Thursday, 04 August 2011 Asian Daily (Asia Edition)img.jrjimg.cn/2011/08/20110805133437402.pdf ·...

34

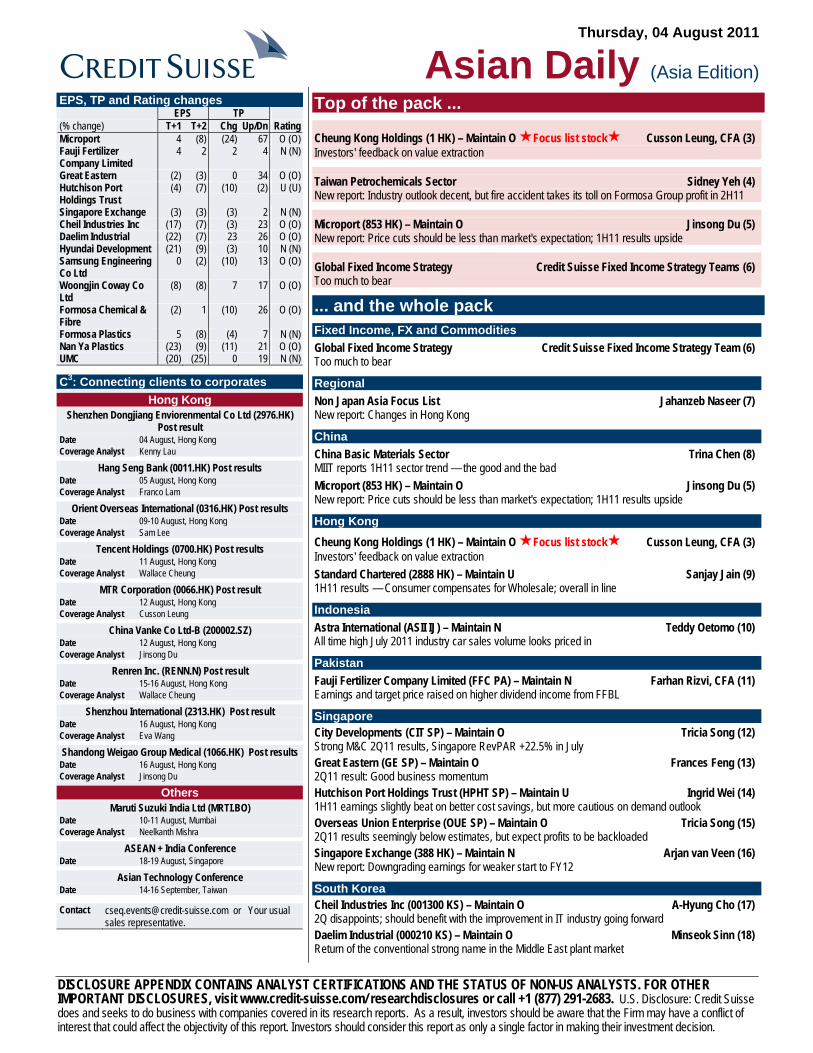

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Thursday, 04 August 2011 Asian Daily (Asia Edition) EPS, TP and Rating changes EPS TP (% change) T+1 T+2 Chg Up/Dn Rating Microport 4 (8) (24) 67 O (O) Fauji Fertilizer Company Limited 4 2 2 4 N (N) Great Eastern (2) (3) 0 34 O (O) Hutchison Port Holdings Trust (4) (7) (10) (2) U (U) Singapore Exchange (3) (3) (3) 2 N (N) Cheil Industries Inc (17) (7) (3) 23 O (O) Daelim Industrial (22) (7) 23 26 O (O) Hyundai Development (21) (9) (3) 10 N (N) Samsung Engineering Co Ltd 0 (2) (10) 13 O (O) Woongjin Coway Co Ltd (8) (8) 7 17 O (O) Formosa Chemical & Fibre (2) 1 (10) 26 O (O) Formosa Plastics 5 (8) (4) 7 N (N) Nan Ya Plastics (23) (9) (11) 21 O (O) UMC (20) (25) 0 19 N (N) C 3 : Connecting clients to corporates Hong Kong Shenzhen Dongjiang Enviorenmental Co Ltd (2976.HK) Post result Date 04 August, Hong Kong Coverage Analyst Kenny Lau Hang Seng Bank (0011.HK) Post results Date 05 August, Hong Kong Coverage Analyst Franco Lam Orient Overseas International (0316.HK) Post results Date 09-10 August, Hong Kong Coverage Analyst Sam Lee Tencent Holdings (0700.HK) Post results Date 11 August, Hong Kong Coverage Analyst Wallace Cheung MTR Corporation (0066.HK) Post result Date 12 August, Hong Kong Coverage Analyst Cusson Leung China Vanke Co Ltd-B (200002.SZ) Date 12 August, Hong Kong Coverage Analyst Jinsong Du Renren Inc. (RENN.N) Post result Date 15-16 August, Hong Kong Coverage Analyst Wallace Cheung Shenzhou International (2313.HK) Post result Date 16 August, Hong Kong Coverage Analyst Eva Wang Shandong Weigao Group Medical (1066.HK) Post results Date 16 August, Hong Kong Coverage Analyst Jinsong Du Others Maruti Suzuki India Ltd (MRTI.BO) Date 10-11 August, Mumbai Coverage Analyst Neelkanth Mishra ASEAN + India Conference Date 18-19 August, Singapore Asian Technology Conference Date 14-16 September, Taiwan Contact [email protected] or Your usual sales representative. Top of the pack ... Cheung Kong Holdings (1 HK) – Maintain O Focus list stock Cusson Leung, CFA (3) Investors' feedback on value extraction Taiwan Petrochemicals Sector Sidney Yeh (4) New report: Industry outlook decent, but fire accident takes its toll on Formosa Group profit in 2H11 Microport (853 HK) – Maintain O Jinsong Du (5) New report: Price cuts should be less than market's expectation; 1H11 results upside Global Fixed Income Strategy Credit Suisse Fixed Income Strategy Teams (6) Too much to bear ... and the whole pack Fixed Income, FX and Commodities Global Fixed Income Strategy Credit Suisse Fixed Income Strategy Team (6) Too much to bear Regional Non Japan Asia Focus List Jahanzeb Naseer (7) New report: Changes in Hong Kong China China Basic Materials Sector Trina Chen (8) MIIT reports 1H11 sector trend — the good and the bad Microport (853 HK) – Maintain O Jinsong Du (5) New report: Price cuts should be less than market's expectation; 1H11 results upside Hong Kong Cheung Kong Holdings (1 HK) – Maintain O Focus list stock Cusson Leung, CFA (3) Investors' feedback on value extraction Standard Chartered (2888 HK) – Maintain U Sanjay Jain (9) 1H11 results — Consumer compensates for Wholesale; overall in line Indonesia Astra International (ASII IJ) – Maintain N Teddy Oetomo (10) All time high July 2011 industry car sales volume looks priced in Pakistan Fauji Fertilizer Company Limited (FFC PA) – Maintain N Farhan Rizvi, CFA (11) Earnings and target price raised on higher dividend income from FFBL Singapore City Developments (CIT SP) – Maintain O Tricia Song (12) Strong M&C 2Q11 results, Singapore RevPAR +22.5% in July Great Eastern (GE SP) – Maintain O Frances Feng (13) 2Q11 result: Good business momentum Hutchison Port Holdings Trust (HPHT SP) – Maintain U Ingrid Wei (14) 1H11 earnings slightly beat on better cost savings, but more cautious on demand outlook Overseas Union Enterprise (OUE SP) – Maintain O Tricia Song (15) 2Q11 results seemingly below estimates, but expect profits to be backloaded Singapore Exchange (388 HK) – Maintain N Arjan van Veen (16) New report: Downgrading earnings for weaker start to FY12 South Korea Cheil Industries Inc (001300 KS) – Maintain O A-Hyung Cho (17) 2Q disappoints; should benefit with the improvement in IT industry going forward Daelim Industrial (000210 KS) – Maintain O Minseok Sinn (18) Return of the conventional strong name in the Middle East plant market

-

Upload

vuongthuan -

Category

Documents

-

view

212 -

download

0

Transcript of Thursday, 04 August 2011 Asian Daily (Asia Edition)img.jrjimg.cn/2011/08/20110805133437402.pdf ·...

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Thursday, 04 August 2011

Asian Daily (Asia Edition)EPS, TP and Rating changes EPS TP (% change) T+1 T+2 Chg Up/Dn Rating Microport 4 (8) (24) 67 O (O) Fauji Fertilizer Company Limited

4 2 2 4 N (N)

Great Eastern (2) (3) 0 34 O (O) Hutchison Port Holdings Trust

(4) (7) (10) (2) U (U)

Singapore Exchange (3) (3) (3) 2 N (N) Cheil Industries Inc (17) (7) (3) 23 O (O) Daelim Industrial (22) (7) 23 26 O (O) Hyundai Development (21) (9) (3) 10 N (N) Samsung Engineering Co Ltd

0 (2) (10) 13 O (O)

Woongjin Coway Co Ltd

(8) (8) 7 17 O (O)

Formosa Chemical & Fibre

(2) 1 (10) 26 O (O)

Formosa Plastics 5 (8) (4) 7 N (N) Nan Ya Plastics (23) (9) (11) 21 O (O) UMC (20) (25) 0 19 N (N)

C3: Connecting clients to corporates

Hong Kong Shenzhen Dongjiang Enviorenmental Co Ltd (2976.HK)

Post result Date 04 August, Hong Kong Coverage Analyst Kenny Lau

Hang Seng Bank (0011.HK) Post results Date 05 August, Hong Kong Coverage Analyst Franco Lam

Orient Overseas International (0316.HK) Post results Date 09-10 August, Hong Kong Coverage Analyst Sam Lee

Tencent Holdings (0700.HK) Post results Date 11 August, Hong Kong Coverage Analyst Wallace Cheung

MTR Corporation (0066.HK) Post result Date 12 August, Hong Kong Coverage Analyst Cusson Leung

China Vanke Co Ltd-B (200002.SZ) Date 12 August, Hong Kong Coverage Analyst Jinsong Du

Renren Inc. (RENN.N) Post result Date 15-16 August, Hong Kong Coverage Analyst Wallace Cheung

Shenzhou International (2313.HK) Post result Date 16 August, Hong Kong Coverage Analyst Eva Wang

Shandong Weigao Group Medical (1066.HK) Post results Date 16 August, Hong Kong Coverage Analyst Jinsong Du

Others Maruti Suzuki India Ltd (MRTI.BO)

Date 10-11 August, Mumbai Coverage Analyst Neelkanth Mishra

ASEAN + India Conference Date 18-19 August, Singapore

Asian Technology Conference Date 14-16 September, Taiwan

Contact [email protected] or Your usual sales representative.

Top of the pack ...

Cheung Kong Holdings (1 HK) – Maintain O Focus list stock Cusson Leung, CFA (3) Investors' feedback on value extraction

Taiwan Petrochemicals Sector Sidney Yeh (4) New report: Industry outlook decent, but fire accident takes its toll on Formosa Group profit in 2H11

Microport (853 HK) – Maintain O Jinsong Du (5) New report: Price cuts should be less than market's expectation; 1H11 results upside

Global Fixed Income Strategy Credit Suisse Fixed Income Strategy Teams (6) Too much to bear

... and the whole pack Fixed Income, FX and Commodities Global Fixed Income Strategy Credit Suisse Fixed Income Strategy Team (6) Too much to bear

Regional Non Japan Asia Focus List Jahanzeb Naseer (7) New report: Changes in Hong Kong

China China Basic Materials Sector Trina Chen (8) MIIT reports 1H11 sector trend — the good and the bad Microport (853 HK) – Maintain O Jinsong Du (5) New report: Price cuts should be less than market's expectation; 1H11 results upside

Hong Kong

Cheung Kong Holdings (1 HK) – Maintain O Focus list stock Cusson Leung, CFA (3) Investors' feedback on value extraction Standard Chartered (2888 HK) – Maintain U Sanjay Jain (9) 1H11 results — Consumer compensates for Wholesale; overall in line

Indonesia Astra International (ASII IJ) – Maintain N Teddy Oetomo (10) All time high July 2011 industry car sales volume looks priced in

Pakistan Fauji Fertilizer Company Limited (FFC PA) – Maintain N Farhan Rizvi, CFA (11) Earnings and target price raised on higher dividend income from FFBL

Singapore City Developments (CIT SP) – Maintain O Tricia Song (12) Strong M&C 2Q11 results, Singapore RevPAR +22.5% in July Great Eastern (GE SP) – Maintain O Frances Feng (13) 2Q11 result: Good business momentum Hutchison Port Holdings Trust (HPHT SP) – Maintain U Ingrid Wei (14) 1H11 earnings slightly beat on better cost savings, but more cautious on demand outlook Overseas Union Enterprise (OUE SP) – Maintain O Tricia Song (15) 2Q11 results seemingly below estimates, but expect profits to be backloaded Singapore Exchange (388 HK) – Maintain N Arjan van Veen (16) New report: Downgrading earnings for weaker start to FY12

