Thriveability PPP You've Got It Now What (1) · 2020-06-10 · Where We’ve Been • PPP Loan...

32

Transcript of Thriveability PPP You've Got It Now What (1) · 2020-06-10 · Where We’ve Been • PPP Loan...

Agenda

8:30 Welcome 8:35 Greg Blurton, Vice President, Sr. Commercial Loan Officer, Edison National

Bank8:45 Erica Harp, CPA, Hughes, Snell & Co., PA8:55 Sara Qureshi, Esq., Henderson, Franklin, Starnes & Holt, PA9:05 Michael Lehnert, Esq., Henderson, Franklin, Starnes & Holt, PA9:15 Q&A9:25 Closing

* Information provided in this webinar is fluid and subject to change.

Greg BlurtonVice President, Sr. Commercial Loan Officer

Edison National Bank

YOU’VE GOT THE PPP, NOW WHAT?

PPP Forgiveness through a Lender’s Lens

PAYCHECK PROTECTION PROGRAM –IN A NUTSHELL

Courtesy of EDS, YouTube video, https://www.youtube.com/watch?v=L2zqTYgcpfg

Where We’ve Been• PPP Loan Forgiveness Application Form 3508 released (11 pages) on May 18th

• IFRs on Loan Forgiveness and SBA Loan Review Procedures and Related Borrower and Lender Responsibilities released over Memorial Day weekend

• A few days later on May 28th, the House passed H.R. 7010, Paycheck Protection Program Flexibility Act of 2020, which proposes wholesale changes to the program.

• Through May 30th, 5,554 lenders approved 4,475,599 loans for a total of $510,234,498,923

• The Senate passed the Paycheck Protection Program Flexibility Act of 2020 on June 3, 2020.

So...Where Are We Going?

Expect More ChangesCurrent • 75/25 rule

• 8‐week “Covered Period”

• Loan payments deferred 6 months (SBA covers interest)

• Loans have a maturity of 2 years and interest rate of 1%

• Complex loan forgiveness application and process

Proposed* • 60/40

• Up to 24‐week “Covered Period”

• Loan payments deferred until forgiveness determination is granted by the SBA (could be up to 11 months)

• Loan maturity up to 5 years

• More streamlined application and process

*H.R. 7010, Paycheck Protection Program Flexibility Act of 2020

In The Meantime…As the program currently stands, borrowers have significant responsibilities for the forgiveness process. Some considerations:

• Review and reference the Interim Final Rules (IFR) regarding loan forgiveness, lenders’ and borrowers’ responsibilities as well as the loan forgiveness application and instructions

• Understand eligible non‐payroll expenses

• Understand safe harbors (salary/wage reduction, FTE reduction, offers to rehire)

• No such thing as too much documentation – there are retention requirements

• Lenders have 60 days to perform a “good‐faith review, in reasonable time, of the borrower’s application, calculations and supporting documents concerning amounts eligible for loan forgiveness.”

• The SBA then has an additional 90 days to approve and grant forgiveness.

• SBA Reviews and Audits

Erica Harp, CPA, Hughes, Snell & Erica Harp

CPAHughes, Snell & Co., PA

What Uses of PPP Funds Qualify for Forgiveness?

PPP loan forgiveness is determined based on certain costs incurred and payments made during the covered period

