Topic 12: IAS 33 Earnings Per Share

14

|CIMA F2 – HTFT Partnership: Student Notes Learning outcome C2a: Discuss additional disclosure requirements related to the group accounts: Transaction between related parties IAS 24- Related party disclosures We have to have a standard on earnings per share (EPS) because it is the most important accounting ratio. It forms part of the price/earnings ratio (P/E ratio) and, rightly or wrongly, the stock market places great emphasis on a company’s P/E ratio and therefore a standard form of measurement of EPS is required. The basic EPS calculation is simply –––––––– This should be presented as dollars or cents per share to one decimal place. We have to have a standard that governs both calculation and disclosure, because companies will follow the calculation rules but will then sometimes do their ‘own’ calculations of EPS and present them with equal prominence. Another ratio? Yes, it is just a ratio – earnings means: The amounts attributable to ordinary equity holders of the parent entity i.e. Profit or loss from continuing operations attributable to the parent entity; and Profit or loss attributable to the parent entity These profit or loss figures should be adjusted for the after-tax amounts of preference dividends, differences arising on the settlement of preference shares, and other similar effects of preference shares classified as equity. The figure ‘earnings per share’ (EPS) is used to assess the ongoing financial performance of a company from year to year, and to compute the major stock market indicator of performance, the price/earnings ratio (P/E ratio). The calculation for the P/E ratio is: P/E = ––––––––––––––––––– Topic 12: IAS 33 Earnings Per Share

Transcript of Topic 12: IAS 33 Earnings Per Share

|CIMA F2 – HTFT Partnership: Student Notes

Learning outcome C2a:

Discuss additional disclosure requirements related to the group accounts:

Transaction between related parties

IAS 24- Related party disclosures

We have to have a standard on earnings per share (EPS) because it is the most important accounting ratio. It forms part of the price/earnings ratio (P/E ratio) and, rightly or wrongly, the stock market places great emphasis on a company’s P/E ratio and therefore a standard form of measurement of EPS is required.

The basic EPS calculation is simply ––––––––

This should be presented as dollars or cents per share to one decimal place.

We have to have a standard that governs both calculation and disclosure, because companies will follow the calculation rules but will then sometimes do their ‘own’ calculations of EPS and present them with equal prominence.

Another ratio?

Yes, it is just a ratio – earnings means:The amounts attributable to ordinary equity holders of the parent entity i.e.

Profit or loss from continuing operations attributable to the parent entity; and

Profit or loss attributable to the parent entity

These profit or loss figures should be adjusted for the after-tax amounts of preference dividends, differences arising on the settlement of preference shares, and other similar effects of preference shares classified as equity.

The figure ‘earnings per share’ (EPS) is used to assess the ongoing financial performance of a company from year to year, and to compute the major stock market indicator of performance, the price/earnings ratio (P/E ratio). The calculation for the P/E ratio is:

P/E = –––––––––––––––––––

Topic 12: IAS 33 Earnings Per Share

|CIMA F2 – HTFT Partnership: Student Notes

So, what is it trying to achieve?

The aim of IAS 33 is to improve the comparison of the performance of different periods and between entities in the same period by prescribing the way EPS is to be calculated and how it is to be disclosed.

Apply Your Knowledge 1

Here is some information relating to a listed company, Jamie Inc.

Calculate Jamie Inc.’s earnings per share (EPS) in respect of the year ended 31 December 20X4 on the basis that there was no change in the issued equity share capital of the company during the year ended 31 December 20X4

Jamie Inc.

Draft Statement of profit or loss for the year ended 31 December 20X4

$000

Profit before tax 4,508

Tax (2,300)

Profit after tax 2,208

On 1 January 20X4 the issued equity share capital of Jamie was 9,200,000 6% preference shares of $1 each and 8,280,000 ordinary shares of $1 each.

