Transitioning to a world-class country Dr Roelof Botha.

62

Transitioning to a world- class country Dr Roelof Botha

-

Upload

jayden-ballard -

Category

Documents

-

view

226 -

download

1

Transcript of Transitioning to a world-class country Dr Roelof Botha.

Transitioning to a world-class countryTransitioning to a world-class country

Dr Roelof Botha Dr Roelof Botha

• Health data – a snapshot

• Megatrends impacting on the global economy

• SA’s competitiveness challenges

• Policies employed by advancing nations with high growth

• Rewards of free enterprise reforms

• Pockets of excellence in SA

• A pragmatic policy agenda for South Africa

• Economic growth prospects – gradual improvement

Overview of themes – getting SA to the elusive high

road scenario

The Southern African economy Prospects for sustained growth

The Southern African economy Prospects for sustained growth

Global health trends – a snapshot

Global health trends – a snapshot

Structural increase in household expenditure on

health (SA)

90

110

130

150

170

190

210Index; 1997 = 100

Health

Total

Health expenditure as % of totals – government &

households (SA)

7

8

9

10

11

12

13

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

% Government

Households

Composition of government expenditure (functional

classification) FY 2013/14 (Rb)

General services 70.9

Public order 106.2

Other economic serv. 60.7

Health 137.7

Education 225.8

Environ. & culture 13.8

Social protection 171.5

Interest 99.7

Transport 60.8

Housing & comm. Dev. 105.4

Defence 40.6

Total R 1.1 trillion

Composition of household consumption expenditure

in South Africa 2012 (R billion)

Clothing 97Housing 302

Health 182

Recreation 73 Other 215

Education 57

Household goods 129

Transport 310

Food & hospitality 542

Total 1,9 trillion

Life expectancy at birth 2011 – selected African

countries

45 50 55 60 65 70 75

Sierra Leone

DR Congo

Lesotho

Angola

Nigeria

Zimbabwe

Uganda

South Africa

Tanzania

Namibia

Mauritius

Years

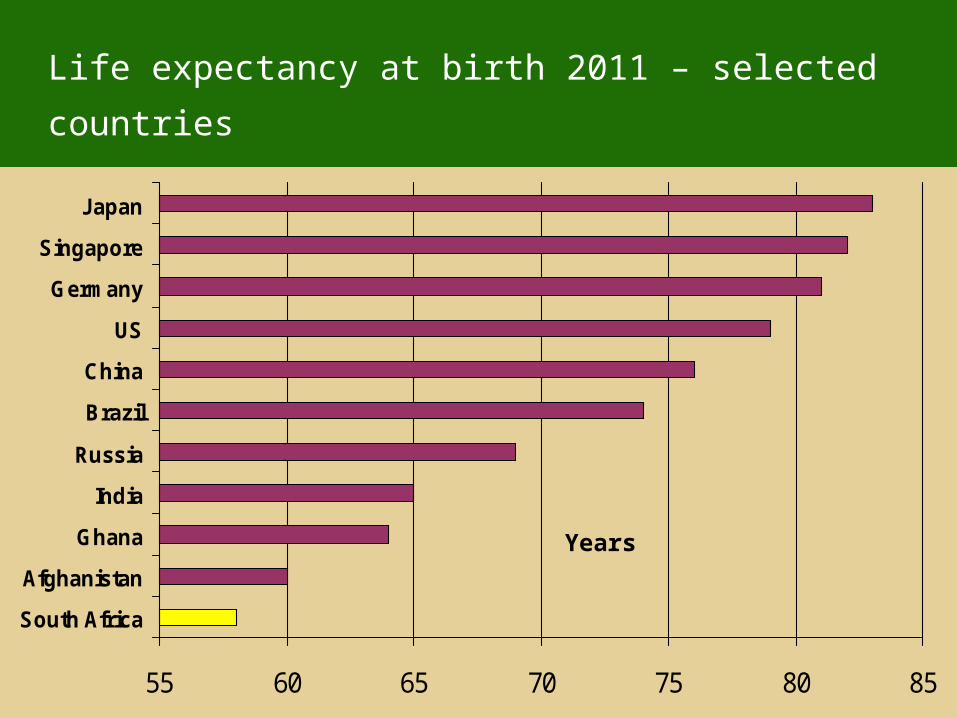

Life expectancy at birth 2011 – selected countries

55 60 65 70 75 80 85

South Africa

Afghanistan

Ghana

India

Russia

Brazil

China

US

Germany

Singapore

Japan

Years

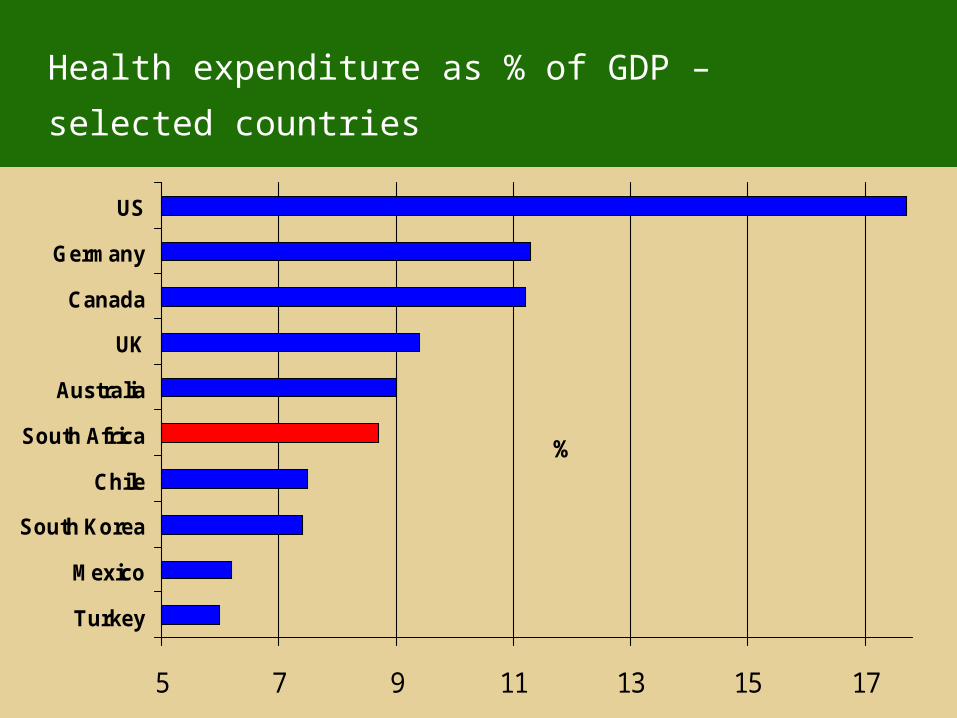

Health expenditure as % of GDP – selected countries

5 7 9 11 13 15 17

Turkey

Mexico

South Korea

Chile

South Africa

Australia

UK

Canada

Germany

US

%

Megatrends & the emergence of

multiple superpowers

The World Economic League

1st Division

HighIncome

Countries

2nd Division

EmergingMarket

Economies

3rd Division

Potential EmergingMarkets

4th Division(a)

SmallEconomies

(b)Failed states

Recommended route of progress (higher per capita income)

Megatrends en route to 2020 (selection)

