Transitional Issues & GST Readiness - CTFA Malaysia · Transitional Issues & GST Readiness GST...

42

Transitional Issues & GST Readiness GST SEMINAR Date: 19 June 2014 Venue: Hotel Holiday Inn Glenmarie, Shah Alam, Selangor

Transcript of Transitional Issues & GST Readiness - CTFA Malaysia · Transitional Issues & GST Readiness GST...

Transitional Issues

& GST Readiness

GST SEMINAR

Date: 19 June 2014

Venue: Hotel Holiday Inn Glenmarie,

Shah Alam, Selangor

22

Agenda

Supply Spanning GST

1

2

Acts Repealed

3

Non-Reviewable Contract4

Special Refund5

Business Preparation6

Registration

1

3

From the appointed date (AD – implementation of GST)

Still enforced on matters where tax is due and payable and liability

(offences) incurred:

Repeal of Sales Tax and Service Tax

Collection

Recovery

Drawback

Remission

Refund

Penalty

4

5

Final return for Sales tax

• Final return must be submitted not later than 28 days from the date

the GST Act comes into force (GST implementation date)

• All tax liabilities must be accounted in the final return

Final return for Services tax

• Return can be submitted in accordance with the Service Tax Act

(payment basis). The licensee may have to submit two returns:

GST return

Special form for service tax until the expiry of 12 months from the GST

implementation date

Repeal of Sales Tax and Service Tax

6

When to submit final or last return under Sales Tax / Services Tax?

Return For Last Taxable Period

Feb Mac April

Last date of submission : 28 April

Appointed Date

1 April 2015

Mac April

Last date of submission : 28 April

Appointed Date

1 April 2015

Taxable Period : Feb / Mac

Taxable Period : Mac / April

2

7

8

What is supply spanning GST?

Payment or invoice before appointed date and supply takes place on

and after appointed date or vice versa e.g. sales of goods, airline

tickets and cinema

General Rule

Any supply before appointed date is not subject to GST

Any supply on or after appointed date is subject to GST

Exception to general rule

Supply of warranty

Provision of goods where sales tax has been charged

Provision of services where service tax has been charged

Non-reviewable contracts

Supplies Spanning GST

9

Supplies Spanning GST

AD – 1st. April, 2015

(Appointed Date)

General Rule:

No tax (GST) on:-

a. Supply of goods,

b. Supply of services

c. Importation of goods

10

Supplies Spanning GST

AD – 1st. April, 2015

(Appointed Date)

1st. scenario:

Deemed:-

Invoice issued or payment

received on AD

Invoice issued

Payment received

Goods supplied

Services performed

Value of supply

[GST inclusive]

