Tourism Destination Plan 2018-2023 - Lockyer Valley Region · Tourism Destination Plan (the Plan)...

81

Lockyer Valley Tourism Destination Plan 2018 – 2023 July 2018

Transcript of Tourism Destination Plan 2018-2023 - Lockyer Valley Region · Tourism Destination Plan (the Plan)...

Lockyer Valley Tourism Destination Plan 2018 – 2023

July 2018

Prepared For Lockyer Valley Regional Council | July 2018

EXECUTIVE SUMMARY ............................................................................................... 1

1.1. Introduction ........................................................................................................................................................... 1 1.2. Visitor Economy Analysis ................................................................................................................................... 1 1.3. Barriers to Address to Activate the Visitor Economy ................................................................................ 3 1.4. The Destination Vision ....................................................................................................................................... 4 1.5. Opportunities to Activate the Visitor Economy .......................................................................................... 5 1.6. Target Markets to Focus On ............................................................................................................................. 6 1.7. Summary................................................................................................................................................................ 7

SITUATION ANALYSIS ............................................................................................... 9

2.1. Methodology ........................................................................................................................................................ 9 2.2. The Lockyer Valley ............................................................................................................................................. 9 2.3. SWOT Analysis.................................................................................................................................................... 15

VISITOR ECONOMY SNAPSHOT ............................................................................. 17

3.1. Total Visitation .................................................................................................................................................... 17 3.2. Visitor Nights ....................................................................................................................................................... 18 3.3. Average Length of Stay ....................................................................................................................................19 3.4. Visitor Spend .......................................................................................................................................................19 3.5. Purpose of Visit................................................................................................................................................. 20

PRODUCT AUDIT ....................................................................................................... 22

4.1. Accommodation ................................................................................................................................................ 22 4.2. Attractions .......................................................................................................................................................... 23 4.3. Markets ................................................................................................................................................................ 24 4.4. Food and Beverage .......................................................................................................................................... 24 4.5. Events & Festivals ............................................................................................................................................. 25

BARRIERS TO ADDRESS .......................................................................................... 27

5.1. Product and Supporting Infrastructure ........................................................................................................ 27 5.2. Marketing and Destination Awareness ........................................................................................................ 30 5.3. Tourism Governance......................................................................................................................................... 32

ACTIVATING THE VISITOR ECONOMY .................................................................. 35

6.1. The Destination Vision ..................................................................................................................................... 35 6.2. The opportunities for activation .................................................................................................................... 36 6.3. Target Markets .................................................................................................................................................... 51

ACTION PLAN ........................................................................................................... 59

7.1. Overview ............................................................................................................................................................. 59 7.2. Activation Areas and Associated Actions .................................................................................................. 60

SUPPORTING DOCUMENTATION ...........................................................................67

Figure 1: The Lockyer Valley’s Visitor Economy ...................................................................................................................... 2

Figure 2: Barriers to address to activate the visitor economy .......................................................................................... 3

Figure 3: The destination vision ...................................................................................................................................................... 4

Figure 4: Activation opportunities ................................................................................................................................................ 5

Figure 5: Lockyer Valley visitor target markets ....................................................................................................................... 6

Figure 6: Map of the Lockyer Valley ........................................................................................................................................... 10

Figure 7: Lockyer Valley Population Growth (2007-2016) ................................................................................................. 11

Figure 8: Lockyer Valley Population Forecasts to 2036 ..................................................................................................... 12

Figure 9: Change in Age Structure, Lockyer Valley Population (2011 to 2016)......................................................... 13

Figure 10: Visitation to Lockyer Valley (based on 3-year averages from 2009-2017) .......................................... 17

Figure 11: Visitor Nights in Lockyer Valley (based on 3-year averages from 2009-2017) .................................... 18

Figure 12: Average Length of Stay in Lockyer Valley (based on 3-year averages from 2009-2017) .............. 19

Figure 13: Purpose of Visit to Lockyer Valley, by Visitor Type (based on 3-year average to 2017) .............. 20

Figure 14: Share of Accommodation Type ............................................................................................................................... 23

Figure 15: Share of Attractions Product Type ........................................................................................................................ 23

Figure 16: Share of Food and Beverage Type ........................................................................................................................ 24

Figure 17: Visitation to Gatton VIC .............................................................................................................................................. 32

Figure 18: The destination vision and activation areas ....................................................................................................... 35

Figure 19: Traditional caravan park examples ........................................................................................................................ 37

Figure 20: Destination holiday park examples ....................................................................................................................... 38

Figure 21: Positioning Strategies, Key Towns in the Lockyer Valley .............................................................................. 41

Figure 22: Potential Tourism Precinct (Plainland and Laidley) ....................................................................................... 43

Figure 23: Market readiness stages ............................................................................................................................................ 49

Figure 24: Lockyer Valley visitor target markets ................................................................................................................... 51

Table 1: Population of Major Towns within the Lockyer Valley ......................................................................................... 11

Table 2: Median Age of Lockyer Valley (2006 to 2016) ...................................................................................................... 13

Table 3: Lockyer Valley SWOT Analysis .................................................................................................................................... 15

Table 4: Visitor Spend in the Lockyer Valley ........................................................................................................................... 19

Table 5: Accommodation Audit Summary ............................................................................................................................... 23

Table 6: Attractions Audit Summary .......................................................................................................................................... 23

Table 7: Lockyer Valley Markets Audit ...................................................................................................................................... 24

Table 8: Food and Beverage Audit Summary......................................................................................................................... 24

Table 9: Events and Festivals Audit Summary ....................................................................................................................... 25

Table 10: Lockyer Valley 2018 Events & Festivals Calendar ............................................................................................. 25

Table 11: Actions to strengthen tourism governance .......................................................................................................... 49

Table 12: Activation Area 1: Accommodation, Experiences and Infrastructure Development ......................... 60

Table 13: Activation Area 2: Destination Awareness, Branding and Visitor Services ............................................ 62

Table 14: Activation Area 3: Events Diversification and Development ....................................................................... 64

Table 15: Activation Area 4: Governance, Collaboration and Support ........................................................................ 65

Table 16: Previous actions listed in the 2013 Tourism Destination Plan ...................................................................... 68

Table 17: Lockyer Valley Accommodation Audit ................................................................................................................... 72

Table 18: Lockyer Valley Markets Audit ..................................................................................................................................... 73

Table 19: Lockyer Valley Attractions Audit .............................................................................................................................. 74

Table 20: Lockyer Valley Food & Beverage Audit ................................................................................................................ 75

Table 21: Illustrative List of Government and Non-Government Assistance Resources....................................... 76

1

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Executive Summary

1.1. Introduction

Stafford Strategy1 (Stafford) was commissioned by Lockyer Valley Regional Council (Council) to complete a

Tourism Destination Plan (the Plan) for the Lockyer Valley, covering the period 2018-2023. The purpose of the Plan

is to:

▪ recognise the key outcomes from the earlier 2013 Tourism Destination Plan, including the development and

investment opportunities that have been realised (and those that are ongoing or yet to be achieved);

▪ review and update the suggested strategies and opportunities, at the 5-year mark of the 2013 Plan;

▪ update the understanding of the Lockyer Valley visitor economy;

▪ determine the priority areas for tourism growth;

▪ define the differentiated destination experience or proposition to appeal to target markets; and

▪ provide high-level, updated, recommendations/actions with regards to the positioning of Lockyer Valley

Tourism and opportunities for growth.

