Training Seminar on an Information Point for FP7 in Palestine Witkowski Jacob, BA,CPA, CIA...

34

Training Seminar on Training Seminar on an Information Point an Information Point for FP7 in Palestine for FP7 in Palestine Witkowski Jacob, BA,CPA, CIA Witkowski Jacob, BA,CPA, CIA [email protected] Nicosia, Cyprus 23-28 November 2008 Nicosia, Cyprus 23-28 November 2008

-

Upload

james-nicholson -

Category

Documents

-

view

220 -

download

2

Transcript of Training Seminar on an Information Point for FP7 in Palestine Witkowski Jacob, BA,CPA, CIA...

Training Seminar onTraining Seminar onan Information Point for an Information Point for FP7 in PalestineFP7 in Palestine

Witkowski Jacob, BA,CPA, CIAWitkowski Jacob, BA,CPA, [email protected]

Nicosia, Cyprus 23-28 November 2008Nicosia, Cyprus 23-28 November 2008

Audit JustificationAudit Justification

The Commission may at any time during The Commission may at any time during the grant period, and up to 5 years after the grant period, and up to 5 years after the end of the project, arrange for audit to the end of the project, arrange for audit to be carried outbe carried out

(Article II 22 of the Fp7 Model Grant (Article II 22 of the Fp7 Model Grant Agreement)Agreement)

Audit PurposeAudit Purpose

To substantiate the financial reports (Form C)To substantiate the financial reports (Form C)

To verify that expenses are according to To verify that expenses are according to financial FP7 regulations (eligible expenses)financial FP7 regulations (eligible expenses)

To verify that the reports are based on To verify that the reports are based on appropriate recordsappropriate records

To insure that the internal control of the To insure that the internal control of the organization allows for sampling checkingorganization allows for sampling checking

To make sure that expenses have got a right To make sure that expenses have got a right audit trailaudit trail

By WhomBy Whom??

DG in chargeDG in charge

Court of auditorsCourt of auditors

External ProfessionalsExternal Professionals

In house employeesIn house employees

WHO IS BEING AUDITEDWHO IS BEING AUDITED??

CoordinatorCoordinator

PartnerPartner

Sub Contractor ?Sub Contractor ?

Third Party?Third Party?

Is there a difference in the scope of audit?Is there a difference in the scope of audit?

