Transportation Outlook 21st Breakbulk Americas ... · Memo - New vessels are ... effectively...

30

Transportation Outlook 21 st Breakbulk Americas Transportation Conference Houston October 14th, 2010

Transcript of Transportation Outlook 21st Breakbulk Americas ... · Memo - New vessels are ... effectively...

Transportation Outlook

21st Breakbulk Americas Transportation Conference

Houston

October 14th, 2010

Transportation Outlook

1 Introduction

2 Cargo

3 Fleet

4 Market outlook & forecasts

Agenda

Transportation OutlookMajor MPV seaborne trade routes

ExporterImporterExporter and importer

Steel

14-16m tonnesSteel

10-12m tonnes

Steel

10-12m tonnes

South

Korea

JapanMed

China

North

Europe

Forest products

28-32m tonnes

Indonesia

USA

Forest products

10-12m tonnes

EU27

Forest products

10-12m tonnes

Taiwan

Construction commodities

15-18m tonnes

Brazil

Fertilisers

2-3m tonnes

India

Fertilisers

3-4m tonnes

Algeria

Grain (mpv routes)

3-4m tonnes

Argentina

Grain (mpv routes)

4-5m tonnes

Construction commodities

5-6m tonnes

FranceRussia

Transportation Outlook

0

500

1,000

1,500

2,000

2,500

2000 2002 2004 2006 2008 2010

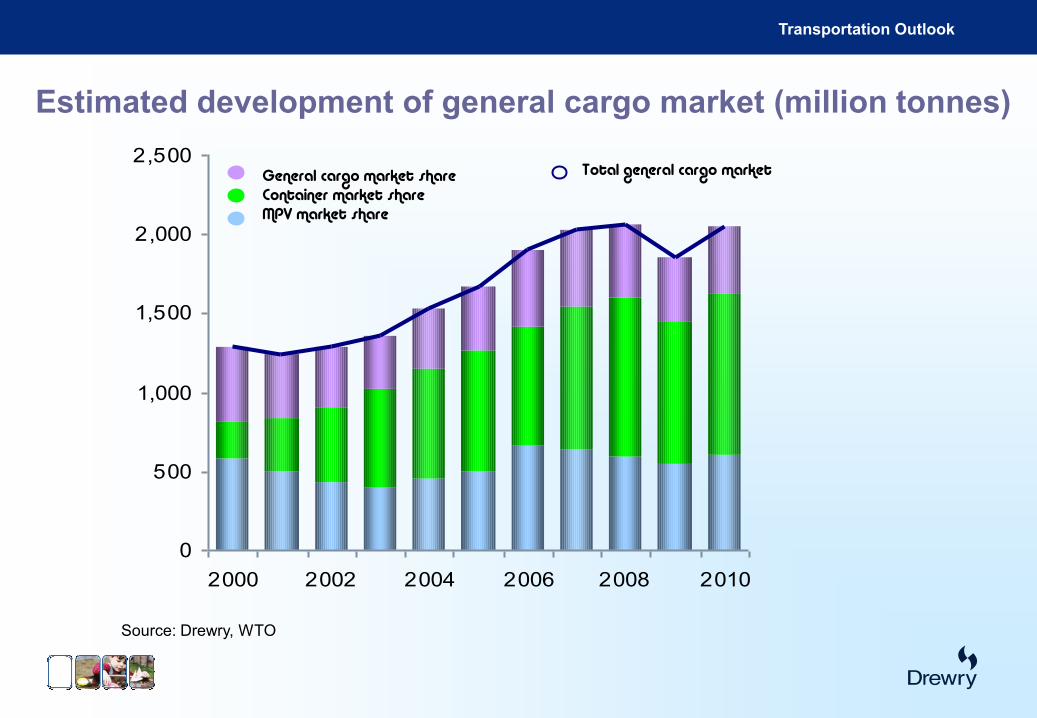

Estimated development of general cargo market (million tonnes)

General cargo market shareContainer market shareMPV market share

Total general cargo market

Source: Drewry, WTO

Transportation Outlook

2 Cargo

Transportation Outlook

Source: Drewry

Dry cargo market segmentsSeaborne

Cargo

2010(mill.t)