This is part of a suite of strategies and plans being developed and updated from the 2013 versions, including the

Economic Development Plan, inclusive of a Regional Food Sector Strategy. As such, there is some deliberate and

strategic overlap, although effort has been made to avoid duplication.

This report also aligns to Councils Corporate Plan 2017-2022 which sets out Councils vision for the region. This Plan

also aligns with Councils corporate goals of:

▪ Lockyer Business – our business community is a thriving and inclusive network where it is easy to do business.

We create opportunities and encourage innovation that inspires business confidence and collaborative

partnerships.

▪ Lockyer Farming – as custodians we manage our water and land assets to ensure our farming future. We pride

ourselves on our innovation and clean, green reputation. We work together to support our farmers of current

and future generations.

▪ Lockyer Livelihood – we are a community where lifelong learning opportunities exist. Our quality education

facilities are highly regarded and provide diverse career pathways. We look to develop skills and generate job

opportunities for all.

1.2. Visitor Economy Analysis

Figure 1 on the following page provides a graphical summary of the Lockyer Valley’s visitor economy. Importantly,

it demonstrates that while visitation to the LGA has been growing, a large proportion of the visitor market (69%)

are domestic day trippers. While the domestic day tripper market is an important sector, visitor spend data

demonstrates that the domestic and international overnight visitor markets are far higher yielding. By way of

1 Formerly The Stafford Group prior to December 2017

2

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

example, while domestic overnight visitors represented only 26% of the total visitor market in terms of visitation,

this market generated 61% of total visitor spend.

This Plan, therefore, deliberately focuses on initiatives to increase overnight visitation to the Lockyer Valley and to

grow the average length of stay as these will deliver far higher economic benefits including local jobs and

investment.

Figure 1: The Lockyer Valley’s Visitor Economy2

2 International Visitor Survey and National Visitor Survey, Tourism Research Australia, 2017

3

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

1.3. Barriers to Address to Activate the Visitor Economy

The following categorises the key elements of the Lockyer Valley visitor economy, identifying areas of improvement

and potential to stimulate industry growth.

Figure 2: Barriers to address to activate the visitor economy

Accommodation quality - Actively encouraging existing accommodation providers to enhance and refresh

facilities to meet an increasingly discerning market and to encourage longer length of visitor stay.

Accommodation supply – Diversification of the accommodation mix, including a new destination holiday

park opportunity.

Coordination of events - A more coordinated tourism events strategy is necessary to avoid congestion and

conflicting events and ensure each event can maximise economic and social benefit for the region, including

residents and visitors.

Commissionable product to leverage regional strengths - Investigate creating additional commissionable

tourism product through leveraging off its USPs (agricultural production, farm gates, natural environment

etc.) to increase the marketability of the area and to grow average length of visitor stay.

Experiences for the working holiday market – The Lockyer’s working holiday visitors often travel out of the

LGA for recreational experiences. There is a need to introduce product which is packaged for this market

to encourage them to recreate in the Lockyer Valley.

Family-friendly product – While the Lockyer has a range of natural recreational experiences, these are not

always suitable for the family market with children under 10 years of age. There is a need to investigate the

introduction of experiences for younger children – for locals and visitors alike.

Interpretation and directional signage – The potential exists to introduce directional and interpretive

signage to: showcase the Lockyer’s attractions (natural and built); encourage dispersal throughout the LGA;

and to explain the Lockyer Valley’s history.

Majority of operators are small businesses – While this brings a boutique nature and a personalised

experience, a balance is required as larger operators often bring with them larger marketing budgets which

not only markets their product but also the region.

Town centre activation - The various town centres throughout the Lockyer Valley play an important role

in encouraging longer length of visitor stay and higher spend. Every effort should be made to enhance

streetscapes and town attractiveness to generate greater visitor appeal.

Brand awareness - The Lockyer Valley tourism brand (Luvya Lockyer) could be further developed to help

position the region as an attractive visitor destination. Successful messaging and branding would help

generate awareness of the unique selling points of the region (i.e. contribution to agricultural production).

Digital savviness of operators - While there are some operators in the Lockyer Valley who have an up-to-

date digital presence, there are some who lack the tools for developing this. There is a need to ensure that

all tourism operators in the Lockyer Valley are listed on the Australian Tourism Data Warehouse.

Product packaging - As additional new, marketable product is introduced, there is a need to develop

packages which visitors can book, rather than providing suggested itineraries. Packages could include

accommodation, transport, guided walks/cycling, food and beverage etc.

Visitor information services – The nature of visitor information services is changing; the challenge is how

to best utilise visitor services so that they best meet the needs of a changing visitor market and attract

more overnight visitors to the Lockyer Valley. There is a need to investigate additional ways of providing

visitor information, including more digitally accessible information.

Strengthening the LTO - With improvements to its tourism structure, as well as clearly defined roles and

responsibilities, the local tourism association can improve its operations and better support the Lockyer

Valley visitor economy. The local tourism association could also improve its effectiveness through

increasing collaborations and formal partnerships with Brisbane Marketing as well as neighbouring tourism

organisations. There is a need to encourage members to collect and provide data on visitor profiles to

better inform tourism statistics.

PRODUCT & SUPPORTING INFRASTRUCTURE

MARKETING & DESTINATION AWARENESS

TOURISM GOVERNANCE

4

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

1.4. The Destination Vision

To guide the development of the Lockyer Valley as a destination, and to strengthen the visitor economy, it is

essential that a destination vision is created which industry buys into and supports. The destination vision proposed

is outlined in Figure 3 below, along with four activation areas to achieve the vision. The opportunities summarised

in section 1.5 are categorised under these activation areas.

