TO: Community and Corporate Services Committee-Budget FROM ...

21

Page 1 of Report F-01-15 TO: Community and Corporate Services Committee-Budget FROM: Finance Department SUBJECT: 2015 Budget Overview Report Report Number: F-01-15 Wards Affected: All File Numbers: 435.01 Date to Committee: January 12, 2015 Date to Council: January 26, 2015 Recommendation: Receive the proposed 2015-2024 capital budget and forecast book and the proposed 2015 current budget review documents; and Direct finance staff to present the recommendations in Appendix A to the Community and Corporate Services (C&CS) Committee on January 29, 2015 for review and approval of the capital budget taking into consideration committee amendments; and Direct finance staff to present the recommendations in Appendix B to the Community and Corporate Services Committee on February 17, 2015 for review and approval, of the current budget taking into consideration committee amendments. Purpose: This report provides an overview of the 2015 proposed current budget and the 2015- 2024 proposed capital budget and forecast. Executive Summary: Council approved the city’s strategic plan Burlington, Our Future as a guide for 2011- 2014, including strategic directions related to vibrant neighbourhoods, prosperity and excellence in government. Council approved the long term financial plan (finance department report F-22-12) on November 26, 2012, with the following key financial strategic objectives for the city:

Transcript of TO: Community and Corporate Services Committee-Budget FROM ...

Page 1 of Report F-01-15

TO: Community and Corporate Services Committee-Budget

FROM: Finance Department

SUBJECT: 2015 Budget Overview Report

Report Number: F-01-15 Wards Affected: All

File Numbers: 435.01

Date to Committee: January 12, 2015 Date to Council: January 26, 2015

Recommendation:

Receive the proposed 2015-2024 capital budget and forecast book and the proposed 2015 current budget review documents; and

Direct finance staff to present the recommendations in Appendix A to the Community and Corporate Services (C&CS) Committee on January 29, 2015 for review and approval of the capital budget taking into consideration committee amendments; and

Direct finance staff to present the recommendations in Appendix B to the Community and Corporate Services Committee on February 17, 2015 for review and approval, of the current budget taking into consideration committee amendments.

Purpose:

This report provides an overview of the 2015 proposed current budget and the 2015-2024 proposed capital budget and forecast.

Executive Summary:

Council approved the city’s strategic plan Burlington, Our Future as a guide for 2011-2014, including strategic directions related to vibrant neighbourhoods, prosperity and excellence in government.

Council approved the long term financial plan (finance department report F-22-12) on November 26, 2012, with the following key financial strategic objectives for the city:

Page 2 of Report F-01-15

1) Competitive Property Taxes 2) Responsible Debt Management 3) Improved Reserves and Reserve Funds 4) Predictable Infrastructure Investment 5) Recognized Value for Services

The 2015 proposed budgets adhere to the guiding principles and recommendations of the long term financial plan, as well as the goals of the City’s strategic plan representing Council’s priorities.

Furthermore, this report will provide the following;

• Overview of the 2015 proposed current budget and 2015-2024 proposed capital budget submission

• Summarize key budget items and highlight notable changes as a result of the city’s budget review process

In summary;

• The proposed 2015 budget, presents a balanced program based on the city’s long term financial plan and strategic plan focused on providing continued value and service delivery to taxpayers.

• Delivered a base budget increase of 1.86% aligned with inflation as per the objectives of the long term financial plan, providing Burlington residents with Competitive Property Taxes.

• Base budget submission includes the $4.8 million contribution to the Joseph Brant Hospital reserve fund to meet the city’s $60 million commitment.

• Recommended budget submission does not include any service cuts, and is below the 2015 projection of 4% in the 20 year multi year simulation

• The 2015 proposed city tax increase is 3.55% (including local boards & committees business case requests), resulting in an overall tax impact of 2.1%, and a tax bill impact of $19.36 per $100,000 CVA.

Page 3 of Report F-01-15

Table A: 2015 Proposed City Tax Impact

2015

Budget Tax

Impact

BASE BUDGET

Base Budget * $2,232 0.89%

Growth Services $371 0.27%

Corporate Expenditures/ Revenues $1,077 0.70%

Total Impact - Base Budget ($/ %) $3,680 1.86%

PRIOR POLICY DECISION

Capital Infrastructure $1,745 1.20%

Cumulative Impact ($ / %) $5,425 3.06%

BUSINESS CASES

Expanded/New Business – City $517 0.38%

Cumulative Impact ($ / %) $5,942 3.44%

Local Board & Committee requests $155 0.11%

Cumulative Impact ($ / %) $6,097 3.55%

Overall Tax Impact (City, Region, Education)

2.1%

* Including $4.8 million levy for the city’s contribution towards the Joseph Brant Hospital redevelopment project

The 2015 current budget is provided to Council and the public in a service based format. A budget refocused on services is beneficial to the city as it ensures decision making reflects service adjustments, and increases public awareness of service investment. This is the city’s first step into service based budgeting, and there will be opportunity for refinement as the process evolves over time. Service based budgeting will bring focus to budget discussions and enhance transparency and decision making.

As in previous budgets, staff has continued to recognize the importance of vacancy management. As a result, regular reviews of staff vacancies are undertaken and redeployments to other service areas are considered that are both appropriate and provide added value to the city, thereby, controlling headcount and human resource costs. The city through its redeployments and job rotations fosters employee development, providing opportunity for personal and professional growth within the organization, and allowing the city to grow our talent from within. Overall staff has submitted a base budget with reduced FTE’s of 2.7. Three service business cases, two from Transit and one from Fire, have been brought forward for council’s consideration that if approved would add to the city’s complement by 6.2 FTE’s, for a net city FTE

Page 4 of Report F-01-15

impact of 3.5. Council will have to assess these business cases based on the enhanced service value for investment required.

