Title of the panel - IPPA · Title of the panel Going Universal? Universal Health Coverage on Paper...

39

1 3 rd International Conference on Public Policy (ICPP3) June 28-30, 2017 – Singapore Panel T17a P07 Session 1 Title of the panel Going Universal? Universal Health Coverage on Paper and in Practice Title of the paper Implementing Policy Under A Decentralized And Democratic Polity: Lesson Learned From Indonesian Policy Transition Towards Universal Health Coverage Author Wahyudi Kumorotomo Gadjah Mada University, Indonesia [email protected] Date of presentation June 28th, 2017

Transcript of Title of the panel - IPPA · Title of the panel Going Universal? Universal Health Coverage on Paper...

1

3rd International Conference

on Public Policy (ICPP3) June 28-30, 2017 – Singapore

Panel T17a P07 Session 1

Title of the panel

Going Universal?

Universal Health Coverage on Paper and in Practice

Title of the paper

Implementing Policy Under A Decentralized And Democratic Polity:

Lesson Learned From Indonesian Policy Transition Towards Universal Health Coverage

Author

Wahyudi Kumorotomo Gadjah Mada University, Indonesia

Date of presentation June 28th, 2017

2

Implementing Policy Under A Decentralized and Democratic Polity: Lesson Learned from Indonesian Policy Towards UHC (Universal Health Coverage)

ABSTRACT This study is aimed at explaining the implementation process of a public policy using an Indonesian case, especially the health policy towards a UHC (Universal Health Coverage), an area of policy that is being planned and implemented in many developing countries. Since 2014, the Indonesian government launched a comprehensive policy for more effective social welfare system. Under a grand design of the National Social Security System, two agencies called BPJS (Badan Pelaksana Jaminan Sosial, Social Security Administering Bodies) are set up. The BPJS program on health is targeted to cover at least 121.6 million Indonesian in the first year and would cover all the population in 2019. The government is trying to deal with a far-reaching health-care reform to create a Universal Health Coverage (UHC) that has been in practice in many developed countries. In order to finance the program, the government has worked out two systems. First, individuals living below the poverty line will get financial assistance under the Premium Payment Assistance (PPA). Second, individuals who are employed and able to finance the premium are included in the non-PPA group consisting civil servants, private sector employees, entrepreneurs, military and police officers. However, it is still unclear whether the government is ready to deal with financial provision according to the initiated coverage. The financial shortage might also be expected in providing premium for wage-earners and non-salaried workers. The BPJS finance has run a deficit in the last three years at about 4 percent. Under a decentralized system, there have been issues about coordination of policy and expenditures between the central and regional governments, in the interests of both equity and also efficiency. Deteriorated quality of services in health care have forced well-paid workers to seek higher-quality care elsewhere under a financial scheme of insurance providers. Keywords: democratic governance, health finance, Universal Health Coverage, policy implementation, Indonesia.

3

I. INTRODUCTION

Having been stalled for years, the Indonesian government launched a

comprehensive policy for more effective social welfare system. Under a grand

design of the SJSN (Sistem Jaminan Sosial Nasional, National Social Security

System), two agencies called BPJS (Badan Pelaksana Jaminan Sosial, Social

Security Administering Bodies) have been set up. The first BPJS on health is

initiated under the universal health-‐‑care program, known as Jaminan Kesehatan

Nasional (JKN) or National Health Insurance. This BPJS on health has been

operational since January 2014 by merging four state-‐‑owned companies that

traditionally focusing their businesses on health insurance. The second BPJS will

be launched in July 2015 to offer accident and life insurance as well as pension

programs.

The BPJS program on health is targeted to cover all the population by the

end of 2019. In effect, the coverage target is planned from a process of a

conversion and a registration procedure. The conversion includes 24.5 million

individuals formerly registered under Askes and Jamsostek, the state insurance

provider for public officials and formal private companies' employees, 86.4

million individuals under the community health insurance scheme (Jamkesmas),

and 1.6 million individuals from the military and the police registered under the

scheme of Asabri. The registration is expected to come from individuals who

would see the benefit of having a health insurance under the government-‐‑

administered system.

It appeared that the Indonesian government is trying to deal with a far-‐‑

reaching health-‐‑care reform to create a Universal Health Coverage (UHC) that

has been in practice in many developed countries. The JKN covers

comprehensive benefits from infectious diseases such as influenza to expensive

medical treatment such as heart surgery, dialysis and cancer therapies. In order

to finance the JKN, the government has worked out two systems. First,

individuals living below the poverty line will get financial assistance under the

PBI (Penerima Bantuan Iuran, Premium Payment Assistance). Second,

individuals who are employed and able to finance the premium are included in

4

the non-‐‑PBI group consisting civil servants, private sector employees,

entrepreneurs, military and police officers.

However, it is still unclear whether the government is ready to deal with

financial provision according to the initiated coverage. In 2014, while the

government has increased budget allocation for Jamkesmas from Rp 8.29 trillion

to Rp 19.3 trilion, the minimum premium remained at Rp 19,225 ($ 1.57) per

person. The financial shortage might also be expected as the premium collected

from wage-‐‑earners and non-‐‑salaried workers would not be enough to finance

health services. Dr. Fahmi Idris, the director of BPJS, was quoted as saying that

until December 2014, the government could only collect Rp 41 trillion from the

premium while the claims liability has amounted to Rp 42.6 trillion, a mismatch

of 103.88 percent (Kontan, 17 Feb 2015). Nevertheless, according to the

government plan, the proposal to raise the premium from Rp 19,225 to Rp

27,500 would only be materialized in 2016.

In order to avoid insolvency in the JKN system, the Ministry of Health has

set low reimbursement levels for hospitals. Although most of the hospitals have

signed up for JKN, the low reimbursement might eventually dampen the interest

of private clinics and hospitals, which lead to overcrowding in state hospitals.

Another possibility is that the deteriorated quality of services in health care

would force well-‐‑paid workers to seek higher-‐‑quality care elsewhere under a

financial scheme of insurance providers.

This study is aimed at explaining the implementation process of the

Indonesian new health-‐‑care system administered by the BPJS with the focus on

financial aspect. As a national policy involving millions of citizens, it is important

to understand how the JKN will affect the government budget, whether the policy

is financially solvent, and whether the targeted coverage is realistically

sustainable. Aside from describing the national picture of the JKN policy, the

study will be explaining its implementation at the regional level.

The analysis is conducted based on the available online data on the

national government budget, especially from the master plan of the SJSN and the

JKN schemes that are published by the Indonesian Ministry of Health. In order to

get the international perspectives, comparative analysis will be exercised using

the experience of countries adopted or those that are in transition towards the

5

UHC. Policy notes, journals, and references that are available in the WHO

headquarter and UNRISD were referred to conduct the analysis. Aside from the

available online resources and WHO library, interviews and discussions with

experts in Graduate Institute of International and Development Studies,

University of Geneva, are also carried out.

In Indonesia, statistics on local hospitals, clinics, diagnostic centers, and

the available human resources such as doctors, nurses and paramedic officers

are collected from the local Dinas Kesehatan (Local Agency of Health) and public

hospitals. Interviews with the director of regional BPJS and the Jamkesda were

undertaken to understand what has been happening on the ground. Some

additional interviews with stake-‐‑holders and medical doctors and patients who

registered into the BPJS system have also been undertaken.

The master plan for implementing JKN has been laid out by the Ministry

of Health in the Road-‐‑Map for National Health Insurance 2012-‐‑2019, a

complicated and ambitious policy for a country that is targeting universal

coverage for 252.8 million people. Table 1 describes the main elements of JKN.

Table 1. Financial Plan for Indonesian Universal Health Coverage

Resource Collection Pooling Purchasing / Provision Government budget to public facilities.

Existing funds to be pooled and managed by BPJS.

Payments to public and private health facilities.

Government contribution for poor and near-‐‑poor: Rp 22,000 -‐‑ 27,000 ($ 2.2 -‐‑ 2.7) per month.

Jamkesmas Jamkesda (some) Askes Asabri Jamsostek. 2014 target: Rp 121.6 million covered.

Public Health Clinics and private providers: capitation. Hospitals: Diagnosis Related Groups (INA-‐‑CBG) based payments to be negotiated and varied according to region.

