Transwester 3Q 2010

9

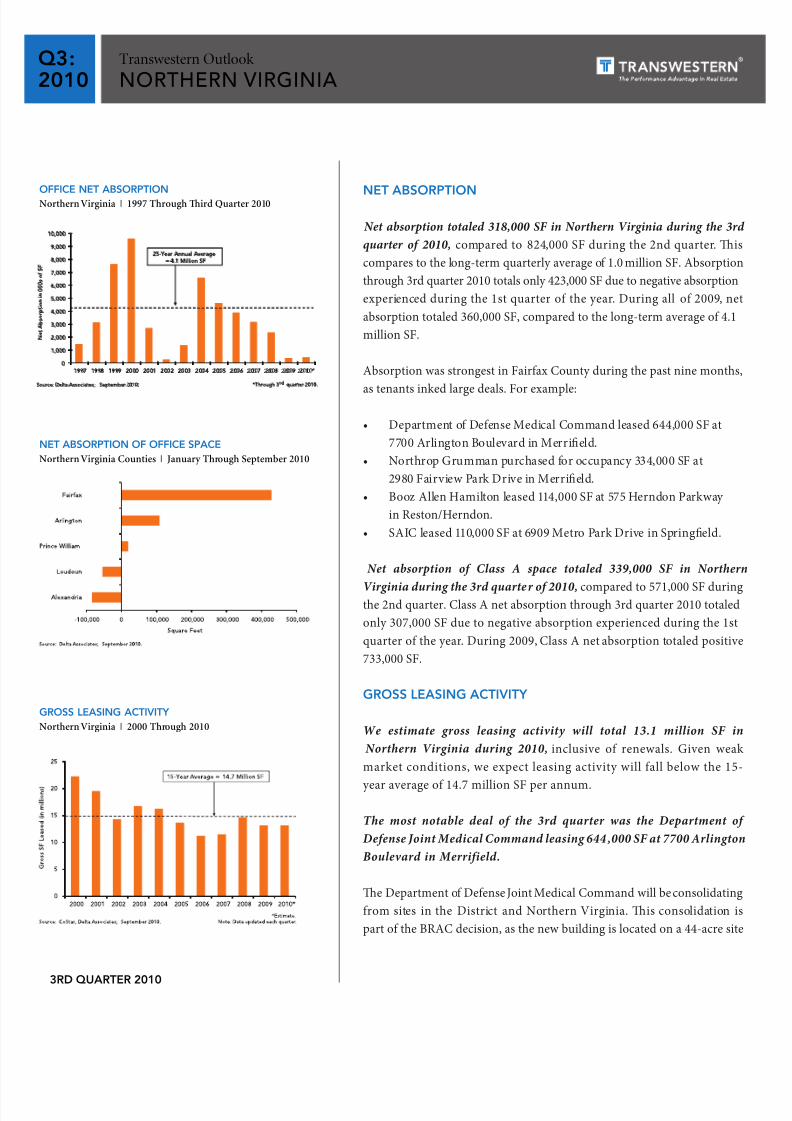

Q3:10 Transwestern Outlook northern virginia 3rd quarter 2010 Positive O fce Absorption and Vacancy’s Cyclical Decline Continu e; E ective Rent Decline Easing Te Northern Virginia ofce market is stabilizing, by several metrics, setting the stage or recovery by 2012 market-wide – sooner in select submarkets: • Net absorp tio n has been po sit ive during the last two quarters – driv en by job growth and government leasing. • Over all v acan cy h as e dge d down fro m o ne year ag o. • e rat e o f e ectiv e r ent dec line is eas ing . • Lessthan 900,000SF of space isunder constructionan d7 6% ofi tis preleased. How ever, the vacancy rate remains elevat ed, putting down ward pressure on ren ts. Eect ive ren ts declined 4.8% durin g the past nine mo nths, as landlor dscontinue tou segenero usconcessio npackagestoattracttenant s. Yetrentdeclinesappeartobeeasingcomparedto2009.Vacancyisexpected todecline overthe nexttwo years,asp re-leasedprojectsdeliver tothe market andGSAleaseslargeblocksofspace. Tird Quarter 2010 Market Highlights: • Net absorption: 318, 000 SFi nth e3rd qua rter ,423,000SF YTD , compared t o 360, 00 0 SF in all of 2009. • Overall vacancy rate: 13.4%,down from13.8%a tmid-yearand 13.5% one year ago. • Direct vacancy rate: 12.2%,upfrom11.9%oneyearago. • Sublease space: Decreasedby338,000S F .Subleasespacerepr esentsjust 1.2% of t he in ve ntory . • Pipeline (U/C and U/R): 804,000SF,downfrom1.6millionSFone year ago. • Pipeline pre-lease rate:76%,upfrom27%ayearago. • Rents: Down4.8%thr ough3rdqua rter2010,compa redtodeclining 6.7% in a ll o f 200 9. • Investment sales: $612million ($239/SF) through3rdq uarter2010, compare dto $296 mill ion inthecom para ble period last year .

