Title III, Regulation A+, and State Crowdfunding Regimes (Series: EQUITY CROWDFUNDING)

39

Title III, Regulation A+, & State Crowdfunding Regimes EQUITY CROWDFUNDING Premiere Date: January 19, 2017 This webinar is sponsored by: EisnerAmper 1

-

Upload

stephanie-strait -

Category

Education

-

view

144 -

download

0

Transcript of Title III, Regulation A+, and State Crowdfunding Regimes (Series: EQUITY CROWDFUNDING)

Title III, Regulation A+, & State Crowdfunding Regimes

EQUITY CROWDFUNDINGPremiere Date: January 19, 2017

This webinar is sponsored by: EisnerAmper

1

2

3

4

5

MODERATOR

Chris Cahill Financial Poise

PANELISTSAlex Davie Riggs DavieJordan Fishfeld CFX MarketsAndrew Stephenson CrowdcheckAmy Wan CrowdfundingLawyers.net

MEET THE FACULTY

6

SERIES SPONSOR

7

ABOUT THIS WEBINAR

"Crowdfunding" is an elastic term, covering general solicitation of accredited investors as well as equity investments in private companies available to all investors (Title III). Private companies within certain size limits may be able sell shares to all investors under Regulation A+. State crowdfunding laws may complicate the picture or afford more opportunities, or both. We look at the range of "crowdfunding."

8

ABOUT THIS SERIESThis webinar series explores the purchase of ownership shares in private companies via crowdfunding websites. "Crowdfunding" for this series refers both to investments made in this way by accredited investors -- given greater scope by Title II of the 2012 JOBS Act -- and those made by any investor under Title III of the JOBS Act. Episodes in the series address the modes of angel investing in a company during its early stages, the opportunities and perils of crowdfunding real estate investments, the money-raising entity's perspective, and a close look at crowdfunding options under federal and state law. Each episode is delivered in Plain English understandable to business owners and executives without much background in these areas. Yet, each episode is proven to be valuable to seasoned professionals. As with all Financial Poise Webinars, each episode in the series brings you into engaging, sometimes humorous, conversations designed to entertain as it teaches. And, as with all Financial Poise Webinars, each episode in the series is designed to be viewed independently of the other episodes, so that participants will enhance their knowledge of this area whether they attend one, some, or all of the episodes.

9

EPISODES IN THIS SERIES

Dates shown are premiere dates; all webinars will be available on demand after premiere date

EPISODE #1 Title III, Regulation A+, and 1/19/2017State Crowdfunding Regimes

EPISODE #2 Angel Investing Through Equity 2/23/2017Crowdfunding Websites

EPISODE #3 Investing in Real Estate through 4/6/2017Equity Crowdfunding Websites

EPISODE #4 Raising Money for a Start-Up Through 5/11/2017Equity Crowdfunding

10

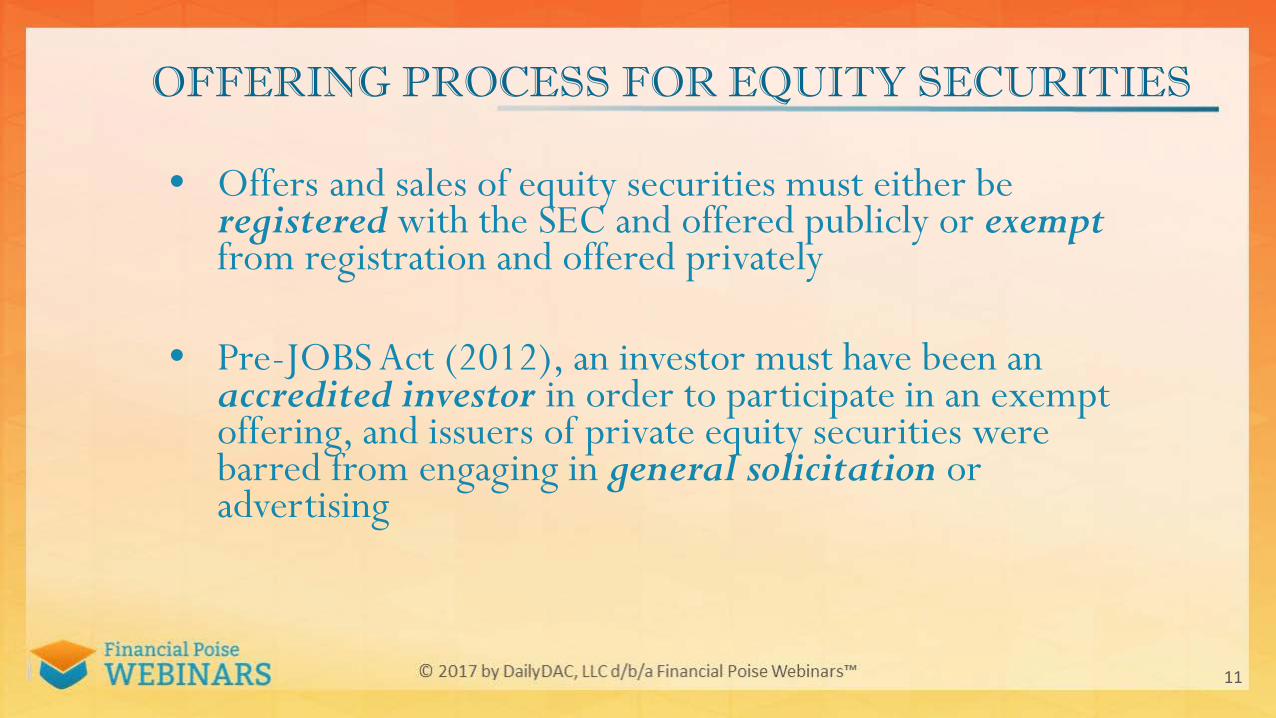

OFFERING PROCESS FOR EQUITY SECURITIES

• Offers and sales of equity securities must either be registered with the SEC and offered publicly or exempt from registration and offered privately

• Pre-JOBS Act (2012), an investor must have been an accredited investor in order to participate in an exempt offering, and issuers of private equity securities were barred from engaging in general solicitation or advertising

11

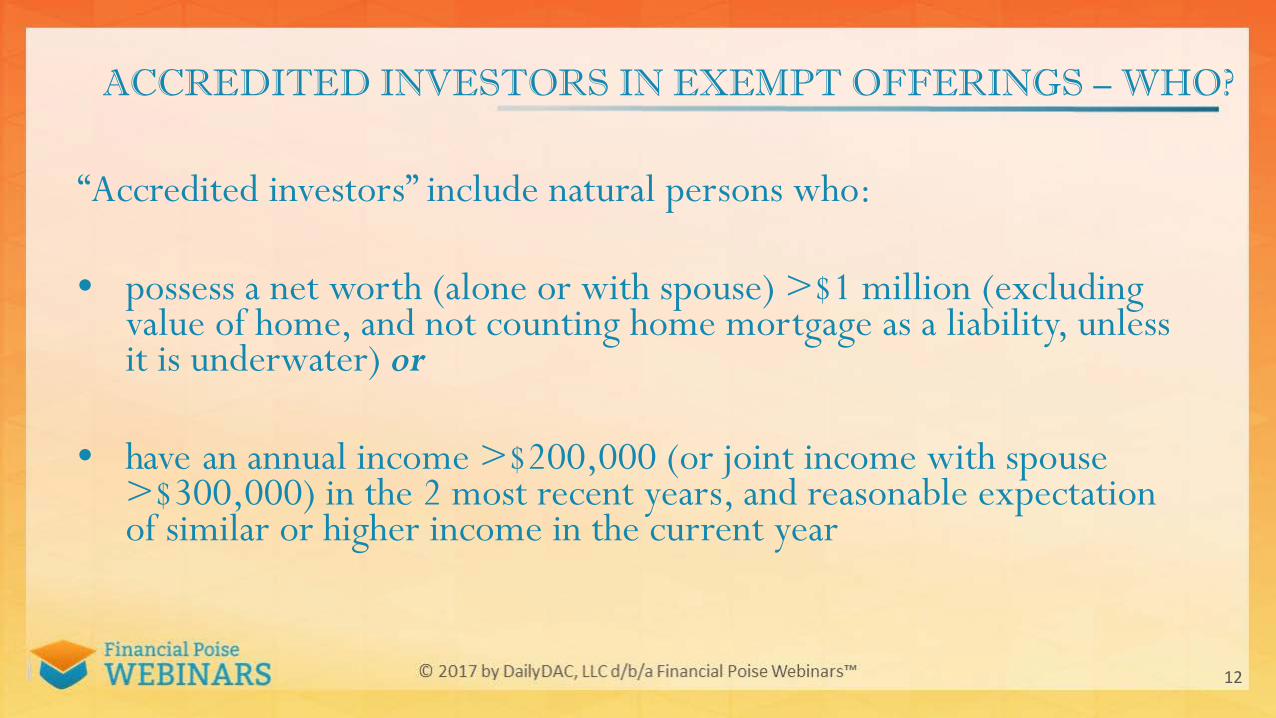

ACCREDITED INVESTORS IN EXEMPT OFFERINGS – WHO?