Self funded contributions. Laborers: 5-‐‑6% of monthly wages. Non-‐‑wage laborers / informal sector: 5-‐‑6% of monthly wages. To be covered partly by the government.

2019 target: Entire population, including the remaining Jamkesda scheme. Total predicted coverage in 2019: 256.5 million people.

Benefit packages: Comprehensive. Initially third-‐‑class hospital for government funded and second-‐‑class hospital for self funded. Target: second-‐‑class for all by 2019.

Source: Road-‐‑map of JKN; Mboi,2014

6

According to the plan, the transformation of five existing schemes

(Jamkesmas, Askes, Asabri, Jamsostek, and parts of Jamkesda) into a single

scheme under BPJS should be completed in 2014. Then, the BPJS will manage the

health insurance scheme for all people who have paid the premium and all for

whom it has been paid. As explained earlier, the BPJS system will cover both the

premium payers as well as poor individuals whose premium is paid by the

government under the Premium Payment Assistance (PBI). Monthly premium

and membership fee (4.5% of salary) are made compulsory for all the workers,

and the registration is to be completed in mid 2015. By 2017, all big and medium

enterprises are expected to have the scheme. By 2018, the small enterprises are

targeted to join. And by 2019 all Indonesian citizens and foreigners who work

permanently in the country should be covered by the BPJS scheme.

At the international level, studies on the transition of health financing

towards universal coverage are still lacking or fragmented at best. According to

Savedoff (2012), there are typically four areas of study on health financing; First,

studies that address the growth in health spending and are mostly concerned

with efforts to reduce costs and improve cost-‐‑effectiveness. Second, studies on

the rising share of pooled funding that are usually focus on institutional issues

such us the merits of public and private provision, insurance, and services.

Thirds, studies on the effects of public policies like user fees and community

health insurance, the impact of out-‐‑of-‐‑pocket (OOP) expenditures on people's

risks of impoverishment, and generally focus on how to reduce OOP spending on

health. Fourth, studies that try to disentangle causality, asking whether rising

incomes are responsible for improved health or if improvements in health have

driven economic growth.

Under such research mapping, this study relates to the second category

and seeks to provide a better picture on how to raise pooled public fund that is

critical for extending health services to attain universal coverage. How should

decisions are made when there is an issue of government contribution? Given the

coverage that would imply a large number of individuals in diverse regional

health facilities, is the national standard applicable for all the regions? What

should be done if there is a problem of insolvency and financial sustainability?

7

These are the questions during the implementation stage that would determine

the success of health policy in Indonesia.

II. PATHWAYS TOWARD UNIVERSAL HEALTH COVERAGE (UHC)

a. The Social Nature of Universal Coverage

The main issue of health services for the poor is the burden of payments

that have to be born by individuals, that is the so-‐‑called out-‐‑of-‐‑pocket payments.

Around the globe, out-‐‑of-‐‑pocket payments create financial barriers that prevent

millions of people from receiving needed health services. And many of those who

pay for health services are confronted with financial catastrophe and

impoverishment (Carrin et al, 2008). Even some people who have enough

income might eventually confront financial problem when they are getting old or

experiencing health problem and cannot get sufficient insurance to cover health

services.

Therefore, the idea of universal coverage is to protect people, at all

income levels, from financial risks associated with ill health. In all countries, the

question is how to create health financing systems that are able to achieve and

maintain universal coverage. By definition, universal coverage certainly implies

basic social security as it meant to secure access for all individuals to appropriate

promotive, preventive, curative and rehabilitative services at an affordable cost.

One should note, however, that the concept of universal coverage is not based on

subjective judgment of the policy makers. Many politicians say that they have

launched a social health protection and are committed to implement health

finance for all. Yet political statements and program launching is not enough. The

conceptual fault here is that universal coverage sometimes can be used to justify

practically any health financing reform (Kutzin, 2013) while the objective

coverage is not entirely attained. The objective of universal coverage is efficiency

and equity in health resource distribution so that objectivity, transparency and

accountability have to be assured.

Before a country can set up a full-‐‑fledged universal coverage, it usually

takes a route of gradually implementing Social Health Insurance (SHI). The WHO

8

recognizes SHI as a social mechanism for raising and pooling funds to

finance health services, along with tax-‐‑financing, private health insurance,

community insurance, and others (Carrin & James, 2004). In many European

countries, working people and their employers, as well as the self-‐‑employed, pay

contributions that cover a package of health services available to other people,

who then become their dependents or the insurees.

The governments sometimes also pay subsidies into these systems in

order to ensure the financial sustainability. This is something that might be

problematic in most developing countries for two reasons; First, the

governments are not able to collect taxes and enough revenues to support the

subsidy. Second, the contribution should be made compulsory and therefore it

has to be explicitly stated in the law and the government has to enforce the

provision. Therefore, it is important that the government should give attention to

the issues of financial adequacy while expanding coverage can only be attained

through a strong policy determination towards better health services for the

whole society.

One of the most formidable challenges for policy makers is how to make

public contribution compulsory for certain elements of the society so that a large

pool of funding would be enough for universal coverage. It should be noted that

no country has attained universal coverage by relying on voluntary

contributions. There are many possible schemes for health insurance that are

offered by commercial companies, state-‐‑owned enterprises, non-‐‑government

organizations, or community raised funding, but at the end the government

should regulate that the contribution for universal coverage is compulsory.

Once the government makes it compulsory for all the citizens to register

and to contribute to a nationally-‐‑pooled insurance, a necessary condition for

universality is attained. Some middle-‐‑income countries may opt to explore

voluntary prepayment mechanisms as an alternative to out-‐‑of-‐‑pocket payments,

but experts say that this would rarely become a long-‐‑term solution toward a

universal coverage (Kutzin, 2012). For that reason, it is important that the

government understand the ultimate goal of universal health coverage as parts

of social program that needs long-‐‑term vision of national development.

Although the idea of risk pooling is appealing for policy makers in many

9

countries, however, there fact is rather disappointing. The World Health

Organization reported in 2010 that more than half of the world population is

lacking any type of social and healthcare protection. In many cases, lack of health

care services is caused by low level of income in developing countries. Individual

and household health care programs cannot be sufficiently financed as the

governments cannot get enough revenues from taxes and service charges.

Surprisingly, universal coverage is also an issue in developed countries.

The United States of America, for example, is an economic giant and spends more

than 17.9 percent of its GDP (among the highest proportion in the world), yet

15.4 percent of its population remains uncovered by health insurance (US

Census Bureau, 2012; World Bank, 2014). The ineffective free-‐‑market

mechanism to provide health services for the poor is the main reason for many

countries to embrace universal coverage. Therefore, it is encouraging that the

USA and China, the two major economic powers that previously relied on private

insurance for health care, are currently moving back to universal coverage

policy.

Low-‐‑income and middle-‐‑income countries are recently making steps

towards developing health systems that would cover all of its population, a

policy that has been adopted in most European countries since World War II. The

BRIC (Brazil, Russia, India, China) are among the most populated countries

implementing policies toward universal coverage. Countries in Africa, such as

Ghana, Moldova and Rwanda are adopting the new health systems to cover all

the citizens. In Asia, similar policies have been implemented in Kyrgystan,

Malaysia, Thailand and Indonesia.

In Europe, universal coverage emerged from a belief in solidarity, a fear of

revolution, and a changing view of the role of the state. Substantial benefits

accruing from universal health care have been acknowledged from the

experience of European countries, especially Germany, France, England,

Netherlands and Switzerland, which have implemented the policy since the end

of World War II. However, even when the policy has been in practice for decades,

the universal benefits cannot be taken for granted. Recently, due to economic

slow down in some parts of Europe, universal health care is under a threat

(McKee, 2013). Even in well developed European countries, radical austerity

10

policies posed a threat for universal health coverage, particularly in countries

where the governments perceived serious moral hazards in their social security

programs.

