TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO. 1 … · Accordance With Government Auditing Standards 1-3...

41

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO. 1 MIDDLESEX COUNTY, NEW JERSEY REPORT OF AUDIT .FOR THE YEAR ENDED DECEMBER 31, 2014 HODULIK & MORRISON, P.A. CERTIFIED PUBLIC ACCOUNTANTS REGISTERED MUNICIPAL ACCOUNTANTS HIGHLAND PARK, N.J.

Transcript of TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO. 1 … · Accordance With Government Auditing Standards 1-3...

TOWNSHIP OF PISCATAWAYFIRE DISTRICT NO. 1

MIDDLESEX COUNTY, NEW JERSEY

REPORT OF AUDIT. FOR THE YEAR ENDED

DECEMBER 31, 2014

HODULIK & MORRISON, P.A.CERTIFIED PUBLIC ACCOUNTANTS

REGISTERED MUNICIPAL ACCOUNTANTSHIGHLAND PARK, N.J.

TOWNSHIP OF PISCAT AWAYFIRE DISTRICT NO.1

MIDDLESEX COUNTY, NEW JERSEY

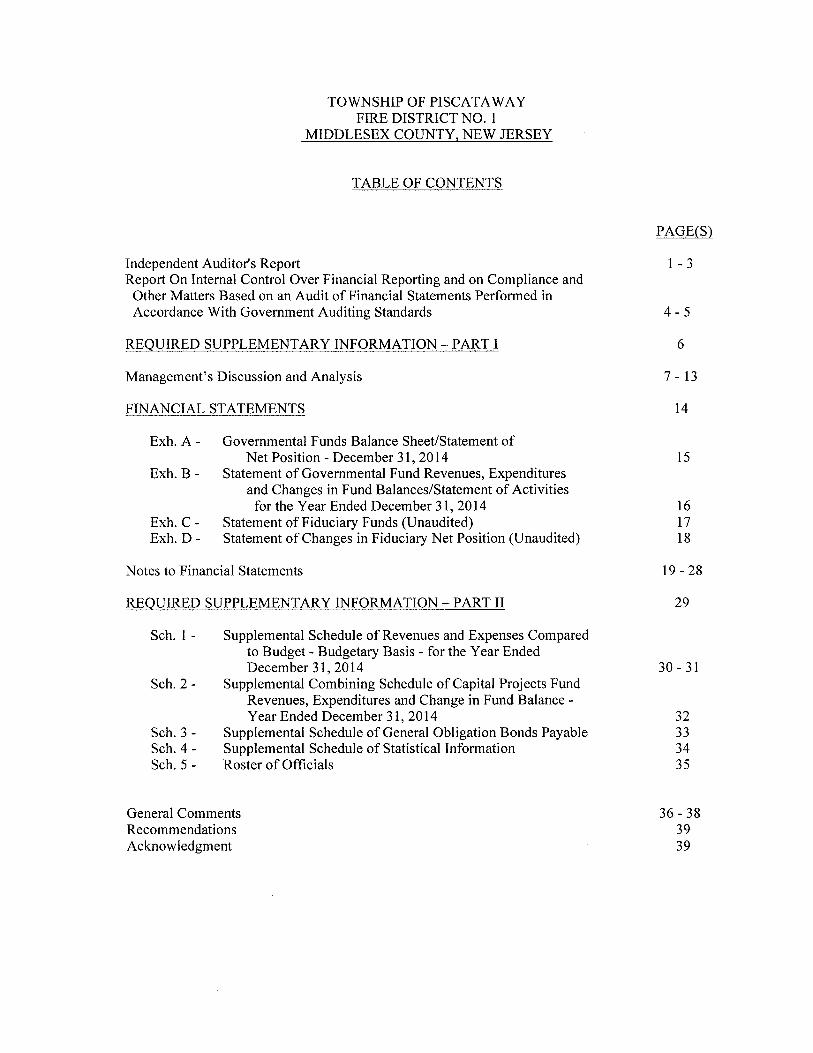

TABLE OF CONTENTS

PAGE(S)

Independent Auditor's ReportReport On Internal Control Over Financial Reporting and on Compliance andOther Matters Based on an Audit of Financial Statements Performed inAccordance With Government Auditing Standards

1 - 3

4-5

REQUIRED SUPPLEMENTARY INFORMATION -PART I 6

Management's Discussion and Analysis 7 - 13

FINANCIAL STATEMENTS 14

Exh. A-

Exh. B-

Exh. C-Exh. D-

Governmental Funds Balance Sheet/Statement ofNet Position - December 31,2014

Statement of Governmental Fund Revenues, Expendituresand Changes in Fund Balances/Statement of Activitiesfor the Year Ended December 31,2014

Statement of Fiduciary Funds (Unaudited)Statement of Changes in Fiduciary Net Position (Unaudited)

15

161718

Notes to Financial Statements 19 - 28

REQUIRED SUPPLEMENTARY INFORMATION - PART II 29

Sch. 1 -

Sch. 2-

Sch. 3 -Sch. 4-Sch. 5 -

General CommentsRecommendationsAcknowledgment

Supplemental Schedule of Revenues and Expenses Comparedto Budget - Budgetary Basis - for the Year EndedDecember 31, 2014

Supplemental Combining Schedule of Capital Projects FundRevenues, Expenditures and Change in Fund Balance -Year Ended December 31, 2014

Supplemental Schedule of General Obligation Bonds PayableSupplemental Schedule of Statistical InformationRoster of Officials

30 - 31

32333435

36 - 383939

HODULIK & MORRISON, P.A.CERTIFIED PUBLIC ACCOUNTANTS

REGISTERED MUNICIPAL ACCOUNTANTS

PUBLIC SCHOOL ACCOUNTANTS1102 RARITAN AVENUE, P.O. BOX 1450

HIGHLAND PARK, NJ 08904

(732) 393-1000(732) 393-1196 (FAX)

(E-MAIL)[email protected]

ANDREW G. HODULIK, CPA, RMA, PSAROBERT S. MORRISON, CPA, RMA, PSA

MEMBERS OF:AMERICAN INSTITUTE OF CPA'SNEW JERSEY SOCIETY OF CPA'S

REGISTERED MUNICIPAL ACCOUNTANTS OF N.J10 ANN BOOS, CPA, PSA

INDEPENDENT AUDITOR'S REPORT

Board of Fire Commissioners of theTownship of Piscataway Fire District No.1

Middlesex County, New Jersey

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities and each major fundand the aggregate remaining fund information of the Township of Piscataway Fire District No.1, MiddlesexCounty, New Jersey, (the "District"), as of and for the year ended December 31,2014, and the related notes tothe financial statements, which collectively comprise the Township of Piscataway Fire District No.1 's basicfinancial statements, as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordancewith the accounting principles generally accepted in the United States of America; this includes the designimplementation, and maintenance of internal control relevant to the preparation and fair presentation offinancial statements that are free from material misstatement, whether due to error or fraud.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted ouraudit in accordance with auditing standards generally accepted in the United States of America, the standardsapplicable to financial audits contained in Government Auditing Standards, issued by the Comptroller Generalof the United States and the audit requirements prescribed by the Division of Local Government Services,Department of Community Affairs, State of New Jersey. Those standards require that we plan and perform theaudit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in thefinancial statements. The procedures selected depend on the auditor's judgment, including the assessment ofthe risks of material misstatement of the financial statements, whether due to fraud or error. In making thoserisk assessments, the auditor considers internal control relevant to the entity's preparation and presentation ofthe financial statements in order to design audit procedures that are appropriate in the circumstances, but notfor the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, weexpress no such opinion. An audit also includes evaluating the appropriateness of accounting policies used andthe reasonableness of significant accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

- 1-

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for ouraudit opinion.

Length of Service Award Program (LOSAP)

The financial statements referred to in the first paragraph include the assets, liabilities and net position of theDistrict's Length of Service Award Program (LOSAP), which represent 100% of the District's fiduciary fund.Pursuant to N.J. State regulation, LOSAP is subject to an independent accountant's review.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the respectivefinancial position of the governmental activities and each major fund and the aggregate remaining fundinformation of the Township of Piscataway Fire District No.1, as of December 31,2014, and the respectivechanges in financial position and, where applicable, cash flows thereof for the year then ended in accordancewith accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management'sdiscussion and analysis and budgetary comparison information as listed in the table of contents be presented tosupplement the basic financial statements. Such information, although not a part of the basic financialstatements, is required by the Governmental Accounting Standards Board, which considers it to be an essentialpart of financial reporting for placing the basic financial statements in an appropriate operational, economic, orhistorical context. We have applied certain limited procedures to the required supplementary information inaccordance with auditing standards generally accepted in the United States of America, which consisted ofinquiries of management about the methods of preparing the information and comparing the information forconsistency with management's responses to our inquires, the basic financial statements, and other knowledgewe obtained during our audit of the basic financial statements. We do not express an opinion or provide anyassurance on the information because the limited procedures do not provide us with sufficient evidence toexpress an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming an opinion on the financial statements that collectivelycomprise the Township of Piscataway Fire District No. 1's basic financial statements as a whole. Thesupplemental schedules, as listed in the table of contents, are presented for purposes of additional analysis andare not a required part of the basic financial statements of the Township of Piscataway Fire District No.1,Middlesex County, New Jersey.

HODULIK & MORRISON, P.A.- 2-

The Supplemental Data and Schedules are the responsibility of management and were derived directly fromand related directly to the underlying accounting and other records used to prepare the basic financialstatements. Such information has been subjected to the auditing procedures applied in the audit of the basicfinancial statements and certain additional procedures, including comparing and reconciling such informationdirectly to the underlying accounting and other records used to prepare the basic financial statements or to thebasic financial statement themselves, and other additional procedures in accordance with auditing standardsgenerally accepted in the United States of America. In our opinion, the supplemental data section is fairlystated in all material respects in relation to the basic financial statements taken as a whole.

The supplemental data section has not been subjected to the audit procedures applied on the audit of the basicfinancial statements and, accordingly we do not express an opinion or provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued a report dated June 22, 2015 on ourconsideration of the Township of Piscataway Fire District No.T's internal control over financial reporting andour tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements andother matters. The purpose of that report is to describe the scope of our testing of internal control over financialreporting and compliance and the results of that testing, and not to provide an opinion on the internal controlover financial reporting or on compliance. That report is an integral part of an audit performed in accordancewith Government Accounting Standards in considering the Township of Piscataway Fire District No. l'sinternal control over financial reporting and compliance.