Figure 3: The destination vision

5

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

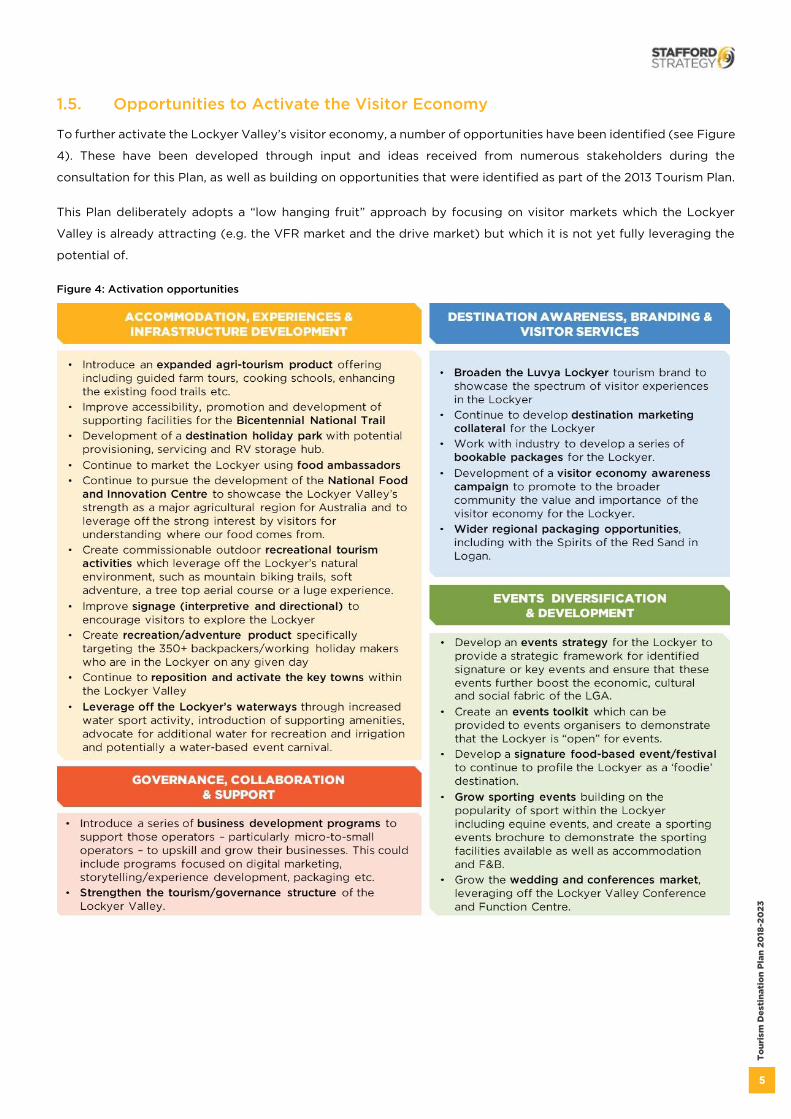

1.5. Opportunities to Activate the Visitor Economy

To further activate the Lockyer Valley’s visitor economy, a number of opportunities have been identified (see Figure

4). These have been developed through input and ideas received from numerous stakeholders during the

consultation for this Plan, as well as building on opportunities that were identified as part of the 2013 Tourism Plan.

This Plan deliberately adopts a “low hanging fruit” approach by focusing on visitor markets which the Lockyer

Valley is already attracting (e.g. the VFR market and the drive market) but which it is not yet fully leveraging the

potential of.

Figure 4: Activation opportunities

6

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

1.6. Target Markets to Focus On

Figure 5 outlines six target markets which the Lockyer Valley should focus on to sustainably grow its visitor

economy. The target markets have been identified because they either: align with the Lockyer’s existing key assets

and strengths; align with the opportunities identified in this Plan; or reflect the markets already being captured by

Lockyer. Over time, and as the Lockyer Valley continues to develop as a destination, the opportunity may exist to

refine these target markets into primary and secondary markets to achieve greater focus.

Figure 5: Lockyer Valley visitor target markets3

3 These visitor segments are based on visitor activity categories provided by Tourism Research Australia, as well as Queensland’s Exper ience Framework provided by Tourism and Events Queensland. Each of the visitor segments are based on areas of interest, demographics and purpose of trip.

7

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

1.7. Summary

The Lockyer Valley is a relatively youthful tourism destination, advantageously situated within close proximity to a

number of destinations with large visitor markets. The opportunities identified in this Plan focus in on selective

product areas – such as agri-tourism, sports-based tourism activity and nature-based recreational tourism, rather

than replicating what is available in surrounding areas.

Activating many of the opportunities identified, and, shifting the Lockyer Valley’s position from being a day trip

destination (currently 69% of visitors are day trippers) to an overnight one, hinges on the development of new

visitor attractions and experiences as well as accommodation. Importantly, it is considered that the development

of such product will not ‘cannibalise’ market share from existing operators, but rather, will “grow the pie” by

enabling the Lockyer Valley to attract a more diverse visitor and higher yielding visitor market.

Achieving the goals of this Plan will require the active participation of a range of stakeholders, including Council,

industry and State Government. There is a need for greater stakeholder collaboration and participation if the visitor

economy is going to be further activated in the Lockyer Valley.

The number of opportunities identified in this Plan has deliberately been kept focused, rather than creating a “wish

list”; a sustainable level of activity is seen as the key, rather than trying to attempt too much with too few (current)

industry players and limited resourcing. Often the temptation is to try and take on too much, too quickly and as a

result, resources are often spread far too thinly to achieve desired results.

In summary, the visitor economy for the Lockyer Valley has the potential to grow significantly in the short to

medium term, especially if a number of major economic development projects get activated. Having the facilities

and products to better meet current and future visitor markets needs is the imperative.

8

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

9

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Situation Analysis

This section provides a summary of the methodology to complete the project, as well as a comprehensive overview

of the Lockyer Valley, including historic and projected population, as well as the demographic profile of the region.

This helps set the context for the Plan and, when combined with an examination of the visitor market, ensures the

development of recommendations are tailored to the specific needs of the community.4

2.1. Methodology

The methodology adopted for this Plan has included the following:

▪ consultation with key personnel, including Councillors, Council staff and industry stakeholders (including local

businesses, growers and developers);

▪ a site visit to the Lockyer Valley, including key towns and landmarks;

▪ a thorough assessment of the 2013 Tourism Destination Plan developed by Stafford;

▪ a review of relevant strategies and policies to build the context for the updated Plan;

▪ a review of demographic and visitor data;

▪ examination of visitor segmentation, target markets and forecasting visitor growth;

▪ identification of key strengths, opportunities and priorities for tourism growth;

▪ development of an Action Plan and recommendations, including an update to the 2013 Plan;

▪ preparation of the draft Plan and presenting interim recommendations and findings to Council; and

▪ finalisation of the Tourism Destination Plan.

2.2. The Lockyer Valley

The Lockyer Valley Local Government Area (LGA) is located in South East Queensland (SEQ), around one hour’s

drive – or 70km – to the west of Brisbane (along the Western Growth Corridor) and borders Toowoomba to the

east. It is easily accessible by car, via the Warrego Highway, which runs in an east-west direction through the LGA

and provides vehicle access from Toowoomba to the coast.

The LGA covers approximately 2,200km2. It is primarily an agricultural region and recognised as one of the “top

ten most fertile farming areas in the world”5. Most of the land is rich agricultural farmland, which is heavily cultivated

to produce “the most diverse commercial range of vegetables and fruit of any area in Australia”. As such, the region

is often referred to as “Australia’s salad bowl” and comprises 12-14% of the Queensland agricultural economy.6

There are several main towns and hubs across the LGA, most of which border the Warrego Highway (the A2). While

the largest town is Gatton, located in the centre of the Region, other centres include Laidley, Withcott, Plainland,

Hatton Vale, Helidon, Forest Hill, Grantham and Murphys Creek. Figure 6 illustrates these towns and proximity to

the highway.

4 Please note a more detailed economic profile is included in the update to the Lockyer Valley Economic Development Plan. 5 http://lockyervalleygrowers.com.au/ 6 Ibid

10

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Figure 6: Map of the Lockyer Valley

11

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

2.2.1. Population

2.2.1.1. Historic Population Growth

As demonstrated in Figure 7, the population of the Lockyer Valley was 39.5k in 2016. Over the last ten years, the

Lockyer’s population has increased by 23% (7.4k residents), which exceeds the total state average growth of 21%,

as well as the Brisbane growth rate of 20%.

The population of SEQ has also experienced significant growth over the past decade which is important to note

given the potential for the Lockyer Valley to leverage off a growing domestic visitor market of over 3 million people

situated within 1 to 1.5 hours’ drive of Lockyer Valley.

Figure 7: Lockyer Valley Population Growth (2007-2016)7

Table 1 shows the concentration spread of residents across the LGA’s major town centres. The largest concentration

of residents is in Gatton (18%), which serves as the Lockyer Valley’s ‘hub’, followed by Laidley (10%). The remainder

of the population is reasonably dispersed, due to the spread of farms across the LGA; while the remaining Lockyer

Valley residents reside in smaller townships across the LGA.