That is why strong national leadership and long-‐‑term commitment are

essential to achieve and sustain universal coverage policy. Experience from

middle-‐‑income countries tells how national leadership in can be critical in the

overall goal achievement. For example, the national government in Turkey

clearly stated that it is illegal for a hospital to retain patients who are unable to

pay for a healthcare service (Atun et al, 2013). Such a measure was taken under a

comprehensive health plan started in 2003. Although Turkey is still in progress

towards an appropriate scale of equitable coverage, its clear policy on access and

affordability would help a long the way.

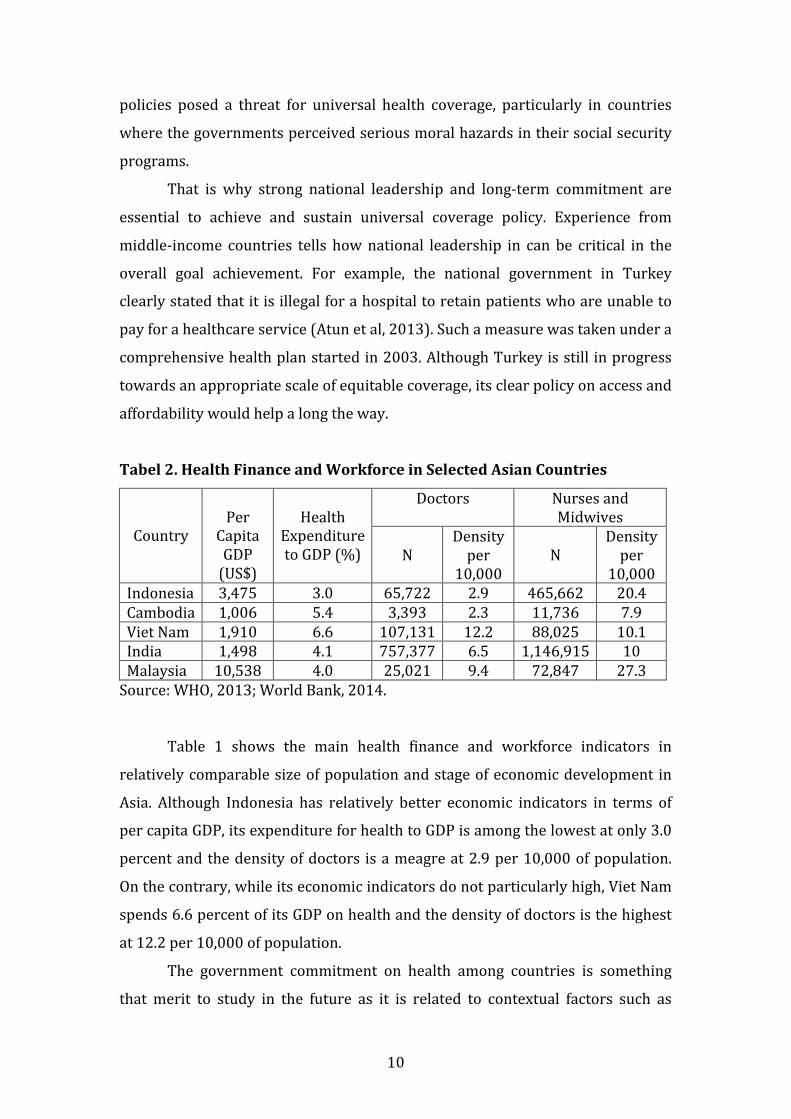

Tabel 2. Health Finance and Workforce in Selected Asian Countries

Country

Per Capita GDP (US$)

Health

Expenditure to GDP (%)

Doctors Nurses and Midwives

N

Density per

10,000

N

Density per

10,000 Indonesia 3,475 3.0 65,722 2.9 465,662 20.4 Cambodia 1,006 5.4 3,393 2.3 11,736 7.9 Viet Nam 1,910 6.6 107,131 12.2 88,025 10.1 India 1,498 4.1 757,377 6.5 1,146,915 10 Malaysia 10,538 4.0 25,021 9.4 72,847 27.3 Source: WHO, 2013; World Bank, 2014.

Table 1 shows the main health finance and workforce indicators in

relatively comparable size of population and stage of economic development in

Asia. Although Indonesia has relatively better economic indicators in terms of

per capita GDP, its expenditure for health to GDP is among the lowest at only 3.0

percent and the density of doctors is a meagre at 2.9 per 10,000 of population.

On the contrary, while its economic indicators do not particularly high, Viet Nam

spends 6.6 percent of its GDP on health and the density of doctors is the highest

at 12.2 per 10,000 of population.

The government commitment on health among countries is something

that merit to study in the future as it is related to contextual factors such as

11

political history, education, and culture. The similar notion also applies when one

should analyze the transition towards universal coverage for health services.

b. Indonesian MoH Road Map

The Ministry of Health has set up an action plan for BPJS Kesehatan

consisting six task forces that are responsible for the following implementation

areas:

a. Health facilities, referral system and infrastructures;

In total, the country provides 2,302 hospitals with 264,303 beds. There

are 40 medical doctors, 11 dentists, 75 midwives and 158 nurses for

every 100,000 population.

b. Finance, transformation of programs and institutions;

Setting premiums and tariffs are among the crucial task for the BPJS. The

transformation of existing insurance and health schemes (Jamkesmas,

Askes, Jamsostek) into a universal health insurance is in progress.

c. Regulatory supports for implementation;

Government Regulation No.101/2012 on the beneficiaries of government

subsidy and Presidential Decree No.12/2013 on social health insurance

have been operational. However there are more technical regulations,

MoH decrees, and procedures for health insurance scheme to be

formulated and implemented.

d. Human resource and capacity building;

It is to develop human resource mapping, distribution, and assignment. As

the universal health insurance requires new approach in managing

hospitals, doctors, nurses and other human resources, new mind-‐‑set is to

be disseminated among them.

e. Pharmaceutical and medical devices;

The tasks include developing e-‐‑catalogue for national medical system,

setting formularies for drugs and medical devices, and establishing a

Health Technology Assessment that is responsible for supervising

pharmaceutical industries.

f. Socialization and advocacy;

12

This task-‐‑force is responsible for preparing materials, strategies, and

media for national campaigns or socialization. It remains to be seen

whether the 2019 target of creating a single healthcare system is realistic

enough to be completed.

In accordance to the MoH Decree No.69/2013, the BPJS adopts the latest

version of Indonesia Case Based Groups (INA-‐‑CBG) tariff as its pattern for

processing and paying medical claims. The INA-‐‑CBG is a diagnostic

reimbursement system that replaced the previous fee-‐‑for-‐‑service

reimbursement system. After being launched on January 2014, the BPJS has

collected Rp 5.4 trillion ($ 475.2 million) in premiums and paid out Rp 1.04

trillion in claims to hospitals. Most of high-‐‑rank officials in the MoH believe that

BPJS will be financially strong in the long run.

However, many hospital managements and doctors do not share those

beliefs. Increased numbers of BPJS members seeking hospital services under the

JKN program have led public hospitals struggling with expenses. Indicative

observations also noted that many poor patients have been rejected by public

hospitals. The patients have been desperately seek appropriate beds for medical

treatments in the Community Health Service and Type C hospitals as the

management declares that all beds are fully occupied. The hospital managements

worry that they would face financial insolvency if they accept all the poor patient

applications (Tijan, 2014).

The financial consequence of universal health insurance for the national

budget is something that has not been made public, including the plan of

president Joko Widodo who keen on making Kartu Sehat (Health Cards) in line

with the BPJS system. Already in April 2014, Minister of Health Nafsiah Mboi

stated the need to revise healthcare tariff for JKN by arguing that the health

facilities and medical workers paid less than what procedures cost (National

News, Jakarta, 01/04/2014). The contribution rate will ultimately have to be

increased if the benefit is higher, or else the benefits will ultimately have to be

reduced in order to keep the cost the same (World Bank, 2012). Again, this

indicates that continuous assessment on the INA-‐‑CBG tariffs is one of the

prerequisite to ensure BPJS financial viability, a big task for Mrs. Nila Moelok, the

newly appointed Minister of Health.

13

As a single entity allowed to collect medical funds for all Indonesian

citizens, the BPJS will have an enormous power to ensure that all the services

provider (hospitals, clinics, doctors, diagnostic centers) to follow the standards

for quality, efficiency, timeliness and service effectiveness. This will in effect

abolish fee-‐‑for-‐‑service system that is proven to be costly. However, the JKN

system is still unclear about how to make the BPJS held accountable to the public.

