TRANSNET PRESENTATION ON THE INDUSTRIAL POLICY ACTION PLAN TO THE PORTFOLIO COMMITTEE ON TRADE AND...

33

TRANSNET PRESENTATION ON THE INDUSTRIAL POLICY ACTION PLAN TO THE PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY Chris Wells: Acting Group Chief Executive 16 April 2010 CONFIDENTIAL

-

Upload

benedict-watson -

Category

Documents

-

view

216 -

download

2

Transcript of TRANSNET PRESENTATION ON THE INDUSTRIAL POLICY ACTION PLAN TO THE PORTFOLIO COMMITTEE ON TRADE AND...

TRANSNET PRESENTATION ON THE INDUSTRIAL POLICY ACTION PLAN TO THE PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY

Chris Wells: Acting Group Chief Executive16 April 2010

CONFIDENTIAL

22

1. Transnet Performance and targets

2. Cost of doing business regarding rail and freight

3. Utilising public procurement spend to reduce supply chain costs- challenges and implications

4. Opportunities and challenges presented by IPAP2

Contents

Topics

33

The need for a turnaround strategy in 2004

• Huge derivative liabilities arising from unfavourable contracts entered into with major clients for the transportation of commodities

• Pension funds reflected deficits• Loss making non-core businesses in the Group• Low profitability• Gearing ratio had reached an unsustainably high level of 83%

Liabilities

Investment • Absence of a structured investment programme even though key infrastructure

and rolling stock badly needed maintenance and replacement• Low returns on investments and delays in execution

Market share • Competition (mainly from road operators) was eating into Transnet’s market share.

General Freight volumes declined by 2.5% p.a. between 1997 and 2003 • Constraints in capacity and efficiencies handicapped growth

• The company was not sufficiently oriented towards its customers• Low efficiencies resulted in congestion at the ports and unstable service delivery in

freight transport

Efficiencies

Transnet was facing a number of challenges

44

Revenue

• Continuous increase in revenue showing results of

initiatives to grow the business, with revenue

increasing from R25.3bn in 2004/05 to R33.6bn in

2008/09 (7.4% CAGR)

EBITDA

• Improvements through:

Operational efficiency improvements, effective cost cutting initiatives, mainly due to reengineering projects

Sale of non-core businesses

• Improvement from R7.9bn in 2004/05 to R13.2bn in 2008/09 (13.7% CAGR)

• Balance sheet restructuring and cost effective debt structures yielding positive results with consistent below target gearing from 61% in 2004/05 to 36.2% in 2008/09

• This enables Transnet to fund capital investments more cost effectively and without government guarantees 08/0

9

36%

07/08

30%

06/07

39%

05/06

46%

04/05

61% 50%Max

Gearing (%)

Transnet has effected a successful financial turnaround over the past six years

13.212.810.710.4

7.9

04/05

05/06

06/07

07/08

08/09

33.630.1

26.926.025.3

08/09

07/08

06/07

05/06

04/05

R billion

R billion

55

18.519.4

15.8

11.7

6.6

Capital investment has shifted to a new trajectory

Transnet Group Historical Capital Investment(R billion)

2008/09

2007/08

2006/07

2005/06

Total Investment over past 5

years:R72bn

2009/10 e

15,29216,22617,119

21,91322,831

10/11

14/15

13/14

12/13

11/12

R m

illio

n

Current 5 year investment

plan:R93.4bn

Transnet 5 year Capital Investment(R million)

66

“The Transnet R80bn capital investment programme (based on 2009/10 5-year plan) will make a significant contribution in terms of additional GDP – both in terms of magnitude and spread”

(2018 difference with and without investment programme)

Direct impact Indirect impact Induced impact Total impact

Impact on GDP (m) R 38 436 R 31 712 R 42 399 R 112 548

Impact on Capital Formation (m) R 116 797 R 67 079 R 86 043 R 269 920

Impact on Employment [numbers] 119 108 193 154 263 594 575 856

Skilled 27 105 43 589 62 742 133 436

Semi-skilled 57 475 79 869 105 435 242 778

Unskilled 34 529 69 696 95 417 199 642

Source: DPE Study, Measurement of the impact of Transnet on the South African economy, 2010