HODULIK & MORRISON, P.A.Certified Public AccountantsRegistered Municipal Accountants

Andrew G. HodulikRegistered Municipal AccountantNo. 406

Highland Park, New JerseyJune 22, 2015

HODULIK & MORRISON, P.A.-3-

HODULIK & MORRISON, P.A.CERTIFIED PUBLIC ACCOUNTANTS

REGISTERED MUNICIPAL ACCOUNTANTSPUBLIC SCHOOL ACCOUNTANTS

1102 RARITAN AVENUE, P.O. BOX 1450HIGHLAND PARK, NJ 08904

(732) 393-1000(732) 393-1196 (FAX)

(E-MAIL)[email protected]

ANDREW G. HODUUK, CPA.RMA. PSAROBERT S. MORRISON. CPA. RMA.PSA

MEMBERS OF:AMERICAN INSTITUTE OF CPA'SNEW JERSEY SOCIEfY OF CPA'S

REGISTERED MUNICIPAL ACCOUNTANTS OFNJJO ANN BOOS. CPA, PSA

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING ANDON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OFFINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH

GOVERNMENT AUDITING STANDARDS

INDEPENDENT AUDITOR'S REPORT

Board of Fire Commissioners of theTownship of Piscataway Fire District No.1

Middlesex County, New Jersey

We have audited, in accordance with auditing standards generally accepted in the United States ofAmerica, the standards applicable to financial audits contained in Government Auditing Standards,issued by the Comptroller General of the United States and audit requirements as prescribed by theDivision of Local Government Services, Department of Community Affairs, State of New Jersey, thefinancial statements of the governmental activities; each major fund, and the aggregate remaining fundinformation of the Township of Piscataway Fire District No. 1 (the "District") as of and for the yearended December 31, 2014, and the related notes to the financial statements and have issued our reportthereon dated June 22, 2015.

Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered the Township ofPiscataway Fire District No.T's internal control over financial reporting (internal control) to determinethe audit procedures that are appropriate in the circumstances for the purpose of expressing our opinionon the financial statements, but not for the purpose of expressing an opinion on the effectiveness of theTownship of Piscataway Fire District No. l's internal control. Accordingly, we do not express anopinion on the effectiveness of the Township of Piscataway Fire District No.1 's internal control.

A deficiency in internal control exists when the design or operation of a control does not allowmanagement or employees, in the normal course of performing their assigned functions, to prevent, ordetect and correct misstatements on a timely basis. A material weakness is a deficiency, or acombination of deficiencies, in internal control such that there is a reasonable possibility that a materialmisstatement of the entity's financial statements will not be prevented, or detected and corrected on atimely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal controlthat is less severe than a material weakness, yet important enough to merit attention by those chargedwith governance.

-4-

Our consideration of internal control was for the limited purpose described in the first paragraph of thissection and was not designed to identify all deficiencies in internal control that might be materialweaknesses or significant deficiencies. Given these limitations, during our audit we did not identify anydeficiencies in internal control that we consider to be material weaknesses. However, materialweaknesses may exist that have not been identified.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Township of Piscataway Fire District No.l 's financial statements are free of material misstatement, we performed tests of its compliance withcertain provisions of laws, regulations, contracts, and grant agreements, noncompliance with whichcould have a direct and material effect on the determination of financial statement amounts. However,providing an opinion on compliance with those provisions was not an objective of our audit and,accordingly, we do not express such an opinion. The results of our tests disclosed no instances ofnoncompliance or other matters that are required to be reported under Government Auditing Standardsand audit requirements as prescribed by the Division of Local Government Services, Department ofCommunity Affairs, State of New Jersey.

We noted other matters involving internal control over financial reporting that we have reported tomanagement of the Township of Piscataway Fire District No. I in the General Comments section of theReport of Audit.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control andcompliance and the results of that testing, and not to provide an opinion on the effectiveness of theentity's internal control or on compliance. This report is an integral part of an audit performed inaccordance with Government Auditing Standards in considering the entity's internal control andcompliance. Accordingly, this communication is not suitable for any other purpose.

HODULIK & MORRISON, P.A.Certified Public AccountantsPublic School Accountants

Highland Park, New JerseyJune 22, 2015

HODULIK & MORRISON, P.A.-5-

REQUIRED SUPPLEMENTARY INFORMATION - PART I

-6-

PISCATAWAY TOWNSHIP FIRE DISTRICT #1MIDDLESEX COUNTY, NEW JERSEY

MANAGEMENT'S DISCUSSION AND ANALYSISDecember 31, 2014

(Unaudited)

The Piscataway Township Fire District #1 (the "District") is not included in any othergovernmental "reporting entity" as defined by the GASB pronouncement, since firecommissioners are elected by the public and have decision-making capabilities within the Districtto levy taxes, the power to designate management, the ability to significantly influence operationsand primary accountability for fiscal matters. The District is not considered a component-unit ofthe Township of Piscataway, Middlesex County, New Jersey (the "Township"). The District doesnot have any component-units. The following Management's Discussion and Analysis of theactivities and financial performance of the District provide an introduction to the financialstatements of the District for the year ended December 31, 2014. Please read it in conjunctionwith the District's financial statements and accompanying notes.

The Management's Discussion and Analysis is an element of the new reporting model adopted bythe Governmental Accounting Standards Board (GASB) in their Statement No.34, BasicFinancial Statements - and Management's Discussion and Analysis - for State and LocalGovernments, issued June 1999 and amended by GASB Statement No. 37. Certain comparativeinformation between the current year and the prior year is required to be presented in the MD&A.

FINANCIAL HIGHLIGHTS

Total current and other assets increased by $182,001.94 (15.92%) to $1,324,926.29 in 2014 from$1,142,924.35 in 2013.

Total liabilities increased by $22,242.16 (48.84%) to $67,787.40 in 2014 from $45,545.24 in2013.

Revenues decreased by $47,263.12 (3.74%) to $1,217,079.37 in 2014 from $1,264,342.49 in2013.

Expenses decreased by $21,910.37 (2.03%) to $1,057,319.59 in 2014 from $1,079,229.96 in2013.

USING THIS REPORT

This annual report consists of a series of financial statements and notes to those statements. Thesestatements are organized so the reader can understand Piscataway Township Fire District No.1 asa financial whole, an entire operating entity. The statements then proceed to provide anincreasingly detailed look at specific financial activities.

This annual report consists of three parts - management's discussion and analysis (this section),the basic financial statements, and required supplementary information. The basic financialstatements include two kinds of statements that present different views of the District:

-7-

DISTRICT-WIDE FINANCIAL STATEMENTS

These statements provide both short-term and long-term information about the District's overallfinancial status.

FUND FINANCIAL STATEMENTS

Fund financial statements focus on individual parts of the District, reporting the District'soperations in more detail than the district-wide statements.

• The governmental funds statements tell how basic services were financed in the shortterm as well as what remains for future spending

• Fiduciary funds statements provide information about the financial relationships inwhich the District acts solely as a trustee for future spending.

The financial statements also include notes that explain some of the information in the statementsand provide more detailed data. The statements are followed by a section of requiredsupplementary information that further explains and supports the financial statements with acomparison of the District's budget for the year ..

Fund Financial StatementsDistrict -wide Statements Governmental Funds Fiduciarv Funds

Scope Entire district (except The activities of the district that are Instances in which the districtfiduciary funds) not proprietary or fiduciary administers resources on behalf

of someone else

Required -Statement of net position -Balance Sheet -Statement of fiduciary netfinancial -Statement of activities -Statement of revenues, expenditures, positionstatements and changes in fund balance -Statement of changes in

fiduciary net position

Accounting Accrual accounting and Modified accrual accounting and Accrual accounting and

basis and economic resources focus current financial resources focus economic resources focus

measurementfocusType of All assets and liabilities, Generally assets expected to be used All assets and liabilities, bothasset/liability both financial and capital, up and liabilities that come due short-term and long-term. Theinformation short-term and long-term during the year or soon thereafter, no District's funds do not

capital assets or long-term liabilities currently contain capital assets,included although they can

Type of All revenues and expenses Revenues for which cash is received All additions and deductions,inflow/outflow during the year, regardless during or soon after the end of the during the year, regardless ofinformation of when cash is received of year, expenditures when goods or when cash is received or paid

paid services have been received and therelated liability is due and payable

Figure A-I summarizes the major features of the District's financial statements, including theportion of the District's activities they cover and the types of information they contain. Theremainder of this overview section of management's discussion and analysis highlights thestructure and contents of each of the statements.

The Statement of Net Position and Statement of Activities provide information about theactivities of the whole District, presenting both an aggregate view of the District's finances and alonger-term view of those finances. Fund financial statements provide the next level of detail. Forgovernmental funds, these statements tell how services were financed in the short-term as well aswhat remains for future spending. In the case of Piscataway Township Fire District No.1, theGeneral Fund is by far the most significant fund.

-8-

REPORTING THE DISTRICT AS A WHOLESTATEMENT OF NET POSITION AND THE STATEMENT OF ACTIVITIES

While this document contains the large number of funds used by the District to provide programsand activities, the view of the District as a whole looks at all financial transactions and asks thequestion, "How did we do financially during 2014?" The Statement of Net Position and theStatement of Activities answer this question. These statements include all assets and liabilitiesusing the accrual basis of accounting similar to the accounting used by most private-sectorbusinesses. This basis of accounting takes into account all of the current year's revenues andexpenses regardless of when cash is received or paid.

These two statements report the District's net position and changes in those assets. This change innet position is important because it tells the reader that, for the District as a whole, the financialposition of the District has improved or diminished. The cause of this change may be the result ofmany factors, some financial and some not. Non-financial factors include the District's propertytax base, current laws in New Jersey restricting revenue growth, facility condition, requiredprograms, and other factors.

REPORTING THE DISTRICT'S MOST SIGNIFICANT FUNDSFUND FINANCIAL STATEMENTS

Fund financial reports provide detailed information about the District's funds. The District usesmany funds to account for a multitude of financial transaction. The District's governmental fundsare the General Fund and Capital Projects Fund.