11

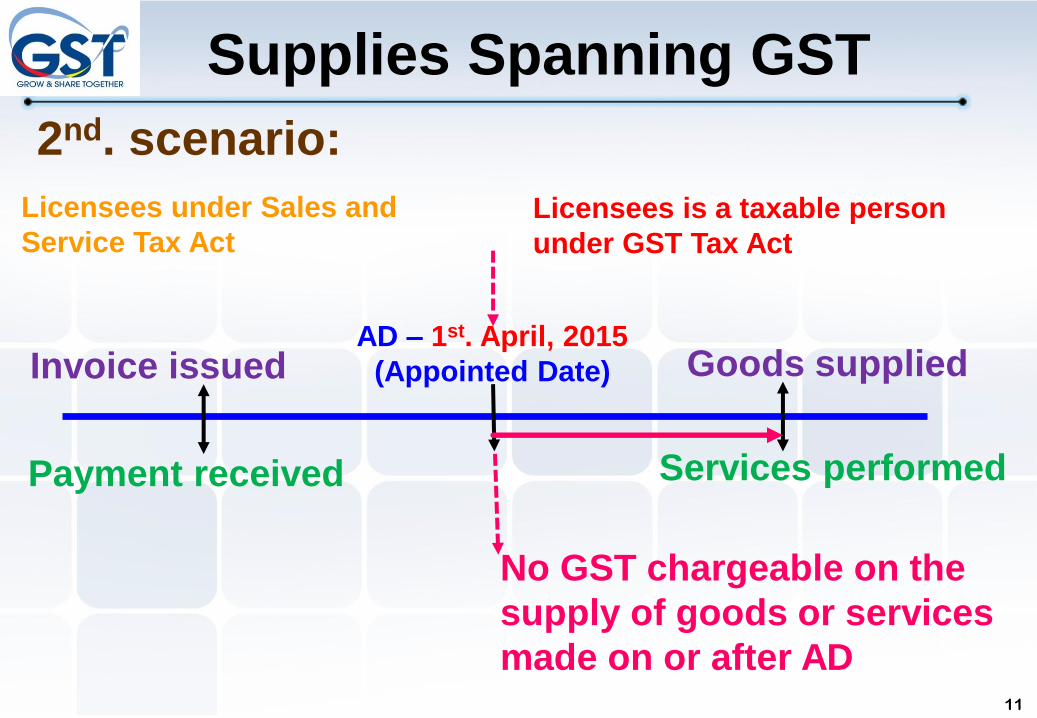

Supplies Spanning GST

2nd. scenario:

No GST chargeable on the

supply of goods or services

made on or after AD

Licensees under Sales and

Service Tax Act

AD – 1st. April, 2015

(Appointed Date)Invoice issued

Payment received

Goods supplied

Services performed

Licensees is a taxable person

under GST Tax Act

3

12

13

Registration

Registration effective on or

from the appointed date

AD – 1st. April, 2015

(Appointed Date)

3 months before

Registration

application

Registration during the transitional period:-

4

14

15

Non-reviewable contract

Written contract with no provision to review consideration

for the supply until a review opportunity arises

AND

24 months before the date of GST implementation (AD)

Non-Reviewable Contract

16

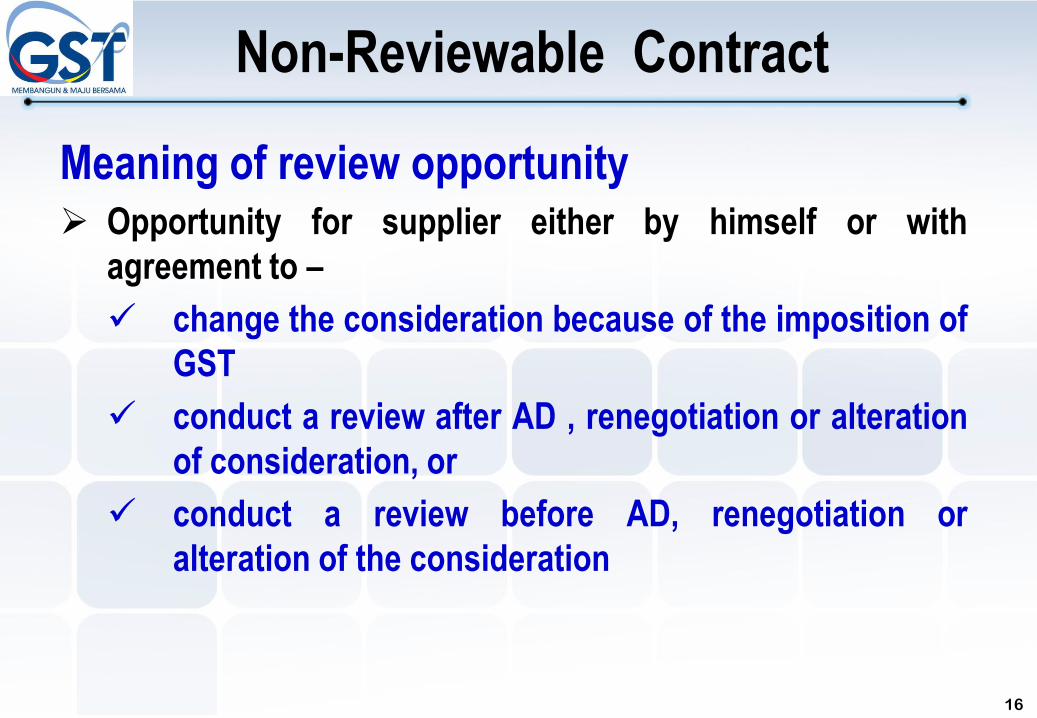

Meaning of review opportunity Opportunity for supplier either by himself or with

agreement to –

change the consideration because of the imposition of

GST

conduct a review after AD , renegotiation or alteration

of consideration, or

conduct a review before AD, renegotiation or

alteration of the consideration

Non-Reviewable Contract

17

Zero rate supply for 5 years (charge GST at 0%) after

appointed date or when a review opportunity arises

whichever is the earlier if:

Both supplier and recipient are registered persons;

Supply is a taxable supply; and

The recipient of the supply is entitled to claim input tax

on that supply

After 5 years period, revert to either standard rate or zero

rate

Non-Reviewable Contract

18

AD – 1 st. April, 2015

(Appointed Date) 5 years after AD

Review

Opportunity

Non-Reviewable Contract

Review

Opportunity

Zero rate supply for 5 years after appointed date or

when a review opportunity arises whichever is the

earlier

5

19

20

Special Refund-Retailing

21

Special Refund-Manufacturing

22

Entitled for special refund of Sales tax if

claimant is registered (mandatory) person

hold goods on appointed date for making taxable supply

goods are subject to sales tax and sales tax has been paid

holds relevant invoices or import document to show sales

tax has been paid

Special Refund

23

Goods not eligible for special refund

capital goods e.g. building and land

goods used partially or incorporated into other goods e.g. raw

materials, work in progress

goods for hire e.g. cars, generators

goods not for business e.g. personal use

goods not for sale or exchange e.g. containers, pellets, stationeries,

moulds, manufacturing aids

goods entitled to drawback

goods allowed sales tax deduction under Section 31A STA 1972

(credit system)

Special Refund

24

Manner to claim special refund

claim within 6 months from appointed date

for special refund < RM10,000 require audit certificate signed by a

chartered accountant

for special refund ≥ RM10,000 require audit certificate signed by

an approved company auditor

use special form to claim refund (online only)

to be given in eight (8) equal installments over a period of two (2)

years

to account as output tax if special refund is claimed and goods are

returned

Special Refund

26

Reduce special refund to 20%

(20% method)

purchase goods from non licensed manufacturers

goods are subject to sales tax

holds invoices which does not show sales tax has been

charged

claimant is a registered (mandatory) person

hold goods on appointed date for making taxable goods

Special Refund

27

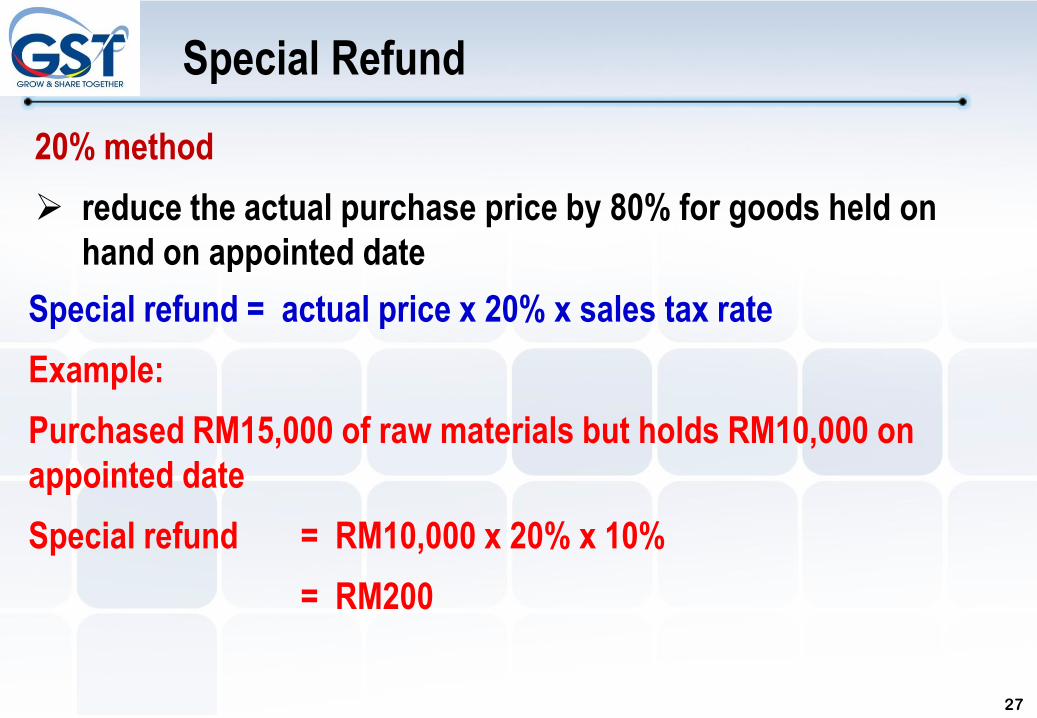

20% method

reduce the actual purchase price by 80% for goods held on

hand on appointed date

Special refund = actual price x 20% x sales tax rate

Example:

Purchased RM15,000 of raw materials but holds RM10,000 on

appointed date

Special refund = RM10,000 x 20% x 10%

= RM200

Special Refund

6

28

29

BUSINESS PREPARATION FOR GST

GST

Readiness

Human

Resource

Sales &

Marketing

System

& Processes

Accounting

& Finance

Purchasing

& supply chain

Government

30

ESTABLISHING GST COMMITTEE

To implement a GST compliant system

GST

Project

Team

Initiate

impact

study

Pre GST and

dry run

1st phase 2nd phase 3rd phase

Make changes to

system processes

and staff training

Key areas requiring attention

Tax

regulatory

compliance

Documentation

and system

Legal and

transitional

issues

Education

and training

Vendor and

supplier

communication

Apr 2014 -- June 2014

(3 months)

July 2014 -- Jan 2015

(7 months)

Feb 2015 -- Mar 2015

(2 months)

31

GST Implication on System

review system and processes

perform complete mapping of transactions to

identify required changes

GST liability on every transaction and deadlines

use of online submissions to tax agency

computerised system

ready made software

upgrading present system

BUSINESS PREPARATION FOR GST

32

GST Implication on the Repeal of Sales Tax and Service

Tax

Chargeability

Facilities under the taxes repealed

Taxable goods and services

Non taxable goods and services

Invoices issued and payment received before implementation date

Invoices issued or payment received after implementation date

Obligation to submit return and pay tax

Invoice issued deemed inclusive of GST

BUSINESS PREPARATION FOR GST

33

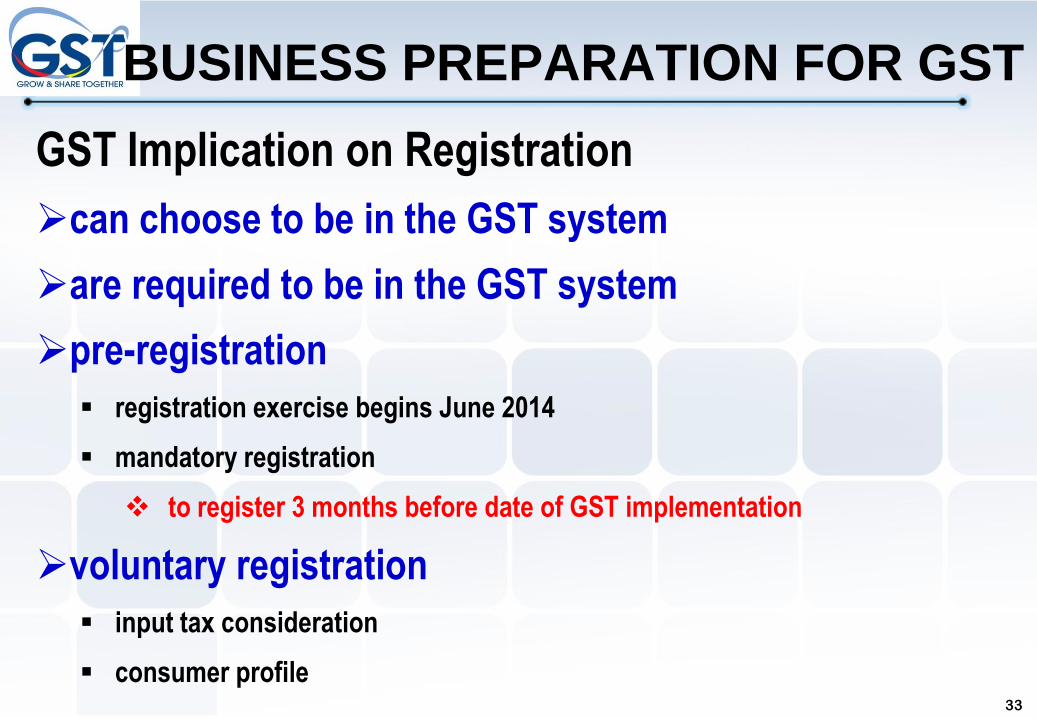

