thyssenkrupp Meet Management · Capital Market Day 2016 – Meet Management Components Technology...

89

Capital Market Day 2016 Meet Management

Transcript of thyssenkrupp Meet Management · Capital Market Day 2016 – Meet Management Components Technology...

Capital Market Day 2016 Meet Management

Capital Market Day 2016 – Meet Management

Components Technology

Essen, December 9th, 2016 Karsten Kroos (CEO) | Carsten Evers (CFO)

2 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

thyssenkrupp – a diversified industrial group Sales €39.6 bn; EBIT adj. €1.5 bn

Components Technology (CT)

Materials Services (MX)

Financial figures FY 15/16

Steel Americas (AM)

€1.5 bn €(33) mn

Steel Europe (SE)

€7.6 bn €315 mn

€11.9 bn €128 mn

Elevator Technology (ET)

€7.5 bn €860 mn

€6.8 bn €335 mn

Industrial Solutions (IS)

€5.7 bn €355 mn

3 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

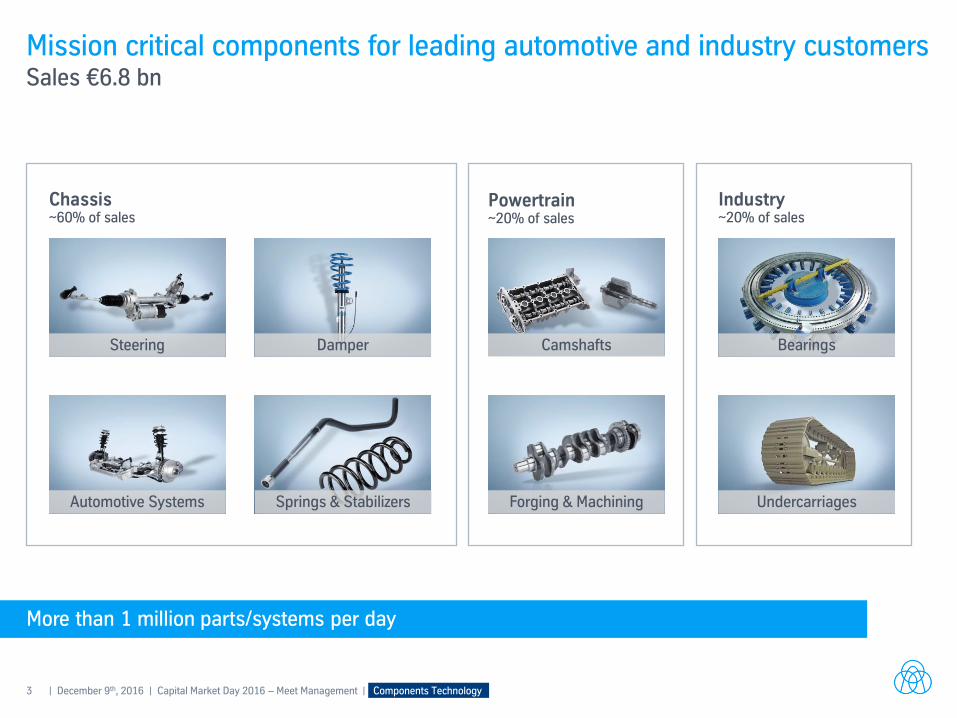

Mission critical components for leading automotive and industry customers Sales €6.8 bn

Powertrain ~20% of sales

Industry ~20% of sales

Chassis ~60% of sales

Springs & Stabilizers

Camshafts

Forging & Machining

Bearings

Undercarriages

Steering Damper

Automotive Systems

More than 1 million parts/systems per day

4 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

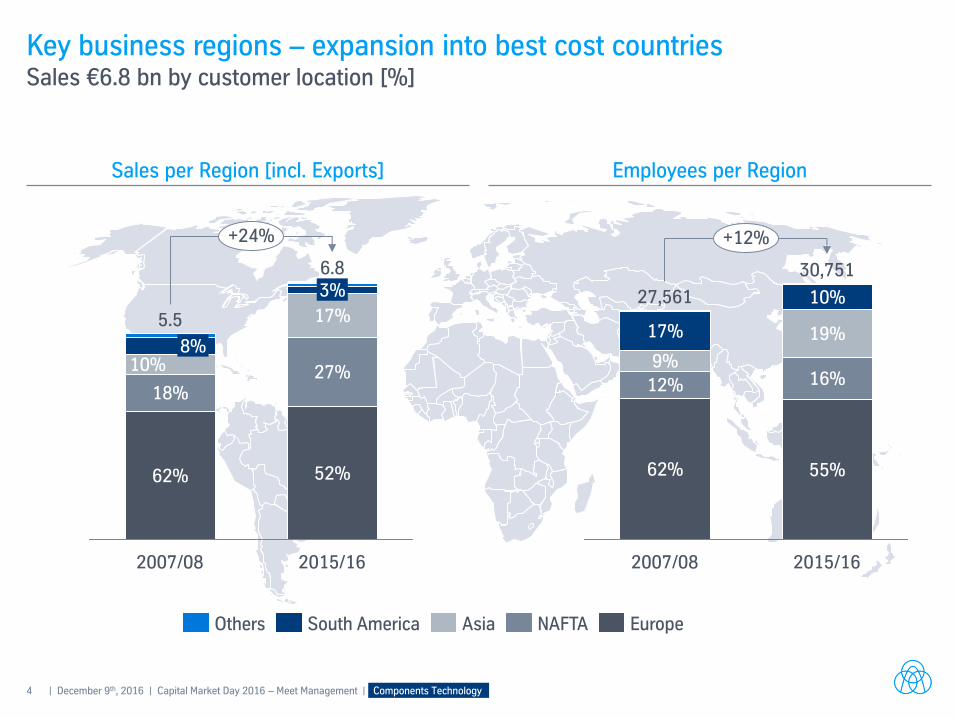

Key business regions – expansion into best cost countries Sales €6.8 bn by customer location [%]

Sales per Region [incl. Exports] Employees per Region

+24%

2015/16

6.8

52%

27%

17%

3%

2007/08

5.5

62%

18%

10% 8%

Europe NAFTA Asia South America Others

9%

17%

+12%

2015/16

30,751

55%

16%

19%

10%

2007/08

27,561

62%

12%

5 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

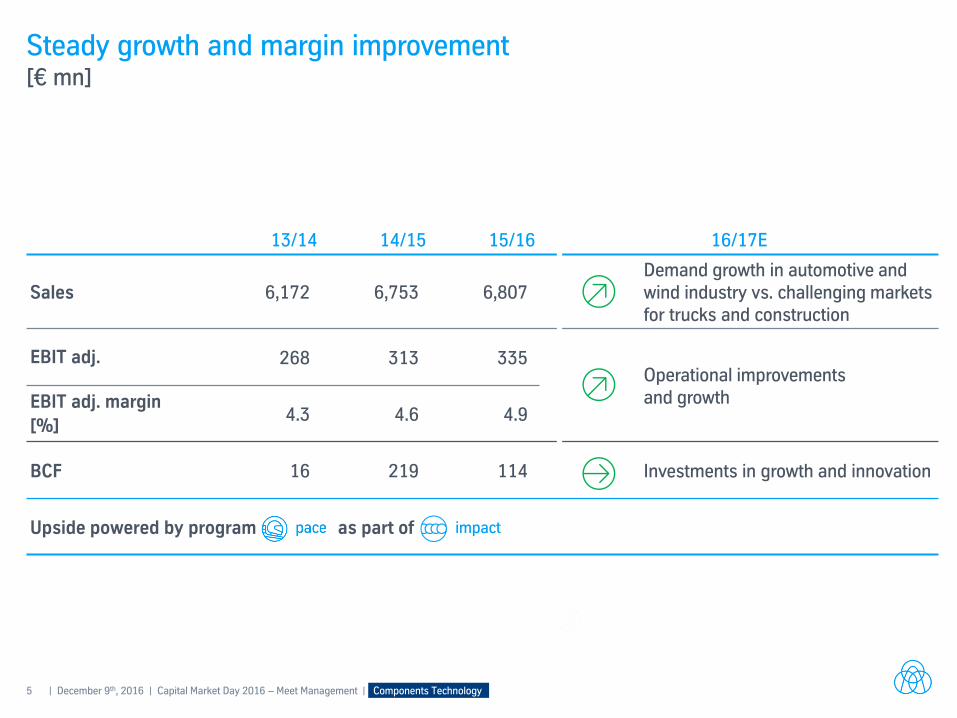

Steady growth and margin improvement [€ mn]

13/14 14/15 15/16 16/17E

Sales

6,172 6,753 6,807 Demand growth in automotive and wind industry vs. challenging markets for trucks and construction

EBIT adj. 268 313 335 Operational improvements and growth EBIT adj. margin

[%] 4.3 4.6 4.9

BCF 16 219 114 Investments in growth and innovation

Upside powered by program as part of

6 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

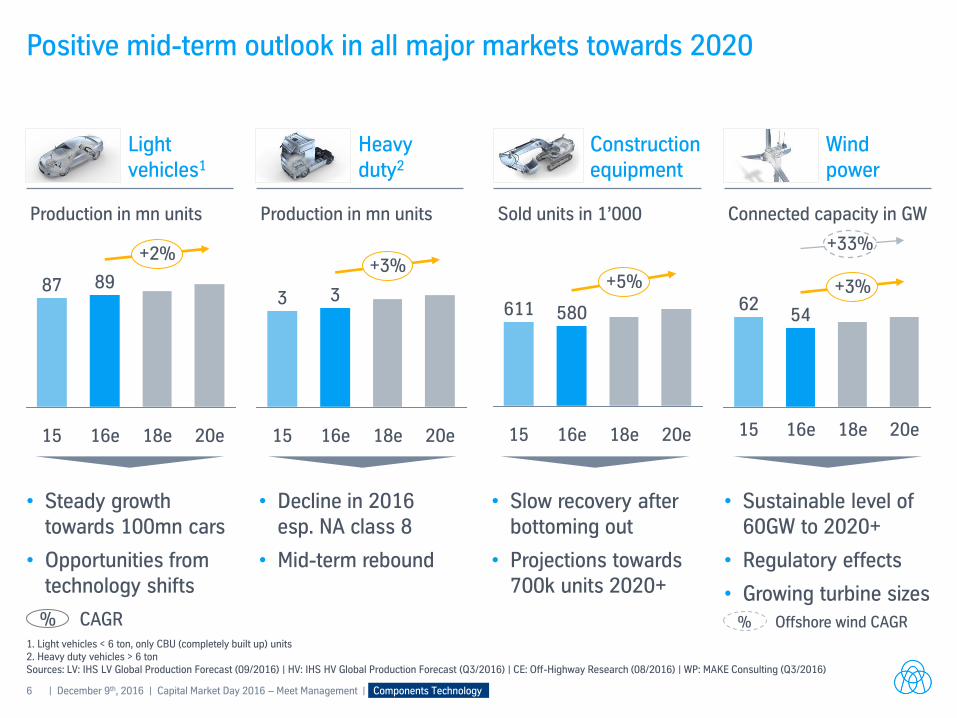

Positive mid-term outlook in all major markets towards 2020

1. Light vehicles < 6 ton, only CBU (completely built up) units 2. Heavy duty vehicles > 6 ton Sources: LV: IHS LV Global Production Forecast (09/2016) | HV: IHS HV Global Production Forecast (Q3/2016) | CE: Off-Highway Research (08/2016) | WP: MAKE Consulting (Q3/2016)

15 20e

+3%

3

18e 16e

3

16e

580

18e 20e

611

15

+5%

16e

+3%

54

15 18e 20e

62

% CAGR

Light vehicles1

Production in mn units

Heavy duty2

Production in mn units

Construction equipment

Sold units in 1’000

Wind power

Connected capacity in GW

• Steady growth towards 100mn cars

• Opportunities from technology shifts

• Decline in 2016 esp. NA class 8

• Mid-term rebound

• Slow recovery after bottoming out

• Projections towards 700k units 2020+

• Sustainable level of 60GW to 2020+

• Regulatory effects

• Growing turbine sizes

89

15

87

16e

+2%

20e 18e

+33%

% Offshore wind CAGR

7 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

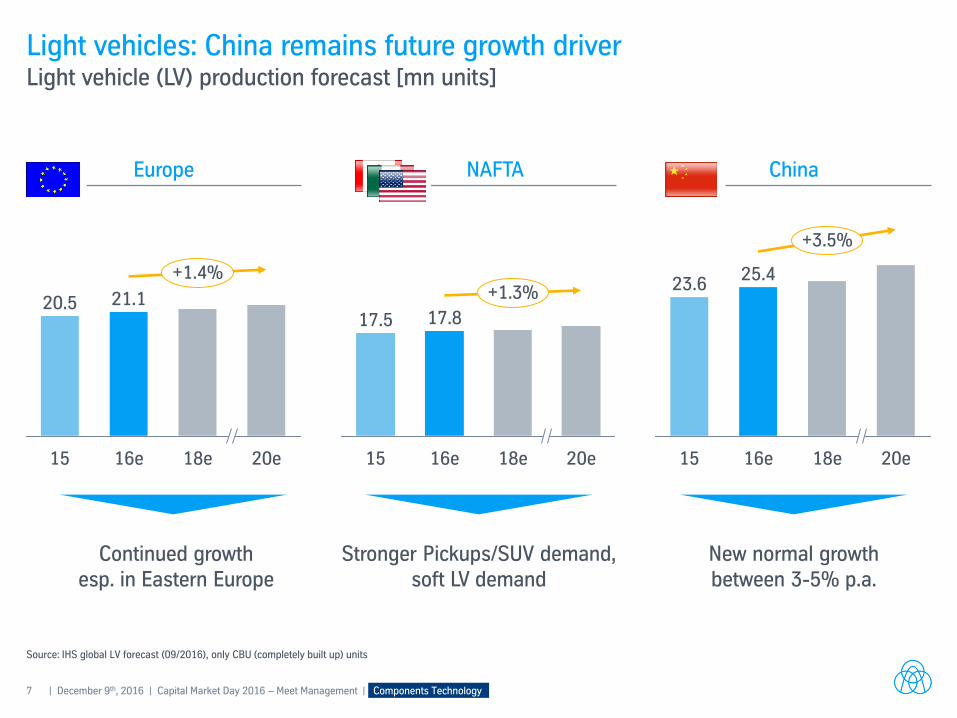

Light vehicles: China remains future growth driver Light vehicle (LV) production forecast [mn units]

China

Source: IHS global LV forecast (09/2016), only CBU (completely built up) units

Europe

Continued growth esp. in Eastern Europe

Stronger Pickups/SUV demand, soft LV demand

New normal growth between 3-5% p.a.

20.5

+1.4%

20e 18e 16e

21.1

15 18e 16e

17.8

15

17.5

20e

+1.3%

20e

+3.5%

18e 16e

25.4

15

23.6

NAFTA

8 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

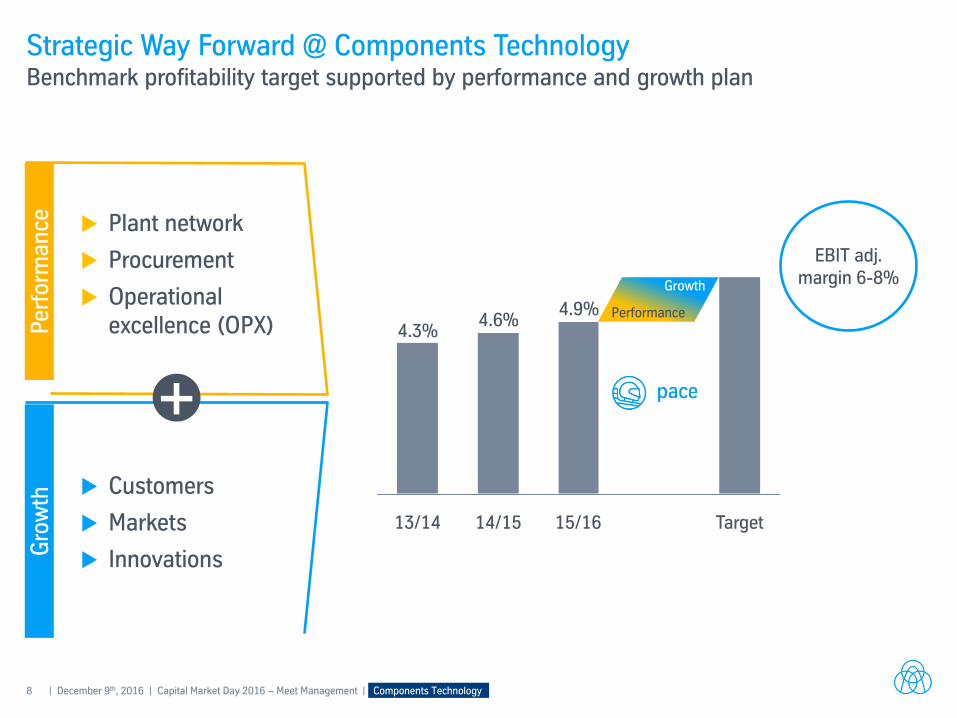

Customers

Markets

Innovations

Plant network

Procurement

Operational excellence (OPX)

Strategic Way Forward @ Components Technology Benchmark profitability target supported by performance and growth plan

Target 15/16

4.9%

14/15

4.6% 4.3%

13/14

Per

form

an

ce

Gro

wth

+

Growth

Performance

EBIT adj. margin 6-8%

9 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

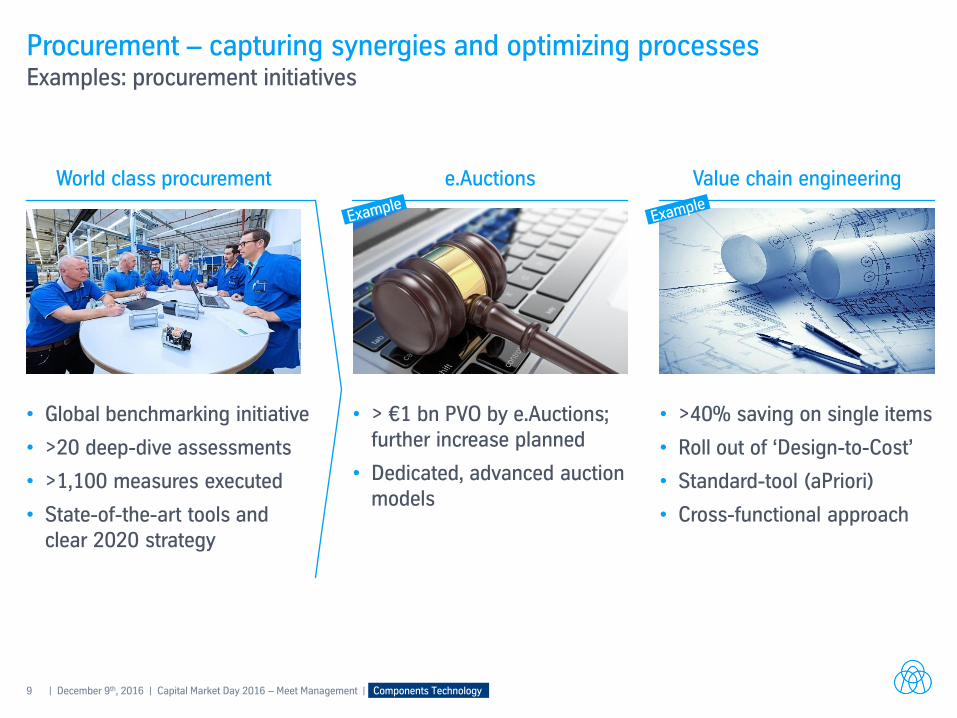

Procurement – capturing synergies and optimizing processes Examples: procurement initiatives

World class procurement

• Global benchmarking initiative

• >20 deep-dive assessments

• >1,100 measures executed

• State-of-the-art tools and clear 2020 strategy

Value chain engineering

• >40% saving on single items

• Roll out of ‘Design-to-Cost’

• Standard-tool (aPriori)

• Cross-functional approach

e.Auctions

• > €1 bn PVO by e.Auctions; further increase planned

• Dedicated, advanced auction models

10 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

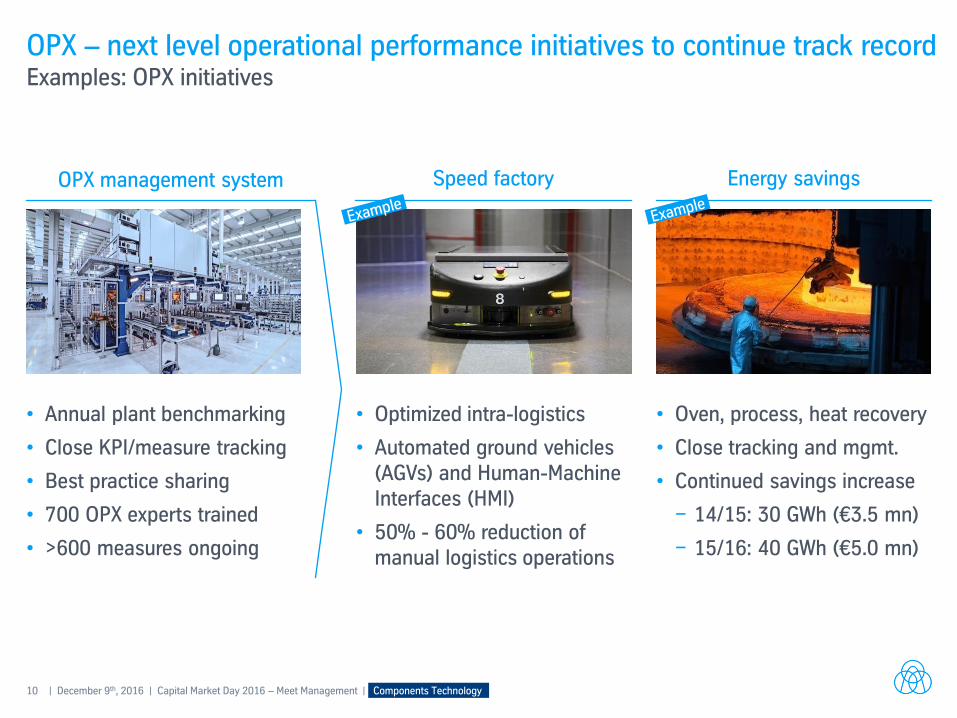

OPX – next level operational performance initiatives to continue track record Examples: OPX initiatives

Energy savings

• Oven, process, heat recovery

• Close tracking and mgmt.