The 2015 proposed capital budget is approximately $48 million, with a ten year program of $577 million, focusing on the city’s infrastructure requirements. The capital budget presentation has been refocused to highlight infrastructure renewal projects showing commitment to the city’s asset management plan and the city’s long term objectives regarding infrastructure needs. The budget also reflects recent climate change events by introducing a Climate Change & Flood Mitigation project in the capital budget. This project provides $4.5 million in the first four years for maintenance and rehabilitation works addressing recommendations resulting from the AMEC study.

The city is making good progress on its infrastructure renewal needs as Council has provided Predictable Infrastructure Investment, in the form of a dedicated incremental infrastructure levy of $1.7 million and dedicated funding towards the city’s roads resurfacing program of $3 million annually. These initiatives combined have assisted the city in meeting the 20-year asset management financing plan.

The ten year capital program is 73% infrastructure renewal projects, 17% growth related projects with 10% for new / enhanced projects. As per the city’s strategic and long term financial plan staff have submitted a capital program which also considers new / enhanced projects but aims to strike a balance between our need to protect our existing capital investments versus providing new capital projects in the city. Any new projects are supported by a capital budget business case.

We encourage council to continue its strategic approach to budget review and empower staff to implement the financial and service directions provided by the annual budget process.

Background:

2015 PROPOSED CURRENT BUDGET

In 2014, a current budget process review took place with a cross functional team composed of Finance, the Business Performance unit and other stakeholders. The team conducted interviews with Council, senior staff and departmental staff, as well as conducted a detailed process mapping exercise and risk analysis to determine opportunities, and risks in the process. The project was completed with several improvements incorporated in the 2015 budget process as quick-wins, and others which will be a work in progress as they encompass larger process changes. Though the process review was limited to the current budget cycle, quick-wins were adapted in both the capital and current budget processes to achieve efficiencies and consistency.

The 2015 proposed current budget continues to align with the long term financial plan with a focus on providing Recognized Value for Service. The 2015 budget is presented in a service based format allowing Council and residents to see how our services meet the core needs and growing demand of our community. The identification of revenues and expenditures by service ensure staff and Council is considering service

Page 5 of Report F-01-15

adjustments when making budget decisions, as well as providing increased transparency and awareness to the public of investments and service alignment. For presentation, Council will be provided a service based budget, along with the traditional departmental based budget as supplementary information. It should be noted that service based budgeting is not intended to be a detailed activity based costing exercise. As we move forward the service based structure and presentation may be refined over time.

Financial Summary

The 2015 proposed budget responds to providing services and infrastructure maintenance through a Competitive Property Tax increase, striking a balance between minimizing tax increases while maintaining service levels in a climate of increasing costs.

• The city’s base budget is presented with a 1.86% increase, below the three year rolling average of the Toronto Consumer Price Index (1.91%)

• Including prior policy decision to increase the dedicated infrastructure levy, the increase is 3.06%

• City business cases bring the increase to 3.44% • Local Boards and Committee business cases result in a city tax impact of 3.55%. • Combined with the Region of Halton increase and education, the overall increase

is 2.1%, compared to the most recent Toronto CPI figure of 2.50% (average October 2013-2014)

Page 6 of Report F-01-15

The following table provides a breakdown of the city’s tax increase.

Table B: 2015 Proposed City Tax Impact

2015

Budget Tax

Impact

BASE BUDGET

Base Budget * $2,232 0.89%

Growth Services $371 0.27%

Corporate Expenditures / Revenues $1,077 0.70%

Total Impact - Base Budget ($ / %) $3,680 1.86%

PRIOR POLICY DECISION

Capital Infrastructure $1,745 1.20%

Cumulative Impact ($ / %) $5,425 3.06%

BUSINESS CASES

Expanded/New Business – City $517 0.38%

Cumulative Impact ($ / %) $5,942 3.44%

Local Board & Committee requests $155 0.11%

Cumulative Impact ($ / %) $6,097 3.55%

Overall Tax Impact (City, Region, Education)

2.1%

* Including $4.8 million levy for the city’s contribution towards the Joseph Brant Hospital redevelopment project

The 2015 net tax levy is the amount of property taxes required to support city services. The total proposed net tax levy is $139,912,648 (net of assessment growth) which includes the $4.8 million levy for the city’s contribution towards the Joseph Brant Hospital redevelopment project.

As per report F-30-14, 2015 Budget Framework presented to Committee on July 8, 2014, staff indicated that the 2015 proposed current budget will keep with the objectives identified in the long term financial plan, as follows;

• Base budget tax rate changes of 1.86% are aligned closely with inflation, represented by the three year annual rolling average of the Consumer Price Index (Toronto). The 2011-2013 annual average is 1.91%.

The projections of the 20 year simulation (F-08-14) presented to Council on March 17, 2014, identified the key budget drivers to maintain service levels and minimize associated tax rate increases. The simulation indicated a city tax increase of 4.0% for 2015. Staff have brought forward a 2015 proposed budget with a base budget tax

Page 7 of Report F-01-15

increase of 1.86%, and total city tax increase of 3.55% including business cases, below the 4.0% previously indentified figure. One time funding

In accordance with the city’s approved one-time funding policy, some of the budgeted expenditures in the 2015 Proposed Current Budget were identified as one-time in nature and funded from a one-time source of revenue (net zero impact). The total amount of one-time funding being proposed as per recommended business cases is $287,000. As in previous years, the anticipated prior year’s retained savings has been relied upon to supplement the Tax Rate Stabilization Reserve Fund for the purpose of offsetting one-time expenditures. Staff will recommend that $287,000 of the favourable year-end variance be transferred into the Tax Rate Stabilization Reserve Fund, which will later be applied to offset the proposed one-time items identified for funding in 2015.

Growth Impacts As indicated in the 20 year simulation report growth impacts account for a portion of the city’s increased costs year over year. In the 2015 proposed base budget, growth related impacts of approximately $371,000, are reflected including additional winter control due to growth in lane kilometers, enhanced creek maintenance and technical and maintenance costs resulting from expansion of business applications and technology across the organization.