A supervisory body at the national level is yet to be established. Another

uncertainty is how the government will impose sanctions on employers and

employees who fail to participate in the BPJS programs. The BPJS registration is

currently conducted on voluntary basis and ultimately there are risks that the

universal health coverage cannot be completed according to the plan.

III. CONNECTING FINANCE WITH GOALS: THE BPJS PERFORMANCE

a. Coverage

In order to assess the effectiveness of Indonesian health finance policy to

cover health services for the population, it is important to consider how has been

the performance of the BPJS in integrating various health schemes in the country.

As a health scheme specifically targeted for the poor and near-‐‑poor, the

Jamkesnas is now managed by the BPJS. Jamkesnas program was started in 2005

as Askeskin, literary means health insurance for the poor. In 2007, the Askeskin

that was originally based on households was renamed Jamkesmas to be based on

individuals and expanded to also cover the near-‐‑poor. With the official estimates

indicate that there are 76.4 million poor and near-‐‑poor beneficiaries of the 252.8

million total population in 2014, the BPJS is managing formerly Jamkesmas to

cover almost one third of the population.

With the funding of about a quarter of the central government budget on

health, the BPJS handling on Jamkesmas target is likely determine the Indonesian

government intention to attain a universal coverage. It is therefore important to

analyze the whole institutional arrangement for health policy in Indonesia as

administrative efficiency is also a key factor determining the quality and the

coverage of health services in the country.

14

Indonesia spent 3.0 percent of its GDP on health with the total health

expenditure per capita of US$ 104.25 in 2014. The public spending accounted for

41.1 percent of the total health expenditure and almost half of the public

spending was at the district level. As described earlier, this level of spending is

relatively low among countries with comparable levels of income. And, due to

decentralization policy started in 2001, the effectiveness of health spending

might even lower as it depends on how the district governments spend their

budget on health. Under Indonesia's decentralized system, provincial and district

governments are responsible for health service delivery and that is why they

account for nearly half of the government spending on health.

Since 2014, the BPJS is aimed at integrating Jamkesmas, Jamsostek, Askes,

and Jamkesda (which actually means insurance schemes managed by provincial

and district governments). However, it turned out that most of Jamkesda

schemes are currently managed by the provincial and district governments.

There have been resistance from some of the provincial governors and district

heads to fully integrate to the BPJS systems on the grounds that most

beneficiaries at the local levels are in favor of the Jamkesda and they have been

registered by the Jamkesda. As a compromise, the BPJS is applying the so-‐‑called

"bridging" program for registration and for reimbursement of health services

provided by public as well as private hospitals. Therefore, in many provinces and

districts the Jamkesmas is complemented and even substituted by the Jamkesda

Based on the SHA (System of Health Accounts) for Indonesia (Soewondo

et al, 2011), it is also indicated that 51.6% financial resources for healthcare

provision is carried out by public and private hospitals. Nevertheless, the

institutional picture is actually more complicated. At the community level,

healthcare services are undertaken by voluntary workers in the Poskesdes

(Village Health Posts) and Posyandu (Integrated Service Posts). Voluntary

midwives and nurses work at the Poskesdes to provides curative services.

During a monthly gatherings, voluntary workers run the Posyandus that are

assisted by a doctor and nurses from the Puskesmas (Sub-‐‑district Health Clinics)

and the Pustu (smaller scale Puskesmas). In 77,465 villages throughout the

country, there are 53,152 Poskesdes' and 268,439 Posyandus.

15

Puskesmas and Pustu at the sub-‐‑district level are managed by a medical

doctor and assisted by nurses and midwives to carry out basic health services.

Six basic services for the Puskesmas and Pustu include: 1) health promotion, 2)

environmental health, 3) maternal and child health services (including family

planning), 4) community nutrition program, 5) prevention and eradication of

communicable diseases, and 6) basic medical treatments. The number of

Puskesmas and Pustu has increased from 7,699 in 2005 to 9,321 in 2011, which

means an average growth of 3.5 percent per annum (Suryahadi et al, 2014). Due

to geographical and financial diversity across the districts, however, there is

diversity in Puskesmas and Pustu services. In some urbanized districts,

Puskesmas may have inpatient facilities and more comprehensive medical

treatments. But in remote districts of Maluku or Papua islands, the Puskesmas

may not have a professional medical doctor while medicines and treatments are

severely lacking.

The total number of hospital in Indonesia has increased from 1,145 in

2000 to 2,302 in 2014. The inpatient facilities are also improved as the total bed

number increased from 107,537 to 264,303 in the same period. Nevertheless, as

also indicated earlier, the bed to population ratio in Indonesia is still among the

lowest among East Asian and Pacific countries. The Ministry of Health

categorizes general hospitals into classes: Class A with more than 400 beds,

certain number of specialized medical doctors, and advanced equipment; Class B

with 200-‐‑400 beds, some specialized doctors and standard equipment; Class C

with 100-‐‑200 beds, general medical doctors and basic equipment; and Class D

with 50-‐‑100 beds with mostly general medical doctors. As explained, Class A and

B hospitals tend to be available in more urban areas while Class C and Class D

hospitals and Puskesmas are those mostly available in rural and remote areas.

There are also three classes of Special Hospitals with health services focusing on

medical specialties (obstetric and gynecology, ophthalmology, oncology,

dentistry, internist, surgery, urology, cardiology, psychiatry, neurology, etc).

As a middle-‐‑income country with GDP per capita of US$ 3,475 in 2014 and

enjoyed good economic growth rates in the last few decades, Indonesia has made

impressive health gains. Life expectancy at birth has increased from 45 years in

1960 to almost 70 years in 2010. Infant mortality rate has dropped from 128 per

16

1,000 live births to 27 per 1,000 live births in the same period. However, poverty

and poor health services continue to be a fundamental issue in the country.

About 18 percent of its population continues to live below US$ 1 a day.

Malnutrition rates are particularly high as reflected in the fact that 35.6 percent

of Indonesian children under 5 are stunted. The government envisioned that

issues on poverty and health services could be addressed by Jamkesmas

program.

Figure 2. Out-‐‑of-‐‑Pocket (OOP) Shares of Total Health Expenditure (%)

Source : WHO, SUSENAS.

Figure 3. Insurance Coverage Among Three Population Groups

Source: Adapted from Thangcharoensathien, 2011; MoH, 2014

46.6 48.2

41.844.7

49.1 47.2 45.442.5

14.418.1

27.2 28.1 26

36.2

46.3 47.2

0

10

20

30

40

50

60

1995 1998 2001 2004 2007 2010 2013 2015

OOP shares

Insurance Coverage

16% 20%

64%

100%

15%20%

13%

48%

0%

20%

40%

60%

80%

100%

120%

Formal sector

The poor Informal sector

Total

Population

Insurance Coverage

17

The access and the quality of health care facilities remain a problem in

Indonesian remote districts. Starting from 2010s, the health insurance coverage

has surpassed the percentage of out-‐‑of-‐‑pocket spending. Yet even after the

establishment of BPJS and further implementation of Jamkesmas, the out-‐‑of-‐‑

pocket spending in the country in 2015 is predicted to remains high at 42.5

percent (Figure 2), far above the WHO recommended rates of 15 to 20 percent.

One should note that the WHO recommended rates of 15-‐‑20 percent are based

on the assumption that only at those levels is risk of impoverishment due to

catastrophic health spending generally found to be low (WHO, 2010).

Although the BPJS program may help Indonesia to catch up international

standard of coverage, the challenge is formidable given its sheer size of

population and its diverse targets. Figure 3 shows that while the formal sector

workers have been mostly covered by insurance schemes and the poor may be

covered under the PBI scheme, only 13% of informal sector workers are covered

by health insurance. These are the people belong to the precarious group who

can be impoverished once a family member is severely sick and the family have

to bear the out-‐‑of-‐‑pocket burden of health services.