South Korea Cheil Industries Inc (001300 KS) – Maintain O A-Hyung Cho (17) 2Q disappoints; should benefit with the improvement in IT industry going forward Daelim Industrial (000210 KS) – Maintain O Minseok Sinn (18) Return of the conventional strong name in the Middle East plant market

Thursday, 04 August 2011

Asian Daily

- 2 of 34 -

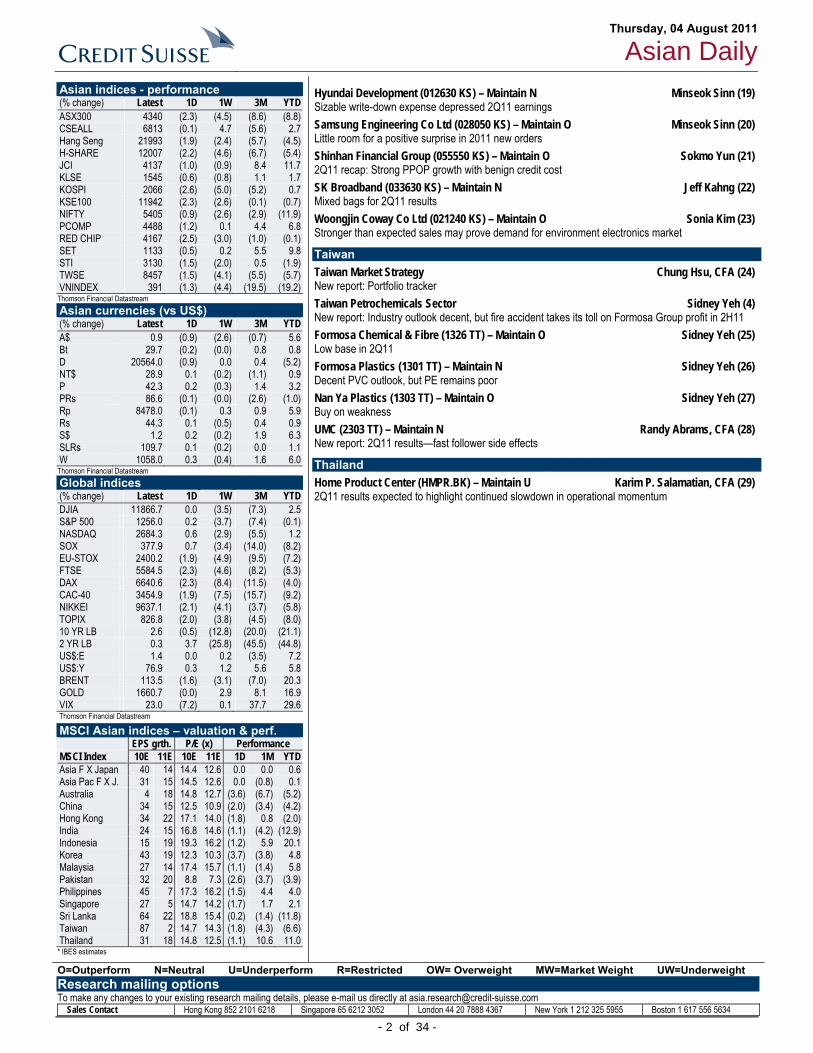

Asian indices - performance (% change) Latest 1D 1W 3M YTD ASX300 4340 (2.3) (4.5) (8.6) (8.8) CSEALL 6813 (0.1) 4.7 (5.6) 2.7 Hang Seng 21993 (1.9) (2.4) (5.7) (4.5) H-SHARE 12007 (2.2) (4.6) (6.7) (5.4) JCI 4137 (1.0) (0.9) 8.4 11.7 KLSE 1545 (0.6) (0.8) 1.1 1.7 KOSPI 2066 (2.6) (5.0) (5.2) 0.7 KSE100 11942 (2.3) (2.6) (0.1) (0.7) NIFTY 5405 (0.9) (2.6) (2.9) (11.9) PCOMP 4488 (1.2) 0.1 4.4 6.8 RED CHIP 4167 (2.5) (3.0) (1.0) (0.1) SET 1133 (0.5) 0.2 5.5 9.8 STI 3130 (1.5) (2.0) 0.5 (1.9) TWSE 8457 (1.5) (4.1) (5.5) (5.7) VNINDEX 391 (1.3) (4.4) (19.5) (19.2)

Thomson Financial Datastream Asian currencies (vs US$) (% change) Latest 1D 1W 3M YTD A$ 0.9 (0.9) (2.6) (0.7) 5.6 Bt 29.7 (0.2) (0.0) 0.8 0.8 D 20564.0 (0.9) 0.0 0.4 (5.2) NT$ 28.9 0.1 (0.2) (1.1) 0.9 P 42.3 0.2 (0.3) 1.4 3.2 PRs 86.6 (0.1) (0.0) (2.6) (1.0) Rp 8478.0 (0.1) 0.3 0.9 5.9 Rs 44.3 0.1 (0.5) 0.4 0.9 S$ 1.2 0.2 (0.2) 1.9 6.3 SLRs 109.7 0.1 (0.2) 0.0 1.1 W 1058.0 0.3 (0.4) 1.6 6.0

Thomson Financial Datastream Global indices (% change) Latest 1D 1W 3M YTD DJIA 11866.7 0.0 (3.5) (7.3) 2.5 S&P 500 1256.0 0.2 (3.7) (7.4) (0.1) NASDAQ 2684.3 0.6 (2.9) (5.5) 1.2 SOX 377.9 0.7 (3.4) (14.0) (8.2) EU-STOX 2400.2 (1.9) (4.9) (9.5) (7.2) FTSE 5584.5 (2.3) (4.6) (8.2) (5.3) DAX 6640.6 (2.3) (8.4) (11.5) (4.0) CAC-40 3454.9 (1.9) (7.5) (15.7) (9.2) NIKKEI 9637.1 (2.1) (4.1) (3.7) (5.8) TOPIX 826.8 (2.0) (3.8) (4.5) (8.0) 10 YR LB 2.6 (0.5) (12.8) (20.0) (21.1) 2 YR LB 0.3 3.7 (25.8) (45.5) (44.8) US$:E 1.4 0.0 0.2 (3.5) 7.2 US$:Y 76.9 0.3 1.2 5.6 5.8 BRENT 113.5 (1.6) (3.1) (7.0) 20.3 GOLD 1660.7 (0.0) 2.9 8.1 16.9 VIX 23.0 (7.2) 0.1 37.7 29.6

Thomson Financial Datastream

MSCI Asian indices – valuation & perf. EPS grth. P/E (x) Performance MSCI Index 10E 11E 10E 11E 1D 1M YTD Asia F X Japan 40 14 14.4 12.6 0.0 0.0 0.6 Asia Pac F X J. 31 15 14.5 12.6 0.0 (0.8) 0.1 Australia 4 18 14.8 12.7 (3.6) (6.7) (5.2) China 34 15 12.5 10.9 (2.0) (3.4) (4.2) Hong Kong 34 22 17.1 14.0 (1.8) 0.8 (2.0) India 24 15 16.8 14.6 (1.1) (4.2) (12.9) Indonesia 15 19 19.3 16.2 (1.2) 5.9 20.1 Korea 43 19 12.3 10.3 (3.7) (3.8) 4.8 Malaysia 27 14 17.4 15.7 (1.1) (1.4) 5.8 Pakistan 32 20 8.8 7.3 (2.6) (3.7) (3.9) Philippines 45 7 17.3 16.2 (1.5) 4.4 4.0 Singapore 27 5 14.7 14.2 (1.7) 1.7 2.1 Sri Lanka 64 22 18.8 15.4 (0.2) (1.4) (11.8) Taiwan 87 2 14.7 14.3 (1.8) (4.3) (6.6) Thailand 31 18 14.8 12.5 (1.1) 10.6 11.0

* IBES estimates

Hyundai Development (012630 KS) – Maintain N Minseok Sinn (19) Sizable write-down expense depressed 2Q11 earnings Samsung Engineering Co Ltd (028050 KS) – Maintain O Minseok Sinn (20) Little room for a positive surprise in 2011 new orders Shinhan Financial Group (055550 KS) – Maintain O Sokmo Yun (21) 2Q11 recap: Strong PPOP growth with benign credit cost SK Broadband (033630 KS) – Maintain N Jeff Kahng (22) Mixed bags for 2Q11 results Woongjin Coway Co Ltd (021240 KS) – Maintain O Sonia Kim (23) Stronger than expected sales may prove demand for environment electronics market

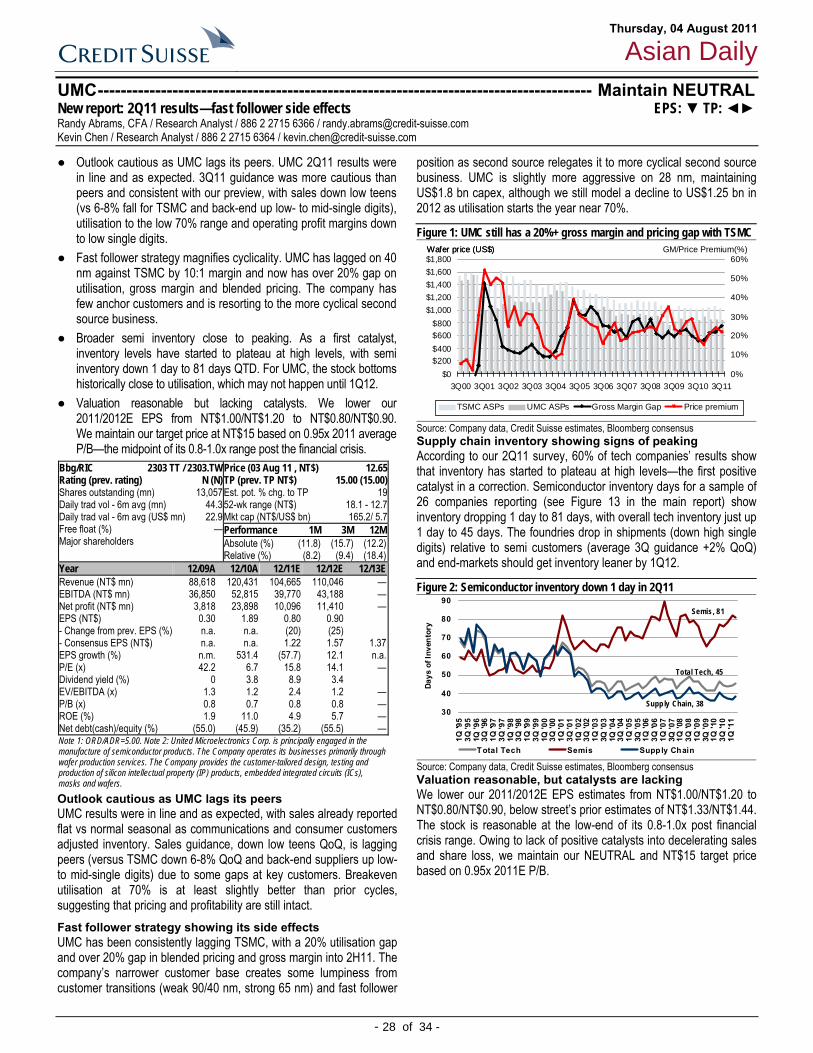

Taiwan Taiwan Market Strategy Chung Hsu, CFA (24) New report: Portfolio tracker Taiwan Petrochemicals Sector Sidney Yeh (4) New report: Industry outlook decent, but fire accident takes its toll on Formosa Group profit in 2H11 Formosa Chemical & Fibre (1326 TT) – Maintain O Sidney Yeh (25) Low base in 2Q11 Formosa Plastics (1301 TT) – Maintain N Sidney Yeh (26) Decent PVC outlook, but PE remains poor Nan Ya Plastics (1303 TT) – Maintain O Sidney Yeh (27) Buy on weakness UMC (2303 TT) – Maintain N Randy Abrams, CFA (28) New report: 2Q11 results—fast follower side effects

Thailand Home Product Center (HMPR.BK) – Maintain U Karim P. Salamatian, CFA (29) 2Q11 results expected to highlight continued slowdown in operational momentum

O=Outperform N=Neutral U=Underperform R=Restricted OW= Overweight MW=Market Weight UW=Underweight Research mailing options To make any changes to your existing research mailing details, please e-mail us directly at [email protected]

Sales Contact Hong Kong 852 2101 6218 Singapore 65 6212 3052 London 44 20 7888 4367 New York 1 212 325 5955 Boston 1 617 556 5634

Thursday, 04 August 2011

Asian Daily

- 3 of 34 -

Top of the pack ... Cheung Kong Holdings ---------------------------------------------------- Maintain OUTPERFORM Investors' feedback on value extraction EPS: ◄► TP: ◄► Cusson Leung, CFA / Research Analyst / 852 2101 6621 / [email protected] Joyce Kwock / Research Analyst / 852 2101 7496 / [email protected]

● Most investors believe our CK restructuring is interesting but there are also some push-backs, with the property sector risk being the key one. However, we believe CK’s willingness to sell help it generate constant cashflow even in a difficult market.

