THIRD POINT OFFSHORE FUND, LTD. · 2018-09-20 · Year ended December 31, 2016 1. Organization...

67

THIRD POINT OFFSHORE FUND, LTD. FINANCIAL STATEMENTS As of and for the Year Ended December 31, 2016 With Report of Independent Auditors

Transcript of THIRD POINT OFFSHORE FUND, LTD. · 2018-09-20 · Year ended December 31, 2016 1. Organization...

THIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2016

With Report of Independent Auditors

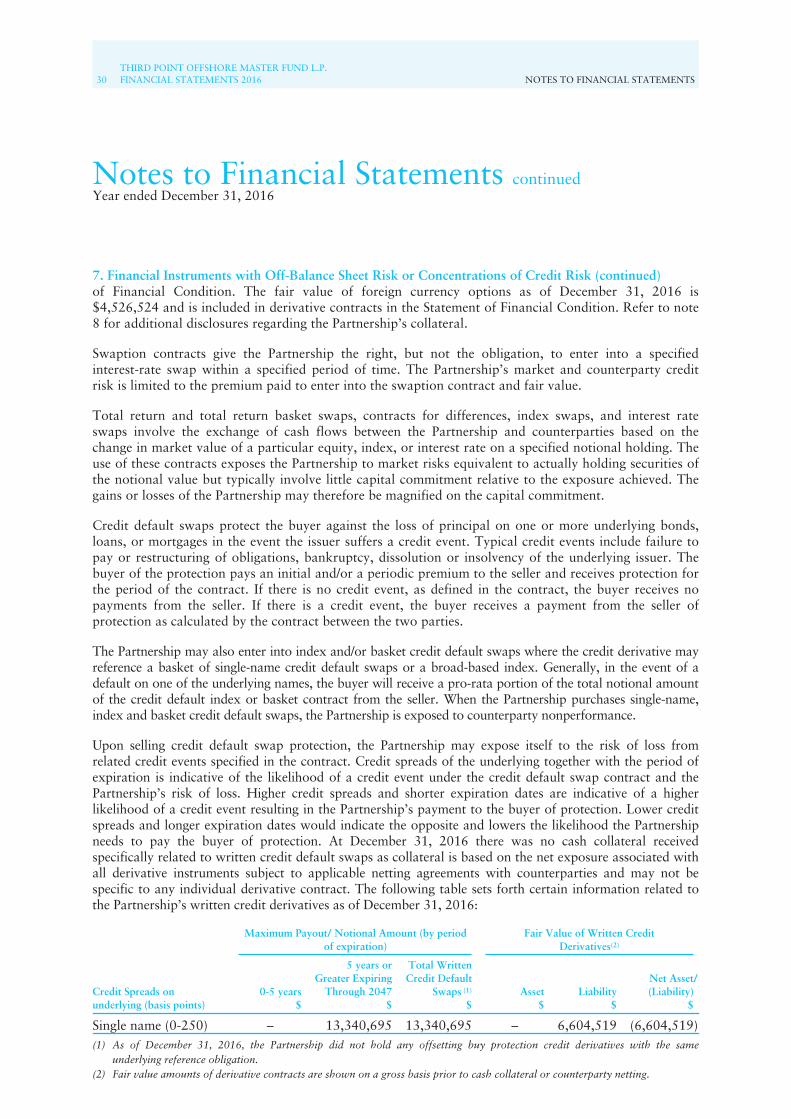

Contents

01 Report of Independent Auditors02 Statement of Assets and Liabilities03 Condensed Schedule of Investments04 Statement of Operations06 Statement of Changes in Net Assets07 Statement of Cash Flows08 Notes to Financial Statements

Financial Statements of Third Point Offshore Master Fund L.P.

REPORT OF INDEPENDENT AUDITORSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 1

Ernst & Young Ltd. 62 Forum Lane Camana BayP.O. Box 510Grand Cayman KY1-1106CAYMAN ISLANDS

Tel: +1 345 949 8444 Fax: +1 345 949 8529 ey.com

Report of Independent Auditors

The Board of DirectorsThird Point Offshore Fund, Ltd.

We have audited the accompanying financial statements of Third Point Offshore Fund, Ltd. whichcomprise the statement of assets and liabilities, including the condensed schedule of investments, as ofDecember 31, 2016, and the related statements of operations, changes in net assets and cash flows forthe year then ended, and the related notes to the financial statements.

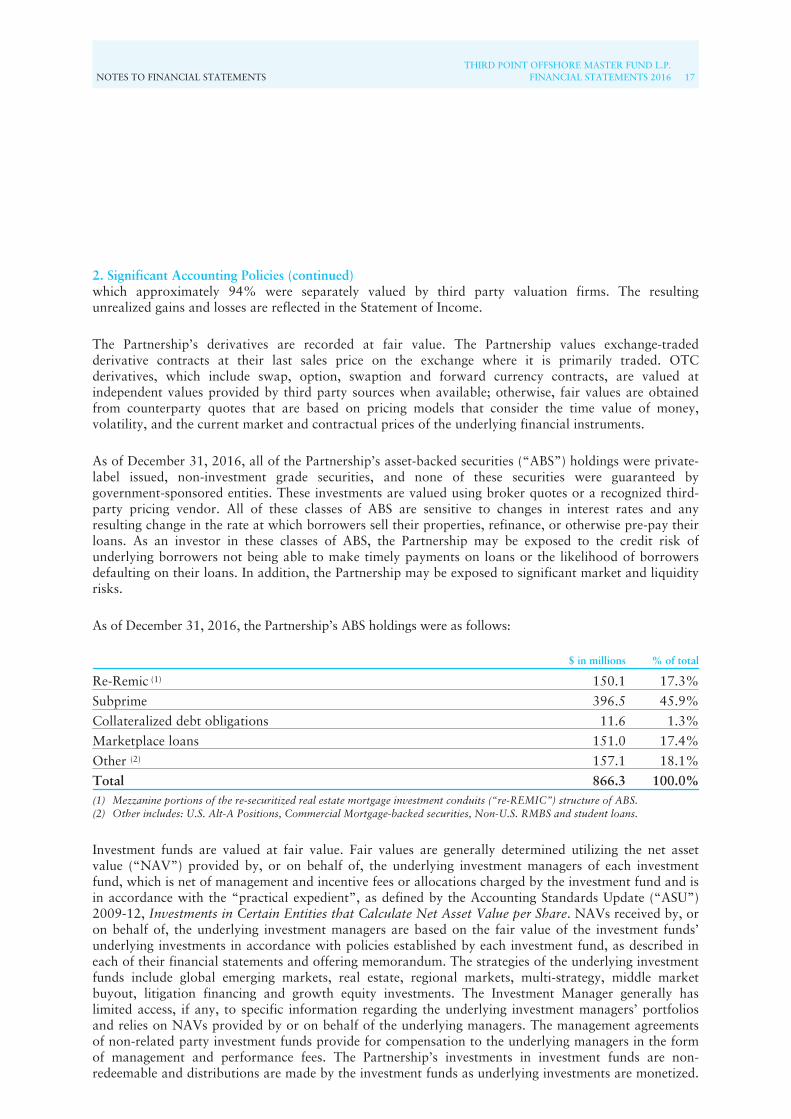

Management’s Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these financial statements inconformity with U.S. generally accepted accounting principles; this includes the design, implementationand maintenance of internal control relevant to the preparation and fair presentation of financialstatements that are free of material misstatement, whether due to fraud or error.

Auditor’s ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audit. Weconducted our audit in accordance with auditing standards generally accepted in the United States. Thosestandards require that we plan and perform the audit to obtain reasonable assurance about whether thefinancial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures inthe financial statements. The procedures selected depend on the auditor’s judgment, including theassessment of the risks of material misstatement of the financial statements, whether due to fraud orerror. In making those risk assessments, the auditor considers internal control relevant to the entity’spreparation and fair presentation of the financial statements in order to design audit procedures that areappropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness ofthe entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluatingthe appropriateness of accounting policies used and the reasonableness of significant accountingestimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour audit opinion.

OpinionIn our opinion, the financial statements referred to above present fairly, in all material respects, thefinancial position of Third Point Offshore Fund, Ltd. at December 31, 2016, and the results of itsoperations, changes in its net assets and its cash flows for the year then ended in conformity with U.S.generally accepted accounting principles.

March 17, 2017

A member firm of Ernst & Young Global Limited

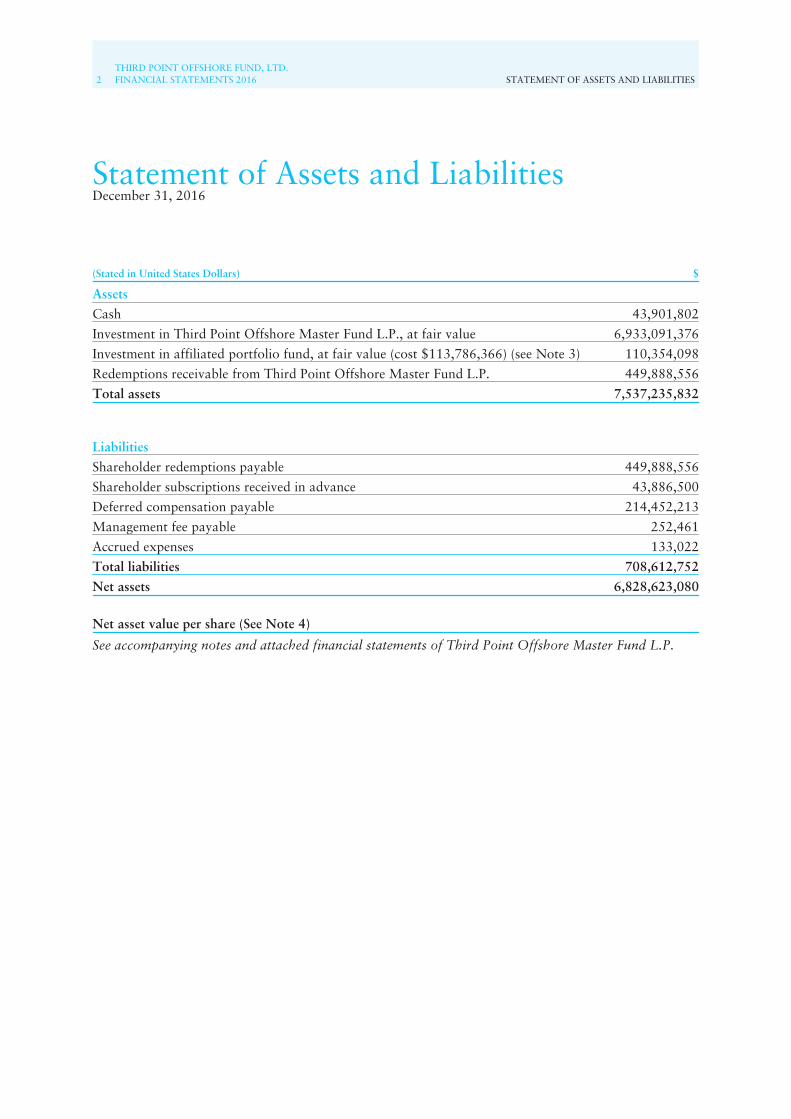

2THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 STATEMENT OF ASSETS AND LIABILITIES

Statement of Assets and LiabilitiesDecember 31, 2016

(Stated in United States Dollars) $

Assets

Cash 43,901,802

Investment in Third Point Offshore Master Fund L.P., at fair value 6,933,091,376

Investment in affiliated portfolio fund, at fair value (cost $113,786,366) (see Note 3) 110,354,098

Redemptions receivable from Third Point Offshore Master Fund L.P. 449,888,556

Total assets 7,537,235,832

Liabilities

Shareholder redemptions payable 449,888,556

Shareholder subscriptions received in advance 43,886,500

Deferred compensation payable 214,452,213

Management fee payable 252,461

Accrued expenses 133,022

Total liabilities 708,612,752

Net assets 6,828,623,080

Net asset value per share (See Note 4)

See accompanying notes and attached financial statements of Third Point Offshore Master Fund L.P.

CONDENSED SCHEDULE OF INVESTMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 3

Condensed Schedule of InvestmentsDecember 31, 2016

(Stated in United States Dollars)Description

Fair Value$

Percentage ofNet Assets

%

Investment in Third Point Offshore Master Fund L.P. 6,933,091,376 101.53

Investment in Affiliated Portfolio Fund

Latin America and the Caribbean:

Multi-Strategy 110,354,098 1.62

Total Investment in Affiliated Portfolio Fund (cost $113,786,366) 110,354,098 1.62

See accompanying notes and attached financial statements of Third Point Offshore Master Fund L.P.

4THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 STATEMENT OF OPERATIONS

Statement of OperationsYear ended December 31, 2016

(Stated in United States Dollars) $

Realized and unrealized gain/(loss) on investment transactions allocated from Third PointOffshore Master Fund L.P.

Net realized gain from securities, affiliated funds, derivative contracts and foreigncurrency translations 222,084,997

Net change in unrealized gain on securities and foreign currency translations 283,517,319

Net change in unrealized gain on affiliated funds and foreign currency translations 2,976,578

Net change in unrealized gain on derivative contracts and foreign currency translations (22,133,392)

Net gain from currencies 7,458,468

Net realized and unrealized gain from investment transactions allocated fromThird Point Offshore Master Fund L.P. 493,903,970

Fund realized and unrealized gain/(loss) on investment

Net change in unrealized gain on affiliated portfolio fund (77,647,012)

Net realized and unrealized loss from investment (77,647,012)

Investment income allocated from Third Point Offshore Master Fund L.P.

Interest 166,232,574

Dividends, net of withholding taxes of $20,687,201 54,613,314

Stock loan fees 237,968

Other 2,630,555

Total investment income allocated from Third Point Offshore Master Fund L.P. 223,714,411

Investment expenses allocated from Third Point Offshore Master Fund L.P.

Incentive fee 79,033,970

Interest 21,833,899

Dividends on securities sold, not yet purchased 6,657,515

Stock borrow fees 3,695,562

Administrative and professional fees 9,111,464

Research fees 6,492,544

Other 5,596,039

Total investment expenses allocated from Third Point Offshore Master Fund L.P. 132,420,993

Net investment income allocated from Third Point Offshore Master Fund L.P. 91,293,418

STATEMENT OF OPERATIONSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 5

(Stated in United States Dollars) $

Fund income

Depreciation of deferred compensation 67,739,092

Total Fund income 67,739,092

Fund expenses

Management fee 145,378,094

Administrative and professional fees 200,335

Other 95,673

Total Fund expenses 145,674,102

Net fund expense (77,935,010)

Net investment income 13,358,408

Net increase in net assets resulting from operations 429,615,366

See accompanying notes and attached financial statements of Third Point Offshore Master Fund L.P.

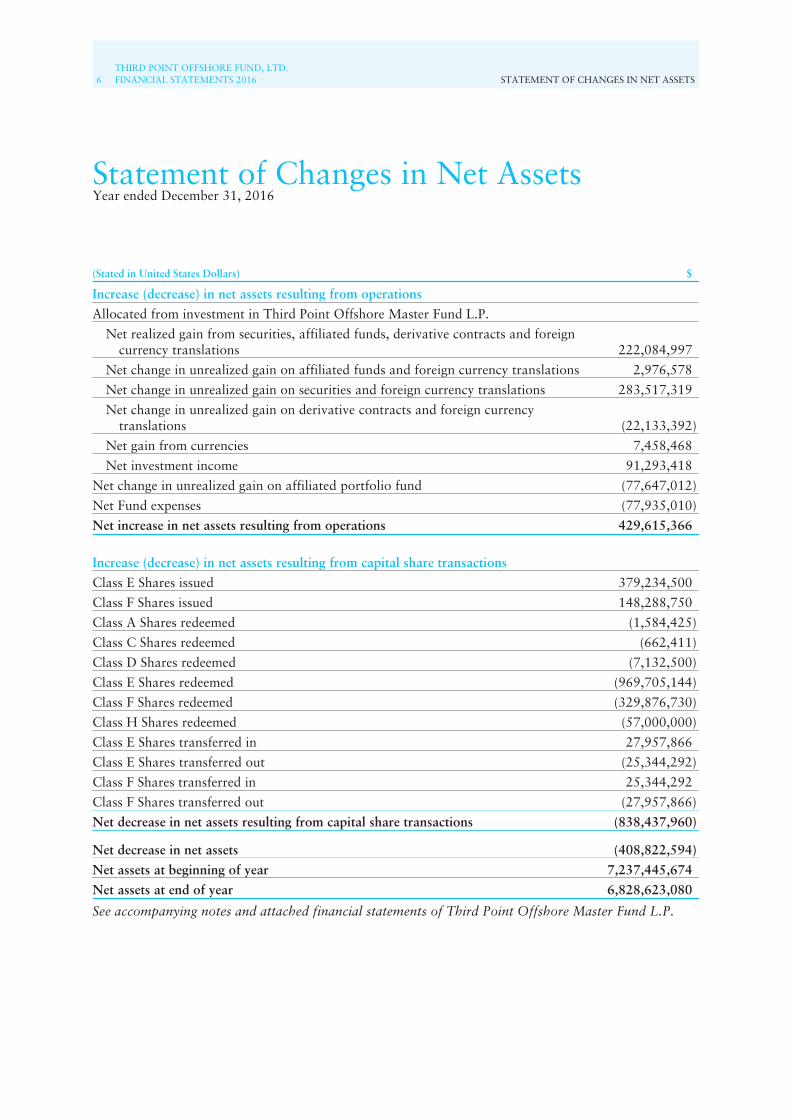

6THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 STATEMENT OF CHANGES IN NET ASSETS

Statement of Changes in Net AssetsYear ended December 31, 2016

(Stated in United States Dollars) $

Increase (decrease) in net assets resulting from operations

Allocated from investment in Third Point Offshore Master Fund L.P.

