Treasurer's /Bookkeepers Manual - QUT

42

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-1 Part 4: GETTING READY FOR YEAR-END 4.1 Introduction This part of the manual discusses the year-end accounting requirements that are particularly relevant for nonprofit bookkeepers and treasurers. Its aim is to provide an explanation of the steps required to assist the external accountant and auditor in preparing the financial statements, as well as provide a summary of the statutory regulations imposed under the Associations Incorporation Act (1981) and the Corporations Act (2001). Specifically, the chapter addresses the following issues: the difference between management accounts and external financial statements; whether your organisation is a reporting entity or a non-reporting entity; the difference between general purpose financial reports and special purpose financial reports; external reporting and audit requirements of incorporated associations and companies limited by guarantee; checklist of documents to provide your external accountant or auditor with at year-end; a sample agenda for an Annual General Meeting; and a summary of the forms required to be prepared and lodged with the regulatory authorities for incorporated associations and companies limited by guarantee. 4.2 The Difference between Management Accounts and External Financial Statements So far, this manual has specifically dealt with the preparation of management accounts. Management accounts are typically prepared by a bookkeeper for internal reporting purposes. These accounts are usually prepared monthly and are specifically tailored to management’s needs. In most cases, management accounts are prepared using computerised software accounting packages, such as MYOB or QuickBooks. Some bookkeepers export the reports produced by MYOB or QuickBooks into electronic spreadsheets such as EXCEL for manipulation, comparison of actual results to budget and the preparation of charts and graphs etc. This comparison of actual to budgeted results should be done on a monthly or quarterly basis or more frequently (eg. in preparation for periodic financial reporting to funding providers. And, in the event that an organisation is in receipt of multiple grants, and has multiple periodic reporting obligations, the results being compared may need to be separated by identifiable cost centres for ease of reporting. This was specifically illustrated in Part 2. The Standard Chart of Accounts presented in Part 1 of this manual was specifically developed to assist bookkeepers prepare an account list for internal reporting purposes. The management accounts are usually passed onto the external accountant at the end of the financial year so that the external accountant can prepare the external financial statements. In most cases, these accounts are audited and presented to members at the Annual General Meeting.

Transcript of Treasurer's /Bookkeepers Manual - QUT

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-1

Part 4: GETTING READY FOR YEAR-END 4.1 Introduction This part of the manual discusses the year-end accounting requirements that are particularly relevant for nonprofit bookkeepers and treasurers. Its aim is to provide an explanation of the steps required to assist the external accountant and auditor in preparing the financial statements, as well as provide a summary of the statutory regulations imposed under the Associations Incorporation Act (1981) and the Corporations Act (2001). Specifically, the chapter addresses the following issues: the difference between management accounts and external financial statements; whether your organisation is a reporting entity or a non-reporting entity; the difference between general purpose financial reports and special purpose financial

reports; external reporting and audit requirements of incorporated associations and companies

limited by guarantee; checklist of documents to provide your external accountant or auditor with at year-end; a sample agenda for an Annual General Meeting; and a summary of the forms required to be prepared and lodged with the regulatory

authorities for incorporated associations and companies limited by guarantee. 4.2 The Difference between Management Accounts and External Financial

Statements So far, this manual has specifically dealt with the preparation of management accounts. Management accounts are typically prepared by a bookkeeper for internal reporting purposes. These accounts are usually prepared monthly and are specifically tailored to management’s needs. In most cases, management accounts are prepared using computerised software accounting packages, such as MYOB or QuickBooks. Some bookkeepers export the reports produced by MYOB or QuickBooks into electronic spreadsheets such as EXCEL for manipulation, comparison of actual results to budget and the preparation of charts and graphs etc. This comparison of actual to budgeted results should be done on a monthly or quarterly basis or more frequently (eg. in preparation for periodic financial reporting to funding providers. And, in the event that an organisation is in receipt of multiple grants, and has multiple periodic reporting obligations, the results being compared may need to be separated by identifiable cost centres for ease of reporting. This was specifically illustrated in Part 2. The Standard Chart of Accounts presented in Part 1 of this manual was specifically developed to assist bookkeepers prepare an account list for internal reporting purposes. The management accounts are usually passed onto the external accountant at the end of the financial year so that the external accountant can prepare the external financial statements. In most cases, these accounts are audited and presented to members at the Annual General Meeting.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-2

An annual financial report is required to be lodged with the Office of Fair Trading if your organisation is an incorporated association and with the Australian Securities and Investments Commission (ASIC) if your organisation is a company limited by guarantee. The primary purpose of the financial report is to provide information relevant to external users. The financial report usually consists of the following: a Profit and Loss Statement; a Balance Sheet, and a Cash Flow Statement.

In some cases, an additional statement entitled a “Statement of Changes in Equity” is also prepared, showing the link between the Profit and Loss Statement and the Balance Sheet.

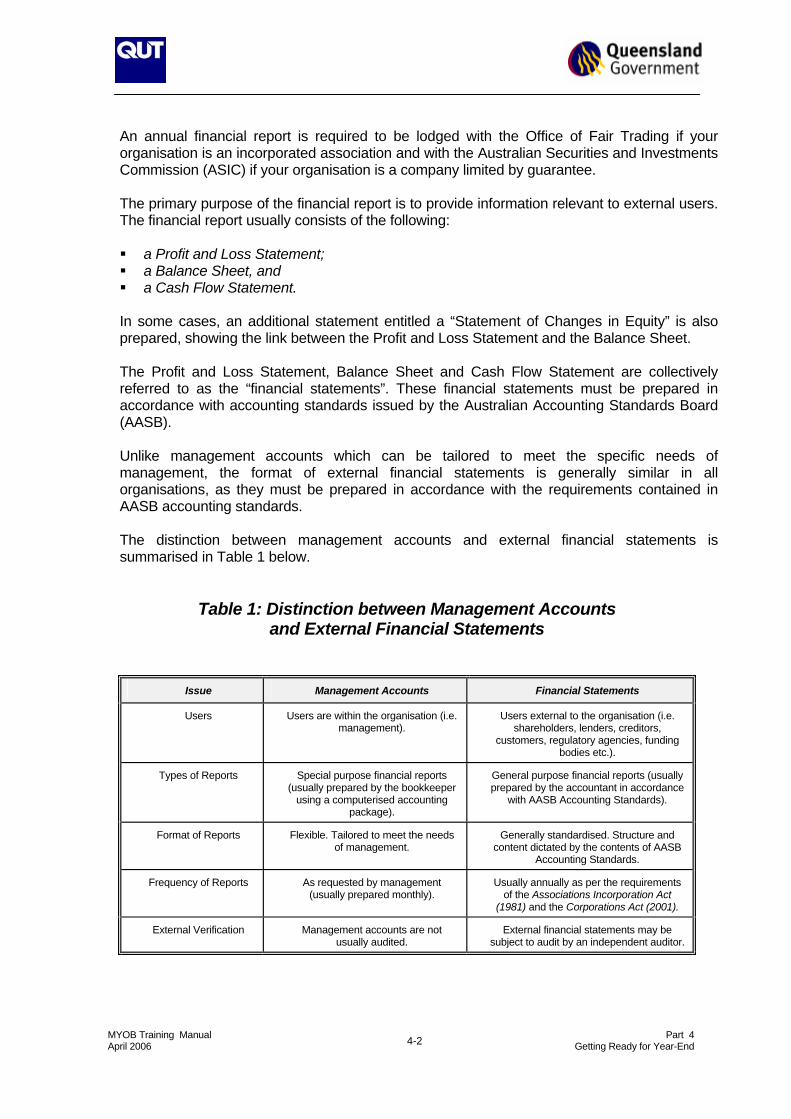

The Profit and Loss Statement, Balance Sheet and Cash Flow Statement are collectively referred to as the “financial statements”. These financial statements must be prepared in accordance with accounting standards issued by the Australian Accounting Standards Board (AASB). Unlike management accounts which can be tailored to meet the specific needs of management, the format of external financial statements is generally similar in all organisations, as they must be prepared in accordance with the requirements contained in AASB accounting standards. The distinction between management accounts and external financial statements is summarised in Table 1 below.

Table 1: Distinction between Management Accounts and External Financial Statements

Issue Management Accounts Financial Statements

Users Users are within the organisation (i.e. management).

Users external to the organisation (i.e. shareholders, lenders, creditors,

customers, regulatory agencies, funding bodies etc.).

Types of Reports Special purpose financial reports (usually prepared by the bookkeeper

using a computerised accounting package).

General purpose financial reports (usually prepared by the accountant in accordance

with AASB Accounting Standards).

Format of Reports Flexible. Tailored to meet the needs of management.

Generally standardised. Structure and content dictated by the contents of AASB

Accounting Standards.

Frequency of Reports As requested by management (usually prepared monthly).

Usually annually as per the requirements of the Associations Incorporation Act

(1981) and the Corporations Act (2001).

External Verification Management accounts are not usually audited.

External financial statements may be subject to audit by an independent auditor.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-3

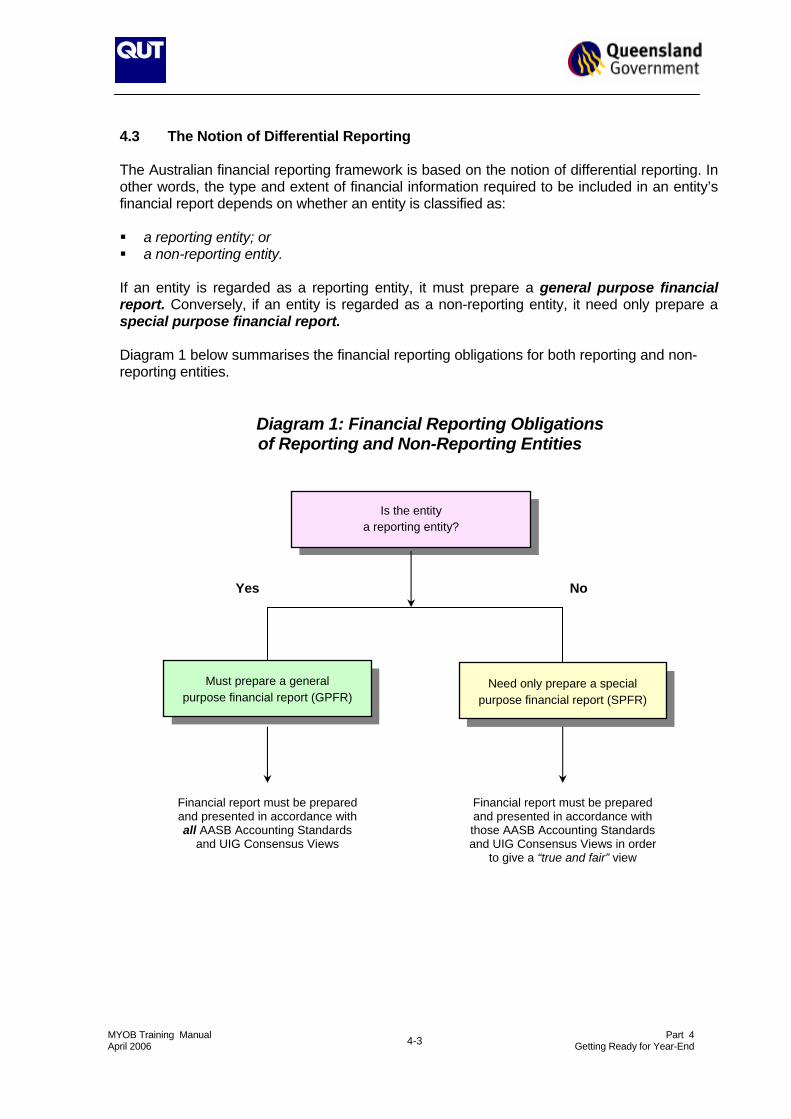

4.3 The Notion of Differential Reporting The Australian financial reporting framework is based on the notion of differential reporting. In other words, the type and extent of financial information required to be included in an entity’s financial report depends on whether an entity is classified as: a reporting entity; or a non-reporting entity.

If an entity is regarded as a reporting entity, it must prepare a general purpose financial report. Conversely, if an entity is regarded as a non-reporting entity, it need only prepare a special purpose financial report.

Diagram 1 below summarises the financial reporting obligations for both reporting and non-reporting entities.

Diagram 1: Financial Reporting Obligations

of Reporting and Non-Reporting Entities

Is the entity a reporting entity?

Must prepare a general purpose financial report (GPFR)

Need only prepare a special purpose financial report (SPFR)

Yes No

Financial report must be prepared and presented in accordance with all AASB Accounting Standards

and UIG Consensus Views

Financial report must be prepared and presented in accordance with those AASB Accounting Standards and UIG Consensus Views in order

to give a “true and fair” view

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-4

4.3.1 What is a Reporting Entity?

Paragraph 40 of SAC 1 Definition of the Reporting Entity defines a reporting entity as:

… all entities in respect of which it is reasonable to expect the existence of users dependent on general purpose financial reports for information which will be useful to them for making and evaluating decisions about the allocation of scarce resources.

Put simply, a reporting entity is one which has many (and varied) users of its financial statements who require this report to be prepared and published so that they can make informed decisions about the entity. Whilst management is entrusted with the responsibility for determining whether the entity is classified as a reporting entity or not, usually the external accountant/auditor will have significant input into this decision. The primary question to ask in determining whether an entity is a reporting entity or not is: “Who are the users of the reports?” The more users, the more likely the entity is to be a reporting entity. Further guidance is included in paragraphs 20 to 22 of SAC 1 to assist when deciding whether or not an entity is a reporting entity. (a) Separation of management from economic interest (paragraph 20): The greater the spread of ownership/membership and the greater the

extent of the separation between management and owners/members or others with an economic interest in the entity, the more likely it is that there will exist users dependent on general purpose financial reports as a basis for making and evaluating resource allocation decisions.