Table 1: Population of Major Towns within the Lockyer Valley8

Town Population (2016) Percentage of Lockyer

Valley Population

Gatton 7,101 18%

Laidley 3,808 10%

Withcott 1,844 5%

Plainland 1,596 4%

Hatton Vale 1,521 4%

Helidon 1,059 3%

Forest Hill 968 2%

Grantham 634 2%

Murphys Creek 629 2%

Total 19,160 50%

7 http://profile.id.com.au/lockyer-valley/population-estimate 8 Australian Bureau of Statistics Census Data 2016

32.1k33.0k

34.3k35.1k

35.9k36.5k

37.7k38.4k 38.9k

39.5k

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

23% (7.4k residents)

12

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

2.2.1.2. Population Forecasts

Figure 8 shows the Queensland Government’s projected population growth of the region to 2036, which provides

the following results:

▪ using a ‘low series’ growth scenario, at an average annual growth rate (AAGR) of 1.6%, the population could

grow to 53k (a 33% increase) by 2036.

▪ using a ‘medium series’ growth scenario, at an AAGR of 2.1%, the population could grow to 57k (a 45% increase)

by 2036.

▪ using a ‘high series’ growth scenario, at an AAGR of 2.7%, the population could grow to 62k (a 57% increase)

by 2036.

With population growth, there will be a commensurate increase in demand for services, jobs and supporting

infrastructure along with a variety of leisure and entertainment amenities.

Figure 8: Lockyer Valley Population Forecasts to 20369

9 Queensland Government population projections, 2015 edition; Australian Bureau of Statistics, Regional population growth, Australia, 2013-14

39k

43k

46k

49k

53k

39k

44k

48k

53k

57k

39k

45k

50k

56k

62k

2016 2021 2026 2031 2036

Low Series Medium Series High Series

13

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

2.2.2. Age

As demonstrated in Table 2, the median age of Lockyer Valley residents is 39, while the Queensland average is 37.

Between 2006 and 2016, the median age of the Lockyer Valley increased at a faster rate than the Queensland

average, growing by 1.4 years compared to 1 year.

Table 2: Median Age of Lockyer Valley (2006 to 2016)10

Area 2006 2011 2016

Lockyer Valley 37.6 37.4 39.0

Queensland 36.0 36.6 37.0

Figure 9 demonstrates that the Lockyer Valley, like most other regional areas, has an ageing population; between

2011 and 2016, the number of residents under the age of 17 remained relatively constant, while the number of

residents aged over 50 increased by more than 20%.

This is an important factor for the growth of the visitor economy, as younger people (i.e. those under 35) often

make up a high percentage of the tourism workforce (being in pubs and clubs, hotels and motels, cafes and

restaurants, tour operating and guiding etc.). With the Lockyer Valley’s desire to grow its visitor economy, there is

a need to ensure a ready workforce is available to fill job vacancies. To encourage young people to live (or stay) in

the Lockyer necessitates not only providing jobs but also improving the range of recreational and leisure-based

activities, food and beverage offer and other experiences.

Figure 9: Change in Age Structure, Lockyer Valley Population (2011 to 2016)11

10 Australian Bureau of Statistics, Population by Age and Sex, Regions of Australia 2016 11 http://profile.id.com.au/lockyer-valley/service-age-groups

2.4k

3.6k

3.3k

3.2k

3.9k

7.1k

4.6k

3.9k

2.5k

0.5k

2.3k

3.6k

3.2k

3.7k

4.7k

7.3k

5.2k

4.6k

3.4k

0.6k

Babies and pre-schoolers (0 to 4)

Primary schoolers (5 to 11)

Secondary schoolers (12 to 17)

Tertiary education and independence (18 to 24)

Young workforce (25 to 34)

Parents and homebuilders (35 to 49)

Older workers and pre-retirees (50 to 59)

Empty nesters and retirees (60 to 69)

Seniors (70 to 84)

Elderly aged (85 and over)

2011 2016 (and % change from 2011 - 2016)

(+28%)

(+35%)

(+17%)

(+14%)

(+2%)

(+20%)

(+15%)

(-1%)

(+0.4%)

(-4%)

14

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

2.2.3. Community Expectations

Continuing the trend in the 2013 Plan, with a growing and aging population, there will be increasing pressure on

public resources, as well as a need to engage young people and young families to keep them within the region.

Strategies recommended in this updated Plan are made with these needs and community expectations in mind.

2.2.4. Stakeholder Consultation

Consultation with key community stakeholders, including Council, local chambers of commerce, local businesses,

developers and the agricultural industry, revealed the following information relating to tourism strengths,

opportunities and priorities.

▪ The region should use its strength in the agricultural sector by focusing on agri-tourism opportunities to

increase visitation, particularly overnight stays.

▪ A greater range of tourism products and services are required, particularly consumer-focused food related

experiences that leverage off the agricultural industry (e.g. food trails, farm gates, cooking schools etc.).

▪ There should be more opportunities for local businesses to partner with, and support, festivals and events, in

order to maximise opportunities for growth.

▪ The main towns in the area should be better positioned and marketed, each with a clear focus on how it can

support visitors and contribute to the visitor economy. This could include theming/branding local towns to

enhance the look and feel of the towns.

▪ There is strength in clustering various tourism products (attractions and experiences) which could be

incorporated in one of the main town centres, such as Gatton, Plainland or Laidley, to create a hub or precinct.

▪ Retail trading hours should ideally expand into the evening/night-time, as well as over weekends. However,

there are challenges in achieving this due to perceived limited consumer demand and often higher operating

costs associated with weekend wage rates etc.

▪ Council, the Chambers of Commerce and the LTO should proactively work together in establishing and

promoting tourism activities.

▪ Additional recreational activities and experiences should be developed, particularly outdoor and water-based

activities, utilising the natural assets of the region.

15

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

2.3. SWOT Analysis

Table 3 synthesises the visitor market analysis and provides a SWOT analysis for the Lockyer’s visitor economy.

Table 3: Lockyer Valley SWOT Analysis12

▪ Proximity to major population centres across SEQ,

including Brisbane, Gold Coast, Toowoomba and Ipswich

▪ Accessibility to surrounding areas via the Warrego Highway

▪ The farming and agricultural sector (“Australia’s salad bowl”)

▪ The prevalence of national parks and outdoor recreation activities (bird watching, bushwalking, horse riding)

▪ Produce market offering locally made and locally sourced food

▪ Providence of food story ▪ The ability to attract short-term international farm

workers

▪ Improvements and upgrades needed to accommodation facilities

▪ Night time economy activation ▪ Improvements needed to activate key towns and

improve their vibrancy ▪ Community ambivalance of the visitor economy ▪ Limited commissionable product to complement

outdoor recreation activities ▪ Strong community events program but limited

destination/signature events ▪ Other industry sectors need to grow in order to

compete with agriculture

▪ Develop agri-tourism opportunities to leverage off and complement the dominant agricultural sector including high-quality food experiences, including food trails, cooking schools and paddock to plate experiences

▪ The tourism destination brand (Luvya Lockyer) can be broadened and further developed

▪ Develop a signature destination event with a broad regional focus

▪ Foster partnerships between local cafés/restaurants and farms to promote locally made/branded produce

▪ Leverage off support from neighbouring RTOs and tourism associations

▪ Development of high-quality holiday destination park to capture the family market

▪ Package product, including accommodation, F&B and experiences to target the short break market

▪ The Toowoomba Second Range Crossing, which bypasses central Toowoomba, could draw additional road traffic (and day visitors) to Lockyer Valley

▪ Leverage off the Lockyer’s waterways to stimulate growth in water sport activity

▪ Continue to promote the Lockyer as a ‘foodie’ destination

▪ Run a visitor economy awareness campaign to increase the support and pride in local tourism

▪ Run business support programs to increase the skill base of tourism operators (including in the digital/web space as well as marketing)

▪ Continue to grow the wedding and conferences market leveraging off the Lockyer Valley Conference and Function Centre

▪ Unforeseen environmental/weather-related disasters that impact the agricultural sector

▪ Greater investment in existing and new accommodation stock is needed to stimulate overnight visitation

▪ Inability to invest in, or activate, the town centres could drive residents and visitors away from the Lockyer Valley towards neighbouring population centres (Toowoomba, Ipswich, etc.)

