Todos los derechos reservados para XM S.A E.S.P. 2007 APEx Conference October 14 to October 17...

13

Todos los derechos reservados para XM S.A E.S.P. 2007 APEx Conference October 14 to October 17 Paris, France Central and South American Markets Luis Alejandro Camargo S. Wholesale Market Manager XM S.A. E.S.P.

-

Upload

chad-oconnor -

Category

Documents

-

view

213 -

download

0

Transcript of Todos los derechos reservados para XM S.A E.S.P. 2007 APEx Conference October 14 to October 17...

Todos los derechos reservados para XM S.A E.S.P.

2007 APEx ConferenceOctober 14 to October 17

Paris, France

Central and South American Markets

Luis Alejandro Camargo S.Wholesale Market Manager

XM S.A. E.S.P.

2

Contents

• Markets characteristics

• Markets situation

• Conclusions

3

0

10,000

20,000

30,000

40,000

50,000

60,000

MER MÉXICO

R: 35%

R: 25%

GH Capacity GenerationD Demand

Central American and Mexican Power Systems

G D

49,8

32,4

GW

Mexico

GD

1,4

1,8

GW

Guatemala

G D

1,09

0,88

GW

Salvador

G D

1,6

1,13

GWHonduras

Nicaragua

G D

0,56

0,48

GW

Costa Rica

G D

2,1

1,4

GW

Panama

G D

1,3

1

GW

R: 35%

R: 24%

R: 19%

R: 28%

R: 14%

R: 32% R: 21%

MER

Mexico

Demand MW

Generation MW

Reserves %

Mexico 32,423 49,834 35%Guatemala 1,383 1,824 24%El Salvador 882 1,095 19%Honduras 1,126 1,555 28%Nicaragua 485 566 14%Costa Rica 1,419 2,093 32%Panama 1,024 1,296 21%Total (1) 38,741.01 58,262.79 34%(1) Mesoamerica