Net realized gain from securities, affiliated funds, derivative contracts and foreigncurrency translations 222,084,997

Net change in unrealized gain on affiliated funds and foreign currency translations 2,976,578

Net change in unrealized gain on securities and foreign currency translations 283,517,319

Net change in unrealized gain on derivative contracts and foreign currencytranslations (22,133,392)

Net gain from currencies 7,458,468

Net investment income 91,293,418

Net change in unrealized gain on affiliated portfolio fund (77,647,012)

Net Fund expenses (77,935,010)

Net increase in net assets resulting from operations 429,615,366

Increase (decrease) in net assets resulting from capital share transactions

Class E Shares issued 379,234,500

Class F Shares issued 148,288,750

Class A Shares redeemed (1,584,425)

Class C Shares redeemed (662,411)

Class D Shares redeemed (7,132,500)

Class E Shares redeemed (969,705,144)

Class F Shares redeemed (329,876,730)

Class H Shares redeemed (57,000,000)

Class E Shares transferred in 27,957,866

Class E Shares transferred out (25,344,292)

Class F Shares transferred in 25,344,292

Class F Shares transferred out (27,957,866)

Net decrease in net assets resulting from capital share transactions (838,437,960)

Net decrease in net assets (408,822,594)

Net assets at beginning of year 7,237,445,674

Net assets at end of year 6,828,623,080

See accompanying notes and attached financial statements of Third Point Offshore Master Fund L.P.

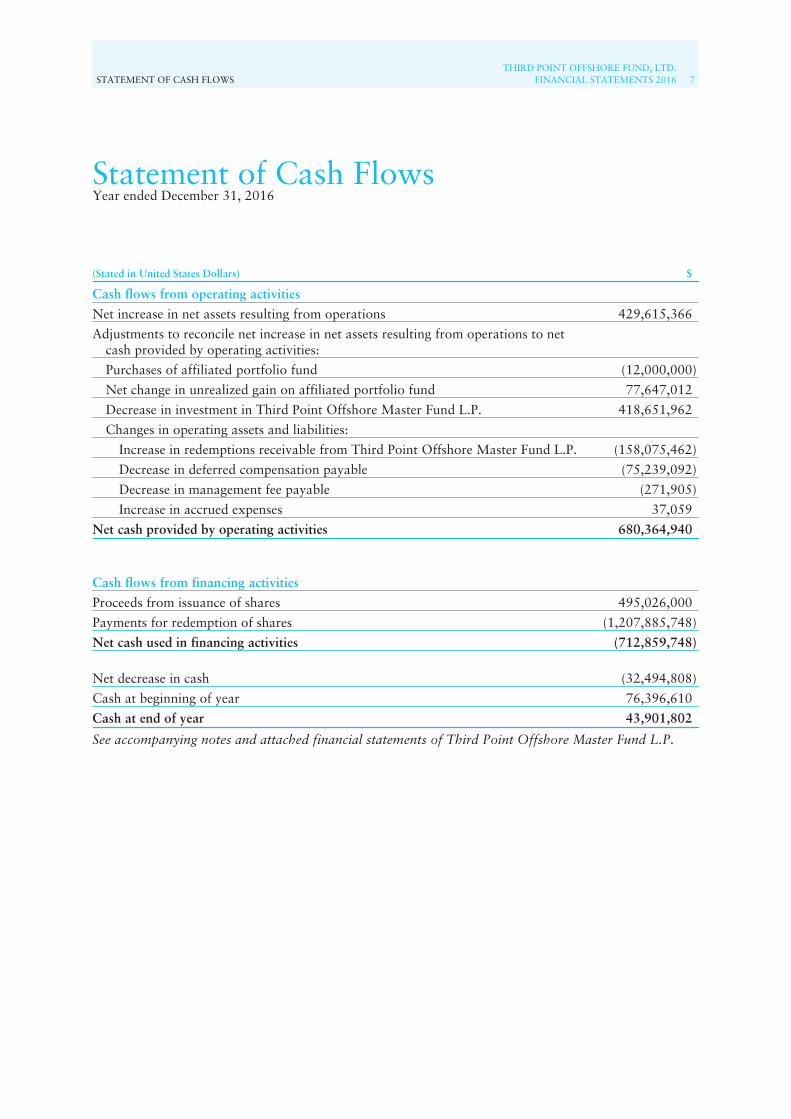

STATEMENT OF CASH FLOWSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 7

Statement of Cash FlowsYear ended December 31, 2016

(Stated in United States Dollars) $

Cash flows from operating activities

Net increase in net assets resulting from operations 429,615,366

Adjustments to reconcile net increase in net assets resulting from operations to netcash provided by operating activities:

Purchases of affiliated portfolio fund (12,000,000)

Net change in unrealized gain on affiliated portfolio fund 77,647,012

Decrease in investment in Third Point Offshore Master Fund L.P. 418,651,962

Changes in operating assets and liabilities:

Increase in redemptions receivable from Third Point Offshore Master Fund L.P. (158,075,462)

Decrease in deferred compensation payable (75,239,092)

Decrease in management fee payable (271,905)

Increase in accrued expenses 37,059

Net cash provided by operating activities 680,364,940

Cash flows from financing activities

Proceeds from issuance of shares 495,026,000

Payments for redemption of shares (1,207,885,748)

Net cash used in financing activities (712,859,748)

Net decrease in cash (32,494,808)

Cash at beginning of year 76,396,610

Cash at end of year 43,901,802

See accompanying notes and attached financial statements of Third Point Offshore Master Fund L.P.

8THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial StatementsYear ended December 31, 2016

1. OrganizationThird Point Offshore Fund, Ltd. (the “Fund”) was incorporated under the laws of the Cayman Islandson October 21, 1996, commenced operations on December 1, 1996 and is registered under the CaymanIslands Mutual Funds Law and with the Cayman Islands Monetary Authority. The Fund’s objective is toseek to generate consistent long-term capital appreciation.

The Fund invests substantially all of its net assets in Third Point Offshore Master Fund L.P., anexempted limited partnership formed under the laws of the Cayman Islands (the “Master Partnership”),which, in turn conducts substantially all investment and trading activities on behalf of the Fund. ThirdPoint Advisors II L.L.C. (the “General Partner”), a limited liability company formed under the laws ofthe State of Delaware and an affiliate of Third Point LLC, serves as the general partner of the MasterPartnership.

Third Point LLC (the “Investment Manager”) is the Investment Manager of the Fund and the MasterPartnership. The Investment Manager is registered with the Securities and Exchange Commission as anInvestment Adviser under the Investment Advisers Act of 1940. The Investment Manager is responsiblefor the operation and management of the Fund.

The Fund is an investment company and applies specialized accounting guidance as outlined in FinancialServices – Investment Companies (Topic 946). The Investment Manager evaluated this guidance anddetermined that the Fund meets the criteria to be classified as an investment company. Accordingly, theFund reflects its investments in the Statement of Assets and Liabilities at their estimated fair value, withunrealized gains and losses resulting from changes in fair value, if any, reflected in net change inunrealized gain/loss on securities, affiliated portfolio fund, affiliated funds, derivative contracts andforeign currency translations in the Statement of Operations.

International Fund Services (Ireland) Limited serves as the administrator (the “Administrator”) andtransfer agent to the Fund.

2. Significant Accounting PoliciesThe Fund’s financial statements have been prepared in accordance with U.S. generally acceptedaccounting principles (“U.S. GAAP”) and are expressed in United States dollars. The following is asummary of the significant accounting and reporting policies:

The Fund is exempt from all forms of taxation in the Cayman Islands, including income, capital gainsand withholding taxes. In jurisdictions other than the Cayman Islands, in some cases foreign taxes will bewithheld at source on dividends and certain interest received by the Fund. Capital gains derived by theFund in such jurisdictions generally will be exempt from foreign income or withholding taxes at thesource.

The Investment Manager has reviewed the Fund’s tax positions in accordance with Accounting forUncertainty in Income Taxes and has concluded that no material provision for income tax is required inthe Fund’s financial statements. Generally, the Fund is subject to income tax examinations by majortaxing authorities including United States and other authorities for open tax years since inception.

The Fund would recognize interest and penalties, if any, related to unrecognized tax positions as incometax expense in the Statement of Operations. During the year ended December 31, 2016, the Fund did notincur any interest or penalties.

See attached financial statements of Third Point Offshore Master Fund L.P.

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 9

2. Significant Accounting Policies (continued)The Fund records securities transactions and related income and expense on a trade-date basis. Realizedgains and losses are determined using cost calculated on a specific identification basis. Dividends arerecorded on the ex-dividend date. Income and expenses, including interest income and expenses, arerecorded on the accrual basis.

The fair value of the Fund’s assets and liabilities, which qualify as financial instruments, approximatesthe carrying amounts presented in the Statement of Assets and Liabilities.

The preparation of financial statements in conformity with U.S. GAAP requires management to makeestimates and assumptions that affect the amounts and disclosures in the financial statements andaccompanying notes. Actual results could differ from these estimates.

The Fund’s investment in the Master Partnership is valued at fair value, which is represented by theFund’s proportionate interest in the Partners’ Capital of the Master Partnership, which was$6,933,091,376 at December 31, 2016. The fair value represents the amount the Fund would expect toreceive at December 31, 2016 if it were to liquidate its investment in the Master Partnership. The percentof the Master Partnership owned by the Fund at December 31, 2016 was approximately 99.45%. TheFund’s allocated share of each item of the Master Partnership’s income and expense is reflected in theaccompanying Statement of Operations. The performance of the Fund is directly affected by theperformance of the Master Partnership and is subject to the same risks to which the Master Partnershipis subject. Attached are the audited financial statements of the Master Partnership.

Valuation of investments held by the Master Partnership is discussed in the notes to the MasterPartnership’s audited financial statements. The Fund records monthly its proportionate share of theMaster Partnership’s income, expenses, and realized and unrealized gains and losses. In addition, theFund accrues its own income and expenses. The Fund records subscriptions and redemptions related toits investment in the Master Partnership on the transaction date.

The investment in affiliated portfolio fund is valued at fair value. Fair value is defined as the price thatthe Fund would receive to sell an asset or pay to transfer a liability in an orderly transaction betweenmarket participants at the measurement date. The disclosure requirements also establish a framework formeasuring fair value, and a three-level hierarchy for fair value measurements based upon thetransparency of inputs to the valuation of an asset or liability. The three-tier hierarchy of inputs issummarized below:

• Level 1 – Quoted prices available in active markets/exchanges for identical investments as of thereporting date. The types of assets and liabilities that are classified at this level generally include listedinvestment funds.

• Level 2 – Pricing inputs other than observable inputs including but not limited to prices quoted forsimilar assets or liabilities in active markets/exchanges or prices quoted for identical or similar assets orliabilities in markets that are not active, and fair value is determined through the use of models or othervaluation methodologies. The types of assets and liabilities that are classified at this level generallyinclude non-exchange listed investment funds with immediate liquidity.

• Level 3 – Pricing inputs are unobservable due to little, if any, market activity for the investment. Theinputs into determination of fair value require significant management judgment and estimation. Thetypes of assets and liabilities that are classified at this level generally include non-exchange traded illiquidinvestment funds.

See attached financial statements of Third Point Offshore Master Fund L.P.

10THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial Statements continuedYear ended December 31, 2016

2. Significant Accounting Policies (continued)Inputs refer broadly to the assumptions that market participants would use in pricing the asset orliability, including assumptions about risk, for example, the risk inherent in a particular valuationtechnique used to measure fair value including such a pricing model and/or the risk inherent in the inputsto the valuation technique. Inputs may be observable or unobservable.

Observable inputs are inputs that reflect the assumptions market participants would use in pricing theasset or liability based on market data obtained from sources independent of the reporting entity.Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptionsmarket participants would use in pricing the asset or liability developed based on the best informationavailable in the circumstances.

In certain cases, the inputs used to measure fair value may fall into different levels of the fair valuehierarchy. In such cases, an investment’s level within the fair value hierarchy is based on the lowest levelof input that is significant to the fair value measurement. The Investment Manager’s assessment of thesignificance of a particular input to the fair value measurement in its entirety requires judgment, andconsiders factors specific to the investment.