GOVERNMENTAL FUNDSThe District's activities are reported in governmental funds, which focus on how money flows inand out of those funds and the balance left at year-end available for spending in the future years.These funds are reported using an accounting method called modified accrual accounting, whichmeasures cash and all other financial assets that can readily be converted to cash. Thegovernmental fund statements provide a detailed short-term view of the District's generalgovernment operations and the basic services it provides. Governmental fund information helpsthe reader determine whether there are more or fewer financial resources that can be spent in thenear future to finance programs. The relationship (or differences) between governmental activities(reported in the Statement of Net Position and the Statement of Activities) and governmentalfunds is reconciled in the financial statements.

NOTES TO THE FINANCIAL STATEMENTS

The notes provide additional information that is essential to a full understanding of the dataprovided in the District-wide and fund financial statements.

THE DISTRICT AS A WHOLE

Recall that the Statement of Net Position provides the perspective of the District as a whole. Netposition may serve over time as a useful indicator of a government's financial position. TheDistrict's financial position is the product of several financial transactions including the netresults of activities, the acquisition and payment of debt, the acquisition and disposal of capitalassets, and the depreciation of capital assets.

-9-

Table A-ISummary of Net Position

% Increase/2014 2013 (Decrease)

Current and Other Assets $730,289.29 $1,142,924.35 -36.10%Due from Township of Piscataway

District Taxes 594,637.00Capital Assets 2,473,842.63 2,628,840.04 -5.90%

Total Assets 3,798,768.92 3,771,764.39 0.72%

Other Liabilities 8.10,836.15 915,828.37 -11.46%

Total liabilities 810,836.15 915,828.37 -11.46%

Net Position:Net Investment in Capital Assets 1,743,842.63 1,773,840.04 -1.69%Restricted 669,884.70 465,321.74 43.96%Unrestricted 574,205.44 616,774.24 -6.90%

Total Net Position $2.987,932.77 $2,855,236.02 4.62%

Table A-2Change in Net Position

% Increase/2014 2013 (Decrease)

Revenues:General Revenues

Property Taxes $1,189,274.00 $1,198,722.00 -0.79%State Formula Aid 4,606.25 4,606.25 0.00%Interest on Investments 853.34 810.61 5.27%Other 22,345.78 60,203.63 -62.88%

Total revenues $1,217,079.37 $1,264,342.49 -3.74%

Expenses:Administration $83,808.70 $80,008.81 4.75%Cost of Operations and Maintenance 966,828.81 869,395.67 11.21%Interest on Long Term Debt 34,445.11 39,682.50 -13.20%

Total Expenses $1 ,085,082.62 $989,086.98 9.71%

Excess (Deficiency) of Revenues Over(Under) Expenditures $131,996.75 $275,255.51 52.05%

-10 -

GOVERNMENTAL ACTIVITIES

The unique nature of property taxes in New Jersey creates the legal requirements to annually seekvoter approval for the District's operations. Property taxes made up 97.71% of revenue forgovernmental activities for Piscataway Township Fire District No.1 for 2014. The District'stotal revenues were $1,217,079.37 for the year ended December 31, 2014. State aid accounted foranother 0.38% of revenue, and other miscellaneous revenue accounted for the remaining 1.91%.

The Statement of Activities shows the cost of program services and the charges for services andgrants offsetting those services. Table A- shows the total cost of services and the net cost ofservices. The net cost shows the financial burden that was placed on the District's taxpayers byeach of these functions.

Table A-3Cost of Services vs. Net Cost of Services

Total Cost Net Cost Total Cost Net Costof Services of Services of Services of Services

2014 2014 2013 2013--

Administration $ 83,808.70 $ 83,808.70 $ 80,008.81 $ 80,008.81Cost of Operations and Maintenance 939,322.65 939,322.65 829,395.67 829,395.67Length of Service Awards Program 27,506.16 27,506.16 40,000.00 40,000.00Interest on Long Term Debt 34,445.11 34,445.11 39,682.50 39,682.50

Total $1~085~082.62 $1~085~082.62 $989~086.98 $989~086.98

Administration includes expenses associated with administrative and financial supervision of theDistrict.

Cost of Operations and Maintenance includes keeping equipment in an effective workingcondition.

THE DISTRICT'S FUNDS

All governmental funds (i.e., general fund and capital projects fund presented in the fund-basedstatements) are accounted for using the modified accrual basis of accounting. Total revenuesamounted to $1,217,079.37 and expenditures were $1,057,319.59. The change in fund balance forthe year in the general fund was an increase of $205,196.82 and a decrease of $45,437.04 in thecapital projects fund.

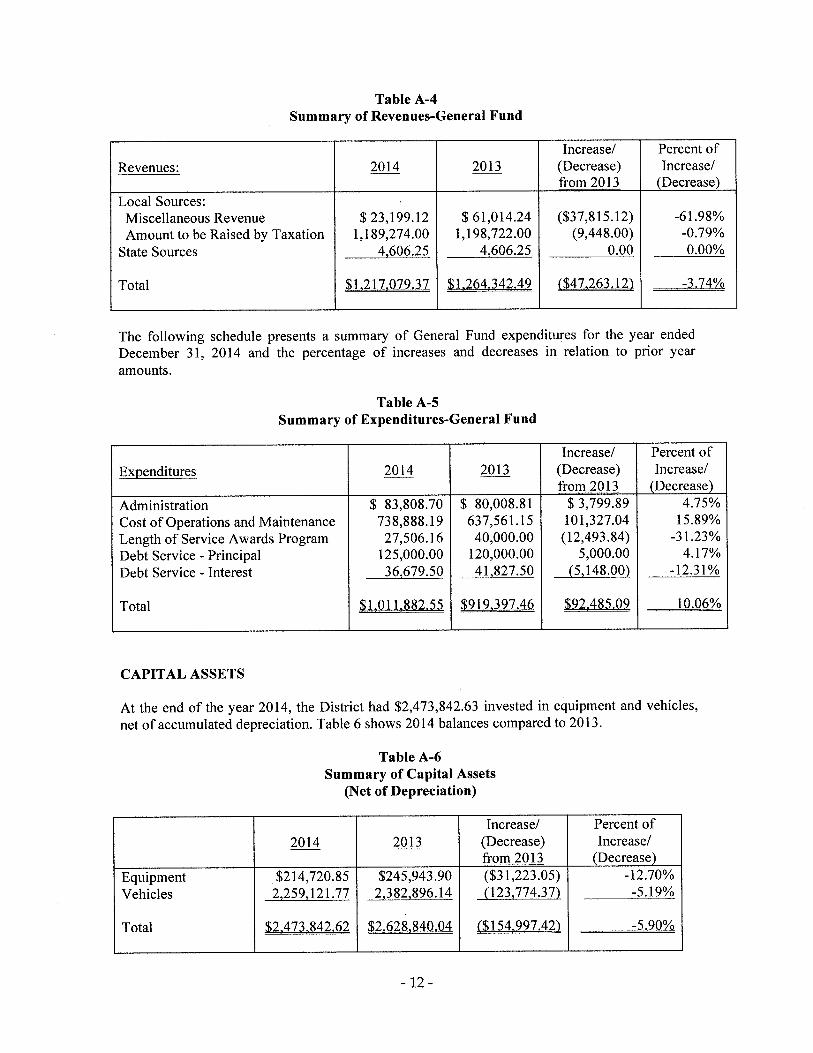

As demonstrated by the various statements and schedules included in the financial section of thisreport, the District continues to meet its responsibility for sound financial management. Thefollowing schedules present a summary of the revenues of the General Fund for the year endedDecember 31,2014, and the amount and percentage of increases and decreases in relation to prioryear revenues.

-11-

Table A-4Summary of Revenues-General Fund

Increase! Percent ofRevenues: 2014 2013 (Decrease) Increase!--

from 2013 (Decrease)Local Sources:Miscellaneous Revenue $ 23,199.12 $ 61,014.24 ($37,815.12) -61.98%Amount to be Raised by Taxation 1,189,274.00 1,198,722.00 (9,448.00) -0.79%

State Sources 4,606.25 4,606.25 0.00 0.00%

Total $1~217~079.37 $1~264,342.49 ($47,263.12) -3.74%

The following schedule presents a summary of General Fund expenditures for the year endedDecember 31, 2014 and the percentage of increases and decreases in relation to prior yearamounts.

Table A-5Summary of Expenditures-General Fund

Increase! Percent ofExpenditures 2014 2013 (Decrease) Increase!

from 2013 (Decrease)Administration $ 83,808.70 $ 80,008.81 $ 3,799.89 4.75%Cost of Operations and Maintenance 738,888.19 637,561.15 101,327.04 15.89%Length of Service Awards Program 27,506.16 40,000.00 (12,493.84) -31.23%Debt Service - Principal 125,000.00 120,000.00 5,000.00 4.17%Debt Service - Interest 36,679.50 41,827.50 (5,148.00) -12.31%

Total $1~011,882.55 $919~397 .46 $92A85.09 10.06%

CAPITAL ASSETS

At the end of the year 2014, the District had $2,473,842.63 invested in equipment and vehicles,net of accumulated depreciation. Table 6 shows 2014 balances compared to 2013.

TableA-6Summary of Capital Assets

(Net of Depreciation)

Increase! Percent of2014 2013 (Decrease) Increase!

from 2013 (Decrease)Equipment $214,720.85 $245,943.90 ($31,223.05) -12.70%Vehicles 2,259,121.77 2,382,896.14 (123,774.37) -5.19%

Total $2,473,842.62 $2,628,840.04 ($154~997.42) -5.90%

-12 -

LONG-TERM DEBT

During 2009 the fire district issued $1,300,000 in bonds. Principal is due in August commencingin 2010 through maturity of 2019 and interest is due semi-annually in February and August withan interest rate of 4.29%. The district's outstanding long-term debt at December 31, 2014 is$730,000.00.

CONTACTING THE DISTRICT'S MANAGEMENT

This financial report is designed to provide Piscataway Township residents and taxpayers, and theDistrict's customers, investors and creditors, with a general overview of the District's financesand to demonstrate the District's accountability for the money it receives. If you have questionsabout this report or need additional information, please contact the District Treasurer, PiscatawayTownship Fire District #1, 801 South Washington Avenue P.O. Box 8060, Piscataway, NewJersey, 08855.