● The rise in the accounting gearing may not be a real issue if Cheung Kong does not want further acquisitions or capex spends for expansion. The rise in accounting gearing is an inconvenient hurdle for its expansion in the future, in our view.

● The restructuring exercise is our logical deduction to help extract the hidden value within the group. While timing appears far fetched, we believe CK’s deep discount and the ‘possibility’ of it happening will already be enough to narrow the discount.

● Specifically for the idea of distributing Hutch In Specie, how to tackle the dilution in KS Li’s stake in Hutch? Buy back from the market is one way. CK can sell assets to Hutch for new stock but we believe Husky Energy could also be sold by KS Li to Hutch for new stock, which will likely help boost his stake immediately.

● Cheung Kong Holdings is a Credit Suisse NJA Focus List stock.

General feedback on our Cheung Kong call

Following the issuance of our note on Cheung Kong, Value transformer dated 2 August 2011, and our day-long discussion with investors, we are summarising some key feedback. Although most clients are positive on either Cheung Kong or Hutch, the major push-backs are summarised below: Macro risks is rising, not the right time to long beta A major concern about our positive call on Cheung Kong is from the general lack of risk appetite. Cheung Kong, being partially a Hong Kong property company, is also facing the potential downside risks of the local property market.

CS view: While there is concern about the property market, Cheung Kong is the one name always willing to move its inventory whether it is in an up/down market largely due to its landbank size and the relatively low development costs. The fact that the company has already made HK$14 bn of sales revenue so far demonstrates its ability to generate cashflow in a difficult property market. Potential rise in consolidated gearing is not a major issue An argument we highlight in the report as a catalyst for restructuring is the potential rise in Cheung Kong’s gearing due to the change in accounting rules. However, most clients believe the gearing increase would not impact Cheung Kong at all as these are mainly Hutch borrowings.

CS view: The rise in the proforma gearing is not an issue to Cheung Kong if the company does not want to spend capex on expanding itself in the future. Once the company start spending capex or making acquisitions, the proforma gearing will not be at our projected level. The acquisition of the water business in the UK was a case in point. To avoid this, we believe the overall direction of the group is to first deleverage as mush as it can. The idea is speculative and the timing is highly uncertain The restructuring exercise has not been confirmed by the company and the timing of this happening can actually be very sketchy. Why should the discount narrow now?

CS view: The restructuring exercise is our logical deduction with the assumed objectives of removing the holding company discount and potential excessive gearing. The most important point of the call is that the valuation of Cheung Kong is cheap to an extent that it warrants this sort of restructuring exercise to extract hidden value. With this valuation backdrop, followed by the market starting to realise there are actually ways to extract this value, the discounts will unwind faster than the market can expect. The major shareholder will not likely want to do this Specifically referring to the scenario of distributing Hutch In Specie to Cheung Kong shareholders, some investors believe the heavy dilution of KS Li’s stake in Hutch to only 24% will make the distribution near impossible.

CS view: The distribution will not happen on its own but together with the potential purchase of shares from KS Li or from the market in both companies. Besides this, to alleviate the pressure of buy from the market, Cheung Kong can sell assets to Hutch for a stake. KS Li can also sell some assets to Hutch in exchange for shares. For example, KS Li holds a 34% share in Husky Energy while Hutch holds 32%. We believe there could be a possibility of KS Li selling his stake in Husky Energy to Hutch for shares that result in an immediate boost to his holdings in Hutch.

Price (03 Aug 11, HK$) 119.70TP (prev. TP HK$) 151.90 (151.90) Est. pot. % chg. to TP 2752-wk range (HK$) 135.4 - 96.6Mkt cap (HK$/US$ bn) 277.2/ 35.6

Bbg/RIC 1 HK / 0001.HK Rating (prev. rating) O (O) Shares outstanding (mn) 2,316.16 Daily trad vol - 6m avg (mn) 4.2 Daily trad val - 6m avg (US$ mn) 64.9 Free float (%) — Major shareholders

Performance 1M 3M 12MAbsolute (%) 3.2 0.7 23.8Relative (%) 6.6 6.1 21.4

Year 12/09A 12/10A 12/11E 12/12E 12/13EEBITDA (HK$ mn) 19,553 23,119 48,263 34,842 33,153Net profit (HK$ mn) 19,886 26,478 45,898 29,445 28,204EPS (HK$) 8.6 11.4 19.8 12.7 12.2- Change from prev. EPS (%) n.a. n.a. 0 0 0- Consensus EPS (HK$) n.a. n.a. 17.9 10.1 12.2EPS growth (%) 28.1 33.1 73.3 (35.8) (4.2)P/E (x) 13.9 10.5 6.0 9.4 9.8Dividend yield (%) 2.3 2.5 2.5 2.5 2.5EV/EBITDA (x) 15.4 12.5 6.0 8.1 8.3ROE (%) 8.5 10.4 16.1 9.3 8.3Net debt(cash)/equity (%) 9.3 4.5 3.3 1.7 (0.2)NAV per share (HK$) — — 164 — —Disc./prem. to NAV (%) — — (27.0) — — Note 1: ORD/ADR=1.00. Note 2: Cheung Kong (Holdings) Limited is a Hong Kong-based company engaged in investment holding and project management activities. The company’s subsidiaries are engaged in property development and investment, hotel and serviced suite operation, property and project management and investment in securities.

Thursday, 04 August 2011

Asian Daily

- 4 of 34 -

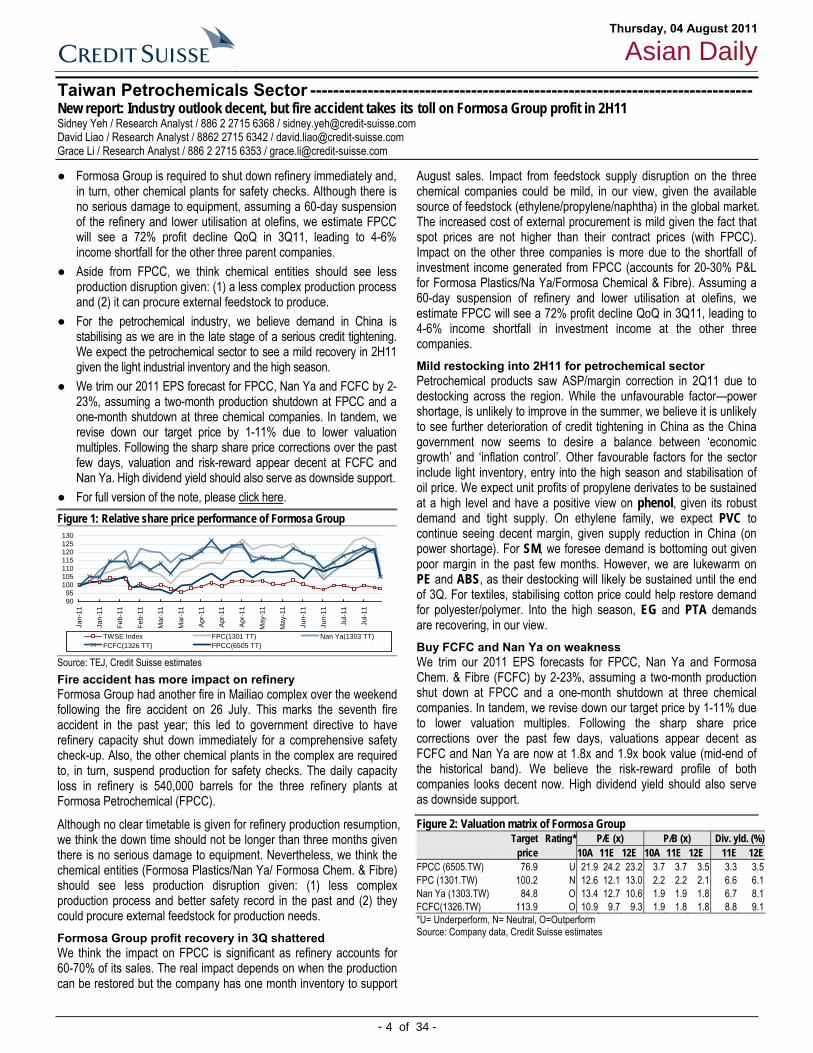

Taiwan Petrochemicals Sector ----------------------------------------------------------------------------- New report: Industry outlook decent, but fire accident takes its toll on Formosa Group profit in 2H11 Sidney Yeh / Research Analyst / 886 2 2715 6368 / [email protected] David Liao / Research Analyst / 8862 2715 6342 / [email protected] Grace Li / Research Analyst / 886 2 2715 6353 / [email protected]

● Formosa Group is required to shut down refinery immediately and, in turn, other chemical plants for safety checks. Although there is no serious damage to equipment, assuming a 60-day suspension of the refinery and lower utilisation at olefins, we estimate FPCC will see a 72% profit decline QoQ in 3Q11, leading to 4-6% income shortfall for the other three parent companies.

● Aside from FPCC, we think chemical entities should see less production disruption given: (1) a less complex production process and (2) it can procure external feedstock to produce.

● For the petrochemical industry, we believe demand in China is stabilising as we are in the late stage of a serious credit tightening. We expect the petrochemical sector to see a mild recovery in 2H11 given the light industrial inventory and the high season.

● We trim our 2011 EPS forecast for FPCC, Nan Ya and FCFC by 2-23%, assuming a two-month production shutdown at FPCC and a one-month shutdown at three chemical companies. In tandem, we revise down our target price by 1-11% due to lower valuation multiples. Following the sharp share price corrections over the past few days, valuation and risk-reward appear decent at FCFC and Nan Ya. High dividend yield should also serve as downside support.

● For full version of the note, please click here. Figure 1: Relative share price performance of Formosa Group

9095

100105110115120125130

Jan-

11

Jan-

11

Feb-

11

Feb-

11

Mar

-11

Mar

-11

Apr-1

1

Apr-1

1

Apr-1

1

May

-11

May

-11

Jun-

11

Jun-

11

Jul-1

1

Jul-1

1

TWSE Index FPC(1301 TT) Nan Ya(1303 TT)FCFC(1326 TT) FPCC(6505 TT)

Source: TEJ, Credit Suisse estimates Fire accident has more impact on refinery Formosa Group had another fire in Mailiao complex over the weekend following the fire accident on 26 July. This marks the seventh fire accident in the past year; this led to government directive to have refinery capacity shut down immediately for a comprehensive safety check-up. Also, the other chemical plants in the complex are required to, in turn, suspend production for safety checks. The daily capacity loss in refinery is 540,000 barrels for the three refinery plants at Formosa Petrochemical (FPCC).

Although no clear timetable is given for refinery production resumption, we think the down time should not be longer than three months given there is no serious damage to equipment. Nevertheless, we think the chemical entities (Formosa Plastics/Nan Ya/ Formosa Chem. & Fibre) should see less production disruption given: (1) less complex production process and better safety record in the past and (2) they could procure external feedstock for production needs. Formosa Group profit recovery in 3Q shattered We think the impact on FPCC is significant as refinery accounts for 60-70% of its sales. The real impact depends on when the production can be restored but the company has one month inventory to support

August sales. Impact from feedstock supply disruption on the three chemical companies could be mild, in our view, given the available source of feedstock (ethylene/propylene/naphtha) in the global market. The increased cost of external procurement is mild given the fact that spot prices are not higher than their contract prices (with FPCC). Impact on the other three companies is more due to the shortfall of investment income generated from FPCC (accounts for 20-30% P&L for Formosa Plastics/Na Ya/Formosa Chemical & Fibre). Assuming a 60-day suspension of refinery and lower utilisation at olefins, we estimate FPCC will see a 72% profit decline QoQ in 3Q11, leading to 4-6% income shortfall in investment income at the other three companies. Mild restocking into 2H11 for petrochemical sector Petrochemical products saw ASP/margin correction in 2Q11 due to destocking across the region. While the unfavourable factor—power shortage, is unlikely to improve in the summer, we believe it is unlikely to see further deterioration of credit tightening in China as the China government now seems to desire a balance between ‘economic growth’ and ‘inflation control’. Other favourable factors for the sector include light inventory, entry into the high season and stabilisation of oil price. We expect unit profits of propylene derivates to be sustained at a high level and have a positive view on phenol, given its robust demand and tight supply. On ethylene family, we expect PVC to continue seeing decent margin, given supply reduction in China (on power shortage). For SM, we foresee demand is bottoming out given poor margin in the past few months. However, we are lukewarm on PE and ABS, as their destocking will likely be sustained until the end of 3Q. For textiles, stabilising cotton price could help restore demand for polyester/polymer. Into the high season, EG and PTA demands are recovering, in our view. Buy FCFC and Nan Ya on weakness We trim our 2011 EPS forecasts for FPCC, Nan Ya and Formosa Chem. & Fibre (FCFC) by 2-23%, assuming a two-month production shut down at FPCC and a one-month shutdown at three chemical companies. In tandem, we revise down our target price by 1-11% due to lower valuation multiples. Following the sharp share price corrections over the past few days, valuations appear decent as FCFC and Nan Ya are now at 1.8x and 1.9x book value (mid-end of the historical band). We believe the risk-reward profile of both companies looks decent now. High dividend yield should also serve as downside support.