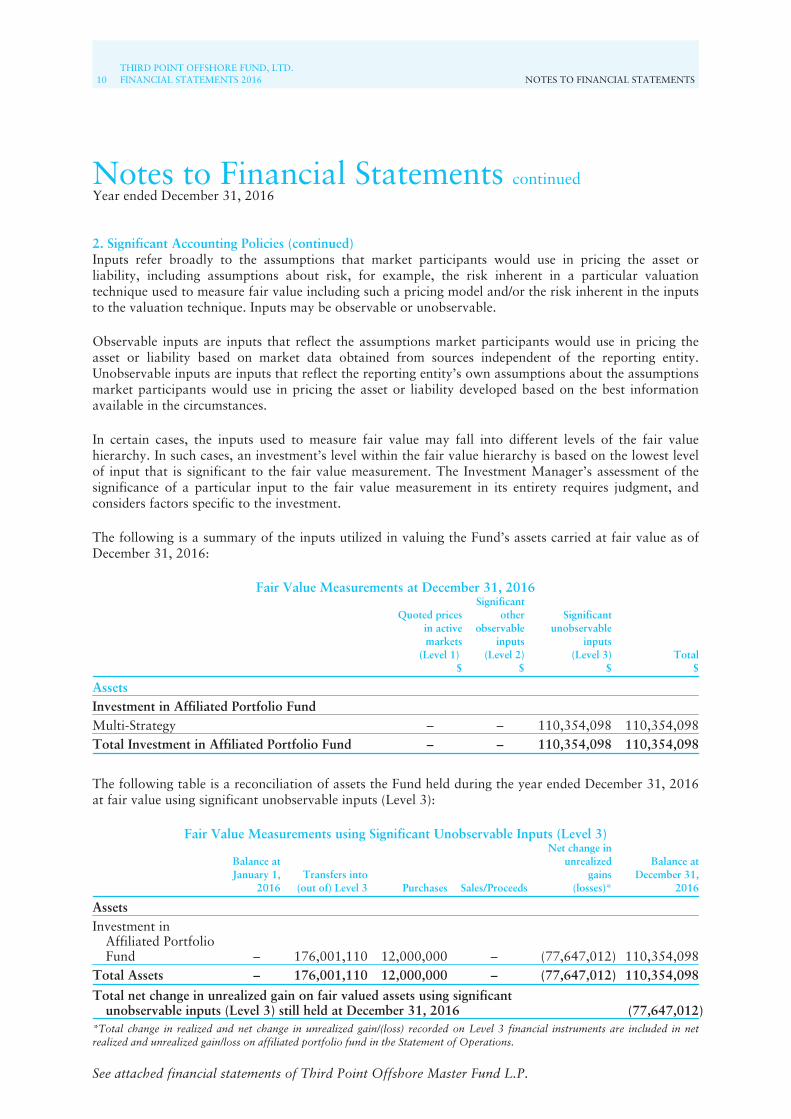

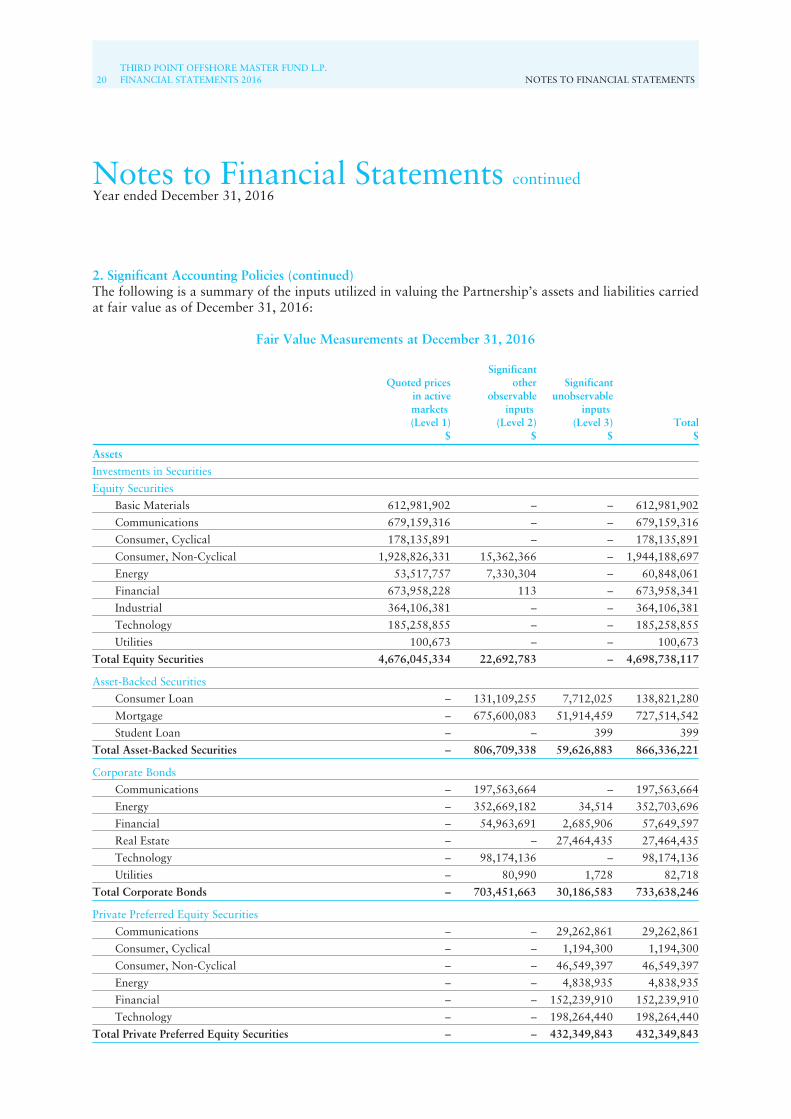

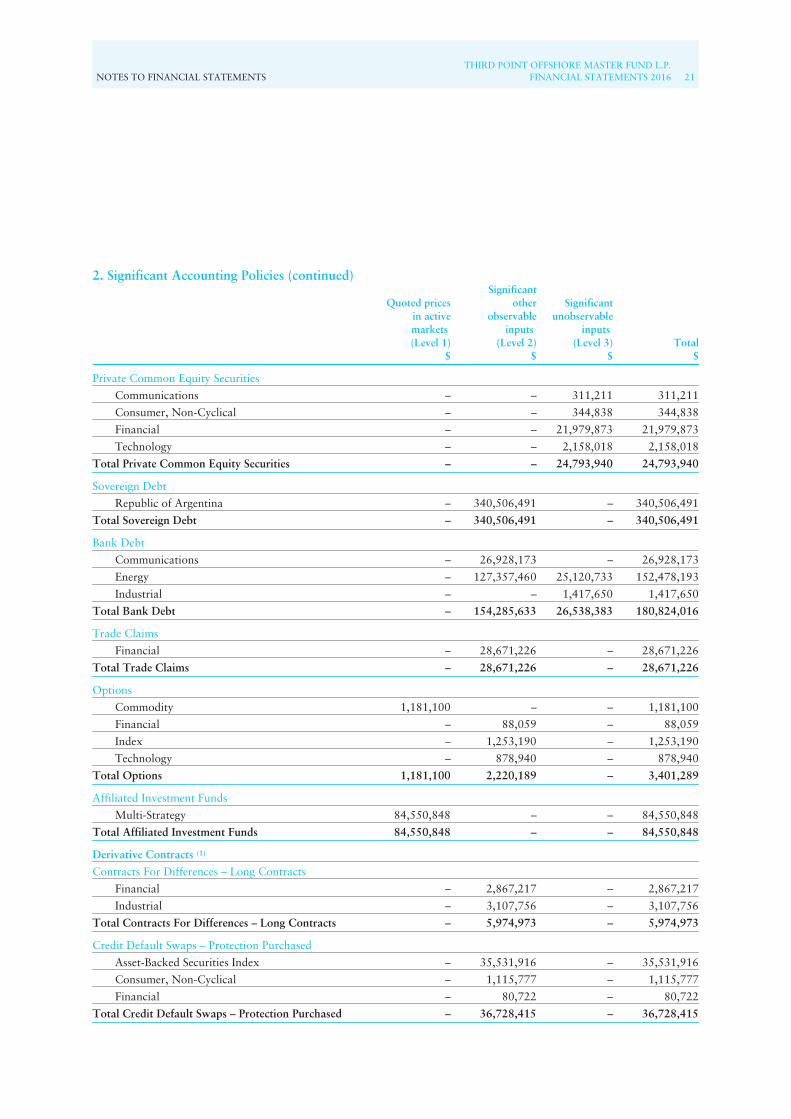

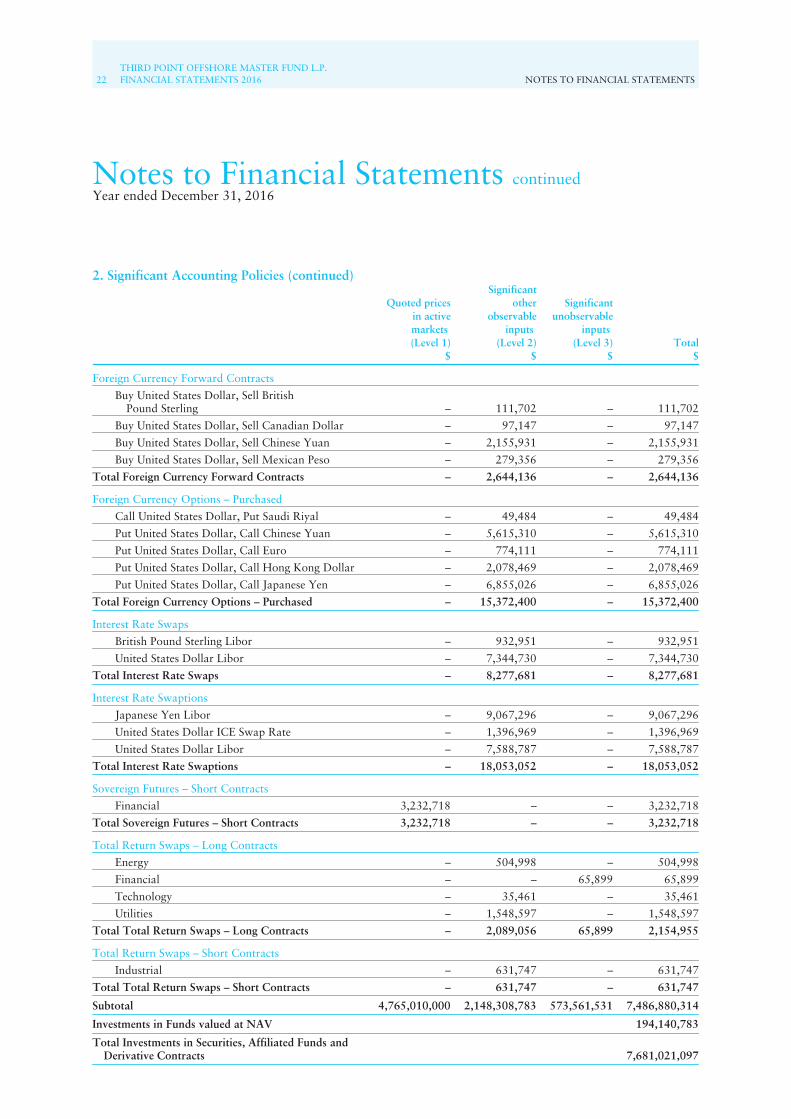

The following is a summary of the inputs utilized in valuing the Fund’s assets carried at fair value as ofDecember 31, 2016:

Fair Value Measurements at December 31, 2016

Quoted pricesin activemarkets

(Level 1)$

Significantother

observableinputs

(Level 2)$

Significantunobservable

inputs(Level 3)

$Total

$

AssetsInvestment in Affiliated Portfolio FundMulti-Strategy – – 110,354,098 110,354,098Total Investment in Affiliated Portfolio Fund – – 110,354,098 110,354,098

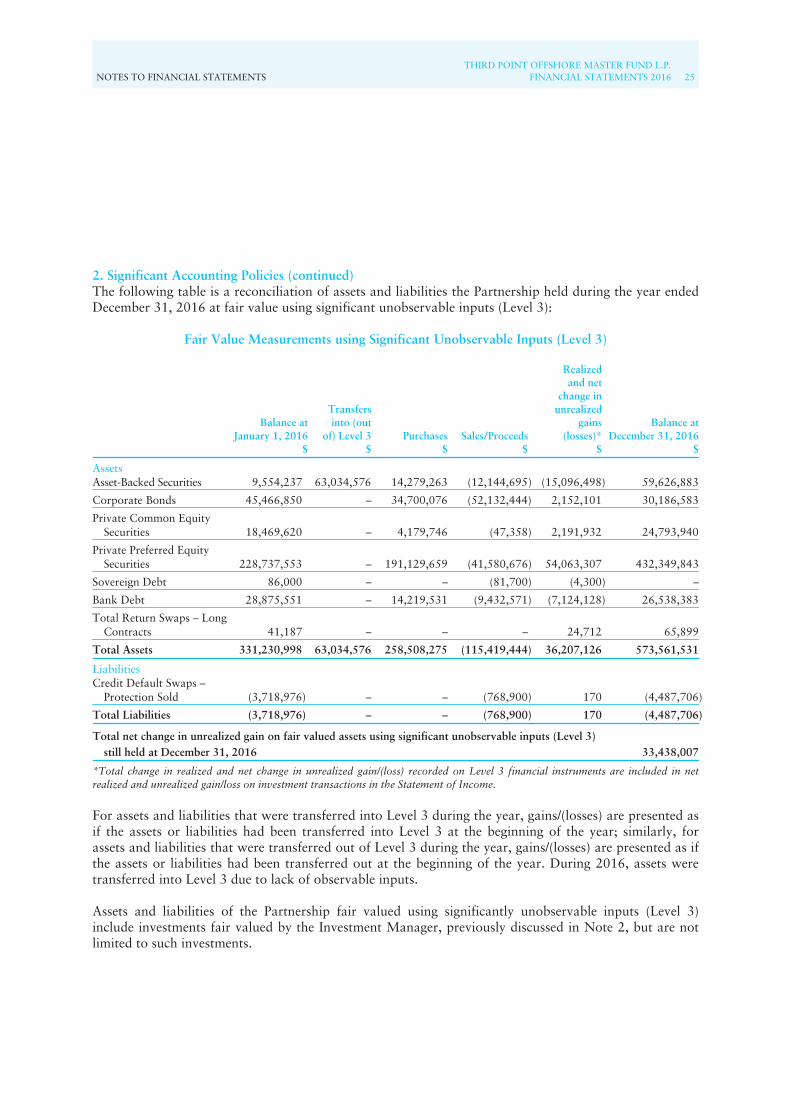

The following table is a reconciliation of assets the Fund held during the year ended December 31, 2016at fair value using significant unobservable inputs (Level 3):

Fair Value Measurements using Significant Unobservable Inputs (Level 3)

Balance atJanuary 1,

2016Transfers into

(out of) Level 3 Purchases Sales/Proceeds

Net change inunrealized

gains(losses)*

Balance atDecember 31,

2016

AssetsInvestment in

Affiliated PortfolioFund – 176,001,110 12,000,000 – (77,647,012) 110,354,098

Total Assets – 176,001,110 12,000,000 – (77,647,012) 110,354,098

Total net change in unrealized gain on fair valued assets using significantunobservable inputs (Level 3) still held at December 31, 2016 (77,647,012)

*Total change in realized and net change in unrealized gain/(loss) recorded on Level 3 financial instruments are included in netrealized and unrealized gain/loss on affiliated portfolio fund in the Statement of Operations.

See attached financial statements of Third Point Offshore Master Fund L.P.

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 11

2. Significant Accounting Policies (continued)For assets that were transferred into Level 3 during the year, gains/(losses) are presented as if the assetshad been transferred into Level 3 at the beginning of the year. During 2016, assets were transferred intoLevel 3 due to lack of observable inputs.

The Investment Manager employs a third party valuation firm to conduct a separate valuation of theaffiliated portfolio fund. The third party valuation firm provided the Investment Manager with a writtenreport documenting their recommended valuation as of the determination date for the specifiedinvestment. In the determination of fair value of the affiliated portfolio fund, a significant unobservableinput was used. A 26% discount was applied to the net asset value of the affiliated portfolio fund inorder to account for lack of marketability. As of December 31, 2016, the fair value of the affiliated fundwas $110,354,098.

3. Related Party TransactionsPursuant to the investment management agreement, the Fund pays the Investment Manager amanagement fee equal to 2% per annum of the net asset value of the Class A, B, C, D, E, F and H shares,and 2.5% per annum of the net asset value of the Class J shares as of the beginning of each month beforethe accrual of any incentive fee. The Investment Manager, in its sole discretion, may elect to reduce,waive or calculate differently the management fee with respect to partners, members, employees,affiliates or other related investors of the Investment Manager or the General Partner. For the year endedDecember 31, 2016, the management fee expense was $145,378,094, of which $252,461 was payable atDecember 31, 2016.

As set forth in the Agreement, certain fees including closing, directors’, or break-up fees paid to theInvestment Manager or its affiliates as a result of the Fund’s investments will be treated as an offsetagainst the Fund’s management fees. For the year ended December 31, 2016, $52,815 of fees weretreated as an offset against the management fee.

The Fund pays an incentive fee to the Investment Manager, allocated to the General Partner of the MasterPartnership, equal to 20% of the annual increase in the aggregate net asset value of each series of Class A,B, C, D, E, F and H shares and 25% of the annual increase in the aggregate net asset value of each seriesfor Class J shares (each the “Full Incentive Fee”). The incentive fee is accrued monthly and allocated to theGeneral Partner of the Master Partnership at the end of each fiscal year. The incentive fee is calculated in amanner which ensures that appropriate adjustments are made in order to accommodate the inflows andoutflows of capital during the course of each fiscal year resulting from shareholder subscriptions andredemptions. If a particular series depreciates during any fiscal year and during subsequent years there is aprofit attributable to such series, the series must recover an amount equal to 2.5 times the amount ofdepreciation in the prior years before the General Partner of the Master Partnership is entitled to the FullIncentive Fee allocation. Until this occurs, the series will be subject to a reduced incentive fee equal to halfof the Full Incentive Fee.

Prior to January 1, 2009 and pursuant to the provisions of the Investment Manager’s deferred incentivefee agreement (the “Deferred Fee Agreement”), the Investment Manager was able to elect to defer thereceipt of all or a portion of the incentive fee, if any, earned with respect to a particular fiscal year, andwas able to elect to have a portion or all of the deferred fee invested in either the same manner as theFund’s assets, or in another manner approved by the Fund. The value of such deferred amountsconstitutes a liability of the Fund to the Investment Manager. Any amounts invested under the provisionsof the Deferred Fee Agreement continue for all purposes to be part of the general assets of the Fund, andthe Investment Manager has no property interest in any of such assets. For the year endedDecember 31, 2016, the Investment Manager redeemed $7,500,000 attributable to deferredcompensation earned in prior years. As of December 31, 2016, the deferred compensation payable was$214,452,213 and is scheduled for distribution in 2017. For the year ended December 31, 2016, thedeferred compensation payable depreciated $67,739,092.

See attached financial statements of Third Point Offshore Master Fund L.P.

12THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial Statements continuedYear ended December 31, 2016

3. Related Party Transactions (continued)In relation to the Deferred Fee Agreement, the Fund was invested in an affiliated portfolio fund duringthe year ended December 31, 2016. The resulting net gains or losses of such investments are reflected inthe Statement of Operations and allocated strictly to the deferred compensation payable accountreflected in the Statement of Assets and Liabilities. The value of the affiliated portfolio fund atDecember 31, 2016 was $110,354,098.