• World population exceeds 7.6 billion

• Increased urbanisation, ageing rises

• Life expectancy increases to 71 years

• Further spread of democracy

• Rising per capita incomes

• New applications for nano-technology

• Further progress with bio-technology

• Computers will be 200 times faster

• Increased focus on renewable energy

• Emergence of multiple superpowers

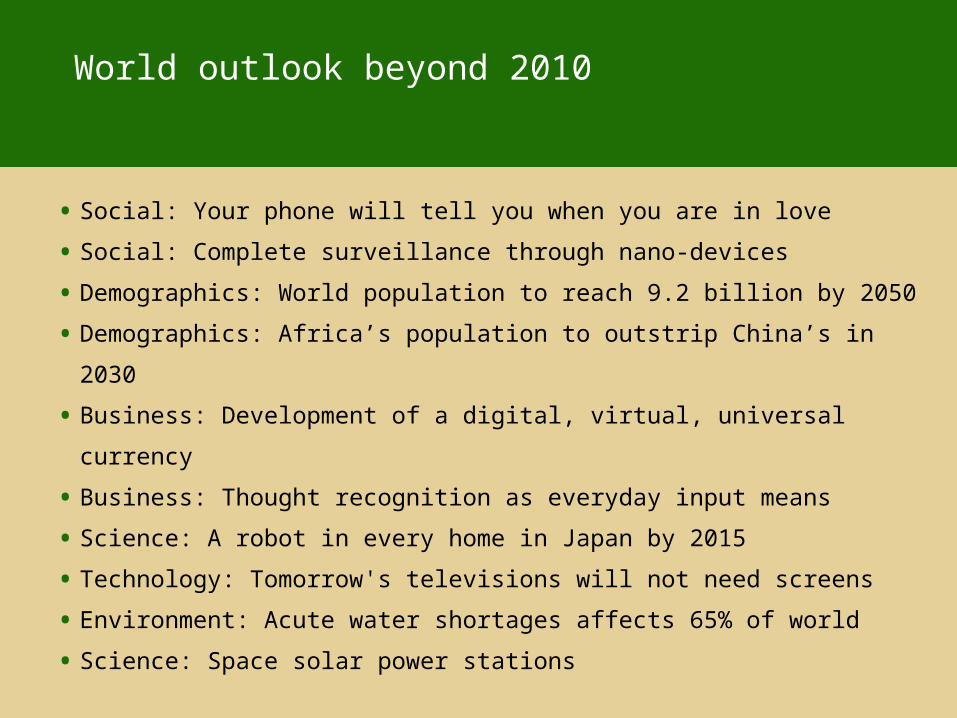

World outlook beyond 2010

• Social: Your phone will tell you when you are in love

• Social: Complete surveillance through nano-devices

• Demographics: World population to reach 9.2 billion by 2050

• Demographics: Africa’s population to outstrip China’s in 2030

• Business: Development of a digital, virtual, universal currency

• Business: Thought recognition as everyday input means

• Science: A robot in every home in Japan by 2015

• Technology: Tomorrow's televisions will not need screens

• Environment: Acute water shortages affects 65% of world

• Science: Space solar power stations

No of Boeing 747s in service

600

650

700

750

800

850

900

1985 1990 1995 2000 2005 2010 2013

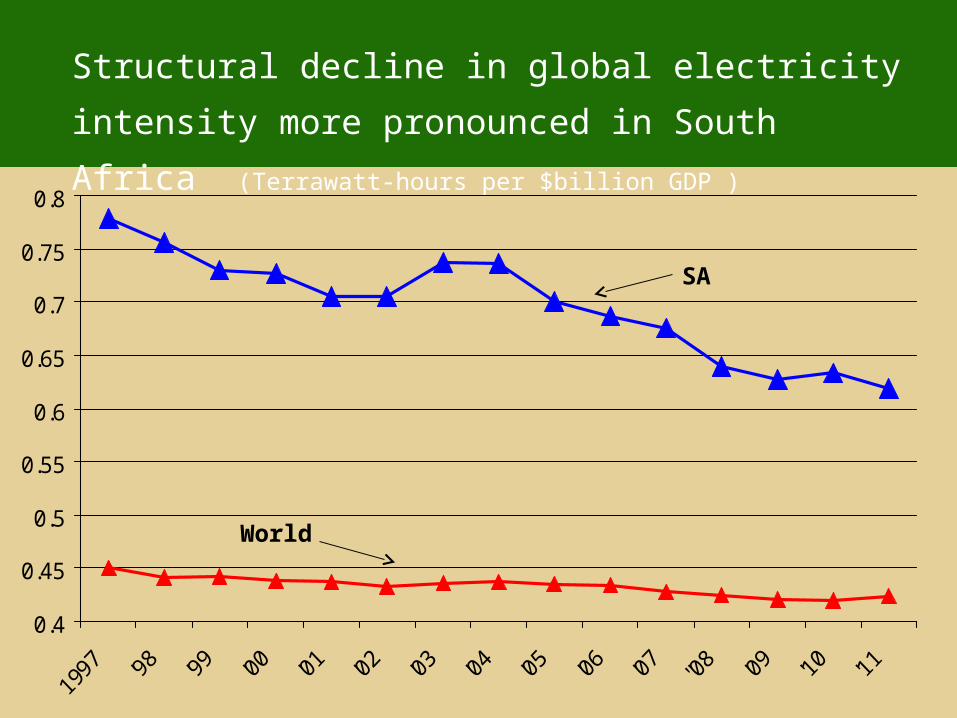

Structural decline in global electricity intensity more

pronounced in South Africa (Terrawatt-hours per $billion GDP )

0.4

0.45

0.5

0.55

0.6

0.65

0.7

0.75

0.8

World

SA

Share of global GDP (PPP) of emerging markets &

developing economies

25

30

35

40

45

50

55

1980 1985 1990 1995 2000 2005 2010 2017

%

Sizeable gap between the GDP growth performance

of advanced & emerging economies (Source: IMF)

-4

-2

0

2

4

6

8

1998 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 2012

% (real)

Emerging markets

Advanced

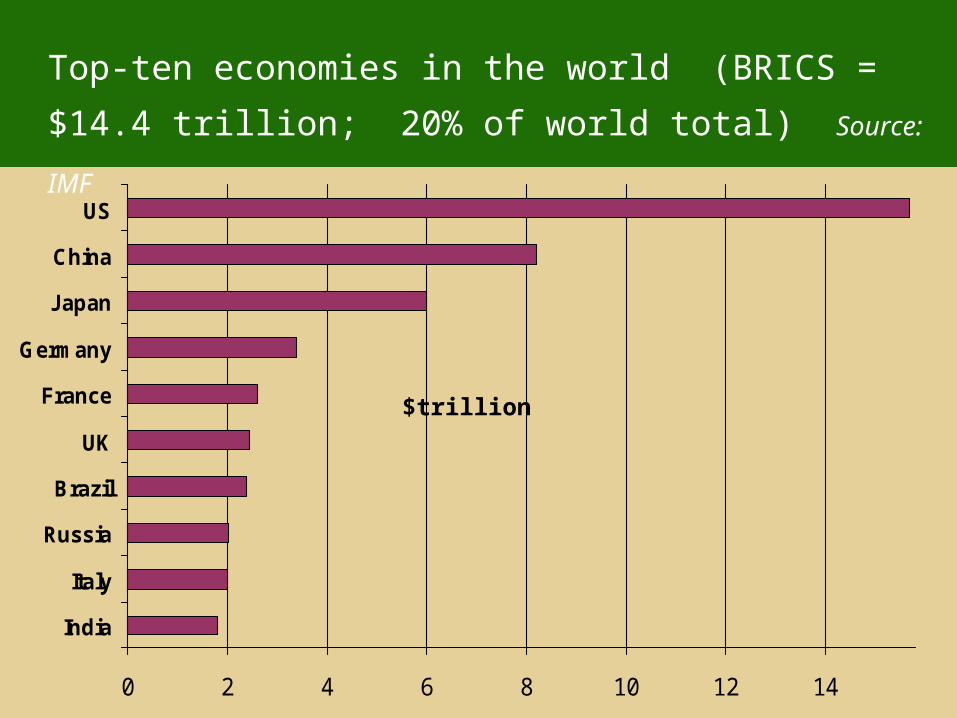

Top-ten economies in the world (BRICS = $14.4 trillion;

20% of world total) Source: IMF

0 2 4 6 8 10 12 14

India

Italy

Russia

Brazil

UK

France

Germany

Japan

China

US

$trillion

Regional composition of world population 2011

(BRICS = 42% of world total) (Source: UNDP)