“Accredited investors” include natural persons who:

• possess a net worth (alone or with spouse) >$1 million (excluding value of home, and not counting home mortgage as a liability, unless it is underwater) or

• have an annual income >$200,000 (or joint income with spouse >$300,000) in the 2 most recent years, and reasonable expectation of similar or higher income in the current year

12

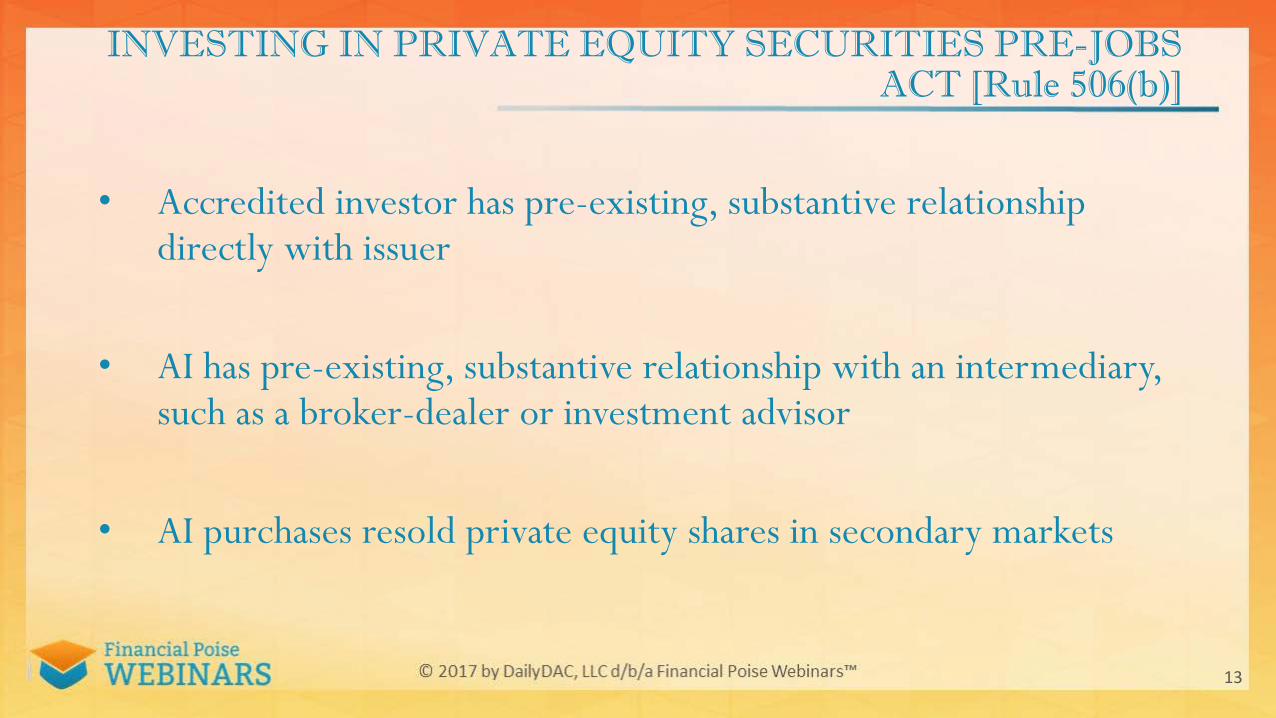

INVESTING IN PRIVATE EQUITY SECURITIES PRE-JOBS ACT [Rule 506(b)]

• Accredited investor has pre-existing, substantive relationship directly with issuer

• AI has pre-existing, substantive relationship with an intermediary, such as a broker-dealer or investment advisor

• AI purchases resold private equity shares in secondary markets

13

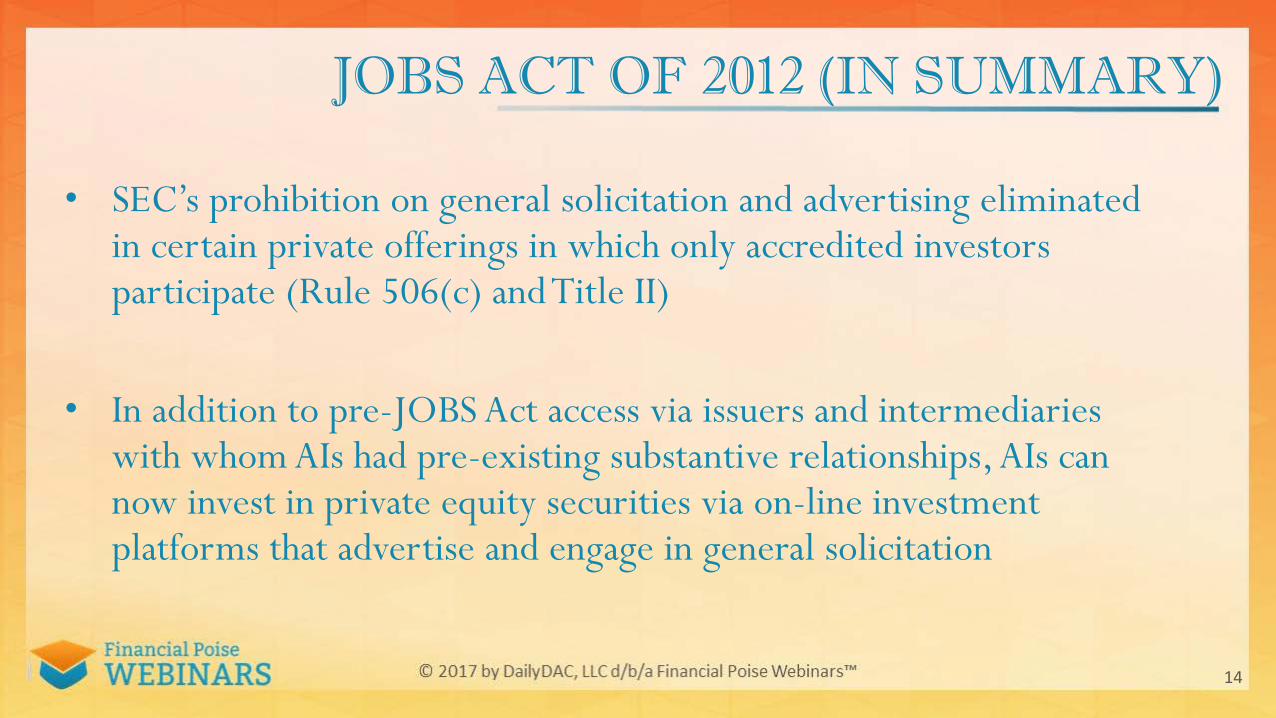

JOBS ACT OF 2012 (IN SUMMARY)

• SEC’s prohibition on general solicitation and advertising eliminated in certain private offerings in which only accredited investors participate (Rule 506(c) and Title II)

• In addition to pre-JOBS Act access via issuers and intermediaries with whom AIs had pre-existing substantive relationships, AIs can now invest in private equity securities via on-line investment platforms that advertise and engage in general solicitation

14

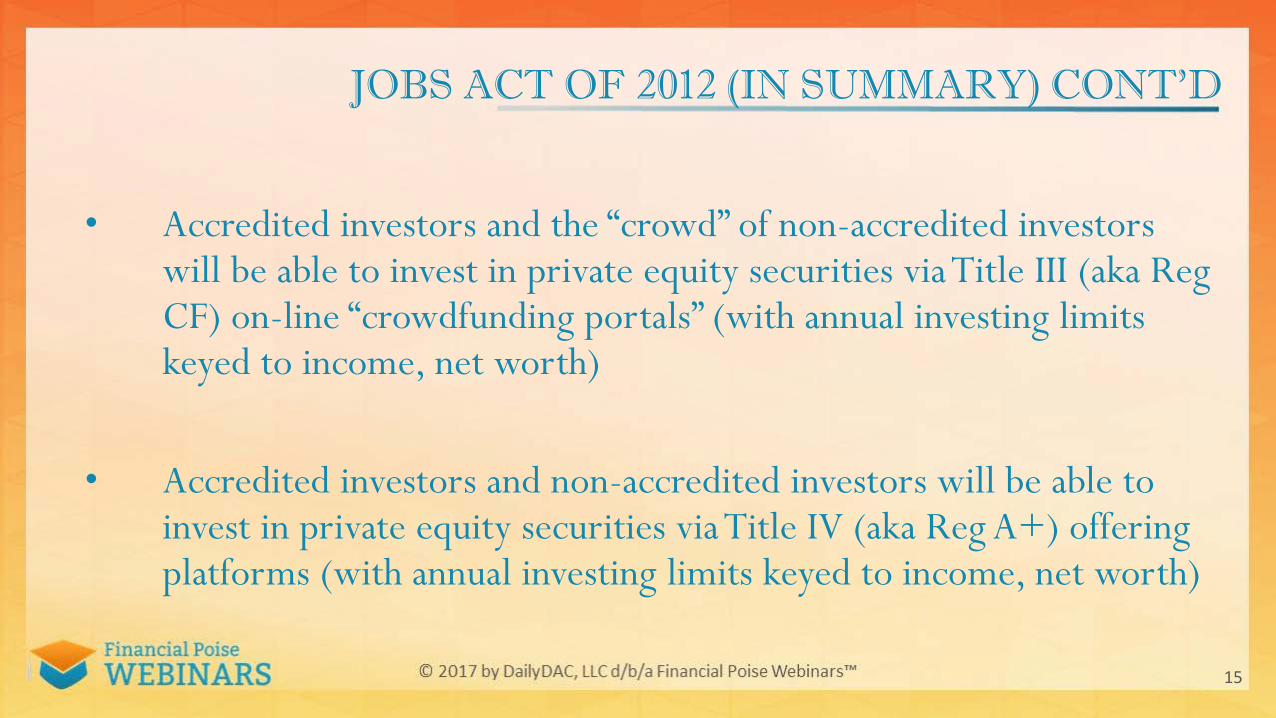

JOBS ACT OF 2012 (IN SUMMARY) CONT’D

• Accredited investors and the “crowd” of non-accredited investors will be able to invest in private equity securities via Title III (aka RegCF) on-line “crowdfunding portals” (with annual investing limits keyed to income, net worth)