As of December 31, 2016, the Partnership had a balance of $1,585 due to the Investment Manager. Inaccordance with the Partnership Agreement, this amount is related to professional fees paid by theInvestment Manager on behalf of the Partnership and is included in accrued expenses in the Statement ofAssets and Liabilities. For the year ended December 31, 2016, the Investment Manager paid $4,000 ofprofessional fees on behalf of the Partnership, which are included in administrative and professional feesand other expenses in the Statement of Operations. The amounts are non-interest bearing and areintended to be reimbursed by the Partnership through distributions of current income and dispositionproceeds.

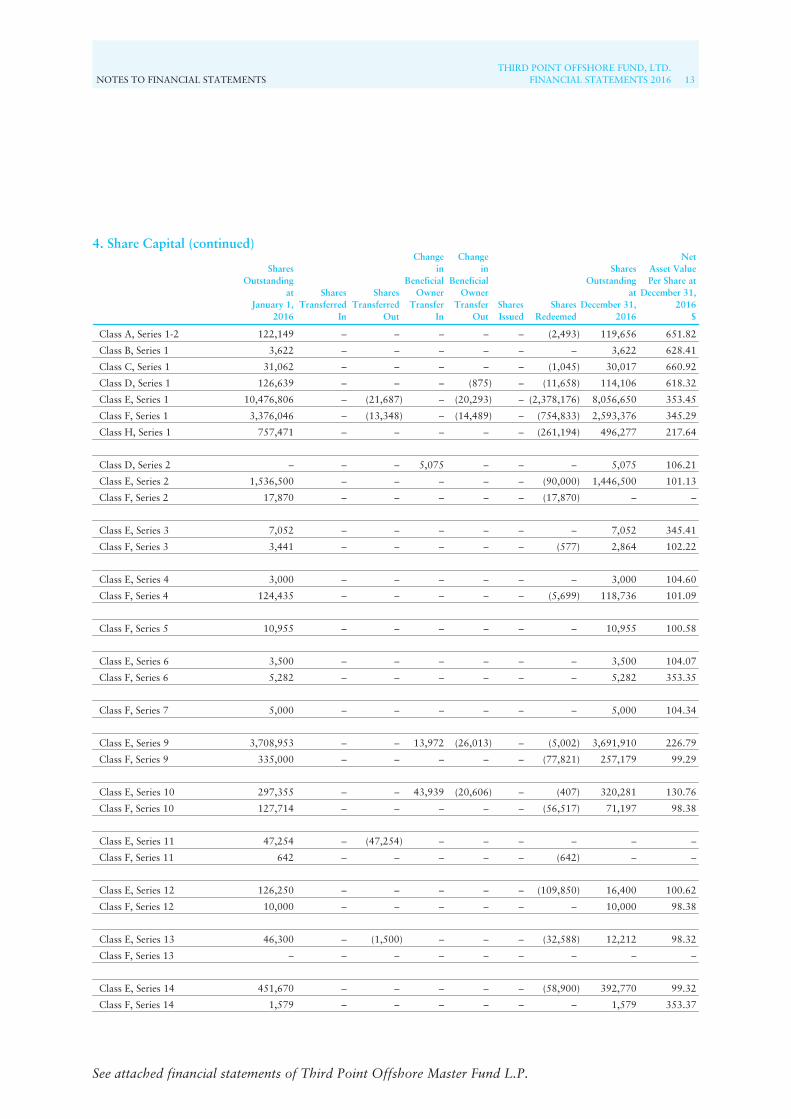

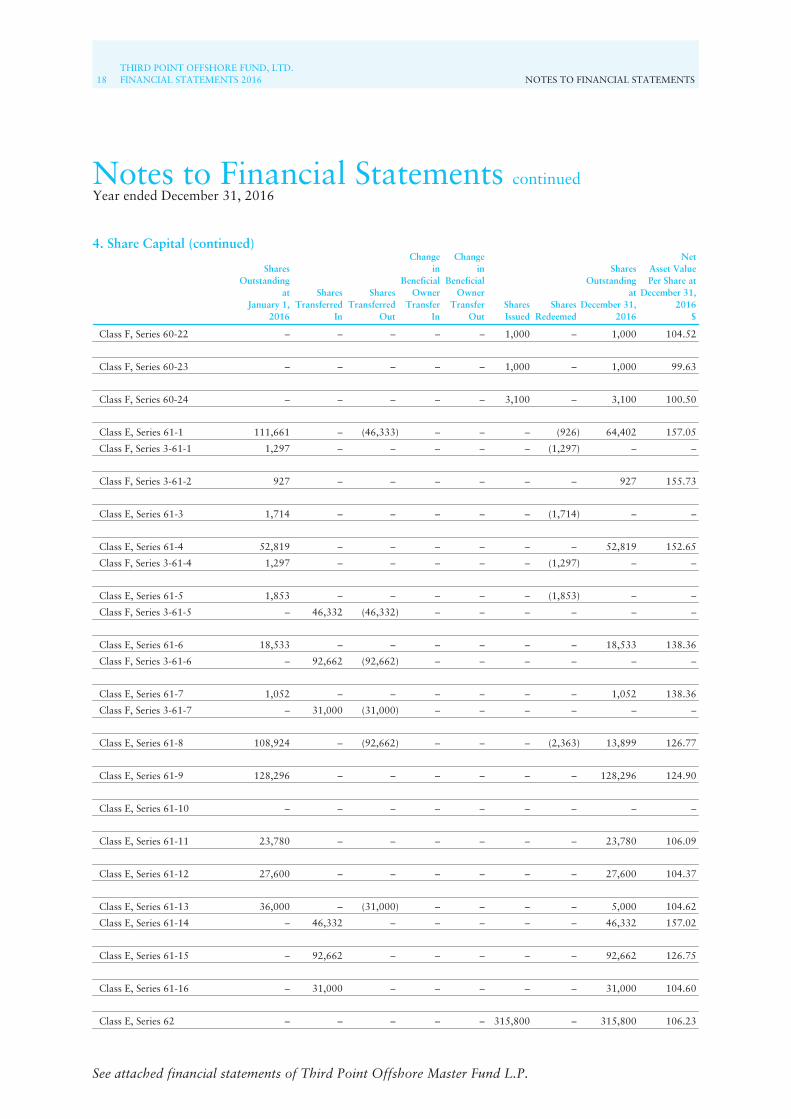

4. Share CapitalThe Fund has an authorized share capital consisting of $2,000,000 divided into 200,000,000participating shares of $0.01 each. The Fund issues a separate series of shares to those investors whopurchase shares as of the first business day of each month. A different series of shares is issued in orderto equitably reflect the differing incentive fees attributable to each series because of the differing issuedates throughout the fiscal year. Shares are offered in series at a purchase price of $100 per share. AtDecember 31, 2016, there were seven outstanding classes (each, a “Class”) of shares: Class A, B, C, D, E,F and H and within each class there is one or more separate series. Each share is equal to every othershare of the same series with respect to earnings, assets, dividends and voting privileges. Class E and Fare currently offered. Class B, D and F shares will in aggregate participate only up to 10% of profits andlosses from “new issues”.

Class A and B shares have monthly redemption rights. Class C, D, E, F and H shares have quarterlyredemption rights. Redemptions made during the initial subscription year are subject to a redemption feeequal to 5% of the redemption proceeds for Class D, E and H shares. The redemption fee is for thebenefit of the Fund and proceeds are allocated on a pro-rata basis to the remaining shareholders. Allredemption rights are subject to an overall limit, at the discretion of the Fund’s Board of Directors, ofaggregate redemptions in any calendar quarter of 20% of the Fund’s NAV as of the first day of suchcalendar quarter.

The Board of Directors has the right to create additional classes, series and sub-series for an investor as itdetermines appropriate in its sole discretion. Each series of a Class will have equal rights and privilegeswith each other series of that Class.

If at the end of a fiscal year, a series of a class of shares is charged a Full Incentive Fee, the shares of suchseries may be redesignated and converted on the first business day following the end of the fiscal yearinto the first series of such class at the prevailing net asset value of such series. No redesignation orconversion shall occur with respect to a series of a class if at the end of a fiscal year such series has notbeen charged a Full Incentive Fee.

The Fund may invest, directly or indirectly, in equity securities in initial public offerings deemed “newissues” under Rule 5130 of the Financial Industry Regulatory Authority (“FINRA”) ConsolidatedRulebook. “New issues” are defined as any initial public offering of an equity, regardless of whethersuch security is trading at a premium in the secondary market. FINRA members generally may not sell“new issues” to an account, in which certain persons or entities designated as restricted persons havebeneficial interest.

See attached financial statements of Third Point Offshore Master Fund L.P.

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 13

See attached financial statements of Third Point Offshore Master Fund L.P.

SharesOutstanding

atJanuary 1,

2016

SharesTransferred

In

SharesTransferred

Out

Changein

BeneficialOwner

TransferIn

Changein

BeneficialOwner

TransferOut

SharesIssued

SharesRedeemed

SharesOutstanding

atDecember 31,

2016

NetAsset ValuePer Share at

December 31,2016

$

Class A, Series 1-2 122,149 – – – – – (2,493) 119,656 651.82

Class B, Series 1 3,622 – – – – – – 3,622 628.41

Class C, Series 1 31,062 – – – – – (1,045) 30,017 660.92

Class D, Series 1 126,639 – – – (875) – (11,658) 114,106 618.32

Class E, Series 1 10,476,806 – (21,687) – (20,293) – (2,378,176) 8,056,650 353.45

Class F, Series 1 3,376,046 – (13,348) – (14,489) – (754,833) 2,593,376 345.29

Class H, Series 1 757,471 – – – – – (261,194) 496,277 217.64

Class D, Series 2 – – – 5,075 – – – 5,075 106.21

Class E, Series 2 1,536,500 – – – – – (90,000) 1,446,500 101.13

Class F, Series 2 17,870 – – – – – (17,870) – –

Class E, Series 3 7,052 – – – – – – 7,052 345.41

Class F, Series 3 3,441 – – – – – (577) 2,864 102.22

Class E, Series 4 3,000 – – – – – – 3,000 104.60

Class F, Series 4 124,435 – – – – – (5,699) 118,736 101.09

Class F, Series 5 10,955 – – – – – – 10,955 100.58

Class E, Series 6 3,500 – – – – – – 3,500 104.07

Class F, Series 6 5,282 – – – – – – 5,282 353.35

Class F, Series 7 5,000 – – – – – – 5,000 104.34

Class E, Series 9 3,708,953 – – 13,972 (26,013) – (5,002) 3,691,910 226.79

Class F, Series 9 335,000 – – – – – (77,821) 257,179 99.29

Class E, Series 10 297,355 – – 43,939 (20,606) – (407) 320,281 130.76

Class F, Series 10 127,714 – – – – – (56,517) 71,197 98.38

Class E, Series 11 47,254 – (47,254) – – – – – –

Class F, Series 11 642 – – – – – (642) – –

Class E, Series 12 126,250 – – – – – (109,850) 16,400 100.62

Class F, Series 12 10,000 – – – – – – 10,000 98.38

Class E, Series 13 46,300 – (1,500) – – – (32,588) 12,212 98.32

Class F, Series 13 – – – – – – – – –

Class E, Series 14 451,670 – – – – – (58,900) 392,770 99.32

Class F, Series 14 1,579 – – – – – – 1,579 353.37

4. Share Capital (continued)

14THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial Statements continuedYear ended December 31, 2016

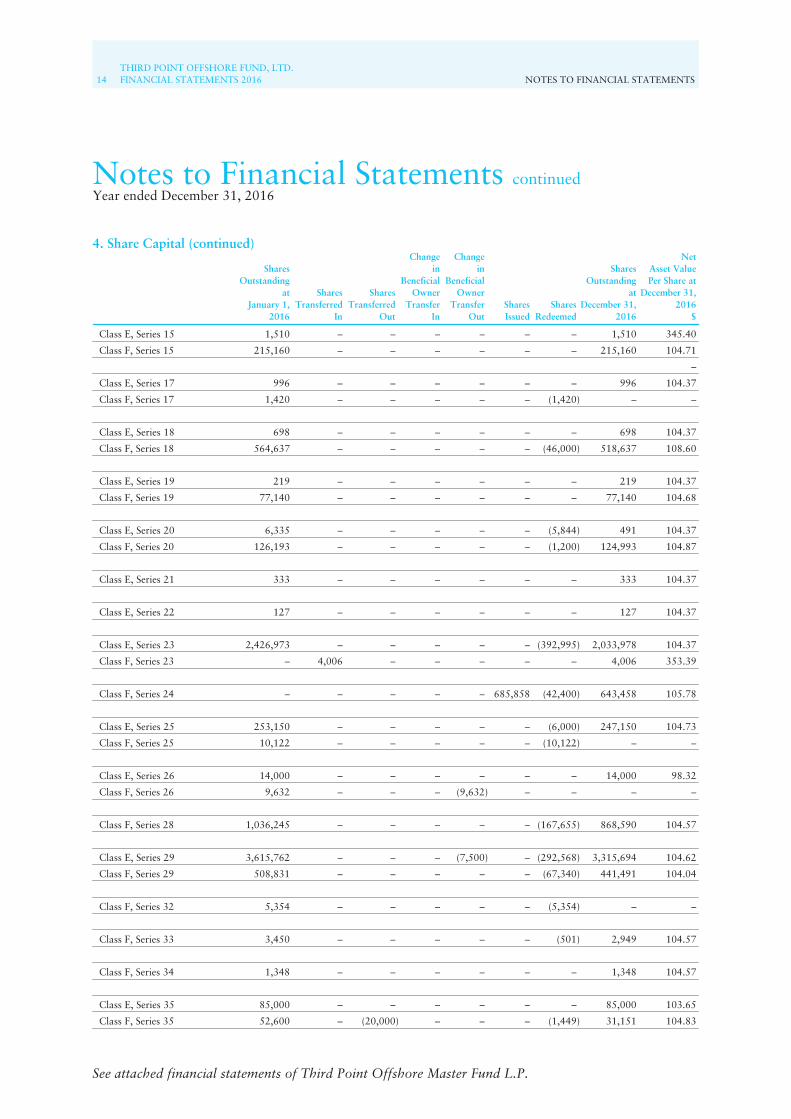

4. Share Capital (continued)

SharesOutstanding

atJanuary 1,

2016

SharesTransferred

In

SharesTransferred

Out

Changein

BeneficialOwner

TransferIn

Changein

BeneficialOwner

TransferOut

SharesIssued

SharesRedeemed

SharesOutstanding

atDecember 31,

2016

NetAsset ValuePer Share at

December 31,2016

$

Class E, Series 15 1,510 – – – – – – 1,510 345.40

Class F, Series 15 215,160 – – – – – – 215,160 104.71

–

Class E, Series 17 996 – – – – – – 996 104.37

Class F, Series 17 1,420 – – – – – (1,420) – –

Class E, Series 18 698 – – – – – – 698 104.37

Class F, Series 18 564,637 – – – – – (46,000) 518,637 108.60

Class E, Series 19 219 – – – – – – 219 104.37

Class F, Series 19 77,140 – – – – – – 77,140 104.68

Class E, Series 20 6,335 – – – – – (5,844) 491 104.37

Class F, Series 20 126,193 – – – – – (1,200) 124,993 104.87

Class E, Series 21 333 – – – – – – 333 104.37

Class E, Series 22 127 – – – – – – 127 104.37

Class E, Series 23 2,426,973 – – – – – (392,995) 2,033,978 104.37

Class F, Series 23 – 4,006 – – – – – 4,006 353.39

Class F, Series 24 – – – – – 685,858 (42,400) 643,458 105.78

Class E, Series 25 253,150 – – – – – (6,000) 247,150 104.73

Class F, Series 25 10,122 – – – – – (10,122) – –

Class E, Series 26 14,000 – – – – – – 14,000 98.32

Class F, Series 26 9,632 – – – (9,632) – – – –

Class F, Series 28 1,036,245 – – – – – (167,655) 868,590 104.57

Class E, Series 29 3,615,762 – – – (7,500) – (292,568) 3,315,694 104.62

Class F, Series 29 508,831 – – – – – (67,340) 441,491 104.04

Class F, Series 32 5,354 – – – – – (5,354) – –

Class F, Series 33 3,450 – – – – – (501) 2,949 104.57

Class F, Series 34 1,348 – – – – – – 1,348 104.57

Class E, Series 35 85,000 – – – – – – 85,000 103.65

Class F, Series 35 52,600 – (20,000) – – – (1,449) 31,151 104.83

See attached financial statements of Third Point Offshore Master Fund L.P.