China 1.4

SADC 0.3

Russia 0.14

North America 0.53

South America 0.2

Other Africa 0.7

Europe 0.6 Brazil 0.2

Other Asia 1.6

India 1.2

Total 6.9 billion

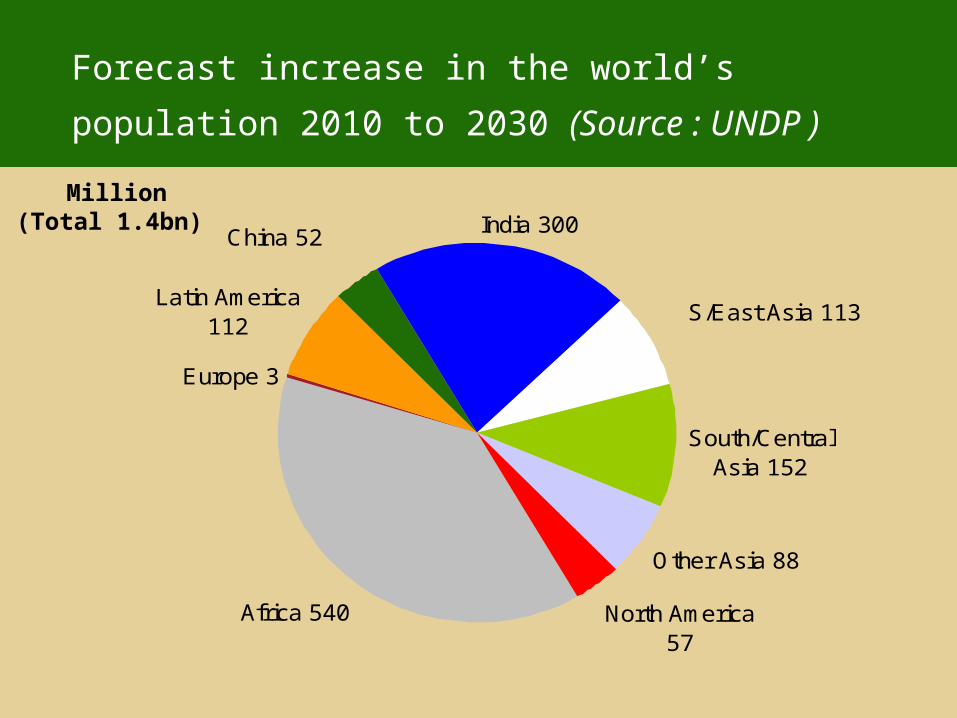

Forecast increase in the world’s population 2010 to

2030 (Source : UNDP )

Europe 3

Latin America 112

India 300

South/Central Asia 152

Other Asia 88

North America 57

China 52

S/East Asia 113

Africa 540

Million(Total 1.4bn)

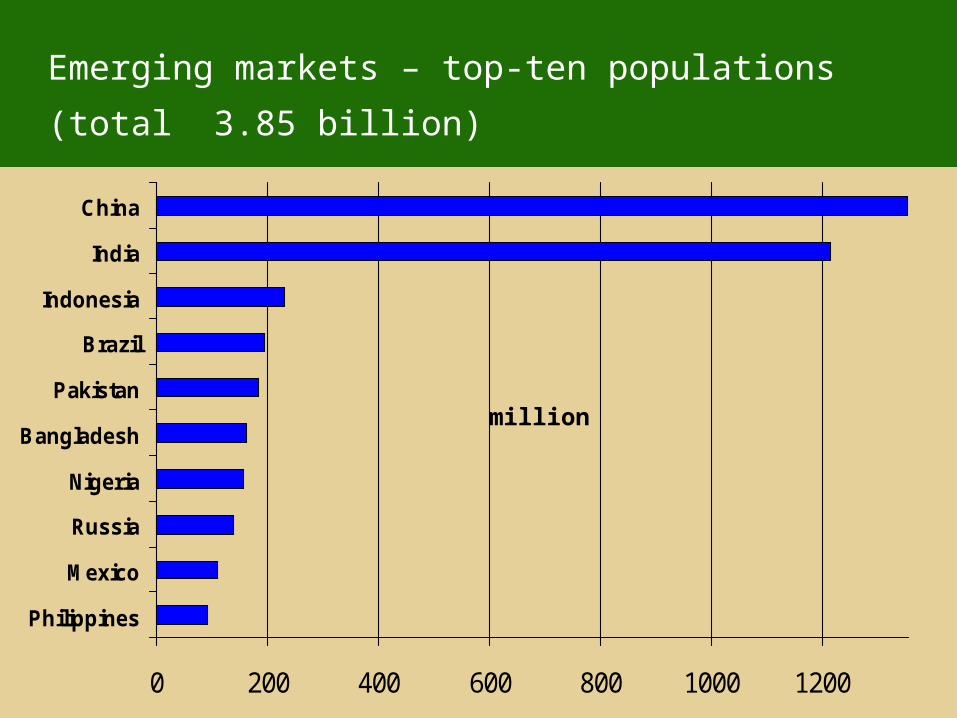

Emerging markets – top-ten populations

(total 3.85 billion)

0 200 400 600 800 1000 1200

Philippines

Mexico

Russia

Nigeria

Bangladesh

Pakistan

Brazil

Indonesia

India

China

million

Most populous developing countries & SADC

population

0 250 500 750 1000 1250

Philippines

Mexico

Russia

Nigeria

Bangladesh

Pakistan

Brazil

Indonesia

SADC

India

China

Million

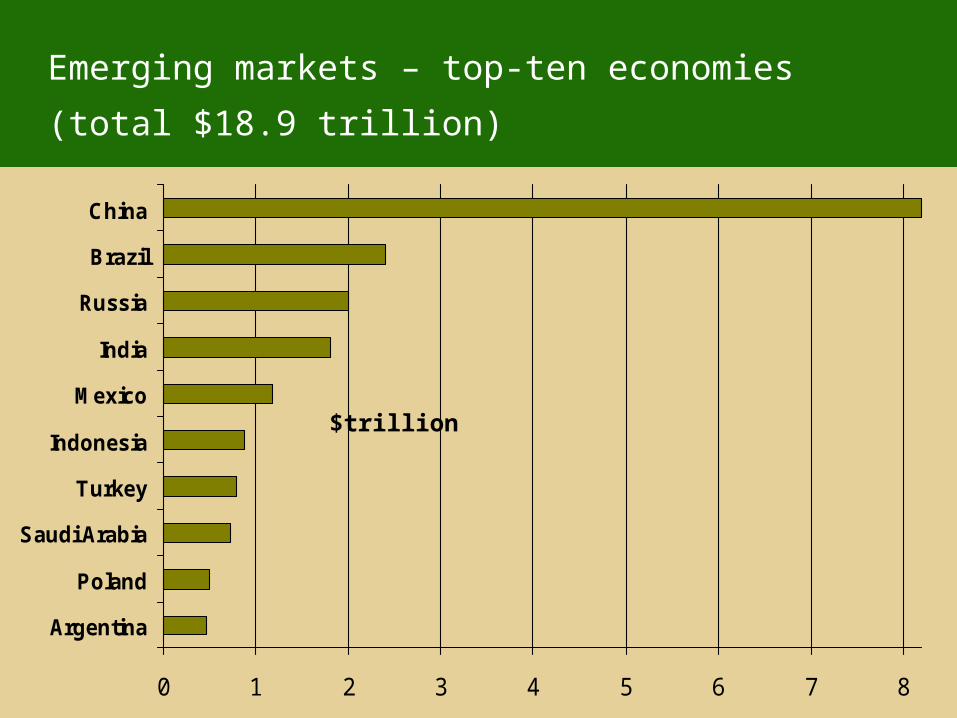

Emerging markets – top-ten economies

(total $18.9 trillion)