77

Rail

Ports

Pipelines

Transnet has improved efficiencies but operations are not yet at world class levels

Locomotive efficiency (gross ton per loco) exceed set targets for GFB

Overall reduction in number of derailments compared to previous year

Overall availability and reliability of rolling stock improved as a result of maintenance regime

Iron ore line tempos continue to improve

Turnaround times of wagonsPredictability service delivery (on-

time departures and arrivals)Reduction in number of train

cancellationsReducing security incidents (i.e.

cable theft)

Achievements Efficiencies to be improved

Improved planning/integration with rail

Loading rates at Saldanha Iron Ore Terminal (export iron ore)

Shipping delays due to tugs and pilots

Container handling ratesShip turnaround times

Achievements Efficiencies to be improved

Increased capacity utilisation in Durban-Jhb pipeline through drag-reducing agents

Successful implementation of Bridging Plan

Maintain world-class efficiency

Achievements Efficiencies to be improved

Certain efficiencies not meeting world class

standards

88

Reduce wagon cycle/turnaround times by 21.1%

Reduce deviation from schedule by 26.8% (departures/arrivals)

Improve locomotive efficiencies by 33.2% (GTK/loco/month)

Rail

Ports

Improve cargo handling efficiency from 22 to 28 with target of 30 GCM/h

Reduce shipping delays and ship turnaround time (Durban) and increase

Volumes per STAT Hour by 21%

Security of supply and reduce production interruptions by 21.5%

Pipelines

• Average 8.4% increase in

operational efficiency and

productivity

• Cumulative 20%

improvement over 3

years

Quantum leap targets for 2010/11

5-Year Corporate Plan Deliverable*

* Improvements/reductions – average improvement for all relevant KPIs from 2009/10 to 2014/15

Challenging efficiency targets have been set across all operations

Improved customer service delivery

99

14/15

13/14

12/13

11/12

10/11

09/10

50

Gearing (%)

3,0

3.5

14/15

4.1

13/14

3.4

12/13

3.1

11/12

3.0

10/11

3.2

09/10

11.2

13/14

10.0

12/13

9.6

11/12

8.9

10/11

7.4

09/10

6.58

14/15

Return on Total Assets (%)

Cash interest cover (times) Max/min

10

EBITDA (Rm)

15 116

+19%

14/15

30 435

13/14

26 311

12/13

22 965

11/12

19 765

10/11

09/10

12 759

1) The improvement in EBITDA and EBITDA margin is largely driven by the cumulative growth in volumes of 40% over the 5-years.

2) Improvement in operational efficiencies (8.4% in 2010/11) resulting in lower cost structures

Projected financial performance and key ratios

Budget+

LE

LE

LE

LE

1010

1. Transnet Performance and targets

2. Cost of doing business regarding rail and freight

3. Utilising public procurement spend to reduce supply chain costs- challenges and implications

4. Opportunities and challenges presented by IPAP2

Contents

Topics

1111

SA is ranked 28th out of 155 countries and is the highest logistics performer amongst upper middle income countries

Country LPI Customs Infrastructure International shipments

Logistics competence

Tracking & tracing

Timeliness

High income: all (income average) 3.55 3.36 3.56 3.28 3.5 3.65 3.98

South Africa 3.46 3.22 3.42 3.26 3.59 3.73 3.57

Upper middle income (income

average) 2.82 2.49 2.54 2.86 2.71 2.89 3.36

1212

The cost of logistics in South Africa in 2008 was R339 Billion (14.7% of GDP)

• South Africa has a GDP of R2.3 trillion,

• We transport goods weighing 935 million tons

• Over an average transport distance of 337 km

• At a cost of R339 billion • Plus an additional R34 billion

for externalities

Logistics costs as a percentage of GDP is at its lowest level since measurement started.