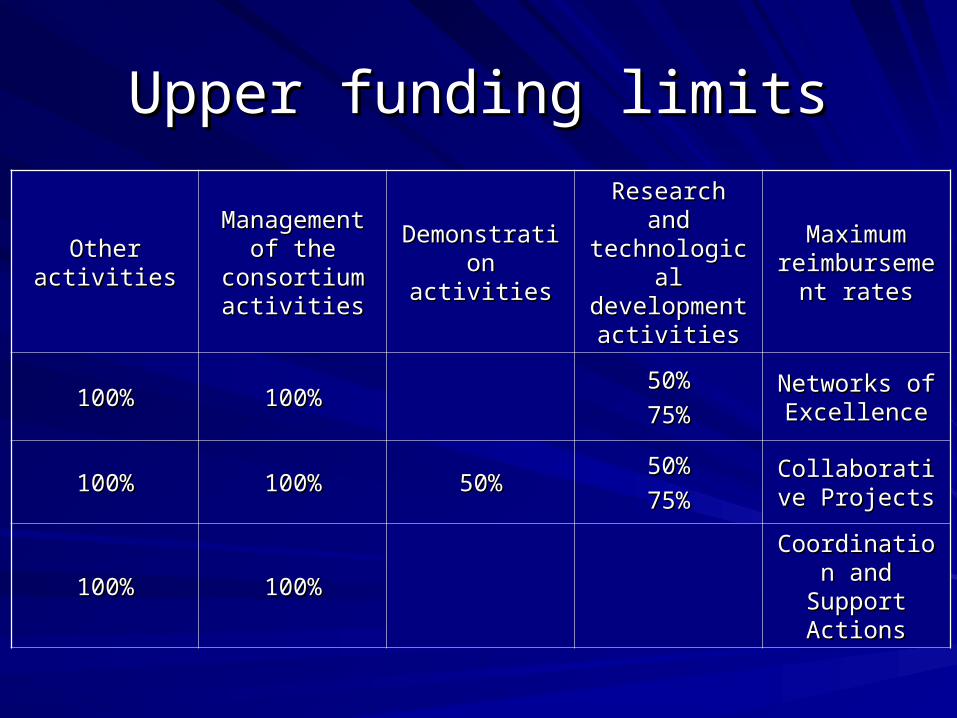

Upper funding limitsUpper funding limits

Maximum Maximum reimbursement reimbursement

ratesrates

Research and Research and technological technological development development

activitiesactivities

Demonstration Demonstration activitiesactivities

Management of Management of the consortium the consortium

activitiesactivitiesOther activitiesOther activities

Networks of Networks of ExcellenceExcellence

50%50%

75%75%100%100%100%100%

Collaborative Collaborative ProjectsProjects

50%50%

75%75%50%50%100%100%100%100%

Coordination Coordination and Support and Support

ActionsActions100%100%100%100%

Forum CForum C

Typical Direct CostsTypical Direct Costs

Personnel Costs/Staff SalariesPersonnel Costs/Staff Salaries Travel and subsistenceTravel and subsistence Durable Equipment (depreciation) Durable Equipment (depreciation) ConsumablesConsumables Subcontracting costsSubcontracting costs

Indirect Costs (Overheads)Indirect Costs (Overheads)

• Actual Indirect CostsActual Indirect Costs

• Flat Rate (20%-60%) Flat Rate (20%-60%)

RentRentElectricityElectricityMunicipal taxesMunicipal taxesMaintenanceMaintenanceOffice SupplyOffice SupplyBooks & NewspapersBooks & NewspapersDepreciation on office equipmentDepreciation on office equipmentLawyers and Bookkeeping& AuditingLawyers and Bookkeeping& Auditing

Typical Indirect CostsTypical Indirect Costs

1. Actual Indirect Costs1. Actual Indirect Costs

Real Indirect CostsReal Indirect Costs

Simplified method: Simplified method: – A participant may use a simplified method to A participant may use a simplified method to

calculate its indirect costs at the level of the calculate its indirect costs at the level of the legal entity:legal entity: If the organisation does not have an accounting If the organisation does not have an accounting

system with detailed cost allocationsystem with detailed cost allocation In accordance with its usual management and In accordance with its usual management and

accounting principles accounting principles Based on actual costs of the last closed Based on actual costs of the last closed

accounting yearaccounting year

2. Flat Rate2. Flat Rate Standard Flat Rate of 20%Standard Flat Rate of 20% Special transitional* flat rate of 60% only Special transitional* flat rate of 60% only

applicable for funding schemes with RTD applicable for funding schemes with RTD activities for:activities for:– Non-profit Public BodiesNon-profit Public Bodies– Secondary and Higher Education EstablishmentsSecondary and Higher Education Establishments– Research OrganisationsResearch Organisations– SMEsSMEs