-13 -

FINANCIAL STATEMENTS

-14 -

Exhibit-A

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, NEW JERSEY

GOVERNMENTAL FUNDS BALANCE SHEET/STATEMENT OF NET POSITlON

DECEMBER 31. 2014

CAPITAL

GENERAL PROJECTS STATEMENT OF

ASSETS FUND FUND TOTAL ADJUSTMENTS NETPOSITlON

Cash and Cash Equivalents s 539,406.85 s 190,882.44 s 730,289.29 s s 730,289.29

Due from Township of Piscataway

District Taxes 594,637.00 594,637.00 594,637.00

Capital Assets, net ofaccumulated depreciation 2,473,842.63 2,473,842.63

Total Assets s 1,134,043.85 s 190,882.44 s 1,324,926.29 s 2,473,842.63 s 3,798,768.92

LIABILITIES AND NET POSITION

Liabilities:Accounts Payable s 67,787.40 s s 67,787.40 s $ 67,787.40

Accrued Interest on Bonds 13,048.75 13,048.75

Noncurrent Liabilitites

Due Within One Year 130,000.00 130,000.00

Due Beyond One Year 600,000.00 600,000.00

Total Liabilities 67,787.40 67,787.40 743,048.75 810,836.15

Fund BalanceslNet Position:Fund Balances:

Restricted:Future Capital Outlays 479,002.26 479,002.26 (479,002.26)

Capital Projects 190,882.44 190,882.44 (190,882.44)

Assigned:Designated for Subsequent

Year's Expenditures 216,487.00 216,487.00 (216,487.00)

Unassigned 370,767.19 370,767.19 (370,767.19)

Total Fund Balances 1,066,256.45 190,882.44 1,257,138.89 (1,257,138.89)

Total Liabilities and Fund Balances s 1,134,043.85 s 190,882.44 s 1,324,926.29

Net PositionNet Investment in Capital Assets 1,743,842.63 1,743,842.63

Restricted for Capital Projects 669,884.70 669,884.70

Unrestricted 574,205.44 574,205.44

Total Net Position s 2,987,932.77 s 2,987,932.77

Note: See Notes to Financial Statements

-15 -

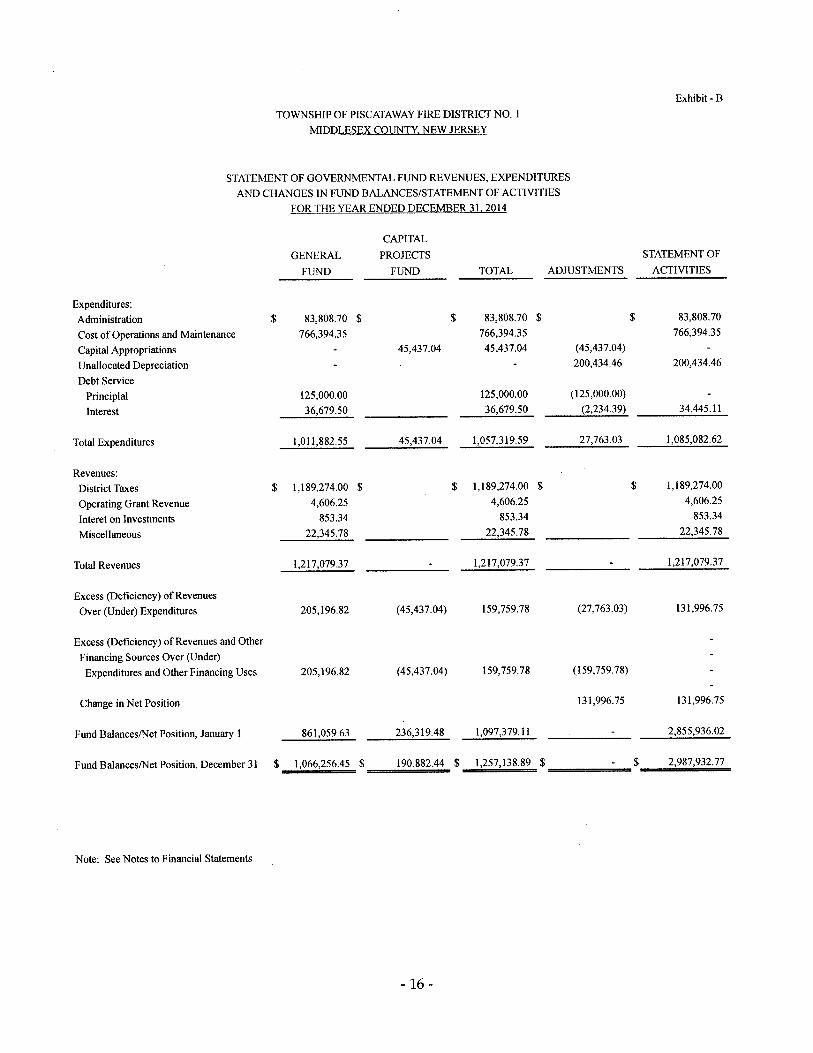

Exhibit - B

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1

MIDDLESEX COUNTY, NEW JERSEY

STATEMENT OF GOVERNMENTAL FUND REVENUES, EXPENDITURES

AND CHANGES IN FUND BALANCES/STATEMENT OF ACTIVITIESFOR THE YEAR ENDED DECEMBER 31. 2014

CAPITAL

GENERAL PROJECTS STATEMENT OF

FUND FUND TOTAL ADJUSTMENTS ACTIVITIES

Expenditures:

Administration $ 83,808.70 $ $ 83,808.70 $ $ 83,808.70

Cost of Operations and Maintenance 766,394.35 766,394.35 766,394.35

Capital Appropriations 45,437.04 45,437.04 (45,437.04)

Unallocated Depreciation 200,434.46 200,434.46

Debt Service

Principlal 125,000.00 125,000.00 (125,000.00)

Interest 36,679.50 36,679.50 (2,234.39) 34,445.11

Total Expenditures 1,011,882.55 45,437.04 1,057,319.59 27,763.03 1,085,082.62

Revenues:

District Taxes $ 1,189,274.00 $ $ 1,189,274.00 $ $ 1,189,274.00

Operating Grant Revenue 4,606.25 4,606.25 4,606.25

Interet on Investments 853.34 853.34 853.34

Miscellaneous 22,345.78 22,345.78 22,345.78

Total Revenues 1,217,079.37 1,217,079.37 1,217,079.37

Excess (Deficiency) of Revenues

Over (Under) Expenditures 205,196.82 (45,437.04) 159,759.78 (27,763.03) 131,996.75

Excess (Deficiency) of Revenues and Other

Financing Sources Over (Under)

Expenditures and Other Financing Uses 205,196.82 (45,437.04) 159,759.78 (159,759.78)

Change in Net Position 131,996.75 131,996.75

Fund BalanceslNet Position, January 1 861,059.63 236,319.48 1,097,379.11 2,855,936.02

Fund BalanceslNet Position, December 31 $ 1,066,256.45 $ 190,882.44 $ 1,257,138.89 $ $ 2,987,932.77

Note: See Notes to Financial Statements

- 16-

Exhibit - C

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, NEW JERSEY

FIDUCIARY FUNDSDECEMBER3}' 2014

LOSAP

ASSETS

Assets Held by Fiscal Agent - LOSAP $ __ 38_1....:....,2......4......6.......30_

Total Assets $ 381,246.30

NET POSITION

Held in Trust for:Deferred Compensation $ 381,246.30

Total Net Position $ ==3=:8=1,=24==6=.3~0

Note: See Notes to Financial Statements

-17 -

Exhibit - D

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1STATEMENT OF CHANGES IN FIDUCIARY NET POSITION

FIDUCIARY FUNDSFOR THE YEAR ENDED DECEMBER 31,2014

LOSAP

ADDITIONSContributions:District Contributions $ 19,134.72

Total Contributions 19,134.72

Investment Earnings:Net Increase/(Decrease) in Fair Value of Investments $ 30,135.74

Net Investment Earnings 30,135.74

Total Additions 49,270.46

DEDUCTIONSWithdrawals 3,299.90

Administrative Fees 800.00

Total Deductions 4,099.90

Change in Net Position 45,170.56

Net Position - Beginning of the Year 336,075.74

Net Position - End of the Year $ 381,246.30

Note: See Notes to Financial Statements

-18 -

TOWNSHIP OF PISCAT AWAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, NEW JERSEY

NOTES TO FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31,2014

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. Reporting Entity

The District was organized under the laws of the State of New Jersey relating to Fire Districtsand established pursuant to N.J.S.A. 40A: 14-70, et seq. The District receives funding fromlocal and state government sources and must comply with the concomitant requirements ofthese funding source entities. However, the District is not included in any othergovernmental "reporting entity" as defined by the GASB pronouncement, since firecommissioners are elected by the public and have decision-making capabilities within theDistrict to levy taxes, the power to designate management, the ability to significantlyinfluence operations and primary accountability for fiscal matters. In addition, there are nocomponent units, as defined in Governmental Accounting Standards Board Statement 14,which are included in the District's reporting entity.

B. General

The financial statements of the Township of Piscataway Fire District No. 1 have beenprepared in conformity with generally accepted accounting principles (GAAP) as applicableto governmental units. The Governmental Accounting Standards Board (GASB) is theaccepted standard-setting body for establishing governmental accounting and financialreporting principles. The more significant of the District's accounting policies are describedbelow.

The accounting policies of the Township of Piscataway Fire District No. 1 ("the District")conform to the accounting principles applicable to special districts which have beenprescribed by the Division of Local Government Services, Department of CommunityAffairs, State of New Jersey ("the Division"). The Division has determined that specialdistricts are separate entities for purposes of financial reporting. Accordingly, the Townshipof Piscataway Fire District No. 1 is not considered a component unit of any othergovernmental unit for financial reporting purposes.

C. GASB Statement No. 34

The Fire District adopted the prOVISIOnsof GASB Statement No. 34, Basic FinancialStatements - and Management's Discussion and Analysis - for State and Local Governmentsduring the fiscal year ended December 31, 2003. Statement 34 established standards forexternal financial reporting for all state and local governmental entities, which includes aManagement's Discussion and Analysis section, a Balance Sheet and a Statement ofRevenues, Expenses and Change in Net Assets. It requires the classification of Net Assetsinto three components - Invested in Capital Assets, net of related debt; Restricted for DebtService; and Unrestricted. GASB Statement No. 63 amended GASB Statement No. 34.