GST Implication on Registration

can choose to be in the GST system

are required to be in the GST system

pre-registration

registration exercise begins June 2014

mandatory registration

to register 3 months before date of GST implementation

voluntary registration

input tax consideration

consumer profile

BUSINESS PREPARATION FOR GST

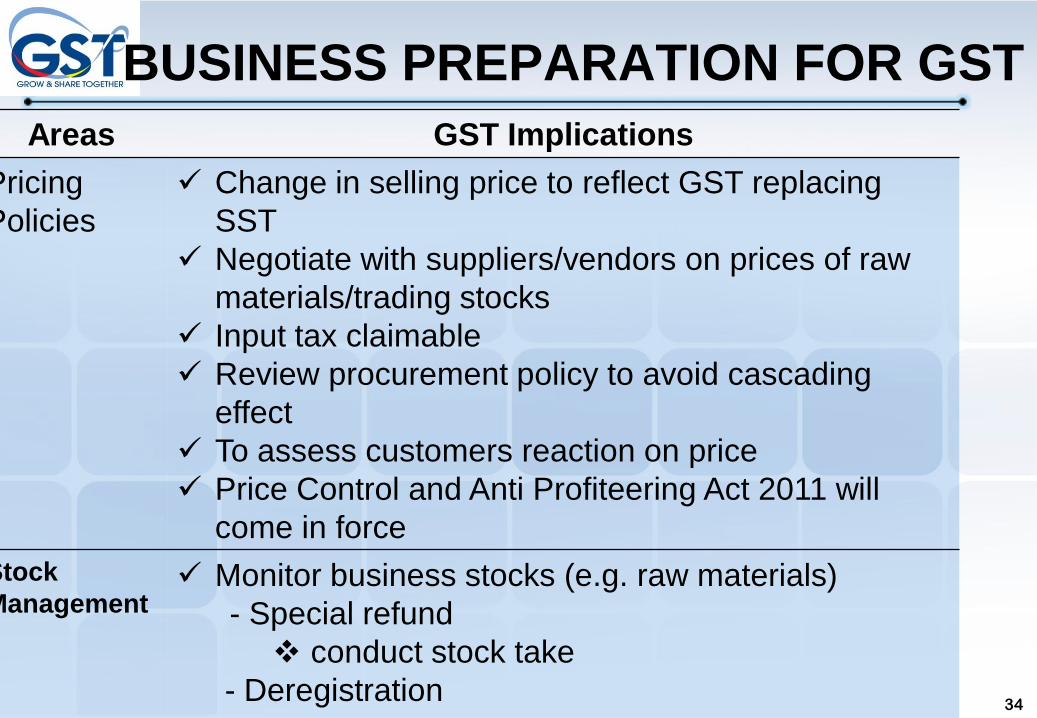

Areas GST Implications

Pricing

Policies

Change in selling price to reflect GST replacing

SST

Negotiate with suppliers/vendors on prices of raw

materials/trading stocks

Input tax claimable

Review procurement policy to avoid cascading

effect

To assess customers reaction on price

Price Control and Anti Profiteering Act 2011 will

come in force

Stock

Management Monitor business stocks (e.g. raw materials)

- Special refund

conduct stock take

- Deregistration

BUSINESS PREPARATION FOR GST

34

Areas GST Implications

Cash Flow Need to analyze cash flow impact

to assess the need to create a one time

fund to cater for GST payment up-front

cash maybe recovered from customer

before GST is due

Credit Terms Need to review credit terms and issuance of

invoice

timing differences may impact cash flow of

business

may result making payments of GST before

collection from customers

BUSINESS PREPARATION FOR GST

35

Areas GST Implications

Bad debts Ensure a proper matching of payment of tax to

government and payment received from

customers

Ensure GST compliance by reviewing the

accounting / recording system

Bad debt claims evidence of ‘reasonable efforts’