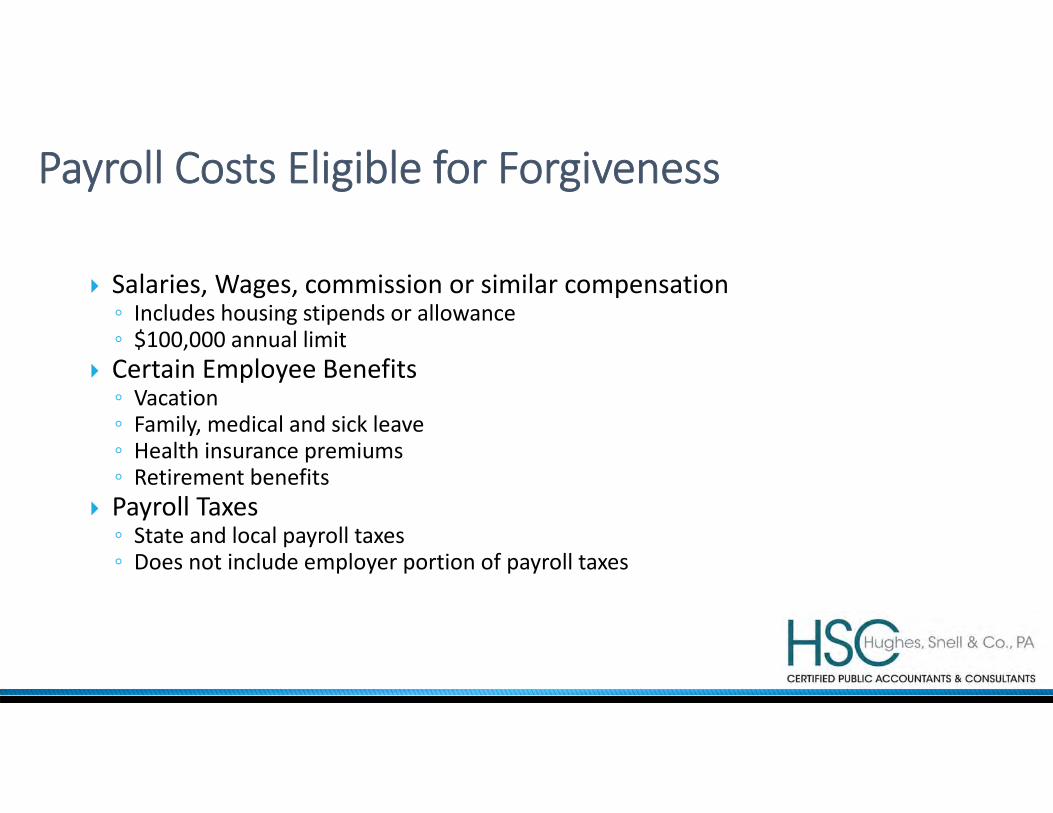

Payroll Costs Eligible for Forgiveness

Salaries, Wages, commission or similar compensation◦ Includes housing stipends or allowance◦ $100,000 annual limit

Certain Employee Benefits ◦ Vacation◦ Family, medical and sick leave◦ Health insurance premiums◦ Retirement benefits

Payroll Taxes◦ State and local payroll taxes ◦ Does not include employer portion of payroll taxes

Timing of Payment for Payroll Costs

Paid or incurred during covered period◦ Normal billing cycle

Alternative Payroll Covered Period Election◦ Only available for borrowers with biweekly (or more frequent) payroll schedules ◦ Calculates covered period starting with the first day of the first pay period following the PPP loan disbursement date◦ Must be consistently applied

Non‐Payroll Costs Eligible for Forgiveness

Interest payments on a mortgage for real or personal property Rent Payments under lease agreement Utility payments◦ Electricity / Gas◦ Water◦ Transportation◦ Telephone / Internet

Mortgages, lease agreements, and/or service contracts must be in existence as of February 15, 2020 in order to qualify

Timing of Payment for Non‐Payroll Costs

Covered period starts with loan funding – no elections No prepayment of expenses permitted◦ Must be either paid or incurred during the covered period◦ Normal billing cycle◦ Exception for some unpaid expenses prior to funding

No Double Dipping on Benefits

Internal Revenue Notice 2020‐32 Nondeductible expenses to extent of forgiveness◦ Further guidance expected on applying when multiple taxable periods are involved

Sara Qureshi, Esq.Henderson, Franklin, Starnes & Holt, PA

Loan Forgiveness: FTE Reduction• What effect does a reduction in a borrower’s number of full-time equivalent (FTE) employees have on the loan forgiveness amount?

Full-Time Equivalent Employees• What exactly does “full-time equivalent employee” mean?

• How should the borrower calculate its number of full-time equivalent employees?

Loan Forgiveness: Compensation Reduction• What effect does a borrower’s reduction in employees’ salary or wages have on the loan forgiveness amount?

Safe Harbors• If the borrower restores reductions made to employees’ salaries and wages or FTE employees by no later than December 31, 2020*, can the borrower avoid a reduction in its loan forgiveness amount?

Exemptions to Reduction• Will a borrower’s loan forgiveness amount be reduced if the borrower laid-off or reduced the hours of an employee, then offered to rehire the same employee for the same salary and same number of hours, or restore the reduction in hours, but the employee declined the offer?

• Are there any additional safe harbors available to borrowers if they are unable to rehire employees?

Loan Forgiveness Reduction: Exception• Will loan forgiveness be reduced if the employee was fired for cause, voluntarily resigned, or voluntarily requested a reduction in hours?