▪ Delays in any of the major regional State Government projects could stagnate economic growth and negatively impact the tourism industry

▪ Farmers and local businesses fail to understand the importance of contributing to the visitor economy

▪ More product needs to be developed to support growth

12 Some of this information also builds on the SWOT analysis undertaken in the 2013 Plan.

OPPORTUNITIES THREATS

STRENGTHS WEAKNESSES

16

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

17

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Visitor Economy Snapshot

This section provides a comprehensive examination of the visitor economy, including historic trends, the current

state of play and future projections. The analysis covers both market demand and supply to:

▪ identify the target visitor markets for the region;

▪ assess the gaps (and opportunities) in tourism-related product and infrastructure; and

▪ determine the priority areas for tourism growth.

3.1. Total Visitation

Visitor data for the Lockyer Valley has been based on the International Visitor Survey (IVS) and National Visitor

Survey (NVS) which are undertaken by Tourism Research Australia (TRA)13. Because of sample size challenges

when assessing visitor data at a local government area level, three-year averages have been utilised14.

Figure 10 demonstrates that the Lockyer Valley received 347k visitors per annum in 201715. While this is up 37%

from 254k visitors in 201116, it is lower than the average visitation per annum achieved over the period 2012-2014

(445k visitors). This may be due to various natural events such as floods etc. which has taken the Lockyer time to

recover and change market perceptions that the area was not fully open for business and visitation.

The vast majority of visitors to the Lockyer Valley are domestic day trippers (which typically includes visitors from

within a two-hour drive of the area from Toowoomba, Ipswich, Brisbane and other parts of Southern Queensland),

comprising 72% of visitation (from 2015-2017), followed by domestic overnight visitors (26% of total visitation). The

international market to the Lockyer Valley currently represents a fairly small share (2%) of visitation.

Figure 10: Visitation to Lockyer Valley (based on 3-year averages from 2009-2017)17

13 Lockyer Valley visitor data was calculated by amalgamating the ‘Statistical Area (SA) Level 2’ ABS geographic data that falls within the LGA boundaries. This includes the following SA2 areas: Gatton, Lockyer Valley – West and Lockyer Valley – East 14 This is consistent with the methodology applied by TEQ, as well as other state tourism agencies nationally, for local government area visitor data. 15 Based on average visitation over a three-year period from 2015-2017 16 Based on average visitation over a three-year period from 2009-2011 17 International Visitor Survey and National Visitor Survey, Tourism Research Australia, 2017

153k

344k

250k

96k 96k 90k

5.1k 5.3k 7.1k

254k

445k

347k

2009-2011 2012-2014 2015-2017

Domestic Day Domestic Overnight International Total visitation

18

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

While the domestic day tripper market is an important visitor market, it tends to be lower yielding than overnight

markets. By way of example (and as demonstrated in more detail in section 3.4), domestic overnight visitors to the

Lockyer Valley contribute over six times the spend, per visit, when compared with domestic day trippers. This

supports the Lockyer Valley’s desire to focus on growing the overnight visitor market. To achieve this, however,

necessitates the investigation of: additional accommodation options to meet the needs of these markets; additional

experiences/attractions; and targeted product packaging (accommodation, transport, experiences, food and

beverage etc.).

3.2. Visitor Nights

Figure 11 provides a summary of visitor nights to the Lockyer Valley. It demonstrates that:

▪ although international visitors make up a small share of the Lockyer Valley’s total visitation (2%), in terms of

visitor nights spent in the LGA, they represent 66% of visitor nights18;

▪ total visitor nights in the Lockyer Valley increased over the period assessed, growing from 450k to 757k nights

(a total growth of 68% or 307k nights); and

▪ while both domestic visitor nights increased marginally over the period assessed, the majority of growth

stemmed from the international market, increasing by 262k nights (109% growth).

The primary reason for the skew towards the international market (in terms of visitor nights) is the number of

international agricultural workers arriving on short-term/seasonal contracts, along with international students

staying at the University of Queensland (Gatton Campus).

Figure 11: Visitor Nights in Lockyer Valley (based on 3-year averages from 2009-2017)19

18 Based on three-year average from 2015-2017. 19 International Visitor Survey and National Visitor Survey, Tourism Research Australia, 2017

209k

263k 254k

241k

347k

503k

450k

610k

757k

2009-2011 2012-2014 2015-2017

Domestic Overnight International Total visitor nights

19

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

3.3. Average Length of Stay

Figure 12 provides a summary of the average length of stay (ALOS) of visitors to the Lockyer Valley. It demonstrates

that while the international market has a far higher ALOS than the domestic market (72 days for international

visitors in 2017 compared with 2.9 days for domestic visitors), this is reflective of the large numbers of international

workers (who stay in the Lockyer and pick fruit and vegetables to extend their visas) as well as students studying

in the LGA. Based on discussions with industry, the international leisure visitor market to the Lockyer Valley is more

likely to have an ALOS of approximately 2 nights.

Figure 12: Average Length of Stay in Lockyer Valley (based on 3-year averages from 2009-2017)20

3.4. Visitor Spend

While there is currently no visitor spend data for the Lockyer Valley, an estimation of visitor spend has been derived

using average visitor spend data for the Brisbane Region (which the Lockyer Valley is part of) and applying this to

Lockyer Valley visitation data. Table 4 demonstrates the following.

▪ Estimated spend by visitors to the Lockyer Valley totalled just under $94m – the majority of which ($56.8m)

was spent by the domestic overnight visitor market.

▪ While the domestic day trip market comprised 72% of visitation to the Lockyer Valley, the market only

represented 26% in terms of spend. On the other hand, the domestic overnight visitor market represented 26%

of visitation, but contributed to 61% of total spend. Similarly, the international market which represented 2% of

visitation, contributed to 13% of total visitor spend. This demonstrates the far higher yielding nature of overnight

visitors to the Lockyer Valley.

Table 4: Visitor Spend in the Lockyer Valley

Visitor Expenditure: Brisbane Region21 Visitation 2017 spend Spend

p/visitor

Domestic Daytrips 14.0m $1.36b $97

Domestic Overnight 6.5m $4.11b $633

International Overnight 1.3m $2.24b $1,762

Visitor Expenditure: Lockyer Visitors22 Spend

p/visitor 2017 spend ALOS23 Spend/p night

Domestic Daytrips 250k $97 $24.2m - -

Domestic Overnight 90k $633 $56.8m 2.9 $221.71

International Overnight 7.1k $1,762 $12.5m 61.6 $28.61

Total $93.5m

20 International Visitor Survey and National Visitor Survey, Tourism Research Australia, 2017 21 Based on Brisbane Regional Snapshot YE September 2017, Tourism Events Queensland (https://cdn1-teq.queensland.com/~/media/0d4920fbfbb24658839ff0038b991513.ashx?vs=1&d=20180130T100044 22 Based on average visitation over the period 2015-2017 23 Based on average from 2009-2017

2.3 2.9 2.9

46.6

6672

2009-2011 2012-2014 2015-2017

Domestic Overnight Visitors International Visitors

20

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

3.5. Purpose of Visit

Over the past four years, visitation to the region has been driven primarily by a leisure market – including for the

purpose of holidaying and to visit friends and relatives (VFR).