-

Upload

david-captain -

Category

Documents

-

view

221 -

download

0

Transcript of Transwester 3Q 2010

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 1/9

Q3:10

Transwestern Outlook

northern virginia

3rd quarter 2010

Positive Ofce Absorption and Vacancy’s Cyclical

Decline Continue; Eective Rent Decline Easing

Te Northern Virginia ofce market is stabilizing, by several metrics, setting

the stage or recovery by 2012 market-wide – sooner in select submarkets:

• Netabsorptionhasbeenpositiveduringthelasttwoquarters–driven

by job growth and government leasing.

• Overallvacancyhasedgeddownfromoneyearago.

• erateofeectiverentdeclineiseasing.

• Lessthan900,000SFofspaceisunderconstructionand76%ofitis

preleased.

However, the vacancy rate remainselevated, puttingdownwardpressur

on rents. Eective rents declined 4.8% during thepast nine months, a

landlordscontinuetousegenerousconcessionpackagestoattracttenants

Yetrentdeclinesappeartobeeasingcomparedto2009.Vacancyisexpecte

todeclineoverthenexttwoyears,aspre-leasedprojectsdelivertothemarke

andGSAleaseslargeblocksofspace.

Tird Quarter 2010 Market Highlights:

• Net absorption: 318,000SFinthe3rdquarter,423,000SFYTD,

comparedto360,000SFinallof2009.

• Overall vacancy rate: 13.4%,downfrom13.8%atmid-yearand13.5%

one year ago.

• Direct vacancy rate: 12.2%,upfrom11.9%oneyearago.

• Sublease space: Decreasedby338,000SF.Subleasespacerepresentsjust

1.2%oftheinventory.

• Pipeline (U/C and U/R): 804,000SF,downfrom1.6millionSFone

year ago.

• Pipeline pre-lease rate:76%,upfrom27%ayearago.

• Rents:Down4.8%through3rdquarter2010,comparedtodeclining

6.7%inallof2009.

• Investment sales:$612million($239/SF)through3rdquarter2010,

comparedto$296millioninthecomparableperiodlastyear.

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 2/9

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 3/9

Transwestern Outlook

northern virginia

q3:2010

3rd quarter 2010

providingtherequiredsecuritysetbacks.eagencywillbebackllingspace tobe vacated byRaytheon,as thiscompany relocates toitsnew

headquartersontheformerAOLcampus.

eDepartmentofDefenseJointMedicalCommandlease,coupledwith

Northrop Grumman’s purchase of 334,000 SF for occupancy at 2980

FairviewParkDrivebroughtthedirectvacancyrateinMerrieldfrom

13.3%atmid-year 2010 to8.5% atSeptember 2010.Notably,Northrop

GrummanwillberelocatingitsheadquartersfromLosAngelestoFairfax

County.

Government leas ing activity increased to 31% o all lease deals inkedin Northern Virginia during 2009,comparedto21%during2008,and

7%in2007.Comparably,leasingfromprofessionalbusinessesincreasedto

49%in2009,from42%in2008,butisdownfrom63%in2007.