* * Until end 2010Until end 2010

Excluding SubcontractingExcluding Subcontracting

Excluding third partyExcluding third party

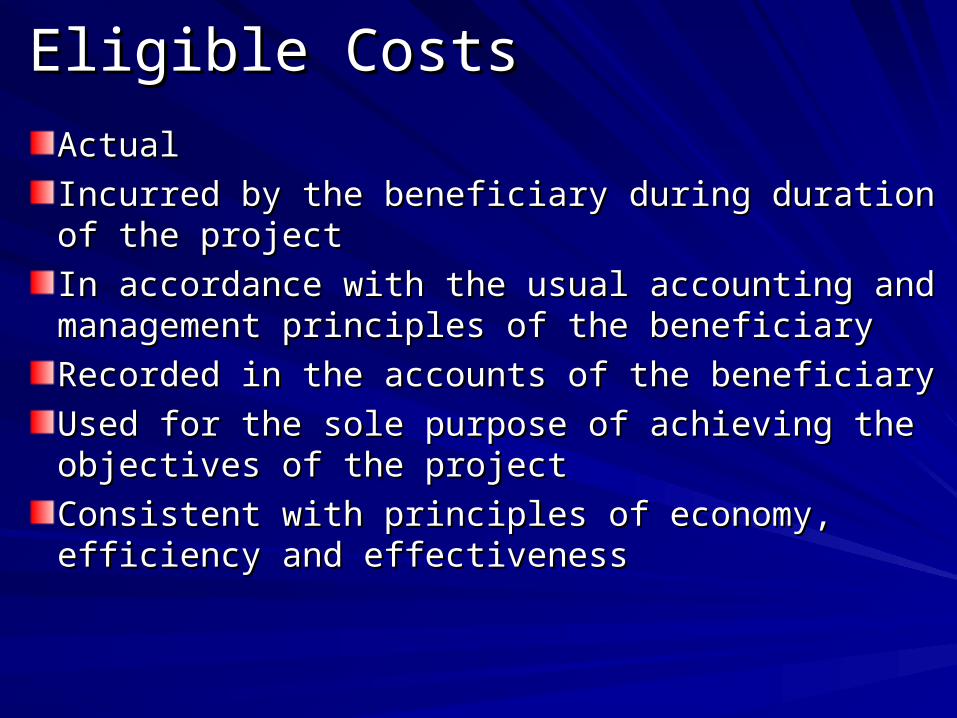

Eligible CostsEligible Costs

ActualActual

Incurred by the beneficiary during duration of the Incurred by the beneficiary during duration of the projectproject

In accordance with the usual accounting and In accordance with the usual accounting and management principles of the beneficiarymanagement principles of the beneficiary

Recorded in the accounts of the beneficiaryRecorded in the accounts of the beneficiary

Used for the sole purpose of achieving the Used for the sole purpose of achieving the objectives of the projectobjectives of the project

Consistent with principles of economy, efficiency Consistent with principles of economy, efficiency and effectivenessand effectiveness

Non-Eligible CostsNon-Eligible Costs

Identifiable indirect taxes including VATIdentifiable indirect taxes including VAT

Bank-interest, exchange rate differencesBank-interest, exchange rate differences

Costs in other EU-projectsCosts in other EU-projects

Overpriced or economically unjustified costsOverpriced or economically unjustified costs

Not documented costsNot documented costs

ReservesReserves

Examples of Non-eligible CostsExamples of Non-eligible Costs

Costs not incurred during the official life Costs not incurred during the official life time of the project and paid up to 60 days time of the project and paid up to 60 days from project end or the date of submission from project end or the date of submission of final report –the earliest of themof final report –the earliest of them

TariffsTariffs

Alternative expensesAlternative expenses

AssessmentsAssessments

DividendsDividendsYield-ProfitYield-ProfitAllowance for lossAllowance for lossBank ChargesBank ChargesDoubtful and bad debtsDoubtful and bad debtsInterest in leasing chargesInterest in leasing chargesVatVatFederal Taxes ( not city & municipality)Federal Taxes ( not city & municipality)