• Continued savings increase

− 14/15: 30 GWh (€3.5 mn)

− 15/16: 40 GWh (€5.0 mn)

OPX management system Speed factory

• Optimized intra-logistics

• Automated ground vehicles (AGVs) and Human-Machine Interfaces (HMI)

• 50% - 60% reduction of manual logistics operations

• Annual plant benchmarking

• Close KPI/measure tracking

• Best practice sharing

• 700 OPX experts trained

• >600 measures ongoing

11 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

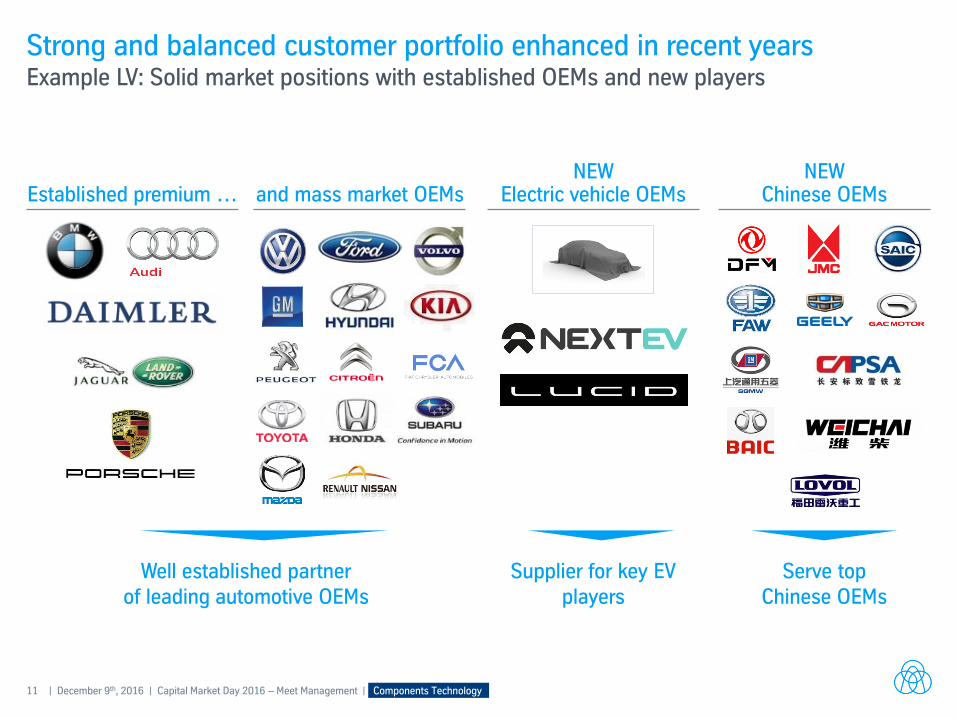

Strong and balanced customer portfolio enhanced in recent years Example LV: Solid market positions with established OEMs and new players

Established premium …

Well established partner of leading automotive OEMs

NEW Electric vehicle OEMs

Supplier for key EV players

NEW Chinese OEMs

Serve top Chinese OEMs

and mass market OEMs

12 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

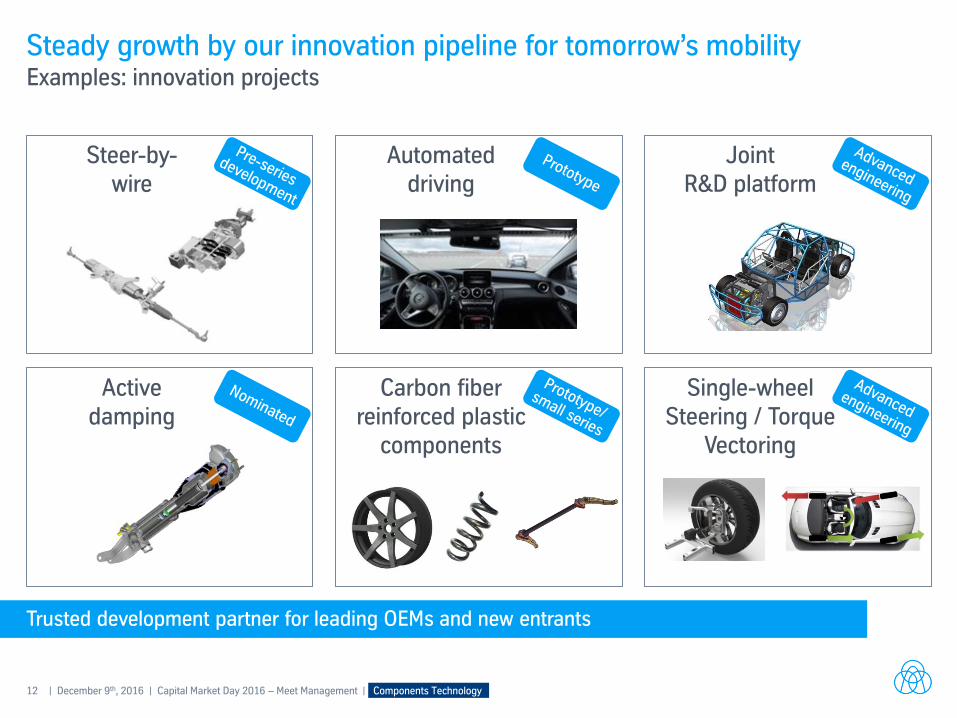

Steady growth by our innovation pipeline for tomorrow’s mobility Examples: innovation projects

Trusted development partner for leading OEMs and new entrants

Automated driving

Active damping

Carbon fiber reinforced plastic

components

Single-wheel Steering / Torque

Vectoring

Joint R&D platform

Steer-by- wire

13 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

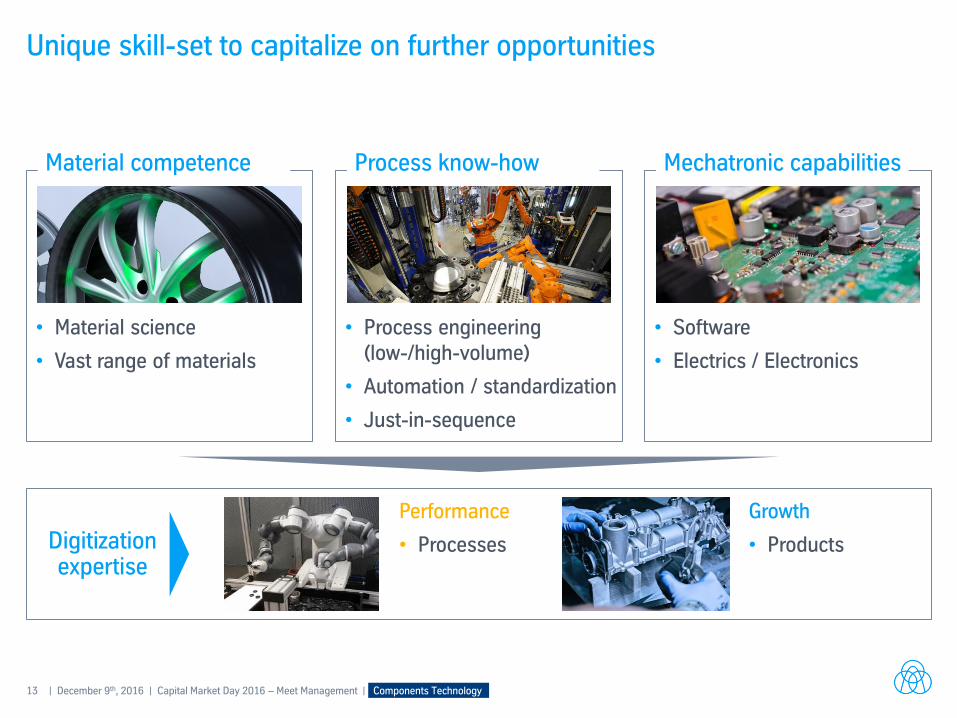

Unique skill-set to capitalize on further opportunities

Material competence Process know-how Mechatronic capabilities

Digitization expertise

• Material science

• Vast range of materials

• Process engineering (low-/high-volume)

• Automation / standardization

• Just-in-sequence

• Software

• Electrics / Electronics

Performance

• Processes

Growth

• Products

14 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Components Technology

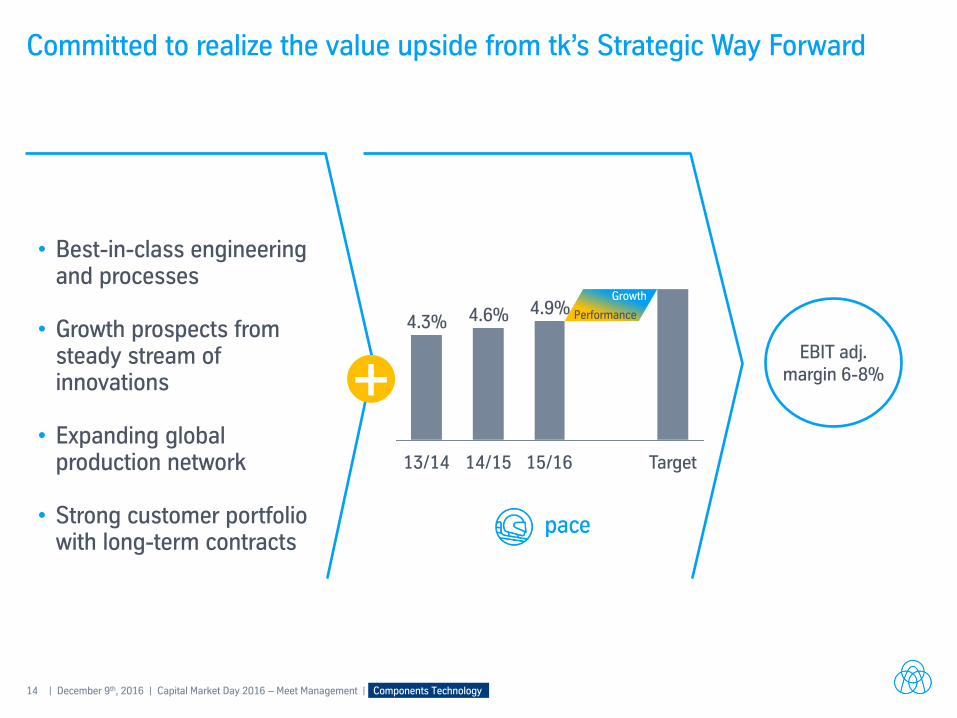

Committed to realize the value upside from tk’s Strategic Way Forward

• Best-in-class engineering and processes

• Growth prospects from

steady stream of innovations

• Expanding global

production network • Strong customer portfolio

with long-term contracts

+ Target 15/16

4.9%

14/15

4.6%

13/14

4.3%

Growth

Performance

EBIT adj. margin 6-8%

Capital Market Day 2016 Meet Management

Capital Market Day 2016 – Meet Management

Elevator Technology

Essen, December 9th, 2016 Andreas Schierenbeck (CEO) I Ercan Keles (CFO)

2 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

thyssenkrupp – a diversified industrial group Sales €39.6 bn; EBIT adj. €1.5 bn

Components Technology (CT)

Materials Services (MX)

Financial figures FY 15/16

Steel Americas (AM)

€1.5 bn €(33) mn

Steel Europe (SE)

€7.6 bn €315 mn

€11.9 bn €128 mn

Elevator Technology (ET)

€7.5 bn €860 mn

€6.8 bn €335 mn

Industrial Solutions (IS)

€5.7 bn €355 mn

3 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

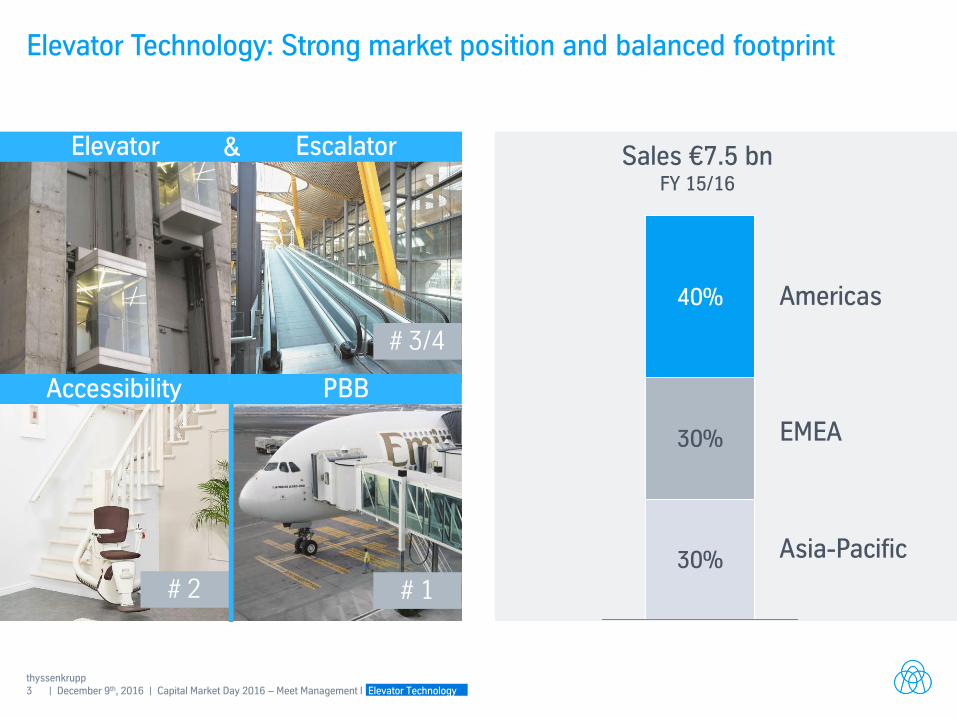

Elevator Technology: Strong market position and balanced footprint

13%

Escalator

Accessibility PBB

# 1

# 3/4

Elevator & Sales €7.5 bn FY 15/16

Americas

# 2

30%

30%

40%

EMEA

Asia-Pacific

4 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

Elevator World Project of the Year 2016

36 elevators I 28 escalators

22 award-winning iwalks

Medina Airport, Saudi Arabia

5 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

Largest PBB contract ever at Istanbul Grand Airport

143 Passenger Boarding Bridges

World’s largest airport by 2020

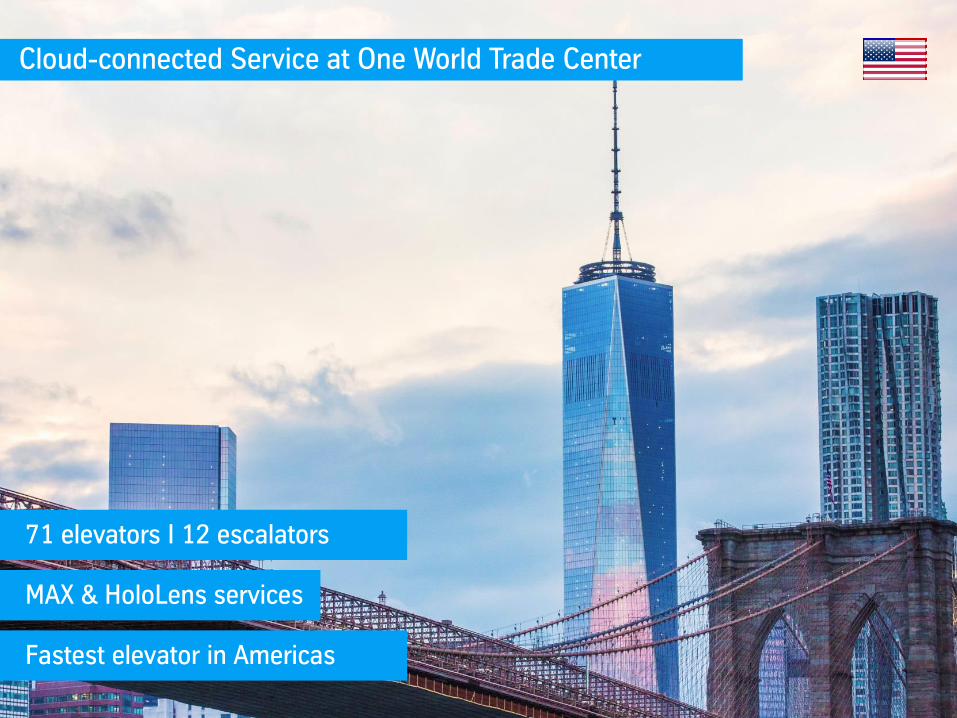

Cloud-connected Service at One World Trade Center

71 elevators I 12 escalators

MAX & HoloLens services

Fastest elevator in Americas

7 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

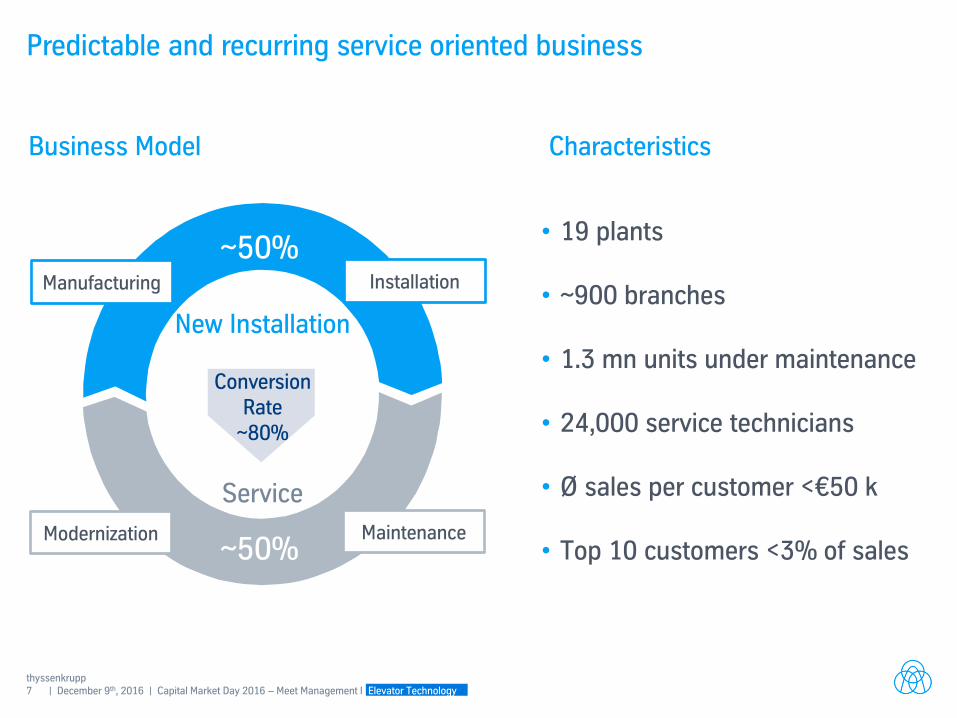

Predictable and recurring service oriented business

• 19 plants

• ~900 branches

• 1.3 mn units under maintenance

• 24,000 service technicians • Ø sales per customer <€50 k

• Top 10 customers <3% of sales

Service

New Installation

Conversion Rate

~80%

~50%

~50% Manufacturing Installation

Modernization Maintenance

Business Model Characteristics

8 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

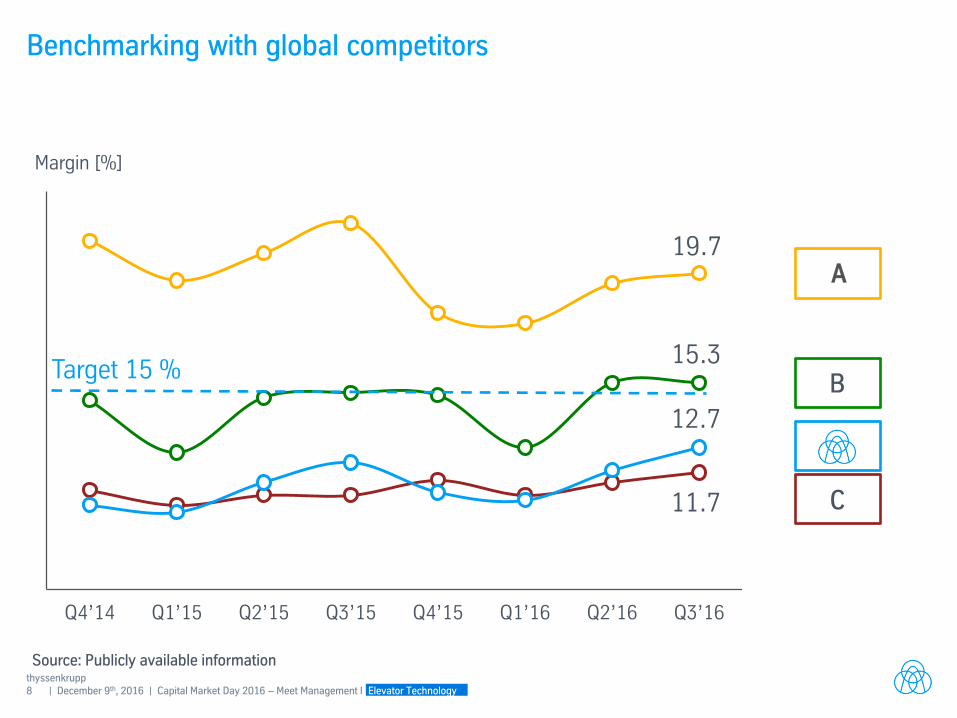

Benchmarking with global competitors

Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16 Q3’16

19.7

15.3

12.7

11.7

Target 15 %

Source: Publicly available information

A

B

C

Margin [%]

9 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

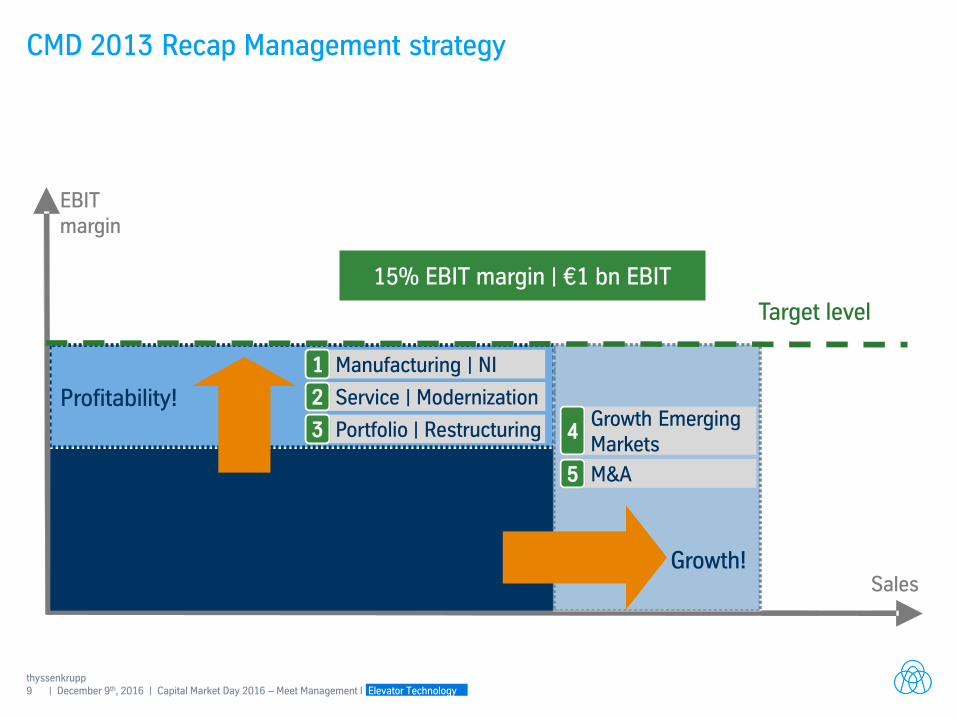

CMD 2013 Recap Management strategy

EBIT margin

Sales

Target level

Profitability!