Primary

Cargo Markets

for

Multi -Purpose

Ships

Competing Vessel

Types

Dry

Cargo

Bulk

Cargo

Major

Bulk

Cargo

Major Bulk

Cargo

Major Bulk Cargo Iron ore,

coal,

grain

2,022 Major BulkBulk carriers

Minor

Bulk

Cargo

Other Minor

Bulk Cargo

Other Minor Bulk

Cargo

Phosrock,

bauxite,

other

532 Other Minor BulkHandy bulkers

Neo/Agri-

Bulk Cargo

Neo/Agri-Bulk

Cargo

Iron & steel,forest products,

fertilisers,

sugar, rice

598 Neo/Agri-Bulk(Multi - Purpose

ships part)

Handy bulkers

Ro-Ro ships

Non -

Bulk

Cargo

General

Cargo

Unitised

General

Cargo

Containerised

General Cargo

General cargo

in containers1,342

Containerised

General Cargo(Multi -Purpose ships

part)

Containerships

Ro-Ro ships

Con-bulkers

Other Unitised

General Cargo

General cargo

in trailers

(short sea)

340 Other Unitised General Cargo

Ro-Ro ships

Ferries

Non -Unitised

General

Cargo

Specialised

General Cargo

Reefer,

vehicles 57 SpecialisedGeneral Cargo

Reeferships

Car carriers

Ro-Ro ships

Non -Specialised

Breakbulk

General Cargo

All types of non-unitisedgeneral & project

304

Non-Specialised

Breakbulk

General Cargo

Ro-Ro ships

Heavy lift ships

(Multi-Purposeships part)

(Multi-Purpose

ships part)

Est. Global

cargo

Transportation Outlook

Project cargo – the invisible break-bulk volume

1) Nowhere to be seen in port and trade statistics, but it has become

the foundation for the most dynamic part of the break-bulk market

and home to many fast growing specialist companies such as

Beluga, BBC, Clipper, Rickmers, SAL, Intermarine and others.

2) Wide range of industries generate project cargo, but they can be

combined into just 4 sectors:- Transportation (46%); Logistics

(34%); Power & Water (16%);Oil &Gas (4%)

3) Global annual project value, give or take a few billion, is estimated

at $275 bn. Assuming sea freight = 7.5% of value; average freight

rate of $150/rev ton; 2.5 cbm/tonne; and 60% of cargo seaborne,

this would indicate an annual project cargo flow of 33 million

tonnes or 82.5 million cbm pa.

