· Notes to Consolidated Financial Statements ... SD 57117-5125 | T 605.339.1999 | F 605.339.1306...

89

Transcript of · Notes to Consolidated Financial Statements ... SD 57117-5125 | T 605.339.1999 | F 605.339.1306...

ATTACHMENT Lutheran Social Services of South Dakota

Governing Board of Directors 2015

Board members may serve up to 3 consecutive 3-year terms. Name Title Address Phone Term CHAIR Thomas Dempster

Director, IFM Capital Advisors

1209 S. Sugar Maple Dr. Sioux Falls, SD 57110

605-339-3223 Term III ends 12/31/16

CHAIR ELECT Malcom Chapman

Owner, The Chapman Group

3213 W. Main St., #182 Rapid City, SD 57702

605-716-6210 Term II ends 12/31/17

SECRETARY/TREASURER Rita Karels

5709 S. Shadow Ridge Ave. Sioux Falls, SD 57108

605-271-3149 Term II ends 12/31/17

Richard Aguilar Senior Vice President, Citi

2400 E. Stanton Dr. Sioux Falls, SD 57103

605-331-1842 Term I ends 12/31/17

Bobbi Brown Guidance Counselor, Riggs High School

1122 N. Oneida Ave. Pierre, SD 57501

605-224-0318 Term I ends 12/31/15

Kim Elbers VP Human Resources, 1st Natl. Bank in Sioux Falls

315 N. Sandberg Dr. Sioux Falls, SD 57110

605-335-5207 Term I ends 12/31/17

Barbara Fishback 501 8th St. Brookings, SD 57006

605-692-2614 Term III ends 12/31/16

Phil Hogen Retired Chairman, National Indian Gaming Commission

11312 N. High Meadows Dr. Black Hawk, SD 57718

605-787-6901 Term I ends 12/31/15

Rev. Betsy Hoium Assoc. Pastor, Peace Lutheran Church

1610 S. Carter Pl. Sioux Falls, SD 57105

706-361-3683 Term I ends 12/31/17

Mike Jamison Principal, TSP, Inc. 5000 E. Fernwood Dr. Sioux Falls, SD 57110

605-371-2138 Term I ends 12/31/15

Brenda Koenig South Dakota Marketing Representative, ProAg

108 W. 20th Ave. Tyndall, SD 57066

605-464-4451 Term II ends 12/31/17

Rev. Carl Larson Pastor, American Evangelical Lutheran Church

401 S. Flynn Dr. Milbank, SD 57252

605-432-5566 Term I ends 12/31/16

Name Title Address Phone Term Dr. Mary E. Minton Asst. Professor of

Nursing, SDSU 108 Gilley Ave. S. Brookings, SD 57006

605-688-4114 Term III ends 12/31/16

Russell Olson Chief Executive Officer, Heartland Consumers Power District

221 Lake Ridge Dr. Wentworth, SD 57075

605-256-6536 Term I ends 12/31/16

Reed Rasmussen Partner, Siegel, Barnett & Schutz, L.L.P.

PO Box 490 Aberdeen, SD 57402

605-225-2017 Term II ends 12/31/17

Jim Tharp Broker/Owner, Montgomery Agency Real Estate

1968 McDonald Dr. Huron, SD 57350

605-352-3332 Term I ends 12/31/16

Bishop David B. Zellmer Bishop, South Dakota Synod, Evangelical Lutheran Church in America

2001 S. Summit Ave. Sioux Falls, SD 57197

605-274-4011 Bishop serves continuously

www.eidebai l ly.com

Financial Statements June 30, 2015 and 2014

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Table of Contents

June 30, 2015 and 2014

Independent Auditor’s Report .................................................................................................................................... 1

Financial Statements

Consolidated Statements of Financial Position ...................................................................................................... 3 Consolidated Statements of Activities ................................................................................................................... 4 Consolidated Statement of Functional Expenses ................................................................................................... 5 Consolidated Statements of Cash Flows ................................................................................................................ 7 Notes to Consolidated Financial Statements .......................................................................................................... 9

Supplementary Information

Consolidating Statement of Financial Position .................................................................................................... 26 Consolidating Statement of Activities ................................................................................................................. 28 Consolidating Statement of Cash Flows .............................................................................................................. 30 Schedule of Expenditures of Federal Awards ...................................................................................................... 33

Schedule of Prior Year Audit Findings .................................................................................................................... 36

Independent Auditor’s Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards .............................................................................................................................................. 39

Independent Auditor’s Report on Compliance for Each Major Federal Program and Report on Internal Control Over Compliance ................................................................................................................................... 41

Schedule of Findings and Questioned Costs ............................................................................................................ 43

Corrective Action Plan ............................................................................................................................................. 50

www.eidebail ly.com

200 E. 10th St., Ste. 500 | P.O. Box 5125 | Sioux Falls, SD 57117-5125 | T 605.339.1999 | F 605.339.1306 | EOE

1

Independent Auditor’s Report To The Board of Directors and Audit Committee Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Sioux Falls, South Dakota Report on the Financial Statements We have audited the accompanying consolidated financial statements of Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates, which comprise the consolidated statements of financial position as of June 30, 2015 and 2014, and the related consolidated statements of activities, functional expenses, and cash flows for the years then ended, and the related notes to the consolidated financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

2

Opinion In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates as of June 30, 2015 and 2014, and changes in net assets and cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America. Emphasis of Matter As discussed in Note 1 to the consolidated financial statements, the Organization has elected to change its method of accounting for reporting donor restricted contributions in 2015 and 2014 with time or purpose restrictions and the related release of those restrictions. Our opinion is not modified with respect to this matter. Report on Supplementary Information Our audit was conducted for the purpose of forming an opinion on the consolidated financial statements taken as a whole. The consolidating statements on pages 26 through 32 and the schedule of expenditures of federal awards, as required by U.S. Office of Management and Budget Circular A-133, on pages 33 through 34 are presented for the purposes of additional analysis and are not a required part of the consolidated financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the consolidated financial statements. The information has been subjected to the auditing procedures applied in the audits of the consolidated financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the consolidated financial statements or to the consolidated financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the consolidated financial statements as a whole. Report Issued in Accordance with Government Auditing Standards In accordance with Government Auditing Standards, we have also issued a report dated November 10, 2015 on our consideration of Lutheran Social Services of South Dakota, Inc.’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Lutheran Social Services of South Dakota, Inc.’s internal control over financial reporting and compliance.

Sioux Falls, South Dakota November 10, 2015

See Notes to Consolidated Financial Statements 3

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidated Statements of Financial Position

June 30, 2015 and 2014

2015 2014Assets

Cash and cash equivalents 1,307,830$ 1,118,132$ Accounts receivable, net 1,457,074 1,408,959 Accrued income receivable 1,119,866 667,991 Prepaid expenses 58,235 72,673 Investments 6,317,901 6,412,671 Note receivable 214,273 221,972 Restricted assets 235,063 198,845 Assets held under split-interest agreements 309,562 300,544 Beneficial interest in charitable trusts held by others 245,500 242,781 Debt issuance costs, net 37,548 42,858 Property and equipment, net 14,043,779 15,459,302

25,346,631$ 26,146,728$

Liabilities and Net Assets

LiabilitiesAccounts payable 400,792$ 539,856$ Accrued liabilities 1,035,465 1,037,756 Liabilities under split-interest agreements 89,117 104,599 Deferred revenue 9,848 28,706 Lines of credit 636,914 - Interest rate swap agreement 299,085 322,143 Notes payable 5,731,085 6,718,059

Total liabilities 8,202,306 8,751,119

Net AssetsUnrestricted

Controlling interest 12,049,106 12,271,659 Non-controlling interest - 237,508

Temporarily restricted 5,095,219 4,886,442

Total net assets 17,144,325 17,395,609

25,346,631$ 26,146,728$

See Notes to Consolidated Financial Statements

TemporarilyUnrestricted Restricted Total

Public Support, Revenue, and Other SupportPublic support:

Contributions 648,086$ 406,482$ 1,054,568$ Church support 170,847 107,762 278,609 United Way - 814,413 814,413 Fees and grants from government agencies 12,735,173 48,267 12,783,440 Other grants 374,397 447,828 822,225