Source: 2009 State of Logistics Survey

• South Africa saw an increase of 6,9% in logistics costs to R339-billion in 2008, compared with the previous year’s R317-billion, and 2004’s R213-billion

• Despite the increase, 2008 costs were at their lowest as a percentage of gross domestic product (“GDP”) since the survey was first introduced in 2004, totaling 14,7% of GDP, down from last year’s 15,9%.

1313

Share of cost by category%

Cost breakdown by categoryIndexed 2003 for 2008

80

130

180

230

280

2003 2004 2005 2006 2007 2008

Inde

xed

= 2

003

Transport Storage and PortsManagement, Admin & Profit Inventory carrying cost

Inventory carrying cost

Management, Admin & Profit

Storage and Ports

Transport

Transport costs and inventory carrying costs have increased at a faster rate than other cost components

Implications for supplier development

• South Africa requires more transport over

the coming years.

• High forecast volume growth will put an

impossible strain on current transport

infrastructure if the current modal split

remains intact.

• Increasing rail market share will reduce

transport costs.

• Furthermore, if the oil price significantly

increases, this will seriously harm the

country’s competitiveness.

• Therefore, mitigation against oil price

fluctuations is critical.

• Increase in electricity tariffs places

additional costs and informs infrastructure

and rolling stock procurement strategies.

19%

50%

14%

17%

1414

Next steps

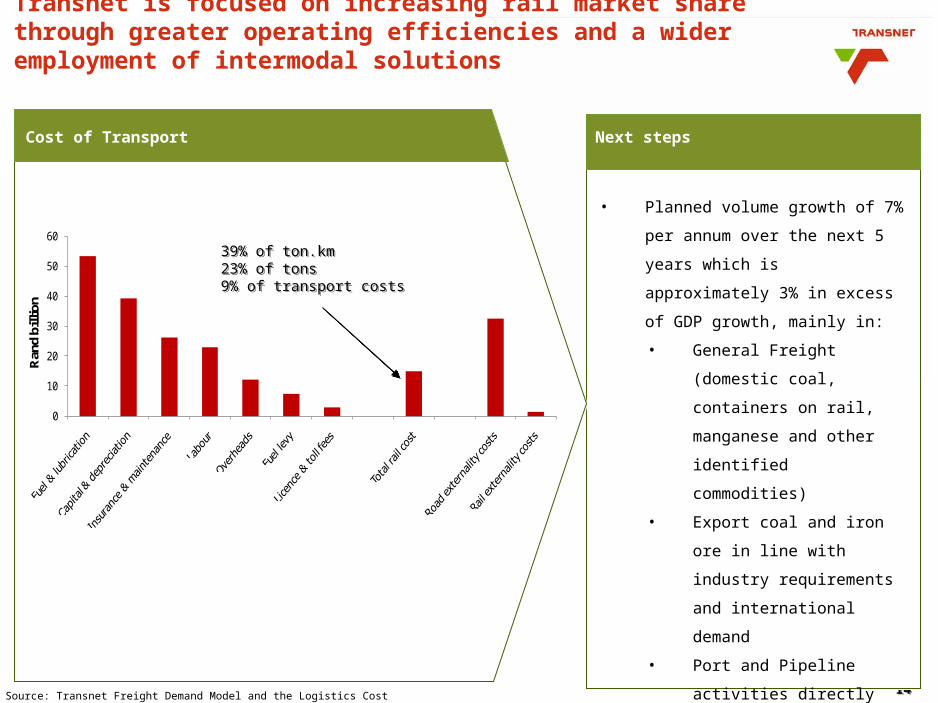

Transnet is focused on increasing rail market share through greater operating efficiencies and a wider employment of intermodal solutions

Source: Transnet Freight Demand Model and the Logistics Cost Model

0

10

20

30

40

50

60

Ran

d bi

llion

39% of ton.km23% of tons9% of transport costs

39% of ton.km23% of tons9% of transport costs

• Planned volume growth of 7%

per annum over the next 5

years which is approximately

3% in excess of GDP growth,

mainly in:

• General Freight (domestic

coal, containers on rail,

manganese and other

identified commodities)

• Export coal and iron ore in

line with industry

requirements and

international demand

• Port and Pipeline activities

directly linked to GDP

growth and demand

(economic activity)