Figure 13 shows the purpose of visit, by visitor type, to the Lockyer Valley, and demonstrates the following.

▪ Domestic day trippers are primarily VFR visitors (39%), closely followed by holiday (38%). To convert a

proportion of these day trippers into overnight visitors, there is a need to introduce more accommodation as

well as experiences to undertake.

▪ Domestic overnight visitors are primarily VFR visitors (57%), more so than holiday/leisure (21%). The VFR

market tends to be motivated to undertake experiences by those friends and relatives they are visiting. It is,

therefore, important that residents are advocates for the Lockyer Valley and understand what is available in

their own “backyard” so they are able to encourage visiting friends and relatives to undertake these

experiences.

▪ While, based on the data, international overnight visitors are primarily visiting for a holiday (68%), we suspect

that the number coming for work, in particular, is underrepresented, considering the extent (based on

discussions with industry and Council) of working holiday makers in the Lockyer Valley. We suspect there is an

element of sampling confusion with international working holiday makers registering as holiday visitors rather

than those actually working within an area. Often, the working holiday market travels out to major city areas to

undertake tourism-based experiences. There is a need to introduce a variety of experiences catering for this

market (including passive adventure experiences and potentially leveraging off the Lockyer Valley’s

waterways) to encourage this market to spend their free time within the Lockyer Valley rather than travelling

out on their time off.

Figure 13: Purpose of Visit to Lockyer Valley, by Visitor Type (based on 3-year average to 2017)24

24 Three-year average from 2015-2017. Note: ‘other’ includes education and in-transit purposes

38%

21%

68%

39%

57%

16%

11% 10%

2% 3%

10%12% 12%

Domestic Day Domestic Overnight International

Holiday VFR Business Employment Education Other

21

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

22

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Product Audit

This section provides an audit of Lockyer Valley accommodation, tourism-based experiences, and the food and

beverage offering. It is important to note the following.

▪ This is a top line audit completed via a desktop research exercise, it, therefore, may exclude those products

which are not currently listed on major accommodation and destination websites.

▪ A qualitative assessment (i.e. the quality/star rating) of product has not been undertaken. As such, the audit

does not reflect its marketability or viability. This is an important consideration because, often, the quality of

accommodation stock is highly variable, and at times, not easily marketed.

▪ The complete set of findings is detailed in Section 2 - 5 of the Supporting Documentation.

4.1. Accommodation

Table 5 provides a summary of the accommodation audit, while Figure 14 illustrates the share of accommodation

type. It demonstrates that:

▪ the majority of accommodation facilities are camping grounds (11), followed by hotels (7) and B&Bs (6);

▪ the largest built accommodation facility – Rooms Motel (Gatton) – includes 33 rooms (with an additional 6

rooms to be added in 201825);

▪ the outdoor accommodation options primarily comprise a mixture of free and paid camping and caravan/RV

sites), including the recent development of a recreational vehicle (RV) park in Gatton, which has certified the

town as ‘RV Friendly’; and

▪ the Lockyer Valley has an estimated 382 bookable rooms (in hotels, motels, B&Bs etc.) and an estimated 646

bookable beds26 in hostels.

▪ And there are 26 rooms at Porters Plainland Hotel currently under construction.

In general, the current accommodation stock lacks diversity and is of a relatively small scale, unable to

accommodate large volumes of visitors or large-scale conferences/events. While we understand that the Lockyer

Valley has had significant investment in backpacker-style accommodation, there is a need to diversify the

accommodation offering, including investigating developing a branded destination holiday park (which offers

chalets/cabins, powered and unpowered RV/caravan sites etc. along with family-friendly facilities such as water

parks etc.), eco-lodges and guest houses.

25 Note these additional rooms were not included in the audit. 26 This includes the backpacker development in Grantham, currently under construction, which will provide tremendous value to the visitor economy by offering larger scale farm-worker accommodation. It is projected that stage 1, including 236 beds, will be completed in early 2018 (the full project includes 600 beds), attracting larger volumes of international workers to the region.

23

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Table 5: Accommodation Audit Summary

Type # of Properties Approximate # of

Rooms/Beds

Camping 11 170 beds

Number of sites n/a

Hotel 7 71 rooms

Bed & Breakfast

6 18 rooms

Motel 5 96 rooms

Caravan Park 5 n/a

Farm Stay 2 27 rooms

Hostel 2 646 beds

Total 33 1,014

4.2. Attractions

Table 6 and Figure 15 summarises the findings of the attractions/experiences audit and demonstrates that the

majority of product that is available falls into the ‘outdoor/nature’ category, comprising 37% of all product

identified. This is primarily passive product involving lookouts, waterways, national parks and walks. To leverage

off these natural assets, there is a need to investigate complementary (and environmentally friendly) nature-based

passive and more active recreational product.

While the Lockyer has a desire to continue to push the region as a ‘foodie’ destination and has rolled out a number

of successful initiatives to promote this, there is a need for the agri-tourism and related foodie experiences to be

diversified.

Table 6: Attractions Audit Summary

Type #

Outdoor/Nature 12

Museum/Gallery 8

Farmgate/food/wine 5

Arts/Culture 5

Tourist Drive 2

Activity Operator 1

Total 33

Figure 14: Share of Accommodation Type

Camping28%

Hotel18%

B&B15% Motel

13%

Caravan Park13%

Farm Stay8%

Hostel5%

Figure 15: Share of Attractions Product Type

Outdoor/Nature35%

Museum/Gallery23%

Farmgate/food/wine15%

Arts/Culture15%

Tourist Drive9%

Activity Operator3%

24

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

4.3. Markets

Table 7 summarises the various different markets that operate throughout the region, ranging from farmer/produce

markets to arts & crafts.

Table 7: Lockyer Valley Markets Audit27

Name Location Product Type

Laidley Village Markets Laidley Markets

Mulgowie Farmers Market Mulgowie Markets

Ma Ma Creek Markets Ma Ma Creek Markets

Plainland Country Markets Plainland Markets

Murphys Creek Markets Murphy's Creek Markets

Twilight Markets Hatton Vale Markets

Ferrari Park Markets Laidley Markets

The Handmade Expo and Vintage Markets Forest Hill Markets

4.4. Food and Beverage

There are approximately 46 food and beverage28 offerings throughout the Lockyer Valley (see Table 8), including:

▪ café/restaurant facilities (48%), some of which offer a complementary retail element (an additional 4%);

▪ pubs (28%); and

▪ farmgate/produce centres (18%), where locally made and locally sourced food can be purchased directly from

a farm.

Feedback from stakeholders indicated a desire to grow the Lockyer’s food and beverage offer, including offering

a wider range and more higher quality dining experiences as well as more farm gate experiences to showcase the

quality of the Lockyer Valley’s locally grown and made produce.