Examples of Non-eligible CostsExamples of Non-eligible Costs

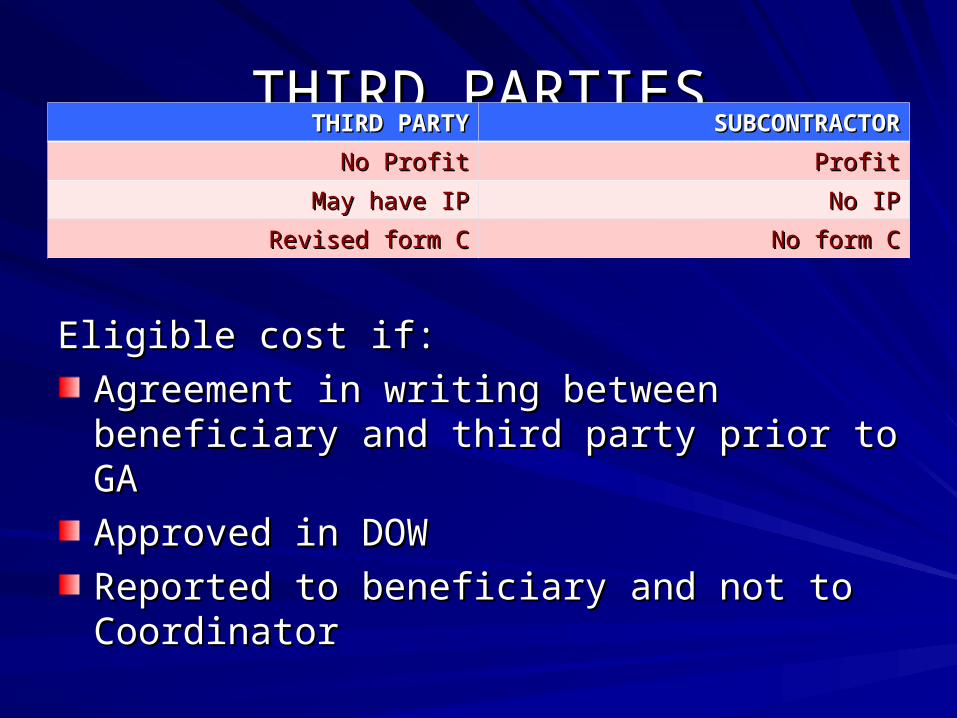

THIRD PARTIESTHIRD PARTIESSUBCONTRACTORSUBCONTRACTORTHIRD PARTYTHIRD PARTY

ProfitProfitNo ProfitNo Profit

No IPNo IPMay have IPMay have IP

No form CNo form CRevised form CRevised form C

Eligible cost if:Eligible cost if:

Agreement in writing between beneficiary and Agreement in writing between beneficiary and third party prior to GAthird party prior to GA

Approved in DOWApproved in DOW

Reported to beneficiary and not to CoordinatorReported to beneficiary and not to Coordinator

Professors ExceptionProfessors Exception

Professors being paid directly from Professors being paid directly from Government and not from the University Government and not from the University are eligible costs because the professor is are eligible costs because the professor is made available to the department and not made available to the department and not to a specific Project. In this case the to a specific Project. In this case the Government would be a Third PartyGovernment would be a Third Party

FINANCIAL REPORTFINANCIAL REPORT

All expenses in the financial report must All expenses in the financial report must be reported according to the budget line in be reported according to the budget line in form Cform C

Example: travel expenses which are direct Example: travel expenses which are direct expenses can not be reported as part of expenses can not be reported as part of managementmanagement