The existence of prepayment system does not guarantee financial

protection. The international experience has proven this caveat. For example, in

India, 15% of individuals enrolled in the Self-‐‑Employed Women Association are

faced financially catastrophic level of payment even after reimbursement for

hospital admission; in China, Chinese Rural Cooperative Medical System covers

only 30% of inpatient expenditure, yet there is relatively a rare case of financial

catastrophes (Thangcharoensathien et al, 2011). Therefore, the Indonesian

authorities should really be careful in assessing the Jamkesnas scheme,

particularly in evaluating whether the scheme is effective in reducing out-‐‑of-‐‑

pocket spending among the poor and near-‐‑poor.

BPJS scheme on healthcare system is designed to cover both the premium

payers as well as poor individuals whose premium is paid by the government

under the Premium Payment Assistance (PBI). All the standards for services,

eligibility for members, and premium rates, are set by the Ministry of Health. To

expand healthcare coverage, the BPJS is responsible for registering health

18

beneficiaries, administering membership, supervising health-‐‑care providers, and

managing claims and complaints. For registering beneficiaries, BPJS and MoH

refers to national statistics that is compiled by the BPS (Badan Pusat Statistik,

National Bureu of Statistics). The providers -‐‑-‐‑ public and private hospitals, health

clinics, and community health centers -‐‑-‐‑ would then claim fees and medical

services provided by the Ministry of Health via the BPJS offices.

For the formal sector workers, the monthly premium and membership

fee (4.5% of salary) are made compulsory, and the registration is to be

completed in mid 2015. For the informal workers, the nearly-‐‑poor and the poor,

the minimum monthly premium under the PBI scheme has been adjusted from

Rp 5,000 (0.6 US$) in 2007 to Rp 19,225 (1.57 US$) in 2014. According to MoH

Decree No.69/2013, the BPJS must adopt the latest version of Indonesia Case

Based Groups (INA-‐‑CBG) tariff as its pattern for processing and paying medical

claims. The INA-‐‑CBG is a diagnostic reimbursement system that replaced the

previous fee-‐‑for-‐‑service reimbursement system.

Based on the estimate that the government finance is targeted to cover

86.4 million with the PBI premium of Rp 19,225 per person per month, the

central government's contribution to BPJS would equal to Rp 19.9 trillion. Since

the government budget in 2014 was only Rp 44.9 trillion, it implies that almost

half of the overall government health budget would be used to finance the BPJS.

Then, the consequence is straightforward: the share for financing other areas of

spending such as salaries and operating costs for centrally-‐‑financed hospitals,

investments in improving supply and much-‐‑needed preventive and promotive

interventions would have to be shrunk. The 2015 budget is allocating Rp 47.8

trillion. With this incremental increase in the government budget, there would

only two possibilities: pending the reimbursement of BPJS claims, or reducing

other expenditure components in health. Without additional funds to cover the

elderly, orphanage children, street children, homeless people and informal sector

workers, the envisaged universal coverage is still a long way to go.

19

b. Composition of Risk Pools

In theory, the fundamental principle of universal coverage affirms that

contributions are not risk-‐‑based but are instead based on ability-‐‑to-‐‑pay. This

principle reflects a desire for equal access to healthcare and a certain degree of

equity in contribution setting. However, the principle implies a problem of the

so-‐‑called adverse selection, where high risks chase low risks out of the insurance

market. Adverse selection is a particular tendency when the health scheme

registration is voluntary and the same benefit package is offered to all those in

the pool (Carrin & James, 2004).

The phenomena of adverse selection can be explained as a moral hazard

in health service. A certain degree of prepayment combined with risk pooling

may result in some individuals being entitled to more health care than they have

paid for. This suggests that individuals may have an excess demand for health

care or aspire for "free" health care as they are confronted with a subsidized

price of health care. Some may argue that moral hazard would not happen in

health as one should expect people to prefer being healthy to demanding care.

However, the reality is that as one get sick, he or she may want to obtain as much

care as possible. Moreover, when there are no financial barriers to demand

health care at various levels of the health care system, people may want to

bypass the lower echelons and demand care from more specialized and

expensive facilities.

The reality of adverse selection and moral hazard in health care seem

occurred when the BPJS started registration and pay for claims from the general

hospitals in the country. Insofar, the MoH rules that while registration is

voluntary, a similar benefit package of health care is offered to those who have

registered. After nation-‐‑wide voluntary registration was started in January 2014,

many people who perceived themselves as having a serious illness rushed to

register in the BPJS offices. Some of the new members are in fact relatively

healthy, but some others had been indicated with acute diseases that needed

urgent medical treatments. Therefore, during the first months of

implementation, the BPJS has to pay a large amount of claims from the

catastrophic disease in many general hospitals.

20

Table 3. Costs of Catastrophic Medical Treatments in General Hospitals (%) Components General Hospital Class

A (N=6) General Hospital Class B

(N=2) Special Hospital

(N=3) CD C S CD C S CD C S

Accommodation 9.86 12.84 13.47 11.74 7.61 13.89 26.69 9.71 11.23 Ward treatment 15.7 9.87 14.79 26.17 9.75 25.15 28.36 8.38 32.12 Laboratory 19.1

9 11.17 23.01 14.94 6.63 11.87 10.85 11.25 12.35

Radiology 2.55 3.05 12.17 5.33 1.55 12.91 3.45 2.98 8.33 Surgery 2.44 21.74 5.29 1.46 12.53 2.61 0.00 32.77 0.00 Non-‐‑surgery 10.4

5 0.05 0.13 0.00 0.00 0.00 0.00 0.00 0.00

Medical rehab 3.12 0.09 1.27 0.00 0.00 0.00 0.00 0.00 2.21 Other treatment 4.74 3.47 2.12 4.69 1.04 5.34 8.78 14.83 2.23 Medicine 28.0

9 37.53 26.46 26.61 11.78 19.96 21.87 20.07 31.42

Medical consumables

3.86 0.18 1.30 9.06 49.12 8.27 0.00 0.00 0.00

Total 100 100 100 100 100 100 100 100 100 Average Costs (Million Rp)

410.0

236.24

228.68

396.13 136.48

305.97

38.22 86.71 62.13

Note: CD: Cardiac Disease C : Cancer S : Stroke Source: Budiarto, 2012; MoH, 2014.

Table 4. Comparison Between Actuarial Costs and Claims from INA-‐‑CBG (Rp) Hospital

Actuarial Costs Claims (INA-‐‑CBG) CD C S CD C S

General (Class A)

83,590,111 90,018,978 69,295,894 93,227,404 71,828,561 16,212,746

General (Class B)

4,079,878 6,867,048 3,271,237 6,936,283 4,495,967 2,977,179

Special 8,190,252 13,692,311 3,657,221 16,647,900 11,999,754 3,217,077 Average 45,568.486 72,554,004 36,255,390 52,127,993 57,818,963 8,240,261 Source: Budiarto, 2012; MoH, 2014.

Table 3 shows the proportion of costs for medical treatment for

catastrophic diseases (cardiac disease with open surgery, cancer, and stroke) in

selected general hospitals. It turns out that the major costs in all hospitals are for

medicine (11.78-‐‑31.42%) and inpatient accommodation (7.61-‐‑26.69%). The

pattern of costs for medicine, accommodation, and ward treatment has

similarities among the three hospital categories. However, surgeries and medical

rehabilitation are only carried out in higher class hospitals, either Class A or

Class B. For non-‐‑surgery treatment, higher class hospitals tend to charge more

21

while for other treatment there is no pattern, but the tendency is that special

hospitals would charge more. An exception for higher cost in Class B for stroke

inpatients is because these patients tend to stay longer in the hospital for ward

treatment, physiotherapy, and other health services.

The data evidently shows that higher class hospitals would charge more

(Table 4). The expense for cardiac inpatient treatment in Class A hospitals is

twenty times higher than that in Class B and ten times higher than that in Special

Hospital. For cancer inpatients, the expense for medical treatment in Class A

hospital is also much higher in comparison to that in Class B hospital and Special

Hospital. For stroke inpatients, between Class B hospitals and Special Hospital

the expense is about the same, but it would be twenty times higher if they go to

Class A hospitals.

