Trading at SET - The Stock Exchange of Thailand

33

Dr. Pakorn Peetathawatchai Chief Strategy and Finance Officer The Stock Exchange of Thailand 2 March 2013 Thailand’s investment opportunities

Transcript of Trading at SET - The Stock Exchange of Thailand

Dr. Pakorn Peetathawatchai

Chief Strategy and Finance Officer

The Stock Exchange of Thailand

2 March 2013

Thailand’s investment opportunities

1

Thailand’s investment opportunities

• Thailand’s economic fundamental

• Robustness and profitability of Thai listed companies

• Resilience and performance of SET

• Trading at SET

2Source: Office of the National Economic and Social Development Board and Department of Tourism

(%YoY)2009 2010 2011 2012 2013

Q3 Q4Full year

Q3 Q4Full year

Projection

GDP Growth - 2.3 7.8 3.5 -9.0 0.1 3.1 18.9 6.4 4.5-5.5

- Private consumption -1.1 4.8 2.4 -3.0 1.3 6.0 12.2 6.6 3.5

- Private investment -13.1 13.8 9.1 -1.3 7.2 16.2 21.7 14.6 8.0

- Public consumption 7.5 6.0 1.1 1.5 1.4 9.8 12.1 7.4 3.5

- Public investment 2.7 -2.2 -10.9 -11.9 -8.7 13.2 31.1 8.9 12.0

- Export value of goods (USD)

-14.0 28.5 27.3 -5.2 16.4 -3.0 19.0 3.2 11.0

- Import value of goods (USD)

-25.2 36.8 33.4 12.2 24.7 -2.5 14.7 7.8 11.3

- Number of tourists (growth rate: Y-o-Y)

-3.0 11.7 29.9 -12.4 19.8 13.1 39.3 16.0 8.5

• GDP is expected to grow 4.5-5.5% in 2013, driven mainly by public and private investment, and

continued domestic demand stimulation policies.

Thailand’s economic fundamental

data as at December 2012

3

Thailand’s economic fundamental

Public debt to GDP and fiscal deficit to GDP

Source: Bank of Thailand; Ministry of Finance

0

10

20

30

40

50

-5

-4

-3

-2

-1

0

1

2005 2006 2007 2008 2009 2010 2011 2012e

Fiscal balance/ GDP (LHS) Public debt/ GDP (RHS)

%%

External debt and international reserves

Unit: billion USD

0

50

100

150

200

2005 2006 2007 2008 2009 2010 2011 2012

Short-term

Gross External Debt

International reserves

• Thailand’s fiscal position remains strong, with public debt at 43.3% of GDP

• With large international reserves, Thailand is well positioned to weather external financial shocks.

• Maintaining low and stable inflation rate, moderate monetary policy could be applied.

Inflation

-4

-2

0

2

4

6

8

10

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2007 2008 2009 2010 2011 2012

headline inflation core inflation

%

Policy interest rate

%

0

1

2

3

4

5

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2007 2008 2009 2010 2011 2012

43.3

-1.2

182

134

58

3.2

1.8 2.75

4Source: Bank of Thailand

• Loan growth has been accommodated by fundamental strength of Thai banks which have improved

markedly since the financial crisis of 1997.

Capital adequacy of Thai banks

%

Note: From August 2008 to November 2008, risk assets included risk-weighted assets for credit risk and market risk.From December 2008 onwards, risk assets included risk-weighted assets for credit risk, market risk and operational risk.

6

8

10

12

14

16

18

Tier 1 CAR

%

Non-performing loans

0

5

10

15

20

25

30

35

40

45

50

0

500

1,000

1,500

2,000

2,500

3,000

NPLs NPLs to Total lending ratio

Billion baht

Thailand’s economic fundamental

16.2

11.0

2.3

255

5

Gross Provincial Product of Greater Bangkok and Provinces

Thailand’s Gross Provincial Product growth (rebased 2001)

0

50

100

150

200

250

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Provinces

Greater Bangkok

221.2

170.2

Rebased, 2001=100

Thailand’s economic fundamental: economic drivers

• Thailand’s growth momentum has been supported by the growth of provincial economies.