0 1 2 3 4 5 6 7 8

Argentina

Poland

Saudi Arabia

Turkey

Indonesia

Mexico

India

Russia

Brazil

China

$trillion

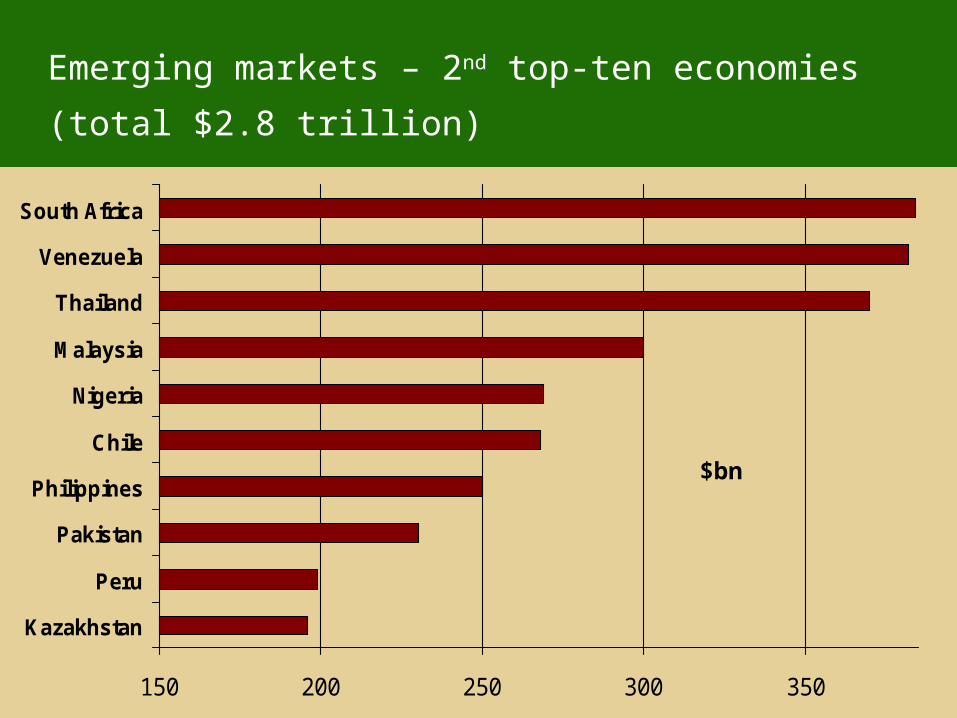

Emerging markets – 2nd top-ten economies

(total $2.8 trillion)

150 200 250 300 350

Kazakhstan

Peru

Pakistan

Philippines

Chile

Nigeria

Malaysia

Thailand

Venezuela

South Africa

$bn

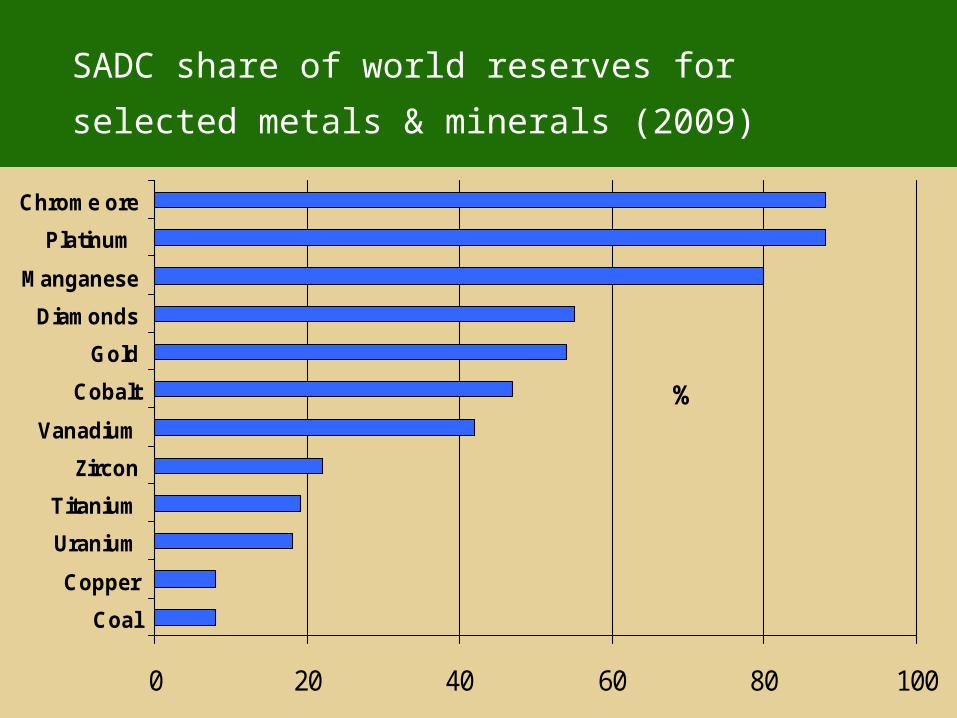

SADC share of world reserves for selected metals &

minerals (2009)

0 20 40 60 80 100

Coal

Copper

Uranium

Titanium

Zircon

Vanadium

Cobalt

Gold

Diamonds

Manganese

Platinum

Chrome ore

%

South Africa’s keycompetitiveness challengesSouth Africa’s keycompetitiveness challenges

Sharp contrast between the GDP growth paths of

Zambia and Zimbabwe (nationalisation in action)

2

5

8

11

14

17

20

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

$ billion Zambia

Zimbabwe

South Africa’s lowest ranked global competitiveness

indicators (out of 144 countries)

Cooperation in labour-employer relations 144

Hiring & firing practices 143

HIV prevalence 141

Quality of the educational system 140

Flexibility of wage determination 140

Pay & productivity 134

Business costs of crime & violence 134

Life expectancy 133

Business impact of tuberculosis 132

Burden of government regulation 123

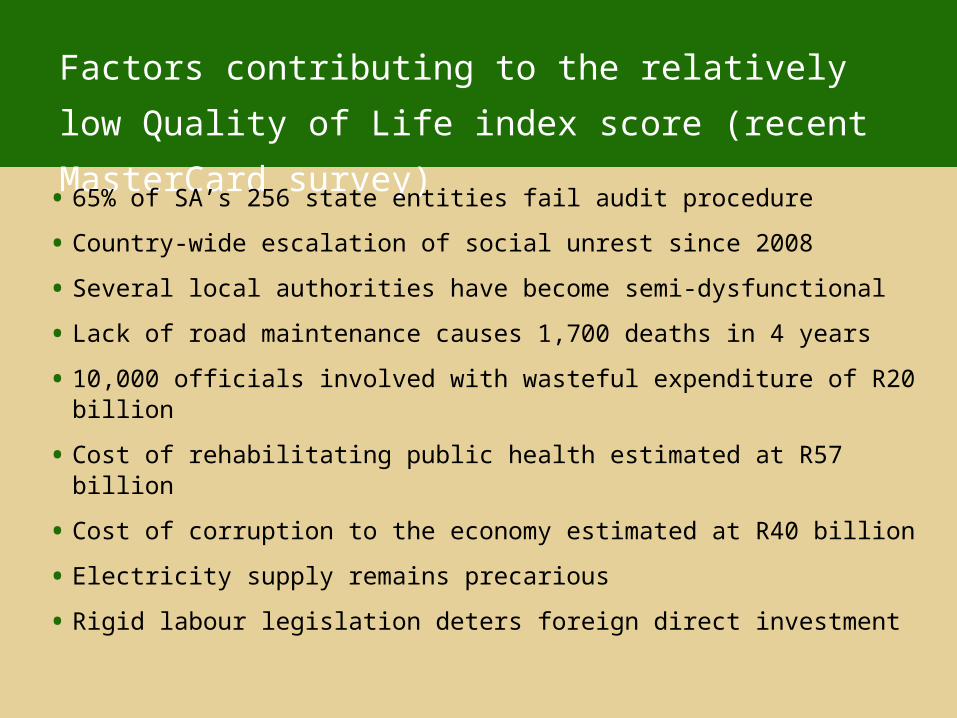

Factors contributing to the relatively low Quality of

Life index score (recent MasterCard survey)