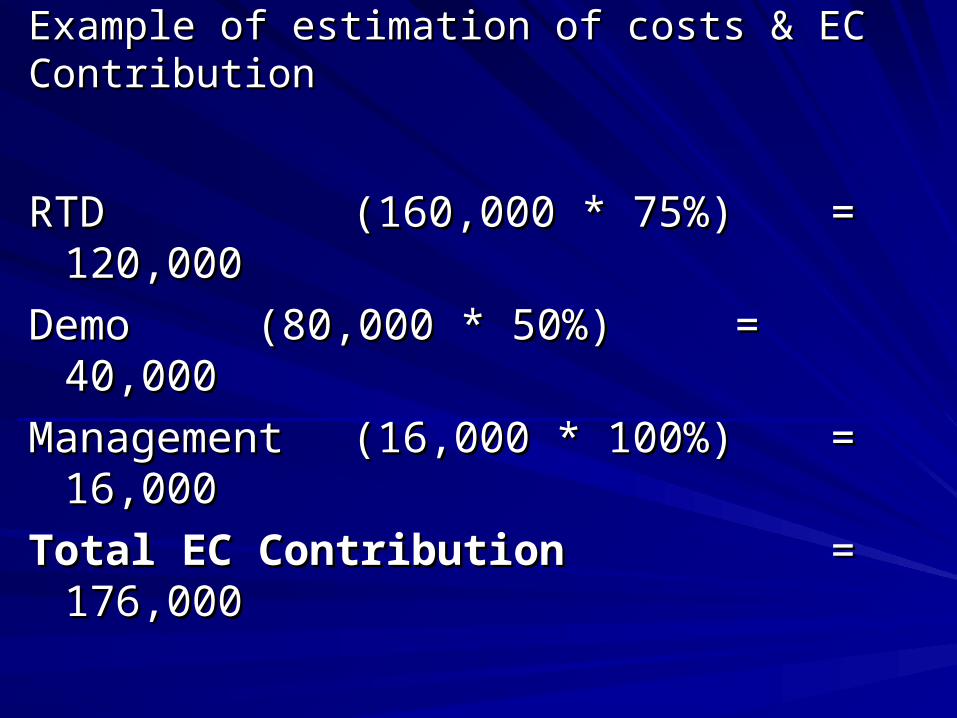

Example of estimation of costs & EC Example of estimation of costs & EC ContributionContribution

UniversityUniversity participating in a participating in a Collaborative ProjectCollaborative Project using the using the 60%60% flat rate for indirect costsflat rate for indirect costs

Direct CostsDirect Costs

RTD activitiesRTD activities 100,000100,000

Demo activitiesDemo activities 50,000 50,000

Other activitiesOther activities 10,000 10,000

TotalTotal 160,000160,000

Example of estimation of costs & EC Example of estimation of costs & EC ContributionContribution

+ Indirect Costs (60%)+ Indirect Costs (60%)

RTD activitiesRTD activities (100,000+60,000)(100,000+60,000)160,000160,000

Demo activities (50,000+30,000)Demo activities (50,000+30,000) 80,00080,000

Other activities (10,000+6,000)Other activities (10,000+6,000) 16,000 16,000

TotalTotal 256,000256,000

Example of estimation of costs & EC Example of estimation of costs & EC ContributionContribution