Growth!

Growth Emerging Markets

2

M&A 5

Portfolio | Restructuring 3

Manufacturing | NI 1 Service | Modernization 2

Manufacturing | NI 1

15% EBIT margin | €1 bn EBIT

1

2

3 4

5

10 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

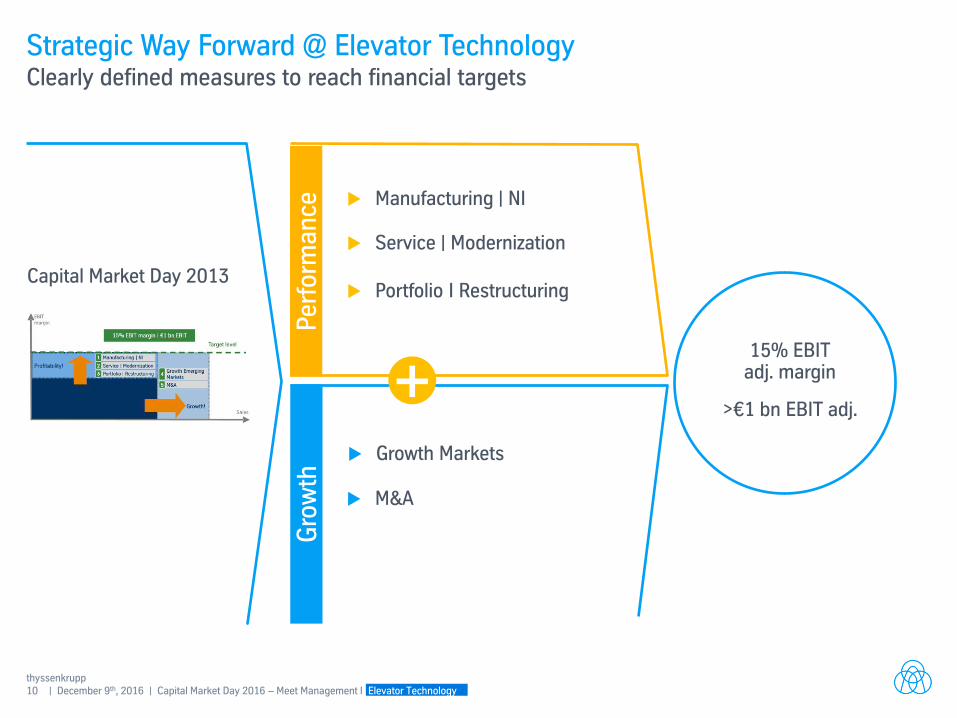

Growth Markets

Strategic Way Forward @ Elevator Technology Clearly defined measures to reach financial targets

Manufacturing | NI

+

Per

form

an

ce

Gro

wth

15% EBIT adj. margin

>€1 bn EBIT adj.

Service | Modernization

Portfolio I Restructuring

M&A

Capital Market Day 2013

11 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

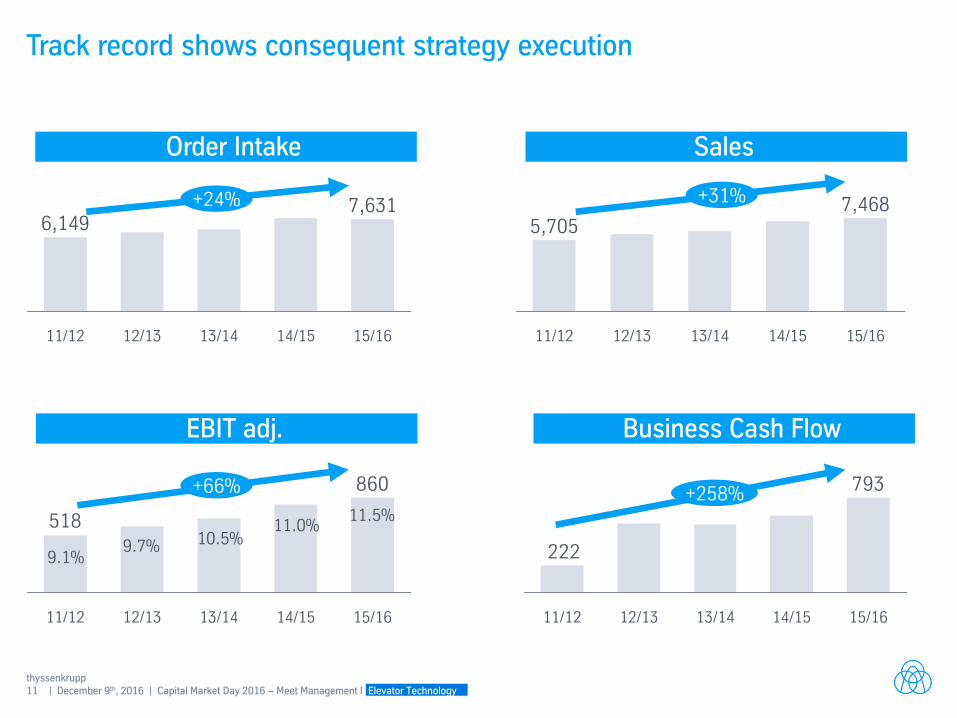

Track record shows consequent strategy execution

Order Intake

15/16

7,631

14/15 13/14 12/13 11/12

6,149 +24%

Sales

14/15 13/14 12/13 11/12

5,705

15/16

7,468 +31%

EBIT adj.

860

518

12/13 11/12 13/14 15/16 14/15

+66%

Business Cash Flow

793

222

15/16 13/14 14/15 12/13 11/12

+258% 11.5%

11.0% 10.5%

9.1% 9.7%

12 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

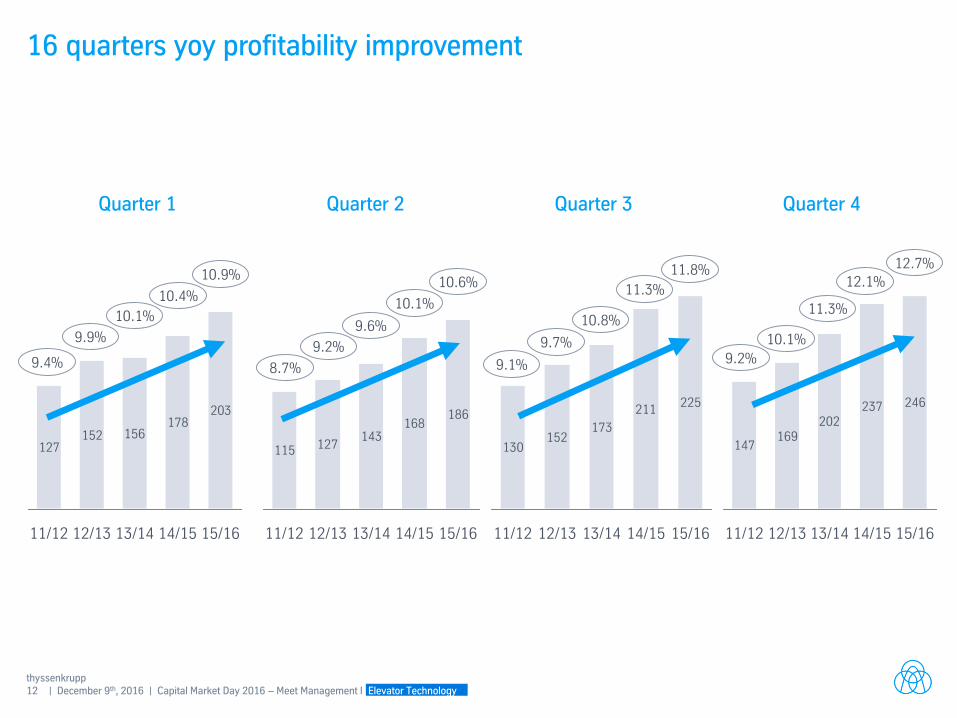

Quarter 1 Quarter 2

127152

178203

15/16 14/15 13/14

156

12/13 11/12

115 127143

168186

13/14 12/13 11/12 15/16 14/15

10.1%

9.9%

9.4%

Quarter 3

130152

173

211225

15/16 14/15 13/14 12/13 11/12

9.6%

9.2%

8.7%

Quarter 4

147169

202237 246

14/15 13/14 12/13 11/12 15/16

10.4% 10.1%

10.9% 10.6%

10.8%

9.7%

9.1%

10.1%

9.2%

11.3%

11.3% 12.1%

11.8%

16 quarters yoy profitability improvement

12.7%

13 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

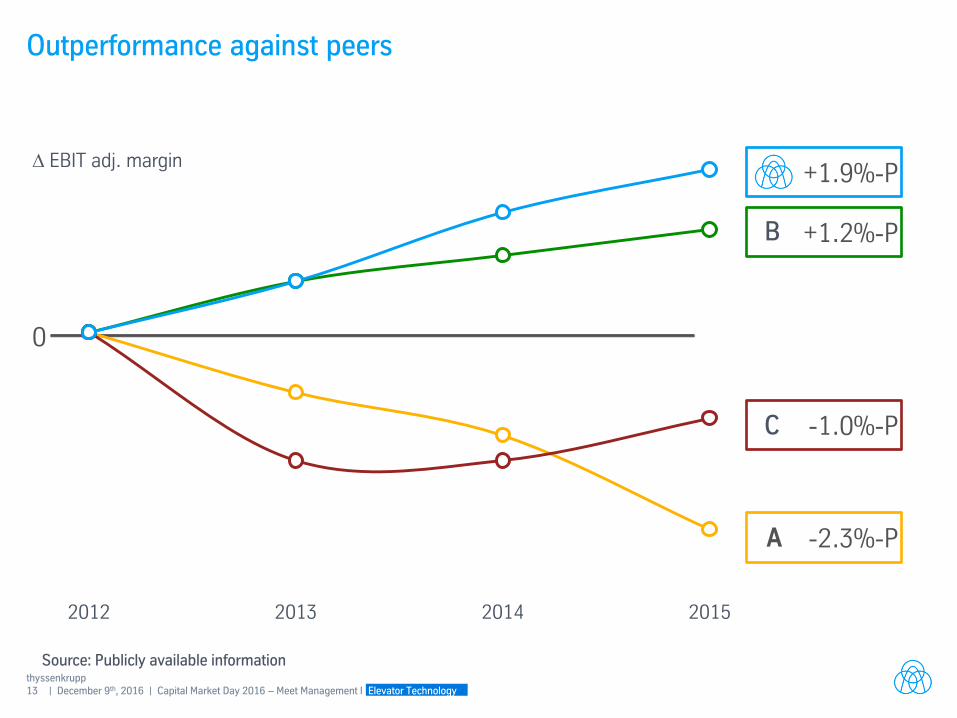

Outperformance against peers

Source: Publicly available information

-2.3%-P

+1.2%-P

+1.9%-P

-1.0%-P

0

2012 2013 2014 2015

A

B

C

∆ EBIT adj. margin

14 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

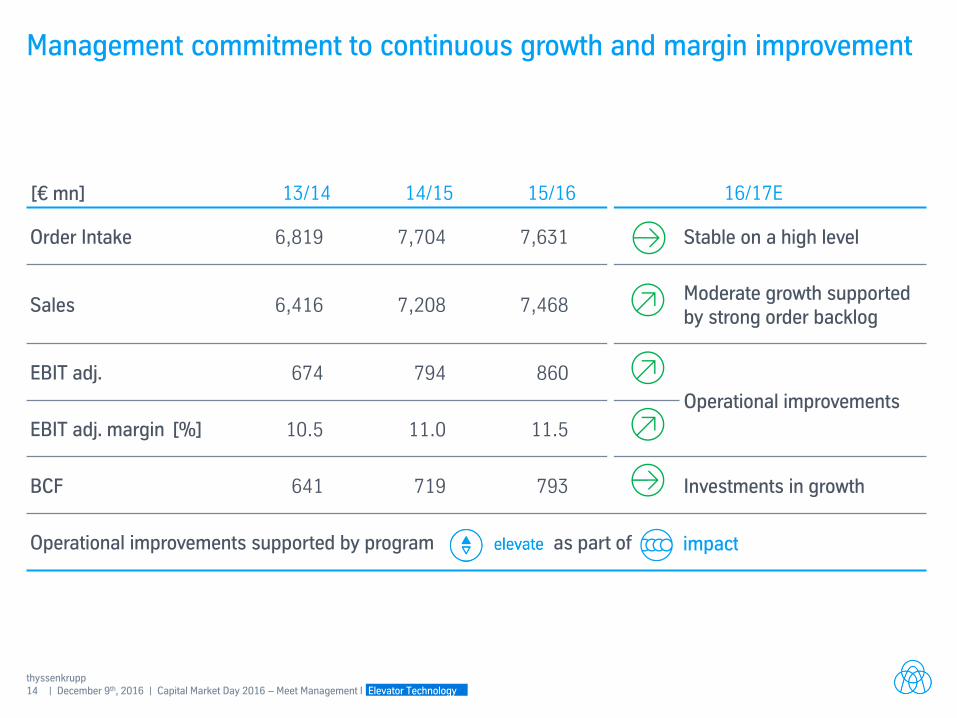

Management commitment to continuous growth and margin improvement

13/14 14/15 15/16 16/17E

Order Intake 6,819 7,704 7,631 Stable on a high level

Sales

6,416 7,208 7,468 Moderate growth supported by strong order backlog

EBIT adj. 674 794 860

Operational improvements

EBIT adj. margin [%] 10.5 11.0 11.5

BCF 641 719 793 Investments in growth

Operational improvements supported by program as part of

[€ mn]

