TLIP5035A Presentation 6

20

PRESENTATION 6: MONITOR AND CONTROL ACTIVITIES AGAINST PLANS

-

Upload

careers-australia -

Category

Education

-

view

16 -

download

0

Transcript of TLIP5035A Presentation 6

PRESENTATION 6: MONITOR AND CONTROL ACTIVITIES AGAINST PLANS

PRESENTATION 6 OUTLINE

The following areas are covered in this presentation:

• Delegation

• Responsibilities

• Authority

• Funds Allocation

• Allocating Costs

• Master Budget to Cost Centres

• The Time Dimension

• Best Practice Budgeting

DELEGATION

• Each department should base the appropriate levels of resource

delegation on its business activities, structure, size, procedures

and capabilities

• Departments should reassess their management structures to

ensure that the financial, administrative and personnel authorities

delegated to the managers responsible for service and

expenditure decisions are consistent.

• With effective communication, training and management

information systems, departments can progressively implement

the full flexibility and efficiency that the budget offers.

• Managers must ensure that key elements are in place as more

authorities are delegated

RESPONSIBILITIES

• It is important that everyone who needs to understand and

implement the budget is clear on their actual responsibilities.

Responsibility indicates the duty assigned to a position.

• The person holding the position has to perform the duty assigned.

It is their responsibility.

• The term responsibility is often referred to as:

An obligation to perform a particular task assigned to a subordinate. In an organisation, responsibility is the duty as per the organisational

guidelines issued.

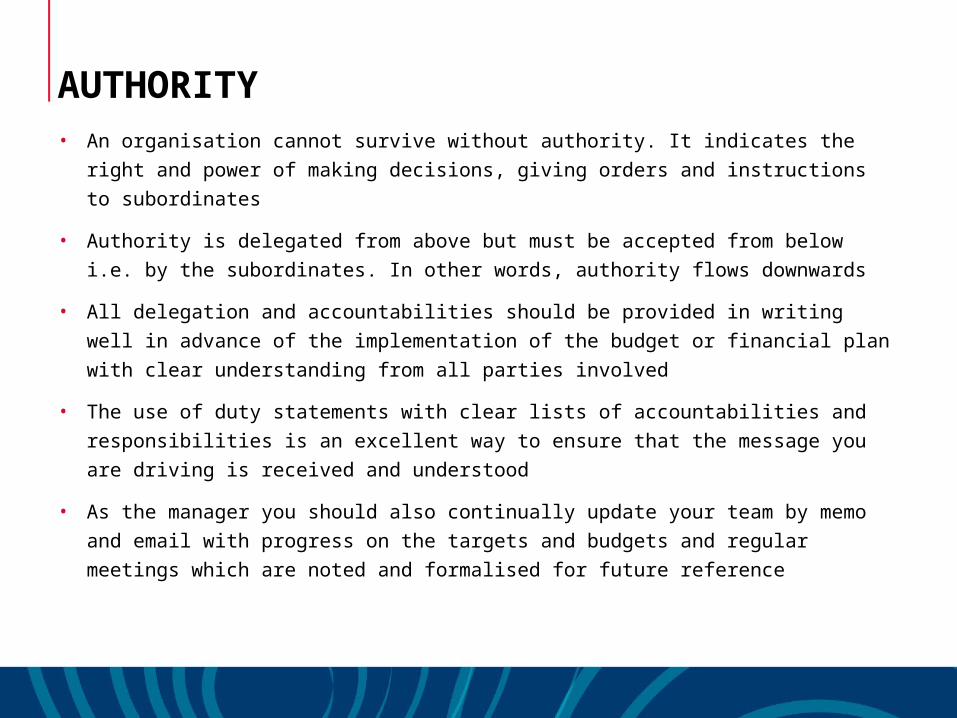

AUTHORITY• An organisation cannot survive without authority. It indicates the right

and power of making decisions, giving orders and instructions to

subordinates

• Authority is delegated from above but must be accepted from below i.e.

by the subordinates. In other words, authority flows downwards

• All delegation and accountabilities should be provided in writing well in

advance of the implementation of the budget or financial plan with clear

understanding from all parties involved

• The use of duty statements with clear lists of accountabilities and

responsibilities is an excellent way to ensure that the message you are

driving is received and understood

• As the manager you should also continually update your team by memo

and email with progress on the targets and budgets and regular

meetings which are noted and formalised for future reference

FUNDS ALLOCATION• The funds required for a section of the organisation will have been

allocated in the budget. The funds must be allocated and distributed

for the smaller budget sections to work, thus enabling the bigger

elements to work and the overall plan to be carried out.

• It is important to be fair and appropriate when you allocate your

funding based on the budget requirements.

• You need to look at the budget parameters which have been set and

ensure that they are realistic and that there are sufficient funds

available to meet those objectives.