We expect the share o government lea sing to remain high in 2010 and

into 2011, as non-government tenants remain less certain about budgets

untiltheeconomyrms.However,privatecompanieswiththebudgetand

need shouldcontinuetotakelargeblocksofClassAspaceinaquality

locationothemarketasdiscountsonrentareoered.

here are 506 buildings with blocks o space available over 10,000 SFin Northern Virginia at September 2010,upfrom500buildingson

yearago.FairfaxCountyhosts62%oftheseblocks.

here are 52 buildings with blocks o space available over 100,000 SF

in Northern Virginia at September 2010,downfrom58buildingson

yearago.Notably,FairfaxCountyhas33oftheseblocks.Tenantshave

feweroptionsoflargeblocksofspaceinArlington/Alexandria,asonly13

suchblocksareavailableasof3rdquarter2010.

he largest block o space is 606,000 SF o renovated space at 5001

Eisenhower Avenue.isblockofspacecouldbeleasedbytheGSAinthenear-term,asthissiteisintherunningtolandtheDefenseIntelligenc

Agencyleasefor523,000SF.enextlargestblockis402,000SFat5275

LeesburgPike.eDefenseInformationSystemsAgencyplanstovacate

thisspacebyOctober2011andrelocatetoFortBelvoirundertheBRAC

decision.

buiLdiNGs with coNtiGuous bLocksoF avaiLabLe space

Northern Virginia | September 2010

oFFice LeasiNG activity by sector

Northern Virginia | 2005 - 2009

bLocks oF avaiLabLe space over 100,000 sFtop Five buiLdiNGs

Northern Virginia | September 2010

sm sF sm5001 Eisenhower Ave 606,000 I-395 Corridor

5275 Leesburg Pike 402,000 I-395 Corridor

1851 S. Bell Street 356,000 Crystal/Pentagon City

8111 Gatehouse Road 282,000 Merrifeld

1411 Jeerson Davis 278,000 Crystal/Pentagon City

Source: CoStar, Delta Associates; September 2010.