15 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

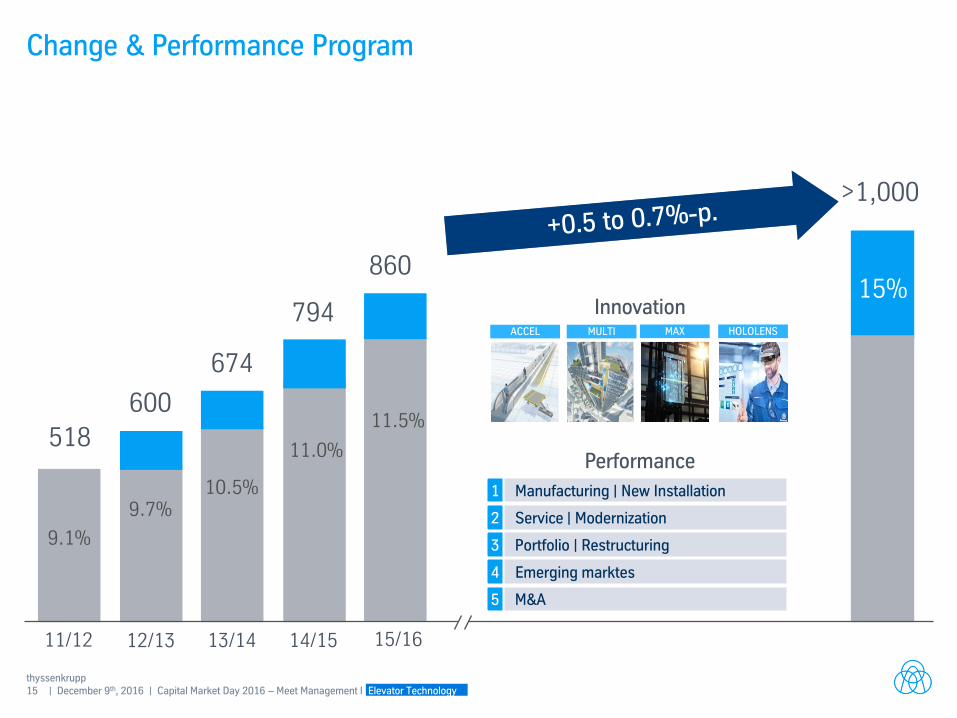

>1,000

15% 860

11.5% 518

9.1%

11/12

600

9.7%

12/13

674

10.5%

13/14

794

11.0%

14/15 15/16

Innovation

Manufacturing | New Installation

Service | Modernization

Portfolio | Restructuring

Emerging marktes

M&A

1

2

3

4

5

MAX HOLOLENS ACCEL MULTI

Performance

Change & Performance Program

16 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

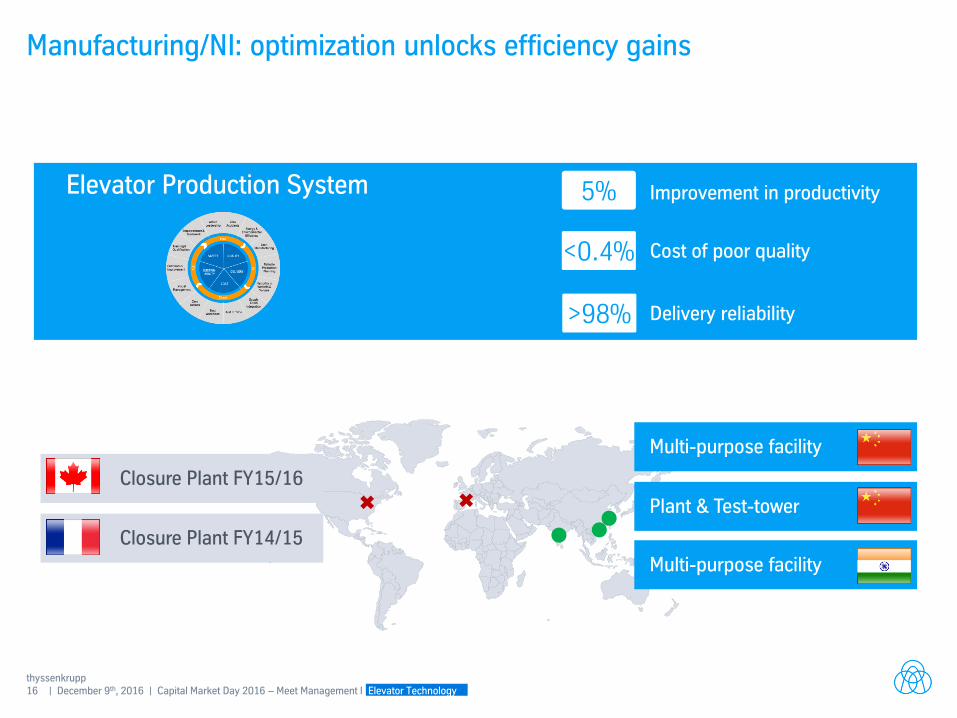

Improvement in productivity

Delivery reliability >98%

5%

Manufacturing/NI: optimization unlocks efficiency gains

Multi-purpose facility

Multi-purpose facility

Plant & Test-tower

Closure Plant FY15/16

Closure Plant FY14/15

Elevator Production System

Cost of poor quality <0.4%

17 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

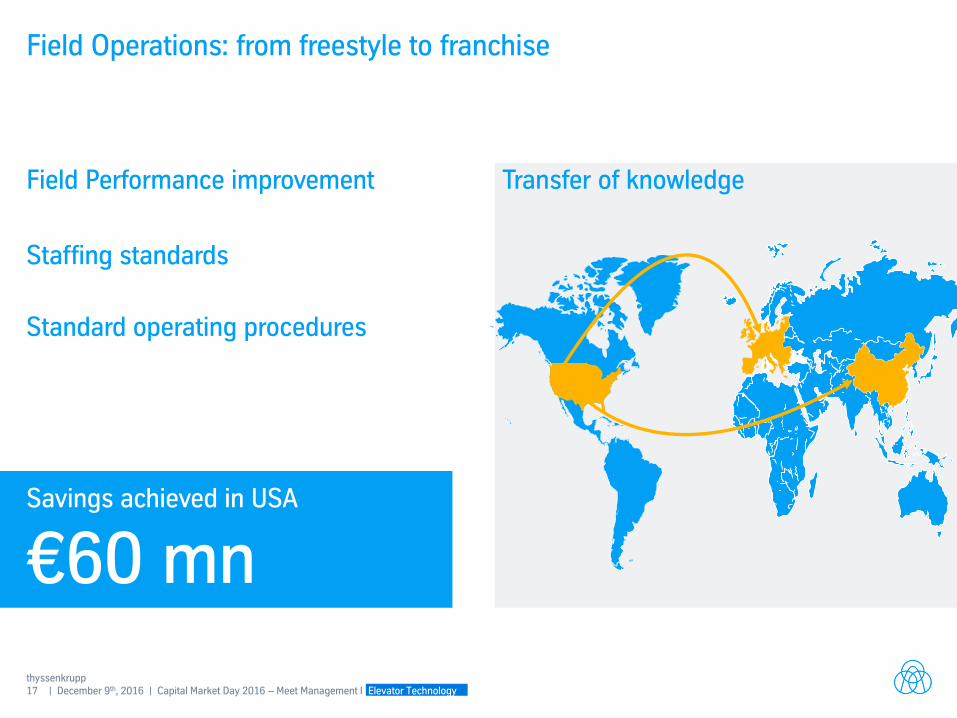

Field Operations: from freestyle to franchise

Field Performance improvement

Staffing standards

Standard operating procedures

Transfer of knowledge

Savings achieved in USA

€60 mn

18 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

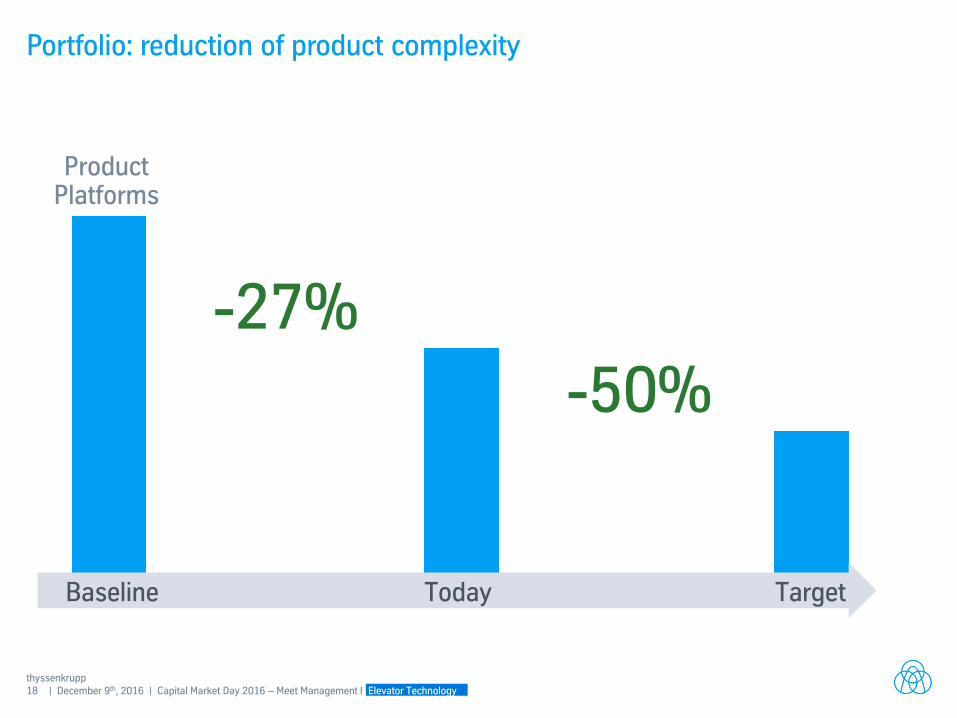

Portfolio: reduction of product complexity

Baseline

-27%

-50%

Product Platforms

Today Target

19 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

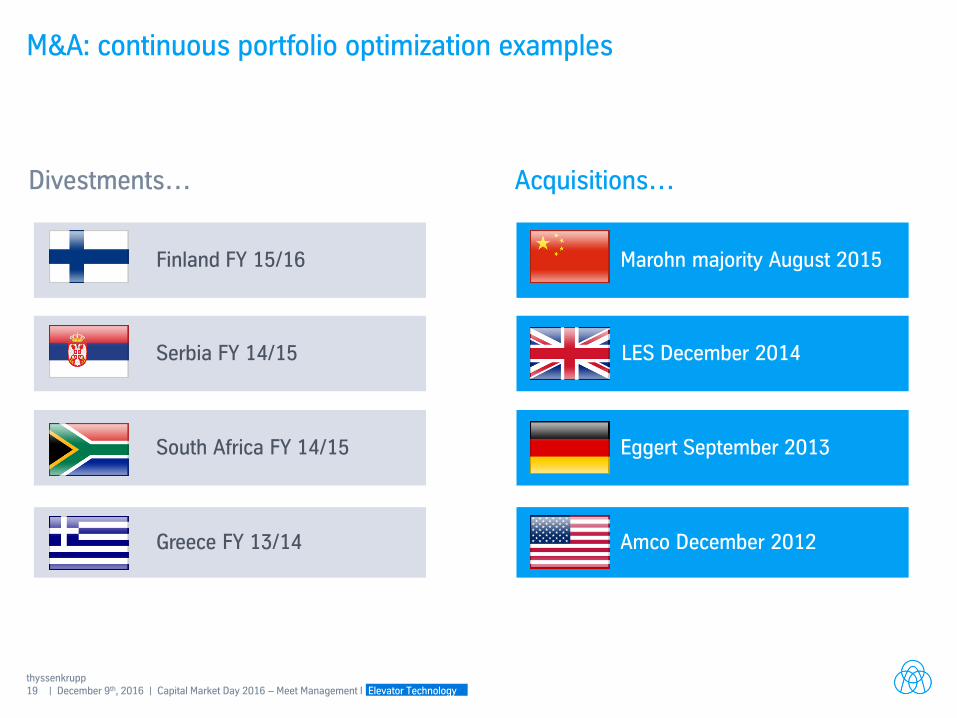

Eggert September 2013

Marohn majority August 2015

LES December 2014

South Africa FY 14/15

Greece FY 13/14

Serbia FY 14/15

Finland FY 15/16

M&A: continuous portfolio optimization examples

Divestments… Acquisitions…

Amco December 2012

20 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

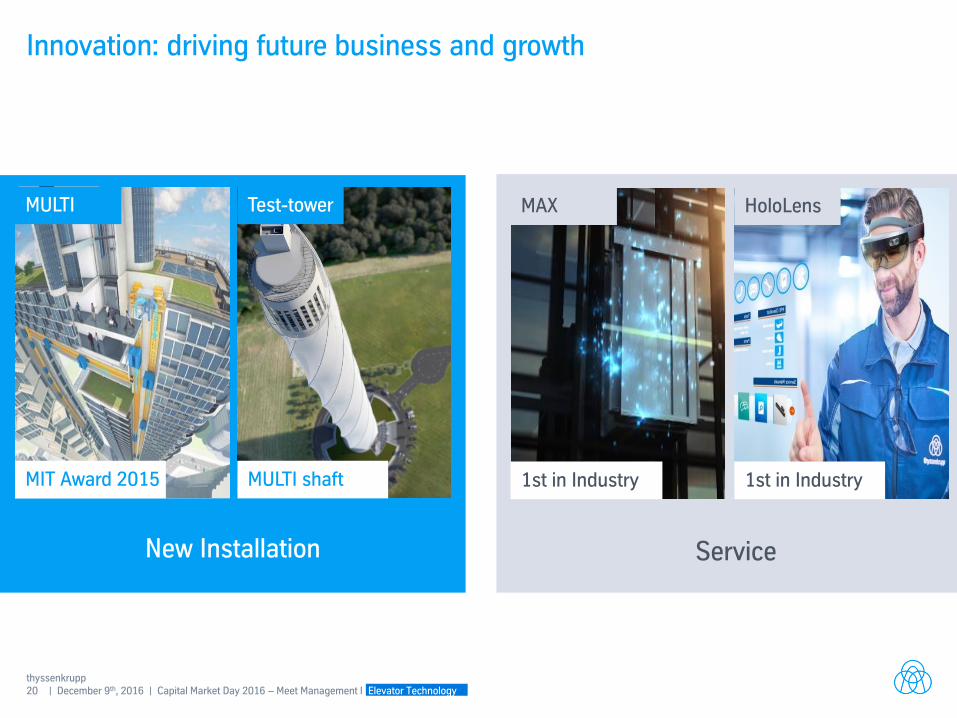

Service

New Installation

Innovation: driving future business and growth

Test-tower MAX HoloLens

MULTI shaft 1st in Industry 1st in Industry

MULTI

MIT Award 2015

21 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

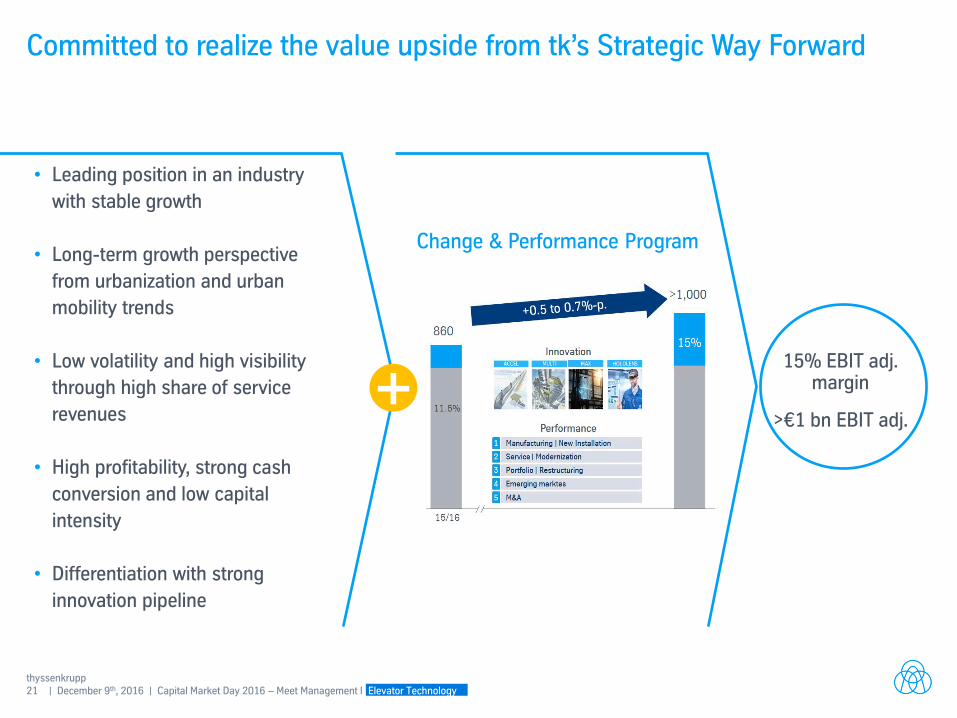

Committed to realize the value upside from tk’s Strategic Way Forward

• Leading position in an industry

with stable growth

• Long-term growth perspective

from urbanization and urban

mobility trends

• Low volatility and high visibility

through high share of service

revenues

• High profitability, strong cash

conversion and low capital

intensity

• Differentiation with strong

innovation pipeline

15% EBIT adj. margin

>€1 bn EBIT adj. +

Change & Performance Program

22 | December 9th, 2016 | Capital Market Day 2016 – Meet Management I Elevator Technology thyssenkrupp

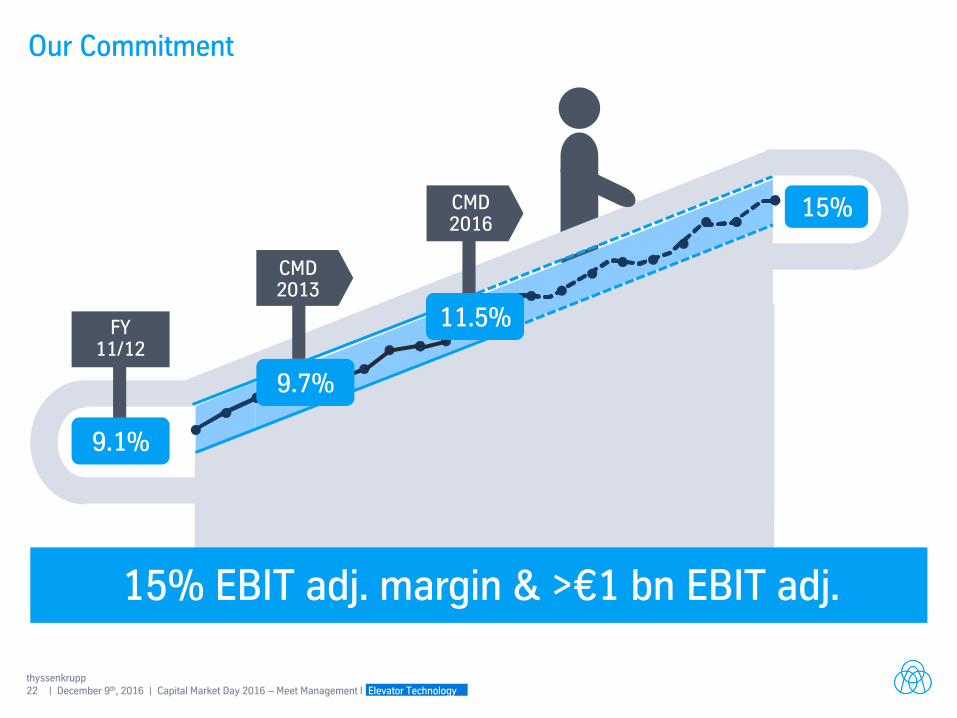

Our Commitment

15% EBIT adj. margin & >€1 bn EBIT adj.

FY 11/12

CMD 2016

9.1%

9.7%

15%

11.5%

CMD 2013

Capital Market Day 2016 Meet Management

Capital Market Day 2016 – Meet Management

Industrial Solutions

Essen, December 9th, 2016 Stefan Gesing (CEO/CFO) | Johan P. Cnossen (COO)

2 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

thyssenkrupp – a diversified industrial group Sales €39.6 bn; EBIT adj. €1.5 bn

Components Technology (CT)

Materials Services (MX)

Financial figures FY 15/16

Steel Americas (AM)

€1.5 bn €(33) mn

Steel Europe (SE)

€7.6 bn €315 mn

€11.9 bn €128 mn

Elevator Technology (ET)

€7.5 bn €860 mn

€6.8 bn €335 mn

Industrial Solutions (IS)

€5.7 bn €355 mn

3 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

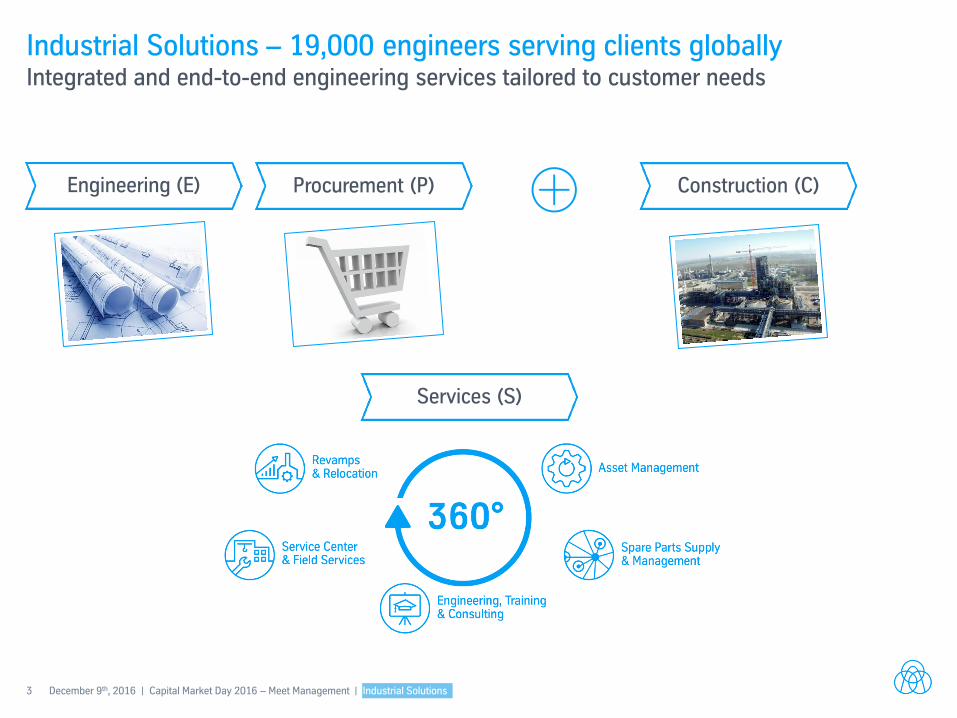

Industrial Solutions – 19,000 engineers serving clients globally Integrated and end-to-end engineering services tailored to customer needs

Construction (C) Engineering (E) Procurement (P)

Services (S)

4 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

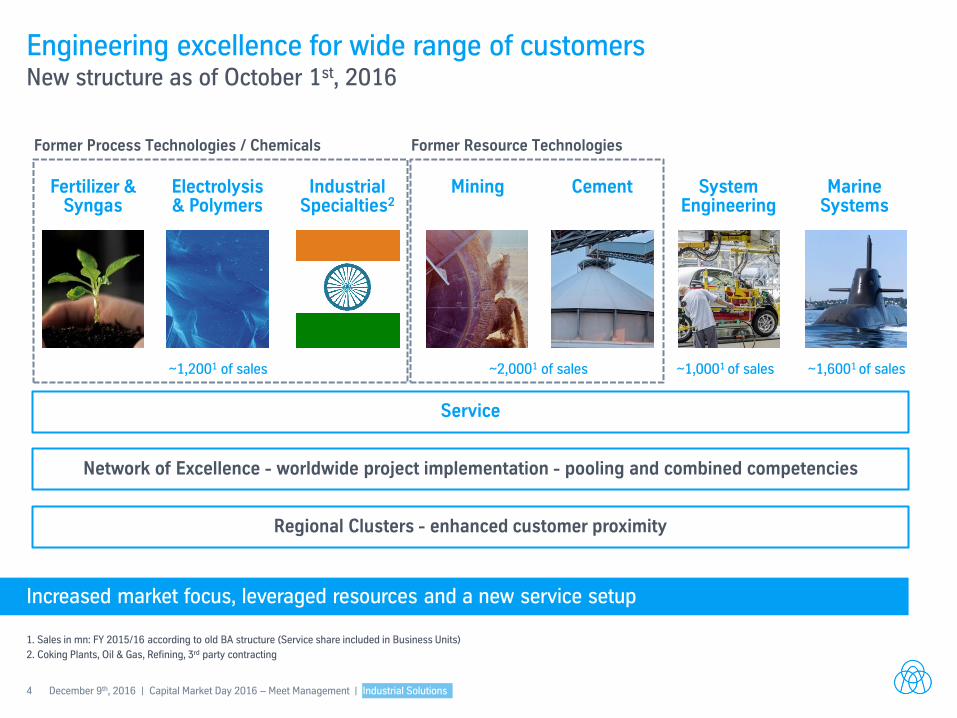

Engineering excellence for wide range of customers New structure as of October 1st, 2016

Fertilizer & Syngas

Electrolysis & Polymers

Cement Mining System Engineering

Industrial Specialties2

Marine Systems

2. Coking Plants, Oil & Gas, Refining, 3rd party contracting

Former Process Technologies / Chemicals Former Resource Technologies

1. Sales in mn: FY 2015/16 according to old BA structure (Service share included in Business Units)

~1,2001 of sales ~2,0001 of sales ~1,0001 of sales ~1,6001 of sales

Network of Excellence - worldwide project implementation - pooling and combined competencies

Regional Clusters - enhanced customer proximity

Service

Increased market focus, leveraged resources and a new service setup

5 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

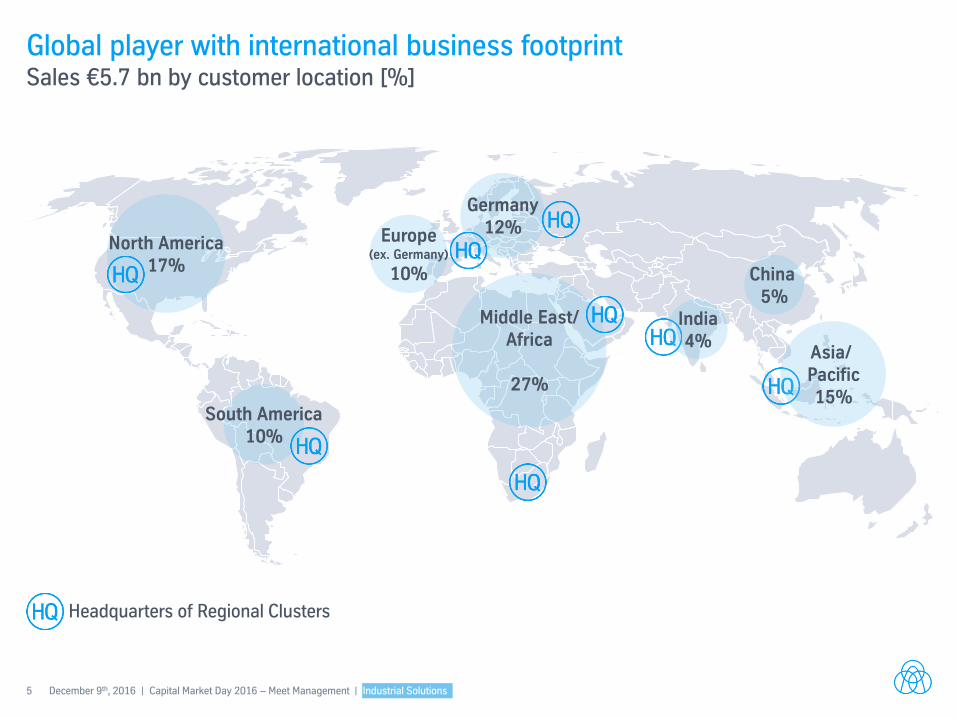

Global player with international business footprint Sales €5.7 bn by customer location [%]

North America 17%

South America 10%

Middle East/ Africa

27%

Germany 12% Europe

(ex. Germany)

10%

Headquarters of Regional Clusters

India 4%

China 5%

Asia/ Pacific 15%

6 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

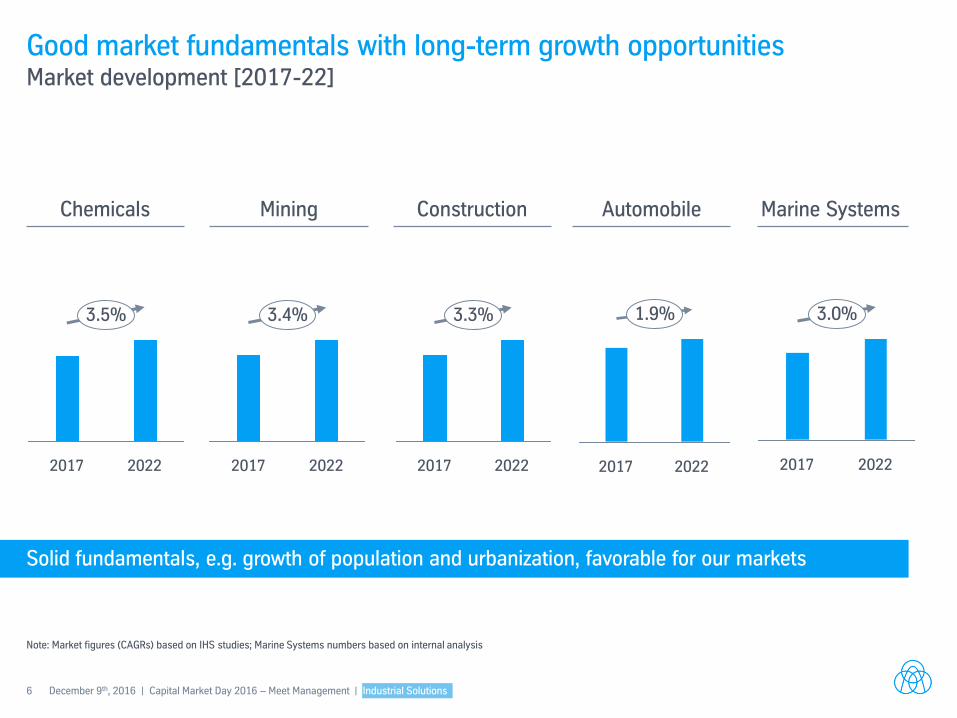

Good market fundamentals with long-term growth opportunities Market development [2017-22]