Therefore, to ensure financial sustainability with pooled funding it is

important that the so-‐‑called "clinical pathways" or medical referential system

among different hospital classes have to be applied consistently. Within a pooled

funding of general insurance system, a patient with relatively less severe illness

who can be treated in the Puskesmas or Class C hospital should not be allowed to

go to Class A hospital for similar treatment because it would create an excess

demand for health care, which would incur unnecessary costs.

The comparison in Table 4 also suggests that, with an exception for

cancer treatment, the average amount of health care claims under the INA-‐‑CBG

index are higher than the actuarial. Overall, the nominal gap of between actuarial

costs and claims is Rp 2,925,540. This notion is important because most of those

who have registered to the BPJS believed that the nominal claims from INA-‐‑CBG

scheme are lower than what they should pay to the hospitals.

From a macro perspective, this confirms that there has been adverse

selection during the early stages of BPJS registration. Cardiac failures, cancer and

stroke are categorized as catastrophic diseases that imply high costs in the

hospitals. And if the costs cannot be recovered by the pooled fund and the

government subsidy that are being administered by the BPJS, the whole system

would financially fail. Therefore, there are strategic principles that has to be

considered by the decision makers: 1) the sustainability of finance and services,

2) people's ability-‐‑to-‐‑pay for insurance, 3) equity and fairness in health services,

22

and 4) fair competition among hospital managements. Many aspects have to be

taken account to attain expand insurance coverage, and the clinical pathway is

just one of them.

IV. DECENTRALIZED HEALTH SERVICES: THE JAMKESDA

a. Local Budget and Health Financing

It is envisaged in the Road-‐‑Map for National Health Insurance 2012-‐‑2019

that all the financial resources managed by different agencies should be

integrated into a single system under the BPJS. However, in the Indonesian

decentralized political context, it is a tough challenge for the Ministry of Health

to integrate health, let alone the newly established BPJS. The fundamental

fragmentation is between the ex-‐‑Jamkesmas schemes that are presently

managed by the BPJS and the Jamkesda schemes managed by provincial and

district governments. Of the total 34 provinces in the country, only Papua and

West Papua that do not have Jamkesda schemes. Jamkesda funds currently cover

an estimated 31.6 million people in almost all provinces and 352 districts/cities.

Law No.36/2009 national health policy stipulates that 10 percent of the

government budget must be allocated on health. However, most of the provincial

and local governments have not reach this percentage as the average is only 9.56

percent. At the provincial level, the lowest allocation is Riau at 6.57 percent and

the highest is Bali at 12.7 percent. As explained earlier, the Indonesian

government financial commitment on health is relatively weak in comparison to

other countries in the region.

After the political transition into a relatively more democratic

government in late 1990s, there was so much hope that decentralization would

bring the local government closer to the people's need. It was an illusive hope as

most decision makers at the sub-‐‑national government do not give appropriate

attention on health, education, social security, and all elements of public services

that have been badly needed by the local people. Many of the politicians have in

fact spend local budgets more on public official salaries, building monuments,

sport stadiums, and more grandiose projects for their own political populism.

23

As most of the sub-‐‑national governments allocate too little for financing

health programs, the per capita budget for health is also very low from the

international standard. Among the provinces, the national average of health

budget per capita is only Rp 286,665 (US$ 22.05) per person/year in 2014. One

should note that different levels of political commitment among the governors,

fiscal capacity and total population in the provinces are among the critical factors

influencing their budget priority on health. The provincial government of Riau is

among the highest in terms of fiscal capacity, yet they only allocate 6 percent of

the budget on health. On the contrary, Aceh provincial government is among the

lowest on fiscal capacity, but they allocate 10 percent of the budget on health.

While the BPJS encounter difficulties in integrating the local Jamkesda

into a universal scheme, there is also a large variety on how Jamkesda perform in

the provinces and districts. As described in Table 6, the percentage of Jamkesda

member to the total population is highly diverse from 1.89 percent (East Java) to

65.35 percent (South Sumatra). It is somewhat ironical that East Java province,

one of the most populated provinces with more than 37.4 million people, only

registered the least percentage of its people to Jamkesda scheme. It appears that

there is a legal vacuum on how the sub-‐‑national governments should formulate

policies on health. The central government has to acknowledge and support

decentralization policy as it is written in the constitution. However, there should

be some policy instruments to ensure that the sub-‐‑national governments really

undertake health care programs more seriously since it is fundamental for the

whole nation.

Table 6. Jamkesda Membership

No. Province Population Jamkesda Member

% Population

1 Aceh 4,842,238 2,226,352 45.98 2 North Sumatra 12,982,204 1,208,893 9.31 3 West Sumatra 4,846,909 1,141,149 23.54 4 Riau 5,538,367 1,341,395 24.22 5 Jambi 3,092,265 254,167 8.22 6 South Sumatra 7,450,394 4,868,723 65.35 7 Bengkulu 1,715,518 73,560 4.29 8 Lampung 7,608,405 4,513,155 59.32 9 Bangka Belitung 1,223,296 739,027 60.41 10 Riau Islands 1,679,163 174,730 10.41 11 Jakarta Capital

Region 9,607,787 4,300,000 44.76

24

12 West Java 43,053,732 5,082,200 11.80 13 Central Java 32,382,657 2,926,402 9.04 14 Jogja 3,457,491 1,007,153 29.13 15 East Java 37,476,757 706,982 1.89 16 Banten 10,632,166 479,170 4.51 17 Bali 3,890,757 2,440,964 62.74 18 West

Nusatenggara 4,500,212 572,976 12.73

19 East Nusatenggara 4,683,827 725,824 15.50 20 West Kalimantan 4,395,983 585,157 13.31 21 Central

Kalimantan 2,212,089 840,339 37.99

22 South Kalimantan 3,626,616 1,077,575 29.71 23 East Kalimantan 3,553,143 1,868,741 52.59 24 North Sulawesi 2,270,596 490,981 21.62 25 Central Sulawesi 2,635,009 483,968 18.37 26 South Sulawesi 8,034,776 4,892,070 60.89 27 South-‐‑East

Sulawesi 2,232,586 89,643 4.02

28 Gorontalo 1,040,164 495,869 47.67 29 West Sulawesi 1,158,651 48,447 4.18 30 Maluku 1,533,506 657,470 42.87 31 North Maluku 1,038,087 319,196 30.75 32 West Papua 760,422 n.a. n.a. 33 Papua 2,833,381 n.a. n.a. 34 North Kalimantan 723.005 n.a. n.a. National 237,989,154 46,632,278 19,59

Note : North Kalimantan is newly established province in 2012, data on Jamkesda is unavailable Source : MoH, 2014.

In order to assess the performance of Jamkesda, whether or not the

scheme would result in equitable health services that cover all of Indonesian

citizens, there are at least three aspects of health care management to be

evaluated, namely: membership or registration, financial management, and

benefit package distribution. Again, decision makers in Indonesia should learn

from experience of other countries that universal coverage cannot be

materialized within a short time. It needs strong political commitment,

perseverance, and appropriate adjustment during the implementation.

First, the membership to the JKN system depends on how the sub-‐‑

national governments accept the poor families or individuals who come to the

Jamkesda or BPJS regional offices. Some local government authorities admit and

include all the citizens who had not registered in any of the public insurance

system. The only difference is that those who come with enough money would

25

have to pay the premium and those who cannot afford to pay would be

registered under the PBI assistance. There are also other local governments that

essentially register all the citizens with the minimum benefit as a benchmark. It

means that all the citizens are entitled to at least a minimum benefit from the

local government. Those who cannot pay the premium, or presumably the poor

and near-‐‑poor, would be entitled to Level III health care services at the public

hospitals. And those who can afford to pay the premium may aspire for higher

level of health care services. Still, there are two provinces that use rather

procedural approach by registering poor individuals into the Jamkesda scheme

only if they bring the SKTM (Surat Keterangan Tidak Mampu, Poor Family

Identities), a letter of recommendation issued by the Dinas Sosial (Local Agency

for Social Affairs). All these government approaches are likely determine why in

certain provinces the level of membership to Jamkesda is very low while in other

provinces it is surprisingly high as shown in Table 6.

Second, the way provincial governments collect and manage health

insurance funds is critical in the national effort to attain universal coverage.