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 4/9

Transwestern Outlook

northern virginia

q3:2010

3rd quarter 2010

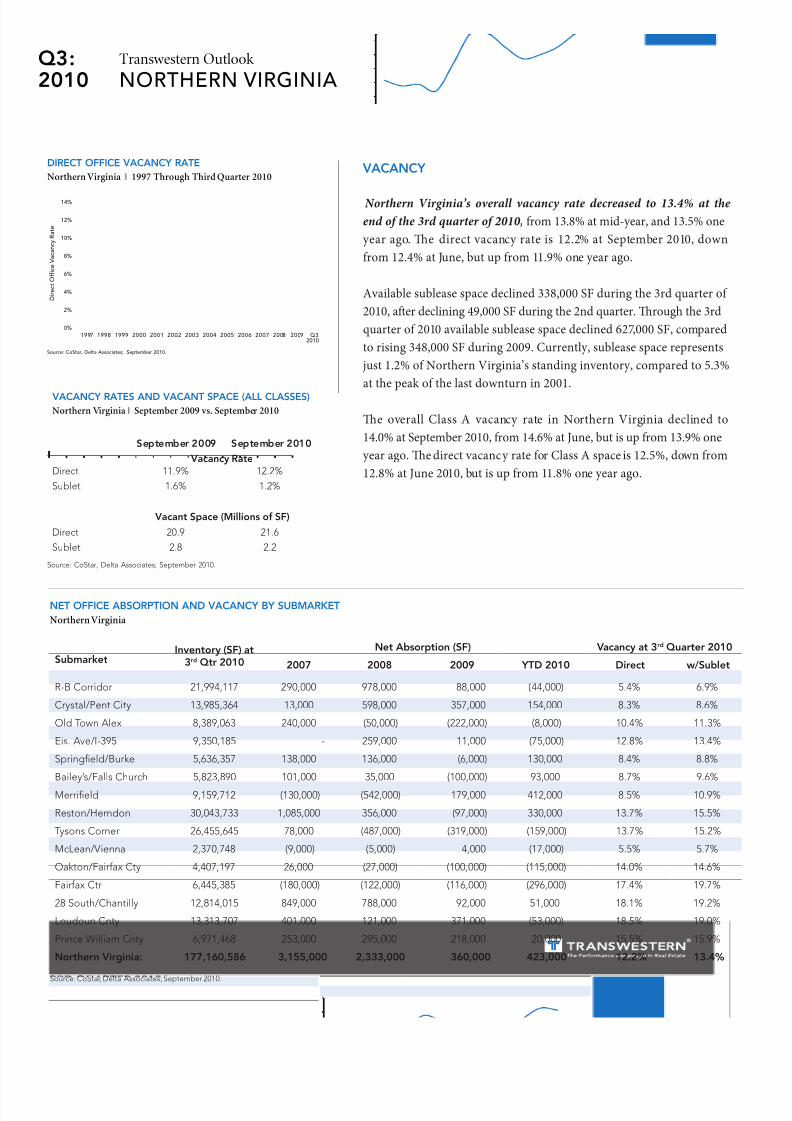

Net oFFice absorptioN aNd vacaNcy by subMarket

Northern Virginia

sminn (sF)

3 q 2010

N an (sF) vn 3 q 2010

2007 2008 2009 ytd 2010 d /sl

R-B Corridor 21,994,117 290,000 978,000 88,000 (44,000) 5.4% 6.9%

Crystal/Pent City 13,985,364 13,000 598,000 357,000 154,000 8.3% 8.6%

Old Town Alex 8,389,063 240,000 (50,000) (222,000) (8,000) 10.4% 11.3%

Eis. Ave/I-395 9,350,185 - 259,000 11,000 (75,000) 12.8% 13.4%

Springfeld/Burke 5,636,357 138,000 136,000 (6,000) 130,000 8.4% 8.8%

Bailey’s/Falls Church 5,823,890 101,000 35,000 (100,000) 93,000 8.7% 9.6%

Merrifeld 9,159,712 (130,000) (542,000) 179,000 412,000 8.5% 10.9%

Reston/Herndon 30,043,733 1,085,000 356,000 (97,000) 330,000 13.7% 15.5%

Tysons Corner 26,455,645 78,000 (487,000) (319,000) (159,000) 13.7% 15.2%

McLean/Vienna 2,370,748 (9,000) (5,000) 4,000 (17,000) 5.5% 5.7%

Oakton/Fairax Cty 4,407,197 26,000 (27,000) (100,000) (115,000) 14.0% 14.6%

Fairax Ctr 6,445,385 (180,000) (122,000) (116,000) (296,000) 17.4% 19.7%

28 South/Chantilly 12,814,015 849,000 788,000 92,000 51,000 18.1% 19.2%

Loudoun Cnty 13,313,707 401,000 121,000 371,000 (53,000) 18.5% 19.0%

Prince William Cnty 6,971,468 253,000 295,000 218,000 20,000 15.5% 15.9%

Nn vgn: 177,160,586 3,155,000 2,333,000 360,000 423,000 12.2% 13.4%

Source: CoStar, Delta Associates; September 2010.