• Accredited investors and non-accredited investors will be able to invest in private equity securities via Title IV (aka Reg A+) offering platforms (with annual investing limits keyed to income, net worth)

15

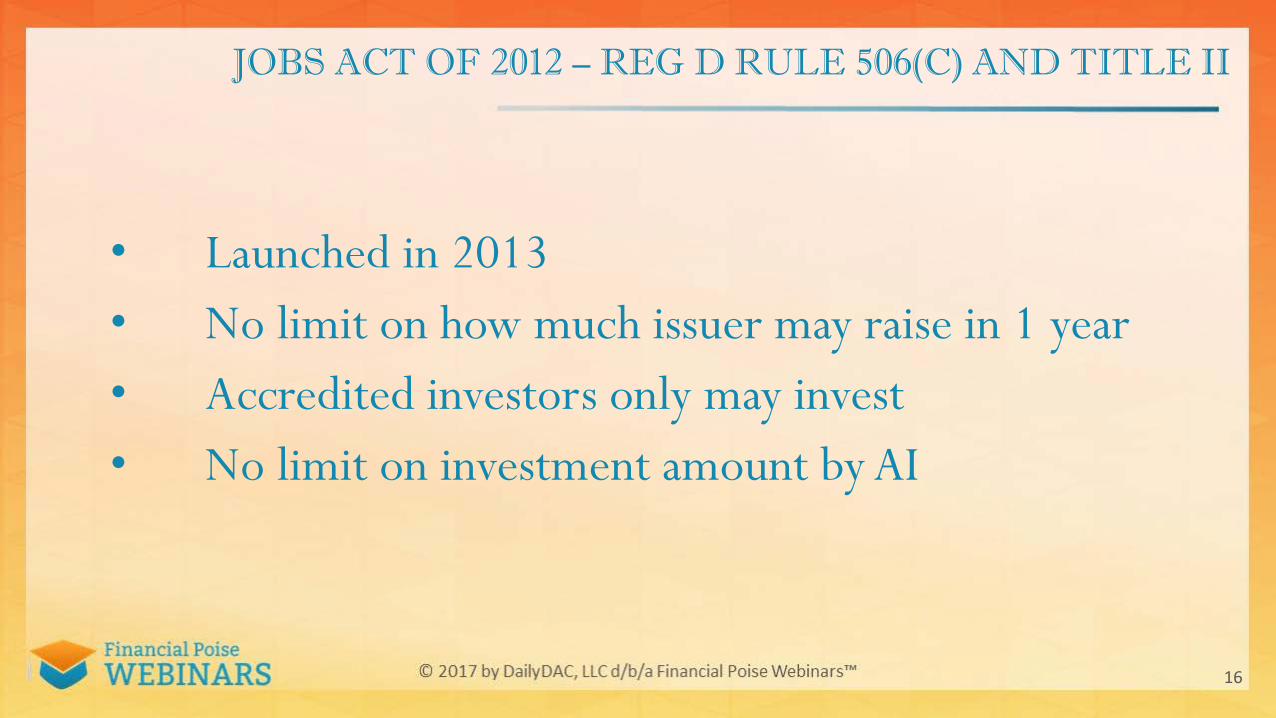

JOBS ACT OF 2012 – REG D RULE 506(C) AND TITLE II

• Launched in 2013• No limit on how much issuer may raise in 1 year• Accredited investors only may invest• No limit on investment amount by AI

16

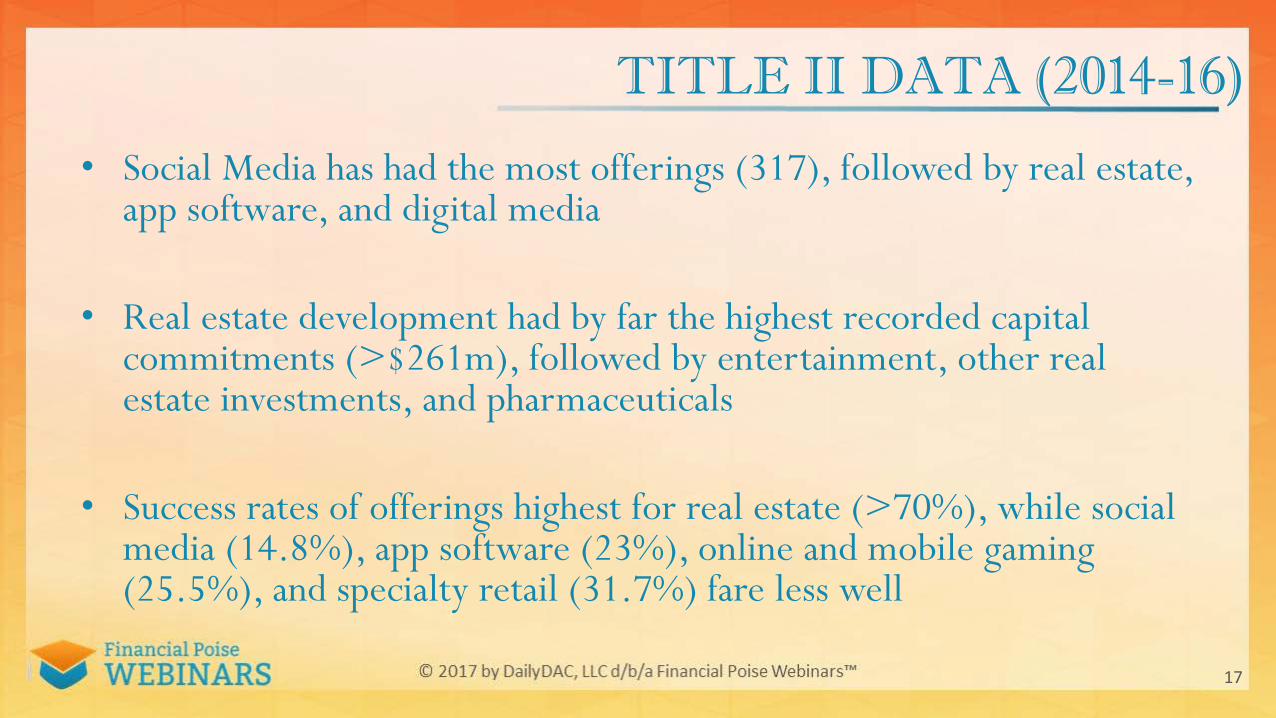

TITLE II DATA (2014-16)

• Social Media has had the most offerings (317), followed by real estate, app software, and digital media

• Real estate development had by far the highest recorded capital commitments (>$261m), followed by entertainment, other real estate investments, and pharmaceuticals

• Success rates of offerings highest for real estate (>70%), while social media (14.8%), app software (23%), online and mobile gaming (25.5%), and specialty retail (31.7%) fare less well

17

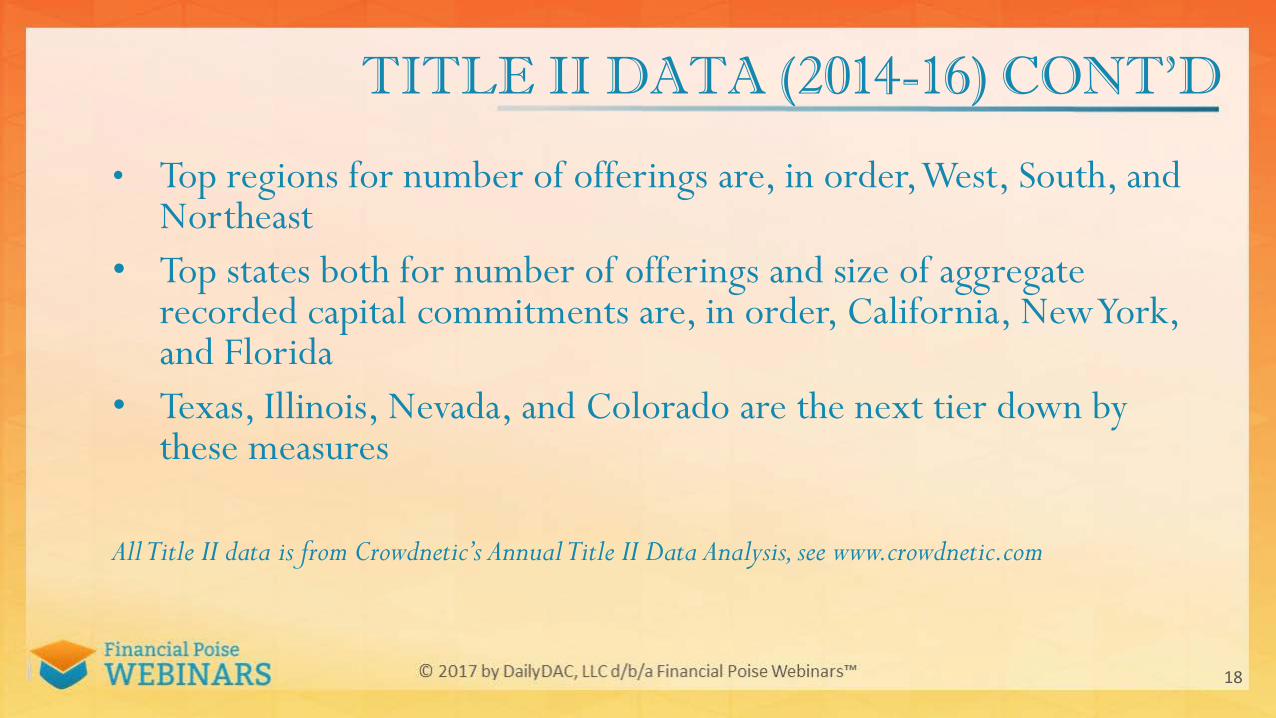

TITLE II DATA (2014-16) CONT’D

• Top regions for number of offerings are, in order, West, South, and Northeast

• Top states both for number of offerings and size of aggregate recorded capital commitments are, in order, California, New York, and Florida