Local Boards & Committees

Local Boards include the Burlington Public Library, Burlington Museums, Art Gallery of Burlington, Burlington Performing Arts Centre, Tourism Burlington and the Burlington Economic Development Corporation (BEDC). For 2015 an increase of 1.5% was provided for local boards. The base budget increase to local boards and committees in 2015 equates to $216,403 or 1.5% year over year. Including business cases, the overall submission for local boards and committees equates to an increase of $370,903.

As in prior years, the business case submissions by Boards and Committees have not been included in the city’s budget submission, however, have been provided to Council for their consideration, to add to the city’s net budget. Business cases were received from Burlington Performing Arts Centre, Sound of Music, and Heritage Burlington. Approval of the business cases would increase the city’s tax rate by 0.11% to 3.55%.

Page 8 of Report F-01-15

Key Budget Items

The following areas present notable items as part of the 2015 budget.

Human Resource Management

Continuing the city’s efforts to be an ‘employer of choice’ and to encourage

excellence and optimize the use of existing financial and human resources,

weekly meetings were held in 2014 to review vacancies and consider

redeployments where possible to priority areas of service. Over a three year

period, the city has redeployed 41 full time equivalents (FTEs) to other value

added areas of service as summarized in the following chart:

Year Full Time Part Time Contract Total

2013 3.0 7.6 3.2 13.8

2014 3.0 9.5 4.4 16.9

2015 4.0 1.1 5.2 10.3

Total 10.0 18.2 12.8 41.0

Furthermore, Human Resource costs have averaged 49% of the city’s gross budget over the past 10 years. The 2015 costs are approximately 47%.

In the 2015 proposed budget, staff has included appropriate redeployments of human resources as a result of regular reviews of vacant positions. Overall, the continuation of the city’s vacancy management program has demonstrated effectiveness, as the 2015 FTE count has been managed, with needs accommodated within existing complement. The exception are two Transit service expansion business cases and one Fire business case put forward for Council’ consideration, discussed below, that generate a net FTE impact of 3.5 for increased service. Council will need to assess each business case based on priorities, value and investment. Overall Burlington has the lowest FTE’s per 1,000 population of ten similar lower tier municipalities, with a total of 6.24 FTE’s per 1,000 population. The range of the other municipalities was from a low of 6.71 to a high of 11.06, with an average of 8.08 per 1,000 population. (Source: 2012 FIR’s)

Transit Service Expansion

Put forward for Council’s consideration are two business cases supporting increased level of service for Transit. The Community Connection business case encourages greater movement for locals and seniors throughout Burlington to locations that serve the needs of seniors by way of a scheduled service. The additional business case for Handi-Van users, allows the city to better serve a growing segment of our population through a specialized service, where bookings per year have been steadily increasing. The two Transit service expansions allow the city to

Page 9 of Report F-01-15

provide expanded service for an existing and growing need within the senior’s community, with an overall 0.38% tax impact.

Employee Parking Staff have researched the taxable benefit status of employee parking and the tighter regulations from the Canadian Revenue Agency (CRA). An employer provided benefit is considered income and therefore subject to taxable deductions (i.e./. income tax, CPP, EI). The review included assistance from external experts regarding tax and employment law as well as information from other municipalities who have also recently reviewed their employee parking tax status.

It has been determined that employer provided parking in the downtown is a taxable benefit, impacting 365 city employees, including union, non-union and members of Council. Exemptions to the above include an employee who is provided a parking spot due to a disability and employees who use their vehicle for regular business purposes. As per CRA guidelines regular use of a vehicle for business purposes constitutes an average of 3 or more days in a five day work week.

In order to treat all city employees equitably (those that work downtown versus employees who work in other areas of the city where employer provided parking is not a taxable benefit), the 2015 budget includes $150,000 to offset the annual impact of the net pay reduction for those existing affected employees.

Weighted Assessment Growth

Assessment growth allows a municipality to finance increased costs without increasing taxes. As residential Greenfield build out occurs, the city’s assessment growth will be impacted. Over the past three years Burlington’s weighted assessment growth is as follows;

• 2012 1.01% • 2013 0.87% • 2014 0.58%

The weighted assessment growth for the 2015 budget is 0.97%, which provides approximately $1.3 million of additional revenue (0.97% tax reduction) reducing the city’s tax increase to 3.55%.

Cultural Program As part of the 2015 proposed budget, staff included a base level of funding of $100,000 to be used towards a provision to a cultural initiatives reserve fund. The city has been working towards enhancing the culture program through the Culture service, to facilitate opportunities for visual and performing arts, festivals, heritage, public art, and culture service providers.

Page 10 of Report F-01-15

The $100,000 base funding will be managed by the culture service on an annual basis and be used in a multitude of ways to support Culture a few being;

• Culture Action Plan – development of a cultural grants program • Contribution to the Public Art reserve fund - for the commissioning and

maintenance of public art in the city.

Corporate Policy and Initiatives

As part of the 2015 proposed budget, staff included a base level of funding of $100,000 to be used towards a provision to a reserve fund for the City’s work on policy initiatives as policy work does not represent capital spending and is now longer part of the capital budget. For 2015 the funding will be allocated towards the Official Plan review, as per report PB-86-13, additional funding would be required to complete the review. In future, these funds in the Policy Initiatives reserve fund can be used for areas such as Mobility Hub master plans. The reserve fund will ensure there are not significant fluctuations on the current budget for ongoing policy studies and better aligns spending.