Figure 2: Valuation matrix of Formosa Group Target Rating* P/E (x) P/B (x) Div. yld. (%) price 10A 11E 12E 10A 11E 12E 11E 12EFPCC (6505.TW) 76.9 U 21.9 24.2 23.2 3.7 3.7 3.5 3.3 3.5FPC (1301.TW) 100.2 N 12.6 12.1 13.0 2.2 2.2 2.1 6.6 6.1Nan Ya (1303.TW) 84.8 O 13.4 12.7 10.6 1.9 1.9 1.8 6.7 8.1FCFC(1326.TW) 113.9 O 10.9 9.7 9.3 1.9 1.8 1.8 8.8 9.1*U= Underperform, N= Neutral, O=Outperform Source: Company data, Credit Suisse estimates

Thursday, 04 August 2011

Asian Daily

- 5 of 34 -

Microport------------------------------------------------------------------------ Maintain OUTPERFORM New report: Price cuts should be less than market's expectation; 1H11 results upside EPS: ▼ TP: ▼ Jinsong Du / Research Analyst / 852 2101 6589 / [email protected] Lefei Sun / Research Analyst / 852 2101 7658 / [email protected] Duo Chen / Research Analyst / 852 2101 7350 / [email protected]

● Microport’s share price has fallen 46% YTD, underperforming the MSCI China and Healthcare indices by 44% and 26%, respectively, due to concerns about the potential price cut in drug eluting stents. Click here for our full report.

● Talks with government officials and industry experts suggest that Beijing may announce a price cut of 15-20% in the next few months, much less than the 30-40% being discussed in the market. Although this is higher than our original assumption of a 10% cut, we expect Microport to reduce the impact by negotiating with distributors and bundling the sale of PCI surgery accessories under government’s pilot for disease-related-group initiatives.

● Moreover, Microport recently made a breakthrough in product diversification by receiving a major order of US$3 mn from Turkey for its in-house orthopaedics products in July 2011.

● We increase our 2011E EPS by 4%, but reduce our 2012E and 2013E EPS due to the delayed but more significant price cut. We continue to expect Microport’s 1H11 results to beat consensus. We maintain OUTPERFORM.

What’s the price-cut level for upcoming tendering?

The last centralised drug eluting stent procurement was in 2008, and usually the industry expectation for annual ASP erosion from the tendering price-cut is about 5-8%. Given the three-year compounded impact, the market fears that price cut in the upcoming tendering will be relatively significant, at 30-40%, while we consider 15-20% as a more reasonable range given the three-year compounded impact. Even if the tendering kicks off in 2H 2011, the real impact would most likely be booked in 2012, and not in 2011. We believe Microport’s 2011 results could outperform expectations, but may be under pressure in 2012.

Scenario analysis for price cut impact on Microport ● Base case scenario: Since volume growth for the industry is over

25% across different players, we conservatively assume that volume growth is 25% and that ASP erosion will be shared by both the manufacturer and distributor by best efforts negotiations. Further, the company could offer longer credit terms for distributors in exchange for sharing the price-cut impact.

● Worst case scenario: Even if we assume that the company takes no action for price-cut and bears the whole 20% ASP erosion, since the volume growth would be over 25% and the company has more room to improve operating margin, the bottom line could still grow slightly in 2012.

● Best case scenario: The company is working on other ways to digest the potential price-cut impact. For example, it is considering to offer bundled sale with PCI surgery accessories by partnering with overseas strategic players. Since the government is also encouraging disease-related-group reimbursement schemes in developed regions such as Beijing and Shanghai, hospitals would increasingly encourage suppliers for one-stop shop offerings targeting certain disease procedures such as PCI surgery. Limited qualified local players can supply PCI surgery accessories in China and as the market leader, Microport can bundle purchase accessories with strategic overseas partners at higher discount and sell to distributors and hospitals in exchange for better DES prices, leveraging its No.1 market share position and high turnover volume. In this scenario, the overall growth volume can also get a boost, given the higher potential market share gain and limited price-cut impact as distributors will share more burden.

Figure 1: Scenario analysis for price cut impact on Microport 2012 Worst case Base case Best case DES price cut -20% -15% -10% DES volume growth 25% 25% 30% DES sales growth 0% 6% 17% Total sales growth ~5% ~10% ~20% Total profit growth >5% >10% >20% Comments Company takes no

actions and fully absorbs price-cut impact

Negotiates with distributors to split the impact

Bundles sale of PCI surgery accessories with strategic partners to digest price-cut impact

Source: Company data, Credit Suisse estimates Potential upside from business diversification Microport is also actively looking for opportunities to diversify its business to derisk the concentration of drug eluting stents. It has increasingly been making progress: in July 2011, it confirmed the first overseas order (US$3 mn) from Turkey for its in-house developed orthopaedics products, which successfully got CE marks at end of last year. Although this is still marginal contribution, the company is moving towards more diversifications. More in-house products are also being developed, covering orthopaedics, electrophysiology and interventional cardiovascular devices markets. It is also actively looking for merger and acquisition opportunities in high potential areas such as orthopaedics. Potential upside could arise in 2H 2011 or 2012 if the diversification strategy progresses smoothly.

Price (03 Aug 11 , HK$) 4.01TP (prev. TP HK$) 6.70 (8.80) Est. pot. % chg. to TP 6752-wk range (HK$) 8.86 - 4.01Mkt cap (HK$/US$ mn) 5,784.7/ 741.9

Bbg/RIC 853 HK / 0853.HK Rating (prev. rating) O (O) [V] Shares outstanding (mn) 1,442.57 Daily trad vol - 6m avg (mn) 2.2 Daily trad val - 6m avg (US$ mn) 1.6 Free float (%) — Major shareholders

Performance 1M 3M 12MAbsolute (%) (23.2) (28.5) —Relative (%) (17.8) (23.4) —

Year 12/09A 12/10A 12/11E 12/12E 12/13ERevenue (Rmb mn) 561 728 865 947 1,129EBITDA (Rmb mn) 286.6 312.9 401.4 467.9 565.8Net profit (Rmb mn) 186.4 240.1 309.4 354.0 431.6EPS (Rmb) 0.16 0.20 0.21 0.25 0.30- Change from prev. EPS (%) n.a. n.a. 4 (8) (6)- Consensus EPS (Rmb) n.a. n.a. 0.21 0.26 0.32EPS growth (%) 3.2 20.3 9.2 14.4 21.9P/E (x) 20.3 16.9 15.4 13.5 11.1Dividend yield (%) 0 0 0 0 0EV/EBITDA (x) 16.4 12.5 8.8 7.2 5.1P/B (x) 9.7 2.0 — — —ROE (%) 46.9 20.4 14.1 13.6 14.2Net debt(cash)/equity (%) (22.1) (44.3) (50.8) (49.7) (57.4) Note 1: MicroPort Scientific Corporation, along with its subsidiaries, is engaged in the manufacturing and distribution of medical devices in the People’s Republic of China (the PRC). It is a developer, manufacturer and marketer of medical devices, focusing primarily on minimally invasive interventional products for the treatment of vascular diseases and disorder.

Thursday, 04 August 2011

Asian Daily

- 6 of 34 -

Global Fixed Income Strategy Too much to bear Credit Suisse Fixed Income Strategy Teams

● This week’s intensification of doubts about European and global growth was the straw to break the camel’s back: while a short and temporary period in which Italian yields trade above 6% is not necessarily fatal, interest costs would spiral unsustainably if that lasts for long.

● This is Europe’s Minsky moment: the point where problems in funding the ‘sub-prime’ sovereigns and their banks have finally infected the ability to fund prime borrowers. Unless this vicious circle dynamic can be broken, we stand on the brink of another Lehmans like shock – and ultimately not just to European growth but to global growth too.

● All of a sudden, therefore, global equity markets have started to trade like 2008 again. And global risk appetite has lurched down into panic.

● Panic episodes can be very short or quite extended, but most of the time global equity markets are much nearer the end of their sell-off than the beginning. The clear exception to that rule came after the failure of Lehmans! click here for the full report.

Figure 1: Global risk appetite panic episodes—entry to trough

Source: Credit Suisse, the BLOOMBERG PROFESSIONAL™ service, Thomson Reuters Datastream

Ultimately, market pressures are likely to force an overwhelming policy response. But while we are waiting, the likelihood is that we will see different varieties of bullish flattening in the US, Germany and Japan, downward pressure on growth sensitive commodities and most global equity markets, combined with upward pressure on gold and perhaps the dollar more generally. Emerging markets: All about growth – and the lack of it While most of the negative headline news on growth in recent months has focused on the US, the EM economies have not been immune to the downdraft in global growth. Sequential industrial output growth in the EM world fell abruptly in 2Q of the current year. It seems now to have stabilized in China but the PMI data point to additional weakness in most of the rest of the EM world.

EM asset prices have been helped by the resilience of global commodity prices. But this resilience will be tested over the coming month. Commodity prices are drawing support primarily from signs of a moderate growth rebound in China (a key commodities importer) and the possibility that the Fed may respond to the growth weakness

with a new round of quantitative easing. But there is probably predominantly downside risk to commodity prices in the coming weeks and months if the global growth data are representative of the commodities demand trends.

Figure 2: EM outperformance in recent weeks more clearly evident in theequity markets than in the credit markets

Source: The BLOOMBERG PROFESSIONAL™ service, Credit Suisse

The weakening of the global growth data would probably – as long as it does not lead to a complete meltdown of credit in the European periphery and attendant blind asset dumping – support strength (against the dollar) of currencies in EM countries with low sovereign credit spreads. It would also, in part because of the currency strength and because of the weakening of the EM growth outlook, support a decline in EM local currency yields in the same countries. The main underlying investor theme would be one of ‘wanting to shed dollar holdings’ (on account of weak growth and the possibility of further Fed monetary policy loosening) and not wanting to be exposed to the euro zone given that zone’s sovereign liquidity/solvency problems. On the rates side, EM five-year swaps rates have in most cases fallen much less significantly in recent months than have five-year US swaps rates, and it is not clear to us why EM rates should outperform US rates in the coming months.

(This is an extract from the Strategy Snapshot report, Too Much To Bear, published on 3 August 2011. For details, please see the CS Research & Analytics website.) THE FOLLOWING REPORT(S) HAVE BEEN PREPARED BY THE FIXED INCOME DIVISION OF CREDIT SUISSE. ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES ARE IN THE DISCLOSURE APPENDIX. FOR OTHER IMPORTANT DISCLOSURES, PLEASE REFER TO https://firesearchdisclosure.credit-suisse.com.