Required:

Calculate the earnings per share (EPS) in respect of the year ended 31 December 20X4 on the basis that there was no change in the issued equity share capital of the company during the year ended 31 December 20X4.

Basic earnings per share is calculated by dividing the profit or loss attributable to ordinary equity holders of the parent (the numerator) by the weighted average number of ordinary shares outstanding (the denominator) during the period.

|CIMA F2 – HTFT Partnership: Student Notes

|CIMA F2 – HTFT Partnership: Student Notes

Apply Your Knowledge 2

When calculating the earnings figure for inclusion in the basic earnings per share calculation in accordance with IAS 33 Earnings per share, which of the following should be deducted from the profit after tax figure?

A. Ordinary dividend declared for the current year B. Profit after tax attributable to the non-controlling interest C. Redeemable preference dividend payable in the current year D. Irredeemable preference dividend that relates to a previous year, but has been paid out of the

current year

|CIMA F2 – HTFT Partnership: Student Notes

What if the company issues shares in the year?

Well, if the number of shares has changed during the period, a weighted average number of shares has to be used under the line.

Apply Your Knowledge 3

In the example of Jamie, suppose that the company had issued 3,312,000 shares at full market value on 30 June 20X4.

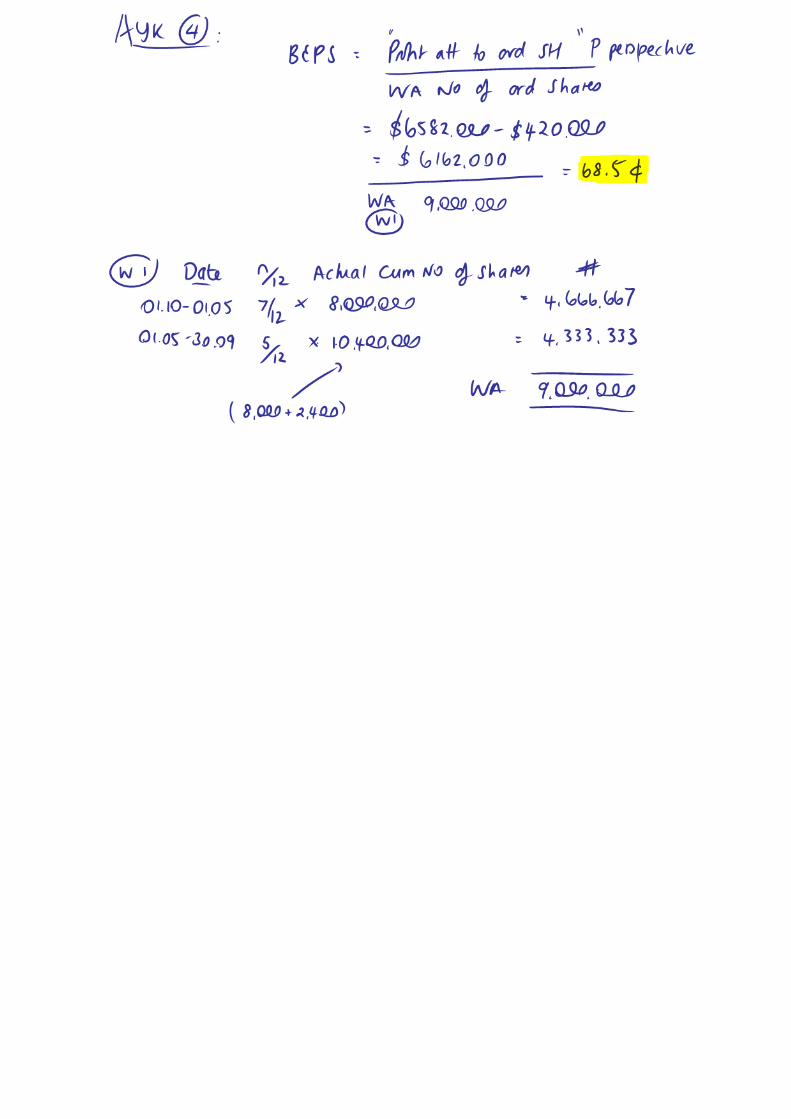

Apply Your Knowledge 4

On 1st October 20X1 KB, a listed entity, had 8 million $1 ordinary shares in issue. On 1st May 20X2 KB issued a further 2.4 million new ordinary shares for $9.20 the full market price.