Cost of Transport

1515

However, perception of rail is weak globally in comparison to other modes

Source: World Bank, Connecting to Compete, 2010

“So far there are few examples of efficient

container movement by rail that compete with

roads”

“Price signalling alone is unlikely to encourage a substantial shift towards

freight rail beyond captive markets such as

bulk goods”

1616

1. Transnet Performance and targets

2. Cost of doing business regarding rail and freight

3. Utilising public procurement spend to reduce supply chain costs- challenges and implications

4. Opportunities and challenges presented by IPAP2

Contents

Topics

1717

Transnet has increased its spend with BBBEE suppliers significantly over the past 4 years

Source: Transnet

• Significant focus has been placed on the BBBEE scorecard ratings

• Emphasis has been placed on improving on Preferential Procurement and Enterprise Development

• Spend with BBBEE companies has increased significantly

201020102009200920082008

BBBEE Spend (R billions)

1818

Off a Total Procurement Spend of R20,68bn R13.52bn was spent on BBBEE companies in 2009/10

BEE procurement

R13.5bn accounting for 65.35% of total procurement spend against a target of 65%

Exempted Micro Enterprise (turnover below R5m) procurement

R1.9bn accounting for 9.23% of total procurement spend against a target of 5%

Qualifying Small Enterprise (turnover between R5m and R35m) procurement

R2.7bn accounting for 13.24% of total procurement spend against a target of 5%

Black Women Owned (30% shareholding) procurement

R837m accounting for 4.05% of total procurement spend against a target of 6%

Black Owned (50% shareholding) procurement

R3.1bn accounting for 15.33% of total procurement spend against a target of 9%

1919

Supplier development is influenced by industrial policy and Transnet is currently partnering with government on a number of key action plans

Strengthen NIPP

Strengthen alignment between CSDP and NIPP

Alignment between BBBEE and industrial policy

• Transnet has made significant progress in the adoption of CSDP. Over the past two years a phased approach to embedding CSDP at Transnet has been followed:

• Phase 1: Develop the Plan;

• Phase 2: Build the Foundation; and

• Phase 3: Embed CSDP.

• Significant CSDP transactions leading to high value supplier development interactions have been concluded with:

• EMD; and

• GE.

• Transnet will augment its short term purchasing strategy with a move towards more long term strategic Fleet Procurement (Locomotives).

• Transnet, together with UNIDO, is participating in the National Foundry Technology Network (NFTN), which is an initiative with the key objective of facilitating the development of a South African foundry industry through appropriate skills training and technology transfer.

• Transnet has made significant progress in the adoption of CSDP. Over the past two years a phased approach to embedding CSDP at Transnet has been followed:

• Phase 1: Develop the Plan;

• Phase 2: Build the Foundation; and

• Phase 3: Embed CSDP.

• Significant CSDP transactions leading to high value supplier development interactions have been concluded with:

• EMD; and

• GE.

• Transnet will augment its short term purchasing strategy with a move towards more long term strategic Fleet Procurement (Locomotives).

• Transnet, together with UNIDO, is participating in the National Foundry Technology Network (NFTN), which is an initiative with the key objective of facilitating the development of a South African foundry industry through appropriate skills training and technology transfer.

IPAP Key Action PlansIPAP Key Action Plans Transnet’s Participation in IPAPTransnet’s Participation in IPAP

Overhaul of PPPFA

Identification of strategic fleets

Source: Transnet and IPAP2

Current phase

2020

Transnet has already secured three major CSDP transactions

§ The current CSDP plan with EMD was finalised in November 2009.§ The EMD CSDP plan aims for (1) TRE to become part of EMD’s Global Supply Chain for

rebuilt traction motors and diesel engines, (2) to accredit TRE’s maintenance facilities for EMD locomotive maintenance and (3) to localise the supply of at least 10% of the value and/or quantity of the parts listed per the Spare Parts Agreement.

§ These CSDP goals will be achieved through the transfer of skills and relevant intellectual property required to carry out the activities mentioned.