RTDRTD (160,000 * 75%) (160,000 * 75%) = = 120,000120,000

Demo Demo (80,000 * 50%) (80,000 * 50%) = = 40,00040,000

Management Management (16,000 * 100%) (16,000 * 100%) = = 16,00016,000

Total EC Contribution Total EC Contribution = = 176,000176,000

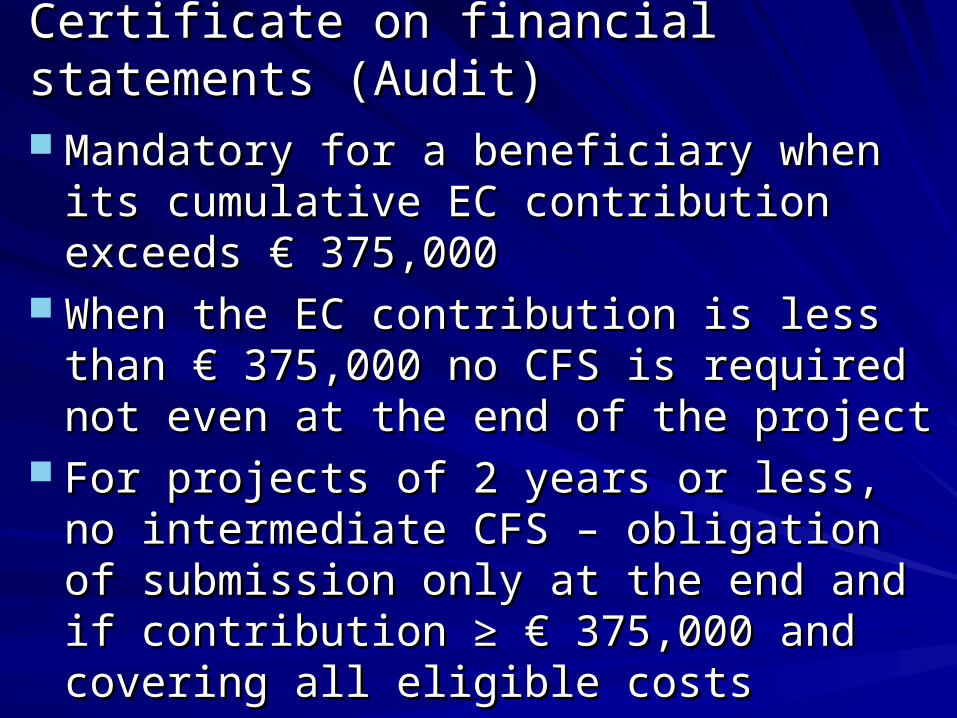

Certificate on financial statements Certificate on financial statements (Audit)(Audit) Mandatory for a beneficiary when its Mandatory for a beneficiary when its

cumulative EC contribution exceeds cumulative EC contribution exceeds €€ 375,000375,000

When the EC contribution is less than When the EC contribution is less than €€ 375,000 no CFS is required not even at 375,000 no CFS is required not even at the end of the projectthe end of the project

For projects of 2 years or less, no For projects of 2 years or less, no intermediate CFS intermediate CFS –– obligation of obligation of submission only at the end and if submission only at the end and if contribution ≥ contribution ≥ €€ 375,000 and covering 375,000 and covering all eligible costsall eligible costs

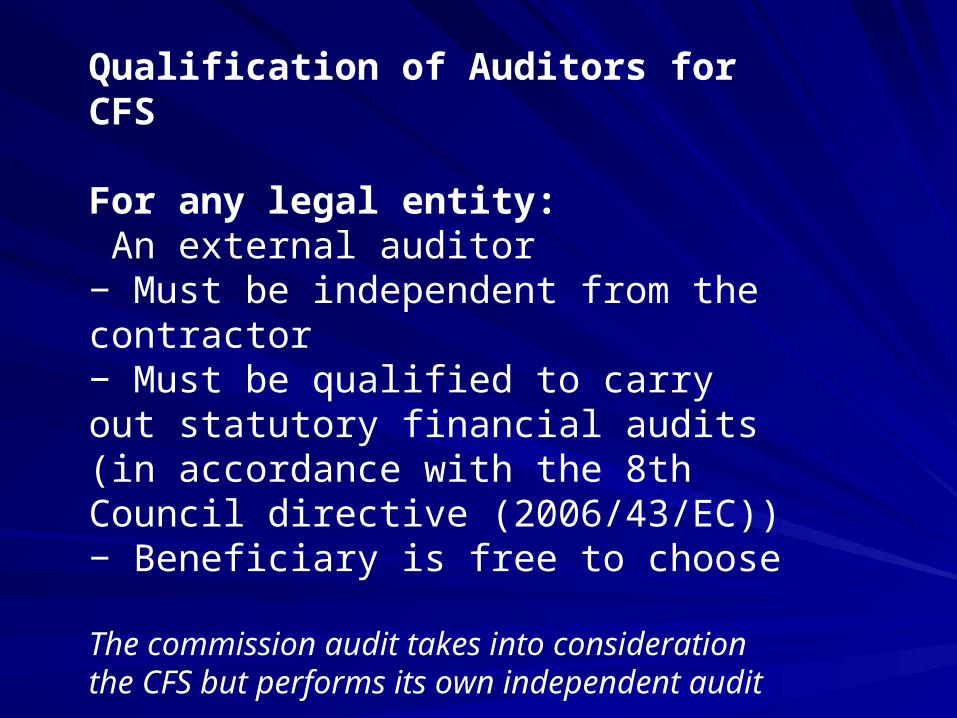

Qualification of Auditors for CFS

For any legal entity: An external auditor− Must be independent from the contractor− Must be qualified to carry out statutory financial audits (in accordance with the 8th Council directive (2006/43/EC))− Beneficiary is free to choose