There are varieties of methods applied by the provincial governments in

determining their member contributions. In general, three methods are applied:

1) Free or no payment, 2) Contribution with the rate below the BPJS standard,

and 3) Contribution with the rate above the BPJS standard. Majority of the

Jamkesda (in 25 provinces) impose contribution with the rate below the BPJS

standard (Rp 19,255 basic premium), while three provinces impose contribution

with the rate above the BPJS standard, and four provinces do not impose any

payment. It means that, although many complained that the basic premium was

too low, the BPJS standard rate has in fact higher than those being applied in

regional Jamkesda.

It would be interesting to check whether the Jamkesda that do not impose

payment can really maintain a good quality for health services and those that

charge more are delivering better benefit packages for the consumers.

Maintaining appropriateness or a fair balance between the premium rate and

health service quality is important though majority of the Jamkesda has seen the

BPJS standard rate as a good reference. Given the diversity in health care

facilities across the provinces, the Ministry of Health should also encourage

26

governors and district heads to develop and maintain hospitals, clinics and other

health facilities and upgrade medical human resources accordingly.

In managing the pooled fund of Jamkesda, some of the provincial

governments are engaged in collaborative contracts with PT Askes (that is

transformed into regional BPJS) and the Dinas Kesehatan (Local Agency for

Health), which together form a Badan Pelaksana (Executing Body) of local health

insurance. There are also certain provincial governments that consider Jamkesda

as a part of the government agencies and its managerial decisions has to be

reported to the governor. The costs of delivering health services for the citizens

under its jurisdiction are to be shared between the provincial and the district

governments. There are 14 provinces in which the costs are fully financed by the

district government. In several provinces that are using traditional approach in

in health care financing, functions are simply separated into two: administrative

function and service function, in which the Jamkesda is to carry out

administrative function such as registration, determining the contribution, and

allocating government budget while hospitals (mostly treated as the BUMD, the

local government public enterprise) and clinics are to carry out health services,

determining tariff for services, and reporting capitation funds.

Third, the benefit package for medical treatment undertaken by the

Jamkesda is also the key indicator on how the government proceeds to universal

coverage. Out of the total 34 provinces in Indonesia, 18 provinces set the benefit

according to the JKN or previously Jamkesmas standard of services. This would

include preventive and curative personal health care, rehabilitative services and

ward accommodation. But in the other 16 provinces, the governments set the

benefit according to their local regulation (Peraturan Daerah). There are two

different reasons why these provinces do not follow the central government

regulation; First, the provincial authorities consider that they are able to provide

better health services than that being offered by the central government, and

therefore they wanted to regulate the benefit under local regulation. Relatively

rich provinces like Jakarta Special Region or East Kalimantan should have been

able to offer more comprehensive services for their citizens. A study in six

provinces, however, found that although provinces use local regulations, the

benefits are similar to those regulated by the central government (Supriyantoro,

27

2014). Second, some provincial authorities do not follow the central government

regulation on the benefit due to financial constraint. These are the provincial

governments that can offer only class-‐‑three services and many elements of the

services are scrapped.

b. The Premium Payment Assistance (PBI) For the first time, Law No.40/2004 on National Social Security System

rules that individuals living below the poverty line will get financial assistance

for their health care under the PBI (Penerima Bantuan Iuran, Premium Payment

Assistance), with the basic amount of Rp 19,225 (1.57 US$). After started the

nation-‐‑wide registration in 2014, the BPJS reported that 86.4 million PBI

recipients have been recorded. The BPJS also stated that the recorded numbers

are still increasing along with the Jamkesda integration into the JKN system.

However, after verifications were carried out in the regions, it also turned

out that many of the PBI registrations were incorrect and presumably the

benefits were miss-‐‑targeted. The Center of Health Finance and Insurance (P2JK)

of the MoH stated that 2,558,490 (2.96 percent) of the total 86.4 million PBI

records were incorrect. These are the number of those who cannot actually be

considered as the poor or near-‐‑poor. In South Sumatra, only 704 PBI recipients

were wrongly recorded and in North Sulawesi the number was only 1,271.

However, in Banten 290,438 (9.01%) PBI recipients of its 3,221,969 population

were wrongly recorded.

At this point, it seems that the notion on incorrect number was a result of

misperceptions between authorities in the MoH, the BPJS and the sub-‐‑national

governments. According to Law No.40/2004, the universal health coverage is

defined as a condition when all the Indonesian citizens are entitled to health

insurances by either paying premiums or being admitted to the public insurance

schemes under the government assistance of the PBI. Meanwhile, many of the

sub-‐‑national government authorities consider that universal health coverage is

to ensure that every citizen in their administrative jurisdictions must be entitled

to a minimum of class-‐‑three health care services. Regardless of their income, all

have the rights to get a medical treatment in class-‐‑three services. Due to this

different understanding about the universal coverage, many of the PBI

28

registrations may have double-‐‑counted or in fact under-‐‑represented in certain

regions.

Admittedly, the issue of data validity on poverty in Indonesia is something

that hindered the effectiveness of various programs in the country. Policies on

Bantuan Langsung Mandiri (BLT), a cash-‐‑transfer to help the poor after the

economic crisis in early 2000s, the labor-‐‑capital program for rural development

under PNPM Mandiri, have been among the miss-‐‑targeted programs due to data

accuracy. Regarding the data on the poor and near-‐‑poor referred by central

government and BPJS, there are possible inconsistencies with regional data

recorded by the Jamkesda. One should note that data on individuals who are

considered as the poor is not static. A poor family may succeed to climb up the

ladder to higher income status when one of its members can get a formal job,

which then help the entire family. On the contrary, a family with decent income

may be suddenly thrown back into poverty if one of its member severely sick and

has to pay out-‐‑of-‐‑the-‐‑pocket health services without additional income. Many of

this so-‐‑called "transient poor" is simply unrecorded by the central government

agency.

While integration is fundamental to pursue universal coverage and to

avoid inefficient funding for health services, there have been good intentions on

the part of sub-‐‑national governments. Many of the governors and district heads

do not want to see near-‐‑poor people are impoverished because they are not

registered in the BPJS system. Therefore, the policies are just to cover all to class-‐‑

three services, though sometimes it is politically labeled as "free health services".

The provincial government of Gorontalo, for example, affirmed that they want to

retain Jamkesda insurance because many of poor people in this province were

not covered by the Jamkesmas and were not registered as PBI recipients by the

central BPJS. Established as a province only in 2002 with a million population,

Gorontalo is governed by authorities who have a better commitment to improve

health services through Jamkesda. Policy coordination among the provincial and

district authorities has been relatively effective in monitoring the PBI assistance.

Gorontalo province is relatively successful not only in helping the poor with PBI

but also in improving local human resources for public health.

29

The Gorontalo approach is different from what has been taken in West

Sumatra. The governor of West Sumatra from the beginning of BPJS registration

has stated that Jamkesda should be integrated to JKN in order to ease the fiscal

burden on the provincial budget. For those who have enough income to buy the

premium, the provincial government urged them to join a program called Jamkes

Mandiri (self reliant health insurance). Therefore, the result is a combination of

locally managed health insurance system and the subsidized PBI system that is

managed under the national JKN.

A rather unsuccessful story is in East Nusatenggara province. The

provincial government has been committed to provide PBI assistance to all of its

poor citizens. They provided a special allocated dana talangan

(floating/reserved funds) from the provincial budget for whoever registered as

PBI members. Unfortunately, the beneficiary data was not accurately verified

while repayment of claims from the local hospitals was not adequately

controlled. For several months, the provincial government budget was

overburdened with health claims from the local hospitals to the extent that other

local development priorities are set aside. As the provincial government was

finally stop the repayment, many of the local hospitals were financially insolvent

to carry out their health services.

There have been various issues on how to allocate financial resources to

assist the poor via PBI scheme, which apparently centered on the integration

between central and sub-‐‑national governments, data accuracy and consistency,

and close monitoring during the implementation so as to ensure accountability

for further progress on health equity and quality. Another shortcoming of

financial health assistance for the poor is the fact that in nearly all regions the

focus of health program has been only on the curative aspect (Gani, 2010). In the

future, the PBI assistance would be more efficient when the authorities manage

to shift the focus onto the promotive and preventive aspects so that curative

treatments can be reduced while the coverage is expanded.