• 65% of SA’s 256 state entities fail audit procedure

• Country-wide escalation of social unrest since 2008

• Several local authorities have become semi-dysfunctional

• Lack of road maintenance causes 1,700 deaths in 4 years

• 10,000 officials involved with wasteful expenditure of R20 billion

• Cost of rehabilitating public health estimated at R57 billion

• Cost of corruption to the economy estimated at R40 billion

• Electricity supply remains precarious

• Rigid labour legislation deters foreign direct investment

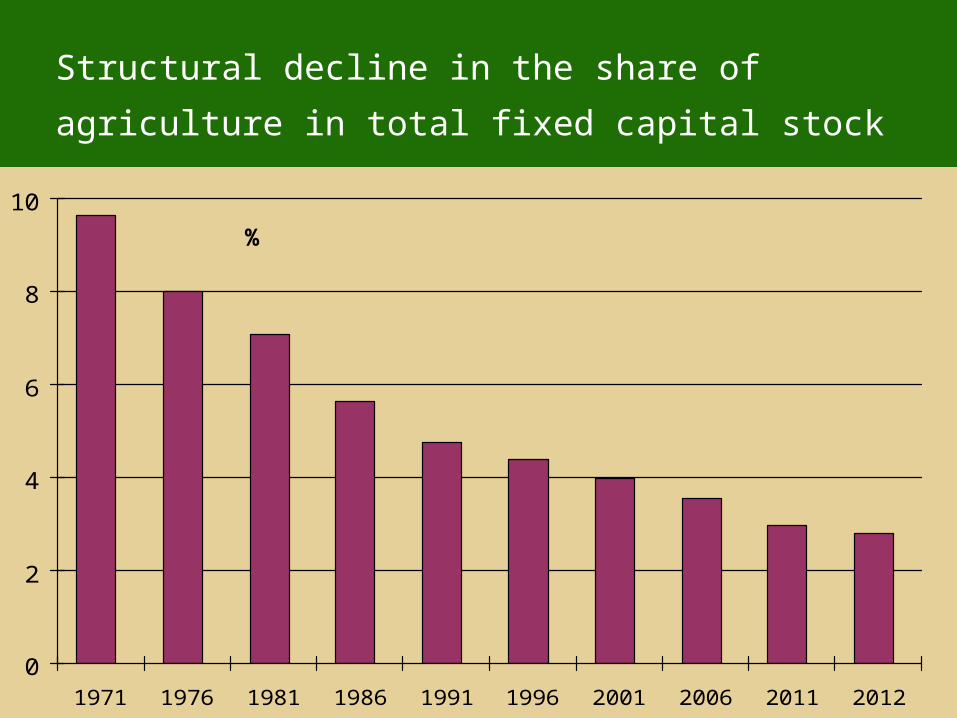

Structural decline in the share of agriculture in total

fixed capital stock

0

2

4

6

8

10

1971 1976 1981 1986 1991 1996 2001 2006 2011 2012

%

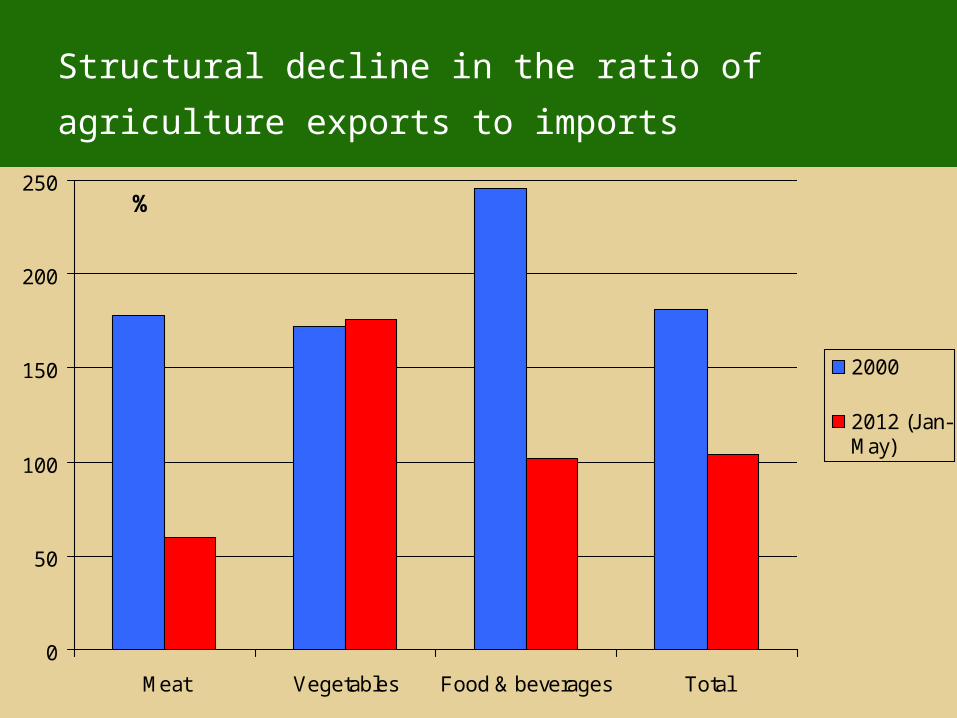

Structural decline in the ratio of agriculture exports

to imports

0

50

100

150

200

250

Meat Vegetables Food & beverages Total

2000

2012 (Jan-May)

%

Employment in agriculture in South Africa

(forecast for 2013)

400

500

600

700

800

900

1000

1100

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

‘000

Indices of labour productivity & unit labour costs in

manufacturing (2000 = 100)

90

110

130

150

170

190

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

Index Labour costs

Productivity

The recession is over – prepare for higher growthThe recession is over – prepare for higher growth

Dr Roelof BothaDr Roelof Botha

Policies implemented by winning countries

Policies implemented by winning countries

• Privatisation

• Market-related & productivity-related wage determination

• Lower direct tax rates

• Pro-active export promotion

• Lower import duties

• Separation of judicial & executive powers

• Public/private partnerships

• Vigilant stance towards preventing undue corruption

• Effective performance monitoring in the public sector

• Deregulation & other measures to encourage SMMEs

Post-1980 reforms - high growth economies

• Adequate expenditure on R&D

• Strategic industry status afforded to agriculture

• Guaranteed property rights (intellectual & physical)

• Prudent & transparent fiscal policy

• Emphasis on primary education

• Improved access to affordable health care

• Pro-active monetary policy

• Expansion & maintenance of infrastructure

• Cooperation between government, labour & business

• Expansion & diversification of international trade

Post-1980 reforms - high growth economies

(continued)

• Fiscal stability & expanding tax base

• Improvement of global competitiveness

• Relatively low inflation

• Enhanced food security

• Balance of payments stability

• Increased levels of FDI inflows

• Sustained economic growth & employment creation

• Higher national skills base

• Increased longevity

• Relatively high level of socio-political stability

Rewards of consolidating the tenets underpinning

free enterprise and democracy (Selection)

Progress with

the transition –

slow, but visible

Progress with

the transition –

slow, but visible

Towards a radical transformation of institutionalised

society in South Africa (* denotes qualified success)

Pre-1994 Post-1994

• Exclusive• Adversarial• Labour vs. capital• International isolation• Patronising• Neglect of common place• Hierarchial• Subordination of law to state• Violation of human rights

• Inclusive*• Co-operative*• Labour plus capital*• International assistance• Empowering/enabling• Illumination of common place• Networking• Law above the state• Manifestation of human rights

• 3 million RDP houses

• 1000 new health clinics

• Access to clean water for 10 million people

• New sanitation facilities for 7 million people

• 4.5 million new electricity connections

• Free education

• Redistribution of 3 million hectares of land

• Primary School Nutrition Programme for 5 million children

• 15 million new social grant beneficiaries (BIG?)