Source: Office of the National Economic and Social Development Board; SET

Note: Greater Bangkok includes Bangkok, Pathumthani, Nonthaburi, Samutsakorn, Samutprakarn and Nakornpathom

46.0% 38.6%

54.0% 61.4%

0%20%40%60%80%

100%

Greater Bangkok Provinces

Major city

Secondary city

Tourism hub

Border trade city

Industrial estate

zone

6

• Thailand stands to benefit from the ASEAN Economic Community (AEC) that will become fully effective

in 2015. Thailand’s exports to ASEAN and CLMV* countries account for 24.7% and 7.4%, respectively.

• Thailand’s border exports with CLMM** countries account for 10% of total exports.

Thailand’s trade balance with other ASEAN countries Thailand’s exports by destination

Source: Bank of Thailand; SET

Note: *CLMV= Cambodia, Laos, Myanmar and Vietnam

**CLMM= Cambodia, Laos, Myanmar and Malaysia (border trade)

Thailand’s exports by destination to total exports

Thailand’s economic fundamental : economic drivers

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,0002009 2010 2011 2012

Million USD

0

10,000

20,000

30,000

40,000

50,000

60,000

ASEAN (9) CLMV CLMM China EU (27) Japan US

2009 2010 2011 2012

Million USD

24.7

7.510.0

11.79.5 10.2 9.9

0

5

10

15

20

25

30

ASEAN (9) CLMV CLMM China EU (27) Japan US

2009 2010 2011 2012

%

7

Thailand’s investment opportunities

• Thailand’s economic fundamental

• Robustness and profitability of Thai listed companies

• Resilience and performance of SET

• Trading at SET

-150

-100

-50

0

50

100

150

200

250

Nationwide

flood

Oct - Dec 2011

EU Debt crisis

May 2012

8

• Thai listed companies’ profits have been able to withstand major domestic and

international shocks.

Net profits of Thai listed companies

Source : SET

Unit: billion baht

Tsunami

Dec 2005

Bird flu

Apr 2006

Coup d’etat

Sep 2006

Lehman Brothers

bankruptcy

Aug 2008

Global economic

slowdown

H1N1 flu

epidemic

Mar 2009

Political

unrest April

- May 2010

Robustness and profitability of Thai listed companies

9

• While SET’s P/E is attractive compared to peers, SET’s dividend yield is above average.

Source : Bloomberg; SET

3.73.4

3.02.8

2.4

2.1 2.0

1.3

2.7

Unit: percent; data as at 31 January 2013

Market Dividend Yield

17.9

14.9 14.8 14.5 14.2

11.5

10.39.8

13.6

Forward P/E ratio

Unit: times; data as at 31 January 2013

Robustness and profitability of Thai listed companies

10

2007 2010 2012

1.Hong Kong (67) 1.Singapore (67) 1.Singapore (69)

2.Singapore (65) 2.Hong Kong (65) 2.Hong Kong (66)

3.India (56) 3.Japan (57) 3.Thailand (58)

4.Taiwan (54) 4.Thailand (55) 4.Japan (55)

5.Japan (52) 4.Taiwan (55) 4.Malaysia (55)

6. Korea (49) 6.Malaysia (52) 6.Taiwan (53)

6. Malaysia (49) 7.India (49) 7.India (51)

8.Thailand (47) 7.China (49) 8.Korea (49)

9.China (45) 9.Korea (45) 9.China (45)

10.Philippines (41) 10.Indonesia (40) 10.Philippines (41)

11.Indonesia (37) 11.Philippines (37) 11.Indonesia (37)

CG Watch market scores: 2007 to 2012

Source: ACGA, September 2012 Source: Thai IOD

• Thai listed companies have made significant improvements in corporate governance:

• Thailand’s CG score ranking increased from the 8th in Asia in 2007 to the 3rd in 2012, according to the

Asian Corporate Governance Association (ACGA); and

• 59 companies were awarded excellent standard in 2012 by the Thai Institute of Directors (Thai IOD).

RatingNumber of listed companies

2008 % 2012 %

5 stars 22 5% 59 12%

4 stars 123 27% 150 29%

3 stars 177 40% 171 33%

2 stars and below

(including companies in

the litigation

procedures/ pending

further clarification to

governing bodies)

126 28% 133 26%

Total 448 100% 513 100%

Thai IOD CG rating: 2008 vs 2012

Robustness and profitability of Thai listed companies

• Leading Thai listed companies have expanded into other ASEAN countries. Around 40% of

SET-50 companies have operations in ASEAN.