Paragraph 20 refers to the extent of separation of the management committee or board of directors from the members. A nonprofit organisation with a large membership base is more likely to be a reporting entity. This is because, each member is unlikely to be able to access the management accounts and other financial information. Conversely, a small nonprofit organisation where members can request monthly management accounts be sent to them and directly participate in the decision-making of the organisation is likely to be considered a non-reporting entity.

(b) Economic or political importance/influence (paragraph 21): Economic or political importance/influence refers to the ability of an entity to

make a significant impact on the welfare of external parties. The greater the economic or political importance of an entity, the more likely it is that there will exist users dependent on general purpose financial reports as a basis for making and evaluating resource allocation decisions.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-5

Hence, a large community service delivery organisation is more likely to be a reporting entity than a small community service organisation.

(c) Financial characteristics (paragraph 22): Financial characteristics that should be considered include the size (for

example, value of sales or assets, or number of employees or customers) or indebtedness of an entity. In the case of non-business entities in particular, the amount of resources provided or allocated by governments or other parties to the activities conducted by the entities should be considered. The larger the size or the greater the indebtedness of resources allocated, the more likely it is that there will exist users dependent on general purpose financial reports as a basis for making and evaluating resource allocation decisions.

The larger the nonprofit organisation (measured in terms of revenue, assets, employees, members etc), the more likely they are to be considered reporting entities.

Application to Nonprofit Organisations: Under SAC 1, most nonprofit organisations would typically be regarded as reporting entities because there are many external users of their financial statements. Importantly, it is up to the Board of Directors (or management committee) of the organisation to determine whether an entity is regarded as a reporting entity or not. Some of the factors that may be used to determine whether a nonprofit organisation is a reporting entity or not include: the number of members; the extent to which the members are involved in running the association, and how

much this is left to the governing body; rights of access to books and records by members; extent of funding other than by members, and the information needs of external

financiers (e.g. providers of grants, loans, etc.); extent of business activity and level of creditors; the size and nature of political or economic activity of the association; the size and number of donors; and number of employees and access of those people to financial information.

In summary, the most common determining factor will be the size and involvement of the membership and the level and nature of the activity conducted. The fewer the members, the greater the likelihood that the nonprofit organisation will be regarded as a non-reporting entity. However, the determining factor is more likely to be whether all members can obtain the financial information they require without examining general purpose financial reports.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-6

If the management committee is the only party that has access to the financial information, then the organisation is more likely to be a considered to be a reporting entity.

Second, the decision-making of the nonprofit organisation also needs to be considered. If not all members of the organisation are able to be involved in the decision-making process, this will tend to indicate that the entity is more likely to be a reporting entity. Third, if the activities are limited, if they involve no external funding, involve only members and are operated with, for example, one bank account and one investment account, the nonprofit organisation is less likely to be a reporting entity.

EXAMPLE: Victims of Criminal Violence Inc. is a small nonprofit incorporated association whose objects are the provision of support, education and advocacy services to victims of criminal violence on the north side of Brisbane. It had gross revenue of $125,000 for the year ended 30 June 2003. It has only one full-time staff member and three volunteers who assist with counselling. 95% of its revenue comes from a government grant with 5% from fundraising activities. No monies are generated from donations or bequests as the entity is not a deductible gift recipient (DGR). The Association has only 12 members, 7 of whom form part of the management committee. Each member can request monthly management accounts be sent to them. The Association has no external borrowings. Under the funding agreement, the granting agency receives quarterly management accounts, budgeted cash flow information and the year end financial report. On this basis, the Victims of Criminal Violence will be regarded as a non-reporting entity. 4.3.2 What if the Organisation is Classified as a Reporting Entity? If an entity (whether it be a company limited by guarantee, incorporated association, hospital foundation, etc) is regarded as a reporting entity, it will be required to prepare a general purpose financial report. In essence, a general purpose financial report is one that is in accordance with: all AASB Accounting Standards; all Urgent Issues Group (UIG) Consensus Views; and all other authoritative pronouncements of the Australian Accounting Standards Board.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-7

As such, a general purpose financial report is very comprehensive, lengthy and more costly as the entity is complying with all accounting regulations.

4.3.3 What if the Organisation is Classified as a Non-Reporting Entity?

If the management regards the entity as a non-reporting entity, it may elect to prepare a special purpose financial report. For non-reporting entities, who prepare special purpose financial reports, there is no requirement to prepare the report in accordance with all AASB Accounting Standards and UIG Consensus Views. Instead, non-reporting entities who prepare special purpose financial reports are only required to apply those Accounting Standards and UIG Consensus Views which are considered necessary to present a "true and fair" view. This is usually less expensive as compliance with all AASB Accounting Standards and UIG Consensus Views is not required. The external accountant/auditor will provide guidance as to which AASB Accounting Standards and UIG Consensus Views the nonprofit organisation must comply with in order to give a “true and fair” view. Some guidance on this issue can be taken from an ASIC document released in July 2005. This document entitled “Reporting Requirements for Non-Reporting Entities" outlines the reporting obligations of non-reporting corporate entities. This document can be downloaded from the ASIC website at:

Web Link : ASIC Guide: Reporting Requirements for Non-Reporting Entities

http://www.asic.gov.au/asic/asic.nsf/lkuppdf/ASIC+PDFW?opendocument&key=Reporting_for_non-reporting_entities_guide_pdf

ASIC confirms that it expects non-reporting entities to: adopt the accrual basis of accounting as set out in AASB 108 Accounting Policies,

Changes in Accounting Estimates and Errors; comply with those AASB Accounting Standards and UIG Consensus Views which are

deemed necessary by the Board of Directors to give a "true and fair" view of the operations and activities of the entity (particularly those accounting standards dealing with recognition and measurement);

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-8

specifically apply the following accounting standards regardless of whether the entity is

a reporting entity or not:

- AASB 101 Presentation of Financial Statements; - AASB 107 Cash Flow Statements; - AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors;

and - AASB 1048 Interpretation and Application of Standards.

comply with the disclosure requirements required under the Corporations Act (2001);

and specifically disclose in their accounting policy note (Note 1) that the financial

statements are special purpose, the purpose for which they have been prepared and the extent to which Accounting Standards and UIG Consensus Views have or have not been adopted.

What is of over-riding significance is the fact that the financial statements provide a "true

and fair" view.

Sample Note 1 Disclosures in Financial Reports Whether an entity has prepared a general purpose financial report or a special purpose financial report must be disclosed in Note 1 Statement of Significant Accounting Policies. The following is a sample Note 1 for a reporting entity that has prepared a general purpose financial report.

Note 1: Statement of Significant Accounting Policies

This financial report is a general purpose financial report which has been prepared in accordance with Australian Accounting Standards, Urgent Issues Group Consensus Views and other authoritative pronouncements of the Australian Accounting Standards Board and the requirements of the [Associations Incorporation Act (1981) or the Corporations Act (2001).]

The financial report has been prepared on an accruals basis and is based on

historical costs and does not take into account changing values or, except where stated, current valuations of non-current assets. Cost is based on the fair values of the consideration given in exchange for assets.

The following is a summary of the material accounting policies adopted by the

Association in the preparation of the financial report. The accounting policies have been consistently applied, unless otherwise stated.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-9

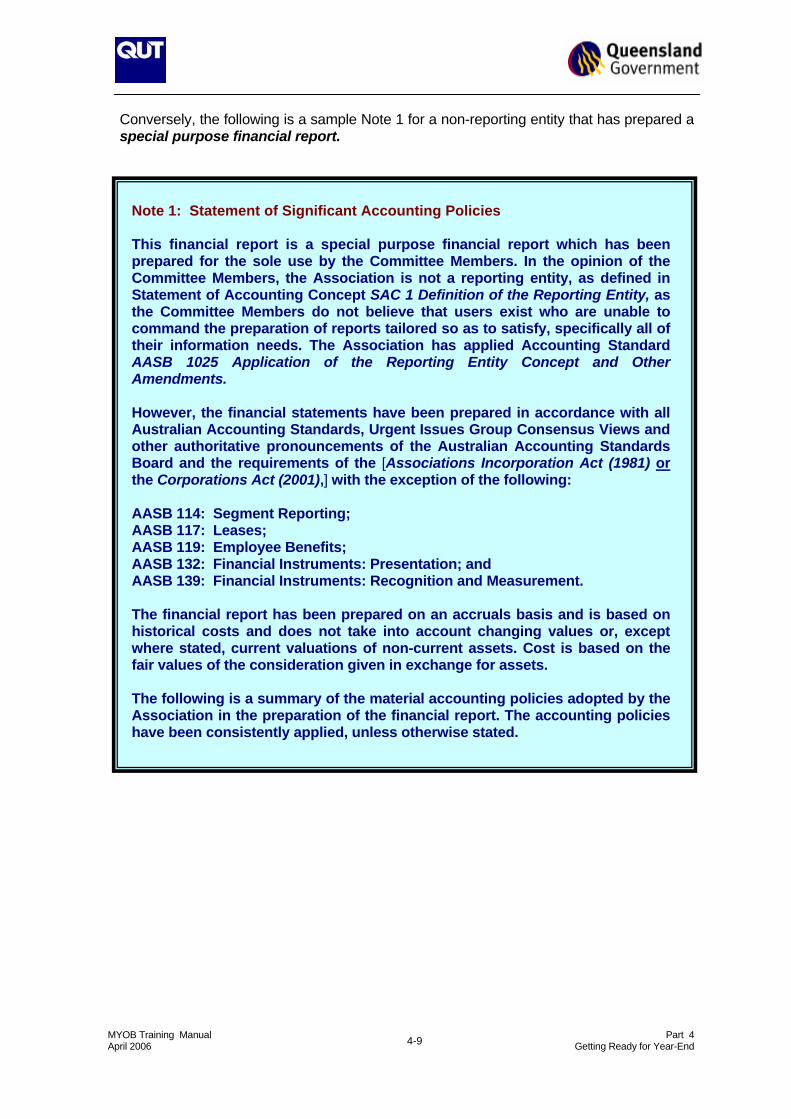

Conversely, the following is a sample Note 1 for a non-reporting entity that has prepared a special purpose financial report.

Note 1: Statement of Significant Accounting Policies

This financial report is a special purpose financial report which has been prepared for the sole use by the Committee Members. In the opinion of the Committee Members, the Association is not a reporting entity, as defined in Statement of Accounting Concept SAC 1 Definition of the Reporting Entity, as the Committee Members do not believe that users exist who are unable to command the preparation of reports tailored so as to satisfy, specifically all of their information needs. The Association has applied Accounting Standard AASB 1025 Application of the Reporting Entity Concept and Other Amendments.

However, the financial statements have been prepared in accordance with all

Australian Accounting Standards, Urgent Issues Group Consensus Views and other authoritative pronouncements of the Australian Accounting Standards Board and the requirements of the [Associations Incorporation Act (1981) or the Corporations Act (2001),] with the exception of the following:

AASB 114: Segment Reporting; AASB 117: Leases; AASB 119: Employee Benefits; AASB 132: Financial Instruments: Presentation; and AASB 139: Financial Instruments: Recognition and Measurement.

The financial report has been prepared on an accruals basis and is based on

historical costs and does not take into account changing values or, except where stated, current valuations of non-current assets. Cost is based on the fair values of the consideration given in exchange for assets.

The following is a summary of the material accounting policies adopted by the

Association in the preparation of the financial report. The accounting policies have been consistently applied, unless otherwise stated.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-10

4.4 Financial Reporting Requirements of Companies Limited by Guarantee

Some nonprofit organisations are companies limited by guarantee. These organisations are regarded as public companies for the purposes of the Corporations Act (2001). Section 292(1) requires these companies to prepare a financial report at the end of each financial year.

The financial report for a financial year (Section 295(1)) must include: (a) the financial statements; (b) the notes to the financial statements; and (c) the Directors' Declaration. Financial statements (Section 295(2)) are defined as: (i) a profit and loss statement for the year; (ii) a balance sheet as at the end of the year; and (iii) a statement of cash flows for the year. Furthermore, the Directors are required to make a declaration as part of the financial report (Section 295(4)), stating:

(a) whether the company’s financial statements comply with the AASB Accounting Standards;

(b) whether the company’s financial statements give a "true and fair"

view in accordance with Section 297. A “true and fair” view is regarded as having being achieved when the entity complies with AASB Accounting Standards; and

(c) whether, in the Director’s opinion, there are reasonable grounds to

believe that the company will be able to pay its debts as and when they fall due.

There is no mention in the Corporations Act (2001) of the reporting entity concept. The reporting entity concept is an accounting concept, not a legal concept. Accordingly, a company limited by guarantee may be either a reporting entity or a non-reporting entity. Once again, this is a decision to be made by the Board of Directors in consultation with the external accountant. The auditor of the company will also be interested in the classification of the company as a non-reporting entity in forming an opinion under Section 307 of the Corporations Act (2001) and in particular, whether the entity’s financial report complies with AASB Accounting Standards.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-11

4.5 Financial Reporting Requirements of Incorporated Associations

The format and manner in which the annual financial statements of incorporated associations are regulated is not uniform in the various Australian states. In Queensland, the financial reporting requirements of incorporated associations are governed by the Associations Incorporation Act (1981). According to the Section 59(1) of the Act: The members of the management committee of an incorporated

association must ensure the association, within 6 months of the close of the financial year prescribed, or more frequently if the rules of the incorporated association so provide:

(a) prepares a statement concerning the following particulars:

(i) the income and expenditure of the incorporated association during its last financial year; and

(ii) the assets and liabilities of the incorporated association at the close of the said year; and

(iii) all mortgages, charges and securities of any description affecting any of the property of the incorporated association at the close of the said year.

These financial statements are required to be audited and lodged with the Office of Fair Trading. However, like the Corporations Act (2001), the Associations Incorporation Act (1981) provides no specific mention as to which Accounting Standards must be complied with in the preparation of the financial statements. Once again, there is no mention in the Associations Incorporation Act (1981) of the reporting entity concept. Accordingly, an incorporated association may either be a reporting entity or a non-reporting entity. Once again, this is a decision to be made by the Management Committee in consultation with the external accountant and auditor.