• Prioritising your objectives will be a major consideration when

determining the allocated funds

• Everyone involved will argue the need to be in the top priority for

funding but use the realistic approach and refer to previous budgets

to determine where the most practical place for the funds will be.

FUNDS ALLOCATION

• Consider the growth of the organisation and the funds needed to

promote and expand the current business if it has been included in

the operational strategies and business plan

• You need to allow for emergencies or unplanned events. As

mentioned you will have contingencies in place for such effects

but you need to ensure that funds have been allocated as well.

• Remember when allocating your funds you meet all the legal and

regulatory requirements of the industry and sector.

• The use of company funds for personal use or without company

approval is considered embezzlement and should be avoided at all

times. If you are unsure about where particular funds need to be

allocated, seek the advice of a qualified accountant or financial

expert for clarification.

ALLOCATING COSTS

• To facilitate planning and control, the budget process needs to

match costs with the business’s productive activities, and with

those managers responsible for the productive activities of the

business

• Activity-based costing (ABC) is a special costing model that:

− identifies activities in an organisation

− assigns the cost of resources via these activities to all

products/services provided to customers

− supports strategic decisions regarding pricing, outsourcing and

process improvement initiatives.

ALLOCATING COSTS• The ABC model assigns more indirect costs (overheads) into direct

costs compared to conventional costing models. With ABC an

organisation can better estimate the cost elements of products and

services.

• This can assist in:

− identifying and eliminating products and services that are

unprofitable

− raising/lowering the prices of products and services that are

under/overpriced

− identifying and eliminating production or service processes that

are ineffective, and

− promoting processing concepts that lead to the very same

product or service but at a better yield.

MASTER BUDGET TO COST CENTRES

In order to break up a firm’s master budget into the various cost

centres you will need to determine the following:

• The basis of cost centre splits, i.e. by location or by function type.

• The name and number of cost centres.

• The metrics for each cost centre, e.g. customer number,

production numbers, sales amount, sales units.

• The basis for allocating overheads, e.g. per client, by use, equally

between the cost centres.

• When splitting a master budget into cost centres, the first aspect

to focus on is the revenue or production details. These will help

determine the allocation of overheads.

MASTER BUDGET TO COST CENTRES

• Consider the example below:

Sales team

Sales % % Break upAllocating $10,000

telephone

Central 450,000 45% $4,500

North 250,000 25% $2,500

South 300,000 30% $3,000

Total 1,000,000 100% $10,000

MASTER BUDGET TO COST CENTRES

Other types of budgets:

1. The Marketing Manager’s budget will specify the financial resources

available for sales staff salaries, advertising and promotions

expenditure...but will include sales and revenue targets too.

2. The Operations Manager’s budget may specify the financial resources

available for raw materials, staff salaries, and equipment...but may

include production, cost and efficiency targets as well.

3. The Finance Manager needs to control and manage the flow of money

in and out of the company...and use a cash flow budget to do it.

4. The Finance Manager will also assist the CEO manage the MASTER

BUDGET...the one that brings all the contributing budgets together to

help ensure that the profit objectives of the business plan are being

met.

THE TIME DIMENSION

Cash vs. Accrual Accounting

• Another problem in allocating costs is the need to take into

account when costs (and revenues too) are associated with the

productive activities of the business. To deal with this problem,

Accountants distinguish between two approaches to accounting,

that is, Cash vs. Accrual Accounting.Cash accounting – this method is usually used by sole traders,

partnerships and small businesses. In cash accounting,

only the revenues actually received and the expenses

actually paid are recognised in the financial statements for the

relevant accounting period.

Accrual accounting – this method is generally used by medium to large businesses.

Revenues are recognised in the accounting period in which they

are earned (regardless of whether the payment has been

received) and expenses are recognised in the accounting

period in which they are incurred (regardless of whether payment

has been made).

THE TIME DIMENSIONCash vs. Accrual Accounting

• Accrual accounting is the preferred method as it allows for the matching of

revenues with the expenses incurred in earning that revenue in any given period

(known as the matching principle). This allows for more accurate evaluation of

the performance of the business as a whole, and individual managers.

• In order to accurately reflect the revenues and expenses for a specific period the

following accounts are needed:

− Accrued revenue (asset) – revenue that has been earned but the cash has

not yet been received

− Accrued expense (liability) – an expense that has been incurred but not yet

paid

− Prepaid revenue (liability) – cash has been received but the revenue has not

yet been earned

− Prepaid expense (asset) – an expense that has been paid for but has not yet

been incurred

THE TIME DIMENSION

Budget Cycle

Budget cycles can be:

• SHORT TERM (monthly or quarterly e.g. sales budgets)

• MEDIUM TERM (annually e.g. the business plan)

• LONG TERM (three to five years e.g. the strategic plan)

There is an example of a business plan and budget process cycle in

the following slide.