Total public support 13,928,503 1,824,752 15,753,255

RevenueClient and program income 5,125,261 63,124 5,188,385 Adoptive income 204,268 - 204,268 Investment return 221,265 10,008 231,273 Rent income 585,182 - 585,182 Donated supplies income 125,308 - 125,308 Unrealized gain on interest rate swap agreement 23,057 - 23,057 Change in value of split-interest agreements - 14,492 14,492 Distributions from and change in value of

beneficial interest in charitable trusts - (15,146) (15,146) Miscellaneous income 362,105 2,303 364,408

Total revenue 6,646,446 74,781 6,721,227

Net assets released from restrictions 1,690,756 (1,690,756) -

Total public support, revenue, and other support 22,265,705 208,777 22,474,482

ExpensesProgram Services

Residential services 6,012,009 - 6,012,009 Foster care 2,221,555 - 2,221,555 Community services 6,186,074 - 6,186,074 Center for financial resources 918,145 - 918,145 Center for new americans 3,907,267 - 3,907,267 Lutheran housing-apartments 677,292 - 677,292

Supporting Services Management and general 1,844,800 - 1,844,800 Resource development 768,496 - 768,496

Total expenses 22,535,638 - 22,535,638

Excess (Deficit) of Public Support, Revenue, and Other Support over Expenses (269,933) 208,777 (61,156)

Acquisition of non-controlling interest (190,128) - (190,128)

Change in Net Assets (460,061) 208,777 (251,284)

Net Assets, Beginning of Year 12,509,167 4,886,442 17,395,609

Net Assets, End of Year 12,049,106$ 5,095,219$ 17,144,325$

2015

4

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidated Statements of Activities Years Ended June 30, 2015 and 2014

TemporarilyUnrestricted Restricted Total

392,823$ 216,529$ 609,352$ 164,026 216,108 380,134

- 605,975 605,975 12,669,957 4,130 12,674,087

246,603 163,750 410,353 13,473,409 1,206,492 14,679,901

4,896,206 9,202 4,905,408 247,140 - 247,140 816,765 32,873 849,638 622,607 - 622,607

98,472 - 98,472 29,641 - 29,641

- 3,937 3,937

- 5,892 5,892 104,299 400 104,699

6,815,130 52,304 6,867,434

1,084,285 (1,084,285) -

21,372,824 174,511 21,547,335

5,713,191 - 5,713,191 2,191,970 - 2,191,970 5,175,512 - 5,175,512

946,366 - 946,366 3,912,802 - 3,912,802

667,132 - 667,132

1,593,047 - 1,593,047 735,187 - 735,187

20,935,207 - 20,935,207

437,617 174,511 612,128

- - -

437,617 174,511 612,128

12,071,550 4,711,931 16,783,481

12,509,167$ 4,886,442$ 17,395,609$

2014 - Restated

See Notes to Consolidated Financial Statements

Center for Residential Foster Community Financial Center for New

Services Care Services Resources Americans

Salaries 3,768,114$ 948,733$ 3,421,056$ 565,233$ 1,819,683$ Employee health and

retirement benefitsand housing allowance 312,925 90,733 282,794 56,485 139,059

Payroll taxes 369,949 85,242 298,326 49,878 163,108 Travel 87,491 86,193 221,925 14,836 63,639 Conference and training 59,027 27,498 99,357 13,154 63,821 Professional fees 185,293 23,162 204,166 46,961 333,076 Client related expenses 347,063 619,825 749,855 3,056 954,611 Supplies 72,256 55,834 138,151 21,369 41,731 Communications 19,400 26,930 73,565 26,803 43,795 Occupancy expenses 406,249 178,919 353,343 51,544 238,974 Outside printing 3,874 4,699 123,764 43,600 4,659 Dues and subscriptions 5,466 997 7,148 1,250 8,828 Building and equipment

maintenance 1,518 85 296 - - Uncollectibles - - 37,797 - 543 Donated supplies 33,263 35,182 31,133 - 8,029 Miscellaneous expenses 33,126 4,339 22,636 3,422 20,138

5,705,014 2,188,371 6,065,312 897,591 3,903,694

Depreciation and amortization 306,995 33,184 120,762 20,554 3,573

6,012,009$ 2,221,555$ 6,186,074$ 918,145$ 3,907,267$

Program Services

5

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidated Statement of Functional Expenses

Year Ended June 30, 2015

Lutheran Total TotalHousing Program Management Resource Supporting Total

Corporations Services and General Development Services Expenses

43,394$ 10,566,213$ 1,070,403$ 353,844$ 1,424,247$ 11,990,460$

- 881,996 71,495 47,535 119,030 1,001,026 - 966,503 33,577 25,582 59,159 1,025,662 - 474,084 (6,915) 20,488 13,573 487,657 - 262,857 85,821 11,350 97,171 360,028

55,067 847,725 168,213 39,729 207,942 1,055,667 - 2,674,410 1,019 94 1,113 2,675,523

13,725 343,066 63,605 19,717 83,322 426,388 - 190,493 26,410 23,804 50,214 240,707

358,281 1,587,310 69,629 39,338 108,967 1,696,277 6,524 187,120 30,241 133,342 163,583 350,703

- 23,689 7,897 3,808 11,705 35,394

- 1,899 - - - 1,899 4,318 42,658 (1,546) - (1,546) 41,112

- 107,607 - 17,701 17,701 125,308 (84) 83,577 117,154 24,392 141,546 225,123

481,225 19,241,207 1,737,003 760,724 2,497,727 21,738,934

196,067 681,135 107,797 7,772 115,569 796,704

677,292$ 19,922,342$ 1,844,800$ 768,496$ 2,613,296$ 22,535,638$

Supporting Services

See Notes to Consolidated Financial Statements

Center for Residential Foster Community Financial Center for New

Services Care Services Resources Americans

Salaries 3,522,447$ 909,073$ 2,955,943$ 574,583$ 1,856,157$ Employee health and

retirement benefitsand housing allowance 303,556 82,226 232,498 56,007 135,275

Payroll taxes 327,521 78,001 250,250 49,361 163,917 Travel 64,318 82,988 146,697 12,828 70,842 Conference and training 57,274 61,212 46,075 11,674 52,510 Professional fees 172,005 25,228 205,137 60,946 333,398 Client related expenses 342,436 677,322 482,869 1,400 1,010,421 Supplies 79,718 41,282 122,588 23,032 50,792 Communications 22,358 27,421 63,884 25,153 48,373 Occupancy expenses 428,060 146,788 317,302 49,108 139,588 Outside printing 2,361 4,380 131,620 47,540 5,886 Dues and subscriptions 2,933 1,074 5,188 1,070 10,655 Building and equipment

maintenance 2,166 10 1,768 36 - Uncollectibles 897 - 27,163 - - Donated supplies 28,267 18,714 43,165 910 3,210 Miscellaneous expenses 52,157 4,217 28,567 10,374 23,695

5,408,474 2,159,936 5,060,714 924,022 3,904,719

Depreciation andamortization 304,717 32,034 114,798 22,344 8,083

5,713,191$ 2,191,970$ 5,175,512$ 946,366$ 3,912,802$

Program Services

6

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidated Statement of Functional Expenses

Year Ended June 30, 2014

Lutheran Total TotalHousing Program Management Resource Supporting Total

Corporations Services and General Development Services Expenses

52,286$ 9,870,489$ 969,977$ 351,262$ 1,321,239$ 11,191,728$

251 809,813 109,665 41,103 150,768 960,581 - 869,050 87,250 25,749 112,999 982,049 - 377,673 5,390 17,080 22,470 400,143 - 228,745 55,477 11,757 67,234 295,979

60,057 856,771 153,948 18,991 172,939 1,029,710 - 2,514,448 431 - 431 2,514,879

23,908 341,320 45,260 35,787 81,047 422,367 - 187,189 23,169 22,067 45,236 232,425

328,608 1,409,454 29,454 40,827 70,281 1,479,735 4,625 196,412 7,118 135,031 142,149 338,561

- 20,920 4,365 637 5,002 25,922

- 3,980 58 14 72 4,052 2,075 30,135 (51,924) - (51,924) (21,789)

- 94,266 126 4,080 4,206 98,472 2,401 121,411 71,012 22,023 93,035 214,446

474,211 17,932,076 1,510,776 726,408 2,237,184 20,169,260

192,921 674,897 82,271 8,779 91,050 765,947

667,132$ 18,606,973$ 1,593,047$ 735,187$ 2,328,234$ 20,935,207$

Supporting Services

See Notes to Consolidated Financial Statements 7

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidated Statements of Cash Flows

Years Ended June 30, 2015 and 2014

2015 2014Operating Activities

Change in net assets (251,284)$ 612,128$ Adjustments to reconcile change in net assets to net cash (used for) from operating activities