The commission audit takes into consideration the CFS but performs its own independent audit

For public bodies/research organizations: An external auditor or a competent public officerPublic officer: − May not be involved in preparation of financial statements− Independence/legal capacity has to be assessed by responsible nationalauthorities

Necessity of Certification (1)

CERTIFICATE ON FINANCIAL STATEMENTS (CFS) to deliver to Commissionwithin 60 days after end of period CFS only mandatory, when requested funding for the period exceeds EUR 375.000 per beneficiaryIf Certification on Methodology – no intermediate CFSFor projects of 2 years or less, only CFS at the end – no intermediate CFSEC-Contribution ≤ EUR 375.000 – no Certificate (not even at the end)

Necessity of Certification (2)

Example: Year 1: EC Contribution EUR 200.000 – no CFS Year 2: EC Contribution EUR 180.000 – CFS has to be submitted(EUR 200.000 + EUR 180.000 > EUR 375.000) Year 3: EC Contribution EUR 250.000 – no CFS because < EUR 375.000Example certificate on methodology : Year 1: EC contribution EUR 200.000 - no CFS because < EUR 375.000 Year 2: EC contribution EUR 180.000 (EUR 200.000 + EUR 180.000> EUR 375.000) no intermediate CFS (because of certificate on methodology Year 3: EC contribution EUR 250.000 - CFS for all years

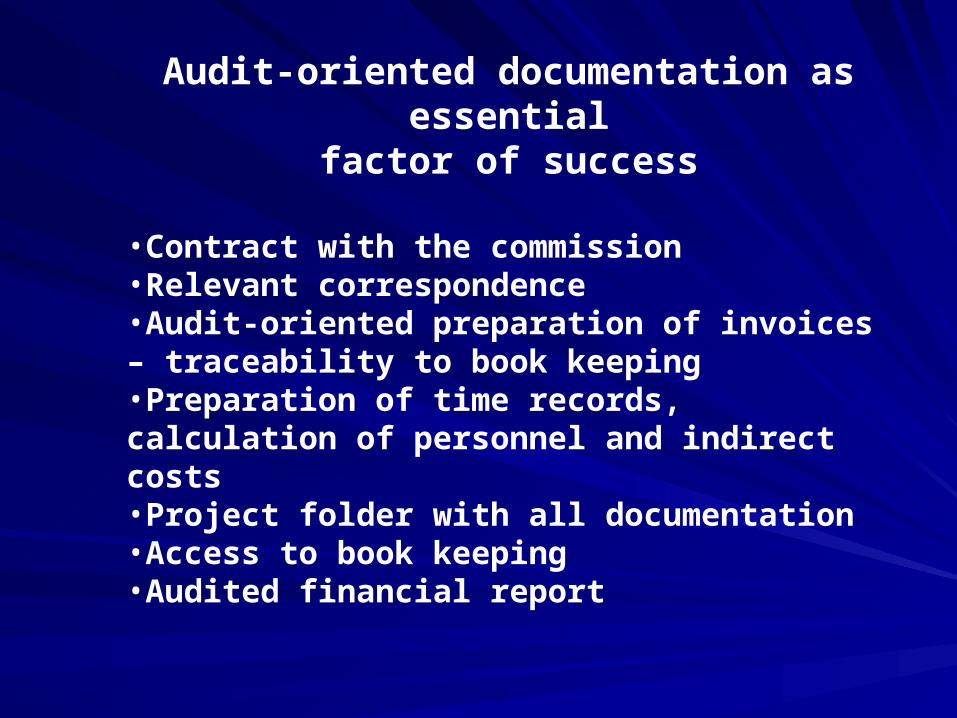

Audit-oriented documentation as essentialfactor of success

•Contract with the commission•Relevant correspondence•Audit-oriented preparation of invoices – traceability to book keeping•Preparation of time records, calculation of personnel and indirect costs•Project folder with all documentation•Access to book keeping•Audited financial report

Lets discussLets discuss!!