-19 -

NOTES TO FINANCIAL STATEMENTS

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

D. GASB Statement No. 63

This Statement amends the net asset reporting requirements in Statement No. 34, BasicFinancial Statements-and Management's Discussion and Analysis-for State and LocalGovernments, and other pronouncements by incorporating deferred outflows of resourcesand deferred inflows of resources into the definitions of the required components of theresidual measure and by renaming that measure as net position, rather than net assets.

E. Basis of Presentation - Fund Accounting

The accounts of the District are organized on the basis of funds or account groups, each ofwhich is considered a separate accounting entity. The operations of each fund are accountedfor with a separate set of self-balancing accounts that comprise its assets, liabilities, reserves,fund balance, revenues and expenditures or expenses as appropriate. The various funds aresummarized by type in the financial statements. The District uses the following fund types:

Governmental Fund Types

General Fund - The General Fund is the general operating fund of the District and accountsfor all revenues and expenditures of the District not encompassed within other funds. Allgeneral tax revenues and other receipts that are not allocated by law or contractual agreementto some other fund are accounted for in this fund. General operating expenditures and thecapital improvement costs that are not paid through other funds are paid from the GeneralFund. The District budgets for capital appropriations, which includes reserves for futurecapital outlays. The amount raised in the budget for these items are included as reserves offund balance within the General Fund.

Capital Projects Fund - The Capital Projects Fund is used to account for all resources for theacquisition of capital facilities, including property, plant and equipment spanning more thanone budgetary accounting period, by the District.

Fiduciary Fund Types

Trust Funds - The Trust Funds are used to account for assets held by the District in a trusteecapacity or as an agent for individuals, private organizations, other governments and/or otherfunds.

F. Basis of Accounting

The accounting and financial reporting treatment applied to a fund is determined by itsmeasurement focus. All governmental fund types are accounted for using a current financialresources measurement focus. With this measurement focus, only current assets and currentliabilities generally are included on the balance sheet. Operating statements of these fundspresent increases (i.e., revenues and other financing sources) and decreases (i.e. expendituresand other financing uses) in net current assets.

- 20-

NOTES TO FINANCIAL STATEMENTS

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

F. Basis of Accounting (cont'd.)

The governmental fund types follow the modified accrual basis of accounting. Under themodified accrual basis of accounting, revenues are recorded when susceptible to accrual, i.e.,both measurable and available. Available means collectible within the current period or soonenough thereafter to be used to pay liabilities of the current period. Expenditures, other thaninterest on long-term debt, are recorded when the related fund liability is incurred, ifmeasurable.

Revenues from local sources consist primarily of property taxes. Property tax revenues andrevenues received from the state are recognized when susceptible to accrual. Miscellaneousrevenues are recorded as revenue when received in cash because they are generally notmeasurable until actually received. Investment earnings are recorded as earned since they aremeasurable and available.

G. BudgetslBudgetary Controls

The District is required by state law to adopt an annual budget for the General Fund. Formalbudgetary integration into the accounting system is employed as a management controldevice during the year. For governmental funds there are no substantial differences betweenthe budgetary basis of accounting and generally accepted accounting principles.Encumbrance accounting is also employed as an extension of formal budgetary integration inthe governmental fund types.

H. Encumbrances

Encumbrances are not liabilities and, therefore, are not recorded as expenditures until receiptof material or service. Under encumbrance accounting, purchase orders, contracts, and othercommitments for the expenditure of resources are recorded to reserve a portion of theapplicable appropriation. Open encumbrances in governmental funds are reported asreservations of fund balances at year-end as they do not constitute expenditures or liabilitiesbut rather commitments related to unperformed contracts for goods and services. Theencumbered appropriation the District carries over into the next year. For budgetarypurposes, an entry will be made at the beginning of the next year to increase theappropriation reflected in the certified budget by the outstanding encumbrance amount as ofthe current year-end.

I. Cash and Cash Equivalents

Cash and cash equivalents include petty cash, change funds, cash in banks and all highlyliquid investments with a maturity of three months or less at the time of purchase and arestated at cost plus accrued interest. U.S. Treasury and agency obligations and certificates ofdeposit with maturities of one year or less when purchased are stated at cost. All otherinvestments are stated at fair value.

New Jersey fire districts are limited as. to the types of investments and types of financialinstitutions they may invest in.

- 21-

NOTES TO FINANCIAL STATEMENTS

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

I. Cash and Cash Equivalents (cont'd.)

Additionally, the District utilizes a cash management plan that requires it to deposit publicfunds in public depositories protected from loss under the provisions of the GovernmentalUnit Deposit Protection Act ("GUDPA"). GUDPA was enacted in 1970 to protectGovernmental Units from a loss of funds on deposit with a failed banking institution in NewJersey.

N.J.S.A. 17:9-41 et. seq. establishes .the requirements for the security of deposits ofgovernmental units. The statute requires that no governmental unit shall deposit public fundsin a public depository unless such funds are secured in accordance with the Act. Publicdepositories include Savings and Loan institutions, banks (both state and national banks) andsavings banks the deposits of which are federally insured. All public depositories mustpledge collateral, having a market value at least equal to five percent of the average dailybalance of collected public funds, to secure the deposits of Governmental Units. If a publicdepository fails, the collateral it has pledged, plus the collateral of all other publicdepositories, is available to pay the full amount of their deposits to the Governmental Units.

J. Interfund ReceivableslPayables

Interfund receivables and payables arise from interfund transactions and are recorded by allfunds affected in the period in which transactions are executed. Interest is not accrued forthese receivables/pay abies.

K. Inventories of Supplies

Purchases of materials and supplies are recognized and recorded as expenditures when theyare acquired, regardless of when used. The cost of inventories included on the balance sheetis equally offset by a fund balance reserve account.

L. Prepaid Expenses

The cost of prepaid insurance and other similar items extending over more than oneaccounting period is accounted for as expenditures of the period of acquisition and notallocated between or among accounting periods. The amount of such prepayments recordedon the balance sheet is equally offset by a fund balance reserve account.

M. Employee Benefits

Vacation, sick pay, and other employee benefits are recorded as expenditures when paid.

N. Capital Assets

Capital assets are capitalized at historical cost, or estimated historical cost for assets whereactual historical cost is not available. Donated assets are recorded as capital assets at theirestimated fair market value at the date of the donation. The district maintains a thresholdlevel of $5,000 or more for capitalizing capital assets. The system for accumulation of fixedassets cost data does not provide the means for determining the percentage of assets valued atactual and those valued at estimated cost.

- 22-

NOTES TO FINANCIAL STATEMENTS

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

N. Capital Assets (cont'd.)

Capital assets are recorded in the District-wide financial statement, but are not reported in theFund financial statements. Capital assets are depreciated using the straight-line method overtheir estimated useful lives. Since surplus assets are sold for an immaterial amount whendeclared as no longer needed by the District, no salvage value is taken into consideration fordepreciation purpose. Useful lives vary from 20 to 50 years for land improvements andbuildings, and 5 to 15 years for equipment. Capital assets not being depreciated include landand construction in progress.

The District does not possess any material amounts of infrastructure capital assets such assidewalks and parking lots. Such items are considered to be part of the cost of building orother reportable improvable property.

O. Long- Term Obligations

In the government-wide financial statements, long-term debt and other long-term obligationsare reported as liabilities in the applicable governmental activities. Bond premiums anddiscounts, as well as issuance costs, are deferred and amortized over the life of the bondsusing the effective interest method. Bonds payable are reported net of the applicable bondpremium or discount. Bond issuance costs are reported as deferred charges and amortizedover the term of the related debt.

In the fund financial statements, governmental fund types recognize bond premiums anddiscounts, as well as bond issuance costs, during the current period. The face amount of debtissued is reported as other financing sources. Premiums received on debt issuances arereported as other financing sources while discounts on debt issuances are reported as otherfinancing uses. Issuance costs, whether or not withheld from the actual debt proceedsreceived, are reported as debt service expenditures.

P. Fund Equity

Reserves represent those portions of fund equity not appropriable for expenditures or legallysegregated for a specific future use. Designated fund balances represent plans for future useof financial resources.

Q. Net Position

Net position represents the difference between the assets and liabilities in the District-widefinancial statements. Net investment in capital assets consists of capital assets, net ofaccumulated depreciation, reduced by outstanding balance of any long-term debt used tobuild or acquire the capital assets. Net position is reported as restricted in the District-widefinancial statement when there are limitations imposed on their use through externalrestrictions imposed by creditors, grantors, or laws or regulations of other governments.

- 23-

NOTES TO FINANCIAL STATEMENTS

Note 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

R. Reconciliation of Adjustments

The following adjustments/reclassifications were required for the combining of thegovernment-wide and fund financial statements in accordance with GASB:

Statement of Net Position and Governmental Fund Balance Sheet:

Fund BalanceRestrictedAssigned, DesignatedUnassigned

From Adjustment To

0 $ 2,473,842.63 $ 2,473,842.63

0 13,048.75 13,048.75

0 130,000.00 130,000.000 600,000.00 600,000.00

669,884.70 (669,884.70) 0216,487.00 (216,487.00) 0370,767.19 (370,767.19) 0

AssetsCapital Assets, net ofaccumulated depreciation

LiabilitiesAccrued Interest PayableNoncurrent Liabilities:Due Within One YearDue Beyond One Year

Net PositionNet Investment in CapitalAssets

Restricted for Capital ProjectsUnrestricted

ooo

1,743,842.63669,884.70574,205.44

1,743,842.63669,884.70574,205.44 .

