income .......................................................................................................... 183 Investment Classifications ................................................................................................................ 184 The Realized and Unrealized Gain or Loss ....................................................................................... 187 Purchase and Sale of Investments ................................................................................................... 187

The Gain or Loss Calculation ........................................................................................................ 188 Noncash Acquisition of Securities ................................................................................................. 188 Assignment of Costs to Securities ................................................................................................. 188 Lump-Sum Purchases .................................................................................................................. 189 Restricted Stock ........................................................................................................................... 189 Conversion of Securities ............................................................................................................... 190 Sale of Securities.......................................................................................................................... 190

Table of Contents

vii

Accounting for Dividends and Interest Income .................................................................................. 190 Stock Dividends and Stock Splits .................................................................................................. 191 Noncash Dividends ....................................................................................................................... 191

Ongoing Accounting for Investments ................................................................................................ 192 Investment Transfers .................................................................................................................... 193 The Effective Interest Method ....................................................................................................... 193

Impairment of Investments ............................................................................................................... 195 What is a Derivative? ....................................................................................................................... 196 Hedge Accounting – General ........................................................................................................... 198 Hedge Accounting – Fair Value Hedges ........................................................................................... 199 Hedge Accounting – Cash Flow Hedges .......................................................................................... 200 Accounting for Insurance .................................................................................................................. 203

Insurance Payments ..................................................................................................................... 203 Claims Receipts ........................................................................................................................... 204

Chapter Summary ............................................................................................................................ 204 Review Questions ............................................................................................................................ 205 Review Answers .............................................................................................................................. 206

Chapter 15 – Treasury Management Systems .................................................................................. 207

Learning Objectives ......................................................................................................................... 207 Introduction ...................................................................................................................................... 207 Components of a Treasury Management System ............................................................................. 207 Advantages of a Treasury Management System............................................................................... 208 Disadvantages of a Treasury Management System .......................................................................... 208 Additional TMS Considerations ........................................................................................................ 209 Data Feeds ...................................................................................................................................... 210 Chapter Summary ............................................................................................................................ 210 Review Questions ............................................................................................................................ 211 Review Answers .............................................................................................................................. 212

Chapter 16 – Treasury Controls ........................................................................................................ 213

Learning Objectives ......................................................................................................................... 213 Introduction ...................................................................................................................................... 213 The Cash Forecasting Controls Environment.................................................................................... 213 The Funds Investment Control Environment ..................................................................................... 214 The Foreign Exchange Hedge Control Environment ......................................................................... 216 The Debt Procurement Control Environment .................................................................................... 217 The Stock Issuance Control Environment ......................................................................................... 218 Additional Treasury Controls – Fraud Related .................................................................................. 219 Terminating Controls ........................................................................................................................ 220 Chapter Summary ............................................................................................................................ 221 Review Questions ............................................................................................................................ 222 Review Answers .............................................................................................................................. 223

Chapter 17 – Treasury Measurements .............................................................................................. 225

Learning Objectives ......................................................................................................................... 225 Introduction ...................................................................................................................................... 225 Treasury Metrics .............................................................................................................................. 225 Cash Conversion Cycle .................................................................................................................... 225

Days Sales in Accounts Receivable .............................................................................................. 226 Days Sales in Inventory ................................................................................................................ 227 Days Payables Outstanding .......................................................................................................... 227