A copy of the Associations Incorporation Act (1981) can be found at the following address:

Web Link : Associations Incorporation Act (1981)

http://www.legislation.qld.gov.au/Acts_SLs/Acts_SL_A.htm

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-12

4.6 Audit Requirements An audit can be defined as an independent examination of an organisation’s financial

records, transactions and supporting documents in order to express an opinion as to whether the financial statements comply with certain levels of quality, as specified in the Accounting Standards and present a “true and fair” view of the entity’s performance and financial position.

An auditor is engaged to provide an independent opinion as to whether the accounts have

been drawn up to give a “true and fair” view. 4.6.1 Audit of Companies Limited by Guarantee As previously mentioned, companies limited by guarantee are regarded as public

companies for the purposes of the Corporations Act (2001). According to Section 301 of the Corporations Act (2001), the accounts of a public company are subject to an annual audit.

Sections 327A to 327C of the Corporations Act (2001) govern the appointment of auditors

to public companies. According to Section 327A(1), the Board of Directors of a public company must appoint an auditor within one month after the day in which the company is registered. That auditor only holds office until the first Annual General Meeting (AGM).

Consequently, at its first AGM, and at subsequent AGMs, where there is a vacancy, the

company must appoint a registered company auditor (Section 327A(3)). The auditor holds office until:

(a) he/she dies; (b) is removed or resigns; or (c) ceases to be capable of acting as auditor.

Under the Corporations Act (2001), an auditor has a statutory duty to: conduct an audit and form an audit opinion (Section 307); conduct an audit in accordance with the auditing standards (Section 307A); retain audit working papers for seven years (Section 307B); complete the auditor’s declaration (Section 307C); report to members on the annual report (Section 308); and report contraventions to ASIC (Section 311).

According to Section 307, an auditor must form an opinion about: (a) whether the financial report is in accordance with this Act, including:

(i) Section 296 (compliance with accounting standards); and (ii) Section 297 (true and fair view); and

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-13

(aa) if the financial report includes additional information under paragraph 295(3)(c)

(information included to give true and fair view of financial position and performance) whether the inclusion of that additional information was necessary to give the true and fair view required by section 297; and

(b) whether the auditor has been given all information, explanation and assistance

necessary for the conduct of the audit; and (c) whether the company, registered scheme or disclosing entity has kept financial

records sufficient to enable a financial report to be prepared and audited; and (d) whether the company, registered scheme or disclosing entity has kept other

records and registers as required by this Act. This audit opinion must be presented in an audit report. The audit report is covered by Section 308. This section requires the auditor to provide a report stating whether or not, in the auditor’s opinion, the financial report is properly drawn up: in accordance with Australian Accounting Standards and other mandatory

reporting requirements (Section 296); and so as to give a “true and fair” view of the matters with which they are required to

deal (Section 297). There are two types of audit opinions: unqualified (no issues of significance were discovered by the auditor); and qualified (the auditor has discovered an issue of some significance).

A clean audit opinion is referred to as an unqualified audit opinion. A qualified audit opinion means that the auditor has found something which s/he disagrees with or something which is of concern. The auditor must explain the nature of the qualification in a separate paragraph in the audit report. A serious qualification is one where the auditor disagrees with the treatment or disclosure of an accounting transaction. The worst type of qualification is where the auditor is unable to express an opinion due to the severe uncertainty as to whether the entity will be able to continue as a going concern. This is referred to as an “inability to form an opinion”. If, in the auditor’s opinion, the financial statements are not drawn up in accordance with a particular Accounting Standard, the audit report must give particulars of the quantified financial effect thereof on the financial statements (Section 308(2)). A sample audit report for a public company with an unqualified opinion is presented below.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-14

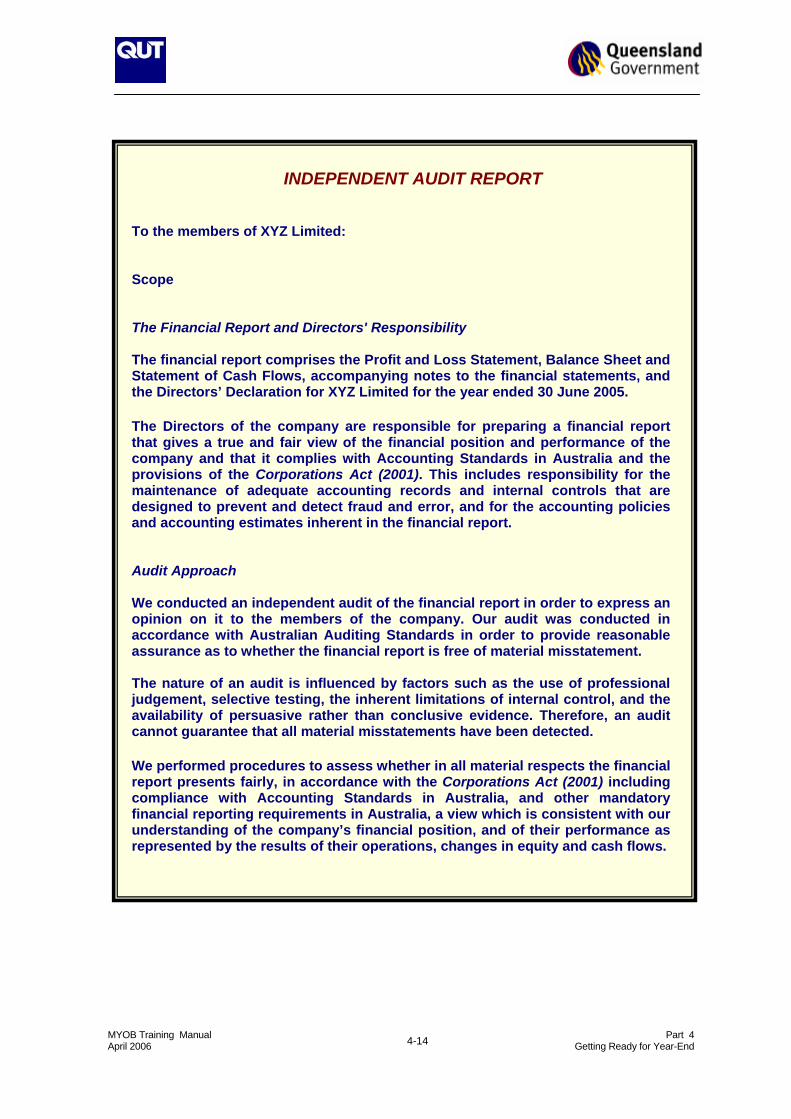

INDEPENDENT AUDIT REPORT

To the members of XYZ Limited: Scope The Financial Report and Directors' Responsibility The financial report comprises the Profit and Loss Statement, Balance Sheet and Statement of Cash Flows, accompanying notes to the financial statements, and the Directors’ Declaration for XYZ Limited for the year ended 30 June 2005.

The Directors of the company are responsible for preparing a financial report that gives a true and fair view of the financial position and performance of the company and that it complies with Accounting Standards in Australia and the provisions of the Corporations Act (2001). This includes responsibility for the maintenance of adequate accounting records and internal controls that are designed to prevent and detect fraud and error, and for the accounting policies and accounting estimates inherent in the financial report. Audit Approach

We conducted an independent audit of the financial report in order to express an opinion on it to the members of the company. Our audit was conducted in accordance with Australian Auditing Standards in order to provide reasonable assurance as to whether the financial report is free of material misstatement. The nature of an audit is influenced by factors such as the use of professional judgement, selective testing, the inherent limitations of internal control, and the availability of persuasive rather than conclusive evidence. Therefore, an audit cannot guarantee that all material misstatements have been detected.

We performed procedures to assess whether in all material respects the financial report presents fairly, in accordance with the Corporations Act (2001) including compliance with Accounting Standards in Australia, and other mandatory financial reporting requirements in Australia, a view which is consistent with our understanding of the company’s financial position, and of their performance as represented by the results of their operations, changes in equity and cash flows.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-15

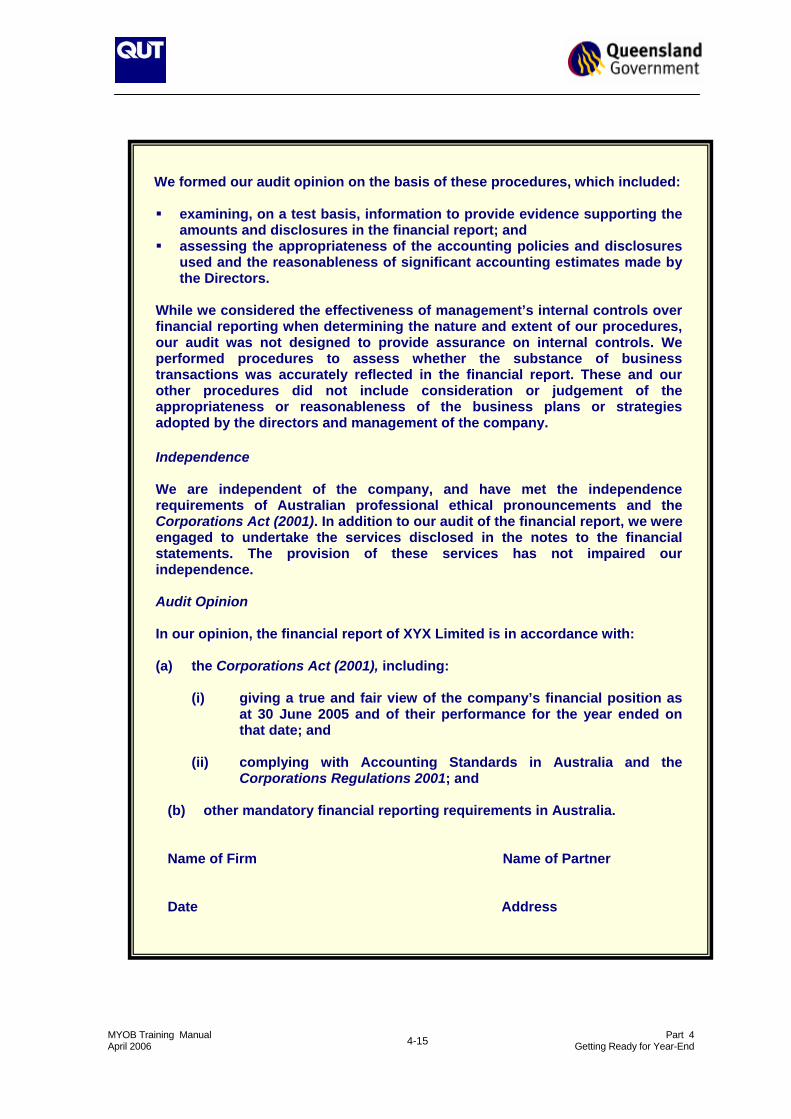

We formed our audit opinion on the basis of these procedures, which included:

examining, on a test basis, information to provide evidence supporting the amounts and disclosures in the financial report; and

assessing the appropriateness of the accounting policies and disclosures used and the reasonableness of significant accounting estimates made by the Directors.

While we considered the effectiveness of management’s internal controls over financial reporting when determining the nature and extent of our procedures, our audit was not designed to provide assurance on internal controls. We performed procedures to assess whether the substance of business transactions was accurately reflected in the financial report. These and our other procedures did not include consideration or judgement of the appropriateness or reasonableness of the business plans or strategies adopted by the directors and management of the company.

Independence We are independent of the company, and have met the independence requirements of Australian professional ethical pronouncements and the Corporations Act (2001). In addition to our audit of the financial report, we were engaged to undertake the services disclosed in the notes to the financial statements. The provision of these services has not impaired our independence.

Audit Opinion

In our opinion, the financial report of XYX Limited is in accordance with:

(a) the Corporations Act (2001), including:

(i) giving a true and fair view of the company’s financial position as

at 30 June 2005 and of their performance for the year ended on that date; and

(ii) complying with Accounting Standards in Australia and the

Corporations Regulations 2001; and

(b) other mandatory financial reporting requirements in Australia.