Statement of Activities and Governmental Revenues, Expenditures, and Changes in FundBalance:

From Adjustment ToCapital Appropriation 45,437.04 (45,437.04) 0Depreciation 0 200,434.46 200,434.46Principal on Long Term Debt 125,000.00 (125,000.00) 0Interest on Long-Term Debt 36,679.50 (2,234.39) 34,445.11

Excess/(Deficiency) of RevenuesOver/(Under) Expenditures 159,759.78 (27,763.03) 131,996.75

Change in Net Position 0 131,996.75 131,996.75

- 24-

NOTES TO FINANCIAL STATEMENTS

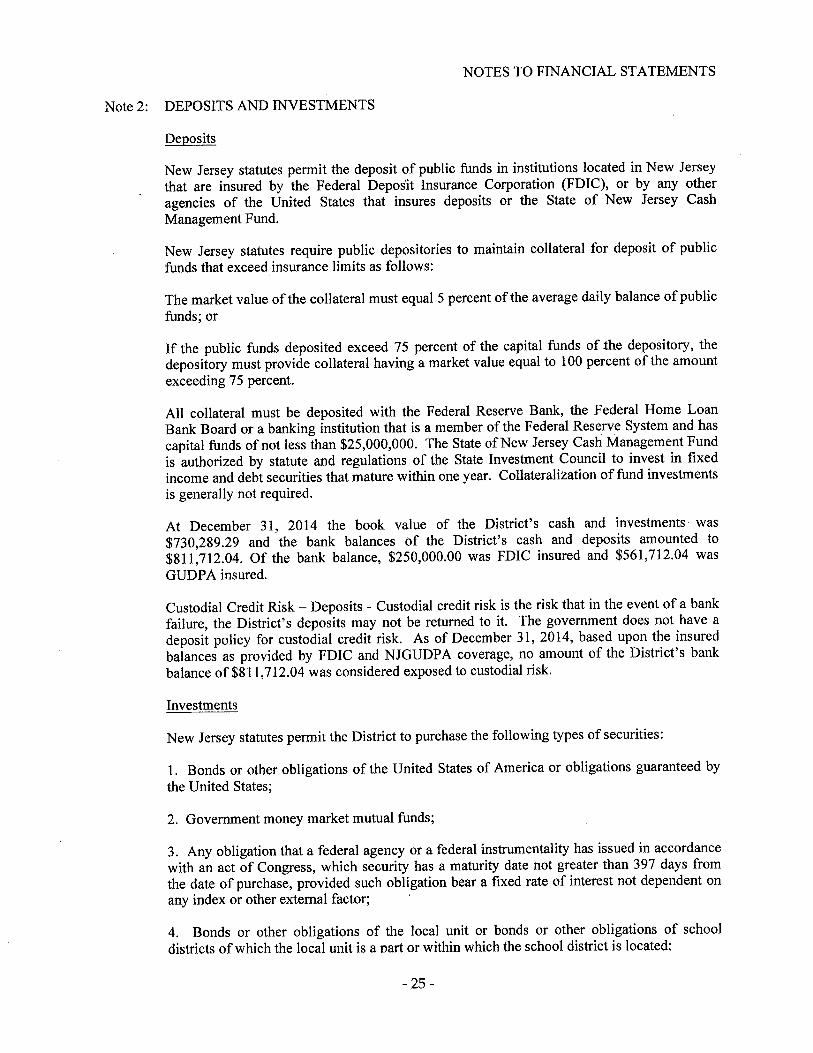

Note 2: DEPOSITS AND INVESTMENTS

Deposits

New Jersey statutes permit the deposit of public funds in institutions located in New Jerseythat are insured by the Federal Deposit Insurance Corporation (FDIC), or by any otheragencies of the United States that insures deposits or the State of New Jersey CashManagement Fund.

New Jersey statutes require public depositories to maintain collateral for deposit of publicfunds that exceed insurance limits as follows:

The market value of the collateral must equal 5 percent of the average daily balance of publicfunds; or

If the public funds deposited exceed 75 percent of the capital funds of the depository, thedepository must provide collateral having a market value equal to 100 percent of the amountexceeding 75 percent.

All collateral must be deposited with the Federal Reserve Bank, the Federal Home LoanBank Board or a banking institution that is a member of the Federal Reserve System and hascapital funds of not less than $25,000,000. The State of New Jersey Cash Management Fundis authorized by statute and regulations of the State Investment Council to invest in fixedincome and debt securities that mature within one year. Collateralization of fund investmentsis generally not required.

At December 31, 2014 the book value of the District's cash and investments was$730,289.29 and the bank balances Of the District's cash and deposits amounted to$811,712.04. Of the bank balance, $250,000.00 was FDIC insured and $561,712.04 wasGUDPA insured.

Custodial Credit Risk - Deposits - Custodial credit risk is the risk that in the event of a bankfailure, the District's deposits may not be returned to it. The government does not have adeposit policy for custodial credit risk. As of December 31, 2014, based upon the insuredbalances as provided by FDIC and NJGUDPA coverage, no amount of the District's bankbalance of$811,712.04 was considered exposed to custodial risk.

Investments

New Jersey statutes permit the District to purchase the following types of securities:

1. Bonds or other obligations of the United States of America or obligations guaranteed bythe United States;

2. Government money market mutual funds;

3. Any obligation that a federal agency or a federal instrumentality has issued in accordancewith an act of Congress, which security has a maturity date not greater than 397 days fromthe date of purchase, provided such obligation bear a fixed rate of interest not dependent onany index or other external factor;

4. Bonds or other obligations of the local unit or bonds or other obligations of schooldistricts of which the local unit is a part or within which the school district is located:

- 25-

NOTES TO FINANCIAL STATEMENTS

Note 2: DEPOSITS AND INVESTMENTS (CONT'D.)

Investments (Cont'd)

5. Bonds or other obligations, having a maturity date of not more than 397 days from thedate of purchase, approved by the Division of Investment in the Department of the Treasuryfor investment by local units;

6. Local government investment pools;

7. Deposits with the State of New Jersey Cash Management Fund established pursuant tosection 1 ofP.L. 1997, c. 281 (C.52: 18A-90.4); or

8. Agreements for the repurchase offully collateralized securities, if:

a. the underlying securities are permitted investments pursuant to paragraphs (1) and (3);

b. the custody of collateral is transferred to a third party;

c. the maturity of the agreement is not more than 30 days;

d. the underlying securities are purchased through a public depository as defined in section 1ofP.L. 1970, c. 236 (C.19:9-41) and for which a master repurchase agreement providing forthe custody and security of collateral is executed.

Note 3: ACCOUNTS RECEIVABLE

At December 31, 2014, the District had an amount due from the Township of Piscataway of$594,637.00. This amount represents the 3rd and 4thquarter taxes. Subsequent to the balancesheet date, the District received these funds from the Township.

Note 4: CAPITAL ASSETS NOTE DISCLOSURE

The following is disclosure of information about capital assets. Capital asset activity for theyear ended December 31,2014 was as follows:

Beginning EndingBalance Additions Retirements Balance

Governmental Activities:Vehicles $3,963,459.00 $45,437.04 $0.00 $4,008,896.04Equipment 438,802.45 0.00 0.00 438,802.45

Totals at Historical Cost 4,402,261.45 45,437.04 0.00 4,447,698.49

Less Accumulated Depreciation For:Vehicles 1,580,562.86 169,211.42 0.00 1,749,774.27Equipment 192,858.55 31,223.05 0.00 224,081.60

Total Accumulated Depr. 1,773,421.41 200,434.46 0.00 1,973,855.86

Government Activities CapitalAssets, Net $2~628~840.04 ($154~997 .42) $0.00 $2~473~842.63

- 26-

NOTES TO FINANCIAL STATEMENTS

Note 5: LONG TERM DEBT

A. Bonds Payable -- Bonds are authorized in accordance with State law by the voters of theDistrict through referendums. All bonds are retired in serial installments within the statutoryperiod of usefulness. Bonds issued by the District are general obligation bonds.

Principal and interest due on bonds outstanding as at December 31, 2014 is as follows:

DATE PRINCIPAL INTEREST TOTAL

2015 $ 130,000.00 $ 31,317.00 $ 161,317.002016 140,000.00 25,740.00 165,740.002017 150,000.00 19,734.00 169,734.002018 150,000.00 13,299.00 163,299.002019 160,000.00 6,864.00 166,864.00

$730,000.00 $96,954.00 $826,954.00

Note 6: LENGTH OF SERVICE AWARD PROGRAM (LOSAP)

The Fire District offers its employees a Length of Service Awards Program (LOSAP) inaccordance with Internal Revenue Code Section 457, which has been approved by theDirector of the Division of Local Government Services. Pursuant to regulation, the financialstatements of the LOSAP Program are subject to an annual independent accountant's review.Accordingly, the LOSAP Program is unaudited. The deferred compensation is not availableto participants until termination, retirement, death or unforeseeable emergency.

All amounts of compensation deferred under the Program and all income attributed to thoseamounts are the exclusive property of the Fire District, subject to the claims of its generalcreditors. Participants' rights under the program are equal to those of a general creditor ofthe Fire District in an amount equal to the fair value of the deferred account for eachparticipant. It is unlikely that the Fire District would use Program assets to satisfy claims ofthe general creditors in the future.

The District has selected Lincoln Financial to administer its LOSAP Program. As ofDecember 31,2014 the District's LOSAP Program had assets of$381,246.30.

Note 7: FUND BALANCE APPROPRIATED

General Fund - Of the $1,066,256.45 General Fund fund balance at December 31, 2014,$216,487.00 has been appropriated and included as anticipated revenue for the year 2015,$479,002.26 is for future capital outlays and $370,767.19 is unassigned.

Capital Projects Fund - Of the $190,882.44 Capital Projects Fund fund balance at December31, 2014, $80,825.92 is designated for the purchase of House 2IBuilding Improvements,$50,000.00 is designated for Building Improvements, $54,562.96 is designated for thepurchase of two utility trucks, and $5,493.56 is designated for the computer project.

- 27-

NOTES TO FINANCIAL STATEMENTS

Note 8: COMMITMENTS AND CONTINGENCIES

The District receives a substantial amount of its support from local and state governments.In the event of significant reductions in the levels of this support, the District's ability toprovide services at current levels may be adversely effected.

Note 9: PENDING LITIGATION

As at the date of this report, the Fire District's legal counsel is unaware of any litigationpending.

Note 10: SUBSEQUENT EVENTS

Reviews of events subsequent to the date of the financial statements and through June 22,2015 indicated no matters for which additional disclosure are required.