Depreciation 786,659 759,454 Amortization 10,045 6,493 (Gain) loss on sale of property and equipment (255,557) 19,185 Unrealized gain on interest rate swap agreement (23,057) (29,641) Change in value of split-interest agreements (14,492) (3,937) Change in value of beneficial interest in assets held by others (2,719) (39,922) Investment loss (gain) 3,467 (638,497) Acquisition of non-controlling interest 190,128 -

Change in assets and liabilitiesAccounts receivable (48,115) (221,183) Accrued income receivable (451,875) 331,051 Prepaid expenses 9,703 14,946 Accounts payable (139,065) 164,050 Accrued liabilities 47,709 235,234 Deferred revenue (18,858) (31,237)

Net Cash (used for) from Operating Activities (157,311) 1,178,124

Investing ActivitiesPurchase of long-term investments (2,507,567) (1,541,237) Sales and maturities of long-term investments 2,589,852 1,535,659 Change in restricted deposits and funded reserves (36,218) (13,063) Cash received on notes receivable 7,699 7,427 Cash received on sale of property and equipment 796,430 456,609 Net purchases of property and equipment (653,227) (428,734)

Net Cash from Investing Activities 196,969 16,661

Financing ActivitiesAdvances on long-term debt 272,500 - Principal payments on long-term debt (468,384) (443,692) Net change in lines of credit 636,914 - Payments to beneficiaries of split-interest agreements (990) (990) Purchase of non-controlling interest (290,000) -

Net Cash from (used for) Financing Activities 150,040 (444,682)

Net Change in Cash and Cash Equivalents 189,698 750,103

Beginning Cash and Cash Equivalents 1,118,132 368,029

Ending Cash and Cash Equivalents 1,307,830$ 1,118,132$

See Notes to Consolidated Financial Statements 8

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidated Statements of Cash Flows

Years Ended June 30, 2015 and 2014

2015 2014

Supplemental Disclosures of Cash Flow InformationCash payments for interest 240,444$ 248,873$

Noncash Investing and Financing ActivitiesRepayment of long-term debt upon sale of property and equipment 791,090$ -$

9

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 1 - Nature of Activities and Summary of Significant Accounting Policies Nature of Activities Lutheran Social Services of South Dakota, Inc. and consolidated affiliates (the Organization) are nonprofit corporations organized under the laws of the State of South Dakota for the purpose of providing social services with the church and other community health and welfare organizations. Principles of Consolidation The accompanying consolidated financial statements also include the accounts of Lutheran Social Services of South Dakota Foundation, Inc., Lutheran Housing Corporation/Broadway, Lutheran Housing Corporation/Meadowlands, Lutheran Housing Corporation/Northport, Lutheran Housing Corporation/Gateway, and Lutheran Housing Corporation/Prairie Lakes, which are nonprofit South Dakota corporations under common control. Lutheran Housing Corporation/Gateway was a 1% managing general partner of Gateway Apartments Limited Partnership. Lutheran Housing Corporation/Broadway, Lutheran Housing Corporation/Meadowlands, Lutheran Housing Corporation/Northport, Gateway Apartments Limited Partnership, and Lutheran Housing Corporation/Prairie Lakes were formed for the purpose of developing elderly/family congregate housing projects. All inter-organization transactions were eliminated in the accompanying consolidated financial statements. Effective January 1, 2015, Lutheran Housing Corporation/Gateway purchased the non-controlling interest of Gateway Apartments Limited Partnership. Lutheran Housing Corporation/Gateway sold all of its property and equipment effective June 15, 2015. Cash and Cash Equivalents The Organization considers all cash and highly liquid financial instruments with original maturities of three months or less, and which are neither held for nor restricted by donors for long-term purposes, to be cash and cash equivalents. Cash and highly liquid financial instruments restricted to capital expenditures, or other long-term purposes of the Organization are excluded from this definition. Receivables and Credit Policies Trade receivables are uncollateralized customer obligations due under normal trade terms requiring payment within 30 days from the invoice date. Trade receivables are stated at the amount billed to the customer. Customer account balances with invoices dated over 60 days old are considered delinquent. Payments of trade receivables and notes receivable are allocated to the specific invoices identified on the customer’s remittance advice or, if unspecified, are applied to the earliest unpaid invoices. Management determines the allowance for uncollectable accounts receivable based on historical experience, an assessment of economic conditions, and a review of subsequent collections. Accounts receivable are written off when deemed uncollectable. At June 30, 2015 and 2014, the allowance was $26,465 and $28,011, respectively. Investments Investment purchases are recorded at cost, or if donated, at fair value on the date of donation. Thereafter, investments are reported at their fair values in the consolidated statements of financial position. Net investment gain/(loss) is reported in the statements of activities and consists of interest and dividend income, realized and unrealized capital gains and losses.

10

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Assets Held and Liabilities Under Split-Interest Agreements Charitable Gift Annuities Under charitable gift annuity contracts, the Foundation receives immediate and unrestricted title to contributed assets and agrees to make fixed recurring payments over the stipulated period. Contributed assets are recorded at fair value on the date of receipt. The related liability for future payments to be made to the specified beneficiaries is recorded at fair value using present value techniques and risk-adjusted discount rates designed to reflect the assumptions market participants would use in pricing the liability. The excess of contributed assets over the annuity liability is recorded as an unrestricted contribution. In subsequent years, the liability for future annuity payments is reduced by payments made to the specified beneficiaries and is adjusted to reflect amortization of the discount and changes in actuarial assumptions at the end of the year. Upon termination of the annuity contract, the remaining liability is removed and recognized as income. Beneficial Interests in Charitable Trusts Held by Others The Foundation has been named as an irrevocable beneficiary of several charitable trusts held and administered by independent trustees. These trusts were created independently by donors and are administered by ELCA as designated by the donors. Therefore, the Foundation has neither possession nor control over the assets of the trusts. At the date the Foundation receives notice of a beneficial interest, a temporarily or permanently restricted contribution is recorded in the consolidated statement of activities, and a beneficial interest in charitable trusts held by others is recorded in the statement of financial position at fair value using present value techniques and risk-adjusted discount rates designed to reflect the assumptions market participants would use in pricing the expected distributions to be received under the agreement. Thereafter, beneficial interests in the trusts are reported at fair value in the statements of financial position, with trust distributions and changes in fair value recognized in the statement of activities. Upon receipt of trust distributions and/or expenditures in satisfaction of the restricted purpose stipulated by the donor, if any, temporarily restricted net assets are released to unrestricted net assets. Fair Value Measurements Certain assets and liabilities are reported at fair value in the consolidated financial statements. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal, or most advantageous, market at the measurement date under current market conditions regardless of whether that price is directly observable or estimated using another valuation technique. Inputs used to determine fair value refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability based on the best information available. A three-tier hierarchy categorizes the inputs as follows:

Level 1 – quoted prices (unadjusted) in active markets for identical assets or liabilities that the Organization can access at the measurement date. Level 2 – Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly. These include quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability, and market-corroborated inputs.

11

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014

Level 3 – Unobservable inputs for the asset or liability. In these situations, the Organization develops inputs using the best information available in the circumstances.

Property and Equipment Property and equipment additions over $2,000 are recorded at cost, or if donated, at fair value on the date of donation. Depreciation and amortization are computed using the straight-line method over the estimated useful lives of the assets ranging from three to forty years, or in the case of capitalized leased assets or leasehold improvements, the lesser of the useful life of the asset or the lease term. Depreciation expense is allocated to the various functions on a specific basis for certain assets and on a square footage basis for certain other assets. When assets are sold or otherwise disposed of, the cost and related depreciation or amortization are removed from the accounts, and any remaining gain or loss is included in the statement of activities. Costs of maintenance and repairs that do not improve or extend the useful lives of the respective assets are expensed currently. The Organization reviews the carrying values of property and equipment for impairment whenever events or circumstances indicate that the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. When considered impaired, an impairment loss is recognized to the extent carrying value exceeds the fair value of the asset. There was no indication of asset impairment during the years ended June 30, 2015 and 2014. Financial Instruments and Credit Risk The Organization manages deposit concentration risk by placing cash, money market accounts, and certificates of deposit with financial institutions believed by management to be creditworthy. At times, amounts on deposit may exceed insured limits or include uninsured investments in money market mutual funds. To date, the Organization has not experienced losses in any of these accounts. Credit risk associated with accounts receivable is considered to be limited due to high historical collection rates and because substantial portions of the outstanding amounts are due from governmental agencies, and organizations supportive of the Organization’s mission. Investments are made by diversified investment managers whose performance is monitored by management and the Investment Committee of the Board of Directors. Although the fair values of investments are subject to fluctuation on a year-to-year basis, management and the Investment Committee believe that the investment policies and guidelines are prudent for the long-term welfare of the Organization. Interest Rate Exchange Agreement The Organization uses an interest-rate swap to mitigate interest-rate risk on a note payable (Note 9). The related liability or asset is reported at fair value in the statements of financial position, and unrealized losses or gains are included in the consolidated statements of activities. Net Assets Net assets, revenues, gains, and losses are classified based on the existence or absence of donor-imposed restrictions. Accordingly, net assets and changes therein are classified and reported as follows:

Unrestricted Net Assets – Net assets available for use in general operations. Unrestricted board-designated net assets consist of net assets designated by the Board of Directors for operating reserve and quasi-endowment.