vacaNcy

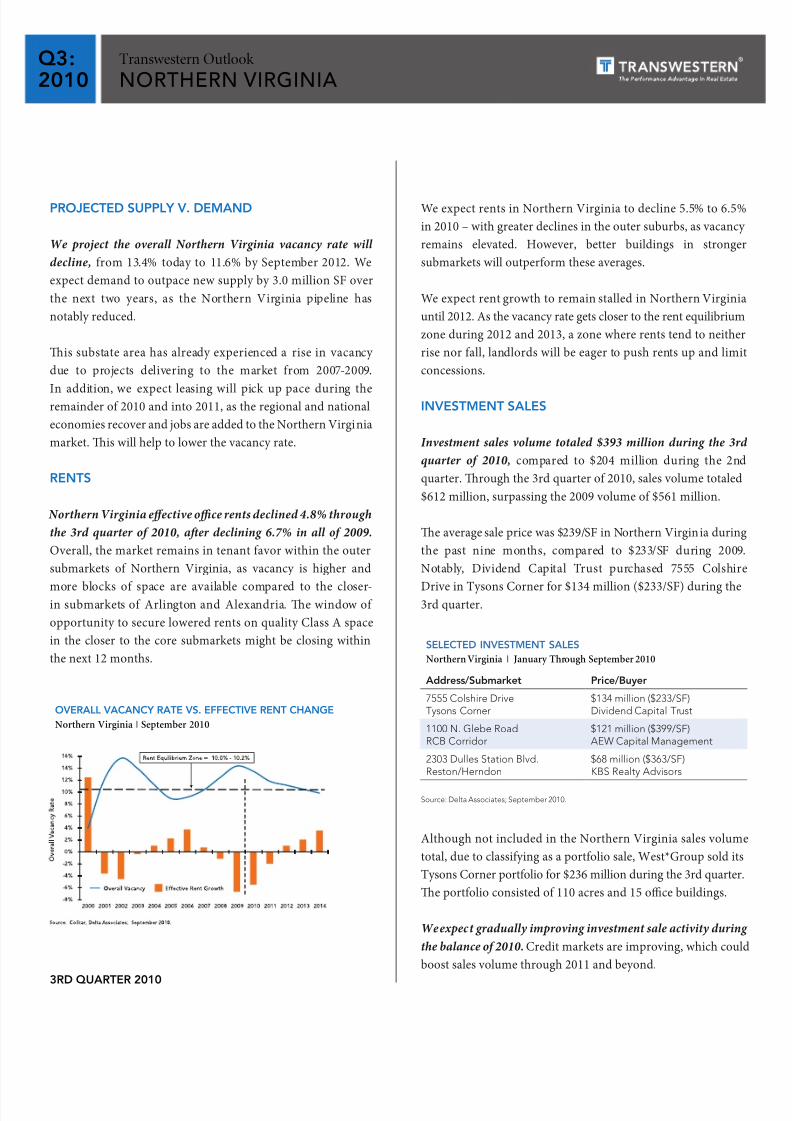

Northern Virginia’s overall vacancy rate decreased to 13.4% at the

end o the 3rd quarter o 2010, from13.8%atmid-year,and13.5%one

year ago.e direct vacancyrateis 12.2%atSeptember2010,down

from12.4%atJune,butupfrom11.9%oneyearago.

Availablesubleasespacedeclined338,000SFduringthe3rdquarterof

2010,aerdeclining49,000SFduringthe2ndquarter.roughthe3rd

quarterof2010availablesubleasespacedeclined627,000SF,compared

torising348,000SFduring2009.Currently,subleasespacerepresents

just1.2%ofNorthernVirginia’sstandinginventory,comparedto5.3%

atthepeakofthelastdownturnin2001.

e overallClass A vacancy rate inNorthern Virginia declined to

14.0%atSeptember2010,from14.6%atJune,butisupfrom13.9%one

yearago.edirectvacancyrateforClassAspaceis12.5%,downfrom

12.8%atJune2010,butisupfrom11.8%oneyearago.

vacaNcy rates aNd vacaNt space (aLL cLasses)

Northern Virginia | September 2009 vs. September 2010

sm 2009 sm 2010

vn rDirect 11.9% 12.2%

Sublet 1.6% 1.2%

vn s (Mlln f sF)

Direct 20.9 21.6

Sublet 2.8 2.2

Source: CoStar, Delta Associates; September 2010.

direct oFFice vacaNcy rate

Northern Virginia | 1997 Through Third Quarter 2010

0%

2%

4%

6%

8%

10%

12%

14%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Q32010

D i r e c t O f f i c e V a c a n c y R a t e

Source: CoStar, Delta Associates; September 2010.

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 5/9

q3:2010

Transwestern Outlook

northern virginia

3rd quarter 2010

Tere were no groundbreakings during the 3rd quarter o 2010, ae

two projects started during the 2nd quarter. Developersstartedo

448,000SFintwoprojectsduringthepastninemonths.During2009

groundbreakingstotaled447,000SFonthreeprojects–wellbelowth

10-yearannualaverageof4.8millionSF.

We expect uture groundbreakings in the Springeld submarket give

the close proximity to Fort Belvoir, whereover19,000governmen

workerswilltransferbySeptember2011undertheBRACdecision

Of note, Corporate OceProperties Trust (COPT) plans to sta

constructiononocespaceinthenear-terminSpringeldtomee

thedemand generatedby BRAC. During the4th quarterof 2010COPT plansto break groundon240,000 SFon the15-acre plot

PatriotRidge.

esecurityrequirements enforced underBRAC have encourage

somedeveloperstochangeplans.Forinstance,PetersonCompani

originally planneda 76-acre site along Rt. 28 South/Chantilly fo

residential, but with the change in housing market conditions an

increaseddemandforsecureocespace,thecompanyisnowplanning

todevelop1.2millionSFofsecuredocespaceonthisparcel.