Table 8: Food and Beverage Audit Summary

Type #

Café/Restaurant 22

Pub 14

Farmgate/Produce 8

Café/Restaurant and Retail 2

Total 46

27 Based on: http://www.luvyalockyer.com.au/whats-on/markets and Council input 28 Note this excludes fast food outlets

Figure 16: Share of Food and Beverage Type

Café/Restaurant48%

Pub31%

Farmgate/Produce17%

Café/Restaurant and Retail

4%

25

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

4.5. Events & Festivals

The following table provides a summary of the major events held in the Lockyer Valley (provided by Council).29 It

demonstrates that the majority of events held are categorised as ‘cultural events’, comprising 39% of events. This

is followed by truck/car-related events (17%).

Table 9: Events and Festivals Audit Summary

Type # %

Cultural event 9 39%

Truck/Car-related event 4 17%

Horse-related event 2 9%

A&I Show 2 9%

Cycling 1 4%

Community Awards 1 4%

Food event 1 4%

Music event 1 4%

Rodeo 1 4%

Fun Run 1 4%

Total 23 100%

In addition, Table 10 illustrates the events & festivals calendar and demonstrates that the months of February and

December do not currently have any major events scheduled, while, the months of March, September and October,

in particular, have a higher concentration of events scheduled.

Furthermore, while the events audit includes major events (as identified by Council), these primarily would still

draw a local rather than broader regional crowd. There is a need to investigate the potential to introduce a major

destination event for the Lockyer Valley which would encourage visitation to the Lockyer from a far wider

catchment.

Table 10: Lockyer Valley 2018 Events & Festivals Calendar30

Month Event

January ▪ Australia Day Awards & Community Event

February ▪ -

March ▪ Gatton Motorfest

▪ Laidley Country Music Festival

▪ Ride the Range

April ▪ Laidley Heritage Weekend

May ▪ Clydesdale and Heavy Horse Field Days

▪ Lockyer Multi-Cultural Festival

June ▪ Chrome and Clutter Retro Festival

July ▪ Gatton A&I Show

▪ Laidley A&I Show

August ▪ Helidon Heritage Fair

▪ LAMA (Lockyer Antique Motor Assoc) Tractor Trek

September

▪ Fossil Downs Bush Rodeo

▪ Gatton Dance Eisteddfod

▪ HCVAQ Historic Truck and Machinery Show

▪ Laidley Spring Festival

29 Note this list of events was provided by Council and excludes smaller local civic-based events. 30 Ibid

Month Event

October

▪ Country Challenge on Campus

▪ Lights on the Hill Memorial Convoy

▪ Murphys Creek Chilli Festival

▪ Laidley Motorcycle Swap Meet

November ▪ Celtic Festival of Queensland

▪ Christmas in the Country Art & Craft Show

December ▪ -

Throughout the year

▪ Lockyer Valley Speedway

▪ Lockyer Valley Turf Club Race Days

26

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

27

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Barriers to Address

The following section outlines the barriers which should be addressed to continue to activate the Lockyer Valley’s

visitor economy. They have been listed alphabetically and segmented according to the following categories.

▪ Product and supporting infrastructure

▪ Marketing and destination awareness

▪ Tourism governance

Section 6 of this Plan highlights opportunities which provide further detail on how many of these barriers can be

mitigated and positive outcomes achieved.

5.1. Product and Supporting Infrastructure

5.1.1. Accommodation Quality

As identified in the 2013 Plan, aside from some better-quality B&Bs in the area, the quality of the existing

accommodation stock is mixed. There is a need to establish a strong B&B network targeting market sectors.

There is a need to improve the quality and maintenance of some accommodation facilities, to ensure they are not

tired and can continue to attract higher yielding overnight visitors and offer a standard capable of competing in

the broader tourism market.

Overall, improvement to the supply and quality of accommodation will generate the following improvements to

the visitor economy:

▪ increases the volume of higher-yielding overnight visitors staying in the region;

▪ enhances the perception of the Lockyer Valley as a visitor destination in its own right (rather than a ‘drive-

through’ region);

▪ it enables the region to host larger-scale events, festivals, conferences, etc, which could attract a number of

new, niche visitor markets; and

▪ it increases the level of visitor spend in the area.

5.1.2. Accommodation Supply

Recent investment in accommodation facilities has increased the supply of accommodation and stock of available

beds. The product audit (Section 4.1) combined with a recent Accommodation Study completed in 2016

(commissioned by Council) identified a number of improvements, including:

▪ New accommodation in Gatton, with the development of the 4-star Rooms Motel (33 beds)

▪ Development of a, soon to be completed, large backpacker/farm worker accommodation facility, which will

include over 600 beds. This will alleviate some of the lack of farm/seasonal worker accommodation and is

expected to grow this visitor market in the short and long-term. As such, it should drive growth in the Lockyer

Valley visitor economy.

It is important to note that the new backpacker facility has the potential to attract increasing visitors from the

international backpacker market seeking seasonal farm work. In addition, if complementary retail and entertainment

28

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

product is included alongside the facility, the potential exists to create the Lockyer as an international backpacker

‘hub’ that allows for an increased length of stay and also enables greater volumes of visitor spend in the Lockyer

Valley.

However, the supply of accommodation could be improved with the development of a higher quality branded

destination holiday park in the region. As mentioned in the 2013 Plan, these facilities offer a full holiday experience,

including swimming pools and water features, outdoor and indoor recreation, retail, etc. As such, they could attract

the high-yielding family and help promote the region as a family-friendly destination.

5.1.3. Coordination of Events

Stakeholders also indicated that the current community events calendar is at capacity and needs better

coordination. The region’s event calendar is busy, with events often occurring at the same time and within the same

community (this is particularly the case for farmer’s markets). This creates conflict and reduces the ability for events

to grow and become successful. In addition, not all events and festivals are adequately marketed to the visitors to

the region.

There is a need to consider:

▪ developing a better coordinated, consolidated events strategy, that is heavily promoted;

▪ clearly articulate the difference between community events (i.e. those which predominantly draw a local

market) and tourism/destination events (i.e. those which attract external visitors to the region); and

▪ developing a separate destination events calendar (in addition to a community events calendar) which focuses

only on those major tourism events to showcase to visitor markets the various major events in the region.

5.1.4. Commissionable product to leverage regional strengths

As demonstrated in the audit, the Lockyer Valley possesses a number of strengths that make it attractive to visitors,

including the agricultural industry and prevalence of outdoor, nature-based, recreational product. To fully expand

these strengths and grow the visitor economy, it is critical that the region provides more commissionable product

that complements these experiences, in order to maximise the duration of visitor stays and increase visitor yield. In

addition, this will also increase interest from the wider tourism industry such as wholesalers and tour operators who

are eager for new, unique commissionable product.

5.1.5. Growing agri-tourism product

The region has the potential to maximise the range of agri-tourism experiences. Provision of unique farmgate

product, farm tours or food-related experiences will enable the region to attract more visitors and meet the needs

of the increasingly mature food tourism visitor market segment. In doing so, visitors will find it easier to fully

appreciate one of the Lockyer Valley’s unique selling point, being one of the primary food producers in Australia

(and one of the most fertile regions in the world).

To achieve this will require careful coordination from Council, industry operators and producers/farmers. In turn,

this may lead to new farm gate experiences, farmers markets and an annual signature food-based festival.

29

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

5.1.6. Introducing outdoor recreational experiences

Key findings from the product audit and stakeholder consultation with respect to outdoor recreational activities

can be synthesised as follows.