12

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014

Temporarily Restricted Net Assets – Net assets subject to donor restrictions that may or will be met by expenditures or actions of the Organization and/or the passage of time, and certain income earned on permanently restricted net assets that has not yet been appropriated for expenditure by the Organization’s Board of Directors.

The Organization reports contributions as temporarily restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the consolidated statements of activities as net assets released from restrictions. Permanently Restricted Net Assets – Net assets whose use is limited by donor-imposed restrictions that neither expire by the passage of time nor can be fulfilled or otherwise removed by action of the Organization. The Organization had no permanently restricted net assets.

Change in Accounting Principle The Organization changed its method of recognizing donor restricted contributions effective July 1, 2014. To more efficiently account for the donor restricted contributions, all contributions with donor time or purpose restrictions are reflected as temporarily restricted support, regardless of when the restriction expires. Previously, donor restricted contributions whose restrictions were met within the same fiscal year as received were reflected as unrestricted. Comparative consolidated financial statements of the prior year have been adjusted to apply the new method retrospectively. As a result of the accounting change, certain line items in the 2014 consolidated statements of activities were affected. Unrestricted total public support decreased by $189,266 and temporarily restricted total public support increased by $189,266. Unrestricted total revenue decreased by $9,202 and temporarily restricted total revenue increased by $9,202. Net assets released from restrictions increased by $198,468. There were no changes to the 2014 consolidated statements of financial position, functional expenses, or cash flows, as a result of the accounting change. Revenue and Revenue Recognition Revenue is recognized when earned. Program service fees and payments under cost-reimbursable contracts received in advance are deferred to the applicable period in which the related services are performed or expenditures are incurred, respectively. Contributions are recognized when cash, securities or other assets, an unconditional promise to give, or notification of a beneficial interest is received. Conditional promises to give are not recognized until the conditions on which they depend have been substantially met. Donated Services and In-Kind Contributions Volunteers contribute significant amounts of time to the Organization’s program services, administration, and fundraising and development activities; however, the financial statements do not reflect the value of these contributed services because they do not meet recognition criteria prescribed by generally accepted accounting principles. Contributed goods are recorded at fair value at the date of donation. The Organization records donated professional services at the respective fair values of the services received. Donated materials and services for the years ended June 30, 2015 and 2014, were approximately $125,000 and $98,000, respectively.

13

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Management estimates that volunteers donated approximately 81,400 and 57,100 hours of service in 2015 and 2014, respectively. Functional Allocation of Expenses The costs of providing the various programs and other activities have been summarized on a functional basis in the consolidated statements of activities. The statements of functional expenses present the natural classification detail of expenses by function. Accordingly, certain costs have been allocated among the programs and supporting services benefited based upon specific identification where possible and estimates made by management. Advertising Advertising and promotion costs are expensed as incurred. Such costs were $314,038 and $283,988 for the years ending June 30, 2015 and 2014, respectively. Fundraising The Organization incurred expenses amounting to $768,496 and $735,187 for the years ended June 30, 2015 and 2014, respectively, related to development and fundraising. Such amounts are reflected as resource development expenses in the accompanying consolidated statements of activities. Estimates The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates and those differences could be material. Income Taxes Lutheran Social Services of South Dakota, Inc. and consolidated corporations are organized as South Dakota nonprofit corporations and have been recognized by the Internal Revenue Service (IRS) as exempt from federal income taxes under Section 501(a) of the Internal Revenue Code as organizations described in Section 501(c)(3). Each entity is annually required to file a Return of Organization Exempt from Income Tax (Form 990) with the IRS. In addition, the entities are subject to income tax on net income that is derived from business activities that are unrelated to their exempt purposes. Each entity has determined it is not subject to unrelated business income tax and has not filed an Exempt Organization Business Income Tax Return (Form 990-T) with the IRS. Each entity believes that it has appropriate support for any tax positions taken affecting its annual filing requirements, and as such, does not have any uncertain tax positions that are material to the financial statements. The entities would recognize future accrued interest and penalties related to unrecognized tax benefits and liabilities in income tax expense if such interest and penalties are incurred. Reclassifications Certain reclassifications have been made to the 2014 consolidated financial statements to conform to the 2015 presentation. The reclassifications had no effect on previously reported change in net assets.

14

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 2 - Cash and Cash Equivalents

2015 2014Undesignated

Cash on hand 3,395$ 2,885$ Cash in checking 1,253,160 1,018,811

Total undesignated 1,256,555 1,021,696 Designated for apartment project operations 51,275 96,436

Total cash and cash equivalents 1,307,830$ 1,118,132$

Note 3 - Investments

2015 2014

Cash and cash equivalents 36,344$ 185,930$ Certificates of deposit 1,072,634 1,071,395 Mutual funds - equity

securities 3,621,738 3,408,234 Mutual funds - fixed income 1,885,587 1,893,085 Life insurance policies 11,160 154,571

Total investments 6,627,463$ 6,713,215$

The above investments are included on the consolidated statements of financial position as:

2015 2014

Investments 6,317,901$ 6,412,671$ Assets held under split-interest agreements 309,562 300,544

6,627,463$ 6,713,215$

The investment return for the years ended June 30, 2015 and 2014, consists of the following components:

2015 2014Interest earned, dividends received,

and mutual fund capital gains reinvested 234,740$ 211,141$ Realized and unrealized (loss) gain on securities (3,467) 638,497

231,273$ 849,638$

15

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 4 - Note Receivable In 2011, the Organization sold property located in Beresford, SD for $285,000 under a contract for deed. The contract for deed is recorded as a note receivable and had a balance of $214,273 and $221,972 as of June 30, 2015 and 2014, respectively. The note is due in quarterly installments of $1,688 through July 1, 2012 at 0%, and in monthly installments with interest at 2% through August 1, 2011, 3% through August 1, 2012, 5% through August 1, 2013, 7% through August 1, 2015, when the full unpaid balance of principal and interest is due. Principal payments to be received on note receivable are $214,273 for the year ending June 30, 2016. Note 5 - Fair Value of Investments Assets and liabilities measured at fair value on a recurring basis at June 30, 2015 and 2014 are as follows:

2015 2014

Certificates of deposit 1,072,634$ 1,071,395$ Mutual funds 5,507,325 5,301,319 Beneficial interest in charitable trusts held by others 245,500 242,781

Total assets 6,825,459$ 6,615,495$

Liabilities under split-interest agreements 89,117$ 104,599$ Interest rate swap agreement 299,085 322,143

Total liabilities 388,202$ 426,742$

16

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 The related fair values of these assets and liabilities are determined as follows:

OtherQuoted Prices in Observable UnobservableActive Markets Observable Inputs

(Level 1) (Level 2) (Level 3)

Certificates of deposit -$ 1,072,634$ -$ Mutual funds 5,507,325 - - Beneficial interest in charitable trusts

held by others - - 245,500

Total assets 5,507,325$ 1,072,634$ 245,500$

Liabilities under split-interest agreements -$ -$ 89,117$ Interest rate swap agreement - 299,085 -

Total liabilities -$ 299,085$ 89,117$

Certificates of deposit -$ 1,071,395$ -$ Mutual funds 5,301,319 - - Beneficial interest in charitable trusts

held by others - - 242,781

Total assets 5,301,319$ 1,071,395$ 242,781$

Liabilities under split-interest agreements -$ -$ 104,599$ Interest rate swap agreement - 322,143 -

Total liabilities -$ 322,143$ 104,599$

June 30, 2015

June 30, 2014

The fair value for mutual funds is determined by reference to quoted market prices. The certificates of deposit are valued by the custodian of the securities using pricing models based on credit quality, time to maturity, stated interest rates and market-rate assumptions, and are classified within Level 2. For charitable remainder trusts, fair value is estimated at present value of future cash flows. For the interest rate swap agreement, fair value is estimated at the present value of expected future cash flows. The fair value of the interest rate swap is based upon estimates of the related LIBOR swap rate during the term of the swap agreement.