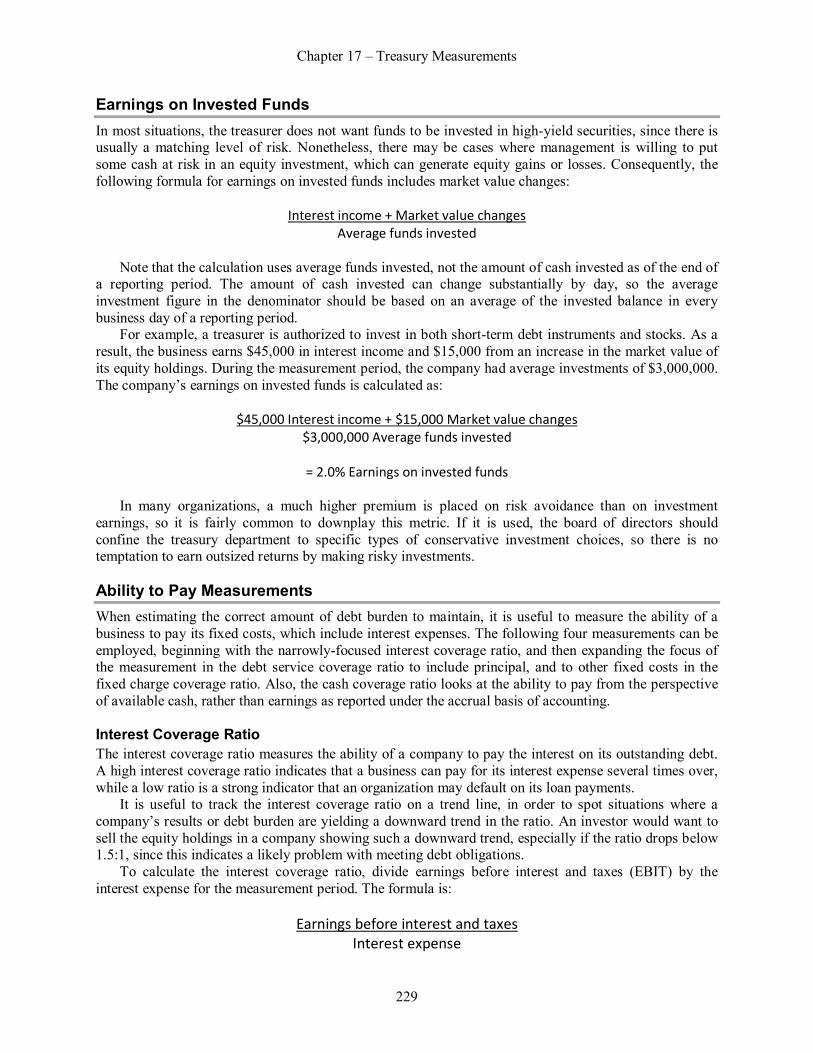

Actual Cash Position versus Forecast .............................................................................................. 228 Earnings on Invested Funds ............................................................................................................. 229 Ability to Pay Measurements ............................................................................................................ 229

Interest Coverage Ratio ................................................................................................................ 229 Debt Service Coverage Ratio........................................................................................................ 230

Table of Contents

viii

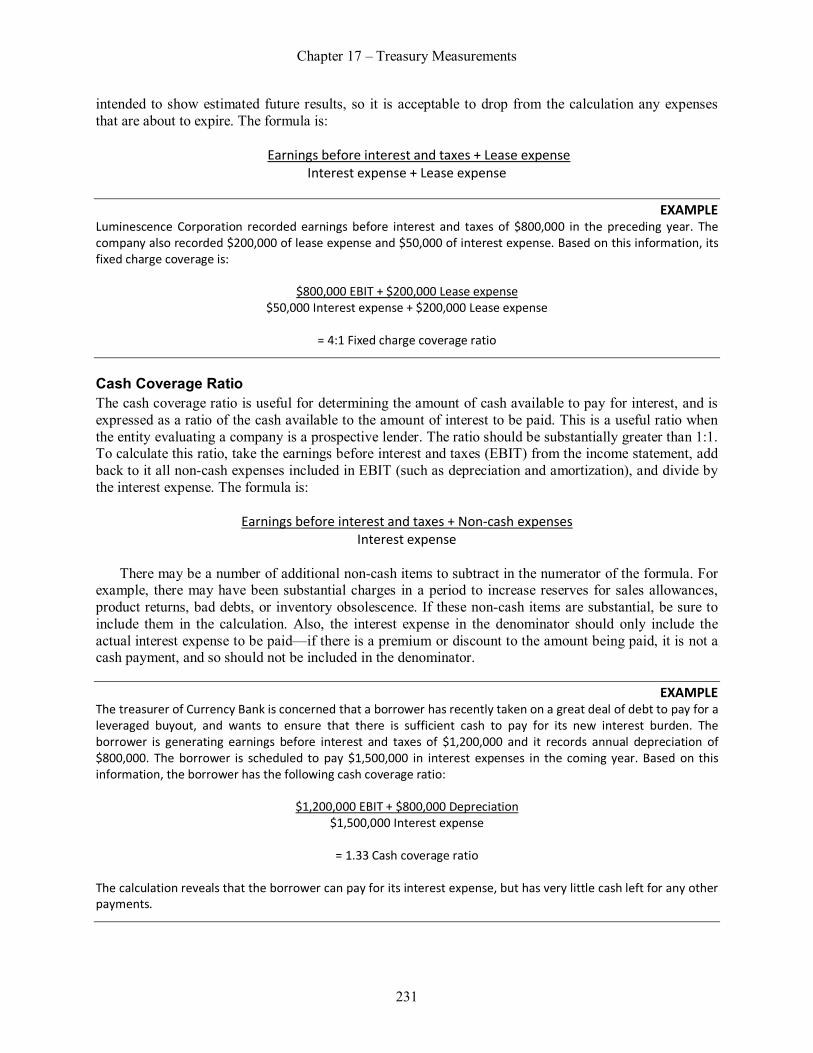

Fixed Charge Coverage Ratio ....................................................................................................... 230 Cash Coverage Ratio ................................................................................................................... 231