§ EMD is already actively supporting TRE in acquiring new work in Africa. Such deals will be handled on a partnership basis – TRE is to do the work but commits to purchase the parts from EMD.

§ Execution of the EMD CSDP plan is well underway – Tooling has already been provided and EMD experts (approximately 5 at any one time) have been on the floor since 1 January 2010, guiding, training and advising employees to achieve the desired end state.

§ The contract for the building of the 100 Locomotives was awarded to GE and signed on 17 December 2009.

§ GE developed a CSDP plan consisting of 3 main initiatives – training for maintenance development, Lean Six Sigma and Candidate Engineers; localisation of various components and parts as well as a licence agreement with TRE for the overhaul and modernisation of GE locomotives.

§ The details of this plan are under negotiation with every attempt being made by Transnet to ensure that activities provided meet the desired end state.

§ The signing of the CSDP Plan is likely to be postponed to June 2010 to ensure that a licensing commitment is reached between GE and Transnet.

§ The Licence Agreement would allow for TRE and GE to enter into a technology partnership for locomotive overhauls and modernisations, with GE being the prime contractor and TRE the sub-contractor.

• The GE 100 loco deal is the biggest CSDP transaction to date making Transnet the leader in CSDP execution

• The DPE has indicated their satisfaction with Transnet ‘s CSDP progress thus far

• TRE will be a centre of excellence for locomotive OEMs.

EMD:Spare partsContract Value:R550 million

GE: 100 Loco dealContract Value:R2.6 billion

50 “Like new” locomotives

§ 50 “Like-new” programme now complete under the equivalent of the CSDP Framework using Transnet Rail Engineering

2121

CSDP/SD Component Strategic Thrust

Transnet has also had a number of successful Supplier Development (SD) initiatives over the past 3 years resulting in significant development opportunity for the local industry

•Local manufacturing of railway crossings

•Transnet and the National Foundry Technology Network matched foundry to 100% local supply component

•CSDP obligations were also included into the new tenders

•Local re-profiling of gears•Feasibility study to establish localisation opportunity

•Skills Development•Building a Cargotec (port handling equipment and freight solutions) training school with free training hours

•Specific will be centred around Ngqura

•Has previous NIPP obligations which they need to fulfill within 7 years from start of obligation

•Training facility

•Training for approximately 20 TRE maintenance practitioners

Extension of the 19E contract – electric locomotive – by 35 vehicles

2222

Further opportunity exists to participate in Government’s metal fabrication, capital equipment and transport equipment key action plan (KAP)

New Areas of Focus

Metal Fabrication, capital equipment and transport equipment

Opportunities for growing the sector / achieving higher impact include:

•Leveraging the public infrastructure programme presents an opportunity to stimulate the industry through reducing import leakage of the capital and operational expenditure programmes.

•Export opportunities in the rest of Africa and South America.

•Opportunity to extend value chains through further downstream manufacturing.

Opportunities for growing the sector / achieving higher impact include:

•Leveraging the public infrastructure programme presents an opportunity to stimulate the industry through reducing import leakage of the capital and operational expenditure programmes.

•Export opportunities in the rest of Africa and South America.

•Opportunity to extend value chains through further downstream manufacturing.

Key Action Programme

Transnet, working together with the United Nations Industrial Development Organisation (“UNIDO”), is participating in the National Foundry Technology Network (“NFTN”), which is an initiative with the key objective of facilitating the development of a South African foundry industry through appropriate skills training and technology transfer.

Outcomes of this initiative:

• Reduced import leakage;

• Increased investments in key manufacturing processes and activities; and

• Increased employment.

Key Action Programme

Transnet, working together with the United Nations Industrial Development Organisation (“UNIDO”), is participating in the National Foundry Technology Network (“NFTN”), which is an initiative with the key objective of facilitating the development of a South African foundry industry through appropriate skills training and technology transfer.

Outcomes of this initiative:

• Reduced import leakage;

• Increased investments in key manufacturing processes and activities; and

• Increased employment.

Source: 2010/11 – 2012/13 Industrial Policy Action Plan

2323

Integrated South African Procurement

Academy (ISAPA): Independent Procurement Academy has been established.