Thursday, 04 August 2011

Asian Daily

- 7 of 34 -

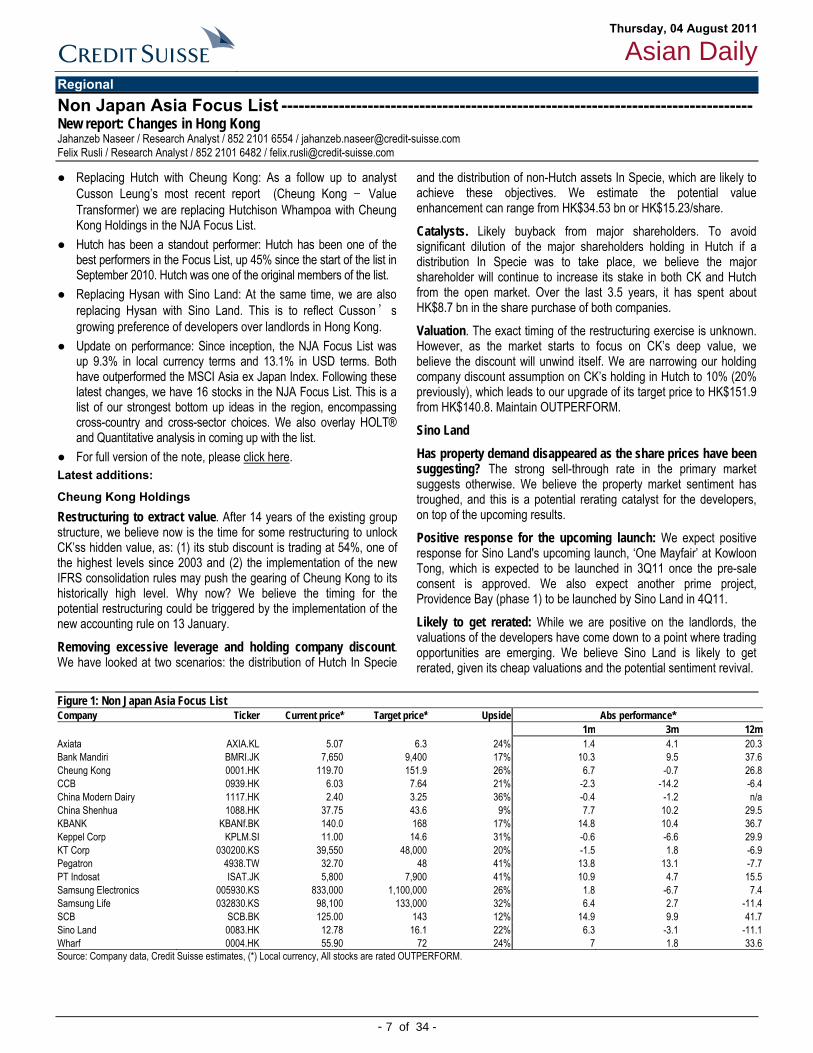

Regional Non Japan Asia Focus List ---------------------------------------------------------------------------------- New report: Changes in Hong Kong Jahanzeb Naseer / Research Analyst / 852 2101 6554 / [email protected] Felix Rusli / Research Analyst / 852 2101 6482 / [email protected]

● Replacing Hutch with Cheung Kong: As a follow up to analyst Cusson Leung’s most recent report (Cheung Kong – Value Transformer) we are replacing Hutchison Whampoa with Cheung Kong Holdings in the NJA Focus List.

● Hutch has been a standout performer: Hutch has been one of the best performers in the Focus List, up 45% since the start of the list in September 2010. Hutch was one of the original members of the list.

● Replacing Hysan with Sino Land: At the same time, we are also replacing Hysan with Sino Land. This is to reflect Cusson’s growing preference of developers over landlords in Hong Kong.

● Update on performance: Since inception, the NJA Focus List was up 9.3% in local currency terms and 13.1% in USD terms. Both have outperformed the MSCI Asia ex Japan Index. Following these latest changes, we have 16 stocks in the NJA Focus List. This is a list of our strongest bottom up ideas in the region, encompassing cross-country and cross-sector choices. We also overlay HOLT® and Quantitative analysis in coming up with the list.

● For full version of the note, please click here. Latest additions:

Cheung Kong Holdings Restructuring to extract value. After 14 years of the existing group structure, we believe now is the time for some restructuring to unlock CK’ss hidden value, as: (1) its stub discount is trading at 54%, one of the highest levels since 2003 and (2) the implementation of the new IFRS consolidation rules may push the gearing of Cheung Kong to its historically high level. Why now? We believe the timing for the potential restructuring could be triggered by the implementation of the new accounting rule on 13 January.

Removing excessive leverage and holding company discount. We have looked at two scenarios: the distribution of Hutch In Specie

and the distribution of non-Hutch assets In Specie, which are likely to achieve these objectives. We estimate the potential value enhancement can range from HK$34.53 bn or HK$15.23/share.

Catalysts. Likely buyback from major shareholders. To avoid significant dilution of the major shareholders holding in Hutch if a distribution In Specie was to take place, we believe the major shareholder will continue to increase its stake in both CK and Hutch from the open market. Over the last 3.5 years, it has spent about HK$8.7 bn in the share purchase of both companies.

Valuation. The exact timing of the restructuring exercise is unknown. However, as the market starts to focus on CK’s deep value, we believe the discount will unwind itself. We are narrowing our holding company discount assumption on CK’s holding in Hutch to 10% (20% previously), which leads to our upgrade of its target price to HK$151.9 from HK$140.8. Maintain OUTPERFORM.

Sino Land Has property demand disappeared as the share prices have been suggesting? The strong sell-through rate in the primary market suggests otherwise. We believe the property market sentiment has troughed, and this is a potential rerating catalyst for the developers, on top of the upcoming results.

Positive response for the upcoming launch: We expect positive response for Sino Land's upcoming launch, ‘One Mayfair’ at Kowloon Tong, which is expected to be launched in 3Q11 once the pre-sale consent is approved. We also expect another prime project, Providence Bay (phase 1) to be launched by Sino Land in 4Q11.

Likely to get rerated: While we are positive on the landlords, the valuations of the developers have come down to a point where trading opportunities are emerging. We believe Sino Land is likely to get rerated, given its cheap valuations and the potential sentiment revival.

Figure 1: Non Japan Asia Focus List Company Ticker Current price* Target price* Upside Abs performance* 1m 3m 12mAxiata AXIA.KL 5.07 6.3 24% 1.4 4.1 20.3Bank Mandiri BMRI.JK 7,650 9,400 17% 10.3 9.5 37.6Cheung Kong 0001.HK 119.70 151.9 26% 6.7 -0.7 26.8CCB 0939.HK 6.03 7.64 21% -2.3 -14.2 -6.4China Modern Dairy 1117.HK 2.40 3.25 36% -0.4 -1.2 n/aChina Shenhua 1088.HK 37.75 43.6 9% 7.7 10.2 29.5KBANK KBANf.BK 140.0 168 17% 14.8 10.4 36.7Keppel Corp KPLM.SI 11.00 14.6 31% -0.6 -6.6 29.9KT Corp 030200.KS 39,550 48,000 20% -1.5 1.8 -6.9Pegatron 4938.TW 32.70 48 41% 13.8 13.1 -7.7PT Indosat ISAT.JK 5,800 7,900 41% 10.9 4.7 15.5Samsung Electronics 005930.KS 833,000 1,100,000 26% 1.8 -6.7 7.4Samsung Life 032830.KS 98,100 133,000 32% 6.4 2.7 -11.4SCB SCB.BK 125.00 143 12% 14.9 9.9 41.7Sino Land 0083.HK 12.78 16.1 22% 6.3 -3.1 -11.1Wharf 0004.HK 55.90 72 24% 7 1.8 33.6Source: Company data, Credit Suisse estimates, (*) Local currency, All stocks are rated OUTPERFORM.

Thursday, 04 August 2011

Asian Daily

- 8 of 34 -

China China Basic Materials Sector ------------------------------------------------------------------------------- MIIT reports 1H11 sector trend — the good and the bad Trina Chen / Research Analyst / 852 2101 7031 / [email protected] Frankie Zhu / Research Analyst / 852 2101 7426 / [email protected]

● MIIT issued 1H11 sector operations for cement, aluminium and steel sectors, including sector profit and investment capex trend.

● The report suggests industry profit surged 170% in cement, declined by 24% for Al and 1% for steel, mostly in line with our expectation. The numbers suggest (1) implied profit of cement is at Rmb47/t, about Rmb30/t higher YoY, (2) stagnant margin in Al at US$0.02/lb as cost pressure couples with higher aluminium price and (3) depressed unit EBITDA of US$40-50/t in steel.

● For 2H11, MIIT highlighted (1) supply pressure emerging for cement sector in western China, (2) potentially improving pricing and margin for 2H11 in Al as a result of government constrain on new lines and (3) persistent low margin to stay for steel sector. While industry capex declined by 15% for cement and picked up for Al and steel, we believe implied new capacity remains high for cement and Al, when taking the base in 2010 into consideration.

● We maintain our view that soften demand may lead to extended trough for steel and Al in 2H, and increasing in favor of cement names with strong M&A story such as CR cement and Shanshui. given the stable margin outlook in 2012E.

Figure 1: Summary of valuation peers – China basic materials Company Ticker Ratings Target Upside Price Mkt cap P/E (x) P/B (x) EV/EBITDA(updated on 8/3/11) % Tccy US$ bn 11E 12E 11E 12E 11E 12EShenhua 1088.HK O 43.6 15% 37.8 96.3 13 11 2.7 2.3 6.9 5.2Chinacoal 1898.HK O 12.7 19% 10.6 18.1 12 9 1.4 1.3 6.9 5.8Yanzhou 1171.HK N 30.0 3% 29.2 18.4 12 11 2.7 2.3 6.9 6.1Baosteel 600019.SS N 6.8 19% 5.7 15.4 11 6 0.8 0.8 4.1 2.8Angang 0347.HK U 7.1 -12% 8.0 7.4 83 17 0.9 0.9 8.4 5.9Maanshan 0323.HK N 3.5 5% 3.3 3.3 46 16 0.8 0.7 5.3 4.3Conch 0914.HK N 37.0 -1% 37.6 25.5 13 10 3.6 2.8 8.2 6.6CNBM 3323.HK O 23.3 56% 14.9 10.3 9 8 2.5 2.0 5.6 5.1CRC 1313.HK O 8.7 17% 7.5 6.2 12 10 2.6 2.1 8.5 6.6Shanshui 0691.HK O 10.4 10% 9.5 3.4 9 7 2.9 2.1 5.9 4.5CNM 1893.HK N 5.9 14% 5.2 2.4 9 8 1.4 1.2 3.0 1.9TCCI 1136.HK N 4.0 -21% 5.1 2.1 10 9 1.4 1.2 7.2 5.9BBMG 2009.HK O 15.2 38% 11.0 6.1 9 7 1.7 1.4 5.8 4.1Chalco 2600.HK U 4.8 -25% 6.4 11.1 32 29 1.3 1.3 11.5 10.0UC Rusal 0486.HK O 13.8 32% 10.4 20.3 7 9 1.4 1.2 5.7 6.2Jiangxi Cu 0358.HK N 26.0 -2% 26.5 11.8 9 9 1.8 1.6 7.1 6.6Zijin 2899.HK N 4.8 14% 4.2 11.8 13 12 2.9 2.5 6.9 6.0

Source: Company data, Credit Suisse estimates Cement sector 2H11 – supply pressure in selected regions MIIT report reiterated the closure target of 150 mn tonnes for 2011 (higher than 130 mn announced before). Nevertheless, the target can become more challenging given profitability of the sector. MIIT noted new supply pressure, especially in western China. MIIT estimated 150 new lines or 186 mn tonnes (likely in clinker, thus 241 mn tonnes in equivalent cement capacity) will come online in 2011E, including 70% for 2H11. The net supply number is 44 or 2% higher than our ests.

Figure 2: Summary of 1H11 sector operations Cement Aluminum Steel1H11 output mn tonnes 950 8.7 350YoY % +20% +4% 10%App demand mn tonnes 944 8.5 333YoY % +20% +4% +9%Profit* Rmb bn 35.2 5.2** 64.0YoY % +170% -24% -1%Implied unit profit Rmb/t 47 300 182Capex Rmb bn 65.4 16.5 118.9YoY % -15% +52% +7%Implied new capacity mn tonnes 164 1.6 2***% of 1H11 demand % 8% 9% 1%*5M11 number ** for both aluminum and alumina, implied unit profit assumes half of the profit goes to aluminium. ***we assumed Rmb300/t in unit maintenance cost and Rmb4,000/t for new line expansions. Source: MIIT, Credit-Suisse estimates Al sector 2H11 – improving 2H MIIT estimated aluminium output to reach 18 mn tonnes (implies 7% HoH increase in output), driven by new line expansions and seasonality. Cost pressure remains high, due to higher power tariff and carbon costs. Nevertheless, MIIT believes price and margin should improve in 2H, due to government control on new capacity and seasonality. In addition, MIIT encourages the completion of direct power purchase for the designated 15 smelters. Steel sector 2H11 – persistent low margin On the back of decelerating industrial demand, power restriction, elimination of old obsolete capacity and tightened capital, MIIT believes steel output to soften in 2H, with FY11 reaching 690-700 mn tonnes (implies 2H output flat or 3% lower HoH). Apparent demand would be 660-670 mn tonnes. MIIT expects stagnant steel prices and low profit to stay. 1H11 profitability and capex trend The report suggests industry profit has surged 170% in cement, but declined by 24% for aluminium and 1% for steel, mostly in line with our expectations. Implied profit of cement is estimated at Rmb47/t, about Rmb30/t higher YoY. Implied unit profit of aluminium is estimated at US$0.02/lb, about US¢5/lb lower than a year ago, suggests stagnant margin as cost pressure combines with higher aluminium price. Unit profit of steel suggests an average of unit EBITDA of US$40-50/t, trough of the sector.

The 1H11 capex for cement declined 15% from the peak, but was still able to support 160 mn tonnes of new line addition, 8% of 1H11 output run rate. Capax for aluminium and steel, through showing some rebound, is due to low base in our view and remains as depressed.