The consolidated profit for the year was $6,582,000 of which $420,000 was attributable to the non-controlling interest.

The consolidated basic earnings per share of KB for the year ended 30 September 20X2 is:

A. 67.0 cents per share B. 68.5 cents per share C. 73.1 cents per share D. 77.8 cents per share

|CIMA F2 – HTFT Partnership: Student Notes

What if it was a bonus (cash free) issue?

Assume that the bonus shares have always been in issue (and therefore alter the comparative EPS amount).

Apply Your Knowledge 5

Suppose now that Jamie Inc. made no issue of shares at full price but instead made a bonus issue on 1 October 20X4 of one ordinary share for every four shares in issue at 30 September 20X4.

Apply Your Knowledge 6

On 1 January 2009 CSA, a listed entity, had 3,000,000 $1 ordinary shares in issue. On 1 May 2009, CSA made a 1 for 3 bonus issue.

On 1st September 2009 CSA then issued a further 2,000,000 new $1 ordinary shares at full market price, which was $3.20 each.

The profit before tax of CSA for the year ended 31 December 2009 was $1,040,000. The income tax expense for the year was $270,000.

The basic earnings per share for the year ended 31 December 2008 was 15.4 cents.

The basic EPS and the comparative EPS presented in the financial statements for the year ended 31 December 2009 would be:

A. Basic 22.3 cents Comparator 15.4 cents B. Basic 16.5 cents Comparator 15.4 cents C. Basic 16.5 cents Comparator 11.6 cents D. Basic 15.4 cents Comparator 11.6 cents

|CIMA F2 – HTFT Partnership: Student Notes

What if it was a rights issue?

Assume that the shares issued are a mix of bonus and full price shares. For the bonus element assume that they have always been in issue and therefore adjustthe comparative.

Apply Your Knowledge 7

Suppose now that Jamie’s only share issue in 20X4 was a rights issue of $1 ordinary shares on 1 October 20X4 in the proportion of one for every five shares held at a price of $1.20. The market price for the shares on the last day of quotation cum rights was $1.80 per share.

When a rights issue takes place, shares are issued at less than full market price. We treat this as a combination of a bonus issue and an issue at full market price. We will therefore need to calculate the rights issue bonus fraction by using share prices:

Rights issue bonus fraction =

Actual cum rights price =

Theoretical ex rights price =

|CIMA F2 – HTFT Partnership: Student Notes

Apply Your Knowledge 8

Which of the following statements is true in respect to raising equity finance?

A. A rights issue is cheaper than a public share issue B. If an entity raises equity finance by way of a rights issue this would result in a flotation C. A rights issue will result in a dilution to existing shareholders’ percentage ownership in the entity D. A rights issue is when equity shares are available to be purchased by institutional investors only

Apply Your Knowledge 9

BT has raised finance via a rights issue of 1 for 5 at $2.25 per share. The shares were quoted at $2.75 prior to the rights issue.

The theoretical ex rights price is:

A. $2.33 B. $2.50 C. $2.65 D. $2.67

Apply Your Knowledge 10

MS, a listed entity, had 20,000,000 ordinary shares in issue on 1st January 20X2. On 1 June 20X2, MS made a 1 for 4 rights issue at $1.50 per share. The issue was fully taken up by the shareholders.

MS’s share price immediately prior to the rights issue was $2.20 and the theoretical ex rights price relating to the rights issue is $2.06.

The basic earnings per share reported in the financial statements of MS for the year ended 31 December 2) X1 was 46.2 cents.