• Texas, Illinois, Nevada, and Colorado are the next tier down by these measures

All Title II data is from Crowdnetic’s Annual Title II Data Analysis, see www.crowdnetic.com

18

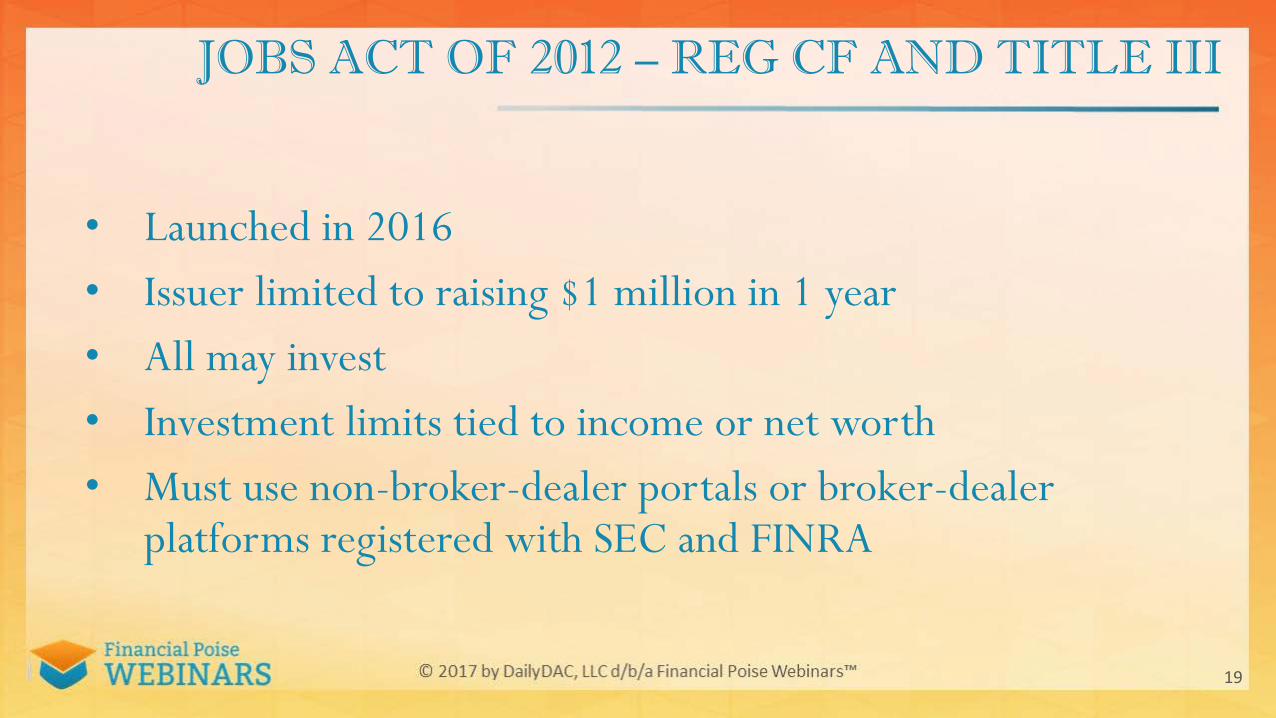

JOBS ACT OF 2012 – REG CF AND TITLE III

• Launched in 2016• Issuer limited to raising $1 million in 1 year• All may invest• Investment limits tied to income or net worth• Must use non-broker-dealer portals or broker-dealer

platforms registered with SEC and FINRA

19

TITLE III LIMITATIONS ON INVESTORS

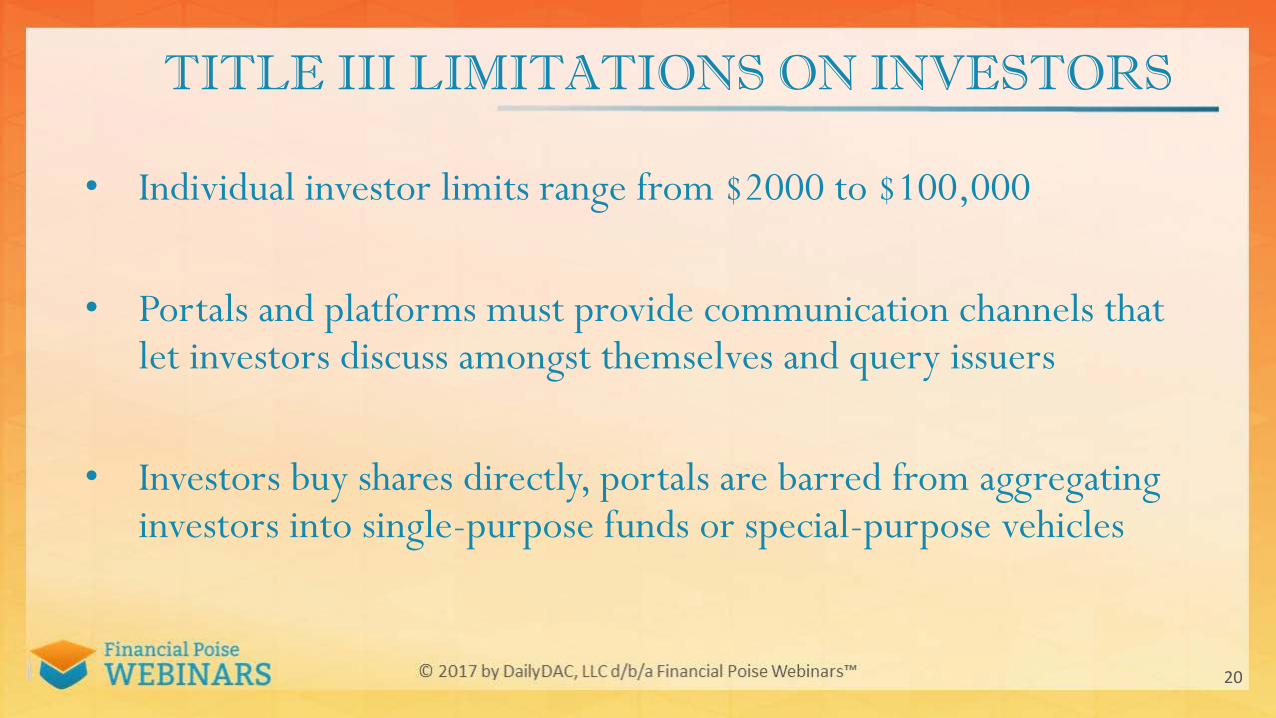

• Individual investor limits range from $2000 to $100,000

• Portals and platforms must provide communication channels that let investors discuss amongst themselves and query issuers

• Investors buy shares directly, portals are barred from aggregating investors into single-purpose funds or special-purpose vehicles

20

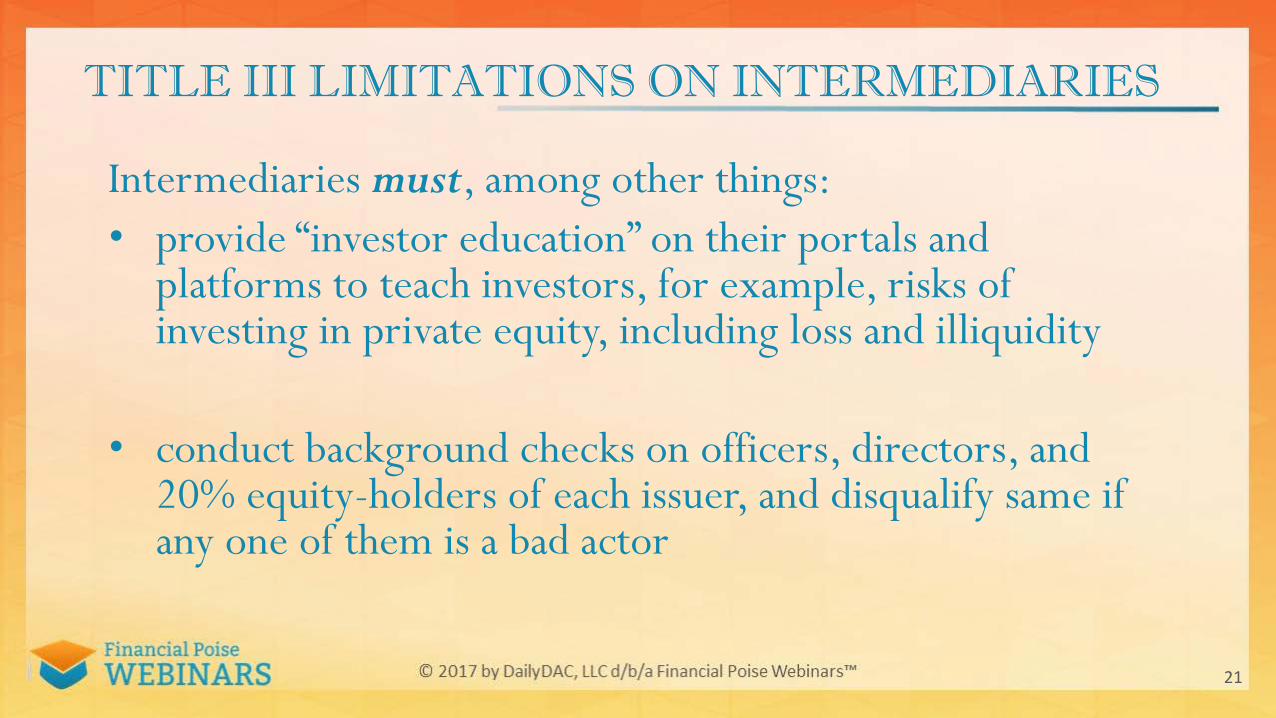

TITLE III LIMITATIONS ON INTERMEDIARIES

Intermediaries must, among other things:• provide “investor education” on their portals and

platforms to teach investors, for example, risks of investing in private equity, including loss and illiquidity