17

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Following is a reconciliation of activity for assets/liabilities measured at fair value based upon significant unobservable (non-market) information for 2014 and 2015:

Beneficial LiabilititesInterest in UnderCharitable Split-Interest

Trusts Agreements

Balance, July 1, 2013 202,859$ (109,526)$ New gifts 34,030 - Change in value 5,892 3,937 Settlements - 990

Balance, June 30, 2014 242,781$ (104,599)$ New gifts 17,865 - Change in value (15,146) 14,492 Settlements - 990

Balance, June 30, 2015 245,500$ (89,117)$

Note 6 - Restricted Assets Pursuant to the regulatory agreements and mortgage agreements with the South Dakota Housing and Development Authority and the U.S. Department of Housing and Urban Development, the Organizations are required to provide cash escrow accounts to fund repairs and maintenance expenses, insurance expenses, development costs, and residual receipts. Total restricted assets as of June 30, 2015 and 2014, were $235,063 and $198,845, respectively. The regulatory agreements and mortgage agreements with the South Dakota Housing and Development Authority and the U.S. Department of Housing and Urban Development also provide for restrictive operating procedure and loan covenants. As of June 30, 2015, the Organizations are in compliance with these agreements.

18

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 7 - Property and Equipment

2014 Accumulated

Useful Life Cost Depreciation Net Net

Land 1,043,367$ -$ 1,043,367$ 1,196,673$ Buildings and 15 - 40 years 16,669,953 4,564,451 12,105,502 13,421,687

improvementsFurniture and equipment 7 - 14 years 2,943,072 2,381,607 561,465 556,309 Automobiles 3 - 5 years 745,574 412,129 333,445 284,633

21,401,966$ 7,358,187$ 14,043,779$ 15,459,302$

2015

Property acquired with federal HUD grants is considered owned by the Organization; however, the grantor agency has interests in certain property. The amount of property acquired with these grants was $3,531,483 at June 30, 2015 and 2014, and is reflected as temporarily restricted net assets. Note 8 - Lines of Credit A line-of-credit agreement has been executed in the total amount of $750,000 on a revolving basis. This line-of-credit expires on March 31, 2016. Interest on unpaid principal is payable monthly at a rate of 1.25% over the Prime Rate set from time to time by the lender, with a minimum rate of 5.00%. The balance outstanding on this line-of-credit at June 30, 2015 was $636,914. An additional line-of-credit agreement has been executed in the total amount of $50,000 on a revolving basis. This line-of-credit expires on March 30, 2016. Interest on unpaid principal is payable monthly at a rate of 2.25% over the Prime Rate set from time to time by the lender, with a minimum rate of 5.50%. The Organization did not have a balance outstanding on this line-of-credit at June 30, 2015.

19

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 9 - Notes Payable Details pertaining to notes and mortgages payable are as follows:

2015 20143.00% note payable to Great Western Bank, due in monthlyinstallments of $3,583, including interest, through August 11, 2015,when a balloon payment is due, secured by a certificate of deposit 263,346$ 298,353$

Wells Fargo, 0.89% bond dated October 29, 1997, collateralizedby substantially all the organization's real estate, payable inmonthly installments of $10,933, including interest throughNovember 1, 2017 296,177 417,835

3.00% note payable to Mission Investment Fund of the Evangelical Lutheran Church in America, interest only payments until February 1, 2016, thereafter monthly principal and interest paymentsof $1,292 through January 1, 2018, when full payment is due,secured by a certificate of deposit 272,500 -

4.15% note payable to Wells Fargo, due in monthly installments of $6,471, including interest, paid in full upon sale of Gatewayin June 2015 - 827,466

1% note payable to U.S. Department of Housing and Urban Development, due in monthly installments of $4,549, includinginterest if cash allows, due December 31, 2019, secured by residential buildings (Meadowlands Apartments) 81,390 81,390

Zero interest note payable to South Dakota Housing Development Authority, due in monthly installments through June 2023(Broadway Apartments) 96,664 104,715

Zero interest note payable to South Dakota Housing Development Authority, with principal deferred from 2000 to 2005, thereafter, monthly principal payments of $150 a month for 240 monthsthrough 2024 (Meadowlands Apartments) 15,050 16,550

Zero interest note payable to South Dakota Housing Development Authority, with principal deferred to January 1, 2025, whenfull payment is due (Meadowlands Apartments) 36,000 36,000

Variable rate (3.31% at June 30, 2015) note payable to FirstWestern Bank, due in monthly installments of $6,670, includinginterest, due August 1, 2025, secured by real property (CanyonHills) 518,295 579,864

20

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014

2015 2014Variable rate (1.32145% at June 30, 2015) Minnehaha County,South Dakota Economic Development Revenue Bonds, Series 2006due in monthly installments, plus interest, due February 1, 2027,secured by real property 2,795,273 2,967,605

3.75% note payable to State Bank of Alcester, due in monthlyinstallments of $2,380, including interest, due March 1, 2033,secured by real property (Stepping Stones) 368,840 382,699

4.125% note payable to U.S. Department of Agriculture,due in monthly installments of $4,793, including interest,due July 27, 2045, secured by real property (Canyon Hills) 987,550 1,005,582

5,731,085$ 6,718,059$

Annual principal and interest payments of $4,549 on the U.S. Department of Housing and Urban Development mortgage are due only if the project generates sufficient restricted net cash. All restricted net cash generated by the project is required to pay any principal and interest payment currently due or in arrears. To minimize the effect of changes in the interest rate, in October 2006, the Organization entered into an interest rate exchange agreement on $3,000,000 of the South Dakota Economic Development Revenue Series 2006 bonds to set the interest at a fixed rate of 4.81% until maturity. Under the agreement, the Organization either pays additional interest or receives an interest credit depending on the relationship between the variable rate and the fixed rate. The Organization recorded unrealized gains in the amount of $23,057 and $29,641 relating to the agreement for the years ended June 30, 2015 and 2014, respectively. Accordingly, the Organization recorded interest rate exchange liabilities equal to the estimated market value in the consolidated statements of financial position as of June 30, 2015 and 2014 of $299,085 and $322,143, respectively. Interest expense for the years ended June 30, 2015 and 2014, was $240,444 and $248,873, respectively. Minimum principal payments on the notes are as follows for the years ended June 30:

2016 3,379,294$ 2017 233,036 2018 416,670 2019 108,923 2020 194,154 Thereafter 1,399,008

5,731,085$

Broadway Apartments has experienced a shortage of cash flows during 2015 and 2014 due to low occupancy. As a result, the required payments were not made on the note payable to South Dakota Housing Development Authority during 2015 and 2014. Therefore, the carrying amount of $96,664 is included in the 2016 minimum principal payments above. The Minnehaha County bond covenants require the Organization to meet certain financial ratios and other requirements. The Organization was not in compliance with the debt coverage ratio as of June 30, 2015. As a result, the balance of the Minnehaha County bond is included in the 2016 principal payments above.

21

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 10 - Net Assets

2015 2014Unrestricted net assets

Designated by the board of the foundationfor endowment purposes 4,631,669$ 4,502,808$

Designated for apartment project operations (checking account) 51,275 96,436 Undesignated 7,366,162 7,672,415 Non-controlling interest - 237,508

12,049,106 12,509,167

Temporarily restricted net assetsRestricted for

Time restricted contributions-split interest agreements 220,445 195,945 Time restricted contributions-United Way contributions 508,824 340,635 ELCA and other annuities 245,500 242,781 Refugee resettlement and placement 59,619 70,172 Disaster response 223,399 153,100 Community services 168,244 198,221 Children and youth programs 42,705 59,105 Capital assets 3,626,483 3,626,483

5,095,219 4,886,442

Total net assets 17,144,325$ 17,395,609$

Net assets were released from donor restrictions by incurring the expenses satisfying the restricted purposes or by occurrence of events specified by donors.