Thursday, 04 August 2011

Asian Daily

- 9 of 34 -

Hong Kong Standard Chartered ----------------------------------------------------- Maintain UNDERPERFORM 1H11 results — Consumer compensates for Wholesale; overall in line EPS: ◄► TP: ◄► Sanjay Jain / Research Analyst / 65 6212 3017 / [email protected] Anand Swaminathan / Research Analyst / 65 6212 3012 / [email protected] Vineet Thodge / Research Analyst / 852 2101 7466 / [email protected]

● STAN’s 1H11 reported PBT of US$3.6 bn was 2.5% ahead of CS est while underlying earnings and total income (US$8.8 bn) were in line. Overall cost-income jaws in the 1H were flat (incl bank levy) (+2.9% excl bank levy). Guidance remains for ‘broadly flat’ jaws for FY excl bank levy implying a negative progression in H2.

● Consumer banking showed strong performance on the back of volume growth, which more than offset asset margin pressures. Wholesale banking was below expectations on account of weaker global markets performance.

● Geographically, Hong Kong and Singapore were particularly strong while the company highlighted that it is facing challenges in India (increasing rates, competition and regulations) and Korea (high costs and inefficient balance sheet).

● In the medium term, we believe cost inflationary pressures remain, revenues (especially in wholesale banking) will be under pressure and overall returns remain low. Trading on c1.7x PTNAV for 15% RoTE, we retain our UNDERPERFORM rating.

Figure 1: STAN – geographical revenue and pre-tax profit breakdown Revenue (1H11) Pre-tax profit (1H11) US$ mn Share HoH YoY US$ mn Share HoH YoYHong Kong 1,531 17% 17.0 28.5 790 16% 33.4 54.6Singapore 1,094 12% 32.6 19.8 465 13% 55.5 11.0Korea 840 10% -6.9 5.5 193 5% -19.2 29.5India 893 10% -12.2 -11.7 378 20% -34.0 -39.4Other APac 1,748 20% 7.6 13.4 846 19% 67.9 46.1Amer+Eur,Gp 862 10% 14.9 11.9 244 4% 121.8 98.4MESA 1,118 13% 0.6 5.9 429 13% -2.7 7.3Africa 678 8% 13.0 5.0 291 10% 17.3 -6.4Total 8,764 100% 7.7 10.6 3,636 100% 21.0 16.7Source: Company data, Credit Suisse estimates

Loan growth driven by Singapore, India and Hong Kong Figure 2: STAN – geographical loan growth 1H11 US$ bn Share '09

YoY'10

YoY 1H11 YoY

2H09HoH

1H10HoH

2H10HoH

1H11HoH

Hong Kong 47.1 18% 7.0 45.1 29.6 2.6 21.0 19.9 8.1Singapore 45.5 17% 54.2 25.2 29.9 19.4 11.5 12.3 15.6Korea 43.2 16% 15.9 8.9 19.1 16.7 -1.8 10.8 7.5India 12.5 5% 12.9 26.7 21.9 7.9 14.3 10.9 9.9Other APac 51.9 19% 9.3 14.2 19.8 11.2 2.7 11.1 7.8Amer+Eur 44.0 16% -2.7 36.9 21.7 0.2 19.6 14.4 6.3MESA+Africa 24.2 9% 7.7 0.9 6.8 3.7 -0.7 1.6 5.1Gross loans 268.5 100% 13.1 21.9 22.0 9.1 8.6 12.3 8.6Source: Company data, Credit Suisse estimates CB stronger than expected, WB weaker Consumer Banking was significantly higher than expected, driven by lower costs and lower provisions. Wholesale banking PBT was 8% weaker than expected despite a gain on structured notes.

Figure 3: STAN – consumer and wholesale banking highlights (1H11) Consumer (incl. SME) Wholesale (%) US$ bn Share HoH% YoY% US$ bn Share HoH% YoY%Loans 125.8 47% 7.4 22.3 142.7 53% 9.8 21.7Revenue 3.34 38% 5.4 14.6 5.43 62% 9.3 8.3Optg exp 2.11 45% -4.6 7.3 2.57 55% 3.4 9.0Optg profit 1.23 30% 28.3 29.8 2.86 70% 15.1 7.7Provisions 0.22 44% -25.1 -29.0 0.27 56% 45.4 46.2Pre-tax profit 1.01 28% 51.2 57.5 2.59 72% 12.7 4.8Source: Company data, Credit Suisse estimates. Funding and capital remain comfortable Core Tier 1 capital slightly improved further to 11.9% (11.8% as of Dec-10). RWA’s grew 7% HoH, in line with estimates.

Figure 4: STAN – financial snapshot (US$ mn) 2009 2010 YoY% 1H10 2H10 1H11 HoH% YoY%Net interest income 7,623 8,470 11.1 4,155 4,315 4,941 14.5 18.9Non interest income 7,561 7,592 0.4 3,769 3,823 3,823 0.0 1.4 Fee income 3,370 4,238 25.8 2,148 2,090 2,179 4.3 1.4 Trading income 2,890 2,577 -10.8 1,351 1,226 1,366 11.4 1.1Operating expenses -7,952 -9,023 13.5 -4,344 -4,679 -4,677 0.0 7.7Pre-prov optg profit 7,232 7,039 -2.7 3,580 3,459 4,087 18.2 14.2Provisions -2,102 -959 -54.4 -487 -472 -484 2.5 -0.6Pre-tax profit 5,151 6,122 18.9 3,116 3,006 3,636 21.0 16.7Net profit 3,380 4,332 28.2 2,148 2,184 2,566 17.5 19.5ROE (%) 13.7 13.2 -0.4 15.1 12.9 13.0 0.1 -2.2ROA (%) 0.78 0.91 0.13 0.94 0.88 0.95 0.07 0.01Loans (US$ bn) 202.7 247.2 21.9 220.1 247.2 268.5 8.6 22.0Deposits (US$ bn) 251.2 307.0 22.2 279.1 307.0 333.5 8.6 19.5Loan-dep ratio (%) 78.9 78.3 -0.6 77.0 78.3 78.6 0.3 1.6Net interest margin 2.32 2.21 -0.11 2.28 2.14 2.27 0.13 -0.01Cost-inc ratio (%) 52.4 56.2 3.8 54.8 57.5 53.4 -4.1 -1.5Non II / revenue (%) 49.8 47.3 -2.5 47.6 47.0 43.6 -3.4 -3.9NPL to loans (%) 2.0 1.9 -0.1 2.0 1.9 1.7 -0.2 -0.3Provisions (bp of loans) 110 43 -67 bp 46 40 38 -3 bp -9 bpLoan loss cover (%) 71 58 -13.5 63 58 61 3 -3Equity Tier 1 CAR (%) 8.9 11.8 2.9 9.0 11.8 11.9 0.1 2.9Source: Company data, Credit Suisse estimates

Price (03 Aug 11, HK$) 201.40TP (prev. TP HK$) 190.79 (190.79) Est. pot. % chg. to TP (5)52-wk range (HK$) 244.0 - 190.6Mkt cap (HK$/US$ bn) 469.0/ 60.2

Bbg/RIC 2888 HK / 2888.HK Rating (prev. rating) U (U) Shares outstanding (mn) 2,379.12 Daily trad vol - 6m avg (mn) 4.8 Daily trad val - 6m avg (US$ mn) 125.9 Free float (%) 100 Major shareholders

Performance 1M 3M 12MAbsolute (%) (2.8) (2.3) (8.6)Relative (%) 0.6 3.1 (11.1)

Year 12/09A 12/10A 12/11E 12/12E 12/13EPre-prov Op profit (US$ mn) 6,968.0 7,039.0 7,730.5 8,578.7 9,460.4Net profit (US$ mn) 3,478 4,247 4,486 5,054 5,633EPS (CS adj. US$) 1.75 1.94 1.88 2.10 2.33- Change from prev. EPS (%) n.a. n.a. 0 0 0- Consensus EPS (US$) n.a. n.a. 2.05 2.35 2.59EPS growth (%) (7.5) 10.5 (3.2) 12.1 10.8P/E (x) 14.7 13.3 13.8 12.3 11.1Dividend yield (%) 3.9 3.8 4.2 4.6 5.1BVPS (CS adj. US$) 13.5 16.3 17.1 18.6 20.2P/B (x) 1.91 1.59 1.51 1.39 1.28ROE (%) 14.1 14.1 11.4 12.0 12.2ROA (%) 0.8 0.9 0.8 0.9 1.0Tier 1 Ratio (%) 11.5 14.0 13.5 13.0 12.7 Note 1: Standard Chartered PLC is a holding company. Through its subsidiaries, the company is engaged in the business of retail and commercial banking, and the provision of other financial services.

Thursday, 04 August 2011

Asian Daily

- 10 of 34 -

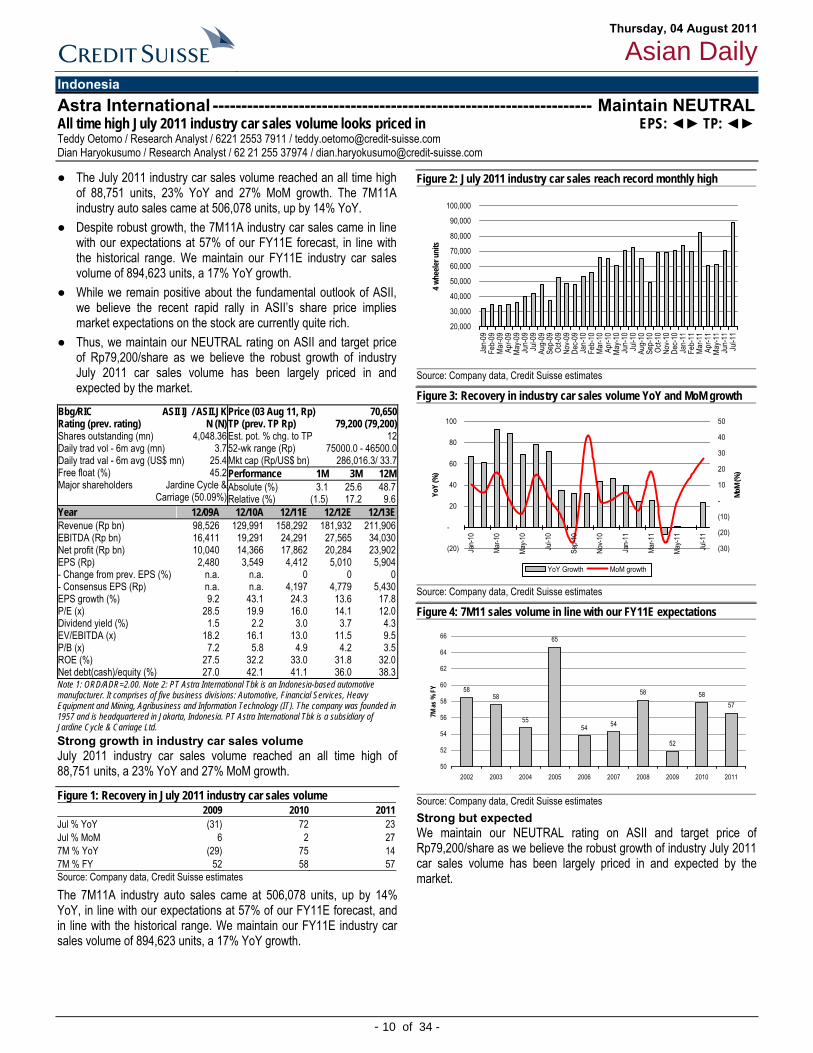

Indonesia Astra International ------------------------------------------------------------------ Maintain NEUTRAL All time high July 2011 industry car sales volume looks priced in EPS: ◄► TP: ◄► Teddy Oetomo / Research Analyst / 6221 2553 7911 / [email protected] Dian Haryokusumo / Research Analyst / 62 21 255 37974 / [email protected]

● The July 2011 industry car sales volume reached an all time high of 88,751 units, 23% YoY and 27% MoM growth. The 7M11A industry auto sales came at 506,078 units, up by 14% YoY.

● Despite robust growth, the 7M11A industry car sales came in line with our expectations at 57% of our FY11E forecast, in line with the historical range. We maintain our FY11E industry car sales volume of 894,623 units, a 17% YoY growth.

● While we remain positive about the fundamental outlook of ASII, we believe the recent rapid rally in ASII’s share price implies market expectations on the stock are currently quite rich.

● Thus, we maintain our NEUTRAL rating on ASII and target price of Rp79,200/share as we believe the robust growth of industry July 2011 car sales volume has been largely priced in and expected by the market.

Strong growth in industry car sales volume July 2011 industry car sales volume reached an all time high of 88,751 units, a 23% YoY and 27% MoM growth.

Figure 1: Recovery in July 2011 industry car sales volume 2009 2010 2011Jul % YoY (31) 72 23 Jul % MoM 6 2 27 7M % YoY (29) 75 14 7M % FY 52 58 57 Source: Company data, Credit Suisse estimates

The 7M11A industry auto sales came at 506,078 units, up by 14% YoY, in line with our expectations at 57% of our FY11E forecast, and in line with the historical range. We maintain our FY11E industry car sales volume of 894,623 units, a 17% YoY growth.