• conduct background checks on officers, directors, and 20% equity-holders of each issuer, and disqualify same if any one of them is a bad actor

21

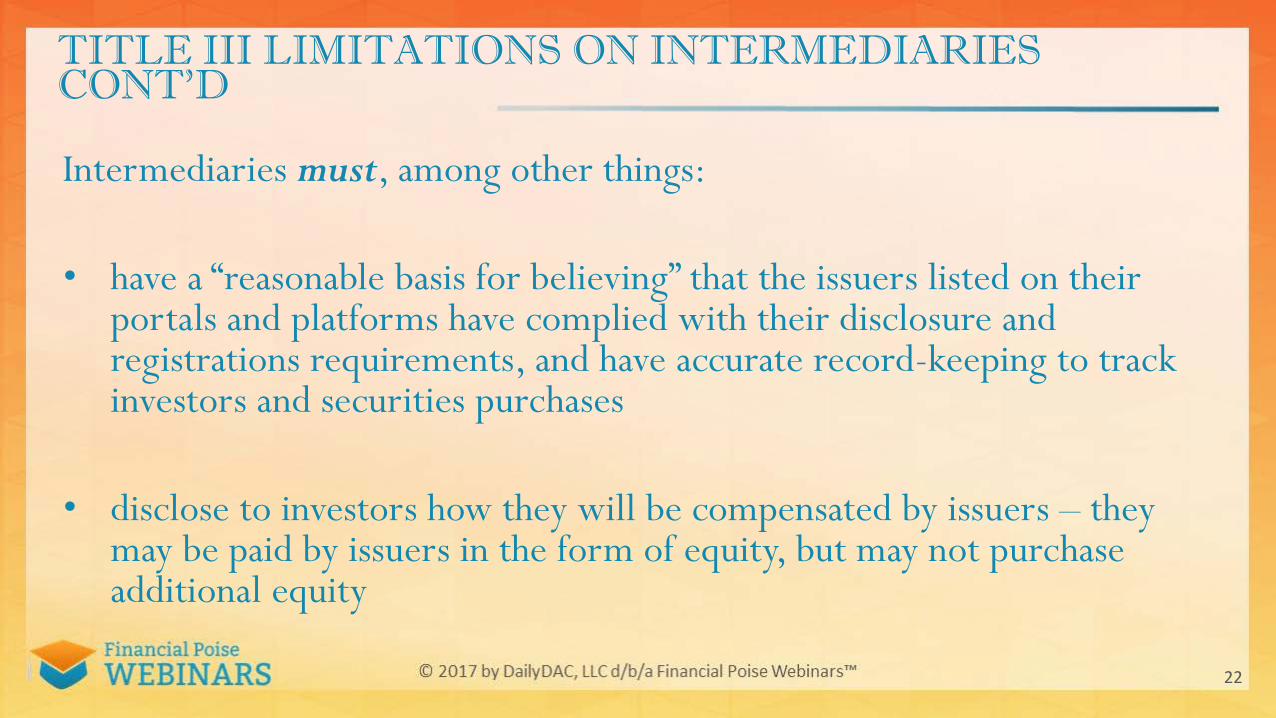

TITLE III LIMITATIONS ON INTERMEDIARIES CONT’D

Intermediaries must, among other things:

• have a “reasonable basis for believing” that the issuers listed on their portals and platforms have complied with their disclosure and registrations requirements, and have accurate record-keeping to track investors and securities purchases

• disclose to investors how they will be compensated by issuers – they may be paid by issuers in the form of equity, but may not purchase additional equity

22

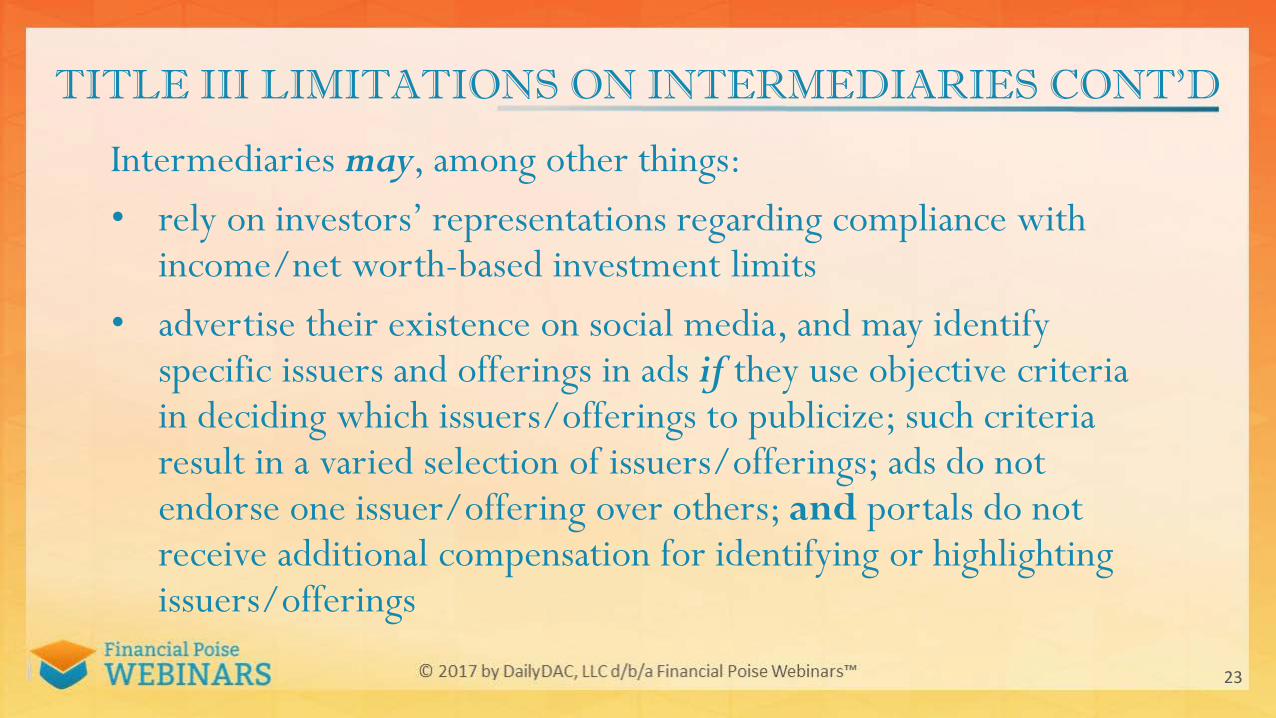

TITLE III LIMITATIONS ON INTERMEDIARIES CONT’D

Intermediaries may, among other things:• rely on investors’ representations regarding compliance with

income/net worth-based investment limits• advertise their existence on social media, and may identify

specific issuers and offerings in ads if they use objective criteria in deciding which issuers/offerings to publicize; such criteria result in a varied selection of issuers/offerings; ads do not endorse one issuer/offering over others; and portals do not receive additional compensation for identifying or highlighting issuers/offerings

23

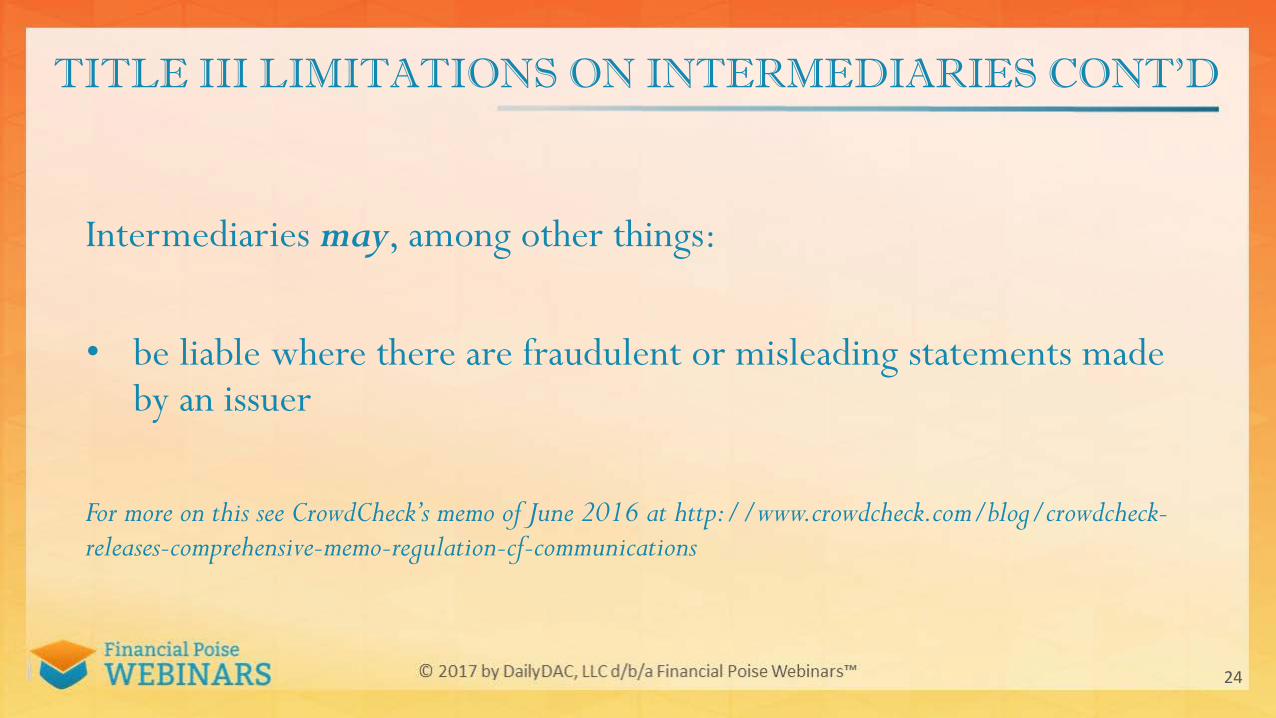

TITLE III LIMITATIONS ON INTERMEDIARIES CONT’D

Intermediaries may, among other things:

• be liable where there are fraudulent or misleading statements made by an issuer

For more on this see CrowdCheck’s memo of June 2016 at http://www.crowdcheck.com/blog/crowdcheck-releases-comprehensive-memo-regulation-cf-communications

24

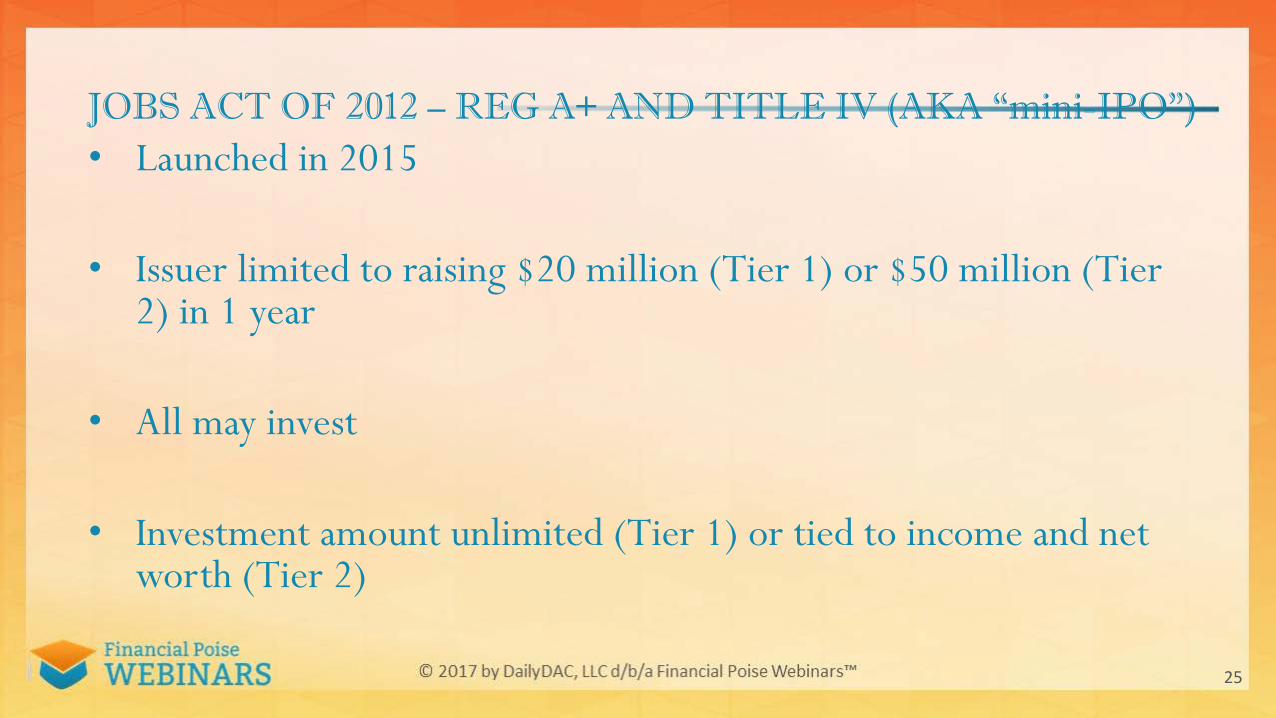

JOBS ACT OF 2012 – REG A+ AND TITLE IV (AKA “mini-IPO”)• Launched in 2015

• Issuer limited to raising $20 million (Tier 1) or $50 million (Tier 2) in 1 year

• All may invest

• Investment amount unlimited (Tier 1) or tied to income and net worth (Tier 2)

25

REG A+ AND TITLE IV

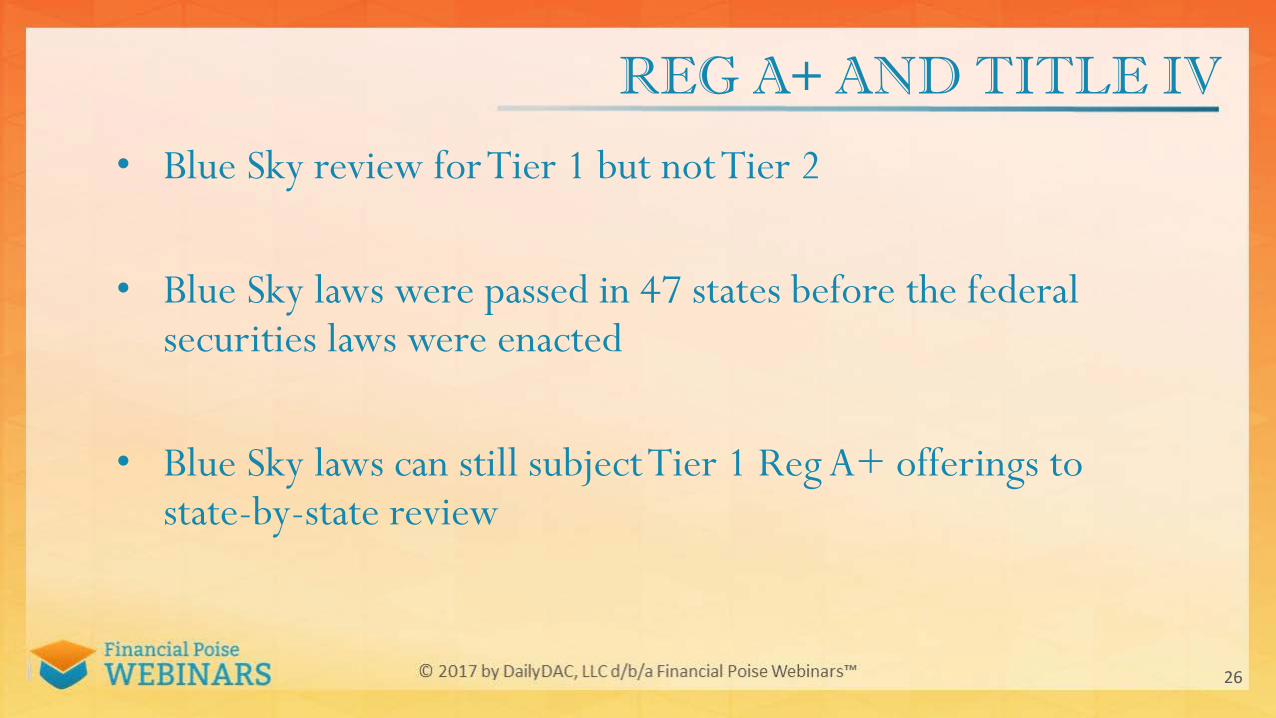

• Blue Sky review for Tier 1 but not Tier 2

• Blue Sky laws were passed in 47 states before the federal securities laws were enacted

• Blue Sky laws can still subject Tier 1 Reg A+ offerings to state-by-state review

26

HOW SUBSTANTIATE AI STATUS IN TITLE II OFFERINGS?