Name of Firm Name of Partner

Date Address

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-16

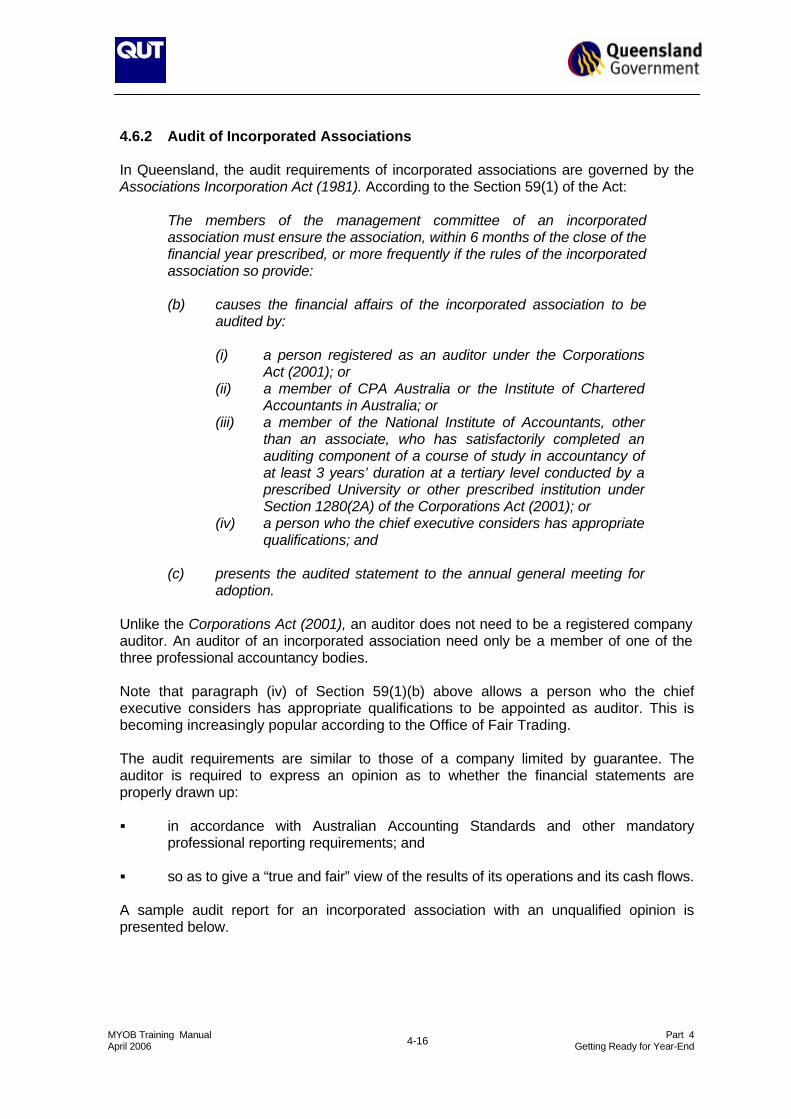

4.6.2 Audit of Incorporated Associations

In Queensland, the audit requirements of incorporated associations are governed by the Associations Incorporation Act (1981). According to the Section 59(1) of the Act: The members of the management committee of an incorporated

association must ensure the association, within 6 months of the close of the financial year prescribed, or more frequently if the rules of the incorporated association so provide:

(b) causes the financial affairs of the incorporated association to be

audited by:

(i) a person registered as an auditor under the Corporations Act (2001); or

(ii) a member of CPA Australia or the Institute of Chartered Accountants in Australia; or

(iii) a member of the National Institute of Accountants, other than an associate, who has satisfactorily completed an auditing component of a course of study in accountancy of at least 3 years’ duration at a tertiary level conducted by a prescribed University or other prescribed institution under Section 1280(2A) of the Corporations Act (2001); or

(iv) a person who the chief executive considers has appropriate qualifications; and

(c) presents the audited statement to the annual general meeting for

adoption. Unlike the Corporations Act (2001), an auditor does not need to be a registered company auditor. An auditor of an incorporated association need only be a member of one of the three professional accountancy bodies. Note that paragraph (iv) of Section 59(1)(b) above allows a person who the chief executive considers has appropriate qualifications to be appointed as auditor. This is becoming increasingly popular according to the Office of Fair Trading. The audit requirements are similar to those of a company limited by guarantee. The auditor is required to express an opinion as to whether the financial statements are properly drawn up: in accordance with Australian Accounting Standards and other mandatory

professional reporting requirements; and so as to give a “true and fair” view of the results of its operations and its cash flows.

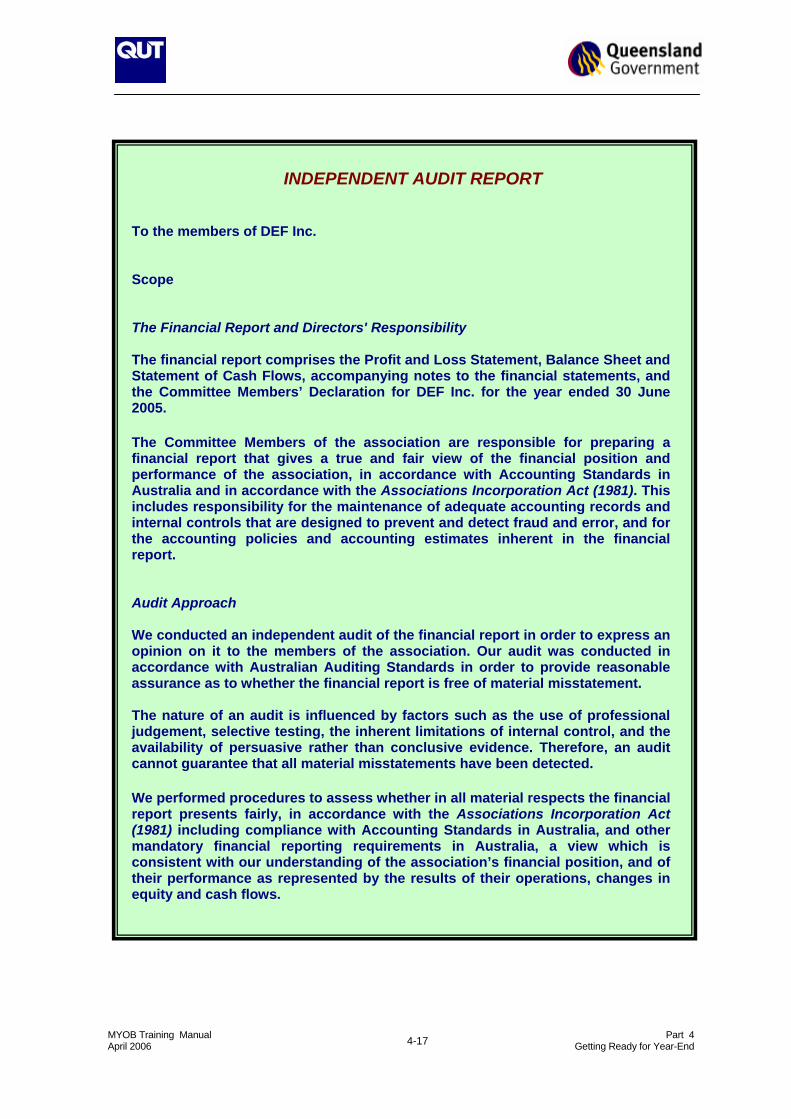

A sample audit report for an incorporated association with an unqualified opinion is presented below.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-17

INDEPENDENT AUDIT REPORT

To the members of DEF Inc. Scope The Financial Report and Directors' Responsibility The financial report comprises the Profit and Loss Statement, Balance Sheet and Statement of Cash Flows, accompanying notes to the financial statements, and the Committee Members’ Declaration for DEF Inc. for the year ended 30 June 2005.

The Committee Members of the association are responsible for preparing a financial report that gives a true and fair view of the financial position and performance of the association, in accordance with Accounting Standards in Australia and in accordance with the Associations Incorporation Act (1981). This includes responsibility for the maintenance of adequate accounting records and internal controls that are designed to prevent and detect fraud and error, and for the accounting policies and accounting estimates inherent in the financial report. Audit Approach

We conducted an independent audit of the financial report in order to express an opinion on it to the members of the association. Our audit was conducted in accordance with Australian Auditing Standards in order to provide reasonable assurance as to whether the financial report is free of material misstatement. The nature of an audit is influenced by factors such as the use of professional judgement, selective testing, the inherent limitations of internal control, and the availability of persuasive rather than conclusive evidence. Therefore, an audit cannot guarantee that all material misstatements have been detected.

We performed procedures to assess whether in all material respects the financial report presents fairly, in accordance with the Associations Incorporation Act (1981) including compliance with Accounting Standards in Australia, and other mandatory financial reporting requirements in Australia, a view which is consistent with our understanding of the association’s financial position, and of their performance as represented by the results of their operations, changes in equity and cash flows.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-18

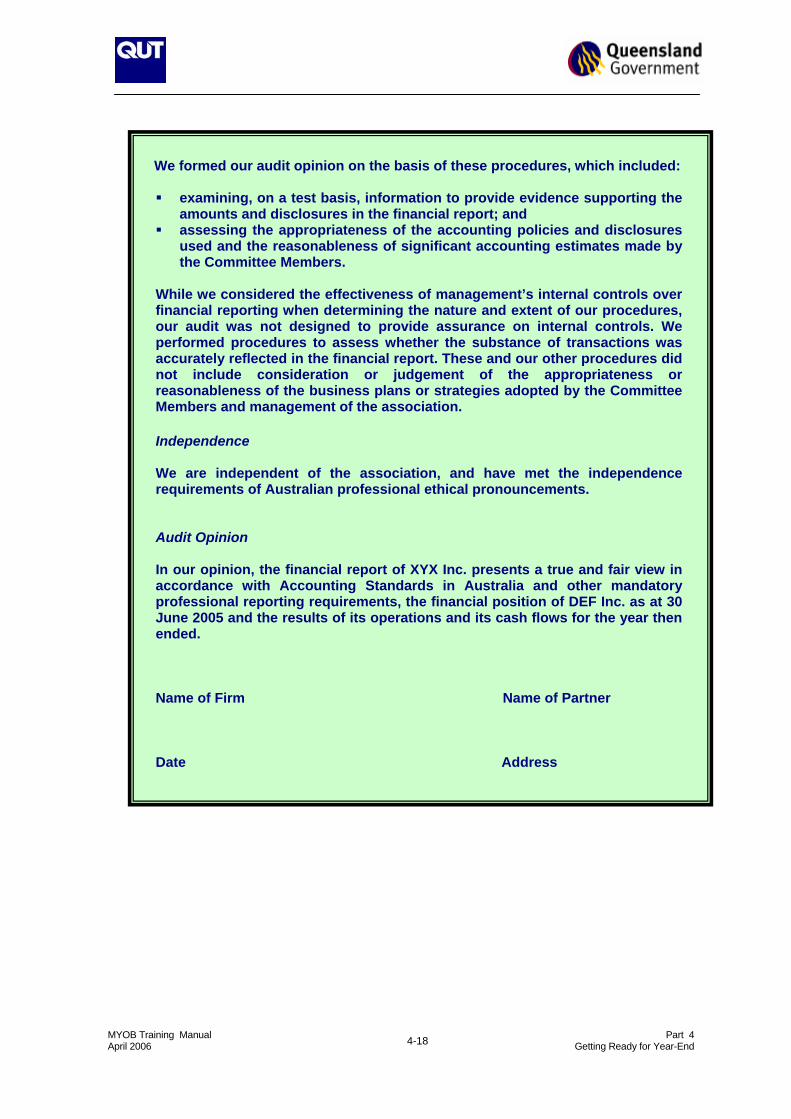

We formed our audit opinion on the basis of these procedures, which included:

examining, on a test basis, information to provide evidence supporting the amounts and disclosures in the financial report; and

assessing the appropriateness of the accounting policies and disclosures used and the reasonableness of significant accounting estimates made by the Committee Members.

While we considered the effectiveness of management’s internal controls over financial reporting when determining the nature and extent of our procedures, our audit was not designed to provide assurance on internal controls. We performed procedures to assess whether the substance of transactions was accurately reflected in the financial report. These and our other procedures did not include consideration or judgement of the appropriateness or reasonableness of the business plans or strategies adopted by the Committee Members and management of the association.

Independence We are independent of the association, and have met the independence requirements of Australian professional ethical pronouncements.

Audit Opinion

In our opinion, the financial report of XYX Inc. presents a true and fair view in accordance with Accounting Standards in Australia and other mandatory professional reporting requirements, the financial position of DEF Inc. as at 30 June 2005 and the results of its operations and its cash flows for the year then ended.

Name of Firm Name of Partner

Date Address

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-19

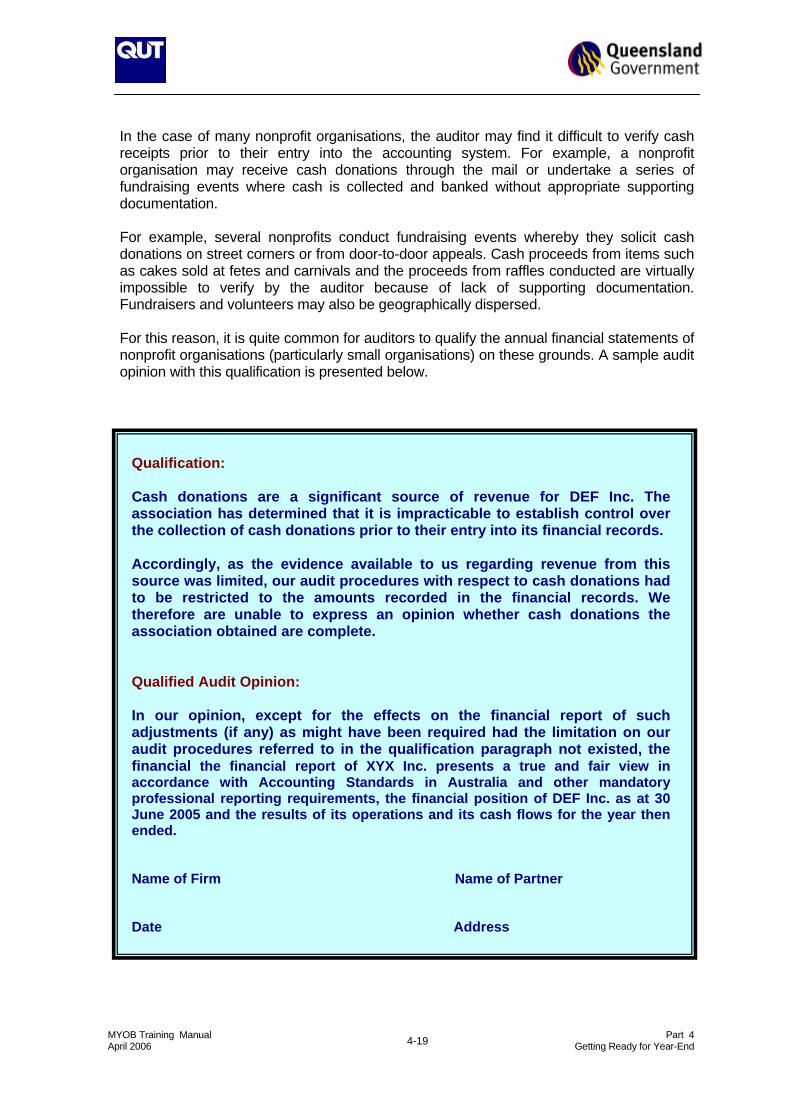

In the case of many nonprofit organisations, the auditor may find it difficult to verify cash receipts prior to their entry into the accounting system. For example, a nonprofit organisation may receive cash donations through the mail or undertake a series of fundraising events where cash is collected and banked without appropriate supporting documentation. For example, several nonprofits conduct fundraising events whereby they solicit cash donations on street corners or from door-to-door appeals. Cash proceeds from items such as cakes sold at fetes and carnivals and the proceeds from raffles conducted are virtually impossible to verify by the auditor because of lack of supporting documentation. Fundraisers and volunteers may also be geographically dispersed. For this reason, it is quite common for auditors to qualify the annual financial statements of nonprofit organisations (particularly small organisations) on these grounds. A sample audit opinion with this qualification is presented below.