Debt to Equity Ratio ......................................................................................................................... 232 Average Cost of Debt ....................................................................................................................... 232 Borrowing Base Usage..................................................................................................................... 233 Additional Treasury Measurements .................................................................................................. 234 Chapter Summary ............................................................................................................................ 234 Review Questions ............................................................................................................................ 235 Review Answers .............................................................................................................................. 236

Glossary ............................................................................................................................................. 237 Index .................................................................................................................................................. 243

Preface The treasurer is responsible for a broad range of activities, which include bank relations, cash forecasting, investments, fund raising, risk management, and even insurance. These are critical high-risk activities, so the treasurer must also have a detailed knowledge of processes, controls, and treasury management systems. The Treasurer’s Guidebook addresses all of these topics and more, with the intent of giving a new treasurer a solid grounding in how to perform the job.

The book is divided into three sections. In Chapters 1 through 10, we focus on the core treasury activities, which begin with an overview of treasury management and then walk through all major job functions. In Chapters 11 through 13, we cover ancillary treasury functions that may not always be in included in a treasurer’s job description. These functions are insurance, credit management, and working capital management. In Chapters 14 through 17, we cover the treasury back office, which deals with administrative functions.

You can find the answers to many questions about treasury activities in the following chapters, including:

What are the differences between cash sweeping and notional pooling? How do I create a cash forecast? Which investment strategy should I follow? How can I reduce the risk of foreign exchange fluctuations? Which types of insurance does my business need? How do I create an internal credit rating system for customers? What is the proper accounting for a hedging transaction? What are the components of a treasury management system? Which controls should be applied to the various treasury transactions?

The Treasurer’s Guidebook is designed primarily for professionals, who can use it as a reference tool

for all aspects of the treasurer’s job, from accounting to risk management.

About the Author Steven Bragg, CPA, has been the chief financial officer or controller of four companies, as well as a consulting manager at Ernst & Young. He received a master’s degree in finance from Bentley College, an MBA from Babson College, and a Bachelor’s degree in Economics from the University of Maine. He has been a two-time president of the Colorado Mountain Club, and is an avid alpine skier, mountain biker, and certified master diver. Mr. Bragg resides in Centennial, Colorado. He has written the following books and courses:

Accountants’ Guidebook Accounting Changes and Error Corrections Accounting Controls Guidebook Accounting for Derivatives and Hedges Accounting for Earnings per Share Accounting for Inventory Accounting for Investments Accounting for Managers Accounting for Stock-Based Compensation Accounting Procedures Guidebook Bookkeeping Guidebook Budgeting Business Combinations and Consolidations Business Insurance Fundamentals Business Ratios Capital Budgeting CFO Guidebook Closing the Books Constraint Management Corporate Cash Management Corporate Finance Cost Accounting Fundamentals Cost Management Guidebook Credit & Collection Guidebook Enterprise Risk Management Fair Value Accounting

Financial Analysis Financial Forecasting and Modeling Fixed Asset Accounting Foreign Currency Accounting GAAP Guidebook Hospitality Accounting Human Resources Guidebook IFRS Guidebook Interpretation of Financial Statements Inventory Management Investor Relations Guidebook Lean Accounting Guidebook Mergers & Acquisitions New Controller Guidebook Nonprofit Accounting Payables Management Payroll Management Project Accounting Public Company Accounting Purchasing Guidebook Real Estate Accounting Revenue Recognition The Soft Close The Year-End Close Treasurer’s Guidebook Working Capital Management

Chapter 1

Treasury Management Learning Objectives

Identify the aspect of a business for which the treasury function is responsible Determine which part of the treasury department executes transactions Recognize how to improve the layout of the treasury department

Introduction The treasury function administers the financial holdings and obligations of an organization. This is a major task in an organization that has millions or even billions of dollars in cash and investments, receivables, payables, and debt. Even in a smaller organization, these tasks are essential to the ability of a business to continue in operation. Consequently, though treasury is an administrative function, it is still one of the most vital parts of a business.