THE TIME DIMENSION

JulyNew Fiscal Year

BeginsAugust-September

Review actual results from prior year for inclusion in Business

Plans

September – DecemberDepartments update business plans and develop Operating

Budget requests

September – DecemberCIP Team meets with

Departments

MayFormal presentation of

recommended Operating and Capital Budgets

FebruaryDepartments submit Operating

Budget Requests for Budget Analysis Review

JuneCommissioners hold public

hearing, work session, and adopt Operating and Capital

Improvement Plan Budgets

JanuaryBoard of Commissioners

Retreat

JanuaryMid-Year Budget

Projections

Business Planning & Budget Process Cycle

Note: This Chart depicts the integration of the annual budget cycle and business planning process

BEST PRACTICE BUDGETING

Link budget development to corporate strategy

• Clearer understanding of corporate goals

• Greater support for goals

• Better coordination of tactics

• Stronger companywide performance

• Fewer revisions

• Faster and less costly budget process

• Less frustration

BEST PRACTICE BUDGETINGAllocate resources strategically

• Within companies, managers compete for scarce resources

• Budgeting involves making choices between alternatives

• Best practice requires:

− careful evaluation of operational plans and operational budget

submissions

− evaluation of risk

− cost-benefit analysis

− contingency planning

Tie incentives to performance measures not budget targets

• Budgets are a means to an end, not an end in themselves

• Incentives for managers should be tied to strategic objectives

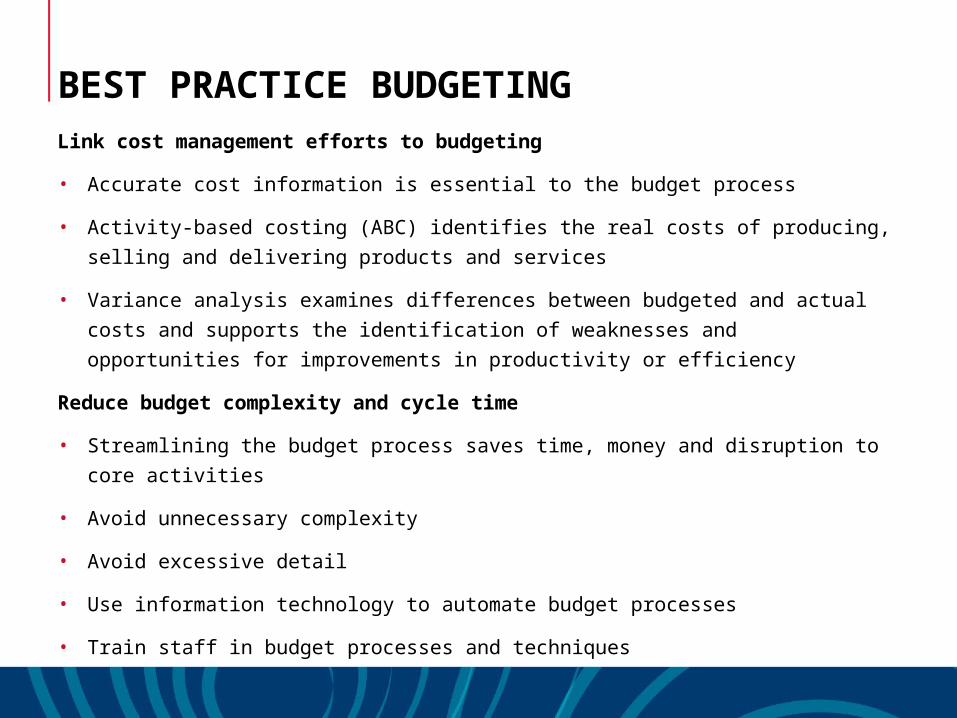

BEST PRACTICE BUDGETINGLink cost management efforts to budgeting

• Accurate cost information is essential to the budget process

• Activity-based costing (ABC) identifies the real costs of producing, selling and

delivering products and services

• Variance analysis examines differences between budgeted and actual costs

and supports the identification of weaknesses and opportunities for

improvements in productivity or efficiency

Reduce budget complexity and cycle time

• Streamlining the budget process saves time, money and disruption to core

activities

• Avoid unnecessary complexity

• Avoid excessive detail

• Use information technology to automate budget processes

• Train staff in budget processes and techniques

BEST PRACTICE BUDGETING

Develop budgets that accommodate change

• Faster and more effective response to competitive threats and

opportunities

• Flexibility increases the scope for managers’ initiative

• Flexibility reduces incentives for managers to build safety margins

into budget estimates and promotes more accurate and more

efficient budgeting

• Report changes in business conditions at the same time that

budgets are reviewed

• Encourage contingency planning to facilitate budget flexibility