Progress with meeting basic needs

South Africa’s highest ranked global competitiveness

indicators (out of 144 countries)

Regulation of securities exchange 1

Auditing & reporting standards 1

Efficacy of corporate boards 1

Soundness of banks 2

Availability of financial services 2

Effectiveness of anti-monopoly policy 6

Reliance on professional management 13

Quality of air transport infrastructure 15

Quality of management schools 15

Efficiency of legal framework 16

SA facts & figures - a random selection

• 11th largest emerging market in the world

• World’s largest paper manufacturer (Sappi)

• World’s 2nd largest beer brewer (SAB)

• Sole producer of MB Class C RHD vehicles

• First-ranked world floral kingdom

• Top global ranking for a secondary capital market (JSE)

• No 2 global competitiveness ranking for soundness of banks

• First heart transplant in the world

• World leader in liquid fuel technology

• World’s most progressive democratic constitution

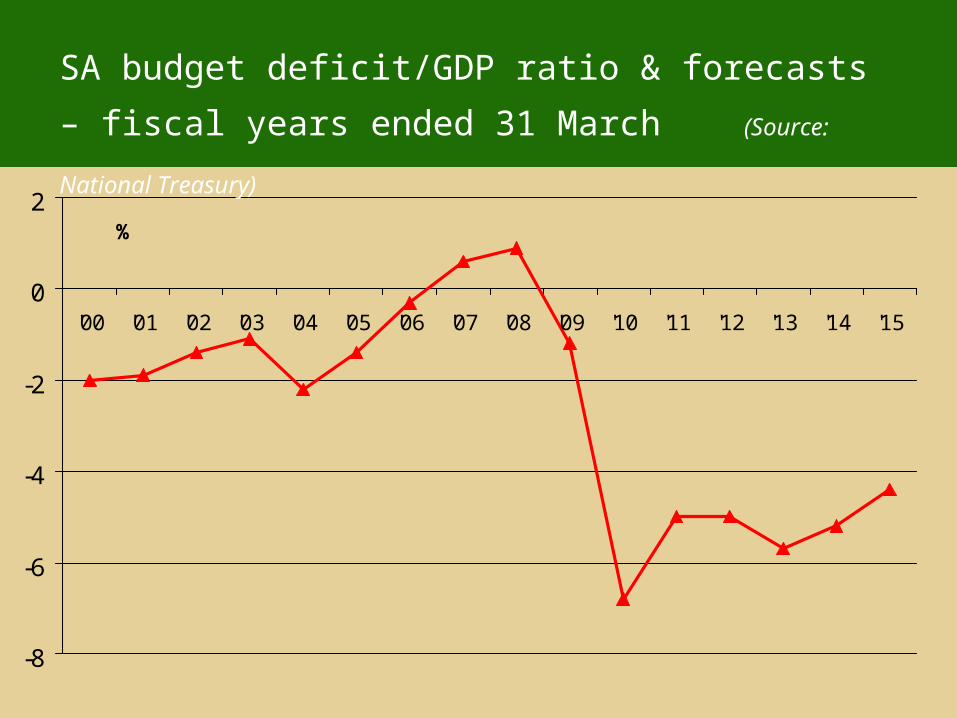

-8

-6

-4

-2

0

2

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

%

SA budget deficit/GDP ratio & forecasts – fiscal years

ended 31 March (Source: National Treasury)

Real effective exchange rate of the rand

80

85

90

95

100

105

110

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Index, 2000 = 100)

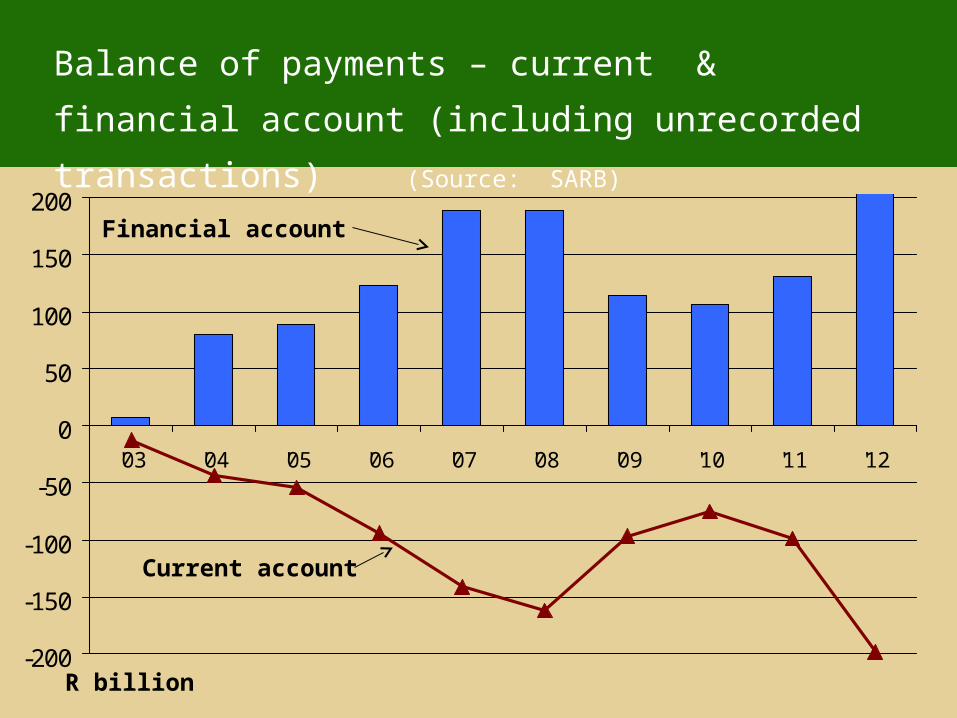

-200

-150

-100

-50

0

50

100

150

200

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12

R billion

Balance of payments – current & financial account

(including unrecorded transactions) (Source: SARB)

Financial account

Current account

Capital expenditure by public sector returns to growth

mode (after an absence of 3 decades)

2

4

6

8

10

12

14

16

'75 '80 '85 '90 '95 '00 '05 '10

Capex/GDP %

Private sector

Public sector

A pragmatic policy agenda

• Introduction of a basic income grant (BIG)

• Combating of corruption & vigilance with tender procedures

• Management training for public service

• Incentives for entrepreneurship & SMMEs

• Task teams to restore functionality of Municipalities

• Implementation of youth wage subsidy

• Restructuring of SETAs

• Multi-tiered system of labour regulations

• Fast-tracking of infrastructure spending

• Public/private partnerships (govt/business/labour “Codesa”)

The recession is over – prepare for higher growthThe recession is over – prepare for higher growth

Dr Roelof BothaDr Roelof Botha

Conclusion - consolidation of economic recoveryConclusion - consolidation of economic recovery

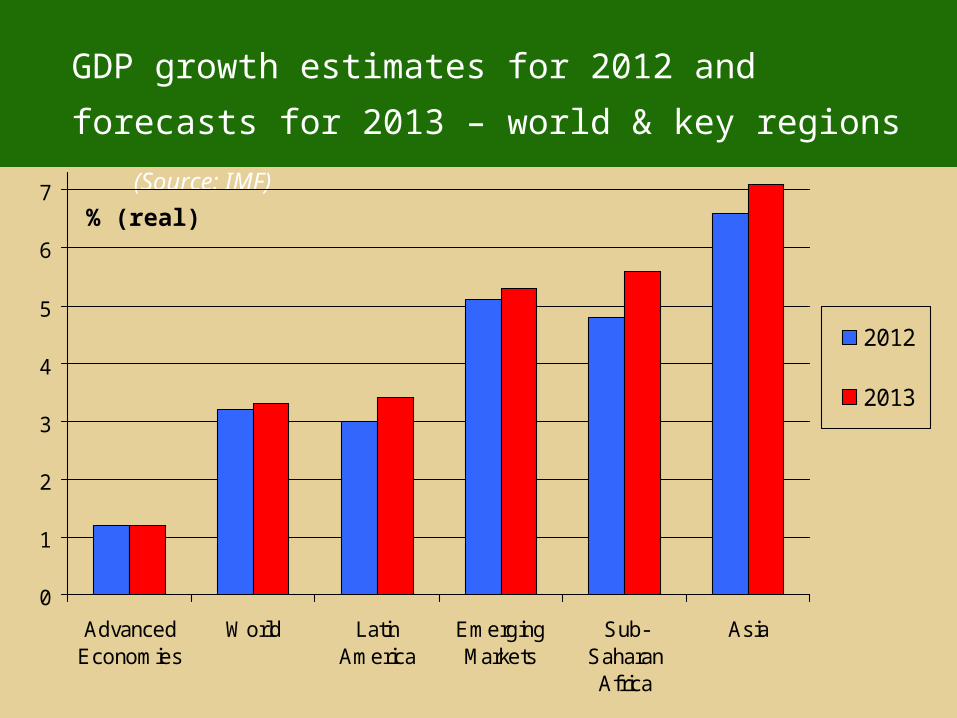

GDP growth estimates for 2012 and forecasts for 2013

– world & key regions (Source: IMF)