BOOTCAMPS:Three successful boot camps have been held to train procurement staff nationally in professional procurement principals.

Member of the Chartered Institute ofPurchasing and Supply (MCIPS): • Transnet launched a comprehensive

procurement capability building programme.

• Core to the programme is an ambitious procurement skills development programme, that is being run in partnership with the Chartered Institute of Procurement in the UK.

• Presently, 235 learners are registered in courses of the programme.

• During phase 1, twelve people have already achieved a fast-track globally recognised honours degree in procurement from the programme.

Capability Building Collaboration forum

Initiated the use of the R&HSCA (Rail & Harbour Supply Chain Association) as a collaborative initiative with local tier 2 & 3 suppliers.

The focus of the association is on exchange of current trends, research and development, future plans and local supplier capability.– SADC operators will also be

encouraged to participate allowing local suppliers to expand into Africa.

• Transnet in partnership with UNIDO:

Has established a benchmarking program of its top twenty tier two South African suppliers as well as the top 60 tier 3 suppliers.

The objective is to enhance the competitiveness of these suppliers and position them as key components of the Transnet Original Equipment Manufacturers supply chain.

To execute on the IPAP requirements, Transnet will focus on its procurement skills and capabilities

2424

1. Overview of Transnet Performance

2. Cost of doing business regarding rail and freight

3. Utilising public procurement spend to reduce supply chain costs- challenges and implications

4. Opportunities and challenges presented by IPAP2

Contents

Topics

2525

Proposed IPAP action plans

• Over the IPAP period the intention is to identify eight to ten large and strategic procurement “fleets”.

• Locomotives, wagons and coaches for freight and commuter rail procured by Transnet and the Passenger Rail Agency of South Africa (“PRASA”) have been selected as a strategic fleet.

• IPAP ensures a mechanism to “designate” large, strategic and repeat “fleet” procurements.

• Procuring entities of designated “fleets” will be required to develop a long-term strategic plan in conjunction with DTI which sets out a detailed specification of the tender setting out explicitly the sequentially increase of local procurement and supplier development requirements.

Migration to programmatic fleet procurement practices provides significant value opportunity for Transnet

Opportunities for Transnet

• Migration from Transactional procurement of locomotive fleet to strategic programmatic procurement practices resulting in:

• Standardisation of local fleet and a standardisation strategy commensurate with international demand to ensure industry sustainability

• Alleviation of the legislative restriction on long term supplier contracts to enhance the opportunity for supplier development (migration from 5 year contracts to 15 year engagements)

• Improved demand visibility resulting in stronger investment commitment from international OEMs

• Renewal of current fleet resulting in improved availability, reliability and reduced cost increased volume capacity

Source: 2010/11 – 2012/13 Industrial Policy Action Plan

2626

There is significant demand to support a strategic procurement programme as envisaged in IPAP2

SA can become supplier to Africa, Australia, Brazil and all other countries that run on Cape (1067mm) or metric (1000mm) gauge.

Can supply new as well as upgrade locomotives for abovementioned countries.

Negate FOREX influence on a major portion of locomotive prices for Transnet.

Boost steel industry in SA by using local supply for structural components.

Stimulate control system industry in SA by increasing technology requirement.

Increased requirements for special steel and copper for electric motor building.

Increase overall engineering & technological capability of SA.

• Transnet has developed a locomotive fleet plan which is aimed at reducing the average age of the locomotive fleet from 30 years to below 20 years.

• To achieve this Transnet will purchase between 75 and 100 locos per annum over a prolonged period.

• Through smoothing the acquisition cycle, Transnet will better enable local development by providing a stable pattern of demand.

• Transnet is also developing a fleet plan for cranes and is investigating CSDP opportunities through this plan.

2727

Transnet is in full support of the Industrial Policy Action Plan and anticipates a number of advantages for Transnet and its domestic supplier industry arising from the implementation of the Plan

• A world class freight system is critical for increased industrialisation in South Africa and the region.

• Transnet is focused on improving market share and customer service through an enhanced focus on operating efficiencies, infrastructure investment and public private partnerships.