Transportation Outlook

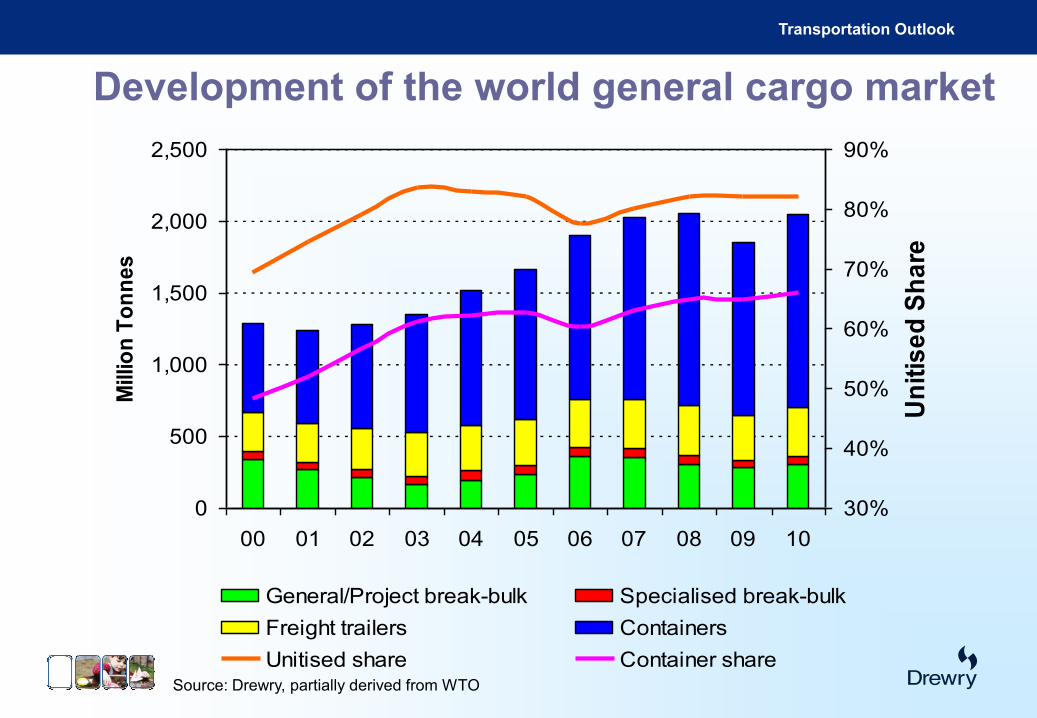

Development of the world general cargo market

0

500

1,000

1,500

2,000

2,500

00 01 02 03 04 05 06 07 08 09 10

Mill

ion

To

nn

es

30%

40%

50%

60%

70%

80%

90%

Un

itis

ed

Sh

are

General/Project break-bulk Specialised break-bulk

Freight trailers Containers

Unitised share Container shareSource: Drewry, partially derived from WTO

Transportation Outlook

Source: Drewry

0%

5%

10%

15%

20%

25%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

MP

V s

ha

re o

f tr

aff

ic

Minor/Neo-bulks Major bulks Containers

Assumed/estimated development of market shares for MPV

Transportation Outlook

Source: Drewry

Development of the cargo pool for MPV

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Mil

lio

n T

on

ne

s

30%

35%

40%

45%

50%

55%

60%

65%

Ge

ne

ral/P

roje

ct

Ca

rgo

Sh

are

General/Project Break-bulk Minor & Neo-Bulk