In this chapter, we address the responsibilities of the treasury function as a whole and the treasurer in particular, how treasury fits into the organizational structure of a business, and numerous management issues. Treasury Responsibilities Ultimately, the treasury function is responsible for the liquidity of a business—the entity must always be able to pay its bills on time, and have sufficient cash available to support its plans. This is the core function of the treasury department. However, this one item represents an excessively simple view of the responsibilities of the group, which can be quite broad in a larger and more complex organization. The following list provides a more detailed view of treasury responsibilities:

Control cash. The department marshals the flow of cash through the organization. Issue credit. A business may loan funds to its customers via accounts receivable. Since this is

essentially a financing function, the examination and granting of customer credit may be assigned to the treasurer.

Mitigate risk. The department is frequently tasked with management of all insurance policies, which allows certain risks to be shifted to a third party. In addition, the treasury group may use hedging instruments to offset the variability in value of certain foreign exchange and interest rate transactions.

Obtain a return. The treasury staff may be expected to earn a significant return on invested funds, though this responsibility can contravene the more important requirement to safeguard funds. The usual outcome is that a modest return is expected, while the safety of invested funds is paramount.

Raise funds. The department is responsible for obtaining debt financing at reasonable rates, and for selling shares under reasonable terms.

Safeguard funds. The department is responsible for investing excess funds appropriately, with an overriding objective of not suffering a capital loss.

Treasurer Job Description The treasurer manages the treasury department. If the department is a small one, then the treasurer may be directly responsible for many tasks that would normally be assigned to specialists within the department. In order to give the broadest possible scope to the treasurer’s job description, we will assume that the

Chapter 1 – Treasury Management

2

treasurer personally handles most activities within the department. Under this assumption, we derive the following job description for a treasurer: Operational Requirements

Forecast cash flows. This information is needed to pinpoint when extra cash is needed, and when excess cash will be available, which then drives the treasurer’s planning to obtain additional fi-nancing or invest funds.

Manage working capital. A key component of the cash forecast is working capital, which is the net amount of current assets and current liabilities. The treasurer is not usually responsible for the management of these items (except for the extension of credit to customers), but can model how changes in operational decisions will result in different working capital requirements.

Aggregate cash. Cash may be separated into a number of bank accounts throughout an organiza-tion. The treasurer must create a system to aggregate this cash so that it can be properly deployed to meet the operational and investment needs of the business.

Invest funds. Excess cash should be invested so that any investment vehicles mature in time for the cash to be available for operational needs. This can result in several tranches of investments, some of which are available on short notice, while other tranches cannot be immediately ac-cessed.

Invest pension funds. If the company has a pension plan, the treasurer is responsible for invest-ing it within the guidelines stated in the plan.

Obtain debt and equity financing. The treasurer works with the Chief Financial Officer (CFO) to raise funds as needed. This can include the sale of stock to the investing public or through private placements, as well as obtaining loans from many types of lenders or selling bonds. These activi-ties will likely require the maintenance of ongoing relations with a number of intermediaries, such as investment bankers and brokers.

Hedge transactions. The interest rates and foreign exchange rates to which a business is subject-ed can vary unfavorably, so the treasurer can engage in hedging activities to mitigate the risk of loss, as well as other risk mitigation strategies.

Issue credit. The treasurer can control the credit policy that forms the basis for issuing credit to customers, and may make the decisions to grant or withhold credit to specific customers. This gives the treasurer a valuable control over one of the larger elements of working capital.

Maintain insurance policies. Since the treasurer is already using hedging to deal with certain types of financial risk, it is logical to extend the risk management concept and have the treasurer oversee all insurance policies. This can include ongoing adjustments to policy coverage to ensure that changes in the business are reflected in its insurance coverage.

Advise management. The treasurer must take a leading role in all financial planning activities, to ensure that a realistic assessment of the funding requirements of the business is included in budg-ets.

Third Party Requirements

Maintain bank relationships. The treasurer is the primary point of contact between the organiza-tion and the banks with which it does business. In this role, the treasurer can consolidate banking services and negotiate for preferential pricing.

Oversee outsourcing relationships. If any tasks within the treasury department have been outsourced, the treasurer oversees the outsourcing relationships, including entering into contracts and measuring performance.

Management Requirements

Oversee the treasury staff. The treasurer hires and fires treasury employees, rates their perfor-mance, approves training, promotes employees when suitable, schedules activities, and engages in other actions normally associated with management.

Chapter 1 – Treasury Management

3

Maintain a system of policies, procedures, and controls. This is a particularly important job responsibility, since the treasury department may handle very large amounts of cash, which can-not be misplaced or stolen. This is one of the few areas in a business in which 100% process compliance is needed.