Temporarily TemporarilyUnrestricted Restricted Unrestricted Restricted

Time restricted contributions-United Way 646,224$ (646,224)$ 591,178$ (591,178)$

Refugee resettlement andplacement 69,412 (69,412) 36,830 (36,830)

Disaster response 453,696 (453,696) 135,125 (135,125) Community services 457,752 (457,752) 153,128 (153,128) Children and youth programs 63,672 (63,672) 168,024 (168,024)

Total net assets releasedfrom restrictions 1,690,756$ (1,690,756)$ 1,084,285$ (1,084,285)$

20142015Restated

22

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 11 - Endowment Net Asset Composition by Type of Fund The Organization’s endowment consists of funds that have been gifted to the Organization by donors with no restrictions and have been designated as funds functioning as endowment by the board of directors. In the event that funds received by the Organization in the future are endowed by the donor, they will be treated as permanently restricted. As required by generally accepted accounting principles, net assets associated with endowment funds, including funds designated by the Board of Directors to function as endowments, are classified and reported based on the existence or absence of donor-imposed restrictions. Interpretation of Relevant Law The Board of Directors of the Organization has interpreted the Uniform Prudent Management of Institutional Funds Act (UPMIFA) as requiring the preservation of the fair value of the original gift as of the gift date of the donor-restricted endowment funds absent explicit donor stipulations to the contrary. As a result of this interpretation, Lutheran Social Services will classify as permanently restricted net assets (a) the original value of gifts donated to the permanent endowment, (b) the original value of subsequent gifts to the permanent endowment, and (c) accumulations to the permanent endowment made in accordance with the direction of the applicable donor gift instrument at the time the accumulation is added to the fund. The remaining portion of the donor-restricted endowment fund that is not classified in permanently restricted net assets will be classified as temporarily restricted net assets until those amounts are appropriated for expenditure by the organization in a manner consistent with the standard of prudence prescribed by UPMIFA. In accordance with UPMIFA, the organization will consider the following factors in making a determination to accumulate donor-restricted endowment funds: (1) The duration and preservation of the fund, (2) The purposes of the organization and the donor-restricted endowment fund, (3) General economic conditions, (4) The possible effect of inflation and deflation, (5) The expected total return from income and the appreciation of investments, (6) Other resources of the organization, and (7) The investment policies of the organization. Endowment Net Asset Composition by Type of Fund as of June 30, 2015 is as follows:

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Board-designated endowment funds 4,631,669$ -$ -$ 4,631,669$

23

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Endowment net assets,4,502,808$ -$ -$ 4,502,808$

Investment return:Investment income 178,089 - - 178,089

Net realized and unrealizeddepreciation (12,339) - - (12,339)

Appropriation of endowmentassets for expenditure (184,884) - - (184,884)

Other changes:Transfers to create board-

designated funds 147,995 - - 147,995

Endowment net assets,4,631,669$ -$ -$ 4,631,669$ June 30, 2015

June 30, 2014

Endowment Net Asset Composition by Type of Fund as of June 30, 2014 is as follows:

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Board-designated endowment funds 4,502,808$ -$ -$ 4,502,808$

Temporarily PermanentlyUnrestricted Restricted Restricted Total

Endowment net assets,4,003,952$ -$ -$ 4,003,952$

Investment return:Investment income 157,198 - - 157,198

Net realized and unrealizedappreciation 506,012 - - 506,012

Appropriation of endowmentassets for expenditure (174,240) - - (174,240)

Other changes:Transfers to create board-

designated funds 9,886 - - 9,886

Endowment net assets,4,502,808$ -$ -$ 4,502,808$ June 30, 2014

June 30, 2013

24

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Return Objectives and Risk Parameters The Organization has adopted investment and spending policies for investment assets that attempt to provide a predictable stream of funding to programs supported by its endowment while seeking to maintain the purchasing power of the endowment assets. Investment assets include those assets of donor-specific funds that the organization will designate for a specific purpose as well as board-designated funds. Under this policy, the assets are invested in a manner that seeks both preservation of capital and growth of capital on a real return basis. Asset allocation guidelines have been established for the assets based on liquidity needs and time horizon. The rebalancing of assets will occur annually, or as needed and will be reviewed by the board of directors. During the course of a complete market cycle, the total return objective shall be to achieve a return greater than capital market returns with a similarly weighted asset allocation. Actual returns in any given year may vary from this amount. Strategies Employed for Achieving Objectives To satisfy its long-term rate-of-return objectives, the Organization relies on a total return strategy in which investment returns are achieved through both capital appreciation (realized and unrealized) and current yield (interest and dividends). The Organization targets a diversified asset allocation that places a greater emphasis on equity-based investments to achieve its long-term return objectives within prudent risk constraints. Spending Policy and How the Investment Objectives Relate to Spending Policy The Organization has a policy of appropriating for distribution each year 5 percent of its endowment fund's average fair value over the prior 12 quarters through the calendar year-end preceding the fiscal year in which the distribution is planned. In establishing this policy, the Organization considered the long-term expected return on its endowment. Note 12 - Leases The Organization leases certain property, building space, and vehicles under various lease agreements with varying terms. Total lease expense for all operating leases and rental agreements was $520,504 and $342,212 for the years ended June 30, 2015 and 2014, respectively. Minimum future lease payments for non-cancelable operating leases are as follows:

Years Ending June 30,

438,026$ 316,714 210,830 147,073

1 Thereafter 73

1,112,717$

20162017201820192020

25

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Notes to Consolidated Financial Statements

June 30, 2015 and 2014 Note 13 - Pension Plan The Organization has a 401(k) (defined contribution) pension plan covering substantially all of its full-time employees. Pension expense was $129,903 and $152,033 for the years ended June 30, 2015 and 2014, respectively. Note 14 - Support from Governmental Units The Organization receives a substantial amount of its support from federal, state, and local governments. A significant reduction in the level of this support, if it were to occur, may have a significant effect on the Organization’s programs and activities. Note 15 - Subsequent Events In September 2015 the Organization executed a real estate purchase agreement to purchase property in Sioux Falls, South Dakota at a purchase price of $3,500,000. The purchase is financed under a contract for deed with monthly payments commencing October 1, 2015 through December 31, 2017, at which time the remaining balance is anticipated to be paid with contributions received from a capital campaign. As a condition of the agreement, the Organization will lease a portion of the property back to the seller. Anticipated lease income will range from $120,000 to $143,000 annually, commencing October 1, 2015 through December 31, 2022. In addition, subsequent to June 30, 2015, the Responsible Fatherhood Grant was not renewed. The federal award was $1,229,141 for the grant period ended September 29, 2015. The Organization has evaluated subsequent events through November 10, 2015, the date which the financial statements were available to be issued.

www.eidebai l ly.com

Supplementary Information June 30, 2015 and 2014

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates

26

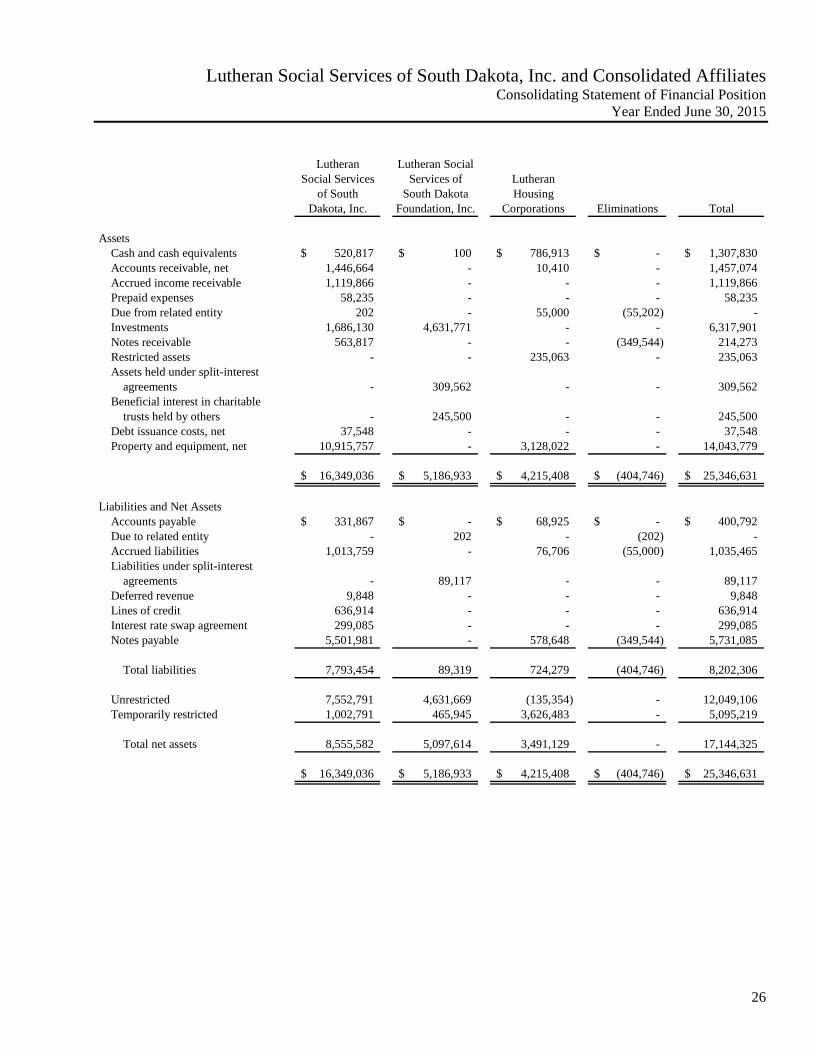

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidating Statement of Financial Position