▪ While there are a number of nature-based recreational areas, as well as outdoor self-driving trails, there is a

need to increase the provision of built infrastructure and supporting services to attract additional visitors, both

day trippers and overnight. By providing more commissionable product (e.g. equipment hires, tours, retail, food

& beverage, etc) as well as high quality roads and signage, the region’s ability to generate income from these

activities would increase.

▪ For example, the Bicentennial National Trail, which passes through the Lockyer Valley, needs more supporting

product/infrastructure as most of it passes through private property. Therefore, the opportunity exists to

create a strategy that better utilises the trail to attract greater usage and associated visitor spend in the area.

▪ Lake Dyer, Lake Clarendon and Lake Apex are underutilised in terms of tourist product, particularly water-sport

opportunities including bird watching and eco-friendly nature based activities at Lake Apex especially.

▪ There is an identified need for more adventure-based commissionable product, particularly those that can

leverage off the region’s natural environment and landscape (e.g. mountain biking trails, treetop walking,

ziplines, etc.). Examples include: Glen Rock National Park, for camping, bushwalking, horse riding, along with

Emu Gully and Edmund Park.

5.1.7. Experiences for the working holiday market

The Lockyer has a significant working holiday backpacker market. And while these visitors tend to stay in the area

for several months, and often have 1-2 days off per week, there are limited experiences that they can undertake.

Many backpackers, therefore, travel to surrounding areas to undertake recreation-based experiences. There is a

need to investigate the potential to introduce experiences in the Lockyer which would appeal to this market such

as 4wd tours, fishing tours and/or boat hire, quad biking tours along with investigating Indigenous cultural tourism

opportunities etc. These should be packaged in with transport to/from the experience as often backpackers do not

have their own vehicles.

5.1.8. Family-friendly experiences

While the Lockyer Valley has a range of natural recreational experiences, these are not always suitable for the

family market with children under 10 years of age. There is a need to investigate the introduction of experiences

for younger children – for locals and visitors alike. This could include development/marketing of family-friendly

walking and cycling trails or other commercial initiatives, such as high ropes and aerial courses, outdoor mazes and

indoor fun parks etc. An indoor family product would also be of benefit to local families.

5.1.9. Interpretation and directional signage

There is a lack of signage – including directional and interpretive – throughout the Lockyer Valley. Directional

signage, particularly within a CBD, is crucial to encourage visitation to places of interest, outline walks that can be

completed through the CBD to attractions (such as heritage and cultural walks).

The improved signposting of the Lockyer’s natural and built attractions which could potentially encourage visitors

and the community to make better use of these facilities for walking, cycling and exploring.

There is also a lack of interpretative signage when entering the Lockyer Valley and at attractions. What should be

considered are attractive gateway signs on major access roads into the Lockyer, highlighting the key experiences

30

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

and branding of the LGA. As the area is steeped in agricultural history, the potential exists to use sign boards,

markers and mobile apps to bring alive the heritage significance of the LGA.

Signage that could potentially be implemented includes attractive static displays (for both directional and

interpretive means) as well as high-tech, innovative electronic information displays and touch screens which could

be in town centre main streets.

5.1.10. Majority of tourism operators are small businesses

The Lockyer Valley has limited commissionable (i.e. pay for) tourism product and the majority of operators in the

sector are smaller-scale. While the boutique nature of operators in the Lockyer is considered an advantage as it

can offer a more personalised experience for visitors, there is a balance required as larger-scale operators tend to

bring with them larger marketing budgets which not only markets their product but also the region.

5.1.11. Town Centre Activation

The towns and villages throughout the region have the potential to offer more in terms of important gateway

destinations and urban hubs to offer tourism product and experiences. This includes the need to offer quality

streetscapes, in order to increase attractiveness and visitor appeal. In addition, there is a need to help activate town

centres (not just Gatton and Laidley) and to help revitalise communities so that they provide the services and

infrastructure to meet the needs of the visitor markets. This is explored in greater detail in the separate Economic

Development Plan.

5.2. Marketing and Destination Awareness

5.2.1. Brand awareness

Although there is a clear tourism brand for the region (Luvya Lockyer), there is benefit in further developing this

to help position the region as an attractive visitor destination and to continue to stimulate the visitor economy. It

requires further investment to the brand and a fulfillment strategy to ensure users of the brand are keeping to

brand principles, presentation requirements etc.

Some of the issues relating to this are summarised below:

▪ While the Lockyer Valley is well known, within the agricultural industry, for its strength in agriculture, it is less

well known for this strength outside the industry to the average consumer. In part, this is due to restrictive

requirements of major supermarkets that do not promote the region’s produce from where it is sourced.

▪ Improvements are needed in directional and interpretive signage, particularly a welcome portal/sign for

incoming visitors and better way finding around the region and gateway signage on the new bypass.

▪ The positioning of the local towns and villages needs improvement, so as to more effectively highlight their

unique features (e.g. heritage buildings, farming industry) and points of difference to visitors. In addition to an

activation strategy (which is already being considered for Gatton and other towns), there is a need for a

positioning strategy to generate tourism.

In addition, the Lockyer Valley brand could be enhanced to better promote the region and its strengths. By way of

example, The Granite Belt is also known as ‘Queensland’s Salad Bowl’; while an online search for ‘Australia’s food

bowl’ leads to Shepparton in Victoria and a search of the term ‘luvya food’ leads to New Zealand apples31.

31 http://www.luvyafruit.co.nz/

31

To

uri

sm

De

sti

na

tio

n P

lan

20

18-2

02

3

Successful branding is a difficult exercise but will be worth it if it can be used to promote the region for business

and tourism and if it can be something the community rallies behind. Cities and states that have reinvented

themselves successfully through branding include Orange; Tamworth and Tweed Valley, as just a few examples.

Once a clear brand is adopted, it can be used to position and promote the region via clothing; seals of approval for

attractions, accommodation facilities; activities, infrastructure and on produce. It can also be the lynch pin for a buy

local campaign etc.

5.2.2. Digital-savvy operators

While there are some operators in the Lockyer Valley who have an up-to-date digital presence, there are some who

lack the tools for developing this.

There is a need to ensure that all tourism operators in the Lockyer Valley are listed on the Australian Tourism Data

Warehouse (ATDW) which is used as a product database by Tourism Australia, TEQ as well as Brisbane Marketing

(as the Lockyer Valley’s RTO).

5.2.3. Product Packaging

There is limited product packaging available on destination-based websites for the Lockyer Valley and existing

operators comment that finding suitable product to package is challenging. As additional new, marketable product

is introduced, there is a need to develop packages which visitors can book, rather than providing suggested

itineraries. Packages could include accommodation, transport, guided walks/cycling, food and beverage etc.

There is also a need for industry training and up-skilling to identify opportunities for packaging product of a similar

quality.

5.2.4. Visitor Information Services

The rapid growth of digital technology has caused a fundamental shift in the way visitor information services are

delivered. While traditionally visitors have relied on VICs and brochures to discover information about a destination

(primarily while in a destination), the emergence of online booking facilities, search engines and destination

websites has meant that visitors can find out significantly and even book their entire trip in advance prior to visiting

a destination. A recent piece of research completed by Tourism Events Queensland found that only 3.6% of visitors

to Queensland went into a VIC – lower than the national average of 4.4%.32 The vexed question, therefore, is how

the remaining 96.4% of visitors to Queensland are being serviced?