2015 PROPOSED CAPITAL BUDGET

As part of the 2015 proposed capital budget and forecast, staff has provided an updated presentation that highlights and refocuses the capital budget in the following three areas;

• Infrastructure renewal projects: repair, refurbishment or replacement of an existing asset to extend its useful life

• Growth projects: capital requirements needed to service growth within the city • New / enhanced projects: increases to current service levels beyond what the

city currently provides, not a result of growth

The capital budget is still broken down by asset category however; each project is identified by 1 of the 3 areas defined above in order to demonstrate the city’s focus on infrastructure renewal as per the city’s long term financial plan.

Each area is supported by a policy attached as Appendix C, D and E, in this report. The policies provide clear definitions and direction to staff to clearly indicate how the project fits into the capital budget. Projects defined as ‘new/enhanced’ will be supported by a business case which is thoroughly reviewed to determine its validity in moving forward as part of the capital budget review process. The business cases are included in the proposed capital budget book under separate tab for review.

The 2015 proposed capital budget continues to focus on infrastructure renewal requirements with infrastructure representing 73% of the city’s ten year capital budget. The budget includes an increase of $1.7 million to the dedicated infrastructure renewal levy, as approved in 2014 per the city’s asset management financing plan, providing Predictable Infrastructure Investment to the city’s capital program. Furthermore, the capital budget and forecast reflects Responsible Debt Management as the budget continues to adhere to the city’s debt policy limits while using debt in the most effective manner when possible as per the city’s long term financial plan.

Page 11 of Report F-01-15

Financial Summary

The proposed 2015-2024 capital budget and forecast project listing is provided under separate cover for Committee’s review and approval. The budget book provides Committee with the ten year capital plan on a project basis, including operating budget impacts. Growth related projects identified in the proposed capital budget align with the 2014 Development Charges study.

The Capital Budget Submission:

• Underwent extensive review by asset category teams and a line-by-line review by the Corporate Infrastructure Committee

• Presents a balance between identified needs, council directions, and available financing.

• Reflects project costs in 2015 dollars. • Includes a minimum 15% contingency for non-routine projects, 2% allowance for

project management costs. • Reflects updated operating budget impacts for ten years for projects in excess of

$1 million and for at least four years for all other projects as required.

The City’s proposed 2015 capital program is approximately $48 million. The 10-year program for 2015-2024 is $577 million. Tax supported funding accounts for roughly 53% of the 2015 budget and forecast. The capital program for stormwater management has increased 31% year over year to reflect base infrastructure needs and additional investment to respond to climate change events, discussed further below.

Table C: 10-year capital budget by project category

Project Type Infrastructure

Renewal project Growth project

New/ enhanced project

Roadways $213,856 $66,352 $8,268

Stormwater Management $21,143 $17,772 -

Facilities & Buildings $68,803 - $23,920

Parks & Open Space $30,468 $10,962 $8,590

Parking $1,032 - $13,400

Information Technology $12,560 - $2,035

Fleet Vehicles $65,857 $2,575 $600

Local Boards $8,189 $324 $400

Total $421,908 $97,985 $57,213

*All values in millions (‘000)

The capital budget uses a variety of sources to fund the capital program. Tax supported funding continues to be the largest component accounting for roughly half (53%) of the overall funding envelope. The budget continues to rely on the cash flow generated from

Page 12 of Report F-01-15

the Burlington Hydro reserve fund (5.4%) to fund infrastructure needs, and the city’s development charge revenue to fund growth projects (11%). Note, the proposed capital budget submission also includes the cost, if any, of on road bike lanes for each project in the first three years of the capital program as requested through a staff direction.

Key Budget Items

The following areas present notable items as part of the 2015 capital budget.

Climate Change & Flood Mitigation Measures This project was included in the 2015 proposed capital budget and forecast in response to the August 4th, storm event. As indicated in report CW-03-14, the major thunderstorm led to riverine flooding, major overland system drainage, sewer backup, and the accumulation of debris and sediment in watercourses and culvert inlets. The city has retained AMEC to assist in flood analysis and identify areas and potential solutions to address damage as a result of the flood and future mitigation projects. The completion of AMEC’s work is expected to yield estimates for future repair and rehabilitation. In order to address those immediate and future works the capital budget includes the Climate Change & Flood Mitigation Measures project (SM-SD-1173) in the Stormwater asset category to implement future stormwater infrastructure renewal needs. The proposed budget includes $4.5 million for this project over the first four years, with additional funding in the later years (total ten year budget $5.57 million) that will be updated as required over future budget cycles based on the work completed and detailed project estimates.

The project is funded with a combination of tax supported funding as well as funding from the Burlington Hydro reserve fund (BHRF). The BHRF funded $3.6 million of the total project cost, scheduled in the first four years (2015-2018). As part of the capital budget process the Hydro cash flow is reviewed and staff determined there is sufficient funding over the next four years to allow for a one-time influx of cash into the capital program ($3.6 million) to address the city’s climate change issues. This was accomplished by removing $2.9 million of special circumstances debt (principal & interest) that was not assigned, replacing it with cash for immediate use. (Note: there is also an increase of $100,000 for enhanced creek maintenance activities in the current budget) Infrastructure Renewal As mentioned above the city’s capital program focuses on the city’s infrastructure requirements to address the required maintenance and renewal of our aging infrastructure. As per the long term financial plan the city has an obligation to protect its capital investment and strike a balance between new / enhanced investment versus infrastructure repair and maintenance. The ten year budget is $577 million, of which 73% represents infrastructure renewal projects. The ten year budget incorporates the increase to the dedicated renewal levy as approved in the city’s asset management financing plan. This results in meeting our

Page 13 of Report F-01-15

planned infrastructure needs as per the 20 year asset management financing plan.

Staff considered the potential for accelerating $20 million in debt funding over the next five years for short term cost avoidance and addressing existing backlog. Staff do not recommend a short term infusion of debt financing at this time. Staff would like to take the time to continue to assess the roads needs, and bring forward to council in Q2 of 2015 the next steps to address road infrastructure requirements as the ability to deliver the existing program with existing resources has been demonstrated, as discussed further below. Taking a holistic approach to consider road, bridge, and storm sewer requirements is appropriate at this time. Staff will continue to evaluate financing options for future financial flexibility for unknown renewal requirements, as well a prioritize infrastructure needs within and between asset categories, as per the asset management plan.