to recover the debt

Advertising Requirement to show price as GST inclusive

BUSINESS PREPARATION FOR GST

36

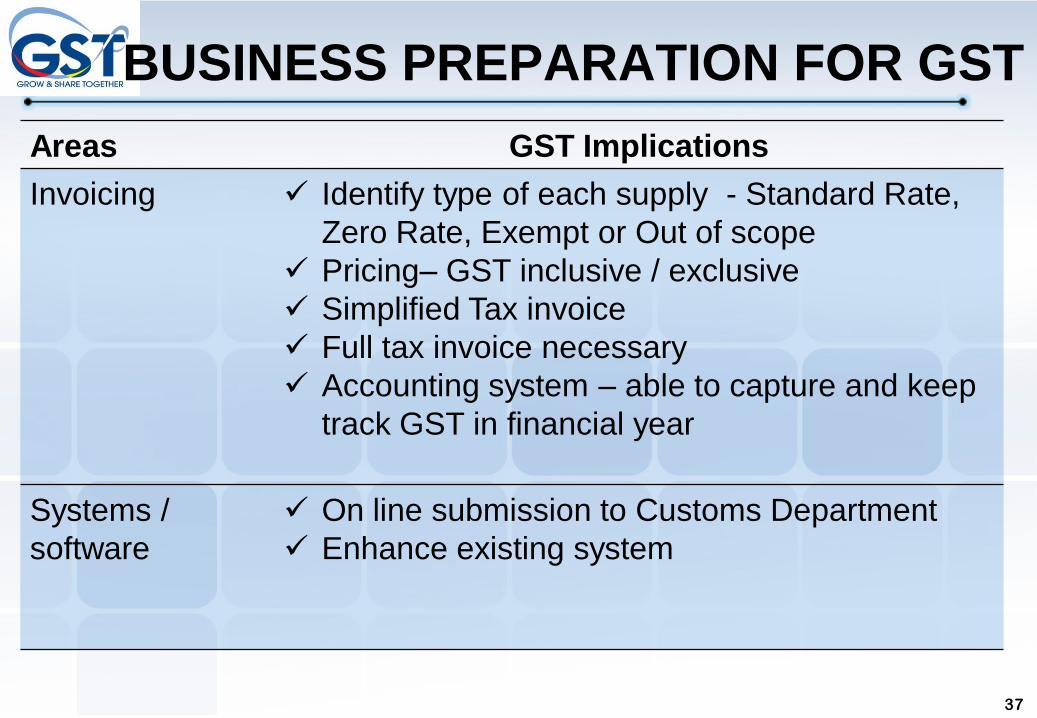

Areas GST Implications

Invoicing Identify type of each supply - Standard Rate,

Zero Rate, Exempt or Out of scope

Pricing– GST inclusive / exclusive

Simplified Tax invoice

Full tax invoice necessary

Accounting system – able to capture and keep

track GST in financial year

Systems /

software

On line submission to Customs Department

Enhance existing system

BUSINESS PREPARATION FOR GST

37

Areas GST Implications

Staff Training To upgrade understanding of GST

To avoid unnecessary mistake

False/wrong information declared may

open for audit case

Monitor business stocks (e.g. raw

materials)

- Special refund

- conduct stock take

Computerised accounting system

Contract Legal advice with regards to contract

Avoid long term contract without legal

review

BUSINESS PREPARATION FOR GST

38

39

There are no major compliance problems. Taxpayers have generally

been compliant and most of the errors uncovered stem from a lack of

awareness of GST obligations or an inadequate understanding of GST

rules.

Wish List:

1. Both business community and Government are well -prepared to

implement GST

2. Implementation problems are minimized

3. Minimum impact on prices of goods and services

4. Public accept GST implementation

General Comment from countries implemented GST /

VAT on compliance:

BUSINESS PREPARATION FOR GST

40

http://www.gst.customs.gov.my

3

Ketua Setiausaha,

Perbendaharaan Malaysia

Pejabat Pelaksanaan GST

Komplek Kementerian Kewangan,

No.5, Persiaran Perdana,

Pusat Pentadbiran Kerajaan Persekutuan Malaysia,

62596 PUTRAJAYA.

Tel : 03-88823000

GST PORTAL

www.gst.customs.gov.my

1

Customs Call Centre (CCC)Tel: 03- 78067200

Fax: 03- 78067599

Email: [email protected]

2

41

INQUIRY

42

Royal Malaysian CustomsMinistry of Finance

Malaysia

Thank you

![GST: Transitional Provisions - Neeraj Bhagat Transitional provisions-Edition 3.pdf · 2 • POT Transition Phase [S.188 and S. 189] • Credit with ISD [S.190 and S. 191] • Goods](https://static.fdocuments.in/doc/165x107/5a78afe77f8b9a273b8d3b61/gst-transitional-provisions-neeraj-bhagat-transitional-provisions-edition-3pdf2.jpg)