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 15

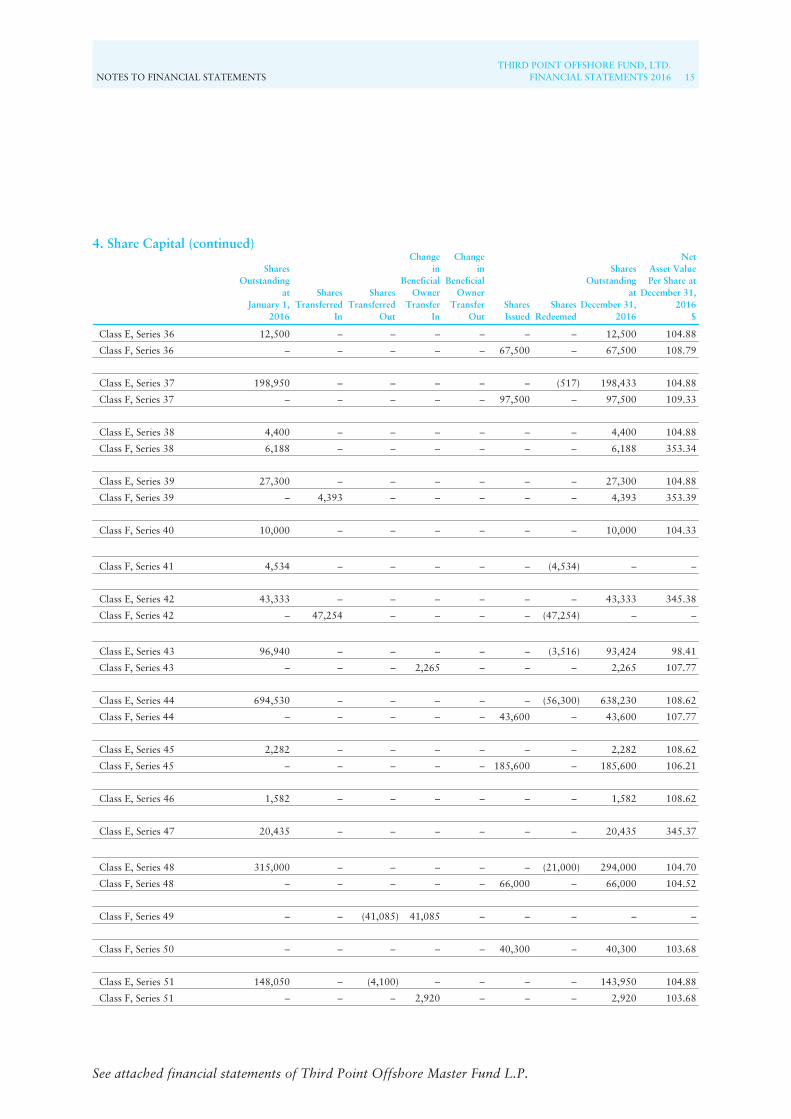

4. Share Capital (continued)

SharesOutstanding

atJanuary 1,

2016

SharesTransferred

In

SharesTransferred

Out

Changein

BeneficialOwner

TransferIn

Changein

BeneficialOwner

TransferOut

SharesIssued

SharesRedeemed

SharesOutstanding

atDecember 31,

2016

NetAsset ValuePer Share at

December 31,2016

$

Class E, Series 36 12,500 – – – – – – 12,500 104.88

Class F, Series 36 – – – – – 67,500 – 67,500 108.79

Class E, Series 37 198,950 – – – – – (517) 198,433 104.88

Class F, Series 37 – – – – – 97,500 – 97,500 109.33

Class E, Series 38 4,400 – – – – – – 4,400 104.88

Class F, Series 38 6,188 – – – – – – 6,188 353.34

Class E, Series 39 27,300 – – – – – – 27,300 104.88

Class F, Series 39 – 4,393 – – – – – 4,393 353.39

Class F, Series 40 10,000 – – – – – – 10,000 104.33

Class F, Series 41 4,534 – – – – – (4,534) – –

Class E, Series 42 43,333 – – – – – – 43,333 345.38

Class F, Series 42 – 47,254 – – – – (47,254) – –

Class E, Series 43 96,940 – – – – – (3,516) 93,424 98.41

Class F, Series 43 – – – 2,265 – – – 2,265 107.77

Class E, Series 44 694,530 – – – – – (56,300) 638,230 108.62

Class F, Series 44 – – – – – 43,600 – 43,600 107.77

Class E, Series 45 2,282 – – – – – – 2,282 108.62

Class F, Series 45 – – – – – 185,600 – 185,600 106.21

Class E, Series 46 1,582 – – – – – – 1,582 108.62

Class E, Series 47 20,435 – – – – – – 20,435 345.37

Class E, Series 48 315,000 – – – – – (21,000) 294,000 104.70

Class F, Series 48 – – – – – 66,000 – 66,000 104.52

Class F, Series 49 – – (41,085) 41,085 – – – – –

Class F, Series 50 – – – – – 40,300 – 40,300 103.68

Class E, Series 51 148,050 – (4,100) – – – – 143,950 104.88

Class F, Series 51 – – – 2,920 – – – 2,920 103.68

See attached financial statements of Third Point Offshore Master Fund L.P.

16THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial Statements continuedYear ended December 31, 2016

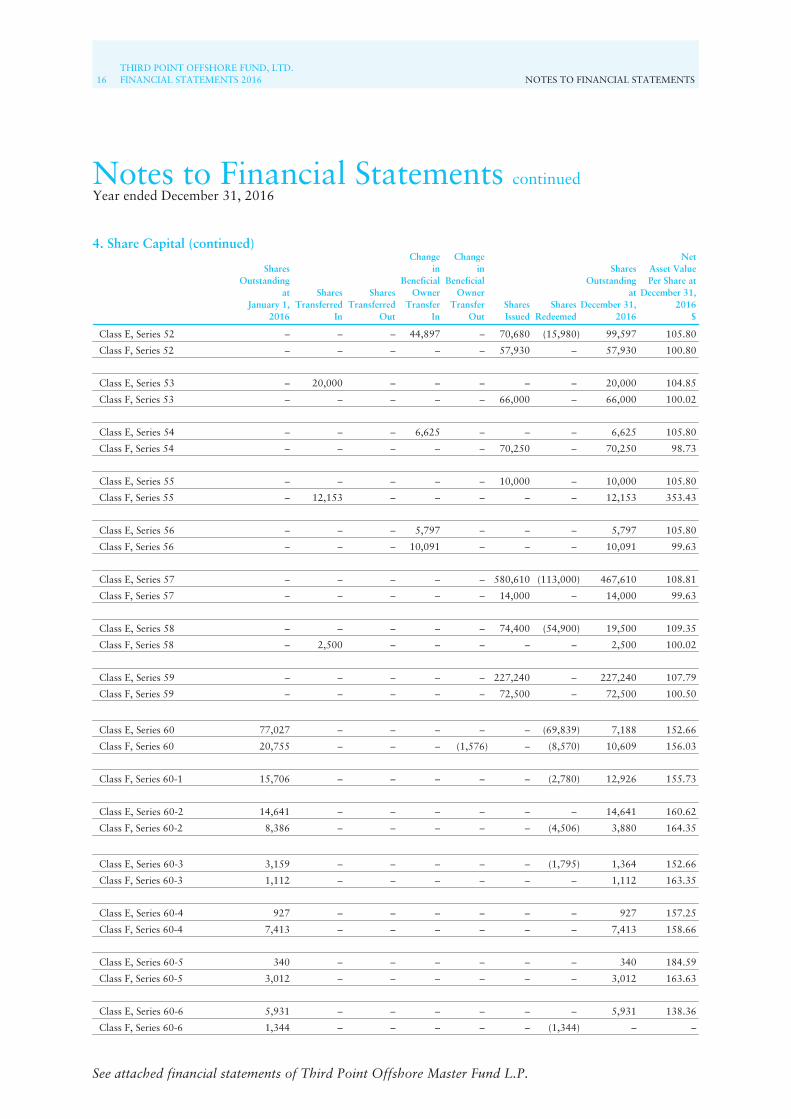

4. Share Capital (continued)

See attached financial statements of Third Point Offshore Master Fund L.P.

SharesOutstanding

atJanuary 1,

2016

SharesTransferred

In

SharesTransferred

Out

Changein

BeneficialOwner

TransferIn

Changein

BeneficialOwner

TransferOut

SharesIssued

SharesRedeemed

SharesOutstanding

atDecember 31,

2016

NetAsset ValuePer Share at

December 31,2016

$

Class E, Series 52 – – – 44,897 – 70,680 (15,980) 99,597 105.80

Class F, Series 52 – – – – – 57,930 – 57,930 100.80

Class E, Series 53 – 20,000 – – – – – 20,000 104.85

Class F, Series 53 – – – – – 66,000 – 66,000 100.02

Class E, Series 54 – – – 6,625 – – – 6,625 105.80

Class F, Series 54 – – – – – 70,250 – 70,250 98.73

Class E, Series 55 – – – – – 10,000 – 10,000 105.80

Class F, Series 55 – 12,153 – – – – – 12,153 353.43

Class E, Series 56 – – – 5,797 – – – 5,797 105.80

Class F, Series 56 – – – 10,091 – – – 10,091 99.63

Class E, Series 57 – – – – – 580,610 (113,000) 467,610 108.81

Class F, Series 57 – – – – – 14,000 – 14,000 99.63

Class E, Series 58 – – – – – 74,400 (54,900) 19,500 109.35

Class F, Series 58 – 2,500 – – – – – 2,500 100.02

Class E, Series 59 – – – – – 227,240 – 227,240 107.79

Class F, Series 59 – – – – – 72,500 – 72,500 100.50

Class E, Series 60 77,027 – – – – – (69,839) 7,188 152.66

Class F, Series 60 20,755 – – – (1,576) – (8,570) 10,609 156.03

Class F, Series 60-1 15,706 – – – – – (2,780) 12,926 155.73

Class E, Series 60-2 14,641 – – – – – – 14,641 160.62

Class F, Series 60-2 8,386 – – – – – (4,506) 3,880 164.35

Class E, Series 60-3 3,159 – – – – – (1,795) 1,364 152.66

Class F, Series 60-3 1,112 – – – – – – 1,112 163.35

Class E, Series 60-4 927 – – – – – – 927 157.25

Class F, Series 60-4 7,413 – – – – – – 7,413 158.66

Class E, Series 60-5 340 – – – – – – 340 184.59

Class F, Series 60-5 3,012 – – – – – – 3,012 163.63

Class E, Series 60-6 5,931 – – – – – – 5,931 138.36

Class F, Series 60-6 1,344 – – – – – (1,344) – –

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 17

4. Share Capital (continued)

SharesOutstanding

atJanuary 1,

2016

SharesTransferred

In

SharesTransferred

Out

Changein

BeneficialOwner

TransferIn

Changein

BeneficialOwner

TransferOut

SharesIssued

SharesRedeemed

SharesOutstanding

atDecember 31,

2016

NetAsset ValuePer Share at

December 31,2016

$

Class F, Series 60-7 2,150 – – – – – (375) 1,775 156.40

Class E, Series 60-8 4,139 – – – – – (745) 3,394 353.45

Class F, Series 60-8 5,884 – – – – – (1,310) 4,574 153.94

Class E, Series 60-9 884 – – – – – (649) 235 152.66

Class F, Series 60-9 2,780 – – – – – (1,853) 927 149.22

Class E, Series 60-10 2,041 – – – – – – 2,041 353.45

Class F, Series 60-10 927 – – – – – – 927 145.94

Class E, Series 60-11 479 – – – – – (479) – –

Class F, Series 60-11 2,131 – – – (2,131) – – – –

Class E, Series 60-12 100,000 – – – – – – 100,000 104.78

Class F, Series 60-12 2,872 – – – – – (1,389) 1,483 126.19

Class E, Series 60-13 50,000 – – – – – – 50,000 104.37

Class F, Series 60-13 50,650 – – – – – (15,299) 35,351 104.04

Class E, Series 60-14 1,924 – – – – – (646) 1,278 353.45

Class F, Series 60-14 125,840 – – – – – (125,440) 400 104.57

Class E, Series 60-15 64,243 – – – – – (3,000) 61,243 353.45

Class F, Series 60-15 30,150 – – – – – (12,698) 17,452 101.09

Class E, Series 60-16 – – – – – 12,000 – 12,000 109.35

Class F, Series 60-16 5,579 – – – – – – 5,579 99.30

Class E, Series 60-17 – 1,134 – – – – – 1,134 353.45

Class F, Series 60-17 1,457 – – – – – – 1,457 98.29

Class E, Series 60-18 – 4,100 – – – – – 4,100 104.88

Class F, Series 60-18 20,750 – – – – – (5,939) 14,811 108.60

Class E, Series 60-19 – – – – – 600 – 600 104.53

Class F, Series 60-19 – – – – – 7,300 – 7,300 105.78

Class E, Series 60-20 – 1,500 – – – – – 1,500 98.32

Class F, Series 60-20 – – – – – 1,450 – 1,450 108.79

Class F, Series 60-21 – – – – – 2,000 – 2,000 109.33

See attached financial statements of Third Point Offshore Master Fund L.P.

18THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial Statements continuedYear ended December 31, 2016

4. Share Capital (continued)

See attached financial statements of Third Point Offshore Master Fund L.P.