Note the following reasons an additional $20 million is not recommended at this

time;

• Additional debt will have an incremental impact (0.20% additional tax

increase, F-39-13) to the operating budget, dependant on timing of

issuance and interest rates.

• The city has responsibly allocated $3 million annually in cash funding to

the city’s shave and pave program to address less costly resurfacing

requirements and backlog which will assist in providing the right treatment

at the right time. As per report (CW-01-15, January 19 Development &

Infrastructure agenda), Roads Pavement Performance update, there has

been significant progress in the local road PQI from 67.5 to 72.1.

• In the short term, the cash flow in the Burlington Hydro reserve fund is

sufficient based on the most recent business plan and assumptions to

assist in providing additional annual funding towards infrastructure needs,

as partly demonstrated above through the allocation towards climate

change response.

• As part of the long term financial plan the city has been phasing down the

use of debt on renewal projects, as it is not a sustainable funding source

to address the city’s ongoing renewal needs. A short term infusion of debt

would be contrary to the long term financial plan, of Responsible Debt

Management, the city’s debt policy, and the recommendations of the 2010

BMA study

• As addressed in the 2014 capital closure report, (F-41-14), a significant

number of projects have been closed. 147 projects of which Roadways

accounts for 33% of the closures demonstrating commitment to

addressing our backlog.

Page 14 of Report F-01-15

Council has maintained infrastructure renewal as the city’s priority, and

significant strides have been made over the last few years, to provide Predictable

infrastructure investment for renewal requirements. This funding has allowed for

the advancement of the city’s shave and pave program, and specifically the

advancement of the local road program. As indicated in report (CW-01-15), the

entire road program will need to be re-evaluated, relative to the city’s asset

management plan to determine the most effective use of current and future

funding for road resurfacing needs. With the additional funding over the last few

years, staff have managed to increase the Pavement Quality Index (PQI) for local

roads to a reasonable state, and there are a number of areas that need to be

considered before further funding is directed to the shave and pave program,

such has;

• Storm sewer needs must be addressed before the local road program is

expanded, to prevent costly re-work due to unexpected requirements

• The current local road program is being delivered with the assistance of a

consultant, further expansion of the program will require greater external

resources, as additional internal capacity has not been provided

• As a result of the August storm event, there may be an impact on the city’s

bridge infrastructure, a place where future funding may be required in

advance of shave and pave needs.

• Decline in PQI for arterial resurfacing needs over the last three years –

more costly and extensive work required, the infrastructure gap is not

closing here.

• Required coordination with the Region, and consideration of future roads

rationalization, before dollars are allocated and work can begin.

Corporate Initiatives Asset Category

As part of the budget process staff reviewed the capital and current budget to

ensure that each budget accurately reflected true capital and true operating

costs. As part of the review it was determined that the Corporate Initiatives asset

category primarily represented budgets for studies, and/ or policy work which are

not reflective of a capital project defined as;

A project that maintains or improves a city asset (infrastructure) such as new

construction, expansion, renovation or replacement, or; major equipment

purchase, with a project cost of over $20,000 over the life the project. Project

costs can include cost of land, engineering, and contract services.

In essence, this asset category primarily represented operating type costs. As a result of the review and reallocation of certain costs and/ or projects the corporate initiatives asset category no longer exists. The following actions were taken for the projects that resided within this asset category;

Page 15 of Report F-01-15

• A few projects were moved to other asset categories for a more accurate fit, those which were primarily funded by development charges.

• Remaining projects were moved over to the current budget. Council will see some of those initiatives being brought forward as a business case on the current budget, others were restated within the base budget with no incremental impact

As a result of the above, the capital budget and forecast, now has 8 asset categories, and more accurately reflects true capital works being undertaken by the city.

As well, the capital budget for Tourism Burlington primarily consisted of operating costs and was restated to the operating budget and removed from the Local Board asset category.

Development charges study

Of the overall funding envelope, the 2015 proposed capital budget and forecast includes development charge funding of approximately 11%. This is slightly lower than the five year historic average, where development charges represented 15% of the overall funding envelope. This can be attributed to the decrease in development charge revenue expected, as the city transitions from development of residential Greenfield to a focus on non residential and infill intensification in which revenue is typically less predictable and slower in realizing. The development charges revenue projection for 2014 is about $3.5 million compared to the five year historic annual average of $5.5 million. The 2015 proposed capital budget and forecast recognizes the reduced revenue stream in the first five years of the forecast and based on current policy ensures that spending in any year does not exceed the uncommitted balance in the reserve fund at the end of the preceding year. The uncommitted year end development charge reserve fund balance is anticipated to be approximately $7 million.

Discussion:

BUDGET PROCESS

As mentioned above the budget process undertook several ‘quick-win’ process changes in order to deliver a timelier budget to Council. This year, the following process changes were implemented:

• Comprehensive Director of Finance review with city departments • Cross functional team of asset leads to conduct panel reviews of capital budget • Executive Budget Committee (EBC) replaced with a smaller group, composed of

the City Manager, General Manager, Executive Director of Human Resources and Director of Finance

• Review of business cases, and strategic discussion for budget presentation at the senior management group level

Page 16 of Report F-01-15

• Elimination and restatement of the Corporate Initiatives asset category • Elimination of budget forms • Enhanced communication with city staff and local boards

As a result, Council was able to receive the budget overview report and the proposed budget books prior to the December holidays, allowing greater time for review ahead of January Committee for budget overview and council information sessions. Moving forward staff will aim for earlier budget approval with the goal being December approvals. Considering 2014 was an election year, earlier budget approval was not possible this year.