• Transnet remains committed to strengthening its role as an active IPAP partner by accelerating the implementation of CSDP across the business.

• Transnet can gain significantly from a migration to programmatic procurement.

27

2828

Thank You

2929

Additional Information

3030

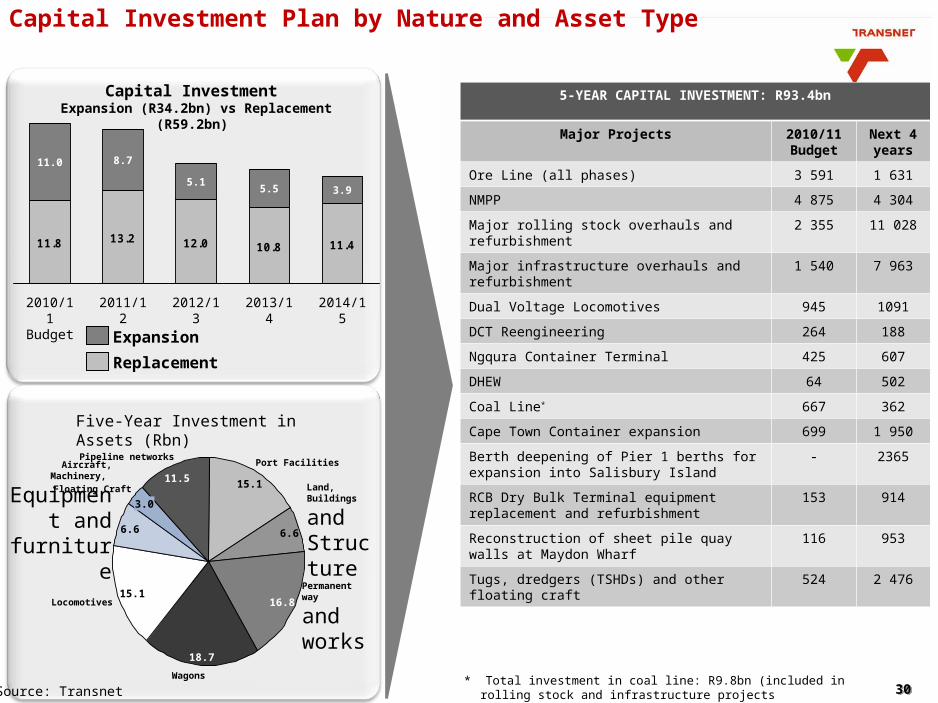

Capital Investment Plan by Nature and Asset Type

11.8 13.2 12.0 10.8 11.4

2014/15

3.9

2013/14

5.5

2012/13

5.1

2011/12

8.7

2010/11

Budget

11.0

Replacement

Expansion

Capital Investment Expansion (R34.2bn) vs Replacement

(R59.2bn)

Pipeline networks

11.5Aircraft, Machinery,

Equipment and

furniture

6.6

Wagons

18.7

16.8

Permanent way

and works

Land, Buildings

and Structure

6.6

Port Facilities

15.1

15.1Locomotives

3.0

Floating Craft

Five-Year Investment in Assets (Rbn)

5-YEAR CAPITAL INVESTMENT: R93.4bn

Major Projects 2010/11 Budget

Next 4 years

Ore Line (all phases) 3 591 1 631

NMPP 4 875 4 304

Major rolling stock overhauls and refurbishment

2 355 11 028

Major infrastructure overhauls and refurbishment

1 540 7 963

Dual Voltage Locomotives 945 1091

DCT Reengineering 264 188

Ngqura Container Terminal 425 607

DHEW 64 502

Coal Line* 667 362

Cape Town Container expansion 699 1 950

Berth deepening of Pier 1 berths for expansion into Salisbury Island

- 2365

RCB Dry Bulk Terminal equipment replacement and refurbishment

153 914

Reconstruction of sheet pile quay walls at Maydon Wharf

116 953

Tugs, dredgers (TSHDs) and other floating craft

524 2 476

* Total investment in coal line: R9.8bn (included in rolling stock and infrastructure projectsSource: Transnet