- 28-

REQUIRED SUPPLEMENTARY INFORMATION - PART II

- 29-

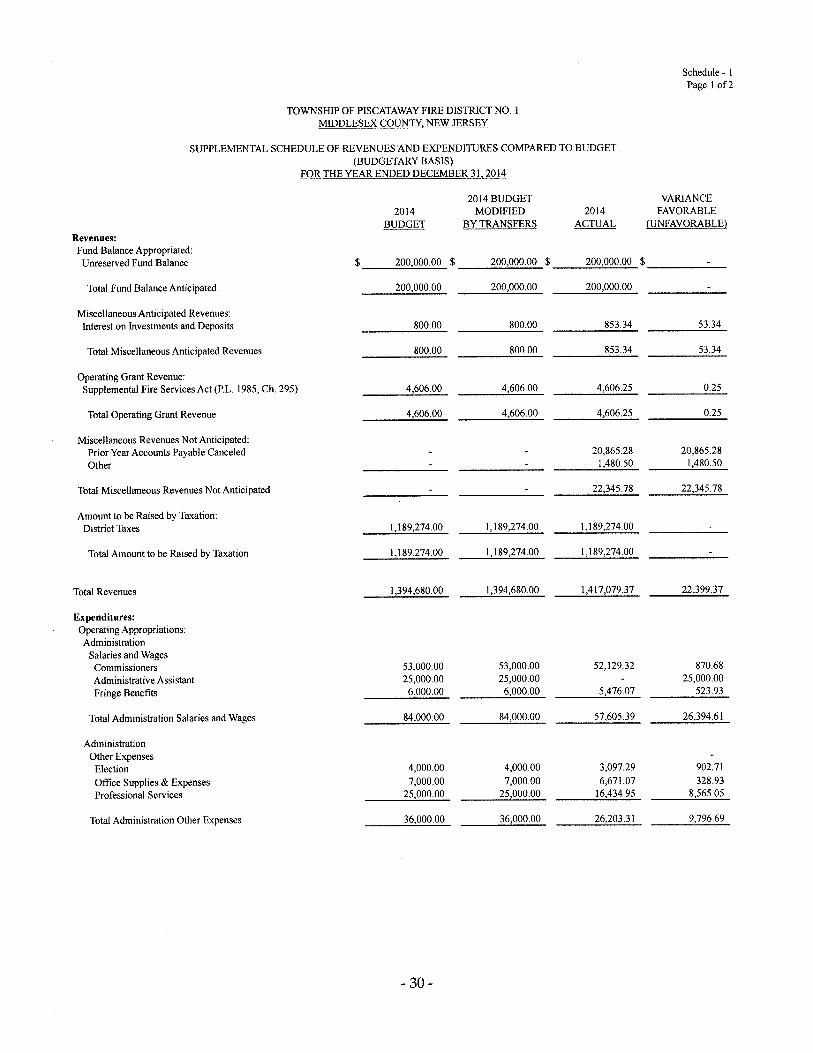

Schedule - 1Page lof2

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, NEW JERSEY

SUPPLEMENTAL SCHEDULE OF REVENUES AND EXPENDITURES COMPARED TO BUDGET(BUDGETARY BASIS)

FOR THE YEAR ENDED DECEMBER 31, 2014

Total Amount to be Raised by Taxation

2014 BUDGET VARIANCE2014 MODIFIED 2014 FAVORABLE

BUDGET BY TRANSFERS ACTUAL (UNFAVORABLE)

$ 200,000.00 $ 200,000.00 $ 200,000.00 $

200,000.00 200,000.00 200,000.00

800.00 800.00 853.34 53.34

800.00 800.00 853.34 53.34

4,606.00 4,606.00 4,606.25 0.25

4,606.00 4,606.00 4,606.25 0.25

20,865.28 20,865.281,480.50 1,480.50

22,345.78 22,345.78

1,189,274.00 1,189,274.00 1,189,274.00

1,189,274.00 1,189,274.00 1,189,274.00

1,394,680.00 1,394,680.00 1,417,079.37 22,399.37

Revenues:Fund Balance Appropriated:Unreserved Fund Balance

Total Fund Balance Anticipated

Miscellaneous Anticipated Revenues:Interest on Investments and Deposits

Total Miscellaneous Anticipated Revenues

Operating Grant Revenue:Supplemental Fire Services Act (P.L. 1985, Ch. 295)

Total Operating Grant Revenue

Miscellaneous Revenues Not Anticipated:Prior Year Accounts Payable CanceledOther

Total Miscellaneous Revenues Not Anticipated

Amount to be Raised by Taxation:District Taxes

Total Revenues

Expenditures:Operating Appropriations:AdministrationSalaries and WagesCommissionersAdministrative AssistantFringe Benefits 5,476.07

870.6825,000.00

523.93

53,000.0025,000.006,000.00

53,000.0025,000.006,000.00

52,129.32

Total Administration Salaries and Wages 84,000.00 84,000.00 57,605.39 26,394.61

AdministrationOther ExpensesElectionOffice Supplies & ExpensesProfessional Services

4,000.007,000.00

25,000.00

4,000.007,000.00

25,000.00

3,097.296,671.0716,434.95

902.71328.93

8,565.05

Total Administration Other Expenses 36,000.00 36,000.00 26,203.31 9,796.69

- 30-

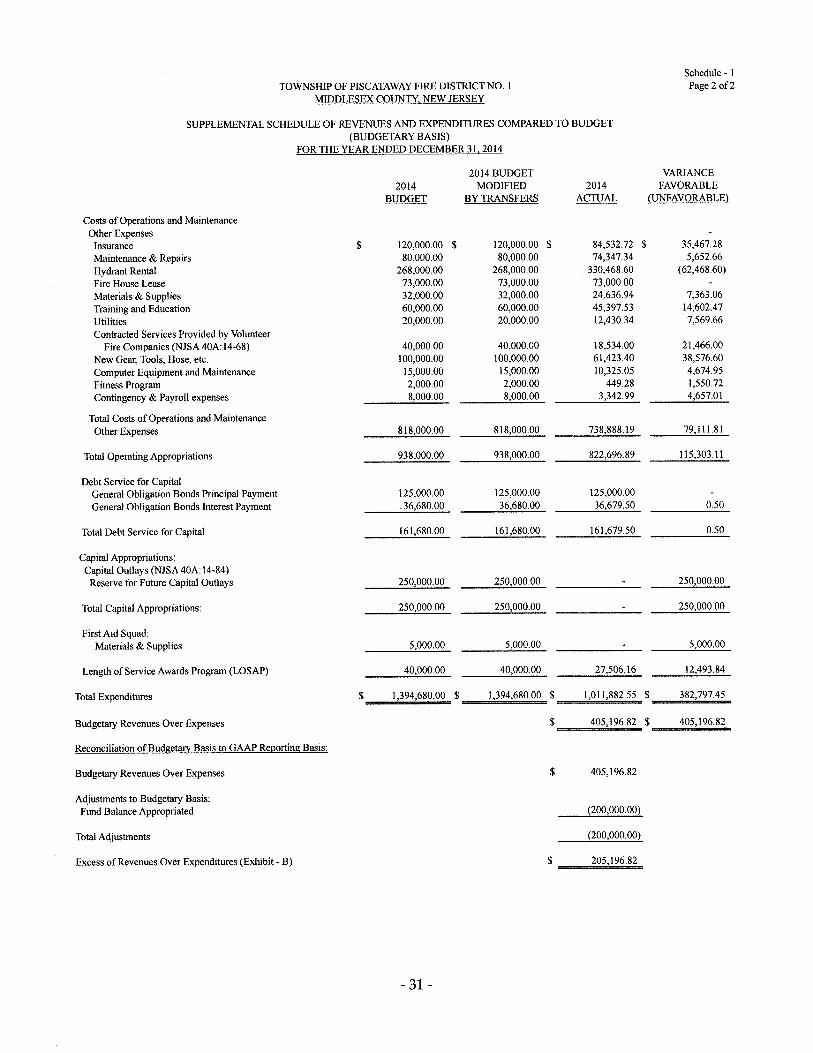

Schedule - 1TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1 Page 2 of2

MIDDLESEX COUNTY, NEW JERSEY

SUPPLEMENTAL SCHEDULE OF REVENUES AND EXPENDITURES COMPARED TO BUDGET(BUDGETARY BASIS)

FOR THE YEAR ENDED DECEMBER 31, 2014

2014 BUDGET VARIANCE2014 MODIFIED 2014 FAVORABLE

BUDGET BY TRANSFERS ACTUAL (UNFAVORABLE)

Costs of Operations and MaintenanceOther ExpensesInsurance $ 120,000.00 $ 120,000.00 $ 84,532.72 $ 35,467.28Maintenance & Repairs 80,000.00 80,000.00 74,347.34 5,652.66Hydrant Rental 268,000.00 268,000.00 330,468.60 (62,468.60)Fire House Lease 73,000.00 73,000.00 73,000.00Materials & Supplies 32,000.00 32,000.00 24,636.94 7,363.06Training and Education 60,000.00 60,000.00 45,397.53 14,602.47Utilities 20,000.00 20,000.00 12,430.34 7,569.66Contracted Services Provided by Volunteer

Fire Companies (NJSA 40A: 14-68) 40,000.00 40,000.00 18,534.00 21,466.00New Gear, Tools, Hose, etc. 100,000.00 100,000.00 61,423.40 38,576.60Computer Equipment and Maintenance 15,000.00 15,000.00 10,325.05 4,674.95Fitness Program 2,000.00 2,000.00 449.28 1,550.72Contingency & Payroll expenses 8,000.00 8,000.00 3,342.99 4,657.01

Total Costs of Operations and MaintenanceOther Expenses 818,000.00 818,000.00 738,888.19 79,111.81

Total Operating Appropriations 938,000.00 938,000.00 822,696.89 115,303.11

Debt Service for CapitalGeneral Obligation Bonds Principal Payment 125,000.00 125,000.00 125,000.00General Obligation Bonds Interest Payment .36,680.00 36,680.00 36,679.50 0.50

Total Debt Service for Capital 161,680.00 161,680.00 161,679.50 0.50

Capital Appropriations:Capital Outlays (NJSA 40A: 14-84)Reserve for Future Capital Outlays 250,000.00 250,000.00 250,000.00