30

c. Jamkesda and Health Services in Jogja Province: A Case In order to understand the implementation of universal coverage policy at

the sub-‐‑national level, a case of the Jamkesda in Jogja Province is presented. The

province of Jogja is relatively small compared to the other provinces as it only

covers 3,185 kilometer square area with a population of 3,340,438 in 2012. It

consists of one city and four rural districts. There are 69 hospitals in the

province, of which 3 are Class A, 11 are Class B, and the rest are Class C, Class D

and non-‐‑classified local hospitals.

Sultan Hamengku Buwono X, the governor of Jogja province, says that the

provincial government prepares 121 Puskesmas, 141 main clinics and dental

service providers, 48 public and private hospitals, three clinical labs, and 11

pharmacies. It is expected that these health facilities would accommodate

2,062,488 individuals who already registered as Jamkesda members. Especially

for the PBI recipients, the provincial government has provided 138 beds of third-‐‑

class facilities, and 60 beds of second and first-‐‑class facilities. In addition, three

units of ambulatory service are also made available for PBI recipients.

According to Governor Regulation No.19/2011, Jamkesda membership is

categorized into three, namely: the PBI recipients whose basic premium are paid

by the provincial government, members or insurees under the COB

(Coordination of Benefits) whose premium are partially funded from cost-‐‑

sharing schemes made available by the provincial and district governments, and

the independent members who are mostly public servants and private company

employees.

Government authorities, BPJS regional officials, and Jamkesda officials are

trying hard to ensure that clinical pathways and medical referential systems are

well functioning in health services. Until November 2014, they had the

experience that many of the applicants to regional BPJS and the newly registered

members rushed to Class A hospitals to get health services, particularly to

Sardjito Hospital, the biggest general hospital in the city. Although Sardjito

Hospital has around 750 beds, it was really hard to reserve a ward

accommodation as everybody wanted to go to this hospital. Therefore, the

government is currently emphasizing the importance of collaborative networks

31

among the Puskesmas, midwives, nurses and paramedics who work in private

clinics and the medical doctors who work in public as well as private hospitals.

According to Dr. Elvy Effendi, the director of Jamkesda, it has been a tough

job to convince all the stake-‐‑holders about the importance of following clinical

pathways and medical referential systems. He has to tirelessly communicate

with medical professionals, officials, and Jamkesda members that the hospitals

can refuse to admit less severe patients who have no reference from the

Puskesmas and lower level hospitals. But moral hazard can take various modus

operandi. A patient may ask for class-‐‑three accommodation when he admitted to

a hospital. Then, while being treated in the ward he would ask to move to first-‐‑

class accommodation as he knew that it would only cost him an extra 40 percent

for accommodation while the medical treatment would follow first-‐‑class

standard.

Things have been more manageable currently as people begin to

understand that they can get standardized services in all Puskesmas, private

clinics, hospitals and pharmacies under Jamkesda jurisdiction. An official at the

Jamkesda claimed that about 70 percent of the medical reference system is

followed. But reducing moral hazard and adverse selection is a hard challenge

for Jamkesda as it closely linked to issue on finance.

Figure 4. Code Entry Accuracy in Panti Rapih Hospital (%)

Source: Nuryanti, 2014.

44.56

3.418.95

18.7624.3

57.12

9.39 9.55 10.3 13.64

0102030405060

Diagnosis

Treatment

32

The other pressing issue is the data accuracy on Jamkesda membership

and the mismatch of health service finance between the hospitals and the claims

to be paid by Jamkesda, both of which would create deteriorating effect on

sustainability. First, it is suspected that there have been double-‐‑counting in

Jamkesda membership. Mr. Effendi said that until end of 2014 there are

1,336,042 individuals registered in Jamkesda (including those insured under

former Jamkesos), leaving 889,198 individuals in the province uninsured.

However, he believes that because many have actually acquired double

insurance under the Jamkesos and Jamkesda, the government should have been

able to expand the coverage to those who are uninsured.

Second, as INA-‐‑CBG system is relatively new for many of the doctors and

computer operators in the hospitals, the overwhelming claims to the regional

BPJS may also due to inaccuracies. Figure 4 shows that in Panti Rapih hospital,

the biggest Class A private hospital in the province, only 44.56 percent of the

diagnosis input to INA-‐‑CBG complies according to correct specification. The fact

that 18.76 percent is mismatched and 24.3 percent is unrecognized confirms the

importance of human resource development in the implementation of INA-‐‑CBG

system in the region. The level of compliance of data entry for treatments is

higher at 57.12 percent but it is still below the WHO standard.

Most of the health services delivered in the region are dealing with

curative and rehabilitative treatments ranging from infectious and

communicable diseases such as influenza, pneumonia, bronchitis and typhus;

injuries from work and social activities; degenerative diseases such as diabetics,

hypertension, and dialysis; to catastrophic diseases such us cardiac failures,

stroke and cancer. The provincial government is urging Jamkesda and local

hospitals to move towards preventive and promotive health services. Preventive

services would deal with clinical pathology, Pap-‐‑smear test, mammography,

echocardiography, thalassemia, total protection for prenatal and antenatal and

children immunology. And promotive services would deal with nutrition

campaign for various groups including pregnants, under-‐‑five children, geriatrics,

and high-‐‑risk individuals. Yet it would take time for all the stake-‐‑holders and the

populace to acknowledge that a focus on preventive and promotive aspects

would eventually reduce financial burden for curative services.

33

The Jogja province authorities find it easier to convince the public

hospital managements compared to those of the private hospitals regarding the

importance of universal coverage. For public hospitals that get most of their

budgets from the government, a mandatory scheme for financing the poor and

informal sector workers would be readily accepted. However, for private

hospitals that have long been investing on assets (lands, buildings) and on staffs

without external help, the idea of servicing the poor has always been linked with

financial break-‐‑even and profit. As explained, this relates to the reason why INA-‐‑

CBG bridging system has been going slow in the private hospitals.

V. CONCLUSIONS

Based on the Indonesian's JKN road map, the government has identified

and followed some general paths for instituting universal health coverage.

Applying prospective payments, mandating a compulsory scheme, expanding

coverage on the poor, and instituting capitation with a case base mix have been

implemented. The government has also been trying to address the issue on

financial fragmentation by defining the collection and pooling the funds under

the BPJS management. Nevertheless, the bold move in Indonesian health

financing has to face with realities in the implementation that may not guarantee

the success toward universal coverage. There are many challenges ahead that

have to be met with strong commitment, perseverance and adequate knowledge

on the core problems of coverage and efficiency while dealing with the raising

demand for health services in the country.

Although the government policy on health has been reinvigorated with

the establishment of BPJS, one should note that the Indonesian financial

commitment remains very low at 3.0 percent or US$ 104.25 per capita

expenditure of GDP. This is a fundamental issue given the fact that the challenge

for insurance coverage is astonishingly high with the greatest proportion coming

from the informal sector workers. The policy makers should understand that

informal sector workers belong to precarious group who would be easily

impoverished from catastrophic illness if out-‐‑of-‐‑pocket health service is the only

available option for them.

34

As a country with large size of population and recently committed to

decentralization, integration and pooled funding as the prerequisites for

universal coverage are problematic. Not only that there is different

understanding between the national and sub-‐‑national authorities on the

meaning and the pathways to be taken for attaining universal coverage,

decentralization also tends to entail different political commitment, perpetuate

fragmentation, and disrupt efforts to vertically integrate the system. This adds

up to the problem of integration already faced at the regional level as evidenced

in the slow process of bridging the INA-‐‑CBG system.

Meanwhile, the immediate impacts of implementing universal coverage

commonly learned from international experience are also dealt by Indonesian

health officials. Adverse selection or moral hazards, double-‐‑counting on

beneficiaries, inconsistent medical database, financial leakages due to mismatch

between actuarial and claims, unclear clinical pathways, and lack of human

resources to administer prospective payments are among the problems that

need to be solved in the incoming years. While aiming for the national target on

coverage, many of health professionals in the country have to deal with technical

difficulties in adjusting to the new system.

Building a strong pooled-‐‑fund for universal health coverage requires