SharesOutstanding

atJanuary 1,

2016

SharesTransferred

In

SharesTransferred

Out

Changein

BeneficialOwner

TransferIn

Changein

BeneficialOwner

TransferOut

SharesIssued

SharesRedeemed

SharesOutstanding

atDecember 31,

2016

NetAsset ValuePer Share at

December 31,2016

$

Class F, Series 60-22 – – – – – 1,000 – 1,000 104.52

Class F, Series 60-23 – – – – – 1,000 – 1,000 99.63

Class F, Series 60-24 – – – – – 3,100 – 3,100 100.50

Class E, Series 61-1 111,661 – (46,333) – – – (926) 64,402 157.05

Class F, Series 3-61-1 1,297 – – – – – (1,297) – –

Class F, Series 3-61-2 927 – – – – – – 927 155.73

Class E, Series 61-3 1,714 – – – – – (1,714) – –

Class E, Series 61-4 52,819 – – – – – – 52,819 152.65

Class F, Series 3-61-4 1,297 – – – – – (1,297) – –

Class E, Series 61-5 1,853 – – – – – (1,853) – –

Class F, Series 3-61-5 – 46,332 (46,332) – – – – – –

Class E, Series 61-6 18,533 – – – – – – 18,533 138.36

Class F, Series 3-61-6 – 92,662 (92,662) – – – – – –

Class E, Series 61-7 1,052 – – – – – – 1,052 138.36

Class F, Series 3-61-7 – 31,000 (31,000) – – – – – –

Class E, Series 61-8 108,924 – (92,662) – – – (2,363) 13,899 126.77

Class E, Series 61-9 128,296 – – – – – – 128,296 124.90

Class E, Series 61-10 – – – – – – – – –

Class E, Series 61-11 23,780 – – – – – – 23,780 106.09

Class E, Series 61-12 27,600 – – – – – – 27,600 104.37

Class E, Series 61-13 36,000 – (31,000) – – – – 5,000 104.62

Class E, Series 61-14 – 46,332 – – – – – 46,332 157.02

Class E, Series 61-15 – 92,662 – – – – – 92,662 126.75

Class E, Series 61-16 – 31,000 – – – – – 31,000 104.60

Class E, Series 62 – – – – – 315,800 – 315,800 106.23

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 19

4. Share Capital (continued)

SharesOutstanding

atJanuary 1,

2016

SharesTransferred

In

SharesTransferred

Out

Changein

BeneficialOwner

TransferIn

Changein

BeneficialOwner

TransferOut

SharesIssued

SharesRedeemed

SharesOutstanding

atDecember 31,

2016

NetAsset ValuePer Share at

December 31,2016

$

Class E, Series 63 – – – 4,903 – – – 4,903 106.23

Class E, Series 64 – – – – – 144,570 – 144,570 104.53

Class E, Series 65 – – – – – 270,040 – 270,040 103.68

Class E, Series 66 – – – – – 68,300 – 68,300 100.81

Class E, Series 67 – – – – – 39,800 (39,800) – –

Class E, Series 68 – 12,454 – – – – – 12,454 104.53

Class E, Series 69 – – (2,500) – – 283,250 – 280,750 100.02

Class E, Series 70 – – – – – 536,000 – 536,000 98.73

Class E, Series 71 – 28,630 – – – – – 28,630 104.53

Class E, Series 72 – – – 6,482 – – – 6,482 98.73

Class E, Series 73 – – – – – 763,555 – 763,555 99.64

Class E, Series 74 – – – – – 395,500 – 395,500 100.50

Class E, Series 75 – – – 14,075 – – – 14,075 100.50

Class E, Series 77 – 6,282 – – – – – 6,282 345.30

Class E, Series 78 – 7,068 – – – – – 7,068 345.30

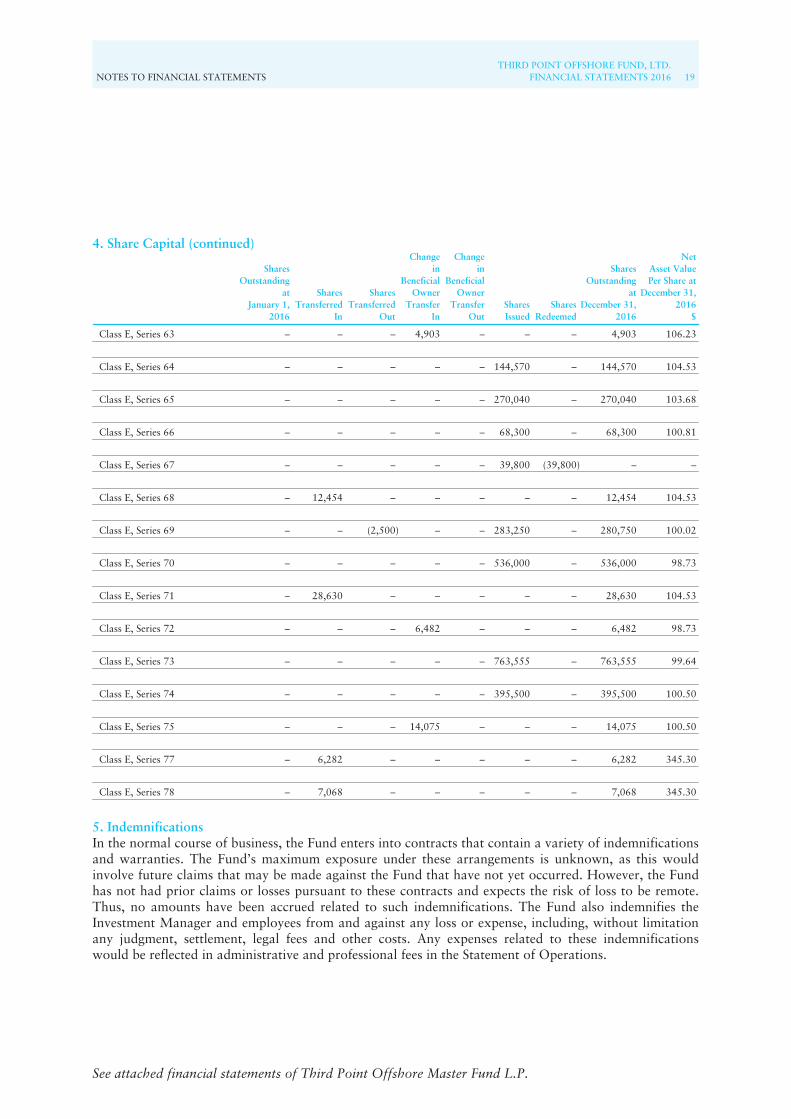

5. IndemnificationsIn the normal course of business, the Fund enters into contracts that contain a variety of indemnificationsand warranties. The Fund’s maximum exposure under these arrangements is unknown, as this wouldinvolve future claims that may be made against the Fund that have not yet occurred. However, the Fundhas not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.Thus, no amounts have been accrued related to such indemnifications. The Fund also indemnifies theInvestment Manager and employees from and against any loss or expense, including, without limitationany judgment, settlement, legal fees and other costs. Any expenses related to these indemnificationswould be reflected in administrative and professional fees in the Statement of Operations.

See attached financial statements of Third Point Offshore Master Fund L.P.

20THIRD POINT OFFSHORE FUND, LTD.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial Statements continuedYear ended December 31, 2016

See attached financial statements of Third Point Offshore Master Fund L.P.

6. Financial HighlightsThe following table represents the per share operating performance, ratios to average net assets and totalreturn information for the year ended December 31, 2016.

Class A,Series 1-2

Class B,Series 1

Class C,Series 1

Class D,Series 1

Class E,Series 1

Class F,Series 1

Class H,Series 1

Per share operating performance

Net asset value at beginning of year $614.42 $592.41 $622.99 $582.90 $333.17 $325.51 $199.82

Income from investment operations:

Net realized and unrealized gain on investments 36.65 35.26 37.16 34.62 19.87 19.34 17.94

Net investment income/(loss) 0.75 0.74 0.77 0.80 0.41 0.44 (0.12)

Total from investment operations 37.40 36.00 37.93 35.42 20.28 19.78 17.82

Net asset value at the end of the year $651.82 $628.41 $660.92 $618.32 $353.45 $345.29 $217.64

Total return before incentive fee 7.25% 7.23% 7.25% 7.23% 7.25% 7.23% 10.28%

Incentive fee (1.16) (1.15) (1.16) (1.15) (1.16) (1.15) (1.37)

Total return after incentive fee 6.09% 6.08% 6.09% 6.08% 6.09% 6.08% 8.91%

Ratios to average net assets

Total expenses before incentive fee anddepreciation of deferred compensation 2.73% 2.73% 2.73% 2.75% 2.77% 2.77% 2.80%

Incentive fee 1.13 1.12 1.13 1.13 1.14 1.12 1.50

Total expenses before depreciation of deferredcompensation 3.86% 3.85% 3.86% 3.88% 3.91% 3.89% 4.30%

Depreciation of deferred compensation (0.94) (0.93) (0.94) (0.94) (0.92) (0.91) (0.84)

Net expenses 2.92% 2.92% 2.92% 2.94% 2.99% 2.98% 3.46%

Net investment income/(loss) 0.13% 0.12% 0.12% 0.12% 0.09% 0.09% (0.36%)

The total return and ratios to average net assets of other series in the same share class may vary based onparticipation in “new issues” and the timing of capital subscriptions and redemptions. The per shareinformation, total return and ratios to average net assets information include the proportionate share ofthe Master Partnership’s income and expenses.

7. Subsequent EventsSubsequent to December 31, 2016, the Fund received approximately $235 million in capitalsubscriptions, of which approximately $44 million was received in advance, and recorded redemptions ofapproximately $208 million. Subsequent events were evaluated by the Fund’s management untilMarch 17, 2017, which is the date the financial statements were issued.

On January 3, 2017, the Investment Manager received the full balance of deferred compensation fromthe Fund. The deferred compensation invested in the affiliated portfolio fund of $110,354,098 wasdistributed in-kind to the Investment Manager. As per the Deferred Fee Agreement, the remainingamount of $104,098,115 was redeemed in cash and simultaneously fully reinvested in the Fund throughan affiliate of the Investment Manager.

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE FUND, LTD.

FINANCIAL STATEMENTS 2016 21

This page has been left intentionally blank

THIRD POINT OFFSHORE MASTERFUND L.P.

FINANCIAL STATEMENTSAs of and for the Year Ended December 31, 2016

With Report of Independent Auditors

Contents

01 Report of Independent Auditors02 Statement of Financial Condition03 Condensed Schedule of Investments11 Statement of Income12 Statement of Changes in Partners’ Capital13 Statement of Cash Flows14 Notes to Financial Statements

REPORT OF INDEPENDENT AUDITORSTHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 1

Ernst & Young LLP 5 Times Square New York, NY 10036-6530

Tel: +1 212 773 3000 Fax: +1 212 773 6350 ey.com

Report of Independent Auditors

To the General Partner ofThird Point Offshore Master Fund L.P.

We have audited the accompanying financial statements of Third Point Offshore Master Fund L.P.,which comprise the statement of financial condition, including the condensed schedule of investments, asof December 31, 2016, and the related statements of income, changes in partners’ capital and cash flowsfor the year then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these financial statements inconformity with U.S. generally accepted accounting principles; this includes the design, implementation,and maintenance of internal control relevant to the preparation and fair presentation of financialstatements that are free of material misstatement, whether due to fraud or error.

Auditor’s ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audit. Weconducted our audit in accordance with auditing standards generally accepted in the United States. Thosestandards require that we plan and perform the audit to obtain reasonable assurance about whether thefinancial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures inthe financial statements. The procedures selected depend on the auditor’s judgment, including theassessment of the risks of material misstatement of the financial statements, whether due to fraud orerror. In making those risk assessments, the auditor considers internal control relevant to the entity’spreparation and fair presentation of the financial statements in order to design audit procedures that areappropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness ofthe entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluatingthe appropriateness of accounting policies used and the reasonableness of significant accountingestimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour audit opinion.

OpinionIn our opinion, the financial statements referred to above present fairly, in all material respects, thefinancial position of Third Point Offshore Master Fund L.P. at December 31, 2016, and the results of itsoperations, the changes in its partners’ capital and its cash flows for the year then ended, in conformitywith U.S. generally accepted accounting principles.

March 17, 2017

A member firm of Ernst & Young Global Limited

2THIRD POINT OFFSHORE MASTER FUND L.P.FINANCIAL STATEMENTS 2016 STATEMENT OF FINANCIAL CONDITION

Statement of Financial ConditionDecember 31, 2016

(Stated in United States Dollars) $

Assets

Cash 4,440

Investments in securities, at fair value (cost $6,746,669,215) 7,334,544,527

Investments in affiliated funds, at fair value (cost $223,898,339) 253,406,493

Due from brokers 750,371,124

Derivative contracts, at fair value(net upfront fees paid and cost of $59,515,462) 93,070,077

Interest and dividends receivable 17,828,012

Other assets 139,202,173

Total assets 8,588,426,846

Liabilities and Partners’ Capital

Liabilities

Securities sold, not yet purchased, at fair value (proceeds $304,388,601) 299,139,655

Due to brokers 713,931,846

Derivative contracts, at fair value(net upfront fees received and proceeds of $21,858,351) 49,704,088

Withdrawals payable to General Partner 100,000,000

Withdrawals payable to Limited Partner 449,888,556

Interest and dividends payable 1,069,759

Accrued expenses 3,305,254

Total liabilities 1,617,039,158

Commitments (See Note 10)

Partners’ Capital

General Partner’s capital 38,296,312

Limited Partner’s capital 6,933,091,376

Total Partners’ capital 6,971,387,688

Total liabilities and partners’ capital 8,588,426,846

See accompanying notes.

CONDENSED SCHEDULE OF INVESTMENTSTHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 3

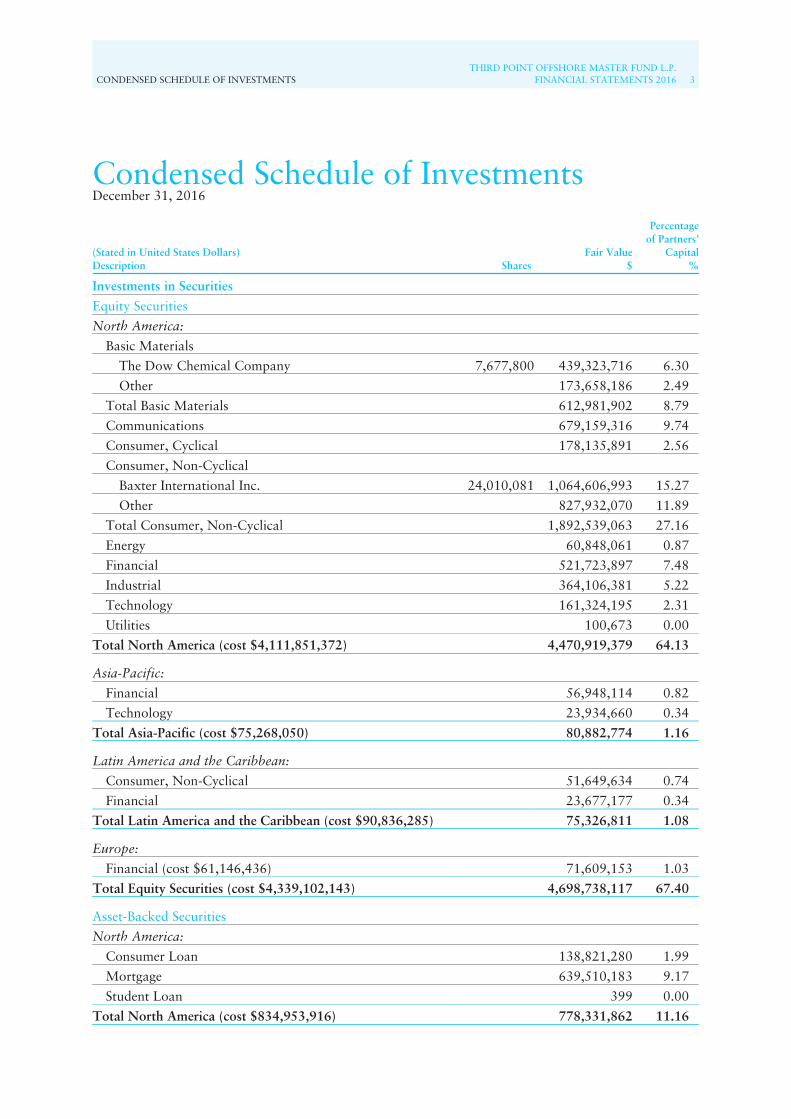

Condensed Schedule of InvestmentsDecember 31, 2016

(Stated in United States Dollars)Description Shares

Fair Value$

Percentageof Partners’

Capital%

Investments in Securities

Equity Securities

North America:

Basic Materials

The Dow Chemical Company 7,677,800 439,323,716 6.30

Other 173,658,186 2.49

Total Basic Materials 612,981,902 8.79

Communications 679,159,316 9.74

Consumer, Cyclical 178,135,891 2.56

Consumer, Non-Cyclical

Baxter International Inc. 24,010,081 1,064,606,993 15.27

Other 827,932,070 11.89

Total Consumer, Non-Cyclical 1,892,539,063 27.16

Energy 60,848,061 0.87

Financial 521,723,897 7.48

Industrial 364,106,381 5.22

Technology 161,324,195 2.31

Utilities 100,673 0.00

Total North America (cost $4,111,851,372) 4,470,919,379 64.13

Asia-Pacific:

Financial 56,948,114 0.82

Technology 23,934,660 0.34

Total Asia-Pacific (cost $75,268,050) 80,882,774 1.16

Latin America and the Caribbean:

Consumer, Non-Cyclical 51,649,634 0.74

Financial 23,677,177 0.34

Total Latin America and the Caribbean (cost $90,836,285) 75,326,811 1.08

Europe:

Financial (cost $61,146,436) 71,609,153 1.03

Total Equity Securities (cost $4,339,102,143) 4,698,738,117 67.40

Asset-Backed Securities

North America:

Consumer Loan 138,821,280 1.99

Mortgage 639,510,183 9.17

Student Loan 399 0.00

Total North America (cost $834,953,916) 778,331,862 11.16

4THIRD POINT OFFSHORE MASTER FUND L.P.FINANCIAL STATEMENTS 2016 CONDENSED SCHEDULE OF INVESTMENTS

Condensed Schedule of Investments continuedDecember 31, 2016

(Stated in United States Dollars)Description

Fair Value$

Percentageof Partners’

Capital%

Investments in Securities (continued)

Asset-Backed Securities (continued)

Europe:

Mortgage (cost $100,590,919) 76,420,379 1.10

Latin America and the Caribbean:

Mortgage (cost $14,978,779) 11,583,980 0.17

Total Asset-Backed Securities (cost $950,523,614) 866,336,221 12.43

Corporate Bonds

North America:

Communications 179,420,003 2.57

Energy 273,682,166 3.93

Financial 14,814,528 0.21

Technology 98,174,136 1.41

Utilities 1,728 0.00

Total North America (cost $399,322,764) 566,092,561 8.12

Latin America and the Caribbean:

Communications 3,303,095 0.05

Energy 79,021,530 1.13

Real Estate 27,464,435 0.39

Total Latin America and the Caribbean: (cost $98,993,995) 109,789,060 1.57

Europe:

Communications 14,840,566 0.21

Financial 42,835,069 0.62

Utilities 80,990 0.00

Total Europe (cost $81,756,673) 57,756,625 0.83

Total Corporate Bonds (cost $580,073,432) 733,638,246 10.52

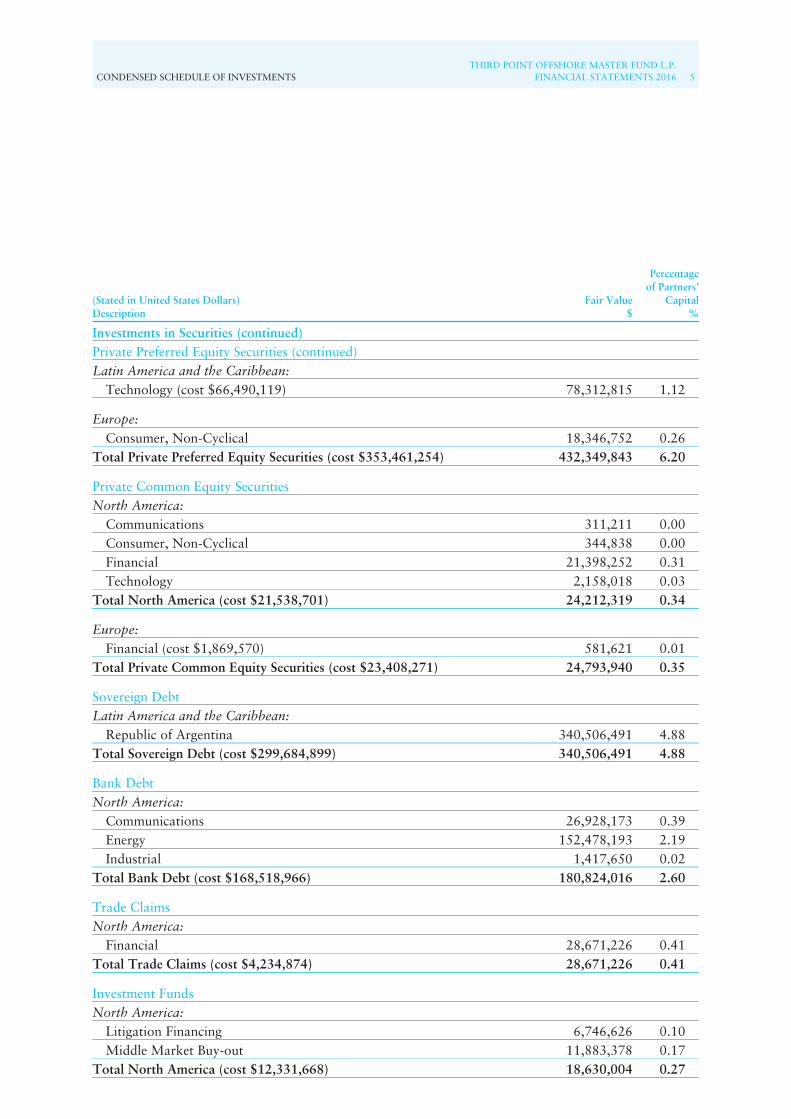

Private Preferred Equity Securities

North America:

Communications 29,262,861 0.42

Consumer, Cyclical 1,194,300 0.02

Consumer, Non-Cyclical 28,202,645 0.41

Energy 4,838,935 0.07

Financial 152,239,910 2.18

Technology 119,951,625 1.72

Total North America (cost $286,971,135) 335,690,276 4.82

CONDENSED SCHEDULE OF INVESTMENTSTHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 5

(Stated in United States Dollars)Description

Fair Value$

Percentageof Partners’

Capital%

Investments in Securities (continued)Private Preferred Equity Securities (continued)Latin America and the Caribbean:

Technology (cost $66,490,119) 78,312,815 1.12

Europe:Consumer, Non-Cyclical 18,346,752 0.26

Total Private Preferred Equity Securities (cost $353,461,254) 432,349,843 6.20

Private Common Equity SecuritiesNorth America:

Communications 311,211 0.00Consumer, Non-Cyclical 344,838 0.00Financial 21,398,252 0.31Technology 2,158,018 0.03

Total North America (cost $21,538,701) 24,212,319 0.34

Europe:Financial (cost $1,869,570) 581,621 0.01

Total Private Common Equity Securities (cost $23,408,271) 24,793,940 0.35

Sovereign DebtLatin America and the Caribbean:

Republic of Argentina 340,506,491 4.88Total Sovereign Debt (cost $299,684,899) 340,506,491 4.88

Bank DebtNorth America:

Communications 26,928,173 0.39Energy 152,478,193 2.19Industrial 1,417,650 0.02

Total Bank Debt (cost $168,518,966) 180,824,016 2.60

Trade ClaimsNorth America:

Financial 28,671,226 0.41Total Trade Claims (cost $4,234,874) 28,671,226 0.41

Investment FundsNorth America:

Litigation Financing 6,746,626 0.10Middle Market Buy-out 11,883,378 0.17

Total North America (cost $12,331,668) 18,630,004 0.27

6THIRD POINT OFFSHORE MASTER FUND L.P.FINANCIAL STATEMENTS 2016 CONDENSED SCHEDULE OF INVESTMENTS

Condensed Schedule of Investments continuedDecember 31, 2016

(Stated in United States Dollars)Description

Fair Value$

Percentageof Partners’

Capital%

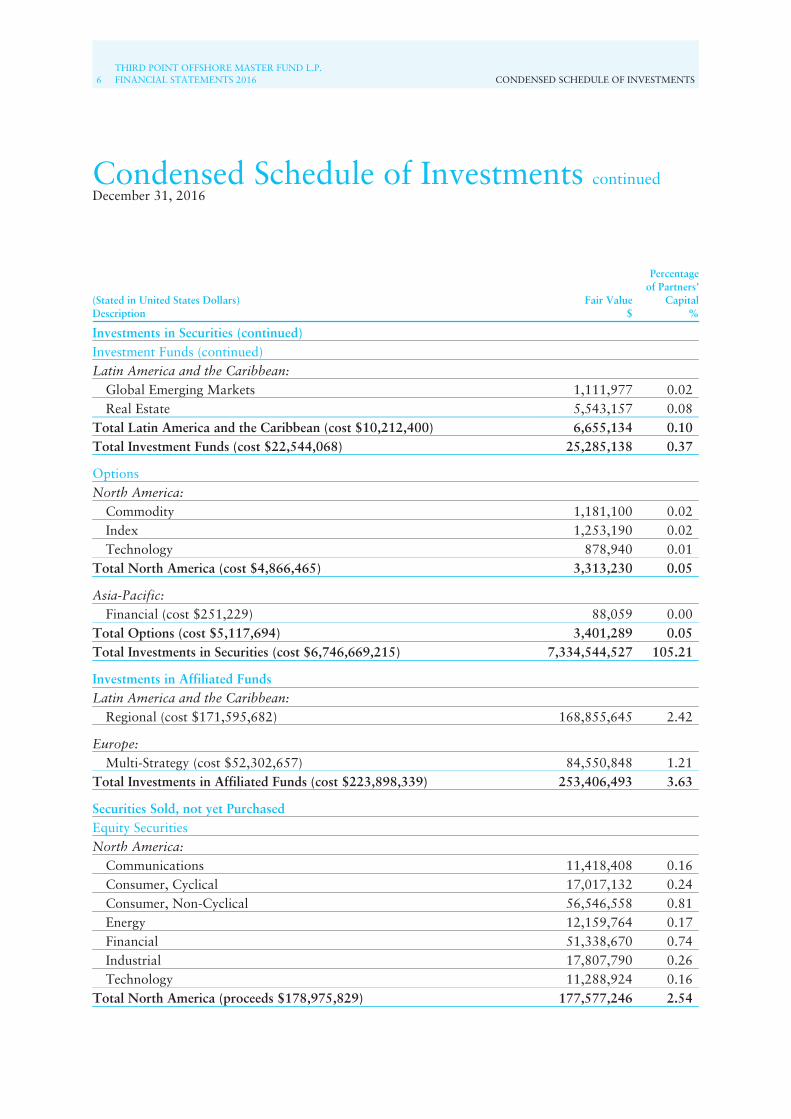

Investments in Securities (continued)Investment Funds (continued)Latin America and the Caribbean:

Global Emerging Markets 1,111,977 0.02Real Estate 5,543,157 0.08

Total Latin America and the Caribbean (cost $10,212,400) 6,655,134 0.10Total Investment Funds (cost $22,544,068) 25,285,138 0.37

OptionsNorth America:

Commodity 1,181,100 0.02Index 1,253,190 0.02Technology 878,940 0.01

Total North America (cost $4,866,465) 3,313,230 0.05

Asia-Pacific:Financial (cost $251,229) 88,059 0.00

Total Options (cost $5,117,694) 3,401,289 0.05Total Investments in Securities (cost $6,746,669,215) 7,334,544,527 105.21

Investments in Affiliated FundsLatin America and the Caribbean:

Regional (cost $171,595,682) 168,855,645 2.42

Europe:Multi-Strategy (cost $52,302,657) 84,550,848 1.21

Total Investments in Affiliated Funds (cost $223,898,339) 253,406,493 3.63

Securities Sold, not yet PurchasedEquity SecuritiesNorth America:

Communications 11,418,408 0.16Consumer, Cyclical 17,017,132 0.24Consumer, Non-Cyclical 56,546,558 0.81Energy 12,159,764 0.17Financial 51,338,670 0.74Industrial 17,807,790 0.26Technology 11,288,924 0.16

Total North America (proceeds $178,975,829) 177,577,246 2.54

CONDENSED SCHEDULE OF INVESTMENTSTHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 7

(Stated in United States Dollars)Description

Fair Value$

Percentageof Partners’

Capital%

Securities Sold, not yet Purchased (continued)Equity Securities (continued)Europe:

Consumer, Non-Cyclical 13,496,238 0.19Industrial 30,753,419 0.45

Total Europe (proceeds $45,222,978) 44,249,657 0.64

Asia-Pacific:Industrial (proceeds $6,524,028) 6,180,223 0.09

Total Equity Securities (proceeds $230,722,835) 228,007,126 3.27

Corporate BondsNorth America:

Consumer, Non-Cyclical 41,736,562 0.60Utilities 17,599,883 0.25

Total Corporate Bonds (proceeds $59,924,454) 59,336,445 0.85

OptionsNorth America:

Basic Materials 664,956 0.01Communications 4,711,200 0.06Consumer, Non-Cyclical 617,472 0.01Financial 2,127,461 0.03Index 2,483,800 0.04Technology 1,191,195 0.02

Total Options (proceeds $13,741,312) 11,796,084 0.17Total Securities Sold, not yet Purchased (proceeds $304,388,601) 299,139,655 4.29

Derivative ContractsContracts for Differences – Long ContractsEurope:

Financial 2,862,208 0.04Industrial 3,107,756 0.05

Total Europe 5,969,964 0.09

Latin America and the Caribbean:Financial 5,009 0.00

Total Contracts for Differences – Long Contracts 5,974,973 0.09

8THIRD POINT OFFSHORE MASTER FUND L.P.FINANCIAL STATEMENTS 2016 CONDENSED SCHEDULE OF INVESTMENTS

Condensed Schedule of Investments continuedDecember 31, 2016

(Stated in United States Dollars)Description

Fair Value$

Percentageof Partners’

Capital%

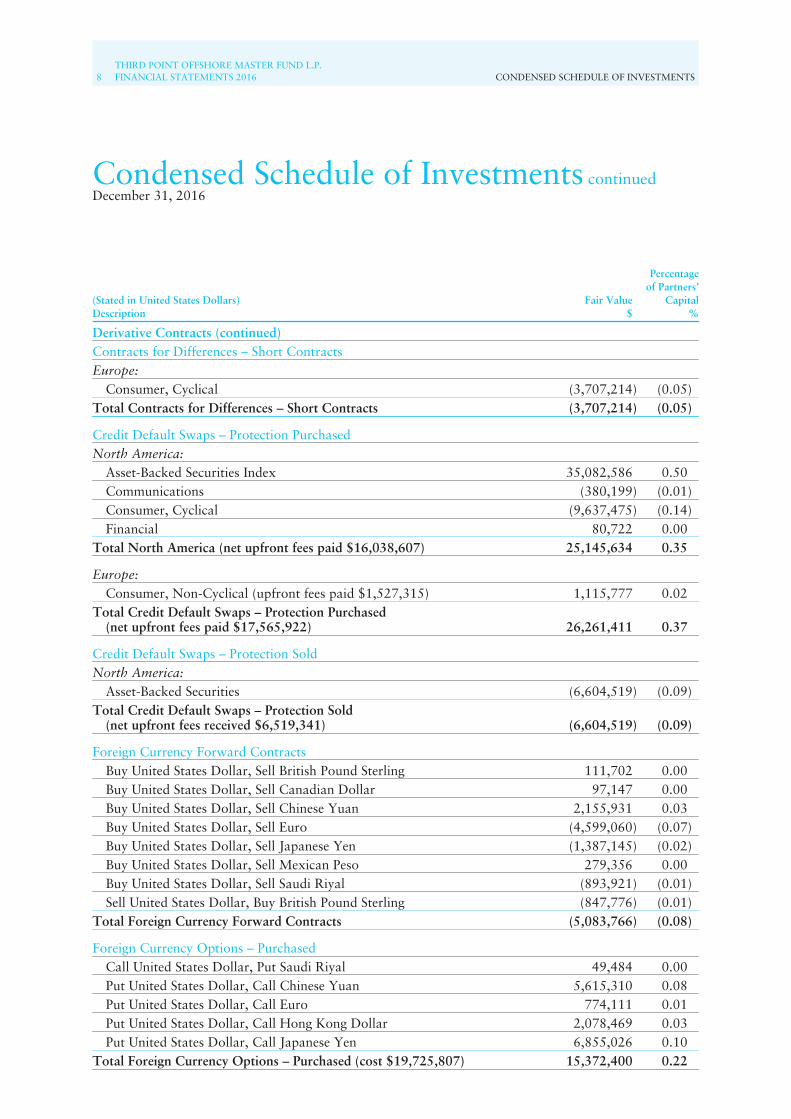

Derivative Contracts (continued)Contracts for Differences – Short ContractsEurope:

Consumer, Cyclical (3,707,214) (0.05)Total Contracts for Differences – Short Contracts (3,707,214) (0.05)

Credit Default Swaps – Protection PurchasedNorth America:

Asset-Backed Securities Index 35,082,586 0.50Communications (380,199) (0.01)Consumer, Cyclical (9,637,475) (0.14)Financial 80,722 0.00

Total North America (net upfront fees paid $16,038,607) 25,145,634 0.35

Europe:Consumer, Non-Cyclical (upfront fees paid $1,527,315) 1,115,777 0.02

Total Credit Default Swaps – Protection Purchased(net upfront fees paid $17,565,922) 26,261,411 0.37

Credit Default Swaps – Protection SoldNorth America:

Asset-Backed Securities (6,604,519) (0.09)Total Credit Default Swaps – Protection Sold

(net upfront fees received $6,519,341) (6,604,519) (0.09)

Foreign Currency Forward ContractsBuy United States Dollar, Sell British Pound Sterling 111,702 0.00Buy United States Dollar, Sell Canadian Dollar 97,147 0.00Buy United States Dollar, Sell Chinese Yuan 2,155,931 0.03Buy United States Dollar, Sell Euro (4,599,060) (0.07)Buy United States Dollar, Sell Japanese Yen (1,387,145) (0.02)Buy United States Dollar, Sell Mexican Peso 279,356 0.00Buy United States Dollar, Sell Saudi Riyal (893,921) (0.01)Sell United States Dollar, Buy British Pound Sterling (847,776) (0.01)

Total Foreign Currency Forward Contracts (5,083,766) (0.08)

Foreign Currency Options – PurchasedCall United States Dollar, Put Saudi Riyal 49,484 0.00Put United States Dollar, Call Chinese Yuan 5,615,310 0.08Put United States Dollar, Call Euro 774,111 0.01Put United States Dollar, Call Hong Kong Dollar 2,078,469 0.03Put United States Dollar, Call Japanese Yen 6,855,026 0.10

Total Foreign Currency Options – Purchased (cost $19,725,807) 15,372,400 0.22

CONDENSED SCHEDULE OF INVESTMENTSTHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 9

(Stated in United States Dollars)Description

Fair Value$

Percentageof Partners’

Capital%

Derivative Contracts (continued)Foreign Currency Options – Sold

Put United States Dollar, Call Chinese Yuan (1,636,064) (0.02)Put United States Dollar, Call Japanese Yen (2,890,460) (0.04)

Total Foreign Currency Options – Sold (proceeds $4,806,047) (4,526,524) (0.06)

Interest Rate SwapsUnited States Dollar Libor 7,344,730 0.10British Pound Sterling Libor (1,482,572) (0.02)

Total Interest Rate Swaps 5,862,158 0.08

Interest Rate SwaptionsJapanese Yen Libor 7,682,479 0.11United States Dollar ICE Swap Rate 1,396,714 0.02United States Dollar Libor 5,421,184 0.08

Total Interest Rate Swaptions (cost $11,690,770) 14,500,377 0.21

Sovereign Futures – Short ContractsNorth America:

Financial 3,232,718 0.05

Europe:Financial (5,407,691) (0.08)

Total Sovereign Futures – Short Contracts (2,174,973) (0.03)

Total Return Swaps – Long ContractsLatin America and the Caribbean:

Utilities 1,548,597 0.02

North America:Energy 164,343 0.00Financial 65,899 0.00Industrial (135,540) (0.00)Technology (299,702) (0.00)

Total North America (205,000) (0.00)Total Total Return Swaps – Long Contracts 1,343,597 0.02

10THIRD POINT OFFSHORE MASTER FUND L.P.FINANCIAL STATEMENTS 2016 CONDENSED SCHEDULE OF INVESTMENTS

Condensed Schedule of Investments continuedDecember 31, 2016

(Stated in United States Dollars)Description

Fair Value$

Percentageof Partners’

Capital%

Derivative Contracts (continued)

Total Return Swaps – Short Contracts

Asia-Pacific:

Industrial (3,851,931) (0.06)

Total Total Return Swaps – Short Contracts (3,851,931) (0.06)

Net Derivative Contracts (including net upfront fees paid and costof $37,657,111) 43,365,989 0.62

See accompanying notes.