11

Robustness and profitability of Thai listed companies

Examples of Thai listed companies operating in ASEAN countries

12

Thailand’s investment opportunities

• Thailand’s economic fundamental

• Robustness and profitability of Thai listed companies

• Resilience and performance of SET

• Trading at SET

0

200

400

600

800

1,000

1,200

1,400

1,600

-80

-60

-40

-20

0

20

40

60

80

Local institutes Proprietary tradingForeign investors Local retail investors SET index

13

SET index and net buying position in SET

Unit: billion baht (LHS), index (RHS)

Source : SETSMART

• Local retail investors have played a key role in providing liquidity to SET and stabilizing SET index

amid volatile international capital flows.

• In 2012, net buy by foreign investors amounted to 76.9 billion baht (2.5 billion USD).

19 18 23 24

61 62 55 55

7 8 9 8

13 12 13 13

2009 2010 2011 2012Foreign investors Local retail investors

Local institutes Proprietary trading

Transactions by investor type

Unit: percent

-24.9

7.2

76.9

-59.2

Local institutes

Proprietary trading

Foreign investors

Local retail investors

2012 Net buying position in SET

Unit: billion baht

Resilience and performance of SET

14

Resilience and performance of SET

• SET’s average daily turnover has been significantly higher than that of other emerging markets in

South East Asia.

• SET’s turnover velocity has been the highest in South East Asia.

Share turnover velocity* (2008 – January 2013)

Unit: percent

Average daily turnover (2008 – January 2013)

Unit: million USD

0%

20%

40%

60%

80%

100%

120%

Singapore Thailand Indonesia

Bursa Malaysia Philippines

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Singapore Exchange Thailand SE

Indonesia SE Bursa Malaysia

Philippines SE

Source : World Federation of Exchanges (WFE)*Share turnover velocity is calculated by {Monthly EOB Domestic Share Turnover / Month-end Domestic Market Capitalization) *12

40.242.0

21.8

27.0

18.9

7.2

14.4

8.7

35.833.0

25.7

19.717.7

12.910.3

7.6

Thailand Philippines India Singapore Vietnam Indonesia Malaysia China

In USD In local currency

Source : SET

114.2 106.8

66.7

49.5

-5.5

25.7

-25.7 -22.7

90.4 89.5

70.3

32.7

11.2 9.3

-16.4-29.4

Philippines Thailand Indonesia Malaysia India Singapore Vietnam China

In USD In local currency

3-year index performance

Unit: percent; data as at end December 2012

2012 index performance

Unit: percent; as at end December 2012

• SET 2012 YTD index performance has reflected confidence in strong recovery and resilience of Thai

listed companies.

• SET 2010-2012 index performance was among the best in the world.