Qualification:

Cash donations are a significant source of revenue for DEF Inc. The association has determined that it is impracticable to establish control over the collection of cash donations prior to their entry into its financial records.

Accordingly, as the evidence available to us regarding revenue from this

source was limited, our audit procedures with respect to cash donations had to be restricted to the amounts recorded in the financial records. We therefore are unable to express an opinion whether cash donations the association obtained are complete.

Qualified Audit Opinion:

In our opinion, except for the effects on the financial report of such adjustments (if any) as might have been required had the limitation on our audit procedures referred to in the qualification paragraph not existed, the financial the financial report of XYX Inc. presents a true and fair view in accordance with Accounting Standards in Australia and other mandatory professional reporting requirements, the financial position of DEF Inc. as at 30 June 2005 and the results of its operations and its cash flows for the year then ended. Name of Firm Name of Partner Date Address

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-20

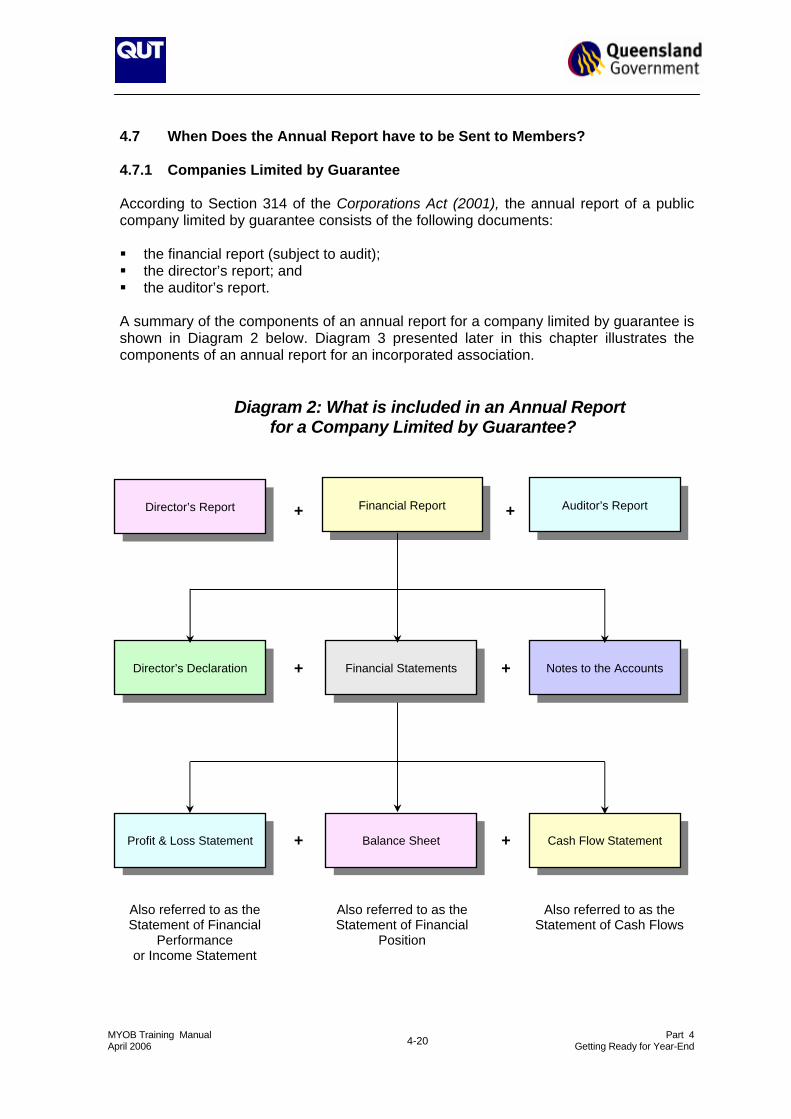

4.7 When Does the Annual Report have to be Sent to Members? 4.7.1 Companies Limited by Guarantee According to Section 314 of the Corporations Act (2001), the annual report of a public company limited by guarantee consists of the following documents: the financial report (subject to audit); the director’s report; and the auditor’s report.

A summary of the components of an annual report for a company limited by guarantee is shown in Diagram 2 below. Diagram 3 presented later in this chapter illustrates the components of an annual report for an incorporated association.

Diagram 2: What is included in an Annual Report

for a Company Limited by Guarantee?

Financial Report

Auditor’s Report Director’s Report

Director’s Declaration

Notes to the Accounts

Financial Statements

+ +

+ +

Profit & Loss Statement

Cash Flow Statement

Balance Sheet + +

Also referred to as the Statement of Financial

Performance or Income Statement

Also referred to as the Statement of Financial

Position

Also referred to as the Statement of Cash Flows

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-21

According to Section 315(1) a public company must send the annual report to its members by the earlier of: (a) 21 days before the AGM after the end of the financial year; or (b) four months after the end of the financial year whichever is the earlier. According to Section 250N(2), a public company’s annual general meeting must be held at least once in each calendar year and within five months after the end of its financial year.

EXAMPLE: Assume that XYZ Limited (a company limited by guarantee) has a financial year ended 30 June. It has just prepared its financial report for the year ended 30 June 2005. According to Section 250N(2), XYZ Limited must conduct its Annual General Meeting no later than 30 November 2005 (i.e. within five months after the end of the financial year). Assuming that XYZ limited holds its AGM on 12 November 2005, it is required to send the annual report to its members by the earlier of: (a) 21 days before the AGM after the end of the financial year (22 October

2005); or (b) 4 months after the end of the financial year (30 October 2005). Hence, XYZ Limited must send its annual report to the members by 22 October 2005. In the case of public companies, Section 314 of the Corporations Act (2001) permits these organisations to send their members either a full annual report or a concise annual report. A concise annual report is an abbreviated version of the full annual report. It consists of a Profit and Loss Statement, a Balance Sheet, a Cash Flow Statement as well as the director’s report, a statement by the auditor that the financial report has been audited (including whether the concise financial report complies with accounting standards) and a copy of the audit qualification (if relevant). The concise financial report must also contain a discussion and analysis by management on the principal factors affecting the organisations financial performance, financial position and financing and investing activities.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-22

Finally, the concise financial report of a public company must also contain a statement confirming that it is a concise financial report and that the full financial report and auditor's report will be sent to the member free of charge if the member asks for them. 4.7.2 Incorporated Associations According to Section 59(1) of the Associations Incorporation Act (1981), the annual report of an incorporated association must be prepared within six months after the end of the financial year or more frequently if the rules of the incorporated association so provide. Under the Associations Incorporation Act (1981), there is no requirement for the association to send the annual report to members before the AGM. However, this may be provided for in the association’s rules. According to Section 55, an incorporated association must hold its first general meeting within 18 months after the day the association is incorporated provided it is incorporated within six months before the date of the financial year. Section 56 provides that the association must hold subsequent AGMs: (a) at least once each year; and (b) within six months after the end of the associations previous financial year. As the timing of both events is the same, the incorporated association will have complied with the requirements of the Act provided the audited accounts are presented to members at the AGM no later than six months after the end of the association’s financial year.

EXAMPLE: Assume that DEF Inc. (an incorporated association) has a financial year ended 30 June. It has just prepared its financial report for the year ended 30 June 2005. According to Section 59(1)(a), DEF Inc. must conduct have its financial report prepared before 30 December 2005 (i.e. within six months after the end of the financial year). The audited accounts must be presented at the AGM, which must also be conducted within six months after the end of the financial year.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-23

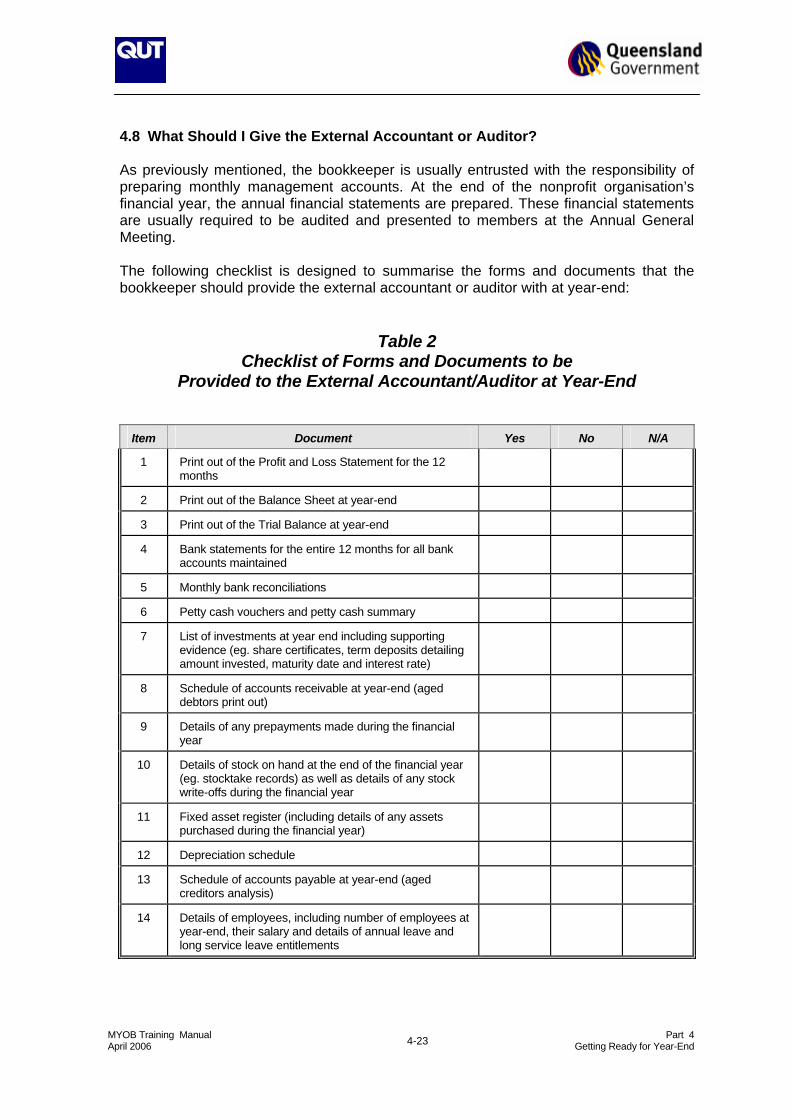

4.8 What Should I Give the External Accountant or Auditor? As previously mentioned, the bookkeeper is usually entrusted with the responsibility of preparing monthly management accounts. At the end of the nonprofit organisation’s financial year, the annual financial statements are prepared. These financial statements are usually required to be audited and presented to members at the Annual General Meeting. The following checklist is designed to summarise the forms and documents that the bookkeeper should provide the external accountant or auditor with at year-end:

Table 2 Checklist of Forms and Documents to be

Provided to the External Accountant/Auditor at Year-End

Item Document Yes No N/A

1 Print out of the Profit and Loss Statement for the 12 months

2 Print out of the Balance Sheet at year-end

3 Print out of the Trial Balance at year-end

4 Bank statements for the entire 12 months for all bank accounts maintained

5 Monthly bank reconciliations

6 Petty cash vouchers and petty cash summary

7 List of investments at year end including supporting evidence (eg. share certificates, term deposits detailing amount invested, maturity date and interest rate)

8 Schedule of accounts receivable at year-end (aged debtors print out)

9 Details of any prepayments made during the financial year

10 Details of stock on hand at the end of the financial year (eg. stocktake records) as well as details of any stock write-offs during the financial year

11 Fixed asset register (including details of any assets purchased during the financial year)

12 Depreciation schedule

13 Schedule of accounts payable at year-end (aged creditors analysis)

14 Details of employees, including number of employees at year-end, their salary and details of annual leave and long service leave entitlements

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-24

Table 2 (Continued) Checklist of Forms and Documents to be

Provided to the External Accountant/Auditor at Year-End

Item Document Yes No N/A

15 Copies of loan contracts, lease agreements or hire purchase agreements entered into by the nonprofit organisation

16 Details of tied funds or restricted funds (in the case of DGRs)

17 Details of all non-monetary donations and supporting documentation as to their market value

18 Names of Board/ Committee Members and the number of board meeting held during the financial year (including details of board attendance) as well as details of appointment/resignation of committee members/directors during the financial year

19 Minutes of Meeting of Management Committee/Directors during the financial year

20 Register of Members

21 Details of amounts paid to committee members/directors during the financial year

22 Copies of any resolutions passed during the financial year (including amendments to the Constitution/rules)

23 Investment statements (eg. dividend statements, managed fund distribution statements etc.)

24 Details of any grants received during the financial year (provide copies of supporting documentation)

25 Copies of the gift receipts for significant donations made by donors during the financial year

26 Copies of each BAS/IAS lodged with the Australian Taxation Office during the financial year showing the amount of GST paid and received as well as PAYG withholding tax

27 Copies of the all PAYG Payment Summaries provided to each employee as well as the annual PAYG Reconciliation Statement showing the gross wages paid to employees during the financial year as well as PAYG withholding tax deducted

28 Permits for raffles, bingos and art unions

29 Details of any other legal correspondence relating to the organisation such as legal claims etc.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-25

TIP: Given the number of documents that need to be passed over to the

external accountant/auditor, it is strongly recommended that the bookkeeper place this information in a lever arch folder. Dividers (or tabs) can be inserted into the folder with each section marked.

It is also useful to place a copy of last year’s audited financial statements at the front. Remember that it has been one year since the external accountant/auditor has seen your accounts. This will serve as a useful reminder and re-acquaint them with your financial statements. Remember, anything you can do to make the task easier and simpler and for the auditor should result in significant time and cost reductions for the auditor. Hopefully, this will ultimately be passed onto the nonprofit organisation in the form of a reduced audit fee.