Weexpectlimitedspecgroundbreakingsduringthebalanceof201

and into 2011, as direct vacancy remains elevated in many submarket

However,weexpectsomegroundbreakingstooccurlatein2010an

2011forthosedevelopersarmedwithcashinselectwell-positione

submarkets–suchasSpringeldandtheRCBCorridor.

Tere was one notable oce delivery during the 3rd quarter o 2010

comparedtoonedeliveryduringthe2ndquarter.A32,000SFprojec

at4500PondWayinPrinceWilliamCountydeliveredduringthe3r

quarterwith notenantsin place.Duringthe2nd quarter, a17,00

SFprojectat112W.WashingtonStreetinLoudounCountydelivere

10%pre-leased.During2009,ocedeliveriestotaled3.4millionS

andcameonlineat23%pre-leased.

Te outer suburbs o Loudoun and Prince William Counties hold the

highest direct vacancy rates in Northern Virginia,at18.5%and15.5%,

respectively.OnlyArlingtonandAlexandriaholdvacancyratesbelow

theNorthernVirginiaaverageof12.2%.

coNstructioN

Tere is 804,000 SF o oce space under construction or renovation in

Northern Virginia at September 2010, downfrom1.6millionSFone

year ago.

76% o the space under construction is pre-leased at September 2010, comparedto27%oneyearago.ecurrentpre-leaserateisabovethe

10-yearaveragepre-leaserateof55%.Pre-leaserateshaveincreased,as

construction starts onspecprojectshaveceased,which shouldallow

demandtograduallycatchuptosupply.

Te RCB Corridor has the greatest amount o space under construction

at mid-year 2010. Tis submarket has 709,000 SF in the pipeline at a

73% pre-lease rate.

oFFice coNstructioN starts

Northern Virginia | 1998 Through Third Quarter 2010

oFFice space u/c or u/r

Northern Virginia | September 2010

sm sF % p-L

Rosslyn, Courthouse, Ballston 709,000 73%

Springfeld/Huntington/I-95 95,000 100%

tl: 804,000 76%

Source: CoStar, Delta Associates; September 2010.

direct oFFice vacaNcy rate

Northern Virginia | September 2010

0

2,000

4,000

6,000

8,000

10,000

12,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010*

S q u a

r e

F e e t

i n

0 0 0 ' s

Source: CoStar, Delta Associates; September 2010.

10-Year Annual Average = 4.8 Million SF

*Through 3rd quarter 2010.

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 6/9

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 7/9

q3:2010

Transwestern Outlook

northern virginia

3rd quarter 2010

LaNd saLes

Tere were no notable oce land sales during the 3rd quarter

o 2010, comparedtoonenotabledealduringthe2ndquarter.

Skanskapurchased 1.0acre at 1716WilsonBoulevard inthe

RCB Corridor for $10.0 million during the 2nd quarter. A

127,000SF spec oce project isplanned for thissite– with

groundbreakingscheduledforyear-end2010.During2009,one

dealclosedwhenCatonHillPropertiespurchased7.6acresat

2730KillarneyDriveinPrinceWilliamCountyfor$3.0million

duringthe4thquarter.

We anticipate land sales will be limited during the remainder

o 2010, givenmodestdemandandlimiteddevelopmentcredit

availability,making it dicult for developers to achieve the

necessary returns in order to make new deals work. Until

buildingsalespricesequalorexceedreplacementcost,wedo

not look or a lot o land sales action.

NortherN virGiNia oFFice Market outLook

Te Northern Virginia oce market will experience stableconditions during the 4th quarter o 2010. Conditionsshould

starttoslowlyimproveduring2011as20,400newjobsare

added to this substate.

Leasing. Non-government tenants are starting to grab large

blocksofspacewherediscountsareoffered.Theamountof

tenantsseekingspacewillincreaseoverthenext12monthsas

theeconomyimprovesandmoreblocksofspaceareremoved

from the market. GSA has also been active in removing

blocksofspacefromthemarketandshouldcontinuetodo

sowith anticipated lease announcements expected duringthe4thquarter.