Year Ended June 30, 2015

Lutheran Lutheran SocialSocial Services Services of Lutheran

of South South Dakota HousingDakota, Inc. Foundation, Inc. Corporations Eliminations Total

AssetsCash and cash equivalents 520,817$ 100$ 786,913$ -$ 1,307,830$ Accounts receivable, net 1,446,664 - 10,410 - 1,457,074 Accrued income receivable 1,119,866 - - - 1,119,866 Prepaid expenses 58,235 - - - 58,235 Due from related entity 202 - 55,000 (55,202) - Investments 1,686,130 4,631,771 - - 6,317,901 Notes receivable 563,817 - - (349,544) 214,273 Restricted assets - - 235,063 - 235,063 Assets held under split-interest

agreements - 309,562 - - 309,562 Beneficial interest in charitable

trusts held by others - 245,500 - - 245,500 Debt issuance costs, net 37,548 - - - 37,548 Property and equipment, net 10,915,757 - 3,128,022 - 14,043,779

16,349,036$ 5,186,933$ 4,215,408$ (404,746)$ 25,346,631$

Liabilities and Net AssetsAccounts payable 331,867$ -$ 68,925$ -$ 400,792$ Due to related entity - 202 - (202) - Accrued liabilities 1,013,759 - 76,706 (55,000) 1,035,465 Liabilities under split-interest

agreements - 89,117 - - 89,117 Deferred revenue 9,848 - - - 9,848 Lines of credit 636,914 - - - 636,914 Interest rate swap agreement 299,085 - - - 299,085 Notes payable 5,501,981 - 578,648 (349,544) 5,731,085

Total liabilities 7,793,454 89,319 724,279 (404,746) 8,202,306

Unrestricted 7,552,791 4,631,669 (135,354) - 12,049,106 Temporarily restricted 1,002,791 465,945 3,626,483 - 5,095,219

Total net assets 8,555,582 5,097,614 3,491,129 - 17,144,325

16,349,036$ 5,186,933$ 4,215,408$ (404,746)$ 25,346,631$

27

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidating Statement of Financial Position

Year Ended June 30, 2014

Lutheran Lutheran SocialSocial Services Services of Lutheran

of South South Dakota HousingDakota, Inc. Foundation, Inc. Corporations Eliminations Total

AssetsCash and cash equivalents 1,021,696$ -$ 96,436$ -$ 1,118,132$ Accounts receivable, net 1,402,506 - 6,453 - 1,408,959 Accrued income receivable 667,991 - - - 667,991 Prepaid expenses 68,905 - 3,768 - 72,673 Due from related entity 677 - 55,000 (55,677) - Investments 1,909,186 4,503,485 - - 6,412,671 Notes receivable 283,915 - - (61,943) 221,972 Restricted assets - - 198,845 - 198,845 Assets held under split-interest

agreements - 300,544 - - 300,544 Beneficial interest in charitable

trusts held by others - 242,781 - - 242,781 Debt issuance costs, net 42,858 - - - 42,858 Property and equipment, net 10,980,673 - 4,478,629 - 15,459,302

16,378,407$ 5,046,810$ 4,839,131$ (117,620)$ 26,146,728$

Liabilities and Net AssetsAccounts payable 464,846$ -$ 75,010$ -$ 539,856$ Due to related entity - 677 - (677) - Accrued liabilities 964,544 - 128,212 (55,000) 1,037,756 Liabilities under split-interest

agreements - 104,599 - - 104,599 Deferred revenue 28,706 - - - 28,706 Interest rate swap agreement 322,143 - - - 322,143 Notes payable 5,651,938 - 1,125,665 (59,544) 6,718,059

Total liabilities 7,432,177 105,276 1,328,887 (115,221) 8,751,119

UnrestrictedControlling interest 8,124,997 4,502,808 (353,747) (2,399) 12,271,659 Non-controlling interest - - 237,508 - 237,508

Temporarily restricted 821,233 438,726 3,626,483 - 4,886,442

Total net assets 8,946,230 4,941,534 3,510,244 (2,399) 17,395,609

16,378,407$ 5,046,810$ 4,839,131$ (117,620)$ 26,146,728$

Lutheran Social Services of Lutheran Social Services ofSouth Dakota, Inc. South Dakota Foundation, Inc.

Temporarily TemporarilyUnrestricted Restricted Unrestricted Restricted

Public Support, Revenue, and Other SupportPublic support:

Contributions 481,136$ 388,617$ 166,950$ 17,865$ Church support 170,847 107,762 - - United Way - 814,413 - - Fees and grants from government agencies 12,735,173 48,267 - - Other grants 374,397 447,828 - -

13,761,553 1,806,887 166,950 17,865 Revenue:

Client and program income 5,125,261 63,124 - - Adoptive income 204,268 - - - Investment return 55,515 - 165,750 10,008 Rent income 2,575 - - - Donated supplies income 125,308 - - - Unrealized gain on interest rate swap agreement 23,057 - - - Change in value of split-interest agreements - - - 14,492 Distributions from and change in value of beneficial

interest in charitable trusts held by others - - - (15,146) Miscellaneous income (loss) 112,963 2,303 (18,955) -

5,648,947 65,427 146,795 9,354

Net assets released from restrictions 1,690,756 (1,690,756) - -

Total public support, revenue, and other support 21,101,256 181,558 313,745 27,219

ExpensesProgram services:

Residential services 6,012,009 - - - Foster care 2,221,555 - - - Community services 6,186,074 - - - Center for financial resources 918,145 - - - Center for new americans 3,907,267 - - - Lutheran housing - apartments - - - -

Supporting services:Management and general 1,844,800 - - - Fundraising and communications 768,496 - - -

21,858,346 - - - Excess (Deficit) of Public Support, Revenue,

and Other Support over Expenses (757,090) 181,558 313,745 27,219

Intercompany Transfers 184,884 - (184,884) -

Acquisition of non-controlling interest - - - -

Change in Net Assets (572,206) 181,558 128,861 27,219

Net Assets, Beginning of Year 8,124,997 821,233 4,502,808 438,726

Net Assets, End of Year 7,552,791$ 1,002,791$ 4,631,669$ 465,945$

28

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidating Statement of Activities

Year Ended June 30, 2015

TemporarilyUnrestricted Restricted Eliminations Total

-$ -$ -$ 1,054,568$ - - - 278,609 - - - 814,413 - - - 12,783,440 - - - 822,225 - - - 15,753,255

- - - 5,188,385 - - - 204,268 - - - 231,273

582,607 - - 585,182 - - - 125,308 - - - 23,057 - - - 14,492

- - - (15,146) 268,097 - - 364,408 850,704 - - 6,721,227

- - - -

850,704 - - 22,474,482

- - - 6,012,009 - - - 2,221,555 - - - 6,186,074 - - - 918,145 - - - 3,907,267

679,691 - (2,399) 677,292

- - - 1,844,800 - - - 768,496

679,691 - (2,399) 22,535,638

171,013 - 2,399 (61,156)

- - - -

(190,128) - - (190,128)

(19,115) - 2,399 (251,284)

(116,239) 3,626,483 (2,399) 17,395,609

(135,354)$ 3,626,483$ -$ 17,144,325$

Lutheran HousingCorporations

Lutheran Social Services of Lutheran Social Services ofSouth Dakota, Inc. South Dakota Foundation, Inc.