4.9 Audit Engagement Letter When an auditor is engaged to conduct an audit, they will usually provide the nonprofit organisation with an engagement letter. The purpose of the engagement letter is to formally document the terms of the audit engagement (preferably before the commencement of the audit). The engagement letter ensures there is a clear understanding by the association’s management committee and the auditor of the extent of the auditor’s duties and responsibilities and is designed to avoid uncertainty and misunderstandings with respect to the engagement. The engagement letter also documents and confirms the acceptance of the appointment as well as the objective and scope of the engagement. It also highlights the extent of the auditor’s responsibilities to the entity and the form of any reports. The Auditing and Assurances Standards Board (AUSAB) has issued AUS 204 Terms of Audit Engagements which provides a standard engagement letter for use by auditors. A copy of a sample audit engagement letter (adapted for an incorporated association) is reproduced on the following pages.

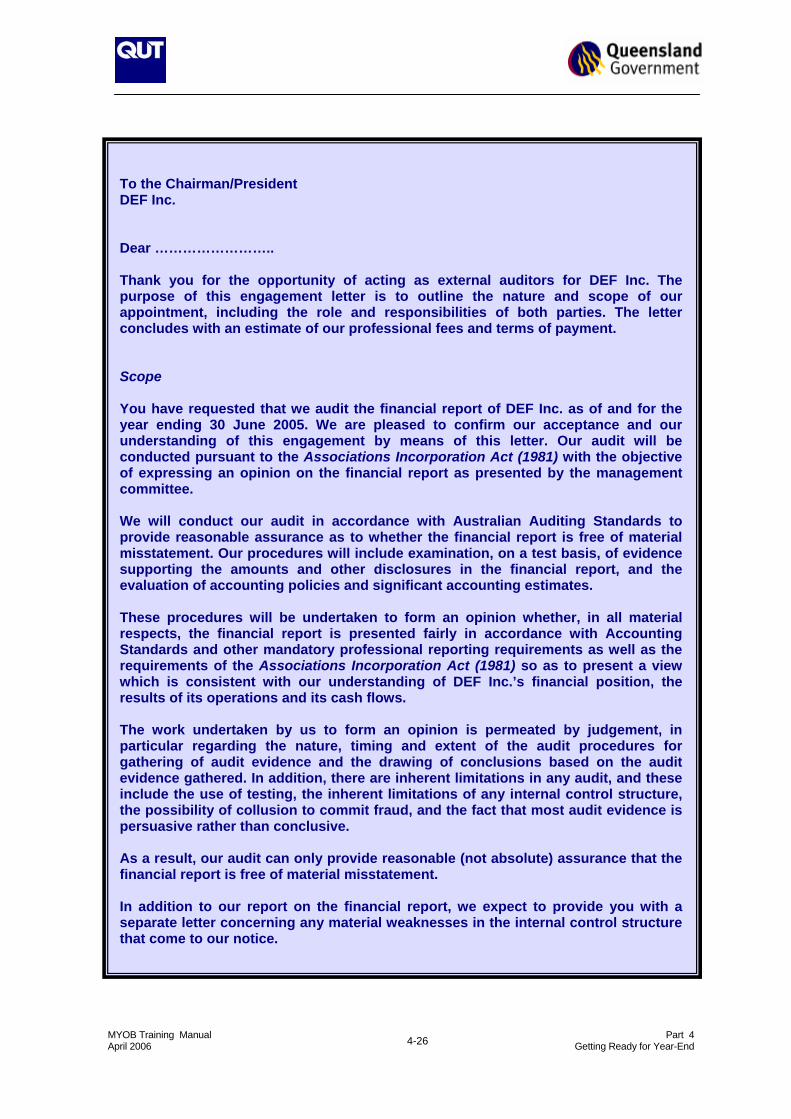

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-26

To the Chairman/President DEF Inc. Dear …………………….. Thank you for the opportunity of acting as external auditors for DEF Inc. The purpose of this engagement letter is to outline the nature and scope of our appointment, including the role and responsibilities of both parties. The letter concludes with an estimate of our professional fees and terms of payment. Scope You have requested that we audit the financial report of DEF Inc. as of and for the year ending 30 June 2005. We are pleased to confirm our acceptance and our understanding of this engagement by means of this letter. Our audit will be conducted pursuant to the Associations Incorporation Act (1981) with the objective of expressing an opinion on the financial report as presented by the management committee. We will conduct our audit in accordance with Australian Auditing Standards to provide reasonable assurance as to whether the financial report is free of material misstatement. Our procedures will include examination, on a test basis, of evidence supporting the amounts and other disclosures in the financial report, and the evaluation of accounting policies and significant accounting estimates. These procedures will be undertaken to form an opinion whether, in all material respects, the financial report is presented fairly in accordance with Accounting Standards and other mandatory professional reporting requirements as well as the requirements of the Associations Incorporation Act (1981) so as to present a view which is consistent with our understanding of DEF Inc.’s financial position, the results of its operations and its cash flows. The work undertaken by us to form an opinion is permeated by judgement, in particular regarding the nature, timing and extent of the audit procedures for gathering of audit evidence and the drawing of conclusions based on the audit evidence gathered. In addition, there are inherent limitations in any audit, and these include the use of testing, the inherent limitations of any internal control structure, the possibility of collusion to commit fraud, and the fact that most audit evidence is persuasive rather than conclusive. As a result, our audit can only provide reasonable (not absolute) assurance that the financial report is free of material misstatement. In addition to our report on the financial report, we expect to provide you with a separate letter concerning any material weaknesses in the internal control structure that come to our notice.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-27

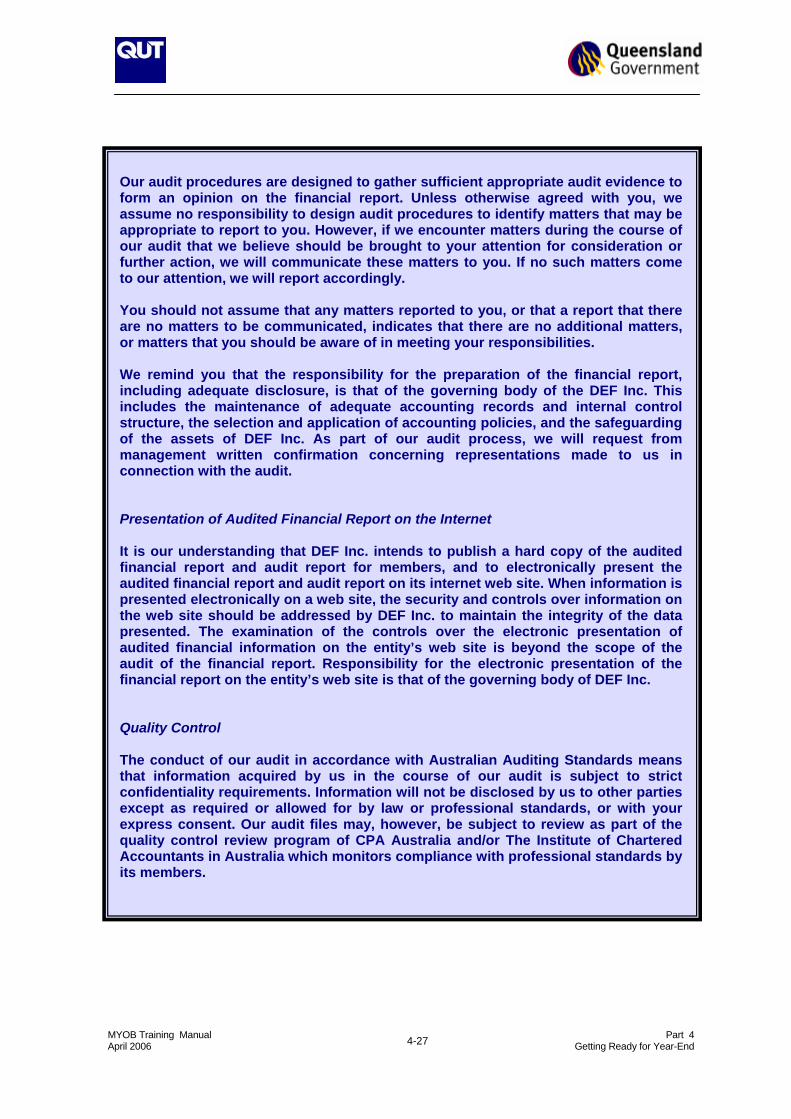

Our audit procedures are designed to gather sufficient appropriate audit evidence to form an opinion on the financial report. Unless otherwise agreed with you, we assume no responsibility to design audit procedures to identify matters that may be appropriate to report to you. However, if we encounter matters during the course of our audit that we believe should be brought to your attention for consideration or further action, we will communicate these matters to you. If no such matters come to our attention, we will report accordingly. You should not assume that any matters reported to you, or that a report that there are no matters to be communicated, indicates that there are no additional matters, or matters that you should be aware of in meeting your responsibilities. We remind you that the responsibility for the preparation of the financial report, including adequate disclosure, is that of the governing body of the DEF Inc. This includes the maintenance of adequate accounting records and internal control structure, the selection and application of accounting policies, and the safeguarding of the assets of DEF Inc. As part of our audit process, we will request from management written confirmation concerning representations made to us in connection with the audit. Presentation of Audited Financial Report on the Internet It is our understanding that DEF Inc. intends to publish a hard copy of the audited financial report and audit report for members, and to electronically present the audited financial report and audit report on its internet web site. When information is presented electronically on a web site, the security and controls over information on the web site should be addressed by DEF Inc. to maintain the integrity of the data presented. The examination of the controls over the electronic presentation of audited financial information on the entity’s web site is beyond the scope of the audit of the financial report. Responsibility for the electronic presentation of the financial report on the entity’s web site is that of the governing body of DEF Inc. Quality Control The conduct of our audit in accordance with Australian Auditing Standards means that information acquired by us in the course of our audit is subject to strict confidentiality requirements. Information will not be disclosed by us to other parties except as required or allowed for by law or professional standards, or with your express consent. Our audit files may, however, be subject to review as part of the quality control review program of CPA Australia and/or The Institute of Chartered Accountants in Australia which monitors compliance with professional standards by its members.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-28

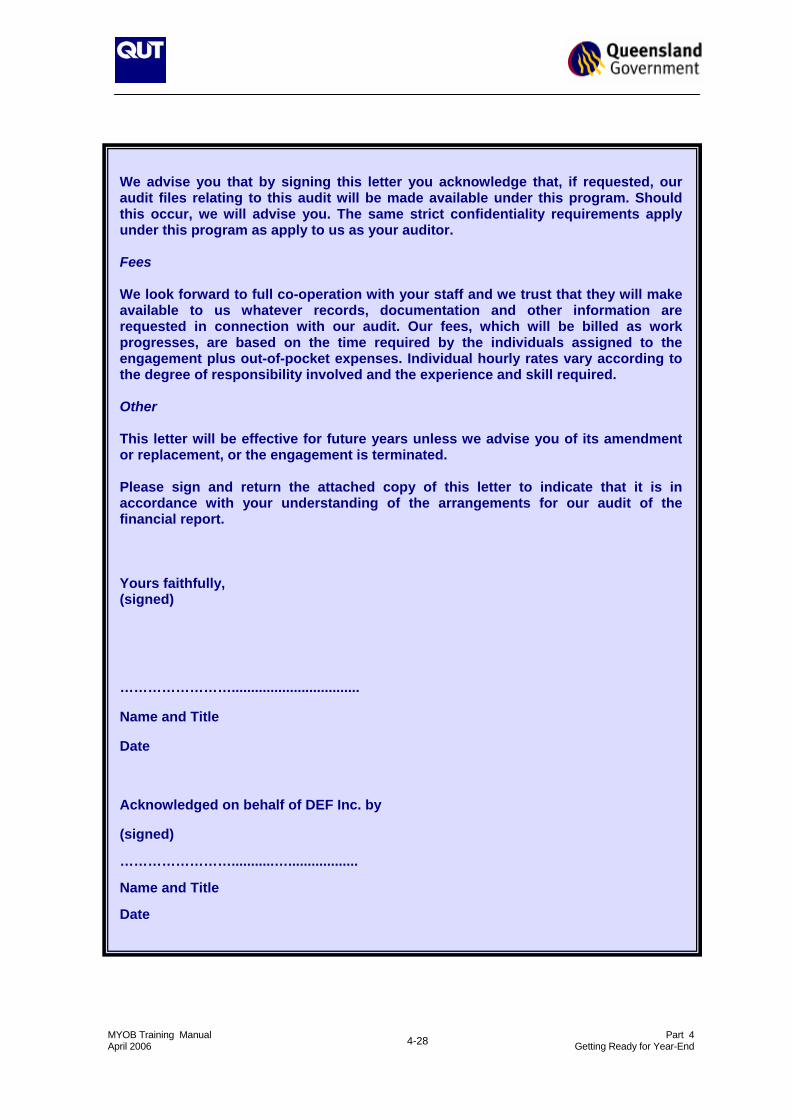

We advise you that by signing this letter you acknowledge that, if requested, our audit files relating to this audit will be made available under this program. Should this occur, we will advise you. The same strict confidentiality requirements apply under this program as apply to us as your auditor. Fees We look forward to full co-operation with your staff and we trust that they will make available to us whatever records, documentation and other information are requested in connection with our audit. Our fees, which will be billed as work progresses, are based on the time required by the individuals assigned to the engagement plus out-of-pocket expenses. Individual hourly rates vary according to the degree of responsibility involved and the experience and skill required. Other This letter will be effective for future years unless we advise you of its amendment or replacement, or the engagement is terminated. Please sign and return the attached copy of this letter to indicate that it is in accordance with your understanding of the arrangements for our audit of the financial report. Yours faithfully, (signed)

…………………….................................