A treasurer should have a Bachelor’s degree in accounting or finance, as well as 10+ years of

progressively more responsible treasury experience. The individual should have a thorough understanding of forecasting, cash management, hedging activities, bank account management, and international transactions. Treasury Organizational Structure In a smaller organization where there is no CFO or treasurer, all treasury tasks are handled by the controller. Once treasury tasks become too overwhelming for the accounting staff, a CFO is usually hired, and the treasury tasks are transferred to this individual. Since a CFO cannot personally handle all of the treasury tasks of a growing business, they are soon transferred to a treasurer. Thus, the treasurer is usually the last person hired in the accounting and finance management troika of the CFO, controller, and treasurer.

Once a treasurer has been hired, it does not mean that the full range of treasury activities is automati-cally placed under this person’s direct supervision. Instead, there is usually a long-term trend toward centralization of treasury activities, which tends to follow these steps:

1. Focus on investment benefits. The treasurer needs to prove the benefits of having a treasury, and so offers to centralize investments so that higher returns can be obtained.

2. Focus on borrowing costs. The treasurer takes over debt management, so that high-cost debt can be replaced. Again, the focus is on contributing to the profit of the business.

3. Focus on netting benefits. The treasurer offers to provide netting services to reduce the amount of foreign exchange fees being incurred by the subsidiaries.

Up to this point, the focus has been on the more obvious profit improvements. The next step is to

point out to senior management that a possible cost area to eliminate is the duplicative treasury positions at the local level, replacing them with a core group of highly-qualified employees in a central treasury department. This will result in one or more of the following changes:

The treasury group takes over all banking relationships, likely eliminating some banks entirely. The treasury group centralizes the management of hedging transactions. The treasury group takes over the credit function. The treasury group establishes and operates a centralized payables system.

Thus, over a period of time, the treasury organizational structure evolves into a key administrative

function that centralizes numerous financial activities. A variation on the gradual centralization concept is that larger organizations may still need to

maintain local treasury staffs. This is because local expertise may be needed in certain markets, where knowledge of local regulations is essential. This is especially important when there are currency controls. There may also be a need to maintain a staff in one or more of the major currency markets, such as London, New York, and Tokyo, as well as to operate regional groups in the approximate time zones in which there are company operations. In short, absolute centralization may not occur—pockets of treasury staff may be required in select locations.

Given the overwhelmingly financial nature of the treasurer’s job, this position always reports to the CFO, alongside the controller. However, the treasury function itself contains numerous activities that cannot all report to the treasurer, for control reasons. Instead, the function is split up into three areas, each of which reports to a different person. These areas are as follows:

Front office. This group focuses on decision making and initiating transactions, and reports to the treasurer. Examples of its tasks include funding, investments, risk management, and bank interac-tions.

Chapter 1 – Treasury Management

4

Back office. This group executes transactions. Examples of its tasks include processing transac-tions, confirmations, settlements, and account reconciliations. Given the essentially accounting orientation of this group, it reports to the controller. By doing so, there is also a clear separation of duties between the front office and back office.

Middle office. This group is tasked with monitoring all treasury activities and reconciling the transactions initiated by the front office with the actual transactions processed by the back office. Its activities can include risk reporting, limit monitoring, valuation, and performance evaluations. This group necessarily must operate independently from the other two groups and so usually re-ports to the CFO. Alternatively, this group could report to the chief risk officer (if such a position exists), or even to the internal audit director.

Treasury Organizational Chart

In addition to the reporting breakdown noted in the preceding organizational chart, the credit department reports to the treasurer. Treasury Centralization A smaller organization with a few locations likely has a decentralized treasury system, where cash is received and paid out locally. The management of cash is probably a minor side function of the

Chapter 1 – Treasury Management

5

accounting staff. As an entity expands in size, a number of factors will appear that make centralization of the treasury function an increasingly attractive option. These factors are:

Cash visibility. There may be a large amount of cash sequestered in local bank accounts that is not earning interest at all, or which is being invested at very low rates of return.

Geographic boundaries. Expansions to the business may result in operations being conducted in countries where cash flows are controlled. If so, it may be difficult to extract funds from some locations.

Risk of loss. When there are large amounts of cash floating in the system with minimal oversight and controls, there is a greater risk of loss.

Cost effectiveness. If individuals in each location are engaged in treasury activities, this repre-sents a very inefficient use of staff time, since it is duplicative.

Service providers. There may be an overabundance of service providers scattered among the subsidiaries, resulting in a large administrative burden to manage them.

These issues may lead management to contemplate the installation of a centralized treasury function.

The following factors all argue in favor of centralization: Controls. It is much easier to maintain a strong system of controls over treasury activities when

all parties engaged in those activities are located in one place. It is also easier to provide con-sistent training to employees, so that a consistent process flow (with integrated controls) is fol-lowed by everyone.