The comparative basic earnings per share that would be presented in the financial statements of MS for the year ended 31 December 20X2 is:

A. 37.0 cents per share B. 43.3 cents per share C. 46.2 cents per share D. 49.3 cents per share

|CIMA F2 – HTFT Partnership: Student Notes

Diluted earnings per share (DEPS)

This is calculated where potential ordinary shares have been outstanding during the period which would cause EPS to fall if exercised (dilutive instruments). It is calculated in addition to basic EPS.

Equity share capital may change in future owing to circumstances which exist now. Diluted EPS (DEPS) attempts to alert shareholders to the potential impact on EPS.

Potential changes may arise for any of the following reasons:

shares not yet ranking for dividend

convertible debt or preference shares in issue

options granted to subscribe for new shares.

To deal with this, adjust basic earnings and number of shares assuming convertibles, options, etc. had converted to equity shares on the first day of the accounting period, or on the date of issue of convertibles, options, etc. if later.

Diluted earnings per share is calculated as follows:

The earnings should be adjusted by adding back any costs that will not be incurred once the dilutive instruments have been exercised. This will include, for example, interest on convertible debt.

The number of shares will be adjusted to take account of the exercise of the dilutive instrument. This means that adjustment is made:

For convertible instruments By adding the maximum number of shares to be issued in the future.

For options or warrants By adding the number of effectively ‘free’ shares to be issued when the options are exercised.

Some companies have more than one dilutive instrument in issue, such as both convertibles and share options. In this case diluted EPS is calculated by adding each dilutive instrument in turn, with the most dilutive first. If any instrument causes the diluted EPS figure to increase, this instrument, and any subsequent instruments, are ignored. The standard calls these antidilutive potential shares.

|CIMA F2 – HTFT Partnership: Student Notes

Apply Your Knowledge 11

Continuing with the example of Jamie we can calculate diluted EPS on the basis that the company made no new issue of shares during the year ended 31 December 20X4, but on that date it had in issue $2,300,000 10% convertible loan stock 20X6 to 20X9. Assume a corporation tax rate of 50%.

This loan stock will be convertible into ordinary $1 shares as follows.

20X6 90 $1 shares for $100 nominal value loan stock

20X7 85 $1 shares for $100 nominal value loan stock

20X8 80 $1 shares for $100 nominal value loan stock

20X9 75 $1 shares for $100 nominal value loan stock

c

The earnings should be adjusted by adding back any costs that will not be incurred once the dilutive instruments have been exercised. This will include, for example, interest on convertible debt.

The number of shares will be adjusted to take account of the exercise of the dilutive instrument. This means that adjustment is made:

For convertible instruments By adding the maximum number of shares to be issued in the future.

|CIMA F2 – HTFT Partnership: Student Notes

What if it was options that are outstanding?

In that case we need to add the number of effectively ‘free’ shares to be issued when the options are exercised.

Apply Your Knowledge 12

Now assume that Jamie made no issue of shares during the year ended 31 December 20X4, but on that date there were outstanding options to purchase 920,000 ordinary $1 shares at $1.70 per share. The average fair value for the year of ordinary shares was $1.80.

![W H O IAS M [1979-2015] - s IAS World History optional Mains Previous Years’ Question Papers [1979-2015] Compiled by: A. N. SINHA | Topic wise Compilation](https://static.fdocuments.in/doc/165x107/5aab05d07f8b9a2b4c8b783f/w-h-o-ias-m-1979-2015-s-ias-world-history-optional-mains-previous-years.jpg)

![History Optional: Topic Wise Question Bank of Modern India ... · IAS Modern Indian History Optional Mains Previous Years’ Questions [1979-2019] HISTORY OPTIONAL: TOPIC WISE QUESTION](https://static.fdocuments.in/doc/165x107/5f0acf3e7e708231d42d7305/history-optional-topic-wise-question-bank-of-modern-india-ias-modern-indian.jpg)