Vacancy.Weexpectvacancytodeclineoverthenexttwoyearto 11.6% bySeptember 2012, asNorthern Virginia’s pipelin

has been signicantly reduced and demand is picking u

pace.Althoughweexpectvacancytodeclineoverthenext2

months,vacancywillremainelevatedatSeptember2012when

comparedtothecyclicallowof8.9%during2005.Giventh

elevatedvacancy,rentsshoulddecline5.5%to6.5%in2010,wit

concessionoeringsremaininggenerous.However,weexpe

selectsubmarketswith superiorsupply/demandfundamenta

tostartclosingthedoortothesedealsoverthenext12month

Rents.Weexpectrentstocontinueunderpressurethrough201market-wide.By2012rentsshouldbegintheircyclicalincreas

– sooner in select submarkets.

Te Northern Virginia oce market remains a strong player i

the intermediate and long-run due to a low pipeline combine

with a concentration o deense agencies and contractor

Northern Virginia also should continue to attract som

District tenants with its competitive buildings at lower rent

especially at Metro-served locations.

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 8/9

Transwestern Outlook

northern virginia

q3:2010

3rd quarter 2010

Flex/Industrial Vacancy Rates Edge Down;Rents Remain Under Pressure

Net absorptioN

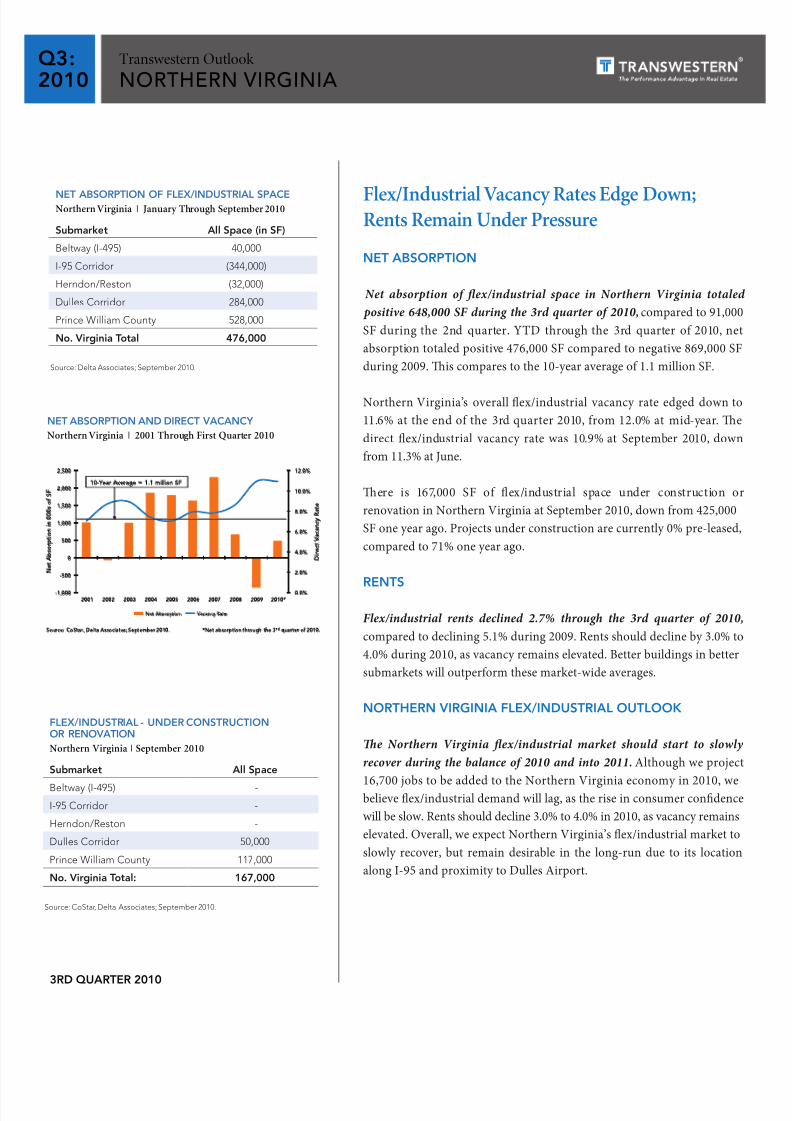

Net absorption o fex/industrial space in Northern Virginia totaled

positive 648,000 SF during the 3rd quarter o 2010, comparedto91,000

SFduringthe 2nd quarter. YTD throughthe 3rdquarterof2010,ne

absorptiontotaledpositive476,000SFcomparedtonegative869,000SF

during2009.iscomparestothe10-yearaverageof1.1millionSF.