STATEMENT OF INCOMETHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 11

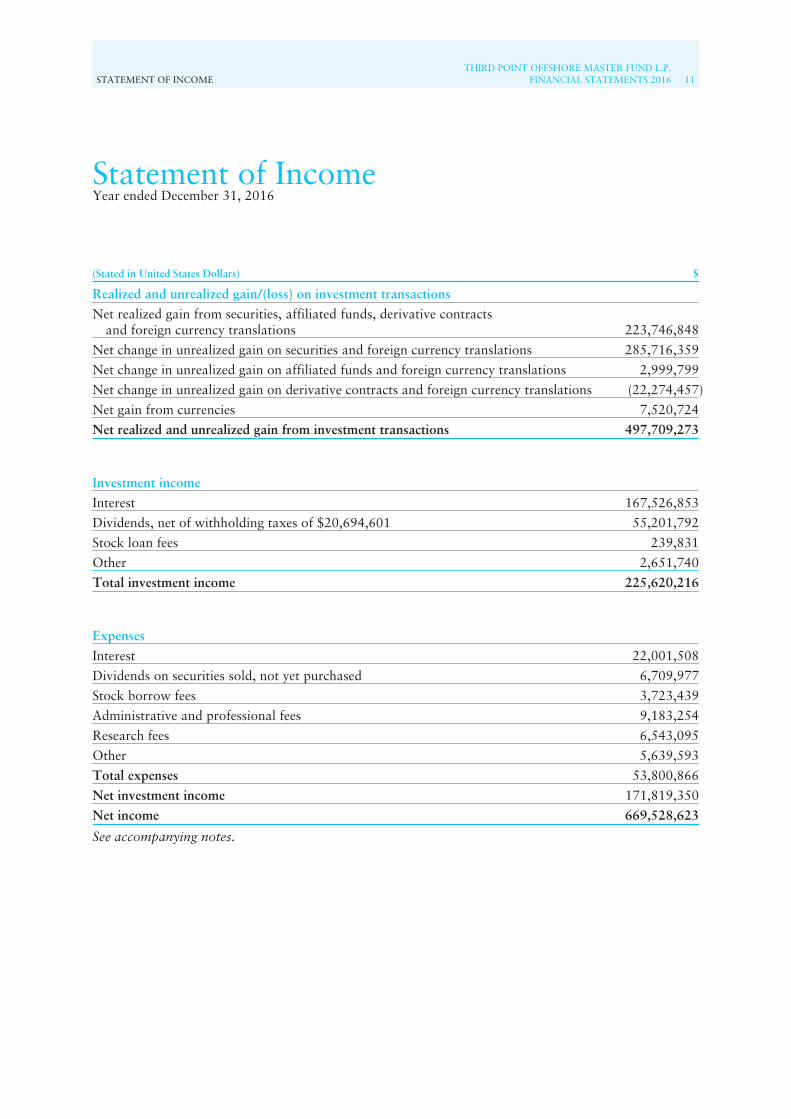

Statement of IncomeYear ended December 31, 2016

(Stated in United States Dollars) $

Realized and unrealized gain/(loss) on investment transactions

Net realized gain from securities, affiliated funds, derivative contractsand foreign currency translations 223,746,848

Net change in unrealized gain on securities and foreign currency translations 285,716,359

Net change in unrealized gain on affiliated funds and foreign currency translations 2,999,799

Net change in unrealized gain on derivative contracts and foreign currency translations (22,274,457)

Net gain from currencies 7,520,724

Net realized and unrealized gain from investment transactions 497,709,273

Investment income

Interest 167,526,853

Dividends, net of withholding taxes of $20,694,601 55,201,792

Stock loan fees 239,831

Other 2,651,740

Total investment income 225,620,216

Expenses

Interest 22,001,508

Dividends on securities sold, not yet purchased 6,709,977

Stock borrow fees 3,723,439

Administrative and professional fees 9,183,254

Research fees 6,543,095

Other 5,639,593

Total expenses 53,800,866

Net investment income 171,819,350

Net income 669,528,623

See accompanying notes.

12THIRD POINT OFFSHORE MASTER FUND L.P.FINANCIAL STATEMENTS 2016 STATEMENT OF CHANGES IN PARTNERS’ CAPITAL

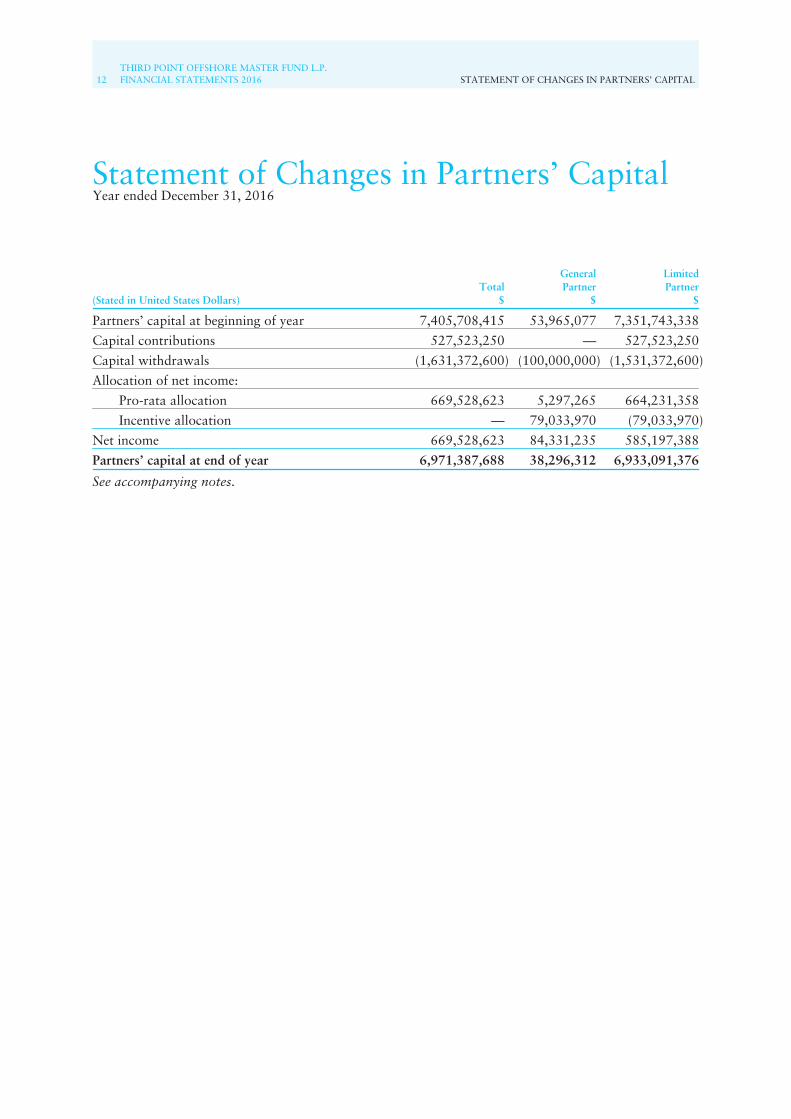

Statement of Changes in Partners’ CapitalYear ended December 31, 2016

(Stated in United States Dollars)Total

$

GeneralPartner

$

LimitedPartner

$

Partners’ capital at beginning of year 7,405,708,415 53,965,077 7,351,743,338

Capital contributions 527,523,250 — 527,523,250

Capital withdrawals (1,631,372,600) (100,000,000) (1,531,372,600)

Allocation of net income:

Pro-rata allocation 669,528,623 5,297,265 664,231,358

Incentive allocation — 79,033,970 (79,033,970)

Net income 669,528,623 84,331,235 585,197,388

Partners’ capital at end of year 6,971,387,688 38,296,312 6,933,091,376

See accompanying notes.

STATEMENT OF CASH FLOWSTHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 13

Statement of Cash FlowsYear ended December 31, 2016

(Stated in United States Dollars) $

Cash flows from operating activities

Net income 669,528,623

Adjustments to reconcile net income to net cash provided by operating activities:

Purchases of investment securities (11,389,809,898)

Proceeds from disposition of investment securities 11,953,689,036

Purchases of investment securities to cover short sales (4,354,006,443)

Proceeds from short sales of investment securities 3,537,437,972

Purchases of affiliated funds (183,671,904)

Proceeds from disposition of affiliated funds 50,176,655

Purchases of derivative contracts (72,815,885)

Proceeds from disposition of derivative contracts 34,766,594

Net realized gain from securities, affiliated funds, derivative contracts and foreigncurrency translations (223,746,848)

Net change in unrealized gain on securities and foreign currency translations (285,716,359)

Net change in unrealized gain on affiliated funds and foreign currency translations (2,999,799)

Net change in unrealized gain on derivative contracts andforeign currency translations 22,274,457

Amortization of premium and accretion of discount, net 15,994,726

Changes in operating assets and liabilities:

Decrease in due from brokers 619,733,170

Decrease in interest and dividends receivable 17,322,904

Decrease in other assets 230,162

Increase in due to brokers 474,184,825

Decrease in securities sold under agreement to repurchase (33,908,222)

Decrease in interest and dividends payable (3,416,092)

Increase in accrued expenses 519,770

Net cash provided by operating activities 845,767,444

Cash flows from financing activities

Capital contributions 527,523,250

Capital withdrawals (1,373,297,138)

Net cash used in financing activities (845,773,888)

Net decrease in cash (6,444)

Cash at beginning of the year 10,884

Cash at end of year 4,440

Supplemental disclosure of cash flow information

Cash paid during the year for interest 21,037,414

See accompanying notes.

14THIRD POINT OFFSHORE MASTER FUND L.P.FINANCIAL STATEMENTS 2016 NOTES TO FINANCIAL STATEMENTS

Notes to Financial StatementsYear ended December 31, 2016

1. OrganizationThird Point Offshore Master Fund L.P. (the “Partnership”) was organized as a limited partnership underthe laws of the Cayman Islands and commenced operations on January 1, 2009. The Partnership wasformed to trade and invest primarily in equity and debt securities of U.S. and foreign companies. Theinvestment objective of the Partnership is to achieve superior risk-adjusted returns by deploying capital ininvestments with a favorable risk/reward scenario across select asset classes, sectors, and geographies,both long and short. Third Point LLC (the “Investment Manager”) identifies these opportunities using acombination of top-down asset allocation decisions and a bottom-up, value-oriented approach to singlesecurity analysis. The Investment Manager supplements single security analysis with an approach toportfolio construction that includes sizing each investment based on upside/downside calculations, allwith a view towards appropriately positioning and managing overall exposures across specific assetclasses, sectors and geographies. The Partnership will continue until terminated as provided for in theThird Amended and Restated Exempted Limited Partnership Agreement (the “Agreement”).

The Partnership serves as the master fund in a “master-feeder” structure whereby Third Point OffshoreFund, Ltd. (the “Feeder”), a Cayman Islands exempted company, invests substantially all of its net assetsin the Partnership, which conducts all investment and trading activities on behalf of the Feeder fund. TheFeeder and the Partnership have the same investment objectives. At December 31, 2016, approximately99.45% of the Partnership’s capital was owned by the Feeder.

Third Point LLC is the Investment Manager of the Partnership. The General Partner of the Partnership isThird Point Advisors II L.L.C. The Investment Manager is registered with the Securities and ExchangeCommission as an Investment Adviser under the Investment Advisers Act of 1940. The InvestmentManager and the General Partner are responsible for the operation and management of the Partnership.

The Partnership is an investment company and applies specialized accounting guidance as outlined inFinancial Services – Investment Companies (Topic 946). The Investment Manager evaluated thisguidance and determined that the Partnership meets the criteria to be classified as an investmentcompany. Accordingly, the Partnership reflects its investments in the Statement of Financial Condition attheir estimated fair value, with unrealized gains and losses resulting from changes in fair value, if any,reflected in net change in unrealized gain/loss on securities, affiliated funds, derivative contracts andforeign currency translations in the Statement of Income.

International Fund Services (Ireland) Limited serves as the administrator (the “Administrator”) andtransfer agent to the Partnership.

2. Significant Accounting PoliciesThe Partnership’s financial statements have been prepared in accordance with U.S. generally acceptedaccounting principles (“U.S. GAAP”) and are expressed in United States dollars. The following is asummary of the significant accounting and reporting policies:

The Partnership is exempt from all forms of taxation in the Cayman Islands, including income, capitalgains and withholding taxes. In jurisdictions other than the Cayman Islands, in some cases foreign taxeswill be withheld at source on dividends and certain interest received by the Partnership. Capital gainsderived by the Partnership in such jurisdictions generally will be exempt from foreign income orwithholding taxes at the source. The Partnership will be treated as a partnership for federal income taxpurposes and each investor will be subject to taxation on its share of the Partnership’s ordinary incomeand capital gains.

NOTES TO FINANCIAL STATEMENTSTHIRD POINT OFFSHORE MASTER FUND L.P.

FINANCIAL STATEMENTS 2016 15

2. Significant Accounting Policies (continued)The Partnership evaluates tax positions taken or expected to be taken in the course of preparing thePartnership’s tax returns to determine whether the tax positions are “more-likely-than-not” of beingsustained by the applicable tax authority. Tax positions not deemed to meet a “more likely-than-not”threshold would be recorded as a tax expense in the current year. The General Partner has reviewed thePartnership’s tax positions and has concluded that no material provision for income tax is required in thePartnership’s financial statements. Generally, the Partnership is subject to income tax examinations bymajor taxing authorities including United States and other authorities for open tax years since inception.

The Partnership would recognize interest and penalties, if any, related to unrecognized tax positions asincome tax expense in the Statement of Income. During the year ended December 31, 2016, thePartnership did not incur any interest or penalties related to unrecognized tax positions.

The Partnership records security transactions and related income and expense on a trade-date basis.Realized gains and losses are determined using cost calculated on a specific identification basis.Dividends are recorded on the ex-dividend date. Income and expense are recorded on the accrual basisincluding interest and premiums amortized and discounts accreted.

The Partnership may enter into repurchase and reverse repurchase agreements with financial institutionsin which the financial institution agrees to resell or repurchase securities and the Partnership agrees torepurchase or resell such securities at a mutually agreed price upon maturity. These agreements arecollateralized primarily by debt securities. As of December 31, 2016, the Partnership did not hold anyrepurchase or reverse repurchase agreements. Interest expense and income related to repurchase andreverse repurchase agreements held during the year are included in interest and dividends payable andinterest and dividends receivable in the Statement of Financial Condition, respectively.

The Partnership may lend securities for securities lending transactions or pledge securities and/or cash forsecurities borrowed transactions. The value of any securities loaned is reflected in investments insecurities in the Statement of Financial Condition. As of December 31, 2016, the Partnership had$775,500 of securities loaned. Any collateral received is reflected in due to brokers in the Statement ofFinancial Condition.

The Partnership engages in securities lending transactions whereby upon the Partnership’s request, itsprime brokers, as lending agents, may loan securities of the Partnership as selected by the Partnership tocertain institutions. The securities loaned are generally collateralized in the form of cash or U.S. treasurysecurities in an amount typically at least equal to the fair value of the securities loaned. The fair value ofthe loaned securities is determined at the close of business on each business day and any additionalrequired collateral is delivered to the Partnership on the next business day. Risks may arise upon enteringinto securities lending transactions to the extent that the value of the collateral is less than the value ofthe securities loaned due to changes in the value of the securities loaned.