Major Bulk Containers

General/Project Share

Transportation Outlook

3 Fleet

Transportation Outlook

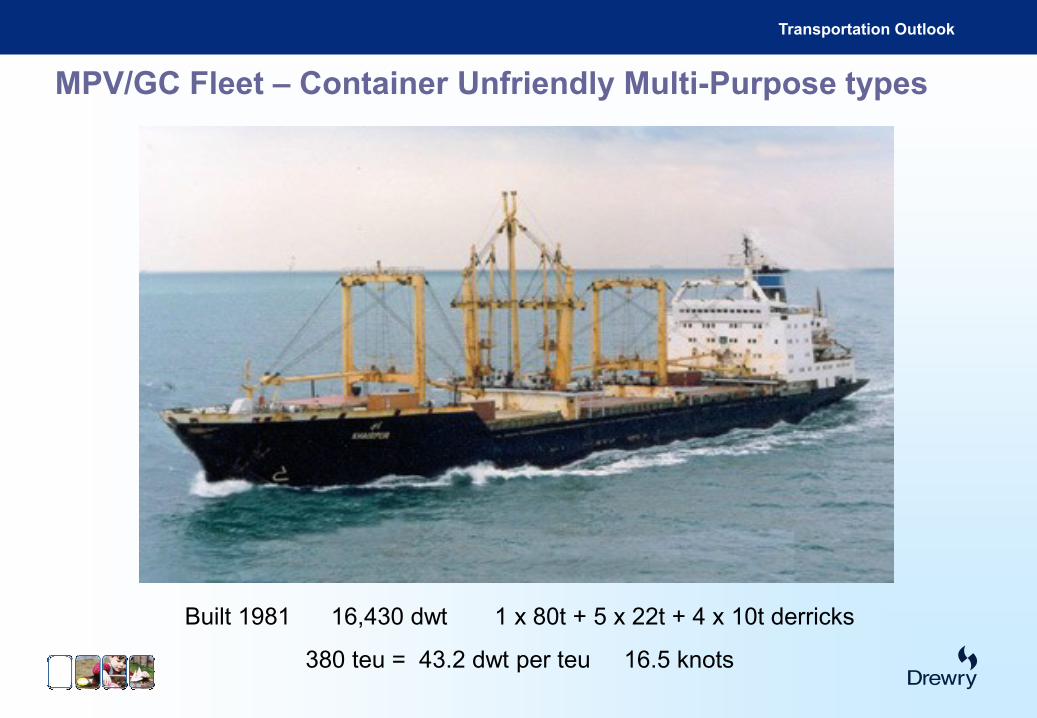

Built 1981 16,430 dwt 1 x 80t + 5 x 22t + 4 x 10t derricks

380 teu = 43.2 dwt per teu 16.5 knots

MPV/GC Fleet – Container Unfriendly Multi-Purpose types

Transportation Outlook

Built 1999: 20,567 dwt: Speed 16 kn

2 x 60t cranes combinable to 120t

1,300 teu = 15.8 dwt per teu

Built 2006: 17,300 dwt: Speed 15 kn

3 x 80t cranes combinable to 160t

958 teu = 18 dwt per teu

MPV/GC Fleet – Container Optimised Multi-Purpose types

Transportation Outlook

Built 2004: 12,744 dwt: Speed 15 kn

2 x 120t cranes combinable to 240t

673 teu = 18.9 dwt per teu

Built 2010: 14,100 dwt: Speed 17.5 kn

2 x 400t, 1 x 80t cranes

985 teu = 14.3 dwt per teu

MPV/GC Fleet – Project Cargo Optimised Multi-Purpose types

Transportation Outlook

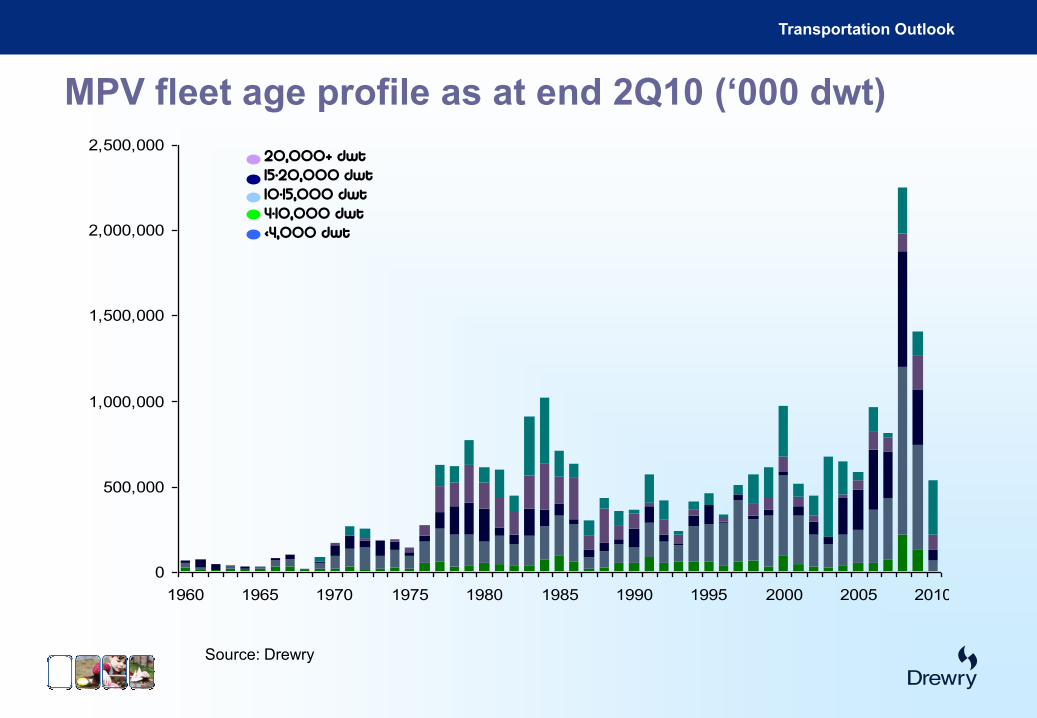

MPV fleet age profile as at end 2Q10 (‘000 dwt)