Resilience and performance of SET

15

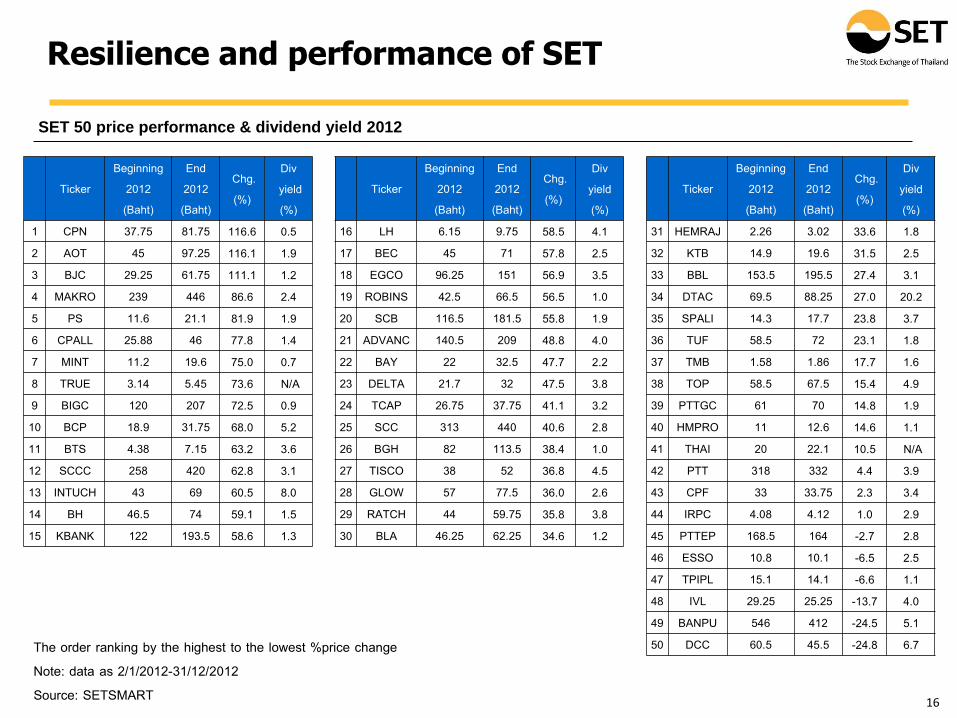

Resilience and performance of SET

TickerBeginning

2012(Baht)

End2012(Baht)

Chg.(%)

Divyield(%)

1 CPN . . . . 2 AOT . . . 3 BJC . . . . 4 MAKRO . . 5 PS . . . . 6 CPALL . . . 7 MINT . . . . 8 TRUE . . . N/A BIGC . . BCP . . . . BTS 4.38 . 63.2 . SCCC . . INTUCH . . BH . . . KBANK . . .

Ticker

Beginning2012(Baht)

End2012(Baht)

Chg.(%)

Div yield(%)

LH . . . . BEC . . EGCO . . . ROBINS . . . . SCB . . . . ADVANC . . . BAY . . . DELTA . . . TCAP . . . . SCC . . BGH . . . TISCO . . GLOW . . . RATCH . . . BLA . . . .

Ticker

Beginning2012(Baht)

End2012(Baht)

Chg.(%)

Div yield(%)

HEMRAJ . . . . KTB . . . . BBL . . . . DTAC . . . . SPALI . . . . TUF . . . TMB . . . . TOP . . . . PTTGC . . HMPRO . . . THAI . . N/A PTT . . CPF . . . IRPC . . . . PTTEP . - . . ESSO . . - . . TPIPL . . - . . IVL . . - . . BANPU - . . DCC . . - . . The order ranking by the highest to the lowest %price change

Note: data as 2/1/2012-31/12/2012Source: SETSMART

SET 50 price performance & dividend yield 2012

16

17

Thailand’s investment opportunities

• Thailand’s economic fundamental

• Robustness and profitability of Thai listed companies

• Resilience and performance of SET

• Trading at SET

• SET has a diverse product ranges to meet the needs of diverse customer segments.

18

Trading at SET

Cash market

• Common stocks

• Warrants

• Derivative warrants

• ETFs

- Gold ETFs

- Index ETFs

- Foreign ETFs

• Property fund (REITs in 2014)

• Index

- FTSE SET index series

- FTSE SET Shariah index

Derivatives market

Equities Commodities Fixed Income Currency

• SET50 index

futures

• SET50 index

options

• Sector index

futures

• Single stock

futures

• Gold futures

• Silver futures

• Oil futures

• 3M BIBOR

futures

• 6M THBFIX

futures

• 5Y Gov bond

futures

• USD futures

Source: Thailand Futures Exchange

Unit: contracts

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

SET50 Index Futures

Single Stock Futures

Gold Futures

2011 2012

Trading volume of gold futures in Asia

Unit: contracts

Trading at SET

19

Average daily volume of major derivative products

Source: The Futures Industry Association

Trade stock-F

Most SET-listed Thai companies have foreign ownership restriction. Check out foreign ownership restriction of each stock via www.set.or.th >> company/securities info >> equity >> then select your preferred company.

20

2 options to get all benefits from investing in Thai stocks.

Option 1: Mostly for strategic shareholders

Trade NVDR stock or stock-R

• Another option is to trade NVDRs. (Non-Voting Depository Receipts)

• Obtain all financial benefits with the exception of voting rights.