Note: Market figures (CAGRs) based on IHS studies; Marine Systems numbers based on internal analysis

Mining Automobile Marine Systems Chemicals Construction

3.5%

2022 2017

3.4%

2022 2017

3.3%

2022 2017 2022 2017

1.9% 3.0%

2022 2017

Solid fundamentals, e.g. growth of population and urbanization, favorable for our markets

7 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

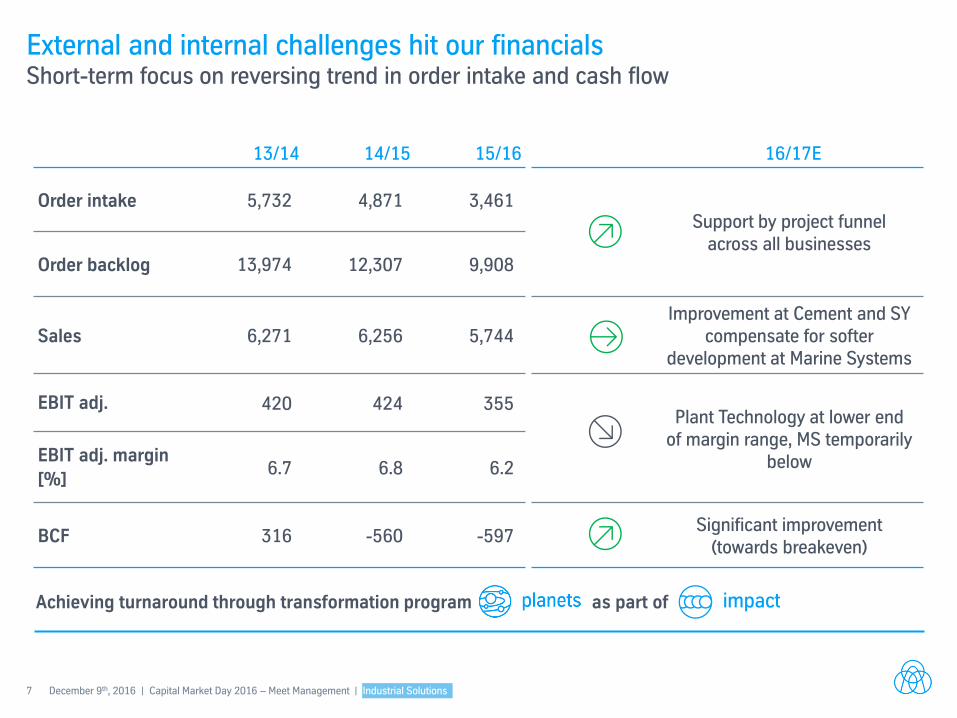

External and internal challenges hit our financials

13/14 14/15 15/16

Order intake 5,732 4,871 3,461

Order backlog 13,974 12,307 9,908

Sales 6,271 6,256 5,744

EBIT adj. 420 424 355

EBIT adj. margin

[%] 6.7 6.8 6.2

BCF 316 -560 -597

16/17E

Support by project funnel across all businesses

Improvement at Cement and SY compensate for softer

development at Marine Systems

Plant Technology at lower end of margin range, MS temporarily

below

Significant improvement (towards breakeven)

Achieving turnaround through transformation program as part of

Short-term focus on reversing trend in order intake and cash flow

8 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

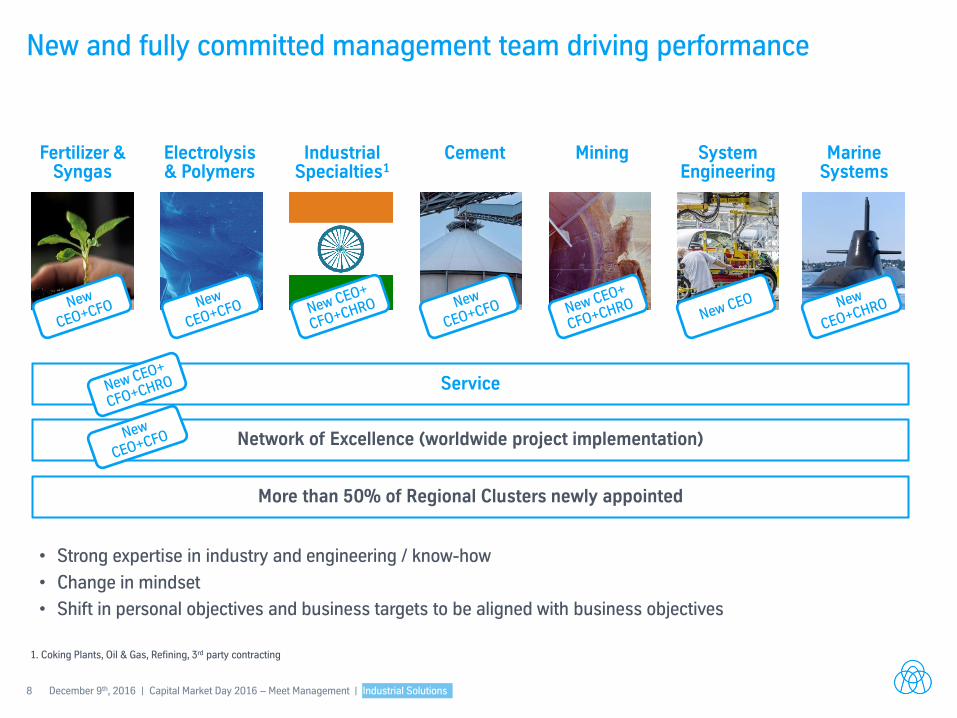

Service

New and fully committed management team driving performance

Cement Industrial Specialties1

Fertilizer & Syngas

Electrolysis & Polymers

Marine Systems

System Engineering

Mining

1. Coking Plants, Oil & Gas, Refining, 3rd party contracting

• Strong expertise in industry and engineering / know-how

• Change in mindset

• Shift in personal objectives and business targets to be aligned with business objectives

Network of Excellence (worldwide project implementation)

More than 50% of Regional Clusters newly appointed

9 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

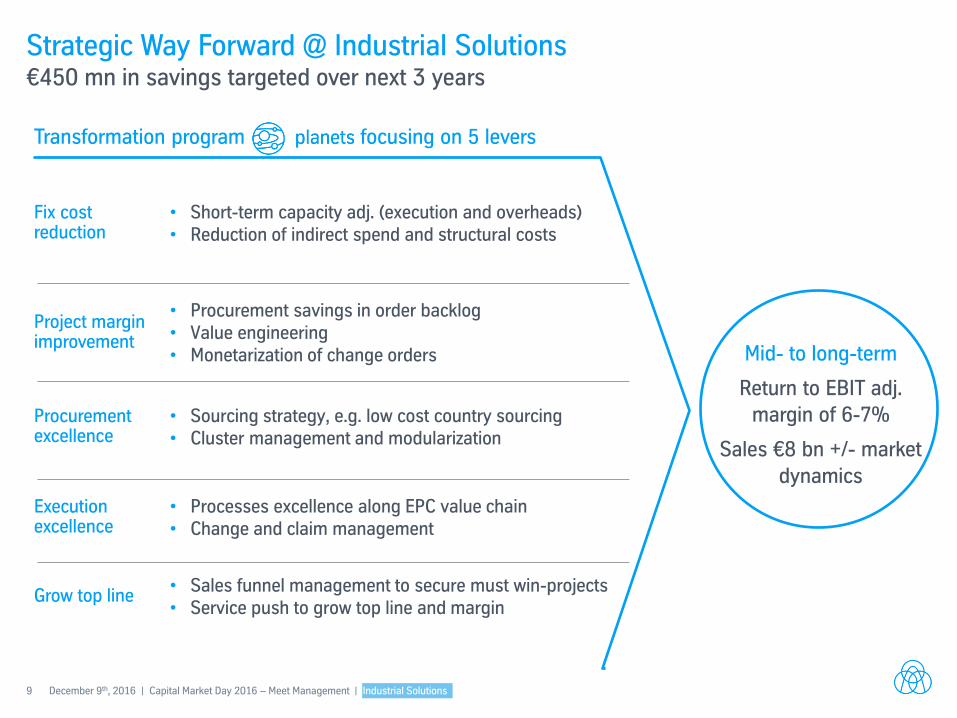

Strategic Way Forward @ Industrial Solutions €450 mn in savings targeted over next 3 years Transformation program focusing on 5 levers

• Sales funnel management to secure must win-projects • Service push to grow top line and margin

Grow top line

• Procurement savings in order backlog • Value engineering • Monetarization of change orders

Project margin improvement

• Sourcing strategy, e.g. low cost country sourcing • Cluster management and modularization

Procurement excellence

• Processes excellence along EPC value chain • Change and claim management

Execution excellence

• Short-term capacity adj. (execution and overheads) • Reduction of indirect spend and structural costs

Fix cost reduction

Mid- to long-term

Return to EBIT adj. margin of 6-7%

Sales €8 bn +/- market

dynamics

10 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

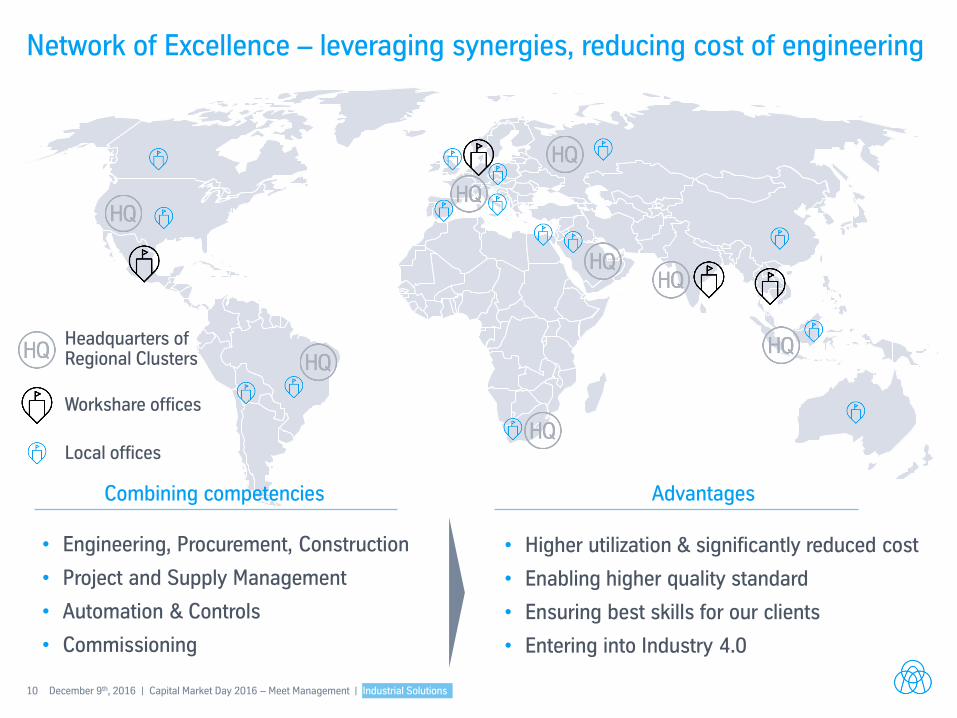

Network of Excellence – leveraging synergies, reducing cost of engineering

• Higher utilization & significantly reduced cost

• Enabling higher quality standard

• Ensuring best skills for our clients

• Entering into Industry 4.0

• Engineering, Procurement, Construction

• Project and Supply Management

• Automation & Controls

• Commissioning

Advantages Combining competencies

Workshare offices

Local offices

Headquarters of Regional Clusters

11 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

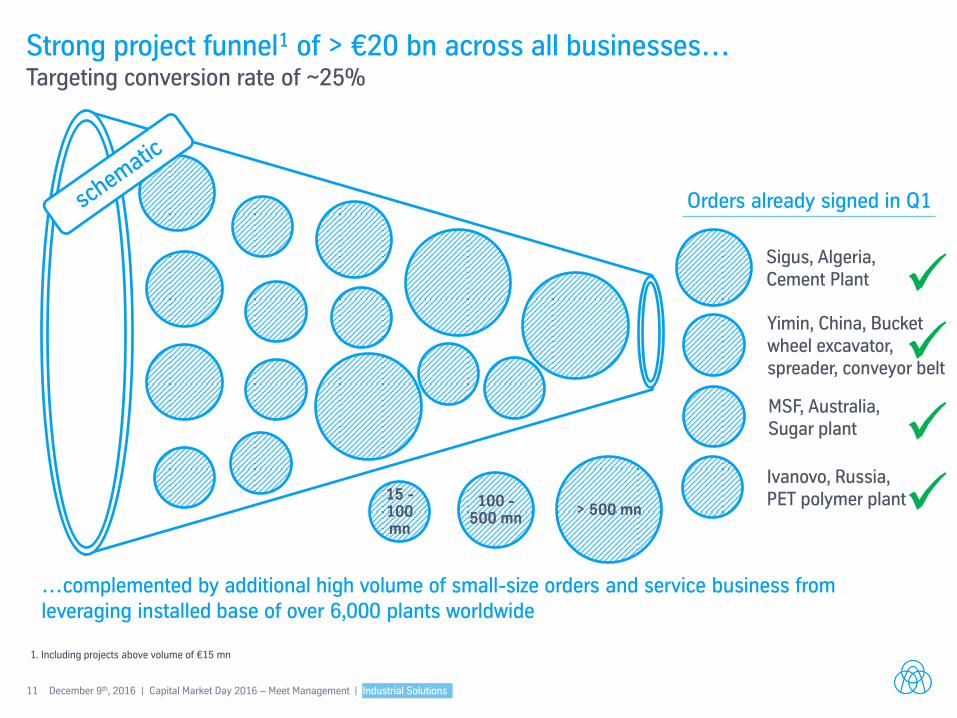

Strong project funnel1 of > €20 bn across all businesses… Targeting conversion rate of ~25%

Orders already signed in Q1

…complemented by additional high volume of small-size orders and service business from leveraging installed base of over 6,000 plants worldwide

1. Including projects above volume of €15 mn

15 -100 mn

100 - 500 mn

> 500 mn

Sigus, Algeria, Cement Plant

Yimin, China, Bucket wheel excavator, spreader, conveyor belt

MSF, Australia, Sugar plant

Ivanovo, Russia, PET polymer plant

12 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

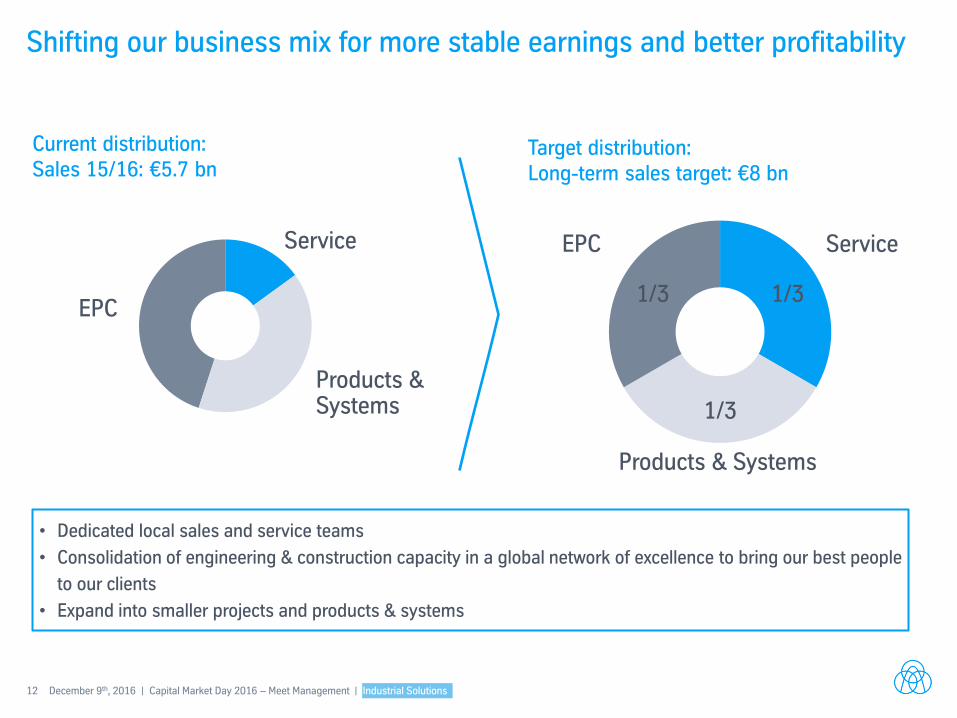

Shifting our business mix for more stable earnings and better profitability

• Dedicated local sales and service teams

• Consolidation of engineering & construction capacity in a global network of excellence to bring our best people

to our clients

• Expand into smaller projects and products & systems

Current distribution: Sales 15/16: €5.7 bn

Target distribution: Long-term sales target: €8 bn

Service

EPC

Products & Systems

1/3

1/3

1/3

EPC

Products & Systems

Service

13 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

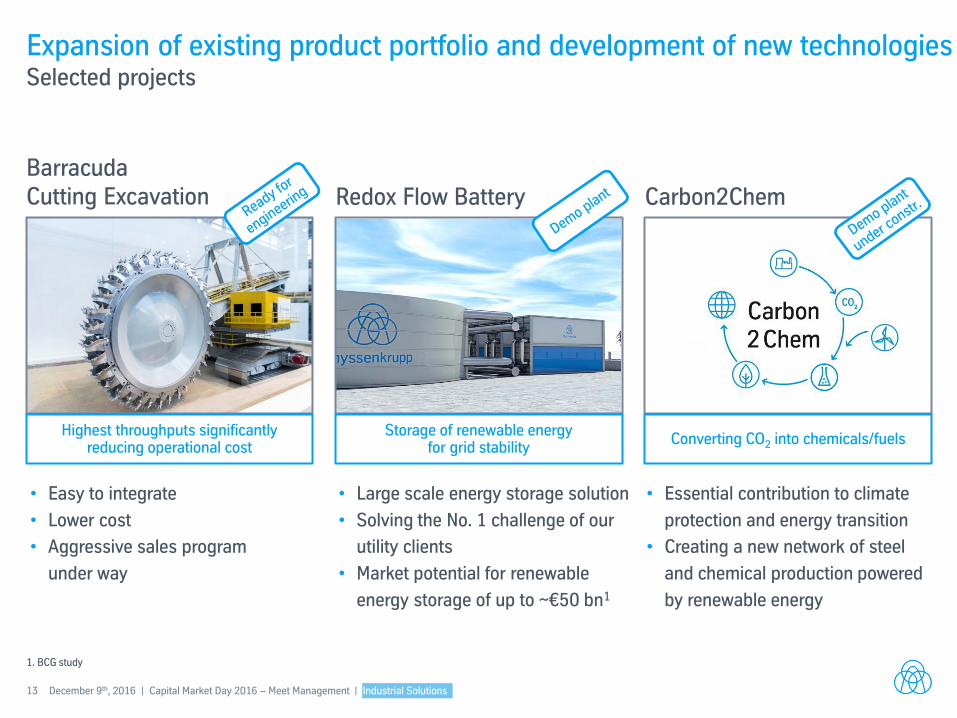

Expansion of existing product portfolio and development of new technologies Selected projects

• Easy to integrate

• Lower cost

• Aggressive sales program

under way

• Large scale energy storage solution

• Solving the No. 1 challenge of our

utility clients

• Market potential for renewable

energy storage of up to ~€50 bn1

• Essential contribution to climate

protection and energy transition

• Creating a new network of steel

and chemical production powered

by renewable energy

Storage of renewable energy for grid stability

Converting CO2 into chemicals/fuels Highest throughputs significantly

reducing operational cost

Barracuda Cutting Excavation Redox Flow Battery Carbon2Chem

1. BCG study

14 December 9th, 2016 | Capital Market Day 2016 – Meet Management | Industrial Solutions

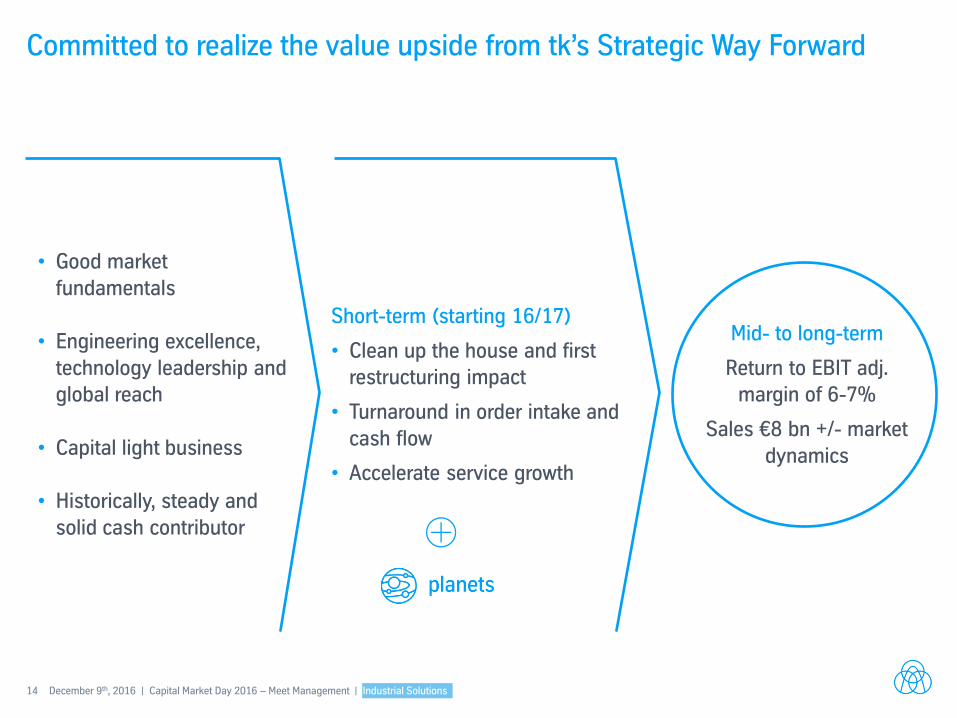

Committed to realize the value upside from tk’s Strategic Way Forward

• Good market

fundamentals

• Engineering excellence,

technology leadership and global reach

• Capital light business

• Historically, steady and

solid cash contributor

Short-term (starting 16/17)