Figure 2: July 2011 industry car sales reach record monthly high

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Jan-

09Fe

b-09

Mar-0

9Ap

r-09

May-0

9Ju

n-09

Jul-0

9Au

g-09

Sep-

09Oc

t-09

Nov-0

9De

c-09

Jan-

10Fe

b-10

Mar-1

0Ap

r-10

May-1

0Ju

n-10

Jul-1

0Au

g-10

Sep-

10Oc

t-10

Nov-1

0De

c-10

Jan-

11Fe

b-11

Mar-1

1Ap

r-11

May-1

1Ju

n-11

Jul-1

1

4 whe

eler u

nits

Source: Company data, Credit Suisse estimates

Figure 3: Recovery in industry car sales volume YoY and MoM growth

(20)

-

20

40

60

80

100

Jan-

10

Mar-1

0

May-1

0

Jul-1

0

Sep-

10

Nov-1

0

Jan-

11

Mar-1

1

May-1

1

Jul-1

1

YoY

(%)

(30)

(20)

(10)

-

10

20

30

40

50

MoM

(%)

YoY Growth MoM growth

Source: Company data, Credit Suisse estimates

Figure 4: 7M11 sales volume in line with our FY11E expectations

5858

55

65

54 54

58

52

5857

50

52

54

56

58

60

62

64

66

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

7M as

% F

Y

Source: Company data, Credit Suisse estimates Strong but expected We maintain our NEUTRAL rating on ASII and target price of Rp79,200/share as we believe the robust growth of industry July 2011 car sales volume has been largely priced in and expected by the market.

Price (03 Aug 11, Rp) 70,650TP (prev. TP Rp) 79,200 (79,200) Est. pot. % chg. to TP 1252-wk range (Rp) 75000.0 - 46500.0Mkt cap (Rp/US$ bn) 286,016.3/ 33.7

Bbg/RIC ASII IJ / ASII.JK Rating (prev. rating) N (N) Shares outstanding (mn) 4,048.36 Daily trad vol - 6m avg (mn) 3.7 Daily trad val - 6m avg (US$ mn) 25.4 Free float (%) 45.2 Major shareholders Jardine Cycle &

Carriage (50.09%)

Performance 1M 3M 12MAbsolute (%) 3.1 25.6 48.7Relative (%) (1.5) 17.2 9.6

Year 12/09A 12/10A 12/11E 12/12E 12/13ERevenue (Rp bn) 98,526 129,991 158,292 181,932 211,906EBITDA (Rp bn) 16,411 19,291 24,291 27,565 34,030Net profit (Rp bn) 10,040 14,366 17,862 20,284 23,902EPS (Rp) 2,480 3,549 4,412 5,010 5,904- Change from prev. EPS (%) n.a. n.a. 0 0 0- Consensus EPS (Rp) n.a. n.a. 4,197 4,779 5,430EPS growth (%) 9.2 43.1 24.3 13.6 17.8P/E (x) 28.5 19.9 16.0 14.1 12.0Dividend yield (%) 1.5 2.2 3.0 3.7 4.3EV/EBITDA (x) 18.2 16.1 13.0 11.5 9.5P/B (x) 7.2 5.8 4.9 4.2 3.5ROE (%) 27.5 32.2 33.0 31.8 32.0Net debt(cash)/equity (%) 27.0 42.1 41.1 36.0 38.3 Note 1: ORD/ADR=2.00. Note 2: PT Astra International Tbk is an Indonesia-based automotive manufacturer. It comprises of five business divisions: Automotive, Financial Services, Heavy Equipment and Mining, Agribusiness and Information Technology (IT). The company was founded in 1957 and is headquartered in Jakarta, Indonesia. PT Astra International Tbk is a subsidiary of Jardine Cycle & Carriage Ltd.

Thursday, 04 August 2011

Asian Daily

- 11 of 34 -

Pakistan Fauji Fertilizer Company Limited ---------------------------------------------- Maintain NEUTRAL Earnings and target price raised on higher dividend income from FFBL EPS: ▲ TP: ▲ Farhan Rizvi, CFA / Research Analyst / 65 6212 3036 / [email protected]

● We increase our EPS estimates for FFC by 1-4% over 2011-13 and target price by 2% to PRs170 to account for higher dividend income from FFBL, lower finance cost and sharp rise in other expenses.

● While 2Q11 earnings (+72% YoY, flat QoQ) were 2% below expectation, significant variance was observed in finance cost (30% behind estimates) and other expense (+105%). Though margins surprised on the upside (59% in 2Q), we maintain our full-year forecast of 54%. We expect increase in gas prices and DAP sales in 4Q to exert downward pressure on margins in 2H11.

● In order to curtail spending on expensive urea imports, government has in principle agreed to ensure 80% gas supply to plants on the Sui network including Engro’s new plant. This move along with agri commodity meltdown should reduce potential for steeper price hikes in the future and limit price driven growth enjoyed by FFC.

● We maintain our NEUTRAL rating for FFC with a revised target price of PRs170. The stock appears fairly valued trading at a 2011E EV/EBITDA of 4.5x (8% discount to historical multiples).

2Q11 results in line but margins surprised on the upside

FFC 2Q11 earnings of PRs4.1bn (EPS PRs4.8) was 2% behind ours and consensus EPS estimate of PRs4.9, with gross margins of 59% surprising on the upside (+7.4%QoQ). Higher urea price (+5% QoQ) was the major reason behind the sharp rise in margins, though we ruled out margins to be sustainable at these levels in 2H11 due to expected increase in gas prices and lower margin DAP sales in 4Q11. The agri commodity price meltdown particularly cotton (down 60% from peak) has significantly altered the farm economics, making it difficult for steeper price hikes in the future. Though margins surprised on the upside, other expenses (+97% YoY, 21% QoQ) negatively impacted earnings in 2Q11.

Figure 1: 2Q11 results snapshot PRs mn 2Q 11A 2Q CS est. +/-(%) 1Q11A 2Q 10A QoQ % YoY % Net sales 13,120 13,433 -2.3 11,100 10,448 18.2 25.6 Cost of sales 5,337 5,937 -10.1 5,190 5,658 2.8 -5.7 Gross profit 7,783 7,495 3.8 5,910 4,789 31.7 62.5 Distribution cost 1,148 1,050 9.3 1,018 967 12.8 18.8 Operating profit 6,635 6,445 2.9 4,892 3,823 35.6 73.6 Finance cost 242 350 -30.9 229 230 5.6 5.1 Other expenses 615 300 105.0 507 311 21.2 97.6 Other income 919 950 -3.2 1,963 263 -53.2 249.9 Profit after tax 4,080 4,182 -2.4 4,109 2,372 -0.7 72.0 EPS (PRs) 4.81 4.93 4.84 2.80Urea sales (k tons) 627 630 -0.5 546 678 14.9 -7.5Price/ton (US$) 242 246 -1.6 230 175 5.2 38.3GP margin 59% 56% 3.5 53% 46% 7.4 13.5ROE (annualised) 84% 86% -1.9 101% 71% 30.0 13.6Source: Company data, Credit Suisse estimates Increase 2011-13E EPS by 1-4%; target price raised to PRs170 We raise our earnings forecast for FFC by 1-4% over 2011-13 and target price by 2% to PRs170 to account for higher dividend income from its subsidiary FFBL, lower financial charges and sharp rise in other expenses in 1H11. FFBL announced a surprisingly high payout of PRs2.25/share in 2Q11 (cumulative dividend of PRs7/share YTD), leading us to increase our 2011E dividend income by 31% to PRs4 bn (PRs8.5/share) from PRs3.1 bn (PRs6.5/share) earlier. Moreover, we have lowered our financial cost estimates by 12-34% due to lower debt levels and increased other expenses estimates by 8-9%.

Figure 2: Summary of estimate revisions 2011E 2012E 2013EDividend income (PRs mn) NEW 4,039 3,089 2,756OLD 3,089 2,851 2,424Change (%) 30.8% 8.3% 13.7%Finance cost (PRs mn) NEW 1,463 927 680OLD 1,667 1,277 1,027Change (%) -12.2% -27.3% -29.7%Other expenses (PRs mn) NEW 2,131 2,321 2,398OLD 1,962 2,139 2,211Change (%) 8.6% 8.5% 8.4%EPS (PRs) NEW 20.0 21.6 21.8OLD 19.2 21.1 21.5Change (%) 4.3% 2.2% 1.3%Source: Credit Suisse estimates Maintain NEUTRAL; positives appear priced in Despite impressive 2Q11 results, we remain NEUTRAL on FFC as we believe positives have been largely priced in (YTD return of 62%). Moreover, meltdown in agri commodity prices and government plans to resolve gas supply issues for plants on the Sui network such as Engro’s new plant would also reduce potential for significant price hikes in the future. We, however, do not rule out 8-10% price hike in 2H11, which would be in response to the likely increase in feed gas prices by 96%. FFC trades at a 2011E EV/EBITDA of 4.6x (a 7% discount to historical multiples).

Price (02 Aug 11 ) 162.85TP (prev. TP) 170.00 (166.00) Est. pot. % chg. to TP 452-wk range 172.0 - 82.4Mkt cap (bn) 138.1/ 1.6

Bbg/RIC FFC PA / FAUF.KA Rating (prev. rating) N (N) Shares outstanding (mn) 848.16 Daily trad vol - 6m avg (mn) 2.0 Daily trad val - 6m avg (mn) 3.2 Free float (%) — Major shareholders

Performance 1M 3M 12MAbsolute (%) 7.0 17.1 81.3Relative (%) 9.7 14.5 63.7

Year 12/09A 12/10A 12/11E 12/12E 12/13ERevenue (mn) 36,163 44,874 53,968 58,100 60,768EBITDA (mn) 16,041 19,591 29,998 31,535 31,724Net profit (mn) 8,823 11,029 16,977 18,323 18,475EPS 10.4 13.0 20.0 21.6 21.8- Change from prev. EPS (%) n.a. n.a. 4 2 1- Consensus EPS n.a. n.a. 19.4 20.5 16.3EPS growth (%) 35.2 25.0 53.9 7.9 0.8P/E (x) 15.7 12.5 8.1 7.5 7.5Dividend yield (%) 5.8 5.9 11.1 11.9 12.7EV/EBITDA (x) 9.1 7.6 4.5 4.2 4.2P/B (x) 8.4 7.2 8.1 7.3 6.9ROE (%) 69.6 77.3 104.2 101.4 95.0Net debt(cash)/equity (%) 65.9 64.9 (21.2) (28.2) (30.8) Note1:Fauji Fertilizer Company Limited is a Pakistan-based company. The principal activity of the Company is manufacturing, purchasing and marketing of fertilizers and chemicals, including investment in other fertilizer, chemical and other manufacturing operations..

Thursday, 04 August 2011

Asian Daily

- 12 of 34 -

Singapore City Developments ---------------------------------------------------------- Maintain OUTPERFORM Strong M&C 2Q11 results, Singapore RevPAR +22.5% in July EPS: ◄► TP: ◄► Tricia Song / Research Analyst / 65 6212 3141 / [email protected]

● CDL's 54% subsidiary M&C reported strong 2Q11 results with headline pre-tax profit up 11% and EPS up 90% YoY, in line with our above-street forecasts. Performance was variable but gateway cities (London, NY, SG) saw accelerating RevPAR growth; excl. refurbishments, hotel EBIT would have risen 25% YoY (from 12%). Click here for report.

● We expect less disruptive impact in 2H and forecast 19% 2H11 EBIT growth, supported by strong current trading trends. For the first 24 days of July, M&C's group RevPAR posted 12.6% YoY rise, with Singapore rising 22.5%, London 14.9% and New York, 12.5%. We retain forecasts and M&C’s TP at 635p.

● CDL will announce its 2Q11 results on 12 Aug. We expect profits to be robust on strong M&C contributions (partially mitigated by 2% QoQ and 6% YoY SGD appreciation against GBP), some divestment gains, and progressive residential profit recognition.

● CDL is trading at unwarranted 27% below its historical average P/B of 2x, and at a 32% discount to its RNAV vs historical average of parity. We like this as a value play on Singapore property which is expected to be resilient on strong fundamentals.

Figure 1: M&C operating statistics £ mn

2Q11

2Q10

Reported Curr chg (%)

Constant curr chg (%)

RevPAR 66.37 63.47 4.6 6.3Revenue - total 196.1 190 3.2 4.5Revenue - hotel 193.8 186.9 3.7 5.1Headline operating profit 43.7 39.1 11.8 10.7Pre-tax profit 60.6 31.6 91.8 89.2Headline pre-tax profit 40 36.1 10.8 9.4EPS per share (p) 15.2 8 90 Source: Company data.