Source: Drewry

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

20,000+ dwt15-20,000 dwt10-15,000 dwt4-10,000 dwt<4,000 dwt

Transportation Outlook

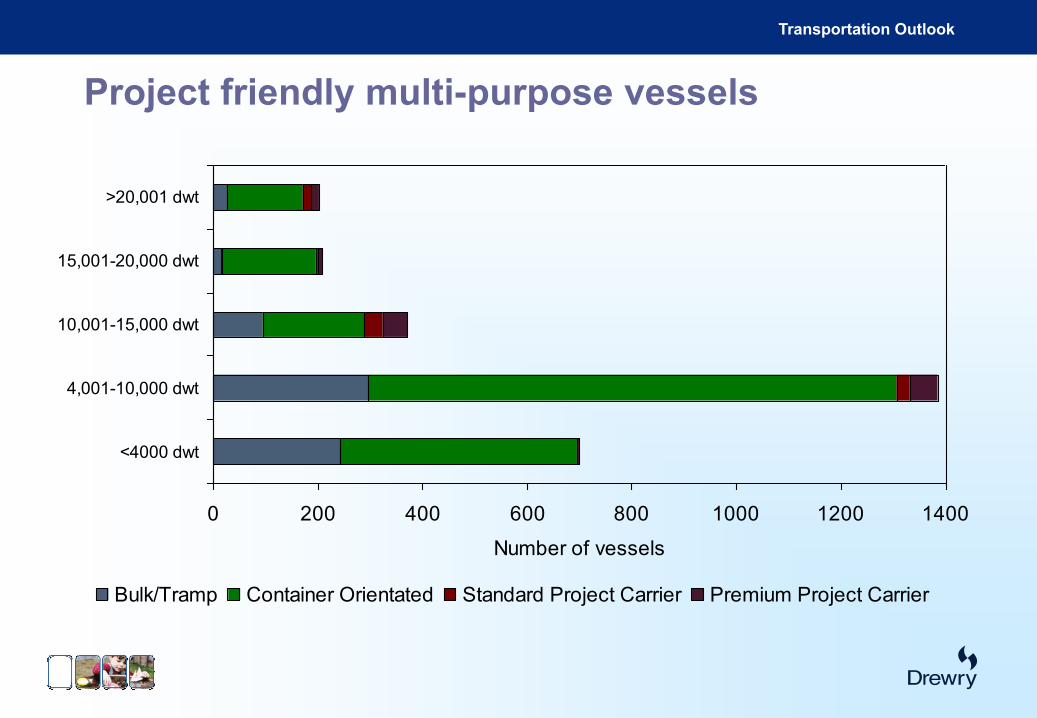

Project friendly multi-purpose vessels

0 200 400 600 800 1000 1200 1400

<4000 dwt

4,001-10,000 dwt

10,001-15,000 dwt

15,001-20,000 dwt

>20,001 dwt

Number of vessels

Bulk/Tramp Container Orientated Standard Project Carrier Premium Project Carrier

Transportation Outlook

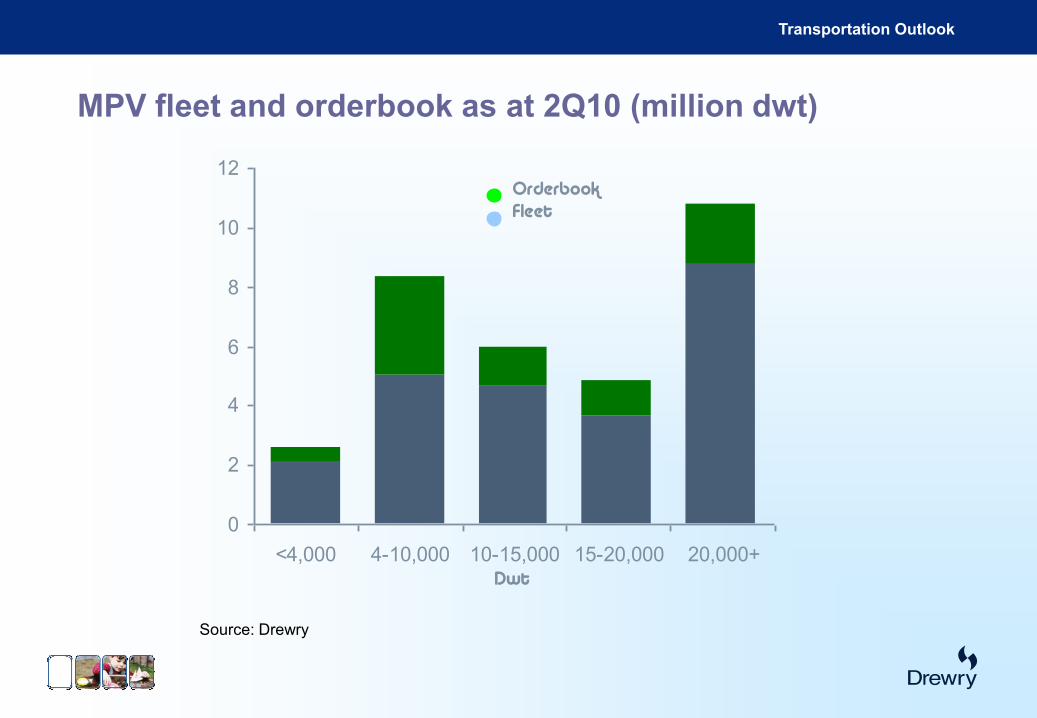

MPV fleet and orderbook as at 2Q10 (million dwt)

Source: Drewry

0

2

4

6

8

10

12

<4,000 4-10,000 10-15,000 15-20,000 20,000+Dwt

OrderbookFleet

Transportation Outlook

Source: Drewry

Suggested development of the multi-purpose fleet

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

2007 2008 2009 2010 2011 2012 2013 2014

'00

0 d

wt

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

36,000

38,000

40,000

'00

0 d

wt

DeliveriesDemolitionFleet (right axis)

Transportation Outlook

4 Market outlook and forecasts

Transportation Outlook

-15%

-10%

-5%

0%

5%

10%

15%

2000 2002 2004 2006 2008 2010f

Real GDP Trade in goods

World economic growth (% change)