• Clean up the house and first restructuring impact

• Turnaround in order intake and

cash flow

• Accelerate service growth

Mid- to long-term

Return to EBIT adj. margin of 6-7%

Sales €8 bn +/- market

dynamics

Capital Market Day 2016 Meet Management

Capital Market Day 2016 - Meet Management

Materials Services

Essen, December 9th, 2016 Joachim Limberg (CEO) | Klaus Keysberg (CFO)

2 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

thyssenkrupp – a diversified industrial group Sales €39.6 bn; EBIT adj. €1.5 bn

Components Technology (CT)

Materials Services (MX)

Elevator Technology (ET)

Industrial Solutions (IS)

Steel Europe (SE)

Steel Americas (AM)

Financial figures FY 15/16

€7.5 bn €860 mn

€5.7 bn €355 mn

€1.5 bn €(33) mn

€7.6 bn €315 mn

€11.9 bn €128 mn

€6.8 bn €335 mn

3 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

Sales driven customer service organization Sales €11.9 bn

• Materials distribution (just-in-time)

• Processing

• Inventory/Warehouse Management

• Supply Chain Management

• Materials

• Raw materials

Stainless steel AST since March 1, 2014

Warehousing Services 71% of sales

Trading 16% of sales

Production 13% of sales

4 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

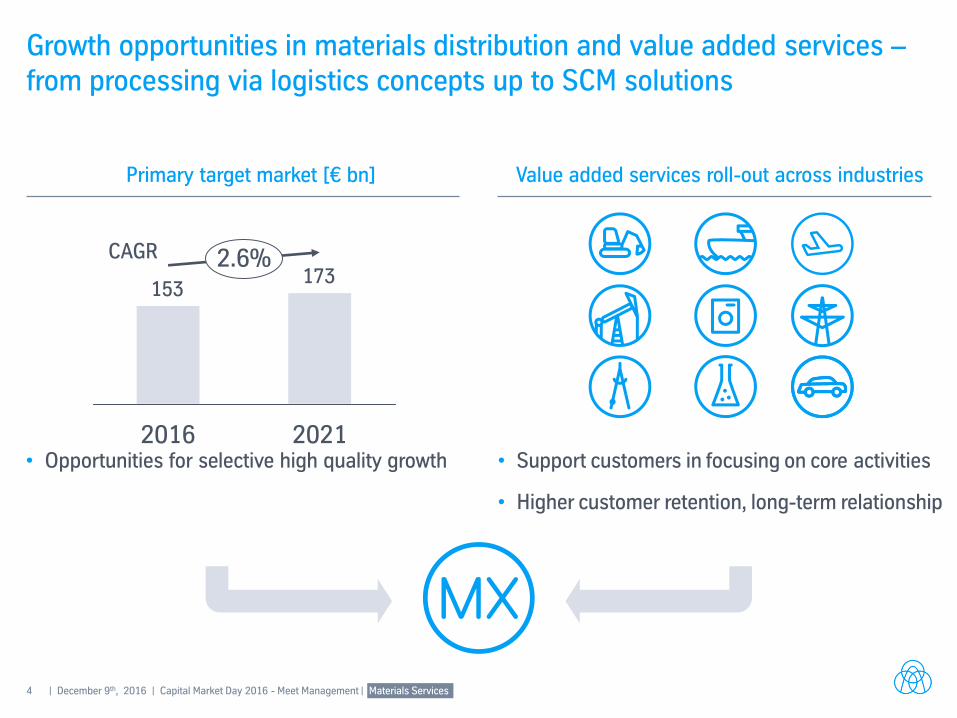

Growth opportunities in materials distribution and value added services – from processing via logistics concepts up to SCM solutions

173153

2.6%

2021 2016 • Opportunities for selective high quality growth • Support customers in focusing on core activities

• Higher customer retention, long-term relationship

Primary target market [€ bn] Value added services roll-out across industries

CAGR

5 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

Well diversified across customer groups with footprint in developed countries w/o Raw Materials, Technical Services and AST1

Sales by customer groups Well-known customers around the world (extract)

14%

5%

Metal- working industry

Energy

Others

Construction

Aerospace 10%

Local Dealer

10%

5%

13%

Mechanical Engineering

25%

Automotive 17%

€9.0 bn

1. FY 15/16

Europe #2 | Germany #1 | Eastern Europe #3 | North America #4 Leading positions in fragmented markets

6 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

One-stop shop for wide range of products and value added services1

Sales by product groups

1. FY 15/16 | 2. mainly Technical Services

Only 10% sourced from SE

5%

Others2

5%

19%

4%

Pipes and Tubes

Raw Materials

8% NF Metals

Stainless Steel 33%

Carbon Steel

Plastics

€11.9 bn AST

26%

7 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

13/14 14/15 15/16 16/17E

Sales

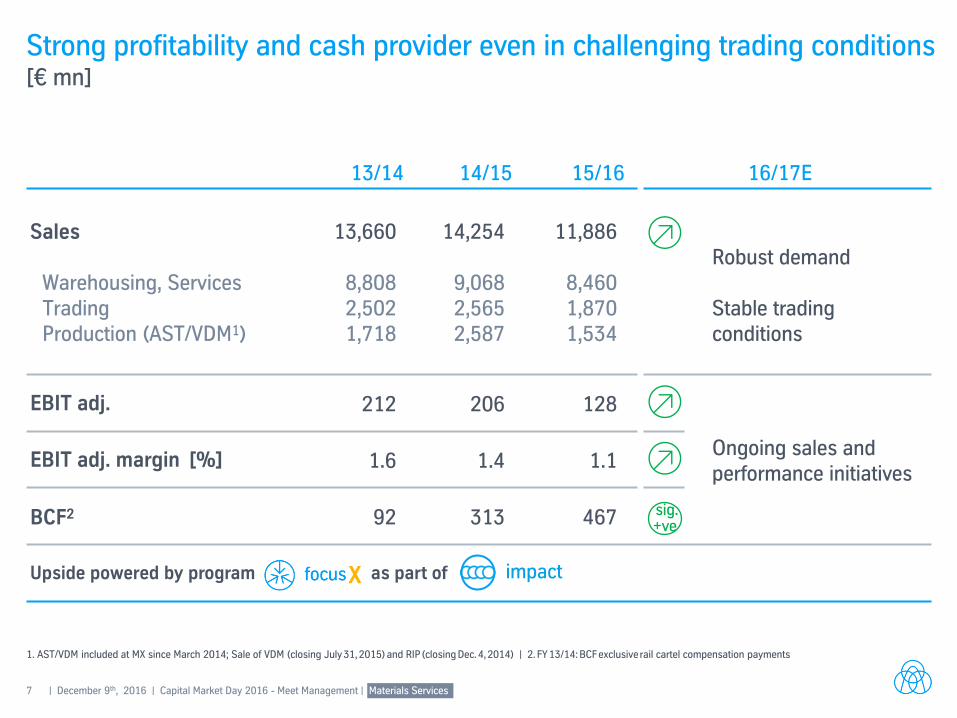

Warehousing, Services Trading Production (AST/VDM1)

13,660

8,808 2,502 1,718

14,254

9,068 2,565 2,587

11,886

8,460 1,870 1,534

Robust demand Stable trading conditions

EBIT adj. 212 206 128

Ongoing sales and performance initiatives

EBIT adj. margin [%] 1.6 1.4 1.1

BCF2 92 313 467

Upside powered by program as part of

Strong profitability and cash provider even in challenging trading conditions [€ mn]

1. AST/VDM included at MX since March 2014; Sale of VDM (closing July 31, 2015) and RIP (closing Dec. 4, 2014) | 2. FY 13/14: BCF exclusive rail cartel compensation payments

sig. +ve

X

8 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

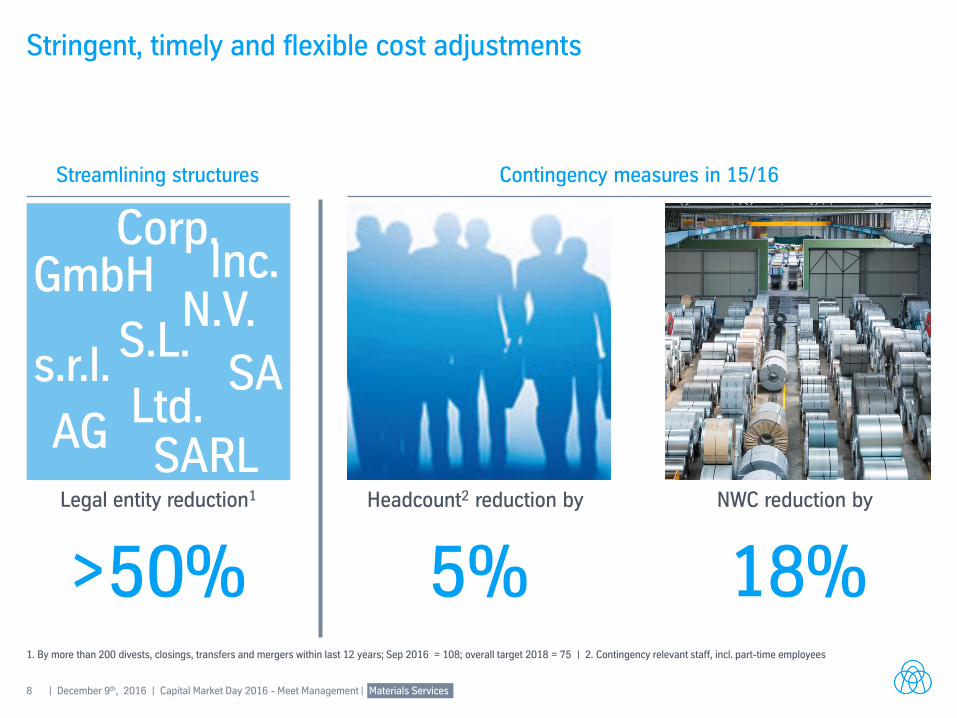

>50% Legal entity reduction1

GmbH

AG Ltd.

S.L.

SARL

s.r.l. SA

Inc. Corp.

N.V.

Stringent, timely and flexible cost adjustments

1. By more than 200 divests, closings, transfers and mergers within last 12 years; Sep 2016 = 108; overall target 2018 = 75 | 2. Contingency relevant staff, incl. part-time employees

5% 18% Headcount2 reduction by NWC reduction by

Contingency measures in 15/16 Streamlining structures

9 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

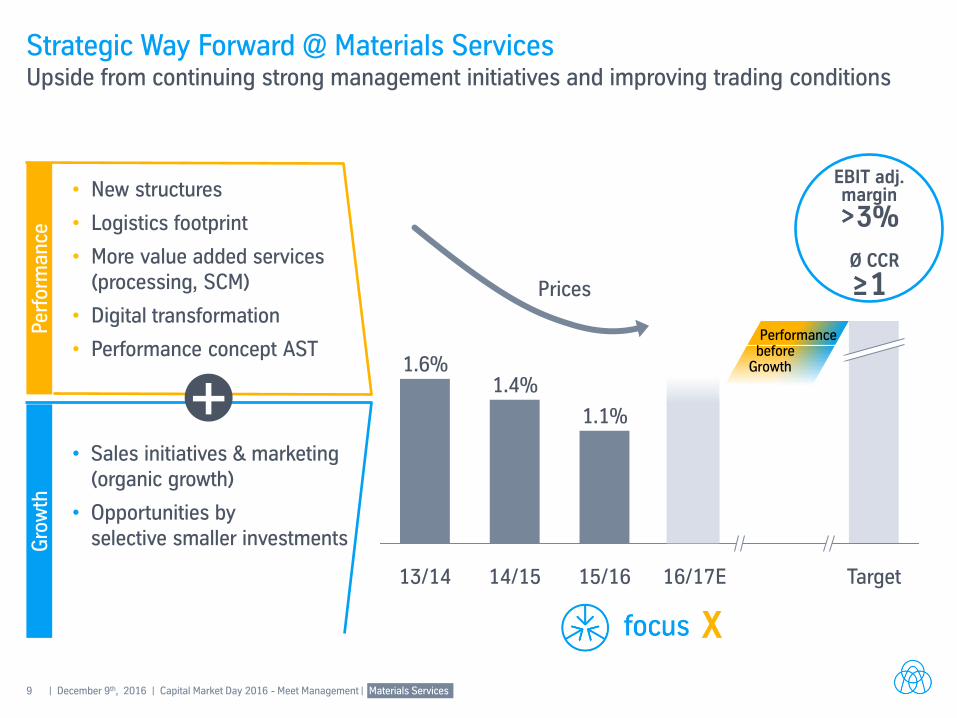

Strategic Way Forward @ Materials Services Upside from continuing strong management initiatives and improving trading conditions

Per

form

an

ce

Gro

wth

+

Prices

1.6% 1.4%

Target 15/16

1.1%

16/17E 14/15 13/14

• New structures

• Logistics footprint

• More value added services (processing, SCM)

• Digital transformation

• Performance concept AST

• Sales initiatives & marketing (organic growth)

• Opportunities by selective smaller investments

EBIT adj. margin

>3%

Ø CCR

≥1

X

Performance before Growth

10 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

Just-in-time deliveries

Efficient

Warehousing and logistics system

Central Regional

Local

Logistics and IT excellence: Largest ERP system worldwide provides basis for efficient processes One SAP template for MX with 8,000 users

11 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

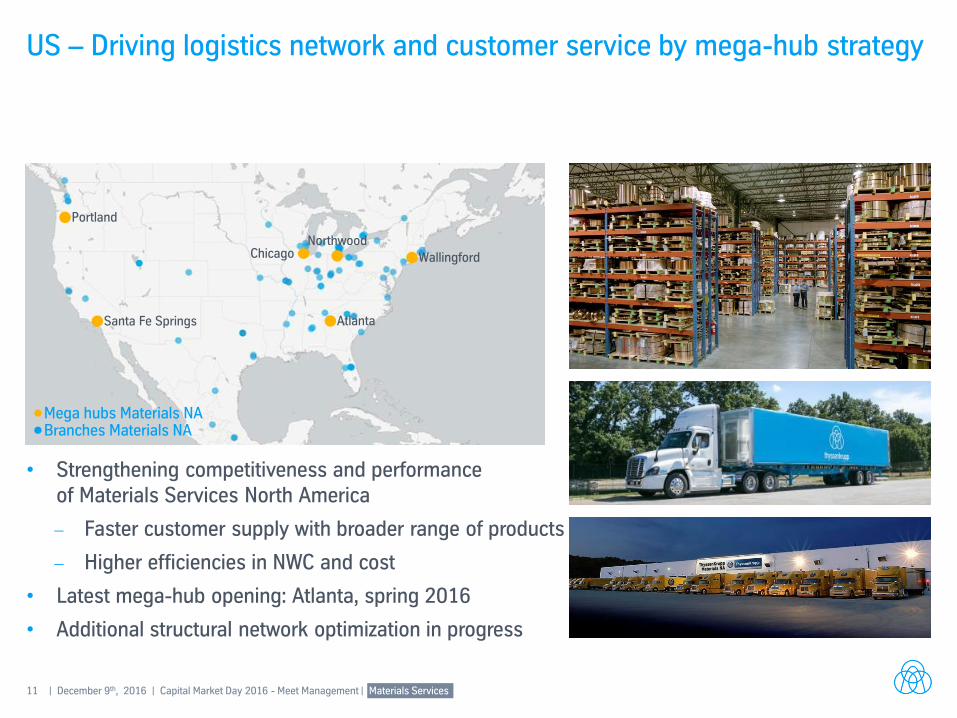

US – Driving logistics network and customer service by mega-hub strategy

• Strengthening competitiveness and performance of Materials Services North America

Faster customer supply with broader range of products

Higher efficiencies in NWC and cost

• Latest mega-hub opening: Atlanta, spring 2016

• Additional structural network optimization in progress

Wallingford

Northwood

Chicago

Portland

Santa Fe Springs Atlanta

Branches Materials NA Mega hubs Materials NA

12 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

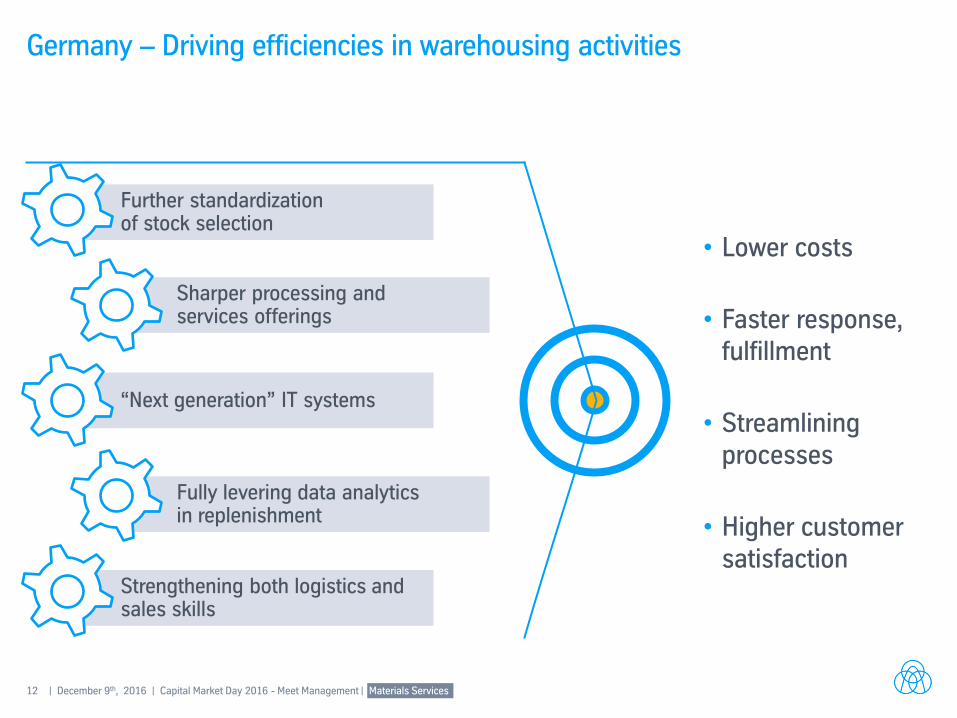

Further standardization of stock selection

Strengthening both logistics and sales skills

Germany – Driving efficiencies in warehousing activities

Sharper processing and services offerings

“Next generation” IT systems

Fully levering data analytics in replenishment

• Lower costs

• Faster response, fulfillment

• Streamlining processes

• Higher customer satisfaction

13 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

Value Added Services

Processing

14 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

Value Added Services Customized

Logistic concepts

Inventory management. Warehouse management. Supply chain management.

15 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

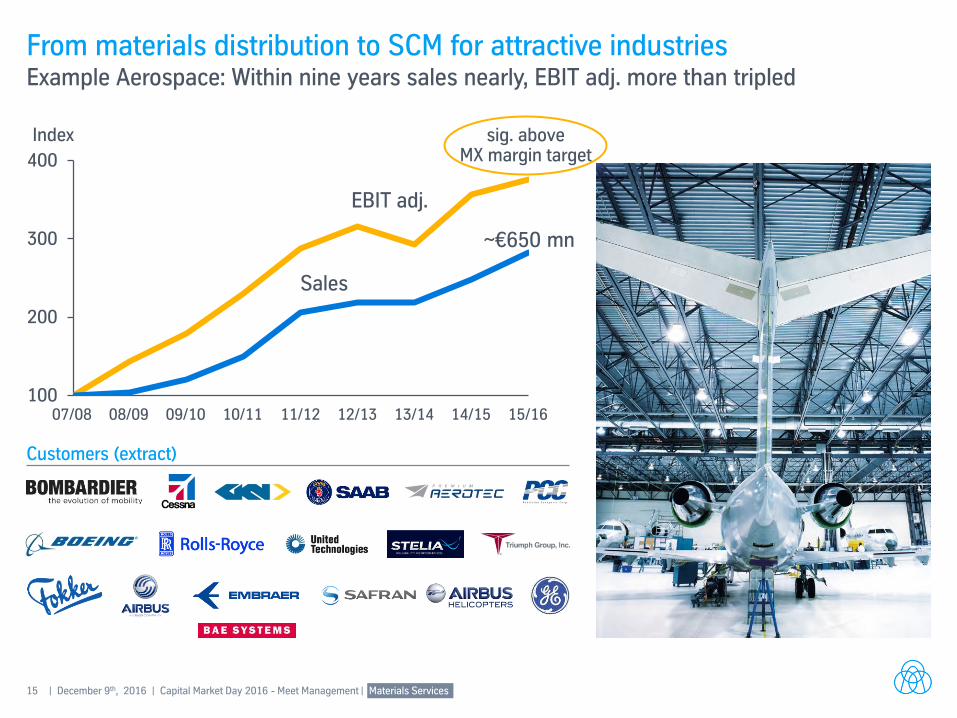

From materials distribution to SCM for attractive industries Example Aerospace: Within nine years sales nearly, EBIT adj. more than tripled

Customers (extract)

100

200

300

400

09/10 10/11 07/08 08/09 11/12 12/13 14/15 13/14 15/16

Index

Sales

EBIT adj.