Strong operating trends, Singapore RevPAR +22.5% in July. M&C has reported in-line 2Q hotel EBIT of £40.7 mn (CS: £39.6 mn, +12% YoY) driven by constant currency RevPAR growth of 6.3% or 7.5% on a like-for-like (LFL) basis (CS: 7.6%). The trading performance is variable with gateway cities (London, New York and Singapore make up 59% of 2011E hotel EBIT) all seeing accelerating RevPAR growth

into 2Q (London 16%, Singapore 12.5% and New York 8.3%), while UK and US regional performance is softer and one-off impacts of refurbishment and asset management hit 1H profit by £6.8 mn, without which hotel EBIT would have risen 25% YoY. We expect less disruptive impact in 2H and forecast 19% 2H11 EBIT growth, supported by strong current trading trends. For the first 24 days of July, M&C's group RevPAR posted year-on-year increase of 12.6%, with Singapore rising 22.5%, London 14.9% and New York, 12.5%. On a like-for-like basis, group RevPAR rose by 11.3% and Singapore by 14.6%. The interim dividend of 2.08 p is maintained.

Figure 2: Group RevPAR +6.3%, driven by London, NY and Singapore RevPAR (£) 2Q11 Reported Curr 2Q10 Const Curr chg (%)New York 138.67 128.04 8.3Regional US 41.14 38.54 6.7Total US 65.3 60.07 8.7London 105.91 91.28 16.0Rest of Europe 52.98 53.21 -0.4Total Europe 76.35 70.07 9.0Singapore 97.76 86.91 12.5Rest of Asia 57.15 60.46 -5.5Total Asia 72.86 72.55 0.4Autstralasia 26.14 30.37 -13.9Total Group 66.37 62.45 6.3Source: Company data, Credit Suisse estimates.

Divestment gains and further asset management progress in 1H: Including M&C’s reported 2Q11 PATMI jumped 92% YoY to £47.9 mn on a £17.4 mn gain from the sale and leaseback of Studio M hotel in Singapore to CDL Hospitality Trusts (CDLHT). The company confirms: 1) the disposal of land beside its Grand Millennium Kuala Lumpur on 1 Aug, and expects to book pre-tax profit of £35.4 mn in 3Q11; 2) the near completion of the Millennium Seoul refurbishment; 3) the Tokyo hotel construction site acquisition and 4) the next stages of the FSCL Chengdu project (larger hotel, sale of commercial units).

At CDL, continued sales of new launches. CDL has sold 150 units of its 602-unit Executive Condo, Blossoms Residences, at Bukit Panjang at S$685/sq ft within the first weekend of launch in early July. It has also sold 18 units of its high-end 64-unit Buckley Classique at S$2,050/sq ft as of 30 June. Its mass market H2O Residences at Sengkang, has sold 351 of its 521 units, at S$950/sq ft, since its launch in March 2011. Its 1/3-owned mass market Hedges Park, has sold 309 of total 501 units, at S$875/sq ft since launch in April.

Completions in 2Q11 to provide some boost to earnings. CDL would announce its 2Q11 results on 12 August. We expect it to recognise more residential profits in 2Q11 given three projects, Cliveden (110 units, 88 sold), Shelford Suites (77 units, 76 sold) and The Residences@ W (228 units, 21 units sold). We expect part of these projects (c.20%) to be sold on deferred payment scheme, which would mean lumpier recognition on FRS115 where it recognises units sold on DPS only upon completion. Its China acquisitions in Suzhou (S$16 7mn land price, Rmb3,000/sq m) and Chongqing (S$45 mn) are still small relative to its asset base of S$14.5 bn.

Price (02 Aug 11 , S$) 10.65TP (prev. TP S$) 15.74 (15.74) Est. pot. % chg. to TP 4852-wk range (S$) 13.7 - 10.0Mkt cap (S$/US$ mn) 9,684.1/ 8,033.2

Bbg/RIC CIT SP / CTDM.SI Rating (prev. rating) O (O) Shares outstanding (mn) 909.30 Daily trad vol - 6m avg (mn) 1.5 Daily trad val - 6m avg (US$ mn) 13.8 Free float (%) 51.4 Major shareholders Hong Leong Group

48%

Performance 1M 3M 12MAbsolute (%) 0.7 (3.2) (15.5)Relative (%) (0.1) (5.3) (20.9)

Year 12/09A 12/10A 12/11E 12/12E 12/13EEBITDA (S$ mn) 1,036 1,242 1,268 1,216 1,397Net profit (S$ mn) 580.5 736.1 731.2 638.3 777.2EPS (S$) 0.61 0.77 0.77 0.67 0.81- Change from prev. EPS (%) n.a. n.a. 0 0 0- Consensus EPS (S$) n.a. n.a. 0.76 0.78 0.84EPS growth (%) 2.2 26.8 (0.7) (12.7) 21.7P/E (x) 17.5 13.8 13.9 15.9 13.1Dividend yield (%) 0.8 1.7 0.9 0.9 0.9EV/EBITDA (x) 12.3 9.7 9.0 8.9 7.1ROE (%) 10.2 11.9 10.8 8.6 9.6Net debt(cash)/equity (%) 39.6 28.7 19.7 12.4 2.6NAV per share (S$) — — 15.7 — —Disc./prem. to NAV (%) — — (32.3) — — Note1:ORD/ADR=1.00.Note2:City Developments Limited (CDL) is a Singapore-based company engaged in property development, ownership and investment holding..

Thursday, 04 August 2011

Asian Daily

- 13 of 34 -

Great Eastern------------------------------------------------------------------ Maintain OUTPERFORM 2Q11 result: Good business momentum EPS: ▼ TP: ◄► Frances Feng / Research Analyst / 852 2101 6693 / [email protected] Arjan van Veen / Research Analyst / 852 2101 7508 / [email protected]

● Great Eastern (GE) reported a 2Q11 NPAT of S$117.7 mn, up strongly by 58% YoY owing to strong insurance underwriting profit. An interim dividend of S$10 cents was declared. We have lowered our forecast by 2–3% on lower-than-expected 1H11 profit.

● New business momentum was robust, with Singapore up 45% YoY, but Malaysia down 11% YoY (but with better product profitability) and other markets (China/Indonesia) down 4% YoY.

● Value metric growth was strong, with VNB (value of new business) up 21% YoY aided by strong new business growth in Singapore (+37%) and margin expansion in Malaysia (now at 53%, 10 p.p. improvement compared with 2Q11). Capital position remains strong with solvency ratio at above 200%.

● Great Eastern is now trading at only 0.9x P/EV (embedded value), 11.5x P/E and 1.5x P/BV, which we believe is very attractive given its strong market position and growth profile. We maintain our OUTPERFORM rating and S$20 target price (16x P/E, 1.4x P/EV).

Great Eastern (GE) reported a strong 2Q11 NPAT of S$117.7 mn, up 58% YoY owing to strong insurance underwriting profit in traditional product (142% YoY) and participating product (27% YoY). New business value grew by 21% in 2Q11 underpinned by strong Singapore new business volume thanks to the success in its premier customer segment in OCBC cooperation. Malaysia new business value slowed to just 9% on lower business volume (-11%) but with strong margin improvement (+10 p.p.).

Figure 1: Strong 2Q11 NPAT due to good underwriting results S$ mn 2Q10 1Q11 2Q11 YoY %Gross written premium 1,367.3 1,461.9 1,587.2 16% Life insurance profit 69.1 149.8 105.9 53%- Participating fund 23.7 30.7 30.2 27%- Non-participating fund 19.4 92.0 46.9 142%- Investment-linked fund 26.0 27.1 28.8 11%General insurance profit 5.9 5.9 7.6 29%Profit from insurance ops 75.0 155.7 113.5 51% Profit from investments 14.9 25.6 36.6 146%Fees and other income 18.4 17.1 24.7 34%Expenses 15.0 19.8 33.5 123% Pre-tax profit 91.3 179.3 140.2 54%Tax 14.3 18.1 20.1 41%NPAT 77.0 161.2 120.1 56%Minorities -2.6 -2.5 -2.4 -8%NPAT attributable 74.4 158.7 117.7 58% EPS 0.16 0.34 0.25 58%Source: Company data, Credit Suisse estimates

Figure 2: Singapore showed strength while Malaysia weak in 2Q11 NB APE growth, VNB growth and VNB margin by markets (%) 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11Singapore NB APE growth (%pa) 61% 28% -12% 20% 33% 45%VNB growth (%pa) 62% 12% 13% 35% 18% 37%VNB margin (% APE) 41% 43% 38% 47% 37% 40%Malaysia NB APE growth (%pa) -23% 20% 48% 15% 24% -11%VNB growth (%pa) 4% 41% 43% 16% 44% 9%VNB margin (% APE) 50% 43% 47% 41% 57% 53%Total NB APE growth (%pa) 19% 30% 11% 26% 33% 14%VNB growth (%pa) 35% 29% 29% 31% 30% 21%VNB margin (% APE) 43% 42% 40% 43% 42% 44%Source: Company data, Credit Suisse estimates

Figure 3: VNB up 21% YoY in 2Q11 Value of one-year new business (VNB -S$ per share) and VNB growth (%)

0

20

40

60

80

100

120

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11F 4Q11F-30%

-20%

-10%

0%

10%

20%

30%

40%

Singapore Malaysia Other Growth (%pa)

F'casts

+25%

Source: Company data, Credit Suisse estimates

Price (02 Aug 11, S$) 14.89TP (prev. TP S$) 20.00 (20.00) Est. pot. % chg. to TP 3452-wk range (S$) 15.8–14.1Mkt cap (S$/US$ mn) 7,047.7/ 5,846.3

Bbg/RIC GE SP / GELA.SI Rating (prev. rating) O (O) Shares outstanding (mn) 473.32 Daily trad vol - 6m avg (mn) 0.0 Daily trad val - 6m avg (US$ mn) 0.3 Free float (%) — Major shareholders OCBC - 85%

Performance 1M 3M 12MAbsolute (%) 1.3 2.4 (5.7)Relative (%) 2.8 6.0 (10.2)

Year 12/09A 12/10A 12/11E 12/12E 12/13ELife premiums (S$ mn) 5,834 6,156 7,176 8,105 8,769P&C GWP (S$ mn) 162.7 171.7 108.1 217.3 244.5Net profit (S$ mn) 516.7 507.2 583.4 630.4 691.8EPS (S$) 1.09 1.07 1.23 1.33 1.46- Change from prev. EPS (%) n.a. n.a. (2) (3) (3)- Consensus EPS (S$) n.a. n.a. 1.15 1.23 1.33EPS growth (%) 89.7 (1.8) 15.0 8.1 9.7P/E (x) 13.6 13.9 12.1 11.2 10.2NAV per share (S$) 7.5 7.7 8.8 10.2 11.6Emb.val.PS (S$) 13.2 14.2 15.5 16.6 17.9Dividend yield (%) 2.7 5.8 4.1 4.5 4.9EV/EBITDA (x) 6.1 7.0 1.8 (0.1) (1.6)P/B (x) 2.0 1.9 1.7 1.5 1.3ROE (%) 15.7 14.0 14.8 14.0 13.4Combined ratio (%) — — — — — Note 1: Great Eastern is the oldest and most established life insurance group in Singapore and Malaysia. With $55 bn in assets and 3.8 mn policyholders, it has two successful distribution channels - the tied agency force and bancassurance. The company also operates in China, Indonesia, Vietnam and Brunei.

Thursday, 04 August 2011

Asian Daily

- 14 of 34 -

Hutchison Port Holdings Trust-------------------------------------- Maintain UNDERPERFORM 1H11 earnings slightly beat on better cost savings, but more cautious on demand outlook EPS: ▼ TP: ▼ Ingrid Wei / Research Analyst / 86 21 3856 0379 / [email protected] Sam Lee / Research Analyst / 852 2101 7186 / [email protected]

● HPHT reported 1H11 net earnings of HK$1 bn, 9.7% ahead of its own IPO target of US$916 mn on better cost savings, despite both volume and earnings missing its target. Interim dividends of HK$0.13/share were declared, which were better than its forecast.

● Nevertheless, what worries us is the volume growth in 2H11. Both its HIT and Yantian terminals reported lower-than-expected volume growth in 1H11, mainly on softer demand from the US and Europe.

● Although we are in the high season, management mentioned no sign of sequential strong volume pick-up and said that demand was weaker than normal seasonality. HPHT’s pure exposure to the PRD means a high probability of weaker volume growth in 2H11. We, therefore, lower our 2011-12 volume growth forecasts.

● Thus, we lower our 2011, 2012 and 2013 EPS estimates by 4%, 7% and 9%, respectively. We also lower our DCF-based target price to US$0.72. Trading at 22.3x and 21.5x 2011-12E P/E, the stock doesn’t look cheap despite a long time weakness. Forecast 2011-12 dividend yields of 6.4% and 8.2% may provide support, but poor demand and earnings outlook will be key overhangs, in our view. We maintain our UNDERPERFORM rating.