COUNCIL INFORMATION SESSIONS

As in prior years, the budget review process includes council information sessions for both the capital and current budget. These sessions provide council with the opportunity to ask questions on the proposed budget from departments/ service owners, and asset leads. Finance and the City Manager will be in attendance for all sessions.

The budget information sessions for members of Council will be held on January 21, 2015, in room 247, from 9:30 a.m. -3:30 p.m. Capital budget asset categories will be scheduled in the morning from 9:30 – 12:30pm and current budget will be scheduled in the afternoon from 1 – 4:30pm. Below are the scheduled time slots.

Capital Budget:

January 21, 2015 Asset Category

9:30 a.m. – 10:50 a.m.

Roadways

Storm Water Management

Fleet Vehicles, Accessories & Equipment

11:00 a.m. – 11:50 a.m. Facilities & Buildings

Local Boards

12:00 noon – 12:30 p.m.

Parks & Open Space

Parking

Information Technology

Page 17 of Report F-01-15

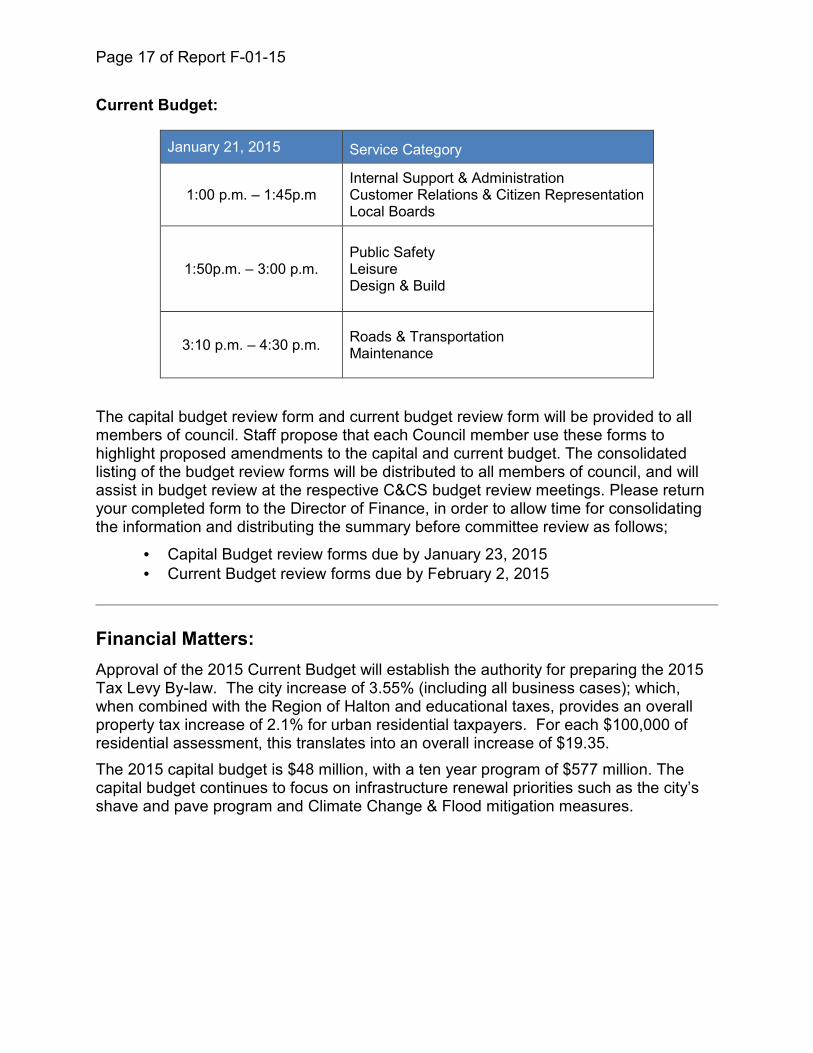

Current Budget:

January 21, 2015 Service Category

1:00 p.m. – 1:45p.m Internal Support & Administration Customer Relations & Citizen Representation Local Boards

1:50p.m. – 3:00 p.m. Public Safety Leisure Design & Build

3:10 p.m. – 4:30 p.m. Roads & Transportation Maintenance

The capital budget review form and current budget review form will be provided to all members of council. Staff propose that each Council member use these forms to highlight proposed amendments to the capital and current budget. The consolidated listing of the budget review forms will be distributed to all members of council, and will assist in budget review at the respective C&CS budget review meetings. Please return your completed form to the Director of Finance, in order to allow time for consolidating the information and distributing the summary before committee review as follows;

• Capital Budget review forms due by January 23, 2015 • Current Budget review forms due by February 2, 2015

Financial Matters:

Approval of the 2015 Current Budget will establish the authority for preparing the 2015 Tax Levy By-law. The city increase of 3.55% (including all business cases); which, when combined with the Region of Halton and educational taxes, provides an overall property tax increase of 2.1% for urban residential taxpayers. For each $100,000 of residential assessment, this translates into an overall increase of $19.35.

The 2015 capital budget is $48 million, with a ten year program of $577 million. The capital budget continues to focus on infrastructure renewal priorities such as the city’s shave and pave program and Climate Change & Flood mitigation measures.