• Gain greater efficiency, flexibility and convenience as if you are local investors.

Option 2: General option

Trading at SET

Remarks: Trading stocks on local board is applicable. However, to get all benefits, stocks should be transferred to stock-F or stock-R.NVDRs traded on local board, no price different from local stocks.

42.77%

49.62%

7.61%

Proportion of trading value by type of stocks by foreign investors

Local

Shares

NVDRs

Foreign

Shares

Source: SET, May 2011-April 2012

21

Trading at SET: www.set.or.th

Search by

stock symbol

Market

summary

1

2

3

Select

“Companies/

Securities

info” tab

22

Trading at SET: www.set.or.th

Detail of each PLC: price,

financial ratio

Stock Calendar of rights and

benefits

Stocks in pipeline for IPOs in this

year

1

2

3

4

5

6

Statistic on the number of listed

companies and market

capitalizations

List of index constituents in SET

100, SET50, FTSE SET index

Opportunity Day: A day for PLC

to communicate with Investors,

Analysts on their recent

business and operations.

1

2

3

4

5

6

Allow SET to broadcast

VDO File of Company’s

Analyst Meeting

Opportunity Day Webcast

1. Website

www.set.or.th/oppday

www.settrade.or.th/oppday

2. iPhone & Smart Phone

3. App OppDay on iPad

Live from Meeting room

23

Trading at SET: Opportunity Day Webcast

3 channels to view and join Live

Opportunity Day

Note: Presentation in English is currently still limited. However, the company presenting in English are increasing gradually.

24

At Invest ASEAN, Malaysia

• PTT Global Chemical Public Company Limited (PTTGC) is a Chemical Flagship of PTT Group with the combined chemical / petrochemical capacity of 8.45 million tons per year and crude oil / condensate distillation capacity of 280,000 barrels per day.

• PTTGC is Thailand’s largest gas-based petrochemical producer with an integrated refining business, also steps to be a leading Asia-Pacific company for its size and product diversity. PTTGC’s competitive advantage remains in its competitive cost structure with a diversified product portfolio that strives to seek for downstream opportunity and bio-based business in the future.

• Thailand’s fifth-largest bank in term of assets, loans, and deposits.

• Krungsri (Bank of Ayudhya) is the largest card issue in Thailand with 6.1 million accounts (credit card, sales finance/ personal loans) in its portfolio.

• Krungsri Auto, the company’s flagship automobile financing service provider, is the second largest auto hire-purchase operator in Thailand.

• Krungsi’s micro finance’s arm (CFGS) is the pioneer in micro finance services.

• A leading investment company in the power generation business in Thailand.

• The key strategies and investment target emphasize on electricity generating, renewable energy business and electricity production related business.

• Has coverage in Lao PDR, Australia and exploring business opportunities in this region.

Appendix

The Stock Exchange of Thailand (SET)

& Thai PLCs

26

The Stock Exchange of Thailand (SET)

For more than three decades, The Stock Exchange of Thailand (SET) has stood the test of time to be the center of Thailand’s capital market and a thriving and dynamic exchange offering a full range of products, services and trading infrastructure for investors, listed companies and other participants. Its progressive developments over the past few years resulted in the upgrade of the Thai capital market by FTSE to the advanced emerging market status.

SET offers investors the advantages of being a one-stop service for securities, derivatives, and bonds for both wholesale and retail markets. Its dividend yield is among the highest in Southeast Asia with market capitalization of $390 billion (at the end of Dec 2012). The exchange has become the region’s highest turnover velocity and the highest average daily turnover in Southeast Asia. The exchange also provides compelling investment opportunities with healthy profitability and attractive returns of Thai listed companies. During last year, SET index has increased by 36%. Furthermore, MSCI Berra, the leading index provider, has added 13 stocks into MSCI Global Standard Indices and MSCI Global Small Cap Indices since November 2012. To raise its competitiveness, SET is now upgrading IT infrastructure with cutting-edge features that match leading global exchanges, making its trading system to be one of the fastest systems in Asia.