Name and Title

Date

Acknowledged on behalf of DEF Inc. by

(signed)

……………………...........….................. Name and Title Date

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-29

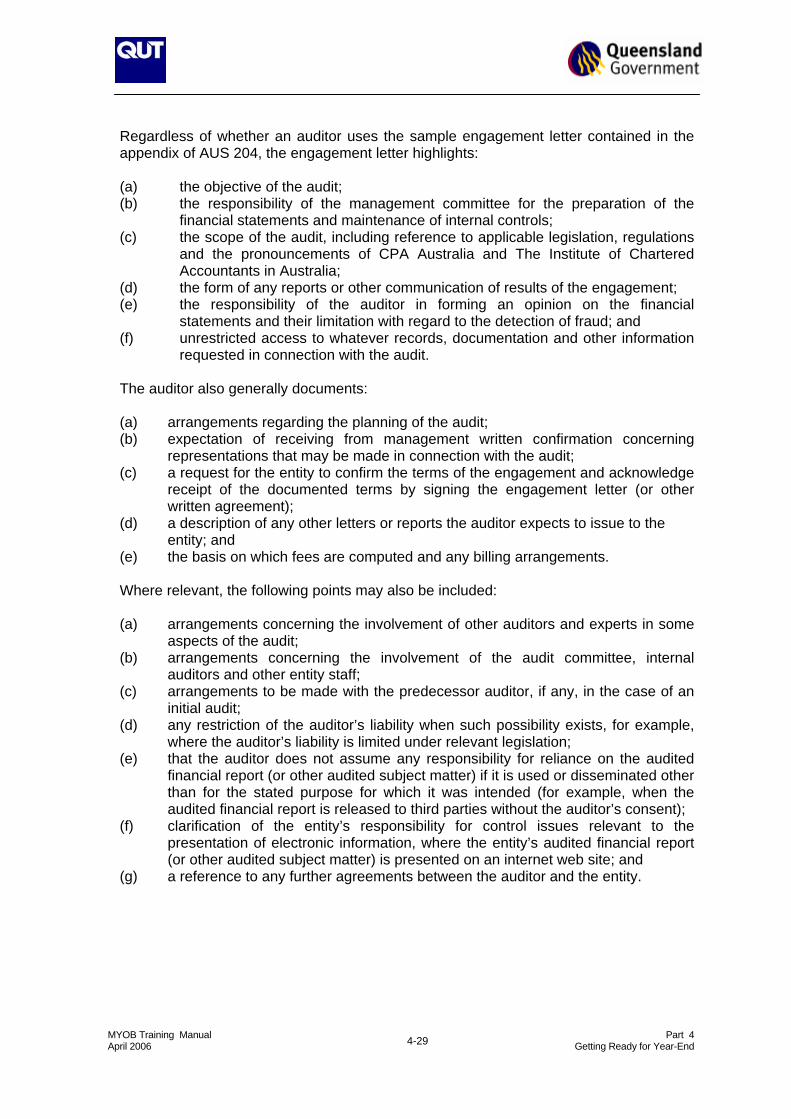

Regardless of whether an auditor uses the sample engagement letter contained in the appendix of AUS 204, the engagement letter highlights: (a) the objective of the audit; (b) the responsibility of the management committee for the preparation of the

financial statements and maintenance of internal controls; (c) the scope of the audit, including reference to applicable legislation, regulations

and the pronouncements of CPA Australia and The Institute of Chartered Accountants in Australia;

(d) the form of any reports or other communication of results of the engagement; (e) the responsibility of the auditor in forming an opinion on the financial

statements and their limitation with regard to the detection of fraud; and (f) unrestricted access to whatever records, documentation and other information

requested in connection with the audit. The auditor also generally documents: (a) arrangements regarding the planning of the audit; (b) expectation of receiving from management written confirmation concerning

representations that may be made in connection with the audit; (c) a request for the entity to confirm the terms of the engagement and acknowledge

receipt of the documented terms by signing the engagement letter (or other written agreement);

(d) a description of any other letters or reports the auditor expects to issue to the entity; and

(e) the basis on which fees are computed and any billing arrangements. Where relevant, the following points may also be included: (a) arrangements concerning the involvement of other auditors and experts in some

aspects of the audit; (b) arrangements concerning the involvement of the audit committee, internal

auditors and other entity staff; (c) arrangements to be made with the predecessor auditor, if any, in the case of an

initial audit; (d) any restriction of the auditor’s liability when such possibility exists, for example,

where the auditor’s liability is limited under relevant legislation; (e) that the auditor does not assume any responsibility for reliance on the audited

financial report (or other audited subject matter) if it is used or disseminated other than for the stated purpose for which it was intended (for example, when the audited financial report is released to third parties without the auditor’s consent);

(f) clarification of the entity’s responsibility for control issues relevant to the presentation of electronic information, where the entity’s audited financial report (or other audited subject matter) is presented on an internet web site; and

(g) a reference to any further agreements between the auditor and the entity.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-30

4.10 Management Representation Letter At the conclusion of the audit, the auditor usually provides the management committee or board of directors with a letter to be put on the organisation’s letterhead and signed by the Chairman. This is referred to as the “Management Representation Letter”. The purpose of the management representation letter is to formally acknowledge that the auditor may have relied upon representation (oral discussions, written statements) by management during the course of the audit. Furthermore, the management representation letter formally acknowledges that the management committee or board of directors is responsible for the preparation of the financial statements and the maintenance of adequate accounting records and internal controls. Although representation letters are signed by management, they are normally prepared by the auditor and submitted to the management for signing. A copy of a sample management representation letter (adapted for an incorporated association) is reproduced on the following pages.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-31

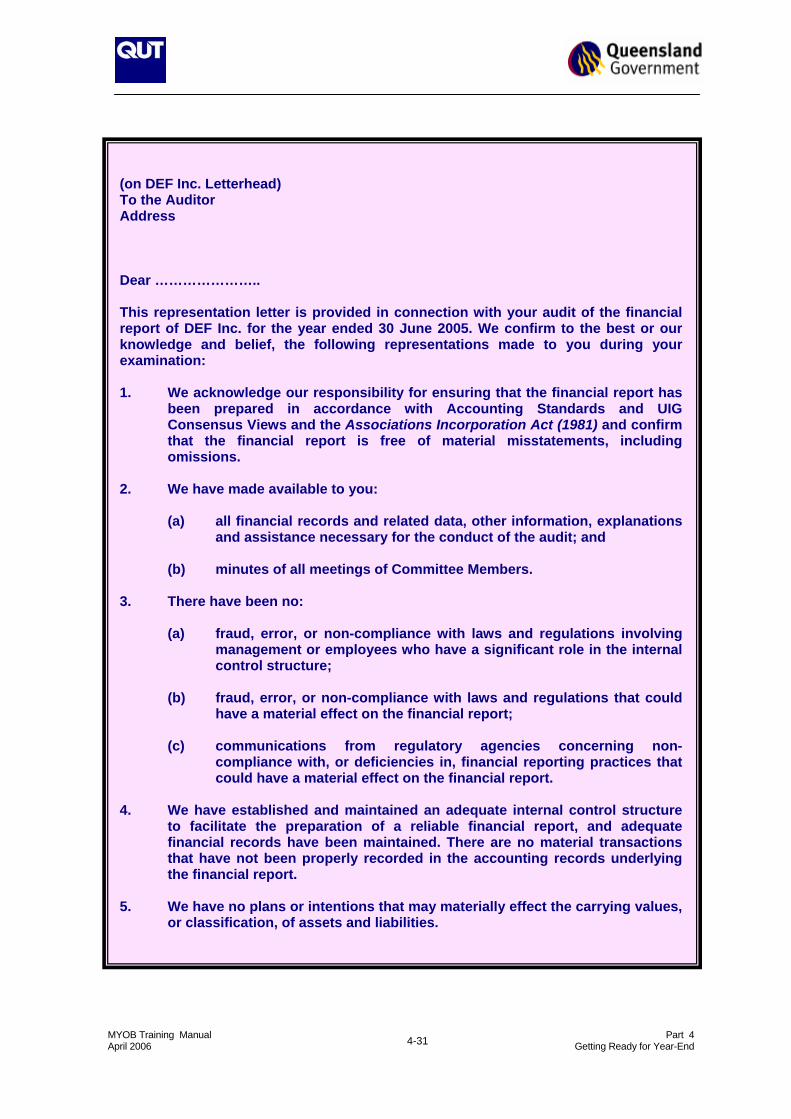

(on DEF Inc. Letterhead) To the Auditor Address Dear ………………….. This representation letter is provided in connection with your audit of the financial report of DEF Inc. for the year ended 30 June 2005. We confirm to the best or our knowledge and belief, the following representations made to you during your examination: 1. We acknowledge our responsibility for ensuring that the financial report has

been prepared in accordance with Accounting Standards and UIG Consensus Views and the Associations Incorporation Act (1981) and confirm that the financial report is free of material misstatements, including omissions.

2. We have made available to you:

(a) all financial records and related data, other information, explanations and assistance necessary for the conduct of the audit; and

(b) minutes of all meetings of Committee Members.

3. There have been no:

(a) fraud, error, or non-compliance with laws and regulations involving management or employees who have a significant role in the internal control structure;

(b) fraud, error, or non-compliance with laws and regulations that could

have a material effect on the financial report; (c) communications from regulatory agencies concerning non-

compliance with, or deficiencies in, financial reporting practices that could have a material effect on the financial report.

4. We have established and maintained an adequate internal control structure

to facilitate the preparation of a reliable financial report, and adequate financial records have been maintained. There are no material transactions that have not been properly recorded in the accounting records underlying the financial report.

5. We have no plans or intentions that may materially effect the carrying values,

or classification, of assets and liabilities.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-32

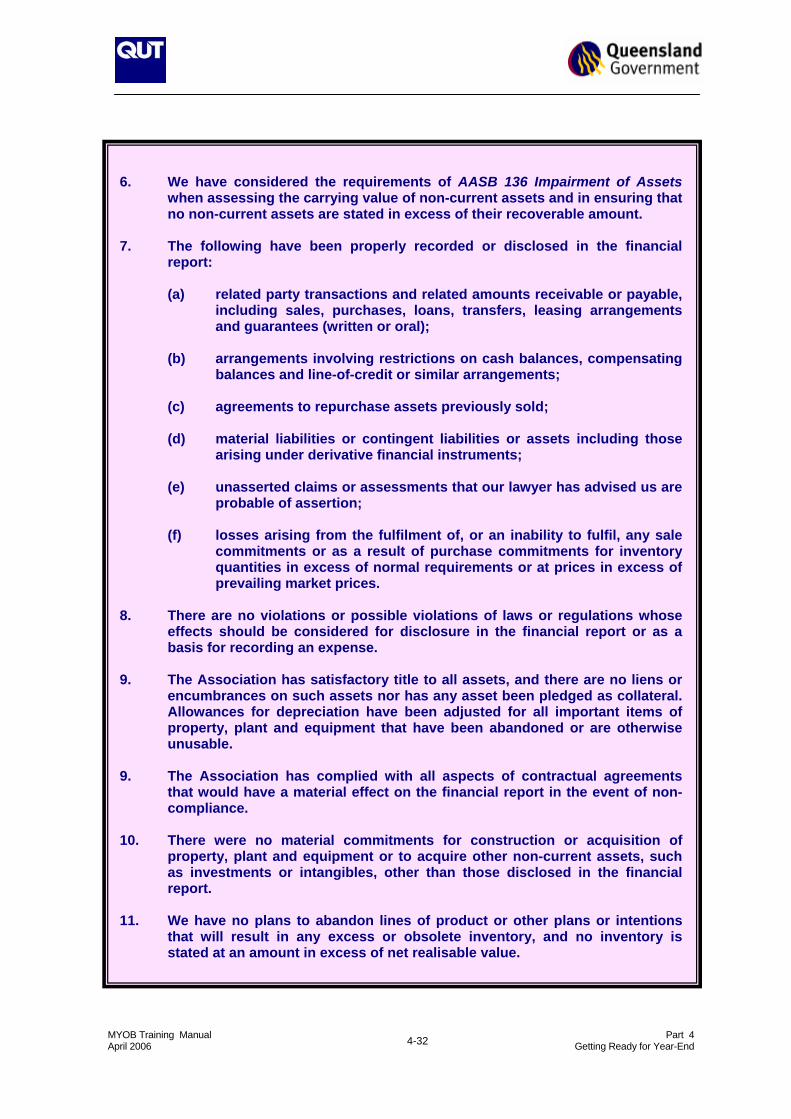

6. We have considered the requirements of AASB 136 Impairment of Assets

when assessing the carrying value of non-current assets and in ensuring that no non-current assets are stated in excess of their recoverable amount.

7. The following have been properly recorded or disclosed in the financial

report:

(a) related party transactions and related amounts receivable or payable, including sales, purchases, loans, transfers, leasing arrangements and guarantees (written or oral);

(b) arrangements involving restrictions on cash balances, compensating

balances and line-of-credit or similar arrangements; (c) agreements to repurchase assets previously sold; (d) material liabilities or contingent liabilities or assets including those

arising under derivative financial instruments; (e) unasserted claims or assessments that our lawyer has advised us are

probable of assertion; (f) losses arising from the fulfilment of, or an inability to fulfil, any sale

commitments or as a result of purchase commitments for inventory quantities in excess of normal requirements or at prices in excess of prevailing market prices.

8. There are no violations or possible violations of laws or regulations whose

effects should be considered for disclosure in the financial report or as a basis for recording an expense.

9. The Association has satisfactory title to all assets, and there are no liens or

encumbrances on such assets nor has any asset been pledged as collateral. Allowances for depreciation have been adjusted for all important items of property, plant and equipment that have been abandoned or are otherwise unusable.

9. The Association has complied with all aspects of contractual agreements

that would have a material effect on the financial report in the event of non-compliance.

10. There were no material commitments for construction or acquisition of

property, plant and equipment or to acquire other non-current assets, such as investments or intangibles, other than those disclosed in the financial report.