RestatedRestated Temporarily Temporarily

Unrestricted Restricted Unrestricted RestrictedPublic Support, Revenue, and Other Support

Public support:Contributions 364,387$ 182,499$ 28,436$ 34,030$ Church support 164,026 216,108 - - United Way - 605,975 - - Fees and grants from government agencies 12,669,957 4,130 - - Other grants 246,603 163,750 - -

13,444,973 1,172,462 28,436 34,030 Revenue:

Client and program income 4,896,206 9,202 - - Adoptive income 247,140 - - - Investment return 158,210 - 663,210 32,873 Rent income - - - - Donated supplies income 98,472 - - - Unrealized gain on interest rate swap agreement 29,641 - - - Change in value of split-interest agreements - - - 3,937 Distributions from and change in value of beneficial

interest in charitable trusts held by others - - - 5,892 Miscellaneous income (loss) 124,319 400 (18,550) -

5,553,988 9,602 644,660 42,702

Net assets released from restrictions 1,084,285 (1,084,285) - -

Total public support, revenue, and other support 20,083,246 97,779 673,096 76,732

ExpensesProgram services:

Residential services 5,713,191 - - - Foster care 2,191,970 - - - Community services 5,175,512 - - - Center for financial resources 946,366 - - - Center for new americans 3,912,802 - - - Lutheran housing - apartments - - - -

Supporting services:Management and general 1,593,047 - - - Fundraising and communications 735,187 - - -

20,268,075 - - - Excess (Deficit) of Public Support, Revenue,

and Other Support over Expenses (184,829) 97,779 673,096 76,732

Intercompany Transfers 174,240 - (174,240) -

Change in Net Assets (10,589) 97,779 498,856 76,732

Net Assets, Beginning of Year 8,135,586 723,454 4,003,952 361,994

Net Assets, End of Year 8,124,997$ 821,233$ 4,502,808$ 438,726$

29

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidating Statement of Activities

Year Ended June 30, 2014

TemporarilyUnrestricted Restricted Eliminations Total

-$ -$ -$ 609,352$ - - - 380,134 - - - 605,975 - - - 12,674,087 - - - 410,353 - - - 14,679,901

- - - 4,905,408 - - - 247,140 - - (4,655) 849,638

622,607 - - 622,607 - - - 98,472 - - - 29,641 - - - 3,937

- - - 5,892 3,530 - (5,000) 104,699

626,137 - (9,655) 6,867,434

- - - -

626,137 - (9,655) 21,547,335

- - - 5,713,191 - - - 2,191,970 - - - 5,175,512 - - - 946,366 - - - 3,912,802

676,385 - (9,253) 667,132

- - - 1,593,047 - - - 735,187

676,385 - (9,253) 20,935,207

(50,248) - (402) 612,128

- - - -

(50,248) - (402) 612,128

(65,991) 3,626,483 (1,997) 16,783,481

(116,239)$ 3,626,483$ (2,399)$ 17,395,609$

Lutheran HousingCorporations

30

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidating Statement of Cash Flows

Year Ended June 30, 2015

Lutheran Lutheran Social Social Services Services of Lutheran

of South South Dakota Housing Dakota, Inc. Foundation, Inc. Corporations Eliminations Total

Operating ActivitiesChange in net assets (390,648)$ 156,080$ (19,115)$ 2,399$ (251,284)$ Adjustments to reconcile change in net assets to net cash (used for) from operating activities:

Depreciation 595,327 - 191,332 - 786,659 Amortization 5,310 - 4,735 - 10,045 Loss (gain) on sale of property and equipment 12,540 - (268,097) - (255,557) Unrealized gain on interest rate swap agreement (23,057) - - - (23,057) Change in value of split-interest agreements - (14,492) - - (14,492) Change in value of beneficial interest in

charitable trusts held by others - (2,719) - - (2,719) Investment loss 1,136 2,331 - - 3,467 Acquisition of non-controlling interest - - 190,128 - 190,128

Change in assets and liabilitiesAccounts receivable (44,158) - (3,957) - (48,115) Accrued income receivable (451,875) - - - (451,875) Prepaid expenses 10,670 - (967) - 9,703 Due to/from related entities 475 (475) - - - Accounts payable (132,980) - (6,085) - (139,065) Accrued liabilities 49,215 - (1,506) - 47,709 Deferred revenue (18,858) - - - (18,858)

Net Cash (used for) from Operating Activities (386,903) 140,725 86,468 2,399 (157,311)

Investing ActivitiesPurchases of long-term investments (934,888) (1,572,679) - - (2,507,567) Sales and maturities of long-term investments 1,053,782 1,536,070 - - 2,589,852 Transfers of long-term investments 103,026 (103,026) - - - Share of income from limited partnership 2,399 - - (2,399) - Change in restricted deposits and funded reserves - - (36,218) - (36,218) Change in notes receivable and other investments (282,301) - - 290,000 7,699 Cash received on sale of property and equipment 2,520 - 793,910 - 796,430 Net purchases of property and equipment (545,471) - (107,756) - (653,227)

Net Cash (used for) from Investing Activities (600,933) (139,635) 649,936 287,601 196,969

Financing ActivitiesAdvances on long-term debt 272,500 - 290,000 (290,000) 272,500 Principal payments on long-term debt (422,457) - (45,927) - (468,384) Net change in lines of credit 636,914 - - - 636,914 Payments to beneficiaries of split-interest

agreements - (990) - - (990) Purchase of non-controlling interest - - (290,000) - (290,000)

Net Cash from (used for) Financing Activities 486,957 (990) (45,927) (290,000) 150,040

Net Change in Cash and Cash Equivalents (500,879) 100 690,477 - 189,698

Beginning Cash and Cash Equivalents 1,021,696 - 96,436 - 1,118,132

Ending Cash and Cash Equivalents 520,817$ 100$ 786,913$ -$ 1,307,830$

31

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidating Statement of Cash Flows

Year Ended June 30, 2015

Lutheran Lutheran Social Social Services Services of Lutheran

of South South Dakota Housing Dakota, Inc. Foundation, Inc. Corporations Eliminations Total

Supplemental Disclosures of Cash Flow InformationCash payments for interest 210,626$ -$ 29,818$ -$ 240,444$

Noncash Investing and Financing ActivitiesRepayment of long-term debt upon sale of

property and equipment -$ -$ 791,090$ -$ 791,090$

32

Lutheran Social Services of South Dakota, Inc. and Consolidated Affiliates Consolidating Statement of Cash Flows

Year Ended June 30, 2014

Lutheran Lutheran Social Social Services Services of Lutheran

of South South Dakota Housing Dakota, Inc. Foundation, Inc. Corporations Eliminations Total

Operating ActivitiesChange in net assets 87,190$ 575,588$ (50,248)$ (402)$ 612,128$ Adjustments to reconcile change in net assets to net cash from (used for) operating activities:

Depreciation 567,717 - 191,737 - 759,454 Amortization 5,309 - 1,184 - 6,493 Loss on sale of property and equipment 19,185 - - - 19,185 Unrealized gain on interest rate swap agreement (29,641) - - - (29,641) Change in value of split-interest agreements - (3,937) - - (3,937) Change in value of beneficial interest in

charitable trusts held by others - (39,922) - - (39,922) Investment gain (99,611) (538,886) - - (638,497)

Change in assets and liabilitiesAccounts receivable (216,629) 2 (4,556) - (221,183) Accrued income receivable 331,051 - - - 331,051 Prepaid expenses (10,859) - 25,805 - 14,946 Due to/from related entities 11,812 (11,812) (5,000) 5,000 - Accounts payable 155,710 - 8,340 - 164,050 Accrued liabilities 255,192 - (14,958) (5,000) 235,234 Deferred revenue (31,237) - - - (31,237)

Net Cash from (used for) Operating Activities 1,045,189 (18,967) 152,304 (402) 1,178,124

Investing ActivitiesPurchases of long-term investments (715,411) (825,826) - - (1,541,237) Sales and maturities of long-term investments 571,009 964,650 - - 1,535,659 Transfers of long-term investments 130,680 (130,680) - - - Share of income from limited partnership (402) - - 402 - Change in restricted deposits and funded reserves - - (13,063) - (13,063) Change in notes receivable and other investments 8,019 - - (592) 7,427 Cash received on sale of property and equipment 456,609 - - - 456,609 Net purchases of property and equipment (358,225) - (70,509) - (428,734)

Net Cash from (used for) Investing Activities 92,279 8,144 (83,572) (190) 16,661