3131

Understanding South Africa’s Port Costs

$0.00

$100,000.00

$200,000.00

$300,000.00

$400,000.00

$500,000.00

$600,000.00

SA

NTO

SV

ER

A C

RU

ZB

UE

NO

S A

IRE

S

LAE

M C

HA

BA

NG

YO

KO

HA

MA

NA

GO

YA

AN

TWE

RP

SIN

GA

PO

RE

LE H

AV

RE

TILB

UR

YB

RE

ME

RH

AV

EN

CA

PE

TO

WN

DU

RB

AN

PO

RT

ELI

ZAB

ETH

CH

AR

LES

TON

BA

LTIM

OR

EN

EW

YO

RK

Terminal Handling Charge Cargo Dues Sea Side Costs

• Cargo dues are the charges that Transnet charges port users for the recovery of its investment in port infrastructure

• Transnet is solely responsible for all port infrastructure investment: land, berths, docks, dredging (berth side, turning basin & channel) and receives no subsidies from central government or local government for these costs

• Comparing SA’s port costs needs to show institutional responsibility for port infrastructure, which varies widely between ports

• Port investments made by central and local governments in other countries are not recovered through port charges

• Transnet must recover its investments in port infrastructure to ensure future investments

DTI’S PORT COSTS COMPARISON GRAPH: AIDC Port Benchmarking Study, 2007

Average Cost per Vessel Call

3232

Understanding South Africa’s Port Costs (cont.)

32

IDENTIFICATION OF INSTITUTIONAL RESPONSIBILITY FOR PORT INVESTMENT ITEMS

Major Category Sub-Items SingaporeChina

(Waigaoqiao)Hong Kong Antwerp

South Africa

Maritime Access Infrastructure Channel CG CG LG CG PA

Breakwater CG CG LG CG PA

Navigation Aids CG CG LG CG PA

Port Infrastructure Land PA TO TO PA PA

Berths PA TO TO PA PA

Docks PA TO TO PA PA

Dredging:

- Berth Side TO TO LG PA PA

- Turning Basin CG PA LG CG PA

- Channel CG PA LG CG PA

Port Superstructure Cranes TO TO TO TO TO

Terminal TO TO TO TO TO

Sheds TO TO TO TO TO

Land Access Infrastructure Road Links CG CG CG CG LG & PA

Rail Links CG CG CG CG Other

Inland N/A CG CG CG N/A

Abbreviations: CG: Central Government; LG: Local Government; PA: Port Authority; TO: Terminal Operator

3333

South Africa’s port performance is higher than average

South Africa

Sub-Saharan Africa

Upper middle

income Clearance time with physical inspection (days)

2.67 4.94 2.94Clearance time without physical inspection (days) 0.5 2.83 1.57Lead time export for port/airport, median case (days) 2.28 7.79 2.91Lead time import for port/airport, median case (days) 3.25 7.05 4.1Typical charge for a 40-foot export container or a semi-trailer (US$) 907.33 2,240.56 1,264.98Typical charge for a 40-foot import container or a semi-trailer (US$) 1,516.22 3,045.00 2,473.01

Source: World Bank, Connecting to Compete, 2010

South Africa and the region are exposed to high container shipping charges and attempts to address this are underway through the establishment of a regional transhipment hub at the Port of

Ngqura.

![Transnet Port Terminal, a division of · Transnet Port Terminal, a division of TRANSNET SOC LTD Registration Number 1990/000900/30 [Hereinafter referred to as Transnet] REQUEST FOR](https://static.fdocuments.in/doc/165x107/5f5e4faa6b0e6821912b906b/transnet-port-terminal-a-division-of-transnet-port-terminal-a-division-of-transnet.jpg)

![Transnet]...TRANSNET FRAIGHT RAIL, a division of TRANSNET SOC LTD Registration Number 1990/000900/30 [thereinafter referred to as Transnet] REQUEST FOR QUOTATION …](https://static.fdocuments.in/doc/165x107/6050751b455b0f3d741c0d14/transnet-transnet-fraight-rail-a-division-of-transnet-soc-ltd-registration.jpg)