Michael Lehnert, Esq.Henderson, Franklin, Starnes & Holt, PA

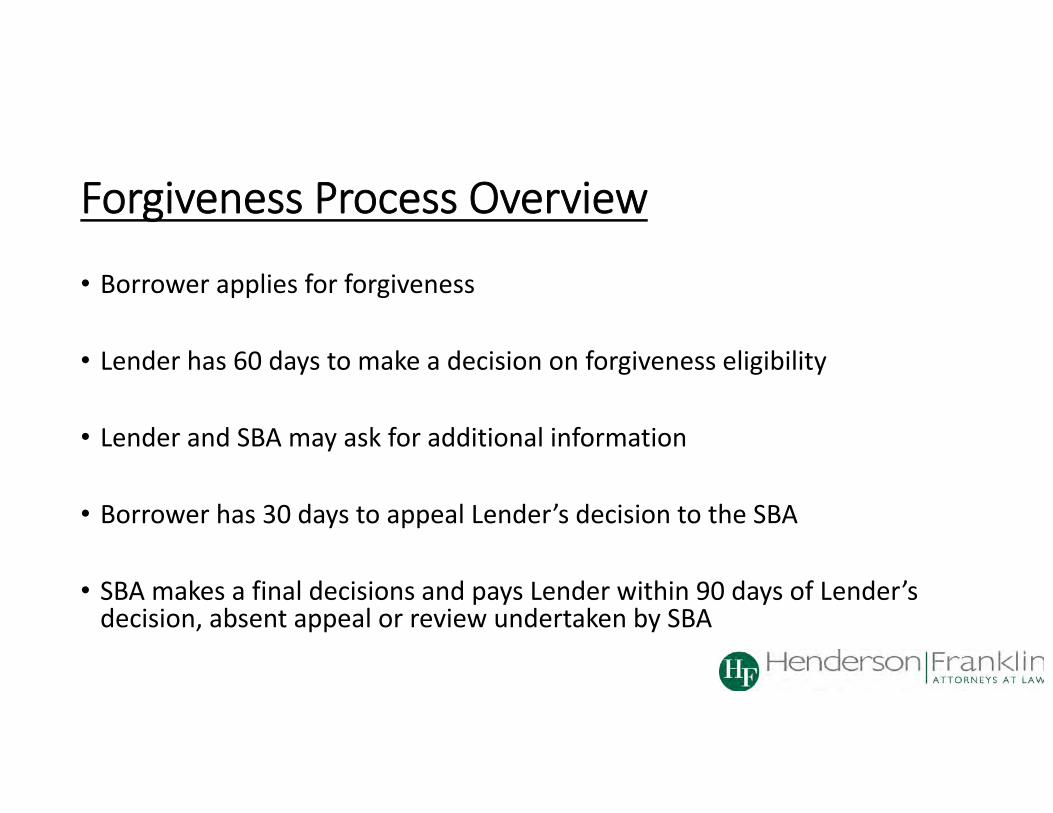

Forgiveness Process Overview

• Borrower applies for forgiveness

• Lender has 60 days to make a decision on forgiveness eligibility

• Lender and SBA may ask for additional information

• Borrower has 30 days to appeal Lender’s decision to the SBA

• SBA makes a final decisions and pays Lender within 90 days of Lender’s decision, absent appeal or review undertaken by SBA

When Should I Prepare My Forgiveness Application?

• Start preparing your forgiveness application early. We recommend including:• Entity formation and structure documentation

• Support for your necessity certification• Payroll reports for the operative periods along with W‐2s for all employees

• Evidence of group health and retirement benefit payments

• Evidence of non‐payroll agreements

What About Unforgiven Funds?

• Two year maturity

• 1% interest

• 6‐month payment deferral

• Funds must be used for permissible purposes ‐ similar to forgiveness purposes – if not repaid

Will You Be Audited?

• Maybe. How will you know?• SBA will notify Lender, and Lender must notify you

• Scope of SBA audit• Required to keep your PPP records for 6 years from the date of forgiveness or repayment in full

• If found ineligible for the loan:• SBA may revoke its guaranty• Lender may hold you in default and demand immediate repayment

• Exception to CARES Act non‐recourse provision

What about the PPPFA?

• Passed overwhelmingly by the House and Senate

• PPPFA* changes to the CARES Act:• 75% payroll rule reduction• Expand covered period• Extend maturity date

• Permit PPP recipients to take advantage of payroll tax deferral

• Expand forgiveness reduction safe harbor*PPPFA – Paycheck Protection Program Flexibility Act of 2020

Q & A

Thank You!