Total Capital Appropriations: 250,000.00 250,000.00 250,000.00

First Aid Squad:Materials & Supplies 5,000.00 5,000.00 5,000.00

Length of Service Awards Program (LOSAP) 40,000.00 40,000.00 27,506.16 12,493.84

Total Expenditures $ 1,394,680.00 $ 1,394,680.00 $ 1,011,882.55 $ 382,797.45

Budgetary Revenues Over Expenses $ 405,196.82 $ 405,196.82

Reconciliation of Budgeta!}, Basis to GAAP ReI10rting Basis:

Budgetary Revenues Over Expenses $ 405,196.82

Adjustments to Budgetary Basis:Fund Balance Appropriated (200,000.00)

Total Adjustments (200,000.00)

Excess of Revenues Over Expenditures (Exhibit - B) $ 205,196.82

- 31-

Schedule - 2

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO. IMIDDLESEX COUNTY, NEW JERSEY

SUPPLEMENTAL COMBINING SCHEDULE OF CAPITAL PROJECTS FUNDREVENUES, EXPENDITURES AND CHANGE IN FUND BALANCE

YEAR ENDED DECEMBER 31, 2014

20132009 2012 Purchase 2013

Computer Building House 2 / Two UtilityProject Improvements Bldg. Improvements Trucks TOTAL

Expenditures:Capital Outlay $ $ $ $ (45,437.04) $ (45,437.04)

Total Expenditures (45,437.04) (45,437.04)

Excess of Revenues Over (Under) Expenditures (45,437.04) (45,437.04)

Fund Balances at Beginning of Year 5,493.56 50,000.00 80,825.92 100,000.00 236,319.48

Fund Balances at End of Year 5,493.56 50,000.00 80,825.92 54,562.96 190,882.44

Analysis of Expenditures - December 31 , 2014

Paid by General Fund (45,437.04) (45,437.04)

Accounts Payable

Total Expenditures (45,437.04) (45,437.04)

- 32-

Schedule 3TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, STATE OF NEW JERSEY

SCHEDULE OF GENERAL OBLIGATION BONDS PAYABLEFOR THE YEAR ENDED DECEMBER 31,2014

Fire District Bonds

AMOUNT OF BALANCE BALANCEDATE OF ORIGINAL MATURITIES MATURITIES INTEREST DECEMBER DECEMBERISSUE ISSUE DATE AMOUNT RATE 31,2013 RETIRED 31,2014

06/30109 $ 1,300,000 08/01115 $ 130,000.00 4.29% $ 855,000.00 $ 125,000.00 $ 730,000.0008/01116 140,000.00 4.29%08/01117 150,000.00 4.29%08/01/18 150,000.00 4.29%08/01119 160,000.00 4.29%

Totals $ 855,000.00 $ 125,000.00 $ 730,000.00

Schedule - 4

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, NEW JERSEY

SUPPLEMENTAL SCHEDULE OF STATISTICAL INFORMATION

Property Tax Levies

The following is a tabulation of District Assessed Valuations, Tax Levies and Property Tax RatesPer $100 of Assessed Valuations for current and the preceding four years:

PropertyTax Rate

Assessed Total Tax Per $100Year Ended Valuations !&YY Assessment

December 31, 2014 $ 2,629,978,073.00 $ 1,189,274.00 0.045 *December 31, 2013 938,652,137.00 1,198,722.00 0.128December 31, 2012 932,721,758.00 1,198,842.00 0.129December 31, 2011 874,290,995.00 1,172,415.00 0.134December 31, 2010 866,739,672.00 1,172,415.00 0.135

* During the fiscal year, the Township of Piscataway performed a revaluation of the township'sassessed property values.

AssignedlUnassigned Fund Balance

The following is a tabulation of District Unreserved Fund Balance at year end and the amountincluded as anticipated revenue in the subsequent year budget for the current and preceding fouryears:

Year Ended

AssignedlUnassignedGeneral

Fund Balance

UtilizedSubsequentBudget

December 31, 2014December 31, 2013December 31, 2012December 31, 2011December 31, 2010

$ 587,254.19672,057.37537,112.34518,369.54554,470.74

$ 216,487.00200,000.00200,000.00194,637.00200,659.00

- 34-

TOWNSHIP OF PISCATAWAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, NEW JERSEY

OFFICIALS IN OFFICE AND SURETY COVERAGEAS AT DECEMBER 31, 2014

The following officials were in office at December 31, 2014:

Board of Fire Commissioners:

John BuchekDavid HospodarNick LombardiArthur HayduckaTimothy Thorn

Other Officials:

Title

PresidentVice PresidentSecretaryTreasurerCommissioner

Richard M. Braslow Esq. Attorney

- 35-

Schedule - 5

TOWNSHIP OF PISCATA WAY FIRE DISTRICT NO.1MIDDLESEX COUNTY, NEW JERSEYYEAR ENDED DECEMBER 31, 2014

GENERAL COMMENTS

An audit of the financial accounts and transactions of the Township of Piscataway Fire DistrictNo.1, Middlesex County, New Jersey, for the year ended December 31, 2014 has beencompleted. The General Comments are herewith set forth:

Scope of Audit

The audit covered the financial transactions of the Township of Piscataway Fire District No.1,Middlesex County, New Jersey.

The audit did not and could not determine the character of services rendered for which paymenthas been made or for which reserves had been set up, nor could it determine the character, properprice or quantity of materials supplied for which claims had been passed. These details werenecessarily covered by the internal review and control before approval of such claims by theGoverning Body. Cash and investment balances were reconciled with independent certificationsobtained directly from the depositories. Revenues and receipts were established and verified as tosource and amount insofar as the records permitted.

INTERNAL CONTROL MATTERS

Control Deficiencies:

Segregation of Duties

Conditions exist whereby the same person may maintain the bookkeeping and cash managementfunction of the District.

This condition is the result of multiple tasks performed by the same individual within the District.

OTHER MATTERS

Contracts and Agreements Required tobe Advertised for N.J.S.A. 40A: 11-4

N.J.S.A. 40A: 11-4 states "Every contract or agreement for the performance of any work or thefurnishing or hiring of any materials or supplies, the cost of the contract price whereof is to bepaid with or out of public funds not included within the terms of Section 3 of this act, shall bemade or awarded only after public advertising for bids and bidding therefore, except as isprovided otherwise in this act or specifically by any other law. No work, materials or suppliesshall be undertaken, acquired or furnished for a sum exceeding in the aggregate of $17,500.00except by contract or agreement."

The Commissioners of the Township of Piscataway Fire District No.1 have the responsibility ofdetermining whether the expenditures in any category will exceed $17,500.00 during the year.Where question arises as to whether any contract or agreement might result in violation of thisstatute, the District Counsel's opinion should be sought before a commitment is made.

- 36-

OTHER MATTERS (cont'd.)

Contracts and Agreements Required tobe Advertised for N .1.S.A. 40A: 11-4 (Cont'd.)

The minutes indicate that bids were requested by public advertising for the following itemstested: District Equipment

Purchases were also made through state approved vendors for various items available which werepermitted under the status.

Inasmuch as the system of records did not provide for an accumulation of payments for categoriesfor the performance of any work or the furnishing or hiring of any materials or supplies, theresults of such an accumulation could not reasonably be ascertained. Disbursements werereviewed, however, to determine whether any clear cut violations existed.

Examination of expenditures revealed no individual payments in excess of $17,500.00 "for theperformance of any work or the furnishing or hiring of any materials or supplies", other thanthose where bids had been previously sought by public advertisement.

The minutes also indicated that resolutions were adopted and advertised authorizing the awardingof contracts or agreements for "Professional Services" per N .1.S.A. 40A: 11-5.

Any interpretation as to possible violation of N.1.S.A. 40A:11 and N.1.A.C. 5:30-14 would be inthe province of the General Counsel.

We suggest that the District review the amendments to the Local Public Contracts Law anddetermine the impact of the comprehensive amendments with regard to the District, including ananalysis of the effect of requiring the position of a "Qualified Purchasing Agent" on a cost benefitbasis or alternate approach.

Payment of Claims

Claims were examined on a test basis for the year under review and they were found to be ingood order. Compliance to certification of availability of funds was reviewed and found to begood condition for items tested.

Condition of Records - Treasurer

The financial records maintained by the Treasurer were found to be in good condition. During2014, a computerized Budget Revenue and Appropriation Ledger was maintained and was foundto be in good condition, with only minor adjustments necessary to reflect audited amounts at yearend.

- 37-

OTHER MATTERS (cont'd.)

Insurance Coverage

Insurance policies in force are on file at the Fire District office. No attempt was made todetermine the adequacy of coverage as part of this report. Adequacy of coverage is theresponsibility of the District.

Compliance with New Jersey Administration Codes

The Local Finance Board, State of New Jersey, adopted the following requirements, previouslyidentified as "technical accounting directives", as codified in the New Jersey administrationCode, as follows:

NJ.A.C. 5:30 - 5.2 - Encumbrance Accounting: This directive requires the development andimplementation of accounting systems, which can reflect the commitment of funds at the point ofcommitment. Our examination indicated that the encumbrance system utilized by the Districtwas operational to the extent necessary to assure effective budgetary control and accountability.

N J .A.C. 5:30 - 5.6 - Fixed Asset Accounting: This directive requires the development andimplementation of accounting systems which assign values to covered assets and can trackadditions, retirements and transfers of inventoried assets. As noted in previous reports, theDistrict is in partial compliance with this directive. Our examination indicated that the Districthas established a fixed asset inventory system and takes a physical inventory on an annual basis.However, the current system does not provide a detailed cost basis allocation for all inventorieditems. Accordingly, the District should develop a costing system for all of its inventoried fixedassets.

NJ.A.C. 5:30 - 5.7 - General Ledger Accounting System: This directive requires theestablishment and maintenance of a general ledger for, at least, the General Fund. The District isin compliance with this directive.

It is suggested that the District comply with NJ.A.C. 5:30 - 5.6 issued by the Division of LocalGovernment Services, Department of Community Affairs, State of New Jersey, in all respects.

- 38-

RECOMMENDATIONS

None

**********

ACKNOWLEDGMENT

During the course of our engagement we received the complete cooperation of the variousofficials and employees of the District, and the courtesies extended to us were greatlyappreciated.

Very truly yours,

HODULIK & MORRISON, P.A.

Andrew G. Hodulik, CPA, RMANo. 406

- 39-