~€650 mn

sig. above MX margin target

16 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

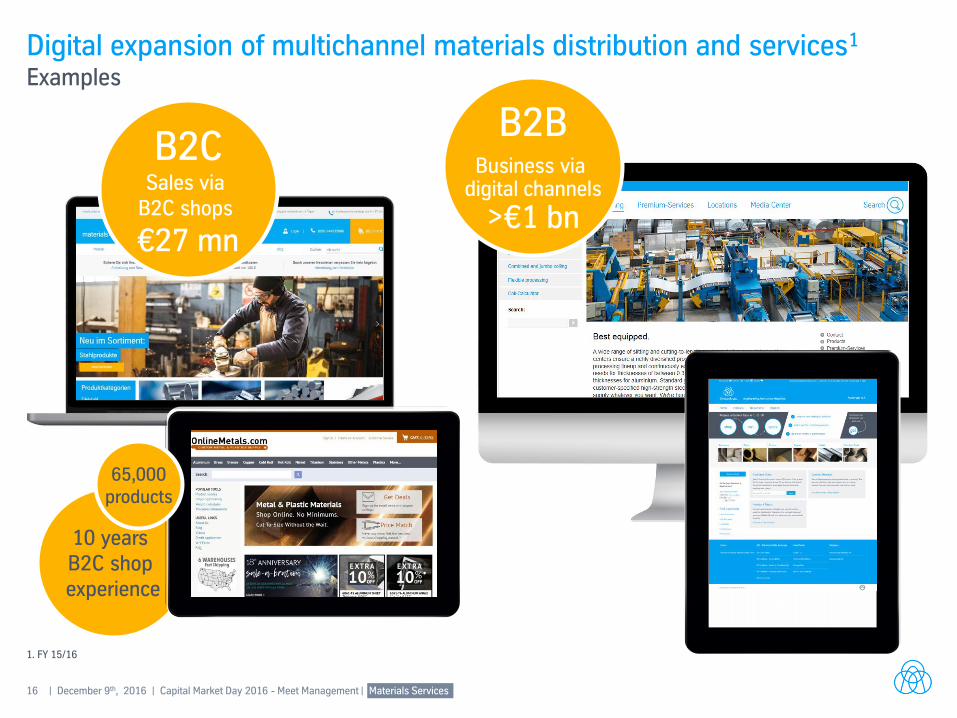

10 years B2C shop experience

Digital expansion of multichannel materials distribution and services1 Examples

B2B

Business via digital channels

>€1 bn

1. FY 15/16

B2C Sales via

B2C shops

€27 mn

65,000 products

17 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

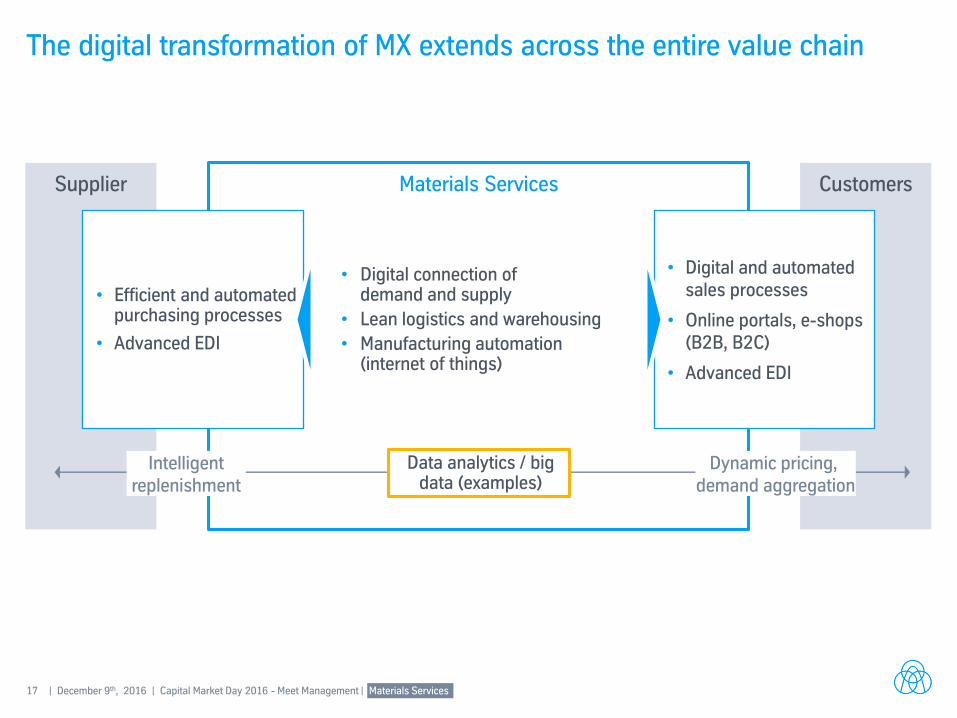

Materials Services

The digital transformation of MX extends across the entire value chain

• Digital connection of demand and supply

• Lean logistics and warehousing

• Manufacturing automation (internet of things)

Supplier Customers

Intelligent replenishment

Dynamic pricing, demand aggregation

Data analytics / big data (examples)

• Digital and automated sales processes

• Online portals, e-shops (B2B, B2C)

• Advanced EDI

• Efficient and automated purchasing processes

• Advanced EDI

18 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

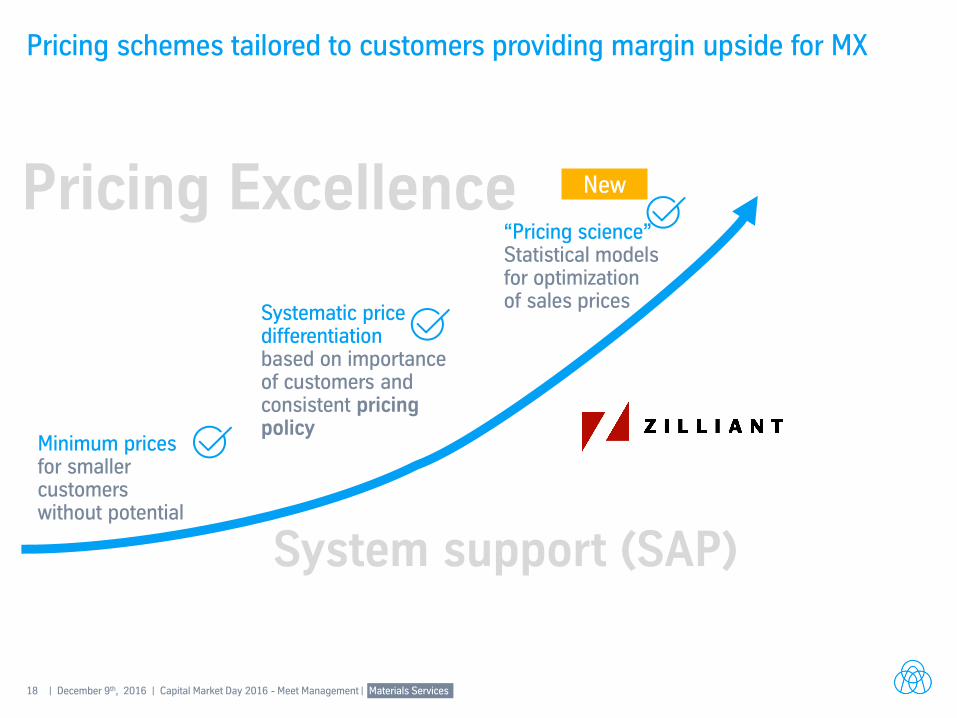

Pricing schemes tailored to customers providing margin upside for MX

New

Minimum prices for smaller customers without potential

Pricing Excellence “Pricing science” Statistical models for optimization of sales prices

System support (SAP)

Systematic price differentiation based on importance of customers and consistent pricing policy

19 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

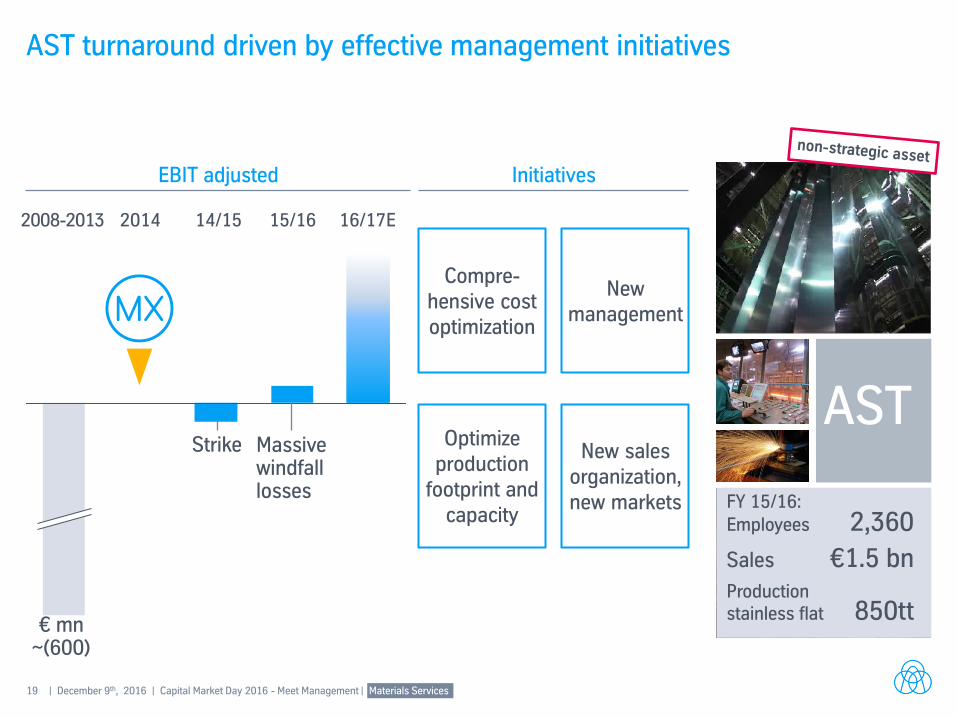

AST turnaround driven by effective management initiatives

2014 2008-2013 14/15 15/16 16/17E

Strike Massive windfall losses

€ mn ~(600)

Initiatives

Optimize production

footprint and capacity

New sales organization, new markets

Compre-hensive cost optimization

New management

AST

FY 15/16: Employees 2,360

Sales €1.5 bn Production stainless flat 850tt

EBIT adjusted

20 | December 9th, 2016 | Capital Market Day 2016 - Meet Management | Materials Services

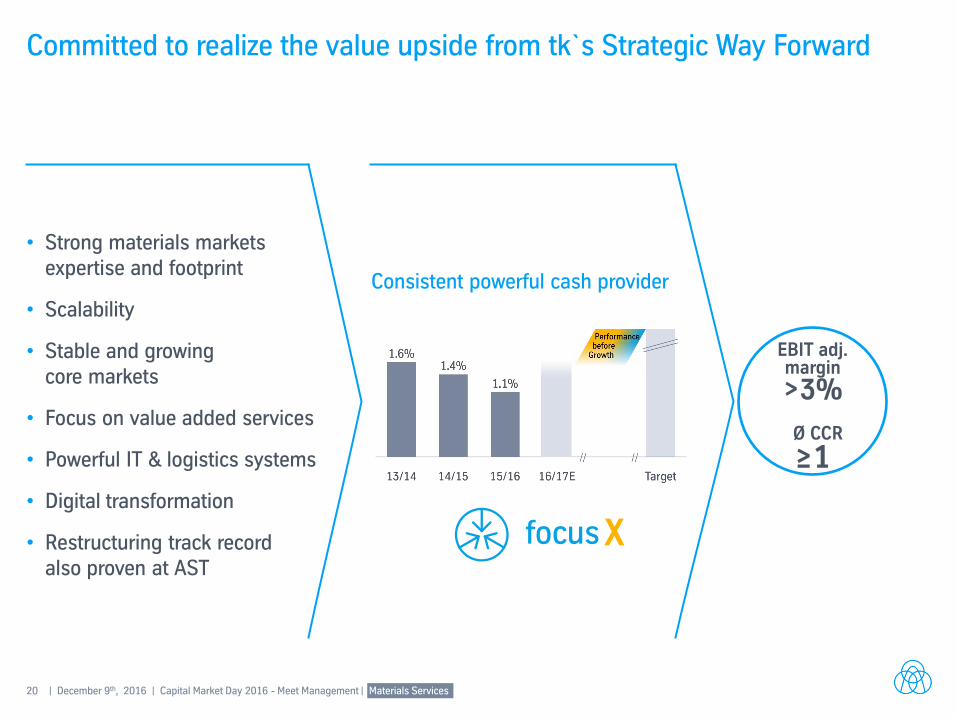

Committed to realize the value upside from tk`s Strategic Way Forward

• Strong materials markets expertise and footprint

• Scalability

• Stable and growing core markets

• Focus on value added services

• Powerful IT & logistics systems

• Digital transformation

• Restructuring track record also proven at AST

X

Consistent powerful cash provider

EBIT adj. margin

>3%

Ø CCR

≥1

Capital Market Day 2016 Meet Management

Capital Market Day 2016 – Meet Management

Steel Europe & Steel Americas Essen, December 9th, 2016 Andreas J. Goss (CEO) | Premal A. Desai (CFO)

2 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

thyssenkrupp – a diversified industrial group Sales €39.6 bn; EBIT adj. €1.5 bn

Components Technology (CT)

Materials Services (MX)

Financial figures FY 15/16

Steel Americas (AM)

€1.5 bn €(33) mn

Steel Europe (SE)

€7.6 bn €315 mn

€11.9 bn €128 mn

Elevator Technology (ET)

€7.5 bn €860 mn

€6.8 bn €335 mn

Industrial Solutions (IS)

€5.7 bn €355 mn

3 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

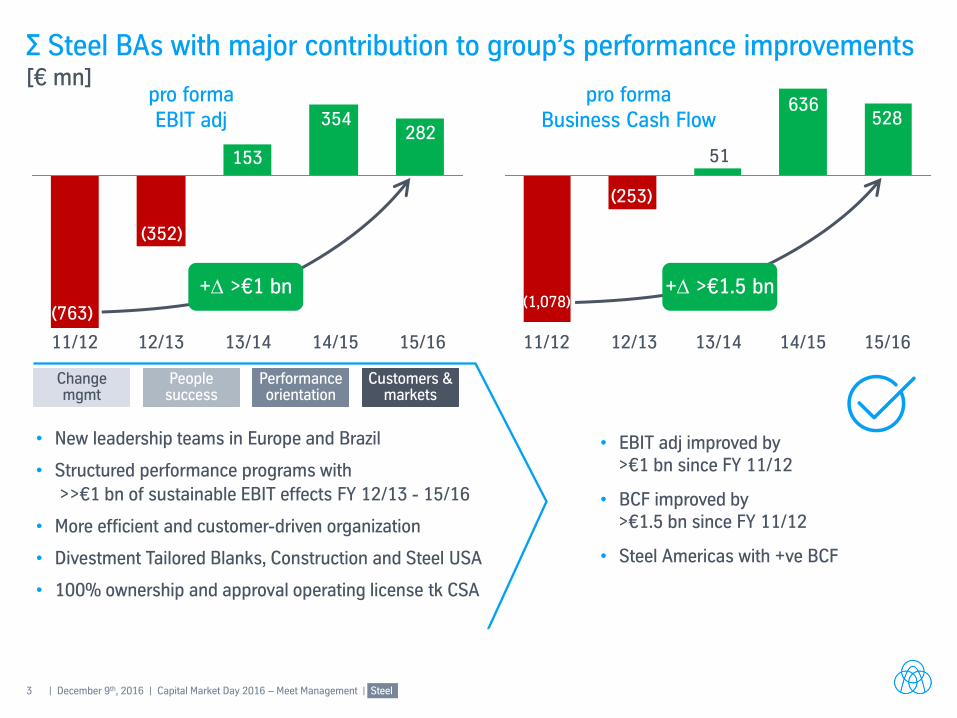

∑ Steel BAs with major contribution to group’s performance improvements [€ mn]

11/12 12/13 13/14 14/15

(763)

(352)

153

(1,078)

(253)

51

pro forma EBIT adj

pro forma Business Cash Flow 354

+ >€1 bn

636

Performance orientation

Customers & markets

People success

Change mgmt

• New leadership teams in Europe and Brazil

• Structured performance programs with

>>€1 bn of sustainable EBIT effects FY 12/13 - 15/16

• More efficient and customer-driven organization

• Divestment Tailored Blanks, Construction and Steel USA

• 100% ownership and approval operating license tk CSA

• EBIT adj improved by >€1 bn since FY 11/12

• BCF improved by >€1.5 bn since FY 11/12

• Steel Americas with +ve BCF

+ >€1.5 bn

15/16 11/12 12/13 13/14 14/15 15/16

282 528

4 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

Current focus on operating improvements in Brazil

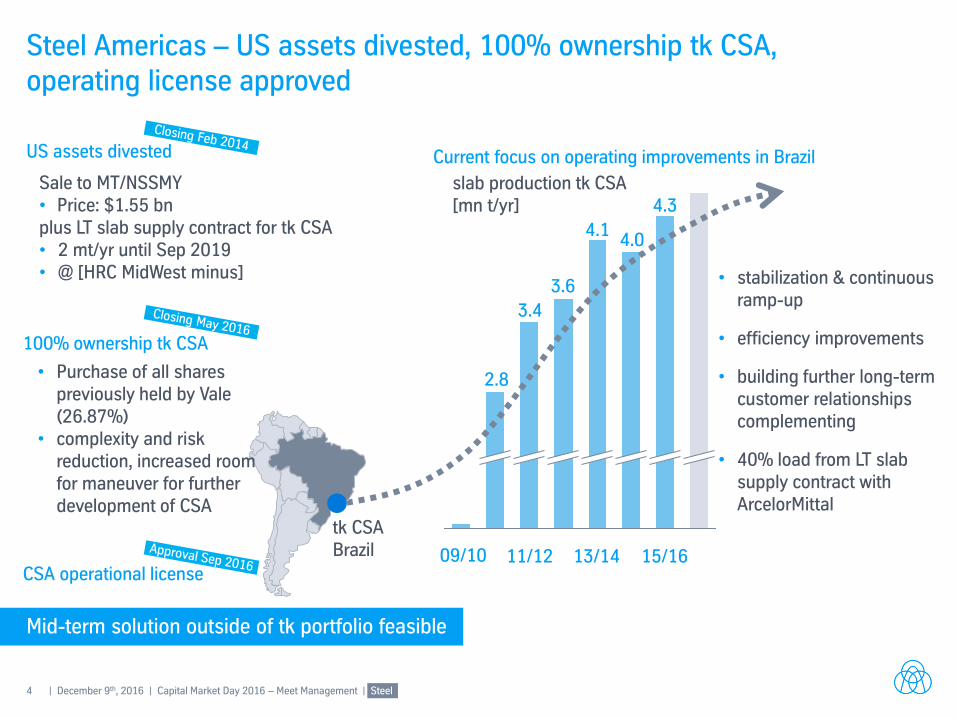

Steel Americas – US assets divested, 100% ownership tk CSA, operating license approved

US assets divested

tk CSA Brazil 13/14

3.6

11/12

3.4

2.8

slab production tk CSA [mn t/yr]

Sale to MT/NSSMY • Price: $1.55 bn plus LT slab supply contract for tk CSA • 2 mt/yr until Sep 2019 • @ [HRC MidWest minus] • stabilization & continuous

ramp-up

• efficiency improvements

• building further long-term customer relationships complementing

• 40% load from LT slab supply contract with ArcelorMittal

4.1

09/10

4.0

100% ownership tk CSA

• Purchase of all shares previously held by Vale (26.87%)

• complexity and risk reduction, increased room for maneuver for further development of CSA

15/16

4.3

Mid-term solution outside of tk portfolio feasible

CSA operational license

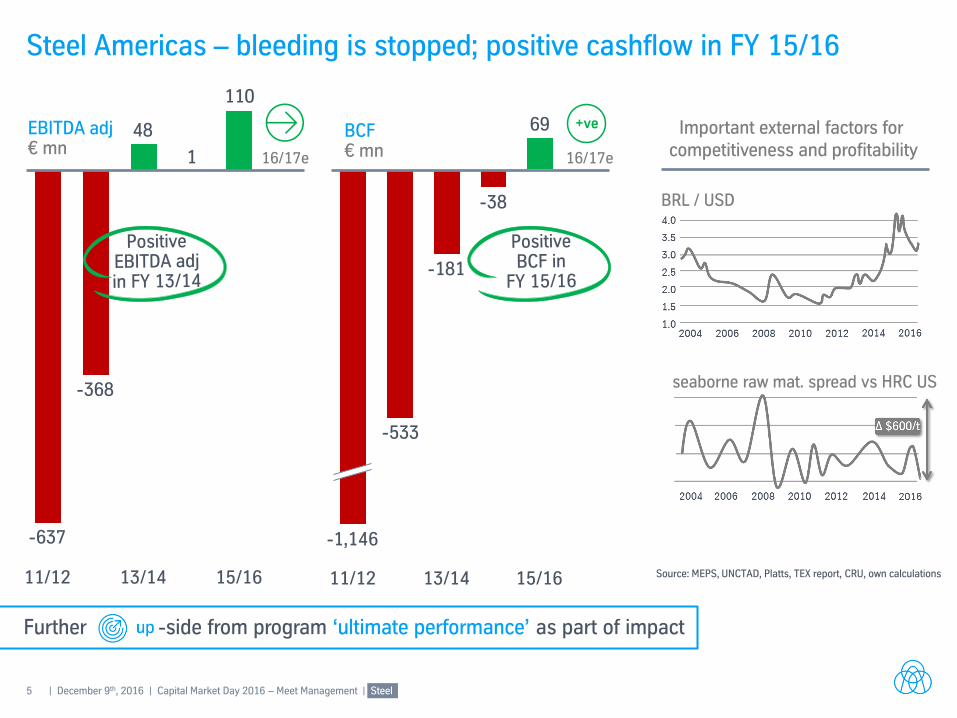

5 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

Further -side from program ‘ultimate performance’ as part of impact

69

-38

-181

-533

15/16 13/14 11/12

-1,146

Steel Americas – bleeding is stopped; positive cashflow in FY 15/16

110

1

48

-368

-637

15/16 13/14 11/12

BCF

€ mn

BRL / USD

seaborne raw mat. spread vs HRC US

Important external factors for competitiveness and profitability

Source: MEPS, UNCTAD, Platts, TEX report, CRU, own calculations

EBITDA adj € mn

16/17e 16/17e

+ve

6 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

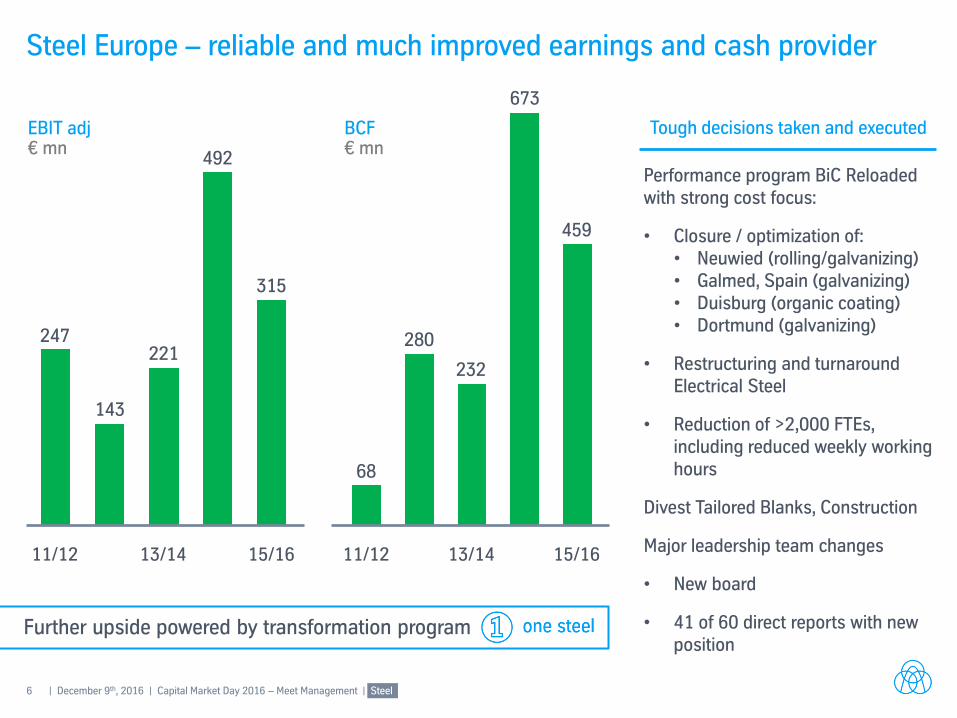

Steel Europe – reliable and much improved earnings and cash provider

315

492

221

143

247

13/14 11/12 15/16

459

673

232

280

68

11/12 13/14 15/16

Further upside powered by transformation program

Performance program BiC Reloaded with strong cost focus:

• Closure / optimization of: • Neuwied (rolling/galvanizing) • Galmed, Spain (galvanizing) • Duisburg (organic coating) • Dortmund (galvanizing)

• Restructuring and turnaround Electrical Steel

• Reduction of >2,000 FTEs, including reduced weekly working hours

Divest Tailored Blanks, Construction

Major leadership team changes

• New board

• 41 of 60 direct reports with new position

Tough decisions taken and executed BCF € mn

EBIT adj € mn

7 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

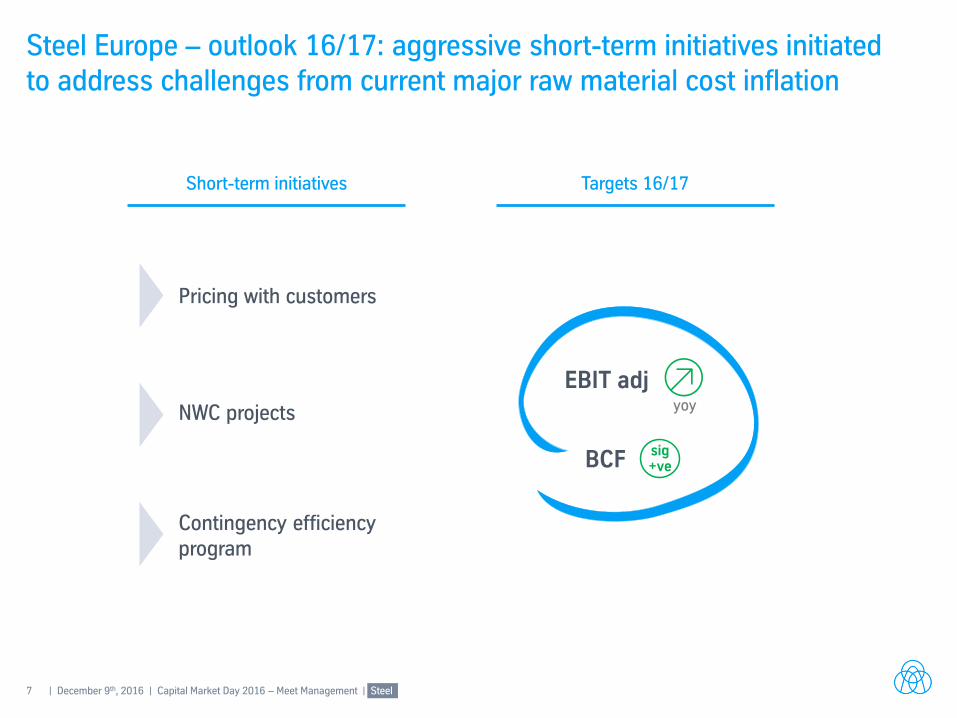

Steel Europe – outlook 16/17: aggressive short-term initiatives initiated to address challenges from current major raw material cost inflation

BCF

yoy

sig+ve

EBIT adj

Short-term initiatives Targets 16/17

Contingency efficiency program

NWC projects

Pricing with customers

8 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

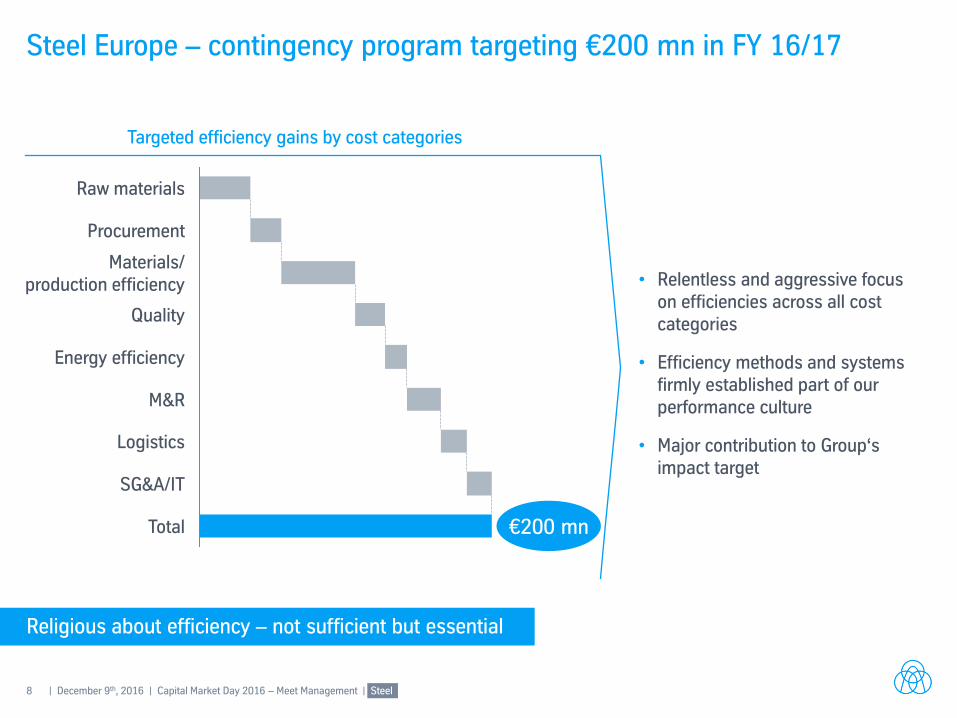

Religious about efficiency – not sufficient but essential

Steel Europe – contingency program targeting €200 mn in FY 16/17

Quality

Energy efficiency

Materials/ production efficiency

Procurement

Raw materials

M&R

Logistics

Total

SG&A/IT

€200 mn

• Relentless and aggressive focus on efficiencies across all cost categories

• Efficiency methods and systems firmly established part of our performance culture

• Major contribution to Group‘s impact target

Targeted efficiency gains by cost categories

9 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

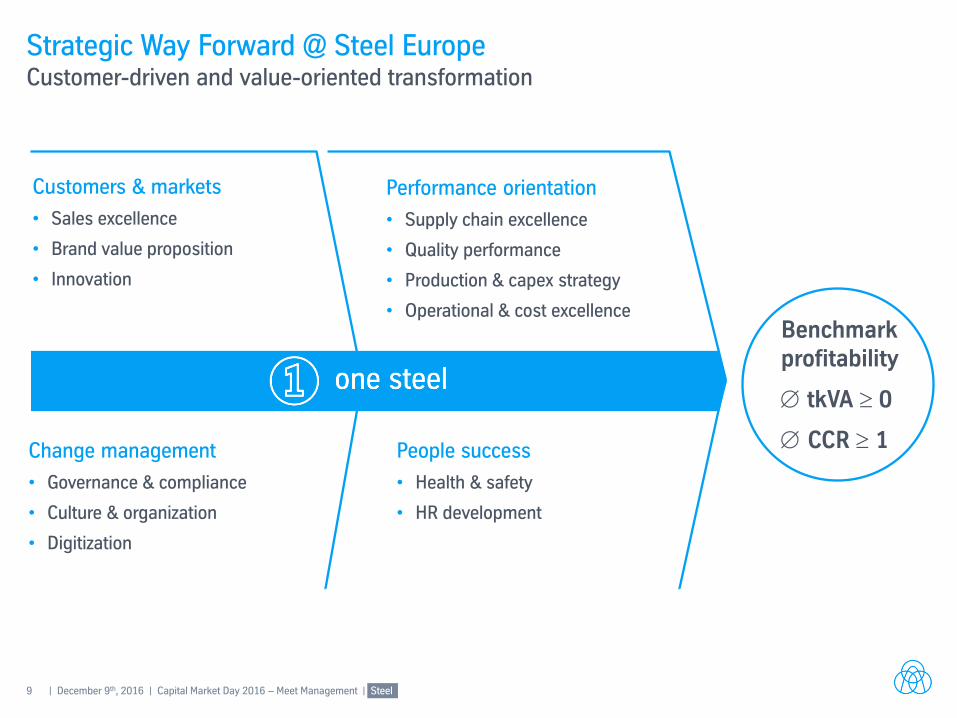

Strategic Way Forward @ Steel Europe Customer-driven and value-oriented transformation

Performance orientation

• Supply chain excellence

• Quality performance

• Production & capex strategy

• Operational & cost excellence

People success

• Health & safety

• HR development

Change management

• Governance & compliance

• Culture & organization

• Digitization

Customers & markets

• Sales excellence

• Brand value proposition

• Innovation

Benchmark profitability

tkVA 0

CCR 1

10 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

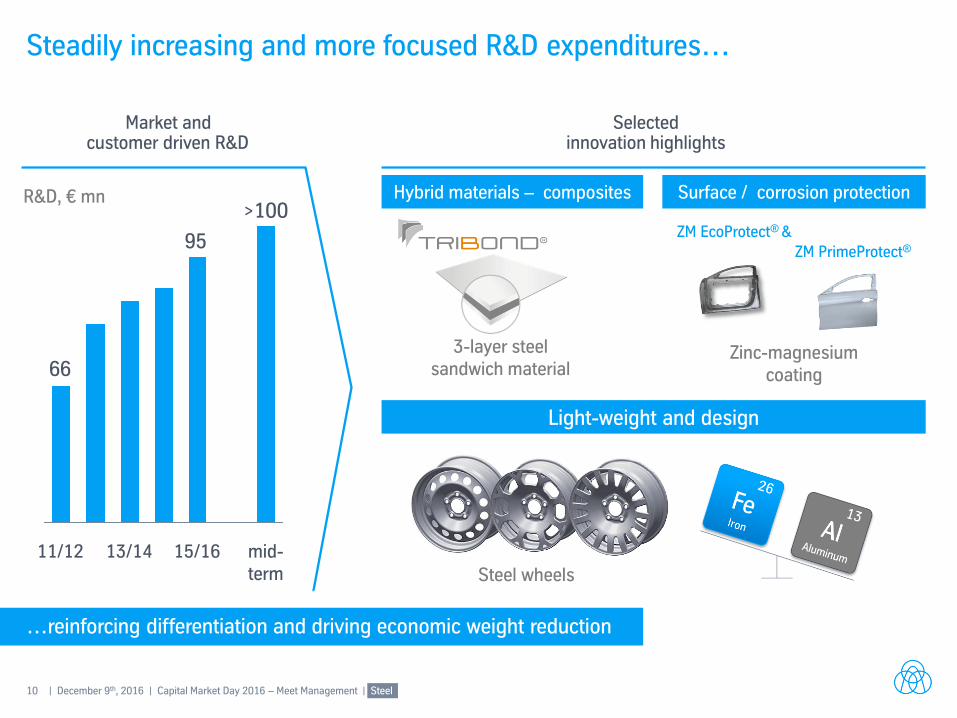

…reinforcing differentiation and driving economic weight reduction

Steadily increasing and more focused R&D expenditures…

Market and customer driven R&D

Selected innovation highlights

95

66

15/16 mid- term

>100

13/14 11/12

R&D, € mn Hybrid materials – composites

3-layer steel sandwich material

Surface / corrosion protection

ZM EcoProtect® &

Zinc-magnesium coating

ZM PrimeProtect®

Light-weight and design

Steel wheels

11 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

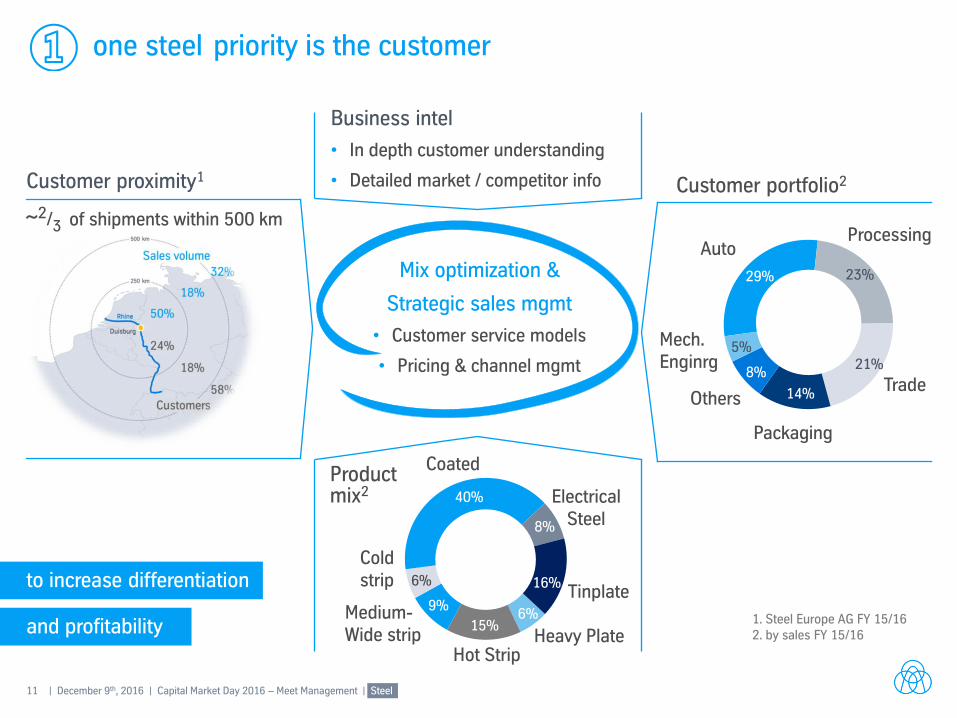

priority is the customer

Customer portfolio2 Customer proximity1

Product mix2

Business intel

• In depth customer understanding

• Detailed market / competitor info

Packaging

14% Others

8%

Mech. Enginrg

5%

Trade 21%

Processing

23%

Auto

29%

6%

8%

Heavy Plate Hot Strip

15%

Coated

40% Electrical Steel

16% Tinplate

Medium- Wide strip

Cold strip

9%

6%

Mix optimization &

Strategic sales mgmt

• Customer service models

• Pricing & channel mgmt

and profitability

to increase differentiation

1. Steel Europe AG FY 15/16 2. by sales FY 15/16

~2/3 of shipments within 500 km

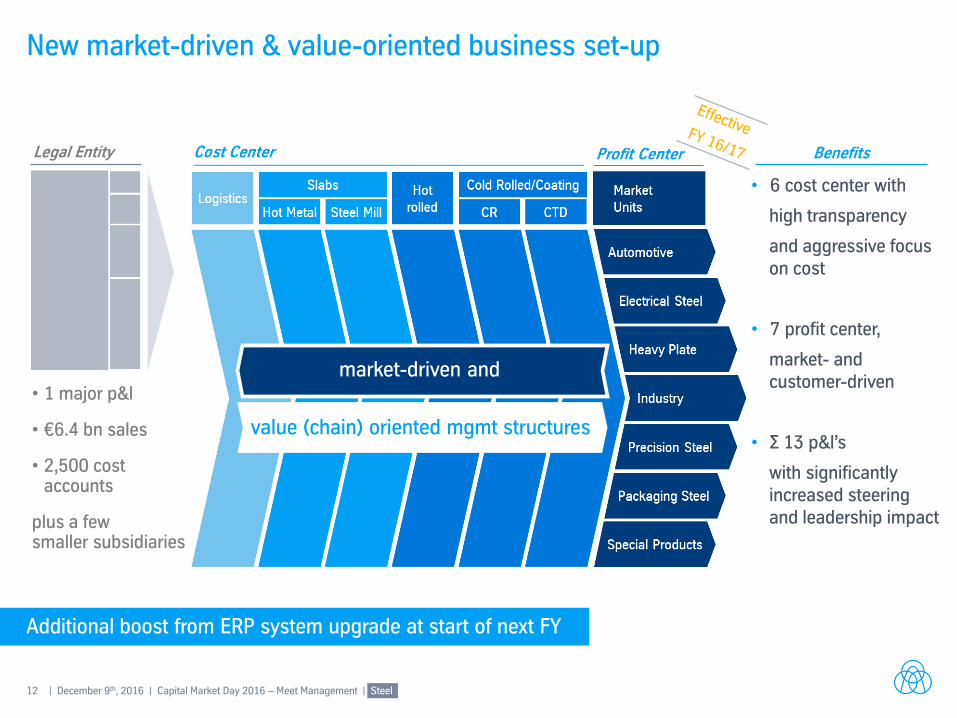

12 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

Additional boost from ERP system upgrade at start of next FY

New market-driven & value-oriented business set-up

• 1 major p&l

• €6.4 bn sales

• 2,500 cost accounts

plus a few smaller subsidiaries

Legal Entity

value (chain) oriented mgmt structures

market-driven and

• 6 cost center with

high transparency

and aggressive focus on cost

• 7 profit center,

market- and customer-driven

• ∑ 13 p&l’s

with significantly increased steering and leadership impact

Benefits

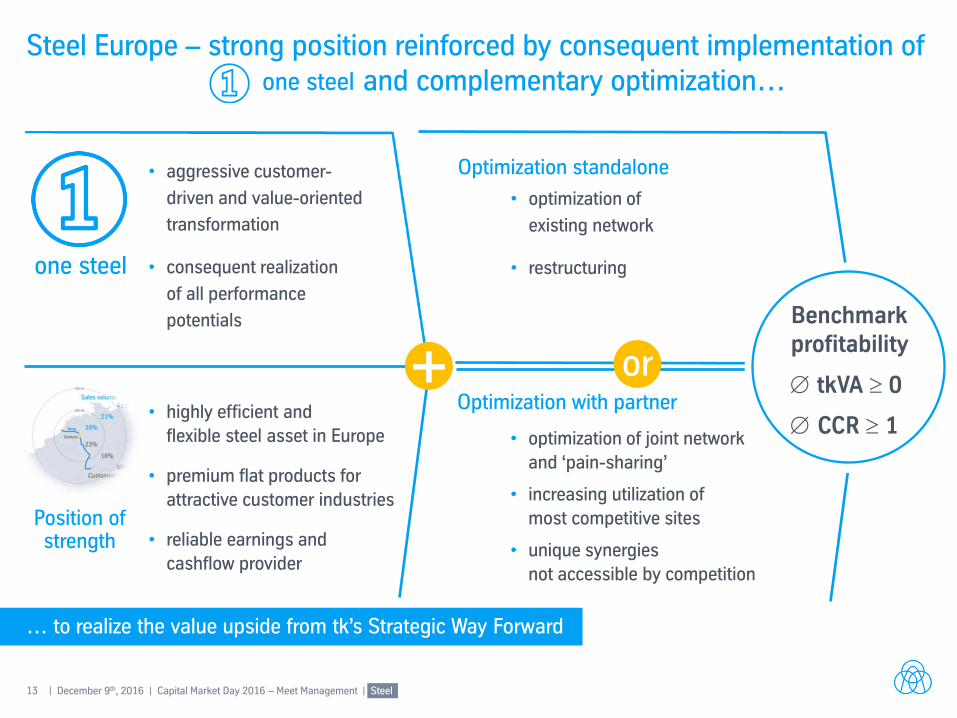

13 | December 9th, 2016 | Capital Market Day 2016 – Meet Management | Steel

• aggressive customer-

driven and value-oriented

transformation

• consequent realization

of all performance

potentials

Steel Europe – strong position reinforced by consequent implementation of and complementary optimization…

• highly efficient and

flexible steel asset in Europe

• premium flat products for

attractive customer industries

• reliable earnings and

cashflow provider

Position of strength

Optimization standalone

• optimization of

existing network

• restructuring

+ Optimization with partner

or

• optimization of joint network

and ‘pain-sharing’

• increasing utilization of

most competitive sites

• unique synergies

not accessible by competition

… to realize the value upside from tk’s Strategic Way Forward

Benchmark profitability

tkVA 0

CCR 1

15 | December 9th, 2016 | Capital Market Day 2016 – Meet Management

Disclaimer thyssenkrupp AG

“The information set forth and included in this presentation is not provided in connection with an offer or solicitation for the purchase or sale of a security and is intended for informational purposes only.

This presentation contains forward-looking statements that are subject to risks and uncertainties. Statements contained herein that are not statements of historical fact may be deemed to be forward-looking information. When we use words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “estimate,” “may” or similar expressions, we are making forward-looking statements. You should not rely on forward-looking statements because they are subject to a number of assumptions concerning future events, and are subject to a number of uncertainties and other factors, many of which are outside of our control, that could cause actual results to differ materially from those indicated. These factors include, but are not limited to, the following:

(i) market risks: principally economic price and volume developments,

(ii) dependence on performance of major customers and industries,

(iii) our level of debt, management of interest rate risk and hedging against commodity price risks;

(iv) costs associated with, and regulation relating to, our pension liabilities and healthcare measures,

(v) environmental protection and remediation of real estate and associated with rising standards for real estate environmental protection,

(vi) volatility of steel prices and dependence on the automotive industry,

(vii) availability of raw materials;

(viii) inflation, interest rate levels and fluctuations in exchange rates;

(ix) general economic, political and business conditions and existing and future governmental regulation; and

(x) the effects of competition.

Please note that we disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.”