The Stock Exchange of Thailand62 Ratchadaphisek Road, Klongtoey, Bangkok 10110

27

SET’s speaker

Dr. Pakorn Peetathawatchai

Chief Strategy and Finance Officer, The Stock Exchange of Thailand

Dr. Pakorn has been appointed as Chief Strategy and Finance Officer, The Stock Exchange of Thailand, since January 2013. He oversees the Exchange’s overall strategy and supervises the exchange’s finance. In addition, he also oversees the Capital Market Research Institution which is the research arm of the exchange to help strengthen and shape the development of capital market in Thailand. Prior to this role, he was Chief Marketing Officer, The Stock Exchange of Thailand, since October 2010. Under this role, he overseen the Exchange's products, which are equities, bonds, and derivatives, and developed products that suit the needs of domestic and overseas investors. He also managed product and product-related information and market access. Lastly, he supervised customer and channel services, strengthened all the services offered to securities companies, retail investors, and domestic and international institutional investors.

Previously Mr. Pakorn was a Senior Executive Vice President for Mit Phol Sugar Corp., Ltd. where he supervised the company's Finance, Information Technology, and Risk Management. He has strong treasury background from Siam Commercial Bank PCL as the Head of the bank's Treasury Group and investment experience as the Chairperson of the Investment Committee at SCNY Life and served as an Advisor to the Investment Committee, Government Pension Fund, and a member of the Capital Development Sub-Committee, Ministry of Finance.

Mr. Pakorn now serves as a member of the Asian Bond Fund - Thailand Monitoring Committee, Bank of Thailand. He received his Ph.D degree in Finance and Economics from Boston University, United States.

28

Corporate Participants

PTT Global Chemical Public Company Limited : PTTGC

• Mr. Patiparn Sukorndhaman – Corporate Speaker

Executive Vice President- Finance and Accounting

• Mr. Thitipong Jurapornsiridee - Vice President – Corporate Finance and

Investor Relations

• Ms. Sinida Pechveerakul - IR Analyst Mr. Suradech Mekmongkolchai - Communication Officer

• Ms. Prang Chudasring - IR Analyst Ms. Kadewaluk Tanantpapat - Communication Officer

• Mr. Vasant Srichanwit - Senior Communication Officer

Bank of Ayudhya Public Company Limited: BAY

• Ms. Duangdao Wongpanitkrit – Corporate Speaker

Chief Finance Officer

• Mr. Poonsit Wongthawatchai - Senior Vice President and Manager,

Investor Relations Department

• Ms. Nucha Sirirattna - First Assistant Vice President

Ratchaburi Electricity Generating Holding Public Company Limited : RATCH

• Mr. Wutthichai Tankuranand – Corporate Speaker

Chief Finance Officer

• Ms. Ananda Muthitacharoen - Head of Investor Relations Department

• Ms. Tanawan Jaiboonma - Investor Relations Officer

29

PTT Global Chemical Public Company Limited:PTTGC

PTT Global Chemical Public Company Limited (PTTGC) registered on 19 October 2011, as a Chemical Flagship of PTT

Group with the combined chemical / petrochemical capacity of 8.45 million tons per year and crude oil /condensate distillation capacity of 280,000 barrels per day. PTTGC consists of seven business groups which are Group Performance Center – Refinery and Shared facilities, Group Performance Center – Aromatics, Group Performance Center – Olefins, Polymers Business Unit, EO-Based Performance Business Unit, Green Chemical Business Unit, and High Volume Specialties Business Unit. PTTGC becomes the largest integrated petrochemical and petroleum refining company in Thailand, also steps to be a leading Asia-Pacific company for its size and product diversity.

Mr. Patiparn Sukorndhaman

Executive Vice President, Finance & Accounting

After having extended services in several major Energy and Petrochemical firms,

Mr. Patiparn Sukorndhaman, currently holds a position of Executive Vice President,

Finance and Accounting at PTT Global Chemical Public Company Limited (PTTGC).

The Company was formed from the amalgamation of PTT Chemical Public Company Limited (PTTCH) and PTT

Aromatics and Refining Public Company Limited. His experience well covers all of financial aspects especially those

specialties for the Energy and Petrochemical industries, plus the extensive project financing expertise as illustrated

by his several bold achievements such as BLCP’s Coal-fired power plant project financing (2003), Best Project

Finance Deal of the Year by Asia Money, of US$ 1,200 million, BCP’s Financial Restructuring (2004) issuing the

awards winning deal “BCP Depository Receipt”, the Product Quality Improvement project financing (2004) funding

of US$ 378 million, and BCP refinancing (2008) total of Baht 28,890 million.