0

1

2

3

4

5

6

7

AdvancedEconomies

World LatinAmerica

EmergingMarkets

Sub-SaharanAfrica

Asia

2012

2013

% (real)

Real retail trade sales (index, 2008 = 100)

93

96

99

102

105

108

111

114Index

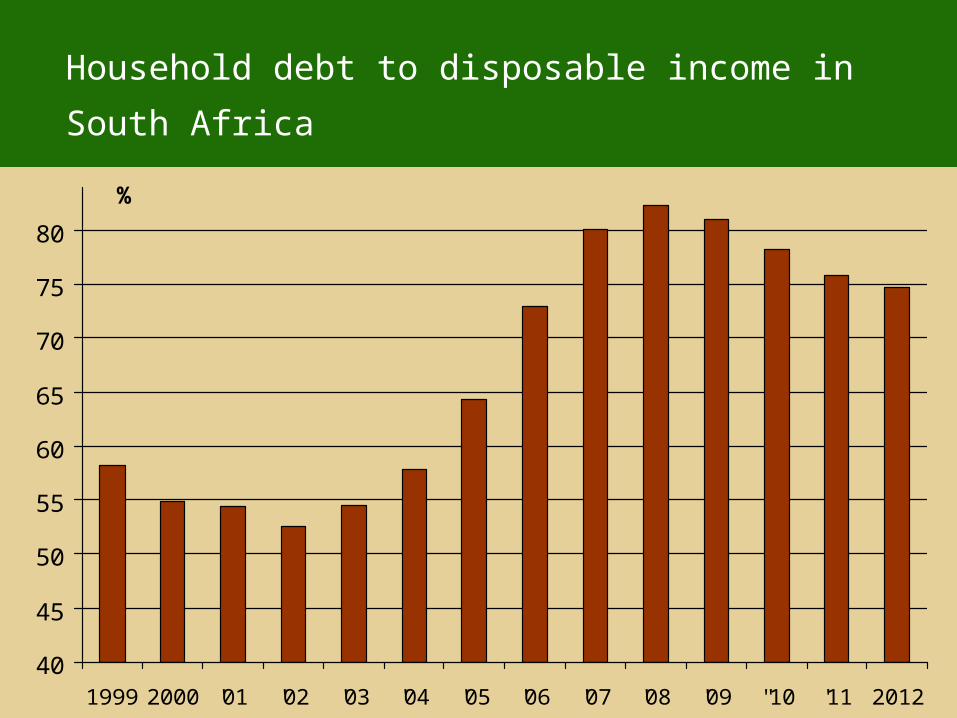

Household debt to disposable income in South Africa

40

45

50

55

60

65

70

75

80

1999 2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 ''10 '11 2012

%

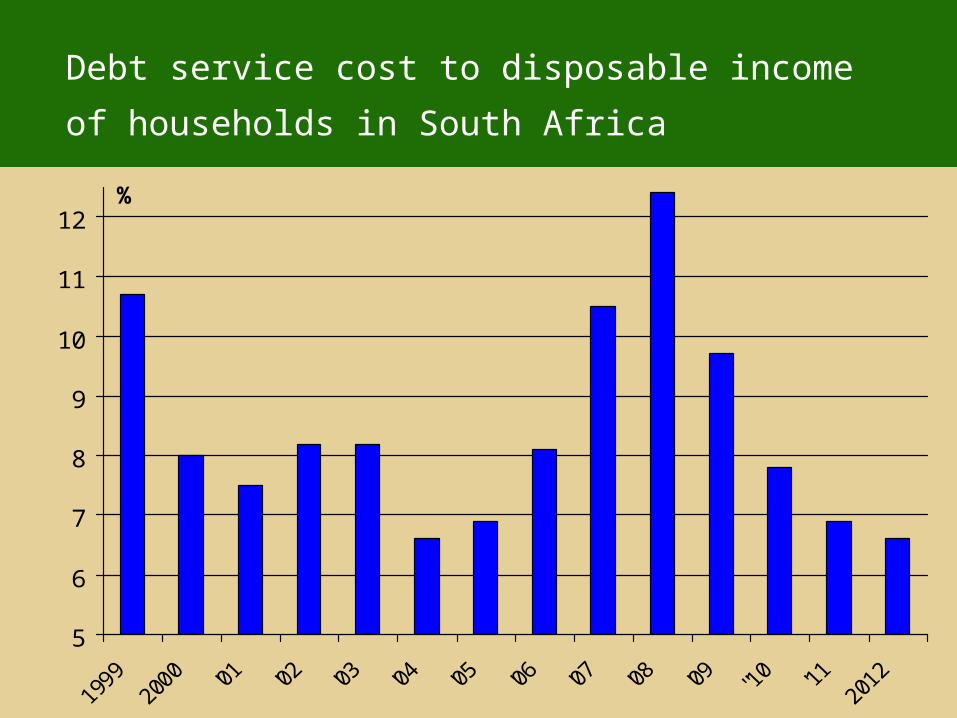

Debt service cost to disposable income of households

in South Africa

5

6

7

8

9

10

11

12%

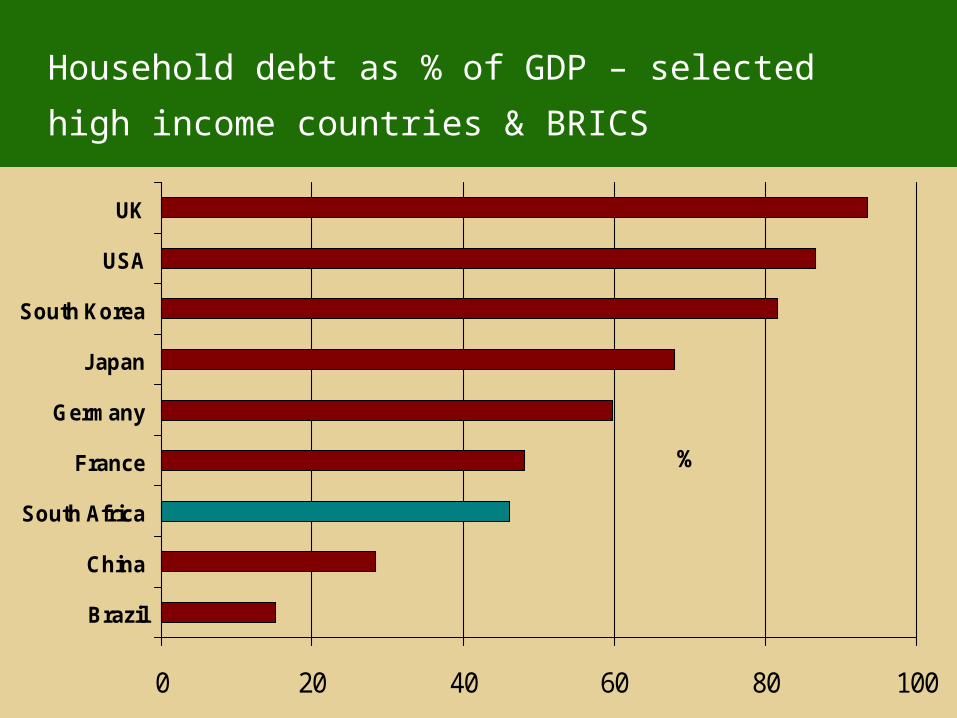

Household debt as % of GDP – selected high income

countries & BRICS

0 20 40 60 80 100

Brazil

China

South Africa

France

Germany

Japan

South Korea

USA

UK

%

Real growth trends for the components of domestic

expenditure (Sources: SARB, own calculations)