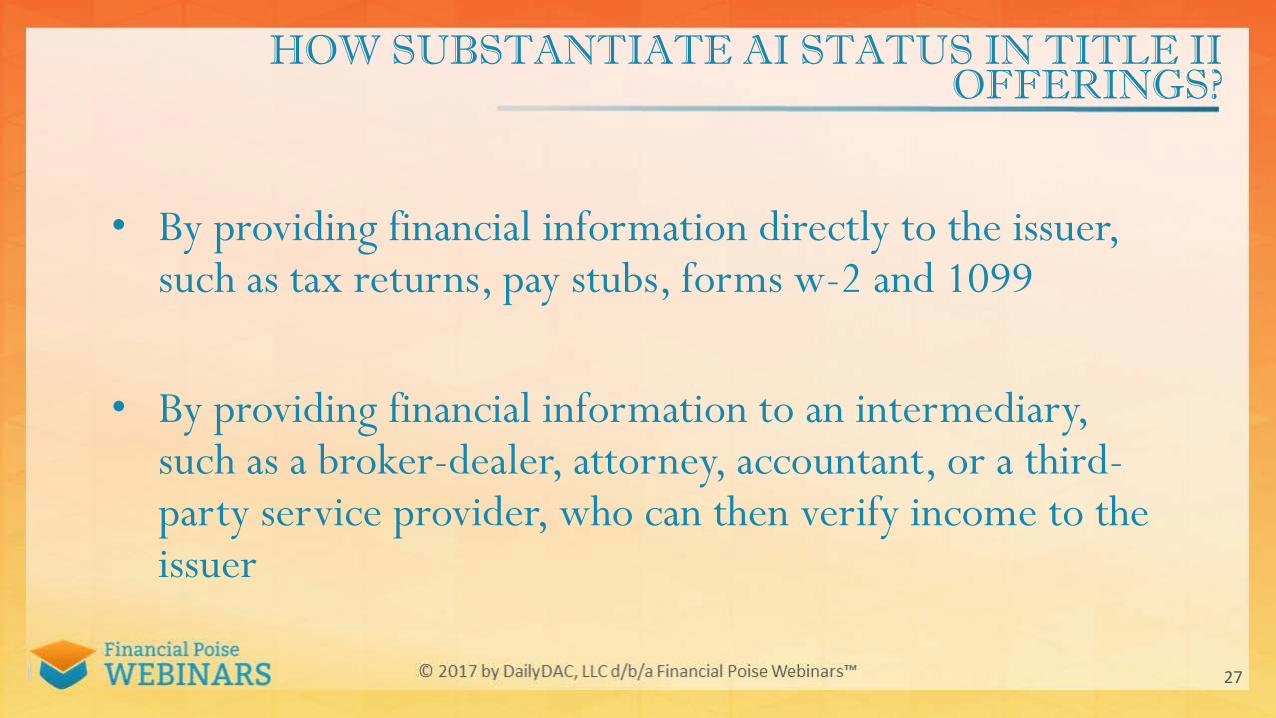

• By providing financial information directly to the issuer, such as tax returns, pay stubs, forms w-2 and 1099

• By providing financial information to an intermediary, such as a broker-dealer, attorney, accountant, or a third-party service provider, who can then verify income to the issuer

27

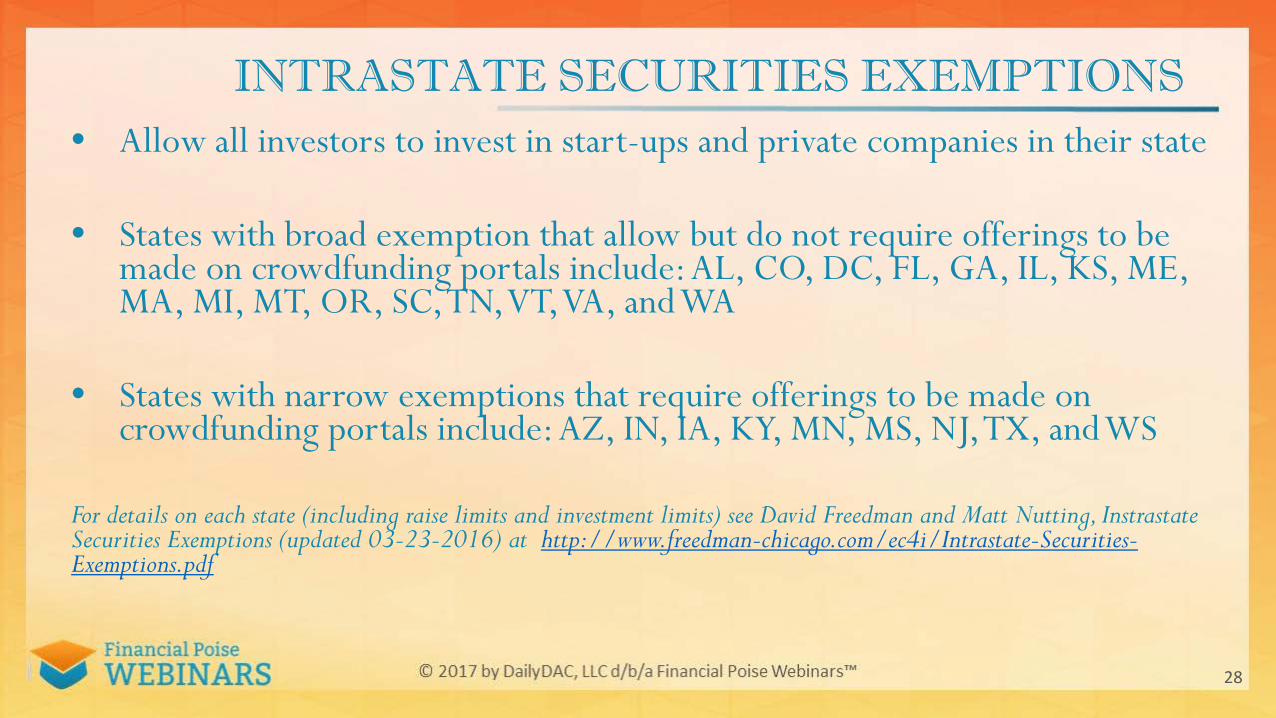

INTRASTATE SECURITIES EXEMPTIONS• Allow all investors to invest in start-ups and private companies in their state

• States with broad exemption that allow but do not require offerings to be made on crowdfunding portals include: AL, CO, DC, FL, GA, IL, KS, ME, MA, MI, MT, OR, SC, TN, VT, VA, and WA

• States with narrow exemptions that require offerings to be made on crowdfunding portals include: AZ, IN, IA, KY, MN, MS, NJ, TX, and WS

For details on each state (including raise limits and investment limits) see David Freedman and Matt Nutting, InstrastateSecurities Exemptions (updated 03-23-2016) at http://www.freedman-chicago.com/ec4i/Intrastate-Securities-Exemptions.pdf

28

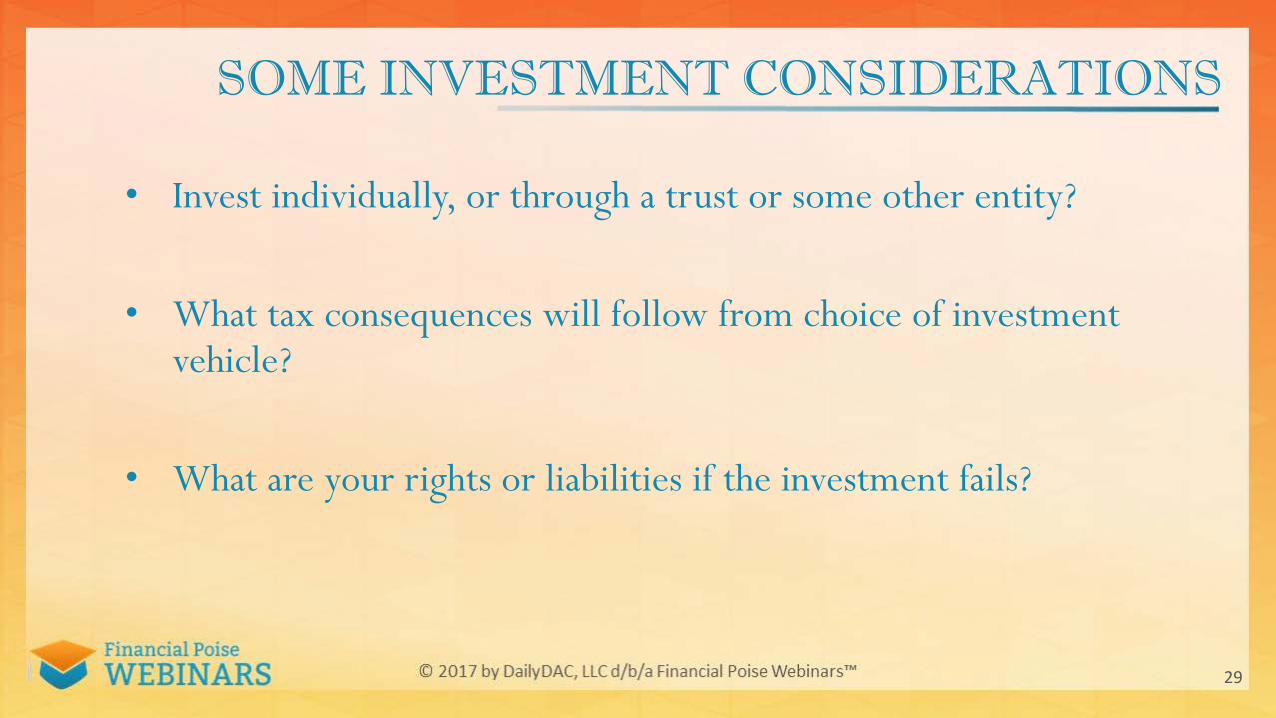

SOME INVESTMENT CONSIDERATIONS

• Invest individually, or through a trust or some other entity?

• What tax consequences will follow from choice of investment vehicle?

• What are your rights or liabilities if the investment fails?