30

Bank of Ayudhya Public Company Limited: BAY

Bank of Ayudhya Public Company Limited (BAY or Krungsri) is the fifth-largest commercial bank in Thailand, with

67 years of history in the country. The Bank provides a comprehensive range of banking, consumer finance, investment, asset management and other financial products and services to individual consumers, SMEs, and large corporations through its 605 branches and over 17,000 service outlets nationwide. Through its Krungsrisubsidiaries, the Group is the largest card issuer in Thailand with 6.1 million of accounts (Credit Cards, Sales Finance/Personal Loans) in its portfolio, a major automobile financing service provider (Krungsri Auto), the fastest growing asset management company (Krungsri Asset Management), and a pioneer in microfinance through CFG Services.

Ms. Duangdao Wongpanitkrit, Chief Finance Officer

Duangdao Wongpanitkrit was appointed as Chief Financial Officer (CFO) of Bank of

Ayudhya (Krungsri) on January 1, 2013. She is also a member of Executive Committee.

Duangdao earned her Bachelor of Business Administration in Financial Accounting from

Thammasart University and an MBA from Chulalongkorn University. She is a Certified Public Accountant (CPA

Thailand). After college, Duangdao served as a senior auditor and accounting supervisor with KPMG and Star

Petroleum Refining Co., Ltd. for about seven years. She began her commercial banking career in 1997 when she joined GE Capital (Thailand)’s Financial Planning & Analysis Department. Four years later, Duangdao progressed to the position of Regional Controller for GE Capital Asia Pacific. Before rejoining GE Capital in 2005, Duangdao spent three years at Standard Chartered Bank (Thailand) in the position of Senior Vice President for Wholesale Banking Business Finance. Duangdao returned to GE Capital in 2005 as CFO for GE Money Retail Bank, where she played an instrumental role in successfully qualifying and establishing GE’s first retail bank in Thailand. After GE became a strategic shareholder in Bank of Ayudhya in January 2007, Duangdao spent the next six years as an Executive Vice President (EVP) in the Financial Planning and Analysis Division. During this important growth stage of the bank, her responsibilities included corporate and strategic planning, acquisition and integration support, financial planning, management reporting and capital planning.

31

Ratchaburi Electricity Generating Holding Public Company Limited : RATCH

Ratchaburi Electricity Generating Holding Public Company Limited, a leading investment company in the power generation business in Thailand, was founded on March 7, 2000 in accordance to the Cabinet's approval on November 30, 1999. The key strategies and investment target emphasize on investment and development in three core businesses are electricity generating, renewable energy business and electricity production related business. Apart from Thailand, the Company currently has large scale investment projects in Lao PDR and Australia where there are high potential in power production capacity expansion due to high domestic demand for electricity. RATCH recorded 3Q2012 net profit of 2,003 million baht (increased 63% YoY)

Mr. Wutthichai Tankuranand

Chief Finance Officer

Wutthichai has joined Ratchburi Electricity Generating Holding

Company Public Company Limited since the beginning of 2012 as the Group CFO.

He has brought in over 20 years of extensive experiences in project and corporate finance which he possessed

while he was in commercial banking and telecommunication industries. While he was in banking, he successfully

concluded several international-scale project finance syndicates. Later on he was instrumental in finalizing a project

finance transaction for a new entrant telecom operator in a very concentrated Thai telecom market.

Wutthichai has an electrical engineering degree from Chulalongkorn University and an MBA from University of

Michigan (Ann Arbor).

32

Disclaimer

This document was prepared by The Stock Exchange of Thailand in good faith

upon sources believed to be reliable but no representation or warranty

expressed or implied is made to their accuracy or correctness. The Stock

Exchange of Thailand accepts no liability for any direct or consequential loss or

damage arising from any use of this document or its contents. All information

and opinion expressed here is subject to change without notice. The copyright

belongs to The Stock Exchange of Thailand. No part of this document may be

published or copied in any form or by any means without the written

permission of The Stock Exchange of Thailand.