11. We have no plans to abandon lines of product or other plans or intentions

that will result in any excess or obsolete inventory, and no inventory is stated at an amount in excess of net realisable value.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-33

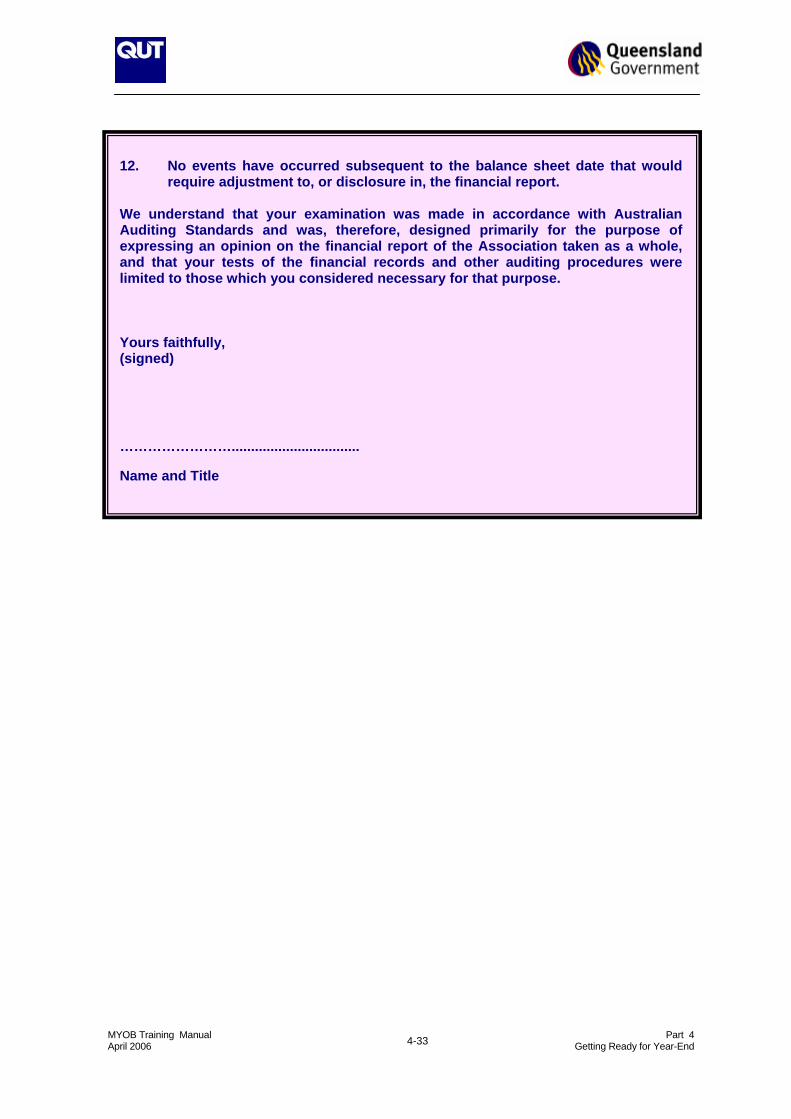

12. No events have occurred subsequent to the balance sheet date that would

require adjustment to, or disclosure in, the financial report. We understand that your examination was made in accordance with Australian Auditing Standards and was, therefore, designed primarily for the purpose of expressing an opinion on the financial report of the Association taken as a whole, and that your tests of the financial records and other auditing procedures were limited to those which you considered necessary for that purpose. Yours faithfully, (signed)

…………………….................................

Name and Title

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-34

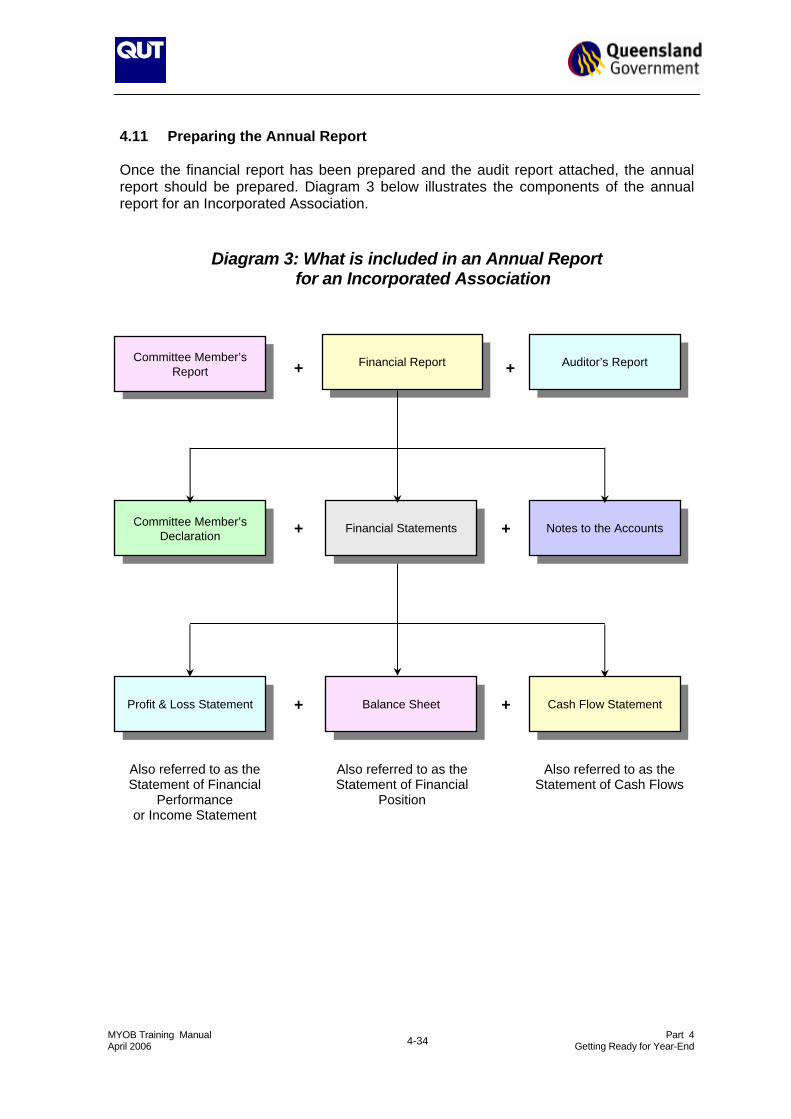

4.11 Preparing the Annual Report Once the financial report has been prepared and the audit report attached, the annual report should be prepared. Diagram 3 below illustrates the components of the annual report for an Incorporated Association.

Diagram 3: What is included in an Annual Report

for an Incorporated Association

Financial Report

Auditor’s Report Committee Member’s

Rep

ort

Committee Member’s

Declaration

Notes to the Accounts

Financial Statements

+ +

+ +

Profit & Loss Statement

Cash Flow Statement

Balance Sheet + +

Also referred to as the Statement of Financial

Performance or Income Statement

Also referred to as the Statement of Financial

Position

Also referred to as the Statement of Cash Flows

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-35

The annual report should be adapted to the requirements of each nonprofit organisation. There is no “one size, fits all” approach. For small organisations, a simple annual report will suffice. However, larger nonprofit organisations may choose to use the annual report as a fundraising/marketing tool. In May 2003, the Institute of Chartered Accountants in Australia (ICAA) released a

report entitled “A Review of Not-For-Profit Financial and Annual Reporting” revealing their findings of a review of 22 annual reports of nonprofit organisations.

The ICAA’s findings revealed that nonprofit organisations need to adopt a tailored financial reporting framework that better reflects the activities they undertake. The report stated:

“Whilst meeting the requirements imposed by Federal and State legislation the ICAA review found the reports of most not-for-profit organisations did not satisfy the needs of two of their key stakeholder groups, the donor and the funding provider”.

“Annual and Financial reports need to explain what the NFP is trying to do, how it is going about it, whether it has achieved its objectives during the year and its plans for the future. It should also help the reader understand the organisational structure and activities of the nonprofit organisation.”

The complete ICAA Report can be downloaded from the following website:

Web Link : Review of Not-For-Profit Financial and Annual Reporting

http://www.icaa.org.au/upload/download/NFP2003w.pdf

Following this review, the ICAA developed a “Checklist” to assist nonprofit organisations prepare their annual report in line with legislative requirements and public expectation for information and transparency. The checklist is divided into five components: Part 1: What we are trying to do? – It is recommended that the annual report

outline the organisations objectives in more detail than simply stating their mission statement.

Part 2: How are we going about doing it? – It is recommended that the annual

report provide a clear statement how the nonprofit organisation will obtain funding so as to meet their objectives and how they will work with other organisations in achieving those objectives.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-36

Part 3: What we have achieved during the year? – It is recommended that the

annual report summarise their financial results during the financial year, including an analysis of key trends. Key performance indicators (KPI’s) should also be identified and reported measuring the effectiveness of the nonprofit organisation’s activities during the year. The ICAA report recommends greater use of statistical information (including pictorial representations, such as tables and charts).

Part 4: Explaining our plans for the future – It is recommended that the annual

report outline expected future plans and in particular plans for future fundraising and any proposed new activities, events or programs that may have a material effect on the nonprofit organisation’s financial position and cash flows.

Part 5: Understanding our organisational structure and activities – It is

recommended that the annual report explain the legal form of the organisation, the composition of the board and committees, including corporate governance processes as well as providing an explanation of the organisational structure and decision making processes.

A complete copy of the ICAA’s Checkist on Improving Nonprofit Reporting can be downloaded from the following website:

Web Link : ICAA Checklist on Improving Nonprofits Annual Reports

http://www.icaa.org.au/upload/download/Checklist_NotForProfit_reporting.doc

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-37

4.12 Preparing for the Annual General Meeting As previously mentioned in the case of a company limited by guarantee, according to Section 250N(2) of the Corporations Act (2001), a public company’s annual general meeting must be held at least once in each calendar year and within five months after the end of its financial year. In the case of an incorporated association, according to Section 56 of the Associations Incorporation Act (1981), the annual general meeting must be held at least once each year and within six months after the end of its financial year or more frequently if the rules of the incorporated association so provide. Typically, the financial report and the auditor’s report are presented at the AGM for presentation to members. The accounts are then usually adopted (signed) by the Management Committee. Once the accounts have been signed, they are typically passed over to the auditor who provides the audit report for inclusion in the financial report. For more information on the requirements on the requirements of the Annual General Meeting (including the provision of appropriate notices of meetings), refer to the Developing Your Own (DYO) website at the following address:

Web Link : DYO Notice of Meetings

https://olt.qut.edu.au/bus/DYO/index.cfm?fa=displayPage&rNum=1767005

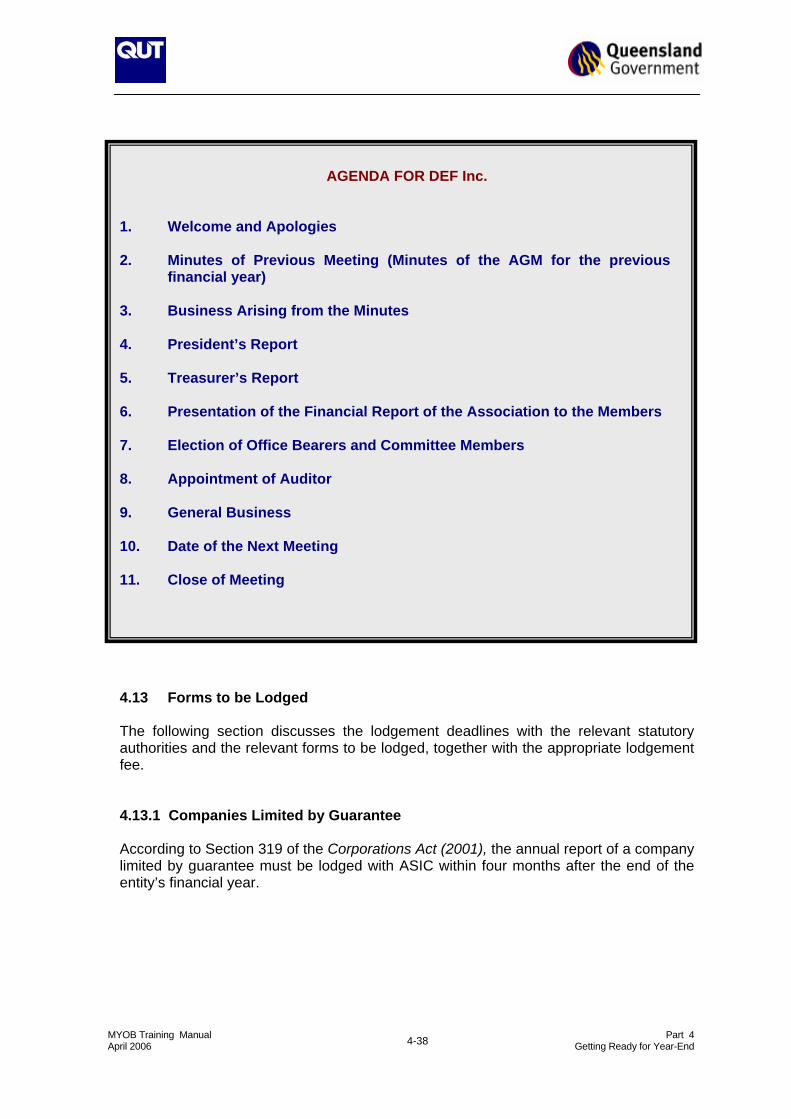

Subject to the rules of the incorporated association, a typical agenda for an AGM is as follows:

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-38

AGENDA FOR DEF Inc.

1. Welcome and Apologies 2. Minutes of Previous Meeting (Minutes of the AGM for the previous

financial year) 3. Business Arising from the Minutes 4. President’s Report 5. Treasurer’s Report 6. Presentation of the Financial Report of the Association to the Members 7. Election of Office Bearers and Committee Members 8. Appointment of Auditor 9. General Business 10. Date of the Next Meeting 11. Close of Meeting 4.13 Forms to be Lodged The following section discusses the lodgement deadlines with the relevant statutory authorities and the relevant forms to be lodged, together with the appropriate lodgement fee. 4.13.1 Companies Limited by Guarantee According to Section 319 of the Corporations Act (2001), the annual report of a company limited by guarantee must be lodged with ASIC within four months after the end of the entity’s financial year.

MYOB Training Manual Part 4 April 2006 Getting Ready for Year-End 4-39