NorthernVirginia’s overallex/industrial vacancyrateedgeddownto

11.6% at theendofthe 3rdquarter2010,from12.0%atmid-year.e

direct ex/industrial vacancyratewas10.9%at September 2010, down

from11.3%atJune.

ere is 167,000 SF of ex/industrial space under construction o

renovationinNorthernVirginiaatSeptember2010,downfrom425,000

SFoneyearago.Projectsunderconstructionarecurrently0%pre-leased

comparedto71%oneyearago.

reNts

Flex/industrial rents declined 2.7% through the 3rd quarter o 2010,

comparedtodeclining5.1%during2009.Rentsshoulddeclineby3.0%to

4.0%during2010,asvacancyremainselevated.Betterbuildingsinbetter

submarketswilloutperformthesemarket-wideaverages.

NortherN virGiNia FLex/iNdustriaL outLook

Te Northern Virginia fex/industrial market should start to slowly

recover during the balance o 2010 and into 2011.Althoughweprojec

16,700jobstobeaddedtotheNorthernVirginiaeconomyin2010,webelieveex/industrialdemandwilllag,astheriseinconsumercondenc

willbeslow.Rentsshoulddecline3.0%to4.0%in2010,asvacancyremains

elevated.Overall,weexpectNorthernVirginia’sex/industrialmarketto

slowly recover, but remain desirable in the long-run due to its location

alongI-95andproximitytoDullesAirport.

Net absorptioN oF FLex/iNdustriaL spaceNorthern Virginia | January Through September 2010

sm all s (n sF)

Beltway (I-495) 40,000

I-95 Corridor (344,000)

Herndon/Reston (32,000)

Dulles Corridor 284,000

Prince William County 528,000

N. vgn tl 476,000

Source: Delta Associates; September 2010.

Net absorptioN aNd direct vacaNcy

Northern Virginia | 2001 Through First Quarter 2010

FLex/iNdustriaL - uNder coNstructioNor reNovatioN

Northern Virginia | September 2010

sm all s

Beltway (I-495) -

I-95 Corridor -

Herndon/Reston -

Dulles Corridor 50,000

Prince William County 117,000

N. vgn tl: 167,000

Source: CoStar, Delta Associates; September 2010.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-1,000

-500

0

500

1,000

1,500

2,000

2,500

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010*

D i r e c t V a c a n c y R a t e

N e t A b s o r p t i o n

i n 0 0 0 s o f S F

Net A bsor pt ion V acancy Rate

10-Year Average = 1.1 million SF

Source: CoStar,Delta Associates; September 2010. *Net absorption through the 3rd quarter of 2010.

8/7/2019 Transwester 3Q 2010

http://slidepdf.com/reader/full/transwester-3q-2010 9/9

Transwestern Outlook Outlook is published quarterly by Delta Associates, the ResearchAfliate o Transwestern Commercial Services, the Washington/

Baltimore metropolitan area’s largest ull service real estate

frm. Every eort has been made to ensure accuracy; however,

Transwestern Commercial Services is not responsible or any

errors or omissions.

q3:2010

Transwestern Outlook

northern virginia

reGioNaL headquarters6700RockledgeDriveSuite400ABethesda,MD20817301.896.9000

washiNGtoN, dc1700KStreet,NWSuite600

Washington,DC20006202.775.7000

NortherN virGiNia8614WestwoodCenterDriveSuite800Vienna,VA22182703.821.0040

baLtiMore-washiNGtoN corridor8820Columbia100Parkway

Suite310Columbia,MD21045301.621.8800

www.transwestern.net

deLta associates500MontgomeryStreetSuite600Alexandria,VA22314703.836.5700

www.DeltaAssociates.com