Source: Drewry

Transportation Outlook

0

50

100

150

200

250

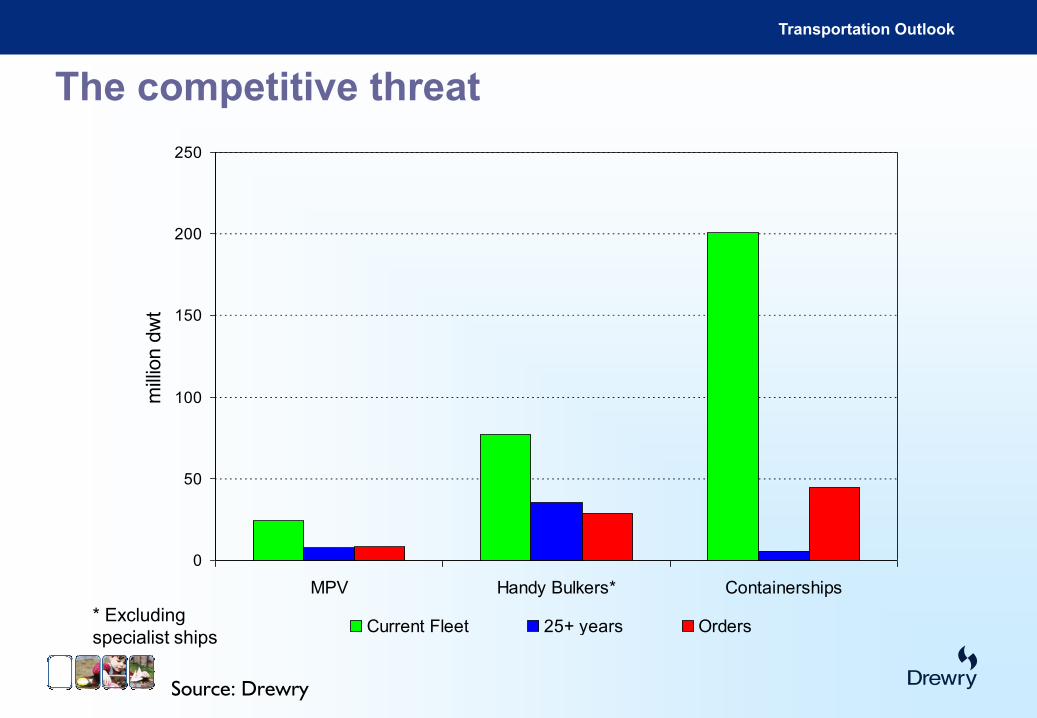

MPV Handy Bulkers* Containerships

mill

ion d

wt

Current Fleet 25+ years Orders

Source: Drewry

* Excluding

specialist ships

The competitive threat

Transportation Outlook

0

500

1,000

1,500

2,000

2,500

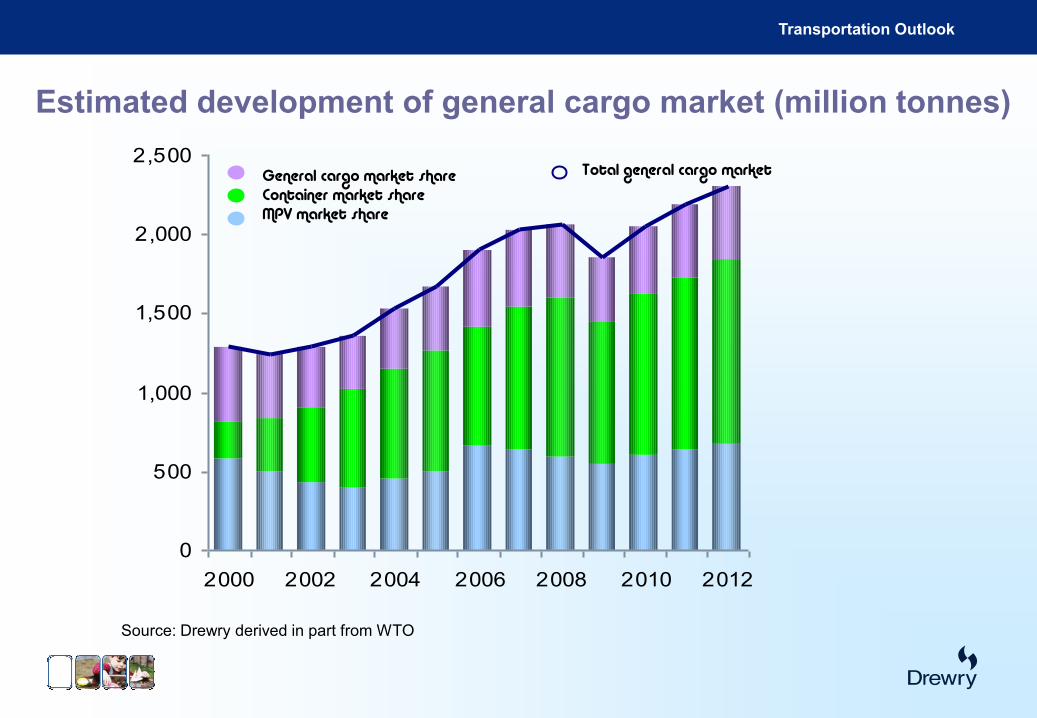

2000 2002 2004 2006 2008 2010 2012

Estimated development of general cargo market (million tonnes)