90

110

130

150

170

190

210

2000 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 2012

Index; 2000 = 100

Capital formation

Household consumption

Govt. consumption

Convergence of consumer & producer inflation to

within the Reserve Bank’s target range of 3% to 6%

1.5

3

4.5

6

7.5

9

10.5%

PPI

CPI

Lowest prime rate in 40 years enhances household

spending power

7

10

13

16

19

22

%

Formal sector employment – progress after recession,

but now stuttering

9 000

9 100

9 200

9 300

9 400

9 500

9 600‘000

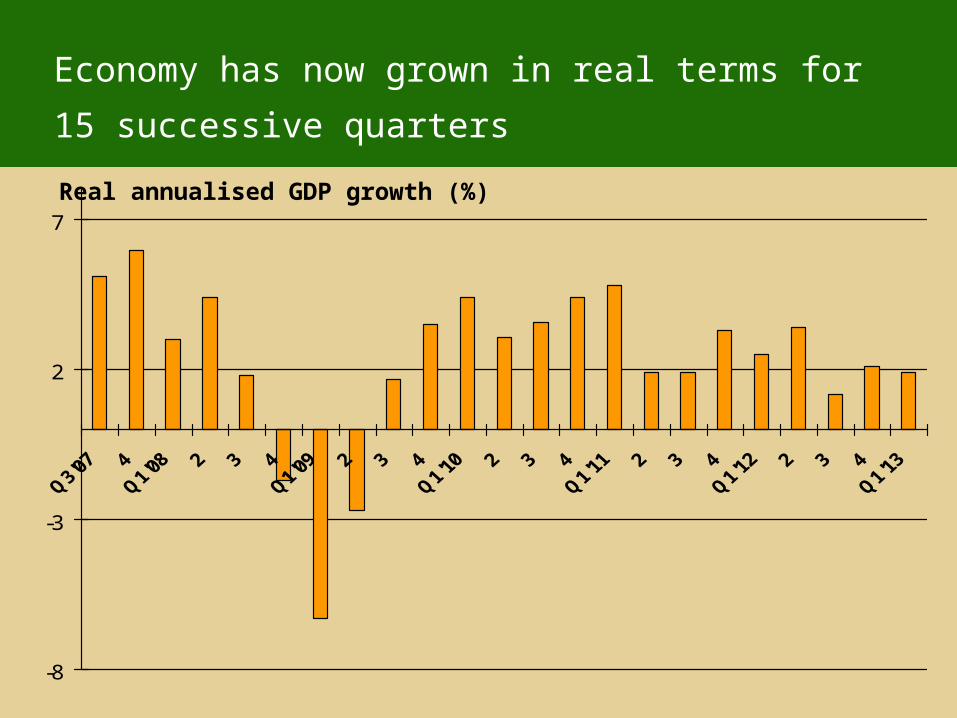

Economy has now grown in real terms for

15 successive quarters

-8

-3

2

7Real annualised GDP growth (%)

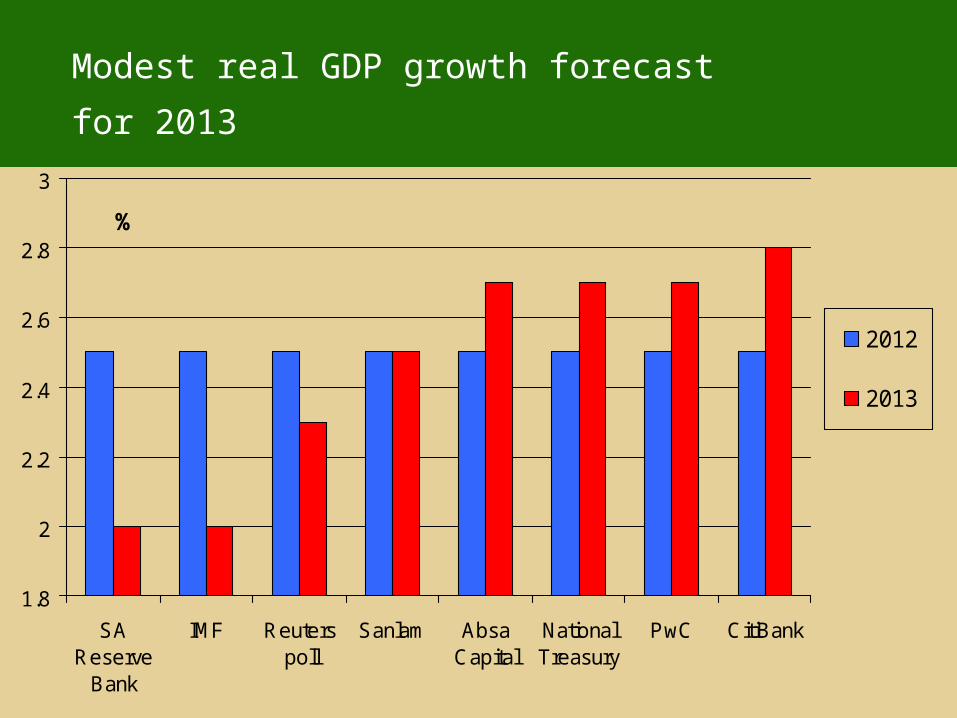

Modest real GDP growth forecast for 2013

1.8

2

2.2

2.4

2.6

2.8

3

SAReserve

Bank

IMF Reuterspoll

Sanlam AbsaCapital

NationalTreasury

PwC CitiBank

2012

2013

%

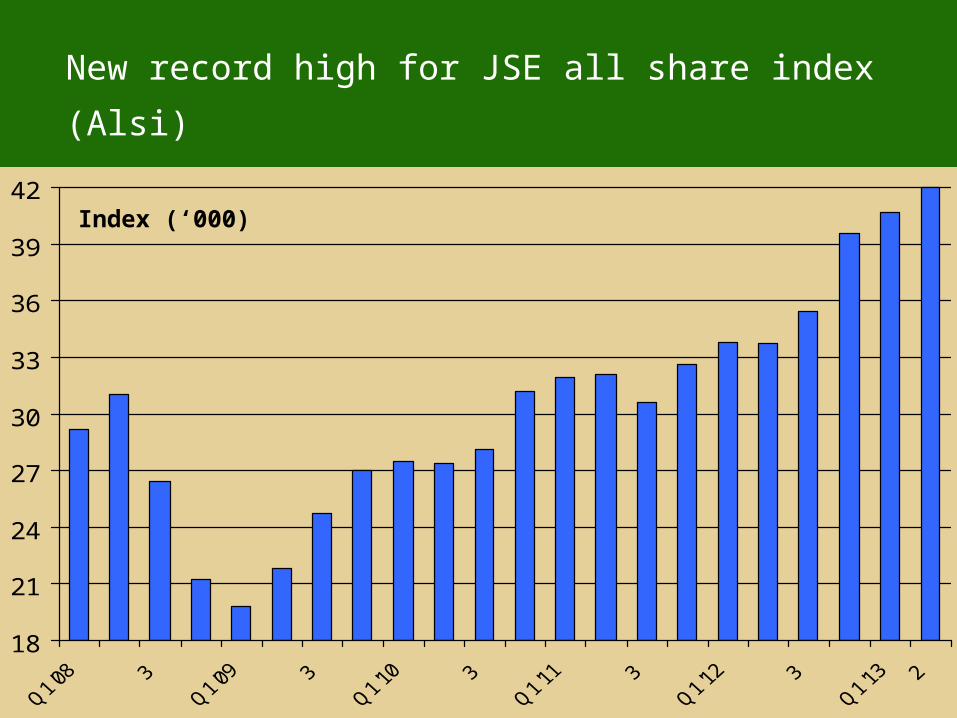

New record high for JSE all share index (Alsi)

18

21

24

27

30

33

36

39

42Index (‘000)

New record high for real disposable income per

capita of households (at constant 2011 prices)

22

24

26

28

30

32

34

36

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

R ‘000