Page 18 of Report F-01-15

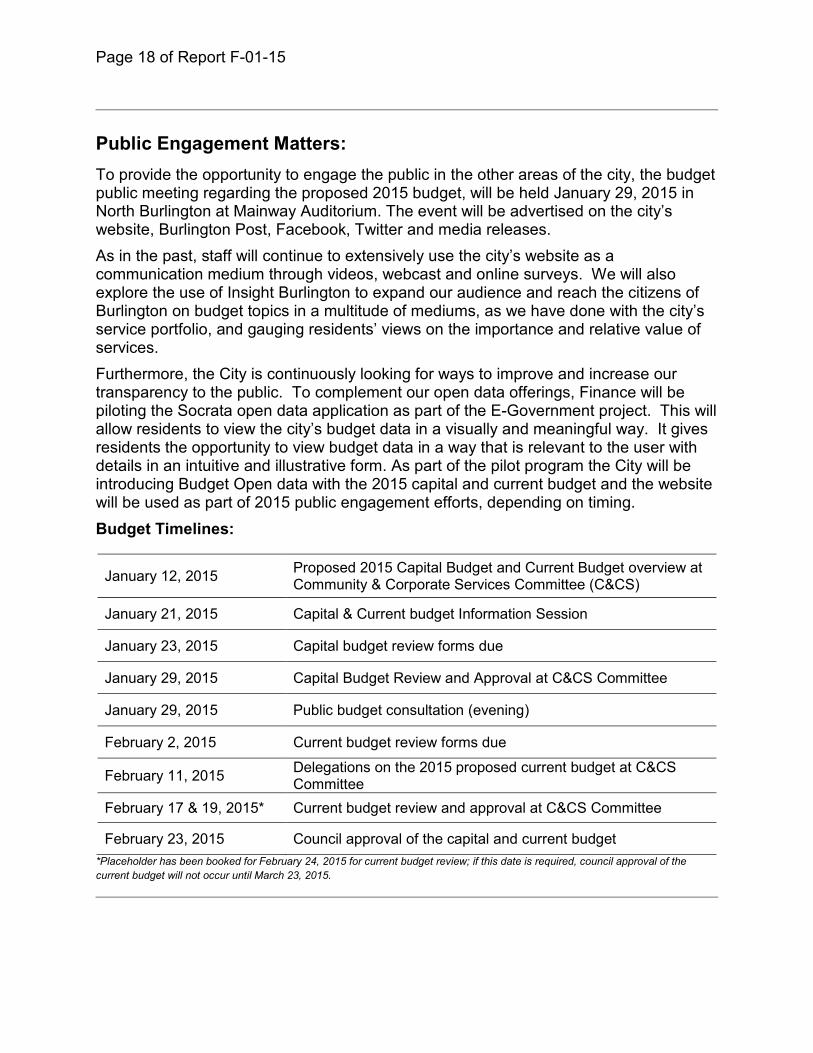

Public Engagement Matters:

To provide the opportunity to engage the public in the other areas of the city, the budget public meeting regarding the proposed 2015 budget, will be held January 29, 2015 in North Burlington at Mainway Auditorium. The event will be advertised on the city’s website, Burlington Post, Facebook, Twitter and media releases.

As in the past, staff will continue to extensively use the city’s website as a communication medium through videos, webcast and online surveys. We will also explore the use of Insight Burlington to expand our audience and reach the citizens of Burlington on budget topics in a multitude of mediums, as we have done with the city’s service portfolio, and gauging residents’ views on the importance and relative value of services.

Furthermore, the City is continuously looking for ways to improve and increase our transparency to the public. To complement our open data offerings, Finance will be piloting the Socrata open data application as part of the E-Government project. This will allow residents to view the city’s budget data in a visually and meaningful way. It gives residents the opportunity to view budget data in a way that is relevant to the user with details in an intuitive and illustrative form. As part of the pilot program the City will be introducing Budget Open data with the 2015 capital and current budget and the website will be used as part of 2015 public engagement efforts, depending on timing.

Budget Timelines:

January 12, 2015 Proposed 2015 Capital Budget and Current Budget overview at Community & Corporate Services Committee (C&CS)

January 21, 2015 Capital & Current budget Information Session

January 23, 2015 Capital budget review forms due

January 29, 2015 Capital Budget Review and Approval at C&CS Committee

January 29, 2015 Public budget consultation (evening)

February 2, 2015 Current budget review forms due

February 11, 2015 Delegations on the 2015 proposed current budget at C&CS Committee

February 17 & 19, 2015* Current budget review and approval at C&CS Committee

February 23, 2015 Council approval of the capital and current budget

*Placeholder has been booked for February 24, 2015 for current budget review; if this date is required, council approval of the

current budget will not occur until March 23, 2015.

Page 19 of Report F-01-15

Conclusion:

The proposed 2015 budget presents a balanced program aimed to deliver on the city’s long term financial plan, focusing on infrastructure renewal, responding to climate change initiatives and value for service.

Respectfully submitted,

Joan Ford, Director of Finance

N/A

Appendices:(if none delete section)

a. Capital Budget recommendations for report F-01-15

b. Current Budget recommendations for report F-01-15

c. Draft policy – Infrastructure renewal projects

d. Draft policy – Growth projects

e. Draft policy – New/ Enhanced projects

Notifications: (after Council decision)

Approved by:

Joan Ford, Director of Finance

Nancy Shea Nicol, Director of Legal Services & City Solicitor

Pat Moyle, Interim City Manager

Reviewed by:

Name: Mailing or E-mail Address:

Page 20 of Report F-01-15

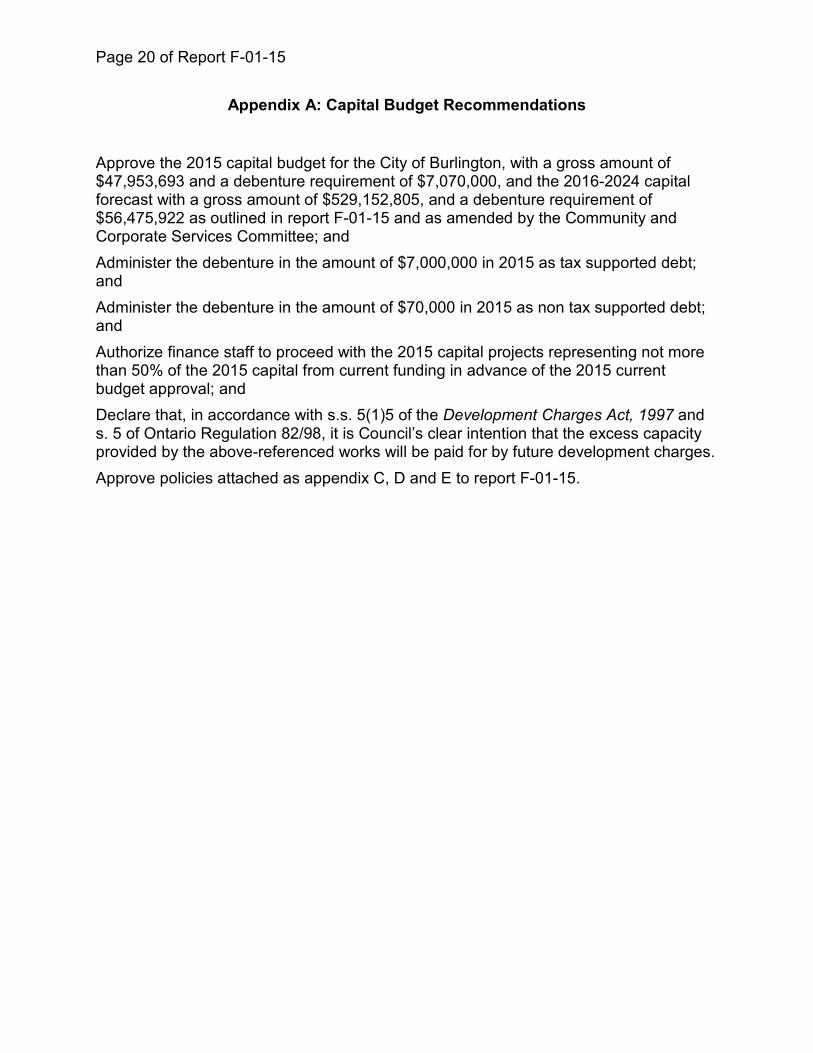

Appendix A: Capital Budget Recommendations

Approve the 2015 capital budget for the City of Burlington, with a gross amount of $47,953,693 and a debenture requirement of $7,070,000, and the 2016-2024 capital forecast with a gross amount of $529,152,805, and a debenture requirement of $56,475,922 as outlined in report F-01-15 and as amended by the Community and Corporate Services Committee; and

Administer the debenture in the amount of $7,000,000 in 2015 as tax supported debt; and

Administer the debenture in the amount of $70,000 in 2015 as non tax supported debt; and

Authorize finance staff to proceed with the 2015 capital projects representing not more than 50% of the 2015 capital from current funding in advance of the 2015 current budget approval; and

Declare that, in accordance with s.s. 5(1)5 of the Development Charges Act, 1997 and s. 5 of Ontario Regulation 82/98, it is Council’s clear intention that the excess capacity provided by the above-referenced works will be paid for by future development charges.

Approve policies attached as appendix C, D and E to report F-01-15.

Page 21 of Report F-01-15

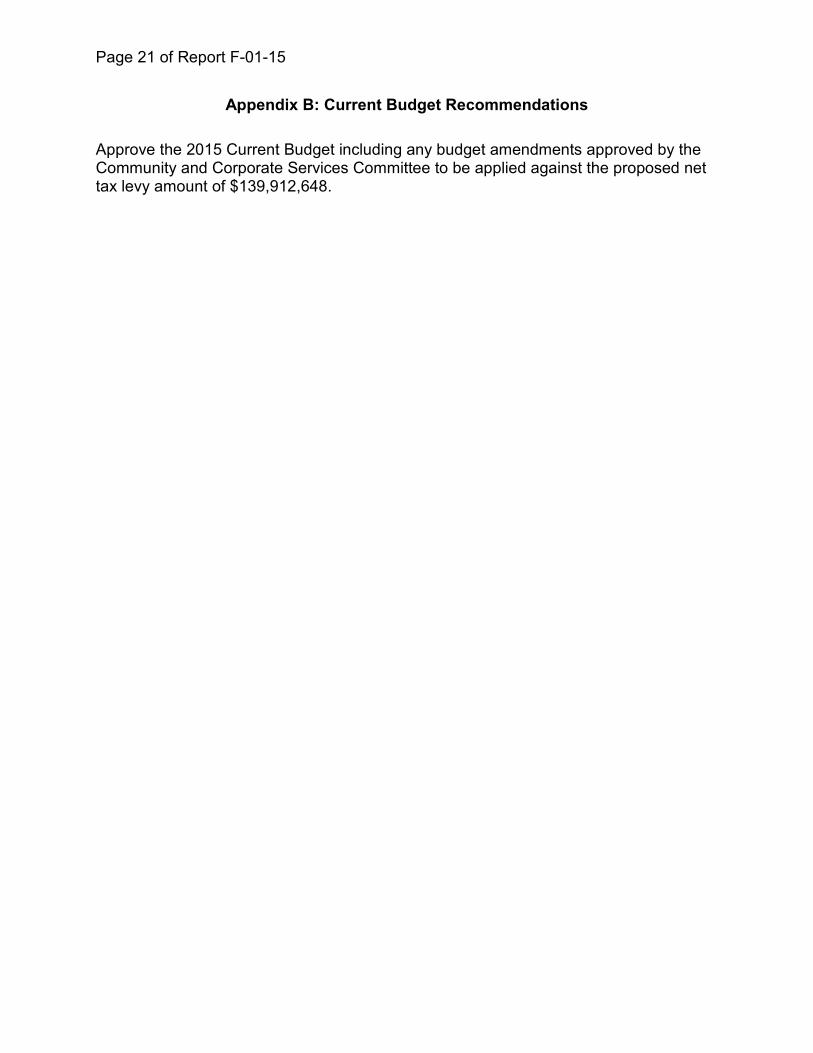

Appendix B: Current Budget Recommendations

Approve the 2015 Current Budget including any budget amendments approved by the Community and Corporate Services Committee to be applied against the proposed net tax levy amount of $139,912,648.