General cargo market shareContainer market shareMPV market share

Total general cargo market

Source: Drewry derived in part from WTO

Transportation Outlook

Source: Drewry

0

500

1,000

1,500

2,000

2,500

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Mil

lio

n T

on

nes

55%

60%

65%

70%

75%

80%

85%

90%

95%

Mark

et

Sh

are

General/Project Break-bulk Specialised Break-bulk

Freight Trailers Containers

Unitised Share Container Share

Forecast development of the general cargo market

Transportation Outlook

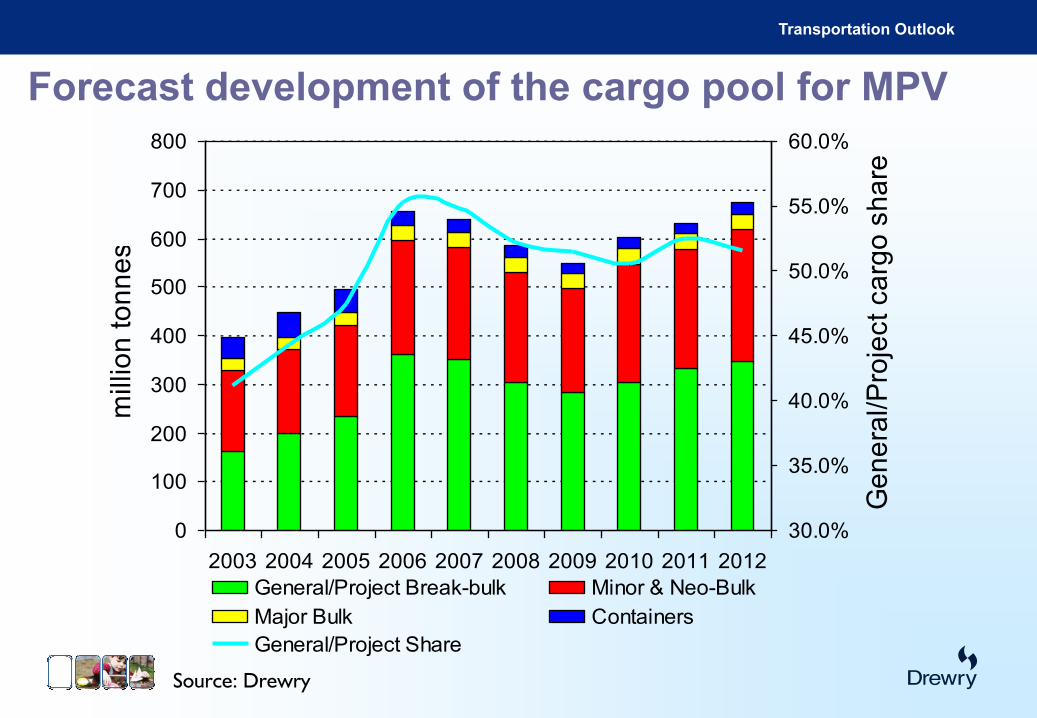

Source: Drewry

0

100

200

300

400

500

600

700

800

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

mill

ion

to

nn

es

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

Ge

ne

ral/P

roje

ct

ca

rgo

sh

are

General/Project Break-bulk Minor & Neo-Bulk

Major Bulk Containers

General/Project Share

Forecast development of the cargo pool for MPV

Transportation Outlook

Growth in effective fleet versus growth in effective demand (%)

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2008 2009 2010 2011 2012

Fleet growthDemand growth

Transportation Outlook

Source: Drewry

5

10

15

20

25

30

35

40

45

50

2002 2003 2004 2005 2006 2007 2008 2009 2Q10

US

$ m

illi

on

15,000 dwt MPV 25-30,000 dwt bulkcarrier

500 teu 8,000 dwt container

* Mid-year

Newbuilding price trends

Transportation Outlook

0

5,000

10,000

15,000

20,000

25,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US

$p

d

4,000-4,999dwt 10,000-14,999 dwt

15,000-19,999 dwt 20,000+ dwt bulkcarrier

Source: Drewry

Forecast MPV time charter rate development

History Forecast

Transportation Outlook

Break-bulk shipping in the future

1) Whilst the long lead times on projects provided some cushioning

against the demand collapse, there is now some lag in regenerating

new demand

2) Global GDP growth is expected to return to an average rate of 4.3%

from 2010 onwards

3) Heavy orientation of the project market to the developing world, where

economic growth will be stronger.

4) Cargo demand in this sector is forecast to increase at an average

annual rate of 7% to 2012,with fleet growth nearer 3% pa.

5) However whilst government involvement in many major infrastructure

projects helped sustain demand over the worst of the recession, it

may be that this has run its course.

Transportation Outlook

Summing up1) The fleet was in seemingly terminal decline, but the trade/economic super-cycle

reversed this and the sector is now seeing managed expansion. Memo - New

vessels are considerably more productive/efficient than the ships they replace

and have the potential to create over-capacity – but they also draw on a

different cargo pool and add value.

2) Many traditional break-bulk lines missed or misread the opportunity and have

effectively abandoned the market to a new breed of logistics based project carriers.

Memo – Possible trend towards more vessel pooling, joint services - & even

consolidation? – amongst the leading project carriers.

3) Through investment in new ships & methods, project carriers have created a partially

insulated niche within the break-bulk market, resulting in higher rates, higher profits

and differentiated products/services. Memo – Can this insulation survive the

global down-turn and extra modal competition?

4) Demand for project cargoes lags the general cargo market but over time is less

volatile. Memo – a sustained period of firm rates may be necessary before we

see any return to the peak rates, as happened in 2003-07