How long should I keep my accounting How long should I keep my accounting records after project end?records after project end?What kind of documents should I supply to What kind of documents should I supply to the auditor?the auditor?How long takes an audit?How long takes an audit?Would I be notified before an audit?Would I be notified before an audit?What is my chances of being audit?What is my chances of being audit?Is the audit performed on the partner or Is the audit performed on the partner or the coordinator or all participants?the coordinator or all participants?

Frequently asked QuestionsFrequently asked Questions

Should I contract sub-contractors or third Should I contract sub-contractors or third parties?parties?

What kind of system should I use in What kind of system should I use in indirect calculation : indirect calculation :

ActualActualSimplifiedSimplifiedStandardStandardTransition flat rate Transition flat rate

Frequently asked QuestionsFrequently asked Questions

How do I calculate the rate of exchange?How do I calculate the rate of exchange?DonationsDonationsIn-kindIn-kindApproval of timesheetsApproval of timesheetsDigital timesheets and digital signatureDigital timesheets and digital signatureOver time calculationOver time calculationEffective hours calculationEffective hours calculationIn house consultants (self employed)In house consultants (self employed)Transfer of money between partners Transfer of money between partners Pre-kick-off meeting Pre-kick-off meeting

Frequently asked QuestionsFrequently asked Questions

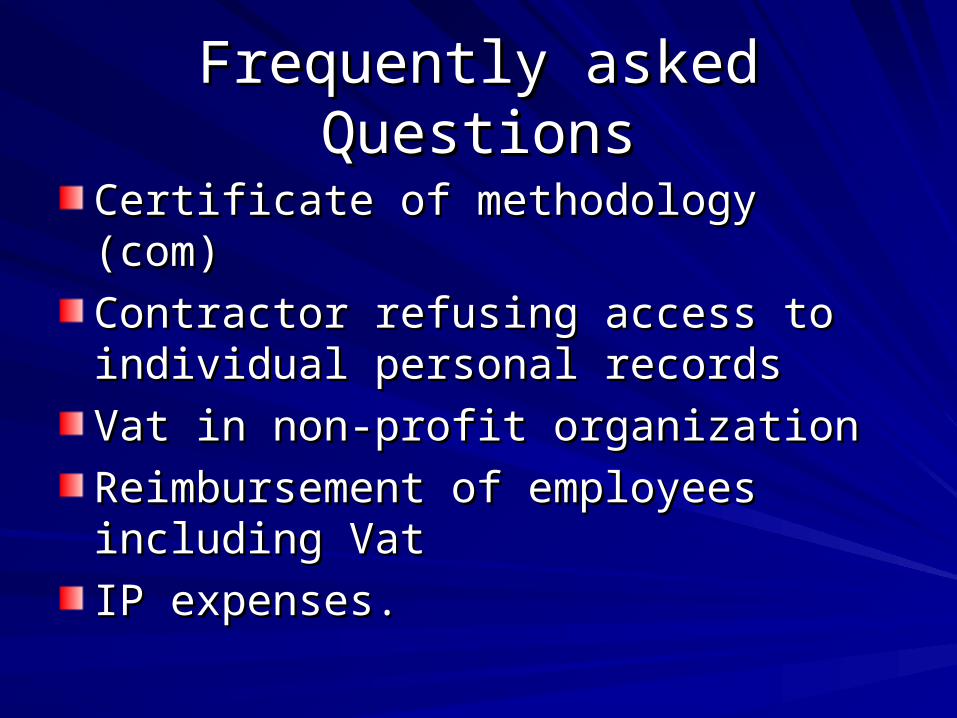

Certificate of methodology (com)Certificate of methodology (com)

Contractor refusing access to individual Contractor refusing access to individual personal recordspersonal records

Vat in non-profit organizationVat in non-profit organization

Reimbursement of employees including Reimbursement of employees including VatVat

IP expenses.IP expenses.

Frequently asked QuestionsFrequently asked Questions