29

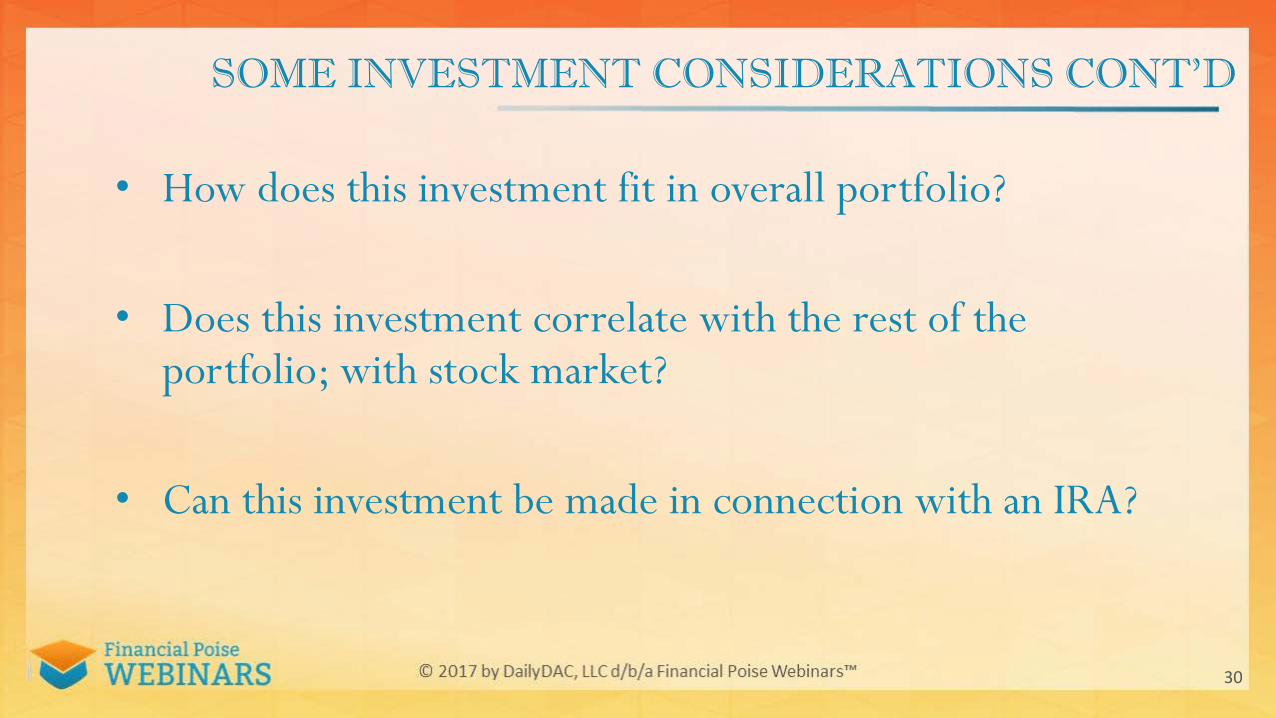

SOME INVESTMENT CONSIDERATIONS CONT’D

• How does this investment fit in overall portfolio?

• Does this investment correlate with the rest of the portfolio; with stock market?

• Can this investment be made in connection with an IRA?

30

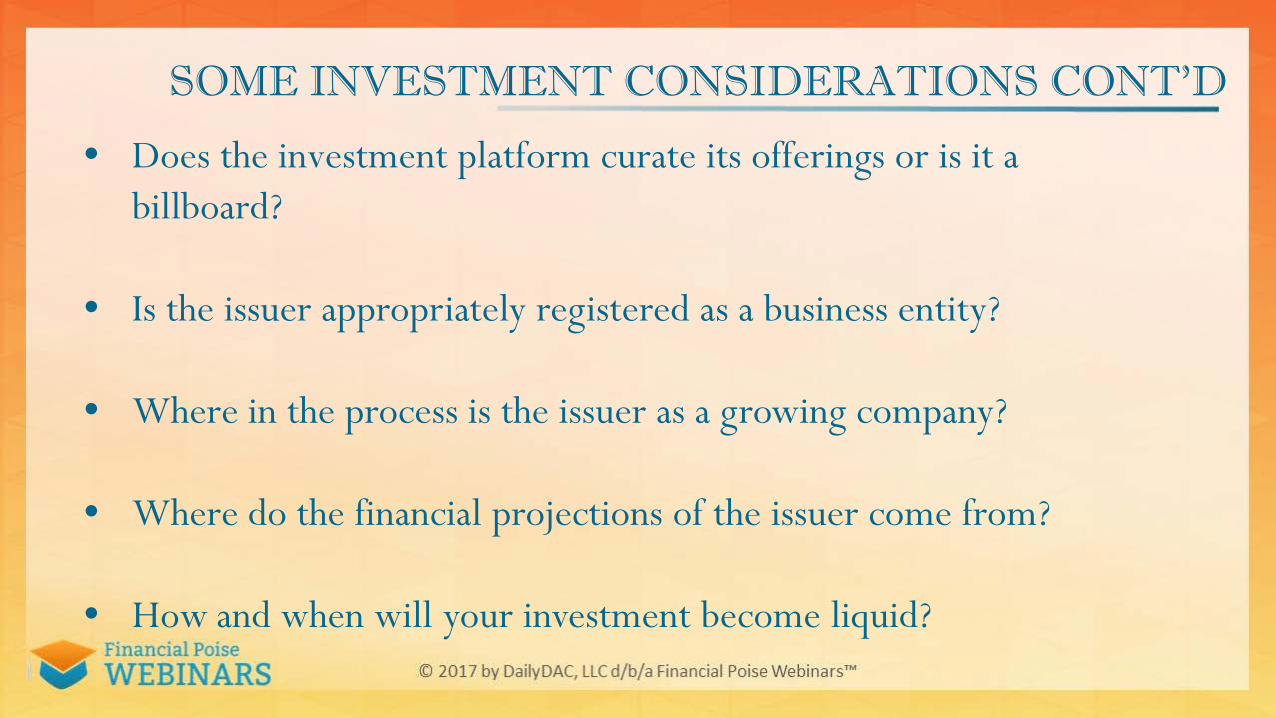

SOME INVESTMENT CONSIDERATIONS CONT’D

• Does the investment platform curate its offerings or is it a billboard?

• Is the issuer appropriately registered as a business entity?

• Where in the process is the issuer as a growing company?

• Where do the financial projections of the issuer come from?

• How and when will your investment become liquid?

ABOUT THE FACULTY

CHRIS [email protected]

Mr. Cahill is counsel with Lowis & Gellen LLP, in Chicago, Illinois. He guides secured lenders, creditors, debtors, creditors’ committees, potential purchasers and others through bankruptcy cases, out-of-court workouts, assignments for the benefit of creditors, and receiverships. Mr. Cahill has substantial mega-case experience at national law firms representing very large debtors, and has counseled and litigated on behalf of manufacturers and secured lenders in large and middle-market cases.

Mr. Cahill also publishes frequently and speaks regularly on commercial insolvency issues. He is an executive editor of Commercial Bankruptcy Litigation, 2d Edition (Jonathan P. Friedland, Elizabeth Vandesteeg & Christopher M. Cahill eds., 2015) and is the host of Accredited Investor Markets Radio, a weekly broadcast for investors, on accreditedinvestormarkets.com.

ABOUT THE FACULTYALEX DAVIE

Alexander J. Davie is a corporate and securities attorney in Nashville, Tennessee. Many businesses look to Alex as their outside “general counsel” for day-to-day legal needs as well as their trusted adviser on high-stakes transactions, such as capital raising, partnership buyouts and disputes, technology transactions, and mergers and acquisitions. His first goal is to provide clients with responsive service and candid and decisive legal advice for the difficult choices they often face. Alex frequently works with technology companies, including startups and emerging growth companies, and with private investment funds, such as private equity, venture capital, and hedge funds. Alex is active in Nashville’s startup community as a member of the board of directors of the Nashville Business Incubation Center and as a mentor at the Nashville Entrepreneur Center, and he participates in numerous other events geared towards making Nashville a nationally ranked location for starting a business.

ABOUT THE FACULTYJORDAN FISHFELD

Jordan Fishfeld is the co-founder and CEO of CFX Markets, a venture-backed trading platform that is changing the way people access alternative assets, in Chicago.

Jordan is the elected Treasurer of the Crowdfunding Professional Association (CfPA), and continues to advocate and educate on behalf of the crowdfunding industry. Jordan was also named one of Chicago’s Jewish Community 36 under 36.

Prior to that, Jordan worked as a finance attorney for Katten Muchin Rosenman, LLP, where he assisted on more than $1 billion worth of syndicated loan transactions. Jordan received his Bachelor of Arts in Political Science and his Bachelor of Science in Business Administration from the University of Florida and his Masters of Business Administration and his Juris Doctor from the University of Miami, where he graduated Magna Cum Laude.

ABOUT THE FACULTY

ANDREW [email protected]

Andrew D. Stephenson is the Vice President of Product Management and Strategy for CrowdCheck. Andrew has a wealth of experience assisting companies with understanding and taking advantage of the new landscape of online capital raising —including reward based crowdfunding, securities crowdfunding, offerings to accredited investors, and exempt public offerings of securities under Regulation A. With CrowdCheck, Andrew assists companies through the due diligence and disclosures required when listing their securities with registered broker-dealers and other online securities intermediaries. That effort includes helping companies identify and work through significant oversights and issues with their corporate governance and securities law compliance. Andrew leads a team of CrowdCheck due diligence analysts and regularly contributes to the national dialog surrounding innovation in capital formation

ABOUT THE FACULTY

Amy Wan is a Partner at CrowdfundingLawyers.net where she practices crowdfunding and securities law in California. Formerly, she was General Counsel at Patch of Land, a real estate crowdfunding platform, where she pioneered a novel iteration of the payment dependent instrument and advised the company on its Series A funding round. Amy also brings extensive experience in legal innovation and rethinking the delivery of legal services. She is the founder and co-organized of Legal Hackers LA, and was named one of ten women to watch in legal technology by the American Bar Association Journal in 2014, was named as a Finalist for the Corporate Counsel of the Year Award 2015 by LA Business Journal, and is a frequent speaker. She has also served as a Presidential Management Fellow at the U.S. Departments of Transportation, Commerce, and State. She is a graduate of the University of Southern California and the London School of Economics.

37

38

39

![[Crowdfunding] Equity Based CrowdFunding platform _Opentrade](https://static.fdocuments.in/doc/165x107/589a9d6e1a28abfc1a8b4c51/crowdfunding-equity-based-crowdfunding-platform-opentrade-59106092114ac.jpg)