0

25

50

75

100

Brazil

Paraguay

Uruguay

Argentina

4

0

30

60

90

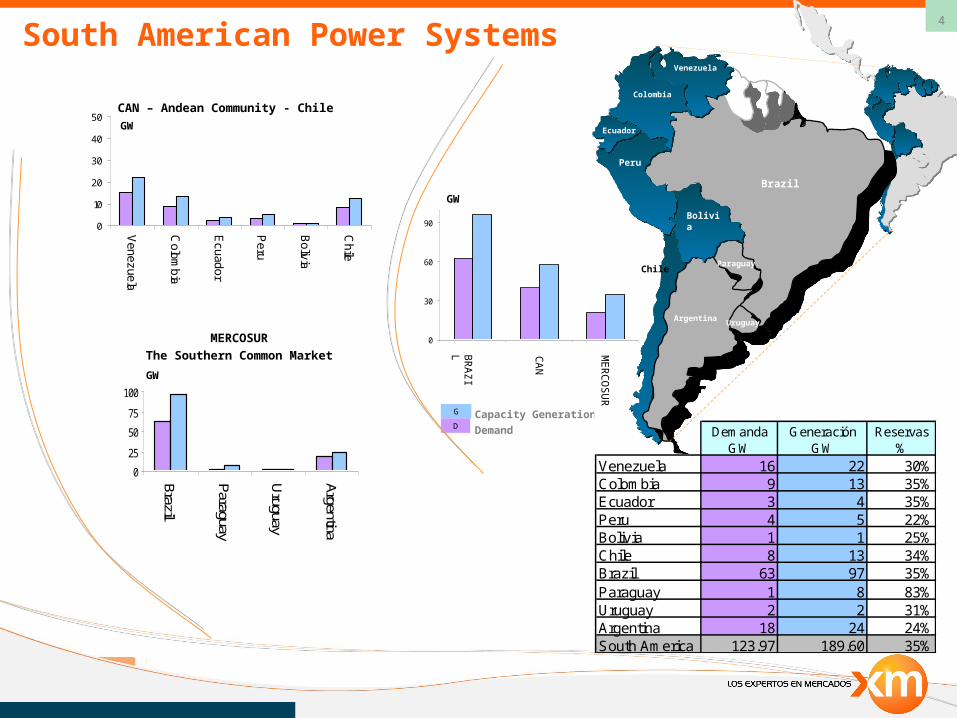

South American Power Systems

CAN – Andean Community - Chile

MERCOSUR The Southern Common Market

Venezuela

G Capacity GenerationD Demand

Colombia

Ecuador

Peru

Bolivia

Chile

Argentina

Brazil

Paraguay

Uruguay

0

10

20

30

40

50

Venezuela

Colom

bia

Ecuador

Peru

Bolivia

Chile

GW

GW

GW

Demanda GW

Generación GW

Reservas %

Venezuela 16 22 30%Colombia 9 13 35%Ecuador 3 4 35%Peru 4 5 22%Bolivia 1 1 25%Chile 8 13 34%Brazil 63 97 35%Paraguay 1 8 83%Uruguay 2 2 31%Argentina 18 24 24%South America 123.97 189.60 35%

0

25

50

75

100

Brazil

Paraguay

Uruguay

Argentina

0

30

60

90

BR

AZ

IL

CA

N

ME

RC

OS

UR

BR

AZ

IL

CA

N

ME

RC

OS

UR

0

25

50

75

100

Brazil

Paraguay

Uruguay

Argentina

5

Markets characteristics

Transmission

Distribution

Trading

GenerationAr

gent

ina

Boliv

ia

Braz

il

Chile

Colom

bia

Cost

a Ri

ca

Ecua

dor

El S

alvad

or

Gua

tem

ala

Hond

uras

Mex

ico

Nica

ragu

a

Pana

ma

Para

guay

Peru

Urug

uay

Vene

zuela

Monopoly

Open Access

Competitive

State Monopoly

Single Buyer (Monopsony)

Wholesale energy market

Honduras

Costa Rica Venezuela

Paraguay

6

State Monopoly

Single Buyer (Monopsony)

Markets characteristics

Wholesale energy market

Honduras

Costa Rica Venezuela

Paraguay

OTC Organized

ArgentinaBoliviaBrazil Diferences

ChileColombia Costa RicaEcuadorEl Salvador None

GuatemalaHondurasNicaraguaPanamáParaguayPeruUruguayVenezuela

None

None

None

None

Monopoly

Financial MarketCountry Spot Market Clearing services

Monopoly

Monopoly

Monopoly

Under ConstructionUnder constructionUnder construction

Monopoly

Monopoly

Monopoly

Monopoly

7

Wholesale Spot Prices

0

30

60

90

120

150

180

210

240

270

300

330

Ene

-06

Feb

-06

Mar

-06

Abr

-06

May

-06

Jun-

06

Jul-0

6

Ago

-06

Sep

-06

Oct

-06

Nov

-06

Dic

-06

USD/MWh

― Nicaragua

― Uruguay

― Guatemala― El Salvador― Panama― Ecuador― Peru

― Bolivia― Argentina― Colombia

8

Markets situation

9

Economic and electricity demand growth

43

109

46

84

57

710

74

17

44

65

38

34

65

77

76

14

Electricity Demand

Economic Growth (05-06)

4.5%

5.0%

5.6%

5.9%South America

Central America

10

Markets situation

• New Reliability Charge scheme• Organized Forward Energy Market• Derivative Clearinghouse• Secondary natural gas market• Interconnection to Panama• Power System Reliability

• Regulation under revision• Policy of nationalization – power

resources. Power taxing• Country Institutions to be

Transformed

• Regulation of Electricity for Imp and Exp • High demand growth• Development of the electrical infrastructure• Electricity market redesign

Peru

• Policy of subsidy fuels• Electricity importation from Colombia: 12%• Policy of self-supplying• High investment in generation. Hydroelectric

projects in construction• Political unstability. Institutions expected to be

Transformed. New constitution

300MW

300MW

500MW

100MW

336MWEcuadorColombia

Bolivia

CAN Region

• Government announces for returning to CAN

• National Electricity Corporation• Policy of nationalization of

power resources and services• Subsidy to the public services

• High dependency on liquid fuels. High prices

• Long rationing in Nicaragua• Regional electricity market where

trading is limited by transmission constrains

• Political influence on regional market • Panama interested to be part of CAN

Framework Treaty (1995) Transitory regulations of Operation and Trading

(2002) Regulator, ISO and PX Regional MER Regulation (2005) Application of the transitory regulation

MER Region (SIEPAC)

Venezuela

200MW

http://www.planpuebla-panama.org/

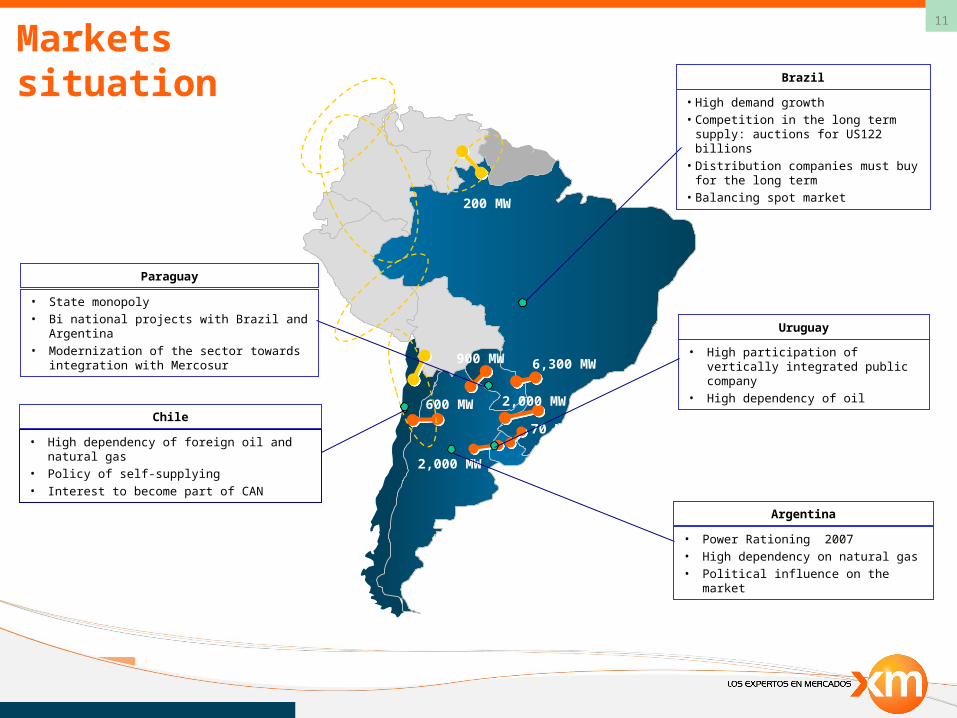

11

200 MW

6,300 MW900 MW

70 MW

2,000 MW

2,000 MW

600 MW

• High demand growth• Competition in the long term supply:

auctions for US122 billions• Distribution companies must buy for

the long term• Balancing spot market

• Power Rationing 2007• High dependency on natural gas• Political influence on the market

• High dependency of foreign oil and natural gas

• Policy of self-supplying• Interest to become part of CAN

Chile

• High participation of vertically integrated public company

• High dependency of oil

• State monopoly• Bi national projects with Brazil and

Argentina• Modernization of the sector towards

integration with Mercosur

Brazil

Uruguay

Argentina

Paraguay

Markets situation

12 Conclusions

• Renewed political influence in Power Sector

• Self-supplying policies in most countries

• Low progress in markets development and regional

agreements: CAN, MERCOSUR and SIEPAC

• Power sector nationalization in Venezuela, Bolivia, …

• High demand growth and fast reserve reductions in the

region

• Subsidies to public services

• Weak market signals for new investments

Todos los derechos reservados para XM S.A E.S.P.